Embed Size (px)

Citation preview

STATE HANDBOOK: SOUTH AUSTRALIA OCTOBER 2017

CONTENTS 2 | Key points 3 | In Focus: A relatively broad-based recovery 4 | Consumer & household sector 5 | NAB customer spending behaviours 6 | Business sector 7 | Commercial property sector 8 | Residential property 9 | Demographics 10 | Labour market 11 | Economic structure and trade 12 | Fiscal outlook 13 | Semi government and credit outlook 14 | State and territory forecasts

CONTACTS

Riki Polygenis Alex Stanley Head of Australian Senior Interest Rate Strategist +61 3 8697 9534 +61 2 9237 8154 +61 475 986 285 [email protected] [email protected]

Important Notice This document has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 ("NAB"). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances. NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it. Please click here to view our disclaimer and terms of use.

-2

0

2

4

6

8

10

1992 1996 2000 2004 2008 2012 2016

SA Australia

CHART 1: STATE GSP GROWTH FORECASTS Annual average growth (%), see last page for table

CHART 2: STATE FINAL DEMAND Year-ended % change

Source: ABS and NAB Group Economics 2

KEY POINTS: South Australia experiencing a modest cyclical recovery

South Australia is experiencing a cyclical recovery at present, with infrastructure spending providing support and a more competitive AUD (despite appreciation this year) assisting international education and tourism, as well as manufacturing (outside of auto and steel, including wine). State final demand expanded by 2.6% in 2016-17 following growth of just 1.1% in 2015-16, with the latest figures for Q2 even faster at a year-ended rate of 4.0% yoy (and above national domestic final demand growth of 2.4% yoy). Real gross state product is estimated to have increased by 1¾-2 % in 2016-17 following growth of 1.9% in 2015-16, although these annual average figures do not fully capture the strengthening momentum in recent quarters.

The recent economic upswing has been reflected in a particularly large surge in business conditions in recent months, with the improvement relatively broad-based across all sectors except mining and retail.

The labour market has improved, with employment growth picking up to 2.0% yoy and the trend unemployment rate dropping to 6.1% in Aug-17 from a peak of almost 8% in mid-15. This has supported housing construction, and helped sustain moderate growth in household consumption in the face of falling average wages, although it has so far been insufficient to stem the slowdown in population growth and negative interstate migration. Encouragingly, there has been a large lift in manufacturing and construction jobs, and in male full-time employment this year, although the closure of Holden’s Elizabeth plant in October will weigh (~1K direct jobs to be lost with estimates up to 24K jobs through the supply chain at risk). Employment growth for females has also picked up more recently, largely in part-time work.

Despite recent momentum, there are some key challenges ahead. The closure of Holden’s Elizabeth plant is imminent, dwelling construction has likely peaked, and uncertainty remains around energy supply (and prices). Construction of the Royal Adelaide Hospital has reached technical completion, and government infrastructure spending overall is forecast to peak in 2017-18 at a record $2.2bn (largely roads, public transport, hospitals and education), and ease off thereafter. That said, attempts to re-purpose and modernise the manufacturing industry, especially via the National Shipbuilding Plan will add significantly to growth in coming years - the redevelopment of the Osborne naval shipyard starts in late 2017, construction of 2 of the 12 offshore patrol vessels commences in 2018, major surface combatants (9 frigates) are to start in 2020 and 12 submarines are to commence in 2022-23 at Osborne. The state government has committed $550m in new spending on energy security, and $50m to ensure the survival of the Arrium Steelworks in Whyalla. Despite strong community opposition, a proposal to store nuclear waste in SA has also not been ruled out. The expansion of BHP’s Olympic Dam was put on hold in 2013, although strength in copper prices may support exports values and state government royalties if sustained. Seasonal conditions are mixed so far in 2017-18, with winter crop production to be lower, although the outlook for wine exports remains bright. Net services exports (international students and tourism) will likely to continue to expand solidly.

Meanwhile, the structural challenges facing the state remain. These include a more rapidly ageing population than the rest of Australia, negative interstate migration (particularly of young workers), and a more narrow industrial base (although policy is moving in the right direction here). Overall, we forecast real GSP growth to pick up to 2¾% in 2017-18 (partly due to the higher base) following estimated growth of ~2% in 2016-17, before easing back to 1¾% in 2018-19. The unemployment rate is forecast at 6.5% on average through 2017-18, with softer employment outcomes offset to some extent by slow population growth, before holding steady in 2018-19. Dwelling prices in Adelaide are forecast to grow modestly overall (see within).

0

1

2

3

4

5

6

NSW VIC QLD SA WA TAS NT ACT

2014-15 2015-16 2016-17 (f) 2017-18 (f) 2018-19 (f)

6.76.6

5.21.7

1.21.00.9

0.70.50.5

0.10.1

0.0-0.2-0.3

-1.0-2.8

-4.9-5.4

-9 -8 -7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

ManufacturingConstruction

Admin servicesArts

Public adminRental services

HealthUtilitiesMining

EducationCommunications

TransportWholesale trade

Other servicesFinance

Retail tradeAgricultureHospitality

Business services

IN FOCUS: A relatively broad-based recovery, for now

Construction activity has also picked up in SA. This has been most evident in public investment figures, while dwelling construction has been steady at a high level. These are both likely to be peaking soon, as discussed on page 2. Meanwhile, household spending has continued at a moderate rate. Net exports are likely to have subtracted from growth in 2016-17, largely due to declines in wheat, meat, copper & automotive parts. These aggregate trade figures mask strength in services exports (international education and tourism). While Victoria and NSW appear to be capturing the greatest share of this growth, international student enrolments are growing rapidly, while domestic and international visitor nights are also picking up (Chart 6). Data on exports by commodity is also likely to show strength in wine exports in 2016-17 (as per the national trend).

Sources: ABS, NAB Group Economics, Tourism Research Australia

The pick-up in economic momentum in South Australia so far in 2017 appears relatively broad-based across industries, with all industries except for retail trade and mining reporting positive business conditions. Large improvements have been evident in wholesale, transport/utilities, manufacturing, construction and finance/business/property services, while recreational and personal services have remained strong. This has translated through to better labour market conditions, with employment growth surging to 2% yoy, although, employment growth has been more concentrated in manufacturing, construction and admin services.

CHART 6: TOURISM AND INTERNATIONAL EDUCATION INDICATORS

CHART 3: SA BUSINESS CONDITIONS BY INDUSTRY Net balance, seasonally adjusted, quarterly

CHART 4: CHANGE IN EMPLOYMENT BY INDUSTRY 12 months to AUGUST 2017, SA, Persons, 000s

CHART 5: COMPONENTS ESTIMATED STATE FINAL DEMAND Contribution to growth in SFD + net exports, annual average

3

-80-60-40-20

020406080

2013 2014 2015 2016 2017Construction Fin/Bus/Prop Manuf Mining

Rec & pers serv Retail Wholesale Trans/Util

5

10

15

20

25

30

35

5

10

15

20

25

30

35

2007 2009 2011 2013 2015 2017International visitor nights (millions)Domestic visitor nights (millions)International Student Enrolments (thousands), YTD July

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

2012-13 2013-14 2014-15 2015-16 2016-17

Net exports

GovernmentconsumptionUnderlying publicinvestmentUnderlying businessinvestmentDwelling investment

Household consumption

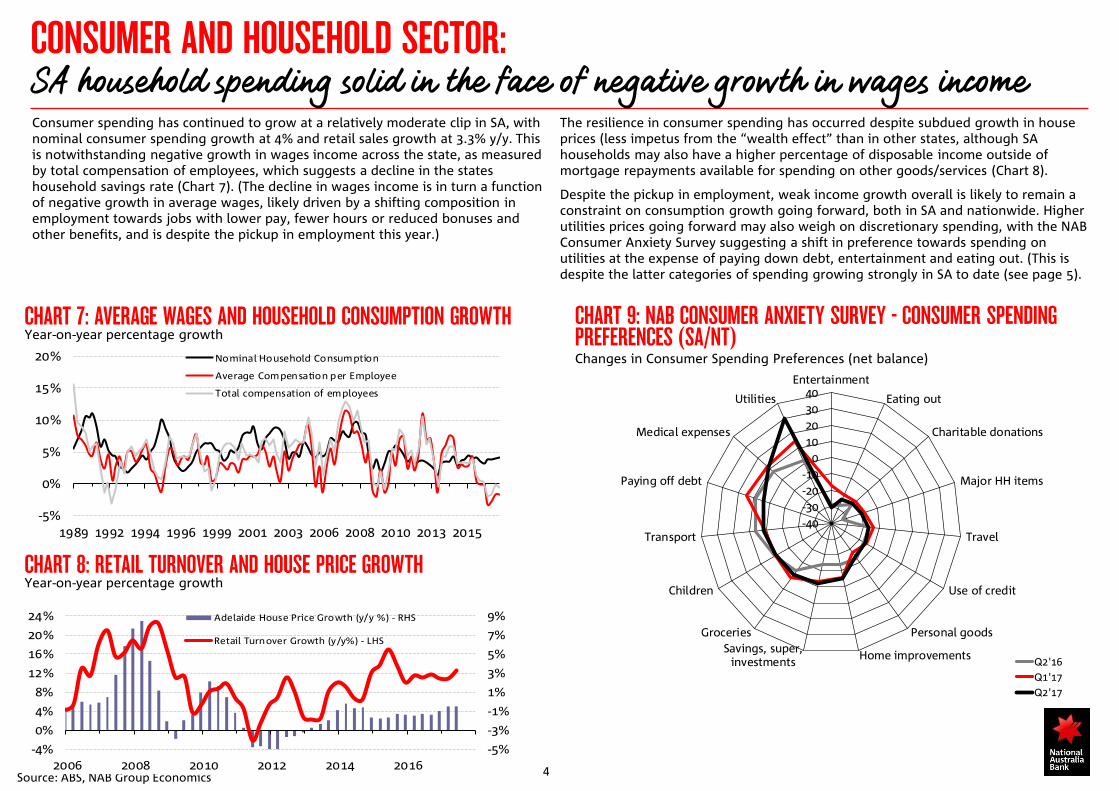

CONSUMER AND HOUSEHOLD SECTOR: SA household spending solid in the face of negative growth in wages income

The resilience in consumer spending has occurred despite subdued growth in house prices (less impetus from the “wealth effect” than in other states, although SA households may also have a higher percentage of disposable income outside of mortgage repayments available for spending on other goods/services (Chart 8).

Despite the pickup in employment, weak income growth overall is likely to remain a constraint on consumption growth going forward, both in SA and nationwide. Higher utilities prices going forward may also weigh on discretionary spending, with the NAB Consumer Anxiety Survey suggesting a shift in preference towards spending on utilities at the expense of paying down debt, entertainment and eating out. (This is despite the latter categories of spending growing strongly in SA to date (see page 5).

Source: ABS, NAB Group Economics 4

Consumer spending has continued to grow at a relatively moderate clip in SA, with nominal consumer spending growth at 4% and retail sales growth at 3.3% y/y. This is notwithstanding negative growth in wages income across the state, as measured by total compensation of employees, which suggests a decline in the states household savings rate (Chart 7). (The decline in wages income is in turn a function of negative growth in average wages, likely driven by a shifting composition in employment towards jobs with lower pay, fewer hours or reduced bonuses and other benefits, and is despite the pickup in employment this year.)

CHART 7: AVERAGE WAGES AND HOUSEHOLD CONSUMPTION GROWTH Year-on-year percentage growth

CHART 8: RETAIL TURNOVER AND HOUSE PRICE GROWTH Year-on-year percentage growth

-5%

0%

5%

10%

15%

20%

1989 1992 1994 1996 1999 2001 2003 2006 2008 2010 2013 2015

Nominal Household Consumption

Average Compensation per Employee

Total compensation of employees

-5%

-3%

-1%

1%

3%

5%

7%

9%

-4%

0%

4%

8%

12%

16%

20%

24%

2006 2008 2010 2012 2014 2016

Adelaide House Price Growth (y/y %) - RHS

Retail Turnover Growth (y/y%) - LHS

-40-30-20-10

010203040

Entertainment

Eating out

Charitable donations

Major HH items

Travel

Use of credit

Personal goods

Home improvementsSavings, super,investments

Groceries

Children

Transport

Paying off debt

Medical expenses

Utilities

Q2'16Q1'17Q2'17

CHART 9: NAB CONSUMER ANXIETY SURVEY - CONSUMER SPENDING PREFERENCES (SA/NT) Changes in Consumer Spending Preferences (net balance)

NAB CUSTOMER SPENDING BEHAVIOURS: Spending growth subdued, but faster in regional areas

Source: ABS, NAB Group Economics 5

NAB’s customer transaction data allows for a more granular look at consumer spending behaviour across regions in SA. In the Adelaide metro area, growth in the value of spending was soft at 1.9% yoy. It was fastest for Arts & Recreation (33.9%), Accommodation & Food Services (10.2%) and Other Services (6.8%), but contracted for Wholesale Trade (-16.0%), Financial & Insurance Services (-11.9%), Education & Training (-6.8%) and Electricity, Gas, Water & Waste (-6.0%). By postcode, overall customer spending growth was fastest in Gepps Cross, Mallala, Virginia and Kangarilla. Spending growth was faster for regional SA (at 6.0% yoy), although average spend was lower at $1,785 compared with $2,143 for Adelaide Metro. By postcode, growth was fastest in Truro, Booleroo Centre, Owen and Edithburgh.

CHART 10: GREATER ADELAIDE METRO AREA Year-ended growth to Q2 2017, nominal

CHART 11: REGIONAL SA (EX METRO) Year-ended growth to Q2 2017, nominal

CHART 12: TOP 20 GROWING METRO POSTCODES FOR SPENDING Year-ended growth to Q2 2017

CHART 13: TOP 20 GROWING REGIONAL POSTCODES FOR SPENDING Year-ended growth to Q2 2017

Overall Growth

1.9%

Average Monthly

Spend (Q2) $2,143

Overall Growth

6.0%

Average Monthly

Spend (Q2) $1,785

24.4

%

22.4

%

17.7

%

16.9

%

15.2

%

15.0

%

14.3

%

12.2

%

12.1

%

11.2

%

10.0

%

9.9%

9.8%

9.6%

9.0%

8.6%

8.5%

8.1%

7.7%

7.4%

0%

5%

10%

15%

20%

25%

30%

Gep

ps

Cro

ss

Mal

lala

Vir

gin

ia

Kan

gar

illa

No

var

Gar

den

s

Penf

ield

Mea

dow

s

Bela

ir

Wal

kerv

ille

Wo

od

ville

Wes

t

Tap

ero

o

Man

sfie

ld P

ark

Myr

tle

Ban

k

Will

un

ga

Lobe

thal

Ker

sbro

ok

Ferr

yden

Par

k

Burt

on

Ku

rral

ta P

ark

Ald

gat

e

5094 5502 5120 5157 5040 5121 5201 5052 5081 5011 5017 5012 5064 5172 5241 5231 5010 5110 5037 5154

53.9

%

36.0

%

32.8

%

28.1

%

26.9

%

25.4

%

25.1

%

24.8

%

23.6

%

22.3

%

20.6

%

20.3

%

20.2

%

19.9

%

19.8

%

19.3

%

19.0

%

17.5

%

16.0

%

15.9

%

0%

10%

20%

30%

40%

50%

60%

Tru

ro

Boo

lero

o C

entr

e

Ow

en

Edit

hb

urg

h

Crys

tal B

roo

k

Ro

ber

tsto

wn

Mila

ng

Lau

ra

Was

leys

Wat

erva

le

Gla

dst

on

e

Port

Ger

mei

n

Wilm

ing

ton

The

Co

oro

ng

Ro

be

Port

Bro

ug

hto

n

Mo

nas

h

Kar

oo

nda

Tin

tin

ara

Kin

gsc

ote

53565482546055835523538152565480540054525473549554855261527655225342530752665223

-20

-10

0

10

20

30

40 Net Balance (%). June quarter 2017

Conditions Confidence

-30

-20

-10

0

10

20

30

40

-30

-20

-10

0

10

20

30

40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Total South Australia

BUSINESS SECTOR: SA business conditions and capacity utilisation have increased notably

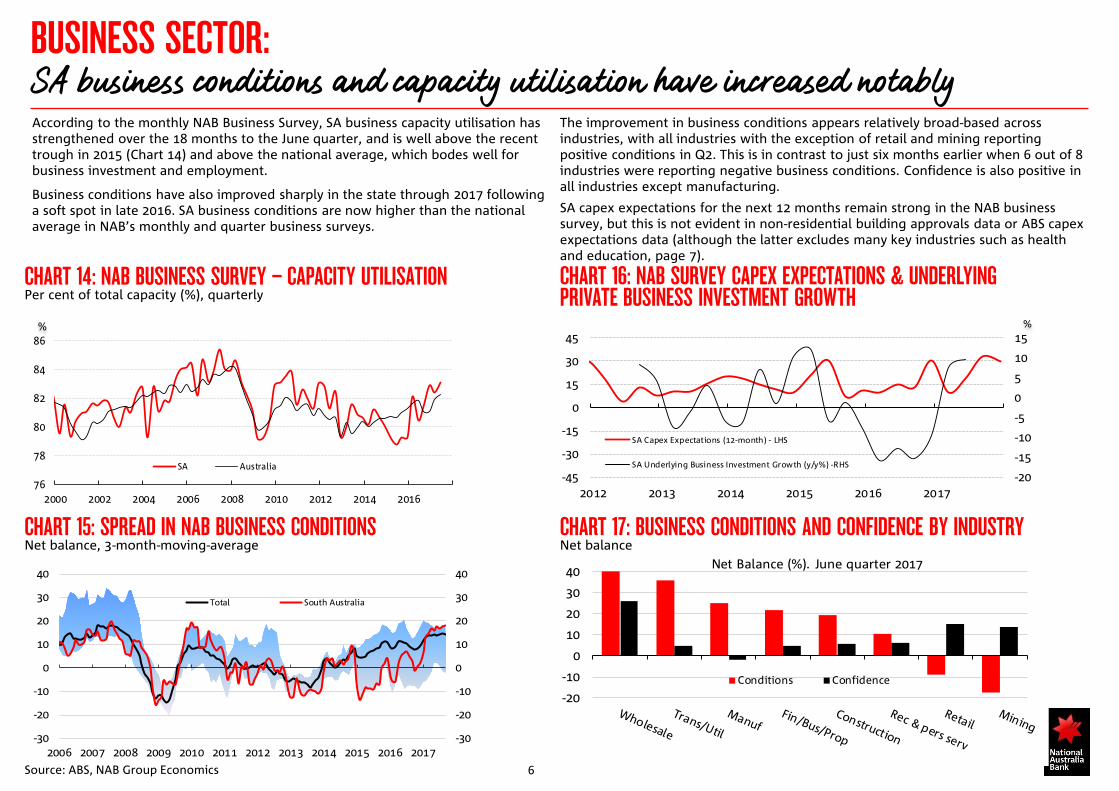

The improvement in business conditions appears relatively broad-based across industries, with all industries with the exception of retail and mining reporting positive conditions in Q2. This is in contrast to just six months earlier when 6 out of 8 industries were reporting negative business conditions. Confidence is also positive in all industries except manufacturing.

SA capex expectations for the next 12 months remain strong in the NAB business survey, but this is not evident in non-residential building approvals data or ABS capex expectations data (although the latter excludes many key industries such as health and education, page 7).

6 Source: ABS, NAB Group Economics

According to the monthly NAB Business Survey, SA business capacity utilisation has strengthened over the 18 months to the June quarter, and is well above the recent trough in 2015 (Chart 14) and above the national average, which bodes well for business investment and employment.

Business conditions have also improved sharply in the state through 2017 following a soft spot in late 2016. SA business conditions are now higher than the national average in NAB’s monthly and quarter business surveys.

CHART 14: NAB BUSINESS SURVEY – CAPACITY UTILISATION Per cent of total capacity (%), quarterly

CHART 15: SPREAD IN NAB BUSINESS CONDITIONS Net balance, 3-month-moving-average

CHART 16: NAB SURVEY CAPEX EXPECTATIONS & UNDERLYING PRIVATE BUSINESS INVESTMENT GROWTH

CHART 17: BUSINESS CONDITIONS AND CONFIDENCE BY INDUSTRY Net balance

76

78

80

82

84

86

2000 2002 2004 2006 2008 2010 2012 2014 2016

SA Australia

%

-20

-15

-10

-5

0

5

10

15

-45

-30

-15

0

15

30

45

2012 2013 2014 2015 2016 2017

SA Capex Expectations (12-month) - LHS

SA Underlying Business Investment Growth (y/y%) -RHS

%

COMMERCIAL PROPERTY/NON-RESIDENTIAL INVESTMENT: Construction activity tracking at low levels, but retail resilient

The decline of automotive manufacturing will also weigh on machinery & equipment investment in the state going forward. Consequently, capital expenditure expectations for 2017-18 are lower than in 2016-17, although we note that these do not include key industries such as health, education and agriculture. Chart 16).

7 Source: ABS, NAB Group Economics

Non-residential building approvals have fallen further, and overall are consistent with a weak outlook for building activity in the state. The drop off has largely been in “other” - this category includes health and may relate to the technical completion of the Royal Adelaide Hospital (which has now been transferred from the private to the public sector). Retail/wholesale building approvals meanwhile have been resilient, despite weak business conditions for retailers. Office approvals are also at low levels, and the recent tick up in the vacancy rate does not bode well for further construction.

CHART 18: NON-RESIDENTIAL BUILDING APPROVALS Million dollars

CHART 19: OFFICE APPROVALS AND VACANCY RATES

CHART 20: SA CAPITAL EXPENDITURE & EXPECTATIONS Actual & expected based on previous realisation ratio ($billion)

0

70

140

210

280

350

420

490

0

10

20

30

40

50

60

70

2002 2004 2006 2008 2010 2012 2014 2016

Retail/Wholesale -LHS Offices - LHS Factories- LHS

Warehouses-LHS Other-RHS

$m

357911131517190

8162432404856

2006 2008 2010 2012 2014 2016

Office Approvals (lhs)

Office Vacancy Rates (inverse, rhs)

%$m

0

10

20

30

40

50

60

NSW VIC TAS SA QLD WA

2012-13 2013-14 2014-15 2015-16 2016-17 2017-18 (e)

-4.0-3.0-2.0-1.00.01.02.0

Q3'

13

Q4'

13

Q1'

14

Q2'

14

Q3'

14

Q4'

14

Q1'

15

Q2'

15

Q3'

15

Q4'

15

Q1'

16

Q2'

16

Q3'

16

Q4'

16

Q1'

17

Q2'

17

Q3'

17

Nex

t 12m

Nex

t 2y

Australia SA/NT

ExpectationsEstimated price growth in relevant survey period

RESIDENTIAL PROPERTY: Housing market slow overall, but price growth has picked up in some places

Meanwhile, regional house prices have accelerated to 5.1% y/y or an average $279K.

The latest NAB Property Survey suggests industry participants expect only very modest price rises for SA/NT in the next two years (Chart 24).

NAB Group Economics’ forecasts for Adelaide houses is for growth of 3.4% in 2017 and 1.7% in 2018. Growth in prices for units/apartments is forecast to be 0.5% in both 2017 and 2018.

8 Source: ABS, NAB Group Economics

Growth in Adelaide dwelling prices remains relatively subdued overall at 2% growth y/y, increasingly lagging behind the 8-capital-city average (Chart 21). This is largely a function of weaker growth in housing demand as a result of slow population growth and population ageing. There has however been a pick up in price growth for Adelaide detached houses to 6% y/y. Price growth for units/apartments is very low at 1% (Chart 22), and varies significantly across suburbs with prices declining in Northern Adelaide but growing strongly in Eastern Adelaide (Chart 23).

CHART 21: ADELAIDE HOUSE PRICES CoreLogic hedonic prices (index)

CHART 22: SA RESIDENTIAL PROPERTY PRICE GROWTH (Y/Y%) Percentage year-on- year growth (%)

CHART 23: ADELAIDE - MEDIAN PROPERTY PRICE GROWTH Percentage growth in the year to Q2 2017 (%)

CHART 24: NAB PROPERTY SURVEY – HOUSE PRICE EXPECTATIONS Percentage growth (%)

-10

-5

0

5

10

15

20

25

-10%

-5%

0%

5%

10%

15%

20%

25%

2004 2006 2008 2010 2012 2014 2016 2018

Adelaide Houses Adelaide Units

Regional Houses

-4 -2 0 2 4 6 8 10

Eastern Adelaide

Northern Adelaide

Southern Adelaide

Western Adelaide

House Prices

Unit Prices

020406080

100120140160

1995 1998 2001 2004 2007 2010 2013 2016

Index

Adelaide Dwelling Prices (lhs)

Capital City Dwelling Prices (lhs)

-10

-5

0

5

10

15

20

25

2002 2004 2006 2008 2010 2012 2014 2016

'000s Natural increase Net overseas migration

Net interstate migration Total population growth

DEMOGRAPHICS: Negative interstate migration continues to weigh on SA’s population growth

SA’s population remains older on average than the national population, and has also aged more quickly, rising to a median age of 40 in 2016 from less than 36 years a decade earlier. SA has the second oldest population after Tasmania. (Chart 27).

SA’s share of the national population continues to decline, as national population growth picks up while SA population growth slows (Chart 28).

9 Source: ABS, NAB Group Economics

South Australia’s population growth has slowed sharply since 2014 and is now at 0.6% y/y (Chart 25). National population growth by contrast has picked up to 1.6% y/y as at Mar-17. The slowdown in SA is largely due to more negative interstate migration (or outflow to other states), while net overseas migration has been broadly stable at a moderate positive rate (Chart 26).

CHART 28: SA SHARE OF AUS POPULATION AND GROWTH IN MIGRATION Quarterly population change (‘000 persons)/SA population as a percentage share of Australian population (%)

CHART 26: POPULATION GROWTH Four-quarter rolling sum (‘000 persons)

CHART 25: SA AND AUS POPULATION GROWTH Year-ended percentage growth (%)

CHART 27: MEDIAN AGE OF POPULATION BY STATE

0.0

0.5

1.0

1.5

2.0

2.5

1982 1986 1990 1994 1998 2002 2006 2010 2014

SA Pop Growth

AUS Pop Growth

%26 28 30 32 34 36 38 40 42 44

AUSNSW

VICQLD

SAWATASNT

ACT

1996

2016

7.0%7.1%7.2%7.3%7.4%7.5%7.6%7.7%7.8%

-3,000-2,000-1,000

01,0002,0003,0004,0005,0006,000

2002 2004 2006 2008 2010 2012 2014 2016

Net overseas migration (LHS)

Net interstate migration (LHS)

Share of Aus population (RHS)

55

57

59

61

63

65

2

3

4

5

6

7

8

2002 2004 2006 2008 2010 2012 2014 2016

Unemployment rate (trend) (LHS)Participation rate (trend) (RHS)Employment to population ratio (trend) (RHS)

2

4

6

8

10

2002 2004 2006 2008 2010 2012 2014 2016

SA Greater Adelaide Rest of SA

LABOUR MARKET: Employment has accelerating, including in traditional areas

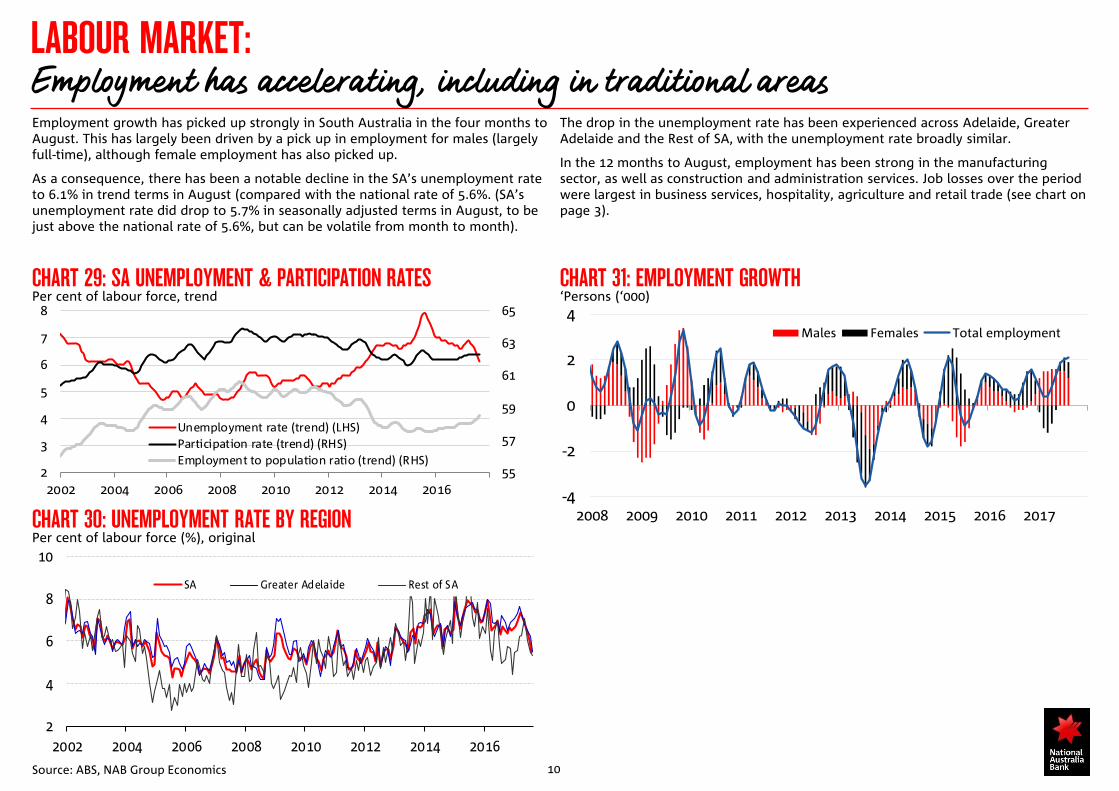

The drop in the unemployment rate has been experienced across Adelaide, Greater Adelaide and the Rest of SA, with the unemployment rate broadly similar.

In the 12 months to August, employment has been strong in the manufacturing sector, as well as construction and administration services. Job losses over the period were largest in business services, hospitality, agriculture and retail trade (see chart on page 3).

10 Source: ABS, NAB Group Economics

Employment growth has picked up strongly in South Australia in the four months to August. This has largely been driven by a pick up in employment for males (largely full-time), although female employment has also picked up.

As a consequence, there has been a notable decline in the SA’s unemployment rate to 6.1% in trend terms in August (compared with the national rate of 5.6%. (SA’s unemployment rate did drop to 5.7% in seasonally adjusted terms in August, to be just above the national rate of 5.6%, but can be volatile from month to month).

CHART 30: UNEMPLOYMENT RATE BY REGION Per cent of labour force (%), original

CHART 31: EMPLOYMENT GROWTH ‘Persons (‘000)

CHART 29: SA UNEMPLOYMENT & PARTICIPATION RATES Per cent of labour force, trend

-4

-2

0

2

4

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Males Females Total employment

CHART 32: COMPOSITION OF EMPLOYMENT & GVA Percentage share (%)

11 Source: ABS, NAB Economics, DFAT

ECONOMIC STRUCTURE AND TRADE Health is the largest sector, and SA’s largest trading partners are in Asia

0% 2% 4% 6% 8% 10% 12% 14% 16%

HealthFinance

ManufacturingConstructionPublic admin

TransportBusiness services

EducationRetail tradeAgriculture

Wholesale tradeUtilitiesMining

Admin servicesRental services

HospitalityOther services

CommunicationsArts

GVA Employment

TABLES 33 & 34: TOP SA EXPORT DESTINATIONS AND IMPORT SOURCE COUNTRIES

The health sector continues to dominate in terms of output and (particularly) employment. The traditional industry pillar of manufacturing has declined as a share of output over time, although as at Q2-17 was the third largest employer, and actually increased marginally as a share of total employment to 10% in the past year, although will face a significant challenge as auto manufacturing shuts down in the coming year. Retail trade remains the second-largest employer, although is the 9th largest industry in terms of output. In 2015-16, finance & insurance services overtook manufacturing as the second largest industry by gross value added production, but remains a relative small employer overall (Chart 32).

The ASEAN bloc and China are SA’s main export and import partners (Chart 33 & 34), followed by the EU and the US, and non-ASEAN countries in Asia such as India, Japan and Singapore.

SA’s top commodity exports in 2015-16 included copper as well as copper ores & concentrates, alcoholic beverages, wheat and meat. SA imports top imports are refined petroleum, passenger motor vehicles, vehicle parts and accessories and goods vehicles (Charts 35 & 36).

Million ($m)

TABLES 35 & 36: TOP SA MERCHANDISE EXPORTS AND IMPORTS

Value of exports ($m)1 ASEAN 23632 China 22703 US 12954 EU 12035 India 9616 Japan 6557 New Zealand 4128 UK 3689 Korea 24610 HK 242

Value of imports ($m)1 ASEAN 20752 China 16913 EU 14904 US 8725 Singapore 8106 Japan 6557 Korea 3618 Germany 2819 New Zealand 20310 UK 157

Major exports, goods, 2015-16 ($m)Copper 1382Alcoholic beverages 1359Wheat 1242Copper ores & concentrates 763Meat (excl beef) 732Beef 536Lead 471Iron ore & concentrates 419Vegetables 288Passenger motor vehicles 275

Major imports goods, 2015-16 ($m)Refined petroleum 949Passenger motor vehicles 714Vehicle parts & accessories 373Goods vehicles 355Alcoholic beverages 256Other ores & concentrates 246Furniture, mattresses & cushions 187Heating & cooling equipment & parts 176Fertilisers (ex crude) 173Rotating electric plant & parts 141

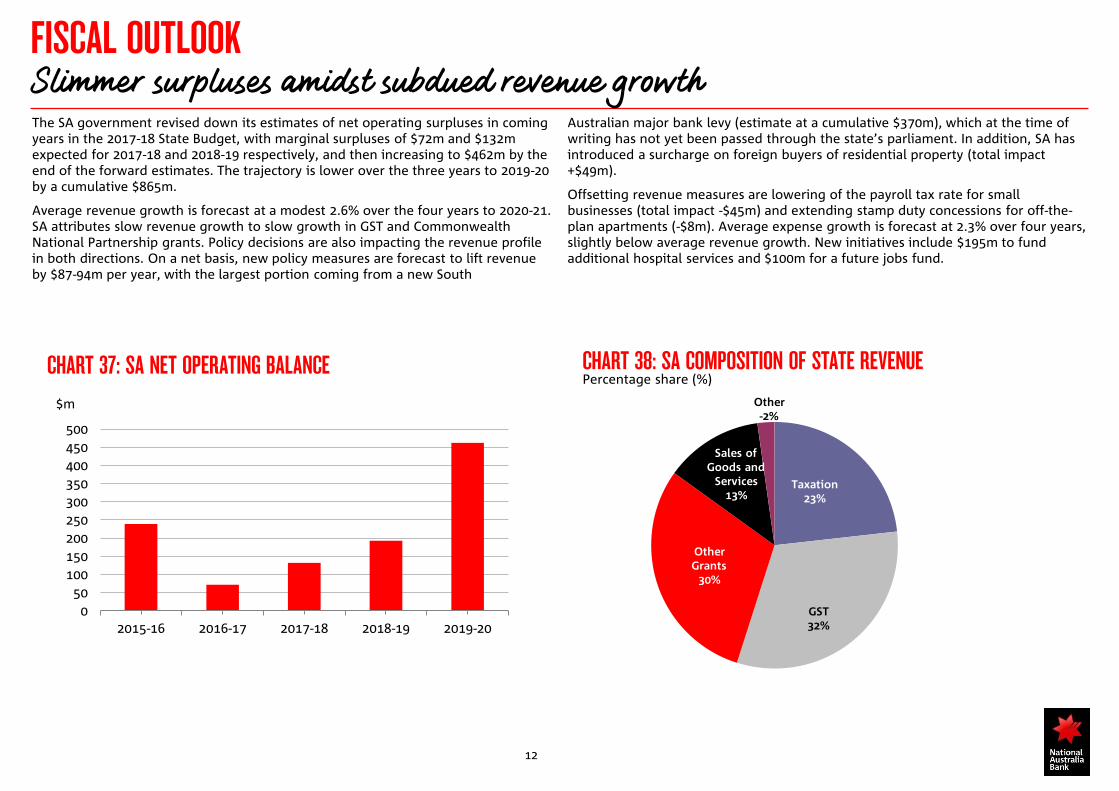

FISCAL OUTLOOK Slimmer surpluses amidst subdued revenue growth

Australian major bank levy (estimate at a cumulative $370m), which at the time of writing has not yet been passed through the state’s parliament. In addition, SA has introduced a surcharge on foreign buyers of residential property (total impact +$49m).

Offsetting revenue measures are lowering of the payroll tax rate for small businesses (total impact -$45m) and extending stamp duty concessions for off-the-plan apartments (-$8m). Average expense growth is forecast at 2.3% over four years, slightly below average revenue growth. New initiatives include $195m to fund additional hospital services and $100m for a future jobs fund.

12

The SA government revised down its estimates of net operating surpluses in coming years in the 2017-18 State Budget, with marginal surpluses of $72m and $132m expected for 2017-18 and 2018-19 respectively, and then increasing to $462m by the end of the forward estimates. The trajectory is lower over the three years to 2019-20 by a cumulative $865m.

Average revenue growth is forecast at a modest 2.6% over the four years to 2020-21. SA attributes slow revenue growth to slow growth in GST and Commonwealth National Partnership grants. Policy decisions are also impacting the revenue profile in both directions. On a net basis, new policy measures are forecast to lift revenue by $87-94m per year, with the largest portion coming from a new South

CHART 37: SA NET OPERATING BALANCE CHART 38: SA COMPOSITION OF STATE REVENUE Percentage share (%)

Taxation23%

GST32%

Other Grants

30%

Sales of Goods and

Services13%

Other-2%

050

100150200250300350400450500

2015-16 2016-17 2017-18 2018-19 2019-20

$m

SEMI GOVERNMENT AND CREDIT OUTLOOK Some budget slippage, but funding needs remain light

SAFA’s term funding requirement for FY17-18 is $2.8bn, which includes $0.1bn of new funding, $2.0bn of maturities and $0.7bn in pre-funding.

SAFA is rated Aa1/stable by Moody’s and AA/positive from S&P. The latest budget slippage suggests S&P is unlikely to act on its positive outlook and upgrade SA’s rating for the foreseeable future.

13

South Australia’s Budget projects slimmer general government surpluses over the next few years. New policy measures have been introduced to increase revenue, including a bank levy, which at the time of writing hasn’t yet passed parliament. Total state net debt is now forecast to rise instead of flattening out in the coming years.

CHART 39: SA NON-FINANCIAL PUBLIC SECTOR NET DEBT CHART 41: S&P CREDIT METRIC: BUDGET PERFORMANCE

METRICS

CHART 40: SAFA TERM BONDS OUTSTANDING

12

13

13

14

14

15

15

16

2016-17 2017-18 2018-19 2019-20 2020-21

$bn

Source: NAB, SA budget

FY-17 BudgetFY17 MYBR

FY18 Budget

Sources: NAB, SA budget

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Adj Operating balance as % of adjusted operating revenues

S&P balance after capital scoring threshold

S%P Operating balance scoring threshold

Balance after capital account as % total adjusted revenue

Budget 17-18

Budget 17-18

MYBR 16-17

MYBR 16-17

0.0

0.5

1.0

1.5

2.0

2.5AUDbn

SAFA bond curve

Issuance as at 30 June 17

Issuance FYTD

FORECASTS BY STATE AND TERRITORY Base effects to drive SA growth higher in 2017-18, before moderation in 2018-19

Source: ABS, CoreLogic, NAB Economics

NAB’s economic forecasts by state and territory are below. For a summary of the outlook by state, please see the States Handbook – Overview which contains links to the detailed handbook for each state and territory.

REAL GROSS STATE PRODUCT AND UNEMPLOYMENT RATE FORECASTS Annual average

14

HEDONIC HOUSE PRICE FORECASTS* Through the year growth to Q4

HEDONIC UNIT/APARTMENT PRICE FORECASTS * Through the year growth to Q4

2015 2016 2017f 2018f 2019f

Sydney 15.5 10.7 5.1 3.7 3.0

Melbourne 15.8 9.5 8.6 5.5 3.4

Brisbane 6.9 2.7 3.1 1.9 1.2

Adelaide 3.8 3.8 3.4 1.7 1.7

Perth -4.2 -2.9 -3.0 0.7 1.2

Hobart 7.0 9.6 10.0 4.9 1.7

Cap City Avg 11.2 7.3 4.6 3.4 2.5

2015 2016 2017f 2018f 2019f

Sydney 13.1 5.8 5.9 0.5 0.6

Melbourne 7.5 4.7 6.4 1.2 -2.4

Brisbane 1.1 -3.0 -1.1 -1.8 -1.2

Adelaide 2.4 0.6 0.5 0.5 0.5

Perth -2.8 -6.3 -1.9 0.4 0.7

Hobart 1.1 6.4 5.7 2.4 0.6

Cap City Avg 8.2 3.5 4.7 0.5 -0.3

15-16 16-17f 17-18f 18-19f 15-16 16-17 17-18f 18-19fNSW 3.5 2.2 3.1 2.5 5.4 5.0 4.7 4.7VIC 3.3 2.9 3.3 2.7 6.0 5.9 5.8 5.4QLD 2.0 2.2 3.2 2.5 6.2 6.2 6.0 5.9SA 1.9 1.8 2.7 1.7 7.3 6.7 6.5 6.5WA 1.9 0.3 3.2 3.0 6.0 6.2 6.2 5.9TAS 1.3 1.0 2.2 1.8 6.5 6.1 6.0 6.0NT 2.7 1.5 1.5 5.0 4.2 3.5 4.0 4.2ACT 3.4 3.0 3.1 2.6 4.5 3.8 4.8 4.8Australia 2.7 2.0 3.2 2.5 5.9 5.7 5.4 5.3

Gross State Product YoY Unemployment RateNAB growth and unemployment rate forecasts for the states