Embed Size (px)

Citation preview

Welcome

1NYSE: G

Program Schedule

Genpact Investor DayMarch 17, 2009

Time Session Speaker / Lead

08:30 - 09:30 am Breakfast & Registration All Attendees

09:30 - 09:40 am Welcome & Introductions Anil Nayar

09:40 - 10:40 am 2008 Update, Strategy & Way Forward Pramod Bhasin

10:40 - 11:15 am Business Pipeline & Customer Growth NV 'Tiger' Tyagarajan

11:15 - 11:25 am Break All Attendees

11:25 - 11:55 pm Financial Overview Vivek Gour

11:55 - 12:00 pm Closing Remarks Pramod Bhasin

2

12:00 - 01:00 pm Question & Answers All Attendees

Disclaimer

These materials contain certain statements concerning our future growth prospects and forward-looking statements, as defined in the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. These statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those in such forward-looking statements. These risks and uncertainties include but are not limited to a slowdown in the economies and sectors in which our clients operate, a slowdown in the BPO and IT Services sectors, the risks and uncertainties arising from our past and future acquisitions, our ability to manage growth, factors which may impact our cost advantage, wage increases, our ability to attract and retain skilled professionals, risks and uncertainties regarding fluctuations in our earnings, general economic conditions affecting our industry as well as other risks detailed in our reports filed with the U.S. Securities and Exchange Commission, including the Company's Annual Report on Form 10-K. These filings are available at www.sec.gov. Genpact may from time to time make additional g g p ywritten and oral forward-looking statements, including statements contained in our filings with the Securities and Exchange Commission and our reports to shareholders. Although the Company believes that these forward-looking statements are based on reasonable assumptions, you are cautioned not to pay undue reliance on these forward-looking statements which reflect management's current analysis ofpay undue reliance on these forward looking statements, which reflect management s current analysis of future events. The Company does not undertake to update any forward-looking statements that may be made from time to time by or on behalf of the Company. In addition, you should be advised that our past performance is not necessarily indicative of future performance, particularly given the current global economic environment

3

economic environment.

2008 Business Update,Strategy & Way ForwardStrategy & Way Forward

Pramod BhasinPresident & CEOPresident & CEO

March 17 2009

4NYSE: G

March 17, 2009

Agenda

Genpact Overview

The Current Environment & Strategies for GrowthThe Current Environment & Strategies for Growth

The Year Ahead

5

Overview

6

Who Are We?

Leaders in Business Process Management solutions and the globalization of these services

Unique End-to-End (E2E) approach: measuring performance metrics (process efficiency) and business outcome (process effectiveness) differentiates us in the market, which typically measures only efficiency

Our deep process excellence, analytical capabilities, technology competence and breadth and depth of services combined with operational and business insights, results in business and strategic value to our clients

7Operational Innovation with Business Process Management

Why Genpact Even in This Environment?Market opport nit remains h ge despite en ironmentMarket opportunity remains huge despite environment

Global business process market, significantly under-penetrated, Est. 6-8% growth vs. flat ITOProven business model – start small and expand with clients

Expanding diversified blue-chip client relationships, and enhancing products and services, support p g p p , g p , ppcontinued growth (85% from existing clients); growth in GE revenues even after 10 years

Breadth and depth of services across verticals and marketsIndustry led solutions around BFSI and manufacturing coupled with domain expertise in F&A, Procurement Analytics and Technology Enablers supports client value creationProcurement, Analytics and Technology Enablers supports client value creationSwiftly allocating resources to new growth areas and to domestic markets of India & China

Proven track record of performance and growth: 30% revenue CAGR over 3 years Driven by Global Client (GC) growth: $551MM in ‘08 GC revenues, more than 13X $42MM in ’05Long-term margin improvement

Strong balance sheet and cash flows, including approximately $385MM of liquidityCash from operations – improved to 20% of revenue compared to 18% in ‘07

Strong pipeline – new prospects driven by new economic realitiesStrong pipeline – new prospects driven by new economic realitiesE2E: a differentiated way to deliver business outcomes for clients

Previous investments in Re-Engineering, Six Sigma, Lean, Process Management & IT drive non-capital intensive operating innovation

8

E2E capabilities, along with IT, process & analytics, and focus on effectiveness not just efficiency

Perfectly Positioned for this Environment

Top-Tier Financial Performance in 200880% f di ti / iRevenue Mix 80% of revenue non-discretionary / recurring; critical for sustainability of client’s operations

Long-term client contracts551

GEGCa

Revenue Mix

CAGR30%1041

823613

‘06-’08

Top 15 GC average remaining term 3-5 years

Strong organic growth of 26% in ’08 despite economic headwinds

481

342

490

551613 86%

4%

203

453

160

61%

2%

114%

6% economic headwinds

Diversified Client Growth

29 clients over $5MM vs. 18 prior year

07 0806

Adjusted Operating Incomeb

($MM) CAGR20 clients grew relationship by over 70%

Organic Growth

Global Client growth 62% over 2007134

178

( ) CAGR36%

134 80bp

97g

GE growth of 7% (adj. for dispositions of GE businesses we continue to serve) demonstrates ability to penetrate business over the long-term

07 0806

17.1%16.3%

97

15.8%

50bp

9Consistent Tier I Performance

a) Global client revenue including GE divested businesses and acquisitions (GAAP)

b) Adjusted Operating Income = Income from Operations + Formation Accounting Amortization + Stock Options Charge + Indian Fringe benefit tax on Stock Option

Governance is a Way of Life

Controllership

Strong GE heritage

Monthly operating reviews with

Independent Audit CommitteeExternal Audits: SAS 70 technology environment audits... SOX certification

Compliance

Business level risk assessment

Framework to comply with cross

CEO / CFO / Business leaders

Quarterly representation letters

from all business units

Stringent financial close

Internal Audits: leveraged GE CAS framework... 20 member strong team with real operating experience...

Client Audits: 100’s of client

border requirements

Strong ombudsperson process

Strong 11 Member Independent Board – Global Experience

Stringent financial close

process... segregation of duties,

checks and balances

operational audits

Strong 11 Member Independent Board Global Experience

Rajat Gupta Chairman of Board, Genpact;Former Managing Partner, McKinsey

J Taylor Crandall

Jagdish KhattarFormer CEO, Maruti Udyog, India

Denis J NaydenManaging Partner Oak Hill Capital

John Barter Chairman of Audit Committee; Former President & CFO, Allied Signal

Michael SpenceJ Taylor CrandallManaging Partner, Oak Hill Capital

Steven Denning,Chairman, General Atlantic

Robert Scott

Managing Partner, Oak Hill Capital

Mark DzialgaManaging Partner, General Atlantic

Jim MaddenFormer CEO Exult

Michael SpenceNobel Laureate, Stanford University

Pramod BhasinPresident & CEO, Genpact

10Compliance and Integrity – Non-negotiable

Former COO, Morgan StanleyFormer CEO, Exult

The Current Environment

11

The World has Changed

Li idit i i M k t ll I t fid h tt d B k tLiquidity crisis… Market collapse… Investor confidence shattered… Bankruptcy

Impact on our clients:

Nissan: Auto sales plunge 41% in Feb 2009 20 000 job cuts; first annual loss in nine yearsNissan: Auto sales plunge 41% in Feb 2009, 20,000 job cuts; first annual loss in nine years

Wachovia: Announced $33B loss, plans 12,000 job cuts; S&P downgrades its debentures

GE: Lost $254B in market capitalization; cut dividend in the 4Q’08

Changing Client Needs Impact on Genpact

Focus from growth & expansion to reduction in cost

Preserve cash & improve working capital mgt.

Improve productivity

Slowness of decision-making

Budget cut-backs in IT spend

Shorter pay-back period – razor-sharp solutions

M ti CAPEX & b tt ROIDeflation focused sourcing & spend requirement

Minimize capital investment

More scrutiny on CAPEX & better ROI

Client business volumes down

Demand for operational innovation

P i i

12

Pricing pressures

Factored These Risks in our Growth Plans

With Change Comes Opportunities

Environment Creates Opportunity for Growth

Focus on cash preservation & cost reduction

How We Are Reacting

Our E2E solutions are non-capital intensiveleading clients to look aggressively at new ideas

New Growth Markets:

China… India

Our E2E solutions are non capital intensive

Scale existing cash / cost solutions

Re-allocate dedicated leadership resources Middle East ... Japan

Growth Opportunities:

Healthcare … Pharma

and swat teams to growth areas

Speed of deployment for 90 day pay-back

Id l ti t i l b l t l tCollections… “Cash Is King”

“Cost out”

Risk Management

P / S l Ch i

Ideal time to acquire global talent

Outcome-based / gain share pay-back model

Operating InnovationProcurement / Supply Chain

Strong Pipeline:

New categories of prospect, driven by economic realities

p g

13

driven by economic realities

Driving Sustainable and Superior Organic Growth

Recession Creates Opportunity to Scale Existing Solutions

Reduce Warranty Costs(COST)

$23MM Excess warranty payouts.. High servicing cost

Multiple legacy systemsManual Intervention

Developed integrated web enabled claims processing tools

30% processing timeWorking Capital

Applicable to all manufacturing companies

Incomplete reporting 35% in disallowed claimsCapital

Improve fraud

24%Detection of fraudulent non-compliant claims taking too long & getting paid out early

Complete process re-designReporting dashboardP i t 25%

Applicable to all insurance companiesdetection

(RISK)

long & getting paid out earlyMultiple hand-offsAbsence of report generation process

Processing steps 25%Processing time 50%Fraudulent

Claims

companies

14E2E Solutions Address Client Needs… Scalable for Growth

I2I and C2C Markets Continue to GrowChiI di ChinaIndia

EnvironmentDomestic BPO Market: $1.3B

Expected BPO growth @ 40% in 2009

Domestic BPO Market: $1.4B

Expected BPO growth @ 26% in 2009

Cost arbitrage not a prime driver

Achieve global standards to compete globally

Expected BPO growth @ 40% in 2009 Expected BPO growth @ 26% in 2009

Lack of process expertise in operations

Build domestic capability; offer E2E solutions

Lack of six sigma, lean and re-engineering skills

Insights

Products: Collection, Customer Service, Procurement, Analytics

Industries: Insurance, Manufacturing, Healthcare Banking Airlines

Products: F&A, Analytics, Re-Engineering, Customer Service

Industries: Banking, Telecom

ActionsHealthcare, Banking, Airlines

Govt. organizations looking for process optimization… efficiency enhancement

Hosted platform / asset takeover

Banking operation to mid-small banks

Potential JVs with local partners

15Domestic Markets – Huge Growth Opportunities – Strong Pipeline

End-to-End: Game Changing Differentiator

What is it?Looking at the complete operational process from start to finish; driving business outcome through overall process effectiveness, rather than discrete transactional efficiency

Most companies do not ha e meas rement metrics for E2EMost companies do not have measurement metrics for E2E

Most service providers only measure process efficiency, providing marginal benefit

Why is it important to clients today?Supports companies drive for step improvement in overall process performance“Capital-light” solution designProvides many times the benefit efficiency metrics can deliver

Why are we best positioned?Leaders in operational innovation… in our DNA due to our process view

Encompasses all attributes of E2E

Worked on over 2000 different kinds of processes – all with data, learnings... Our IP

Benchmark key process metrics

Detailed roadmap for clients to realize value

16Hard to Replicate & Even Harder to Compete Against

Operational rigor to ensure performance… it is not a project

Key Business Outcome Improvement Drivers

End-to-End Process Efficiency Effectiveness

O i i ti↓ Time to key in an invoice Conversion rates on applications… Volumes

Originations ↓ Cost per loan application ↓ Cycle time to open a new customer account

Bill to Cash Collection efficiency % (Cashcollected / Total AR)P t d %

Eliminate billing leakage

↓ Days Sales Outstanding ↓ Past due %

Account Payable

Invoices actioned on time

↓Total AP cycle time

Paid on Time %

↓ Vendor queries

Vendor discountsVendor discounts

Insights – Technology only solves part of the problem:E.g., only 40% of transactions in the Accounts Payable process are “first pass, straight through”E.g., only 40% of transactions in the Accounts Payable process are first pass, straight through

Typically only 5-10% of the end-to-end cycle time of a process is “value-added time”

The E2E approach also leads to higher employee engagement

Will facilitate the move from FTE-based pricing to outcome-based pricing models

17

p g p g

E2E View Enables Critical Business OutcomesAccounts Payable – End-to-End View – Comparison of traditional vs business impact approach

Sourcing Procurement Payment

Accounts Payable End-to-End View Comparison of traditional vs. business impact approach

Spend Analysis

Category Strategy

Planning & PO Issue

Material Receipt

Accounts Payable

Negotiation & Contract

Effectiveness - Key Performance Measures

End-to-End Cycle Time

Invoices/Person/Year

3919

4500011000

5400

25

Efficiency - Key Business Outcomes

Cash Flow Optimization

C t T ti$3

$9Invoices/Person/Year

Vendor Terms

450005400

75030

Cost per Transaction $9$1.3

80%10%Early PaymentDiscount Capture

Highlights

Difference between best and worst is not incremental, but multiple times

Measuring just efficiency misses the opportunity

Focusing on key objectives of a process (as opposed to transactional metrics) will deliver business outcomes

T h l i t th l ti t l i ti

g g

Outcome

Technology is not the solution to solve process variation

For a typical US $5B revenue company – reduce annual purchase spend by $50 – 150MM, increase margins by 100

Focusing on AP will give you 10-15% productivity on FTE offshored... minimal impact

18

p p y $ , g y– 300 bps.

p

Minimum

Genpact Best-in-ClassMedian

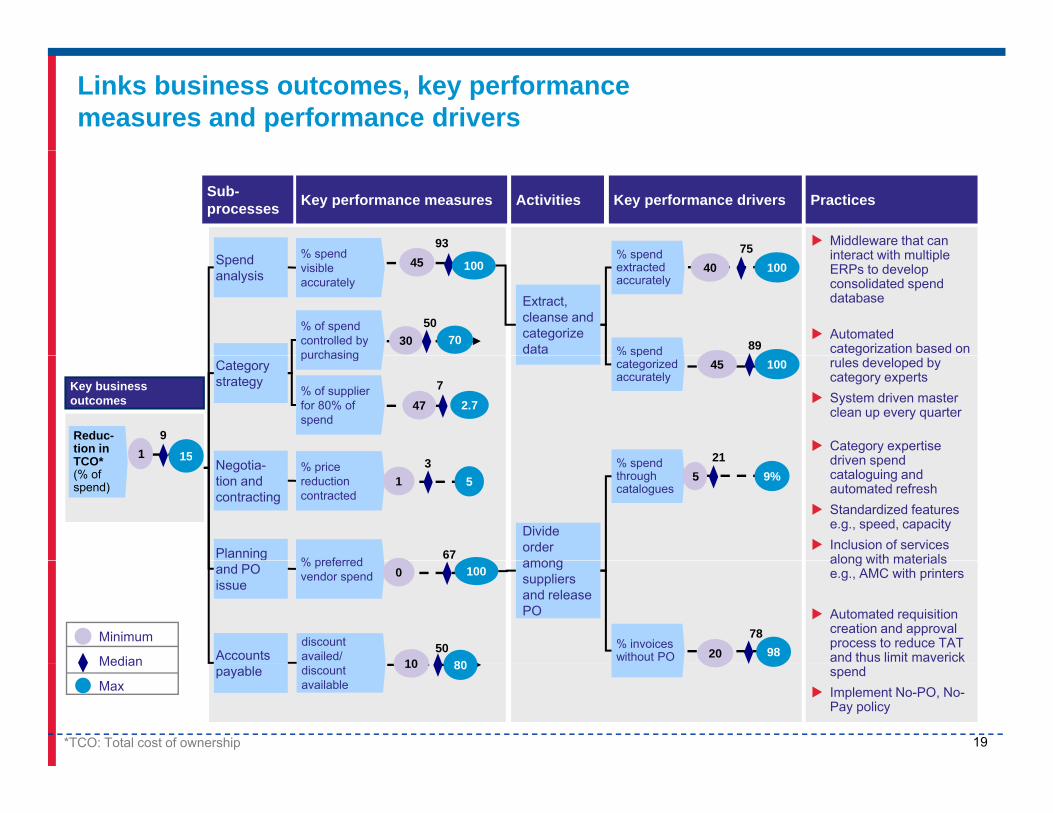

Links business outcomes, key performance measures and performance drivers

Key performance drivers

% spend93

Key performance measuresSub-processes Activities

% spend 75

Practices

Middleware that can interact with multiple% spend

visible accurately

45 100

% of spend controlled by purchasing

30 7050

Spend analysis

% spend extracted accurately

10040

Extract, cleanse and categorize data 89% spend

interact with multiple ERPs to develop consolidated spend database

Automated categorization based on

Key business outcomes

Reduc-tion in TCO* 1 15

9

purchasing

% of supplier for 80% of spend

21

47 2.77

Category strategy

10045p

categorized accurately

grules developed by category expertsSystem driven master clean up every quarter

Category expertise driven spendTCO*

(% of spend)

15

% preferred 67

% spend through catalogues

9%521

Planning

Divide order among

% price reduction contracted

1 53Negotia-

tion and contracting

driven spend cataloguing and automated refreshStandardized features e.g., speed, capacityInclusion of services along with materials% preferred

vendor spend 0 100

discount availed/

% invoices without PO 20 98

78

801050

and PO issue

Accounts

among suppliers and release PO

along with materials e.g., AMC with printers

Automated requisition creation and approval process to reduce TAT and thus limit maverick

Minimum

Median

19

discount available

8010payable spendImplement No-PO, No-Pay policy

Max

Median

*TCO: Total cost of ownership

Proven Experience of Effectively Managing Cost Base

Various levers to drive productivity year over year

SalaryAnnual increases held to 7-8% vs. 10-12% for industryEntry-level wages held flat for 4 years

InfrastructureSEZs locked in rental rates below market by ~50%Tier 2 city costs 25% lower… Tier 3 cities further savingsRenegotiating 15-20% supplier rates to hold price escalation

Telecom Improved utilization by 5-7% from scale and sourcing rate re-negotiation…. Lowest in industry

Improve supervisory spans as client scaleScalability

Return

Improve supervisory spans as client scaleClient profitability increases as accounts mature

Wage inflation and FX sharing built into contractsGain-sharing Paid for impact deliveredGain-sharing – Paid for impact delivered

New InitiativesWork From Home – Targeted 3000 people, reduces cost per person by ~7-8%NIIT JV to improve training effectiveness and reduce costs by ~30%

20Relentless Focus to Drive Internal Efficiencies

Experienced, Global Leadership Executive Yrs of Exp Title

Management TeamManagement TeamExperienced operating leadership… average 20 years of experience

L i i ki h

Pramod Bhasin 27 President & CEO

V.N. (Tiger) Tyagarajan 23 COO

Vivek Gour 23 CFOLongevity in working together ~ average 10 years of experience

Local leader in global locations

Adding key talent where

Robert Pryor 25 EVP, Head of Sales

Mitsuru Maekawa 34 CEO Asia

Patrick Cogny 18 CEO Europe g yrequired

Sales Leader – Robert Pryor

Marketing Leader – Lynda Smith

Patrick Cogny 18 CEO Europe

Walter Yosafat 28 CIO & CEO Americas

Mohit Bhatia 21 Business Leader F&A

World-class HR practices to acquire, develop and retain talent

Mohit Thukral 20 Business Leader BFSI, Wachovia

Rakesh Chopra 31 Business Leader

Anju Talwar 25 Business Leader

Tajinder Vohra 20 Business Leader

Victor Guaglianone 25 General Counsel

21

Longevity of Leadership Team Allows to Build Relationship and Drive Operating Excellence

Piyush Mehta 19 Human Resources

The Year Ahead

22

Key Challenges and How We Will Address Themf %

ClientGrowth

Bulk of our services are non-discretionary and 80-85% recurring

New growth markets and new service areas… I2I / Risk Management / Healthcare

IT more discretionary – will face similar challenges as peer group

C ti t d it i t

Margin

Continues to grow despite environment

Geographic and segment diversification; over 2,700 statements-of-work reduces risk

Multiple levers: manage wage inflation, discretionary spend; utilization of infrastructure P t k d i i fit bl ith i ti li t

GE

Margin Compression

Client

Proven track record in growing profitably with existing clientsContinue relentless focus on cost discipline and improved productivity

Quality of clients establishes roadmap for growth; 29 clients over $5MM… 20 clients Client

Concentrationgrew over 70% in 2008

Low levels of penetration achieved to date

New category of prospects entering pipeline, driven by new economic realitiesPipeline Slower conversion… pricing pressures

Many more entry points

Non-Capital Intensive

E2E led solutions focused on cost/cash improvement

Depth and breadth of industry solutions and process expertise

23Strong Financial Discipline and Hands-on Management

Intensive Solutions

Depth and breadth of industry solutions and process expertise

Quick pay-back

The Year Ahead

Responding to the dramatic change around us from a position of strength.

We can be part of the solution: validation from a strong pipeline with new prospects…demand for our services has never been higher.p p g

Our business model of expanding diversified blue-chip client relationships, and enhancing our products and services, supports continued growth.continued growth.

Investments in Re-Engineering, Six Sigma, Lean, Process Management & IT well-timed to drive non-capital intensive operating innovation in this environmentenvironment.

Allocating resources: investing in talent, domain expertise, new growth areas and markets.

Our unique capabilities (E2E, process management, depth of experience, combined with IT, process & analytics, and focus on effectiveness not just efficiency), represent a huge competitive differentiator, especially today.

24

Acquisitions at the right price, but in no hurry.

Companies that Invest During Recession Emerge as Market Leaders

Thank You

25

www.genpact.com

Business Pipeline& Customer Growth& Customer Growth

‘Tiger’ TyagarajanChief Operating OfficerChief Operating Officer

March 17 2009

26NYSE: G

March 17, 2009

Insights Into Pipeline in These Volatile Times

More activity… many more proof points of success

Activity increases: Regional Banks, Healthcare Providers, Pharma, Retailers

The case against setting up new captives strengthens

Many more entry points into clients

Fast start with Re-Engineering, quick fixes to generate cost savings & cash

Procurement and Finance & Accounting (F&A) often bundled now

New models of adding value and quicker pay-back gain traction

Outcome-based Pricing, Re-Engineering

27

Many More Entry Points… “doors that were always shut are now beginning to open”

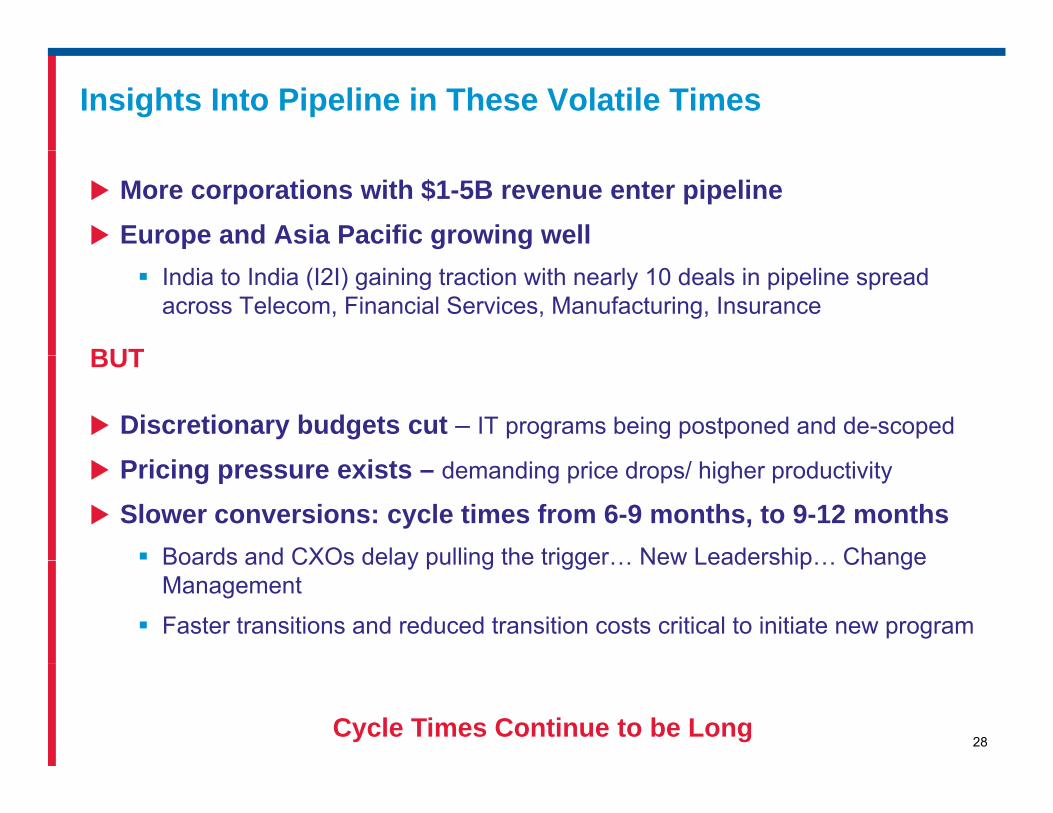

Insights Into Pipeline in These Volatile Times

More corporations with $1-5B revenue enter pipelineEurope and Asia Pacific growing well

India to India (I2I) gaining traction with nearly 10 deals in pipeline spread across Telecom, Financial Services, Manufacturing, Insurance

BUT

Discretionary budgets cut – IT programs being postponed and de-scoped

BUT

Pricing pressure exists – demanding price drops/ higher productivity

Slower conversions: cycle times from 6-9 months, to 9-12 months Boards and CXOs delay pulling the trigger New Leadership ChangeBoards and CXOs delay pulling the trigger… New Leadership… Change Management

Faster transitions and reduced transition costs critical to initiate new program

28Cycle Times Continue to be Long

Environment Driving Different Client Profile

15%Never considered outsourcing beforeFocus on risk mitigation

Depth of talent pool 12 t i l b ll

Client Profile Plays to Our Strength

15% Focus on risk mitigationRequire lower transition time & costWant established geographic presence and depth of capability

12 countries globallyComplex transition abilityExperience & speed of deployment

New clients who know their specific pain-points Want a sharply defined solution

35%Acutely focused Re-Eng. solutionsInvest in industry & domain expertise Cash & cost reduction solutions with

Existing clients

Want a sharply defined solution Cash & cost reduction solutions with faster pay-back

Expand into multiple productsExisting clientsTrusted relationships who want to accelerate to new areas

50% Deploy outcome-based approach, where applicableIncrease investment in Account Management

29

g

New Prospects in Pipeline Driven by New Economic Realities

Pipeline Growth Across Industries and Services R i Mi (D li )Industry Mix

Manufacturing and Services drive pipeline growth, while BFSI holds its ownBFSI

ServicesManufacturing

Region Mix (Delivery)Industry Mix

Industry-specific solutions, Procurement Services, Analytics, Re-Engineering driving growth,

hil F&A h ld itwhile F&A holds it own

60% of our revenue needs global delivery and we are well positioned to deliver

Q2'07 Q4'07 Q2'08 Q4'08

Services Mixto deliver

F&A

ITOIndustry-SpecificSolutions

Customer ServicesProcurement Svcs.Others

30Environment Creating Growth in Pipeline

Q2'07 Q4'07 Q2'08 Q4'08

Why Do Clients Choose to Partner with Us?

Clients gravitating from efficiency to

Why Win?

effectiveness

Seeing business impact E2E can create

Proven track record in operational excellenceexcellence

Global Delivery footprint

Ability to build partnerships quickly

Price higher than competition

Niche capabilities in certain industries

We lose to incumbents in the ITO space

Why Lose?

31

y ose

Increased Client Confidence Through Delivering Business Impact

A Journey to Win a Relationship

Global ERP D i S l t d

Competitive Selection Process RFP to 7providers

Shortlist to 2

H2’08 H2’08

Detailed Due Diligence

H2’08

Design-Invited as functional Experts

H1’09

Selected Preferred Partner

H1’09

Stayed Engaged

Decision made to outsource

H2’08 H2’08 H2’08

Continued Dialogue

H1’09 H1’09

H1’08 H1’08Drive EffectivenessReplicate O2C & P2P - multiple divisionsDrive Working Capital ReductionE2E Process Knowledge ERP template

1st Engagement: Point Solution

H1’07 H2’07

Procurement, HRO, F&A &

IT

Re-Eng: O2C & P2P

Discussion on Captive vs. Outsource

H2’07

E2E Process Knowledge - ERP templateCan all this be done at an effective price?

32Outstanding Execution and Partnership Approach

Growth With Our Clients Reaffirms Our Strategy

$ < 2 MM 17% Existing clients drove ~85% of our

CAGR

es

MM

$5 – 25

$2 – 5 MM

125%

76%

Existing clients drove 85% of our growth in 2008

Increasing client diversification

> $25 MM

Rev

enue MM

12%

125%~20 clients doubled their relationship in 2008 vs. 2007

Several clients won in 2005 & 2006MM 12%

each contributed over $10MM in 2008

Client Base

2006 2007 2008

33Our Growth is Driven by the Strength and Quality of Our Clients

Breadth & Depth of Services Leads to Growth

Several ways to expand a relationship:Analytics

OthersIndustry-Specific Solutions >100%

CAGR

Several ways to expand a relationship:

Expand to different divisionsProgress across functionsReplicate geographically

F&ACustomer Services / CollectionsITO

>100%

Replicate geographicallyRe-Engineering & Analytics to drive outcome

>100%

87%

Foundation remains consistent: Robust day-to-day operational excellence

>100%

Lean & Six Sigma based improvements

2005 2006 2007 2008

52%

34

2005 2006 2007 2008

Each Client has to be “Referenceable” – Only Way to Grow

As We Grow, We Expand Our Footprint Globally

How did we do this?$9MM – $18MMOver $18MM

Latin America - 3 countries

$ $CXO level partnership & dialogue

Jointly own and drive outcomes (Order to Cash Procure to Pay)Addition of IT

• Procurement & Customer Svs.

Transition to Transitions for 5

F&A expansion with 3 countries

(Order-to-Cash, Procure-to-Pay)

Reinforce strategic account ownership - Global Operating Leader & dedicated Relationship

Addition of IT Services

$3MM – $6MM

venu

e ($

)

Transition to Top 5 Countries

10+ countries -

Procurement Svs. 8 - 34 countries

EU countries Manager

Continuous improvement in Net Promoter Score (NPS)

Rev

2007 2008 2009

F&A and Procurement

2 more countriesStarted Re-Eng

10+ countries -Africa & AsiaOutcome Based

India

Europe

China

Americas

35

2007 2008 2009

Start Small and Expand with Clients

Driving Business Outcome: ~$100MM Reduction in Raw Material Inventory

Business Challenge

A client with 30+ product lines each with 20K+ parts across 6 assembly organizations was struggling ith l t i l i t twith low raw material inventory turns

Root Cause

Unavailable complete view of parts level inventory; policy levels determined through manual judgment

Genpact SolutionGenpact Solution

Inventory segmentation into “prior, current, ahead, surplus” with clear definitions

Developed a web-based inventory analysis tool; analyzed order policies and transit timesp y y ; y p

Raw material inventory turns: Improved from 12 to 17

36

Inventory Reduction Support Extended to Other Business Units Reducing Raw Material Inventory - From $220MM to $120MM

Collaborative Approach Strengthens Relationships

Several business impact projects completed … each a $10-25MM idea … replicable across clients and industries

Base Cost Reduction – T&L, Telecom, Fleet, purchased services and program costs

Our DNA500+ Trained BBs / MBBs

Income Leakage – Identify Supplemental Billing Opportunities for Contracts

Inventory Reduction – Reduce Excess and 500+ Trained BBs / MBBs / QLs (175 Certified)9000+ Trained Green Belts (1700+ Certified)650+ Lean Six Sigma

Inventory Reduction Reduce Excess and Obsolete Inventory

Warranty Cost Reduction – Improve Warranty Cost as % of Sales 650+ Lean, Six Sigma

projects certified in 2008

Warranty Cost as % of Sales

37Our Foundation: Best-In-Class and Industrial Strength DNA

Our Relationship with GE

Broad and deep – 30+ sub-businesses across globe, plus multiple products

Strong performance over 10 years: Net Promoter Score at highest ever, 59%

High-level connections – about 200+ different CXO-level relationships across GE business units

Business risks and opportunitiesGE Capital origination volume decline offset by increased collections

Growth in Infrastructure businesses

GE 300,000 employees...Genpact only 14,000

New products under discussion

Europe - an opportunity

Increased quality and quantity of interaction at all levels to leverage theIncreased quality and quantity of interaction at all levels to leverage the opportunities and manage the risk

30+ front-end executives getting business

Dedicated account managers

38Well-Established, Deep Connections – Critical In These Times

Dedicated account managers

Our Client-Centric DNA Yields Top NPS Results

Genpact Achieved a Net Promoter Score (NPS) of 47% in 2008

Genpact compares with the best Services Companies in the U S * 47%Genpact compares with the best Services Companies in the U.S.

More Than 1 in 2 Respondents Are Promoters or “Delighted Customers”

39%

47%

NPS

8pts

gPromoters - customers that indicate they are highly likely (9 or 10 on a 10 point scale) to recommend a company to friends

The Customer Voice Excerpts from our Last Survey

H1 ‘07 H1 ‘08Time

The Customer Voice – Excerpts from our Last Survey

“Relationship to date has been very constructive. Feels like a partnership. Very strong capabilities…”

*Source: “2008 Satmetrix Net Promoter Industry Reports”, As reported on Business Wire, April 10, 2008Net Promoter® is a registered trademark of Bain & Company, Inc., Fred Reichheld and Satmetrix Systems, Inc.”

“Genpact is a true business partner, that brings a wide breadth of talent to help solve and support business processes of the clients.”

39*

Reflects our Continuous Focus and Rigor on Client Satisfaction & Outcomes

2009…Ideal Time to Acquire Talent

“A downturn can give smart companies a chance to upgrade their talent.” (Upgrading Talent, McKinsey Quarterly Dec 2008)

Talent imperatives:

Build talent pipeline for Revenue GrowthStrategic Initiatives industry domain experts banking insurance healthcareStrategic Initiatives...industry domain experts - banking, insurance, healthcare, retail, etc. New Geographies…India to India, China to China

Enhance competitive position on talentEnhance competitive position on talentContinue focus on retention… drive engagement initiativesSeize the opportunity to close critical skill gaps…hire “not-in-play” talent

Benchmark Cost Competitiveness: Cut Fat FastBenchmark Cost-Competitiveness: Cut Fat FastIncrease spans, support, supervision and drive Shared Services

Attrition DownBeneficial to our clients and in line with our focus on Account Management

40

Beneficial to our clients and in-line with our focus on Account Management

Highly Engaged Talent Pool - Meet Changing Client Needs

Takeaways

Despite uncertain economic environment and pricing pressure, long-term market opportunity remains huge

New prospects entering pipeline…driven by new economic realities

Our Industrial Strength Six Sigma, Process Excellence, unique E2E approach and Re Engineering services position us strongly to meet theapproach and Re-Engineering services position us strongly to meet the critical changing needs of our clients today

Our Operational Focus and Operating Rigor help drive End-To-End I t li t ’ t t i i tiImpact on our clients’ strategic imperatives

Momentum with existing clients – further builds on well-established, strong relationships

Focus on the growth areas…invest further in the breadth and depth of our services across verticals and new geographies

Continue to drive productivity and efficiency

41

Continue to drive productivity and efficiency

Thank You

42

www.genpact.com

Break

43NYSE: G

Financial OverviewFinancial Overview

Vivek N GourChief Financial OfficerChief Financial Officer

March 17 2009

44NYSE: G

March 17, 2009

Financial Strategy Aligned with Genpact’s Long-Term Vision of Sustained Profitable Growth

Well-evolved, Mature and Stable Long-term Business ModelScale, risk diversification and investment for growth

Diversified Recurring Revenue Base Driving Sustained Profitable GrowthTremendous mining potential from existing well established clients

Growth markets… Europe, India to India, China to China

Products… E2E, Procurement, F&A, Collections, Re-engineering, Analytics, ‘Cash is King’, ‘Risk Management’, ‘Cost Out’

Industry… Healthcare, BFSI, Services

Drive Operational and Cost efficiencyPermanently change cost structure e.g NIIT training JV: train & hire vs. hire & train

Re-negotiated down terms and costs of new SEZs

Conservative Financial Policy and ControlsStringent deal review and pricing discipline

Rigorous tracking of operating units on business-critical metrics

45

Rigorous tracking of operating units on business critical metrics

Prudent cash management

Strong corporate governance

Global Clients Driving Sustained Revenue Growth

2008 growth at 26%

Global Clients grew 62% over 2007($ in MM)

Global Clients-a)

Genpact Revenue Growth

Global Clients grew 62% over 2007

GE grew 7% (adj. for divested businesses) CAGR30%

823

1,041

GE

Revenue per employee increased 9% to

$30,800 over 2007, 17% since 2006,

reflecting shift towards higher value work,

613

9%

53%

53%160342

551

26%

53%

reflecting shift towards higher value work,

Re-engineering, Analytics, E2E

85% growth from existing clients453 481 490

26%

85% growth from existing clients

Delivered on 2008 guidance

91%74%

2006 2007 2008

74% 47%

Revenue / Employee $K 26.4 28.2 30.8

46Outstanding Global Client Growth-a) Global Clients Revenue including GE Divested businesses and acquisitions (GAAP)

p y $

Revenue Diversified by Geography (Service Delivery)

Europe India Americas Asia ($ in MM) 2006 2007 2008 08 G% CAGR %

Europe 31 84 112 34% 90%11%8%

8%

p

Asia 34 50 81 62% 55%

India 483 609 764 25% 26%

73%

Americas 65 81 84 4% 14%

Total 613 823 1,041 26% 30%

Europe growth 50% (adjusted for ICE acquisition), mainly driven by multi-lingual capability

in F&A practice

Growth in Asia driven by customer services practice in Philippines

F&A, Supply Chain & Analytics driving growth in India

47

Europe, China & Philippines leading the growth trajectory… value of our global delivery model

Revenue Diversified by Industry Vertical

16%

BFSI Manufacturing Services

42%

42%

($ in MM) 2006 2007 2008 08 G % CAGR BFSI 273 361 442 22% 27%

Manufacturing 268 347 435 25% 27%

Services 72 115 164 43% 51%

* Services segments include Media, Retail, Telecom, Hospitality and Transportation

Total 613 823 1,041 26% 30%

48

Balanced growth in Manufacturing and BFSI segment…While increasing penetration in Business Services

Delivered Significant Margin Expansion

Adjusted Income from Operations at $178MM, +33% over 2007, margin at 17.1% 80 bps($MM)

Adjusted Operating Income and Margin-a)

4,6005,300

Adj. Op. Inc. per employee +15% vs. 2007 $5,300, +26% since 2006

CAGR36%

4,200

97134

178Moving up the value and margin chain, over the long term

New offerings like Re-Engineering Analytics

36%

New offerings like Re Engineering, Analytics, E2E, and gain share building momentum

Margin improves as existing global clients gain scale and reach stable state

15.8% 16.3% 17.1%

2006 2007 2008 gain scale and reach stable state

Tight contracting discipline… terms include inflation adjustmentsAdj Op Inc / Employee $

Adj. Diluted 0.44 0.50 0.76EPS $

49

Cost productivity each year on input factors

Adjusted Diluted EPS at $0.76, up 51% from $0.50 in 2007

-a) Adjusted Operating Income = Income from Operations + Formation Accounting Amortization + Stock Options Charge + Indian Fringe benefit tax on Stock Option

Proven Cost Management Disciplines

Wage inflation ~7-8% in 2008 vs market 10-12% minimumCosts Actions

SalariesWage inflation 7-8% in 2008 vs. market 10-12%, minimum increase in entry level compensation, Increment freeze on VP+2009 estimated wage inflation at 4-5%

Span of control up from 15 per supervisor to 16Supervision Span of control up from 15 per supervisor, to 16

Support FunctionSupport headcount held flat since 2007… through 2009

Bench Bench as % of revenue-generating employees ↓ from 13% in 2007 to 10% in 2008; Targeting further reduction of 1-2% in 2009

InfrastructureContinue to expand to Tier 2 cities and SEZ units, productivity in Utility, Transport cost

Costs of hire per associate in India down 8% in 2008;Hiring

Training

Costs of hire per associate in India down 8% in 2008; 2009 target further 10% reduction

Investment in building domain expertise and E2E capabilities; fundamental shift to NIIT JV ‘Train & Hire’

50

IT/Telecom

fundamental shift to NIIT JV Train & Hire

Driving productivity through bandwidth rationalization, better rates and scale benefits

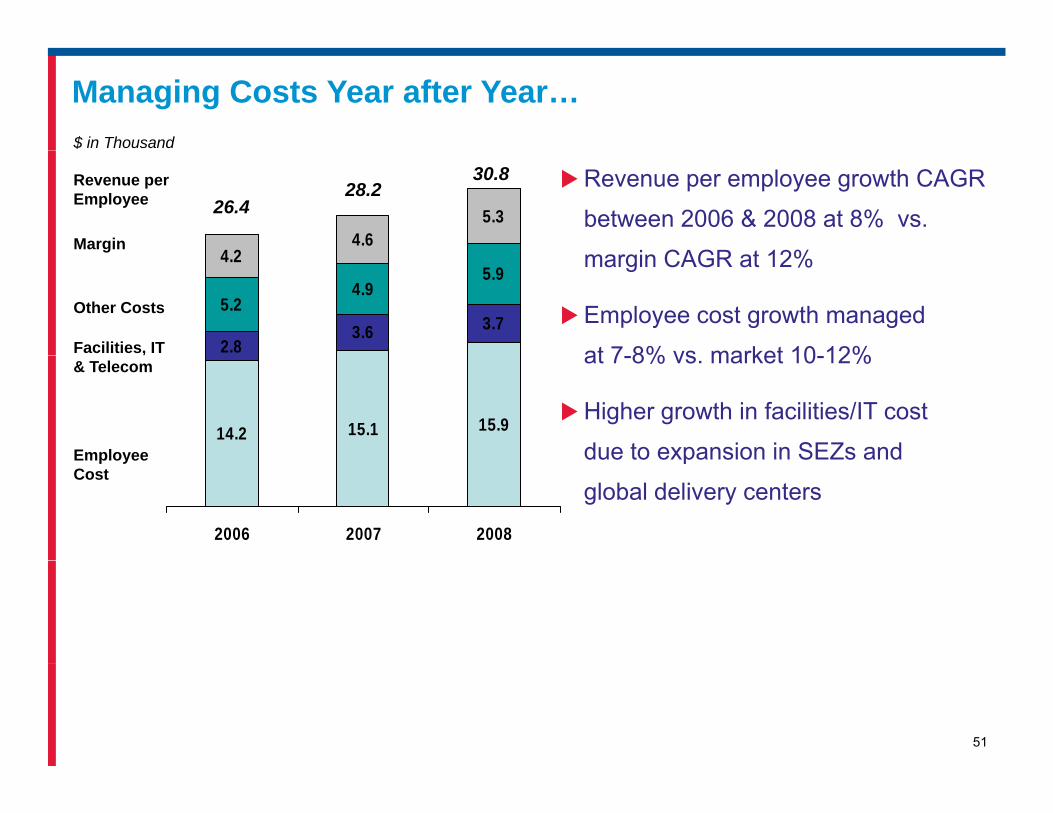

Managing Costs Year after Year…$ in Thousand

4 24.6

5.3Margin

Revenue per Employee 26.4

28.230.8 Revenue per employee growth CAGR

between 2006 & 2008 at 8% vs.

i CAGR t 12%

2.83.6 3.7

5.24.9

5.94.2

Facilities, IT

Other Costs

margin CAGR at 12%

Employee cost growth managed

at 7 8% vs market 10 12%

14.2 15.1 15.9Employee

& Telecom at 7-8% vs. market 10-12%

Higher growth in facilities/IT cost

due to expansion in SEZs and

2006 2007 2008

EmployeeCost

due to expansion in SEZs and

global delivery centers

51

What is Driving SG&A Leverage in Q4’08 vs. Q3’08 ?

(23%)$71$55SG&A 4%$271$282Revenue

V%Q3’08Q4’08$MM

(690 bps)26.3%19.4%% of Revenue

Leverage from lower bench and support headcount levels ~125 bps

Lower travel in Q4 over Q3 ~100 bps

Leadership training spend in Q3 ~50 bps

Annual actuarial true-up of employee benefits ~75 bps

Higher India fringe benefit tax in Q3 over Q4 ~50 bps

Lower bad debt provision ~50 bps

Lower other operational costs (legal, consultants, insurance, G&A) ~100 bps

52

Lower IT costs ~50 bps

Infrastructure leverage ~90 bps

Consistently Generated Strong Cash Flow Growth

Cash flow from Operations and % of Revenue

($MM)18%

20%$66MM from Increase in Operating Income

18%DSO improved from 75 days to 73 days

211

Cash Held in Banks $135MM150

211

US Govt. Treasury Bills $191MM

Short Term deposit with GE $59MM

$385MM

CFOA as a % of Revenue

2007 2008

53Strong Cash Flow Backed by Prudent Liquidity Management

Capital Expenditure

Capital Expenditure and % of Revenue (a) Invested in new sites in Guatemala,

Morocco and Lublin (Poland)($MM)

8%13%

Re-negotiated SEZ terms on capacity

in India7%

Re-negotiated supplier contracts on IT

in India7966 69

7%

2006 2007 2008Capex as a % of Revenue

542009 Estimated Capex 6% of Revenues

(a) Capital expenditure excluding proceeds from sale of assets

2009 Guidance

Revenue Growth 10-15%

GE growth (adjusted for divestiture) Low single digitGE growth (adjusted for divestiture) Low single digit

Adjusted Operating Income Margin% 16-17%

Capex 6% of revenue

Effective Tax Rate 17% - 19%% %

Our guidance represents a cautious approach given the uncertainties in the macro environment.

55

Thank You

56

www.genpact.com

Closing RemarksClosing Remarks

Pramod BhasinPresident & CEOPresident & CEO

March 17 2009

57NYSE: G

March 17, 2009

The World has Changed

Changing Client Needs

From growth & i t t

Opportunities for Growth

Focus on cash preservation and t d ti l di li t t

How We Are Positioned to Capture Opportunity

E2E solutions are non-capital i t iexpansion to cost

reduction

Preservation of cash & improved working capital

cost reduction leading clients to aggressively look at new ideas and operating modelsNew Growth Markets:

China

intensive

Scale existing cash / cost solutions

Re-allocate dedicated Middle EastImprove productivity

Deflation focused sourcing & spend requirements

ChinaIndia

Growth Opportunities:HealthcarePharmaceuticals

leadership resources and swat teams to growth areas

Speed of deployment for 90 day pay-back

Middle East Japan

CollectionsRisk Management

Minimize capital investment

“Cash Is King”“Cost out”

Strong Pipeline:New categories of prospects d i b i liti

Ideal time to acquire global talent

Outcome based / gain share pay-back model

Risk ManagementProcurement / Supply Chain

driven by economic realitiesOperating Innovation

58Factored These Risks in our Growth Plans

Investing for the future

Build our brand, sales engine

Hire great resources… Global talent never more attractive

Expand into new growth markets… Middle East, Russia, Latin America, Scandinavia

E l i i d l M f FTE’ t tEvolve pricing models…. Move away from FTE’s to outcome based

Increasing investment in technology enabling & coreIncreasing investment in technology, enabling & core

Drive E2E across more products & industries, build domain expertisep

59Investing now for future growth

Why Genpact Even in This Environment?Market opport nit remains h ge despite en ironmentMarket opportunity remains huge despite environment

Global business process market, significantly under-penetrated, Est. 6-8% growth vs. flat ITOProven business model – start small and expand with clients

Expanding diversified blue-chip client relationships, and enhancing products and services, support p g p p , g p , ppcontinued growth (85% from existing clients); Growth in GE revenues even after 10 years

Breadth and depth of services across verticals and marketsIndustry led solutions around BFSI and manufacturing coupled with domain expertise in F&A, Procurement Analytics and Technology enablers supports client value creationProcurement, Analytics and Technology enablers supports client value creationSwiftly allocating resources to new growth areas and to domestic markets of India & China

Proven track record of performance and growth: 30% revenue CAGR over 3 years Driven by Global Client (GC) growth: $551MM in ‘08 GC revenues, more than 13X $42MM in ’05Long-term margin improvement

Strong balance sheet and cash flows, including approximately $385MM of liquidityCash from operations – improved to 20% of revenue compared to 18% in ‘07

Strong pipeline – new prospects driven by new economic realitiesStrong pipeline – new prospects driven by new economic realitiesE2E: a differentiated way to deliver business outcomes for clients

Previous investments in Re-Engineering, Six Sigma, Lean, Process Management & IT drive non-capital intensive operating innovation

60

E2E capabilities, along with IT, process & analytics, and focus on effectiveness not just efficiency

Perfectly Positioned for this Environment

The Year Ahead

Responding to the dramatic change around us from a position of strength.

We can be part of the solution: validation from a strong pipeline with new prospects…demand for our services has never been higher.p p g

Our business model of expanding diversified blue-chip client relationships, and enhancing our products and services, supports continued growth.continued growth.

Investments in Re-Engineering, Six Sigma, Lean, Process Management & IT well-timed to drive non-capital intensive operating innovation in this environmentenvironment.

Allocating resources: investing in talent, domain expertise, new growth areas and markets.

Our unique capabilities (E2E, process management, depth of experience, combined with IT, process & analytics, and focus on effectiveness not just efficiency), represent a huge competitive differentiator, especially today.

61

Acquisitions at the right price, but in no hurry.

Companies that Invest During Recession Emerge as Market Leaders

Thank You

62

www.genpact.com

Question and Answer SessionQuestion and Answer Session

63NYSE: G

64NYSE: G