Embed Size (px)

Citation preview

Copyright BieResearch.com 2017 1

United States

Tax cuts lift short-term growth outlook

20 December, 2017

Ulrik Harald Bie, Independent Economist, [email protected]

www.bieresearch.com

• 2018 outlook raised further by 0.3 percentage points to 3.0%

• The adjustment is mainly a reflection of increased consumption growth

• Net export contribution turning negative and trade deficit to increase further

• Increased labor participation should keep unemployment around 4%

• No major effect on wages and inflation, but Federal Reserve to hike rates four times in 2018

Adding fuel to the fire

As Republicans push their proposal for tax reform

across the finish line, the US economy is growing

strongly, fueling fears of overheating. The November

job report showed another 228,000 new jobs, with

2.1 million jobs created during the last year. My as-

sessment is that the US labor market has more slack

than indicated by the unemployment rate of 4.1%, but

also that wage dynamics have changed compared to

the pre-crisis period leading to lower wage growth.

This is also why I am less concerned than most US-

based analysts about higher inflation.

The final tax cuts of USD1,500 billion over ten years

are somewhat larger than I envisioned in October,

and I have added 0.3 percentage points (pp) to the

2018 GDP-growth outlook. It now stands at 3.0%.

That adds USD56 billion to actual (real) GDP; not a

whole lot, but my October forecast was already signif-

icantly above consensus. Federal Reserve/FOMC’s

2018 forecast from September was 2.1%. Using that

growth rate as a benchmark, my new forecast entails

USD164 billion in additional activity in 2018. I expect

growth to lose a little steam in 2019 settling at 2.5%,

primarily due to slower consumption growth. FOMC

expects 2.1% GDP-growth in 2019.

No major effect on corporate investments

The tax cuts are due to take effect in 1Q/2018. Larger

US corporations have enjoyed a period of strong

profit growth and are able to finance the investment

plans they want to undertake. I included a significant

bump to the investment outlook in my October up-

date, partly reflecting anticipated tax cuts and dereg-

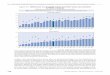

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2013 2014 2015 2016 2017 2018 2019

Current forecast

Change y/y (%)

US GDP growth outlook

October forecast

Source: Macrobond, BieResearch.com

Copyright BieResearch.com 2017 2

ulation, but also the increased underlying wage pres-

sure, which should lead to more purchases of ma-

chinery and technology to improve productivity.

Hence, for larger corporations the tax cuts should

flow almost exclusively to shareholders through in-

creased dividends and/or share buybacks. The stock

market is clearly expecting a quick, tangible return –

not an uncertain future payoff from increased pro-

duction capacity. Smaller businesses could allocate a

larger share to investments, and hiring intentions

have increased. Overall, I do not expect a major addi-

tional effect on business investments (up 7% in 2018

and 5% in 2019) from the final tax legislation com-

pared to my initial assessment.

Labor productivity should increase by 1.5% for the

2015-2019 period. Employment growth peaked at

2.3% in 2015, but has decreased in 2017 to an esti-

mated 1.4% and I expect a further decline to 1% next

year – or a monthly average of 125.000. It is unusual

that employment growth weakens at this stage of the

cycle; normally it is full speed until a recession hits.

However, this is in many ways an unusual recovery.

More tailwind to consumers

The individual tax cuts, a much stronger perception

of the economy and increased dividend payments

(showing up in the savings rate currently at 3.2%) are

likely to lift consumption more than I expected in Oc-

tober. As the cuts are not permanent (expires in

2026), and the tax reform massively increases public

debt, a Richardian-equivalence approach would see

the increased after-tax income move to higher sav-

ings. I doubt US households have this foresight, and

I have increased my forecast for private consumption

growth in 2018 by 0.4 percentage points to 2.8% -

and expect further 2.4% growth in 2019. While

households are increasingly willing to finance con-

sumption through higher debt, I still expect slower

real income growth to become visible.

As the tax reform does nothing to discourage the im-

portation of goods, the higher domestic growth trans-

lates into an even larger trade deficit – and negative

contributions from net exports. This also increases

the risk of adverse trade measures from President

Trump. However, some analysts expect the lower cor-

porate tax rate to reduce the use of transfer pricing

within multinationals, which could deliver a signifi-

cant technical one-off boost to exports and lower the

trade deficit. This would also benefit productivity

growth by lifting overall GDP, while employment stay

the same as actual activity is not affected.

Copyright BieResearch.com 2017 3

Higher potential growth

The level of potential growth is mainly an academic

issue, but has important policy implications. Higher

potential growth improves the (theoretical) ability to

absorb a period of high growth without generating in-

flation. That allows the Federal Reserve to be more

patient – and improves the CBO budget outlook.

The US economy is currently growing at around 3%.

The Congressional Budget Office (CBO) estimate po-

tential growth to be 1.88% in the longer run and the

Federal Reserve’s FOMC kept its projection at 1.8% at

the December meeting - completely dismissing dy-

namic effects from tax cuts and deregulation.

However, I think the current potential-growth esti-

mates will be revised up during 2018. Estimates of

potential growth are basically sophisticated moving

averages of growth in previous years. Hence, after a

period of subdued actual growth, potential growth

declines – without any assessment of why growth was

lower or whether structural changes have moved the

economy towards a more (or less) efficient state.

A 6-year moving average (6Y MA) captures the move-

ment in CBO’s forecast of potential growth well. Us-

ing my own growth forecast, the 6Y MA reaches 2.5%

in 2019. I think that is above the long-term potential,

but in my view the potential for growth in the US has

not declined compared to the pre-recession period

and remains 2.0-2.25%. I expect CBO budget reports

in 2018 to reflect this. President Trump will take full

credit for the better long-term outlook, although it is

mostly a reflection of past performance.

Labor market is key

While I expect productivity to increase substantially

in the coming years, the available supply of labor re-

mains a key issue. The actual level of slack in the labor

market confounds economists; even the Federal Re-

serve is in the dark – as stated repeatedly by Chair

Yellen this autumn.

The unemployment rate points to a very tight labor

market, however the relationship between unemploy-

ment and wage growth has changed substantially

since the recession. A regression using data from

1997-2007 generates an estimated wage growth of

4.1% with a 4%-unemployment rate, while the same

model generates 2.5% wage growth using data from

2012. The two models have comparable explanatory

power. Using a wider definition of unemployment

(U6) does not materially alter the result.

That also implies that a significant decline in the un-

employment rate to 3.5% only generates an estimated

Copyright BieResearch.com 2017 4

wage growth of 2.6% - well within my expectation of

2.5-3.0% wage growth in 2018, and in line with the

expectations priced into the equity market of no ad-

ditional allocation of revenue to labor. The diver-

gence in the wage growth for skilled and unskilled la-

bor is likely to increase as technology substitution are

more of a threat to low-skilled labor.

Looking at the GDP/unemployment relationship

since 1970 (including six recessions and recoveries),

GDP-growth of 3.0% should generate a quarterly de-

cline in the unemployment rate of 0.1 percentage

points. During the current recovery, the implied de-

cline has been even larger, but as productivity invest-

ments do their trick, I expect the relationship to move

closer to the historic average. Using my growth fore-

cast, unemployment should be bottoming out at 3.9%

by mid-2018 (with a model-wage growth of 2.6%).

While population growth is held back by a low

birthrate and a large decline in illegal migration, the

participation rate points to additional available labor

within the active age groups. The participation rate

(63%) remains lower than the one in 2010 (65%) for

all but the oldest cohorts. However, since 2015 par-

ticipation has increased a lot more for men than for

women in the age group 40-59 years – and the picture

is even more pronounced compared to 2010. Hence,

an additional increase in female participation should

be possible and is included in my assessment of the

labor market. Moreover, the 17.5 million part-time

employed women could also increase workhours add-

ing to the labor supply.

Inflation caught in the middle

In October I expected CPI inflation to average 2.1%

this year and 2.0% in 2018. Since then, headline in-

flation has picked up as oil prices have increased

more than expected, while core CPI has remained at

1.7%, and core PCE inflation stands at 1.5%. The ad-

ditional demand created by the tax reform removes

some of the downside risks to inflation, but since I do

not expect a major passthrough to wages, my infla-

tion forecast is unchanged.

For CPI, smaller increases in rents and owners’

equivalent rent exert a downward pressure on overall

inflation due to the weight in the index (33%), while

subdued health inflation (currently 1.2%) should

keep PCE core inflation from moving up substan-

tially. If anything, the lower corporate tax rates allow

for some additional price war in the retail space. I also

expect oil prices to decline in 2018 as US production

increases.

Copyright BieResearch.com 2017 5

Four hikes from the Federal Reserve

The December forecasts from the FOMC can best be

described as “wait and see”. With a tax reform in the

pipeline and Chair Yellen’s last press conference to

consider, substantial changes to the outlook could

have caused unnecessary attention. However, the

higher growth/lower unemployment forecast should

lead to an adjustment of the dot-plot for 2018. Alt-

hough I do not expect an outbreak of inflation, I do

expect Federal Reserve to err on the side of caution

and speed up the interest rate cycle with four hikes in

2018. However, as the business cycle loses steam in

2019, the pace slows to two further hikes. This could

well be the end-point for this hike cycle.

Less recession risk, more financial

Governor Kashkari from Minneapolis Fed – the lead-

ing dove on the FOMC – has argued that the flatten-

ing of the US yield curve indicates increasing risk of a

recession. While a missed opportunity for genuine re-

form of the tax code, I think the tax cuts lowers the

risk of recession before 2020; there is just too much

cash flowing around for the party to stop. I see the

flatter US yield curve as an indirect consequence of

ECB’s and Bank of Japan’s QE-programs and an

above-normal demand for longer, safe bonds.

While US 2Y yields are responding to Fed normaliza-

tion, 10Y yields are affected by arbitrage; the spread

to German 10Y yields cannot exceed the exchange

rate-corrected alternative return. Since German

yields are suppressed by ECB’s QE, US 10Y yields are

too. When German yields begin to rise in 2018, so

should US yields. Normally the relationship is the

other way around, but with interventionist central

banks, normal does not apply.

However, the tax cuts (and too lenient monetary pol-

icy in Europe and Japan) increase the risk of a major

financial correction. With record-breaking prices on

risky assets, the market is priced for a perfection that

could be frustrated. Talks of a US infrastructure pack-

age is the latest market boaster, although I do not ex-

pect much to happen. Convincing Republicans to cut

taxes is one thing. Convincing them to increase public

spending something completely different. Whether

the economy can outrun financial turbulence is un-

certain.

![FCC · Web viewI3 = The smaller of [((1 + 2) * 0.1) = 0.3] and 0.2 (the maximum additional percentage) = 0.2. 2. Calculation of dollar amount associated with the additional percentage](https://img.pdfslide.us/doc/110x75/5f74a68190fce9590854a999/fcc-web-view-i3-the-smaller-of-1-2-01-03-and-02-the-maximum-additional.jpg)

![Human Papillomavirus and Related Diseases Report PERU · Oral contraceptive use (%) among women 9.1 HIV prevalence (%), adults (15-49 years) 0.3 [0.3 - 0.4] Sexual behaviour Percentage](https://img.pdfslide.us/doc/110x75/5eddcef6ad6a402d6669020f/human-papillomavirus-and-related-diseases-report-peru-oral-contraceptive-use-.jpg)