Embed Size (px)

DESCRIPTION

m com Sm

Citation preview

EXECUTIVE SUMMARY

Industrial maps across the world have been constantly redrawn over the years through various forms of corporate restructuring. The most common method of such restructuring is Mergers and Acquisitions (M&A). The term "mergers & acquisitions (M&As)" encompasses a widening range of activities, including joint ventures, licensing and synergising of energies. Industries facing excess capacity problems witness merger as means for consolidation. Industries with growth opportunities also experience M&A deals as growth strategies. There are stories of successes and failures in mergers and acquisitions. Such stories only confirm the popularity of this vehicle.

Merger is a tool used by companies for the purpose of expanding their operations often aiming at an increase of their long term profitability. There are 15 different types of actions that a company can take when deciding to move forward using M&A. Usually mergers occur in a consensual (occurring by mutual consent) setting where executives from the target company help those from the purchaser in a due diligence process to ensure that the deal is beneficial to both parties. Acquisitions can also happen through a hostile takeover by purchasing the majority of outstanding shares of a company in the open market against the wishes of the target's board. In the United States, business laws vary from state to state whereby some companies have limited protection against hostile takeovers. One form of protection against a hostile takeover is the shareholder rights plan, otherwise known as the "poison pill".

Mergers and acquisitions (M&A) have emerged as an important tool for growth for Indian corporates in the last five years, with companies looking at acquiring companies not only in India but also abroad.

1

INTRODUCTION

MERGER

Merger is defined as combination of two or more companies into a single company where one survives and the others lose their corporate existence. The survivor acquires all the assets as well as liabilities of the merged company or companies. Generally, the surviving company is the buyer, which retains its identity, and the extinguished company is the seller. Merger is also defined as amalgamation. Merger is the fusion of two or more existing companies. All assets, liabilities and the stock of one company stand transferred toTransferee Company in consideration of payment in the form of:

· Equity shares in the transferee company,

· Debentures in the transferee company,

· Cash, · A mix of the above modes.

CLASSIFICATIONS OF MERGERS

Mergers are generally classified into 5 broad categories. The basis of this classification is the business in which the companies are usually involved.

2

Different motives can also be attached to these mergers. The categories are:

Horizontal Merger

It is a merger of two or more competing companies, implying that they are firms in the same business or industry, which are at the same stage of industrial process. This also includes some group companies trying to restructure their operations by acquiring some of the activities of other group companies.

The main motives behind this are to obtain economies of scale in production by eliminating duplication of facilities and operations, elimination of competition, increase in market segments and exercise better control over the market.

There is little evidence to dispute the claim that properly executed horizontal mergers lead to significant reduction in costs. A horizontal merger brings about all the benefits that accrue with an increase in the scale of operations. Apart from cost reduction it also helps firms in industries like pharmaceuticals, cars, etc. where huge amounts are spent on R & D to achieve critical mass and reduce unit development costs.

Vertical Mergers

It is a merger of one company with another, which is involved, in a different stage of production and/ or distribution process thus enabling backward integration to assimilate the sources of

3

supply and / or forward integration towards market outlets.The main motives are to ensure ready take off of the materials, gain control over product specifications, increase profitability by gaining the margins of the previous supplier/ distributor, gain control over scarce raw materials supplies and in some case to avoid sales tax.

Conglomerate Mergers

It is an amalgamation of 2 companies

engaged in the unrelated industries. The

motive is to ensure better utilization of

financial resources, enlarge debt capacity

and to reduce risk by diversification.

It has evinced particular interest among researchers because of the general curiosity about the nature of gains arising out of them. Economic gain arising out of a conglomerate is not clear.

Much of the traditional analysis relating to economies of scale in production, research, distribution and management is not relevant for conglomerates. The argument in its favour is that in spite of the absence of economies of scale and complimentaries, they may cause stabilization in profit stream.

Even if one agrees that diversification results in risk reduction, the question that arises is at what level should the diversification take place, i.e. in order to reduce risk should the companydiversify or should the investor diversify his portfolio? Some feel that diversification by the investor is more cost effective and will not hamper the company’s core competence.

4

Others argue that diversification by the company is also essential owing to the fact that the combination of the financial resources of the two companies making up the merger reduces the lenders risk while combining each of the individual shares of the two companies in the investor’s portfolio does not. In spite of the arguments and counter- arguments, some amount of diversification is required, especially in industries which follow cyclical patterns, so as to bring some stability to cash flows.

Concentric Mergers

This is a mild form of conglomeration. It is the merger of one company with another which is engaged in the production / marketing of an allied product. Concentric merger is also called product extension merger. In such a merger, in addition to the transfer of general management skills, there is also transfer of specific management skills, as in production, research, marketing, etc, which have been used in a different line of business. A concentric merger brings all the advantages of conglomeration without the side effects, i.e., with a concentric merger it is possible to reduce risk without venturing into areas that the management is not competent in

Consolidation Mergers

It involves a merger of a subsidiary company with its parent. Reasons behind such a merger are to stabilize cash flows and to make funds available for the subsidiary.

5

Market-extension merger

Two companies that sell the same products in different markets.

Product-extension merger

Two companies selling different but related products in the same market

ACQUISITION

Acquisition in general sense is acquiring the ownership in the property. In the context of business combinations, an acquisition is the purchase by one company of a controlling interest in the share capital of another existing company.

Types of acquisitions:

i. Friendly takeover: Before a bidder makes an offer for another company, it usually first informs the company's board of directors. If the board feels that accepting the offer serves shareholders better than rejecting it, it recommends the offer be accepted by the shareholders.

ii. Hostile takeover: A hostile takeover allows a suitor to take over a target company's management unwilling to agree to a merger or takeover. A takeover is considered "hostile" if the target company's board rejects the offer, but the bidder continues to pursue it, or the bidder makes the offer without informing the target company's board beforehand.

6

iii. Back flip takeover: A back flip takeover is any sort of takeover in which the acquiring company turns itself into a subsidiary of the purchased company. This type of a takeover rarely occurs.

iv. Reverse takeover: A reverse takeover is a type of takeover where a private company acquires a public company. This is usually done at the instigation of the larger, private company, the purpose being for the private company to effectively float itself while avoiding some of the expense and time involved in a conventional IPO

Methods of Acquisition:

An acquisition may be affected by:-

· Agreement with the persons holding majority interest in the company management like members of the board or major shareholders commanding majority of voting power;

· Purchase of shares in open market;

· To make takeover offer to the general body of shareholders;

· Purchase of new shares by private treaty;

· Acquisition of share capital through the following forms of considerations viz. Means of cash, issuance of loan capital, or insurance of share capital.

7

DISTINCTION BETWEEN MERGERS AND ACQUISITIONS

Although they are often uttered in the same breath and used as though they were synonymous, the terms merger and acquisition mean slightly different things.

When one company takes over another and clearly established itself as the new owner, the purchase is called an acquisition. From a legal point of view, the target company ceases to exist, the buyer "swallows" the business and the buyer's stock continues to be traded.

In the pure sense of the term, a merger happens when two firms, often of about the same size, agree to go forward as a single new company rather than remain separately owned and operated. This kind of action is more precisely referred to as a "merger of equals." Both companies' stocks are surrendered and new company stock is issued in its place. For example, both Daimler-Benz and Chrysler ceased to exist when the two firms merged, and a

8

new company, DaimlerChrysler, was created.

In practice, however, actual mergers of equals don't happen very often. Usually, one company will buy another and, as part of the deal's terms, simply allow the acquired firm to proclaim that the action is a merger of equals, even if it's technically an acquisition. Being bought out often carries negative connotations, therefore, by describing the deal as a merger, deal makers and top managers try to make the takeover more palatable.

A purchase deal will also be called a merger when both CEOs agree that joining together is in the best interest of both of their companies. But when the deal is unfriendly - that is, when the target company does not want to be purchased - it is always regarded as an acquisition.

Whether a purchase is considered a merger or an acquisition really depends on whether the purchase is friendly or hostile and how it is announced. In other words, the real difference lies in how the purchase is communicated to and received by the target company's board of directors, employees and shareholders.

Motives behind M&A

9

The following motives are considered to improve financial performance:

1 ) Synergies: the combined company can often reduce its fixed costs by removing duplicate departments or operations, lowering the costs of the company relative to the same revenue stream, thus increasing profit margins.

2 ) Increased revenue/Increased Market Share: This assumes that the buyer will be absorbing a major competitor and thus increase its market power (by capturing increased market share) to set prices.

3 ) Cross selling: For example, a bank buying a stock broker could then sell its banking products to the stock broker's customers, while the broker can sign up the bank's customers for brokerage accounts. Economies of Scale: For example, managerial economies such as the increased opportunity of managerial specialization. Another example is purchasing economies due to increased order size and associated bulk-buying discounts.

4 ) Taxes: A profitable company can buy a loss maker to use the target's loss as their advantage by reducing their tax liability.

5 ) Resource transfer: resources are unevenly distributed across firms

10

and the interaction of target and acquiring firm resources can create value through either overcoming information asymmetry or by combining scarce resources.

6 ) Vertical integration: Vertical Integration occurs when an upstream and downstream firm merges (or one acquires the other). By merging the vertically integrated firm can collect one deadweight loss by setting the upstream firm's output to the competitive level. This increases profits and consumer surplus. A merger that creates a vertically integrated firm can be profitable.

Therefore, additional motives for merger and acquisition that may not add shareholder value include:

1 ) Diversification: While this may hedge a company against a downturn in an individual industry it fails to deliver value, since it is possible for individual shareholders to achieve the same hedge by diversifying their portfolios at a much lower cost than those associated with a merger.

11

2 ) Manager's hubris: manager's overconfidence about expected synergies from M&A which results in overpayment for the target company.

3 ) Empire building: Managers have larger companies to manage and hence more power.

4 ) Manager's compensation: In the past, certain executive management teams had their payout based on the total amount of profit of the company, instead of the profit per share, which would give the team a perverse incentive to buy companies to increase the total profit while decreasing the profit per share (which hurts the owners of the company, the shareholders); although some empirical studies show that compensation is linked to profitability rather than mere profits of the company.

12

STAGES OF A MERGER

Pre-mergers are characteristics by the :-

1. COURTSHIP: -The respective management teams discuss the possibility of a merger and develop a shared vision and set of objectives. This can be achieved through a rapid series of meetings over a few weeks, or through several months of talks and informal meetings

2. EVALUATION AND NEGOTIATION: -

Once some form of understanding has been reached the purchasing company conducts “due diligence” a detailed analysis of the target compan y assets, liabilities and operations. This leads to a formal announcement of the merger and an intense round of negotiations, often involving financial intermediaries. Permission is also sought from trade regulators. The new management team is agreed at this point, as well as the board structure of the new business.

This phase typically lasts three or four months, but it can take as long as a year if regulators decide to launch an investigation into the deal. “C losure”

13

is a commonly referred term to describe the point at which the legal transfer of ownership is completed.

3. PLANNING: -

More and more companies use this time before completing a merger to assemble a senior team to oversee the merger integration and to begin planning the new management and operational structure.

Post Merger is characterized by the

1) THE IMMEDIATE TRANSITION: -

This typically lasts three to six months and often involves intense activity. Employees receive information about whether and how the merger will affect their employment terms and conditions. Restructuring begins and may include site closures, redundancy announcements, divestment of subsidiaries (sometimes required by trade regulators), new appointments

14

and job transfers. Communications and human resources strategies are implemented. Various teams work on detailed plans for integration.

2) THE TRANSITION PERIOD : -

This lasts anywhere between six months to two years. The new organizational structure is in place and the emphasis is now on fine tuning the business and ensuring that the envisaged benefits of the mergers are realized. Companies often consider cultural integration at this point and may embark on a series of workshops exploring the values, philosophy and work styles of the merged business.

15

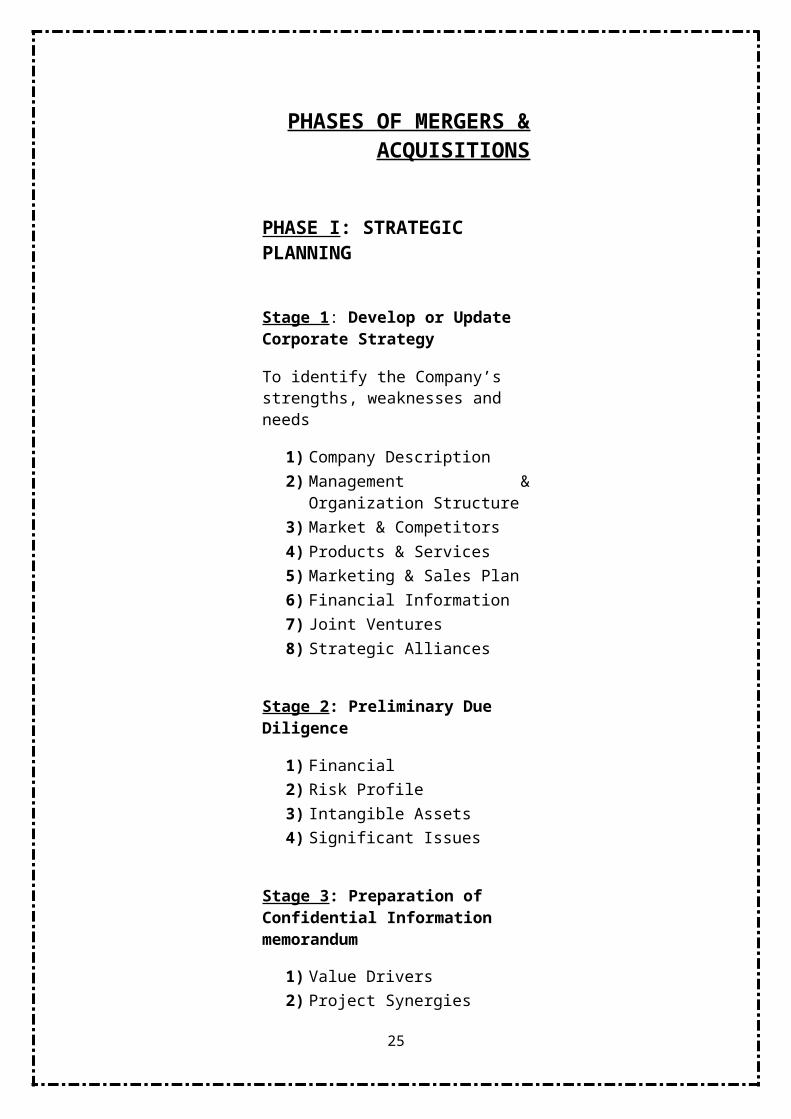

PHASES OF MERGERS & ACQUISITIONS

PHASE I: STRATEGIC PLANNING

Stage 1: Develop or Update Corporate Strategy

To identify the Company’s strengths, weaknesses and needs

1) Company Description 2) Management & Organization

Structure 3) Market & Competitors 4) Products & Services 5) Marketing & Sales Plan 6) Financial Information 7) Joint Ventures 8) Strategic Alliances

Stage 2: Preliminary Due Diligence

1) Financial 2) Risk Profile 3) Intangible Assets 4) Significant Issues

Stage 3: Preparation of Confidential Information memorandum

1) Value Drivers 2) Project Synergies

PHASE II: TARGET/BUYER IDENTIFICATION & SCREENING

Stage 4: Buyer Rationale

16

1) Identify Candidates 2) Initial Screening

Stage 5: Evaluation of Candidates

1) Management and Organization Information2) Financial Information

(Capabilities) 3) Purpose of Merger or Acquisition

PHASE III: TRANSACTION STRUCTURING

Stage 6: Letter of Intent

Stage 7: Evaluation of Deal Points

1) Continuity of Management 2) Real Estate Issues 3) Non-Business Related Assets 4) Consideration Method 5) Cash Compensation 6) Stock Consideration 7) Tax Issues 8) Contingent Payments 9) Legal Structure 10) Financing the Transaction

Stage 8: Due Diligence

1) Legal Due Diligence 2) Seller Due Diligence 3) Financial Analysis 4) Projecting Results of the Structure

17

Stage 9: Definitive Purchase Agreement

1) Representations and Warranties 2) Indemnification Provisions

Stage 10: Closing the Deal

PHASE IV: SUCCESSFUL INTEGRATION

1) Human Resources 2) Tangible Resources 3) Intangible Assets 4) Business Processes 5) Post Closing Audit

Mergers and Acquisitions: Valuation

Investors in a company that is aiming to take over another one must determine whether the purchase will be beneficial to them. In order to do so, they must ask themselves how much the company being acquired is really worth.

Naturally, both sides of an M&A deal will have different ideas about the worth of a target company: its seller will tend to value the company at as high of a price as possible, while the buyer will try to get the lowest price that he can. There are, however, many legitimate ways to value companies. The most common method is to look at comparable companies in an industry, but deal makers employ a variety of other methods and tools when

18

assessing a target company. Here are just a few of them:

Comparative Ratios - The following are two examples of the many comparative metrics on which acquiring companies may base their offers:

Price-Earnings Ratio (P/E Ratio) - With the use of this ratio, an acquiring company makes an offer that is a multiple of the earnings of the target company. Looking at the P/E for all the stocks within the same industry group will give the acquiring company good guidance for what the target's P/E multiple should be.

Enterprise-Value-to-Sales Ratio (EV/Sales) - With this ratio, the acquiring company makes an offer as a multiple of the revenues, again, while being aware of the price-to-sales ratio of other companies in the industry.

Replacement Cost - In a few cases, acquisitions are based on the cost of replacing the target company. For simplicity's sake, suppose the value of a company is simply the sum of all its equipment and staffing costs. The acquiring company can literally order the target to sell at that price, or it will create a competitor for the same cost. Naturally, it takes a long time to assemble good management, acquire property and get the right equipment. This method of establishing a price certainly wouldn't make much sense in a service industry where the key assets - people and ideas - are hard to value and develop.

Discounted Cash Flow (DCF) - A key valuation tool in M&A, discounted cash

19

flow analysis determines a company's current value according to its estimated future cash flows. Forecasted free cash flows (operating profit + depreciation + amortization of goodwill – capital expenditures– cash taxes - change in working capital) are disco unted to a present value using the company's weighted average costs of capital (WACC). Admittedly, DCF is tricky to get right, but few tools can rival this valuation method.

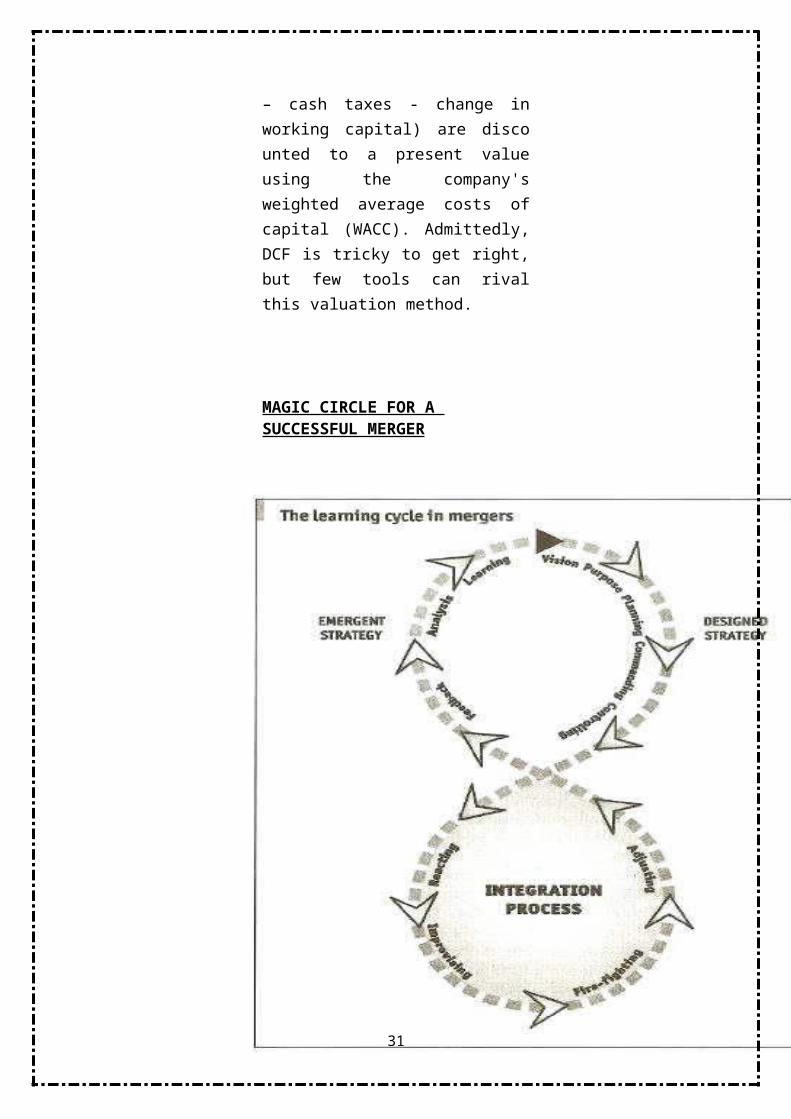

MAGIC CIRCLE FOR A SUCCESSFUL MERGER

20

A company’s integration process can ensure the formation of such a circle. It acts rather like the Gulf Stream, where the flow of hot and cold water ensures a continuous cyclical movement. A well designed integration process ensures that the new entity’s designed strategy reaches deep into the organisation, ensuring a unity of purpose. Basically everyone understands the purpose and logic of the deal. The integration process can ensure that the ideas and the creativity can are not dissipated but are fed into the emergent strategy of the organisation this is achieved through the day to day job of the encouraging and motivating people and also creating forums where people can think the impossible. The chart below demonstrates the relationship between designed and emergent strategy and merger integration. It suggests how merging organizations can become learning organisation; strategy formulation and implementation merges into collective learning.

Some merger failures can be explained by this model. For example, serious problems arise when a company relies too heavily on designed strategy. If the management team is not getting high quality feedback and information from the rest of the organisation, it runs the risk of becoming cut off. Employees may perceive their leaders as being out of touch with reality of the merger, leading to a gradual loss of confidence in senior

21

management’s ability to chart the future of the new entity. Similarly, the leadership team may not receive timely information about external threats, brought about perhaps by the predatory actions of competitors or dissatisfies customers with the result that performance suffers and the new management is criticized for failing to get grips with the complexities of the changeover.

However, too much reliance on emergent strategy can lead to the sense of a leadership vacuum within the combining organizations. The management team may seem to lack direction or to be moving too slow. This often leads political infighting and territory building and the departure of many talented people.

Therefore it is very important that a careful balance is struck between designed and emergent strategy for integration after the merger between two companies is done.

22

SYNERGY

When most people talk about mergers and acquisitions they talk about synergy. But what is synergy?

Synergy is derived from a Greek word “synergos”, wh ich means working together, synergy “refers to the ability of two or more units or comp anies to generate greater value working together than they could working apart”. The abilit y to make 2 + 2 = 5 instead of 4.

Typically synergy is thought to yield gains to the acquiring firm through two sources

1) Improved operating efficiency based on economies of scale or scope

2) Sharing of one or more skills. For managers synergy is when the combined firm creates more value than the independent entity. But for shareholders synergy is when they acquire gains that they could not obtain through their own portfolio diversification decisions. However this is difficult to achieve since shareholders can diversify their ownership positions more cheaply.

For both the companies and individual shareholders the value of synergy must be examined in relation to value that could be created through other strategic options like alliances etc.

23

Synergy is difficult to achieve, even in the relatively unusual instance that the company does not pay a premium. However, when a premium is paid the challenge is more significant. The reason for this is that the payment of premium requires the creation of greater synergy to generate economic value.

The actual creation of synergy is an outcome that is expected from the managers’ work. Achieving this outcome demands effective integration of combined units’ assets, operations and personnel. History shows that at the very least, creating synergy “requires a great deal of work on the part of the managers at the corporate and business levels”. The activities that create synergy include

1) Combining similar processes 2) Co-ordinating business units that

share common resources 3) Centralizing support activities that

apply to multiple units 4) Resolving conflict among

business units

The Types of Synergy

1) Operations SynergyThis is obtained through integrating functional activities. It can be created through economies of scale / or scope.

24

2)Technology Synergy

To create synergies through this, firms seek to link activities associated with research and development processes. The sharing of R&D programs, the transfer of technologies across units, products and programs, and the development of new core business through access to private innovative capabilities are examples of activities of firms trying to create synergies

3) Marketing – Based Synergy

Synergy is created when the firm successfully links various marketing-related activities including those related to sharing of brand names as well as distribution channels and advertising and promotion campaigns.

4) Management Synergy

These synergies are typically gained when competitively relevant skills that were possessed by managers in the formerly independent companies or business units can be transferred successfully between units within the newly formed firm.

5) Private SynergyThis can be created when the acquiring firm has knowledge about the complementary nature of its resources with those of the target firm that is not known to others.

25

REVENUES

Revenue deserves more attention in mergers; indeed, a failure to focus on this important factor may explain why so many mergers don’t pay off. Too many companies lose their revenue momentum as they concentrate on cost synergies or fail to focus on post merger growth in a systematic manner. Yet in the end, halted growth hurts the market performance of a company far more than does a failure to nail costs.

The belief that mergers drive revenue growth could be a myth. A study of 160 companies shows that measured against industry peers, only 36 percent of the targets maintained their revenue growth in the first quarter after the merger announcement. By the third quarter, only 11 percent had avoided a slowdown. It turned out that the targets’ continuing underperformance explained only half of the slowdown; unsettled customers and distracted staff explained the rest.

Only 12 percent of these companies managed to accelerate their growth significantly over the next three years. In

26

fact, most sloths remained sloths, while most solid performers slowed down. Overall, the acquirers managed organic growth rates that were four percentage points lower than those of their industry peers; 42 percent of the acquirers lost ground.

Why should one worry so much about revenue growth in mergers? Because, ultimately, it is revenue that determines the outcome of a merger, not costs; whatever the merger’s objectives, revenue actually hits the bottom line harder

Fluctuations in revenue can quickly outweigh fluctuations in planned cost savings. Given a 1 percent shortfall in revenue growth, a merger can stay on track to create value only if a company achieves cost savings that are 25 percent higher than those it had anticipated. Beating target revenue-growth rates by 2 to 3 percent can offset a 50 percent failure on costs.

Furthermore, cost savings are hardly as sure as they appear: up to 40 percent of mergers fail to capture the identified cost synergies. The market penalizes this slippage hard: failing to meet an earnings target by only 5 percent can result in a 15 percent decline in share prices. The temptation is then to make excessively deep cuts or cuts in inappropriate places, thus depressing future earnings by taking out muscle, not just fat.

Finally, companies that actively pursue

27

growth in their mergers generate a positive dynamic that makes merger objectives, including cost cutting, easier to achieve.

Out of the 160 companies studied only 12 percent achieved organic growth rates (from 1992 to 1999) that were significantly ahead of the organic growth rates of their peers, and only seven of those companies had total returns to shareholders that were better than the industry average. Before capturing the benefits of integration, such merger masters look after their existing customers and revenue. They also target and retain their revenue-generating talent—especially the people who handle relations with customers.

Thus it can be noted that if revenue is not monitored properly and if one does not make an effort to maintain revenue it can result in significant losses to the company.

28

DISADVANTAGES OF MERGERS AND ACQUISITIONS

1 ) All liabilities assumed (including potential litigation)

2 ) Two thirds of shareholders (most states) of both firms must approve 3 ) Dissenting shareholders can sue to receive their “f air” value

4 ) Management cooperation needed

5 ) Individual transfer of ass

29

ets may be costly in legal fees 6 ) Integration difficult without 100% of shares

7 ) Resistance can raise price

8 ) Minority holdouts

9 ) Technology costs - costs of modifying individual organizations systems etc.

STAProcess and organisational change issues – every organisation has its own culture and business processes

1 0 ) Human Iss

30

ues – Staff feeling insecure and uncertain . 1 1 ) A very high failure rate (close to 50%).

31

DEFENCE STRATEGIES AGAINST MERGERS AND ACUISITIONS

Companies can also adopt strategies and take precautionary actions to avoid hostile takeover. This is very necessary in present day industrial rivalry where a small lack in precaution can result in huge loss to the stakeholders of the firm. Some of the defence strategies against takeover are:

Poison Pills

To avoid hostile takeovers, lawyers created this contractual mechanics that strengthen Target Company. One usual poison pill inside a Corporation Statement is the clause which triggers shareholders rights to buy more company stocks in case of attack. Such action can make severe differences for the raider. If shareholders do really buy more stocks of company with advantaged price, it will be harder to acquire the company control for sure.

It is associated with high cost It may keep the good investors away

Stock option workoutPoison Pill may have the same structure of stock options used for payouts. Under these agreements, once the triggering fact

32

happens, investor have the right to turnkey some right. In poison pill event, most common is an option to buy more shares, with some advantages. Pricedwith better conditions, lower than what bidders does for the corporation it serves for the specific purpose of protecting the corporation current shareholders.

The usual stock option is made to situations of high priced stocks. That usually happens under takeover operations. A takeover hard to be defended usually will have a bid offer with a compatible price, at that moment which is higher than usual for shareholders, with conditions to be accepted by stockholders.

Shark Repellent

Among shark repellent instruments there are: golden parachute, poison pills, greenmail, white knight, etc.

White Knight

Another fortune way to handle a hostile takeover is through White Knight bidders. Usually players of some specific market know each ones history, strategy, strength, advantages, clients, bankers and legal supporters. Meaning beyond similarities or not, there're communities around these companies. In this a strategic partner merges with the target company to add value and increase market capitalization. Such a merger can not only deter the raider, but can also benefit shareholders in the short term, if the terms are favorable, as well as in the long term if the merger is a good strategic fit.

White Squire

33

To avoid takeovers bids, some shareholder may detain a large stake of one company shares. A white squire is similar to a white knight, except that it only exercises a significant minority stake, as opposed to a majority stake. A white squire doesn't have the intention, but rather serves as a figurehead in defense of a hostile takeover. The white squire may often also get special voting rights for their equity stake. With friendly players holding relevant positions of shares, the protected company may feel more comfortable to face an unsolicited offer. A White Squire is a shareholder than itself can make a tender offer. Otherwise it has so much relevance over the company stock composition, that can make raiders takeover more difficult or somewhat expensive. Real White Squire does not take over the target company, and only plays as a defense strategy.

In order to defend these companies, some bankers organize funds for that specific purpose. A White Squire fund is designed to increase share participation in companies under stress.

34

Golden Parachutes

A golden parachute is an agreement between a company and an employee (usually upper executive) specifying that the employee will receive certain significant benefits if employment is terminated. . Without it, officers have no stability, and it may represent inaccurate defense strategy in case of bidders pressure. It can further accelerate drastic and unnecessary measures.

From an overall analysis, cost of golden parachutes is relatively low, compared with disadvantages of its absence. Officers can have minimum guarantees after takeover is accomplished. Otherwise inappropriate attitudes can be taken just to keep officers standings in the market an inside the corporation. Golden parachutes try to make these challenges for the corporation and over officers, as natural as possible. Studies show that these benefits can keep chiefs working without excess pressure and drama, defending the corporation against all, till the end, but with responsibility.

Poison put

In stocks trading, the rights assigned to common stock holders that sharply escalates the price of their stockholding, or allows them to purchase the company's shares at a very attractive fixed price, in case of a hostile takeover attempt.

Super majority amendment

Super-majority amendment is a defensive tactic requiring that a substantial majority, usually 67% and sometimes as much as 90%, of the voting interest of outstanding capital stock to approve a merger. This amendment makes a hostile takeover much more difficult to perform. In most existing cases, however, the supermajority provisions have a board-out clause that provides the board with the power to determine when and if the supermajority provisions will be in effect. Pure supermajority provisions would seriously limit management's flexibility in takeover negotiations.

Fair price amendment

A provision in the bylaws of some publicly-traded companies stating that a company seeking to acquire it must pay a fair price to targeted shareholders. Additionally, the fair price provision mandates that the acquiring company must pay all shareholders the same amount per share in multi-tiered shares. The fair price provision exists both to protect shareholders and to discourage hostile acquisitions by making them more expensive.

35

Classified board

A staggered board of directors or classified board is a practice governing the board of directors of a company, corporation, or other organization in which only a fraction (often one third) of the members of the board of directors is elected each time instead of en masse. In this a structure for a board of directors in which a portion of the directors serve for different term lengths, depending on their particular classification. Under a classified system, directors serve terms usually lasting between one and eight years; longer terms are often awarded to more senior board positions. In publicly held companies, staggered boards have the effect of making hostile takeover attempts more difficult. When a board is staggered, hostile bidders must win more than one proxy fight at successive shareholder meetings in order to exercise control of the target firm.

Authorization of preferred stock

The board of directors is authorized to create a new class of securities with special voting rights. This security, typically preferred stock, may be issued to friendly voting rights. The security preferred stock, may be issued to friendly in a control contest. Thus, this device is a defense takeover bid, although historically it was used to provide the board of directors with flexibility in financing under changing economic conditions. Creation of a poison pill security could be included in his category but generally it's excluded from and treated as a different defensive device.

CROSS BORDER MERGERS AND ACQUISITIONS

The rise of globalization has exponentially increased the market for cross border M&A. In 1996 alone there were over 2000 cross border transactions worth a total of approximately $256 billion. This rapid increase has taken many M&A firms by surprise because the majority of them never had to consider acquiring the capabilities or skills required to effectively handle this kind of transaction. In the past, the market's lack of significance and a more strictly national mindset prevented the vast majority of small and mid-sized companies from considering cross border intermediation as an option which left M&A firms inexperienced in this field. This same reason also prevented the development of any extensive academic works on the subject.

Due to the complicated nature of cross border M&A, the vast majority of cross border actions have unsuccessful results. Cross border intermediation has many more levels of complexity to it than regular intermediation seeing as corporate governance, the power of the average employee,company regulations, political factors customer expectations, and countries' culture are all crucial factors that could spoil the transaction.

36

CASE STUDTCASE STUDY ON THE MERGER OF ICICI BANK AND BANK OF RAJASTHAN

ICICI BANK is India’s second largest bank with total assets of Rs.3,634.00 billion (US$81 billion) at March 31,2010 and profit after tax Rs. 40.25 billion (US$ 896 million) for the year ended March 31,2010.The Banks has a network of 2035 branches and about 5,518 ATMs in India and presence in 18 countries. ICICI Bank offers a wide range of banking products and financial services to corporate and retail customers through a variety of delivery channels and through its specialized subsidiaries in the areas of investment banking, life and non-life insurances, venture capital and asset management.

BANK OF RAJASTHAN, with its stronghold in the state of Rajasthan, has a nationwide presence, serving its customers with a mission of “ together we prosper” engaging actively in Commercial Banking, Merchant Banking, Consumer Banking, Deposit and Money Placement services, Trust and Custodial services, International Banking, Priority Sector Banking.At March 31, 2009, Bank of Rajasthan had 463 Branches and 111 ATMs, total assets of Rs. 172.24 billion, deposits of Rs.151.87 billion and advances of Rs. 77.81 billion. It made a net profit of Rs. 1.18 billion in the year ended March 31, 2009 and a net loss rs.0.10 billion in the nine months ended December 31,2009.

WHY BANK OF RAJASTHAN

ICICI Bank Ltd, Indi’s largest Private sector bank, said it agreed to acquire smaller rival Bank of Rajasthan Ltd to strengthen its presence in northern and western India.Deal would substantially enhance its branch network and it would combine Bank of Rajasthan branch franchise with its strong capital base.The deal, which will give ICICI a sizeable presence in the northwestern desert of Rajasthan, values the small bank at 2.9 times its book value, compared with an Indian Banking sector average of 1.84.

ICICI Bank may be killing two birds with one stone through its proposed merger of the Bank of Rajasthan. Besides getting 468 branches, India’s largest private sector bank will also get control of 58 branches of a regional rural bank sponsored by BoR

37

NEGATIVES

The negatives for ICICI Bank are the potential risks arising from BoR’s non-performing loans and that BoR is trading at expensive valuations

As on FY-10 the net worth of BoR was approximately Rs.760 crore and that of ICICI Bank Rs. 5,17,000 crore. For December 2009 quarter, BoR reported loss of Rs. 44 crore on an income of Rs. 373 crore.

ICICI Bank offered to pay 188.42 rupees per share, in an all-share deal, for Bank of Rajasthan, a premium of 89 percent to the small lender, valuing the business at $668 million. The Bank of Rajasthan approved the deal, which was subject to regulatory agreement.

INFORMATIONThe boards of both banks, granted in-principle approval for acquisition in May 2010.The productivity of ICICI Bank was high compared to Bank of Rajasthan. ICICI recorded a business per branch of 3 billion rupees compared with 47 million rupees of BoR for fiscal 2009. But the non-performing assets(NPAs) record for BoR was better than ICICI Bank. For the Quarter ended Dec 09, BoR recorded 1.05 percent of advances as NPA‟s which was far better than 2.1 percent recorded by ICICI Bank.

TYPE OF ACQUISITIONThis is a horizontal Acquisition in related functional area in same industry (banking) in order to acquire assets of a non-performing company and turn it around by better management; achieving inorganic growth for self by access to 3 million customers of BoR and 463 branches.

PROCESS OF ACQUISITION

Haribhakti & Co. was appointed jointly by both the banks to assess the valuation.Swap ratio of 25:118(25 shares of ICICI for 118 for Bank of Rajasthan) i.e. one ICICI Bank share for 4.72 BoR shares.Post – Acquisition, ICICI Bank ‟s Branch network would go up to 2,463 from 2000The NPAs record for Bank of Rajasthan is better than ICICI Bank. For the quarter ended Dec 09, Bank of Rajasthan recorded 1.05 % of advances as NPA‟s which is far better than 2.1% recorded by ICICI Bank.The deal, entered into after the due diligence by Deloitte, was found satisfactory in maintenance of accounts and no carry of bad loans.

38

39

FAILURE OF MERGERS AND ACQUISITION

Historical trend shows that roughly two third of mergers and acquisitions will disappoint on their own terms. This means they lose value on their stock market. In many cases mergers fail

because companies try to follow their own method of doing work. By analyzing the reason for failure in mergers and eliminating the common mistakes, rate of performance in mergers can be improved. Discussions on the increase in the volume and value of Mergers and Acquisitions during the last decade have become commonplace in the economic and business press. Merger-and-acquisition turned faster in 2010 than at any other time during the last five years.

Merger and acquisition deals worth a total value of US$ 2.04 billion were announced worldwide in the first nine months of 2010. This is 43% more than during the same period in 2006. It seems that more and more companies are merging and thus growing progressively larger.

80% of merger and acquisitions failed because they do not focus on other fields, common mistakes should be avoided. M&As are not regarded as a strategy in themselves, but as an instrument with which to realize management goals and objectives. A variety of motives have been proposed for M&A activity, including: increasing shareholder wealth, creating more opportunities for managers, fostering organizational legitimacy, and responding to pressure from the acquisitions service industry. The overall objective of strategic management is to understand the conditions under which a firm could obtain superior economic performance consequently analyzed efficiency-oriented motives for M&As. Accordingly, the dominant rationale used to explain acquisition activity is that acquiring firms seek higher overall performance.

Failure an occur at any stage of process

Research has conclusively shown that most of the mergers fail to achieve their stated goals.

40

Some of the reasons identified are:

· Corporate Culture Clash · Lack of Communication · Loss of Key people and talent · HR issues · Lack of proper training · Clashes between management · Loss of customers due to apprehensions · Failure to adhere to plans · Inadequate evaluation of target

41

Why the Merger Failed

Culture Clash:

To the principles involved in the deal, there was no clash of cultures. “There was a remarkable meeting of the minds at the senior management level. They look like us, they talk like us,

focused on the same things, and their command of English is impeccable. There was definitely no culture clash there.”. Although DaimlerChrysler's Post-Merger Integration Team spent several million dollars on cultural sensitivity workshops for its employees on topics such as "Sexual Harassment in the American Workplace" and "German Dining Etiquette," the larger rifts in business practice and management sentiment remain unchanged. James Holden, Chrysler president from September 1999 through November 2000, described what he saw as the "marrying up, marrying down" phenomenon. "Mercedes was universally perceived as the fancy, special brand, while Chrysler,

Dodge, Plymouth and Jeep [were] the poorer, blue collar relations"16. This fueled an undercurrent of tension, which was amplified by the fact that American workers earned appreciably more than their German counterparts, sometimes four times as much. The dislike and distrust ran deep, with some Daimler-Benz executives publicly declaring that they "would never drive a Chrysler". "My mother drove a Plymouth, and it barely lasted two-and-ahalf years," commented Mercedes-Benz division chief Jürg en Hubbert to the then Chrysler vice-chairman, pointed out to the Detroit Free Press that "The Jeep Grand Cherokee earned much higher consumer satisfaction ratings than the Mercedes M-Class". With such words flying across public news channels, it seemed quite apparent that culture clash has been eroding the anticipated synergy savings. Much of this clash was intrinsic to a union between two companies which had such different wage structures, corporate hierarchies and values. At a deeper level, the problem was specific to this union: Chrysler and Daimler- Benz's brand images were founded upon diametrically opposite premises. Chrysler's image was one of American excess, and its brand value lay in its assertiveness and risk-taking cowboy aura, all produced within a costcontrolled atmosphere. Mercedes-Benz, in contrast, exuded disciplined German engineering coupled with uncompromising quality. These two sets of brands, were they ever to share platforms or features, would have lost their intrinsic value. Thus the culture clash seemed to exist

as much between products as it did among employees. Distribution and retail sales systems had largely remained separate as well, owing generally to brand bias. Mercedes-Benz dealers, in particular, had proven averse to including Chrysler vehicles in their retail product offerings. The logic had been to protect the sanctity of the Mercedes brand as a hallmark of uncompromising quality. This had certainly hindered the Chrysler Group's market penetration in Europe, where market share remained stagnant at 2%19. Potentially profitable vehicles such

42

as the Dodge Neon and the Jeep Grand Cherokee had been sidelined in favor of the less-cost-effective and troubled Mercedes A-Class compact and M-Class SUV, respectively. The A-Class, a 95 hp, 12 foot long compact with an MSRP of approximately $20,000, competed in Europe against similar vehicles sold by Opel, Volkswagen, Renault and Fiat for approximately $9,000-$16,000. Consumers who ordinarily would have paid a premium for Mercedes' engineering and safety record had been disappointed by the A-Class – which failed an emerg ency maneuver test conducted by a Swedish television station in 199920. The A-Class appeared both overpriced and underengineered for the highly competitive European compact market. The Dodge

Neon, in contrast, could have competed more effectively in this segment with an approximate price of $13,000, similar mechanical specifications, and a record of reliability. Brand bias, however, had prevented this scenario from becoming reality. Differing product development philosophies continued to hamper joint

purchasing and manufacturing efforts as well. Daimler-Benz remained committed to its founding credo of "quality at any cost", while Chrysler aimed to produce price-targeted vehicles. This resulted in a fundamental disconnect in supply-procurement tactics and factory staffing requirements. Upon visiting the Jeep factory in Graz, Austria, Hubbert proclaimed: "If we are to produce the M-Class here as well, we will need to create a separate quality control section and double the number of line workers. It simply can't be built to the same specifications as a Jeep21". The M-Class was eventually built in Graz, but not without an expensive round of retooling and hiring to meet Hubbert's manufacturing standards.

43

Sony acquisition of Columbia pictures

Sony: The Early Years and the Betamax

Masura Ibuka and Akio Morita founded Tokyo Tsushin Kogyo (Tokyo Telecommunications Engineering Company) in 1946, with a mission to be “a clever company that would make new high technology products in ingenious ways."2 With the development of the transistor, the cassette tape, and the pocket-sized radio by 1957, the company renamed itself Sony, from the Latin word sonus meaning "sound." In 1967, Sony formed a joint venture with CBS Records to manufacture and sell records in Japan. Norio Ohga, an opera singer by training, was selected to head the CBS/Sony Group, quickly growing the joint venture into the largest record company in Japan.

When Sony was preparing to launch the Betamax home videocassette recorder in 1974, it invited representatives from rival consumer electronics companies to preview the new technology but did not accept any advice or offers for joint development. Two years later, Sony was surprised to learn that Matsushita subsidiary JVC was preparing to introduce its own Video Home System (VHS) to compete with Betamax. While JVC licensed VHS to other electronics firms, Sony chose to keep its Betamax format to itself – and it s prices even higher – insisting that Betamax was superior in quality. When the less expensive VHS started to take hold, motion picture studios began to release a larger number of their library titles on the format. The more expensive Betamax failed despite its technological to release a larger number of their library titles on the format.

Reason for failure:

· Vastly different corporate culture. · Poor understanding of movie business · Legal issues · Japanese recession

44

RECOMMENDATIONS

After analyzing the advantages and disadvantages of mergers and acquisitions along with consideration of the rate of failure of the same, the companies should prioritize their goal and focus on creating long-term benefits for organizations rather than short term achievements . Defining firm goals, aligning with business strategy, conducting the right type of due diligence, and gaining stakeholder value are also top concerns.

Monitor the Pace: It is clear that the pace of M&A in 2012 will return to pre-recession volumes. Activity will be strong for both financial and strategic acquisitions. Take extreme care during these high volume times to not allow the ego to get in front of the brain on acquisition valuations. Overpaying for an acquisition can doom it to failure from the onset.

Define Firm Goals: What outcome do you desire from a merger or acquisition? Determine if the company can be integrated into current operations or left as a standalone unit, realizing that strategies to channel existing customers into the new company can increase revenues. Potential goals for the supply chain operations include evaluation for consolidation, expansion and streamlined distribution processes, as well as using forecasting tools to model combined revenues.

Align with Growth Strategies: Just because an acquisition seems like a “good deal ,” it should still be determined if it fits with your overall growth strategy. Due diligence that incorporates a careful analysis and weighting of all risk factors must be conducted before execution. This will help answer such key questions as, “Does the risk of acquiring a company for new products or new markets outweigh the perceived benefit of the acquisition cost versus a Greenfield approach?”

Identify the Right Targets: Start by making a target shortlist. Typically, a company will gather as much relevant information on markets, companies, products and services as needed to augment its portfolio. Second, develop a profile of the type of company ideal for acquisition; for instance, your profile may include target revenues of $20 million, North America focused, with an EBIDTA of $4 million.

Do Specific Commercial Due Diligence: type of company and market. Typical labor,

The due diligence process will be specific to the areas covered include financial, legal,

45

intellectual property, IT, environment and market/commercial areas. Also, an operational/supply chain review is needed to identify the potential of additional value for the target company by improving its operations; this review can also uncover any serious operational risks. The outcome will provide full visibility and allow you, as the potential buyer to consider aborting the deal or renegotiating the price.

Identify Any Weaknesses Through Due Diligence: Private equity firms will be looking more for the untapped values, or disguised weaknesses, in the operations of acquisition targets. Understanding a company’s operational effectiveness – from sour cing to customer delivery – will help price discovery and expose potentially costly problems. This year, it is not solely about financial engineering; it is also about uncovering the operational values early in the process and realizing what these are fairly quickly.

Accelerate Integration to Boost Stake Holder Confidence: If the acquisition is complete, it is now time to get results based upon the due diligence process. Stake holders are expecting results by the first 100 days, and acquisition partners are looking to boost their confidence. The first step is to organize and supplement your resources to ensure a quick and efficient performance towards achieving theses goals. And within the first 100 days, it is imperative that companies avoid supply chain disruptions, begin the integration and set a pace for achieving results.

Develop Sound Operations Strategies: Even though business strategies can be identified and understood, supply chain managers often launch too quickly into initiatives that appear to integrate the supply chains. But in, they initiate actions that automatically focus on operational cost savings synergies without first considering what the operations strategies should be – and how these should align with business strategies. So, prior to considering the integration of supply chains, establish operations strategies for geographies, customers, product categories, etc.

Set Integration of Processes and Technologies: It is important to dig into the integration of supply chain processes and technologies to really grasp how the integration will work. Address the Mega supply chain processes of Plan-But-Make-Move-Store-Sell– Return to understand the synergies of supply chain cost reduction, optimization of inventories, synergy of the business combination, facilities rationalization, coordination of supply chain innovation, and the selection of technologies to help transform the processes to the desired vision.

46

Validate Market Perception: The perception of the marketplace regarding a new merger or acquisition can be validated by customers and channel partners beforehand. Important issues include customer loyalty and customer service levels, and how the market will perceive this will be affected by the acquisition.

M&A is no longer just about buying or combining companies; it is about integrating supply chains to create greater business value and spur growth. Following these priorities will allow company leaders to prepare for the business, operations and cultural challenges involved in purchasing or acquiring other entities.

47

CONCLUSION

One size doesn't fit all. Many companies find that the best way to get ahead is to expand ownership boundaries through mergers and acquisitions. For others, separating the public ownership of a subsidiary or business segment offers more advantages. At least in theory, mergers create synergies and economies of scale, expanding operations and cutting costs. Investors can take comfort in the idea that a merger will deliver enhanced market power.

By contrast, de-merged companies often enjoy improved operating performance thanks to redesigned management incentives. Additional capital can fund growth organically or through acquisition. Meanwhile, investors benefit from the improved information flow from de-merged companies.

M&A comes in all shapes and sizes, and investors need to consider the complex issues involved in M&A. The most beneficial form of equity structure involves a complete analysis of the costs and benefits associated with the deals.

Let's recap what we learned in this tutorial:

A merger can happen when two companies decide to combine into one entity or when one company buys another. An acquisition always involves the purchase of one company by another.

The functions of synergy allow for the enhanced cost efficiency of a new entity made from two smaller ones - synergy is the logic behind mergers and acquisitions.

Acquiring companies use various methods to value their targets. Some of these methods are based on comparative ratios - such as the P/E and P/S ratios - replacement cost or discounted cash flow analysis.

An M&A deal can be executed by means of a cash transaction, stock-for-stock transaction or a combination of both. A transaction struck with stock is not taxable.

Break up or de-merger strategies can provide companies with opportunities to raise additional equity funds, unlock hidden shareholder value and sharpen management focus. De-mergers can occur by means of divestitures, carve-outs spinoffs or tracking stocks.

Mergers can fail for many reasons including a lack of management foresight, the inability to overcome practical challenges and loss of revenue momentum from a neglect of day-to-day operations.

48

BIBLIOGRAPHY

Book reference

Michael vag, “Strategic management”

Independent Project on Mergers and Acquisitions in India –A Case Study -Kaushik Roy Choudry

-K. Vinay Kuma

Cases in corporate Acquisitions, Mergers and Takeovers -Edited by Kelly Hill

Websites

www.business.gov.in www.investopedia.com www.economictimes.com

49

![ExamplE - personal.utdallas.edusaquib/ENGR3341/... · space of M (i.e., SM) and the probability, P [M = m], where m e SM. Yates & Goodman 3e 69 Bernoulli (p) Random Variable Definition](https://img.pdfslide.us/doc/110x75/5f0995e57e708231d4278945/example-saquibengr3341-space-of-m-ie-sm-and-the-probability-p-m.jpg)