Embed Size (px)

Citation preview

IPSEN

Sophie Compagnon, Melodie Debacker,Gaelle Datchoua, Catherine Lucas

1

Le 05/03/10

2

INTRODUCTION

3

• Specialized world pharmaceutical group

• More than 20 products marketed in the world

• Originally, French independent company

• Headed by Beaufour Family

• Third independent pharmaceutical firm in France (sales)

About IPSEN

4

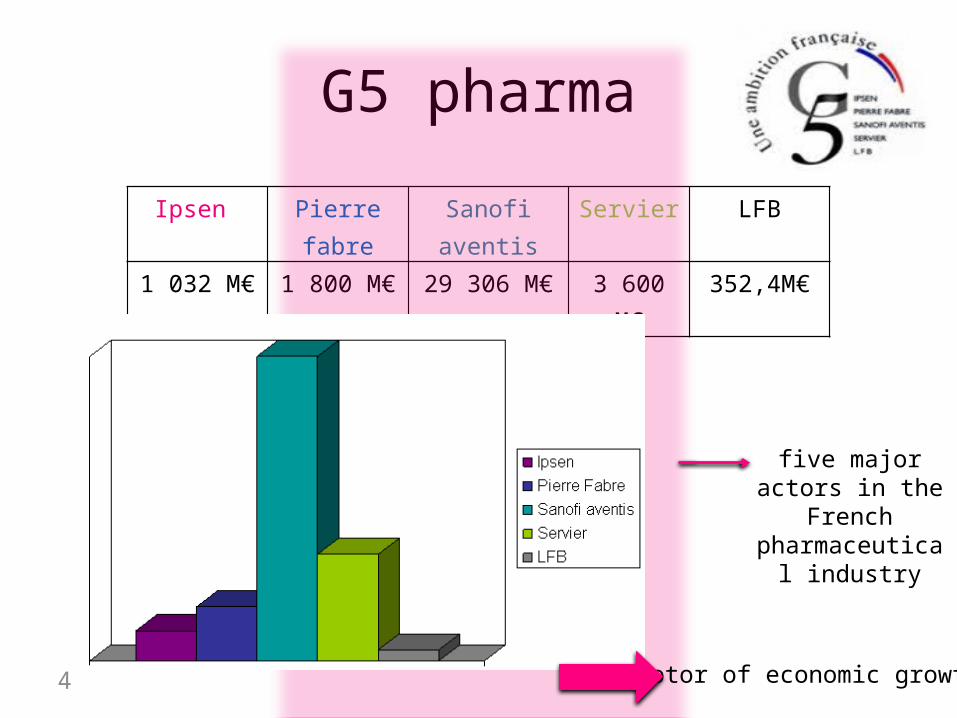

G5 pharma

Ipsen Pierre fabre Sanofi aventis Servier LFB

1 032 M€ 1 800 M€ 29 306 M€ 3 600 M€ 352,4M€

five major actors in the French

pharmaceutical industry

Motor of economic growth

5

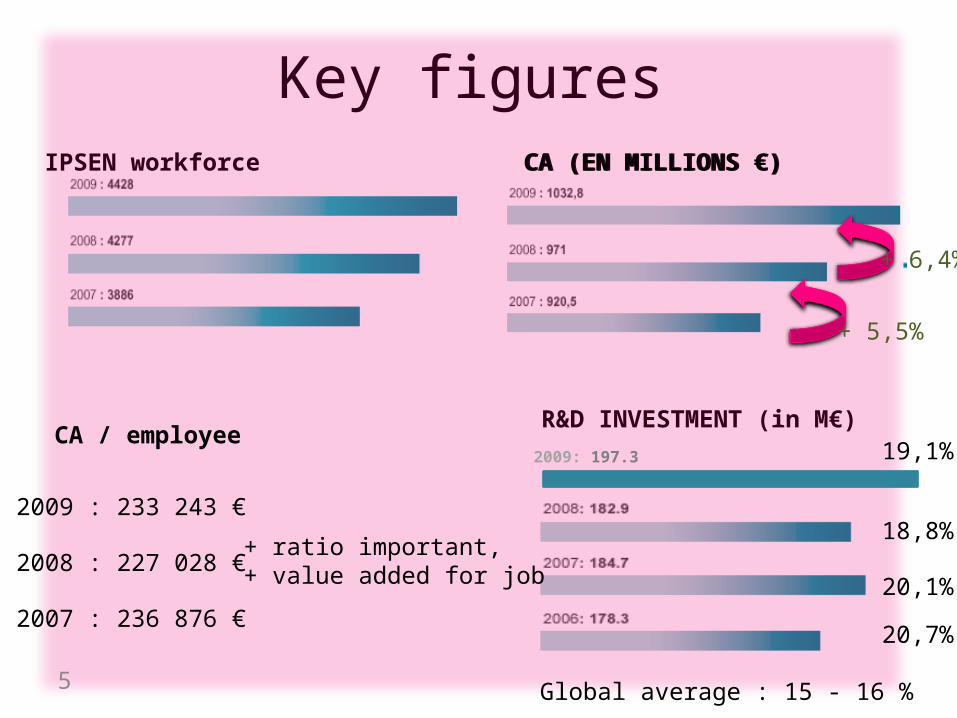

Key figuresIPSEN workforce CA (EN MILLIONS €)

R&D INVESTMENT (in M€)

2009: 197.3 19,1%

18,8%

20,1%

20,7%

CA / employee

2009 : 233 243 €

2008 : 227 028 €

2007 : 236 876 €

+ 5,5%

+ 6,4%

Global average : 15 - 16 %

+ ratio important, + value added for job

CA (EN MILLIONS €)

6

Key figuresSales by therapeutic area 2009

Targeted therapy 60,3% oncology 24,3% endocrinology 19,6% neurology 16,4%

Primary care 36,8% gastroenterology 17,7% cognitive disorders 10,5% cardiovascular 7,1% other 1,5%

Other activities 2,9%

60,3%36,8%

2,9%

Sales by therapeutic area 2006

7

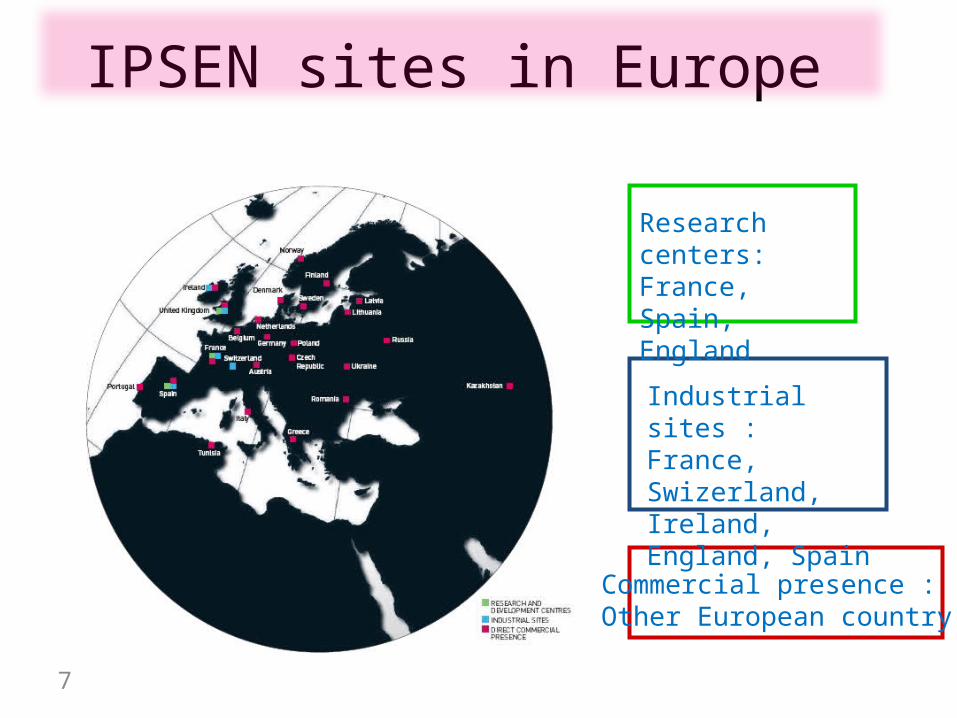

IPSEN sites in Europe

Research centers:France, Spain, England

Industrial sites : France, Swizerland, Ireland, England, Spain

Commercial presence :Other European country

8

Other IPSEN sites

US : research, industrial site and commercial presence

South America : commercial presence

China : industrial site and commercial presence

Rest of Asia : commercial presence

9

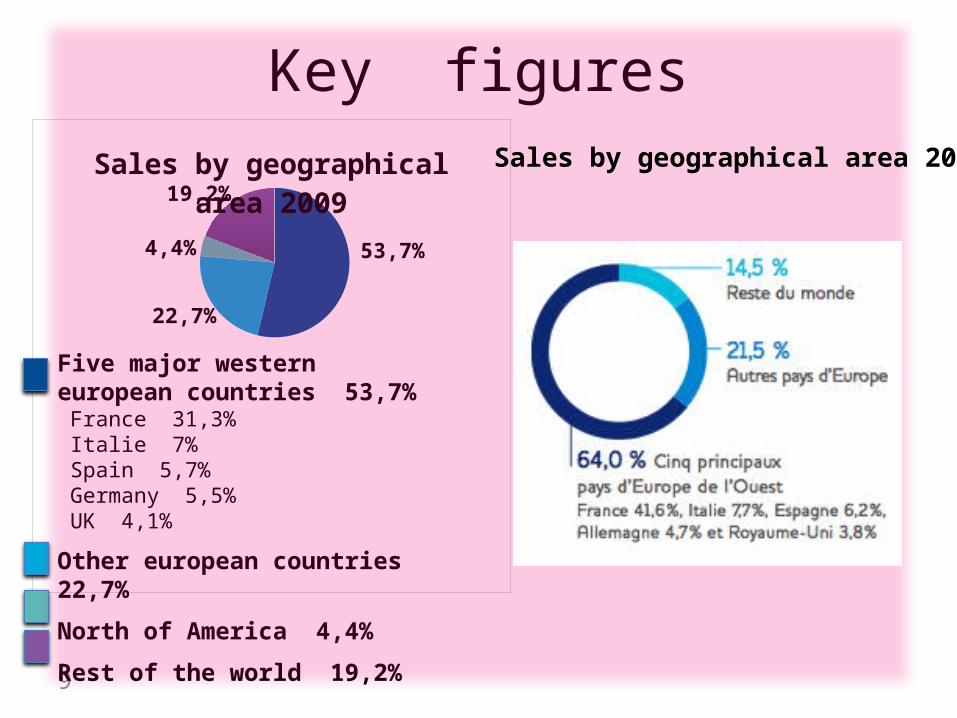

Key figuresSales by geographical area

2009

53,7%

22,7%

4,4%

19,2%

Five major western european countries 53,7% France 31,3% Italie 7% Spain 5,7% Germany 5,5% UK 4,1%

Other european countries 22,7%

North of America 4,4%

Rest of the world 19,2%

Sales by geographical area 2006

10

BACKGROUND

11

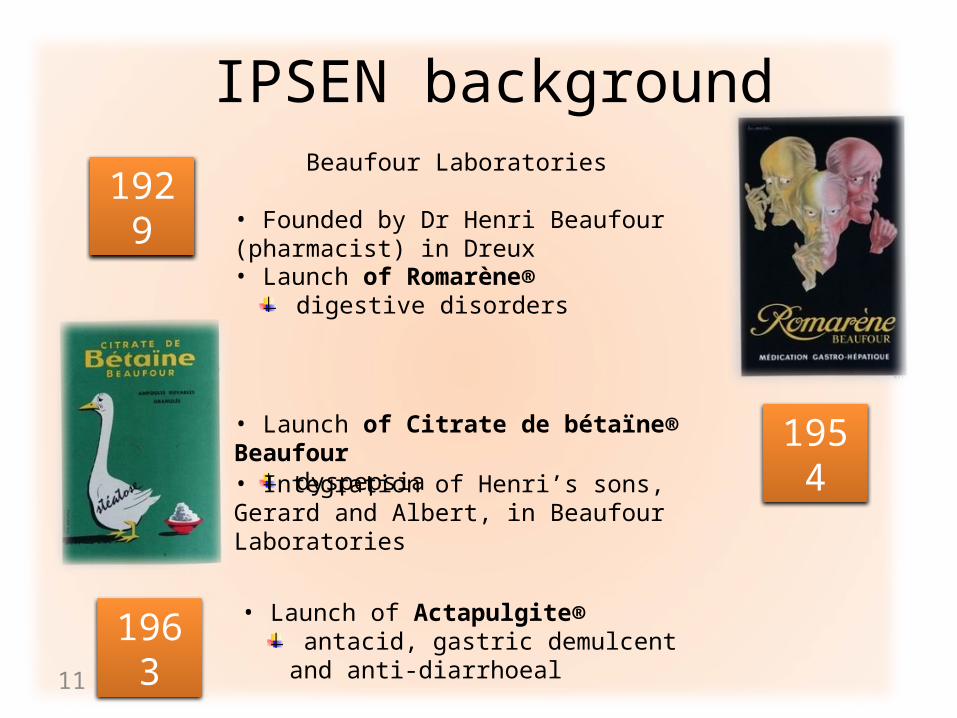

IPSEN background

1929

• Launch of Romarène® digestive disorders

1954• Launch of Citrate de bétaïne® Beaufour dyspepsia

Beaufour Laboratories

• Founded by Dr Henri Beaufour (pharmacist) in Dreux

• Integration of Henri’s sons, Gerard and Albert, in Beaufour Laboratories

1963 • Launch of Actapulgite® antacid, gastric demulcent and anti-diarrhoeal

12

70’s 70’s

Start marketing products of natural origin.

1970

IPSEN background

« IPSEN » creationSubsidiary company of « Beaufour Laboratories »

= Institut des Produits de Synthèse et d’Extraction Naturelle

Gingko biloba

Primary care

13

70’s 70’s

IPSEN background

1972

Indications: Cardiovascular

chronic venous insufficiency

acute haemorrhoid episodes

superficial phlebitis

Ginkor®Active substances:

Ginkgo biloba extract

Heptaminol chlorhydrate

Troxérutine

1987: Ginkor Procto®

1988: Ginkor Fort®

Start marketing products of natural origin.

Primary care

14

70’s 70’s

IPSEN background

1972

Indications: Cognitive disordersAge-related cognitive disorders (excepted Alzheimer’s disease)

Anti-ischemic (atreritis, Raynaud’s phenomenon)

cochleovestibular disorders

Tanakan®

Active substances:EGb 761® (Ginkgo biloba standardized extract)

Start marketing products of natural origin.

Primary care

15

70’s 70’s

IPSEN background

1977

Indications: Gastroenterology

Digestive coating (pain of œsopagus, stomach, duodenum and colon)

Acute and chronic diarrhea

Smecta®Active substances:

diosmectite (clay)

Active substances: montmorillonite beidellitique (clay)

Indications: Gastroenterology Digestive coating Symptomatic treatment of functionnal

colopathies

1980

Start marketing products of natural origin.

Primary care

Bedelix®

16

90’s 90’s

IPSEN background

1996

Indications: Gastrointestinal constipation (adults and children)

Forlax®

Active substances: Macrogol 4000 (polyethylène glycol 4000)

Primary care

17

Start in research

• Albert beaufour : biotechnology research

Biomeasure Boston A. Beaufour research institute : peptide focused engineering

• Research relations with american universities.

1976

18

80’s 80’s

IPSEN backgroundInterest in specialized therapies

Targeted therapy

1980

Partnership with

• Launch of Decapeptyl ®(1986)

• International development

Decapeptyl® 1mois (1995)

Decapeptyl® 3mois (1996)Decapeptyl® 6mois (2009, november)

Active substances: triptoreline (GnRH agonist)

Indications: OncologyProstate cancerUterin fibroidsEndometriosisEarly-onset puberty Female infertility

19

90’s 90’s

IPSEN background

1994

Dysport®

Interest in specialized therapies

Active substances: botilium neurotoxin,type A toxin-haemagglutinin complex.

Indications: Neuromuscular hemifacial spasticityCervical dystonia blepharospasm (glabellaires wrinkles)

Purchase of KEYWOOD (UK)

> 75 countries

Targeted therapy

20

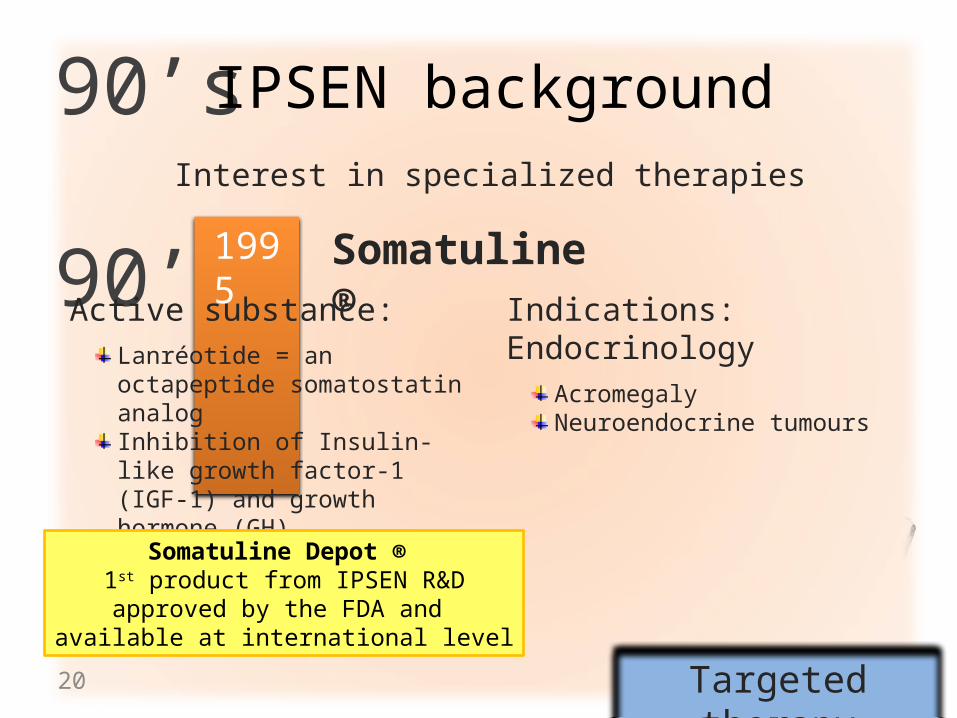

90’s 90’s

IPSEN backgroundInterest in specialized therapies

1995

Somatuline®Active substance:

Lanréotide = an octapeptide somatostatin analog Inhibition of Insulin-like growth factor-1 (IGF-1) and growth hormone (GH).

Indications: EndocrinologyAcromegalyNeuroendocrine tumours

Somatuline Depot ® 1st product from IPSEN R&Dapproved by the FDA and

available at international level

Targeted therapy

21

90’s 90’s

Family businessDisagreements beetwen Albert and Gerard, at last Albert bought Gerard’s parts (50%)

Still an independent family company

Progressively, Stephane Francois, son-in-law of Albert, has more importance.

1996

IPSEN background

22

90’s 90’s

IPSEN backgroundDeath of Albert. Stephane Francois is renowned CEO,but Anne and Henri Beaufour don’t agree with that.

Stephane Francois is fired.

2001

2002

Welcome to Jean-Luc Bélingard !

23

New team

J.L Bélingard •Chairman and Chief Executive Offi cer.•Delegate General and spokesman for G5

1999-2001, he was a member of theExecutive Board and CEO of BioMérieux-Pierre Fabre.

Anne Beaufour Director bachelor’s degree in geology.director of the Company since 1998.

Henri Beaufour Director Bachelor of arts degree.Since 2003,manager of Camilia Holding (LXB)

Claire Giraut 2003: ChiefFinancial Offi cer

member of the ExecutiveBoard of the Technip Group

Eric Drapé Executive Vice-President, Manufacturing and Supply Organisation.

Senior Vice President of the company’s Diabetes Finished Products at Novo Nordisk

Jacques-Pierre Moreau

Executive Vice-President, Chief Scientifi c Offi cer

founded Biomeasure Incorporated,based near Boston

Frédéric Babin Executive Vice-President, Human Resources

Master of Business Law

Christophe Jean Group Vice-PresidentOperations

Chairman and CEO of Pierre Fabre Médicaments.

24

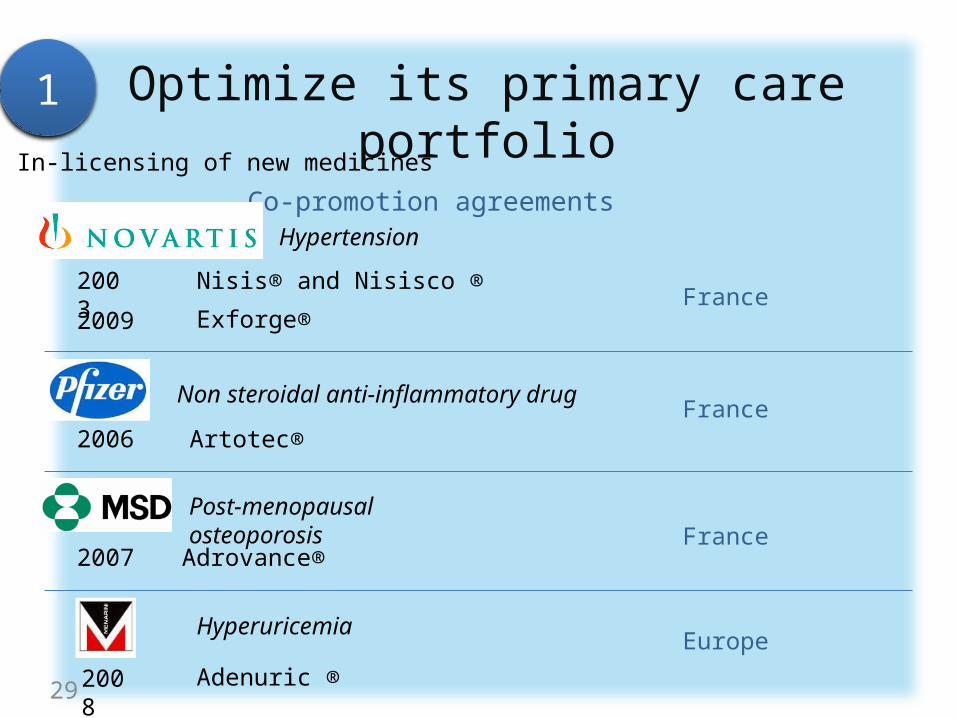

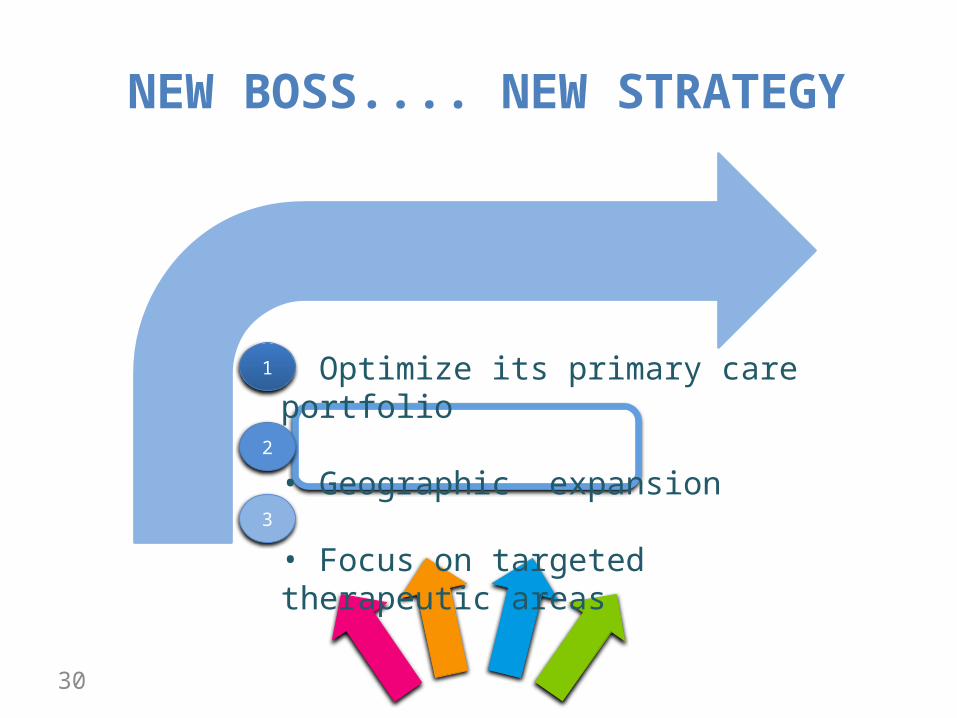

• Optimize its primary care portfolio

• Geographic expansion

• Focus on targeted therapeutic areas

NEW BOSS.... NEW STRATEGY

1

2

3

25

Optimize its primary care portfolio

Life Cycle Management to develop new indications or confirm the medical benefits of selected products

In-licensing of new medicines to sustain Ipsen’s primary care franchise

$$ $ $

CASH COW

R & D

1

26

Life cycle Management

Optimize its primary care portfolio

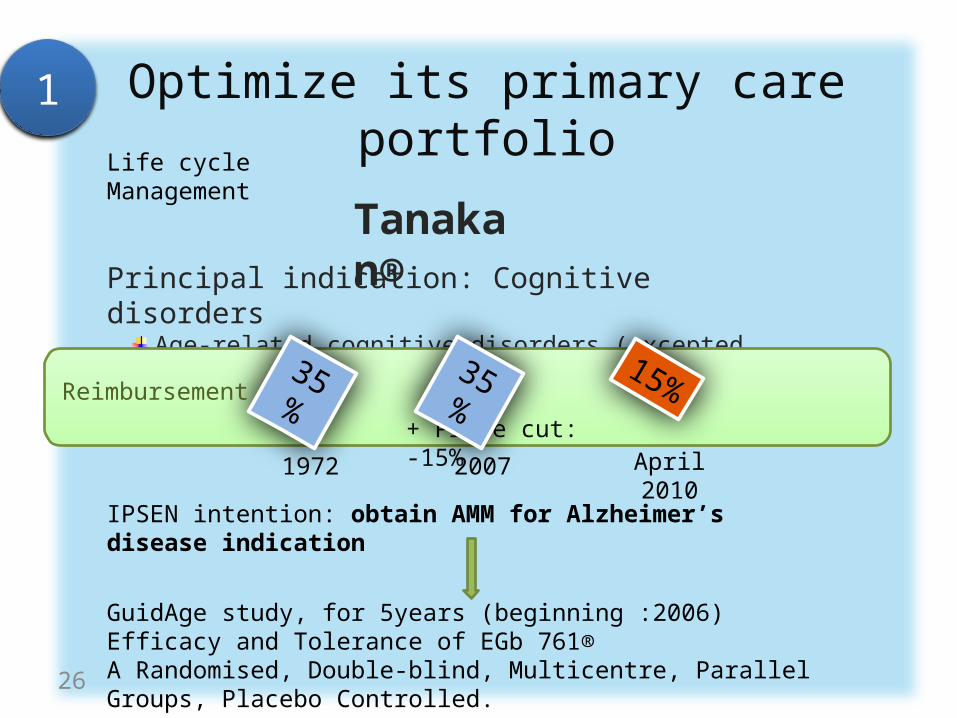

Tanakan®Principal indication: Cognitive disorders

Age-related cognitive disorders (excepted Alzheimer’s disease)

IPSEN intention: obtain AMM for Alzheimer’s disease indication

GuidAge study, for 5years (beginning :2006)Efficacy and Tolerance of EGb 761® A Randomised, Double-blind, Multicentre, Parallel Groups, Placebo Controlled.

1972

35%

2007 April 2010

15%Reimbursement

+ Price cut: -15%

35%

1

27

Life cycle Management

Optimize its primary care portfolio

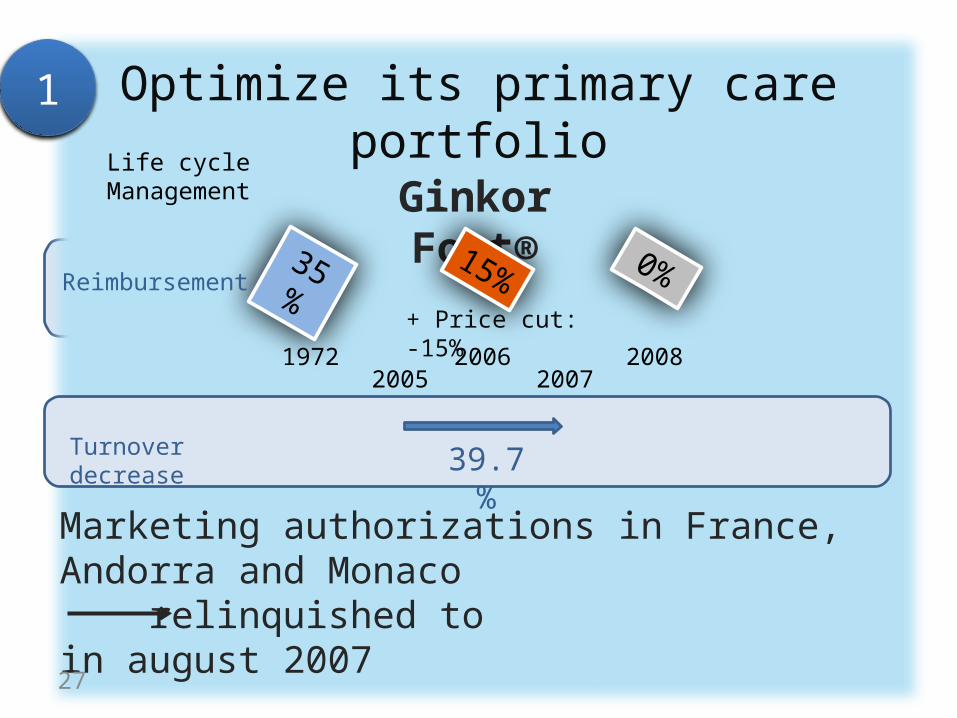

Ginkor Fort®

Marketing authorizations in France, Andorra and Monaco relinquished to in august 2007

1972

35%

2006 2008

15% 0%Reimbursement

20072005

Turnover decrease 39.7%

+ Price cut: -15%

1

28

Life cycle Management

Optimize its primary care portfolio

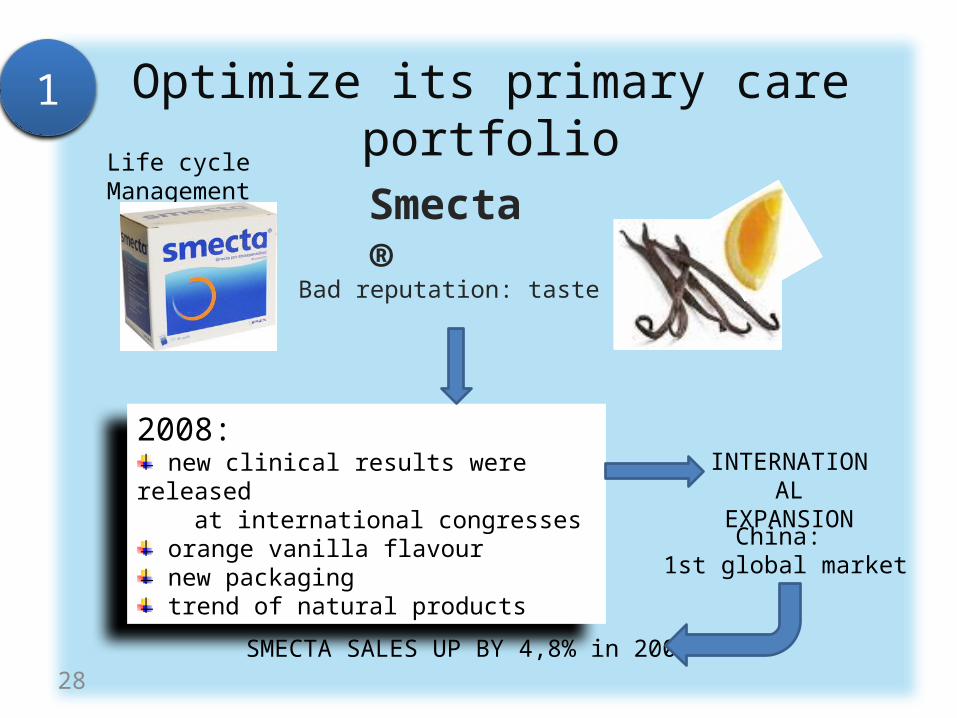

Smecta®

SMECTA SALES UP BY 4,8% in 2008

Bad reputation: taste

2008: new clinical results were released

at international congresses orange vanilla flavour new packaging trend of natural products

INTERNATIONAL EXPANSION

China: 1st global market

1

In-licensing of new medicines

Optimize its primary care portfolio

Co-promotion agreements

Nisis® and Nisisco ®2003

2009 Exforge®

Hypertension

Post-menopausal osteoporosis

2007 Adrovance®

Non steroidal anti-inflammatory drug

Artotec®2006

2008 Adenuric ®

Hyperuricemia

29

France

France

France

Europe

1

30

NEW BOSS.... NEW STRATEGY

• Optimize its primary care portfolio

• Geographic expansion

• Focus on targeted therapeutic areas

1

3

2

31

Geographic expansion

Country % variation 2008-2009

France - 3,2%

Spain 2,3%

Italia 3,3%

Germany 5,3%

UK - 1,1%

Major werstern european countries - 0,9%

Other european countries - 0,8%

North of America 307,1%

Rest of the world (BRIC) 20,8%

2

Big progression

Decrease reimbursement,

generics

32

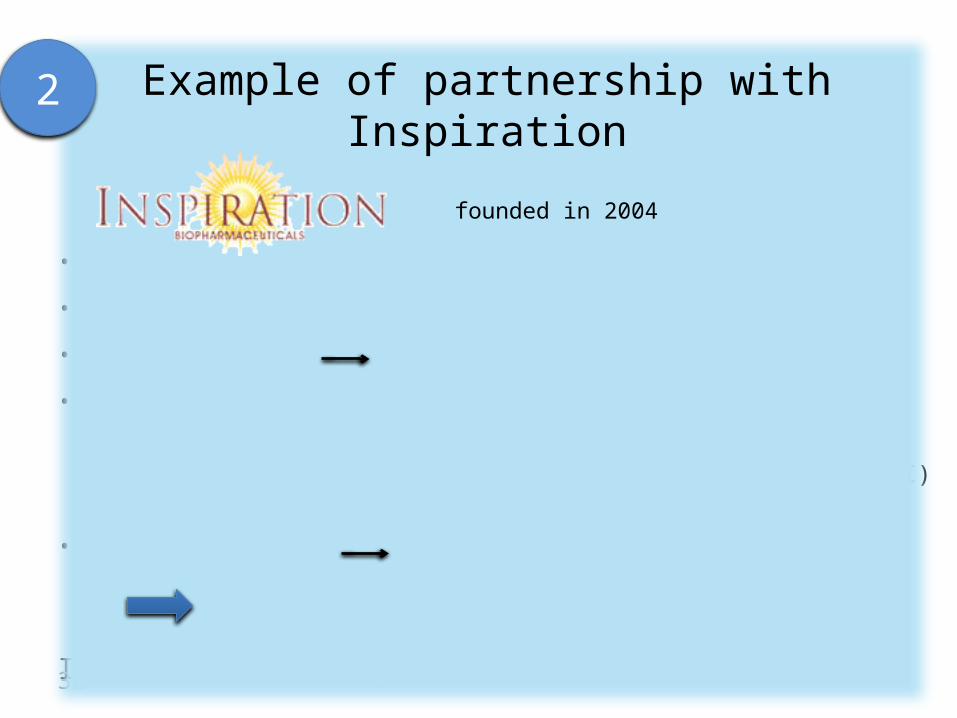

• mission: revolutionize treatment for hemophilia

• Wide portfolio in hemophilia and haemorrhage

• OBI-1 : porcine FVIII treatment of hemophilia A

• Reminder: Hemophilia A = deficit in FVIII controlled by injections of human FVIII ( 2 – 3t/ week)

Pb: 1/3 of cases, immune reaction (Ac anti human FVIII) preventing reinjection of human FVIII

• So OBI-1 : porcine origin low cross-reactivity to Ac anti hFVIII

therapeutic benefit for these patients

IPSEN ambition: engage in a niche sector

Example of partnership with Inspiration

founded in 2004

2

33

Example of partnership with Inspiration

Sublicence OBI-1

IPSEN INSPIRATION

50 M$ + 27,5 % sales50M $ in cash or convertible bond

85 M$ financing85 M$ =

initial investmen

tShares

representing 20% of Ins.

equity

1 member of IPSEN in Board of

directors of Inspiration

Until 174 M$ Based on the successful

development of OBI-1 & IB10011 convertible bond

into equity/payment

259 M$ of funding for

development and

marketing of its

portfolio in hemophilia

IPSEN could hold up to 47% of Inspiration equity!

OBI-1: porcine F VIII belongs

IPSEN

2

34

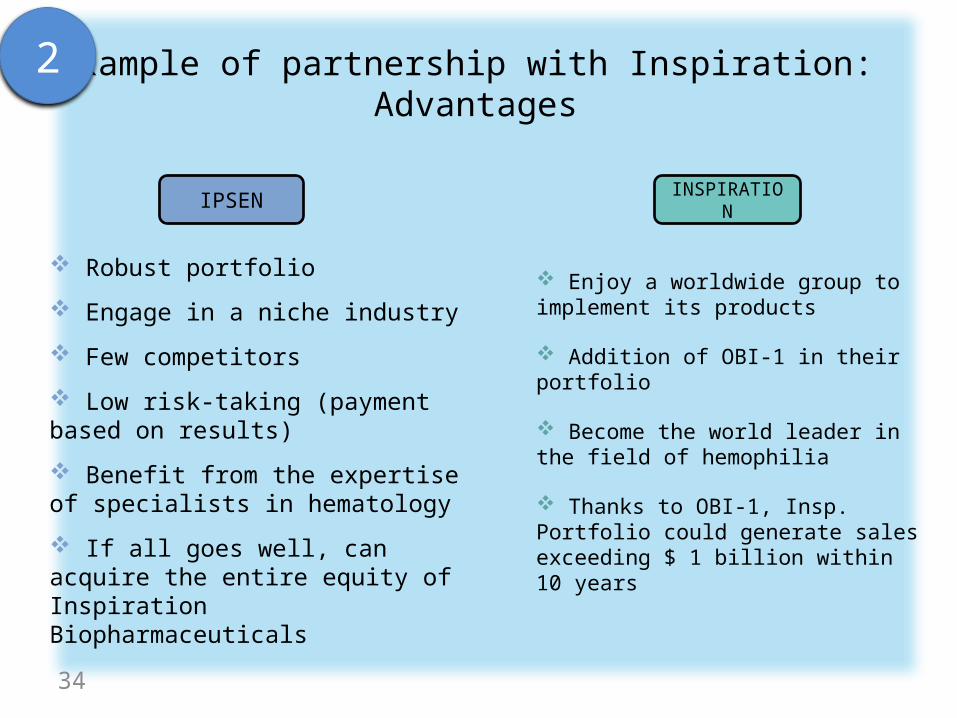

Example of partnership with Inspiration: Advantages

IPSEN INSPIRATION

Robust portfolio

Engage in a niche industry

Few competitors

Low risk-taking (payment based on results)

Benefit from the expertise of specialists in hematology

If all goes well, can acquire the entire equity of Inspiration Biopharmaceuticals

Enjoy a worldwide group to implement its products

Addition of OBI-1 in their portfolio

Become the world leader in the field of hemophilia

Thanks to OBI-1, Insp. Portfolio could generate sales exceeding $ 1 billion within 10 years

2

35

Realize partnership permits to IPSEN:

– sell products that are not in its field (little knowledge)

– engage with partners only if it can make a profit

– eventually buy out his partner / no longer care

So …2

36

Partnership with Medicis and Galderma

Botulinum neurotoxin, type A, bought from Octagen.

Therapeutic indications: hemifacial spasticitycervical dystonia blepharospasm

Esthetic indication: glabellaires wrinkles

Keeps its rights

Partnerships

Market estimated to $ 760 – 800 M

BUTNot part of Ipsen’s

expertise

2

37

Partnership with Medicis and Galderma

USA, Canada and JapanUE, Russia, East Europe,

Central Asia, Israël, Liban.

Developpement, distribution and market rights

$ 90.1 M

$ 26.5 M

$ 75 M

$ 2 M

$ 35 M

$ 228.6 M

30% of turnover

2006, until 2036

Developpement, distribution and promotion rights

Supplies. Fixed price. Supplies.

Fixed price.

2007, until 2019

$ 10M

$ 20M

$ X M 40% of turnover

Min $ 30 M

2

38

Be sure to sell its product for a long period of time

Reach unknown markets throughlocally well-known partners

Develop a product which is already well-known as a medecine No bad surprises, less risky

Be sure to be supplied

Partnership with Medicis and GaldermaAdvantages

IPSENGALDERMA

MEDICIS

2

39

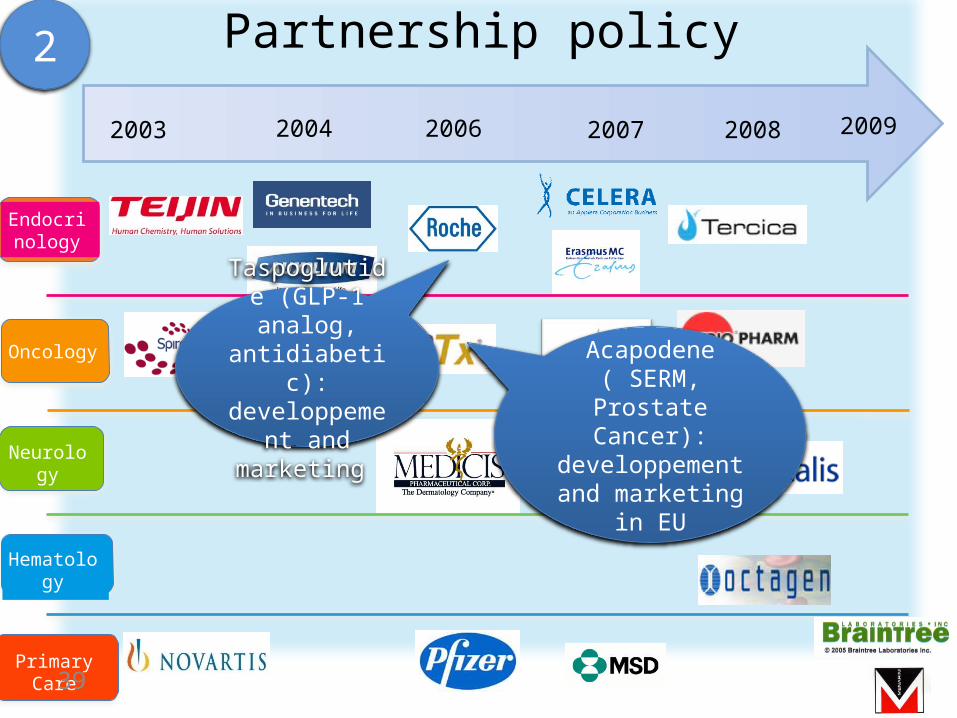

2003 2004 2006 2007

Endocrinology

Oncology

Neurology

Primary Care

2008

Partnership policy

Hematology

2009

Taspoglutide (GLP-1 analog, antidiabetic):

developpement and marketing

Acapodene ( SERM, Prostate Cancer):

developpement and marketing in EU

2

40

• Optimize its primary care portfolio

• Geographic expansion

• Focus on targeted therapeutic areas

NEW BOSS.... NEW STRATEGY

1

2

3

41

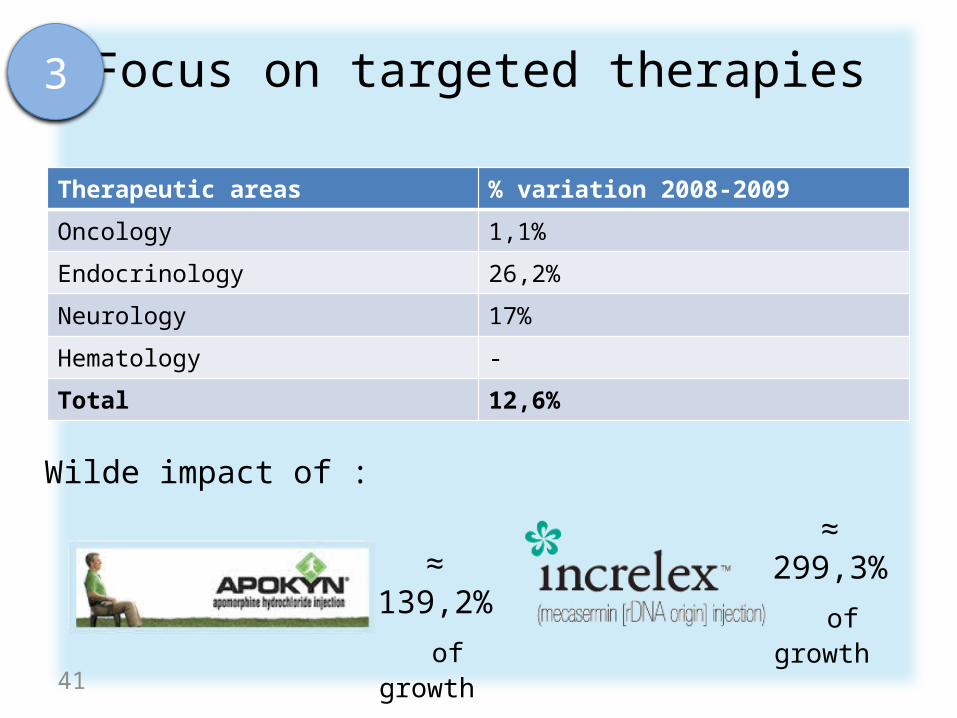

Focus on targeted therapies

Therapeutic areas % variation 2008-2009

Oncology 1,1%

Endocrinology 26,2%

Neurology 17%

Hematology -

Total 12,6%

≈ 299,3%

of growth

Wilde impact of :

≈ 139,2%

of growth

3

42

R&D

Early commitment, since 1969

More 800 personnes in R&D

About 20% of CA for R&D every year

Currently 20 programs

3

43

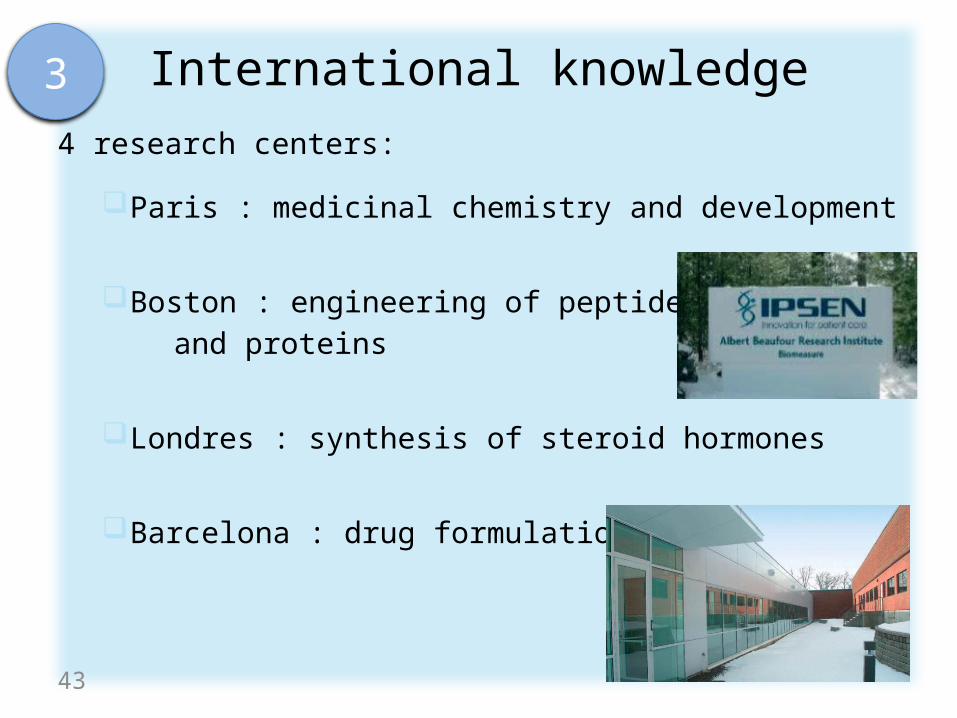

International knowledge4 research centers:

Paris : medicinal chemistry and development

Boston : engineering of peptides and proteins

Londres : synthesis of steroid hormones

Barcelona : drug formulation

3

44

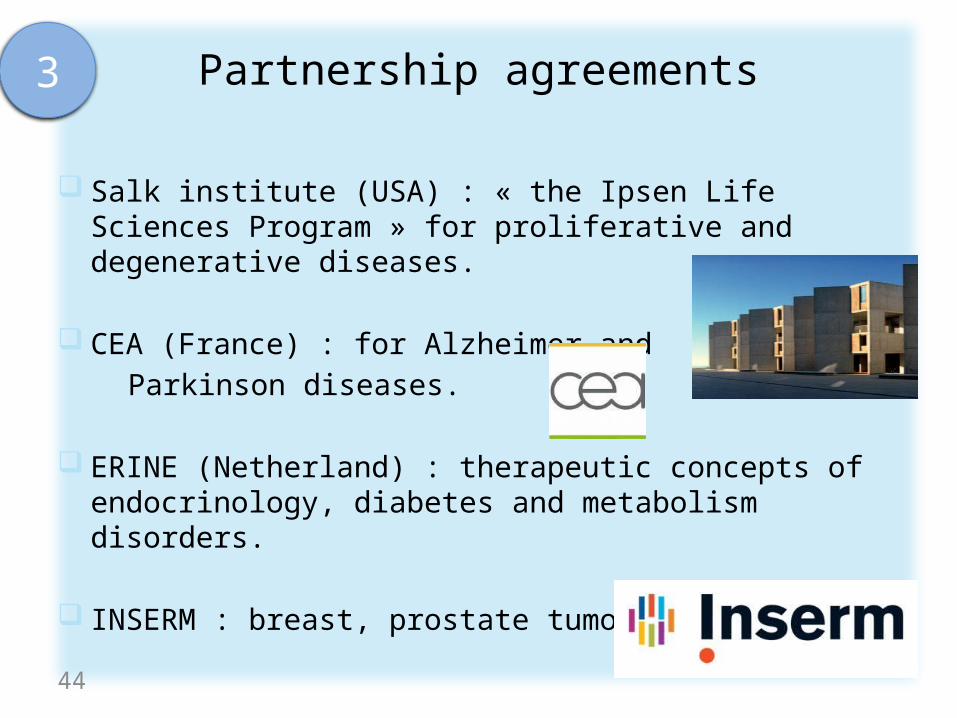

Partnership agreements

Salk institute (USA) : « the Ipsen Life Sciences Program » for proliferative and degenerative diseases.

CEA (France) : for Alzheimer and Parkinson diseases.

ERINE (Netherland) : therapeutic concepts of endocrinology, diabetes and metabolism disorders.

INSERM : breast, prostate tumors

3

45

Pipeline

Their identity

3

46

Oncology :

Angiomates : anticancer agent, anti-angiogenic acquisition of Sterix

BIM 46187 : Cell signalisation, G-protein signal for prostate and lung cancer

Cd25 inhibitors phosphatases : regulation of cell cycleLicencied out to Debiopharm for world exclusive right

Preclinical3

47

Endocrinology :

MSH agonists for the MC4 receptor : metabolic disorders like obesity

Ghrelin agonists (BIM28131) : regulation of food intake and gastro intestinal function and treatment of cachexia

Preclinical

Inhibitor of 11βHSB : for metabolic disorders

NutropinAp® : treatment of growth failure, new formulation for prolonged release

Life cycle management

3

Growingmarkets

48

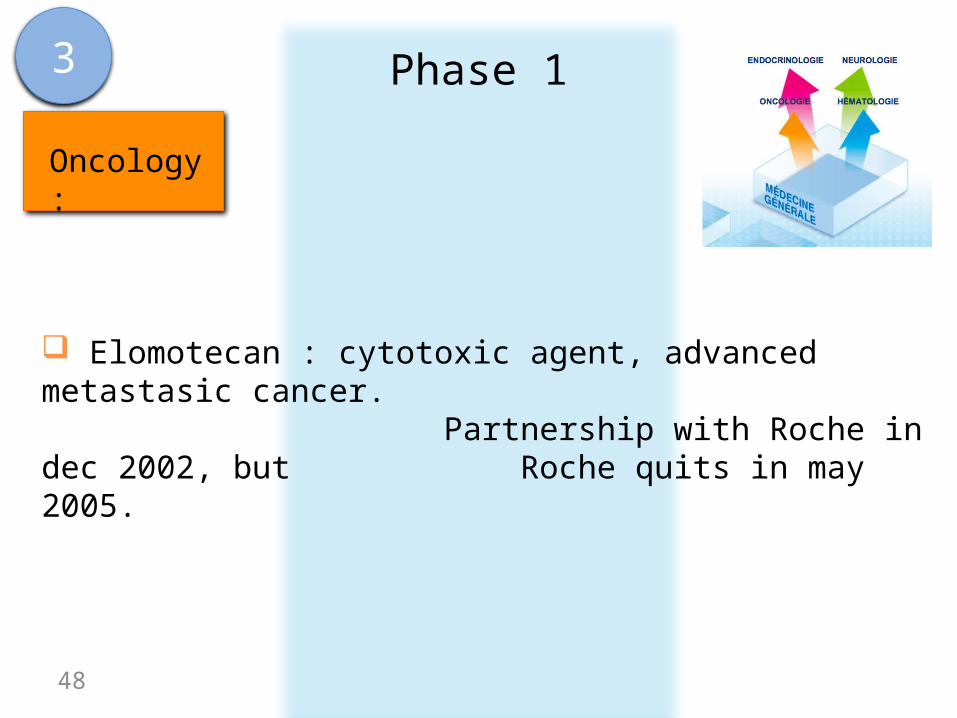

Phase 1

Oncology :

Elomotecan : cytotoxic agent, advanced metastasic cancer. Partnership with Roche in dec 2002, but

Roche quits in may 2005.

3

49

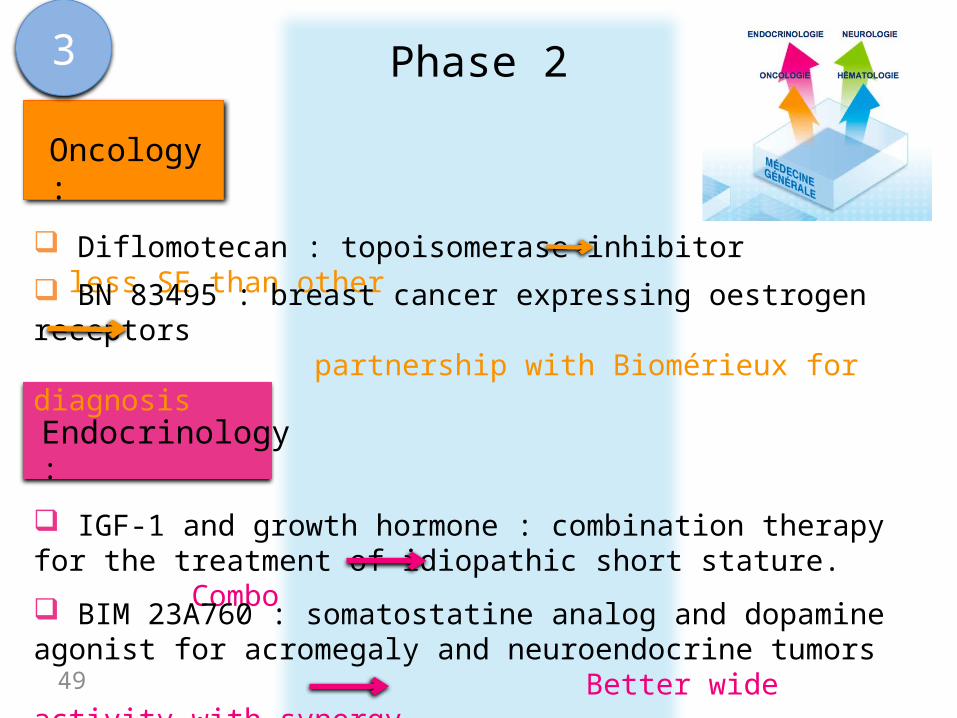

Phase 2

Oncology :

Diflomotecan : topoisomerase inhibitor less SE than other

Endocrinology :

IGF-1 and growth hormone : combination therapy for the treatment of idiopathic short stature. Combo

BIM 23A760 : somatostatine analog and dopamine agonist for acromegaly and neuroendocrine tumors

Better wide activity with synergy

BN 83495 : breast cancer expressing oestrogen receptors partnership with Biomérieux for diagnosis

3

50

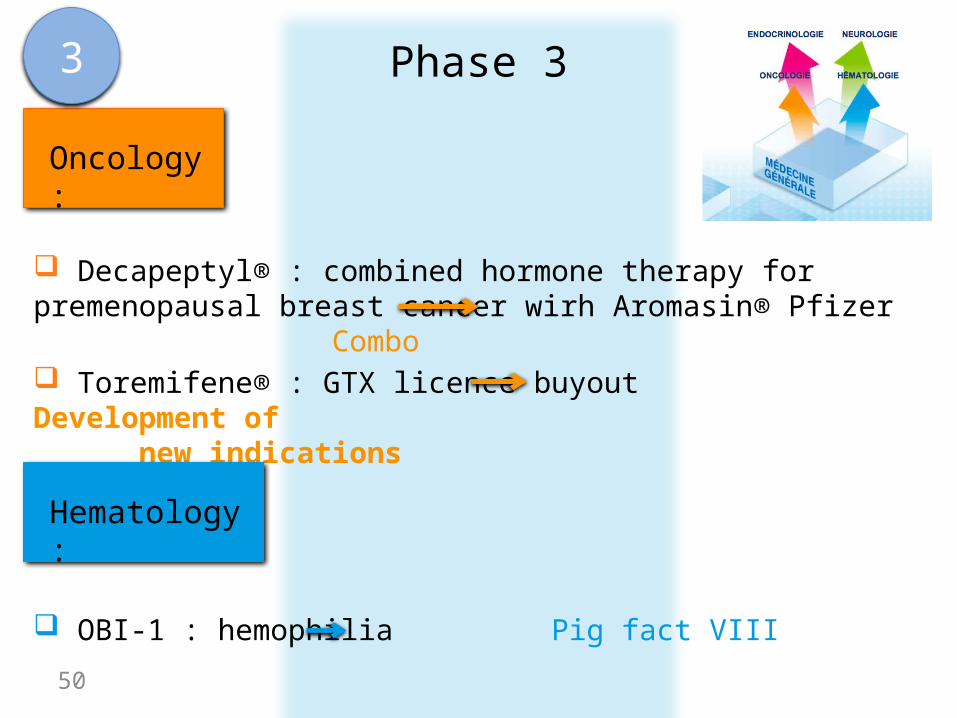

Phase 3

Oncology :

Decapeptyl® : combined hormone therapy for premenopausal breast cancer wirh Aromasin® Pfizer Combo

Toremifene® : GTX licence buyout Development of new indications

Hematology :

OBI-1 : hemophilia Pig fact VIII

3

51

Phase 3

Endocrinology :

Somatuline® Autogel®

Somatuline® Autogel®

Somatuline® Depot®

Increlex® : primary deficit in IGF-1 Global actor in the growth disorders

Taspoglutide : type 2 diabetes (partnership with Roche)

GLP1, third on the market

3

Life cycle management

52

Neurology :

Research program : new formulation for botulique toxin.

Implant on the world market of Dysport® with Galderma, and Medicis and of Apokin® with Vernalis buyout

3

53

New authorization in 2009

• Décapeptyl® 6months : launch in France.

• Dysport® : launch in USA for cosmetic and therapeutic indications.

• Azzalure® : marketing authorization in Spain, Germany, France and UK, and launch by Galderma.

3

54

Hematology

IPSEN gives itself the means of a strong and sustainable growth

EndocrinologyOnc

ology

Neur

olog

y

55

History of stockmarket

56

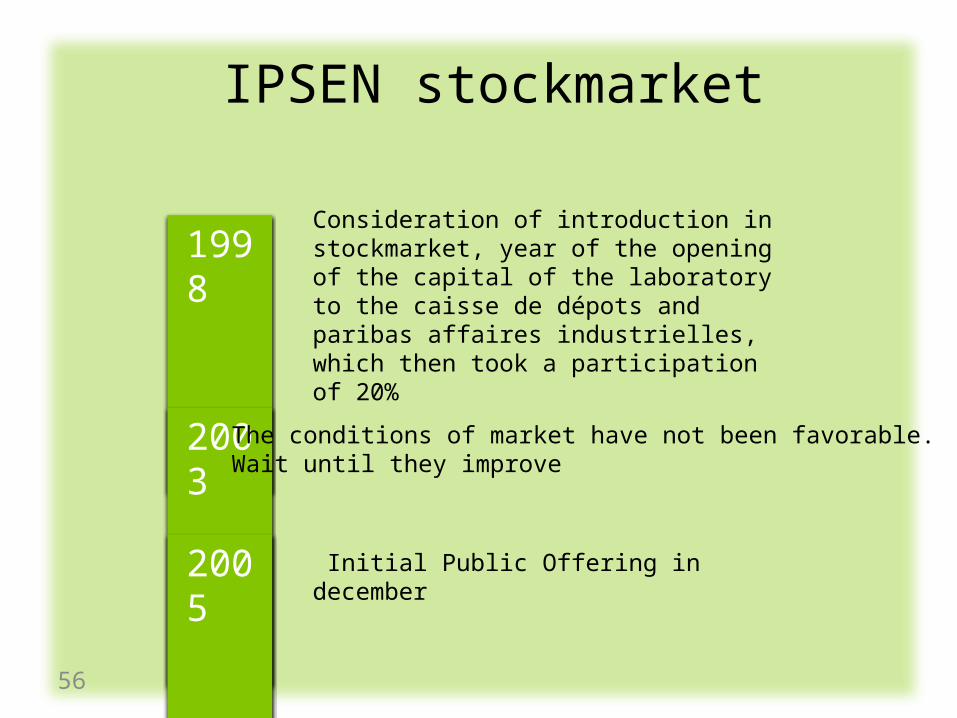

IPSEN stockmarket

1998

2003

Consideration of introduction in stockmarket, year of the opening of the capital of the laboratory to the caisse de dépots and paribas affaires industrielles, which then took a participation of 20%

Initial Public Offering in december2005

The conditions of market have not been favorable.Wait until they improve

57

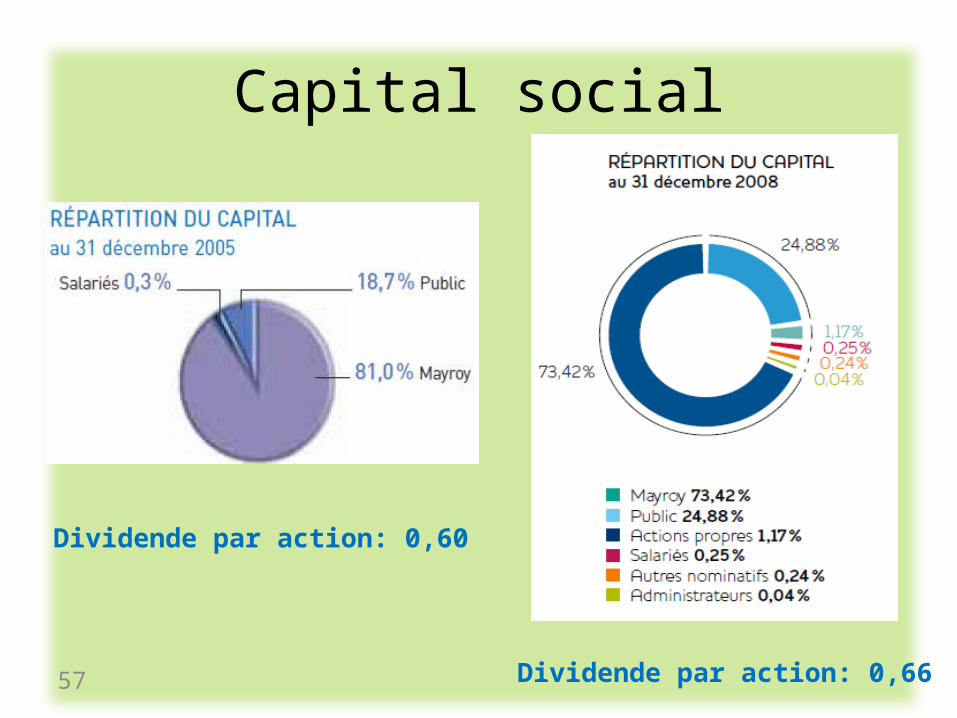

Capital social

Dividende par action: 0,60

Dividende par action: 0,66

58

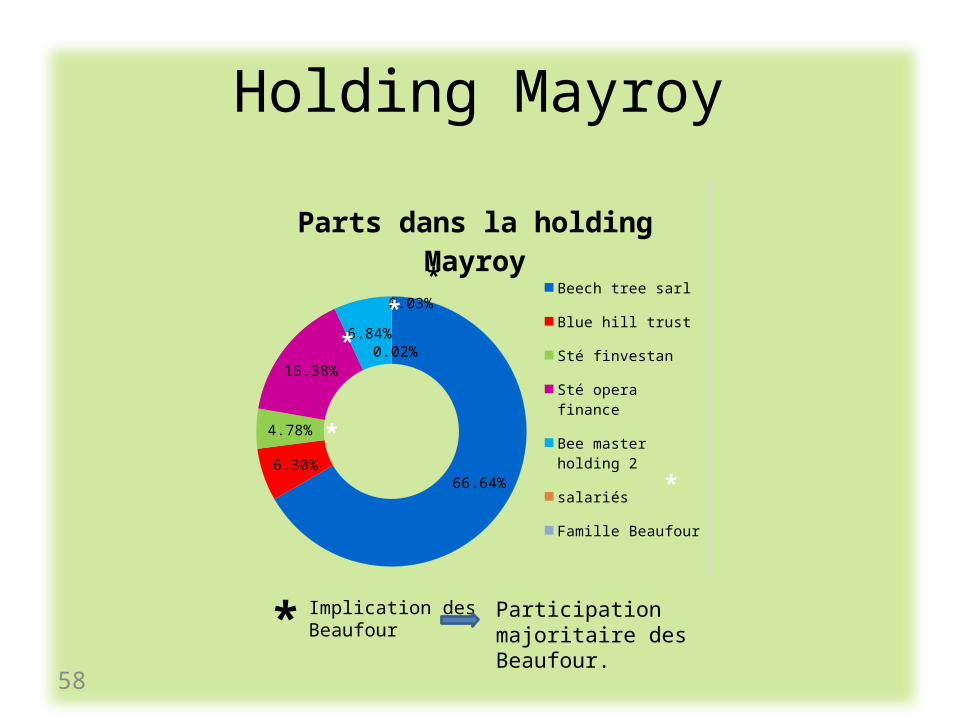

66.64%6.30%

4.78%

15.38%

6.84%0.02%

0.03%

Parts dans la holding Mayroy

Beech tree sarl

Blue hill trust

Sté finvestan

Sté opera finance

Bee master holding 2

salariés

Famille Beaufour

*

*

**

*

* Participation majoritaire des Beaufour.

Implication des Beaufour

Holding Mayroy

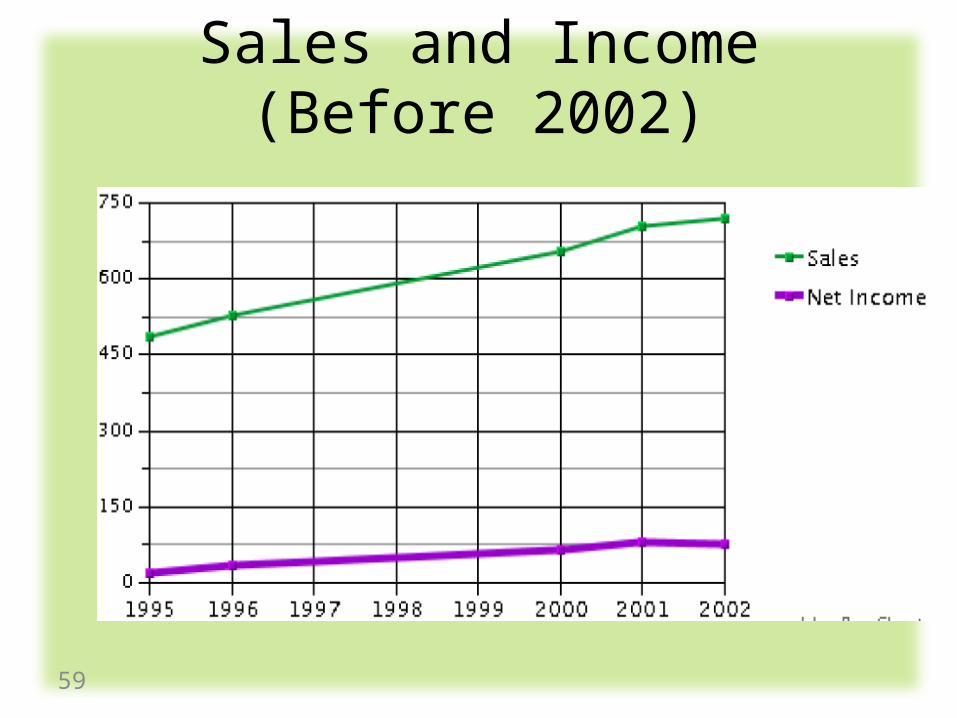

59

Sales and Income (Before 2002)

60

Sales and Income (2004-2008)

2004 2005 2006 2007 20080

200

400

600

800

1000

1200

SalesOperating incomeNet income

2004 2005 2006 2007 20080

200

400

600

800

1000

1200

SalesOperating incomeNet income

61

Changes in Stock Price

Number of shares: 84.105.633 .2005, December 7 : 22,20€ per share

Always above 22, 20€

62

Conclusion

63

SWOT analysisSTRENGHTS

• Independent firm

•Technology plateforms very competitives

• Strong R&D capabilities

• Numerous partnership agreements

• Life cycle management

• Family decision-making power

WEAKNESSES

• Weak sales in primary care

• Lack of critical size

OPPORTUNITIES

• Establishment of commercial presence in the US• Increasing presence in the emerging markets• A esthetic market : Botulinum toxin A

THREATS

• Generics

• End of reimbursement of cash cow

64

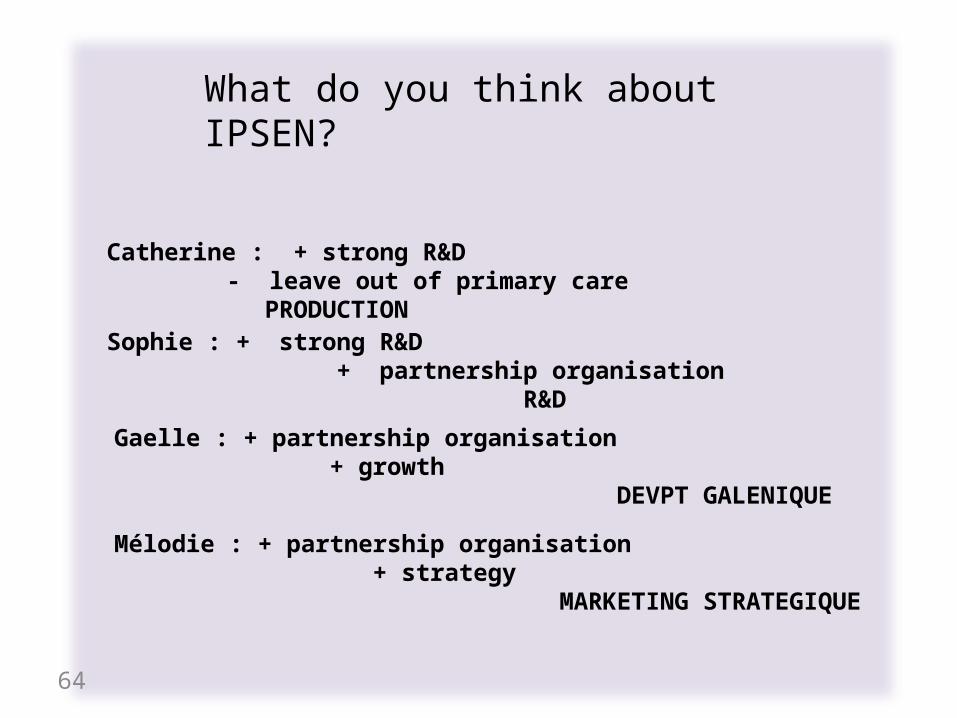

What do you think about IPSEN?

Catherine : + strong R&D - leave out of primary care PRODUCTION

Sophie : + strong R&D + partnership organisation R&D

Gaelle : + partnership organisation + growth DEVPT GALENIQUE

Mélodie : + partnership organisation + strategy MARKETING STRATEGIQUE

65

Thanks for your attention

Any questions ?

66

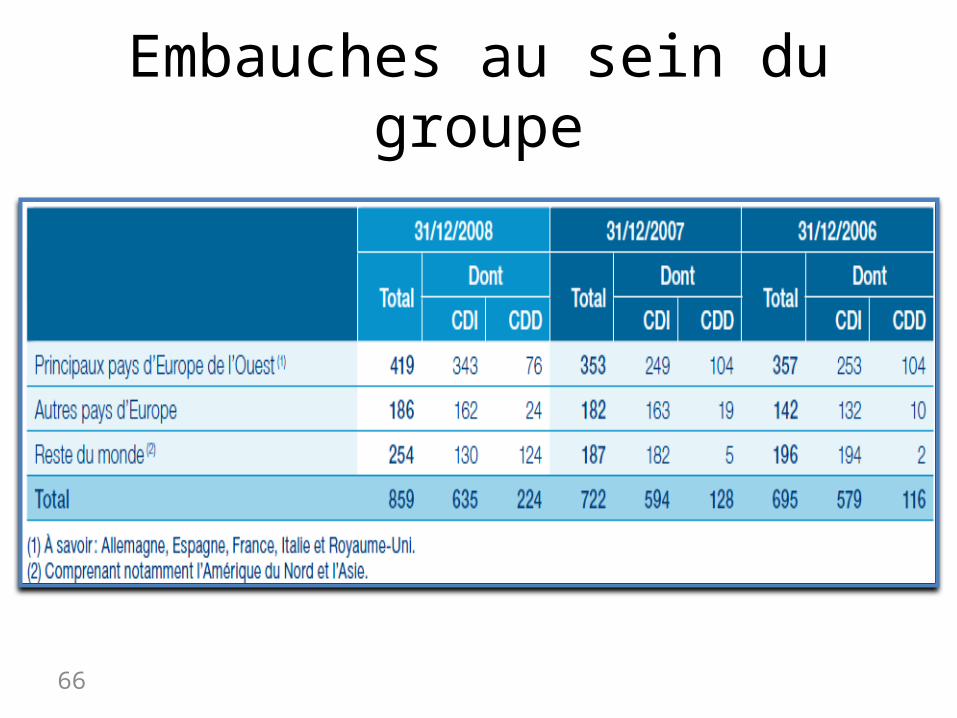

Embauches au sein du groupe

67

Partnership policy

→ Marketing licence for Nisis® & Nisisco®

→ R&D agreement and acquisition 20% of CA : new technologies

Jan 09: co-promotion agreement Exforge® in France

→ R&D agreement formulation growth hormone LP

→ marketing licence for Testim® in France

→ Development and marketing BIM 51077

Many partnership to enrich R&D portfolio and expand products range

→ development and marketing licence Acapodène® in UE

→ R&D collaboration : Market Ipsen’s products in Japan

Oct 09 : new agreement SG2000 (anticancer agent, 1st class)

68

Partnership policy

→ R&D agreement for development of pharmacogenomic tests for growth retardation

→ R&D agreement for development of innovative products in diabete, endocrinology and metabolism

→ R&D agreement for development of diagnostic test in breast cancer

→ co-marketing licence Adrovance® TM in France

→ definitive merger agreement

july 06: licence agreement Somatuline® Autogel®

→ marketing licence Triptoreline under several brandnames (Salvatyl LP®)

1983: 1st development and marketing licence Decapeptyl®

→ final purchase rights Apokyn® (PK)

→ development and marketing licence Toxine botulique (dysport®, Azzalure®)

69

Partnership policy

→ development and marketing licence BLI-800 : colic washing before coloscopy

→ exclusive right of licence for Menarini Adenuric®

→ purchase agreement, recovery of all actives related with OBI-1