Embed Size (px)

Citation preview

SONOMA COUNTY

JUNIOR COLLEGE DISTRICT

SANTA ROSA, CALIFORNIA

FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT

YEAR ENDED JUNE 30, 2010

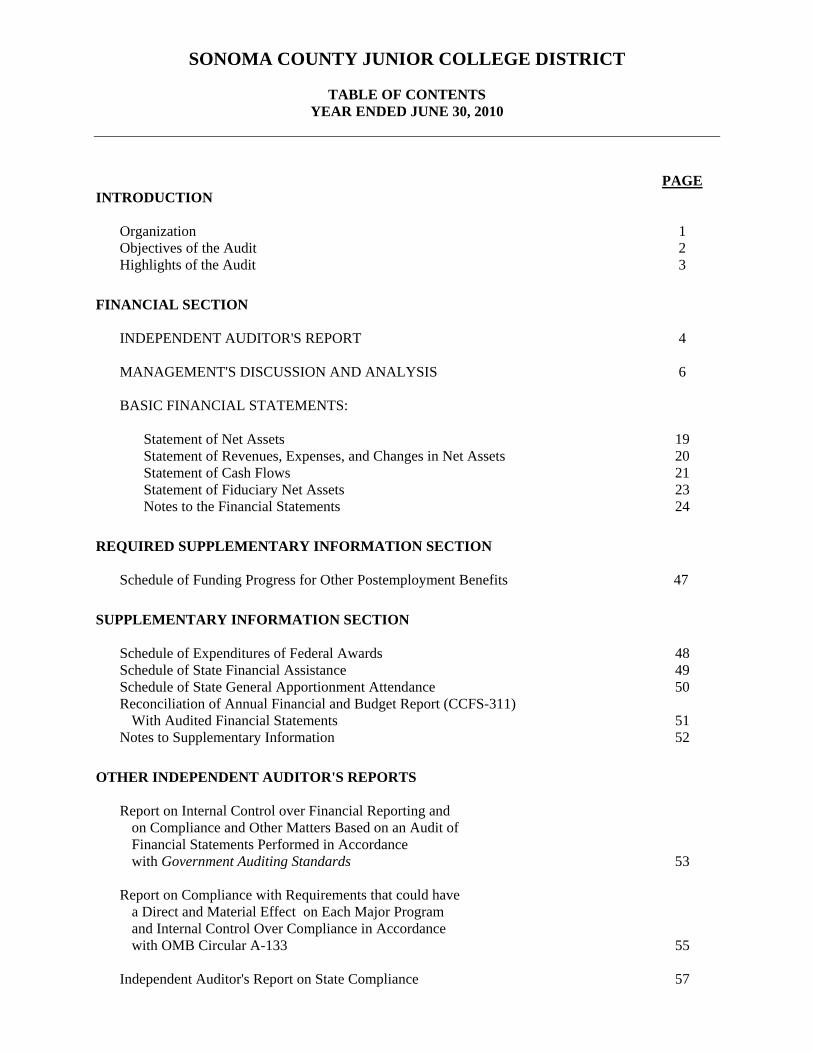

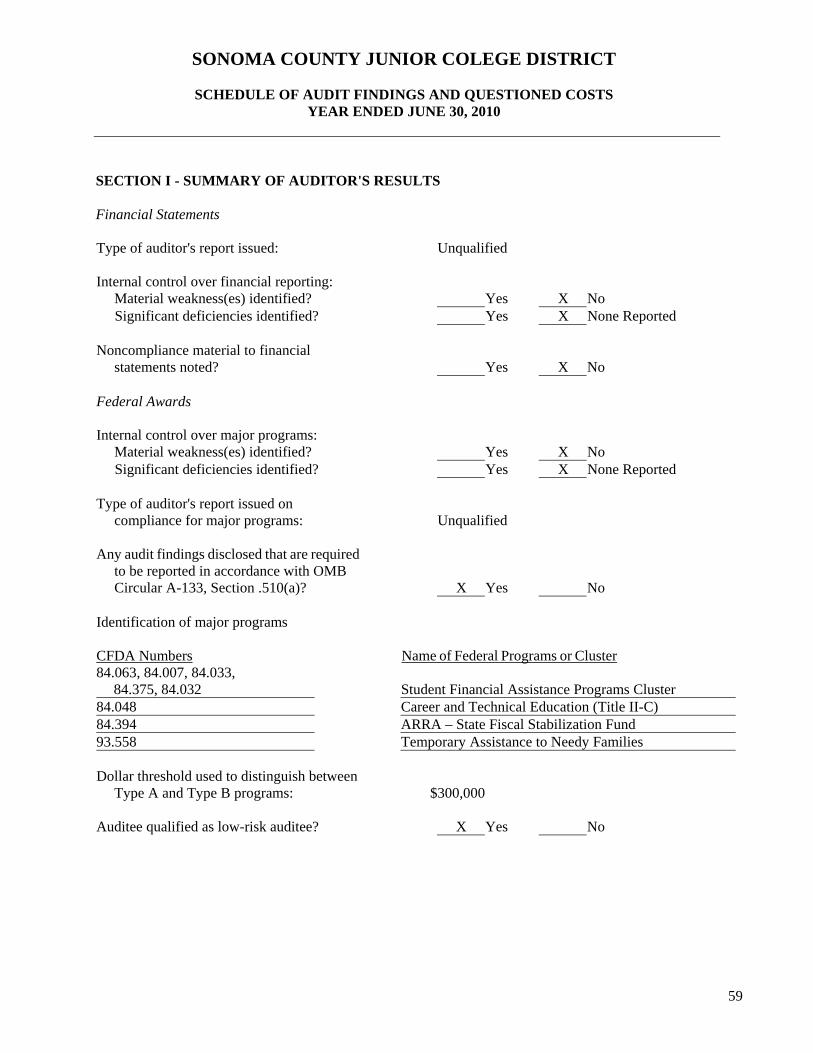

SONOMA COUNTY JUNIOR COLLEGE DISTRICT TABLE OF CONTENTS YEAR ENDED JUNE 30, 2010

PAGE INTRODUCTION Organization 1 Objectives of the Audit 2 Highlights of the Audit 3

FINANCIAL SECTION

INDEPENDENT AUDITOR'S REPORT 4 MANAGEMENT'S DISCUSSION AND ANALYSIS 6 BASIC FINANCIAL STATEMENTS:

Statement of Net Assets 19 Statement of Revenues, Expenses, and Changes in Net Assets 20 Statement of Cash Flows 21 Statement of Fiduciary Net Assets 23 Notes to the Financial Statements 24

REQUIRED SUPPLEMENTARY INFORMATION SECTION

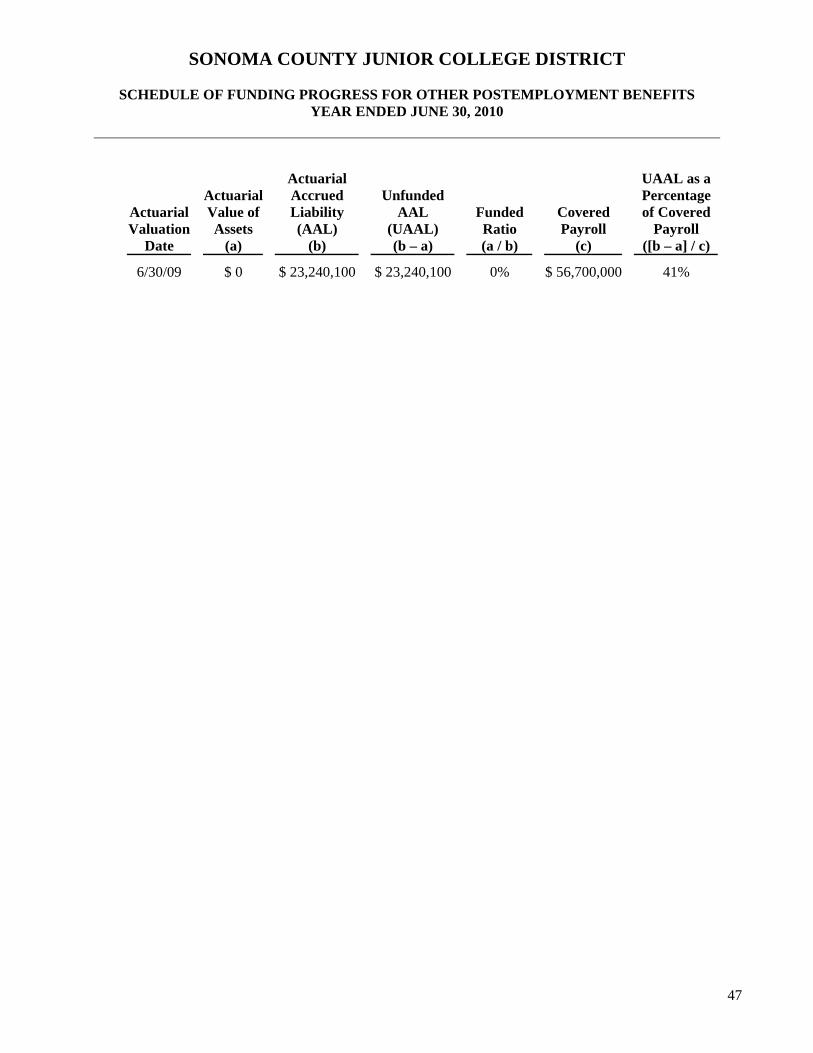

Schedule of Funding Progress for Other Postemployment Benefits 47

SUPPLEMENTARY INFORMATION SECTION

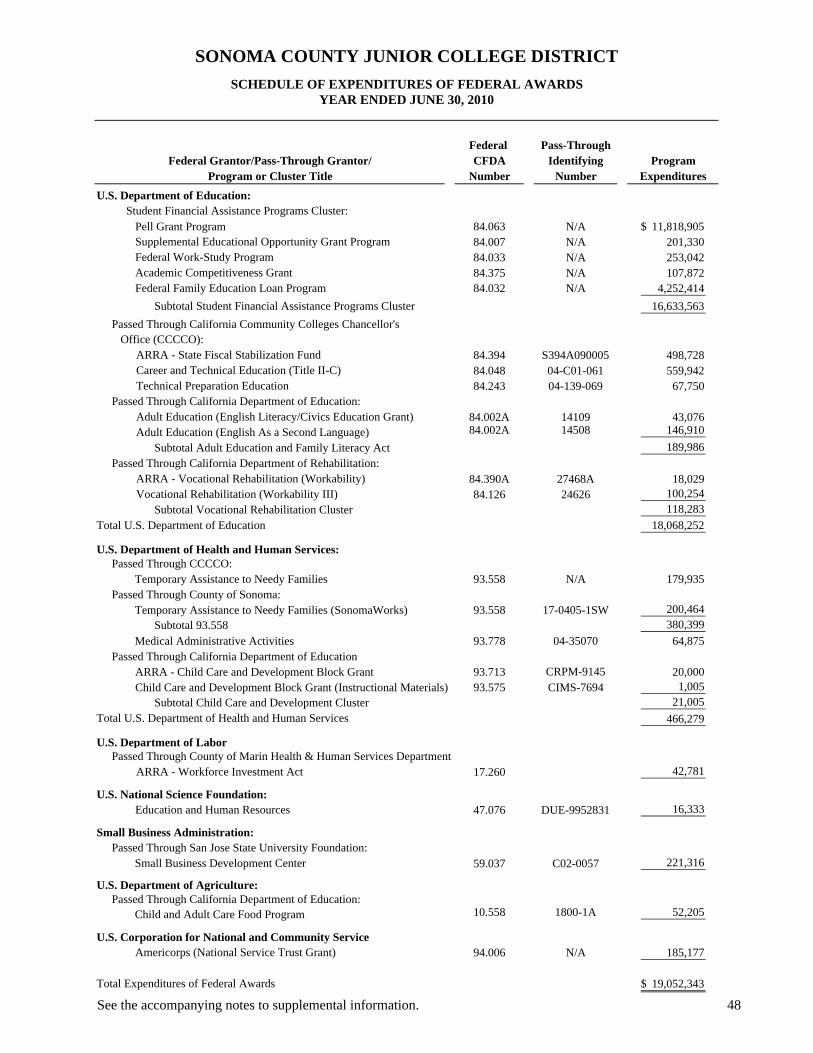

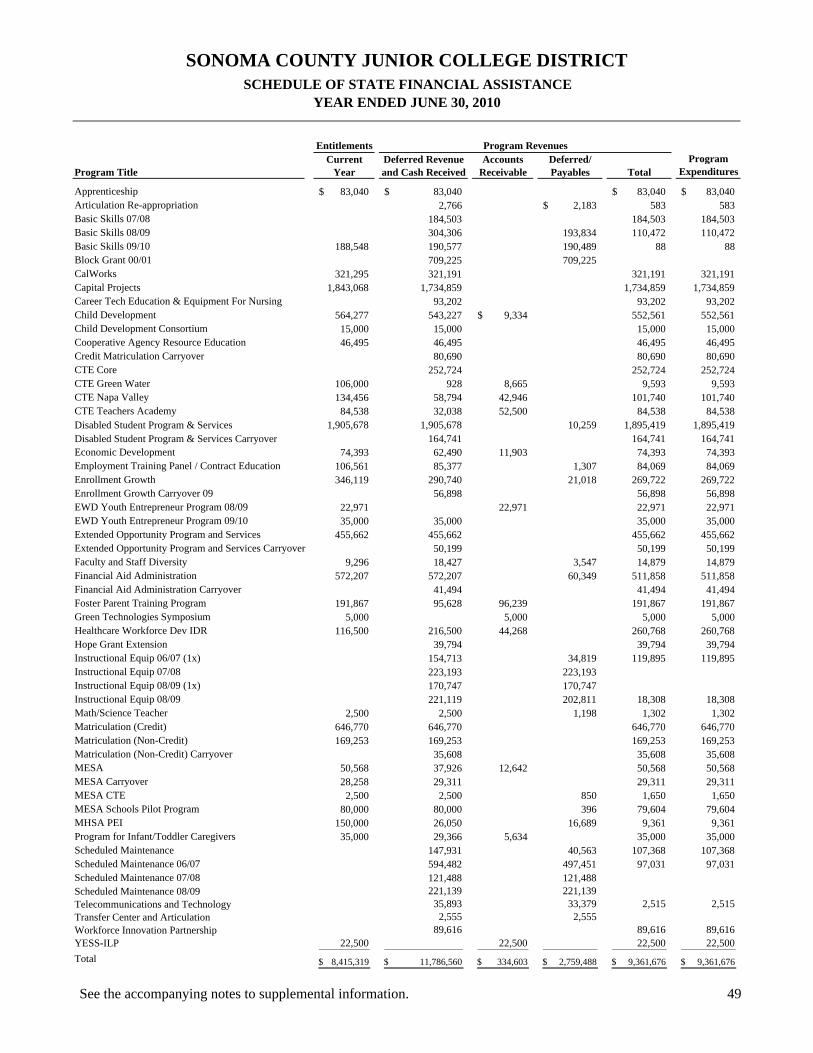

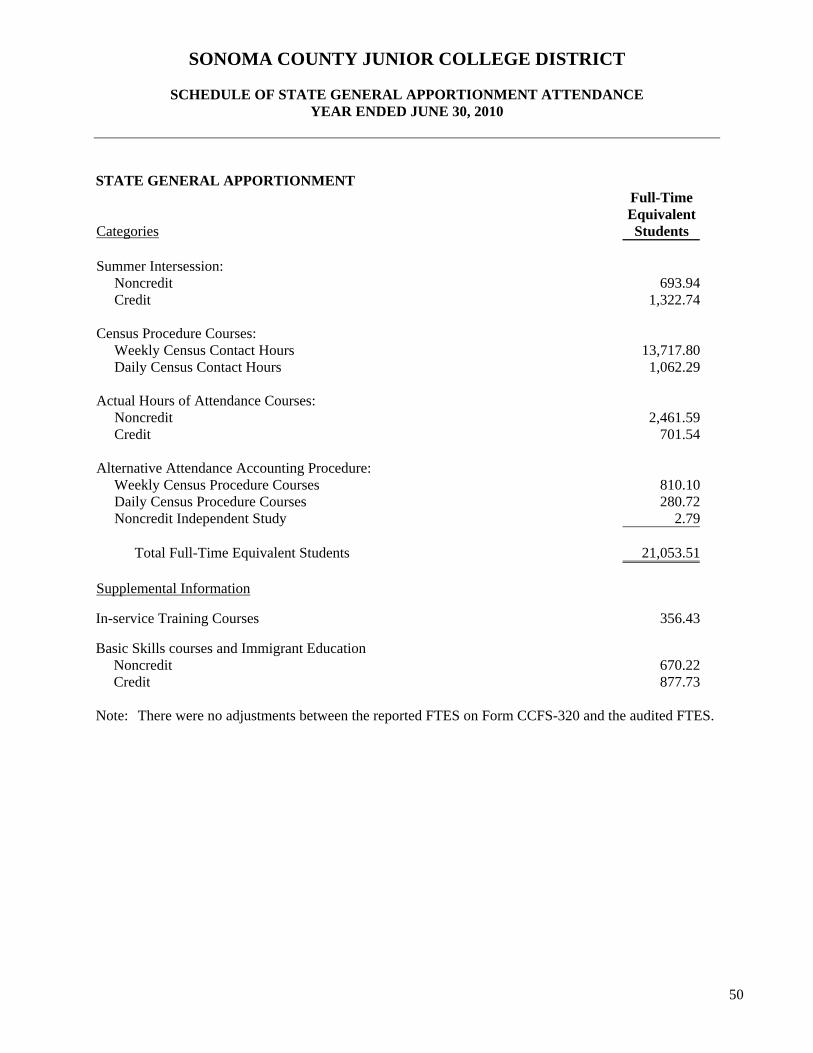

Schedule of Expenditures of Federal Awards 48 Schedule of State Financial Assistance 49 Schedule of State General Apportionment Attendance 50 Reconciliation of Annual Financial and Budget Report (CCFS-311) With Audited Financial Statements 51 Notes to Supplementary Information 52

OTHER INDEPENDENT AUDITOR'S REPORTS

Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 53

Report on Compliance with Requirements that could have

a Direct and Material Effect on Each Major Program and Internal Control Over Compliance in Accordance with OMB Circular A-133 55

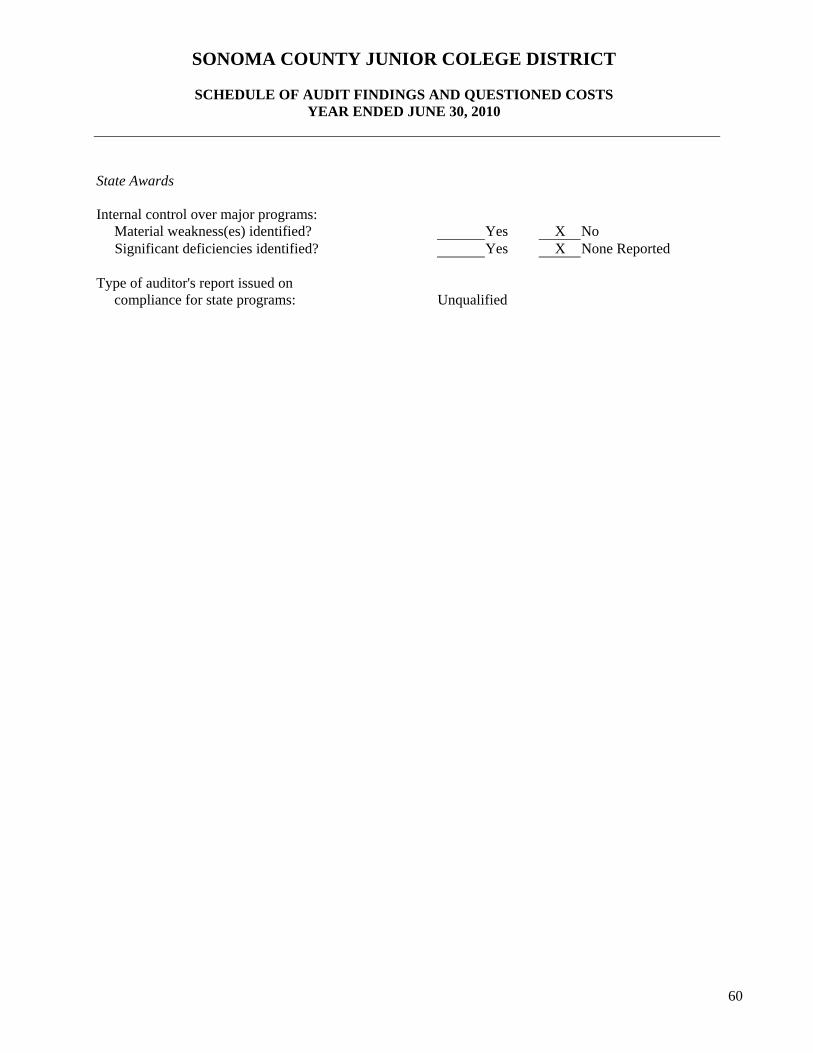

Independent Auditor's Report on State Compliance 57

SONOMA COUNTY JUNIOR COLLEGE DISTRICT TABLE OF CONTENTS YEAR ENDED JUNE 30, 2010

FINDINGS AND RECOMMENDATIONS SECTION

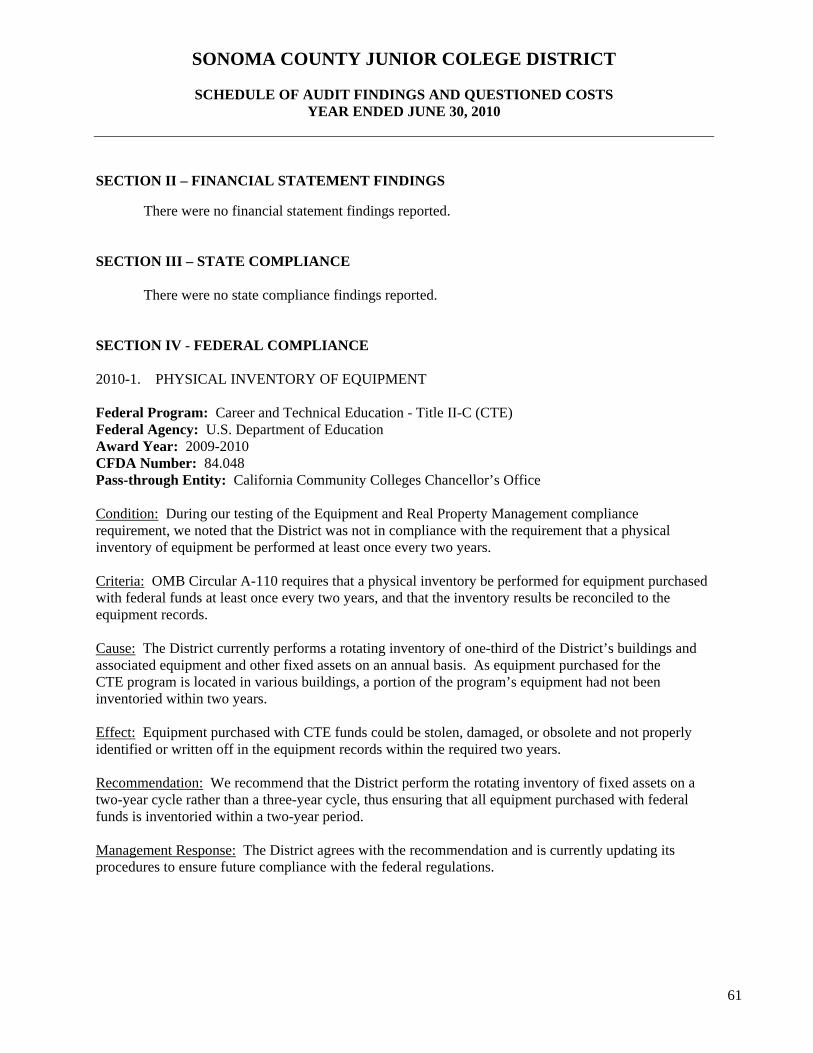

Schedule of Audit Findings and Questioned Costs 59 Status of Prior Year Findings and Recommendations 62

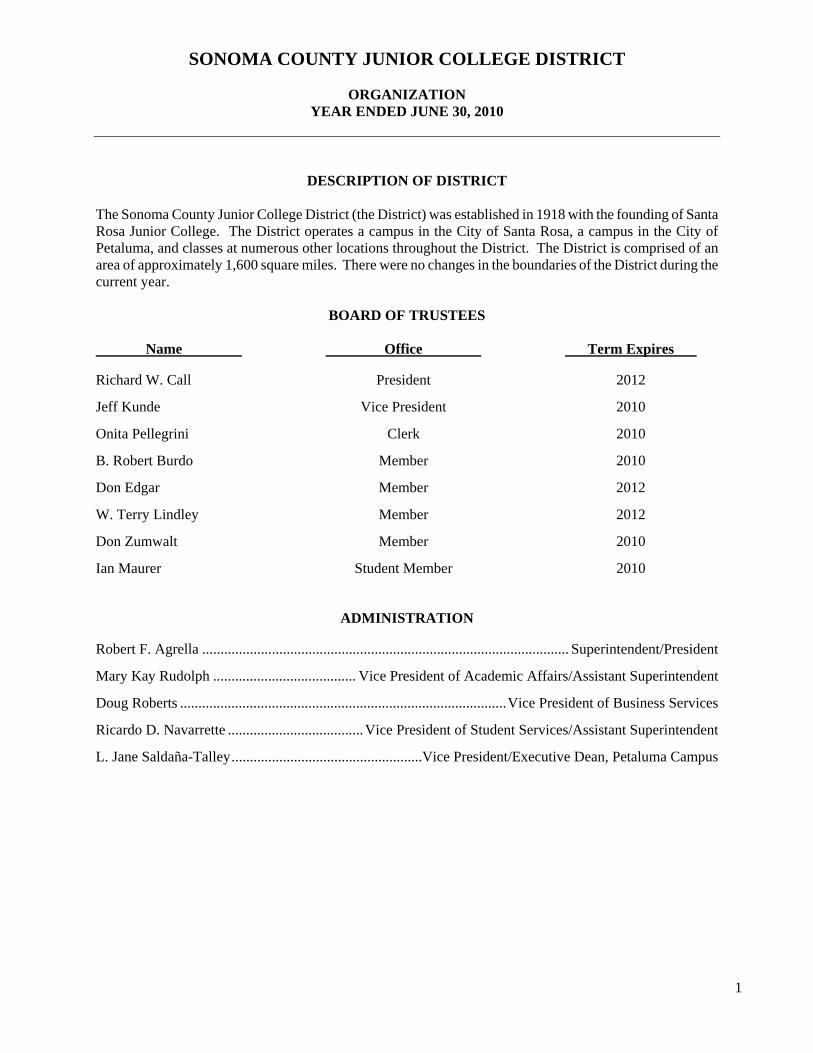

SONOMA COUNTY JUNIOR COLLEGE DISTRICT ORGANIZATION YEAR ENDED JUNE 30, 2010

1

DESCRIPTION OF DISTRICT The Sonoma County Junior College District (the District) was established in 1918 with the founding of Santa Rosa Junior College. The District operates a campus in the City of Santa Rosa, a campus in the City of Petaluma, and classes at numerous other locations throughout the District. The District is comprised of an area of approximately 1,600 square miles. There were no changes in the boundaries of the District during the current year.

BOARD OF TRUSTEES Name Office Term Expires Richard W. Call President 2012 Jeff Kunde Vice President 2010 Onita Pellegrini Clerk 2010 B. Robert Burdo Member 2010 Don Edgar Member 2012 W. Terry Lindley Member 2012 Don Zumwalt Member 2010 Ian Maurer Student Member 2010 ADMINISTRATION Robert F. Agrella .................................................................................................... Superintendent/President Mary Kay Rudolph ....................................... Vice President of Academic Affairs/Assistant Superintendent Doug Roberts .........................................................................................Vice President of Business Services Ricardo D. Navarrette .....................................Vice President of Student Services/Assistant Superintendent L. Jane Saldaña-Talley....................................................Vice President/Executive Dean, Petaluma Campus

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

OBJECTIVES OF THE AUDIT YEAR ENDED JUNE 30, 2010

2

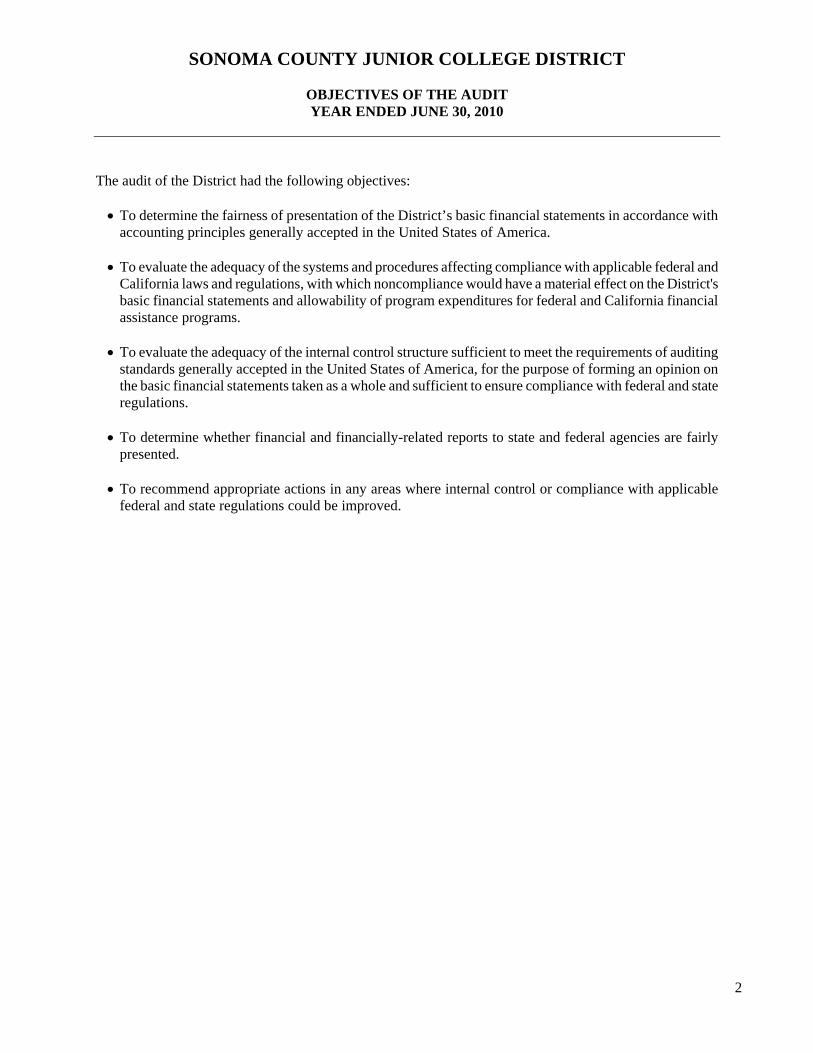

The audit of the District had the following objectives: To determine the fairness of presentation of the District’s basic financial statements in accordance with

accounting principles generally accepted in the United States of America.

To evaluate the adequacy of the systems and procedures affecting compliance with applicable federal and California laws and regulations, with which noncompliance would have a material effect on the District's basic financial statements and allowability of program expenditures for federal and California financial assistance programs.

To evaluate the adequacy of the internal control structure sufficient to meet the requirements of auditing

standards generally accepted in the United States of America, for the purpose of forming an opinion on the basic financial statements taken as a whole and sufficient to ensure compliance with federal and state regulations.

To determine whether financial and financially-related reports to state and federal agencies are fairly

presented.

To recommend appropriate actions in any areas where internal control or compliance with applicable federal and state regulations could be improved.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

HIGHLIGHTS OF THE AUDIT YEAR ENDED JUNE 30, 2010

3

This section highlights findings that were identified during the audit. These findings are discussed in the findings and recommendations section. The independent auditor’s report on the financial statements for the year ended June 30, 2010, is

unqualified (see page 4).

No compliance exceptions with state laws and regulations were noted (see page 61).

One compliance exception related to the federal financial assistance programs was noted (see page 61).

FINANCIAL SECTION

4

INDEPENDENT AUDITOR'S REPORT Members of the Board of Trustees Sonoma County Junior College District Santa Rosa, California We have audited the accompanying financial statements of the business-type activities, discretely presented component unit and remaining fund information of the Sonoma County Junior College District (the District) as of and for the year ended June 30, 2010, which collectively comprise the District’s basic financial statements, as listed in the table of contents. These financial statements are the responsibility of the District's management. Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and the Contracted District Audit Manual, issued by the California Community Colleges Chancellor’s Office. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinions. In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the business-type activities, discretely presented component unit and remaining fund information of the Sonoma County Junior College District, as of June 30, 2010, and the respective changes in financial position and, where applicable, cash flows thereof for the year then ended in conformity with accounting principles generally accepted in the United States of America. In accordance with Government Auditing Standards, we have also issued our report dated November 23, 2010, on our consideration of the District's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit.

Members of the Board of Trustees Sonoma County Junior College District Page 2

5

The Management’s Discussion and Analysis on pages 6 through 18 and the Schedule of Funding Progress for Postemployment Benefits on page 47 are not a required part of the basic financial statements but are supplementary information required by accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the information and express no opinion on it. Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the District's basic financial statements. The accompanying Schedule of Expenditures of Federal Awards is not a required part of the financial statements and is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. The Schedule of State Financial Assistance and other supplemental financial information is not a required part of the financial statements and is presented for purposes of additional analysis as required by the Contracted District Audit Manual, issued by the California Community Colleges Chancellor’s Office. Such information has been subjected to the auditing procedures applied in the audit of the financial statements and, in our opinion, are fairly stated in all material respects in relation to the basic financial statements taken as a whole. GILBERT ASSOCIATES, INC. Sacramento, California November 23, 2010

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

6

Introduction The following discussion and analysis provides an overview of the financial position and activities of the Sonoma County Junior College District (SRJC) for the year ended June 30, 2010. This discussion has been prepared by management and should be read in conjunction with the financial statements and notes which follow this section. The District was required to implement the reporting standards of Governmental Accounting Standards Board Statements No. 34 and 35 during the fiscal year 2002-03. The California Community College Chancellor’s Office, through its Fiscal Standards and Accountability Committee, recommended that all community college districts implement the new reporting standards under the Business Type Activity (BTA) model. To comply with the recommendation of the Chancellor’s Office and to report in a manner consistent with other California Community College Districts, the District has adopted the BTA reporting model for these financial statements. Under the BTA model of financial reporting, a single entity-wide statement is required to report financial activity for all funds of the District. Sonoma County Junior College District is a public two-year community college, which serves approximately 33,300 students. The District has two campuses, located in Santa Rosa and Petaluma, California and two centers, a Public Safety Training Center located in Windsor, California and the Robert Shone Agricultural Center located in Forestville, California. Students may choose from 88 associate degree majors and 162 certificate programs, complete courses toward the first two years of a bachelor’s degree program, or pursue courses for other professional or personal reasons. Reporting Highlights The annual report consists of three basic financial statements that provide information on SRJC as a

whole: the Statement of Net Assets; the Statement of Revenues, Expenses and Changes in Net Assets; and the Statement of Cash Flows. The information provided on the statements that follow includes all funds and the Bookstore, but excludes the fiduciary funds that are reported separately. The following information is provided to assist with the understanding of the financial statements and the financial position of the District. Each statement is presented in a consolidated format and will be discussed separately.

Per GASB 39, the financial statements of the Sonoma County Junior College Foundation are also

included under this cover as a discretely presented component unit as well as presented under separate cover in greater detail.

The District maintains fiduciary funds to account for assets held by the District as an agent on behalf of

others. The District’s fiduciary funds are the Student Representation Fee and Associated Students, both reported as agency funds.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

7

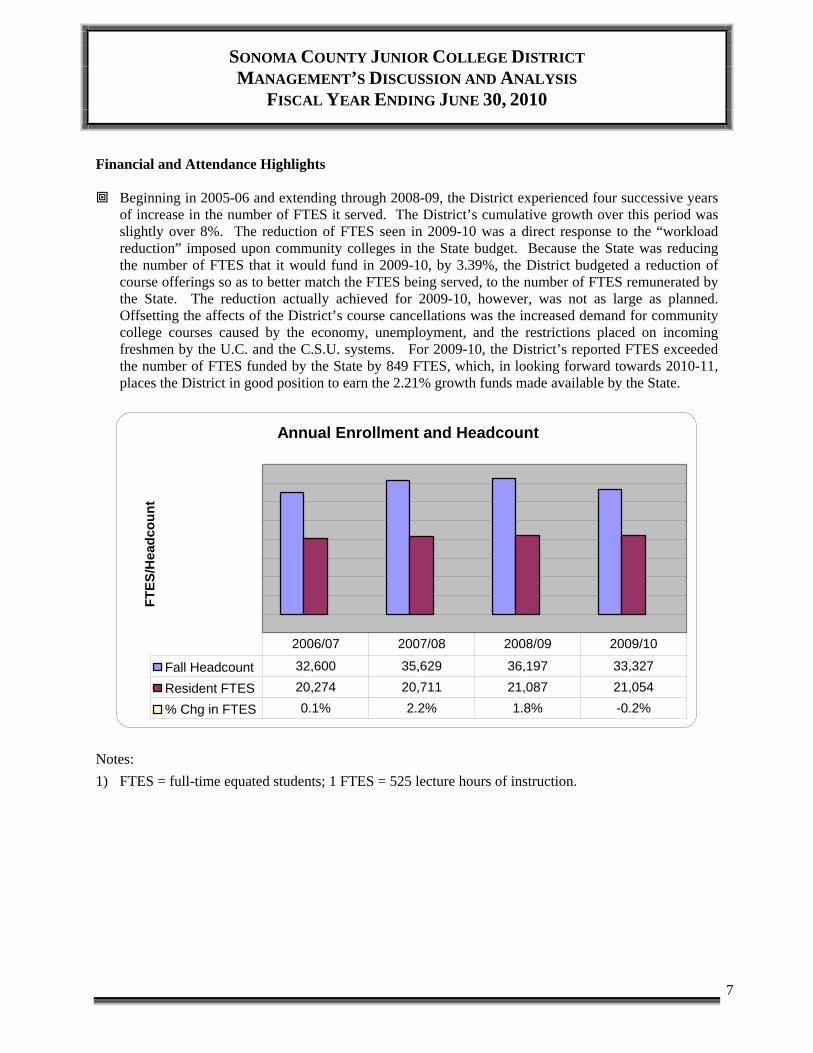

Financial and Attendance Highlights Beginning in 2005-06 and extending through 2008-09, the District experienced four successive years

of increase in the number of FTES it served. The District’s cumulative growth over this period was slightly over 8%. The reduction of FTES seen in 2009-10 was a direct response to the “workload reduction” imposed upon community colleges in the State budget. Because the State was reducing the number of FTES that it would fund in 2009-10, by 3.39%, the District budgeted a reduction of course offerings so as to better match the FTES being served, to the number of FTES remunerated by the State. The reduction actually achieved for 2009-10, however, was not as large as planned. Offsetting the affects of the District’s course cancellations was the increased demand for community college courses caused by the economy, unemployment, and the restrictions placed on incoming freshmen by the U.C. and the C.S.U. systems. For 2009-10, the District’s reported FTES exceeded the number of FTES funded by the State by 849 FTES, which, in looking forward towards 2010-11, places the District in good position to earn the 2.21% growth funds made available by the State.

Annual Enrollment and Headcount

FT

ES

/Hea

dco

un

t

Fall Headcount 32,600 35,629 36,197 33,327

Resident FTES 20,274 20,711 21,087 21,054

% Chg in FTES 0.1% 2.2% 1.8% -0.2%

2006/07 2007/08 2008/09 2009/10

Notes:

1) FTES = full-time equated students; 1 FTES = 525 lecture hours of instruction.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

8

In 2009/10, during the eighth year of implementation of its $251.7 million General Obligation Bond program (Measure A), the District completed numerous maintenance projects as well as the completion of the Lawrence A. Bertolini Student Services Center. The District issued the 2002 General Obligation Bonds, Series A, in the amount of $60 million on February 4, 2003 and the 2002 General Obligation Bonds, Series B, in the amount of $105 million on October 13, 2005. The 2002 General Obligation Bonds, Series C in the amount of $69.71 million were issued on September 17, 2007, and the 2002 General Obligation Bonds, Series D in the amount of $16.99 million were issued on April 2, 2008. The remaining major projects included in Series C is the B. Robert Burdo Culinary Arts Center and the remodel of Bailey Hall. The Series D bond issue is being invested in tax free municipals to address longer term technology needs of the District. While many of the infrastructure and technology needs of the District have been met with this bond, there are still numerous upgrades, buildings, and other projects that are still necessary and will need to be addressed in future years.

The District’s cash is invested in the Sonoma County Pooled Investment Fund, administered by the

County Treasurer. The interest rate (after fees) for the quarter ending June 30, 2010 was 0.9337% compared to 1.647% for the June 30, 2009 quarter.

Financial Aid For the years ended June 30, 2010 and 2009, the following sources of student financial aid and scholarships were disbursed:

2010 2009 Change % Change

Federal $ 16,818,741 $ 11,116,540 $ 5,702,201 51.29%

State 677,229 670,555 6,674 1.00%

Local 65,339 3,342,415 (3,277,076) -98.05%

TOTAL $ 17,561,309 $ 15,129,510 $ 2,431,799 16.07% The local funds are from the "Bridging the Doyle" campaign that the District raised funds through and put in place to provide student scholarships during the suspension of Doyle Trust distributions. The Doyle scholarship funds are derived from the Frank P. Doyle and Polly O’Meara Doyle Trust. Just over fifty percent of the annual dividends generated from the common stock in Exchange Bank are distributed to the Doyle Trust, which then distributes the funds to SRJC for scholarships to assist students attending Santa Rosa Junior College. Two scholarship programs are provided with Doyle funds: The Doyle Scholarship and the Doyle Occupational Education Award. Award amounts range from $1,000 to $1,600 per academic year. In 2008/09, there was a suspension of Exchange Bank stock dividends beginning with the third quarter of 2008 and dividends have not resumed. In 2009-10, a total of 527 Bridging the Doyle scholarships in the amount of $425 were awarded to students.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

9

Statement of Net Assets The Statement of Net Assets includes all assets and liabilities using the accrual basis of accounting, which is similar to the accounting method used by most private sector organizations. Net assets – the difference between assets and liabilities – are an indicator of the financial health of a District. 2010 2009 Change ASSETS Current assets $ 73,625,221 $ 95,534,268 $ (21,909,047)Noncurrent assets 366,379,853 351,398,443 14,981,410TOTAL ASSETS $ 440,005,074 $ 446,932,711 $ (6,927,637)

LIABILITIES Current liabilities $ 27,478,247 $ 33,778,131 $ (6,299,884)Noncurrent liabilities 227,803,921 234,480,923 (6,677,002)TOTAL LIABILITIES 255,282,168 268,259,054 (12,976,886) NET ASSETS Invested in capital assets, net of related debt $ 130,542,329 $ 135,796,115 $ (5,253,786)Restricted 49,903,645 48,283,760 1,619,885Unrestricted 4,276,932 2,093,782 2,183,150 TOTAL NET ASSETS $ 184,722,906 $ 186,173,657 $ (1,450,751) TOTAL LIABILITIES AND NET ASSETS $ 440,005,074 $ 454,432,711 $ (14,427,637)

Current assets at June 30, 2010 consist of: Current cash and cash equivalents, mainly held at the county treasury, total $20.6 million. Restricted cash and cash equivalents includes cash in the Bond Fund ($20.2 million), as well as the

portion of cash in the General Obligation debt service fund that is due to be paid in the next year ($37.2 million).

Deposits held in escrow contains cash held with trustee for major construction projects that have not been completed.

Accounts receivable includes amounts due from State, Federal and local grants, contracts, and general

apportionment earned, but not received, by year-end. Accounts receivable were stable at $14.6 million at the end of the year, a $0.25 million decrease from prior year.

Inventory consists primarily of Bookstore inventory of approximately $.722 million.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

10

Noncurrent assets are: Restricted cash and cash equivalents consists of tax revenues collected by the county for payment of

principal and interest in future years. Restricted investments is the General Obligation Bond, Series D issue that is invested with

BondLogistix. Capital assets are reported at historical cost of land, buildings, and equipment less accumulated

depreciation, where applicable. The footnotes to the financial statements contain detailed information for capital assets.

Current liabilities consist of: Accounts payable consists mainly of amounts due to vendors ($5.4 million) and employees ($1.8

million). This represents a decrease of $5.6 million over prior year, due mainly to the decrease in construction projects in the District. Liabilities related to the Self-Insurance Fund represent $365 thousand of the total accounts payable.

Deferred revenue relates to federal, state and local program funds received but not yet earned as of

the end of the fiscal year. Most grant funds are earned when expended (up to the grant amount awarded). Also included are deferred enrollment fees for the Summer and Fall 2010 semesters ($795 thousand).

Noncurrent liabilities are: Noncurrent liabilities represent debt to be paid in one year or later. The major component of the

noncurrent portion is long-term debt ($218 million). Detailed information regarding the District’s long-term debt can be found in the footnotes to the financial statements.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

11

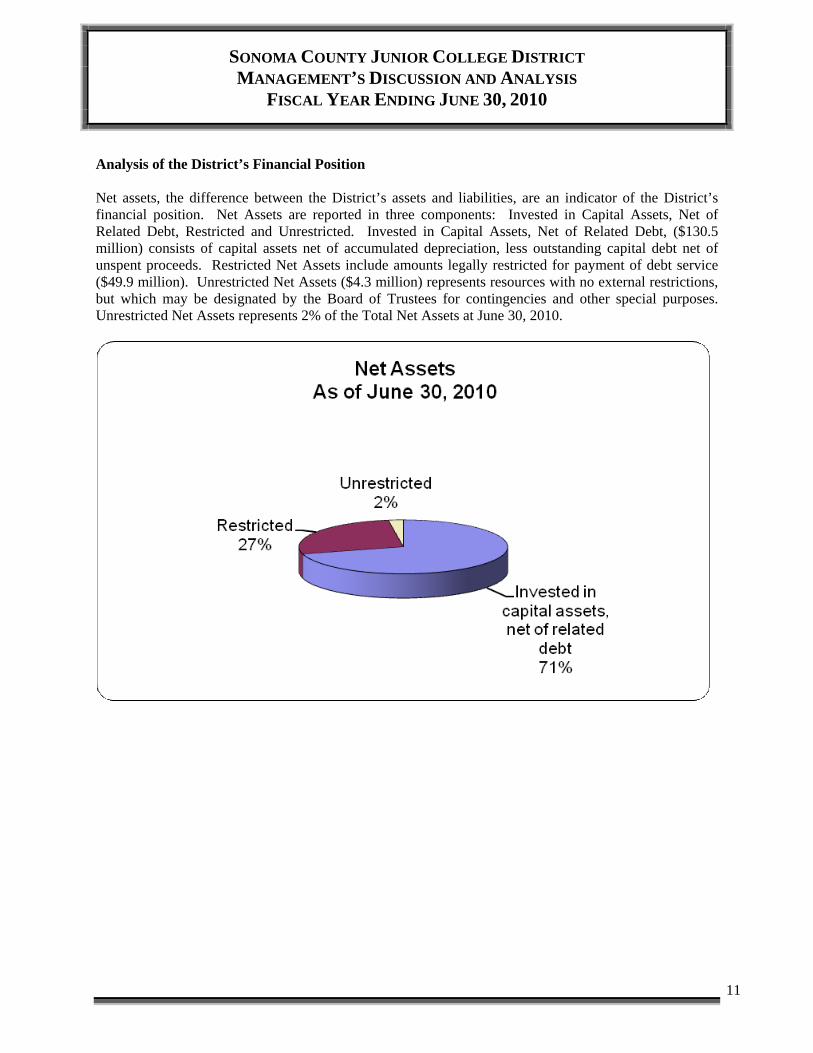

Analysis of the District’s Financial Position Net assets, the difference between the District’s assets and liabilities, are an indicator of the District’s financial position. Net Assets are reported in three components: Invested in Capital Assets, Net of Related Debt, Restricted and Unrestricted. Invested in Capital Assets, Net of Related Debt, ($130.5 million) consists of capital assets net of accumulated depreciation, less outstanding capital debt net of unspent proceeds. Restricted Net Assets include amounts legally restricted for payment of debt service ($49.9 million). Unrestricted Net Assets ($4.3 million) represents resources with no external restrictions, but which may be designated by the Board of Trustees for contingencies and other special purposes. Unrestricted Net Assets represents 2% of the Total Net Assets at June 30, 2010.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

12

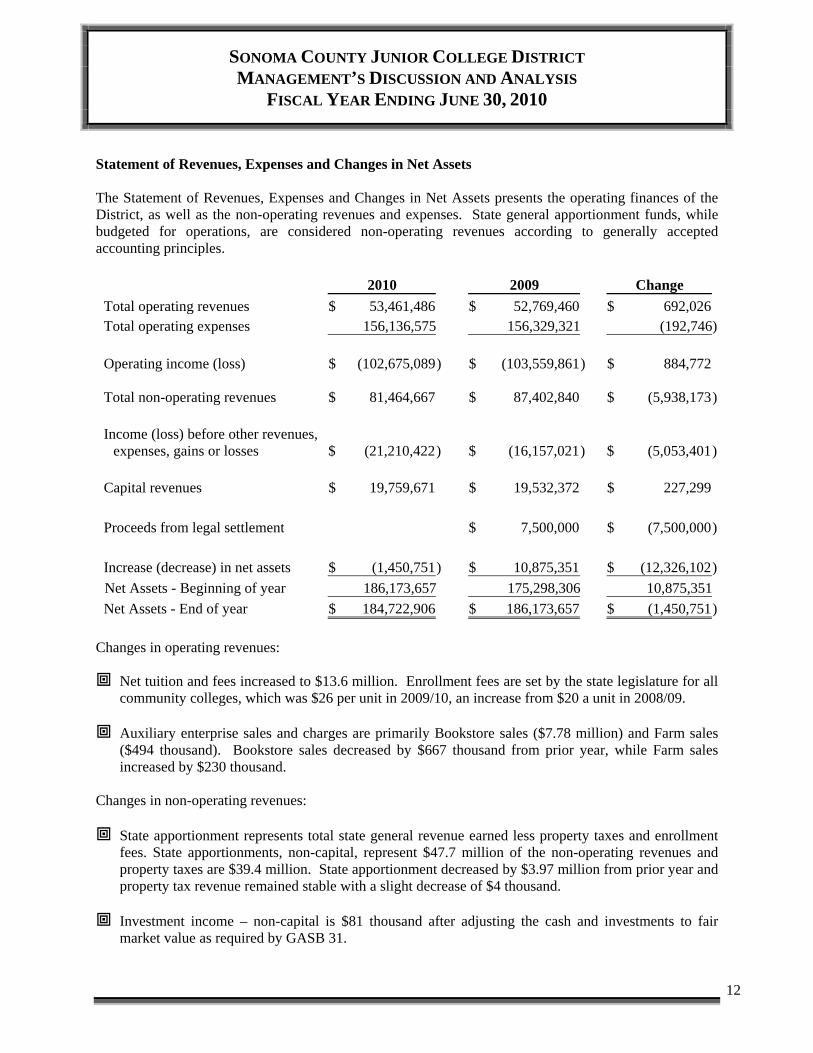

Statement of Revenues, Expenses and Changes in Net Assets The Statement of Revenues, Expenses and Changes in Net Assets presents the operating finances of the District, as well as the non-operating revenues and expenses. State general apportionment funds, while budgeted for operations, are considered non-operating revenues according to generally accepted accounting principles.

2010 2009 Change

Total operating revenues $ 53,461,486 $ 52,769,460 $ 692,026

Total operating expenses 156,136,575 156,329,321 (192,746) Operating income (loss) $ (102,675,089) $ (103,559,861 ) $ 884,772 Total non-operating revenues $ 81,464,667 $ 87,402,840 $ (5,938,173) Income (loss) before other revenues,

expenses, gains or losses $ (21,210,422) $ (16,157,021 ) $ (5,053,401) Capital revenues $ 19,759,671 $ 19,532,372 $ 227,299 Proceeds from legal settlement $ 7,500,000 $ (7,500,000) Increase (decrease) in net assets $ (1,450,751) $ 10,875,351 $ (12,326,102)

Net Assets - Beginning of year 186,173,657 175,298,306 10,875,351

Net Assets - End of year $ 184,722,906 $ 186,173,657 $ (1,450,751)

Changes in operating revenues: Net tuition and fees increased to $13.6 million. Enrollment fees are set by the state legislature for all

community colleges, which was $26 per unit in 2009/10, an increase from $20 a unit in 2008/09. Auxiliary enterprise sales and charges are primarily Bookstore sales ($7.78 million) and Farm sales

($494 thousand). Bookstore sales decreased by $667 thousand from prior year, while Farm sales increased by $230 thousand.

Changes in non-operating revenues: State apportionment represents total state general revenue earned less property taxes and enrollment

fees. State apportionments, non-capital, represent $47.7 million of the non-operating revenues and property taxes are $39.4 million. State apportionment decreased by $3.97 million from prior year and property tax revenue remained stable with a slight decrease of $4 thousand.

Investment income – non-capital is $81 thousand after adjusting the cash and investments to fair

market value as required by GASB 31.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

13

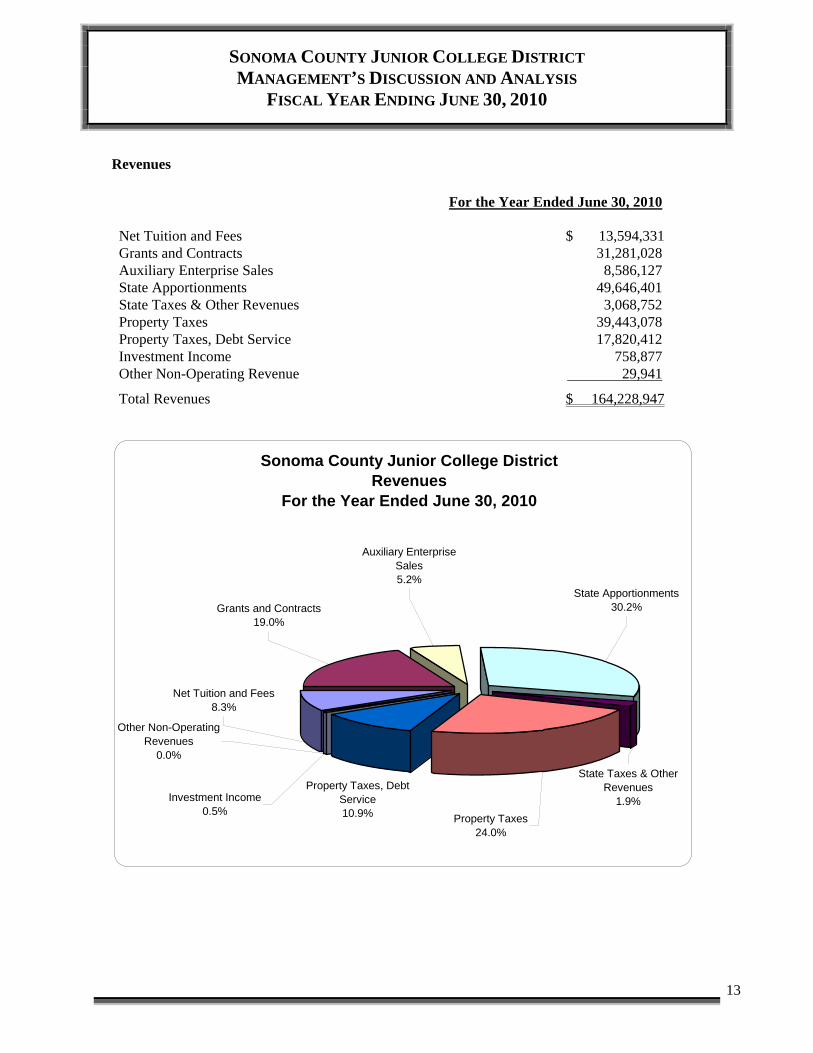

Revenues

For the Year Ended June 30, 2010 Net Tuition and Fees $ 13,594,331 Grants and Contracts 31,281,028 Auxiliary Enterprise Sales 8,586,127 State Apportionments 49,646,401 State Taxes & Other Revenues 3,068,752 Property Taxes 39,443,078 Property Taxes, Debt Service 17,820,412 Investment Income 758,877 Other Non-Operating Revenue 29,941

Total Revenues $ 164,228,947

Sonoma County Junior College DistrictRevenues

For the Year Ended June 30, 2010

Investment Income0.5%

Property Taxes, Debt Service10.9% Property Taxes

24.0%

State Taxes & Other Revenues

1.9%

State Apportionments30.2%

Auxiliary Enterprise Sales5.2%

Grants and Contracts19.0%

Net Tuition and Fees8.3%

Other Non-Operating Revenues

0.0%

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

14

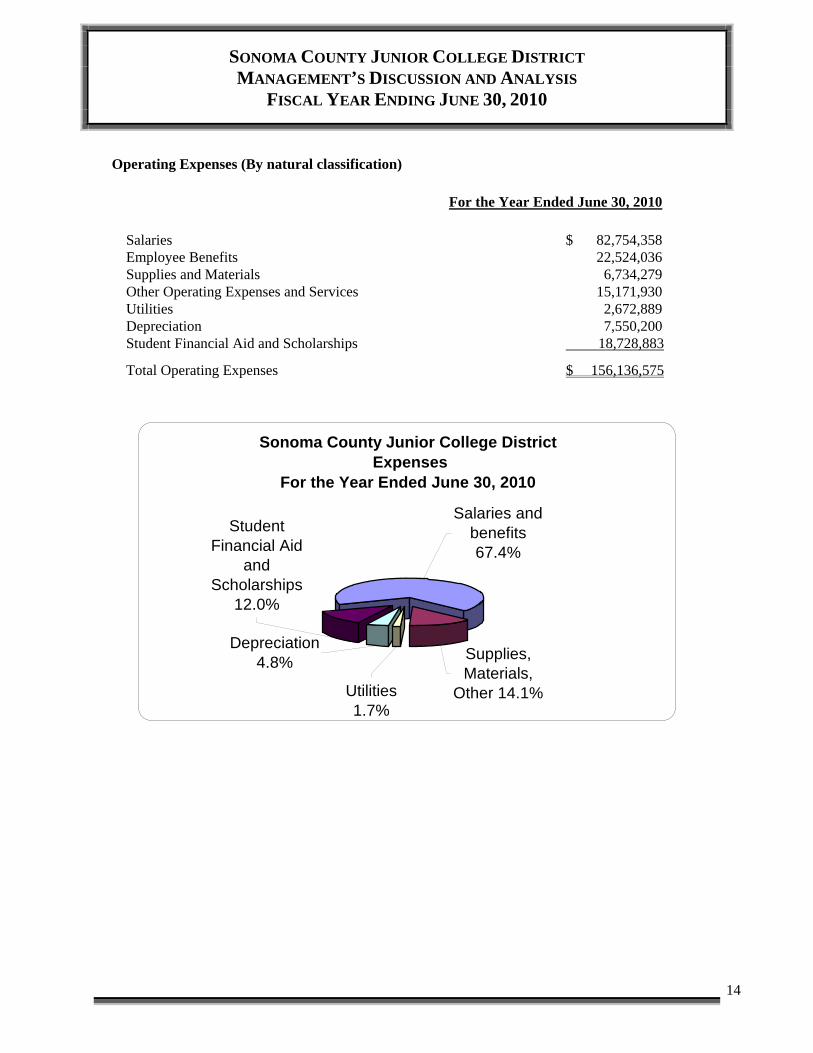

Operating Expenses (By natural classification)

For the Year Ended June 30, 2010

Salaries $ 82,754,358 Employee Benefits 22,524,036 Supplies and Materials 6,734,279 Other Operating Expenses and Services 15,171,930 Utilities 2,672,889 Depreciation 7,550,200 Student Financial Aid and Scholarships 18,728,883

Total Operating Expenses $ 156,136,575

Sonoma County Junior College District Expenses

For the Year Ended June 30, 2010

Student Financial Aid

and Scholarships

12.0%

Depreciation4.8%

Utilities1.7%

Supplies, Materials,

Other 14.1%

Salaries and benefits67.4%

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

15

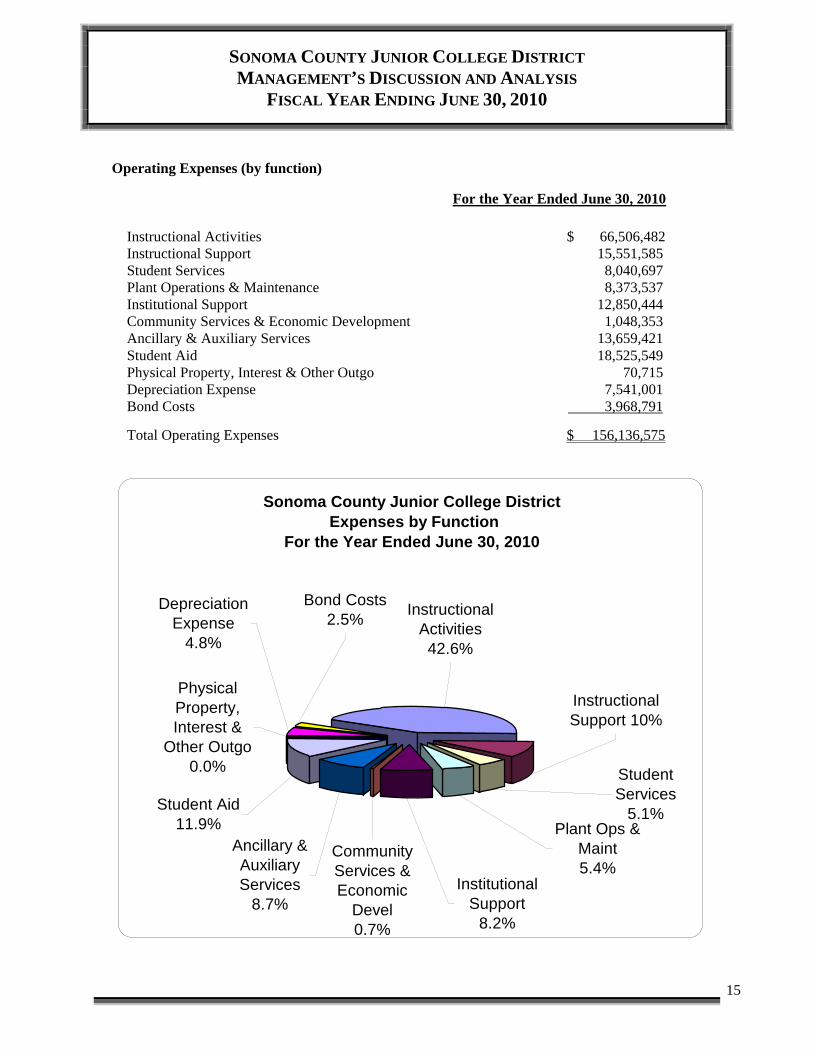

Operating Expenses (by function)

For the Year Ended June 30, 2010

Instructional Activities $ 66,506,482 Instructional Support 15,551,585 Student Services 8,040,697 Plant Operations & Maintenance 8,373,537 Institutional Support 12,850,444 Community Services & Economic Development 1,048,353 Ancillary & Auxiliary Services 13,659,421 Student Aid 18,525,549 Physical Property, Interest & Other Outgo 70,715 Depreciation Expense 7,541,001 Bond Costs 3,968,791

Total Operating Expenses $ 156,136,575

Sonoma County Junior College District Expenses by Function

For the Year Ended June 30, 2010

Bond Costs2.5%

Depreciation Expense

4.8%

Physical Property, Interest &

Other Outgo 0.0%

Student Aid11.9%

Ancillary & Auxiliary Services

8.7%

Community Services & Economic

Devel0.7%

Institutional Support

8.2%

Plant Ops & Maint 5.4%

Student Services

5.1%

Instructional Support 10%

Instructional Activities42.6%

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

16

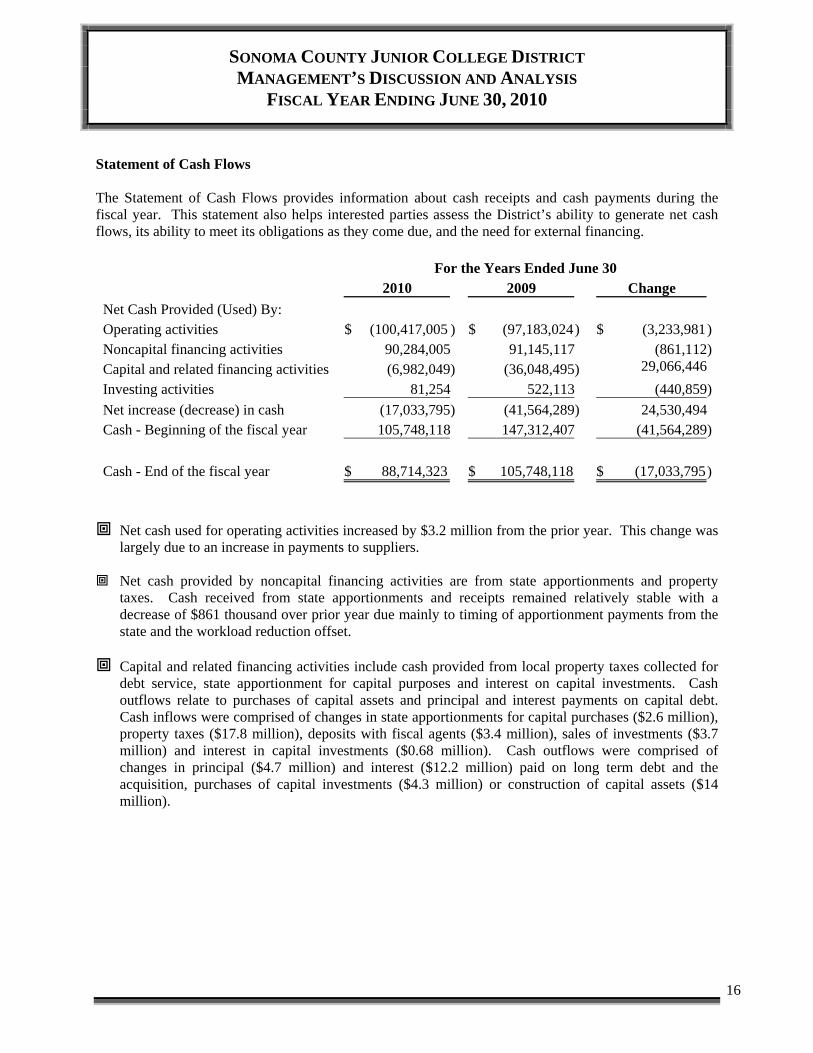

Statement of Cash Flows The Statement of Cash Flows provides information about cash receipts and cash payments during the fiscal year. This statement also helps interested parties assess the District’s ability to generate net cash flows, its ability to meet its obligations as they come due, and the need for external financing. For the Years Ended June 30

2010 2009 Change

Net Cash Provided (Used) By:

Operating activities $ (100,417,005 ) $ (97,183,024 ) $ (3,233,981) Noncapital financing activities 90,284,005 91,145,117 (861,112) Capital and related financing activities (6,982,049) (36,048,495 ) 29,066,446 Investing activities 81,254 522,113 (440,859)

Net increase (decrease) in cash (17,033,795) (41,564,289 ) 24,530,494 Cash - Beginning of the fiscal year 105,748,118 147,312,407 (41,564,289)

Cash - End of the fiscal year $ 88,714,323 $ 105,748,118 $ (17,033,795)

Net cash used for operating activities increased by $3.2 million from the prior year. This change was

largely due to an increase in payments to suppliers. Net cash provided by noncapital financing activities are from state apportionments and property

taxes. Cash received from state apportionments and receipts remained relatively stable with a decrease of $861 thousand over prior year due mainly to timing of apportionment payments from the state and the workload reduction offset.

Capital and related financing activities include cash provided from local property taxes collected for

debt service, state apportionment for capital purposes and interest on capital investments. Cash outflows relate to purchases of capital assets and principal and interest payments on capital debt. Cash inflows were comprised of changes in state apportionments for capital purchases ($2.6 million), property taxes ($17.8 million), deposits with fiscal agents ($3.4 million), sales of investments ($3.7 million) and interest in capital investments ($0.68 million). Cash outflows were comprised of changes in principal ($4.7 million) and interest ($12.2 million) paid on long term debt and the acquisition, purchases of capital investments ($4.3 million) or construction of capital assets ($14 million).

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

17

Capital Assets The District had additions of $14 million in capital assets for the year, of which $13.5 million were for buildings and construction costs. Major projects include the completion of the construction of the Lawrence A. Bertolini Student Services Center and continued construction of the new B. Robert Burdo Culinary Arts Center. Capital assets are primarily acquired with General Obligation Bond proceeds while using matching state funds when available. As of June 30, 2010, the District had contracts and commitments for construction and property acquisitions totaling $15.6 million. The District has budgeted approximately $35.7 million for capital projects in 2010/11. Construction plans include the continued construction of the Lawrence A. Bertolini Student Services Center and the B. Robert Burdo Culinary Arts Center. Other plans include renovation and modernization of classrooms and campus-wide technological upgrades. Long-Term Debt The District’s long-term debt balance of $227.8 million is comprised of: bonds payable, $218.4 million; post-employment health benefits, $2.7 million; interest payable, $5.1 million; and compensated absences, $1.6 million. Additional information regarding the District’s long-term debt can be found in the footnotes to the financial statements.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT MANAGEMENT’S DISCUSSION AND ANALYSIS

FISCAL YEAR ENDING JUNE 30, 2010

18

Economic Factors That May Affect the Future Although 2.21% growth funding is being made available by the State in 2010-11, the increase does

not offset the drastic reductions made in 2009-10, which are being carried forward into future years. Those cuts included a 3.39% workload reduction, a nearly 50% reduction to many categorical programs, some of whose expenses are federally mandated, and a second year of no Cost of Living Adjustment (COLA). Per UCLA’s Anderson Forecast, the State’s economic situation is not expected to improve until 2012.

Compounding the problem of reduced State funding have been the annual increases in the District’s operations costs. These include increases in the costs of utilities, insurance, health benefits and other contractual obligations, over which the District has some control. However, there are other cost increases over which the District has no control such as the rate-increases made by the Public Employee Retirement System (PERS) which will add over $1 million in additional annual costs by 2012-13. Similar rate-increases are expected to be assessed by the State Teachers Retirement System (STRS) as well.

Thus far, the District has made budgetary ends meet through a myriad of cost-cutting measures. These have included a 15% reduction to discretionary operational costs and the implementation of “re-engineering” which includes reducing the cost of temporary employees through a better alignment of the work performed by full-time employees. It should be noted, however, that the largest component of budgetary cost savings achieved by the District has been through temporary salary and benefits concessions which the District negotiated with the thankful help of its employee groups.

The District’s 2010-11 adopted budget included a planned $600,000 reduction to the general fund’s ending fund balance. The advent of growth funding in 2010-11, should it come to fruition, will certainly reverse the budgeted hit to the District’s reserve. But, that will only happen if there are no significant changes to the currently planned community college funding by the State.

In budgeting for 2010-11, the District proactively assumed that it would not receive any growth funding from the State. It also incorporated into its revenue assumptions an additional property tax shortfall for the year. Given the State’s precarious economic situation, the District used conservative revenue projections in the budget it adopted on September 14, 2010, specifically to protect itself from the potential revenue losses.

The District issued General Obligation Bonds, Series D on April 2, 2008, in the amount of $16.99 million. This issuance has been invested with BondLogistix and has been designated to address long-term technology needs of the District, although some portion of these funds may be used to address other bond-related activities.

As the Bond funds are spent down, the District will need to start setting aside funds in order to maintain the new and existing buildings in the future.

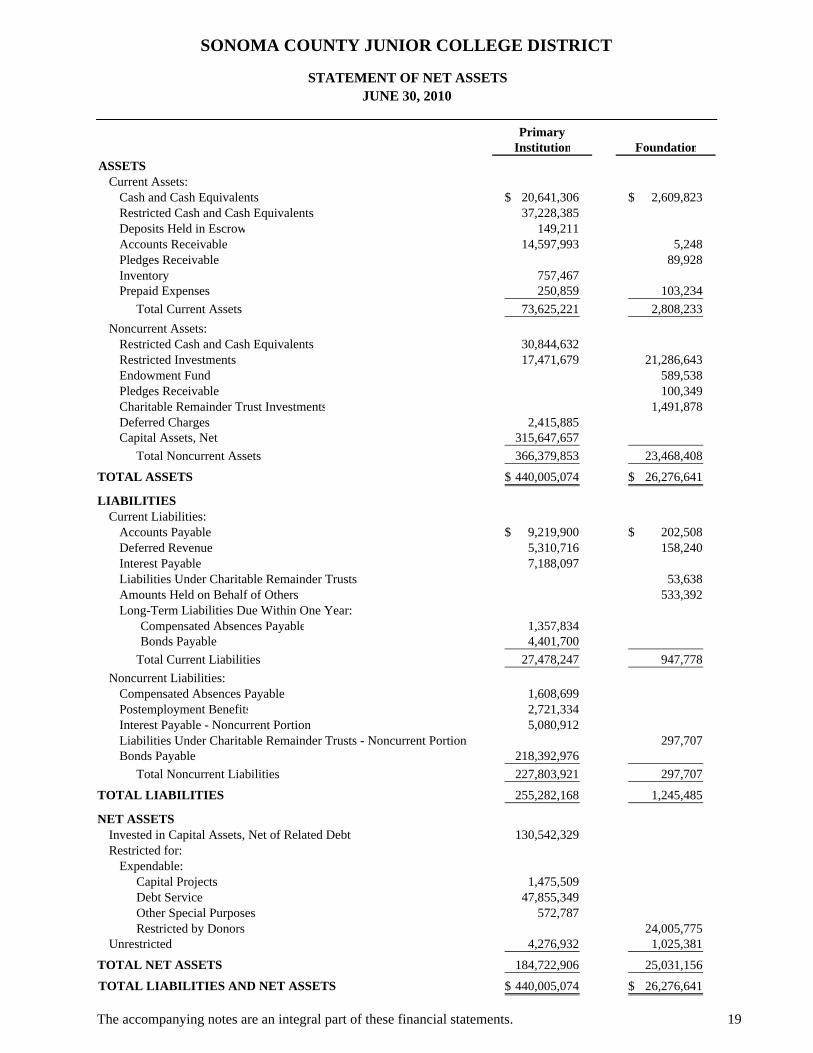

PrimaryInstitution Foundation

ASSETSCurrent Assets:

Cash and Cash Equivalents 20,641,306$ 2,609,823$ Restricted Cash and Cash Equivalents 37,228,385 Deposits Held in Escrow 149,211 Accounts Receivable 14,597,993 5,248 Pledges Receivable 89,928 Inventory 757,467 Prepaid Expenses 250,859 103,234

Total Current Assets 73,625,221 2,808,233

Noncurrent Assets:Restricted Cash and Cash Equivalents 30,844,632 Restricted Investments 17,471,679 21,286,643 Endowment Fund 589,538 Pledges Receivable 100,349 Charitable Remainder Trust Investments 1,491,878 Deferred Charges 2,415,885 Capital Assets, Net 315,647,657

Total Noncurrent Assets 366,379,853 23,468,408

TOTAL ASSETS 440,005,074$ 26,276,641$

LIABILITIESCurrent Liabilities:

Accounts Payable 9,219,900$ 202,508$ Deferred Revenue 5,310,716 158,240 Interest Payable 7,188,097 Liabilities Under Charitable Remainder Trusts 53,638 Amounts Held on Behalf of Others 533,392 Long-Term Liabilities Due Within One Year:

Compensated Absences Payable 1,357,834 Bonds Payable 4,401,700

Total Current Liabilities 27,478,247 947,778

Noncurrent Liabilities:Compensated Absences Payable 1,608,699 Postemployment Benefits 2,721,334 Interest Payable - Noncurrent Portion 5,080,912 Liabilities Under Charitable Remainder Trusts - Noncurrent Portion 297,707 Bonds Payable 218,392,976

Total Noncurrent Liabilities 227,803,921 297,707

TOTAL LIABILITIES 255,282,168 1,245,485

NET ASSETSInvested in Capital Assets, Net of Related Debt 130,542,329 Restricted for:

Expendable:Capital Projects 1,475,509 Debt Service 47,855,349 Other Special Purposes 572,787 Restricted by Donors 24,005,775

Unrestricted 4,276,932 1,025,381

TOTAL NET ASSETS 184,722,906 25,031,156

TOTAL LIABILITIES AND NET ASSETS 440,005,074$ 26,276,641$

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

STATEMENT OF NET ASSETSJUNE 30, 2010

The accompanying notes are an integral part of these financial statements. 19

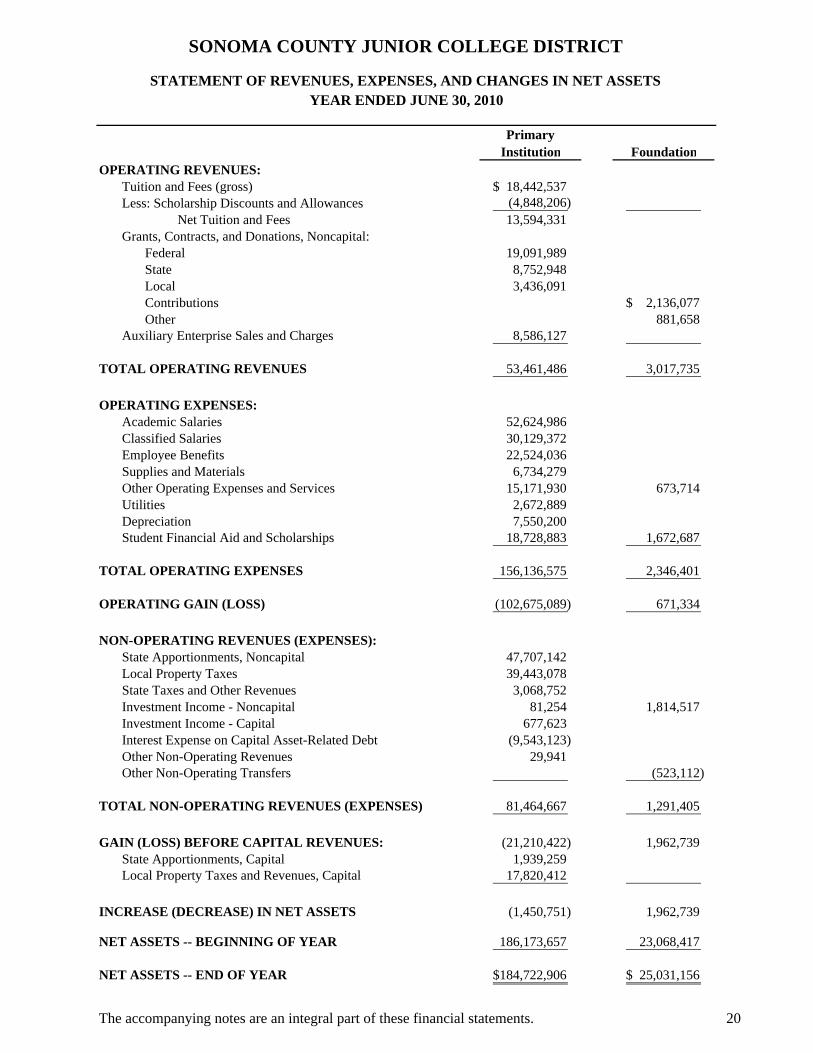

PrimaryInstitution Foundation

OPERATING REVENUES:Tuition and Fees (gross) 18,442,537$ Less: Scholarship Discounts and Allowances (4,848,206)

Net Tuition and Fees 13,594,331 Grants, Contracts, and Donations, Noncapital:

Federal 19,091,989 State 8,752,948 Local 3,436,091 Contributions 2,136,077$ Other 881,658

Auxiliary Enterprise Sales and Charges 8,586,127

TOTAL OPERATING REVENUES 53,461,486 3,017,735

OPERATING EXPENSES:Academic Salaries 52,624,986 Classified Salaries 30,129,372 Employee Benefits 22,524,036 Supplies and Materials 6,734,279 Other Operating Expenses and Services 15,171,930 673,714 Utilities 2,672,889 Depreciation 7,550,200 Student Financial Aid and Scholarships 18,728,883 1,672,687

TOTAL OPERATING EXPENSES 156,136,575 2,346,401

OPERATING GAIN (LOSS) (102,675,089) 671,334

NON-OPERATING REVENUES (EXPENSES):State Apportionments, Noncapital 47,707,142 Local Property Taxes 39,443,078 State Taxes and Other Revenues 3,068,752 Investment Income - Noncapital 81,254 1,814,517 Investment Income - Capital 677,623 Interest Expense on Capital Asset-Related Debt (9,543,123) Other Non-Operating Revenues 29,941 Other Non-Operating Transfers (523,112)

TOTAL NON-OPERATING REVENUES (EXPENSES) 81,464,667 1,291,405

GAIN (LOSS) BEFORE CAPITAL REVENUES: (21,210,422) 1,962,739 State Apportionments, Capital 1,939,259 Local Property Taxes and Revenues, Capital 17,820,412

INCREASE (DECREASE) IN NET ASSETS (1,450,751) 1,962,739

NET ASSETS -- BEGINNING OF YEAR 186,173,657 23,068,417

NET ASSETS -- END OF YEAR 184,722,906$ 25,031,156$

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

STATEMENT OF REVENUES, EXPENSES, AND CHANGES IN NET ASSETSYEAR ENDED JUNE 30, 2010

The accompanying notes are an integral part of these financial statements. 20

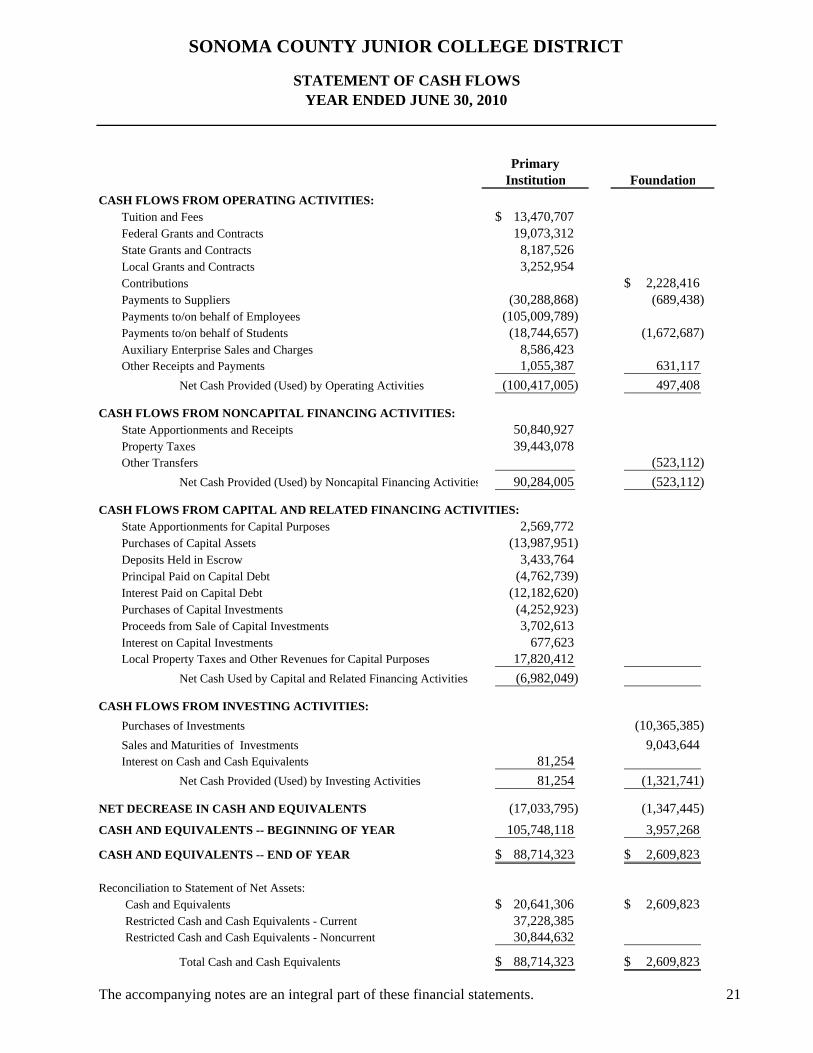

PrimaryInstitution Foundation

CASH FLOWS FROM OPERATING ACTIVITIES:Tuition and Fees 13,470,707$ Federal Grants and Contracts 19,073,312 State Grants and Contracts 8,187,526 Local Grants and Contracts 3,252,954 Contributions 2,228,416$ Payments to Suppliers (30,288,868) (689,438) Payments to/on behalf of Employees (105,009,789) Payments to/on behalf of Students (18,744,657) (1,672,687) Auxiliary Enterprise Sales and Charges 8,586,423 Other Receipts and Payments 1,055,387 631,117

Net Cash Provided (Used) by Operating Activities (100,417,005) 497,408

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIES:State Apportionments and Receipts 50,840,927 Property Taxes 39,443,078 Other Transfers (523,112)

Net Cash Provided (Used) by Noncapital Financing Activities 90,284,005 (523,112)

CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIES:State Apportionments for Capital Purposes 2,569,772 Purchases of Capital Assets (13,987,951) Deposits Held in Escrow 3,433,764 Principal Paid on Capital Debt (4,762,739) Interest Paid on Capital Debt (12,182,620) Purchases of Capital Investments (4,252,923) Proceeds from Sale of Capital Investments 3,702,613 Interest on Capital Investments 677,623 Local Property Taxes and Other Revenues for Capital Purposes 17,820,412

Net Cash Used by Capital and Related Financing Activities (6,982,049)

CASH FLOWS FROM INVESTING ACTIVITIES:

Purchases of Investments (10,365,385)

Sales and Maturities of Investments 9,043,644 Interest on Cash and Cash Equivalents 81,254

Net Cash Provided (Used) by Investing Activities 81,254 (1,321,741)

NET DECREASE IN CASH AND EQUIVALENTS (17,033,795) (1,347,445)

CASH AND EQUIVALENTS -- BEGINNING OF YEAR 105,748,118 3,957,268

CASH AND EQUIVALENTS -- END OF YEAR 88,714,323$ 2,609,823$

Reconciliation to Statement of Net Assets: Cash and Equivalents 20,641,306$ 2,609,823$ Restricted Cash and Cash Equivalents - Current 37,228,385 Restricted Cash and Cash Equivalents - Noncurrent 30,844,632

Total Cash and Cash Equivalents 88,714,323$ 2,609,823$

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

STATEMENT OF CASH FLOWSYEAR ENDED JUNE 30, 2010

The accompanying notes are an integral part of these financial statements. 21

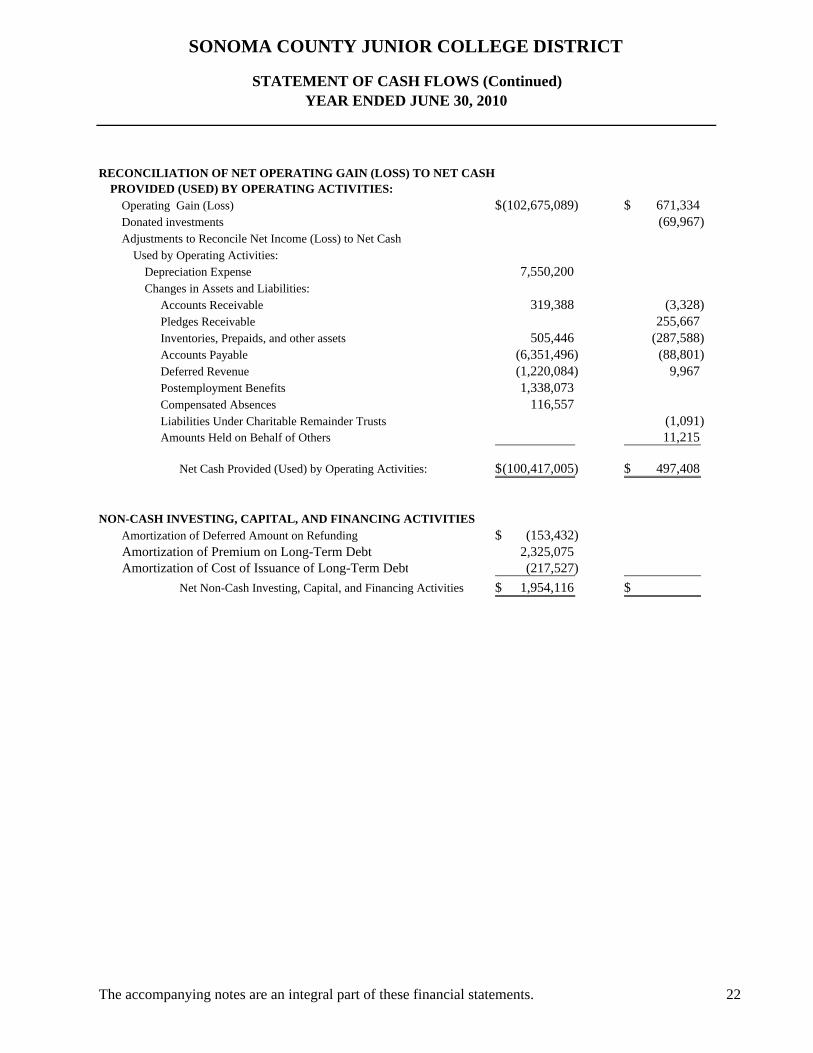

RECONCILIATION OF NET OPERATING GAIN (LOSS) TO NET CASHPROVIDED (USED) BY OPERATING ACTIVITIES:

Operating Gain (Loss) (102,675,089)$ 671,334$ Donated investments (69,967) Adjustments to Reconcile Net Income (Loss) to Net Cash

Used by Operating Activities:Depreciation Expense 7,550,200 Changes in Assets and Liabilities:

Accounts Receivable 319,388 (3,328) Pledges Receivable 255,667 Inventories, Prepaids, and other assets 505,446 (287,588) Accounts Payable (6,351,496) (88,801) Deferred Revenue (1,220,084) 9,967 Postemployment Benefits 1,338,073 Compensated Absences 116,557 Liabilities Under Charitable Remainder Trusts (1,091) Amounts Held on Behalf of Others 11,215

Net Cash Provided (Used) by Operating Activities: (100,417,005)$ 497,408$

NON-CASH INVESTING, CAPITAL, AND FINANCING ACTIVITIESAmortization of Deferred Amount on Refunding (153,432)$ Amortization of Premium on Long-Term Debt 2,325,075 Amortization of Cost of Issuance of Long-Term Debt (217,527)

Net Non-Cash Investing, Capital, and Financing Activities 1,954,116$ $

YEAR ENDED JUNE 30, 2010

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

STATEMENT OF CASH FLOWS (Continued)

The accompanying notes are an integral part of these financial statements. 22

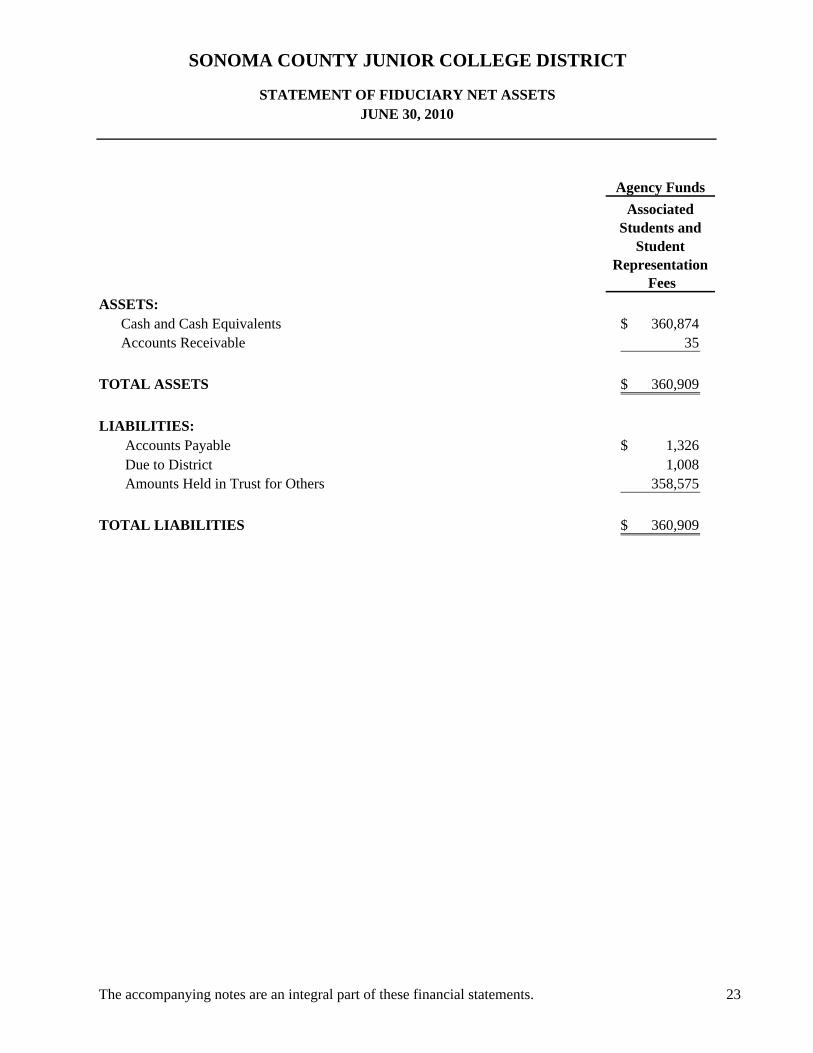

Agency Funds

Associated Students and

Student Representation

Fees

ASSETS:Cash and Cash Equivalents 360,874$ Accounts Receivable 35

TOTAL ASSETS 360,909$

LIABILITIES:Accounts Payable 1,326$ Due to District 1,008 Amounts Held in Trust for Others 358,575

TOTAL LIABILITIES 360,909$

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

STATEMENT OF FIDUCIARY NET ASSETSJUNE 30, 2010

The accompanying notes are an integral part of these financial statements. 23

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

24

1. ORGANIZATION AND REPORTING ENTITY

The Sonoma County Junior College District (the District) was established in 1918 with the founding of Santa Rosa Junior College. The District operates a campus in the City of Santa Rosa, a campus in the City of Petaluma, a criminal justice training center in the Town of Windsor, and classes at numerous other locations throughout the District.

The District has reviewed criteria to determine whether other entities with activities that benefit the District should be included within its financial reporting entity. The decision to include a potential component unit in the reporting entity was made by applying the criteria set forth in generally accepted accounting principles (GAAP) and Governmental Accounting Standards Board (GASB) Statement No. 14 as amended by GASB Statement No. 39. The District, based on its evaluation of these criteria, identified the Santa Rosa Junior College Foundation (the Foundation) as a component unit. Discretely presented component unit – The Foundation was established as a legally separate non-profit entity to support the District and its students through fundraising activities. In addition, the Foundation develops and maintains student scholarships and trust accounts for the District students. Furthermore, the funds contributed by the Foundation to the District and its students are significant to the District’s financial statements. Therefore, the District has classified the Foundation as a component unit that will be discretely presented in the District’s annual financial statements. The Foundation also issues complete audited financial statements that may be obtained from the District or the Foundation.

2. SIGNIFICANT ACCOUNTING POLICIES

Basis of presentation – The accompanying financial statements have been prepared in conformity with generally accepted accounting principles as prescribed by the Governmental Accounting Standards Board and Audits of State and Local Governmental Units, issued by the American Institute of Certified Public Accountants (AICPA) and, where applicable, Financial Accounting Standards Board (FASB) Statements issued through 1989. Basis of accounting – For financial reporting purposes, the District is considered a special-purpose government engaged only in business-type activities. Accordingly, the District’s financial statements have been presented using economic resources measurement focus and accrual basis of accounting. Under the accrual basis, revenues are recognized when earned, and expenses are recognized when an obligation has been incurred. All significant interfund transactions have been eliminated. The budgetary and financial accounts of the District are recorded and maintained in accordance with the Chancellor’s Office of the California Community Colleges’ Budget and Accounting Manual, which is consistent with generally accepted accounting principles in the United States of America.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

25

In addition to the District’s business-type activities, the District maintains fiduciary funds. These funds account for assets held by the District in a trustee capacity or as an agent on behalf of others. Fiduciary funds are accounted for using the economic resources measurement focus. The District reports the following fiduciary funds: Agency Funds – This fund includes the Associated Students and the Student Representation Fee Fund. The amounts reported for student body funds represent the combined totals of all accounts for the various student body clubs and activities within the District. Individual totals, by club, are maintained within the Associated Student’s accounting system. The Student Representation Fee Fund accounts for the student representation fee assessment, which is used by students for legislative advocacy. Budgets and budgetary accounting – By state law, the District's governing board must approve a tentative budget no later than July 1st and adopt a final budget no later than September 15th of each year. A hearing must be conducted for public comments prior to adoption. The budget is revised during the year to incorporate categorical funds which are awarded during the year and miscellaneous changes to the spending plans. Revisions to the budget are approved by the District's governing board.

Estimates used in financial reporting – In preparing financial statements in conformity with accounting principles generally accepted in the United States of America, management is required to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and cash equivalents – For purposes of the Statement of Cash Flows, the District considers all highly liquid investments with a maturity of three months or less at the time of purchase to be cash equivalents. Funds invested in the county treasurer’s investment pool are considered cash equivalents. Restricted cash, cash equivalents and investments – Cash, cash equivalents, and investments that are externally restricted per contractual obligations are classified as current or non-current assets in the statement of net assets based on anticipated use. Deposits held in escrow – Cash deposited in an escrow account as retention on major construction projects that has been earned but will not be released until the project is satisfactorily completed, a notice of completion is filed, and the Board of Trustees have approved the release of retention funds, is classified as deposits held in escrow in the statement of net assets.

Investments – Investments are reported at fair value on the balance sheet based on open market quotes for debt and equity securities. Unrealized gains and losses are recorded on the statement of revenues, expenses and changes in fund balances. Accounts Receivable – Accounts receivable consist of amounts due from federal, state and local governments, or private sources, in connection with reimbursement of allowable expenses based on a contract or agreement between the District and the funding source.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

26

Pledges Receivable – The Foundation accounts for its pledges in accordance with GASB Statement No. 33, Accounting and Financial Reporting for Non-exchange Transactions (GASB 33). GASB 33 establishes reporting standards for non-exchange transactions which, in the case of the Foundation, are restricted pledges to be contributed in the future. Endowed pledges are not recognized according to GASB 33. Inventory – Inventories consist principally of textbooks and are stated at the cost method (first-in, first-out method) or market.

Capital assets – Capital assets are those assets purchased or acquired with an original cost of $20,000 for Buildings and Improvement of Sites, and $5,000 for all other capital assets. These assets are reported at historical cost or estimated historical cost. Additions, improvements, and other capital outlays that significantly extend the useful life of an asset are capitalized. Other costs incurred for repairs and maintenance are expensed as incurred. Depreciation on all assets is provided on a straight-line basis over the following estimated useful lives:

Asset Class Years

Improvement of Sites 20

Buildings 50

Vehicles 8

Restricted Programs - Machinery 5-15

Machinery and Equipment 5-15

Deferred revenues – Deferred revenues include amounts received for tuition and fees and certain categorical program revenues received prior to the end of the fiscal year, but related to the subsequent accounting period. Deferred revenues also include amounts received from grants and contracts that have not yet been earned. When both restricted and unrestricted resources are available for use, it is the District’s policy to use restricted resources first, and then unrestricted resources as they are needed. Compensated absences – Employee vacation pay is accrued at year-end for financial statement purposes based on vacation time accrued and current pay rate. The liability and expense incurred are recorded at year-end as accrued vacation payable in the statement of net assets and as a component of employee benefits. It is the District’s policy to record sick leave in the period taken, since the employee’s right to sick leave payment does not vest upon termination. Non-current liabilities – Non-current liabilities include estimated amounts for accrued compensated absences, post-employment benefits, and bond repayments and related interest that will not be paid within the next fiscal year.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

27

Net assets – The District's net assets are classified as follows: Invested in capital assets, net of related debt – This represents the District's total investment in

capital assets, net of outstanding debt obligations related to those capital assets. To the extent debt has been incurred but not yet expended for capital assets, such amounts are not included as a component invested in capital assets, net of related debt.

Restricted net assets – expendable – Restricted expendable net assets include resources that the District is legally or contractually obligated to spend in accordance with restrictions imposed by external third parties.

Unrestricted net assets – Unrestricted net assets represent resources derived from student tuition and

fees, state apportionments, and sales and services of educational departments and auxiliary enterprises. These resources are used for transactions relating to the educational and general operations of the District, and may be used at the discretion of the governing board to meet current expenses for any purpose.

Classification of revenues – The District has classified its revenues as either operating or non-operating revenues according to the following criteria:

Operating revenues: Operating revenues include activities that have the characteristics of exchange transactions, such as (1) student tuition and fees, net of scholarship discounts and allowances; (2) sales and services of auxiliary enterprises; (3) most Federal, State and local grants and contracts and Federal appropriations.

Non-operating revenues: Non-operating revenues include activities that have the characteristics of non-exchange transactions, such as gifts and contributions, and other revenue sources that are defined as non-operating revenues by GASB No. 9, “Reporting Cash Flows of Proprietary and Nonexpendable Trust Funds and Governmental Entities That Use Proprietary Fund Accounting” and GASB No. 34, such as State Appropriations and investment income.

Scholarship discounts and allowances and financial aid – Student tuition and fee revenues are reported net of scholarship discounts and allowances in the statement of activities. The District offers Board of Governor’s Grants (BOG) to qualified students and these tuition waivers are reported as scholarship discounts and allowances. Grants, such as Federal, State or non-governmental programs, are recorded as operating or non-operating revenues in the District’s financial statements.

Property taxes – Secured property taxes attach as an enforceable lien on property as of January 1, and are payable in two installments on November 1 and February 1. Unsecured property taxes are payable in one installment on or before August 31. The County of Sonoma bills and collects the taxes for the District. Tax revenues are recognized by the District when received.

Reclassifications – Certain reclassifications have been made to the June 30, 2009, balances to conform to the June 30, 2010, presentation.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

28

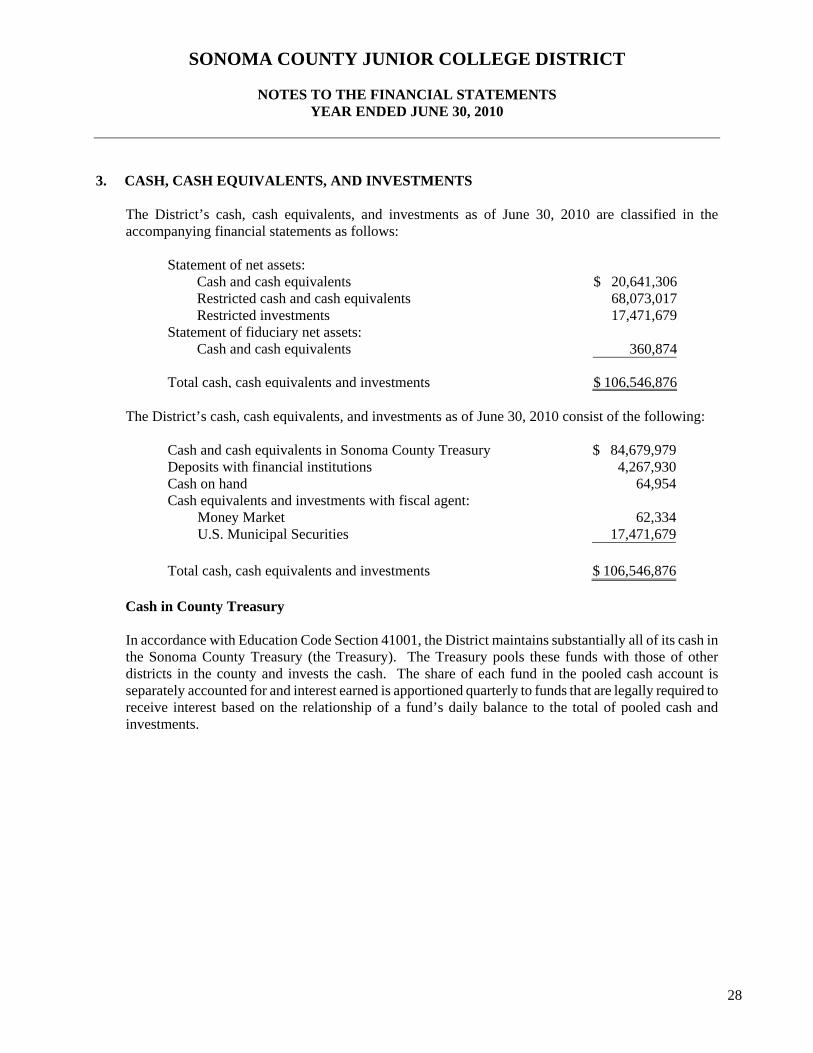

3. CASH, CASH EQUIVALENTS, AND INVESTMENTS The District’s cash, cash equivalents, and investments as of June 30, 2010 are classified in the accompanying financial statements as follows:

Statement of net assets: Cash and cash equivalents $ 20,641,306Restricted cash and cash equivalents 68,073,017Restricted investments 17,471,679

Statement of fiduciary net assets: Cash and cash equivalents 360,874

Total cash, cash equivalents and investments $ 106,546,876 The District’s cash, cash equivalents, and investments as of June 30, 2010 consist of the following:

Cash and cash equivalents in Sonoma County Treasury $ 84,679,979Deposits with financial institutions 4,267,930Cash on hand 64,954Cash equivalents and investments with fiscal agent:

Money Market 62,334U.S. Municipal Securities 17,471,679

Total cash, cash equivalents and investments $ 106,546,876 Cash in County Treasury In accordance with Education Code Section 41001, the District maintains substantially all of its cash in the Sonoma County Treasury (the Treasury). The Treasury pools these funds with those of other districts in the county and invests the cash. The share of each fund in the pooled cash account is separately accounted for and interest earned is apportioned quarterly to funds that are legally required to receive interest based on the relationship of a fund’s daily balance to the total of pooled cash and investments.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

29

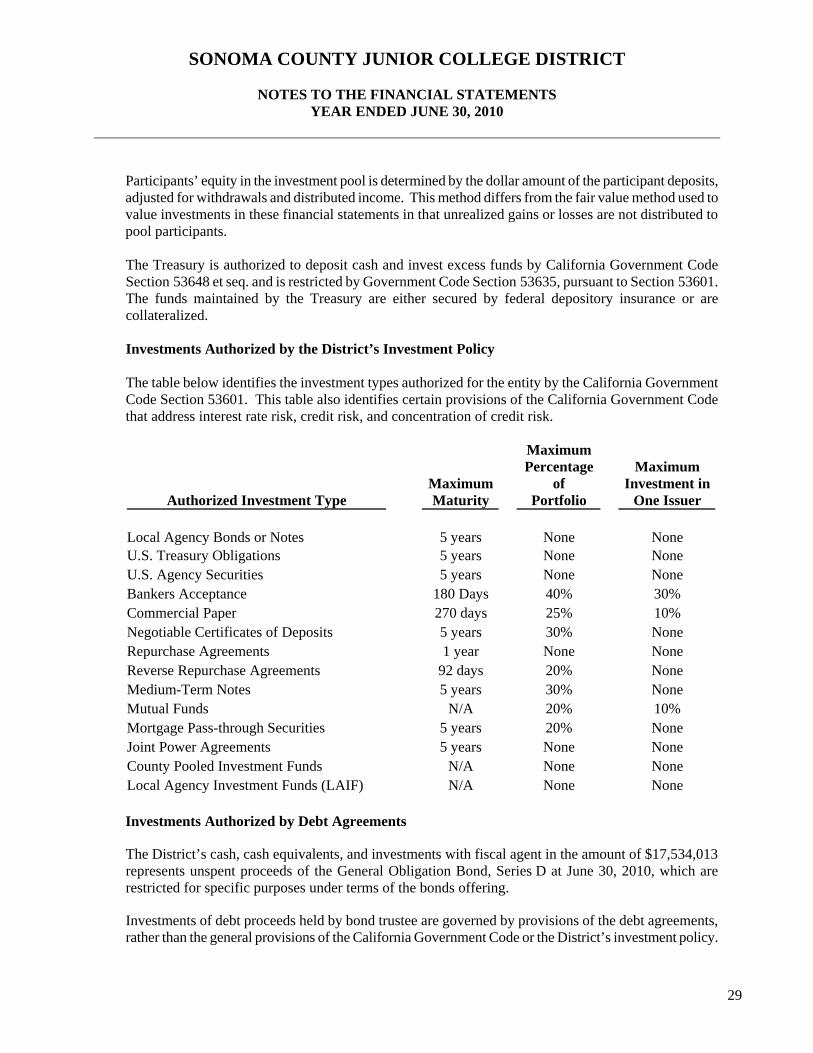

Participants’ equity in the investment pool is determined by the dollar amount of the participant deposits, adjusted for withdrawals and distributed income. This method differs from the fair value method used to value investments in these financial statements in that unrealized gains or losses are not distributed to pool participants. The Treasury is authorized to deposit cash and invest excess funds by California Government Code Section 53648 et seq. and is restricted by Government Code Section 53635, pursuant to Section 53601. The funds maintained by the Treasury are either secured by federal depository insurance or are collateralized. Investments Authorized by the District’s Investment Policy

The table below identifies the investment types authorized for the entity by the California Government Code Section 53601. This table also identifies certain provisions of the California Government Code that address interest rate risk, credit risk, and concentration of credit risk.

Authorized Investment Type

MaximumMaturity

Maximum Percentage

of Portfolio

Maximum Investment in

One Issuer

Local Agency Bonds or Notes 5 years None None U.S. Treasury Obligations 5 years None None U.S. Agency Securities 5 years None None Bankers Acceptance 180 Days 40% 30% Commercial Paper 270 days 25% 10% Negotiable Certificates of Deposits 5 years 30% None Repurchase Agreements 1 year None None Reverse Repurchase Agreements 92 days 20% None Medium-Term Notes 5 years 30% None Mutual Funds N/A 20% 10% Mortgage Pass-through Securities 5 years 20% None Joint Power Agreements 5 years None None County Pooled Investment Funds N/A None None Local Agency Investment Funds (LAIF) N/A None None

Investments Authorized by Debt Agreements

The District’s cash, cash equivalents, and investments with fiscal agent in the amount of $17,534,013 represents unspent proceeds of the General Obligation Bond, Series D at June 30, 2010, which are restricted for specific purposes under terms of the bonds offering.

Investments of debt proceeds held by bond trustee are governed by provisions of the debt agreements, rather than the general provisions of the California Government Code or the District’s investment policy.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

30

Interest Rate Risk

Interest rate risk is the risk that changes in market interest rates will adversely affect the fair value of an investment. Generally, the longer the maturity of an investment, the greater the sensitivity of its fair values to changes in market interest rates. As of June 30, 2010, the weighted average maturity of the investments contained in the District’s Treasury's investment pool is approximately 486 days. As of June 30, 2010, the District had the following investments held by trustees:

Remaining Maturity (in Years)

Total Market Less than 1 to 5 5 to 10 Investment Type Value 1 Year Years Years

U.S. Municipal Securities $ 17,471,679 $ 12,550,000 $ 4,071,565 $ 850,114

Credit Risk Generally, credit risk is the risk that an issuer of an investment will not fulfill its obligation to the holder of the investment. This is measured by the assignment of a rating by a nationally recognized statistical rating organization. The County Treasury investment pool does not have a rating provided by a nationally recognized statistical rating organization.

Rating as of Year End (Standard and Poor’s)

Investment Type Total Market

Value Exempt From

Disclosure AAA AA+ AA

U.S. Municipal Securities $ 17,471,679 $ 11,679,454 $ 736,725 $ 5,055,500

Money Market 62,334 $ 62,334

$ 17,534,013 $ 62,334 $ 11,679,454 $ 736,725 $ 5,055,500

Concentration of Credit Risk

The investment policy contains no limitations on the amount that can be invested in any one issuer. There were no investments in any one issuer (other than U.S. treasury securities and mutual funds) that represent 5% or more of the total investments balance. Cash on Hand, in Banks, and in Revolving Fund

As of June 30, 2010, the carrying amount of the District's bank balance was $3,785,952. Of the bank balance, $272,034 was insured by the Federal Depository Insurance Corporation (FDIC), and $3,542,363 was insured under the FDIC’s Transaction Account Guarantee Program. Cash on hand of $64,954 was not insured. Of the total bank balance, $3,556,745 is held by the primary institution and $229,207 is held by fiduciary funds.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

31

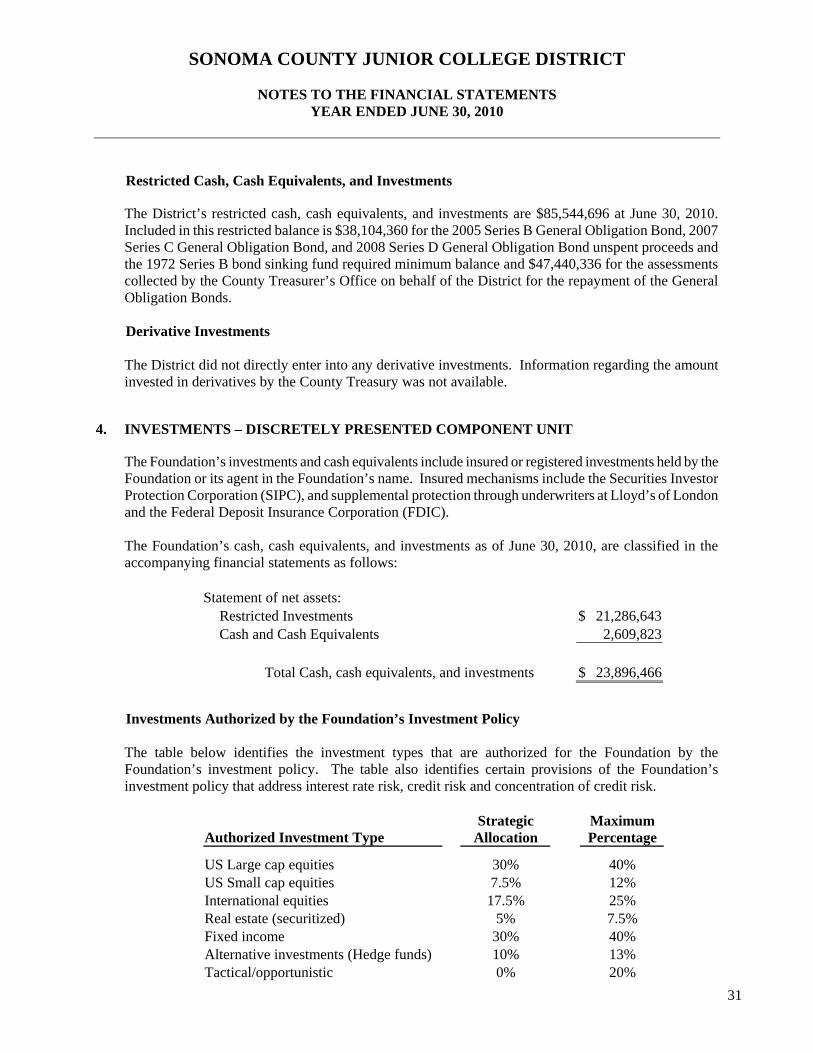

Restricted Cash, Cash Equivalents, and Investments

The District’s restricted cash, cash equivalents, and investments are $85,544,696 at June 30, 2010. Included in this restricted balance is $38,104,360 for the 2005 Series B General Obligation Bond, 2007 Series C General Obligation Bond, and 2008 Series D General Obligation Bond unspent proceeds and the 1972 Series B bond sinking fund required minimum balance and $47,440,336 for the assessments collected by the County Treasurer’s Office on behalf of the District for the repayment of the General Obligation Bonds. Derivative Investments

The District did not directly enter into any derivative investments. Information regarding the amount invested in derivatives by the County Treasury was not available.

4. INVESTMENTS – DISCRETELY PRESENTED COMPONENT UNIT

The Foundation’s investments and cash equivalents include insured or registered investments held by the Foundation or its agent in the Foundation’s name. Insured mechanisms include the Securities Investor Protection Corporation (SIPC), and supplemental protection through underwriters at Lloyd’s of London and the Federal Deposit Insurance Corporation (FDIC). The Foundation’s cash, cash equivalents, and investments as of June 30, 2010, are classified in the accompanying financial statements as follows:

Statement of net assets: Restricted Investments $ 21,286,643Cash and Cash Equivalents 2,609,823

Total Cash, cash equivalents, and investments $ 23,896,466

Investments Authorized by the Foundation’s Investment Policy

The table below identifies the investment types that are authorized for the Foundation by the Foundation’s investment policy. The table also identifies certain provisions of the Foundation’s investment policy that address interest rate risk, credit risk and concentration of credit risk.

Authorized Investment Type Strategic

Allocation Maximum Percentage

US Large cap equities 30% 40% US Small cap equities 7.5% 12% International equities 17.5% 25% Real estate (securitized) 5% 7.5% Fixed income 30% 40% Alternative investments (Hedge funds) 10% 13% Tactical/opportunistic 0% 20%

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

32

The table above does not apply to Doyle funds, charitable remainder trust funds, Foundation holding accounts, or any assets held separate from the investment assets for specific purpose deemed necessary by the Foundation’s Investment Committee. Per the Foundation investment policy, Doyle funds are to be invested only in cash equivalents, certificates of deposit, and US Treasury bonds, with the exception of stock in Exchange Bank that is currently held within the Doyle Fund. Foundation holding accounts are to be segregated and held in separate holding accounts, and investments may include those approved in the above table.

Alternative Investments (Hedge Funds) According to the Foundation’s investment policy, allowable alternative investments include funds of hedge funds and funds of private real estate funds. A fund-of-funds is an investment in which an investment manager invests in hedge funds of multiple underlying investment advisors. Hedge funds are private investments, generally structured as limited partnerships or investment companies. The objective of investing in hedge funds is to diversify the Foundation’s investment portfolio, complement traditional equity and fixed-income investments, improve the overall performance consistency of the portfolio, and lower the overall risk of the portfolio. Hedge funds are expected to provide diversification by investing in strategies that do not correlate directly with traditional equity and fixed-income investments. Such strategies may utilize short-selling and leverage, and may include investments in common and preferred stock, options, warrants, convertible securities, foreign securities, foreign currencies, commodities, commodity futures, financial futures, derivatives, mortgage-backed and mortgage-related securities, real estate, bonds, and other assets. During the year ended June 30, 2009, the Foundation invested $1,795,000 in the Pointer Offshore Ltd fund-of-funds, with a fair value at June 30, 2010, of $2,260,384.

Interest Rate Risk

Changes in market interest rates will adversely affect the fair value of an investment, resulting in interest rate risk. Generally, the longer the maturity of an investment, the greater the sensitivity of its fair value to changes in market interest rates. One of the ways to manage exposure to interest rate risk is by purchasing a combination of shorter term and longer term investments and by timing cash flows from maturities so that a portion of the portfolio is maturing or coming close to maturity evenly over time as necessary to provide the cash flow and liquidity needed for operations.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

33

Information about the sensitivity of fair values of the investments to market interest rate fluctuations is provided by the following table that shows the distribution of the investments by maturity:

Remaining Maturity (in Years)

Investment Type

Total Market Value

Less than 1 Year 1 to 5 Years

5 to 10 Years

Greater than

10 Years

US Treasury notes $ 987,336 $ 84,840 $ 243,148 $ 659,348 Other government

notes/bonds 1,009,211 624,391 384,820 International bonds 19,885 19,885 Corporate bonds 1,537,324 626,805 910,519 Municipal bonds 121,396 25,820 95,576 Common stock 6,313,871 6,313,871 Mortgage securities 659,098 74,790 72,563 $ 511,745Closed-end funds 3,754,353 3,754,353 Alternative

investments 2,260,384 2,260,384 Fixed income mutual

funds 2,244,337 2,244,337 Equity mutual funds 2,329,080 2,329,080 Certificates of deposit 50,368 50,368 Cash 943,936 943,936 Money market 1,665,887 1,665,887

$ 23,896,466 $ 19,647,056 $ 1,594,954 $ 2,142,711 $ 511,745

Highly Sensitive Investments

Mortgage backed securities are highly sensitive to interest rate fluctuations (to a greater degree than already indicated in the information provided in the previous table). These securities are subject to early payment in a period of declining interest rates. The resultant reduction in expected total cash flows affects the fair value of these securities and makes the fair values of these securities highly sensitive to changes in interest rates.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

34

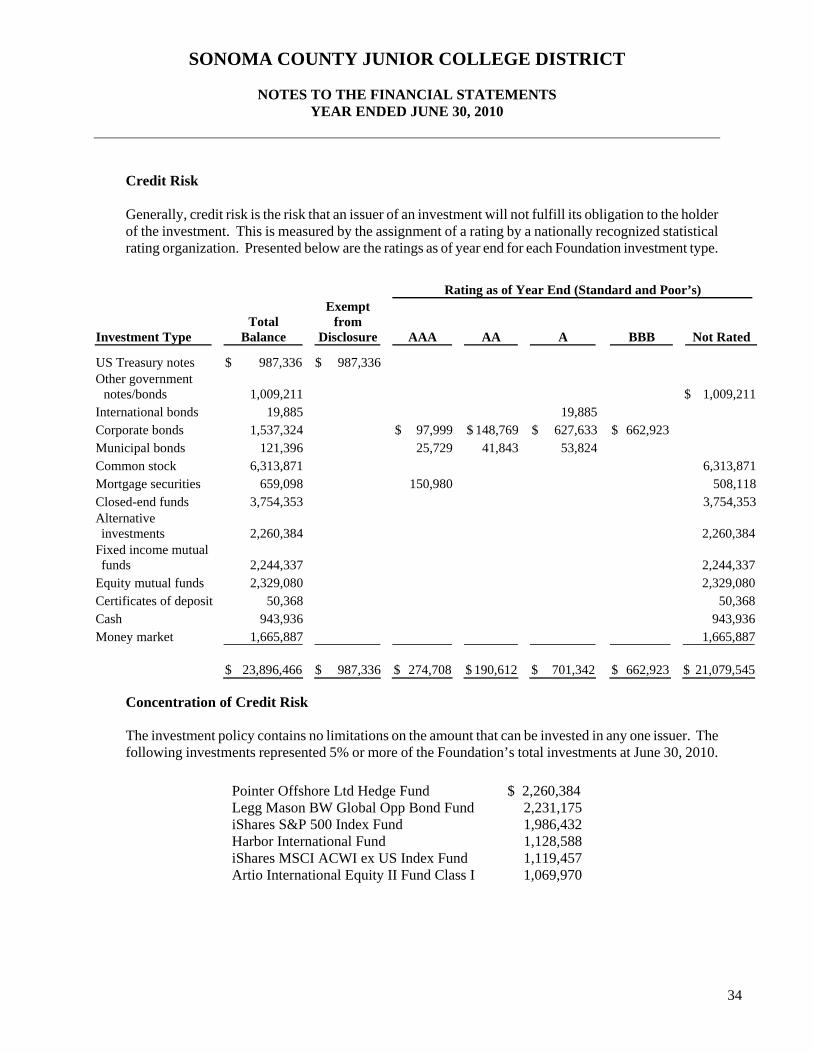

Credit Risk

Generally, credit risk is the risk that an issuer of an investment will not fulfill its obligation to the holder of the investment. This is measured by the assignment of a rating by a nationally recognized statistical rating organization. Presented below are the ratings as of year end for each Foundation investment type.

Rating as of Year End (Standard and Poor’s)

Investment Type Total

Balance

Exempt from

Disclosure AAA AA A BBB Not Rated

US Treasury notes $ 987,336 $ 987,336 Other government

notes/bonds 1,009,211 $ 1,009,211 International bonds 19,885 19,885 Corporate bonds 1,537,324 $ 97,999 $ 148,769 $ 627,633 $ 662,923 Municipal bonds 121,396 25,729 41,843 53,824 Common stock 6,313,871 6,313,871 Mortgage securities 659,098 150,980 508,118 Closed-end funds 3,754,353 3,754,353 Alternative investments 2,260,384 2,260,384

Fixed income mutual funds 2,244,337 2,244,337

Equity mutual funds 2,329,080 2,329,080 Certificates of deposit 50,368 50,368 Cash 943,936 943,936 Money market 1,665,887 1,665,887

$ 23,896,466 $ 987,336 $ 274,708 $ 190,612 $ 701,342 $ 662,923 $ 21,079,545 Concentration of Credit Risk

The investment policy contains no limitations on the amount that can be invested in any one issuer. The following investments represented 5% or more of the Foundation’s total investments at June 30, 2010.

Pointer Offshore Ltd Hedge Fund $ 2,260,384 Legg Mason BW Global Opp Bond Fund 2,231,175iShares S&P 500 Index Fund 1,986,432Harbor International Fund 1,128,588iShares MSCI ACWI ex US Index Fund 1,119,457Artio International Equity II Fund Class I 1,069,970

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

35

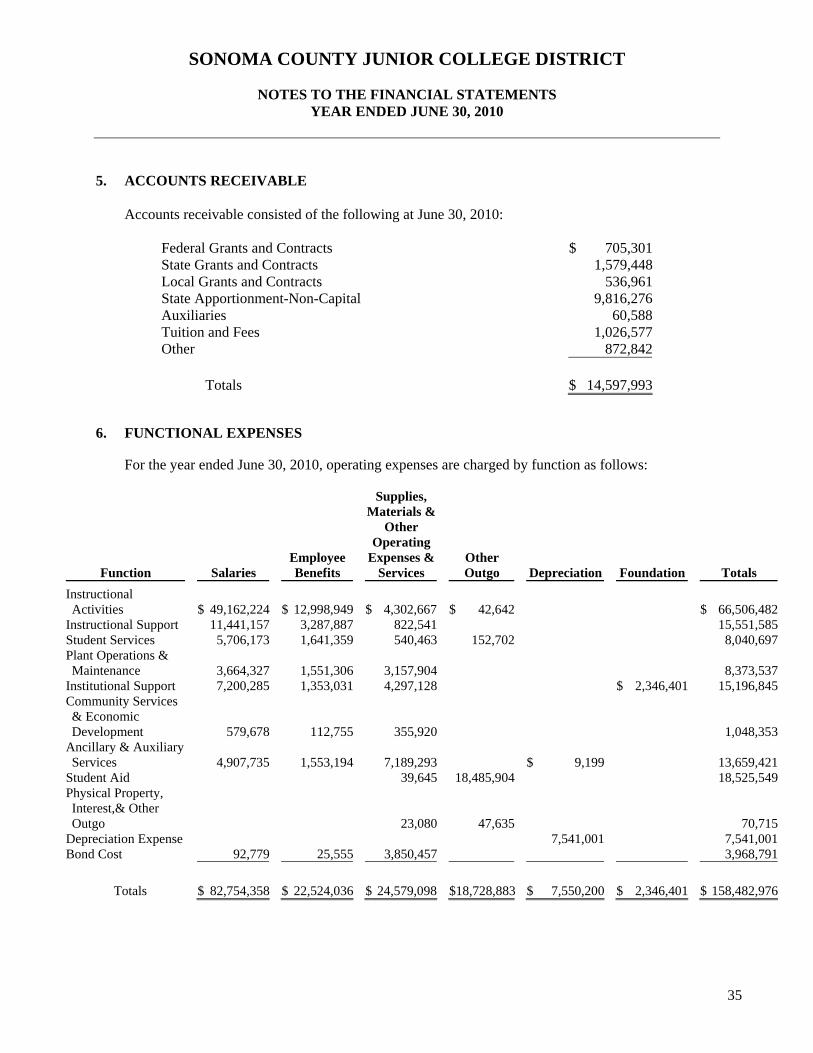

5. ACCOUNTS RECEIVABLE

Accounts receivable consisted of the following at June 30, 2010:

Federal Grants and Contracts $ 705,301State Grants and Contracts 1,579,448Local Grants and Contracts 536,961State Apportionment-Non-Capital 9,816,276Auxiliaries 60,588Tuition and Fees 1,026,577Other 872,842

Totals $ 14,597,993

6. FUNCTIONAL EXPENSES For the year ended June 30, 2010, operating expenses are charged by function as follows:

Function

Salaries Employee Benefits

Supplies, Materials &

Other Operating

Expenses & Services

Other Outgo Depreciation Foundation Totals

Instructional Activities $ 49,162,224 $ 12,998,949 $ 4,302,667 $ 42,642 $ 66,506,482

Instructional Support 11,441,157 3,287,887 822,541 15,551,585Student Services 5,706,173 1,641,359 540,463 152,702 8,040,697Plant Operations & Maintenance 3,664,327 1,551,306 3,157,904 8,373,537

Institutional Support 7,200,285 1,353,031 4,297,128 $ 2,346,401 15,196,845Community Services & Economic Development 579,678 112,755 355,920 1,048,353

Ancillary & Auxiliary Services 4,907,735 1,553,194 7,189,293 $ 9,199 13,659,421

Student Aid 39,645 18,485,904 18,525,549Physical Property, Interest,& Other Outgo 23,080 47,635 70,715

Depreciation Expense 7,541,001 7,541,001Bond Cost 92,779 25,555 3,850,457 3,968,791

Totals $ 82,754,358 $ 22,524,036 $ 24,579,098 $18,728,883 $ 7,550,200 $ 2,346,401 $ 158,482,976

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

36

7. CAPITAL ASSETS AND DEPRECIATION

Capital asset activity for the year ended June 30, 2010 was as follows:

Balance

July 1, 2009 Additions

Decreases/ Reclassific-

ations Balance

June 30, 2010

Capital Assets, Not Depreciated: Land $ 11,966,606 $ 11,966,606Construction in Progress 44,943,867 $ 12,157,596 $ 52,111,231 4,990,232

Total Capital Assets, Not Depreciated 56,910,473 12,157,596 52,111,231 16,956,838

Capital assets, Depreciated: Buildings 277,581,535 53,419,054 331,000,589Improvement of Sites 9,832,020 9,832,020Vehicles 3,502,713 21,948 46,001 3,478,659Restricted – Machinery and Equipment 2,022,652 82,080 5,374 2,099,358Machinery and Equipment 10,964,699 418,504 32,902 11,350,301

Total Capital Assets, Depreciated 303,903,619 53,941,585 84,277 357,760,927

Less Accumulated Depreciation for: Buildings 32,088,217 6,558,144 48,699 38,597,662Improvement of Sites 7,989,364 178,652 8,168,016Vehicles 2,622,314 184,458 38,125 2,768,647Restricted – Machinery and Equipment 1,090,092 198,814 5,320 1,283,586Machinery and Equipment 7,844,140 430,132 22,075 8,252,197

Total Accumulated Depreciation 51,634,127 7,550,200 114,219 59,070,108

Total Capital Assets, Depreciated, Net 252,269,492 46,391,385 (29,942) 298,690,819

Capital Assets, Net $ 309,179,965 $ 58,548,981 $ 52,081,289 $ 315,647,657

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

37

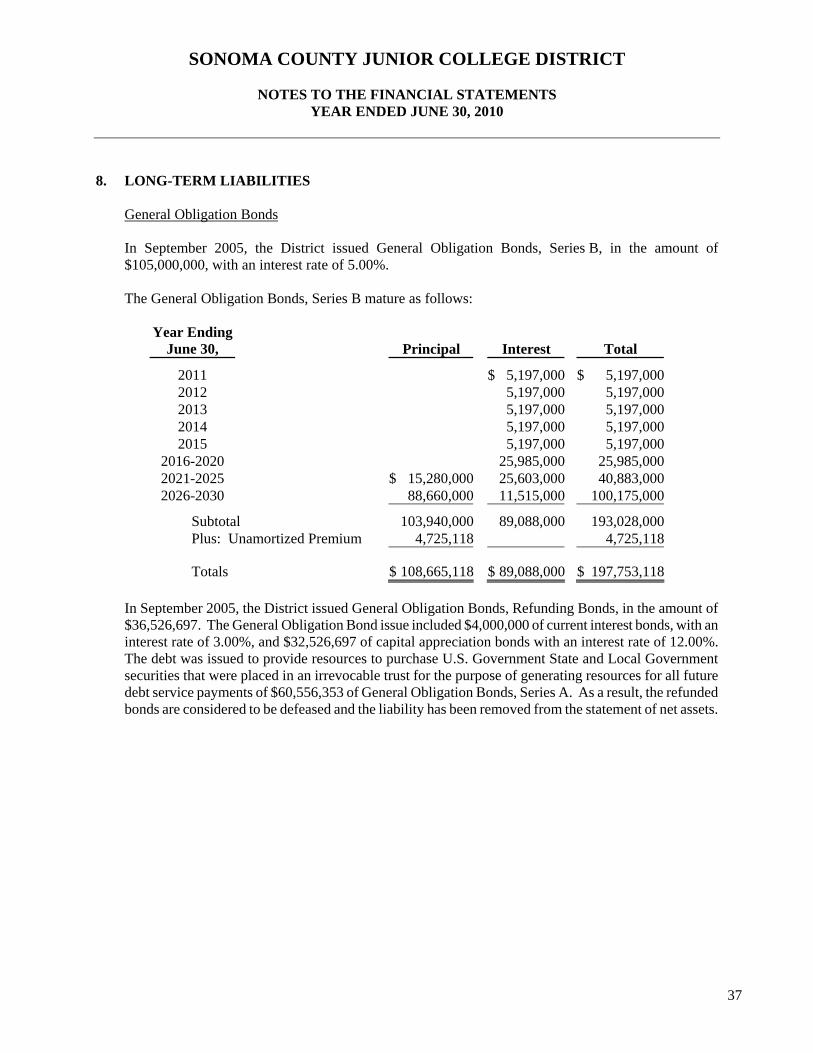

8. LONG-TERM LIABILITIES General Obligation Bonds In September 2005, the District issued General Obligation Bonds, Series B, in the amount of $105,000,000, with an interest rate of 5.00%. The General Obligation Bonds, Series B mature as follows:

Year Ending June 30, Principal Interest Total

2011 $ 5,197,000 $ 5,197,0002012 5,197,000 5,197,0002013 5,197,000 5,197,0002014 5,197,000 5,197,0002015 5,197,000 5,197,000

2016-2020 25,985,000 25,985,0002021-2025 $ 15,280,000 25,603,000 40,883,0002026-2030 88,660,000 11,515,000 100,175,000

Subtotal 103,940,000 89,088,000 193,028,000Plus: Unamortized Premium 4,725,118 4,725,118

Totals $ 108,665,118 $ 89,088,000 $ 197,753,118 In September 2005, the District issued General Obligation Bonds, Refunding Bonds, in the amount of $36,526,697. The General Obligation Bond issue included $4,000,000 of current interest bonds, with an interest rate of 3.00%, and $32,526,697 of capital appreciation bonds with an interest rate of 12.00%. The debt was issued to provide resources to purchase U.S. Government State and Local Government securities that were placed in an irrevocable trust for the purpose of generating resources for all future debt service payments of $60,556,353 of General Obligation Bonds, Series A. As a result, the refunded bonds are considered to be defeased and the liability has been removed from the statement of net assets.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

38

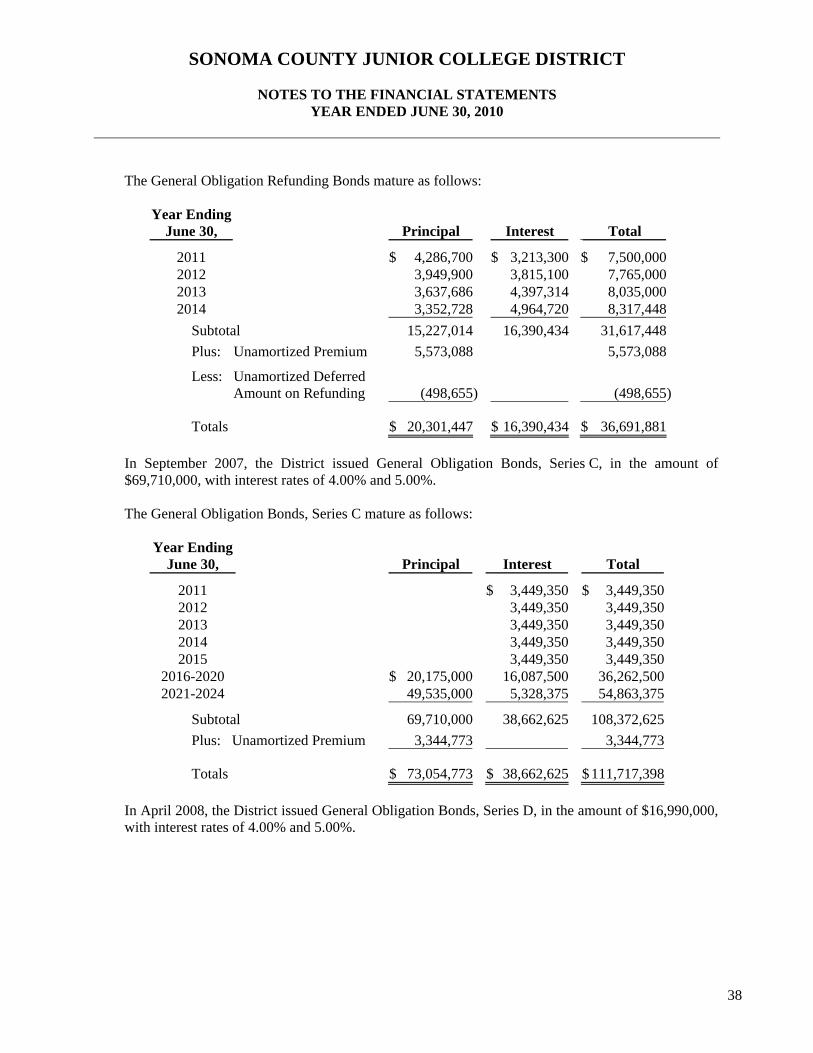

The General Obligation Refunding Bonds mature as follows:

Year Ending June 30, Principal Interest

Total

2011 $ 4,286,700 $ 3,213,300 $ 7,500,0002012 3,949,900 3,815,100 7,765,0002013 3,637,686 4,397,314 8,035,0002014 3,352,728 4,964,720 8,317,448

Subtotal 15,227,014 16,390,434 31,617,448

Plus: Unamortized Premium 5,573,088 5,573,088

Less: Unamortized Deferred Amount on Refunding (498,655) (498,655)

Totals $ 20,301,447 $ 16,390,434 $ 36,691,881 In September 2007, the District issued General Obligation Bonds, Series C, in the amount of $69,710,000, with interest rates of 4.00% and 5.00%. The General Obligation Bonds, Series C mature as follows:

Year Ending June 30, Principal Interest Total

2011 $ 3,449,350 $ 3,449,3502012 3,449,350 3,449,3502013 3,449,350 3,449,3502014 3,449,350 3,449,3502015 3,449,350 3,449,350

2016-2020 $ 20,175,000 16,087,500 36,262,5002021-2024 49,535,000 5,328,375 54,863,375

Subtotal 69,710,000 38,662,625 108,372,625

Plus: Unamortized Premium 3,344,773 3,344,773

Totals $ 73,054,773 $ 38,662,625 $ 111,717,398 In April 2008, the District issued General Obligation Bonds, Series D, in the amount of $16,990,000, with interest rates of 4.00% and 5.00%.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

39

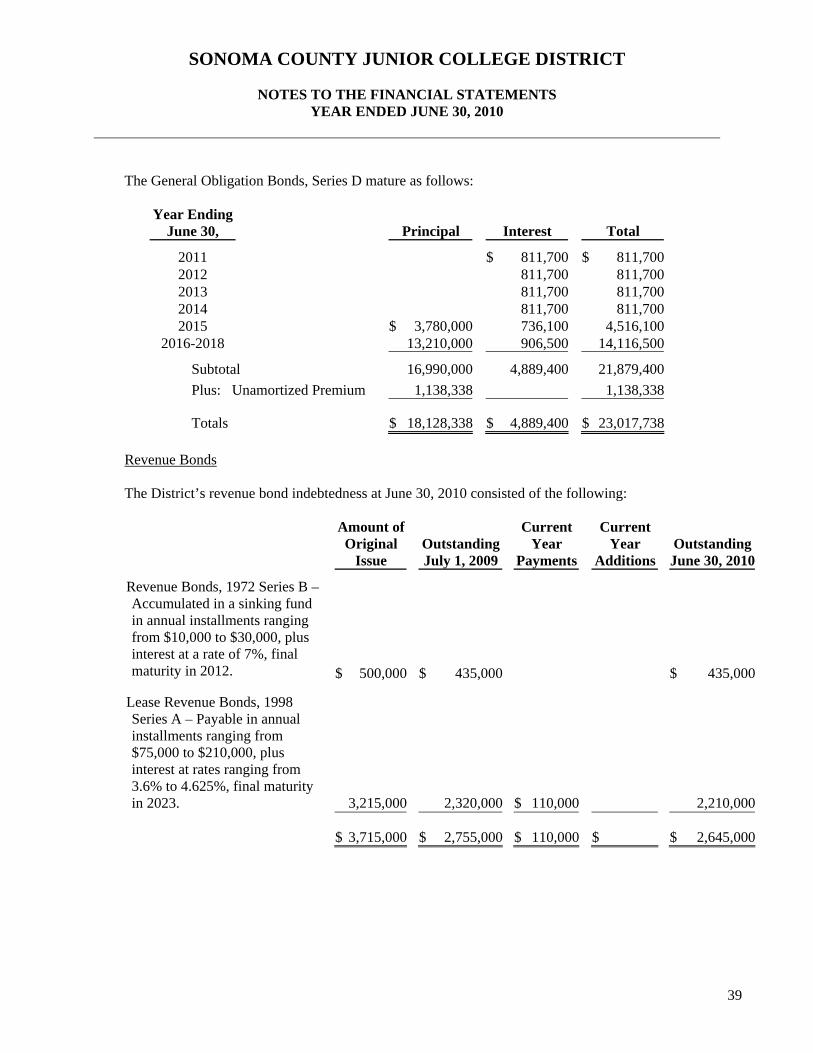

The General Obligation Bonds, Series D mature as follows:

Year Ending June 30, Principal Interest Total

2011 $ 811,700 $ 811,7002012 811,700 811,7002013 811,700 811,7002014 811,700 811,7002015 $ 3,780,000 736,100 4,516,100

2016-2018 13,210,000 906,500 14,116,500

Subtotal 16,990,000 4,889,400 21,879,400

Plus: Unamortized Premium 1,138,338 1,138,338

Totals $ 18,128,338 $ 4,889,400 $ 23,017,738 Revenue Bonds

The District’s revenue bond indebtedness at June 30, 2010 consisted of the following:

Amount ofOriginal

Issue OutstandingJuly 1, 2009

Current Year

Payments

Current Year

Additions

OutstandingJune 30, 2010

Revenue Bonds, 1972 Series B – Accumulated in a sinking fund in annual installments ranging from $10,000 to $30,000, plus interest at a rate of 7%, final maturity in 2012.

$ 500,000

$ 435,000

$ 435,000

Lease Revenue Bonds, 1998 Series A – Payable in annual installments ranging from $75,000 to $210,000, plus interest at rates ranging from 3.6% to 4.625%, final maturity in 2023.

3,215,000 2,320,000

$ 110,000 2,210,000

$ 3,715,000 $ 2,755,000 $ 110,000 $ $ 2,645,000

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

40

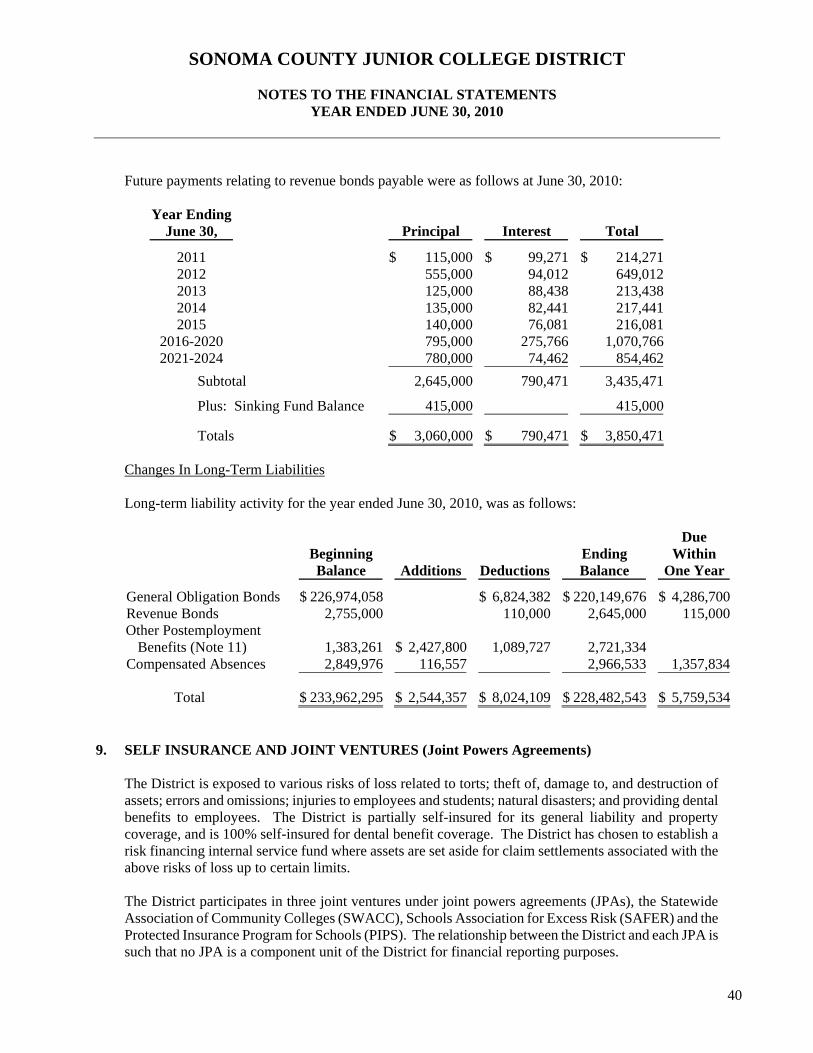

Future payments relating to revenue bonds payable were as follows at June 30, 2010:

Year Ending June 30,

Principal

Interest

Total

2011 $ 115,000 $ 99,271 $ 214,2712012 555,000 94,012 649,0122013 125,000 88,438 213,4382014 135,000 82,441 217,4412015 140,000 76,081 216,081

2016-2020 795,000 275,766 1,070,7662021-2024 780,000 74,462 854,462

Subtotal 2,645,000 790,471 3,435,471

Plus: Sinking Fund Balance 415,000 415,000

Totals $ 3,060,000 $ 790,471 $ 3,850,471

Changes In Long-Term Liabilities

Long-term liability activity for the year ended June 30, 2010, was as follows:

Beginning Balance

Additions

Deductions

Ending Balance

Due Within

One Year

General Obligation Bonds $ 226,974,058 $ 6,824,382 $ 220,149,676 $ 4,286,700Revenue Bonds 2,755,000 110,000 2,645,000 115,000Other Postemployment

Benefits (Note 11) 1,383,261 $ 2,427,800 1,089,727 2,721,334Compensated Absences 2,849,976 116,557 2,966,533 1,357,834

Total $ 233,962,295 $ 2,544,357 $ 8,024,109 $ 228,482,543 $ 5,759,534 9. SELF INSURANCE AND JOINT VENTURES (Joint Powers Agreements)

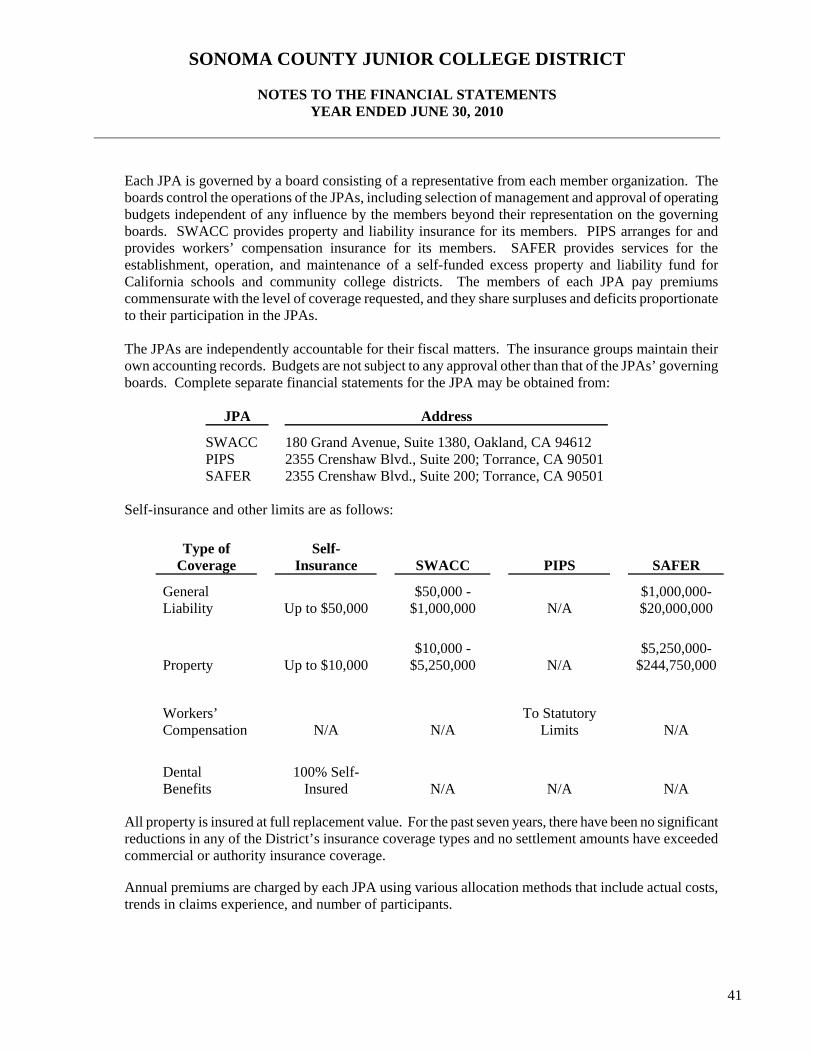

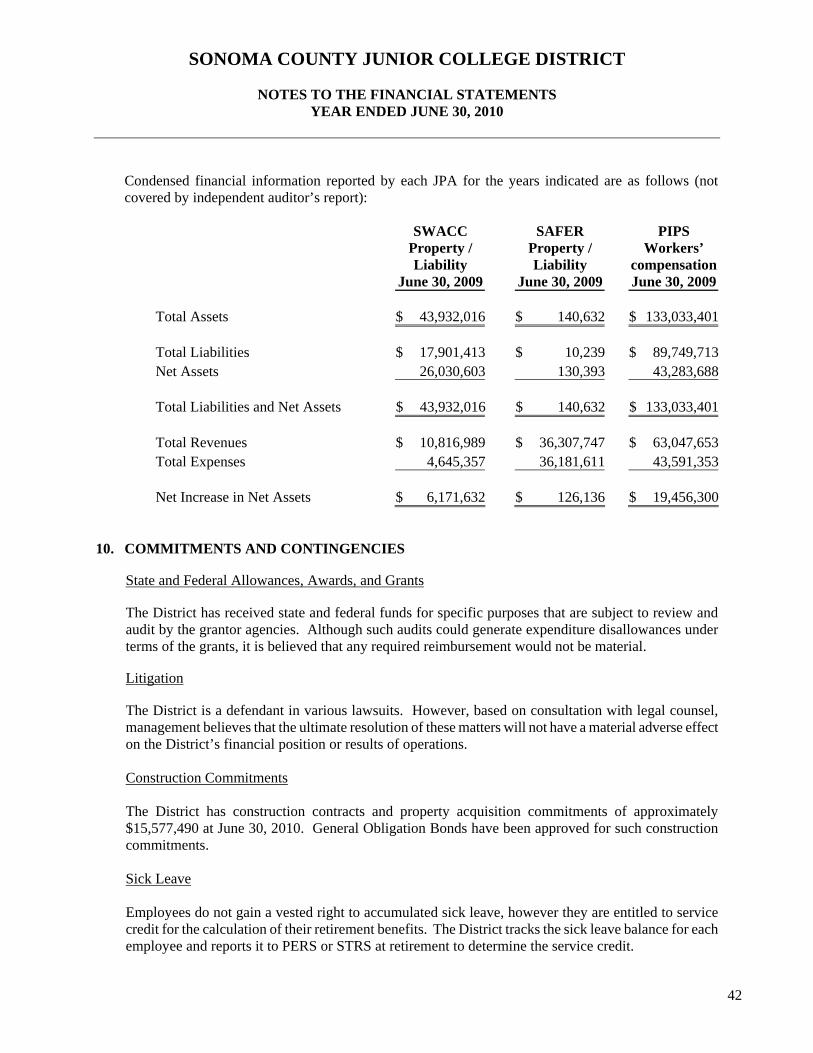

The District is exposed to various risks of loss related to torts; theft of, damage to, and destruction of assets; errors and omissions; injuries to employees and students; natural disasters; and providing dental benefits to employees. The District is partially self-insured for its general liability and property coverage, and is 100% self-insured for dental benefit coverage. The District has chosen to establish a risk financing internal service fund where assets are set aside for claim settlements associated with the above risks of loss up to certain limits. The District participates in three joint ventures under joint powers agreements (JPAs), the Statewide Association of Community Colleges (SWACC), Schools Association for Excess Risk (SAFER) and the Protected Insurance Program for Schools (PIPS). The relationship between the District and each JPA is such that no JPA is a component unit of the District for financial reporting purposes.

SONOMA COUNTY JUNIOR COLLEGE DISTRICT

NOTES TO THE FINANCIAL STATEMENTS YEAR ENDED JUNE 30, 2010

41