Embed Size (px)

Citation preview

SIF IMOBILIARE PLC

REPORT AND CONSOLIDATED FINANCIAL

STATEMENTS31 December 2014

SIF IMOBILIARE PLC

REPORT AND CONSOLIDATED FINANCIAL STATEMENTS31 December 2014

CONTENTS PAGE

Board of Directors and other Officers 1

Report of the Board of Directors 2 - 3

Consolidated statement of profit or loss and other comprehensive income 4

Consolidated statement of financial position 5

Consolidated statement of changes in equity 6

Consolidated cash flow statement 7 - 8

Notes to the consolidated financial statements 9 - 23

SIF IMOBILIARE PLC

BOARD OF DIRECTORS AND OTHER OFFICERS

Board of Directors: Administrare Imobiliare S.A.Chrystalla MinaAndroulla Siaxiate

Company Secretary: Romanos Secretarial Ltd30 Karpenisiou StreetCY-1077 NicosiaCyprus

Independent Auditors: Evoserve Auditors LimitedCertified Public Accountants and Registered Auditors7, Andrea Papakosta, 1037P.O.Box 21550, Elefterias Square1510 Nicosia, Cyprus

Registered office: 30 Karpenisiou StreetCY-1077 NicosiaCyprus

Registration number: ΗΕ323682

1

SIF IMOBILIARE PLC

REPORT OF THE BOARD OF DIRECTORS

The Board of Directors of SIF Imobiliare PLC (the 'Company') presents its report and audited consolidated financialstatements of the Company and its subsidiaries (the 'Group') for the year ended 31 December 2014.

Principal activityThe principal activity of the Group, which is unchanged from last year, is the ownership, exploitation, managementand trading of real estate property located in Romania.

The consolidated results of the Group for the year ended 31 December 2014 include the subsidiary companies of theCompany that are property owners, all incorporated in Romania, that is Comalim SA, SIFI BH EST SA, SIFI Cluj RetailSA, SIFI CJ Logistic SA, SIFI Agro SA, SIFI CJ Storage SA, SIFI CS Retail SA, Uniteh SA, Agrorent SA, AdministrareImobiliare SA, SIFI BH IND VEST SA, Bistrita Cluj SA, Central Petrosani SA, Cora SA, SIFI Baia Mare SA, SIFI SighetSA, Urban SA, SIFI TM Agro, SIFI CJ Office SA, SIFI B One SA and SIFI BH Retail SA.

Out of 21 subsidiary companies mentioned above, 7 are currently listed on Bucharest Stock Exchange on RasdaqMarket: Comalim SA, SIFI BH EST SA, SIFI Cluj Retail SA, SIFI CJ Logistic SA, SIFI CJ Argo SA, SIFI CJ Storage SAand Uniteh SA.

ResultsThe Group's results for the year are set out on page 4.

Principal risks and uncertaintiesDue to the nature of the Group's activities, the main risks that the Group faces are the fluctuation of property valuesand the fluctuations in demand for leasing property.

DividendsThe Board of Directors does not recommend the payment of a dividend and the net profit for the year is retained.

Share capitalThere were no changes in the share capital of the Company during the year under review.

Board of DirectorsThe members of the Company's Board of Directors as at 31 December 2014 and at the date of this report arepresented on page 1. All of them were members of the Board of Directors throughout the year ended 31 December2014.

In accordance with the Company's Articles of Association all directors presently members of the Board continue inoffice.

There were no significant changes in the assignment of responsibilities and remuneration of the Board of Directors.

Events after the reporting periodThere were no material events after the reporting period, which have a bearing on the understanding of theconsolidated financial statements.

2

SIF IMOBILIARE PLC

REPORT OF THE BOARD OF DIRECTORS

Independent Auditors During the year the Independent Auditors of the Group, KPMG Limited, resigned and Evoserve Auditors Limited wasappointed in their place.

The Independent Auditors, Evoserve Auditors Limited, have expressed their willingness to continue in office and aresolution giving authority to the Board of Directors to fix their remuneration will be proposed at the Annual GeneralMeeting.

By order of the Board of Directors,

Romanos Secretarial LtdSecretary

Nicosia, 20 August 2015

3

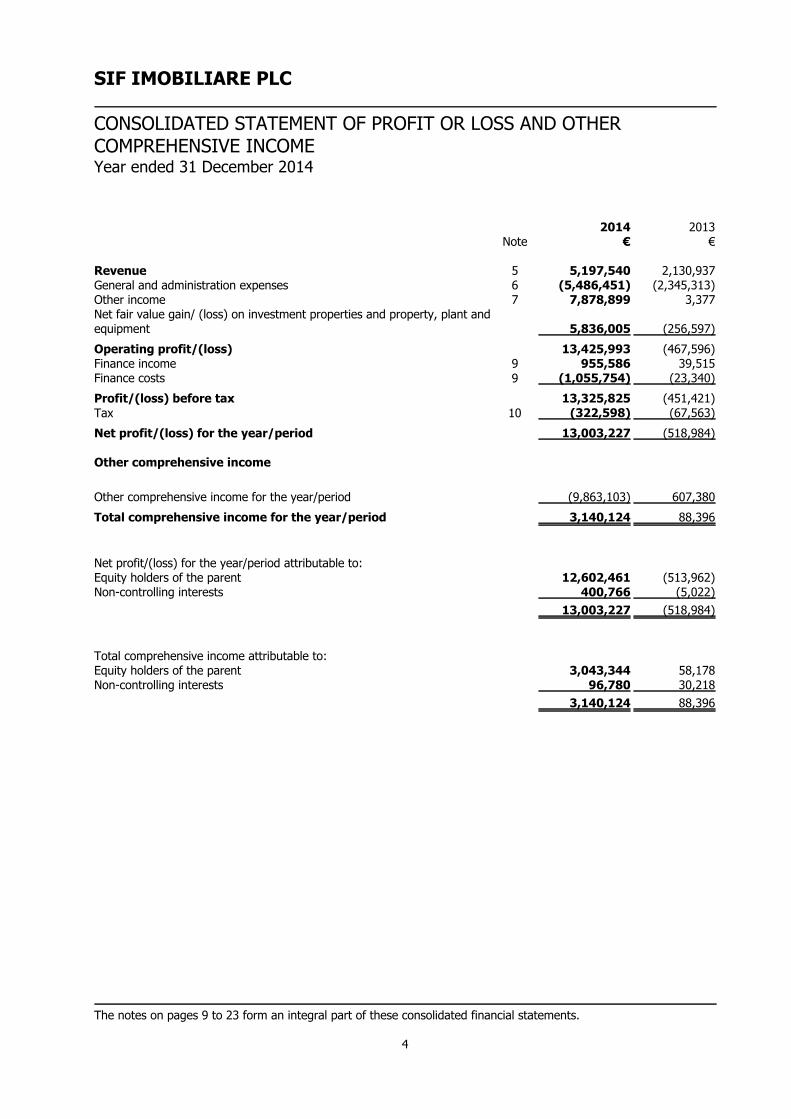

SIF IMOBILIARE PLC

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHERCOMPREHENSIVE INCOMEYear ended 31 December 2014

2014 2013Note € €

Revenue 5 5,197,540 2,130,937General and administration expenses 6 (5,486,451) (2,345,313)Other income 7 7,878,899 3,377Net fair value gain/ (loss) on investment properties and property, plant andequipment 5,836,005 (256,597)

Operating profit/(loss) 13,425,993 (467,596)Finance income 9 955,586 39,515Finance costs 9 (1,055,754) (23,340)

Profit/(loss) before tax 13,325,825 (451,421)Tax 10 (322,598) (67,563)

Net profit/(loss) for the year/period 13,003,227 (518,984)

Other comprehensive income

Other comprehensive income for the year/period (9,863,103) 607,380

Total comprehensive income for the year/period 3,140,124 88,396

Net profit/(loss) for the year/period attributable to:Equity holders of the parent 12,602,461 (513,962)Non-controlling interests 400,766 (5,022)

13,003,227 (518,984)

Total comprehensive income attributable to:Equity holders of the parent 3,043,344 58,178Non-controlling interests 96,780 30,218

3,140,124 88,396

The notes on pages 9 to 23 form an integral part of these consolidated financial statements.

4

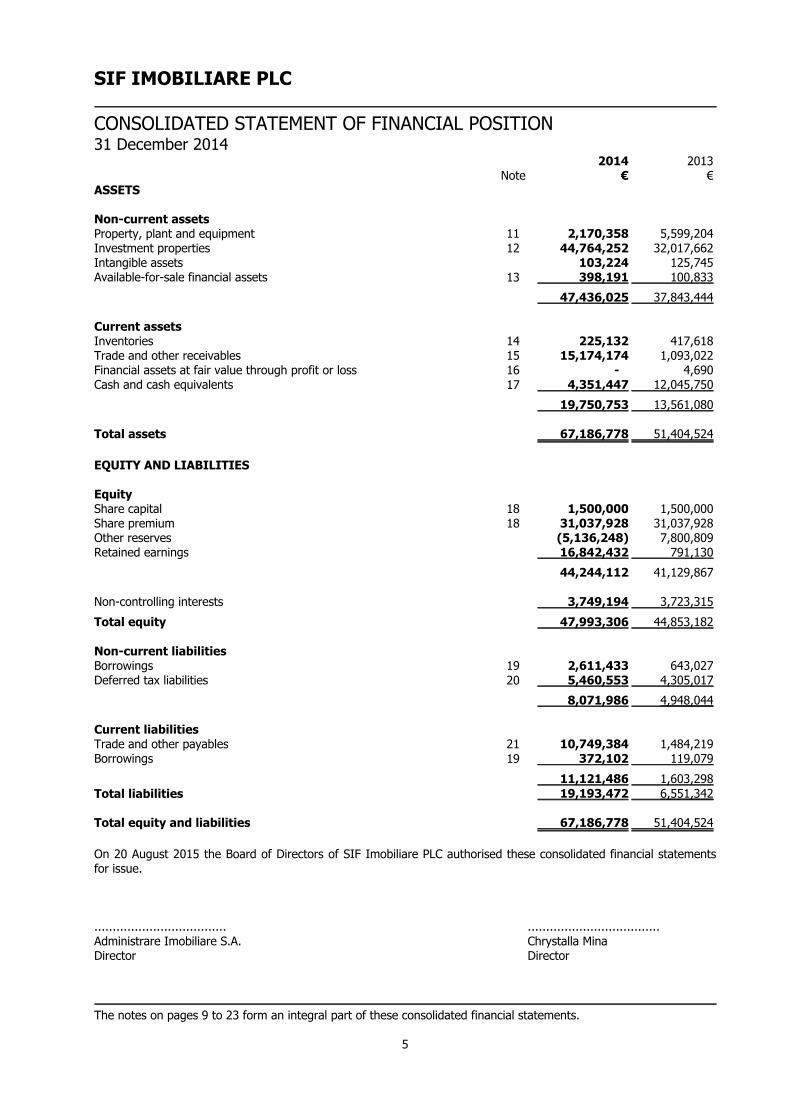

SIF IMOBILIARE PLC

CONSOLIDATED STATEMENT OF FINANCIAL POSITION31 December 2014

2014 2013Note € €

ASSETS

Non-current assetsProperty, plant and equipment 11 2,170,358 5,599,204Investment properties 12 44,764,252 32,017,662Intangible assets 103,224 125,745Available-for-sale financial assets 13 398,191 100,833

47,436,025 37,843,444

Current assetsInventories 14 225,132 417,618Trade and other receivables 15 15,174,174 1,093,022Financial assets at fair value through profit or loss 16 - 4,690Cash and cash equivalents 17 4,351,447 12,045,750

19,750,753 13,561,080

Total assets 67,186,778 51,404,524

EQUITY AND LIABILITIES

EquityShare capital 18 1,500,000 1,500,000Share premium 18 31,037,928 31,037,928Other reserves (5,136,248) 7,800,809Retained earnings 16,842,432 791,130

44,244,112 41,129,867

Non-controlling interests 3,749,194 3,723,315

Total equity 47,993,306 44,853,182

Non-current liabilitiesBorrowings 19 2,611,433 643,027Deferred tax liabilities 20 5,460,553 4,305,017

8,071,986 4,948,044

Current liabilitiesTrade and other payables 21 10,749,384 1,484,219Borrowings 19 372,102 119,079

11,121,486 1,603,298Total liabilities 19,193,472 6,551,342

Total equity and liabilities 67,186,778 51,404,524

On 20 August 2015 the Board of Directors of SIF Imobiliare PLC authorised these consolidated financial statementsfor issue.

.................................... ....................................Administrare Imobiliare S.A. Chrystalla MinaDirector Director

The notes on pages 9 to 23 form an integral part of these consolidated financial statements.

5

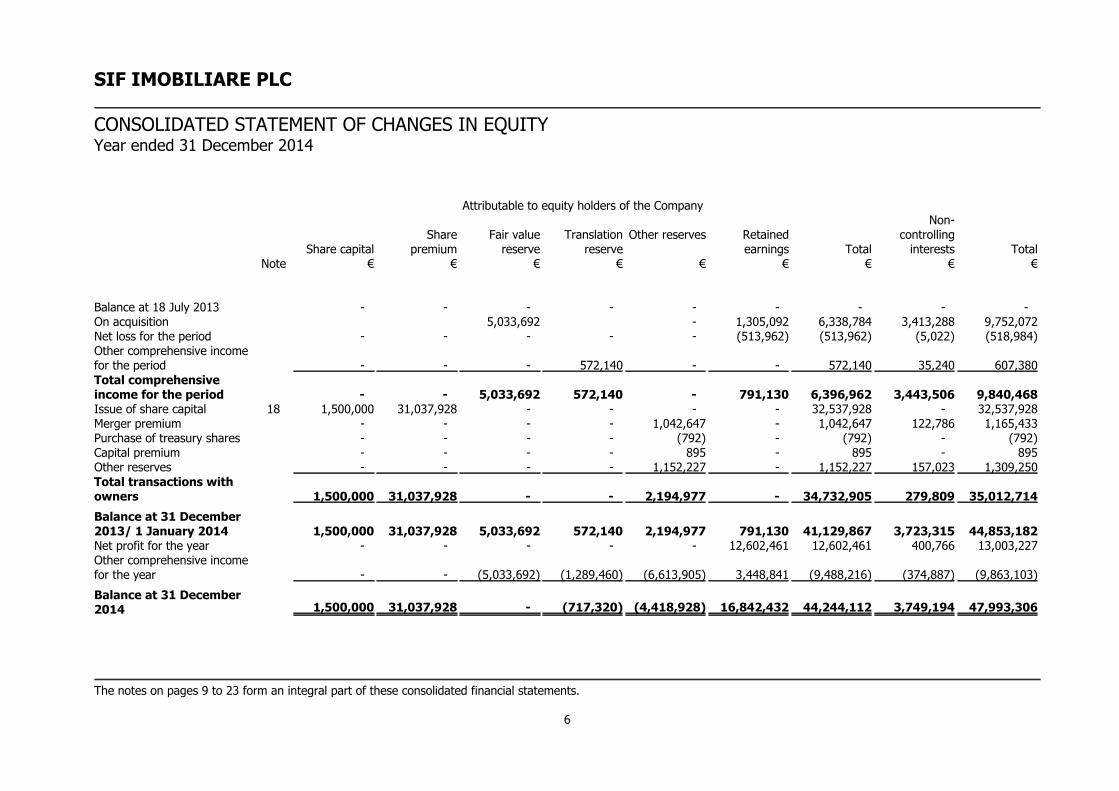

SIF IMOBILIARE PLC

CONSOLIDATED STATEMENT OF CHANGES IN EQUITYYear ended 31 December 2014

Attributable to equity holders of the Company

Share capitalShare

premiumFair value

reserveTranslation

reserveOther reserves Retained

earnings Total

Non-controlling

interests TotalNote € € € € € € € € €

Balance at 18 July 2013 - - - - - - - - -On acquisition 5,033,692 - 1,305,092 6,338,784 3,413,288 9,752,072Net loss for the period - - - - - (513,962) (513,962) (5,022) (518,984)Other comprehensive incomefor the period - - - 572,140 - - 572,140 35,240 607,380Total comprehensiveincome for the period - - 5,033,692 572,140 - 791,130 6,396,962 3,443,506 9,840,468Issue of share capital 18 1,500,000 31,037,928 - - - - 32,537,928 - 32,537,928Merger premium - - - - 1,042,647 - 1,042,647 122,786 1,165,433Purchase of treasury shares - - - - (792) - (792) - (792)Capital premium - - - - 895 - 895 - 895Other reserves - - - - 1,152,227 - 1,152,227 157,023 1,309,250Total transactions withowners 1,500,000 31,037,928 - - 2,194,977 - 34,732,905 279,809 35,012,714

Balance at 31 December2013/ 1 January 2014 1,500,000 31,037,928 5,033,692 572,140 2,194,977 791,130 41,129,867 3,723,315 44,853,182Net profit for the year - - - - - 12,602,461 12,602,461 400,766 13,003,227Other comprehensive incomefor the year - - (5,033,692) (1,289,460) (6,613,905) 3,448,841 (9,488,216) (374,887) (9,863,103)

Balance at 31 December2014 1,500,000 31,037,928 - (717,320) (4,418,928) 16,842,432 44,244,112 3,749,194 47,993,306

The notes on pages 9 to 23 form an integral part of these consolidated financial statements.

6

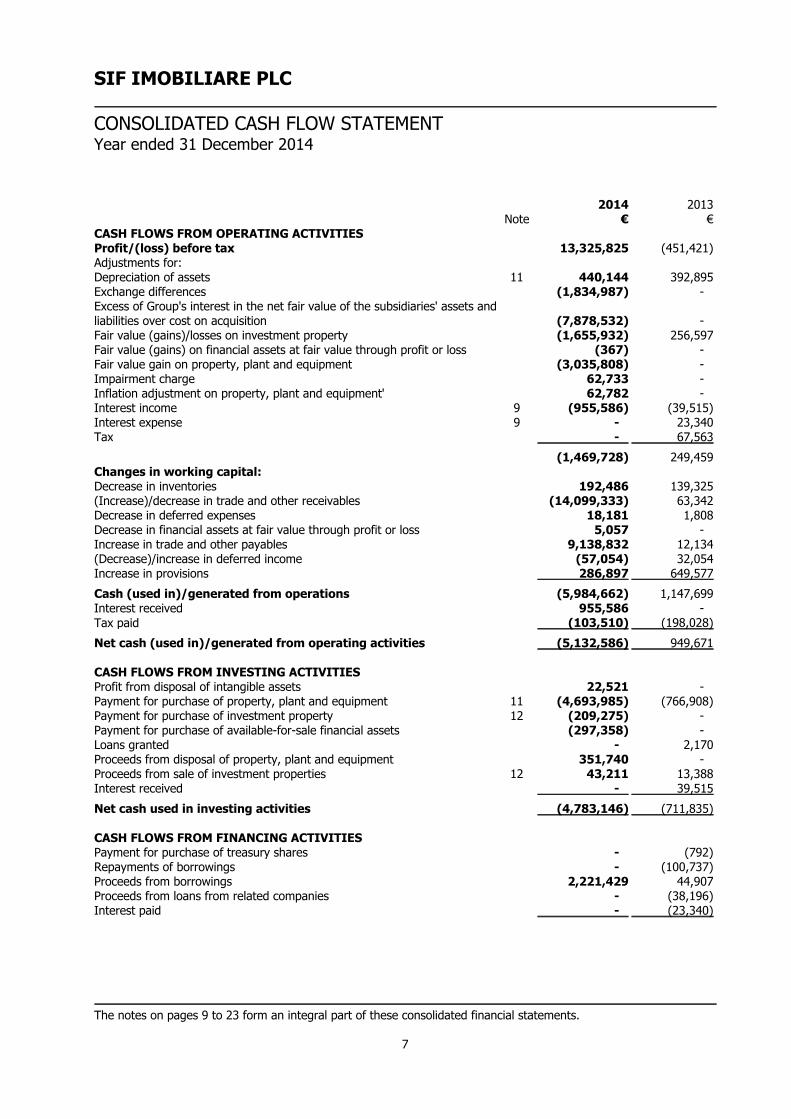

SIF IMOBILIARE PLC

CONSOLIDATED CASH FLOW STATEMENTYear ended 31 December 2014

2014 2013Note € €

CASH FLOWS FROM OPERATING ACTIVITIESProfit/(loss) before tax 13,325,825 (451,421)Adjustments for:Depreciation of assets 11 440,144 392,895Exchange differences (1,834,987) -Excess of Group's interest in the net fair value of the subsidiaries' assets andliabilities over cost on acquisition (7,878,532) -Fair value (gains)/losses on investment property (1,655,932) 256,597Fair value (gains) on financial assets at fair value through profit or loss (367) -Fair value gain on property, plant and equipment (3,035,808) -Impairment charge 62,733 -Inflation adjustment on property, plant and equipment' 62,782 -Interest income 9 (955,586) (39,515)Interest expense 9 - 23,340Tax - 67,563

(1,469,728) 249,459Changes in working capital:Decrease in inventories 192,486 139,325(Increase)/decrease in trade and other receivables (14,099,333) 63,342Decrease in deferred expenses 18,181 1,808Decrease in financial assets at fair value through profit or loss 5,057 -Increase in trade and other payables 9,138,832 12,134(Decrease)/increase in deferred income (57,054) 32,054Increase in provisions 286,897 649,577

Cash (used in)/generated from operations (5,984,662) 1,147,699Interest received 955,586 -Tax paid (103,510) (198,028)

Net cash (used in)/generated from operating activities (5,132,586) 949,671

CASH FLOWS FROM INVESTING ACTIVITIESProfit from disposal of intangible assets 22,521 -Payment for purchase of property, plant and equipment 11 (4,693,985) (766,908)Payment for purchase of investment property 12 (209,275) -Payment for purchase of available-for-sale financial assets (297,358) -Loans granted - 2,170Proceeds from disposal of property, plant and equipment 351,740 -Proceeds from sale of investment properties 12 43,211 13,388Interest received - 39,515

Net cash used in investing activities (4,783,146) (711,835)

CASH FLOWS FROM FINANCING ACTIVITIESPayment for purchase of treasury shares - (792)Repayments of borrowings - (100,737)Proceeds from borrowings 2,221,429 44,907Proceeds from loans from related companies - (38,196)Interest paid - (23,340)

The notes on pages 9 to 23 form an integral part of these consolidated financial statements.

7

SIF IMOBILIARE PLC

CONSOLIDATED CASH FLOW STATEMENTYear ended 31 December 2014

2014 2013Note € €

Net cash generated from/(used in) financing activities 2,221,429 (118,158)

Net (decrease)/increase in cash and cash equivalents (7,694,303) 119,678On acquisition - 12,195,323Cash and cash equivalents at beginning of the year/period 12,045,750 -Effect of exchange rate fluctuations on cash held - (269,251)

Cash and cash equivalents at end of the year/period 17 4,351,447 12,045,750

The notes on pages 9 to 23 form an integral part of these consolidated financial statements.

8

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

1. General information

SIF Imobiliare PLC (the 'Company') and its subsidiaries (together, the 'Group') are engaged in the ownership,exploitation, management and trading of real estate property located in Romania.

The Company was incorporated in Cyprus on 18 July 2013 as a private limited liability company under the CyprusCompanies Law, Cap. 113. Its registered office is at 30 Karpenisiou Street, CY-1077 Nicosia, Cyprus.

2. Basis of preparation

(a) Statement of compliance These consolidated financial statements have been prepared in accordance with International Financial ReportingStandards (IFRSs) as adopted by the European Union (EU) and the requirements of the Cyprus Companies Law,Cap.113.

(b) Basis of measurementThe principal accounting policies adopted in the preparation of these consolidated financial statements are set outbelow. These policies have been consistently applied to all years presented in these consolidated financial statementsunless otherwise stated.

The consolidated financial statements have been prepared under the historical cost convention, except in the case ofland, buildings and equipment, investment property, available-for-sale financial assets, and financial assets andfinancial liabilities at fair value through profit or loss.

(c) Adoption of new and revised IFRS and InterpretationsDuring the current year the Group adopted all the changes to IFRS that are relevant to its operations and areeffective for accounting periods beginning on 18 July 2013. This adoption did not have a material effect on theaccounting policies of the Group.

At the date of approval of these consolidated financial statements, Standards, Revised Standards and Interpretationswere issued by the International Accounting Standards Board which were not yet effective. Some of them wereadopted by the EU and others not yet. The Board of Directors expects that the adoption of these financial reportingstandards in future periods will not have a significant effect on the consolidated financial statements of the Group.

(d) Use of estimates and judgmentsThe preparation of financial statements in accordance with IFRS requires from management the exercise ofjudgment, to make estimates and assumptions that influence the application of accounting principles and the relatedamounts of assets and liabilities, income and expenses. The estimates and underlying assumptions are based onhistorical experience and various other factors that are deemed to be reasonable based on knowledge available atthat time. Actual results may deviate from such estimates.

The estimates and underlying assumptions are revised on a continuous basis. Revisions in accounting estimates arerecognised in the period during which the estimate is revised, if the estimate affects only that period, or in the periodof the revision and future periods, if the revision affects the present as well as future periods.

In particular, information about significant areas of estimation, uncertainty and critical judgments in applyingaccounting policies that have the most significant effect on the amount recognised in the consolidated financialstatements are described below:

Fair value of investment propertyThe fair value of investment property is determined by using valuation techniques. The Group uses itsjudgment to select a variety of methods and make assumptions that are mainly based on market conditionsexisting at each reporting date. The fair value of the investment property has been estimated based on thefair value of the particular investment properties held.

9

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

2. Basis of preparation (continued)

(d) Use of estimates and judgments (continued)

Fair value of financial assetsThe fair value of financial instruments that are not traded in an active market is determined by usingvaluation techniques. The Group uses its judgment to select a variety of methods and make assumptions thatare mainly based on market conditions existing at each reporting date. The fair value of the financial assetsavailable for sale has been estimated based on the fair value of these individual assets.

Impairment of available-for-sale financial assetsThe Group follows the guidance of IAS 39 in determining when an investment is other than temporarilyimpaired. This determination requires significant judgment. In making this judgment, the Group evaluates,among other factors, the duration and extent to which the fair value of an investment is less than its costand the financial health and near term business outlook for the investee, including factors such as industryand sector performance, changes in technology and operational and financing cash flow.

(e) Functional and presentation currencyThe consolidated financial statements are presented in Euro (€) which is the presentation currency of the Group.

3. SIGNIFICANT ACCOUNTING POLICIES

The following accounting policies have been applied consistently in these consolidated financial statements and instating the financial position of the Group. The accounting policies have been consistently applied by all companies ofthe Group.

Basis of consolidationThe Group consolidated financial statements comprise the financial statements of the parent company SIF ImobiliarePlc and the financial statements of the following subsidiaries:

- Comalim SA- SIFI BH EST SA (ex. name: S.C. Legume Fructe S.A.)- SIFI CLUZ Retail SA (ex. name: Arta Culinara SA)- SIFI CJ Logistic SA (ex. name: Comat Cluj SA)- SIFI CJ Agro SA (ex. name: Comcereal Cluj SA)- SIFI CJ Storage SA (ex. name: Napotex SA)- SIFI CS Retail SA (ex. name: Agmonia SA)- Uniteh SA- Agrorent SA- Administrare Imobiliare SA- SIFI BH IND VEST SA (ex. name: Vest Metal SA)- Bistrita Cluj SA- SIFI Baia Mare SA (ex. name: M.C.B. SA)- SIFI SIGHET SA (ex. name: Soiza SA)- Urban SA- SIFI B ONE SA- SIFI BH Retail S.A- SIFI TM AGRO- SIFI CJ Office SA- Central Petrosani SA- Cora SA

Subsidiaries are entities controlled by the Group. Control exists where the Group has the power to govern thefinancial and operating policies of an entity so as to obtain benefits from its activities.

10

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

3. SIGNIFICANT ACCOUNTING POLICIES (continued)

Acquisition of entities under common controlBusiness combinations arising from transfers of interests in entities that are under the control of the shareholder thatcontrols the Group are accounted for as an acquisition at the date when the business combination has occurred. Theassets and liabilities are recognised at the carrying amounts recognised previously in the Group controllingshareholder's financial statements. The difference between the carrying values of the Group's share of the identifiablenet assets and the consideration paid is recorded, in equity as a reserve on acquisition from entities under commoncontrol.

Changes in the Group's ownership interests in existing subsidiariesChanges in the Group's ownership interests in subsidiaries that do not result in the Group losing control over thesubsidiaries are accounted for as equity transactions. The carrying amounts of the Group's interests and the non-controlling interests are adjusted to reflect the changes in their relative interests in the subsidiaries. Any differencebetween the amount by which the non-controlling interests are adjusted and the fair value of the consideration paidor received is recognised directly in equity and attributed to owners of the Company.

When the Group loses control of a subsidiary, the profit or loss on disposal is calculated as the difference between (i)the aggregate of the fair value of the consideration received and the fair value of any retained interest and (ii) theprevious carrying amount of the assets (including goodwill), and liabilities of the subsidiary and any non-controllinginterests. When assets of the subsidiary are carried at revalued amounts or fair values and the related cumulativegain or loss has been recognised in other comprehensive income and accumulated in equity, the amounts previouslyrecognised in other comprehensive income and accumulated in equity are accounted for as if the Company haddirectly disposed of the relevant assets (i.e. reclassified to profit or loss or transferred directly to retained earnings asspecified by applicable IFRSs). The fair value of any investment retained in the former subsidiary at the date whencontrol is lost is regarded as the fair value on initial recognition for subsequent accounting under IAS 39 FinancialInstruments: Recognition and Measurement or, when applicable, the cost on initial recognition of an investment in anassociate or a jointly controlled entity.

The financial statements of subsidiaries acquired or disposed of during the year are included in the consolidatedstatement of profit or loss and other comprehensive income from the date that control commences until the datecontrol ceases. Intra-group balances, and any unrealised income and expenses arising from intra-group transactionsare eliminated in preparing consolidated financial statements.

Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policiesinto line with those used by other members of the Group.

Revenue recognitionRevenues earned by the Group are recognised on the following bases:

Rental incomeRental income is recognised on an accruals basis in accordance with the substance of the relevantagreements.

Rendering of servicesSales of services are recognised in the accounting period in which the services are rendered by reference tocompletion of the specific transaction assessed on the basis of the actual service provided as a proportion ofthe total services to be provided.

Sale of productsSales of goods are recognised when significant risks and rewards of ownership of the goods have beentransferred to the customer, which is usually when the Company has sold or delivered goods to thecustomer, the customer has accepted the goods and collectability of the related receivable is reasonablyassured.

11

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

3. SIGNIFICANT ACCOUNTING POLICIES (continued)

Finance incomeFinance income includes interest income which is recognised based on an accrual basis.

Finance expensesInterest expense and other borrowing costs are recognised to profit or loss using the effective interest method.

Foreign currency translation

Functional and presentation currencyItems included in the Company's financial statements are measured using the currency of the primaryeconomic environment in which the entity operates ('the functional currency'). The financial statements arepresented in Euro (€), which is the Company's functional and presentation currency.

Items included in the subsidiaries financial statements are measured using the currency of the primaryeconomic environment in which the entity operates ('the functional currency'). The financial statements arepresented in Romanian Lei (LEI), which is the subsidiaries' functional and presentation currency. Thefinancial statements of the subsidiary companies have been translated in Euro (€), for consolidationpurposes.

The financial statements of the Group are presented in Euro (€), which is the Group's presentation currency.

Transactions and balancesForeign currency transactions are translated into the functional currency using the exchange rates prevailingat the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of suchtransactions and from the translation at year-end exchange rates of monetary assets and liabilitiesdenominated in foreign currencies are recognised in profit or loss.

The assets and liabilities of the Company's foreign operations (including comparatives) are expressed in Euro usingexchange rates prevailing on the reporting date. Income and expense items (including comparatives) are translated atthe average exchange rates for the period, unless exchange rates fluctuated significantly during that period, in whichcase the exchange rates at the dates of the transactions are used. Exchange differences arising, if any, are classifiedas equity and transferred to the Company's translation reserve. Such translation differences are recognised in profit orloss in the period in which the foreign operation is disposed off.

TaxIncome tax expense represents the sum of the tax currently payable and deferred tax.

Tax liabilities and assets for the current and prior periods are measured at the amount expected to be paid to orrecovered from the taxation authorities, using the tax rates and laws that have been enacted, or substantivelyenacted, by the reporting date. Current tax includes any adjustments to tax payable in respect of previous periods.

Deferred tax is provided in full, using the liability method, on temporary differences arising between the tax bases ofassets and liabilities and their carrying amounts in the consolidated financial statements. Currently enacted tax ratesare used in the determination of deferred tax.

Deferred tax assets are recognised to the extent that it is probable that future taxable profit will be available againstwhich the temporary differences can be utilised.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assetsagainst current tax liabilities and when the deferred taxes relate to the same fiscal authority.

12

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

3. SIGNIFICANT ACCOUNTING POLICIES (continued)

Property, plant and equipmentProperty, plant and equipment are measured at cost less accumulated depreciation and impairment losses.Land and buildings are carried at fair value, based on valuations by external independent valuers, less subsequentdepreciation for buildings. Revaluations are carried out with sufficient regularity such that the carrying amount doesnot differ materially from that which would be determined using fair value at the reporting date. All other property,plant and equipment are stated at historical cost less depreciation.

Increases in the carrying amount arising on revaluation of property, plant and equipment are credited to othercomprehensive income. Decreases that offset previous increases of the same asset are charged against that reserve;all other decreases are charged to profit or loss. Each year the difference between depreciation based on the revaluedcarrying amount of the asset (the depreciation charged to profit or loss) and depreciation based on the asset'soriginal cost is transferred from fair value reserves to retained earnings.

Properties in the course of construction for production, rental or administrative purposes, or for purposes not yetdetermined, are carried at cost, less any recognised impairment loss. Cost includes professional fees and, forqualifying assets, borrowing costs capitalised in accordance with the Group's accounting policy. Depreciation of theseassets, on the same basis as other property assets, commences when the assets are ready for their intended use.

Depreciation is recognised in profit or loss on the straight-line method over the useful lives of each part of an item ofproperty, plant and equipment. The annual depreciation rates used for the current and comparative periods are asfollows:

%Plant and machinery 5 - 33.33Buildings 2 - 5Furniture, fixtures and office equipment 10Tangible assets 6.67 - 33.33

Depreciation methods, useful lives and residual values are reassessed at the reporting date.

Where the carrying amount of an asset is greater than its estimated recoverable amount, the asset is written downimmediately to its recoverable amount.

Expenditure for repairs and maintenance of property, plant and equipment is charged to profit or loss of the year inwhich it is incurred. The cost of major renovations and other subsequent expenditure are included in the carryingamount of the asset when it is probable that future economic benefits in excess of the originally assessed standard ofperformance of the existing asset will flow to the Group. Major renovations are depreciated over the remaining usefullife of the related asset.

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits areexpected to arise from the continued use of the asset. Any gain or loss arising on the disposal or retirement of anitem of property, plant and equipment is determined as the difference between the sales proceeds and the carryingamount of the asset and is recognised in profit or loss.

Investment propertiesInvestment property, which is property held to earn rentals and/or for capital appreciation, is stated at its fair value atthe reporting date. Gains or losses arising from changes in the fair value of investment property are included in profitor loss for the period in which they arise.

An investment property is derecognised upon disposal or when the investment property is permanently withdrawnfrom use and no future economic benefits are expected from the continued use of the asset. Any gain or loss arisingon derecognition of the property (calculated as the difference between the net disposal proceeds and the carryingamount of the asset) is included in profit or loss in the period in which the property is derecognised.

13

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

3. SIGNIFICANT ACCOUNTING POLICIES (continued)

Intangible assetsCosts that are directly associated with identifiable and unique computer software products controlled by the Groupand that will probably generate economic benefits exceeding costs beyond one year are recognised as intangibleassets. Subsequently computer software is carried at cost less any accumulated amortisation and any accumulatedimpairment losses. Expenditure which enhances or extends the performance of computer software programs beyondtheir original specifications is recognised as a capital improvement and added to the original cost of the computersoftware. Costs associated with maintenance of computer software programs are recognised as an expense whenincurred. Computer software costs are amortised using the straight-line method over their useful lives, not exceedinga period of three years. Amortisation commences when the computer software is available for use and is includedwithin administrative expenses.

An intangible asset is derecognised on disposal, or when no future economic benefits are expected from use ordisposal. Gains or losses arising from derecognition of an intangible asset, measured as the difference between thenet disposal proceeds and the carrying amount of the asset, are recognised in profit or loss when the asset isderecognised.

Financial instrumentsFinancial assets and financial liabilities are recognised when the Group becomes a party to the contractual provisionsof the instrument.

(i) Trade receivablesTrade and other receivables are stated at their nominal values after deducting the specific provision for doubtfuldebts, which is calculated based on an examination of all outstanding balances as at the year end. Bad debts arewritten off when identified.

(ii) Investments The Group classifies its investments in equity in the following categories: financial assets at fair value throughprofit or loss and available-for-sale financial assets. The classification depends on the purpose for which theinvestments were acquired. Management determines the classification of investments at initial recognition.

Financial assets at fair value through profit or loss

This category has two subcategories: financial assets held for trading and those designated at fair valuethrough profit or loss at inception. A financial asset is classified in the held for trading category if acquiredprincipally for the purpose of generating a profit from short-term fluctuations in price. Assets in this categoryare classified as current assets if they are either held for trading or are expected to be realised within twelvemonths from the reporting date.

Available-for-sale financial assets

Investments intended to be held for an indefinite period of time, which may be sold in response to needs forliquidity or changes in interest rates, are classified as available-for-sale; these are included in noncurrentassets unless management has the express intention of holding the investment for less than 12 months fromthe reporting date or unless they will need to be sold to raise operating capital, in which case they areincluded in current assets.

Regular purchases and sales of investments are recognised on trade-date which is the date on which the Groupcommits to purchase or sell the asset. Investments are initially recognised at fair value plus transaction costs forall financial assets not carried at fair value through profit or loss. Investments are derecognised when the rightsto receive cash flows from the investments have expired or have been transferred and the Group has transferredsubstantially all risks and rewards of ownership. Available-for-sale financial assets and financial assets at fairvalue through profit or loss are subsequently carried at fair value. Loans and receivables are carried at amortisedcost using the effective interest method.

14

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

3. SIGNIFICANT ACCOUNTING POLICIES (continued)

Financial instruments (continued)

(ii) Investments (continued)

Realised and unrealised gains and losses arising from changes in the fair value of financial assets at fair valuethrough profit or loss are included in profit or loss in the period in which they arise. Unrealised gains and lossesarising from changes in the fair value of available-for-sale financial assets are recognised in other comprehensiveincome and then in equity. When available-for-sale financial assets are sold or impaired, the accumulated fairvalue adjustments are included in profit or loss.

The fair values of quoted investments are based on current bid prices. If the market for a financial asset is notactive (and for unlisted securities), the Group establishes fair value by using valuation techniques. These includethe use of recent arm's length transactions, reference to other instruments that are substantially the same anddiscounted cash flow analysis, making maximum use of market inputs and relying as little as possible on entityspecific inputs. Equity investments for which fair values cannot be measured reliably are recognised at cost lessimpairment.

The Group assesses at each reporting date whether there is objective evidence that a financial asset or a groupof financial assets is impaired. In the case of equity securities classified as available-for-sale, a significant orprolonged decline in the fair value of the security below its cost is considered as an indicator that the securitiesare impaired. If any such evidence exists for available-for-sale financial assets the cumulative loss which ismeasured as the difference between the acquisition cost and the current fair value, less any impairment loss onthat financial asset previously recognised in profit or loss, is removed from equity and recognised in the profit orloss.

For financial assets measured at amortised cost, if in a subsequent period, the amount of the impairment lossdecreases and the decrease can be related objectively to an event occurring after the impairment wasrecognised, the previously recognised impairment loss is reversed through profit or loss to the extent that thecarrying amount of the investment at the date the impairment is reversed does not exceed what the amortisedcost would have been had the impairment not been recognised.

In respect of available for sale equity securities, impairment losses previously recognised in profit or loss are notreversed through profit or loss. Any increase in fair value subsequent to an impairment loss is recognised inother comprehensive income and accumulated under the heading of investments revaluation reserve. In respectof available for sale debt securities, impairment losses are subsequently reversed through profit or loss if anincrease in the fair value of the investment can be objectively related to an event occurring after the recognitionof the impairment loss.

(iii) Cash and cash equivalentsFor the purpose of the consolidated statement of cash flows, cash and cash equivalents comprise cash at bankand in hand.

(iv) BorrowingsBorrowings are recorded initially at the proceeds received, net of transaction costs incurred. Borrowings aresubsequently stated at amortised cost. Any difference between the proceeds (net of transaction costs) and theredemption value is recognised in profit or loss over the period of the borrowings using the effective interestmethod.

(v) Trade payablesTrade payables are stated at their nominal values.

15

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

3. SIGNIFICANT ACCOUNTING POLICIES (continued)

Impairment of assetsAssets that have an indefinite useful life are not subject to amortisation and are tested annually for impairment.Assets that are subject to depreciation or amortisation are reviewed for impairment whenever events or changes incircumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognised for theamount by which the asset's carrying amount exceeds its recoverable amount. The recoverable amount is the higherof an asset's fair value less costs to sell and value in use. For the purposes of assessing impairment, assets aregrouped at the lowest levels for which there are separately identifiable cash flows (cash-generating units).

InventoriesStocks are stated at the lower of cost and net realisable value. The cost is determined using the weighted averagemethod. The net realisable value is based on the estimated selling price less any additional expenses expected tooccur by the stock's date of sale.

Share capitalOrdinary shares are classified as equity. The difference between the fair value of the consideration received by theCompany and the nominal value of the share capital being used is taken to the share premium account.

4. Financial risk management

Financial risk factorsThe Group is exposed to interest rate risk, credit risk, liquidity risk, currency risk and capital risk management arisingfrom the financial instruments it holds. The risk management policies employed by the Group to manage these risksare discussed below:

4.1 Interest rate riskInterest rate risk is the risk that the value of financial instruments will fluctuate due to changes in market interestrates. Borrowings issued at variable rates expose the Group to cash flow interest rate risk. Borrowings issued at fixedrates expose the Group to fair value interest rate risk. The Group's management monitors the interest ratefluctuations on a continuous basis and acts accordingly.

4.2 Credit riskCredit risk arises when a failure by counter parties to discharge their obligations could reduce the amount of futurecash inflows from financial assets on hand at the reporting date. The Group has no significant concentration of creditrisk. The Group has policies in place to ensure that sales of products and services are made to customers with anappropriate credit history and monitors on a continuous basis the ageing profile of its receivables.

4.3 Liquidity riskLiquidity risk is the risk that arises when the maturity of assets and liabilities does not match. An unmatched positionpotentially enhances profitability, but can also increase the risk of losses. The Group has procedures with the objectof minimising such losses such as maintaining sufficient cash and other highly liquid current assets and by havingavailable an adequate amount of committed credit facilities.

The following tables detail the Group's remaining contractual maturity for its financial liabilities. The tables have beendrawn up based on the undiscounted cash flows of financial liabilities based on the earliest date on which the Groupcan be required to pay. The table includes both interest and principal cash flows.

31 December 2014 Carryingamounts

€Bank loans 2,615,336Other loans 368,199Trade and other payables 9,561,216

12,544,751

16

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

4. Financial risk management (continued)

4.3 Liquidity risk (continued)

31 December 2013 Carryingamounts

€Bank loans 749,196Other loans 12,910Trade and other payables 577,834

1,339,940

4.4 Currency riskCurrency risk is the risk that the value of financial instruments will fluctuate due to changes in foreign exchange rates.Currency risk arises when future commercial transactions and recognised assets and liabilities are denominated in acurrency that is not the Group's measurement currency. The Group is exposed to foreign exchange risk arising fromvarious currency exposures. The Group's management monitors the exchange rate fluctuations on a continuous basisand acts accordingly.

4.5 Capital risk managementThe Group manages its capital to ensure that it will be able to continue as a going concern while maximising thereturn to shareholders through the optimisation of the debt and equity balance. The Group's overall strategy remainsunchanged from last year.

5. Revenue2014 2013

€ €Sales of products - 637,924Rental income 3,462,907 1,091,771Other income 1,734,633 401,242

5,197,540 2,130,937

6. General and administration expenses

2014 2013€ €

Costs of materials used 1,448,738 617,788Staff costs (Note 7) 1,027,707 425,736Fuel, power and water 75,318 215,044Taxes and penalties 323,085 73,480Other expenses 985,007 143,571Professional and other related expenses 705,952 156,533Provisions 308,833 246,033Impairment of assets 62,733 59,233Traveling and entertainment expenses 38,500 -Auditors' remuneration 15,000 15,000Rent payable 31,498 -Repairs and maintenance 8,797 -Common expenses charged to tenants 15,139 -Depreciation and amortisation expense 440,144 392,895

5,486,451 2,345,313

17

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

7. Other income

2014 2013€ €

Excess of Group's interest in the net fair value of the subsidiaries' assets andliabilities over cost on acquisition 7,878,532 -Sundry operating income 367 3,377

7,878,899 3,377

8. Staff costs

2014 2013€ €

Wages and salaries 808,650 287,616Social insurance costs 219,057 90,367Other - 47,753

1,027,707 425,736

9. Finance income/cost

2014 2013€ €

Interest income 955,586 39,515

Finance income 955,586 39,515

Net foreign exchange transaction losses - (2,597)Interest expense - (18,012)Sundry finance expenses (1,055,754) (2,731)

Finance costs (1,055,754) (23,340)

Net finance (costs)/income (100,168) 16,175

10. Tax

2014 2013€ €

Corporation tax - current year/period 322,598 67,563

Charge for the year/period 322,598 67,563

The applicable tax rate in Cyprus is 12.5% and in Romania 16%.

18

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

11. Property, plant and equipment

Land andbuildings

Plant andmachinery

Furniture,fixtures and

officeequipment

Tangibleassets inprogress

Total

€ € € € €Cost or valuationAcquisitions through business combinations 39,305,503 1,800,962 222,404 444,859 41,773,728Additions 265,927 6,238 47,732 447,011 766,908Disposals (2,473) (120,545) (105,661) (40,209) (268,888)Exchange differences 175,400 (954) (115) 886 175,217Adjustment on revaluation (575,883) - - - (575,883)Reclassification to investment property (31,957,545) 11,926 10,005 (409,758) (32,345,372)Other - 1,663 576 - 2,239

Balance at 31 December 2013 7,210,929 1,699,290 174,941 442,789 9,527,949

Balance at 31 December 2013/ 1 January2014 7,210,929 1,699,290 174,941 442,789 9,527,949Additions 3,821,338 120,965 5,047 746,635 4,693,985Disposals (212) (345,930) (5,598) - (351,740)Exchange differences 578,400 572,583 18,311 - 1,169,294Adjustment on revaluation 3,148,386 - - (112,578) 3,035,808Reclassification (to)/ from investment property (10,230,905) (38,263) 21,857 (651,515) (10,898,826)Inflation adjustment - - (9,724) - (9,724)

Balance at 31 December 2014 4,527,936 2,008,645 204,834 425,331 7,166,746

DepreciationAcquisitions through business combinations (2,041,459) (1,189,393) (60,259) (244,739) (3,535,850)Charge for the period (223,553) (28,974) (4,235) (136,133) (392,895)

Balance at 31 December 2013 (2,265,012) (1,218,367) (64,494) (380,872) (3,928,745)

Charge for the year (337,765) (62,065) (27,845) (12,469) (440,144)On disposals (289,199) (201,884) (1,627) - (492,710)Impairment charge - (62,733) - - (62,733)Inflation adjustment - (62,900) (9,156) - (72,056)

Balance at 31 December 2014 (2,891,976) (1,607,949) (103,122) (393,341) (4,996,388)

Net book amount

Balance at 31 December 2014 1,635,960 400,696 101,712 31,990 2,170,358

Balance at 31 December 2013 4,945,917 480,923 110,447 61,917 5,599,204

12. Investment properties

2014 2013€ €

Balance at 1 January/ at 21 August 32,017,662 -Acquisitions through business combinations - 32,600,996Additions 209,275 -Disposals (43,211) -Transfer from property, plant and equipment 10,898,826 -Exchange differences 25,768 (326,737)Fair value adjustment 1,655,932 (256,597)

Balance at 31 December 44,764,252 32,017,662

19

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

12. Investment properties (continued)

The investment properties are valued annually on 31 December at fair value comprising open-market value by anindependent professionally qualified valuer. Fair value is based on an active market process adjusted if necessary forany differences in the nature, location or condition of the property.

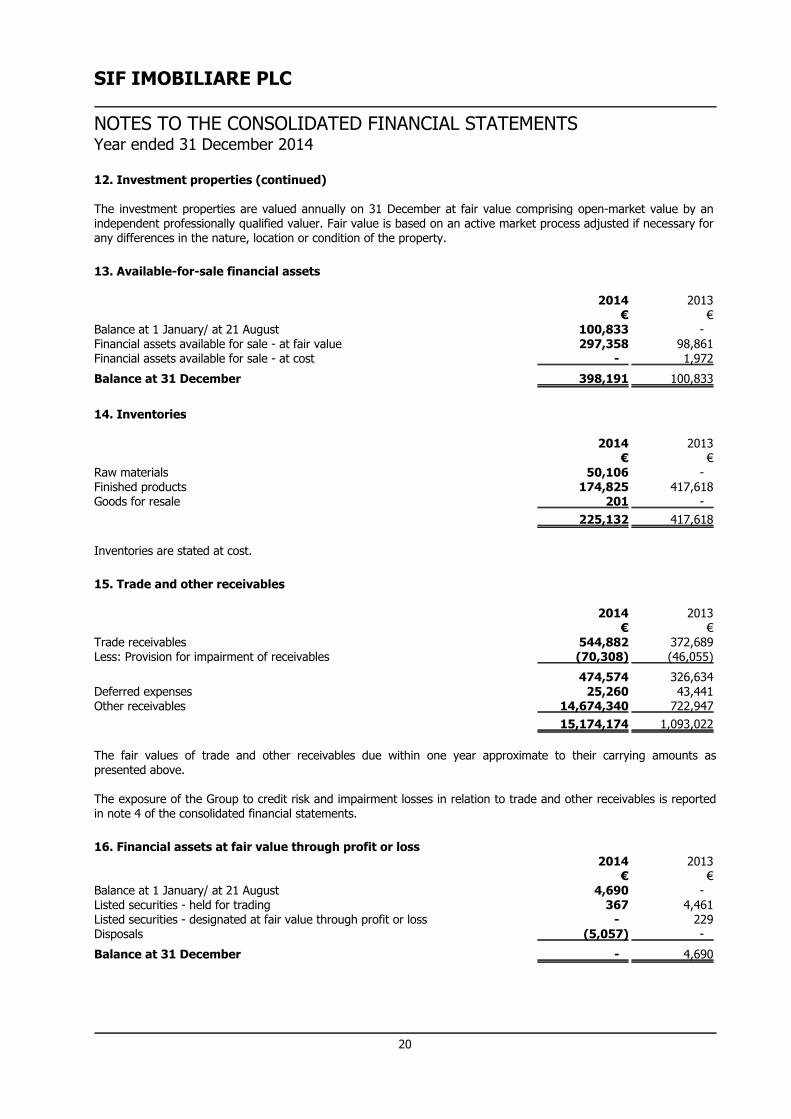

13. Available-for-sale financial assets

2014 2013€ €

Balance at 1 January/ at 21 August 100,833 -Financial assets available for sale - at fair value 297,358 98,861Financial assets available for sale - at cost - 1,972

Balance at 31 December 398,191 100,833

14. Inventories

2014 2013€ €

Raw materials 50,106 -Finished products 174,825 417,618Goods for resale 201 -

225,132 417,618

Inventories are stated at cost.

15. Trade and other receivables

2014 2013€ €

Trade receivables 544,882 372,689Less: Provision for impairment of receivables (70,308) (46,055)

474,574 326,634Deferred expenses 25,260 43,441Other receivables 14,674,340 722,947

15,174,174 1,093,022

The fair values of trade and other receivables due within one year approximate to their carrying amounts aspresented above.

The exposure of the Group to credit risk and impairment losses in relation to trade and other receivables is reportedin note 4 of the consolidated financial statements.

16. Financial assets at fair value through profit or loss2014 2013

€ €Balance at 1 January/ at 21 August 4,690 -Listed securities - held for trading 367 4,461Listed securities - designated at fair value through profit or loss - 229Disposals (5,057) -

Balance at 31 December - 4,690

20

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

16. Financial assets at fair value through profit or loss (continued)

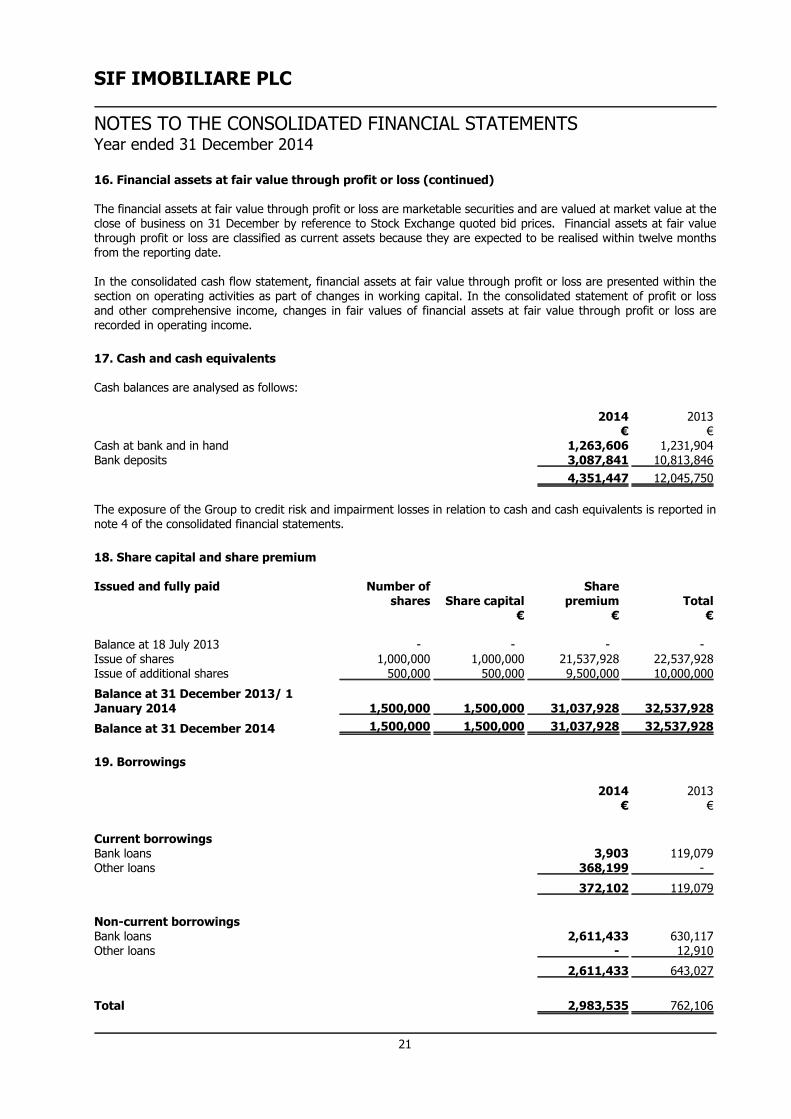

The financial assets at fair value through profit or loss are marketable securities and are valued at market value at theclose of business on 31 December by reference to Stock Exchange quoted bid prices. Financial assets at fair valuethrough profit or loss are classified as current assets because they are expected to be realised within twelve monthsfrom the reporting date.

In the consolidated cash flow statement, financial assets at fair value through profit or loss are presented within thesection on operating activities as part of changes in working capital. In the consolidated statement of profit or lossand other comprehensive income, changes in fair values of financial assets at fair value through profit or loss arerecorded in operating income.

17. Cash and cash equivalents

Cash balances are analysed as follows:

2014 2013€ €

Cash at bank and in hand 1,263,606 1,231,904Bank deposits 3,087,841 10,813,846

4,351,447 12,045,750

The exposure of the Group to credit risk and impairment losses in relation to cash and cash equivalents is reported innote 4 of the consolidated financial statements.

18. Share capital and share premium

Issued and fully paid Number ofshares Share capital

Sharepremium Total

€ € €

Balance at 18 July 2013 - - - -Issue of shares 1,000,000 1,000,000 21,537,928 22,537,928Issue of additional shares 500,000 500,000 9,500,000 10,000,000

Balance at 31 December 2013/ 1January 2014 1,500,000 1,500,000 31,037,928 32,537,928

Balance at 31 December 2014 1,500,000 1,500,000 31,037,928 32,537,928

19. Borrowings

2014 2013€ €

Current borrowingsBank loans 3,903 119,079Other loans 368,199 -

372,102 119,079

Non-current borrowingsBank loans 2,611,433 630,117Other loans - 12,910

2,611,433 643,027

Total 2,983,535 762,106

21

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

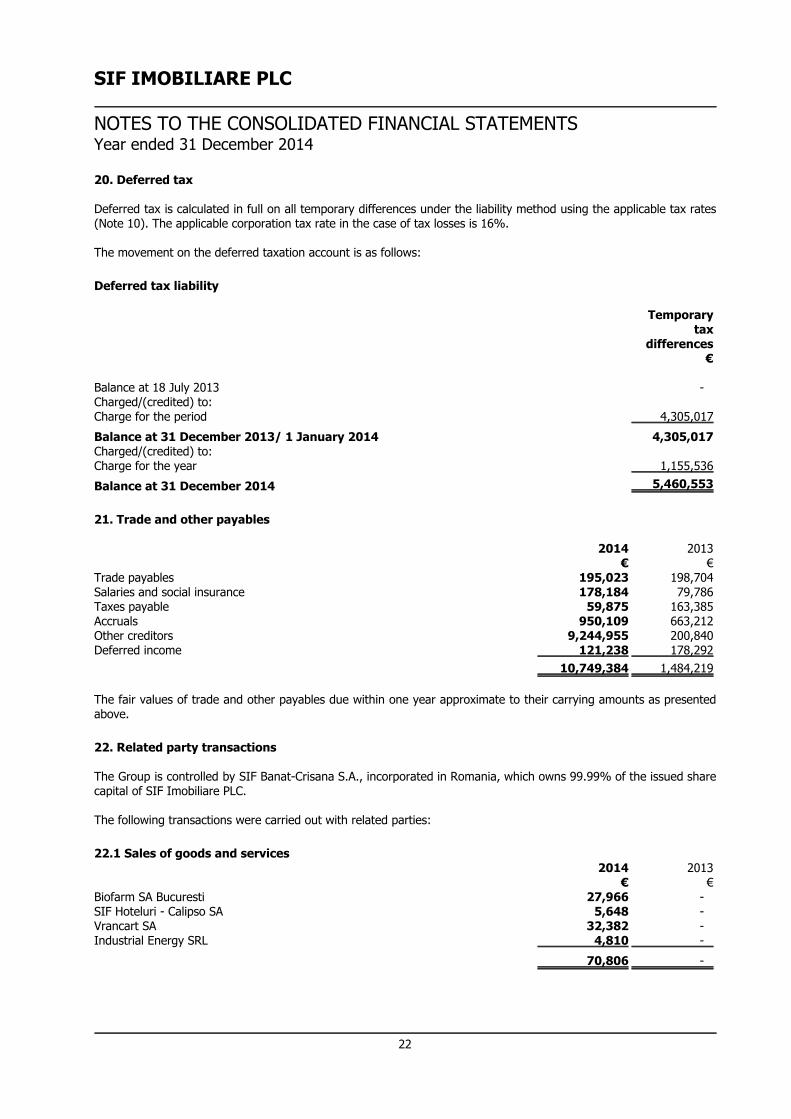

20. Deferred tax

Deferred tax is calculated in full on all temporary differences under the liability method using the applicable tax rates(Note 10). The applicable corporation tax rate in the case of tax losses is 16%.

The movement on the deferred taxation account is as follows:

Deferred tax liability

Temporarytax

differences€

Balance at 18 July 2013 -Charged/(credited) to:Charge for the period 4,305,017

Balance at 31 December 2013/ 1 January 2014 4,305,017Charged/(credited) to:Charge for the year 1,155,536

Balance at 31 December 2014 5,460,553

21. Trade and other payables

2014 2013€ €

Trade payables 195,023 198,704Salaries and social insurance 178,184 79,786Taxes payable 59,875 163,385Accruals 950,109 663,212Other creditors 9,244,955 200,840Deferred income 121,238 178,292

10,749,384 1,484,219

The fair values of trade and other payables due within one year approximate to their carrying amounts as presentedabove.

22. Related party transactions

The Group is controlled by SIF Banat-Crisana S.A., incorporated in Romania, which owns 99.99% of the issued sharecapital of SIF Imobiliare PLC.

The following transactions were carried out with related parties:

22.1 Sales of goods and services2014 2013

€ €Biofarm SA Bucuresti 27,966 -SIF Hoteluri - Calipso SA 5,648 -Vrancart SA 32,382 -Industrial Energy SRL 4,810 -

70,806 -

22

SIF IMOBILIARE PLC

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSYear ended 31 December 2014

22. Related party transactions (continued)

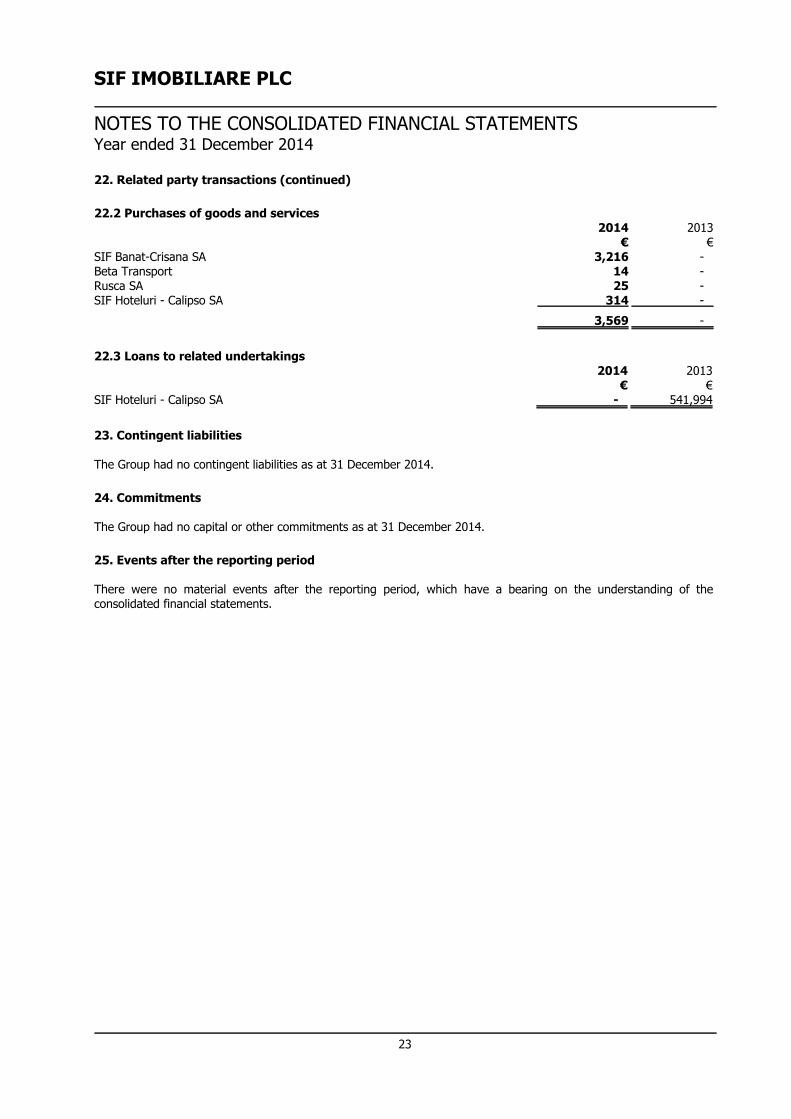

22.2 Purchases of goods and services2014 2013

€ €SIF Banat-Crisana SA 3,216 -Beta Transport 14 -Rusca SA 25 -SIF Hoteluri - Calipso SA 314 -

3,569 -

22.3 Loans to related undertakings2014 2013

€ €SIF Hoteluri - Calipso SA - 541,994

23. Contingent liabilities

The Group had no contingent liabilities as at 31 December 2014.

24. Commitments

The Group had no capital or other commitments as at 31 December 2014.

25. Events after the reporting period

There were no material events after the reporting period, which have a bearing on the understanding of theconsolidated financial statements.

23

![[ANALIZA / STUDIUL PI ETEI IMOBILIARE IN ANUL 2011 ] · [ANALIZA / STUDIUL PI ETEI IMOBILIARE IN ANUL 2011 ] ... cu mediul investional si sectorul imobiliar din judetul Cluj si orasul](https://img.pdfslide.us/doc/110x75/5e52a5346fd3277d832f406a/analiza-studiul-pi-etei-imobiliare-in-anul-2011-analiza-studiul-pi-etei.jpg)