Embed Size (px)

Citation preview

Special Report | October 2014 1

Special Report

AMIR KHAN ECONOMIC RESEARCH OFFICE | LONDONT: +44-(0)207-577-2180 E: [email protected]

The Bank of Tokyo-Mitsubishi UFJ, Ltd.

Have Oil Prices Become Immune to Rising Geopolitical

ensions?

T

A member of MUFG, a global financial group CTOBER 2014 O

ast experience, such as the oil price shocks of the 1970s, suggests that periods of rising geopolitical tensions over a concerted period are accompanied by rising oil and other energy prices, an outcome – which if left unchecked – has the potential to adversely

affect the global economy. More recently, however, despite rising geopolitical tensions associated with the Ukraine conflict, as well as the rise of ISIS in the MENA region, oil prices have shown little or no upward movement in response to these events. In fact, oil prices have exhibited a downward bias recently (see below), suggesting that other factors may well be at play. With this in mind, we will use this note to explore what these factors are and whether geopolitical influences have indeed lost their relevance in influencing oil and for that matter other energy prices.

PP

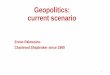

Geopolitical tensions fail to spook the energy markets… Oil prices have remained largely immune to politically generated turmoil this year. Yet, by any measure, 2014 has been an extraordinary year in geopolitics. Perhaps the most dramatic has been the seemingly sudden emergence of ISIS from Syria to Iraq, where it now controls a significant swathe of territory. Also of great significance in geopolitical terms has been the escalation of the Russia/Ukraine conflict, which has prompted four rounds of trade sanctions against the former and sparked new NATO efforts to reassure Ukraine’s nervous neighbours in the former Warsaw Pact countries. But despite the significance of these events, the oil, and other markets more generally, have largely managed to take such stresses in their stride, suggesting that they have increasingly become micro-focused in their assessment of geopolitical risks, seemingly unconcerned with the rise of ISIS as long as it does not openly destroy oil refineries and in the case of the Russia/Ukraine conflict as long as the crisis remains confined to Eastern parts of Ukraine. We will endeavour to elaborate on some of the factors which have been responsible for the markets benign reaction to these events so far, but before doing so will, by way of background, examine how oil prices have behaved over the recent past. Since peaking at around US$115/b in mid-June, as markets reacted to the advance of ISIS in Iraq, benchmark oil prices have fallen back rather sharply, with the key benchmark, Brent Crude, currently oscillating around US$85/b (see Chart 1), a fall of over 25%. While the average price for Brent in the year to date, at just over US$106/b, remains only slightly shy of the previous year’s figure, the recent slump in prices during the peak summer months has been a surprise, especially given the rise of geopolitical tensions not just in the Middle East but

Special Report | October 2014 2

also between Russia and Ukraine. In our mind, a number of factors appear to be at play, including slowing GDP growth in the major (Eurozone and Japan) as well as emerging economies (particularly among the so-called BRIC nations); a lowering of global demand projections by the IEA; higher than expected production growth among non-OPEC countries, namely the US; and an apparent discounting of geopolitical risks as efforts are made to shore up Iraq, including the peaceful replacement of Iraqi Prime Minister Maliki and US airstrikes against ISIS. Recent developments in Ukraine also offer some hopes of an improvement in light of the recent ceasefire agreement between Kiev and rebel groups allied to Russia. With physical markets apparently well supplied, there is little prospect of Saudi production being increased in an uncontrolled fashion, helping to keep global spare capacity at a more comfortable level and thus easing market concerns.

Chart1: Oil prices have continued to edge down despite rising geopolitical tensions

60

70

80

90

100

110

120

130

Jan

-10

Jul-1

0

Jan

-11

Jul-1

1

Jan

-12

Jul-1

2

Jan

-13

Jul-1

3

Jan

-14

Jul-1

4

(US$/b)

Opec oil price target

US$115/b

~US$85/b200-day moving average/trendline

Brent Crude price

Source: Macrobond, BTMU

Against the above backdrop, it is worth asking whether the recent pricing action in the oil markets may already have gone too far? While this is difficult to answer, the obvious point to highlight is that at current levels, prices are well below the OPEC’s stated target of around US$100/b and not to mention the 200-day moving average which market participants see as being an important technical indicator of future pricing trends. As such, all eyes are currently on OPEC ahead of the cartel’s next scheduled meeting on 27 November awaiting a response to the steep price decline. For Saudi Arabia, the biggest producer within OPEC, and indeed most other member states of this organisation, oil prices have dropped under the level required to balance their public finances this year (see chart 2). Hence, it would be logical to expect OPEC to lower its output target from the present 30m b/d. That said, the fact that Saudi Arabia – faced with sharply falling prices – has not shown any greater urgency to undertake such cutbacks any sooner in our minds suggests that the country has been eager to win market share at the expense of some of its rival oil producers. Indeed, this appears to be corroborated by the Saudi decision recently to grant price cuts to its key Asian customers, such as China, which are known to have better demand prospects over the medium to long-term time horizon. But in doing this, the Saudis have reinforced a sense of disunity within OPEC with two other

Special Report | October 2014 3

members of OPEC – Iran and Iraq – following the former country’s lead to offer price reductions to their Asian customers, thereby making the prospects of reaching an agreement for production cuts more difficult. This, in turn, raises the likelihood that OPEC production could remain at current levels, especially within the context of an already oversupplied market (see below). In fact, if this proves to be case we cannot rule out a further slide in Brent prices towards US$80/b.

Chart 2: The prevailing oil price has moved below the fiscal breakeven oil price for the majority of OPEC memeber states

0

20

40

60

80

100

120

140

Alg

eria

Ang

ola

Ecu

ador

Iran

Iraq

Kuw

ait

libya

Nig

eria

Qata

r

Saud

iA

rabi

a

Uae

Ven

ezu

ela

(US$/b)

Prevailing price of benchmark oil = ~US$85/b

NB: Readings are based on the average estimates of a survey of nine oil consultancies, banks and independent

analysts. Source: Reuters, BTMU Separately, it is also worth noting here that Saudi Arabia may actually be in favour of the recent fall in oil prices, as this may serve to disincentivise the further development of certain shale oil and gas deposits, whose breakeven cost of production is higher than for conventional oil and gas. That said, according to estimates from Wood Mckenzie, an oil consultancy, benchmark oil prices would have to fall somewhat further (i.e. towards US$75/b) for this point to be reached. …As fundamentals in the oil market remain weak…. The recent easing of oil prices is not surprising from a fundamental perspective, but the speed and magnitude of the falls has been somewhat unexpected. For quite a while now markets have been expecting non-OPEC supply gains to outstrip demand growth leading to a decline in the call on OPEC supply. The recent revisions from IEA confirm this underlying view, as projected growth in global demand has been cut to around 0.7m b/d this year, while non-OPEC supply is projected to rise to the tune of 1.7m b/d (see Chart 3). However, supply disruptions in Libya and Iraq, and continuing sanctions on Iran, have raised concerns over OPEC’s ability to meet even a reduced call on its crude without recourse to Saudi production, which would then lead to a fall in global spare capacity. As a result, prices have remained supported to some extents this year – failing to reach the low point of under US$50/b seen in the wake of global

Special Report | October 2014 4

financial crisis – despite the underlying market weakness. However, this support now appears to be fading as physical markets remain well supplied even in the face new geopolitical risks from ISIS and the ongoing conflict in Ukraine, helping to temper market concerns over OPEC disruptions.

Chart 3: The change in global oil demand this year is likely to continue to be outpaced by non-OPEC supply, resulting in an oversupplied market

0

400

800

1200

1600

2000

2012 2013 2014

Global Demand Non-Opec Supply

(Annual change, '000 b/d)

Source: IEA, BTMU

The main driver of global supply remains the US, where the development of shale oil is raising crude production by around 1m b/d every year. As a result, its demand for crude oil imports has fallen sharply while its exports of petroleum products have risen. Reflecting this, large volumes of imports from West Africa, the Middle East and Latin America are being progressively diverted elsewhere, much of it to Europe. Meanwhile, crude oil exports, except to Canada, remain banned. But easing interpretations of what constitutes “oil product” are likely to see more and more US production entering global markets which are already struggling to absorb new supply from expanded refinery capacity in the Middle East and China. …And this has not been helped by the rise in value of the US dollar & other market-specific factors either Aside from the changing demand/supply picture that we touched on above, market specific factors have also added to the bearish tendency for oil price recently. Central to such developments include the following: Rising value of the US dollar. With the US currency – in which most commodities are

denominated – on the rise recently as the markets factor in the prospect of an eventual normalisation in US monetary policy (see Chart 4), so oil and other commodity prices have come under increasing pressure, a trend which we expect to persist for some time yet as the world’s major central banks start to embark on divergent paths, something that is likely

Special Report | October 2014 5

to be supportive of the US dollar, given that economic conditions in the US are more conducive to normalization of policy than is the case in the Eurozone and Japan.

Chart 4: The US dollar & oil prices exhibit a negative relationship

70

75

80

85

90

Jan-

10

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Feb

-11

May

-11

Aug

-11

Nov

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Nov

-13

Feb

-14

May

-14

Aug

-14

50

60

70

80

90

100

110

120

130

Brent crude (US$/b), RHS Dollar Index, LHS

Source: Macrobond, BTMU

With the oil price breaching a number of key technical support levels over the past month or so, including the decisive US$100/b mark and more recently the US$90/b mark, this build-up of negative momentum appears to have encouraged investors to place further bets on the oil price remaining weak.

With a number of banks exiting the physical commodity trading business, including oil, due

to regulatory pressure and the need to preserve capital, there has been a lesser tendency to buy commodities “on the dips”, something which may have prevented oil prices from finding “a floor” as quickly as one would have expected in the past.

But the long-term supply outlook remains uncertain due to ongoing geopolitical headwinds Notwithstanding the recent fall in oil prices – which is likely to entail some redistribution of income from oil producers to consumers, thereby helping to support the global economy somewhat – the outlook beyond the near-term does not seem as rosy thanks to ongoing geopolitical uncertainties. Even if the current hostilities in Ukraine subside, recent geopolitical developments still imply long-term instability in countries like Libya, Iraq, Syria and Sudan, all of which face risk of fragmentation and poor security conditions. At the very least this will hamper their efforts to maintain and develop oil resources. This is a particular issue in Iraq which was supposed to provide over 15% of incremental gains in global oil supply through 2019, according to IEA projections. Adverse political and security developments in Venezuela and Nigeria also call into question future production levels. These concerns over the future

Special Report | October 2014 6

supply of oil are being reflected in the fact the back end of the oil price curve has not fallen in line with the front end (see Chart 5) – a phenomenon known as “contango”, something which we expect to persist through the remainder of this year and perhaps into next. Seen from thperspective, it appears that geopolitical fa

is ctors will likely still be relevant in determining oil

rices, especially beyond the near-term. p

Chart 6: The recent shift in the futures oil price curve suggests that the market now thinks that supply constraints will support oil prices going

forward

80

85

90

95

100

105

110

Oct

ober

, 201

4

Janu

ary,

201

5

Ap

ril, 2

015

July

, 201

5

Oct

ober

, 201

5

Janu

ary,

201

6

Ap

ril, 2

016

July

, 201

6

Oct

ober

, 201

6

J O Janu

ary,

201

7

Ap

ril, 2

017

July

, 201

7

ctob

er, 2

017

anu

ary,

201

8

Ap

ril, 2

018

July

, 201

8

Oct

ober

, 201

8

Janu

ary,

201

9

Ap

ril, 2

019

July

, 201

9

Oct

ober

, 201

9

Janu

ary,

202

0

Jan.-14

Oct-14

(US$/b)

Source: Macrobond, BTMU

oncluding remarks

d,

ey oil

ctors

ay well return to spook the oil market in the manner that we are traditionally used to.

C Despite the deteriorating geopolitical environment this year, this has not fed through to rising crude oil prices. Central to this has been the weakening of market fundamentals for oil, withsupply growth overwhelming the sluggish growth in demand. While we expect this trend to persist in the near-term, the long-term picture is somewhat more complex. Indeed, in our minthe MENA region is likely to remain a hot-bed for geopolitical uncertainty going forward and there is a real prospect that this could meaningfully affect oil supplies in an adverse manner going forward from countries, such as Iraq. This, coupled with the likely outages in other kproducing nations, such Nigeria and Venezuela that are also no strangers to geopolitical uncertainty, could see prices experience a sharp rebound from their current lows. With this mind, it is reasonable to conclude that, while today’s geopolitical uncertainties are currently being downplayed by the markets, this should not be treated as a normal state of affairs, giventhat under a less benign supply scenario for crude oil going forward, such geopolitical fam

Special Report | October 2014 7

The Bank of Tokyo-Mitsubishi UFJ, Ltd. (“BTMU”) is a limited liability stock company incorporated in Japan and registered in the Tokyo Legal Affairs Bureau (company no. 0100-01-008846). BTMU’s head office is at 7-1 Marunouchi 2-Chome, Chiyoda-Ku, Tokyo 100-8388, Japan. BTMU’s London branch is registered as a UK establishment in the UK register of companies (registered no. BR002013). BTMU is authorised and regulated by the Japanese Financial Services Agency. BTMU’s London branch is authorised by the Prudential Regulation Authority (FCA/PRA no. 139189) and subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of BTMU London branch’s regulation by the Prudential Regulation Authority are available from us on request.

This report shall not be construed as solicitation to take any action such as purchasing/selling/investing in financial market products. In taking any action, each reader is requested to act on the basis of his or her own judgment. This report is based on information believed to be reliable, but we do not guarantee, and do not accept any liability whatsoever for, its accuracy and we accept no liability whatsoever for any loss or damage of any kind arising out of the use of all or any part of this report. The contents of the report may be revised without advance notice. Also, this report is a literary work protected by copyright. No part of this report may be reproduced in any form without express statement of its source.

The Bank of Tokyo-Mitsubishi UFJ, Ltd. retains copyright to this report and no part of this report may be reproduced or re-distributed without the written permission of The Bank of Tokyo-Mitsubishi UFJ, Ltd. The Bank of Tokyo-Mitsubishi UFJ, Ltd. expressly prohibits the re-distribution of this report to Retail Customers, via the internet or otherwise and The Bank of Tokyo-Mitsubishi UFJ, Ltd., its subsidiaries or affiliates accept no liability whatsoever to any third parties resulting from such re-distribution.