Embed Size (px)

Citation preview

Slide 11-1 Copyright © 2005 Pearson Education, Inc.

SEVENTH EDITION and EXPANDED SEVENTH EDITION

Copyright © 2005 Pearson Education, Inc.

Chapter 11

Consumer Mathematics

Copyright © 2005 Pearson Education, Inc.

11.1

Percent

Slide 11-4 Copyright © 2005 Pearson Education, Inc.

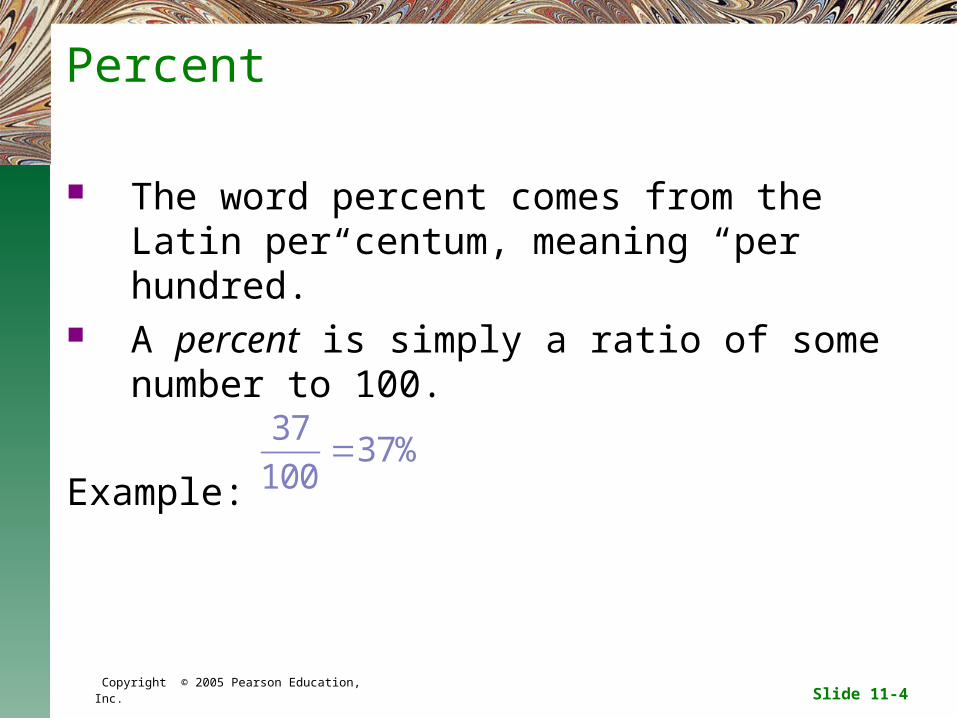

Percent

The word percent comes from the Latin per centum, meaning “per hundred.”

A percent is simply a ratio of some number to 100.

Example: 3737%

100

Slide 11-5 Copyright © 2005 Pearson Education, Inc.

Procedure to Change a Fraction to a Percent Divide the numerator by the denominator. Multiply the quotient by 100 (which has the effect of

moving the decimal point two places to the right). Add a percent sign.

Example: Change to a percent.

Solution: By following the steps above,

1976%.

25

19

25

Slide 11-6 Copyright © 2005 Pearson Education, Inc.

Procedure to Change a Decimal Number to a Percent Multiply the decimal number by 100 Add a percent sign.

Example: Change 0.569 to a percent.

Solution:

0.569 0.569 100 % 56.9%.

Slide 11-7 Copyright © 2005 Pearson Education, Inc.

Procedure to Change a Percent to a Decimal Number Divide the number by 100. Remove the percent sign.Example: Change 14% to a decimal number. Change to a decimal number.Solution:

1%

414

14% 0.14100

1 0.25% 0.25% 0.0025

4 100

Slide 11-8 Copyright © 2005 Pearson Education, Inc.

Percent Change

The percent increase or decrease, or percent change, over a period of time is found by the following formula:

If the amount in the latest period is greater than the amount in the previous period, the answer will be positive and indicate a percent increase.

If the amount in the latest period is smaller than the amount in the previous period, the answer will be negative and indicate a percent decrease.

amount in amount in

latest period previous periodPercent change = 100

amount in previous period

Slide 11-9 Copyright © 2005 Pearson Education, Inc.

Example: Percent Change

The family membership enrollment at a fitness center was 805 families. Five years later, the enrollment was 875 families. Find the percent of change over the five year period.

Solution:

There was about a 8.7% increase in the number of family memberships.

875 805Percent change = 100

8050.08696 100

8.7%

Slide 11-10 Copyright © 2005 Pearson Education, Inc.

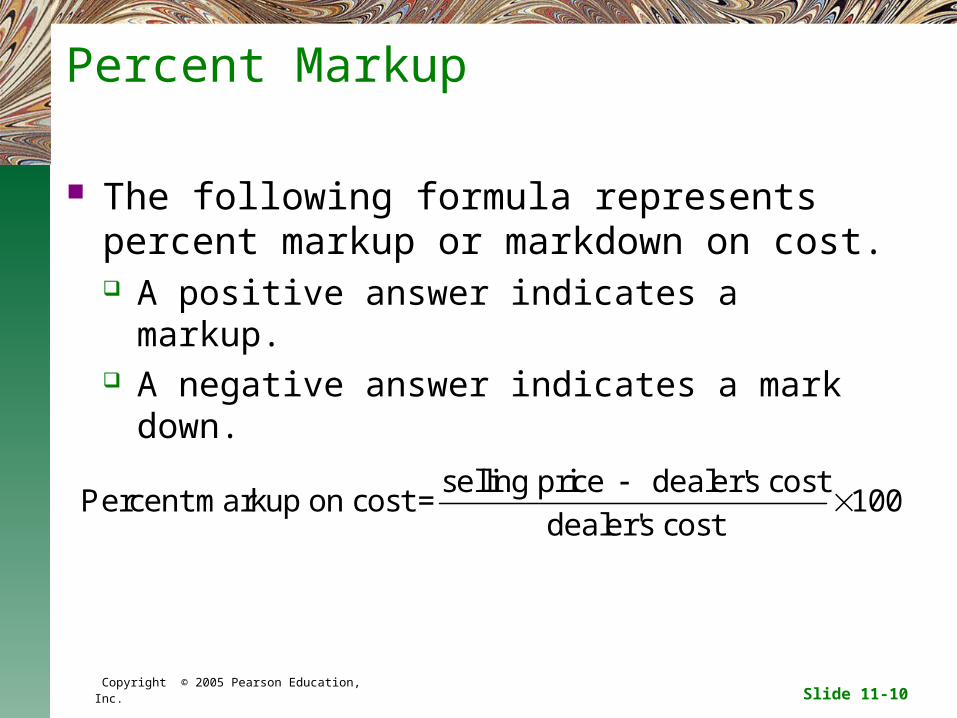

Percent Markup

The following formula represents percent markup or markdown on cost. A positive answer indicates a markup. A negative answer indicates a mark down.

selling price dealer's costPercent markup on cost = 100

dealer's cost

Slide 11-11 Copyright © 2005 Pearson Education, Inc.

Example: Percent Markup

The Dusty Lens Camera Shop pays $68.45 for a camera. The regularly sell them for $157.99. At a weekend sale, they sold for $142.88.

Find: the percentage markup on the regular price the percentage markup on the sale price the percentage decrease of the sale price from the

regular price.

Slide 11-12 Copyright © 2005 Pearson Education, Inc.

Solution:

Thus the percent markup on the regular price was about 130.8%.

Thus the percent markup on the sale price was about 108.7%.

$157.99 - $68.45Percent markup = 100

$68.451.308 100

130.8

$142.88 - $68.45Percent markup = 100

$68.451.087 100

108.7

Slide 11-13 Copyright © 2005 Pearson Education, Inc.

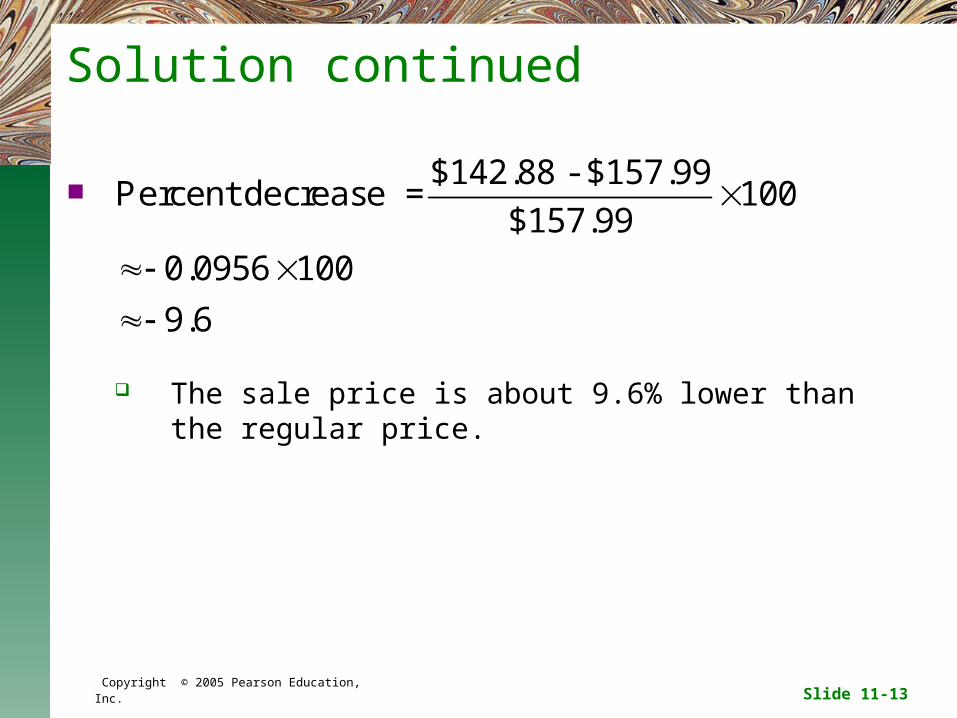

Solution continued

The sale price is about 9.6% lower than the regular price.

$142.88 - $157.99Percent decrease = 100

$157.990.0956 100

9.6

Slide 11-14 Copyright © 2005 Pearson Education, Inc.

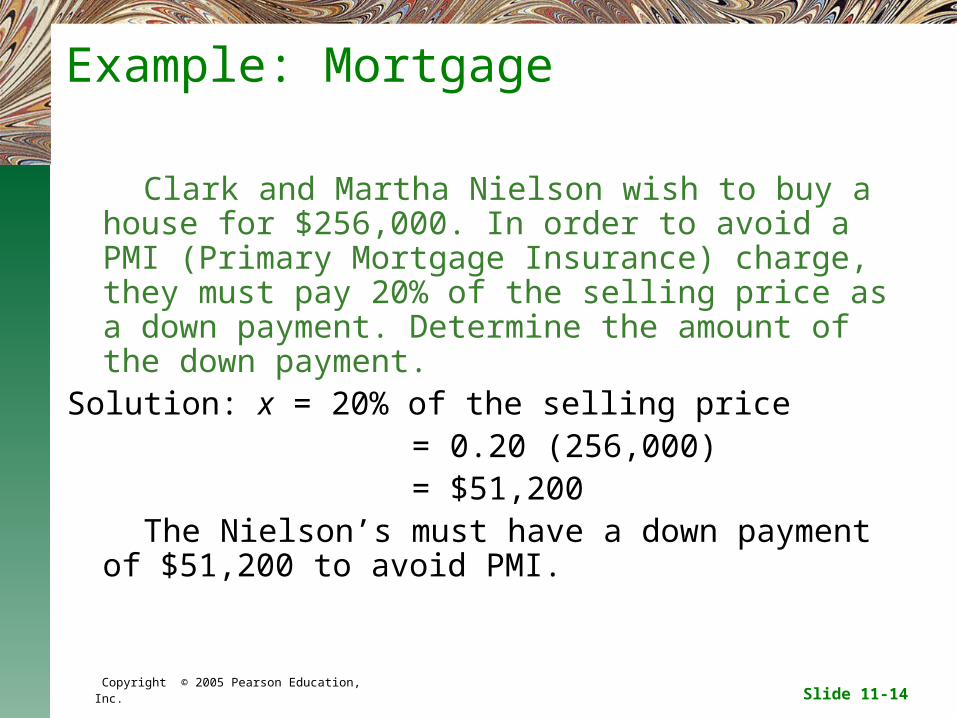

Example: Mortgage

Clark and Martha Nielson wish to buy a house for $256,000. In order to avoid a PMI (Primary Mortgage Insurance) charge, they must pay 20% of the selling price as a down payment. Determine the amount of the down payment.

Solution: x = 20% of the selling price = 0.20 (256,000) = $51,200 The Nielson’s must have a down payment of $51,200 to

avoid PMI.

Copyright © 2005 Pearson Education, Inc.

11.2

Personal Loans and Simple Interest

Slide 11-16 Copyright © 2005 Pearson Education, Inc.

Personal Loans

The amount of credit and the interest that you may obtain depends on the assurance that you can give the lender that you will be able to repay the loan.

Security (collateral) is anything of value pledged by the borrower that the lender may sell or keep if the borrower does not repay the loan.

A personal note is a document that states the terms and conditions of the loan.

Slide 11-17 Copyright © 2005 Pearson Education, Inc.

Interest

Interest is the money the borrower pays to use the lender’s money.

Simple interest is based on the entire amount of the loan for the total period of the loan.

Simple Interest Formula Interest = principal rate time (in years)

i prt

Slide 11-18 Copyright © 2005 Pearson Education, Inc.

Example: Calculating Interest and Payback Amount Lillian needs to borrow $1900 for tuition, from a credit

union. She obtains a 6-month loan with an annual simple interest rate of 5.5%.

Calculate the simple interest on the loan. Determine the amount that Lillian will pay the credit

union at the end of six months.

Slide 11-19 Copyright © 2005 Pearson Education, Inc.

Solution

The simple interest on $1900 at 5.5% for 6 months is $ 52.25.

The amount to be repaid is equal to the principle plus the interest.

To pay off her loan, Lillian will need $1952.25.

$1900 0.055 0.5

$52.25

i p r t

$1900 $52.25

$1952.25

A p i

Slide 11-20 Copyright © 2005 Pearson Education, Inc.

Discount Notes

Another type of loan, the discount note, the interest is paid at the time the borrower receives the loan.

The interest charged in advance is called the bank discount.

Example: Glen Marshall borrowed $2750 on a 8% discount note for a period of 9 months.

Find the interest that must be paid when the loan is received.

Find the actual interest rate for the loan.

Slide 11-21 Copyright © 2005 Pearson Education, Inc.

Solution

The interest that must be paid when he receives the loan is $165.00

9$2750 0.08

12$165.00

i p r t

i

i

Slide 11-22 Copyright © 2005 Pearson Education, Inc.

Solution continued

Calculate the actual interest by using the interest calculated in the previous part. (Note: the principle is actually the amount borrowed minus the interest that was paid.)

The actual rate was 8.5%

9$165.00 $2582

12$165.00 1938.75

165

1938.7500.0851

i p r t

r

r

r

Slide 11-23 Copyright © 2005 Pearson Education, Inc.

The United States Rule

The United States rule states that if a partial payment is made on the loan, interest is computed on the principle from the first day of the loan until the date of the partial payment. The partial payment is used to pay the interest first; the

rest of the payment is used to reduce the principal. The balance due on the date of maturity is found by

computing interest due since the last partial payment and adding this interest to the unpaid principle.

Slide 11-24 Copyright © 2005 Pearson Education, Inc.

Banker’s Rule

The banker’s rule is used to calculate simple interest when applying the United States rule.

The banker’s rule considers a year to have 360 days and any fractional part of a year is the exact number of days of the loan.

Example: Determine the simple interest that will be paid on a $700 loan at an interest rate of 6% for the period March 16 to October 16 using the Banker’s rule.

Slide 11-25 Copyright © 2005 Pearson Education, Inc.

Solution

Referring to Table11.2 on page 607 in your text book, March 16 is the 75th day of the year and October 16 is the 289th day of the year. The period of time in years is 214/360.

The interest is $24.97.

214$700 0.06

360$24.97

i prt

Copyright © 2005 Pearson Education, Inc.

11.3

Compound Interest

Slide 11-27 Copyright © 2005 Pearson Education, Inc.

Investments

An investment is the use of money or capital for income or profit. In a fixed investment, the amount invested as

principle is guaranteed and the interest is computed at a fixed rate.

In a variable investment, neither the principal nor the the interest is guaranteed.

Slide 11-28 Copyright © 2005 Pearson Education, Inc.

Compound Interest Formula

In the formula, A is the amount, p is the principal, r is the rate of interest, t is the time in years, and n is the number of compound periods in a year.

Example: Mr. Martin put $5000 into a trust fund on his daughters 16th birthday. The trust fund pays 9% interest compounded semiannually. What will the trust fund be worth on her 21st birthday?

1nt

rA p

n

Slide 11-29 Copyright © 2005 Pearson Education, Inc.

Solution

The trust fund will be worth $7764.85 on her 21st birthday.

2 5

10

0.095000 1

2

5000 1 0.045

5000 1.5529694

7764.85

A

Slide 11-30 Copyright © 2005 Pearson Education, Inc.

Annual Percent Yield

The effective annual yield or annual percentage yields (APY) is the simple interest rate that gives the same amount of interest as a compound rate over the same period of time.

Slide 11-31 Copyright © 2005 Pearson Education, Inc.

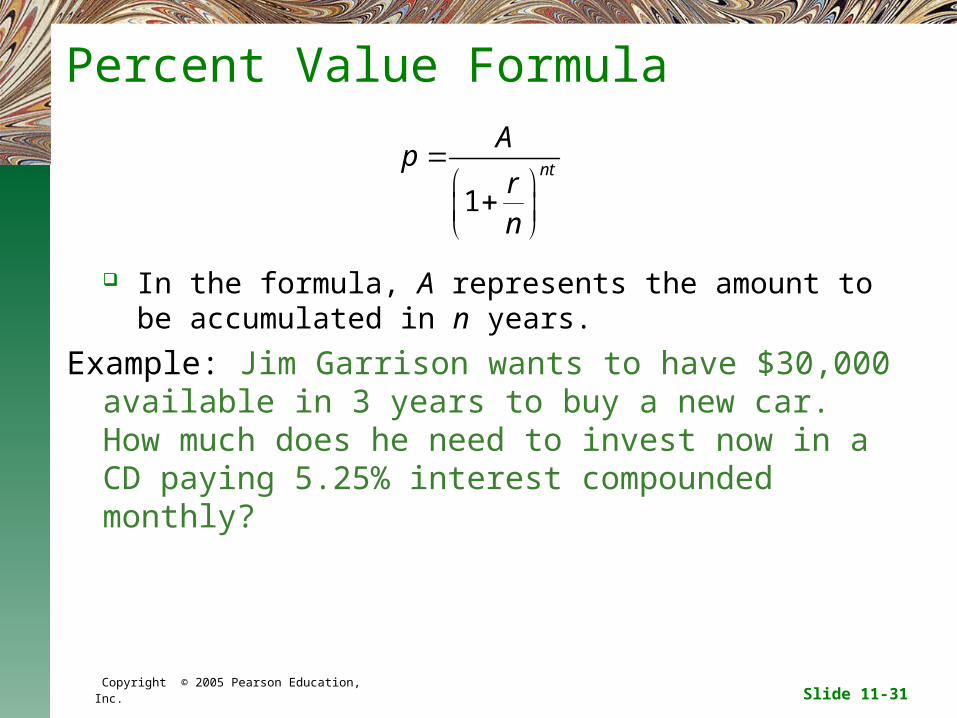

Percent Value Formula

In the formula, A represents the amount to be accumulated in n years.

Example: Jim Garrison wants to have $30,000 available in 3 years to buy a new car. How much does he need to invest now in a CD paying 5.25% interest compounded monthly?

1nt

Ap

rn

Slide 11-32 Copyright © 2005 Pearson Education, Inc.

Solution

12 3

36

1

30,000

0.05251

12

30,000

1.004375

30,000

1.170825,623.51

nt

Ap

rn

Jim Garrison needs to invest approximately $25,623.51 now to have $30,000 in 3 years for his new car.

Copyright © 2005 Pearson Education, Inc.

11.4

Installment Buying

Slide 11-34 Copyright © 2005 Pearson Education, Inc.

Installments

An open-ended installment loan is a loan on which you can make variable payments each month. Examples: credit cards

A fixed installment loan is one on which you pay a fixed amount of money for a set number payments. Examples: college tuition loans, loans for cars etc.

They are usually repaid in 24, 36, 48 or 60 months.

Slide 11-35 Copyright © 2005 Pearson Education, Inc.

Truth in Lending Act in 1969

This law requires that the lending institution tell the borrower two things:

The annual percentage rate (APR) is the true rate of interest charged for a loan.

The total finance charge is the total amount of money the borrower must pay for its use.

Slide 11-36 Copyright © 2005 Pearson Education, Inc.

Fixed Installment Loan

Example: Carlos Ramirez wishes to buy kitchen appliances totaling $3200. The Appliance Center has a finance option of no down payment and 6.5% APR for 36 months.

Determine the finance charge using Table 11.2 on page 623 of your text book.

Determine the monthly payment.

Slide 11-37 Copyright © 2005 Pearson Education, Inc.

Solution

Since Carlos is financing $3200, the number of hundreds is 32.

Total finance charge = $10.34 32 = $330.88. To determine the monthly payments, first calculate the

total installment price by adding the finance charge to the purchase price.

Total Installment = $3200 + $330.88 = $3530.88

Slide 11-38 Copyright © 2005 Pearson Education, Inc.

Solution continued

Next, to determine the number of monthly payments we divide the total installment price by the number of payments:

Monthly payment =

Carlos will have 36 monthly payments of $98.08.

$3530.88$98.08.

36

Slide 11-39 Copyright © 2005 Pearson Education, Inc.

Repaying an Installment Loan Early

Two methods are used to determine the finance charge when you repay an installment loan early.

The actuarial method used the APR tables. The rule of 78s does not use the APR tables

and is less frequently used.

Slide 11-40 Copyright © 2005 Pearson Education, Inc.

Finance Charge Methods

Actuarial method u =

u = unearned interest N = number of remaining monthly

payments (excluding current payment)

P = monthly payment V = the value from the APR table

that corresponds to the annual percentage rate for the number of remaining payments

Rule of 78s u =

u = unearned interest f = original finance charge k = number of remaining monthly

payments (excluding current payment)

n = original number of payments

P V

100

n

V

1

1

f k k

n n

Slide 11-41 Copyright © 2005 Pearson Education, Inc.

Example: Using the Actuarial Method

In our previous example, the APR of the loan was 6.5%. Instead of making the 30th payment, of the 36-payment loan, Carlos wishes to pay the remaining balance and terminate the loan.

Use the actuarial method to determine how much interest Carlos will save by repaying the loan early.

What is the total amount due to pay off the loan early on the day he makes his final payment.

Slide 11-42 Copyright © 2005 Pearson Education, Inc.

Solution

Recall that Carlos makes monthly payments of $98.08. After 30 payments have been made, 6 payments remain. Thus n = 6 and P = $98.08. To determine V, use Table 11.2 on page 623 of your text book. Thus, V = 1.90.

Carlos will save $10.97 in interest.

P V

1006 98.08 1.9

100 1.9$10.97

nu

V

Slide 11-43 Copyright © 2005 Pearson Education, Inc.

Solution continued

Because the remaining payments total 6(98.08) = $588.48. Carlos would have a remaining balance of

$588.48 Total remaining payments

- 10.97 Interest saved

$577.51 Balance due.

A payment of $577.51 plus the 30th monthly payment of $98.08 or $675.59 will terminate the loan.

Slide 11-44 Copyright © 2005 Pearson Education, Inc.

Open-End Installment Loans

A credit card is a popular way of making purchases or borrowing money.

Typically credit card statements contain the following information: balance at the beginning of the period balance at the end of the period (or new balance) the transactions for the period statement closing date payment due date the minimum payment due

Slide 11-45 Copyright © 2005 Pearson Education, Inc.

Average Daily Balance

Many lending institutions use the average daily balance method of calculating the finance charge because they believe that it is fairer to the customer.

With the average daily balance method, a balance is determined each day of the billing period for which there is a transaction in the account.

Slide 11-46 Copyright © 2005 Pearson Education, Inc.

Example: Using the Average Daily Balance Method The balance of Meg Hahn’s credit card on May 1, the

billing date, was $756.50. The following transactions occurred during the month of May.

$64.80Charge: StoreMay 25

$46.25Charge: Restaurant

May 21

$26.50Charge: Gasoline

May 16

$175.00PaymentMay 7

AmountTransactionDate

Slide 11-47 Copyright © 2005 Pearson Education, Inc.

Example: Using the Average Daily Balance Method continued Find the average balance for the billing period. Find the finance charge to be paid on June 1.

Assume, that the interest rate is 2.5% per month.

Find the balance due on June 1.

Slide 11-48 Copyright © 2005 Pearson Education, Inc.

Solution

Find the balance due for each transaction date

+$64.80

+$46.25

+$26.50

$175.00

Transaction

$581.50$756.50May 7

$719.05$654.25May 25

$654.25$608.00May 21

$608.00$581.50May 16

$756.50May 1

Ending Balance

Starting Balance

Date

Slide 11-49 Copyright © 2005 Pearson Education, Inc.

Solution continued

Find the number of days that the balance did not change between each transaction. Multiply the balance due by the number of days the balance did not change. Then find the sum of the products.

$5033.357$719.05May 25

Total 31

4

5

9

6

Days did not change

$5233.50$581.50May 7

Total $20,462.85

$2617.00$654.25May 21

$3040.00$608.00May 16

$4539.00$756.50May 1

Balance(Days)Balance Due Date

Slide 11-50 Copyright © 2005 Pearson Education, Inc.

Solution continued

Next, divide the sum by the number of days in the billing cycle.

Thus, the average daily balance is $660.09. The finance charge is found using the simple interest formula

with the average daily balance as the principal.

Since the finance charge for the month is $16.50, the balance owed on June 1 is $719.05 + $16.50 = $735.55

$20462.85$660.09

31

$660.09 0.025 1 $16.50

Copyright © 2005 Pearson Education, Inc.

7.5

Buying a House with a Mortgage

Slide 11-52 Copyright © 2005 Pearson Education, Inc.

Homeowner’s Mortgage

A long-term loan in which the property is pledged as a security payment of the difference between the down payment and the sale price.

The two types are the adjustable-rate loan and the conventional loan. The major difference between the two is that the interest

rate for a conventional loan is fixed for the duration of the loan, where as the interest rate for the variable-rate loan may change every period, as specified in the loan.

Slide 11-53 Copyright © 2005 Pearson Education, Inc.

Example: Conventional Loans

The Benton’s have decided to purchase a duplex. A selling price of $120,000 was agreed upon. Their bank requires a 20% down payment and a payment of 1 point at closing.

Determine the Benton’s down payment. With a 20% down payment, determine the Benton’s

mortgage. What is the cost of the point paid by the Benton’s on

their mortgage?

Slide 11-54 Copyright © 2005 Pearson Education, Inc.

Solution

The down payment is 0.20 $120,800 = $24,160 The mortgage is the selling price minus the down

payment. $120,800 $24,160 = $96,640. One point equals 1% of the mortgage amount. 0.01 $96,640 = $966.40.

At closing, the Benton’s will pay the down payment of $24,160 to the seller and 1 point, or $966.40 to the bank.

Slide 11-55 Copyright © 2005 Pearson Education, Inc.

Qualifying for a Mortgage

Banks use a formula to determine the maximum monthly payment that they believe is in the purchasers ability to pay.

Example: Suppose the Benton’s gross monthly income is $3600 and that they have 14 payments of $160 per month on their car loan and 11 remaining payments of $45 per month on a loan used to purchase a computer system. The taxes on the duplex they want to purchase is $105 per month and the insurance is $42 per month.

Slide 11-56 Copyright © 2005 Pearson Education, Inc.

Qualifying for a Mortgage continued

What maximum monthly payment does the loan officer think the Benton’s can afford?

The Benton’s want a 25 year $96,640 mortgage. If the interest rate is 7.5%, determine whether the Benton’s qualify for the mortgage.

Solution: Finding 28% of the adjusted monthly income,

0.28 $3395 = $950.60, the maximum monthly payment is determined.

Slide 11-57 Copyright © 2005 Pearson Education, Inc.

Qualifying for a Mortgage continued

Table 11.4 on page 638 of your text book shows that with an interest rate of 7.5%, a 25 year mortgage would have a monthly mortgage payment of $7.39 per thousand of dollars of mortgage.

Then multiply $96.64 $7.39 = $714.17

To this monthly payment (principle and interest) add the taxes and insurance, $861.17. Since this is less than the $950.60 the bank figured they could afford, they should be granted the loan.

96,64096.64

1000

Slide 11-58 Copyright © 2005 Pearson Education, Inc.

Adjustable Rate Mortgages

The monthly mortgage payment rate remains the same for a 1, 2, or 5-year period, even though the interest rate of a mortgage may change.

The monthly payment is readjusted after the time period so the loan will be paid off in the set amount of time or the bank may extend the time period of the loan beyond the predetermined years to make the payment affordable.

Slide 11-59 Copyright © 2005 Pearson Education, Inc.

Other Types of Mortgages

FHA Mortgage VA Mortgage Graduated Payment Mortgage Balloon-Payment Mortgage Home Equity Loans