Embed Size (px)

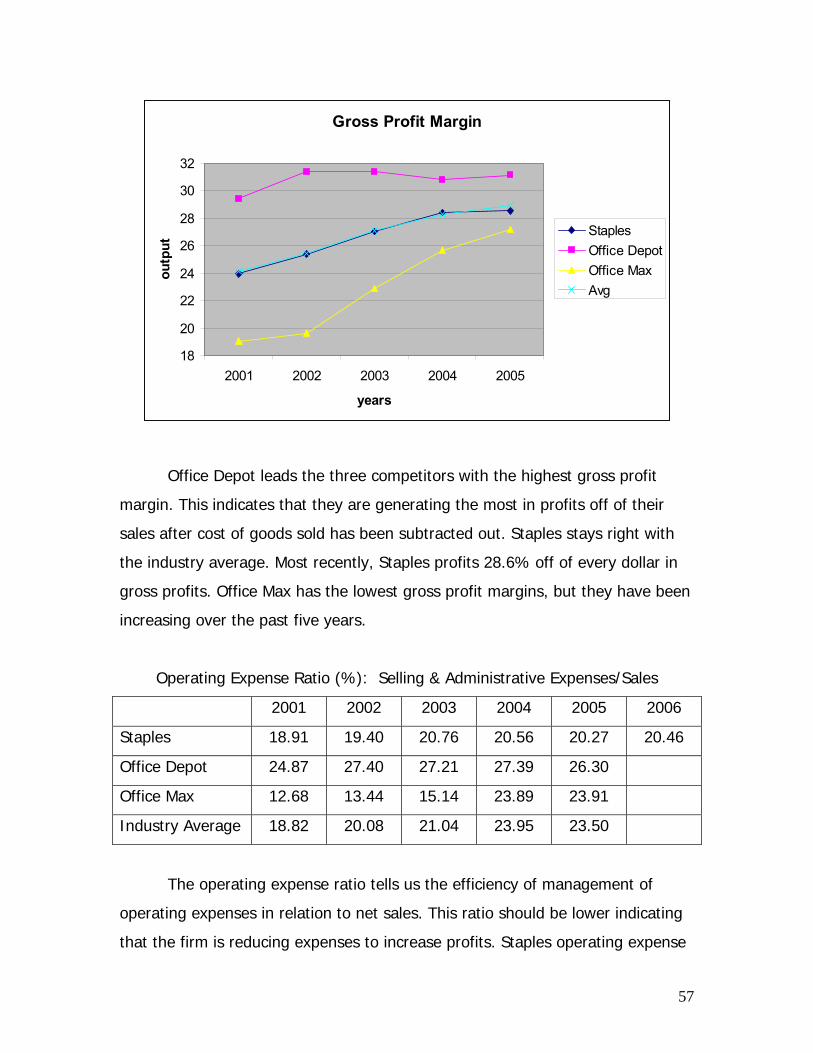

Citation preview

Staples Equity Valuation and Analysis

David Lecky

Chad Loudermilk

Bennett Matkins

Kara Reynolds

Amanda Rhodes

1

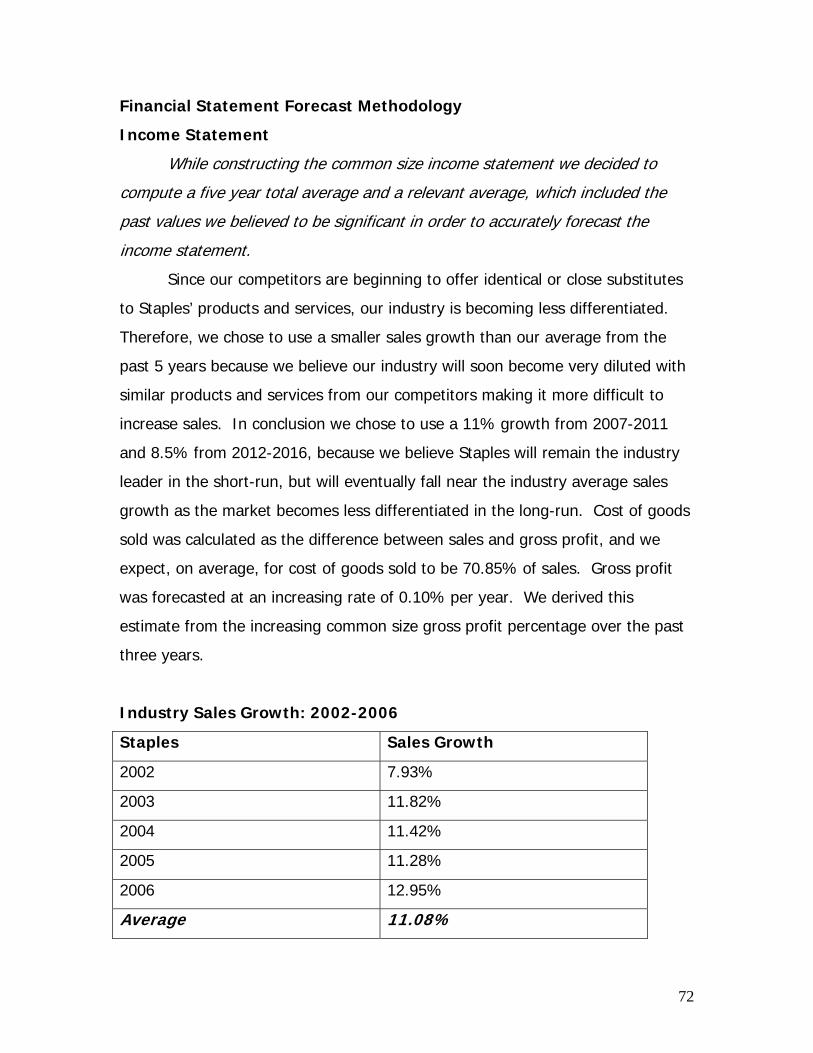

Table of Contents Executive Summary……………………………………………………….. 2 Overview of Staples and the Industry………………………………... 7 Five Forces Model……………………………………………………………………….. 9 Rivalry among Existing Firms……………………………………………………….. 9 Threat of New Entrants……………………………………………………………….. 15 Threat of Substitute Products………………………………………………………. 17 Bargaining Power of Buyers………………………………………………………... 17 Bargaining Power of Suppliers…………………………………………………..... 18 Classifying the Industry………………………………………………………………. 18 Key Success Factors……………………………………………………………………. 19 Competitive Advantage Analysis………………………………………………….. 19 Accounting Analysis………………………………………………………. 25 Key Accounting Policies………………………………………………………………. 25 Accounting Flexibility………………………………………………………………….. 26 Evaluation of Actual Accounting Strategy……………………………………… 29 Quality of Disclosure…………………………………………………………………… 30 Screening Ratio Analysis….…………………………………………………………. 33 Revenue Diagnostics………………………………………………………………….. 34 Expense Diagnostics…………………………………………………………………… 37 Potential “Red Flags”………………………………………………………………….. 39 Undo Accounting Distortions……………………………………………………….. 41 Ratio Analysis………………………………………………………………. 44 Liquidity Ratio……………………………………………………………………………. 44 Profitability Ratio……………………………………………………………………….. 56 Capital Structure Ratio……………………………………………………………….. 66 SGR & IGR………………………………………………………………………………… 71 Financial Statement Forecasting……………………………………… 72 Income Statement……………………………………………………………………… 72 Balance Sheet……………………………………………………………………………. 77 Statement of Cash Flows……………………………………………………………. 80 Analysis of Evaluations………………………………………………….. 83 Cost of Capital………………………………………………………………………….. 83 Method of Comparables…………………………………………………………….. 86 Intrinsic Valuation Models………………………………………………………….. 89 Altman Z-Score…………………………………………………………………………. 96 Appendices: Appendix 1: Screening Ratios…………………………………………………….. 98 Appendix 2: Core Financial Ratios………………………………………………. 99 Appendix 3: Regression Analysis……………………………………………….. 100 Appendix 4: Valuation Models……………………………………………………. 105 Works Cited………..................................................................... 110

2

Executive Summary

Investment Recommendation: Slightly Overvalued: Hold 04/01/07

SPLS - Nasdaq $25.84 EPS Forecast52 week range $21.08 - $28.00 FYE 4/1 2006 (A) 2007 (E) 2008 (E) 2009 (E)Revenue (2006) $18,160,789 EPS $1.32 $1.55 $1.77 $2.01Market Capitalization $18.19 BillionShares Outstanding 717,000,000 Ratio Comparison SPLS ODP OMXDividend Yield .29 (1.1%) Trailing P/E $41.29 $55.99 $37.223-month Avg Daily Trading Vol. 6,120,780 Forward P/E $19.50 $26.44 $17.58Percent Institutional Ownership 84.60% M/B $19.78 $26.72 $72.96Book Value Per Share (mrq) $6.99ROE 22% Valuation EstimatesROA 12.68% Actual Price (as of 4/1/07) $25.84Est. 5 year EPS Growth Rate 13.95% Ratio Based ValuationsCost of Capital Est. R2 Beta Ke P/E Trailing $19.56Ke Estimated 10.24% P/E Forward $15.055-year 0.230 1.146 10.04% Enterprise Value $29.121-year 0.231 1.150 10.19% M/B $3.6810-year 0.230 1.146 9.97%3-month 0.232 1.152 10.24% Intrinsic ValuationsPublished 1.52 Discounted Dividends $3.38Kd 5.547% Free Cash Flows $20.13WACC 9.2292% Residual Income $17.07Altman Z-Score 6.88 LR ROE $12.61

Abnormal Earnings Growth $15.26

Staples stock is traded on the NASDAQ market and the ticker symbol is:

SPLS. The Company had its Initial Public Offering (I.P.O.) on April 27, 1989.

3,250,000 shares sold at $19.00 per share ($0.74 after adjusting for stock splits).

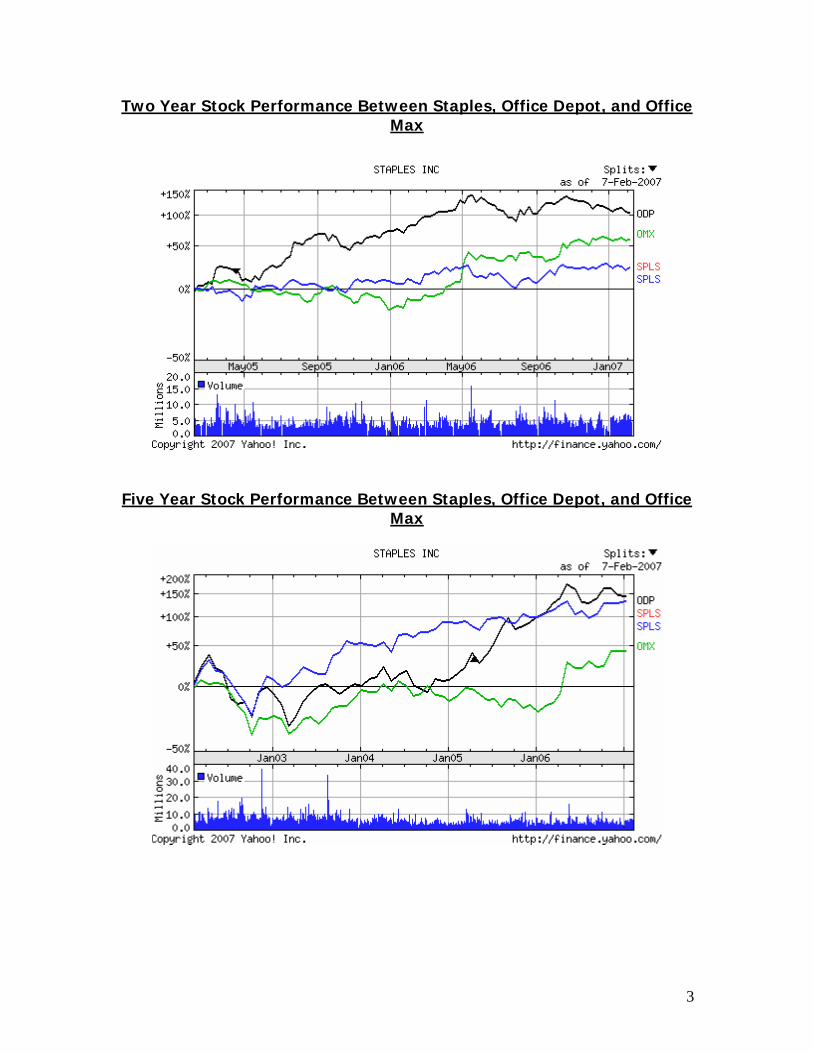

Since 2002, Staples’ stock prices have almost doubled. Their stock prices have

also been fairly consistent with that of its competitors for the past two years.

3

Two Year Stock Performance Between Staples, Office Depot, and Office Max

Five Year Stock Performance Between Staples, Office Depot, and Office Max

4

Industry and Company Overview

Staples Inc. is the world’s largest supplier of office products,

headquartered in Framingham, Massachusetts. Staples competes in the

worldwide office supply superstore industry, with physical locations and an

internet website. Its two main competitors are Office Depot and Office Max.

Staples originated the office products superstore in Brighton, Massachusetts in

1986. They offer a wide variety of office supply products including supplies,

furniture, small business machines, computers, peripherals, and various business

services.

Staples has many key success factors that attribute to its every day

success. One of these main success factors is Staples ability to differentiate itself

form the rest of the competition. Ever since the first Staples opened, the

company has been continuously looking for ways to differentiate itself. One

example of differentiation in the industry that Staples effectively prosecutes is its

ability to offer several different sales channels. These sales channels include

retail stores, catalog, internet, fax, and telephone. Offering all of these sales

channels provides Staples with the capability to reach all of their target market.

In addition, these sales channels also provide customers with an easy and overall

positive shopping experience. Adding to the differentiation concept, Staples

efficiently provides their own brand name items; ultimately giving the company

an extra step ahead of the competition. By providing their own brand name

products, Staples is able to offer a much lower price than the rest of the

products they sell, giving them a competitive advantage. Another competitive

advantage instilled in the Staples Corporation, is the “Easy Service Model” that

was created in 2005. This model introduced the “easy button,” which helped

increase the Staples brand awareness. Additionally this model helped increase

the staples market share from 35% in 2004 to 41% in 2005. This model not only

increased the company’s market share, it also significantly increased their brand

awareness by providing customers with a more positive shopping experience.

5

Accounting Analysis

Staples’ annual 10-K contains information regarding their key accounting

policies and accounting flexibility which can be used to evaluate their accounting

strategies and identify potential red flags. During the process we were able to

conclude that Staples quality of disclosure was superior to its competitors. During

the accounting analysis we were able to relate Staples’ key success factors to

their key accounting policies and identify potential red flags. For example,

Staples finances the majority of their properties with operating leases rather than

capital leases which causes the assets and liabilities to be understated. Also,

since the implementation of SFAS No. 142, Staples has acquired six different

businesses worldwide and has failed to write off any goodwill causing the assets

on the balance sheet to be overstated and the expenses on the income

statement to be understated by a significant amount. After we discovered these

accounting distortions we were able to adjust their accounting methods to

represent true values. We were able to adjust the lease problem by finding the

present value of Staples’ future payments on its operating leases, and increase

the assets and liabilities on the balance sheet by that amount. Also, we

amortized the current value of goodwill over the next ten years down to zero to

make up for Staples failure of not writing off goodwill. After undoing these

accounting distortions, Staples’ true value will be revealed.

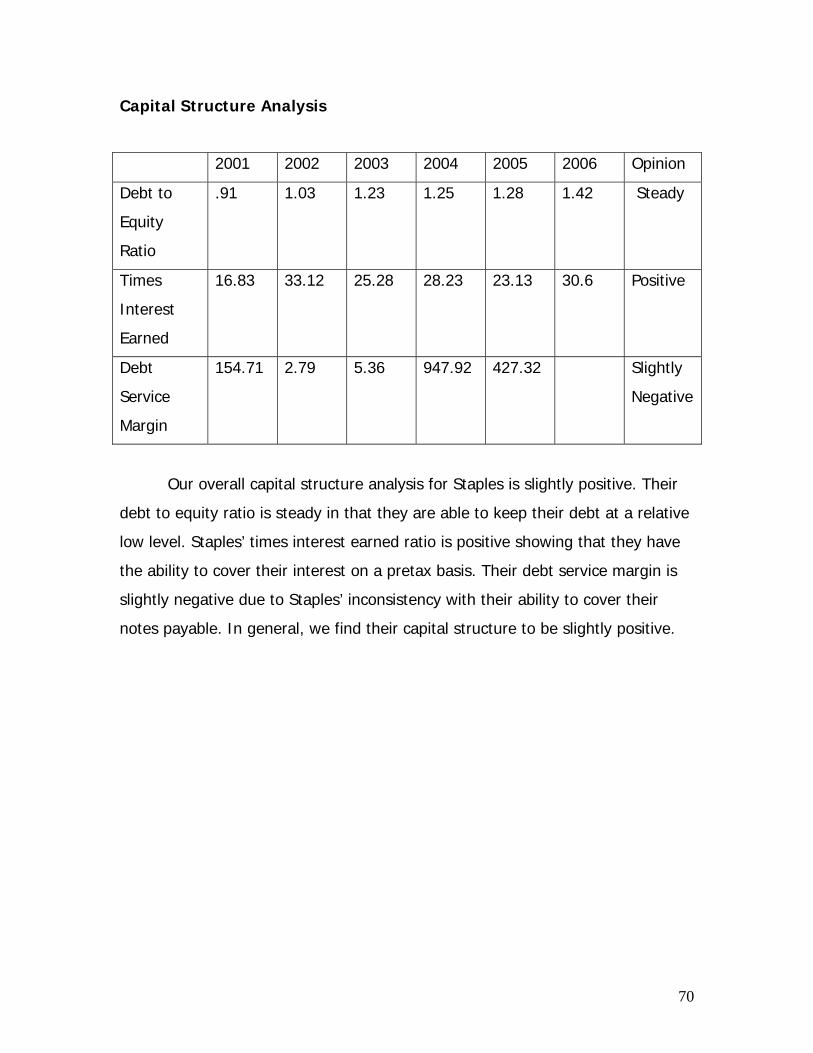

Financial Ratio Analysis

The financial statements for a firm provide significant information that

must be evaluated to analyze their overall performance compared to other firms

in the industry. This analysis provides you with a way to relate different line

items of the financial statements and then assess those relationships. There are

three main groups of ratios: liquidity, profitability, and capital structure. Liquidity

ratios, which determine a firm’s ability to meet current obligations with liquid

assets, include the current ratio, quick asset ratio, accounts receivable turnover

6

and days supply, inventory turnover and days supply, and working capital

turnover. Profitability Ratios, which measure how successful a firm is at

generating a profit, include the gross profit margin, operating profit margin, net

profit margin, asset turnover, return on assets, and return on equity. Lastly,

Capital Structure Ratios determine the sources of financing used to acquire

assets and they include the debt to equity ratio, times interest earned, and debt

service margin. In conclusion, the financial ratio analysis measures the overall

performance of a firm compared to other competitors in an industry.

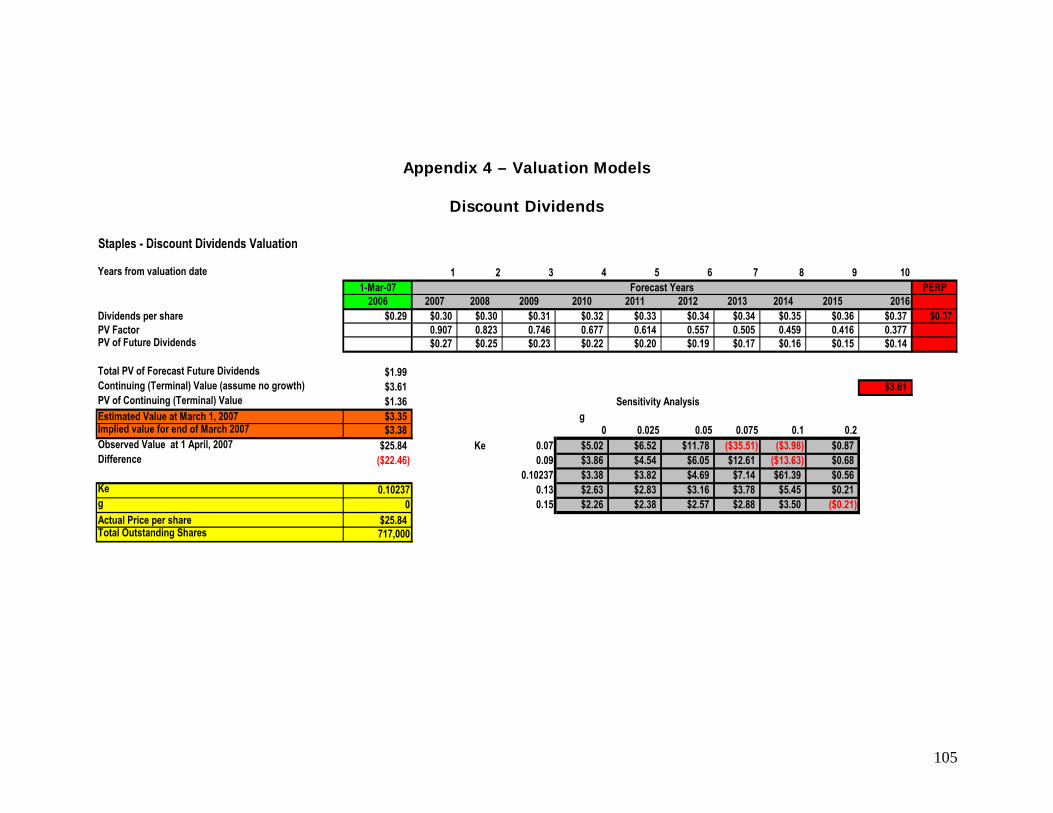

Intrinsic Valuations

After finding the intrinsic values for each of the discount dividends,

discounted free cash flows, residual income, abnormal earnings growth, and long

run residual income perpetuity models, we discovered that Staples is overvalued.

The discount dividends model had a calculated intrinsic value of $3.38, which we

believe to be insignificant because future dividends are relatively difficult to

accurately predict. Next, the discounted free cash flows model resulted in an

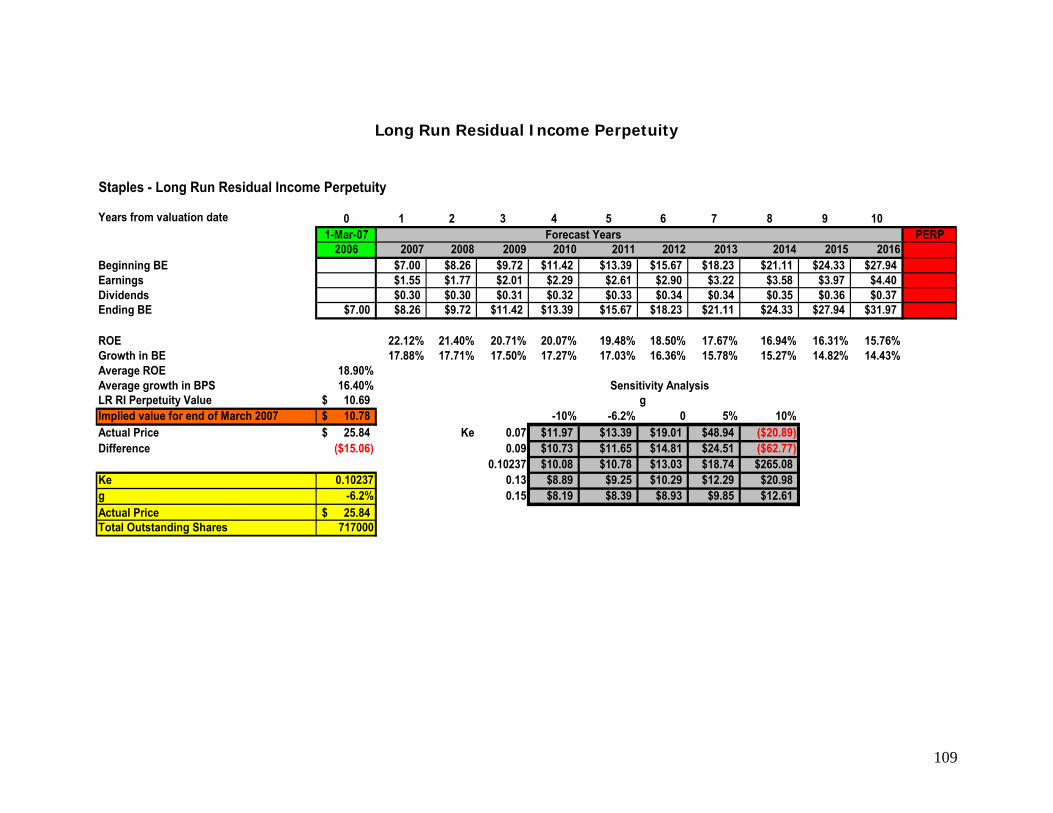

intrinsic value of $20.13, implying Staples is slightly overvalued. The long run

residual income perpetuity model had an intrinsic value of $10.78 which is well

below the observed price of $25.84 at April 1, 2007. As mentioned earlier we

placed the most emphasis on the residual income and abnormal earnings growth

models; we did this because of the link between residual income and abnormal

earnings growth and the significant explanatory power of the residual income

model. The residual income model calculated an intrinsic value of $19.90,

ultimately implying that Staples is again slightly overvalued by $5.94. Lastly, the

abnormal earnings growth model computed an intrinsic value of $22.52, stating

that Staples is slightly overvalued by $3.32. Since, we placed a major emphasis

on the residual income and abnormal earnings growth models, we believe it is

safe to say Staples is a slightly overvalued firm. In addition, the Altman Z-Score

turned out to be 6.88, implying that Staples has a low probability of bankruptcy.

7

The WACC was calculated to be 9.29%, with a cost of equity of 10.237% and a

cost of debt of 5.547%.

Business and Industry Analysis

Company Overview

Staples, Inc. introduced the first office products superstore in Brighton,

Massachusetts in 1986. Launched to serve the needs of small businesses,

Staples, Inc. is a specialty retailer offering a wide array of office supply products

including supplies, furniture, small business machines, computers, and

peripherals. They also offer business services such as color and self-service

copying, printing services, faxing, and pack and ship services. Staples has 1,522

superstores found in 47 states, the District of Columbia, and 11 Canadian

provinces at the fiscal year end of 2005. In addition, 258 stores are found in 19

countries in Europe, South America, and Asia. Staples is continuing to grow with

an average of 119.8 store openings per year over the past 5 years. The company

is headquartered in Framingham, Massachusetts. It also does business via the

Internet, through its own website.

Staples concentrates on superior customer services to differentiate itself

from competitors offering low prices and innovative services. In 2003, Staples

launched its new brand promise: “We make buying office products easy.”

Activating a new customer service model to its employees, offering expanded

product lines, speedy check-outs, in-stock guarantees, and redesigning their

website to make it more customer-friendly are some of the new features Staples

offers to cater to its customers. It currently leads the industry in market

capitalization at 18.6 billion dollars.

8

Staples Sales & Assets

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

Year

$ in

Tho

usan

ds

SPLS SalesSPLS Assets

SPLS Sales $10,744,373 $11,596,075 $12,967,022 $14,448,378 $16,078,852

SPLS Assets $4,093,035 $5,721,388 $6,503,046 $7,071,448 $7,676,589

2002 2003 2004 2005 2006

The office products industry as a whole has been continuously growing

over the past four years. Office Max’s sales have declined in response to Office

Depot and Staples’ sales rapidly increasing. The industry also shows an increase

in individual company assets.

Staples Competitors Sales and Assets (Office Depot & Office Max)

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

$16,000,000

Year

$ in

Tho

usan

ds

ODP SalesODP AssetsOMX SalesOMX Assets

ODP Sales $11,356,633 $12,358,566 $13,564,699 $14,278,944

ODP Assets $4,765,812 $6,145,242 $6,794,338 $6,098,525

OMX Sales $7,412,330 $8,245,146 $13,270,196 $9,157,660

OMX Assets $1,295,750 $7,376,159 $7,542,999 $6,272,142

2002 2003 2004 2005

9

Five Forces Model

The five forces model includes five factors by which to classify the

industry in which a firm is competing. It allows the ability to define the industry

structure and profitability. These five factors include: Rivalry Among Existing

Firms, Threat of New Entrants, Threat of Substitute Products, Bargaining Power

of Buyers, Bargaining Power of Suppliers.

Office Supplies Retail Industry Rivalry Among Existing Firms Moderate

Threat of New Entrants Low Threat of Substitute Products High Bargaining Power of Buyers Moderate

Bargaining Power of Suppliers Low

Rivalry Among Existing Firms

Rivalry among existing firms in an industry influences the average level of

profitability. Competition between existing firms in an industry is determined by

the following factors: industry growth, concentration, differentiation, switching

costs, scale/learning economies, fixed-variable costs, excess capacity, and exit

barriers. The analysis of these factors pertaining to the office products retail

industry shows a high level of competition among existing firms.

The intensity of competition between existing players in an industry

influences the level of profitability. The office products retail industry is highly

competitive among its key competitors of Office Depot, Office Max, and Staples.

These competitors also compete with virtually any company who also offer office

supplies and services, business machines and related products, computers and

related products, and office furniture. These companies include mass

merchants, warehouse clubs, computer and electronics superstores, mail order

firms, contract stationers business, electronic commerce distributors, local

dealers, and direct manufacturers. The office supply superstore industry is very

10

competitive because the key competitors also have to compete against any

company that sells office products.

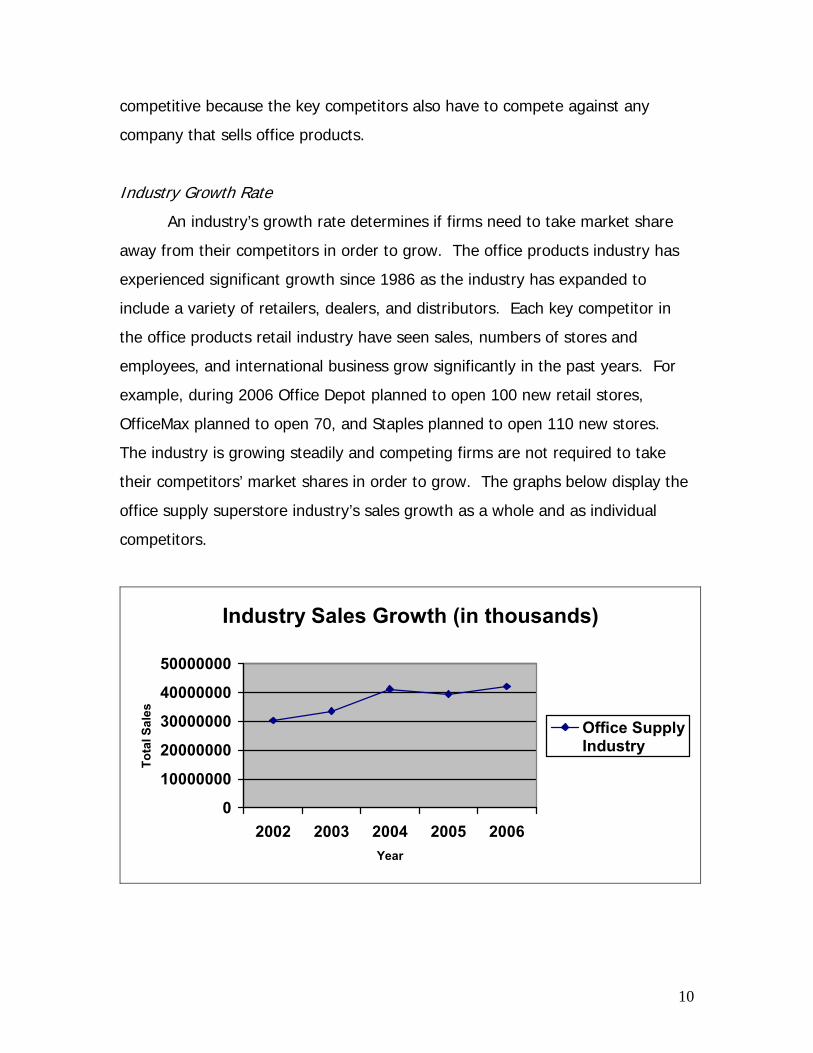

Industry Growth Rate

An industry’s growth rate determines if firms need to take market share

away from their competitors in order to grow. The office products industry has

experienced significant growth since 1986 as the industry has expanded to

include a variety of retailers, dealers, and distributors. Each key competitor in

the office products retail industry have seen sales, numbers of stores and

employees, and international business grow significantly in the past years. For

example, during 2006 Office Depot planned to open 100 new retail stores,

OfficeMax planned to open 70, and Staples planned to open 110 new stores.

The industry is growing steadily and competing firms are not required to take

their competitors’ market shares in order to grow. The graphs below display the

office supply superstore industry’s sales growth as a whole and as individual

competitors.

Industry Sales Growth (in thousands)

0

10000000

20000000

30000000

40000000

50000000

2002 2003 2004 2005 2006Year

Tota

l Sal

es

Office SupplyIndustry

11

SPLS, ODP, OMX Sales (in thousands)

0

5000000

10000000

15000000

20000000

2002 2003 2004 2005 2006Year

Sale

s StaplesOffice DepotOffice Max

Concentration and Balance of Competitors

The degree of concentration and the balance of the competitors in an

industry determine the amount of competition based upon price within the

industry. The office products retail industry’s main competitors are Office Depot,

Office Max, and Staples, but office products are also sold by various firms such

as Wal-Mart, Costco, Best Buy, and Dell. In order to compete with these firms,

office supply superstores have to keep their prices competitive, rely on superior

customer service, broader selection of office products, and convenient store

locations. Since Office Depot, OfficeMax, and Staples are the only main

competitors in the office products retail industry they often cooperate among

themselves to avoid destructive price competition. In conclusion, the office

products retail industry is highly centralized among Office Depot, OfficeMax, and

Staples. The graphs below display the market shares of these competitors in the

office supply superstore industry for the past five years.

12

Market Shares: 2002

39%

37%

24%StaplesOffice DepotOffice Max

For 2002, Staples is the leader owning 39 percent of the office supply

superstore industry. Office Depot is running a close second with 37 percent and

coming in last is OfficeMax with a much lower 24 percent.

Market Shares: 2003

38%

37%

25%StaplesOffice DepotOffice Max

In 2003, Staples remained the leader by a narrow margin of one percent

(38% of industry market share). Following close behind was Office Depot with 37

percent and once again OfficeMax was lagging behind with 25 percent.

Market Shares: 2004

35%

33%

32% StaplesOffice DepotOffice Max

13

In 2004, OfficeMax took a considerable amount of the market share from

its competitors from previous years but remained in last with 32 percent. Again

Staples was the leader in the industry with a lower 35 percent and Office Depot

followed closely with 33 percent.

Market Shares: 2005

41%

36%

23%StaplesOffice DepotOffice Max

For 2005, Staples raised the bar and increased their market share by 6

percent to 41 percent. Office Depot stayed in second with a market share of 36

percent and OfficeMax fell drastically behind to 23 percent.

Market Shares: 2006

43%

36%

21%StaplesOffice DepotOffice Max

In 2006, Staples further increased their market share by 2 percent to a

total of 43 percent. Office Depot remained the same at 36 percent, while

OfficeMax fell further behind to 21 percent.

The above graphs show Staples has remained the office supply

superstore industry’s leader for the past five years. We believe that much of this

success is derived from Staples’ ability to differentiate itself from competitors

while maintaining a low price strategy.

14

Degree of Differentiation and Switching Costs

Firms in any industry must differentiate their products and services in

order to avoid excessive competition. Firms in the office products retail industry

mainly carry identical products or close substitutes to their competitors. In

addition, Office Depot, OfficeMax, and Staples offer similar websites and in-store

copy and print services. Since the products the firms sell and the services they

offer carry a low degree of differentiation, switching costs for customer are very

low. Since, the office products retail industry offers minimal product

differentiation and low switching costs, customers are allowed to switch retailers

purely on the basis of price.

Scale/Learning Economies and the Ratio of Fixed to Variable Costs

If there are any types of scale or learning economies in an industry, firm

sizes become an important factor. When economies of scale exist in an industry,

new firms must be willing and able to invest large amounts of capital in order to

grab market share and compete with industry leaders. In the office products

retail industry there are only three main competitors and large economies of

scale exist making it difficult for new entrants in the industry to compete. Office

Depot, OfficeMax, and Staples therefore compete aggressively for market share.

A firm in any industry must minimize its variable costs in order to maintain

profits. Firms in the office products retail industry are able to obtain low variable

costs by purchasing supplies in bulk from vendors. Also, Staples is able to

further reduce their variable costs by selling their own branded products which

cost 10-15% less than national brands. Firms in the office supply superstore

industry are able to reduce their variable costs allowing them to maintain profits.

Excess Capacity and Exit Barriers

If capacity in an industry is larger than customer demand, there is a

strong incentive for firms to cut prices to fill capacity (Palepu 2-3). High levels of

inventories associated with the office products retail industry create an excess

15

capacity because it creates more supply than demand. The excess capacity can

require firms to cut prices to fill capacity. Exit barriers make it difficult and costly

for firms to exit the industry. The office products retail industry typically does

not have specialized assets or legal barriers. Therefore the exit barriers to the

industry are not costly.

Threat of New Entrants

Economies of Scale

Economies of scale exist within an industry when companies expand the

scope of their operations, resulting in a subsequent decrease in costs for

companies competing within that industry. When economies of scale exist, new

entrants must be willing to invest large amounts of capital in order to compete

with the industry’s leading companies. It is important for a company to

recognize where economies of scale exist because they help the company

understand where its resources should be allocated in order to improve market

share and increase profits. Leading companies within the office product retail

industry, such as Staples and Office Depot, specialize in selling a wide variety of

products in-store. In 2005, Staples’ merchandise inventories were 40% of the

company’s total current assets. A company entering the office products segment

of the specialty retail industry must possess bargaining power with suppliers and

enough capital to acquire, and maintain, a large in-store merchandise inventory,

or the company will not survive in the industry. Another barrier to new entrants

is their limited access to markets. Larger companies have greater access to

markets and can operate with larger geographic reach. Office Depot, for

example, operates 1,016 stores in 49 different states and plans to continue to

open new locations. Staples and its competitors benefit from economies of scale

in advertising as well. In 2005, Staples unveiled the Easy marketing message

which enhanced Staple’s brand promise to make buying office products easy.

Because of increased buying power, market accessibility, and efficient

16

advertising, large economies of scale exist within the office products segment of

the retail industry.

First Mover Advantage

In an industry where price competition and switching costs are minimal, a

company must create a first mover advantage in other aspects of the business.

For example, according to finance.yahoo.com, Office Max recently announced

that it plans on installing the newest, state-of-the art Xerox systems that will

allow customers to produce their work faster and with greater quality. In this

industry, companies create a first mover advantage by introducing innovative

customer service techniques, providing new services to customers first,

introducing new product lines, and expanding into untapped markets globally,

which can be quite costly; therefore, first mover advantage is of moderate risk.

Access to Channels of Distribution and Relationships

Companies in the office supplies retail industry differentiate themselves by

offering superior product variety. To achieve this, it is critical for companies in

this industry to implement efficient inventory methods in order to maintain on-

shelf products. Companies, such as Staples and Office Depot, receive efficient

inventory volumes through retail distribution centers that purchase products

directly from manufacturers. Many of the products sold in these stores come

from competing manufacturers which adversely affects manufacturer relations.

The result of this adverse affect could be that vendors reduce product offerings

in leading office supplies retail companies. Also, many companies in this industry

sell products sourced from a wide variety of third-party vendors, including

international manufacturers. This is a risk factor because leading companies in

this industry cannot control the availability of the raw materials used to make

their products or the stability of foreign supply chains; therefore, companies in

the office supplies retail industry face a high risk of new entrants because of

competition between manufacturers and uncontrollable third-party vendors.

17

Legal Barriers

In this specialized segment of the retail industry prospective entrants do

not face many legal barriers to entry. Licensing regulations, patents, and

copyrights are non-existent within this industry. The only legal barrier to entry is

if a prospective entrant might want to begin Internet operations. There are laws

and regulations that must be followed when conducting business transactions on

the Internet. Because of the absence of extensive legal barriers to entry, this

industry faces a high risk of entrants into the market.

Threat of Substitute Products

The threat of substitutes depends on the relative price and performance

of competing products or services and the customers’ willingness to substitute

(Palepu 2-4). The office products retail industry competes mainly on the basis of

pricing, product selection, convenient locations, and customer service.

Competitors in the industry offer identical products and services and close

substitutes. For example, Office Depot, OfficeMax, and Staples all sell similar

office supplies, technology products, and furniture to consumers. Therefore, the

threat of substitute products among firms in the industry is very high.

Bargaining Power of Buyers

Competitors in the office products superstore industry do compete on the

basis of price. Office products superstores sell office supplies and services to a

large assortment of customers including individual consumers, small, medium,

and large businesses, and government offices. Switching costs for the industry

are low because buyers can find identical products and services or close

substitutes among competitors. Since the products and services have a low level

of differentiation, the bargaining power of buyers increases. Staples is the

world’s leading office products company so they can maintain an effective

bargaining position with vendors. Staples purchases in high volumes and has

centralized distribution facilities allowing them to obtain favorable pricing from

18

their carefully selected suppliers. This in turn helps them offer low price

products in the price sensitive office products industry. In conclusion, Staples

has a moderate bargaining power with its buyers.

Bargaining Power of Suppliers

Suppliers retain bargaining power when they are able to extend enough

pressure on a company to affect its inventory volumes and margins.

Understanding whether or not suppliers exhibit bargaining power within an

industry is important because it aids in analyzing many important factors of the

industry, including selling prices and costs of inventories. The suppliers of the

office supplies retail industry exhibit weak bargaining power for many reasons.

One main reason the bargaining power of suppliers in this industry is weak is

because leading companies, namely Staples, Office Depot, and Office Max,

provide their customers with a wide variety of similar products that come from

competing suppliers. In other words, there is a high concentration of suppliers

selling to small number of leading office supply retail chains. Because Staples,

Office Depot, and Office Max aggregately control most of the industry’s market

share, to maintain high profits from sells of high volume purchase orders,

suppliers must compete with one another to ensure their product is on the

shelves of one of these leading companies. Any one of these three companies

could sustain their bottom line profits if one supplier pulled its products;

therefore, the threat of suppliers bargaining power within this industry is low.

Competitive Advantage Analysis

Classifying the Industry

The office supplies retail industry is a highly competitive industry with

Staples, Office Depot, and Office Max leading the way. It is important for us to

analyze the industry as a whole in order to establish a better understanding of

how Staples creates its own value. Firms in this industry compete on the basis

of offering everyday low prices and high product selection, but each firm must

19

differentiate itself from the competition in order to maintain, or possibly increase,

market share. In the following sections, we will discuss the key success factors

of the office supplies retail industry, as well as explain how Staples implements

business techniques on the basis of these factors.

Key Success Factors of the Industry

The year 1986 marked a revolutionary change to the office products

industry with the introduction of Staples and Office Depot. Before the opening of

these two companies, the office products industry contained a very small amount

of companies and was not a very attractive or competitive industry. Today, this

industry is a very competitive one with many different innovations and company

tactics.

This industry has experienced continual growth since 1986 as it has

acquired many different retailers, dealers, and office supplies distributors.

Leading this dominant industry, Staples currently has over 69,000 employees

operating around 1,800 stores world wide. Office Depot comes in a distant

second with approximately 1,400 stores and 50,000 employees around the

world. The third largest company in the office products industry is OfficeMax with

nearly 1,000 stores and 40,000+ associates. These three prestigious players

“account for annual sales of roughly $30 billion in a North American and

European sales valued at more than $200 billion, (Findarticles.com).”

In such a competitive industry, corporate strategies play a significant role

in the success and survival of a firm. One major focus that is pursued by

companies in this industry is that of differentiation. Differentiation is the act or

process of differentiating oneself from the competition to attract customers. One

way that these three leading companies differentiate themselves from the rest of

the competition is that they all offer several different sales channels including

retail stores, catalog, internet, fax, and telephone. These different sales channels

create a competitive advantage for Staples, Office Depot, and OfficeMax by

permitting them to reach all or most of their target markets as well as providing

20

a much more convenient way of shopping for their customers. Offering all of

these sales channels also helps the firms to obtain a more efficient production

process, which in turn ultimately cuts down production costs. Another very good

example of product differentiation in the industry is the 2005 change in the

availability of Staples’ products. The office supply leader “and Ahold announced,

in March of 2005, a joint collaboration in which all Stop & Shop Supermarkets

and Giant Food Stores throughout the Northeast will have a Staples branded

store-within-store section that will sell traditional school and home office

products in addition to copy and photo paper, ink cartridges, and technology

products. In August 2006, Ahold announced the addition of the Staples section

to all Tops Friendly Markets locations as well, (en.wikipedia.org).” The next value

adding corporate strategy that is a key component of industrial survival is

customer value. Customer value is obtained by offering products or services that

retain the most benefits at the most reasonable price in the eyes of the

customer. A very strong competitive advantage that the large office supply

company’s have is their ability to maintain their own brand name items.

Operating in this industry for many years, these companies have a much larger

collection of knowledge about the needs of their customers and they can better

meet these needs by customizing, producing, and offering their own product. In

addition, these firms can sell their product at a much lower price than the rest of

the products on their shelf, such as “Staples’ brand products are priced 10-15

percent lower than the national average,” giving them a better opportunity to

achieve a higher customer value, (edgarscan.pwcglobal.com).

A recently new trend of major companies in the office products industry is

the transition of competing in multiple industries as opposed to only one. For

instance, Office Depot and Staples have both began to offer services in the

multi-billion dollar copy and print market. By offering these various services,

including high-speed, color and self-service copying, faxing, and pack and ship

capabilities, these two empires create a much larger target market and greatly

increase their opportunities for potential growth. An additional opportunity to

21

increase growth in the office products industry that begun in the late 1990’s

among the larger firms was the expansion to foreign markets. Many of the larger

firms were and still are looking to expand their horizons by entering into foreign

markets, most popular being Europe and China. One of the first companies in

this industry to obtain access to international markets was Office Depot. In 1998,

“Office Depot received government antitrust clearance for its $2.6 billion

acquisition of Viking Office Products,” (Findarticles.com). The wholly-owned

subsidiary operated in 11 countries at the time of acquisition and currently

operates in over 16 countries. Additionally, this attainment significantly increased

the purchasing power for Office Depot, giving them a much stronger ability to

expand and invest in their brand image. This is evidence that expanding into

foreign markets will ultimately ensure growth and create a powerful competitive

advantage over the rest of the industry.

To this day, the office products industry continues to grow at a very rapid

pace. In order to compete with the competition, firms are forced to develop

many different techniques in there day to day promotions and activities. The

three main firms in this industry, Staples, Office Depot, and OfficeMax, work very

hard everyday to maintain their market share by differentiating their product as

well as promoting their brand image. Unfortunately, to survive in this industry

there are many other key components that must be considered including being

the low cost leader, providing quality in their products as well as their customer

service, and achieving efficient production. Without the majority of these

concepts entrusted in to your company strategy, your chances of survival are

slim to none.

Staples’ Competitive Advantages

Staples retains competitive advantages over top industry firms on a

differentiation and cost leadership basis. In the following paragraphs, we will

explain how Staples utilizes its core strengths to achieve these competitive

22

advantages that ultimately create value for the firm and help to sustain market

share.

Customer Service

In 2003, Staples conducted extensive research in order to pinpoint what it

was that customers really wanted when shopping for office products. The

results of the research showed that customers placed significant value on an

easy shopping experience. Staples aims to provide such a shopping experience

for their customers through a number of different business techniques.

To promote an easy shopping atmosphere, Staples rearranged all of its

North American stores to a customer-friendly layout, also known as the Dover

format. This layout opened the interior of the store to give the customer a

better view of Staples’ extensive product array. In addition to this layout

change, the company increased the number of sales associates in the furniture,

business machines, and technology sections of the store because customers

often need assistance in these areas. In 2005, Staples created an “Easy service

model” which helped to increase the knowledge of sales associates and

encouraged them to engage customers in a more effective manner.

Staples also provides many services to its customers which help to

increase customer service. Recently, Staples unveiled its new EasyTech service.

As of January 30, 2007, every Staples store in the U.S. will have an “in-store

technician that provides customers with assistance in computer installations, data

protection and security, and repair and troubleshooting”. (finance.yahoo.com) In

addition, every Staples retail location offers customers copy, fax, and pack and

ship services.

When it comes to customer service, Staples utilizes this value additive

factor extremely well. By providing its customers with an easy-to-shop

atmosphere, friendly sales associates, and numerous services, Staples retains a

high percentage of customers which ultimately helps the company to maintain a

competitive advantage over its competitors.

23

Brand Image

Exceptional brand images are instantly evoked, positive, and almost

always unique among competitive brands. Brand image can be reinforced by

brand communications, such as packaging, advertising, promotion, customer

service, word-of-mouth and other aspects of the brand experience. Staples’

brand image is one of the key ingredients to the success of the company; it is

exclusively centered on the brand promise “we make buying office products

easy”, which was established in 2003.

One way Staples preserves this brand image is through its broad array of

sales channels, which includes retail stores, catalog, and Internet. These sales

channels offer customers the ability to conveniently purchase Staples’

merchandise in the comfort of their home or at well-planned retail locations. By

offering customers numerous ways to purchase products, Staples presents

customers with an easy shopping experience while at the same time increasing

awareness of its name. Increasing brand awareness provides Staples with the

opportunity to establish a positive brand image among new customers, which

could ultimately increase market share. The success of the new brand image

repositioning is evident in the numbers. In 2005, two years after the “easy”

corporate image unveiling, Staples’ market share, when compared with Office

Depot and Office Max, was 40.7%. Office Depot’s market share that year was

considerably lower than Staples’, and Office Max’s market share actually dropped

that year to 23%.

Input Costs

In the year 2000, California experienced an electricity crisis in which the

demand for electricity was rising so rapidly that it eventually began to break

price records across the state. In response to this crisis, Staples, Inc. teamed up

with the energy consulting firm Energy Logic, Inc. in order to figure out a way to

help lower their record breaking electricity cost. With funding from the California

24

Energy Commission, they devised a plan to install wireless control technology

that would allow them to reduce the lighting and HVAC loads at most of their

California locations. Staples associates could send electronic pages from the

internet to reduce the electricity consumption at selected stores. In addition,

Staples also had modem-enabled utility meters installed at each of the stores in

order to verify the load reductions. “Staples now has the ability to curtail up to

2.8 MW of demand within minutes from their Massachusetts headquarters

without affecting customer comfort. This not only leads to significant savings in

demand charges during peak periods, but also strengthens the reliability of

regional electricity supplies in the event of a Stage 2 or Stage 3 emergency,”

(energy.ca.gov). This program not only significantly lowered Staples from the

possibility of a blackout; it also saved the company large amounts of money, as

well as made them allegeable to participate in a California Independent System

Operator program. This program offered incentives for each kW reduced during

peak demand times. All in all, Staples was able to take advantage of real-time

pricing by creating a system that could wirelessly reduce electricity demand at

119 different locations with the “touch of a button.” In addition, this design gave

Staples the ability to considerably lower their input cost as well as track the

electricity demand patterns for review to make further efficiency improvements.

(Baseline vs. Curtailed Graph;.energy.ca.gov)

Conclusion

Staples is able to utilize its competitive advantages over its competitors

because of many different successful business strategies. Staples is capable of

retaining customers due to its provision of superior customer service and brand

image. It also takes a cost leadership position through techniques to lower its

input costs, which increase profit margins. These competitive advantages are

the key contributions to Staples’ increased market share in the office supplies

retail industry.

25

Accounting Analysis

“The purpose of the accounting analysis is to evaluate the degree to

which a firm’s accounting captures the underlying business reality,” (Business

Analysis and Valuation). Reviewing a firms accounting policies and looking for

areas with accounting flexibility allow analyst to assess the extent of distortion in

a company’s accounting numbers. The analyst must then follow with the next

step in the accounting analysis which is to undo any of these distortions. This is

done by recasting the firm’s accounting numbers ultimately producing unbiased

accounting data.

Key Accounting Policies

The key accounting policies of a firm are extremely important because

they relate directly to the firm’s key success factors. In our analysis of Staples’

competitive advantages, we determined that the firm creates its competitive

advantages by utilizing both a low cost strategy and a strategy of differentiation.

Staples is in the office supplies retail industry, which facilitates growth and

profitability by increasing its number of stores, entering into economies of scale

by acquiring competition, and investing in the firm’s brand image. The types of

leases used to increase operations, the creation of goodwill, and the

advertising/marketing expenses incurred to invest in brand image must be

examined when implementing the firm’s key accounting policies.

To utilize its key success factor of increasing operations, Staples must

continue to increase its number of retail stores and distribution centers.

According to the firm’s most recent 10-K, Staples leases almost all of their new

stores and distribution centers. While Staples does acquire some of these new

locations by way of capital leases, a majority of them are leased by way of

operating leases. Accounting policies related to these leases are important to

examine because they affect important items on the firm’s balance sheet.

26

In order to compete on a low cost basis, Staples must decrease

competition within the industry by entering into economies of scale. The firm

does this by acquiring other companies. The accounting policies associated with

these events involve the addition of goodwill to the balance sheet. “Goodwill is

the excess purchase price over the fair value of an acquisition.” (2005 10-k, C-

13) Goodwill is recorded on the balance sheet as an intangible asset and should

be evaluated annually for impairment by the firm.

In 2003, Staples completely changed their brand image. It was at this

time that the “Easy” marketing strategy was created; one of the most dominant

key success factors for Staples. When people see the “Easy button”, they

immediately correlate it to the Staples name, whether it is positive or negative.

This costly investment in the Staples brand image allows the firm to compete on

a differentiation strategy; another major key success factor for the office supply

company. Advertising expenses are involved in accounting for this investment in

brand image. Staples has spent millions of dollars over the past few years

developing new techniques to increase customer awareness in the Staples’ brand

image. The accounting for these advertising expenses is a key accounting policy

because it deals directly with one of Staples’ most important key success factors,

investment in brand image.

Accounting Flexibility

Accounting flexibility allows management to manipulate and control their

reported numbers on their financial statements and reports. Staples is allowed

various amounts of accounting flexibility in their key accounting policies and

estimates when disclosing financial information. Staples’ key accounting policies

relate to their key success factors included in their mixture of cost leadership and

differentiation strategies.

Many of Staples’ key success factors fall under the differentiation

category. For example, Staples is able to provide more flexible delivery and

brand image through their various sales channels including retail, catalog,

27

internet, fax, and telephone methods. Furthermore, Staples normally expenses

advertising costs, with the exception of their catalog costs which are capitalized

and amortized over the life of the catalog giving the firm a form of accounting

flexibility.

Another way Staples is able to differentiate themselves is by creating

customer value and additional brand image by offering numerous services while

competing in multiple industries. For example, Staples offers high-speed, color,

and self-service copying, faxing, and packaging and shipping services to

customers. Also, Staples is expanding globally into foreign markets. Since

Staples adopted the Statement of Financial Accounting Standard No. 142 on

February 3, 2002, they have acquired six businesses world wide: Officenet,

Pressel Versand International, Malling Beck, Globus Office World, Guilbert, and

Medical Arts Press.

The businesses Staples acquired since the change in accounting policy,

included goodwill. SFAS No. 142 requires firms to no longer amortize goodwill

and intangibles with indefinite lives. Instead management of firms is permitted

to estimate these assets’ impairments and they are allowed to determine how

much goodwill to write-off. “Staples uses the fourth quarter to complete its

annual goodwill impairment tests, and as a result management has determined

no impairment charges have been required toward goodwill since they adopted

SFAS No. 142” (Staples’ 10-K). Since this change in accounting policy, Staples’

management has been offered greater accounting flexibility when deciding if

goodwill and intangibles with indefinite lives should be written off. The following

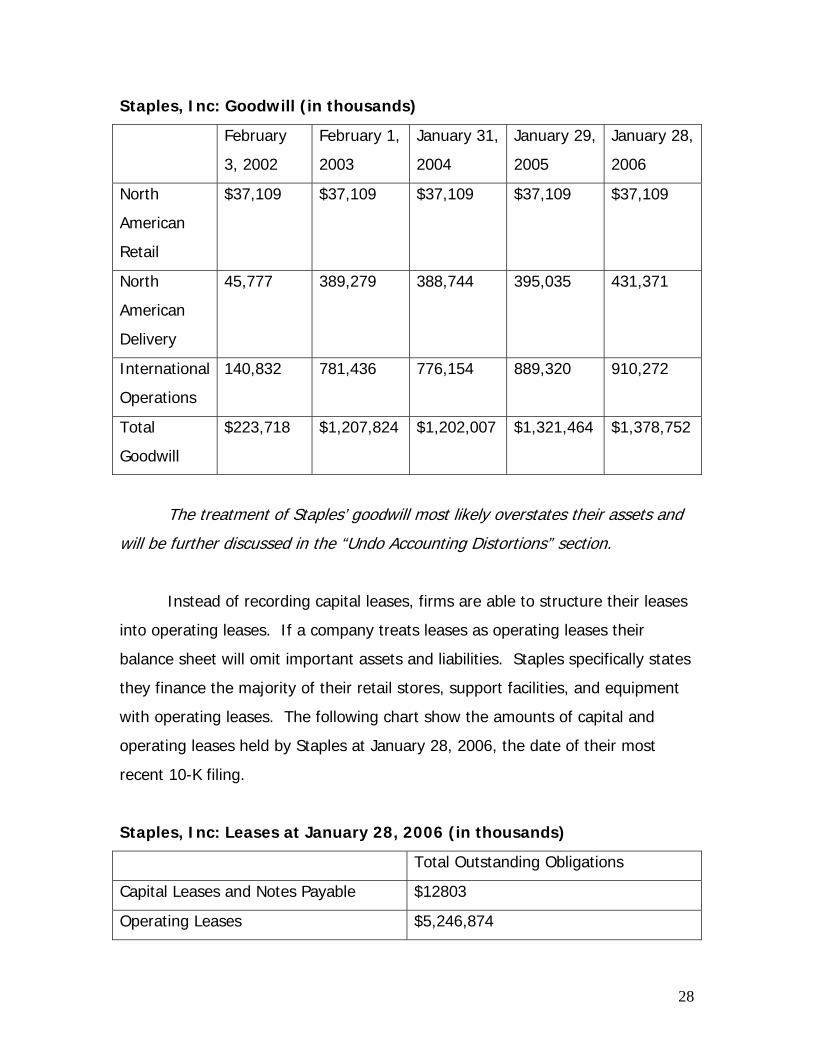

chart shows the steady increases in goodwill since the adoption of SFAS No. 142

on February 3, 2002.

28

Staples, Inc: Goodwill (in thousands)

February

3, 2002

February 1,

2003

January 31,

2004

January 29,

2005

January 28,

2006

North

American

Retail

$37,109 $37,109 $37,109 $37,109 $37,109

North

American

Delivery

45,777 389,279 388,744 395,035 431,371

International

Operations

140,832 781,436 776,154 889,320 910,272

Total

Goodwill

$223,718 $1,207,824 $1,202,007 $1,321,464 $1,378,752

The treatment of Staples’ goodwill most likely overstates their assets and

will be further discussed in the “Undo Accounting Distortions” section.

Instead of recording capital leases, firms are able to structure their leases

into operating leases. If a company treats leases as operating leases their

balance sheet will omit important assets and liabilities. Staples specifically states

they finance the majority of their retail stores, support facilities, and equipment

with operating leases. The following chart show the amounts of capital and

operating leases held by Staples at January 28, 2006, the date of their most

recent 10-K filing.

Staples, Inc: Leases at January 28, 2006 (in thousands)

Total Outstanding Obligations

Capital Leases and Notes Payable $12803

Operating Leases $5,246,874

29

Staples’ also attempts to differentiate themselves from their competitors

by offering an “easy” shopping experience. In order to do so Staples rearranged

all of their North American stores to a customer friendly layout, called the dover

format. The layout opened the interior of the store to give the customer a better

view of Staples’ extensive product array. To account for these improvements,

Staples capitalizes and amortizes these costs in the leasehold improvements

account.

Staples has an ample amount of accounting flexibility when accounting for

advertising costs, goodwill, and leases. The accounting flexibility they have help

management manipulate and manage their reported numbers on their financial

statements and reports.

Evaluation of Actual Accounting Strategy

When evaluating the actual accounting strategy of a firm, it is important

to analyze the accounting policies relative to other leading competitors within the

same industry. It is also critical to relate these accounting strategies to a firm’s

key success factors, which are the most apparent value additives to a firm.

Because Staples, Office Depot, and Office Max possess many similar key success

factors, they do, for the most part, implement similar accounting strategies. In

the following paragraphs, we will identify Staples’ actual accounting strategies of

its key success factors as well as relate them to the accounting strategies of

other leading firms within the industry

Staples’ management has chosen to establish a mixture of aggressive and

conservative accounting policies. For example, Staples’, Office Depot, and Office

Max normally expense advertising costs, but each company has chosen to

capitalize the costs of catalog production, which totaled $28.4 million in 2005

and $30.8 million in 2006. This is an aggressive accounting practice because it

hides advertising expenses in the company’s assets which ultimately increase net

income.

30

Staples and Office Max both take an aggressive stance when it comes to

goodwill impairment. Neither company has recognized an impairment expense

since 2001 which raises a red flag because the assets of both companies might

be overstated. “Managers can use their reporting judgment to delay write downs

on the balance sheet and avoid showing impairment charges in the income

statement” (Palepu, 4-8). The affect of not impairing goodwill each year

increase Staples’ assets by billions of dollars. At the beginning of 2003, Staples

had $1,207,824,000 worth of goodwill. This goodwill was not impaired at the

end of the year, therefore; the assets were overstated and expenses were

understated by a significant amount.

All of the competitors in the office supply superstore industry tend to

avoid capital leases and, instead, expense them as operating leases. For

example, on January 28, 2006 Staples recorded total outstanding lease

obligations amounting to $12,803,000 of capital leases and notes payable, and

$5,246,874,000 of operating leases. This type of aggressive accounting policy

excludes vital lease assets and liabilities from the balance sheet, understating

assets and liabilities.

Overall, the office supplies superstore industry is one that uses

moderately aggressive accounting policies. While Staples does employ some

conservative practices, for the most part, its accounting policies lean more

towards the aggressive side of the spectrum. When compared to Office Depot

and Office Max, however, Staples has accounting policies that are slightly more

conservative than the industry norm.

Quality of Disclosure

The quality of disclosure accounts for the manager’s ability to accurately

disclose information which tells the true story of what is going on in their firm. In

looking at the qualitative disclosure, we will analyze the managers of Staples’

discussion on their business strategy, footnotes explaining accounting policies, its

current performance, and its segment disclosure. We will also conduct a

31

quantitative disclosure using ratios to analyze the firm’s trends and trends within

the industry to see if the firm is overvaluing or undervaluing numbers to make

certain aspects of its business look better than it might actually be.

The quality of disclosure in regards to the business strategy is normally

found in the letter to the shareholders. The business strategy should convey

current industry conditions, the company’s competitive positions, and

management’s plans for the future. Staples provided a letter to the shareholders

along with a business strategy section in the beginning of the 10-k. The letter to

the shareholders informed the readers of Staples’ increase in sales, earnings per

share increase, and an all time high operating margin. It focused mainly on what

it had done over the past year in regards to sales, growth, customer services,

brand development, and supply chain improvements. It did not look at the

future, not did it really give a good analysis of its competitive position. However,

the business strategy section of the 10-k did explain to the shareholders the

company’s competitive position and plans for the future.

The footnotes for a company should explain key accounting policies and

the logic behind them. If any of the policies are different from industry norms,

they need to be explained in the footnotes so that outsiders may have an

explanation of why the balance of numbers might be off. When looking at

Staples’ Footnotes it is apparent that they have adequately explained their key

accounting policies and assumptions. Staples includes information on where they

derived their numbers to formulate their financial statements.

The adequacy with which management discusses its current performance

is a chance for management to relay why certain events took place over the year

or why certain numbers changed in relation to the past. In analyzing their

discussion, we found that Staples did explain why certain numbers changed. For

example, interest income increased to $56.8 million from $39.9 million in the

previous year. In the management’s discussion, they explained that this increase

was due in part to “an increase in interest rates, partially offset by a reduction in

32

outstanding borrowings. Interest expense was also impacted by our November

2004 repayment of 150 million Euro Notes.”(Staples, 10-k)

The Quality of segment disclosure should provide information about how

the firm is divided into product segments and geographic segments. The

information that Staples has disclosed in their segment report gives us details

about their performance. “Staples has three reportable segments: North

American Retail, North American Delivery and International Operations.”

(Staples, 10-k)The information about each segment is broken down into how the

performance is measured by each one. Financial statements are also included to

compare each segments significant accounts and balances. These consolidated

financial statements provide sufficient information to assess staples overall

performance in comparison to their main accounting policies.

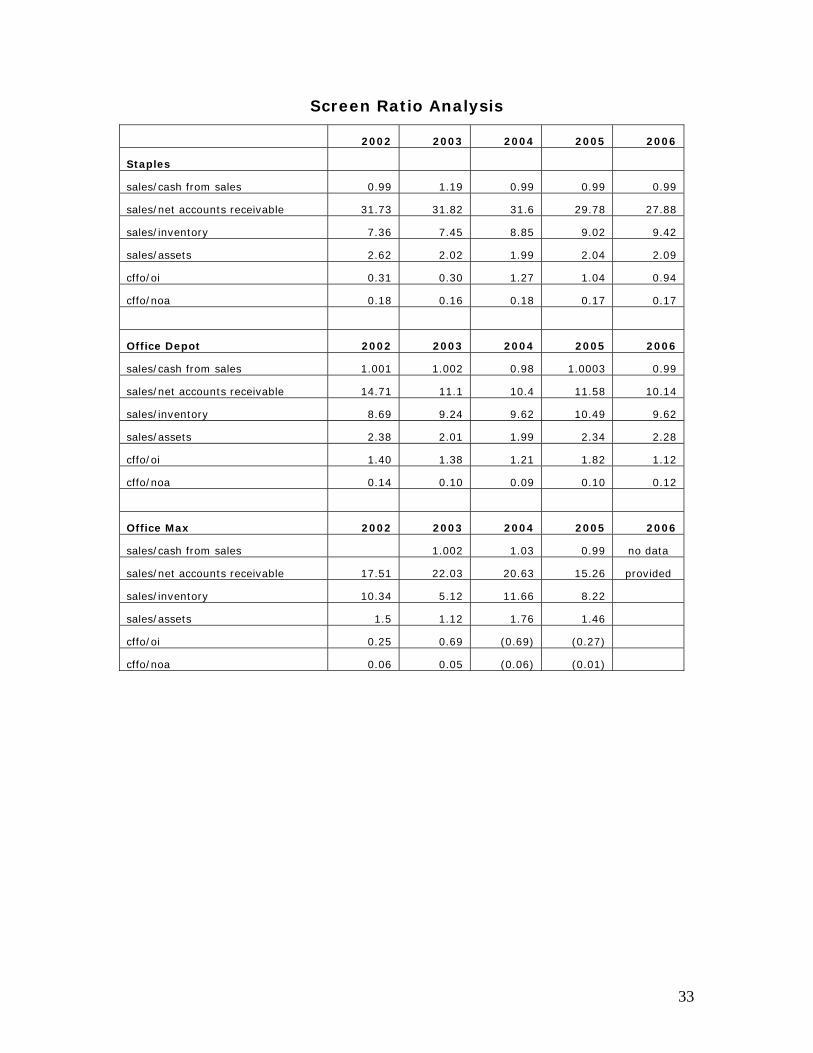

Screen Ratio Analysis will be discussed in the following paragraphs. The

ratios in the table below are core sales and expense diagnostics which help

analysts to see if a company is manipulating its accounting numbers. The

following ratios were not found and will not be discussed due to inadequate

amounts of information: sales/unearned revenues, sales/warranty liabilities, total

accruals/change in sales, pension expense/selling, general, and administrative

costs(SG&A), and other employment expenses/SG&A.

33

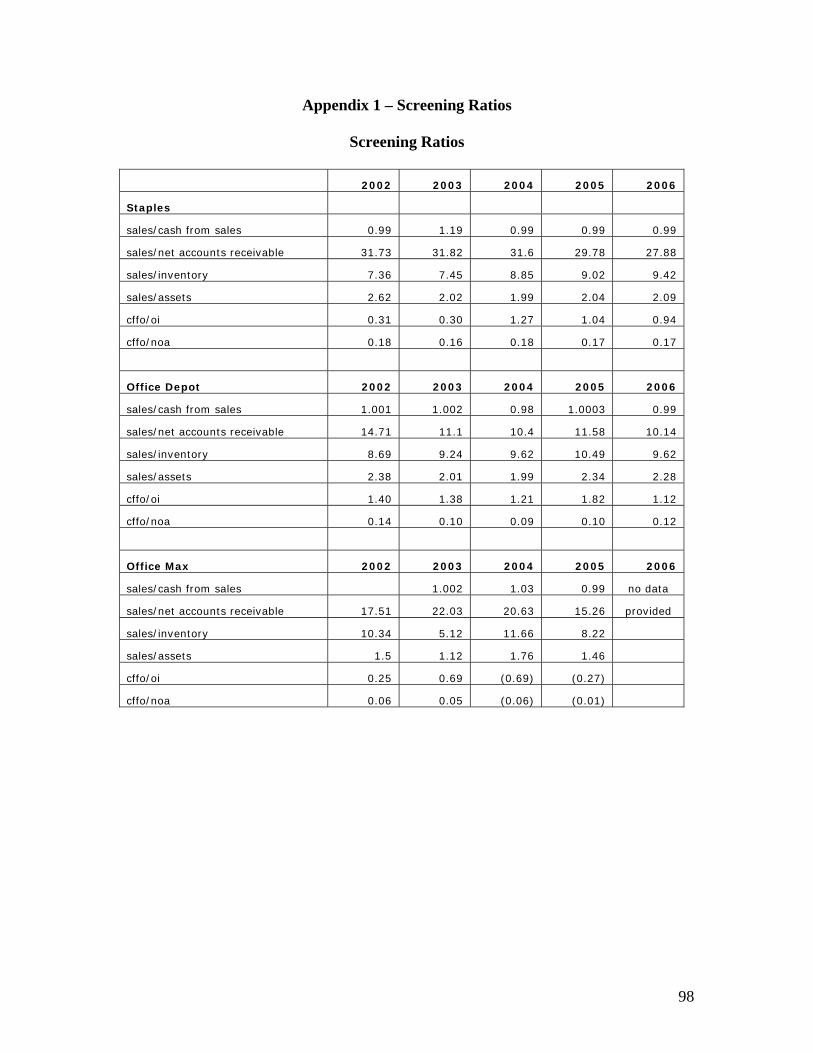

Screen Ratio Analysis

2002 2003 2004 2005 2006

Staples

sales/cash from sales 0.99 1.19 0.99 0.99 0.99

sales/net accounts receivable 31.73 31.82 31.6 29.78 27.88

sales/inventory 7.36 7.45 8.85 9.02 9.42

sales/assets 2.62 2.02 1.99 2.04 2.09

cffo/oi 0.31 0.30 1.27 1.04 0.94

cffo/noa 0.18 0.16 0.18 0.17 0.17

Office Depot 2002 2003 2004 2005 2006

sales/cash from sales 1.001 1.002 0.98 1.0003 0.99

sales/net accounts receivable 14.71 11.1 10.4 11.58 10.14

sales/inventory 8.69 9.24 9.62 10.49 9.62

sales/assets 2.38 2.01 1.99 2.34 2.28

cffo/oi 1.40 1.38 1.21 1.82 1.12

cffo/noa 0.14 0.10 0.09 0.10 0.12

Office Max 2002 2003 2004 2005 2006

sales/cash from sales 1.002 1.03 0.99 no data

sales/net accounts receivable 17.51 22.03 20.63 15.26 provided

sales/inventory 10.34 5.12 11.66 8.22

sales/assets 1.5 1.12 1.76 1.46

cffo/oi 0.25 0.69 (0.69) (0.27)

cffo/noa 0.06 0.05 (0.06) (0.01)

34

O U T P U T

Sales/ Cash From Sales

0

0.2

0.4

0.6

0.8

1

1.2

1.4

2002 2003 2004 2005 2006 Year

Staples

Office Depot

Office Max

Revenue Diagnostics

Over the past five years, Staples ratio of cash to cash from sales has

lingered right around 1 with .99 being a common ratio outcome. This means that

Staples is collecting roughly $0.99 in cash from every sale. Their ratio shot above

the rest of the industry in 2003, but has stabilized in the past three years to

average out with the rest of the industry. Office Depot and Office Max also have

sales to cash from sales ratio at 1. This indicates that the industry as a whole is

collecting cash from sales at relatively the same rate. This would lead us to

believe that the majority of sales in the office supply industry are cash sales.

35

The ratio that divides sales by net accounts receivables has dropped over

the past five years indicating Staples is not collecting their cash receivables. It is

currently at its lowest point from the last five years at 27.88. Although its

receivable turnover is higher than the other two competitors, we still question

why the receivables turnover is decreasing. These two ratios, cash divided by

cash from sales and cash divided by net accounts receivable, should move in the

same direction. However, our ratio of cash divided by cash from sales is

stabilizing while cash divided by net accounts receivables is declining. This would

possibly raise a red flag, but Staples can account for this difference in its 10-K

notes to consolidated financial statements. Staples receivables consist of trade

and non-trade receivables. Trade receivables are receivables from the sale of

goods or services on credit. Trade receivables make up for the majority of

account receivables at $444.8 million. “Concentrations of credit risk with respect

to trade receivables are limited due to Staples large number of customers and

their dispersion across many industries and geographic regions.” (Staples, 10-k)

This indicates that their majority sales are collectable which is why the cash to

cash from sales ratio are at .99. The reason the receivables turnover ratio is

Sales/ Net Accounts Receivable

0

5

10

15

20

25

30

35

2002 2003 2004 2005 2006

Year

Out

put Staples

Office DepotOffice Max

36

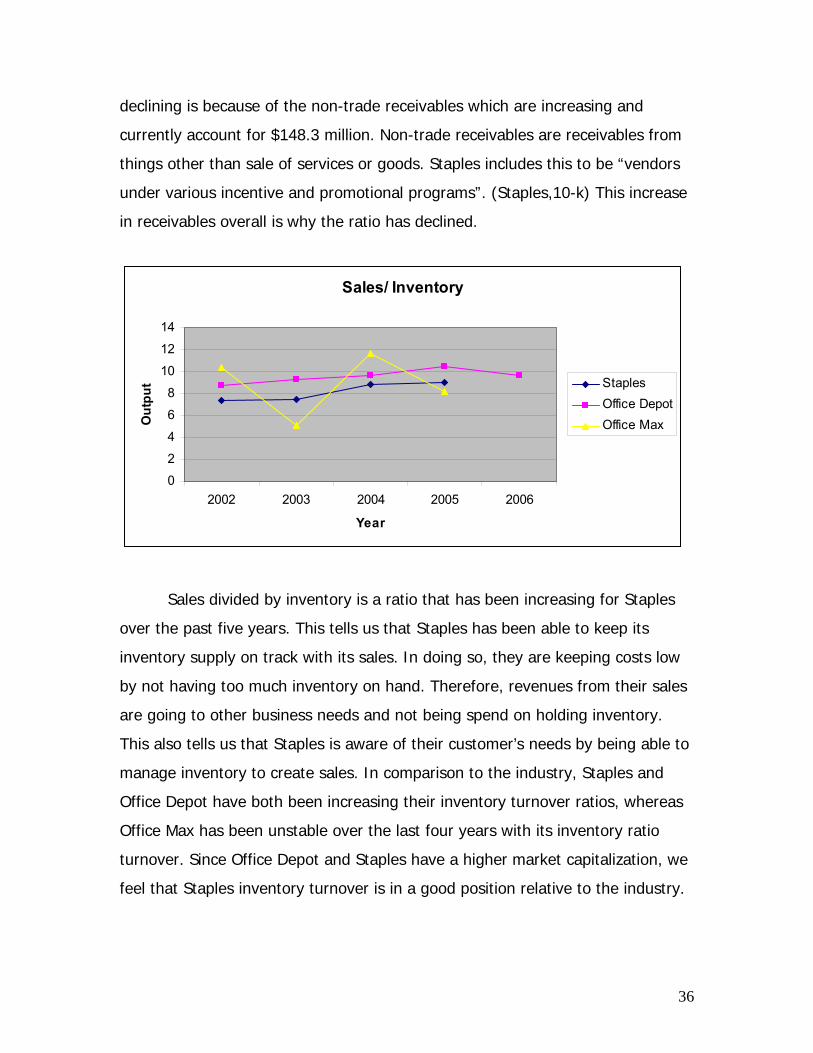

declining is because of the non-trade receivables which are increasing and

currently account for $148.3 million. Non-trade receivables are receivables from

things other than sale of services or goods. Staples includes this to be “vendors

under various incentive and promotional programs”. (Staples,10-k) This increase

in receivables overall is why the ratio has declined.

Sales divided by inventory is a ratio that has been increasing for Staples

over the past five years. This tells us that Staples has been able to keep its

inventory supply on track with its sales. In doing so, they are keeping costs low

by not having too much inventory on hand. Therefore, revenues from their sales

are going to other business needs and not being spend on holding inventory.

This also tells us that Staples is aware of their customer’s needs by being able to

manage inventory to create sales. In comparison to the industry, Staples and

Office Depot have both been increasing their inventory turnover ratios, whereas

Office Max has been unstable over the last four years with its inventory ratio

turnover. Since Office Depot and Staples have a higher market capitalization, we

feel that Staples inventory turnover is in a good position relative to the industry.

Sales/ Inventory

0

2

4

6

8

10

12

14

2002 2003 2004 2005 2006

Year

Out

put Staples

Office DepotOffice Max

37

Expense Diagnostics

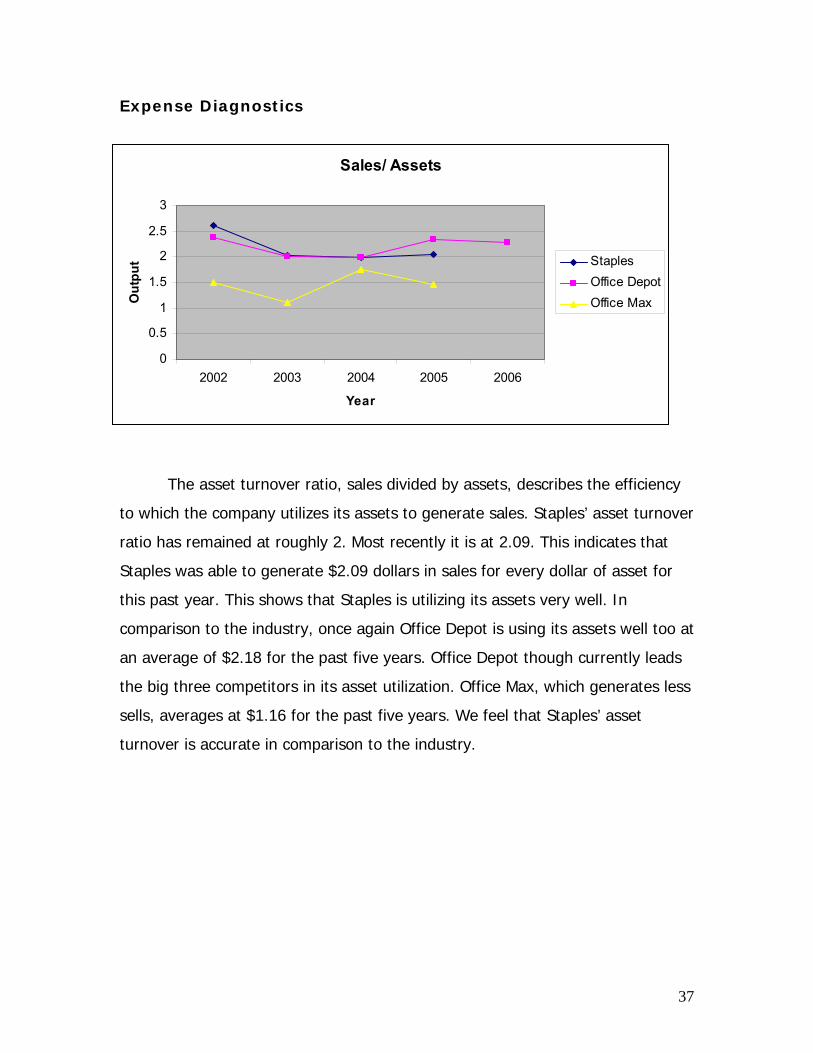

The asset turnover ratio, sales divided by assets, describes the efficiency

to which the company utilizes its assets to generate sales. Staples’ asset turnover

ratio has remained at roughly 2. Most recently it is at 2.09. This indicates that

Staples was able to generate $2.09 dollars in sales for every dollar of asset for

this past year. This shows that Staples is utilizing its assets very well. In

comparison to the industry, once again Office Depot is using its assets well too at

an average of $2.18 for the past five years. Office Depot though currently leads

the big three competitors in its asset utilization. Office Max, which generates less

sells, averages at $1.16 for the past five years. We feel that Staples’ asset

turnover is accurate in comparison to the industry.

Sales/ Assets

0

0.5

1

1.5

2

2.5

3

2002 2003 2004 2005 2006

Year

Out

put Staples

Office DepotOffice Max

38

CFFO/ OI

-1

-0.5

0

0.5

1

1.5

2

2002 2003 2004 2005 2006

Year

Out

put Staples

Office DepotOffice Max

The cash flow from operations (cffo) to operating income (oi) ratio for

Staples has fluctuated around 1 for the past three years. Staples had operating

income as a line item on its income statements filed for 2006, 2005, and 2004.

However, it did not have it as a line item for the reports filed in 2003 and 2002.

This is why the ratio jumps from 0.30 to 1.27 in the filing of 2004. We had to

compute operating income for the 2003 and 2002 filings. Staples ratio for the

past three years is a better comparison to Office Depot, its main competitor,

because we did not have to compute their operating income either. Staples last

filing in 2006 tells us that $0.94 of every dollar of cash flow from operations

results in operating income. Office Depot has remained along 0.2 and Office Max

has been very unstable in its cash flow from operations to operating income

ratios. The graph shows that the companies in the office supply industry have

been inconsistent in their cash flow from operations to operating income. It also

tells us that the industry as a whole is not generating enough operating income

to support cash flows. Noting that we can compare Staples past three years with

the Office Depot, we see that their ratios were very similar in 2004, and in 2005

and 2006 Office Depot has been declining in its ratios and Staples has been

inconsistent. We would need a few more years to see if the industry is just trying

39

to stabilize itself or if there are actual real problems for this industry in profiting

from its operations.

Cash flow from operations divided by net operating assets tells us how

well a company utilizes its assets to generate cash flows. Once again Staples’

ratio has remained stable over the last five years at roughly .172. It leads the

industry since Office Depot’s ratio has been at about .11, and Office Max has

been unstable in this ratio as well. This shows that Staples is utilizing its

operating assets more effectively than its two main competitors and is able to

generate cash flows from them.

Identifying Potential “Red Flags”

When reviewing a firm’s financial statements it is important to be aware of

abnormal and suspicious behavior and information. These “red flags” arise

though a firm’s accounting strategies within their flexibility limitations. They

highlight the need to re-examine accounting procedures and outcomes to

determine if the company overvalued or undervalued its numbers to make the

shareholders believe the company is doing better than it actually is. We believe

CFFO/ NOA

-0.1

-0.05

0

0.05

0.1

0.15

0.2

2002 2003 2004 2005 2006

Year

Out

put Staples

Office DepotOffice Max

40

that the ratios including sales divided by cash from sales, sales divided by net

account receivables, sales divide by inventory, sales divided by assets, cash flow

from operations (cffo), and cash flow from operations divided by net operating

assets (noa) do not raise any potential red flags for Staples.

The treatment of goodwill by firms has significantly changed since the

implementation of SFAS No. 142. Since Staples adopted the accounting policy

on February 3, 2002 they have acquired six businesses globally including a total

increase in goodwill of $1,155,034,000. The problem is, since the change in

accounting policy, Staples has not accounted for any impairment charges nor

written off any goodwill. This aggressive accounting behavior leads to an

overstatement of intangible assets and an understatement of impairment

expenses.

Staples also uses aggressive accounting strategies with advertising costs.

Staples normally expenses advertising costs, but capitalizes and amortizes

catalog costs over the life of the catalog. While the amounts of catalog costs are

relatively low, they still raise concerns over Staples’ accounting strategy, because

they are assuming all these catalogs are assets and will provide future economic

benefits. Capitalized catalog costs amounted to $30,800,000 at January 29,

2005 and $28,400,000 at January 28, 2006. We conclude, these distortions are

not significant enough to be undone due to their low relative magnitude, but

they still raise concern and should have been recognized as an expense.

Treatment of leases plays a significant role on firms’ financial statements.

Staples structures their leases as mainly operating leases to finance their retail

stores, support facilities, and equipment, while using capital leases for the

remainder. Staples’ capital leases at January 28, 2006 totaled $12,803,000 while

their operating leases total $5,246,874,000. Treating leases as operating leases

greatly understates lease asses and lease liabilities, thus having a detrimental

impact on the balance sheet.

41

We did not find any “red flags” associated with our ratio analysis. This

may be a result of Staples’ use of aggressive accounting strategies and number

manipulations.

Undo Accounting Distortions

The red flags stated in the “Potential Red Flags” section of this document

skewed numerical figures to make the firm appear more profitable. It is

important when valuing Staples to undo these accounting distortions in order to

truthfully state the firm’s financial position.

As stated previously, Staples leases a majority of its new properties by

way of operating leases.

Staples’ Operating Lease Obligations:

Operating Leases

Year FV i = 7% PV 1 $617,021 0.935 $576,655.14 2 $593,176 0.873 $518,102.89 3 $558,355 0.816 $455,784.00 4 $526,981 0.763 $402,031.28 5 $491,310 0.713 $350,297.24 6 $492,006 0.666 $327,844.37 7 $492,006 0.623 $306,396.61 8 $492,006 0.582 $286,351.97 9 $492,006 0.544 $267,618.66

10 $492,006 0.508 $250,110.90 $3,741,193.07

The table above shows the present value of Staples’ future payments on its

operating leases. We used ten years because when assuming a 20 year

maturity, the payments decreased from year 5 to years 6-20 by about $300

million dollars. By assuming a ten year maturity, we kept the remaining

payments (Years 5 – 10) fairly close to the payments in the first 5 years. This

effect is somewhat of a tradeoff between having a drastic decrease in payments

42

after 5 years which would be hard to justify in the financial statements and

paying off the leases much faster due to large payments. We assumed a 7%

discount rate because that is about the industry standard. From the table, it can

be determined that Staples is hiding about $3.7 billion worth of liabilities.

To undo this distortion, Staples should increase it leased assets and lease

liabilities by $3.7 billion. Staples should also recognize a depreciation expense

each year of roughly $374 million ($3741193.07/10 years). The affect of this

large expense recognition would ultimately decrease net income, but accurately

state Staples’ assets and liabilities.

Assets:

Leased Assets (Land and Buildings): +$3.7 billion

Liabilities:

Lease Liabilities (Capital Leases): +$3.7 billion

Staples’ also distorted accounting policies when dealing with its

impairment of goodwill. As stated previously, Staples has not evaluated goodwill

for impairment since 2001. By not doing so, the company is overstating its

assets considerably. Even though goodwill is not amortized, we believe an

accurate assumption would be to amortize it over 10 years. This amortization

expense should be similar to the amount that should have been impaired by

Staples’ management at the end of each year. In doing so, Staples would

decrease its assets to portray a truthful figure. Since total goodwill equals

$1,378,752,000, we believe it is fair to amortize this amount over 10 years at a

rate of $137,875,200 per year. This will decrease the current value of goodwill

to zero over ten years because we believe the goodwill already acquired will

have lost its value.

43

Ratio Analysis and Forecasting Financials

Financial Analysis

Financial Analysis is a very important part of valuing a firm. We use the

company’s balance sheets, income statements, and statements of cash flows to

analyze the company’s plans and the performance of the firms and corporate

managers. We do this analysis through the use of ratios in which we compute for

Staples and its competitors. This allows us to make comparisons and note

trends.

Ratio Analysis

In valuing a firm, you must perform a ratio analysis. This provides you

with a way to relate different line items of the financial statements and then

assess those relationships. A cross-sectional comparison allows you to examine

the ratios of your company to its competitors. There are three main groups of

ratios: liquidity, profitability, and capital structure. We will analyze these ratios

for Staples, Office Depot, and Office Max and compare them against each other.

Trend (Time Series) Analysis/ Cross Sectional Analysis

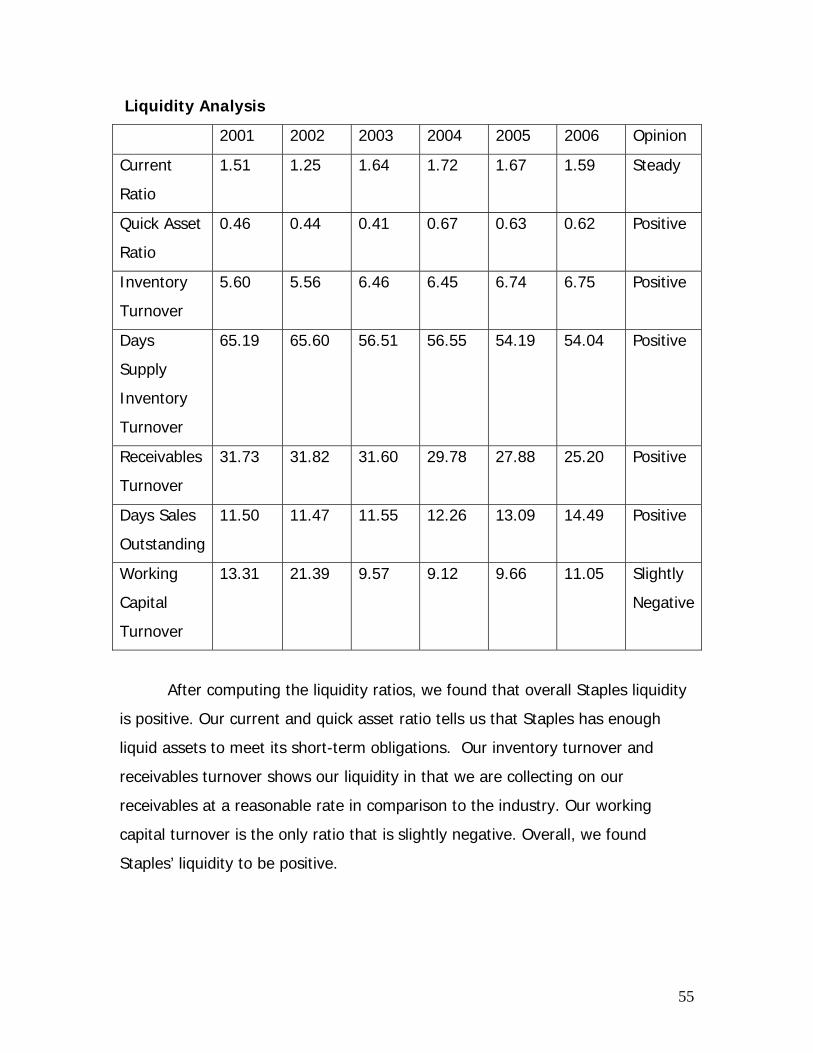

We will begin with the liquidity ratios. These ratios include the current

ratio, quick-asset ratio, inventory turnover, days inventory turnover, receivables

turnover, days receivables turnover, and working capital turnover. Liquidity ratios

look at the amount of cash-equivalence in a company’s assets and its ability to

turn assets into cash to meet financial obligations. After computing the ratios for

Staples and its competitors, we will now analyze these ratios and identify any

trends within Staples as well as within the industry. We will begin with the

current ratio which is found by dividing current assets by current liabilities.

44

Liquidity Ratios

Current Assets: Current Assets/Current Liabilities

2001 2002 2003 2004 2005 2006

Staples 1.51 1.25 1.64 1.72 1.67 1.59

Office Depot 1.61 1.57 1.51 1.43 1.16

Office Max 1.23 1.31 1.75 1.22 1.37

The current ratio is an analysis of the amount of current assets a company

has to cover its current liabilities. Current assets consist of cash and cash

equivalents, short term investments, net receivables, net merchandise

inventories, deferred income tax assets, and prepaid expenses. Current liabilities

consist of accounts payable, accrued expenses and other current liabilities, and

debt maturing within one year. When reading this ratio, you would state that for

every dollar of current liabilities, the company has an amount of current assets to

cover those liabilities. Staples, for example, had a current ratio in 2006 that

shows that for every dollar of current liabilities, they had $1.59 in current assets

to cover those liabilities. A ratio over one suggests that the company has the

ability to pay its short term liabilities with its current assets. A ratio under one

does not necessarily mean the company will go bankrupt, it just shows that

company is not in good financial health. The higher the ratio is, the more liquid

its current assets and therefore it has a better ability to meet short term

obligations. However, if the current ratio is too high, that tells us that the firm is

not utilizing its assets efficiently.

45

Current Asset Ratio

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

2001 2002 2003 2004 2005

years

outp

ut StaplesOffice DepotOffice MaxIndustry Avg.

Staples has an average over the past six years of 1.56 with its high being

at 1.72 and its low at 1.25. These tell us that Staples is using its assets efficiently

and has the ability to cover its short term debt. Its current assets have been

steadily increasing at roughly 80% to 90% and its current liabilities have not

been increasing as consistently. This is why its current ratio has varied over the

past six years. Office Depot and Office Max are also both utilizing their assets