Embed Size (px)

Citation preview

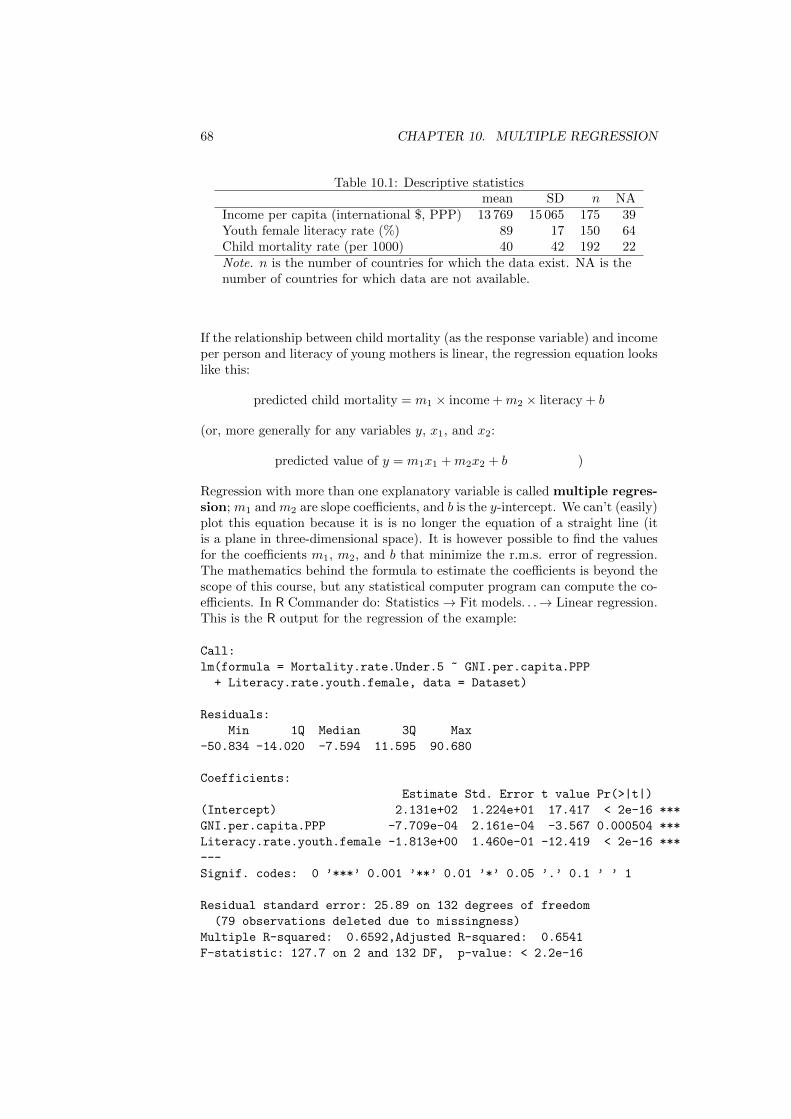

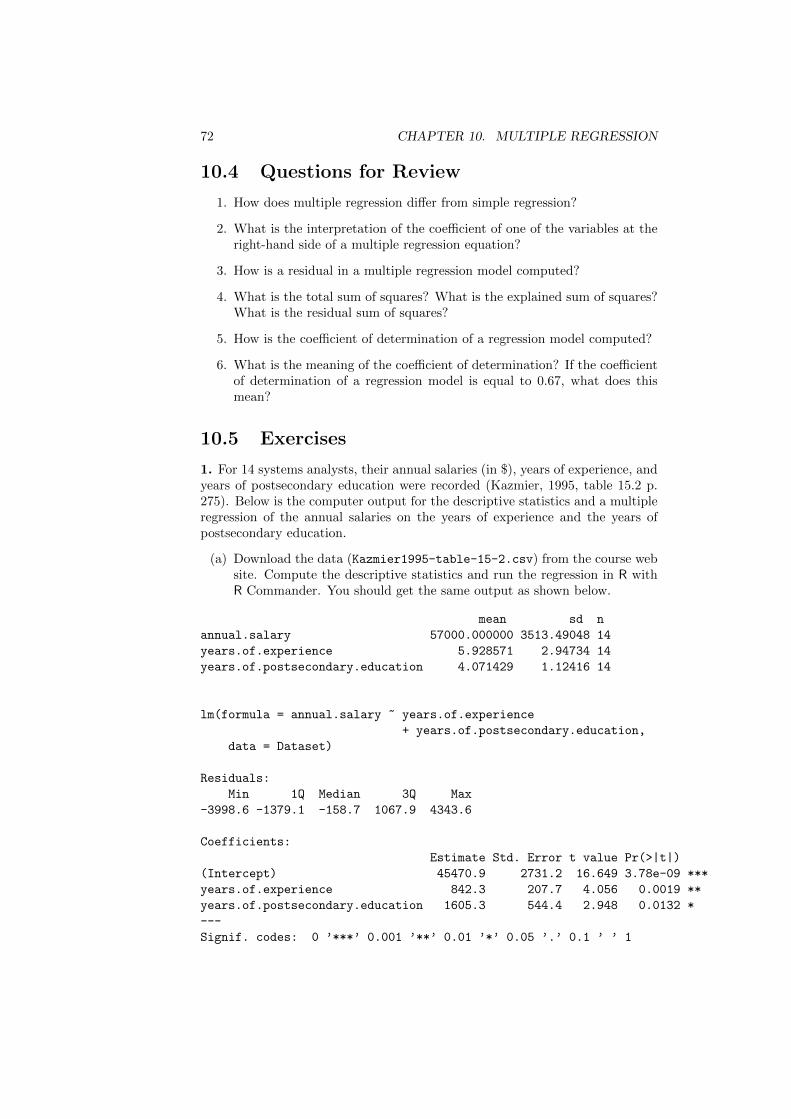

STA201 Intermediate Statistics

Lecture Notes

Luc Hens

15 January 2016

ii

How to use these lecturenotes

These lecture notes start by reviewing the material from STA101 (most of it cov-ered in Freedman et al. (2007)): descriptive statistics, probability distributions,sampling distributions, and confidence intervals. Following the review, STA201then covers the following topics: hypothesis tests (Freedman et al., 2007, chap-ters 26 and 29); the t-test for small samples (Freedman et al., 2007, chapter26, section 6); hypothesis tests on two averages (Freedman et al., 2007, chapter27), and the Chi-square test (Freedman et al., 2007, chapter 28). STA201 thencovers correlation and simple linear regression (Freedman et al., 2007, chapters10, 11, 12). Two related subjects (multiple regression and inference for regres-sion) that are not covered in Freedman et al. (2007) are covered in-depth inthe lecture notes. Each chapter from the lecture notes ends with Questions forReview; be prepared to answer these questions in class. Work the problemsat the end of the chapters in the lecture notes. The key concepts are set inboldface; you should know their definitions. You can find the lectures notes andother material on the course web site:

http://homepages.vub.ac.be/~lmahens/STA201.html

We’ll use the open-source statistical environment R with the graphical userinterface R Commander. The course web page contains a document (Gettingstarted in STA101 ) that explains how to install R and R Commander on yourcomputer, as well as R scripts and data sets used in the course. Thanks to aweb interface (Rweb) you can also run R from any computer or mobile device(tablet or smartphone) with a web browser, without having R installed. Makesure you are connected to the internet. In your web browser, open a new a newtab. Point your browser to Rweb:

http://pbil.univ-lyon1.fr/Rweb/

Remove everything from the window at the top (data(meaudret) etc.). TypeR code (or paste an R script) in the window. Click the Submit button. Waituntil Results from Rweb appears. If the script generates a graph, scroll down tosee the graph.

Practice is important to learn statistics. Students who wish to work addi-tional exercises can find hundreds of solved exercises in Kazmier (1995) (or amore recent edition). Moore et al. (2012) covers the same ground as Freedmanet al. (2007) and has many exercises; the solutions to the odd-numbered exer-cises are in the back of the book. Older but still useful editions of both booksare available in the VUB library.

iii

iv HOW TO USE THESE LECTURE NOTES

Remember the following calculation rules:

– Always carry the units of measurement in the calculations. For instance,when you have two measurements in dollars ($ 2 and $ 3) and you computetheir average, write:

$ 2 + $ 3

2= $ 2.5

– To express a fraction (say 2/5) as a percentage, multiply by 100% (not by100):

2

5× 100% = 40%

The same holds for expressing decimals (say, 0.40) as a percentage:

0.40× 100% = 40%

(STA201 was for a while taught as STA301 Methods: Statistics for Businessand Economics.)

Chapter 1

Descriptive statistics

1.1 Basic concepts of statistics

Suppose you want to find out which percentage of employees in a given companyhas a private pension plan. The population is the set of cases about which youwant to find things out. In this case, the population consists of all employeesin the given company; each employee is a case. A variable is a characteristicof each case in the population. In this case you are interested in the variableprivate pension plan. It can take two values: yes or no (it’s a qualitativevariable). The percentage of employees who have a private pension plan is aparameter: a numerical characteristic of the population. The monthly salaryof the employees is a quantitative variable. The average monthly salary ofall employees in the company is another parameter. We’ll be mainly concernedwith these two types of parameters: percentages (of qualitative variables) andaverages (of quantitative variables).

If you conduct a survey and every employee in the company fills out thesurvey form, the collected data set covers all of the population, and you can findthe exact value of the population parameter. In some cases collecting data forthe population may not be possible; you may have to rely on a sample drawnfrom the population. A sample is a subset of the population. The samplepercentage (which percentage of employees in the sample has a private pensionplan) is called a statistic. Statistical inference is when you use a sample todraw conclusions about the population it was drawn from. We’ll see that whenthe sample is a simple random sample, the sample percentage (the statistic) is agood estimate of the population percentage (the parameter). Much of statisticalinference deals with quantifying the degree of uncertainty that is the result ofgeneralizing from sample evidence.

First we will deal with descriptive statistics: ways to summarize data(from a population or a sample) in a table, a graph, or with numbers.

1.2 Summarizing data by a frequency table

How can we summarize information about a quantitative variable of a sampleor a population, often consisting of thousands of measurements?

1

2 CHAPTER 1. DESCRIPTIVE STATISTICS

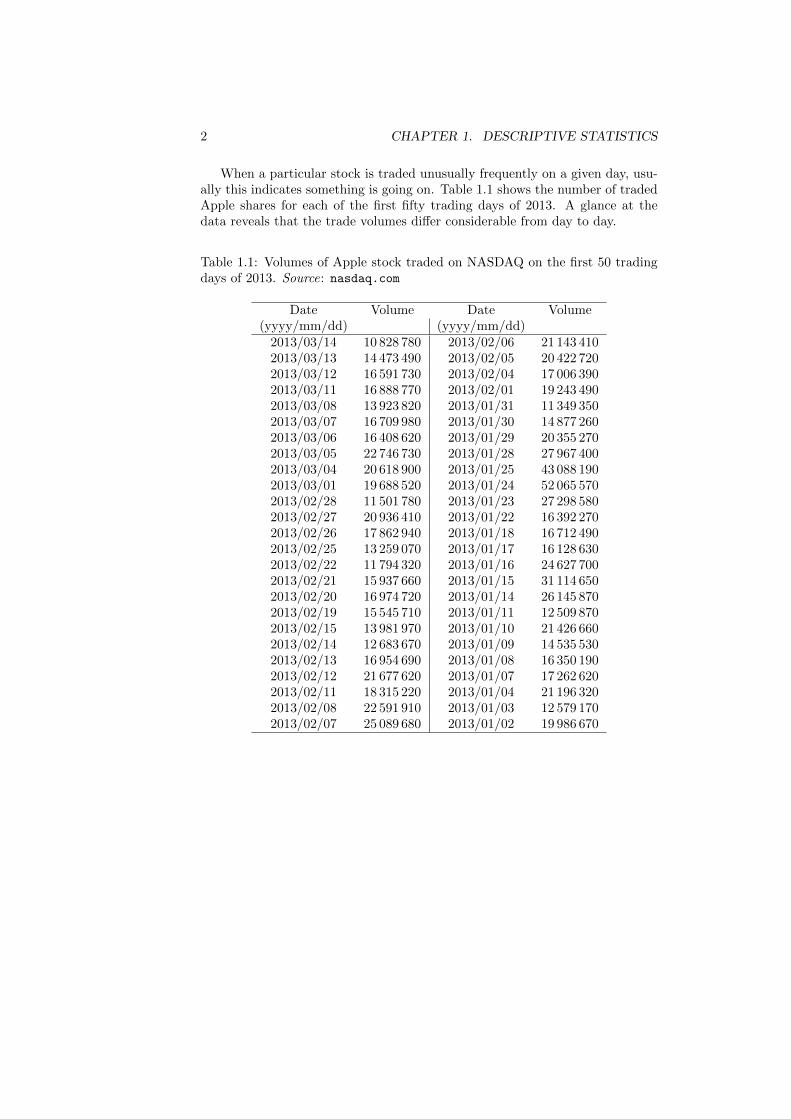

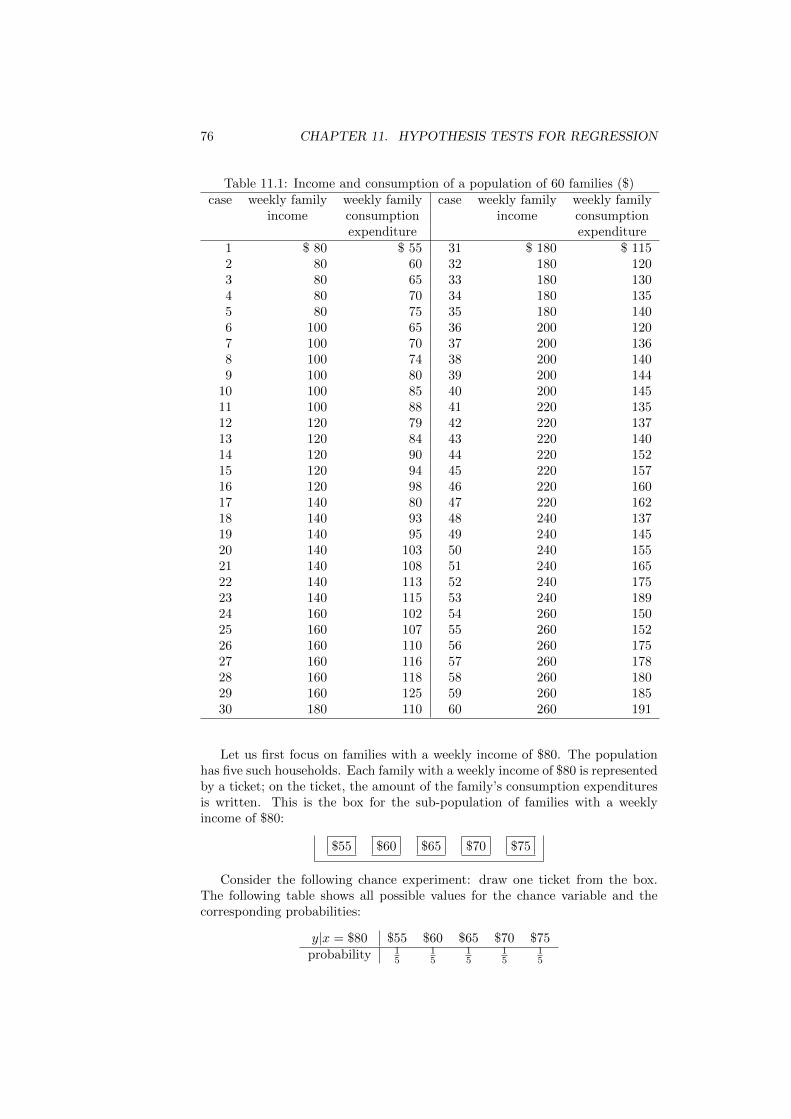

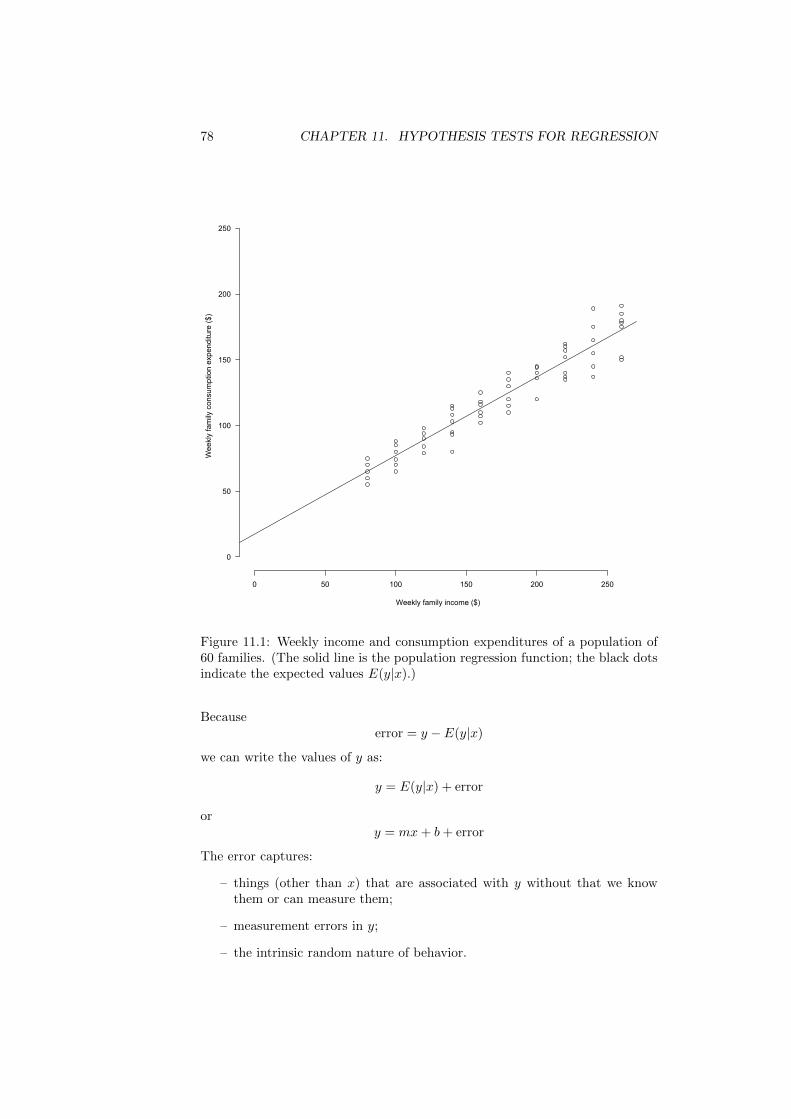

When a particular stock is traded unusually frequently on a given day, usu-ally this indicates something is going on. Table 1.1 shows the number of tradedApple shares for each of the first fifty trading days of 2013. A glance at thedata reveals that the trade volumes differ considerable from day to day.

Table 1.1: Volumes of Apple stock traded on NASDAQ on the first 50 tradingdays of 2013. Source: nasdaq.com

Date Volume Date Volume(yyyy/mm/dd) (yyyy/mm/dd)

2013/03/14 10 828 780 2013/02/06 21 143 4102013/03/13 14 473 490 2013/02/05 20 422 7202013/03/12 16 591 730 2013/02/04 17 006 3902013/03/11 16 888 770 2013/02/01 19 243 4902013/03/08 13 923 820 2013/01/31 11 349 3502013/03/07 16 709 980 2013/01/30 14 877 2602013/03/06 16 408 620 2013/01/29 20 355 2702013/03/05 22 746 730 2013/01/28 27 967 4002013/03/04 20 618 900 2013/01/25 43 088 1902013/03/01 19 688 520 2013/01/24 52 065 5702013/02/28 11 501 780 2013/01/23 27 298 5802013/02/27 20 936 410 2013/01/22 16 392 2702013/02/26 17 862 940 2013/01/18 16 712 4902013/02/25 13 259 070 2013/01/17 16 128 6302013/02/22 11 794 320 2013/01/16 24 627 7002013/02/21 15 937 660 2013/01/15 31 114 6502013/02/20 16 974 720 2013/01/14 26 145 8702013/02/19 15 545 710 2013/01/11 12 509 8702013/02/15 13 981 970 2013/01/10 21 426 6602013/02/14 12 683 670 2013/01/09 14 535 5302013/02/13 16 954 690 2013/01/08 16 350 1902013/02/12 21 677 620 2013/01/07 17 262 6202013/02/11 18 315 220 2013/01/04 21 196 3202013/02/08 22 591 910 2013/01/03 12 579 1702013/02/07 25 089 680 2013/01/02 19 986 670

1.2. SUMMARIZING DATA BY A FREQUENCY TABLE 3

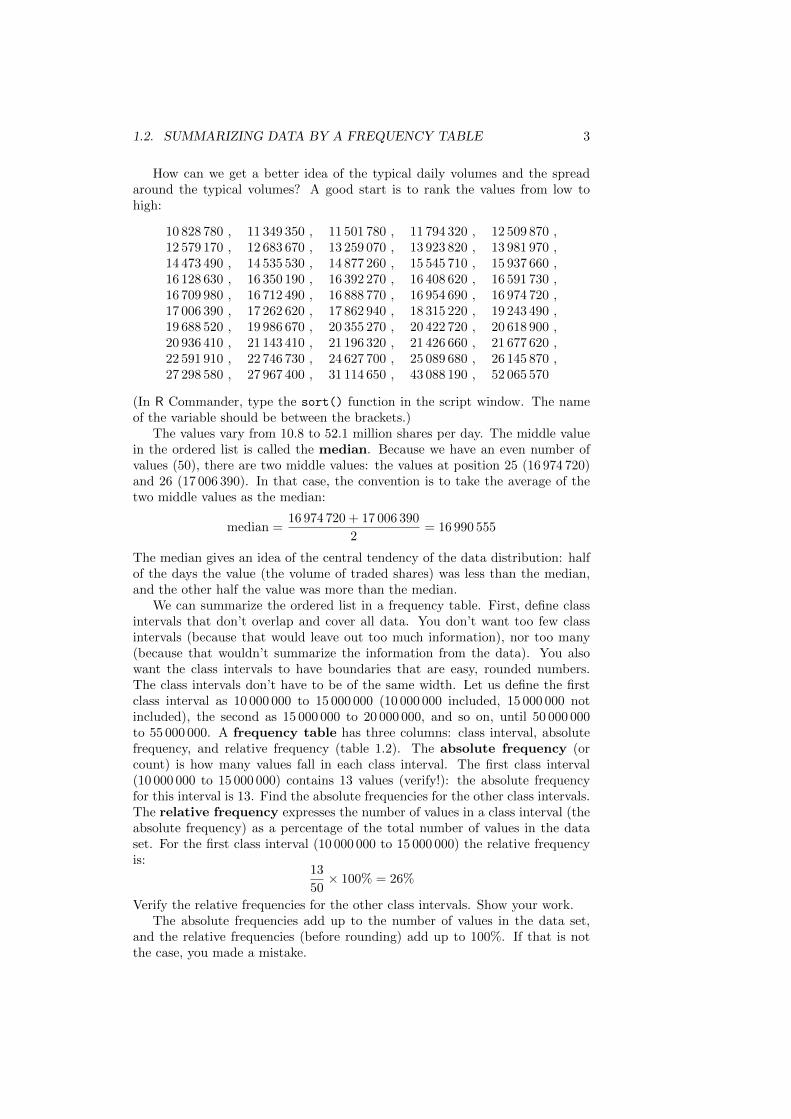

How can we get a better idea of the typical daily volumes and the spreadaround the typical volumes? A good start is to rank the values from low tohigh:

10 828 780 , 11 349 350 , 11 501 780 , 11 794 320 , 12 509 870 ,12 579 170 , 12 683 670 , 13 259 070 , 13 923 820 , 13 981 970 ,14 473 490 , 14 535 530 , 14 877 260 , 15 545 710 , 15 937 660 ,16 128 630 , 16 350 190 , 16 392 270 , 16 408 620 , 16 591 730 ,16 709 980 , 16 712 490 , 16 888 770 , 16 954 690 , 16 974 720 ,17 006 390 , 17 262 620 , 17 862 940 , 18 315 220 , 19 243 490 ,19 688 520 , 19 986 670 , 20 355 270 , 20 422 720 , 20 618 900 ,20 936 410 , 21 143 410 , 21 196 320 , 21 426 660 , 21 677 620 ,22 591 910 , 22 746 730 , 24 627 700 , 25 089 680 , 26 145 870 ,27 298 580 , 27 967 400 , 31 114 650 , 43 088 190 , 52 065 570

(In R Commander, type the sort() function in the script window. The nameof the variable should be between the brackets.)

The values vary from 10.8 to 52.1 million shares per day. The middle valuein the ordered list is called the median. Because we have an even number ofvalues (50), there are two middle values: the values at position 25 (16 974 720)and 26 (17 006 390). In that case, the convention is to take the average of thetwo middle values as the median:

median =16 974 720 + 17 006 390

2= 16 990 555

The median gives an idea of the central tendency of the data distribution: halfof the days the value (the volume of traded shares) was less than the median,and the other half the value was more than the median.

We can summarize the ordered list in a frequency table. First, define classintervals that don’t overlap and cover all data. You don’t want too few classintervals (because that would leave out too much information), nor too many(because that wouldn’t summarize the information from the data). You alsowant the class intervals to have boundaries that are easy, rounded numbers.The class intervals don’t have to be of the same width. Let us define the firstclass interval as 10 000 000 to 15 000 000 (10 000 000 included, 15 000 000 notincluded), the second as 15 000 000 to 20 000 000, and so on, until 50 000 000to 55 000 000. A frequency table has three columns: class interval, absolutefrequency, and relative frequency (table 1.2). The absolute frequency (orcount) is how many values fall in each class interval. The first class interval(10 000 000 to 15 000 000) contains 13 values (verify!): the absolute frequencyfor this interval is 13. Find the absolute frequencies for the other class intervals.The relative frequency expresses the number of values in a class interval (theabsolute frequency) as a percentage of the total number of values in the dataset. For the first class interval (10 000 000 to 15 000 000) the relative frequencyis:

13

50× 100% = 26%

Verify the relative frequencies for the other class intervals. Show your work.The absolute frequencies add up to the number of values in the data set,

and the relative frequencies (before rounding) add up to 100%. If that is notthe case, you made a mistake.

4 CHAPTER 1. DESCRIPTIVE STATISTICS

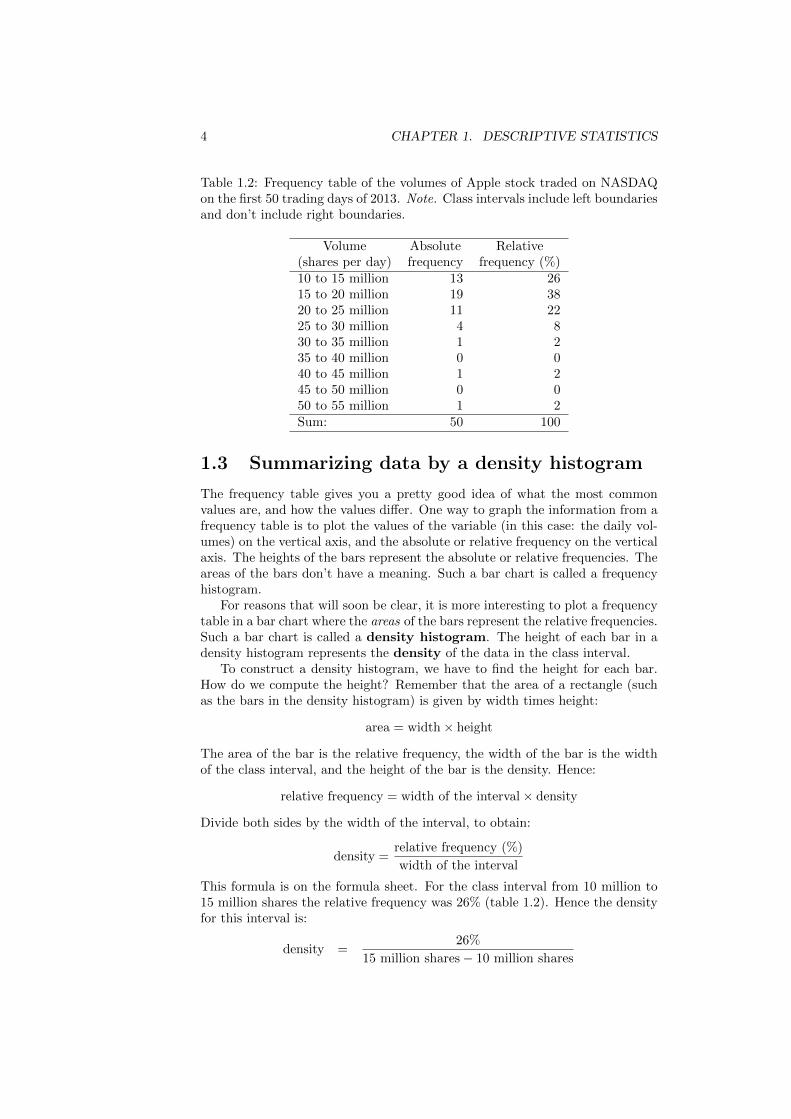

Table 1.2: Frequency table of the volumes of Apple stock traded on NASDAQon the first 50 trading days of 2013. Note. Class intervals include left boundariesand don’t include right boundaries.

Volume Absolute Relative(shares per day) frequency frequency (%)10 to 15 million 13 2615 to 20 million 19 3820 to 25 million 11 2225 to 30 million 4 830 to 35 million 1 235 to 40 million 0 040 to 45 million 1 245 to 50 million 0 050 to 55 million 1 2Sum: 50 100

1.3 Summarizing data by a density histogram

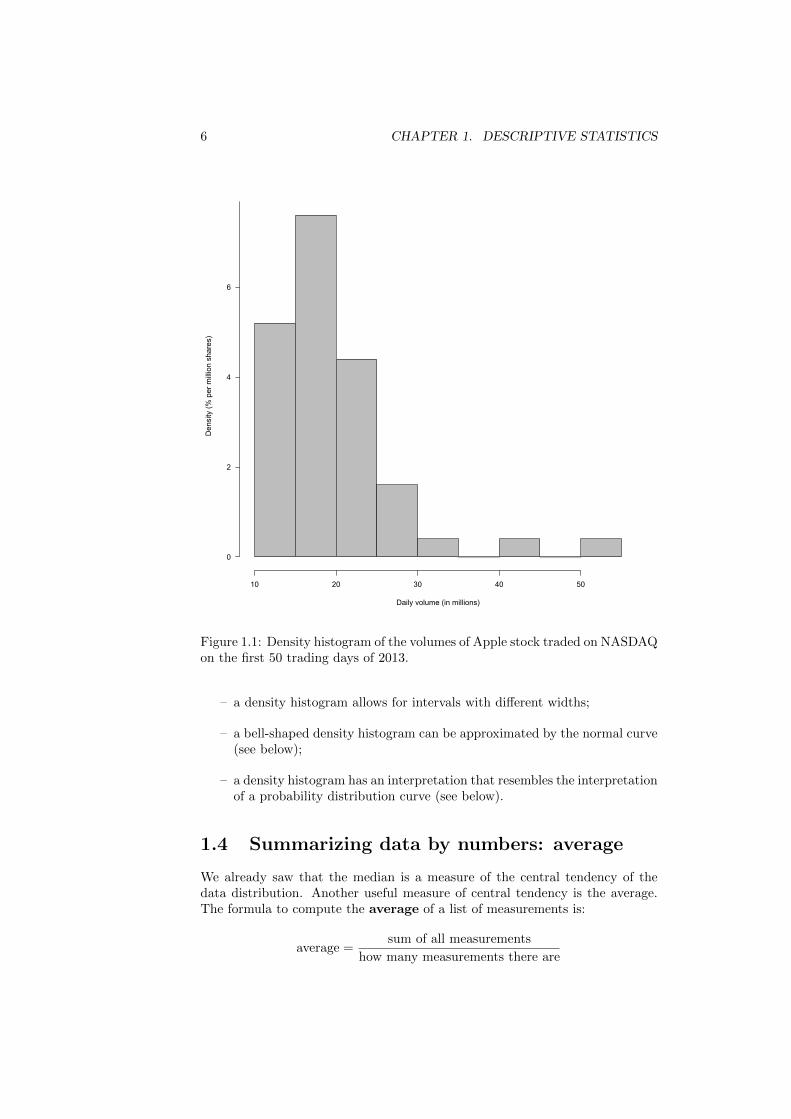

The frequency table gives you a pretty good idea of what the most commonvalues are, and how the values differ. One way to graph the information from afrequency table is to plot the values of the variable (in this case: the daily vol-umes) on the vertical axis, and the absolute or relative frequency on the verticalaxis. The heights of the bars represent the absolute or relative frequencies. Theareas of the bars don’t have a meaning. Such a bar chart is called a frequencyhistogram.

For reasons that will soon be clear, it is more interesting to plot a frequencytable in a bar chart where the areas of the bars represent the relative frequencies.Such a bar chart is called a density histogram. The height of each bar in adensity histogram represents the density of the data in the class interval.

To construct a density histogram, we have to find the height for each bar.How do we compute the height? Remember that the area of a rectangle (suchas the bars in the density histogram) is given by width times height:

area = width× height

The area of the bar is the relative frequency, the width of the bar is the widthof the class interval, and the height of the bar is the density. Hence:

relative frequency = width of the interval× density

Divide both sides by the width of the interval, to obtain:

density =relative frequency (%)

width of the interval

This formula is on the formula sheet. For the class interval from 10 million to15 million shares the relative frequency was 26% (table 1.2). Hence the densityfor this interval is:

density =26%

15 million shares− 10 million shares

1.3. SUMMARIZING DATA BY A DENSITY HISTOGRAM 5

=26%

5 million shares= 5.2%/million shares

Now that you know the height of the bar over the interval from 10 to 15 millionshares (5.2% per million shares), you can draw the bar. The density for theinterval from 10 to 15 million shares tells us which percentage of all 50 valuesfalls in each interval of one unit wide on the horizontal axis, assuming that thevalues in interval from 10 to 15 million shares would be uniformly distributed. Inthe interval from 10 to 15 million shares, about 5.2% of all values falls between10 and 11 million shares, about 5.2% of all values falls between 11 and 12 millionshares, about 5.2% of all values falls between 12 and 13 million shares, about5.2% of all values falls between 13 and 14 million shares, and about 5.2% of allvalues falls between 14 and 15 million shares. It is as if the bar is sliced upin vertical strips of one horizontal unit (here: one million shares) wide. Thedensity measures which percentage of all values falls in such a strip of one unitwide. Note the unit of measurement of density: percent per million shares.More generally, density is expressed in percent per unit on the horizontalaxis.

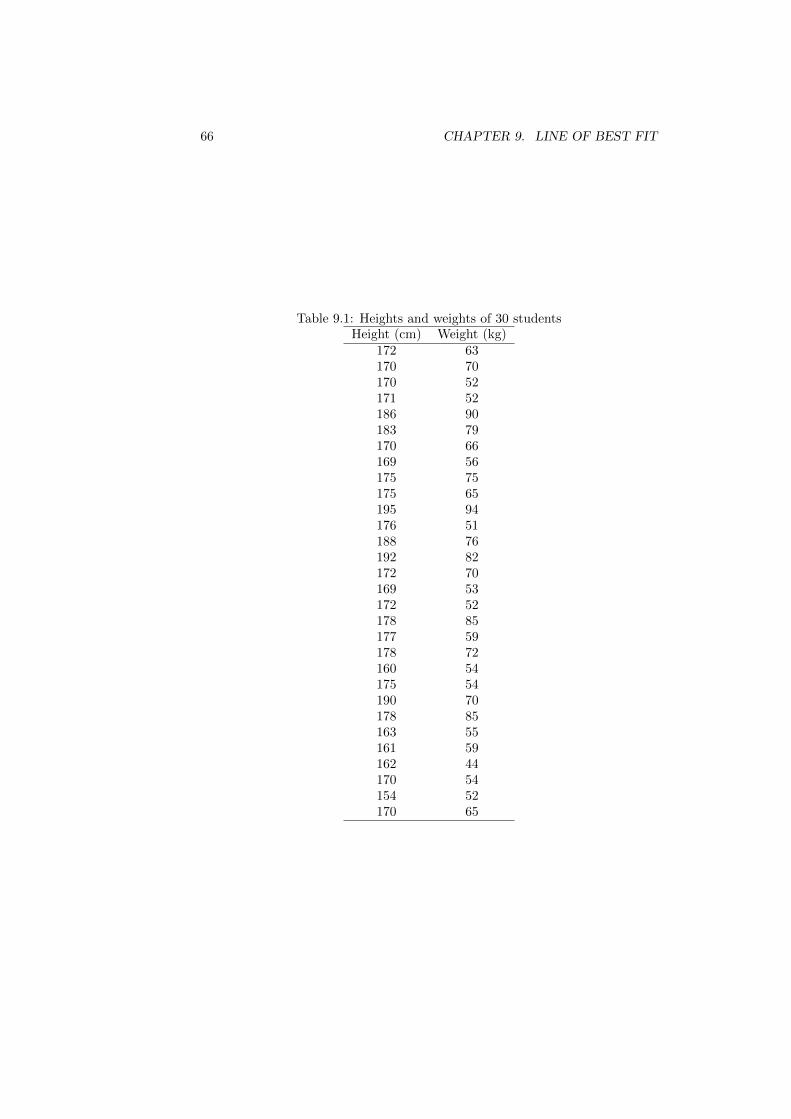

Given a data set such as table 1.1, you should be able to construct a frequencytable and a density histogram. The first assignment asks you to do exactly that.

Figure 1.1 shows the density histogram as generated by R. A script to drawthis density histogram in R Commander is posted on the course web page.

Suppose you don’t have the data set or the frequency table, but just thedensity histogram (figure 1.1). On which percentage of trading days was thevolume of traded Apple shares between 20 and 30 million? Show in the densityhistogram what represents your answer. On (approximately) which percentageof trading days was the volume of traded Apple shares between 24 and 27million? Show in the density histogram what represents your answer.

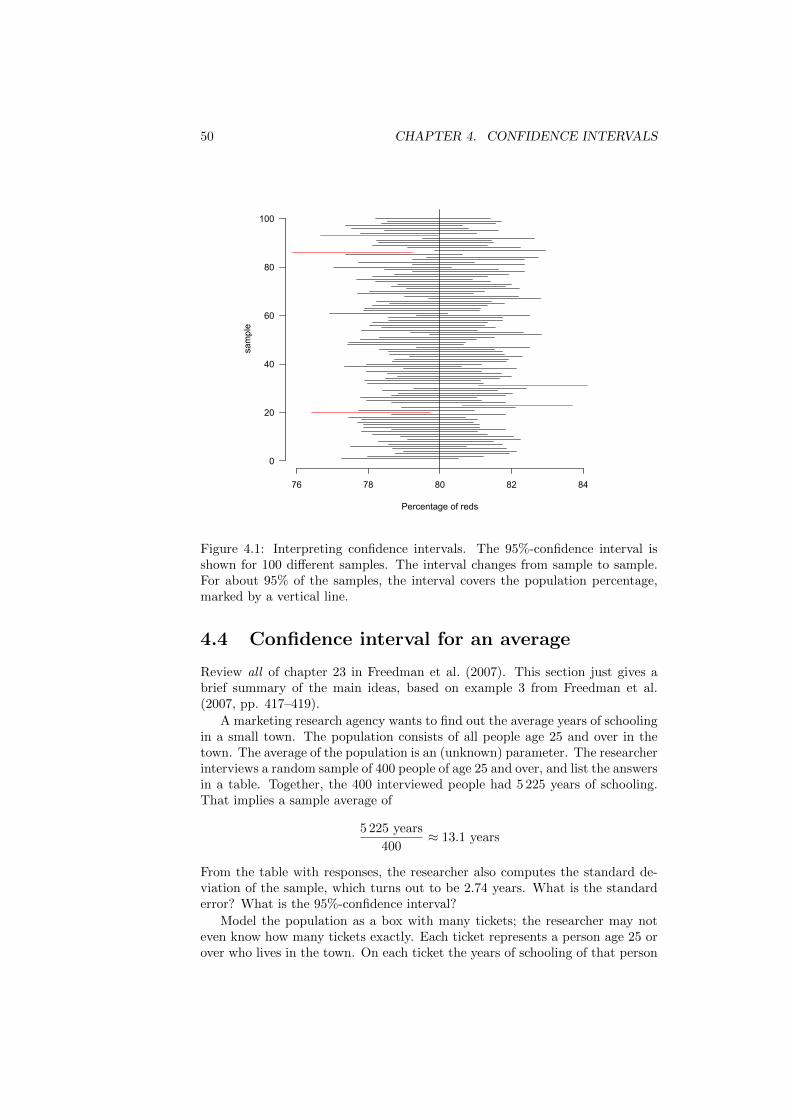

We conclude that the area under de histogram between two values representsthe percentage of observations that falls between those two values.

What is the area under all of the histogram? %.

In a density histogram the vertical axis shows the density of the data. Theareas of the bars represent percentages. The area under a density histogramover an interval is the percentage of data that fall in that interval. The totalarea under a density histogram is 100%. (Freedman et al., 2007, p. 41)

A density histogram reveals the shape of the data distribution. To assessthe shape of the density histogram, locate the median on the horizontal axisand draw a vertical line. Is the histogram symmetric about the median, or is itskewed? Is the histogram skewed to the left (that is, with a long tail to the left)or to the right (with a long tail to the right)? Is the histogram bell-shaped?Watch this two-minute video clip (Rosling, 2015) that uses a histogram to showhow the world income distribution has changed over the last two centuries:

https://youtu.be/_JhD37gSNVU

Although a density histogram is somewhat more complicated than a fre-quency histogram, a density histogram has several advantages:

6 CHAPTER 1. DESCRIPTIVE STATISTICS

Daily volume (in millions)

Den

sity

(% p

er m

illio

n sh

ares

)

10 20 30 40 50

0

2

4

6

Figure 1.1: Density histogram of the volumes of Apple stock traded on NASDAQon the first 50 trading days of 2013.

– a density histogram allows for intervals with different widths;

– a bell-shaped density histogram can be approximated by the normal curve(see below);

– a density histogram has an interpretation that resembles the interpretationof a probability distribution curve (see below).

1.4 Summarizing data by numbers: average

We already saw that the median is a measure of the central tendency of thedata distribution. Another useful measure of central tendency is the average.The formula to compute the average of a list of measurements is:

average =sum of all measurements

how many measurements there are

1.5. SUMMARIZING DATA BY NUMBERS: STANDARD DEVIATION 7

Here is an example. Suppose you collected the price of the same bottle ofwine in five restaurants:

€ 2,€ 2,€ 4,€ 5,€ 7

The average price is:

average =€ 2 +€ 2 +€ 4 +€ 5 +€ 7

5=€ 20

5= € 4

A disadvantage is that the average is sensitive to outliers (exceptionally lowor exceptionally high values). Suppose that the list looked like this:

€ 2,€ 2,€ 4,€ 5,€ 22

The average of this list is:

average =€ 2 +€ 2 +€ 4 +€ 5 +€ 22

5=€ 35

5= € 7

The one exceptionally expensive bottle of € 22 pulled the average up quite a lot.In cases like this we often prefer to use a different measure of central tendency:the median. To find the median, first rank the values from low to high. Thentake the middle value. The median of the list {€ 2, € 2, € 4, € 5, € 22} is € 4.The median of the first list { € 2, € 2, € 4, € 5, € 7} is also € 4. As you cansee, the outlier doesn’t affect the median. When a density histogram is skewedor when there are outliers, the median usually is a better measure of the centraltendency. One example is the distribution of families by income (Freedmanet al., 2007, figure 4 p. 36).

1.5 Summarizing data by numbers: standarddeviation

We have seen how to summarize the central tendency of a data set. Anotherfeature we would like capture is the spread (or dispersion) of the data. Oneway to measure the spread is to look at how much the measurements deviatefrom the average. Let’s go back to the prices of the same bottle of wine in fiverestaurants:

€ 2,€ 2,€ 4,€ 5,€ 7

The average price is:

average =€ 2 +€ 2 +€ 4 +€ 5 +€ 7

5=€ 20

5= € 4

The deviation from the average measures how much a measurement is below(−) or above (+) the average:

deviation = measurement− average

The deviations are:

€ 2−€ 4 = −€ 2

€ 2−€ 4 = −€ 2

€ 4−€ 4 = € 0

€ 5−€ 4 = +€ 1

€ 7−€ 4 = +€ 3

8 CHAPTER 1. DESCRIPTIVE STATISTICS

To get an idea of the typical deviation, we could take the arithmetic mean ofthe deviations:

(−€ 2) + (−€ 2) +€ 0 + (+€ 1) + (+€ 3)

5= € 0

It can be easily proven that—whatever the list of measurements—the arithmeticmean of the deviations is always equal to 0: the negative deviations exactly can-cel out the positive ones. Therefore statisticians use the quadratic mean of thedeviations as a measure of the spread; the outcome is called the standard de-viation.

The standard deviation (SD) is a measure of the typical deviation of themeasurements from their mean. It is computed as the quadratic mean (or root-mean-square size) of the deviations from the average.

The quadratic mean is usually referred to as the root-mean-square (R-M-S)size. To obtain the standard deviation, find the deviations. The compute thequadratic mean (or root-mean-square size) of the deviations, apply the root-mean-square recipe in reverse order: first square the deviations, then find the(arithmetic) mean of the result, and finally take the (square) root. In ourexample:

1. Square the deviations:

(−€ 2)2 = €24

(−€ 2)2 = €24

(€ 0)2 = €20

(+€ 1)2 = €21

(+€ 3)2 = €29

By squaring we get rid of the minus signs. Note that the unit of measure-ment (here: €) is squared, too.

2. Next find the arithmetic mean (or average) of the results from the previousstep:

mean =€

24 +€ 24 +€ 20 +€ 21 +€ 29

5=€

218

5= € 23.6

The unit (€) is still squared (€ 2).

3. Finally take the square root of the result from the previous step:√€

23.6 ≈ € 1.90

This is the standard deviation. Note that by taking the square root, theunits are € again: the standard deviation has the same unit as themeasurements. In this case, the measurements were in euros, so thestandard deviation is also in euros.

1.5. SUMMARIZING DATA BY NUMBERS: STANDARD DEVIATION 9

Expressed as a formula, we get:

SD =

√sum of (deviations)

2

number of measurements

(The formula is on the formula sheet, so you don’t have to learn it by heart.)The formula above is for the standard deviation of a population. For reasons

I won’t explain, a better formula for the standard deviation of a sample is:

SD+ =

√sum of (deviations)

2

sample size×

√sample size

sample size− 1

that is, you compute the SD with the usual formula (the quadratic mean of thedeviations), which is the first factor in the equation above, and then multiplyby √

sample size

sample size− 1

(you don’t have to memorize this formula). Because the second factor is largerthan 1, the formula gives a value larger than SD. That’s why Freedman et al.(2007) use the notation SD+. For large samples, the difference between SD andSD+ is small. In what follows, we’ll use the SD formula for both samples andpopulations, unless stated explicitly otherwise. We’ll return to SD+ when wediscuss small samples.

Remember the following rule: few measurements are more than threeSDs from the average.1 This rule holds for histograms of any shape.

Measurements that are more than three SDs from the average (exceptionallysmall or exceptionally large measurements) are called outliers. To identifyoutliers, compute the standard scores of all measurements. The standard scoreexpresses how many standard deviations a measurement is below (−) or above(−) the average:

standard score =measurement− average

standard deviation

Converting measurements to standard scores is called standardizing.Let us return to the daily traded volumes of Apple shares (table 1.1). The

volumes of Apple shares trade on the first 50 trading days of 2013 have anaverage of 19 315 460 and a standard deviation of 7 466 246. On 14 March 2013only 10 828 780 Apple shares were traded. Is that volume exceptionally small?Compute the standard score for 10 828 780:

10 828 780− 19 315 460

7 466 246=−32 750 110

7 466 246≈ −1.13

De standard score of −1.13 means that the volume of 10 828 780 shares was1.13 standard deviations below the average. Because the absolute value of the

1A more precise statement can be made. It can be proven (Chebychev’s Theorem) that atleast 8/9 of the measurements fall within 3 SDs of the average, that is, between

[average− 3 · SD, average + 3 · SD]

Hence at most 1/9 of the measurements fall outside that interval. You don’t have to memorizethis.

10 CHAPTER 1. DESCRIPTIVE STATISTICS

standard score (after omitting the minus sign: 1.13) is smaller than 3, we don’tconsider 10 828 780 as an outlier.

Standard scores have no units. The following example illustrates this. Alist of incomes per person for most countries in the world (the Penn WorldTable, Heston et al. (2012)) has an average of $ 15 115 and a standard deviationof $ 18 651. Income per person in Belgium is $ 39 759. De standard score forincome per person in Belgium is:

$39 759− $15 115

$18 651=

$24 644

$18 651≈ 1.32

The units in the numerator ($) and denominator ($) cancel each other out, andhence the standard score has no units. That’s why Freedman et al. (2007) referto computing standard scores as converting a measurement to standard units.The standard score of 1.32 means that income per person in Belgium is 1.32standard deviations above the average of all countries in the list. So is incomeper person in Belgium an outlier?

Shortcut formula for the SD of 0-1 lists. Computing the SD is tedious.To estimate percentages, we’ll be dealing with lists that consist of just zeroesand ones (0-1 lists): for instance, we will model an employee with a privatepension plan as a 1, and an employee without a private pension plan as a 0.The following shortcut formula simplifies the calculation of the SD of 0-1lists: the standard deviation of a list that consist of just zeroes and ones can becomputed as:

SD of 0-1 list =

√(fraction of

ones in the list

)×(

fraction ofzeroes in the list

)(This formula is on the formula sheet, so no need to memorize. Just for your

information, I posted a proof on the course home page.)Here is an example. Consider the list {0, 1, 1, 1, 0}. The average is 3/5. The

deviations from the average are: {−3/5, 2/5, 2/5, 2/5,−3/5}, or {−0.6, 0.4, 0.4, 0.4,−0.6}.The SD is the root-mean-square size of the deviations:

1. Square the deviations: {0.36, 0.16, 0.16, 0.16, 0.36}

2. Next find the average of the squared deviations:

0.36 + 0.16 + 0.16 + 0.16 + 0.36

5=

1.20

5= 0.24

3. Finally take the square root to obtain the SD:

SD =√

0.24 ≈ 0.4898979

According to the shortcut rule we can compute the SD as:√(fraction of

ones

)×(

fraction ofzeroes

)which yields: √

3

5× 2

5=

√6

25=√

0.24 ≈ 0.4898979

which indeed yields the same result, with far fewer calculations.

1.6. THE NORMAL CURVE 11

1.6 The normal curve

Many bell-shaped histograms can be approximated by a special curve called thenormal curve. The function describing the normal curve is complicated:

y =1√2πe−x2/2

In practice we won’t need this equation: it is programmed in all statisticalsoftware packages. The equation describes the standard normal curve, whichis the only version of the normal curve we’ll need. In what follows, I’ll refer tothe standard normal curve simply as the normal curve.

Figure 1.2 illustrates the properties of the standard normal curve:

1. the curve is symmetric about 0;

2. the area under the curve is 100% (or 1);

3. the curve is always above the horizontal axis.

0

10

20

30

40

Standard units (z)

Den

sity

(% p

er s

tand

ard

unit)

-4 -3 -2 -1 0 1 2 3 4

Figure 1.2: The standard normal curve

Statisticians use statistical software (on a calculator or a computer) to findareas under the normal curve. On a TI-84, you find the area under the standardnormal curve using the normal cumulative density function (normalcdf). Thearea under the standard normal curve between −1 and 2 is:

12 CHAPTER 1. DESCRIPTIVE STATISTICS

DISTR → normalcdf(−1,2)which yields approximately 0.8186. To express the area as a percentage, multiplyby 100%:

0.8186× 100% = 81.86%

The area under the standard normal curve to the right of −1 (that is, between−1 and infinity) is:

DISTR → normalcdf(−1,1099)The area under the standard normal curve to the left of 2 (that is, betweenminus infinity and 2) is:

DISTR → normalcdf(−1099, 2)For the exams, you have to use the TI-84 to find areas under the normal curve.On the course web page I posted an R script (area-under-normal-curve.R)that computes and plots the area under the normal curve between any twovalues on the horizontal axis. R Commander has a built-in function to find thearea under the normal curve in the left tail or in the right tail:

Distributions → Continuous distributions → Normal distribution→ Normal probabilities . . .

1.7 Approximating a density histogram by thenormal curve

These are scores of 100 job applicants who took a selection test:

74, 82, 70, 84, 54, 60, 79, 62, 72, 66, 72, 79, 73, 73, 84, 59, 53, 65, 62, 81,76, 67, 72, 89, 70, 72, 71, 78, 98, 58, 68, 89, 70, 62, 71, 56, 68, 68, 76, 63,63, 71, 82, 63, 98, 76, 74, 71, 52, 80, 80, 66, 69, 67, 70, 81, 62, 63, 76, 57,89, 60, 87, 80, 75, 71, 87, 59, 69, 65, 66, 67, 62, 87, 58, 58, 60, 54, 74, 83,48, 77, 79, 60, 84, 86, 68, 64, 83, 65, 77, 79, 68, 75, 77, 72, 47, 77, 68, 67

(the data are posted on the course web page)The average of the test scores is about 70, and the standard deviation is about10 (verify using R Commander). Figure 1.3 shows the density histogram. Thehistogram is bell-shaped. In 1870, the Belgian statistician Adolphe Quetelet hadthe idea to approximate bell-shaped histograms by the normal curve (Freedmanet al., 2007, p. 78). The horizontal scale of the histogram differs from that ofthe standard normal curve: most test scores are between 40 and 100, while mostof the standard area under the normal curve extends between −3 and +3 onthe horizontal axis; and the center of the density histogram is about 70, whilethe center of the standard normal curve is 0. If we standardize the values, weget what we want. To obtain the standard scores, do:

standard score =measurement− average

standard deviation

For example, to standardize the first test score (74; in this case the variable hasno units), do:

standard score =74− 70

10= 0.4

The list of standard scores is: 0.4; 1.2; 0.0; . . . ; −0.3. Verify that you cancompute the first couple of standard scores.

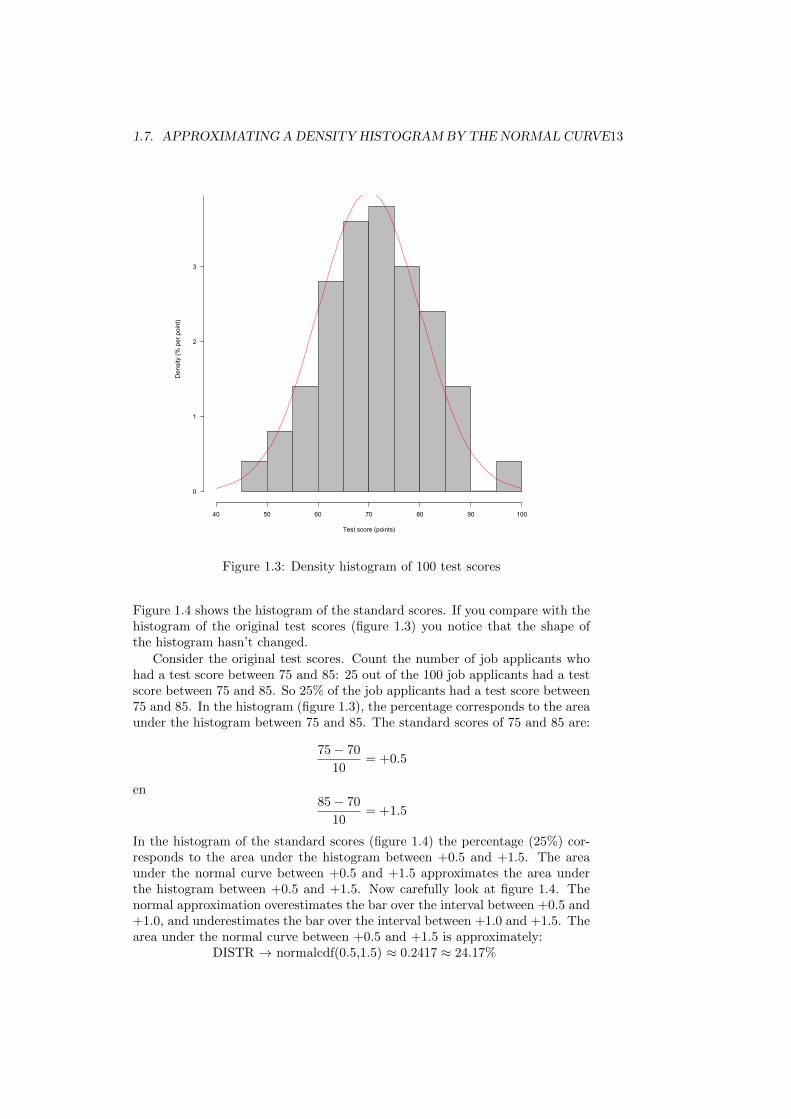

1.7. APPROXIMATING ADENSITY HISTOGRAMBYTHE NORMAL CURVE13

Test score (points)

Den

sity

(% p

er p

oint

)

40 50 60 70 80 90 100

0

1

2

3

Figure 1.3: Density histogram of 100 test scores

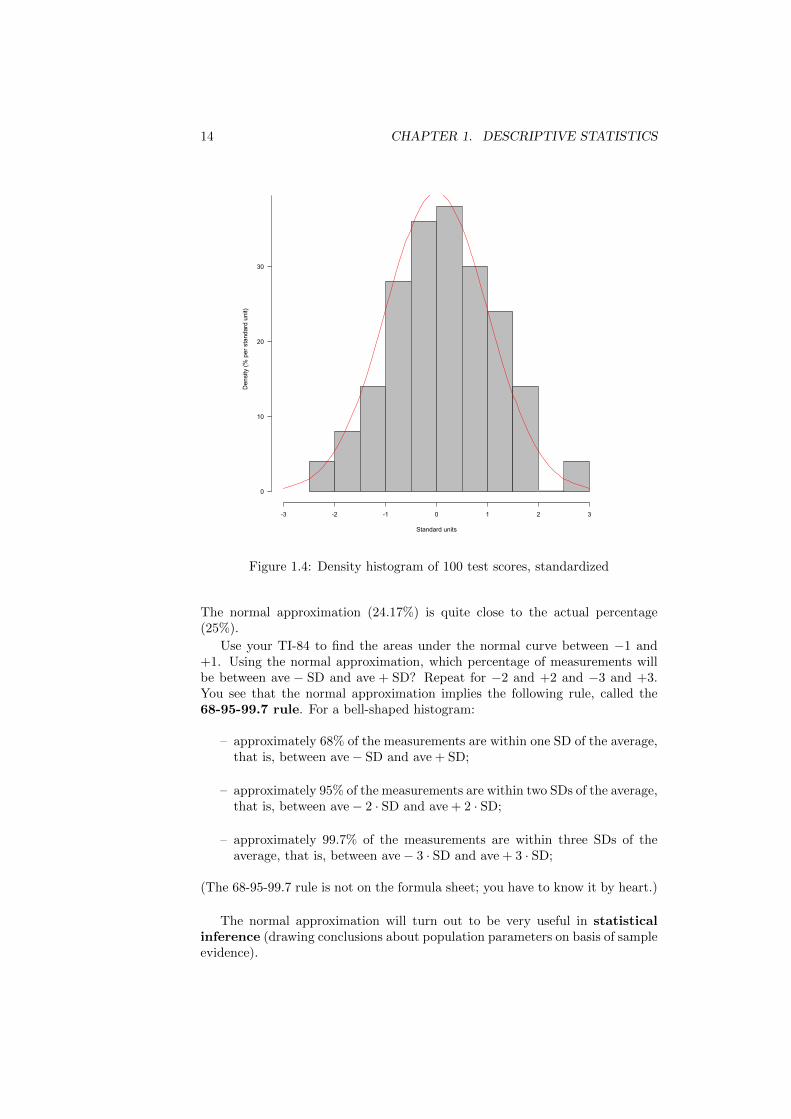

Figure 1.4 shows the histogram of the standard scores. If you compare with thehistogram of the original test scores (figure 1.3) you notice that the shape ofthe histogram hasn’t changed.

Consider the original test scores. Count the number of job applicants whohad a test score between 75 and 85: 25 out of the 100 job applicants had a testscore between 75 and 85. So 25% of the job applicants had a test score between75 and 85. In the histogram (figure 1.3), the percentage corresponds to the areaunder the histogram between 75 and 85. The standard scores of 75 and 85 are:

75− 70

10= +0.5

en85− 70

10= +1.5

In the histogram of the standard scores (figure 1.4) the percentage (25%) cor-responds to the area under the histogram between +0.5 and +1.5. The areaunder the normal curve between +0.5 and +1.5 approximates the area underthe histogram between +0.5 and +1.5. Now carefully look at figure 1.4. Thenormal approximation overestimates the bar over the interval between +0.5 and+1.0, and underestimates the bar over the interval between +1.0 and +1.5. Thearea under the normal curve between +0.5 and +1.5 is approximately:

DISTR → normalcdf(0.5,1.5) ≈ 0.2417 ≈ 24.17%

14 CHAPTER 1. DESCRIPTIVE STATISTICS

Standard units

Den

sity

(% p

er s

tand

ard

unit)

-3 -2 -1 0 1 2 3

0

10

20

30

Figure 1.4: Density histogram of 100 test scores, standardized

The normal approximation (24.17%) is quite close to the actual percentage(25%).

Use your TI-84 to find the areas under the normal curve between −1 and+1. Using the normal approximation, which percentage of measurements willbe between ave − SD and ave + SD? Repeat for −2 and +2 and −3 and +3.You see that the normal approximation implies the following rule, called the68-95-99.7 rule. For a bell-shaped histogram:

– approximately 68% of the measurements are within one SD of the average,that is, between ave− SD and ave + SD;

– approximately 95% of the measurements are within two SDs of the average,that is, between ave− 2 · SD and ave + 2 · SD;

– approximately 99.7% of the measurements are within three SDs of theaverage, that is, between ave− 3 · SD and ave + 3 · SD;

(The 68-95-99.7 rule is not on the formula sheet; you have to know it by heart.)

The normal approximation will turn out to be very useful in statisticalinference (drawing conclusions about population parameters on basis of sampleevidence).

1.8. QUESTIONS FOR REVIEW 15

1.8 Questions for Review

1. What is the difference between a qualitative and a quantitative variable?Illustrate using examples where you consider different characteristics ofthe students in the class.

2. What is the difference between a parameter and a statistic?

3. What does descriptive statistics do?

4. What does statistical inference do?

5. How can you summarize the distribution of a numerical data set in a table?In a graph?

6. In a density histogram, what does the density represent? What are theunits of density? Explain for a hypothetical distribution of heights (incentimeter) of people.

7. When would the median be a better measure of the central tendency of adistribution than the mean? Illustrate by giving an example.

8. What does the standard deviation measure? How is the standard deviationcomputed?

9. What are the properties of the normal curve?

10. What does the standard score measure? How is the standard score com-puted?

11. What does the 68-95-99.7% rule say?

1.9 Exercises

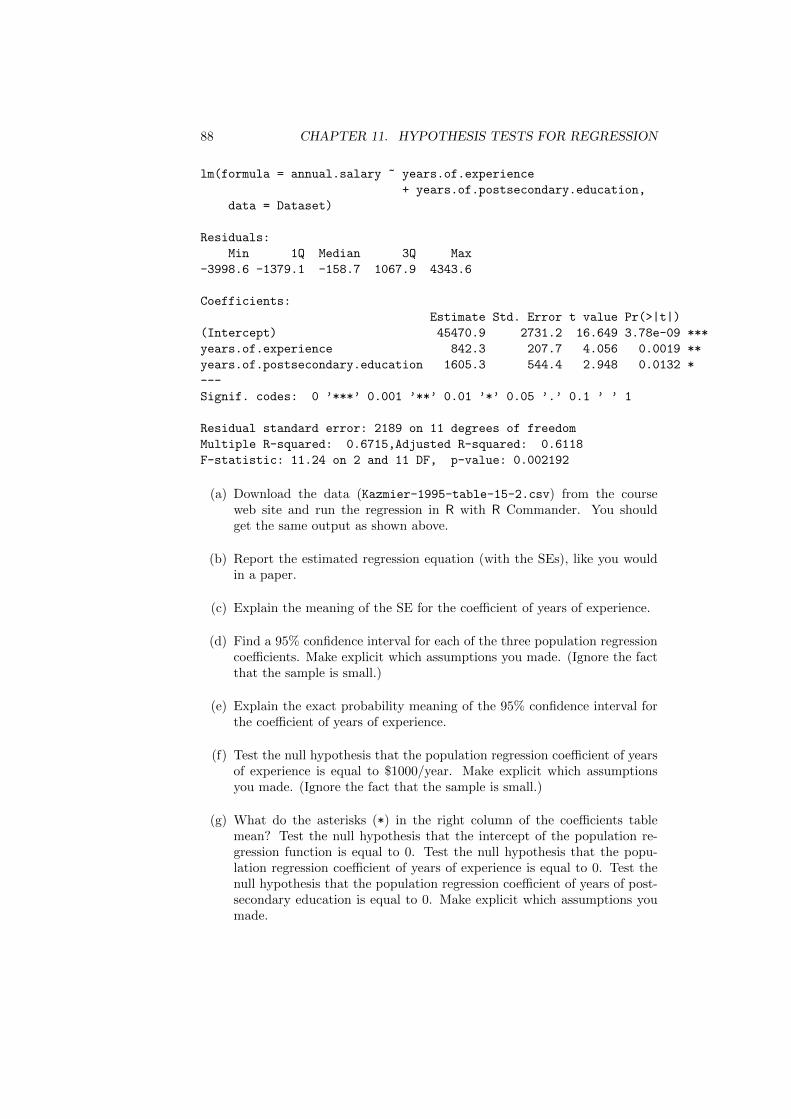

1. Download the data file AAPL-HistoricalQuotes.csv from the course website:

http://homepages.vub.ac.be/~lmahens/STA201.html

and save the data file to your STA201 folder (directory). The data set containsdata about Apple stock. Run R Commander and load the data set: Data →Import data → from textfile, clipboard, or URL. . . . A window opens. For“Location of Data File” select Local file system.” For “Field Separator” select“Commas.” For “Decimal-Point Character” select “Period [.]”. Press OK, nav-igate to the data file AAPL-HistoricalQuotes.csv, abd double-click the file.Your data should now be loaded by R Commander. In the R Commander menu,click the View Data Set button. A new window opens, showing the data set.The variable volume is the variable from table 1.1. Now enter the following lineof script in the R script window:

h <- hist(Dataset$volume/1000000,right=FALSE)

and press the Submit button. This command will compute the numbers neededto make a histogram and store then in an object called h. Next, type in the R

script window:

16 CHAPTER 1. DESCRIPTIVE STATISTICS

h$breaks

and press the Submit button. The output window will display the breaks be-tween the intervals, that is, the boundaries of the intervals used by R when itcomputes the frequency table. Next, type in the R script window:

h$counts

and press the Submit button. The output window will display the absolutefrequencies (counts) of each interval. Next, type in the R script window:

h$density

and press the Submit button. The output window will display the densities ofeach interval. The densities are expressed as decimal fractions per horizontalunit; to get densities expressed as percentages per horizontal unit you have tomultiply by 100%. Finally, type in the R script window:

h$counts/sum(h$counts)

and press the Submit button. The output window will display the relativefrequencies for each interval; to get relative frequencies expressed as percentagesyou have to multiply by 100%.

2. Use the relative frequencies from table 1.2 to compute the densities for theother intervals. Add a column to show the densities. Then draw the densityhistogram on scale on squared paper.

3. Figure 1.1 shows that the daily traded volumes of Apple shares have askewed distribution. The average daily volume is 19 315 460 shares. Find themedian. Show your work. How do mean and median compare? Is that whatyou expected from the shape of the histogram? Explain.

4. Find the standard deviation of {1, 1, 1, 1, 0} using two methods: the usualformula (root-mean-square size of the deviations) and the shortcut formula for0-1 lists. Do you get the same result?

5. The daily traded volumes of Apple shares (table 1.1) have an average of19 315 460 and a standard deviation of 7 466 246. Is 52 065 570 an outlier? And43 088 190? Show your work and explain.

6. Use the TI-84 to find the areas under the standard normal curve:

(a) to the right of 1.87

(b) to the left of −5.20

(c) between −1 and +1

(d) between −2 and +2

(e) between −3 and +3

Make for every case a sketch, with the relevant area shaded. Verify your answersusing the R script. We’ll get back to cases (c), (d), and (e) in a moment.

1.9. EXERCISES 17

7. For the 100 given test scores, find which percentage of job applicants scoredbetween 50 and 60. Then use the normal approximation. Is the normal approx-imation close?

8. For 164 adult Belgian men born in 1962 the average height is 175.7 cen-timeter and the SD is 8.2 centimeter (Garcia and Quintana-Domeque, 2007).Suppose that the histogram of the 164 heights follows the normal curve (heightsusually do). What is, approximately, the percentage of men in this group witha height of 170 centimeter or less? What is, approximately, the percentage ofmen in this group with a height of between 170 centimeter and 180 centimeter?

9. Of the volumes of Apple shares traded in the first 50 trading days of 2013(p. 1.2) the average is 19 315 460 and the SD is 7 466 246. Find the actualpercentage of values between:

ave− SD and ave + SD;

ave− 2 · SD and ave + 2 · SD;

ave− 3 · SD and ave + 3 · SD;

Does the 68-95-99.7 rule give a good approximation? Why (not)?

18 CHAPTER 1. DESCRIPTIVE STATISTICS

Chapter 2

Probability distributions

2.1 Chance experiments

Examples of chance experiments are: rolling a die and counting the dots;tossing a coin and observing whether you get heads or tails; or randomly drawinga card from a well-shuffled deck of cards and observing which card you get.

It is convenient to think of a chance experiment in terms of the followingchance model: randomly drawing one or more tickets from a box. For instance,rolling a die is modeled as randomly drawing a ticket from the box:

1 2 3 4 5 6

In R:

box <- c(1,2,3,4,5,6)

sample(box,1)

Tossing a coin is like randomly drawing a ticket from the box:

heads tails

In R:

box <- c("heads","tails")

sample(box,1)

2.2 Frequency interpretation of probability

Consider the following chance experiment. Roll a die and count the dots. Ifyou get an ace (1), write down 1; if you don’t get an ace (2, 3, 4, 5, or 6),write down 0. Repeat the experiment many times. After each roll, computethe relative frequency of aces up to that point. Make a graph with the numberof tosses on the horizontal axis and the relative frequency on the vertical axis.Figure 2.1 shows the result of 10 000 repetitions in such an experiment. Thefrequency of aces tends towards 1/6 (16.666 . . .%, the horizontal dashed line).The frequency interpretation of probability states that the probability ofan event is the percentage to which the relative frequency tends if you repeat thechance experiment over and over, independently and under the same conditions(Freedman et al., 2007, p. 222).

19

20 CHAPTER 2. PROBABILITY DISTRIBUTIONS

0 2000 4000 6000 8000 10000

0

20

40

60

80

100

Number of repeats

Freq

uenc

y of

ace

s (%

)

Figure 2.1: Frequency of aces in 10,000 rolls of a die

2.3 Drawing with and without replacement

Consider the following box with tickets:

1 2 3 4 5 6

The probability to draw an even number is 3/6:

P ( 2nd draw is even ) =3

6

Suppose you randomly draw a ticket from the box. The ticket turns out to be2 . Suppose you replace the ticket, and again randomly draw a ticket from the

box. This is called drawing with replacement. The conditional probabilityto draw an even number on the second draw, given that the first draw was 2 ,is again 3/6. In mathematical notation:

P ( 2nd draw is even | 1st draw was 2 ) =3

6

The vertical bar (|) is shorthand for “given that.” What comes after the ver-tical bar (|) is called the condition. A probability with a condition is called aconditional probability.

Note that in this case imposing the condition didn’t affect the probability ofdrawing an even number: whether the first draw was 2 or not doesn’t matter

2.4. THE SUM OF DRAWS 21

for the second draw, because we replaced the ticket after the first draw. In bothcases, the probability of getting an even number was the same (3/6):

P ( 2nd draw is even | 1st draw was 2 ) = P ( 2nd draw is even )

The two events (getting an even number on the second draw, and getting an evennumber on the second draw) are said to be independent: the probability of thesecond event is not affected by how the first event turned out. That is becausewe were drawing with replacement. When drawing with replacement, theevents are independent.

Now consider a different chance experiment. Suppose you randomly draw aticket from the box. The ticket turns out to be 2 . Suppose you don’t replacethe ticket. The box now looks like this:

1 3 4 5 6

If we now again randomly draw a ticket from the box, this is called drawingwithout replacement. The conditional probability to draw an even numberon the second draw, given that the first draw was 2 now is :

P ( 2nd draw is even | 1st draw was 2 ) =2

5

In this case, what happened in the first draw (as expressed by the condition

“1st draw was 2 ”) does make a difference: the probability of getting an evennumber differs:

P ( 2nd draw is even | 1st draw was 2 ) 6= P ( 2nd draw is even )

The two events (getting an even number on the second draw, and getting an evennumber on the second draw) are said to be dependent: the probability of thesecond event is affected by how the first event turned out. That is because wewere drawing without replacement. When drawing without replacement,the events are dependent.

Think of a population as a box with tickets. A random sample is like drawinga number of tickets without replacement from this box. The number of draws isthe sample size. Remember this. We’ll use this box model when doing statisticalinference.

2.4 The sum of draws

For the theory of statistical inference, we’ll frequently use the concept of thesum of draws. Here’s a simple example: roll a die twice, and add the numbers.The chance model has the following box:

1 2 3 4 5 6

Draw two tickets with replacement from the box, and add the outcomes. Theresult is the sum of draws.

The sum of draws is a brief way to say the following (Freedman et al.,2007, p. 280):

22 CHAPTER 2. PROBABILITY DISTRIBUTIONS

– Draw tickets from a box.

– Add the numbers on the tickets.

As the following activity makes clear, the sum of draws is itself a random vari-able:

(a) Conduct the chance experiment above using an actual die or the followingR script:

box <- c(1,2,3,4,5,6)

sample(box,1) + sample(box,1)

(b) Repeat the experiment a couple of times and write up the outcomes (usingan actual die, or in R by running the line sample(box,1)+sample(box,1).Would it be fair to say that the sum of draws is a chance variable? Explain.

2.5 Picking an appropriate chance model

We model a population as a box with tickets. Taking a random sample is likerandomly drawing a number of tickets from the box, without replacement; thenumber of draws is the sample size. In order to use such a chance model forinference, we will use some interesting properties of the sum of draws. The trickis to set up the chance model in such a way that the chance variable of interestis the sum of draws, or is computed from the sum of draws. An example clarifiesmy argument.

Suppose you roll a die three times, and want to know what the sum ofthe outcomes is. What is the appropriate chance model? What is the chancevariable?An appropriate chance model is a box with six tickets:

1 2 3 4 5 6

and the chance variable is the sum of three random draws with replacementfrom the box. For instance, if you roll 3, 2, and 6, this corresponds to drawingtickets 3 , 2 , and 6 . The sum of draws ( 3 + 2 + 6 = 11) is obtained byadding up the outcomes.

Now suppose that we are interested in another question: how many times(out of three rolls) will we get a six? First, we need the appropriate chancemodel. When we roll a die, when can get two kinds of outcomes: either we geta six (we’ll label this outcome as a success), or we get another number (1, 2, 3,4, 5: not a success). The term success is used here in a technical meaning: theoutcome we are interested in. Note that we classify the outcomes of a singleroll as a success or not a success. In such a case, the appropriate chance modelis a box with six tickets: one ticket 1 for the outcome 6 labelled as a success,

and five tickets 0 for the outcomes 1, 2, 3, 4, or 5 labelled as not a success:

0 0 0 0 0 1

2.6. PROBABILITY DISTRIBUTIONS 23

Now we are interested in the number of sixes in three rolls, so we need to countthe sixes. Counting the sixes is the same thing as taking the sum of threedraws from the 0-1 box. For instance, if you roll 3, 2, and 6, this correspondsto drawing tickets 0 , 0 , and 1 (we classified each outcome as a success or

not a success). The sum of draws ( 0 + 0 + 1 = 1) is the number of sixes(the number of successes). A box like this, with tickets that can only takevalues 0 and 1, is called a 0-1 box. Remember that when the problem is one ofclassifying and counting, the appropriate box is a 0-1 box.

Here’s a real-world example. Suppose you are the marketing manager of atelecommunications company that doesn’t cover Brussels yet. You would like tofind out which percentage of households in Brussels already has a tablet. Thepopulation of interest is all households in Brussels. Think of each householdin Brussels as a ticket in a box, so there are as many tickets as households. Aticket takes value 1 if the household has a tablet, and 0 if the household doesn’t.Taking a random sample of households is like randomly drawing tickets withoutreplacement from this 0-1 box. The number of households in the sample whohave a tablet is the sum of draws. The percentage of households in the samplewho have a tablet is:

sample percentage =sum of draws

size of the sample× 100%

2.6 Probability distributions

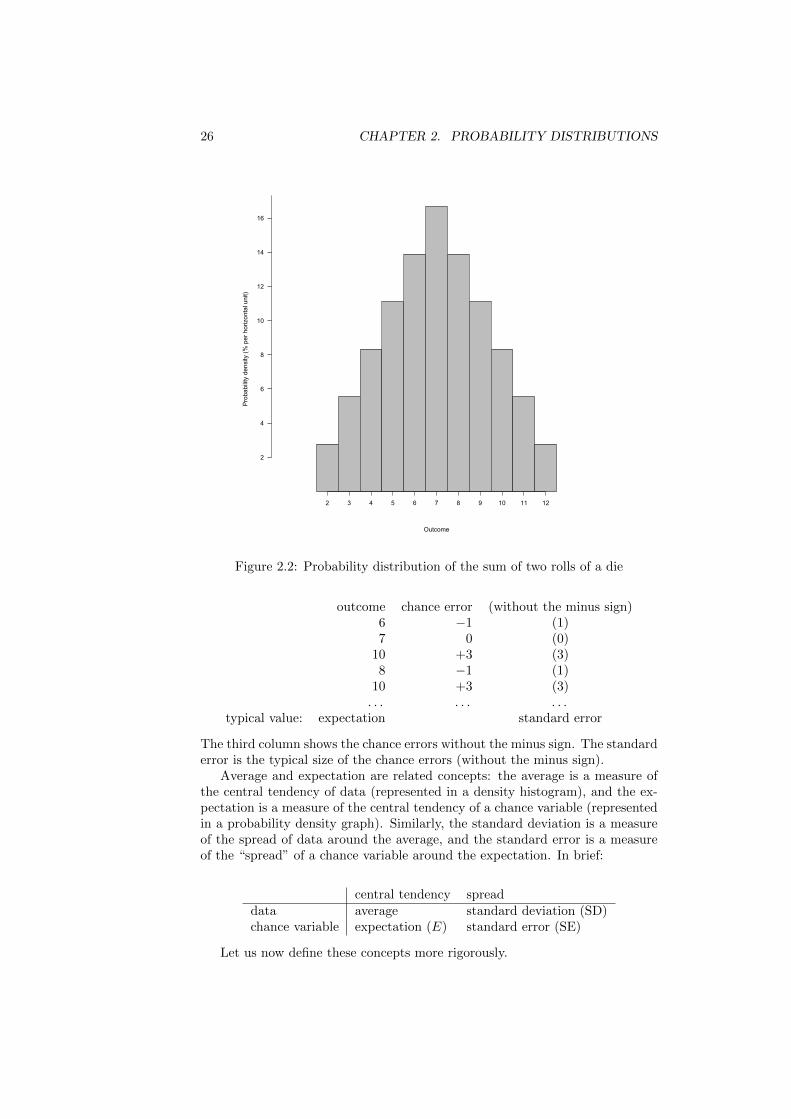

Chance experiments can be described using probability distributions. In whatfollows, we’ll focus on the probability distribution of the sum of draws. Supposeyou roll a die twice and add the outcomes. The chance model is: randomlydraw two tickets with replacement from the box

1 2 3 4 5 6

and add the outcomes.The chance variable (the sum of the two draws) can take the following val-

ues: {2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12} (the chance variable is discrete; we won’tdevelop the theory for continuous chance variables). For each of these possibleoutcomes, we can compute the probability. There are 36 possible combinations:

1 2 3 4 5 61 2 3 4 5 6 72 3 4 5 6 7 83 4 5 6 7 8 94 5 6 7 8 9 105 6 7 8 9 10 116 7 8 9 10 11 12

Each of these 36 combinations has the same probability, and as the probabilitieshave to add up to 1, each combination has a probability of 1/36. By applyingthe rules or probability, we can find the probability that the sum of draws takesthe value 2, and then repeat the work to find the probability that the sum ofdraws takes the value 3, and so on. There are for instance two combinationsthat yield a sum of 3:

24 CHAPTER 2. PROBABILITY DISTRIBUTIONS

– when the first draw is 1 and the second draw is 2 (row 1, column 2 in thetable above)

– when the first draw is 2 and the second draw is 1 (row 2, column 1)

The probability that the sum of draws is 3 is therefore equal to:

P (sum is 3) = P [(first 1, than 2) or (first 2, then 1)]

Apply the addition rule (Freedman et al., 2007, pp. 241–242) to obtain:

P (sum is 3) = P (first 1, than 2) + P (first 2, then 1)− something

The third term (“minus something”) is equal to zero because the events (first 1,than 2) and (first 2, then 1) are mutually exclusive (two events are mutuallyexclusive when as one event happens, the other cannot happen at the sametime). So we get:

P (sum is 3) = P (first 1, than 2) + P (first 2, then 1)− 0 =1

36+

1

36=

2

36

If you do this for all other possible values of the chance variable, you get thefollowing table:

outcome 2 3 4 5 6 7 8 9 10 11 12probability 1

36236

336

436

536

636

536

436

336

236

136

A table that shows all possible values for a (discrete) chance variable and thecorresponding probabilities is called a probability distribution.

We can graph the probability distribution as a bar chart. On the horizontalaxis we put the chance variable, and we construct the bar chart in such a waythat the area of a bar shows the probability (expressed as a percentage), just asin a density histogram the area of a bar showed the relative frequency (expressedas a percentage) of the data over the interval. That is why Freedman et al. (2007,pp. 310–316) call such a bar chart a probability histogram. For a discrete chancevariable the convention is to center the bars on the values that the variable cantake: the bar over 2 will start at 1.5 and end at 2.5; the bar over 3 will startat 2.5 and end at 3.5, and so on. The width of each bar is equal to 1. Theheight of each bar in a probability distribution is called probability density:the probability per unit on the horizontal axis. We find the probability densitiesby applying the formula for the area of a rectangle:

area = width× height

We want the area to represent the probability (expressed as a percentage) andthe height to represent the probability density (expressed as percent per uniton the horizontal axis), and hence the equation becomes:

probability = width of interval on horizontal axis× probability density

Divide both sides of the equation by (width of interval on horizontal axis) toobtain:

probability density =probability

width of interval on horizontal axis

2.6. PROBABILITY DISTRIBUTIONS 25

Because the width of each interval on horizontal axis is one unit of the horizontalaxis, this becomes:

probability density = probability per unit on the horizontal axis

which gives us the meaning of probability density.

For example, the probability to get a 7 is 6/36 (= 16.66 . . .%). The proba-bility density over the interval from 6.5 to 7.5 then is equal to:

probability density =16.66 . . .%

7.5− 6.5= 16.66 . . .% per per unit on the horizontal axis

Figure 2.2 shows the corresponding bar chart representing the probabilitydistribution. The curve traced by the bar chart of the probability distributionis called the probability density function. The probability density functionhas the following properties:

– the curve is always on or above the horizontal axis, that is, the probabilitydensity (on the vertical axis) is always 0 or positive;

– de area under the curve is equal to 1 (or 100%);

– the area under the curve between two values on the horizontal axis givesthe probability.

The probability distribution has an expectation and a standard error. Thefollowing example illustrates the intuition of these concepts. Roll a die twiceand add the numbers. You can do that with an actual die, or run the followingR script:

box <- c(1,2,3,4,5,6)

sample(box,1) + sample(box,1)

Repeat this a couple of times, and write down the outcomes. You will getsomething like {6, 7, 10, 8, 10, . . . }. The outcomes are random. The lowestvalue you can get is 2 (when you roll two aces), and the highest value is 12(when you roll two sixes). If you repeat the experiment many times you’ll noticethat those extreme values occur only occasionally; values like 6, 7, or 8 occurmuch more frequently. The expectation is the typical value that the randomvariable will take; the value around which the outcomes vary. Another wayto think about the expectation is as the center of the probability distribution(figure 2.2). In this case the expectation is 7 (we’ll see below how to computethe expectation). Now define the difference between the outcome of a chanceexperiment and the expectation as the chance error. For instance, our firstoutcome was 6, the expectation is 7, and hence the chance error was:

chance error = outcome− expectation = 6− 7 = −1

(the negative value of 1 means that the outcome was 1 below the expectation).

If we compute the chance errors for the other outcomes, we get:

26 CHAPTER 2. PROBABILITY DISTRIBUTIONS

Outcome

Pro

babi

lity

dens

ity (%

per

hor

izon

tal u

nit)

2 3 4 5 6 7 8 9 10 11 12

2

4

6

8

10

12

14

16

Figure 2.2: Probability distribution of the sum of two rolls of a die

outcome chance error (without the minus sign)6 −1 (1)7 0 (0)

10 +3 (3)8 −1 (1)

10 +3 (3). . . . . . . . .

typical value: expectation standard error

The third column shows the chance errors without the minus sign. The standarderror is the typical size of the chance errors (without the minus sign).

Average and expectation are related concepts: the average is a measure ofthe central tendency of data (represented in a density histogram), and the ex-pectation is a measure of the central tendency of a chance variable (representedin a probability density graph). Similarly, the standard deviation is a measureof the spread of data around the average, and the standard error is a measureof the “spread” of a chance variable around the expectation. In brief:

central tendency spreaddata average standard deviation (SD)chance variable expectation (E) standard error (SE)

Let us now define these concepts more rigorously.

2.7. INTERMEZZO: A WEIGHTED AVERAGE 27

2.7 Intermezzo: a weighted average

To define the expectation and standard error of a discrete chance variable, weneed the concept of a weighted average. A weighted arithmetic average ofa list of numbers is obtained by multiplying each value in the list by a weightand adding up the outcomes; each of the weights is a number between zero(included) and one (included), and the weights add up to one. Suppose the firstvalue in the list is x1 and its weight is w1, the second value in the list is x2 andwith weight w2, . . . , and the last (nth) value in the list is xn and with weightwn, then the weighted average is:

(w1 × x1) + (w2 × x2) + . . .+ (wn × xn)

An example is the way a professor computes the students’ grades for a course.Here are the weights for the graded components of a course, and the results fora student:

component weight (%) result (score/20)assignment 1 7.50 12assignment 2 7.50 14assignment 3 7.50 16assignment 4 7.50 12participation and preparedness 10.00 16midterm exam 30.00 12final exam 30.00 17

Each weight is between 0 and 1: 7.50 percent is 0.075, 10 percent is 0.10, and30 percent is 0.30. Moreover, the sum of the weights is equal to 1:

7.50% + 7.50% + 7.50% + 7.50% + 10.00% + 30.00% + 30.00% = 100% = 1

The weighted average of the scores is:

(0.075× 12) + (0.075× 14) + (0.075× 16) + (0.075× 12)

+(0.10× 16) + (0.30× 12) + (0.30× 17) = 14.35

So this student has an overall score of 14.35/20.

2.8 Expectation (E)

Just as the average is a measure of the central tendency of a density histogram,the expectation of a chance variable is in a sense a measure for the centraltendency of a probability distribution. For a discrete chance variable, the ex-pectation is defined as the weighted average of all possible values that thechance variable can take; the weights are the probabilities.

The probability distribution of the sum of two rolls of a die is:

outcome 2 3 4 5 6 7 8 9 10 11 12probability 1

36236

336

436

536

636

536

436

336

236

136

The expectation of the chance variable “sum of two rolls of a die” (or of twodraws with replacement from a box with the tickets {1,2,3,4,5,6}) is the weighted

28 CHAPTER 2. PROBABILITY DISTRIBUTIONS

average:

2× 1

36+ 3× 2

36+ 4× 3

36+ 5× 4

36+ 6× 5

36+ 7× 6

36+ 8× 5

36

+9× 4

36+ 10× 3

36+ 11× 2

36+ 12× 1

36

=2 + 6 + 12 + 20 + 30 + 42 + 40 + 36 + 30 + 22 + 12

36=

252

36= 7

Let the operator E denote the expectation:

E(sum of two rolls of die) = 7

2.9 Standard error (SE)

Just as the standard deviation is a measure of the spread of a density histogram,the standard error of a chance variable is in a sense a measure for the spread ofa probability distribution.

We defined the chance error as the difference between the outcome of achance variable and the expectation of that chance variable. If the chanceexperiment is to roll a die twice and add the outcomes, we could get 2 as anoutcome; in that case de chance error is 2 − 7 = −5. For the outcome 3, thechance error is 3−7 = −4, etc. It is useful to add the chance errors to the tableof the probability distribution:

outcome 2 3 4 5 6 7 8 9 10 11 12probability 1

36236

336

436

536

636

536

436

336

236

136

chance error -5 -4 -3 -2 -1 0 1 2 3 4 5

The standard error of a discrete chance variable is defined as the weightedquadratic average of the chance errors; the weights are the probabilities. (Aquadratic average is the root-mean-square size.)

Start from the chance errors in the example (the third line we just added tothe table of the probability distribution):

−5,−4,−3,−2,−1, 0, 1, 2, 3, 4, 5

1. Square. First square the chance errors: (−5)2, (−4)2, (−3)2, (−2)2, (−1)2,02, 12,22, 32, 42, 52. This yields:

25, 16, 9, 4, 1, 0, 1, 4, 9, 16, 25

2. Mean. Then take the weighted average. Use the probabilities of the chanceerrors as the weights:

1

36× 25 +

2

36× 16 +

3

36× 9 + . . . ≈ 5.33

Verify that this indeed yields approximately 5.33 (a spreadsheet is helpful).

3. Root. Finally take the square root:√

5.33 ≈ 2.42

The standard error of the sum of two draws from {1, 2, 3, 4, 5, 6} is approxi-mately 2.42. You can think of this as the typical size of the chance errors.

2.10. EXPECTATION AND SE FOR THE SUM OF DRAWS 29

2.10 Expectation and SE for the sum of draws

When doing statistical inference, we’ll use the sum of draws with replacementfrom a box with tickets. The formulas for the expectation and the standarderror of discrete probability distributions from the previous sections also applyif the chance variable is a sum of draws. However, the computations can becometedious. It can be shown that the following formulas hold:

E(sum of draws) = (number of draws)× (average of box)

SE(sum of draws) =√

number of draws× (SD of the box)

“Average of box” means: the average of the values on the tickets in the box;similarly “SD of the box” means the SD of the values on the tickets in the box.You don’t have to memorize these formulas; they are on the formula sheet. Ininference, the box will represent the population, so the average of the box is thepopulation average and the SD of the box is the population SD.

Let us apply these formulas to the example from the previous sections: rolla die twice and add the outcomes. The chance model is: randomly draw twotickets with replacement from the box

1 2 3 4 5 6

and add the outcomes. We found in the previous sections that the expectationis 7 and the SE is approximately 2.42. What is we use the formulas for theexpectation and the SE of the sum of draws?

To apply the formula for the expectation of the sum of draws we first needthe average of the box:

average of box =1 + 2 + 3 + 4 + 5 + 6

6=

21

6

The expectation of the sum of two draws is:

E(sum of draws) = (number of draws)× (average of box) = 2× 21

6=

21

3= 7

This is the same number we found be applying the definition of the expectation.To apply the formula for the standard error for the sum of draws, we first

need the SD of the box; the SD of the box is about 1.71 (exercise: verify this).Then apply the formula for the standard error for the sum of draws:

SE (sum of draws) =√

number of draws× (SD of the box) ≈√

2× 1.71 ≈ 2.42

This is the same number we found be applying the definition of the standarderror.

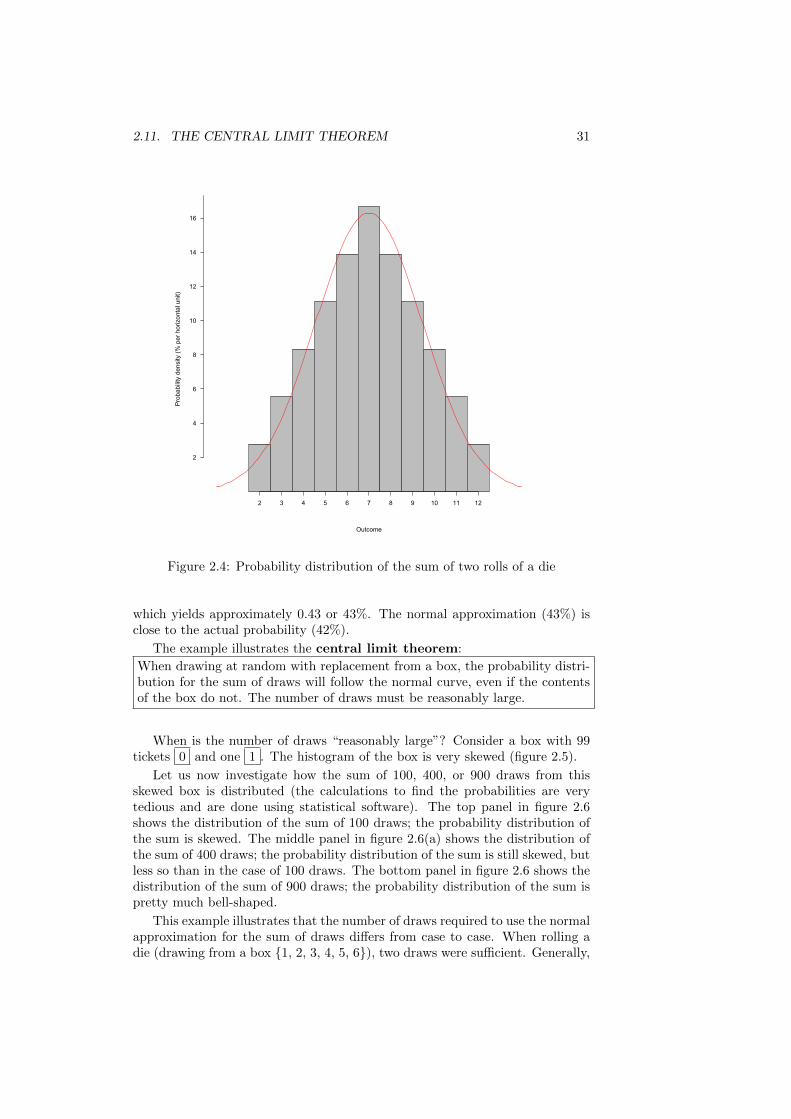

2.11 The Central Limit Theorem

Consider again the chance experiment: roll a die twice and add the outcomes.The chance model is: randomly draw two tickets with replacement from the box

1 2 3 4 5 6

30 CHAPTER 2. PROBABILITY DISTRIBUTIONS

OutcomeD

ensi

ty (%

per

uni

t on

the

horiz

onta

l axi

s)

1 2 3 4 5 6

10

20

Figure 2.3: Histogram of the dots on a die

and add the outcomes. The chance variable is the sum of draws. A histogramof the box (the list of numbers {1, 2, 3, 4, 5, 6}) is shown in figure 2.3. Notethat the histogram is not bell-shaped at all.

We already computed and plotted the probability distribution of the sum oftwo draws (figure 2.2). Figure 2.4 compares the probability distribution withthe normal curve. The normal curve approximates the probability distributionreasonably well. From the probability distribution table (p. 2.9) we know thatthe probability to get an outcome between 5 (included) and 7 (included) is

4

36+

5

36+

6

36=

15

36≈ 42%

In figure 2.4 the probability of 42%corresponds to the area of the bar over 5(between 4.5 and 5.5), plus the area of the bar over 6 (between 5.5 and 6.5), plusthe area of the bar over 7 (between 6.5 and 7.5). The area under the normalcurve between 4.5 and 7.5 approximates the area under the blocks. We can findthe area under the normal curve between 4.5 and 7.5 using statistical software.First, standardize the boundaries of the interval (4.5 and 7.5). The variableon the horizontal axis is a chance variable, not data, so we use the expectationinstead of the average and the standard error instead of the standard deviationto standardize:

chance variable in standard units =value− expectation

SE

The left boundary (4.5) in standard units is approximately:

4.5− 7

2.42≈ −1.04

The right boundary (7.5) in standard units is approximately:

7.5− 7

2.42≈ 0.21

To find the area under the standard normal curve between −1.04 and 0.21 onthe TI-84, use the normalcdf-function:

normalcdf(-1.04,0.21)

2.11. THE CENTRAL LIMIT THEOREM 31

Outcome

Pro

babi

lity

dens

ity (%

per

hor

izon

tal u

nit)

2 3 4 5 6 7 8 9 10 11 12

2

4

6

8

10

12

14

16

Figure 2.4: Probability distribution of the sum of two rolls of a die

which yields approximately 0.43 or 43%. The normal approximation (43%) isclose to the actual probability (42%).

The example illustrates the central limit theorem:

When drawing at random with replacement from a box, the probability distri-bution for the sum of draws will follow the normal curve, even if the contentsof the box do not. The number of draws must be reasonably large.

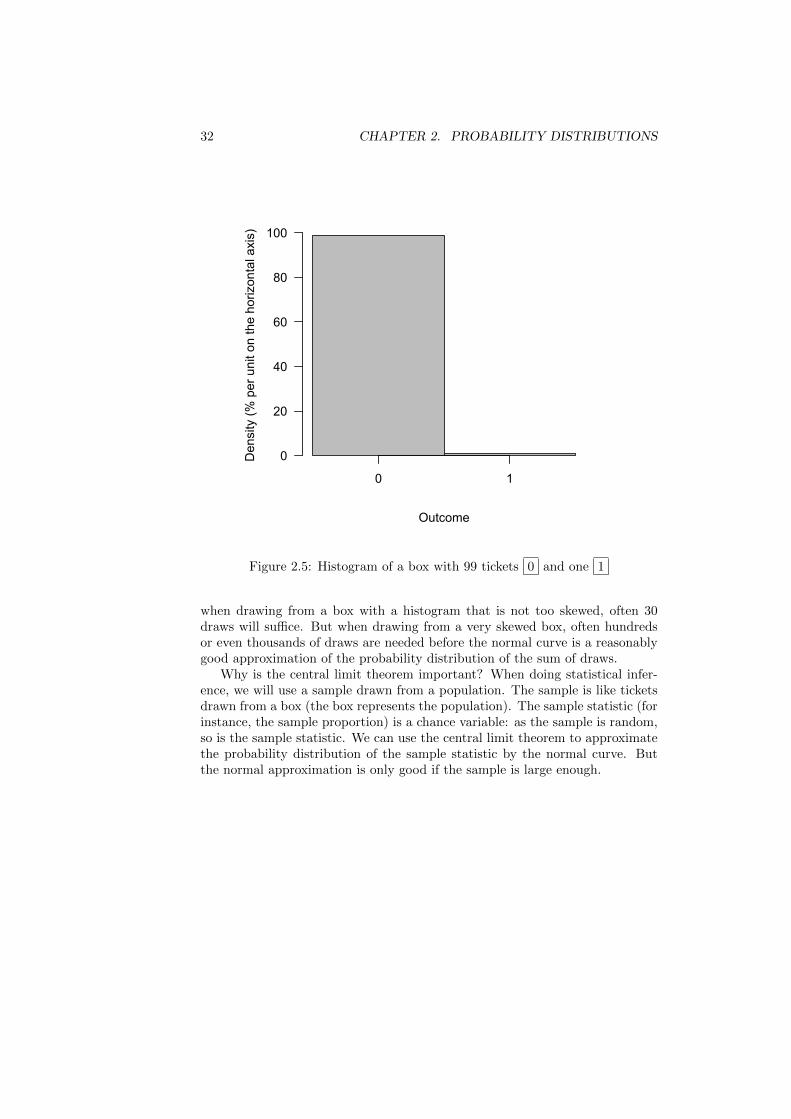

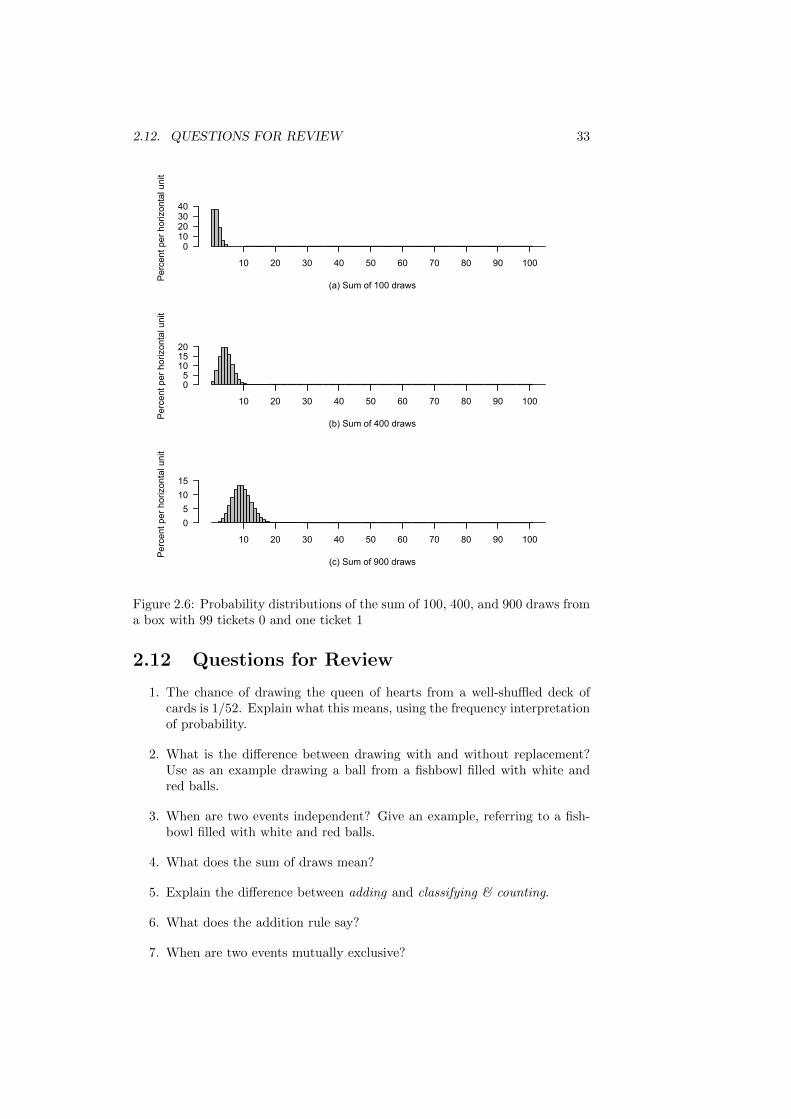

When is the number of draws “reasonably large”? Consider a box with 99tickets 0 and one 1 . The histogram of the box is very skewed (figure 2.5).

Let us now investigate how the sum of 100, 400, or 900 draws from thisskewed box is distributed (the calculations to find the probabilities are verytedious and are done using statistical software). The top panel in figure 2.6shows the distribution of the sum of 100 draws; the probability distribution ofthe sum is skewed. The middle panel in figure 2.6(a) shows the distribution ofthe sum of 400 draws; the probability distribution of the sum is still skewed, butless so than in the case of 100 draws. The bottom panel in figure 2.6 shows thedistribution of the sum of 900 draws; the probability distribution of the sum ispretty much bell-shaped.

This example illustrates that the number of draws required to use the normalapproximation for the sum of draws differs from case to case. When rolling adie (drawing from a box {1, 2, 3, 4, 5, 6}), two draws were sufficient. Generally,

32 CHAPTER 2. PROBABILITY DISTRIBUTIONS

Outcome

Den

sity

(% p

er u

nit o

n th

e ho

rizon

tal a

xis)

0 1

0

20

40

60

80

100

Figure 2.5: Histogram of a box with 99 tickets 0 and one 1

when drawing from a box with a histogram that is not too skewed, often 30draws will suffice. But when drawing from a very skewed box, often hundredsor even thousands of draws are needed before the normal curve is a reasonablygood approximation of the probability distribution of the sum of draws.

Why is the central limit theorem important? When doing statistical infer-ence, we will use a sample drawn from a population. The sample is like ticketsdrawn from a box (the box represents the population). The sample statistic (forinstance, the sample proportion) is a chance variable: as the sample is random,so is the sample statistic. We can use the central limit theorem to approximatethe probability distribution of the sample statistic by the normal curve. Butthe normal approximation is only good if the sample is large enough.

2.12. QUESTIONS FOR REVIEW 33

(a) Sum of 100 draws

Per

cent

per

hor

izon

tal u

nit

010203040

10 20 30 40 50 60 70 80 90 100

(b) Sum of 400 draws

Per

cent

per

hor

izon

tal u

nit

05101520

10 20 30 40 50 60 70 80 90 100

(c) Sum of 900 draws

Per

cent

per

hor

izon

tal u

nit

051015

10 20 30 40 50 60 70 80 90 100

Figure 2.6: Probability distributions of the sum of 100, 400, and 900 draws froma box with 99 tickets 0 and one ticket 1

2.12 Questions for Review

1. The chance of drawing the queen of hearts from a well-shuffled deck ofcards is 1/52. Explain what this means, using the frequency interpretationof probability.

2. What is the difference between drawing with and without replacement?Use as an example drawing a ball from a fishbowl filled with white andred balls.

3. When are two events independent? Give an example, referring to a fish-bowl filled with white and red balls.

4. What does the sum of draws mean?

5. Explain the difference between adding and classifying & counting.

6. What does the addition rule say?

7. When are two events mutually exclusive?

34 CHAPTER 2. PROBABILITY DISTRIBUTIONS

8. What is a probability distribution for a discrete chance variable? Whichproperties should it have?

9. What is a probability density histogram? Which properties does it have?

10. What is probability density?

11. What is a chance error?

12. What is a weighted average?

13. What is the expectation of a discrete chance variable?

14. What is the standard error of a discrete chance variable?

15. What does the Central Limit Theorem say?

2.13 Exercises

1. Conduct the experiment described in section 2.2 using an actual die (orwith http://www.random.org/dice/?num=1). Roll the die ten times. Aftereach roll, compute the relative frequency of aces up to that point. Completethe following table:

Table 2.1: Number of aces in rolls of a die

Repeat Ace (1) or not (0) Absolute Relativefrequency (*) frequency, % (*)

123456789

10(*) Absolute and relative frequency of aces in this and all previous repeats

Plot the number of tosses on the horizontal axis and the relative frequency onthe vertical axis.

2. Conduct the experiment described in section 2.2 using the R script roll-a-die.Ron the course home page (the script simulates 10 000 rolls of a die). How doesthe graph look like? Run the script again. Is the graph exactly the same? Howdoes it differ? In what respect is it similar? Run the script once more. Is therea pattern?

2.13. EXERCISES 35

3. You roll a die twice and add the outcomes. Find the probability to get a10. Show your work and explain.

4. You toss a coin twice and count the number of heads. Construct a prob-ability distribution table and a probability density histogram. What does thearea under a bar in the probability density histogram show? And the height ofa bar? Find the expectation, the chance errors, and the standard error. (Thiswas an exam question in Fall 2015.)

5. Consider the following chance experiment: roll a die and count the num-ber of dots. Formulate an appropriate chance model. What are the possibleoutcomes? What are the probabilities? Make a table and a bar chart of theprobability distribution (in the chart, put the probability density on the verticalaxis). Compute the expectation and the standard error.

6. Work parts (a) and (b) of Freedman et al. (2007, review exercise 2 p. 304).

36 CHAPTER 2. PROBABILITY DISTRIBUTIONS

Chapter 3

Sampling Distributions

A sample percentage is chance variable, with a probability distribution. Theprobability distribution of a sample percentage is called a sampling distri-bution (the probability distribution of a sample average is also a samplingdistribution). This chapter discusses the properties of sampling distributions.The next two chapters build on the properties of sampling distributions to esti-mate confidence intervals and test hypotheses for the percentage or the averageof a population.

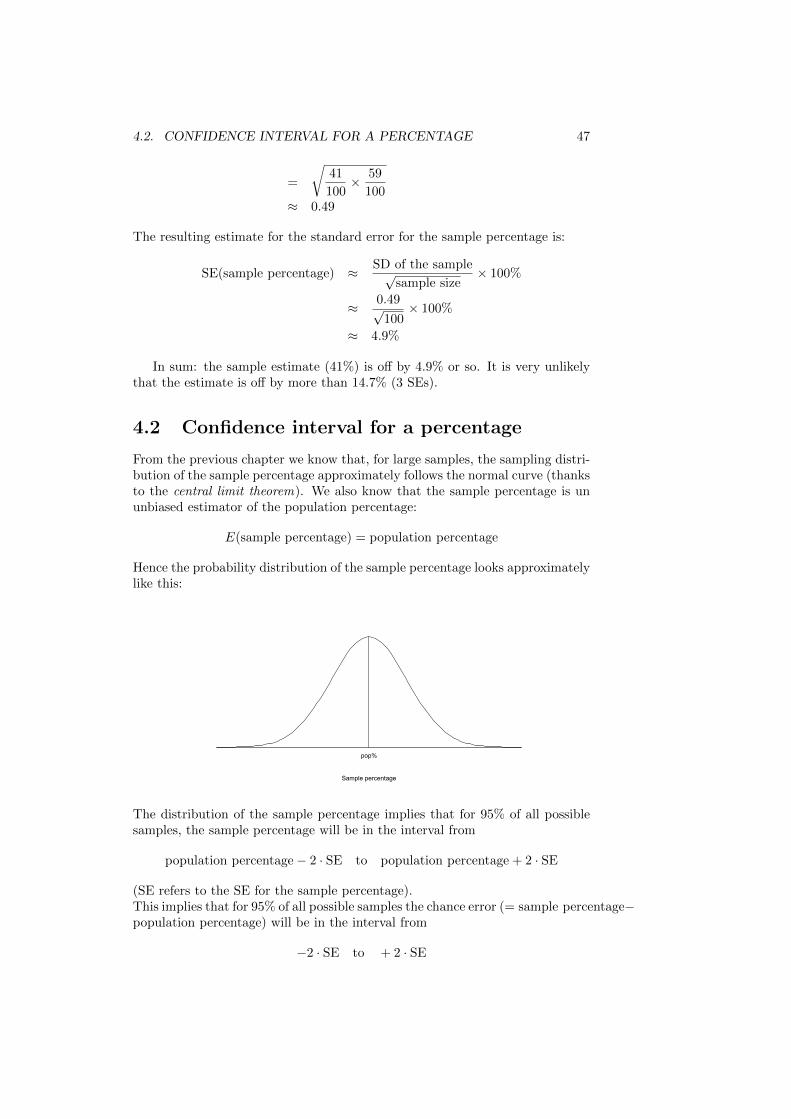

3.1 Sampling distribution of a sample percent-age

In a small town there are 10 000 households. 4 600 households (46% of the total)own a tablet. The population percentage (46%) is a parameter: a numericalcharacteristic of the population.

A market research firm doesn’t know the parameter. It tries to estimate theparameter by interviewing a random sample of 100 households. The researcherscounts the number of households in the sample and computes the sample per-centage:

sample percentage =number in the sample

size of sample× 100%

The sample percentage is a statistic: a numerical characteristic of a sample.We model the population as a box with 10 000 tickets. Every household that

owns a tablet is represented by a ticket 1 , and every household that doesn’t

own a tablet is represented by a ticket 0 :

5400 tickets 0 4600 tickets 1

Of course, the market research firm doesn’t know how many out of the 10 000tickets are tickets with a 1 (but we do). The random sample is like randomlywithout replacement drawing 100 tickets from the box. The researcher countsthe number of tickets with 1 (the number of households in the sample whoown a tablet). Suppose they draw

0 0 1 0 1 . . . 0

37

38 CHAPTER 3. SAMPLING DISTRIBUTIONS

The number of households in the sample who own a tablet is then equal to:

0 + 0 + 1 + 0 + 1 + . . . + 0

that is, the number in the sample is the sum of draws from the 0-1 box. As theresearcher computes the sample percentage:

sample percentage =number in the sample

size of sample× 100%

the numerator (the number of households in the sample who own a tablet) isthe sum of draws from the 0-1 box. Hence the sample percentage is computedfrom the sum of draws. Remember this.

Will the sample percentage be equal to the percentage in the population?We can find out by simulating the experiment described above in R. First wedefine the box with 4 600 tickets 0 and 5 400 tickets 0 :

population <- c(rep(1,4600),rep(0,5400))

This line of code generates a list (called “population”) of 10 000 numbers: 4 600

times 1 and 5 400 times 0 . You can check this by letting R display a tablesummarizing the contents of the list called “population”:

table(population)

Now take a random sample of 100 households from the population:sample(population,100,replace=FALSE)

You get a list of 100 numbers that looks something like this:0 1 1 0 1 1 1 0 ... 1 0 0 1

The researcher is interested in the number of households in the sample who owna tablet. That number is the sum of the draws:

sum(sample(population,100,replace=FALSE))

You get something like: 39

So this sample contained 39 households who own a tablet (and 61 who don’t). Ifyou divide the number in the sample (39) by the sample size (100) and multiplyby 100%, you get the sample percentage:

sample percentage =number in the sample

size of sample× 100% =

39

100× 100% = 39%

So the sample percentage (39%) is not equal to the percentage in the population(46%). That should be no surprise: the sample percentage is just an estimate ofthe population percentage, based on a random sample of 100 out of the 10 000tickets. The difference between the estimate (the sample percentage) and theparameter (the population percentage) is called the chance error:

chance error = sample percentage− population percentage

In this case the chance error is

chance error = 39%− 46% = −7%

(the minus sign indicates that the sample percentage underestimates the popu-lation percentage.

Of course, because the researcher doesn’t know the population percentage,she doesn’t know how big the chance error she made is; all she knows is thatshe made a chance error.

3.1. SAMPLING DISTRIBUTION OF A SAMPLE PERCENTAGE 39

Why is the estimation error called a chance error? That’s because the esti-mation error a chance variable. That can be easily seen by repeating the line

sum(sample(population,100,replace=FALSE))

a couple of times, and computing the sample percentage for every sample. You’llget something like: 39, 43, 46, 37, 43, 52, . . . : the sample percentage is a chancevariable. In a table:

sample percentage chance error (without the minus sign)39 −7 (7)43 −3 (3)46 0 (0)37 −9 (9)52 6 (6). . . . . . . . .

typical value: expectation standard error

So in repeated samples, the sample percentage is a chance variable. The samplepercentage has a probability distribution (called the sampling distributionof the sample percentage). The expectation of the sample percentage is thetypical value around which the sample percentage varies in repeated samples(take a look at the first column: do you have a hunch what the expectation of theof the sample percentage is?). The standard error of the sample percentage isthe typical size of the chance error (after you omitted the minus signs, as shownin the third column).

It can be shown that the expectation of the sample percentage is the popu-lation percentage (proof omitted):

E(sample percentage) = population percentage

The sample percentage is said to be an unbiased estimator of the populationpercentage. This also implies that

E(chance error) = 0

To find the SE for the sample percentage, start from

sample percentage =number in the sample

size of sample× 100%

which can be written as:

sample percentage =sum of draws

number of draws× 100%

Take the standard error of both sides:

SE(sample percentage) =SE(sum of draws)

number of draws× 100%

From the square root law (p. 29) we know that for random draws with replace-ment:

SE(sum of draws) =√

number of draws× (SD of the box)

40 CHAPTER 3. SAMPLING DISTRIBUTIONS

This is still approximately true for draws without replacement, provided thatthe population is much larger than the sample:

SE(sum of draws) ≈√

number of draws× (SD of the box)

So the expression for the SE for the sample percentage becomes:

SE(sample percentage) =

√number of draws× (SD of the box)

number of draws× 100%

or:

SE(sample percentage) ≈ SD of population√sample size

× 100%

You don’t have to memorize this formula. The formula is only approximatelyright because taking a sample is drawing without replacement. When the pop-ulation is much bigger than the sample, the distinction between drawing withand without replacement becomes small (Freedman et al., 2007, pp. 367-370).In that case, the formula gives a good approximation.

To find the SD of the population, use the shortcut rule for 0-1 lists:

SD of population =

√(fraction of

ones

)×(

fraction ofzeroes

)=

√4600

10000× 5400

10000≈ 0.50

(Of course, the researcher doesn’t know the fraction of ones in the population(the fraction of households in the population who own a tablet). If the sampleis large, she can estimate the SD of the population by the SD of the sample.This technique is called the bootstrap. We’ll get back to this when we discussinference.)

Now we can find the standard error of the sample percentage:

SE(sample percentage) ≈ SD of population√sample size

× 100% ≈ 0.50

100× 100% ≈ 5%

In sum: if many researchers would each take a random sample of 100 householdsand compute the sample percentage, the sample percentage will be about 46%(the expectation), give or take 5% (the standard error).

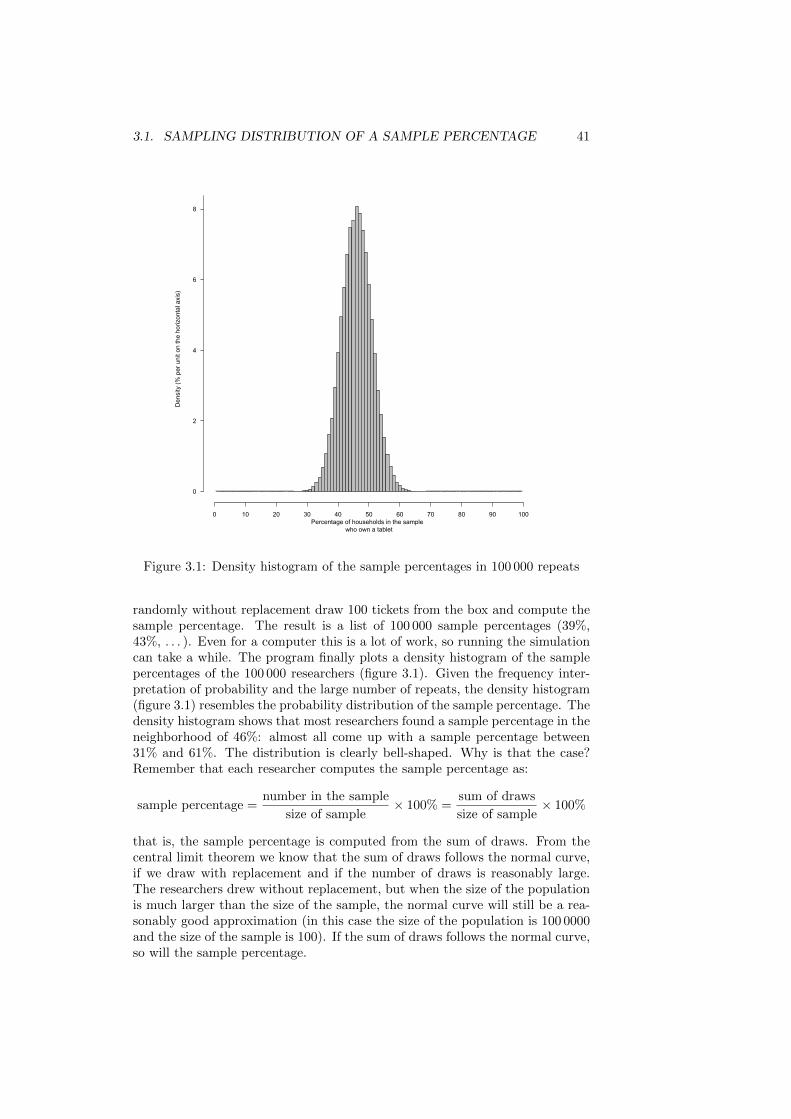

What is the shape of the sampling distribution? A computer simulationis helpful (see the R script 100000-repeats.R). Let us start from the box:

5400 tickets 0 4600 tickets 1

and let a researcher (who doesn’t know the contents of the box) randomly with-out replacement draw 100 tickets from the box. The researcher uses the sampleto compute the sample percentage (the percentage of 1s in the sample). Wewrite down the result (say, 39%) and toss the tickets back in the box. Thenwe let another researcher randomly without replacement draw 100 tickets fromthe box and compute the sample percentage, and so on. The computer simula-tion repeats this chance experiment 100 000 times, so 100 000 researchers each

3.1. SAMPLING DISTRIBUTION OF A SAMPLE PERCENTAGE 41

Percentage of households in the sample who own a tablet

Den

sity

(% p

er u

nit o

n th

e ho

rizon

tal a

xis)

0 10 20 30 40 50 60 70 80 90 100

0

2

4

6

8

Figure 3.1: Density histogram of the sample percentages in 100 000 repeats