Embed Size (px)

Citation preview

“Solid and profitable with potential for growth”

1

JP Morgan London Small/Mid Cap Conference September 8th; 2015

Disclaimer

2

This document has been prepared by NATURHOUSE HEALTH S.A. (“NATURHOUSE” or the “Company”) for its exclusive use during the presentations to investors. NATURHOUSE does not authorise its dissemination, publication or use by any other person, whether physical or legal, to an end other than that which has been expressed above, unless they have prior express consent in writing from NATURHOUSE, and neither does it, consequently, accept any responsibility for the content of the document if it is used to an end other than that expressed above without the authorisation of the Company. Readers are warned that the information in this document has not been audited by the Company’s auditors and it has been summarised. The information and the opinions and statements contained in this document have not been verified by independent third parties and, unless another source is expressly mentioned, they have been drawn up by the Company. This document contains forecasts and estimates relating to the business progress or results of the Company in the future. These forecasts respond to the current opinion and expectations of NATURHOUSE HEALTH, S.A. These forecasts, that are uncertain by nature, are affected by risks, including those mentioned in the prospectus for the IPO and the offering and listing of NATURHOUSE shares, approved by the CNMV (Spanish stock exchange commission) and recorded in its official register on 9 April 2015, and it is available to investors on the issuer’s website (www.naturhouse.com) and that of the CNMV (www.cnmv.es). These risks may cause real results to be significantly different to said forecasts or estimates. The contents of this document must be taken into account by all individuals or entities that may have to make decisions or draw up or disseminate opinions regarding shares issued by NATURHOUSE HEALTH SA, and in particular by the analysts that make use of this document. This document is not an offer of sale or subscription and neither is it an invitation to subscribe to or acquire NATURHOUSE shares or any other securities in Spain or in any other jurisdiction.

Contents

Description of the business model

The Naturhouse Method

Naturhouse Centres

Contractual Framework: Franchises and Master Franchises

International Growth

Main Figures

Centres

Main Figures from the Profit and Loss Account

Net Cash Position and Dividends

Strategy and Outlook

Naturhouse vs. Peers

Conclusions

3

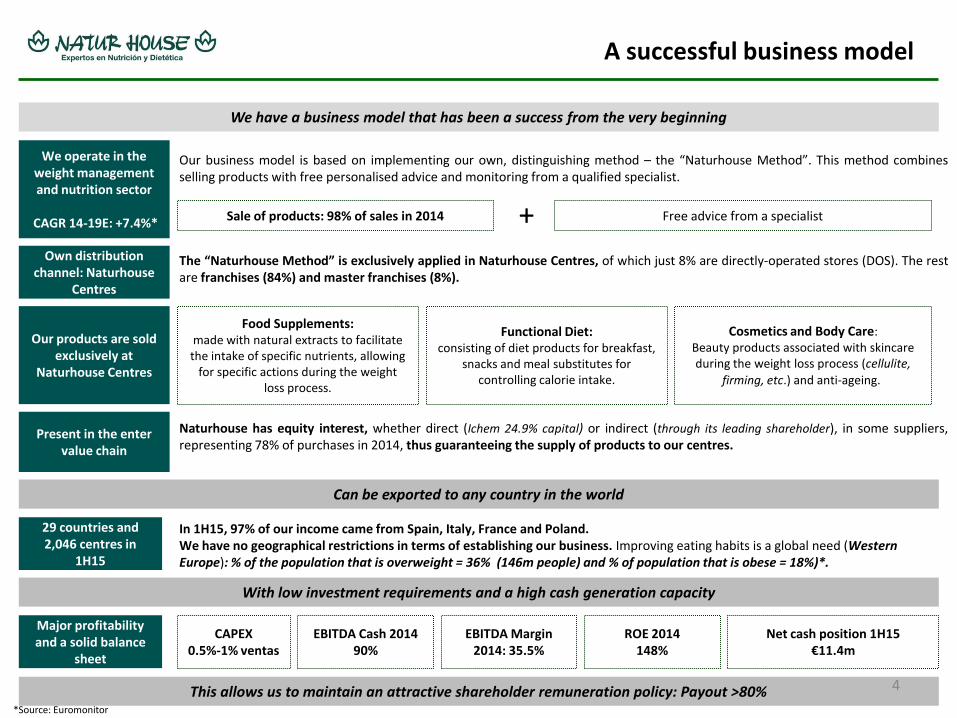

Our business model is based on implementing our own, distinguishing method – the “Naturhouse Method”. This method combines selling products with free personalised advice and monitoring from a qualified specialist.

The “Naturhouse Method” is exclusively applied in Naturhouse Centres, of which just 8% are directly-operated stores (DOS). The rest are franchises (84%) and master franchises (8%). Naturhouse has equity interest, whether direct (Ichem 24.9% capital) or indirect (through its leading shareholder), in some suppliers, representing 78% of purchases in 2014, thus guaranteeing the supply of products to our centres. In 1H15, 97% of our income came from Spain, Italy, France and Poland. We have no geographical restrictions in terms of establishing our business. Improving eating habits is a global need (Western Europe): % of the population that is overweight = 36% (146m people) and % of population that is obese = 18%)*.

A successful business model

We operate in the weight management and nutrition sector

CAGR 14-19E: +7.4%*

Sale of products: 98% of sales in 2014 Free advice from a specialist

Own distribution channel: Naturhouse

Centres

We have a business model that has been a success from the very beginning

Our products are sold exclusively at

Naturhouse Centres

Present in the enter value chain

Can be exported to any country in the world

29 countries and 2,046 centres in

1H15

Food Supplements: made with natural extracts to facilitate the intake of specific nutrients, allowing

for specific actions during the weight loss process.

Functional Diet: consisting of diet products for breakfast,

snacks and meal substitutes for controlling calorie intake.

Cosmetics and Body Care: Beauty products associated with skincare during the weight loss process (cellulite,

firming, etc.) and anti-ageing..

Major profitability and a solid balance

sheet

With low investment requirements and a high cash generation capacity

This allows us to maintain an attractive shareholder remuneration policy: Payout >80%

CAPEX 0.5%-1% ventas

EBITDA Cash 2014 90%

EBITDA Margin 2014: 35.5%

ROE 2014 148%

Net cash position 1H15 €11.4m

4

+

*Source: Euromonitor

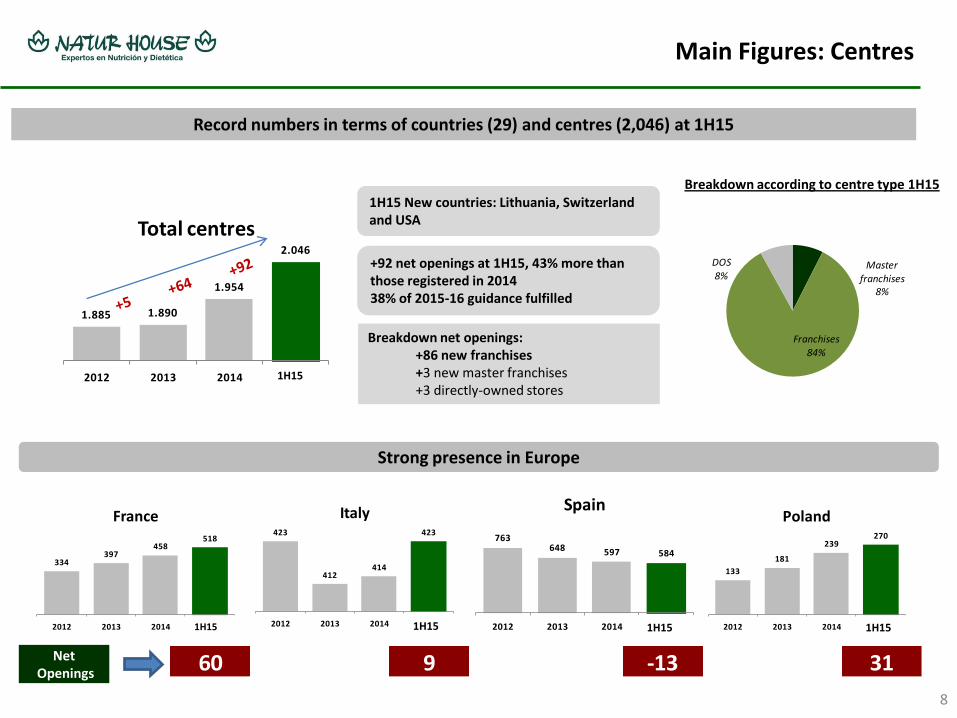

Masterfranchises

8%

Franchises

84%

DOS

8%

Naturhouse Centres

Main characteristics Located in commercial areas with considerable foot traffic Divided into two areas – consultation area and sales area Covering a surface area of between 30m2 and 50m2 All have a similar aesthetic

Centre types

Directly-owned centres are managed by the company with its own staff. They tend to be the laboratories for new ideas for the Group’s other centres as well as a training hub for employees and franchisees. They are also the foundation for growth in new countries.

Franchised centres are Naturhouse Centres operated by third parties under the franchise model.

In addition, Naturhouse has contracts called ‘master franchises’, through which a third party can exclusively operate Naturhouse’s business for a whole country.

Breakdown according to centre type at 1H15 Rapid growth

2,046 centres and 29 countries

Major flexibility

Reduces the need for investment

CAPEX: 0.5%-1% sales

and human capital 440 employees on average in

1H15

Franchises as a channel for growth

Directly-operated stores (DOS)

Franchises

Master Franchises

5

Contractual Framework

Franchises

Duration 5 years. 90% of franchisees have renewed their contract for another 5 years after the first 5-year period.

Main economic points No initial franchise fee Annual franchise fee of €600 + VAT Gross Margin of 60% Compulsory investment of 5% of product purchases in advertising for the store or the Naturhouse brand Payment when placing an order or with a bank guarantee at 30 days Minimum stock: €7,000 (stock rotation every 15 days) Initial investment: €10,000-€40,000 depending on the country

Agreements Obligation to sell only Naturhouse products Non-competition agreement for 1 year after the end of the contract

Support for the franchisee The right to use the Naturhouse brand Use of Peso Perfecto magazine to promote the Naturhouse Method Support from Naturhouse regarding strategy, products, know-how, etc.

Master Franchises Duration 7 years

Main economic points Initial franchise fee of between €50,000 and €300,000

Agreements Obligation to open a specific number of centres during the contracted period

Support for the master franchisee The right to use the Naturhouse brand Use of Peso Perfecto magazine to promote the Naturhouse Method Support from Naturhouse regarding strategy, products, know-how, etc

The master franchisee is responsible for the costs of registering the product and the necessary investment for implementing the

business (staff, furniture and fittings, alteration work on premises, etc.).

6

International Growth

Subsidiaries

Master Franchises

1,882 164

29 countries 2,046 centres at end 1H15

Subsidiaries

Master Franchises

Legal certainty High per capita income High population density levels

Low levels of legal certainty Low per capita income Low population density levels

79% of sales and 83% of EBITDA came from outside Spain at

1H15

7

France Spain Italy Poland Portugal Belgium Germany UK Mexico Canada Lithuania USA

Czech Republic Romania Slovakia Belgium - Master Morocco Croatia Bulgaria Slovenia Peru UAE Dominican Republic Mauritius Philippines Russia Gibraltar* Andorra* Panama Switzerland

Masterfranchises

8%

Franchises

84%

DOS

8%

1.885 1.890

1.954

2.046

2012 2013 2014 1S15

Total centres

Main Figures: Centres

8

Net Openings

60 9 -13 31

334397

458518

2012 2013 2014 1S15

France423

412414

423

2012 2013 2014 1S15

Italy

763648 597 584

2012 2013 2014 1S15

Spain

133

181

239270

2012 2013 2014 1S15

Poland

Breakdown net openings: +86 new franchises +3 new master franchises +3 directly-owned stores

Strong presence in Europe

+92

Record numbers in terms of countries (29) and centres (2,046) at 1H15

+92 net openings at 1H15, 43% more than those registered in 2014 38% of 2015-16 guidance fulfilled

1H15 New countries: Lithuania, Switzerland and USA

Breakdown according to centre type 1H15

1H15

1H15 1H15 1H15 1H15

9.669

19.047

22.758

12.976 13.284

2012 2013 2014 1H14 1H15

Net Income

26,5%

32,8%35,5% 36,5% 36,8%

2012 2013 2014 1H14 1H15

EBITDA Margin

22.657

29.483

33.986

19.117 19.365

2012 2013 2014 1H14 1H15

EBITDA

85.594 89.76895.731

52.382 52.556

2012 2013 2014 1H14 1H15

Sales

Main Figures: P&G

Sustained growth in the Group’s main figures since 2012 EBITDA margin above the industry average (+36.8% at 1H15 vs +16%* for the sector)

Figures in Thousands of euros

+0.3% +1.3%

+2.4%

Sales in 1H14 include non recurrent income of €0.25m from the sale of the master franchises for Switzerland and Slovenia and €0.49m from the sale of products to herbal stores, an activity that came to an end in 2014. Without these effects, sales would have grown by 1.8%.

In 1H15, there was a 7% increase in advertising expenditure, as a result of the company’s clear commitment to recovering the market in Spain.

In 1H15 the contribution from Ichem stood at €0.58m, a 41.6% increase vs 1H14.

A sustained improvement in the EBITDA margin due to the constant implementation of operational efficiency measures. A sustained improvement in procurement costs since 2012. 9

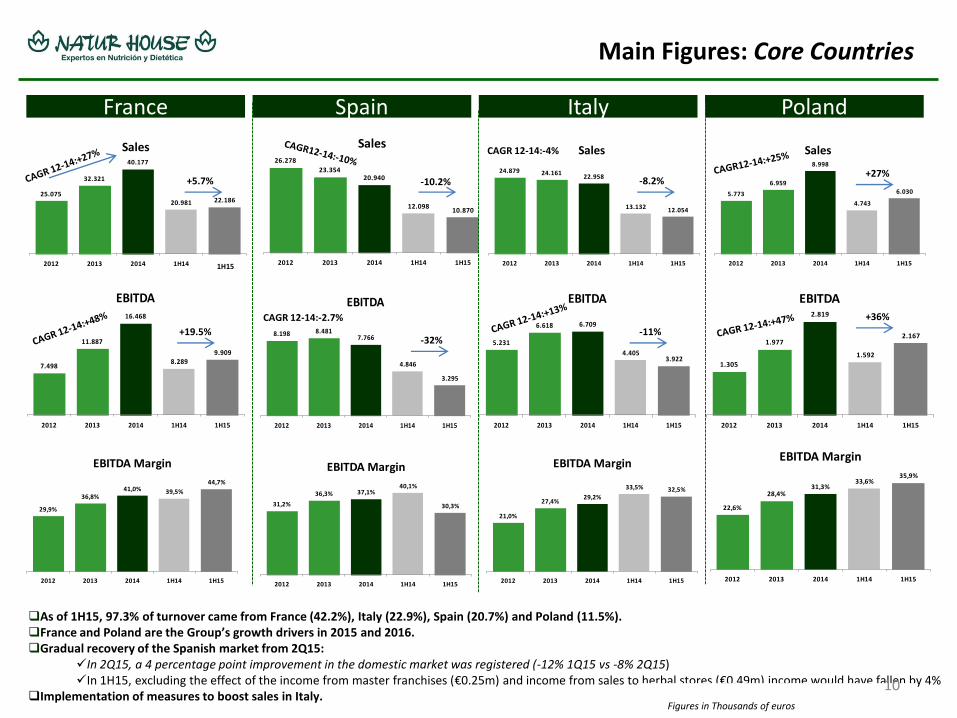

As of 1H15, 97.3% of turnover came from France (42.2%), Italy (22.9%), Spain (20.7%) and Poland (11.5%). France and Poland are the Group’s growth drivers in 2015 and 2016. Gradual recovery of the Spanish market from 2Q15:

In 2Q15, a 4 percentage point improvement in the domestic market was registered (-12% 1Q15 vs -8% 2Q15) In 1H15, excluding the effect of the income from master franchises (€0.25m) and income from sales to herbal stores (€0.49m) income would have fallen by 4%

Implementation of measures to boost sales in Italy.

Figures in Thousands of euros

22,6%

28,4%31,3%

33,6%35,9%

2012 2013 2014 1H14 1H15

EBITDA Margin

21,0%

27,4%29,2%

33,5% 32,5%

2012 2013 2014 1H14 1H15

EBITDA Margin

31,2%

36,3% 37,1%40,1%

30,3%

2012 2013 2014 1H14 1H15

EBITDA Margin

1.305

1.977

2.819

1.592

2.167

2012 2013 2014 1H14 1H15

EBITDA

5.773

6.959

8.998

4.743

6.030

2012 2013 2014 1H14 1H15

Sales

8.198 8.4817.766

4.846

3.295

2012 2013 2014 1H14 1H15

EBITDA

26.278

23.35420.940

12.09810.870

2012 2013 2014 1H14 1H15

Sales

5.231

6.618 6.709

4.4053.922

2012 2013 2014 1H14 1H15

EBITDA

24.879 24.16122.958

13.132 12.054

2012 2013 2014 1H14 1H15

Sales

29,9%

36,8%41,0% 39,5%

44,7%

2012 2013 2014 1H14 1H15

EBITDA Margin

7.498

11.887

16.468

8.2899.909

2012 2013 2014 1H14 1H15

EBITDA

25.075

32.321

40.177

20.981 22.186

2012 2013 2014 1H14 1H15

Sales

1H15

Main Figures: Core Countries

France Spain Italy Poland

CAGR 12-14:-2.7%

CAGR 12-14:-4%

+5.7%

+19.5%

-10.2%

-32%

-8.2%

-11%

+27%

+36%

10

8.100

11.600

25.675

11.050

2012 2013 2014 1H15

Dividends

Main Figures: Net Cash Position & Dividends

11

La solidez del balance y la retribución al accionista son nuestra prioridad

Figures in thousands of euros

7.338

15.087

10.880 11.402

2012 2013 2014 1H15

Net Cash

Figures in thousands of euros Note 1: Data from 2012, 2013 and 2014 include SAS Naturhouse in all periods Note 2: Of the €11.05m in 1H15, €8.5m correspond almost completely to the income generated by Naturhouse Health SA’s subsidiaries in 2014 and the rest to the income from Naturhouse Health SA and its subsidiaries in 2015, up until 16 March.

A solid balance sheet and shareholder remuneration are our priority

Major cash flow generation capacity: Net Cash at the end of 1H15 of €11.4m, after paying out dividends to the amount of €11.05m. The company distributed an interim dividend of €3m (€0.05 gross per share) on September 4, 2015, ahead of its initial forecast of doing so in 2016.

Attractive remuneration policy for shareholders: Payout >80%.

Naturhouse vs. Peers (1)

12

17

108

IGBM Average Sector Average* Naturhouse

24

19

13

IGBM Average Sector Average* Naturhouse

1416

34

IGBM Average Sector Average* Naturhouse

42

26

80

IGBM Average Sector Average* Naturhouse

30

73

148

IGBM Average Sector Average* Naturhouse

EV/EBITDA P/E EBITDA Margin 2014 (%)

Payout (%) ROE 2014 (%)

(1)Herbalife, Weight Watchers, Nutrisystem, Vitamin Shoppe & GNC

Naturhouse trades with a discount vs peers and the Spanish market Its EBITDA Margin is double the sector average*

It has an attractive shareholder remuneration policy ROE is higher than the IBGM and sector averages

Source: Factset

>

Strategy & Outlook

“A succeful Business Model"

13

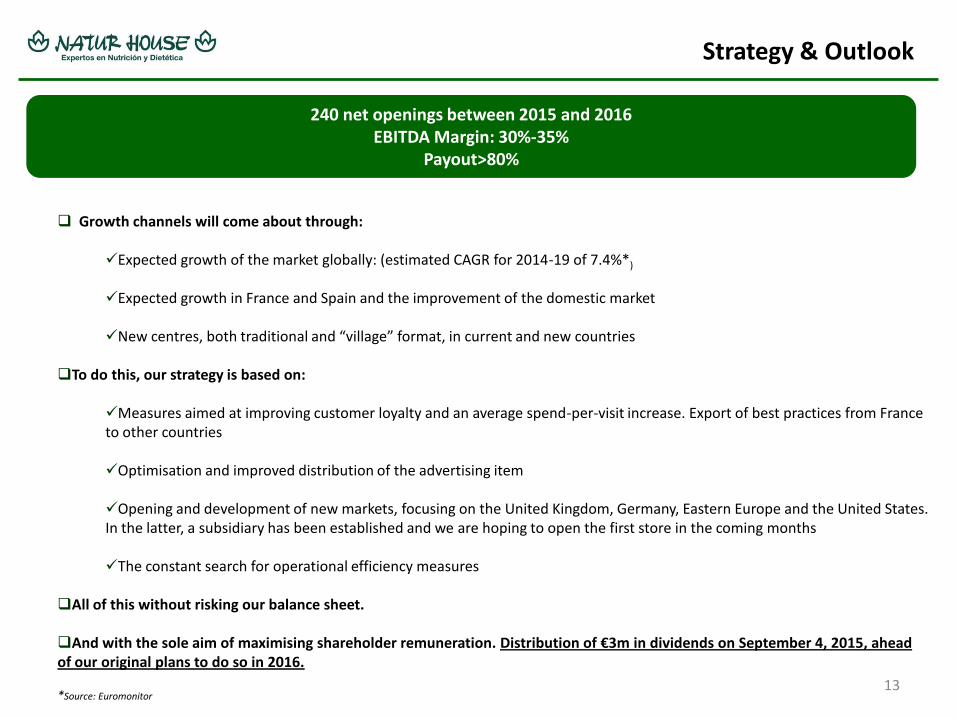

240 net openings between 2015 and 2016 EBITDA Margin: 30%-35%

Payout>80%

Growth channels will come about through:

Expected growth of the market globally: (estimated CAGR for 2014-19 of 7.4%*)

Expected growth in France and Spain and the improvement of the domestic market

New centres, both traditional and “village” format, in current and new countries

To do this, our strategy is based on:

Measures aimed at improving customer loyalty and an average spend-per-visit increase. Export of best practices from France to other countries

Optimisation and improved distribution of the advertising item

Opening and development of new markets, focusing on the United Kingdom, Germany, Eastern Europe and the United States. In the latter, a subsidiary has been established and we are hoping to open the first store in the coming months

The constant search for operational efficiency measures

All of this without risking our balance sheet.

And with the sole aim of maximising shareholder remuneration. Distribution of €3m in dividends on September 4, 2015, ahead of our original plans to do so in 2016. *Source: Euromonitor

Conclusions

*Source: Euromonitor

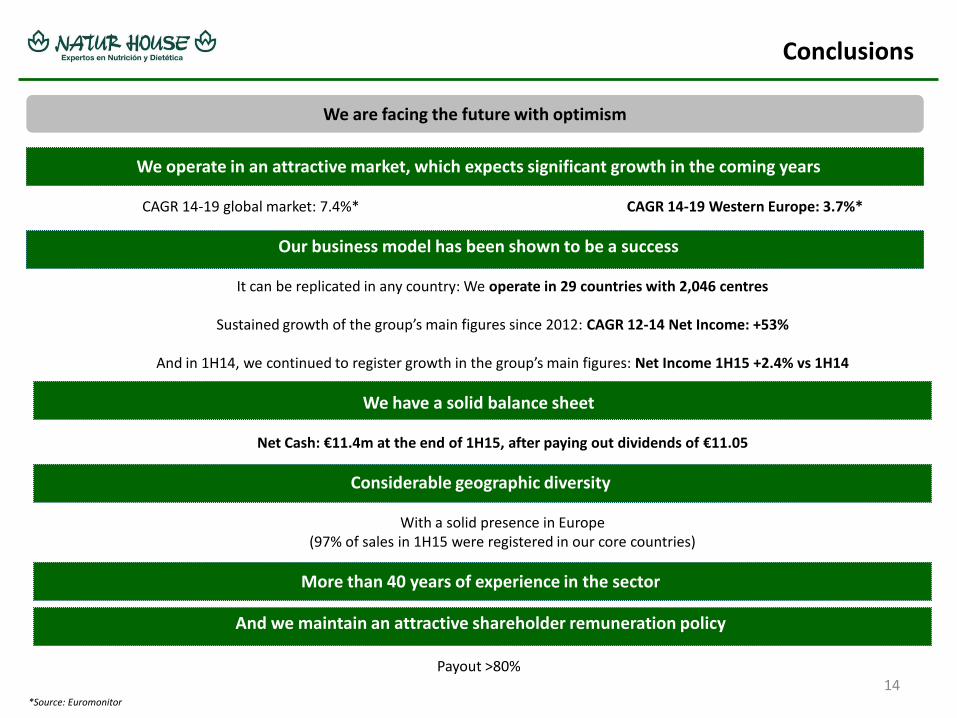

We are facing the future with optimism

We operate in an attractive market, which expects significant growth in the coming years

CAGR 14-19 global market: 7.4%* CAGR 14-19 Western Europe: 3.7%*

Our business model has been shown to be a success

It can be replicated in any country: We operate in 29 countries with 2,046 centres

Sustained growth of the group’s main figures since 2012: CAGR 12-14 Net Income: +53%

And in 1H14, we continued to register growth in the group’s main figures: Net Income 1H15 +2.4% vs 1H14

We have a solid balance sheet

Net Cash: €11.4m at the end of 1H15, after paying out dividends of €11.05

Considerable geographic diversity

With a solid presence in Europe (97% of sales in 1H15 were registered in our core countries)

More than 40 years of experience in the sector

And we maintain an attractive shareholder remuneration policy

Payout >80% 14

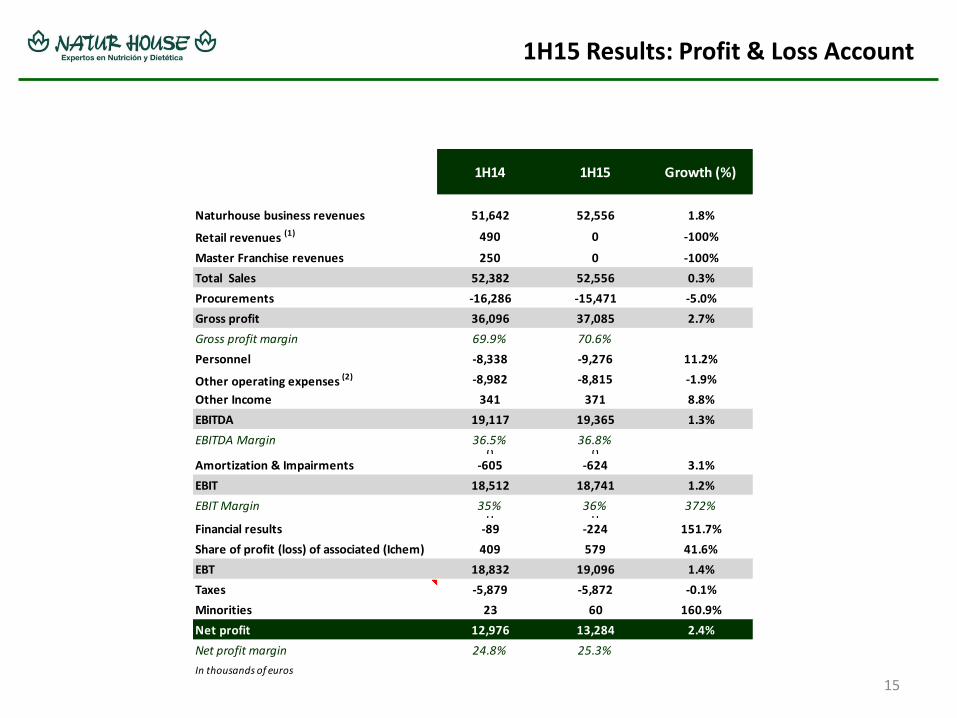

1H15 Results: Profit & Loss Account

15

1H14 1H15 Growth (%)

Naturhouse business revenues 51,642 52,556 1.8%

Retail revenues (1) 490 0 -100%

Master Franchise revenues 250 0 -100%

Total Sales 52,382 52,556 0.3%

Procurements -16,286 -15,471 -5.0%

Gross profit 36,096 37,085 2.7%

Gross profit margin 69.9% 70.6%

Personnel -8,338 -9,276 11.2%

Other operating expenses (2) -8,982 -8,815 -1.9%

Other Income 341 371 8.8%

EBITDA 19,117 19,365 1.3%

EBITDA Margin 36.5% 36.8%0 0

Amortization & Impairments -605 -624 3.1%

EBIT 18,512 18,741 1.2%

EBIT Margin 35% 36% 372%0 0

Financial results -89 -224 151.7%

Share of profit (loss) of associated (Ichem) 409 579 41.6%

EBT 18,832 19,096 1.4%

Taxes -5,879 -5,872 -0.1%

Minorities 23 60 160.9%

Net profit 12,976 13,284 2.4%

Net profit margin 24.8% 25.3%

In thousands of euros

1H15 Results: Balance Sheet

16

2014 1H15

Intangible assets 2,345 2,219

property, plant & equipment 5,522 5,171

Non current financial assets 757 959

Investment in associated companies 2,749 3,317

Deferred tax assets 458 368

Non current Assets 11,831 12,034

Inventories 3,925 3,982

Trade receivables 5,564 7,101

Other current assets 683 741

investment in related companies 11,007 0

Financial assets 42 0

Cash & equivalents 8,659 17,706

Current assets 29,880 29,530

TOTAL ASSETS 41,711 41,564

Equity 15,371 15,877

Non current provisions 798 921

Non current borrowings 4,363 3,045

Long term accrued expenses 456 460

Non current liabilities 5,617 4,426

Current borrowings 4,525 3,259

Financial l iabilities with related companies 2,007 2,040

Suppliers 4,621 5,443

Suppliers related companies 6,369 7,271

Current tax l iabilities and other payables 3,201 3,248

Current liabilities 20,723 21,261

TOTAL LIABILITIES 41,711 41,564

In Thousands of euros

Net cash position of €11.4m at end of 1H15, allowing us to maintain an attractive shareholder remuneration policy.

Payment of interim dividend for the amount of €11.05m (€8.5m almost totally coming from the income of the subsidiaries of Naturhouse Health SA in 2014 and the rest from the income accumulated in 2015 by Naturhouse Health SA and its subsidiaries until 16 March).

29% reduction in the gross financial debt (-€2.6m).

Kiluva SA debt paid off as forecast.

CONTACT

María Pardo Martinez

Investor Relations Manager

Telephone number: +34 914323953

Email: [email protected]

17