Embed Size (px)

DESCRIPTION

Small Business Health Options Program (SHOP). This Training. Four sections to this training: Overview of Tribes and Tribal Entities as Employers Small Business Health Options Program (SHOP) Small Business Tax Credit (Tax Credit) Employer Shared Responsibility. - PowerPoint PPT Presentation

Citation preview

Small Business Health Options Program (SHOP)

Version: August 23, 2013 1

This Training

• Four sections to this training:– Overview of Tribes and Tribal Entities as

Employers – Small Business Health Options Program (SHOP)– Small Business Tax Credit (Tax Credit)– Employer Shared Responsibility

2

Small Business Health Options Program Topics

• What is SHOP?• SHOP Functions• Comparison with Individual Marketplace• Eligibility, Definitions & Application• SHOP Plans• Enrollment, Contributions, & Premium

Aggregation

3

What is SHOP?

4

What is SHOP?• SHOP = Small Business Health Options Program • Designed to help small businesses purchase health

insurance for employees.

• Each State will have a Marketplace (a/k/a Exchange) where individuals and small businesses can shop for health insurance. • State, Federally-facilitated (FF), Partnership & Hybrid model

in pending regulations (e.g., only SHOP run by State)

• Tribes and Tribal entities are eligible to participate.• The SHOP will allow an employer to compare plans

based on price, coverage and quality.5

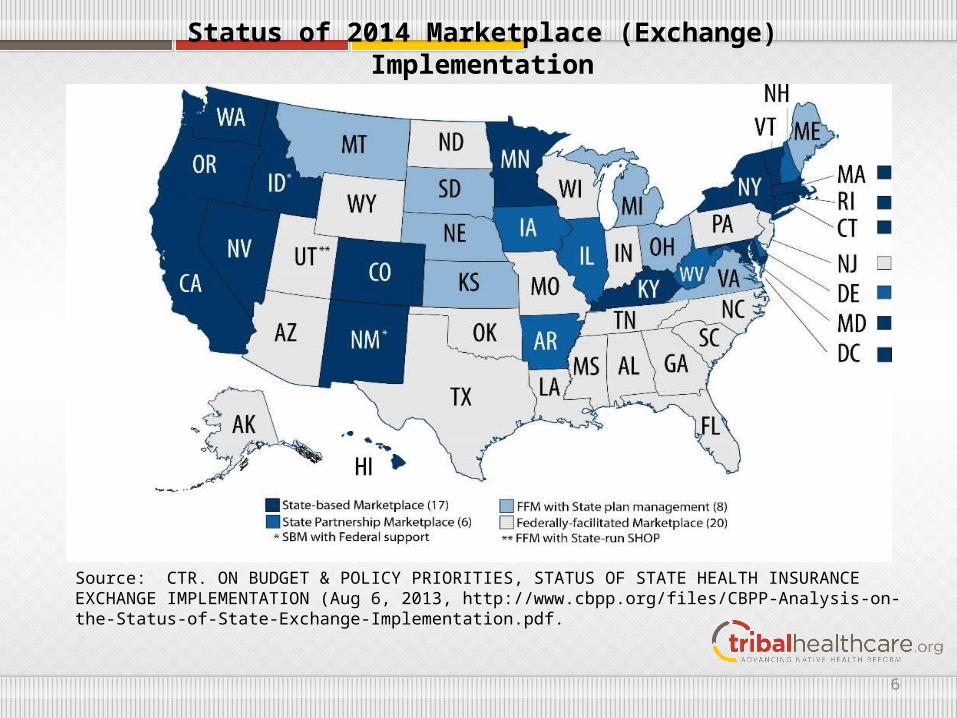

Status of 2014 Marketplace (Exchange) Implementation

Source: CTR. ON BUDGET & POLICY PRIORITIES, STATUS OF STATE HEALTH INSURANCE EXCHANGE IMPLEMENTATION (Aug 6, 2013, http://www.cbpp.org/files/CBPP-Analysis-on-the-Status-of-State-Exchange-Implementation.pdf.

6

SHOP Marketplace in Your State

• Healthcare.gov https://www.healthcare.gov/what-is-the-marketplace-in-my-state/

• The Commonwealth Fund Interactive Maphttp://www.commonwealthfund.org/Maps-and-Data/State-Exchange-Map.aspx

7

SHOP Functions

8

SHOP Functions• Among other functions, the SHOP:– Determines requirements for enrollment and

eligibility. – Provides qualified health plan (QHP) options for

employers.– Administers premium payments. – Certifies QHPs.– Determines participation rules.– Establishes methods for contributions.

9

Comparison with Individual Marketplace

10

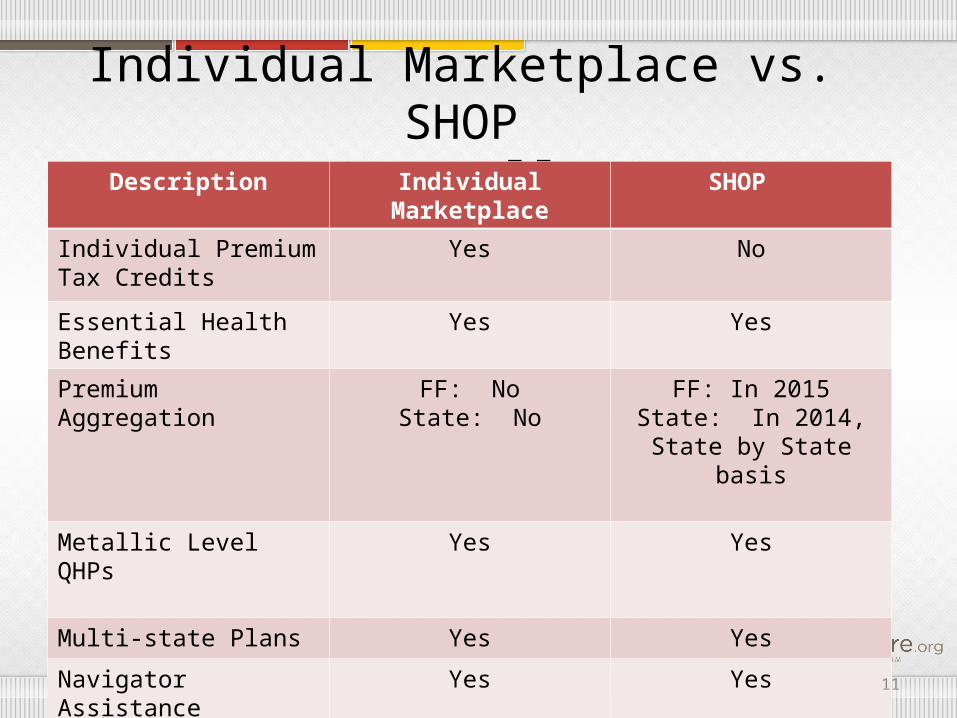

Individual Marketplace vs. SHOPGenerally

Description Individual Marketplace SHOP

Individual Premium Tax Credits

Yes No

Essential Health Benefits Yes Yes

Premium Aggregation FF: NoState: No

FF: In 2015State: In 2014, State by

State basis

Metallic Level QHPs Yes Yes

Multi-state Plans Yes Yes

Navigator Assistance Yes Yes

11

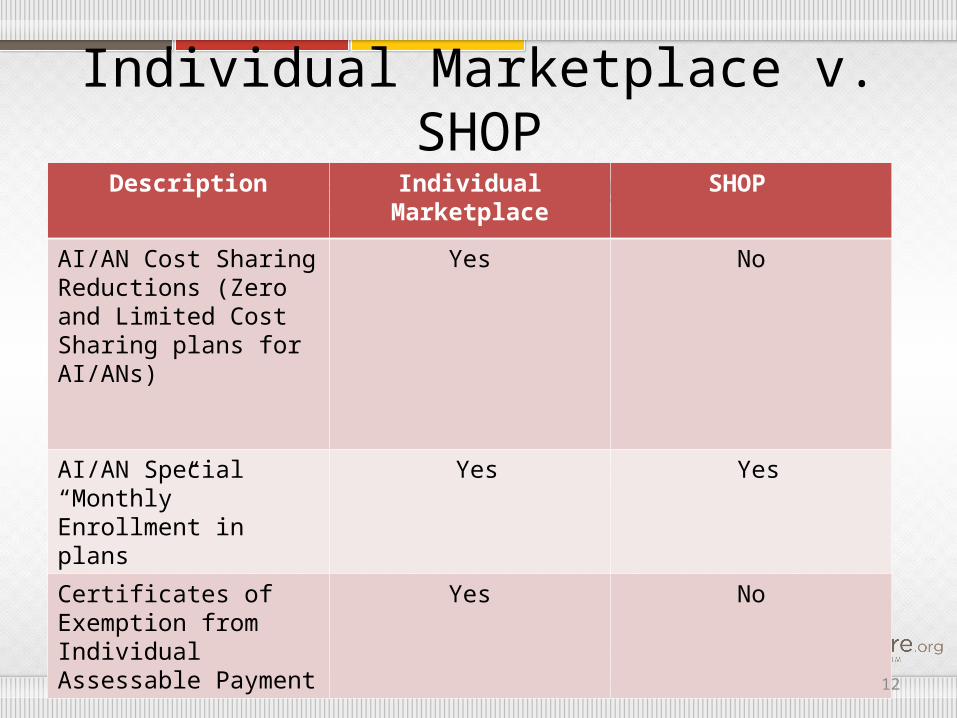

Individual Marketplace v. SHOPSpecific to AI/AN

Description Individual Marketplace SHOP

AI/AN Cost Sharing Reductions (Zero and Limited Cost Sharing plans for AI/ANs)

Yes No

AI/AN Special “Monthly” Enrollment in plans

Yes Yes

Certificates of Exemption from Individual Assessable Payment

Yes No

12

Eligibility, Definitions & Application

13

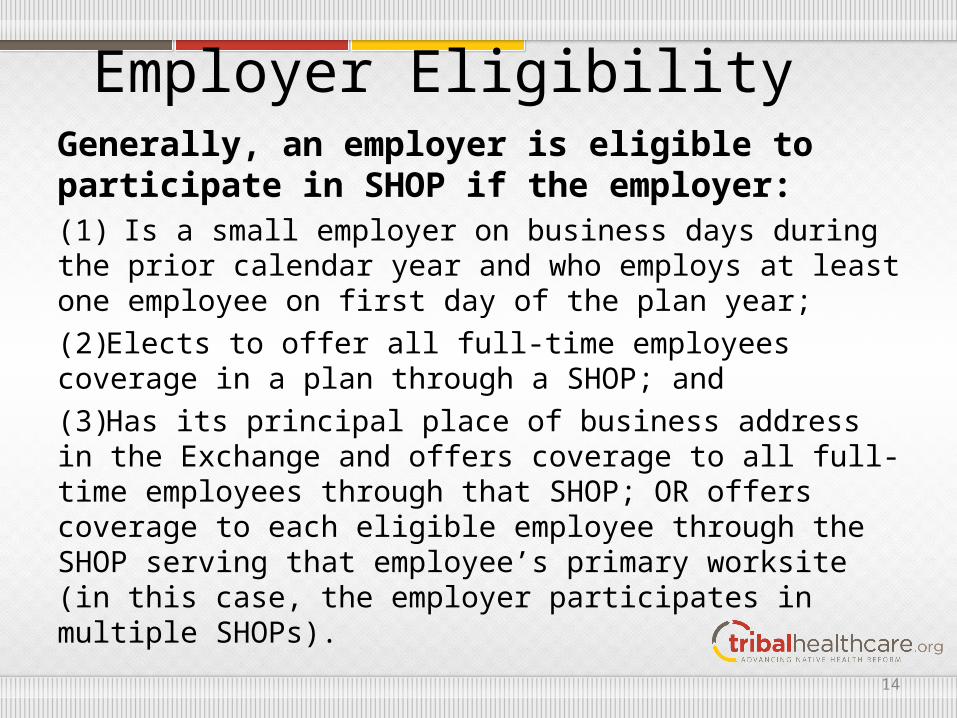

Employer Eligibility Generally, an employer is eligible to participate in SHOP if the employer:(1) Is a small employer on business days during the prior calendar year and who employs at least one employee on first day of the plan year; (2)Elects to offer all full-time employees coverage in a plan through a SHOP; and(3)Has its principal place of business address in the Exchange and offers coverage to all full-time employees through that SHOP; OR offers coverage to each eligible employee through the SHOP serving that employee’s primary worksite (in this case, the employer participates in multiple SHOPs).

14

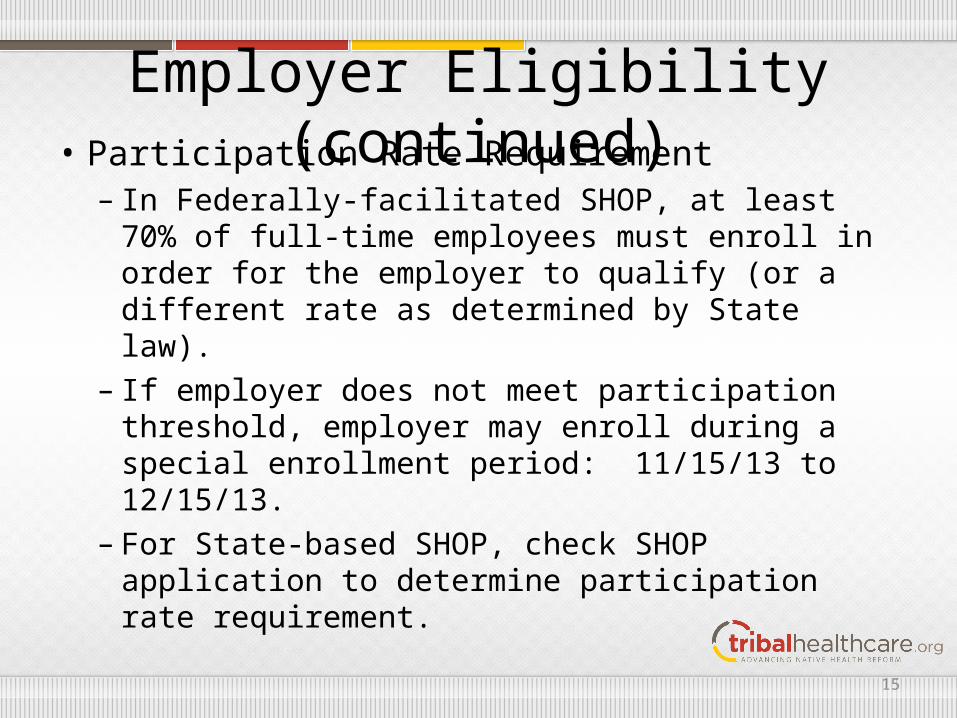

Employer Eligibility (continued)• Participation Rate Requirement– In Federally-facilitated SHOP, at least 70% of full-

time employees must enroll in order for the employer to qualify (or a different rate as determined by State law).

– If employer does not meet participation threshold, employer may enroll during a special enrollment period: 11/15/13 to 12/15/13.

– For State-based SHOP, check SHOP application to determine participation rate requirement.

15

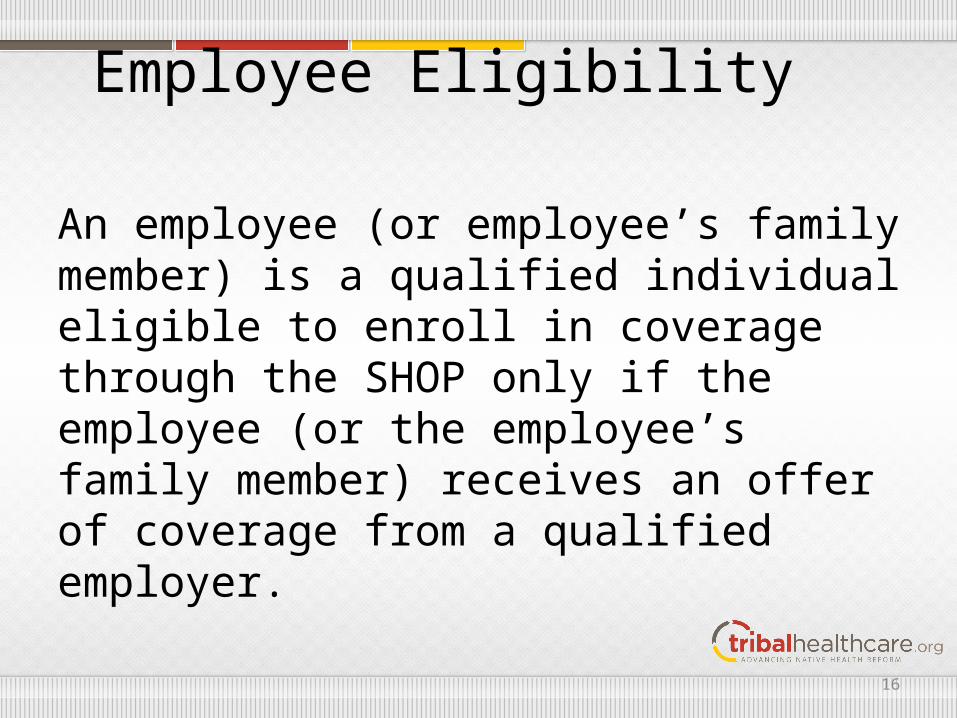

Employee Eligibility

An employee (or employee’s family member) is a qualified individual eligible to enroll in coverage through the SHOP only if the employee (or the employee’s family member) receives an offer of coverage from a qualified employer.

16

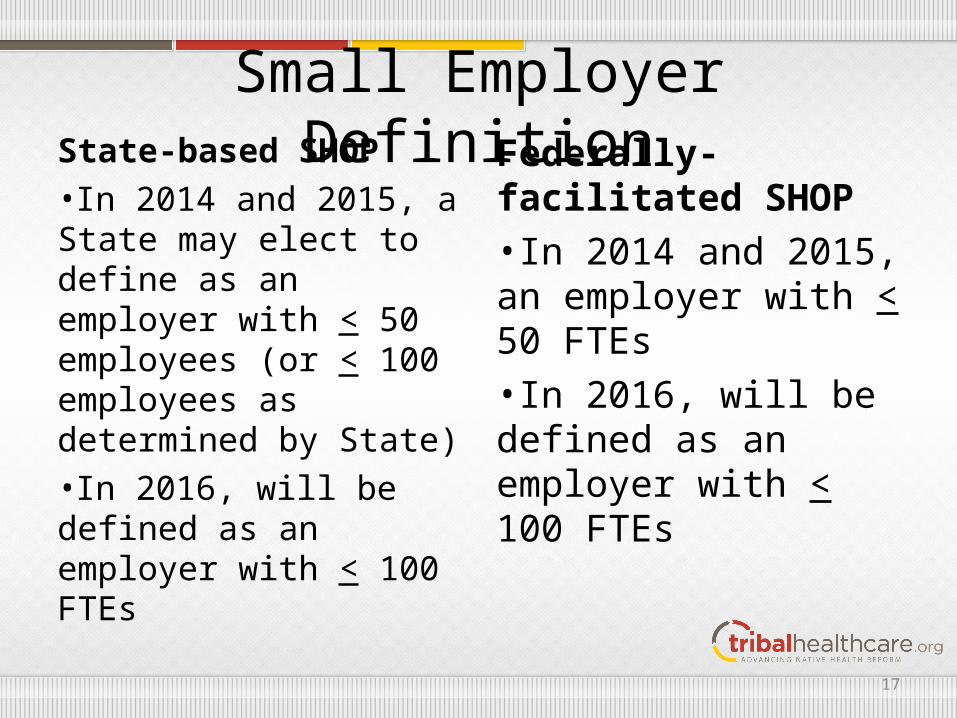

Small Employer DefinitionState-based SHOP•In 2014 and 2015, a State may elect to define as an employer with < 50 employees (or < 100 employees as determined by State) •In 2016, will be defined as an employer with < 100 FTEs

Federally-facilitated SHOP•In 2014 and 2015, an employer with < 50 FTEs •In 2016, will be defined as an employer with < 100 FTEs

17

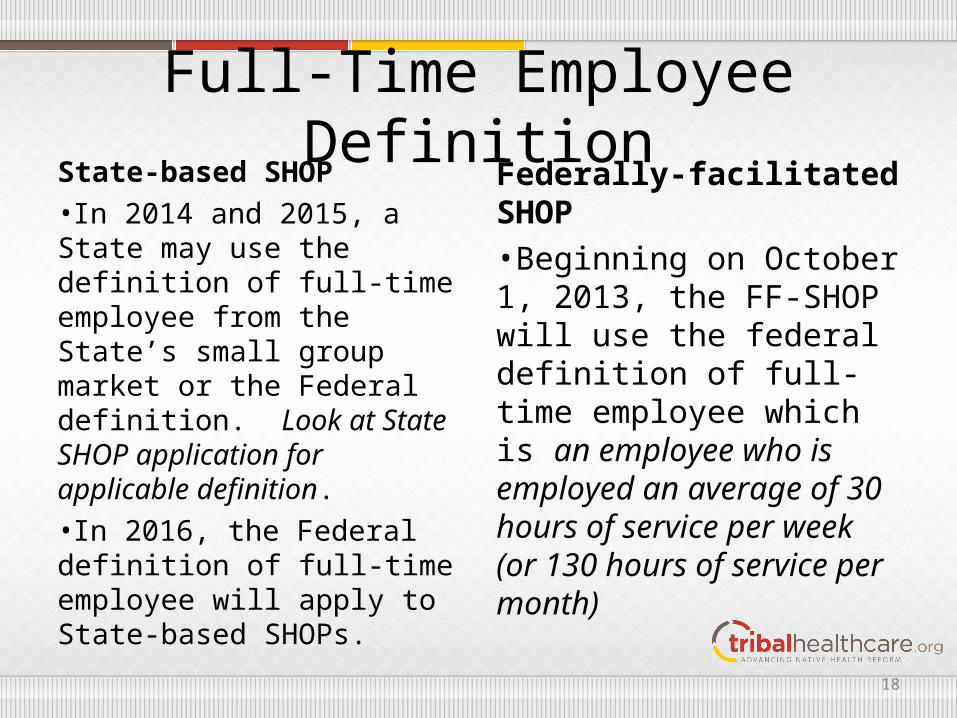

Full-Time Employee Definition

State-based SHOP•In 2014 and 2015, a State may use the definition of full-time employee from the State’s small group market or the Federal definition. Look at State SHOP application for applicable definition.•In 2016, the Federal definition of full-time employee will apply to State-based SHOPs.

Federally-facilitated SHOP•Beginning on October 1, 2013, the FF-SHOP will use the federal definition of full-time employee which is an employee who is employed an average of 30 hours of service per week (or 130 hours of service per month)

18

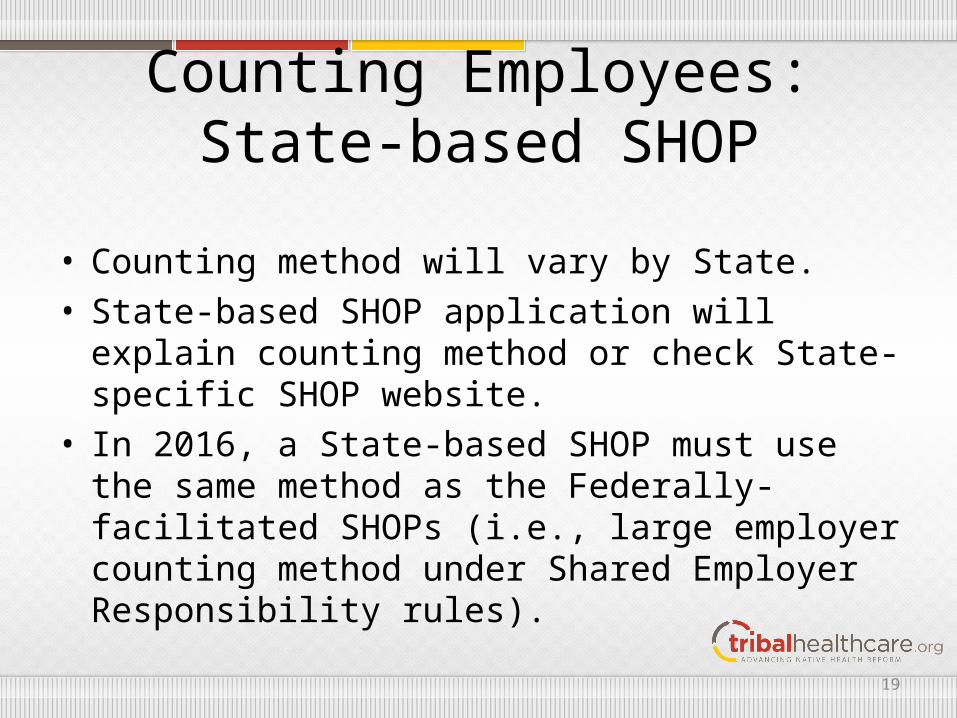

Counting Employees: State-based SHOP

• Counting method will vary by State.• State-based SHOP application will explain counting

method or check State-specific SHOP website.• In 2016, a State-based SHOP must use the same

method as the Federally-facilitated SHOPs (i.e., large employer counting method under Shared Employer Responsibility rules).

19

Counting Employees: Federally-facilitated SHOP

To determine FTEs:1.Count the number of full-time employees for each calendar month in the prior year.2.Determine the number of full-time equivalent employees by adding the total number of hours of service of part-time employees in a calendar month and dividing by 120. 3.Add the number of full-time employees and full-time equivalent employees for each month of the calendar year.4.Add up the 12 monthly numbers and divide by 12.5.Exclude seasonal workers (120 hours or less) for the calendar year.

20

Application Process• An employer may apply through the SHOP

website, a Navigator, an insurance broker, or a call center

• Single SHOP application (on line & paper)– Separate applications for employer & employee

• The SHOP will: – Verify information in applications– Determine employer’s eligibility to participate– Notify employer as to denial or approval of

application21

SHOP Plans

22

Essential Health Benefits

The plans in SHOP will include Essential Health Benefits (EHB):1. Ambulatory patient service2. Emergency services3. Hospitalization4. Maternity and newborn care5. Mental health and substance use disorder services, including

behavioral health treatment6. Prescription drugs7. Rehabilitative and habilitative services and devices8. Laboratory services9. Preventive and wellness services and chronic disease management10. Pediatric services, including oral and vision care

23

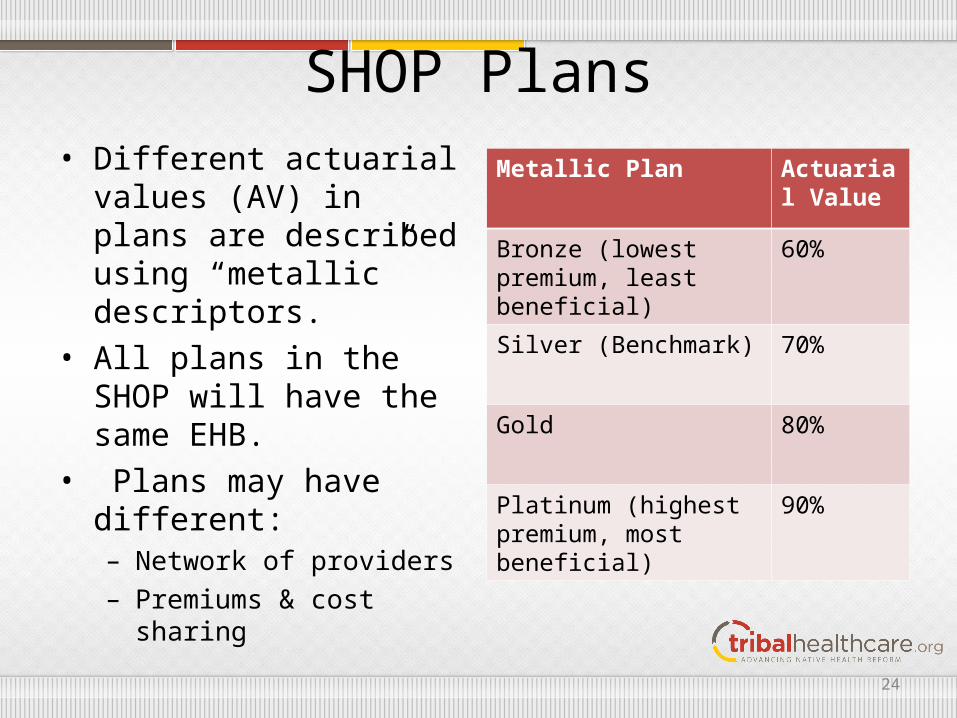

SHOP Plans• Different actuarial values

(AV) in plans are described using “metallic” descriptors.

• All plans in the SHOP will have the same EHB.

• Plans may have different:– Network of providers – Premiums & cost sharing

Metallic Plan Actuarial Value

Bronze (lowest premium, least beneficial)

60%

Silver (Benchmark) 70%

Gold 80%

Platinum (highest premium, most beneficial)

90%

24

SHOP Plans (continued)

Sources for Plans Offered in SHOP:1. Qualified Health Plans (QHPs)2. Multi-State Plans (MSPs)

25

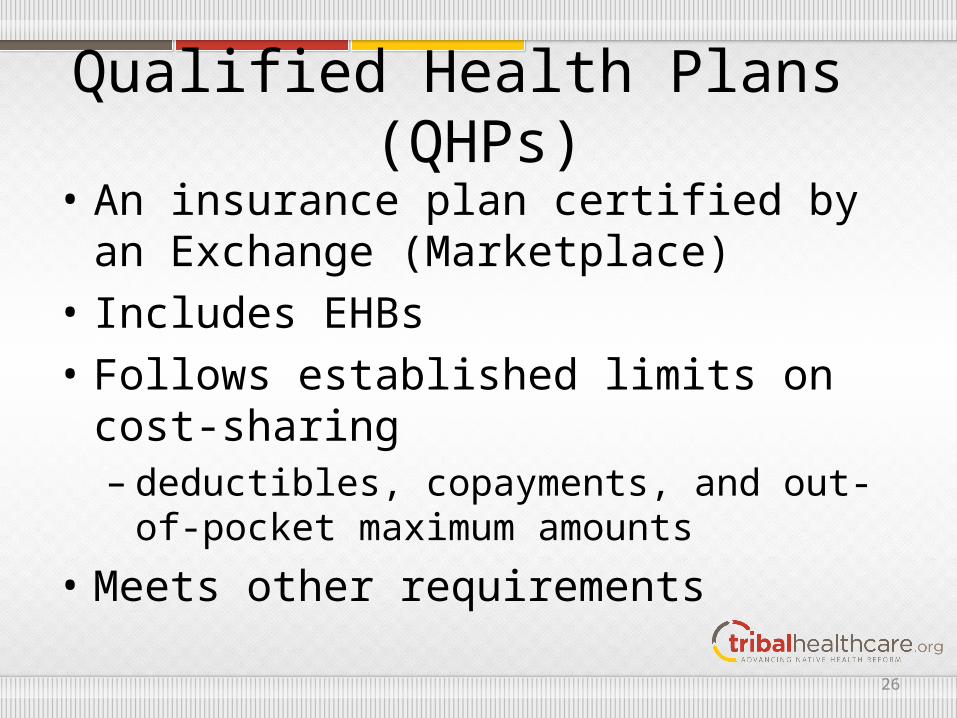

Qualified Health Plans (QHPs)

• An insurance plan certified by an Exchange (Marketplace)

• Includes EHBs• Follows established limits on cost-sharing– deductibles, copayments, and out-of-pocket

maximum amounts

• Meets other requirements

26

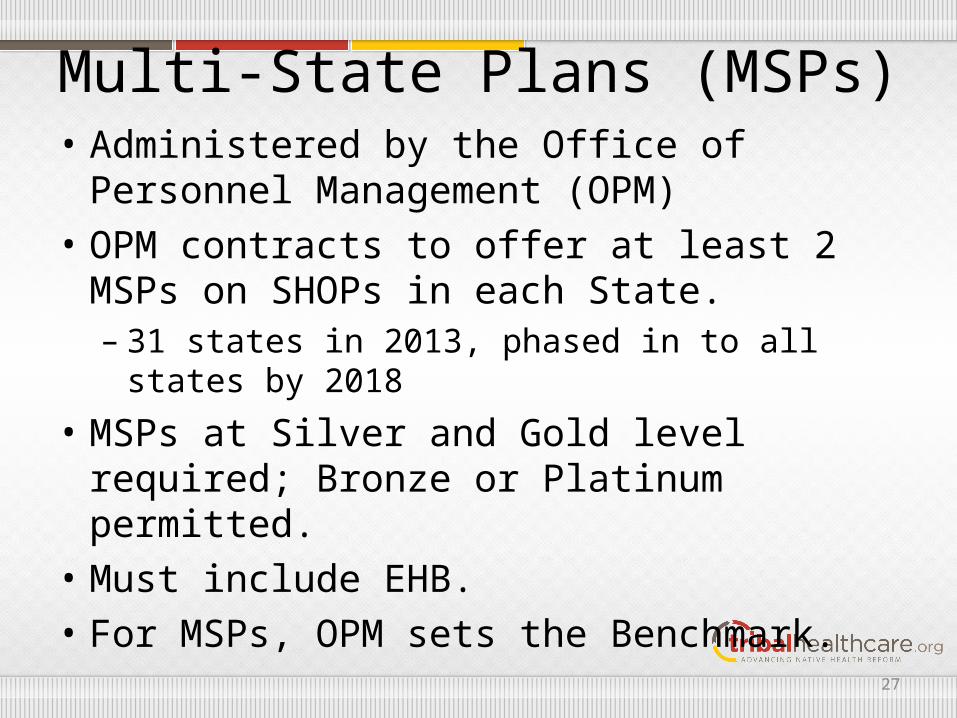

Multi-State Plans (MSPs)• Administered by the Office of Personnel

Management (OPM)• OPM contracts to offer at least 2 MSPs on

SHOPs in each State.– 31 states in 2013, phased in to all states by 2018

• MSPs at Silver and Gold level required; Bronze or Platinum permitted.

• Must include EHB.• For MSPs, OPM sets the Benchmark.

27

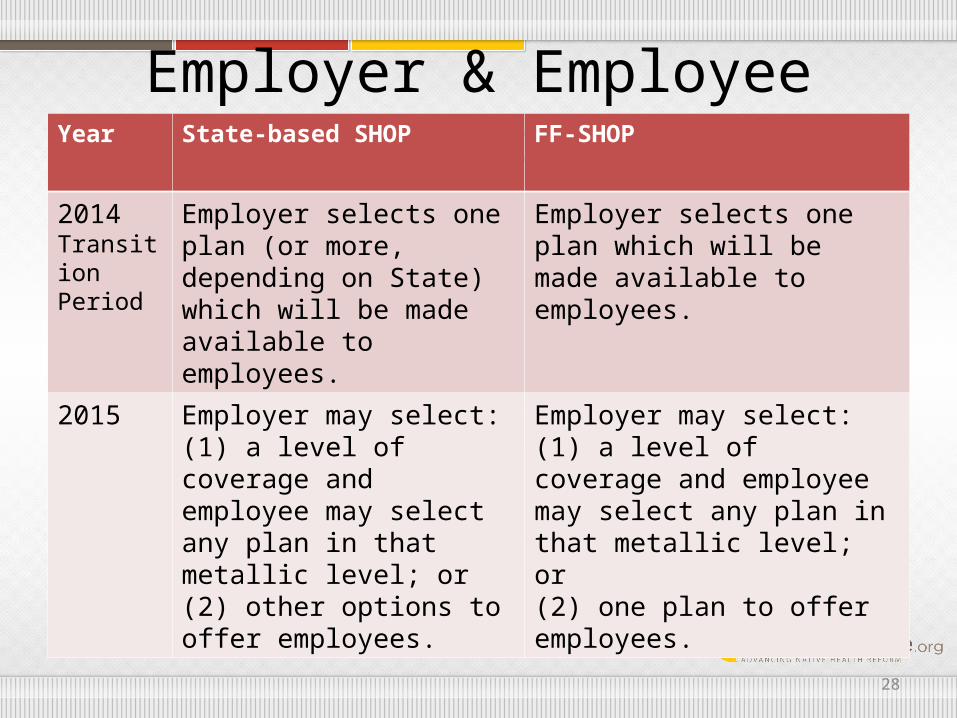

Employer & Employee ChoicesYear State-based SHOP FF-SHOP

2014Transition Period

Employer selects one plan (or more, depending on State) which will be made available to employees.

Employer selects one plan which will be made available to employees.

2015 Employer may select:(1) a level of coverage and employee may select any plan in that metallic level; or(2) other options to offer employees.

Employer may select:(1) a level of coverage and employee may select any plan in that metallic level; or(2) one plan to offer employees.

28

Enrollment, Contributions & Premium Aggregation

29

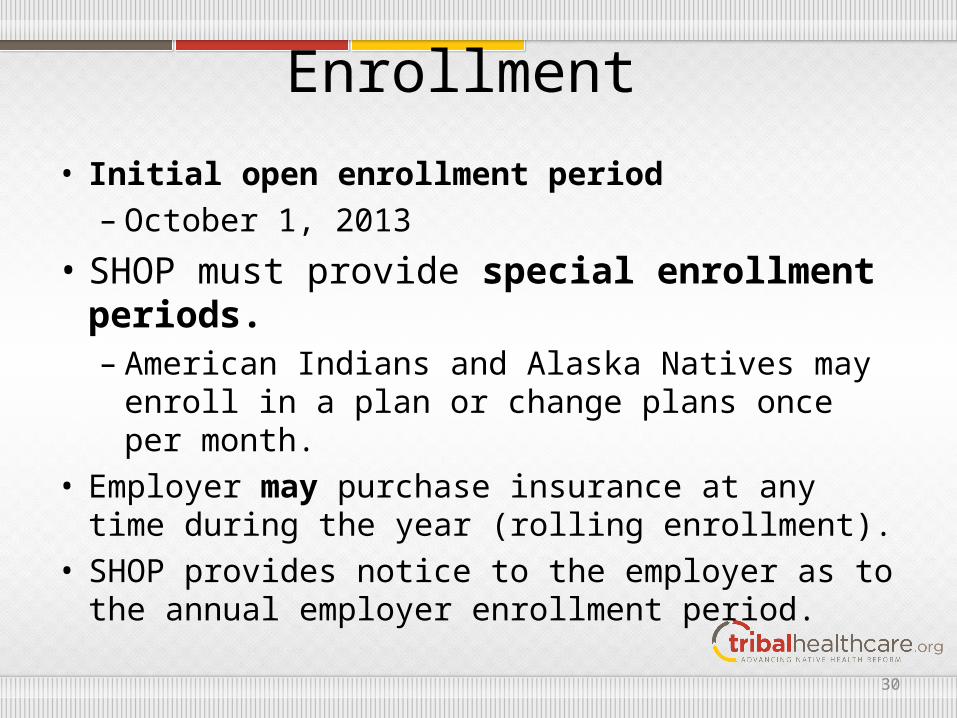

Enrollment

• Initial open enrollment period– October 1, 2013

• SHOP must provide special enrollment periods.– American Indians and Alaska Natives may enroll in a

plan or change plans once per month.• Employer may purchase insurance at any time during

the year (rolling enrollment).• SHOP provides notice to the employer as to the annual

employer enrollment period.

30

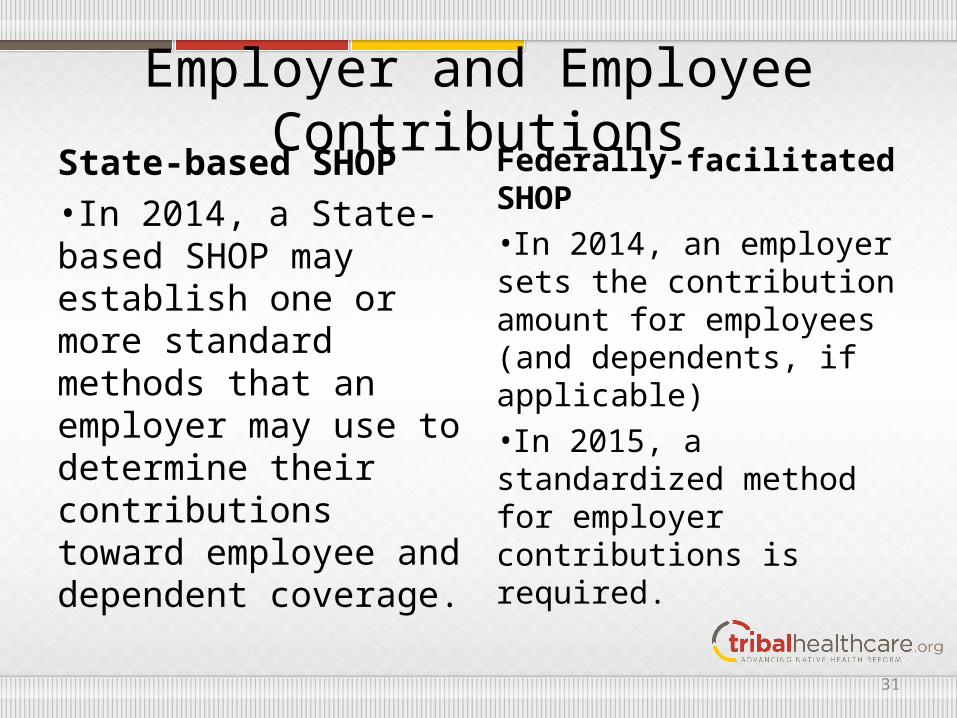

Employer and Employee Contributions

State-based SHOP•In 2014, a State-based SHOP may establish one or more standard methods that an employer may use to determine their contributions toward employee and dependent coverage.

Federally-facilitated SHOP•In 2014, an employer sets the contribution amount for employees (and dependents, if applicable)•In 2015, a standardized method for employer contributions is required.

31

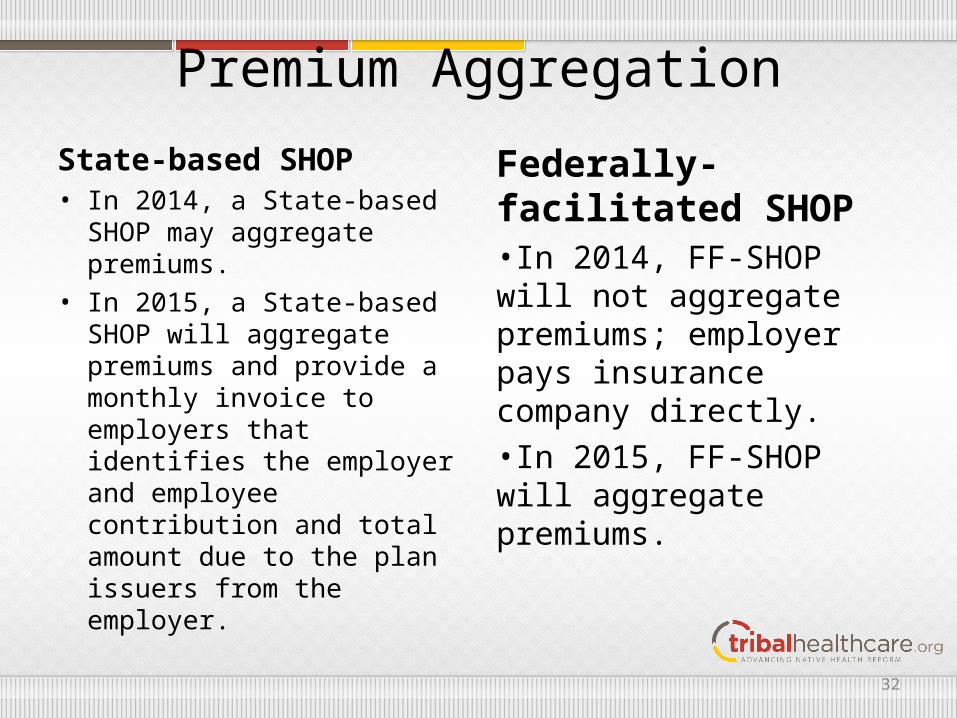

Premium Aggregation

State-based SHOP• In 2014, a State-based SHOP

may aggregate premiums.• In 2015, a State-based SHOP

will aggregate premiums and provide a monthly invoice to employers that identifies the employer and employee contribution and total amount due to the plan issuers from the employer.

Federally-facilitated SHOP•In 2014, FF-SHOP will not aggregate premiums; employer pays insurance company directly. •In 2015, FF-SHOP will aggregate premiums.

32

Preparation• Learn about the options for your business at:

http://business.usa.gov/healthcare• Prepare a budget to determine how much you can

spend on insurance.• Gather and organize information about your

employees. • Talk to your HR Department, attorney and insurance

broker about your options.• Consider participating in SHOP because the Small

Business Tax Credit will only be available for plans purchased in the SHOP in 2014.

33

Section Review• What is SHOP?• Are Tribes and Tribal entities eligible?• Name one difference between SHOP and the

Individual Marketplace?• What is limit on number of employees for

SHOP?• In 2014, how many plans will an employer in

an FF-SHOP offer to employees? In a State-based SHOP?

34

Questions

35