Embed Size (px)

Citation preview

Sidoti Micro Cap Investor Conference January 10, 2011

2

The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for forward-looking statements. Certain information included in this presentation contains statements that are forward-looking, such as statements relating to results of operations and financial conditions and business development activities, as well as capital spending and financing sources. Such forward-looking information involves important risks and uncertainties that could significantly affect anticipated results in the future and, accordingly, such results may differ materially from those expressed in any forward-looking statements made by or on behalf of Mercer. For more information regarding these risks and uncertainties, review Mercer’s filings with the United States Securities and Exchange Commission.

Forward Looking Statements

3

Overview of the Company

4

Company OverviewThree world-class, large, modern mills that produce 1.5 million tonnes of high-quality northern bleached softwood kraft (“NBSK”) pulp, a premium grade of pulp

Strategically located mills in British Columbia and Germany

Excellent fiber baskets, with ready access to key global markets

Significant and growing revenue from sale of excess renewable, carbon-neutral electricity

Mercer has grown through organic expansion, greenfield development and acquisition and its financial structure offers very high leverage to the pulp cycle

Company employs approximately 1,500 people and generated over €820 million (US$1,119 million*) in revenues in the past twelve months

U.S. domiciled corporation listed on both the NASDAQ (MERC) and the TSX (MRI.U)

Management believes the supply/demand outlook for NBSK is strong* At a EUR/USD fx rate of 1.3645

5

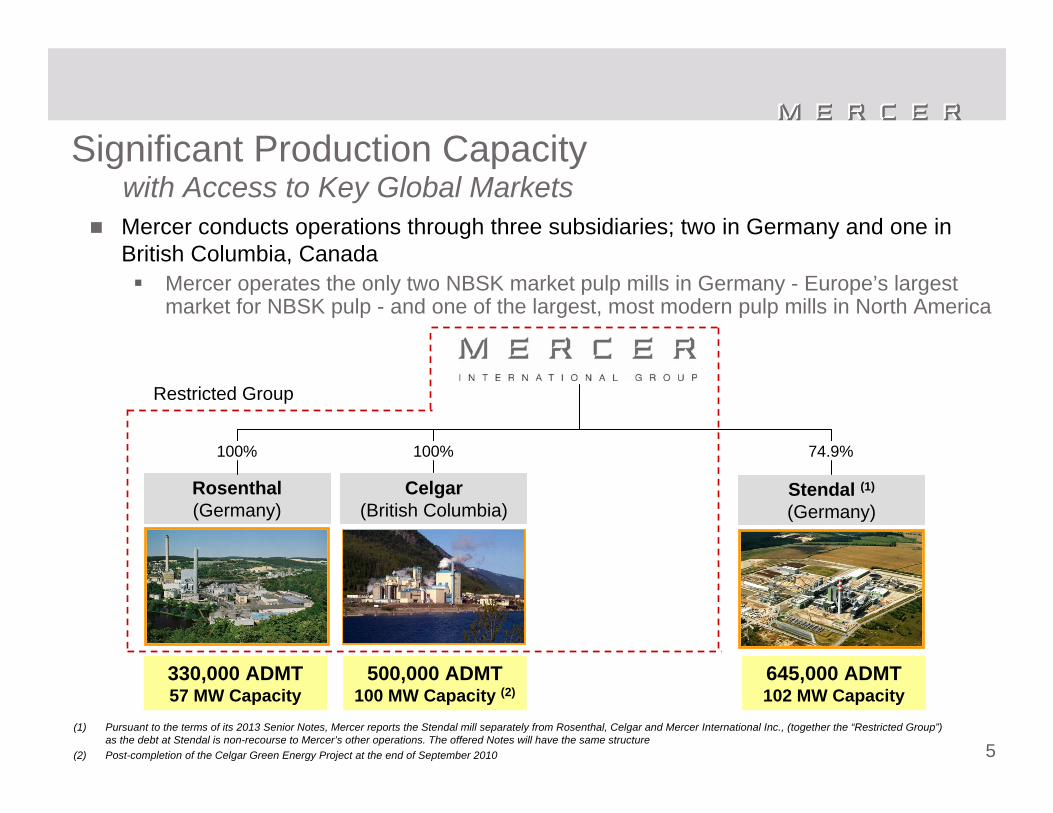

Mercer conducts operations through three subsidiaries; two in Germany and one in British Columbia, Canada

Mercer operates the only two NBSK market pulp mills in Germany - Europe’s largest market for NBSK pulp - and one of the largest, most modern pulp mills in North America

Significant Production Capacitywith Access to Key Global Markets

Rosenthal(Germany)

Celgar(British Columbia)

Stendal (1)

(Germany)

74.9%

Restricted Group

100% 100%

(1) Pursuant to the terms of its 2013 Senior Notes, Mercer reports the Stendal mill separately from Rosenthal, Celgar and Mercer International Inc., (together the “Restricted Group”) as the debt at Stendal is non-recourse to Mercer’s other operations. The offered Notes will have the same structure

(2) Post-completion of the Celgar Green Energy Project at the end of September 2010

500,000 ADMT100 MW Capacity (2)

330,000 ADMT57 MW Capacity

645,000 ADMT102 MW Capacity

6

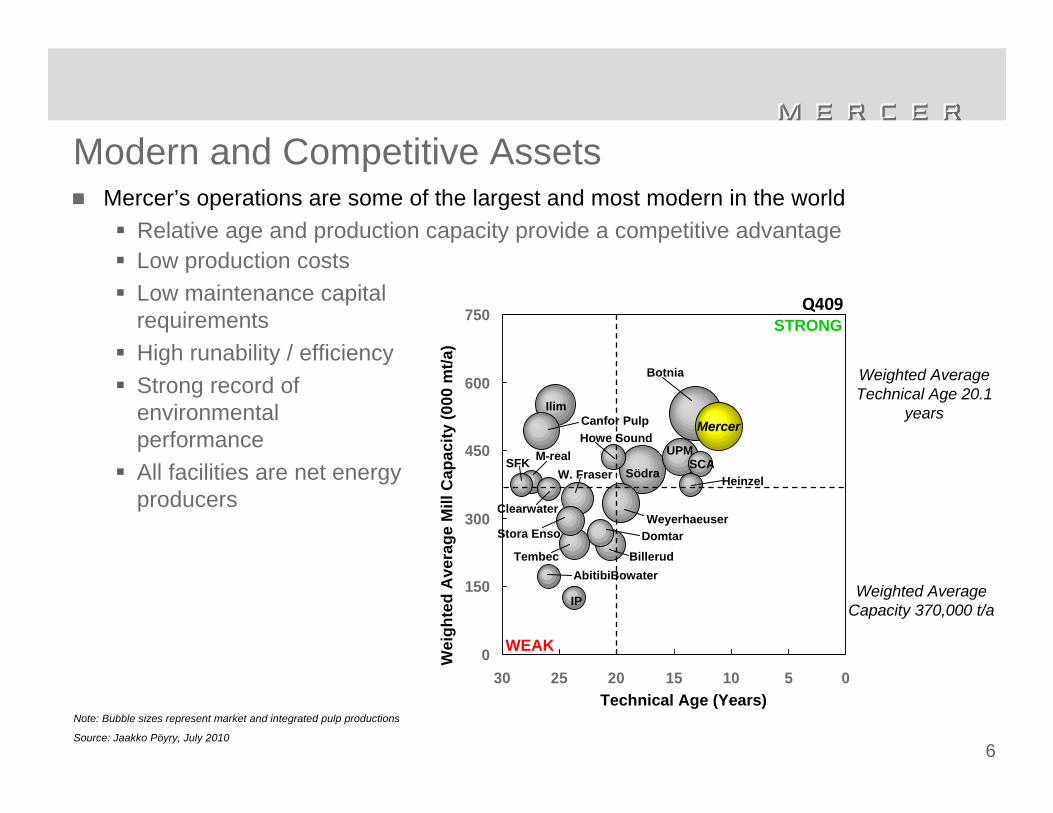

Modern and Competitive AssetsMercer’s operations are some of the largest and most modern in the world

Relative age and production capacity provide a competitive advantage

Note: Bubble sizes represent market and integrated pulp productions

Source: Jaakko Pöyry, July 2010

Low production costsLow maintenance capital requirementsHigh runability / efficiencyStrong record of environmental performanceAll facilities are net energy producers

0

150

300

450

600

750

051015202530Technical Age (Years)

Weighted Average Technical Age 20.1

years

Wei

ghte

d A

vera

ge M

ill C

apac

ity (0

00 m

t/a)

Weighted Average Capacity 370,000 t/a

Q409STRONG

Södra

Weyerhaeuser

Tembec

SCAW. Fraser

Ilim

Domtar

MercerMercerCanfor Pulp

Botnia

UPMHowe Sound

Heinzel

Billerud

IP

Stora Enso

Clearwater

AbitibiBowater

SFK M-real

WEAK

7

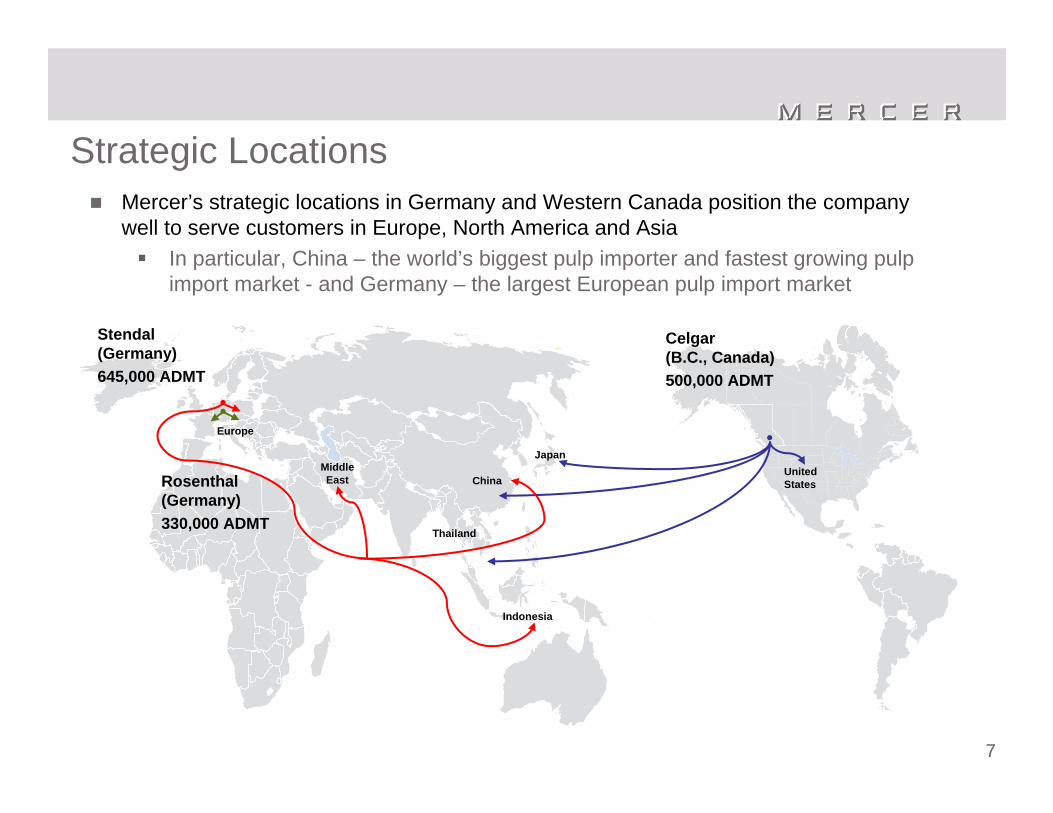

Strategic LocationsMercer’s strategic locations in Germany and Western Canada position the company well to serve customers in Europe, North America and Asia

In particular, China – the world’s biggest pulp importer and fastest growing pulp import market - and Germany – the largest European pulp import market

Celgar(B.C., Canada)500,000 ADMT

●

UnitedStates

Stendal(Germany)645,000 ADMT

Rosenthal(Germany)330,000 ADMT

●●

Indonesia

China

Thailand

MiddleEast

Europe

Japan

8

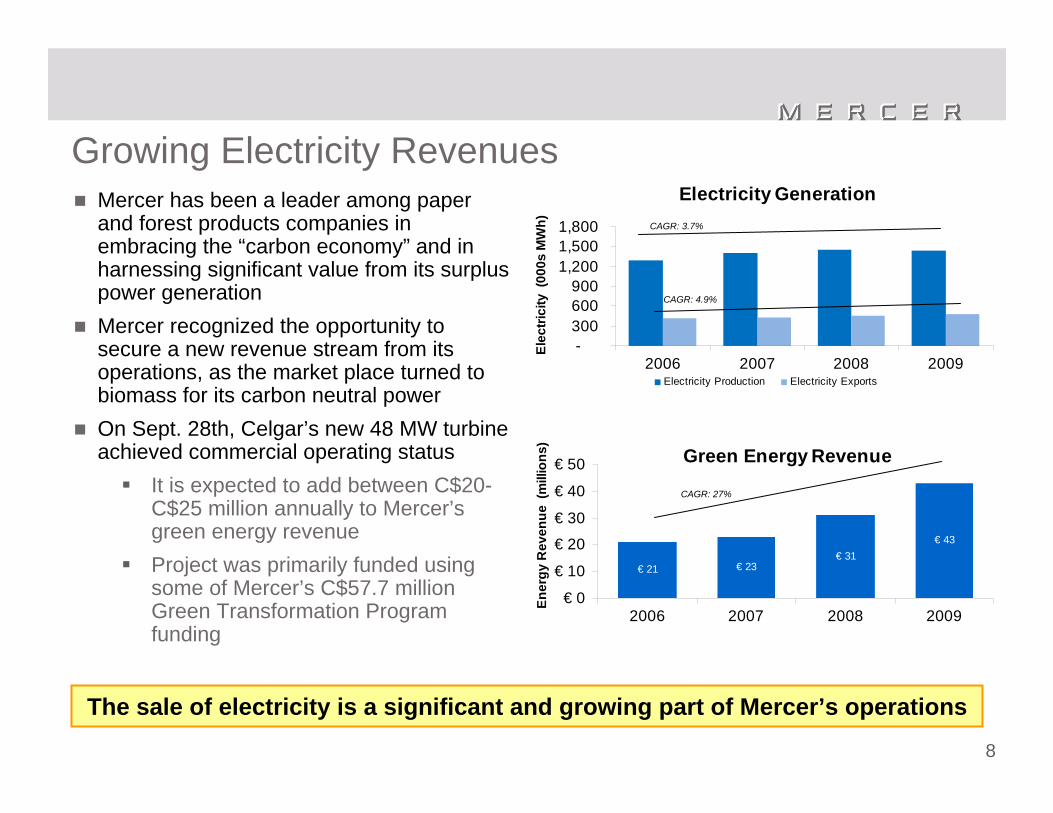

Electricity Generation

-300600900

1,2001,5001,800

2006 2007 2008 2009

Elec

trici

ty (

000s

MW

h)

Electricity Production Electricity Exports

Green Energy Revenue

€ 21 € 23€ 31

€ 43

€ 0

€ 10

€ 20

€ 30

€ 40

€ 50

2006 2007 2008 2009

Ener

gy R

even

ue (

mill

ions

)

Growing Electricity RevenuesMercer has been a leader among paper and forest products companies in embracing the “carbon economy” and in harnessing significant value from its surplus power generationMercer recognized the opportunity to secure a new revenue stream from its operations, as the market place turned to biomass for its carbon neutral powerOn Sept. 28th, Celgar’s new 48 MW turbine achieved commercial operating status

It is expected to add between C$20-C$25 million annually to Mercer’s green energy revenueProject was primarily funded using some of Mercer’s C$57.7 million Green Transformation Program funding

CAGR: 27%

CAGR: 3.7%

CAGR: 4.9%

The sale of electricity is a significant and growing part of Mercer’s operations

9

NBSK Supply/Demand Fundamentals are Positive

Management believes that generally flat supply, overall growing demand and positive exposure to the effects of climate change create an excellent operating

environment for Mercer

Global demand for NBSK remains strong, as global production of tissue and specialty papers grows, emerging markets develop, and standards of living improve

• Chinese production of fine paper and pulp-based tissue are forecast to grow at double-digit rates over the next several years

• NBSK’s strength attributes are needed given the trend by tissue and paper producers towards faster production rates, increased recycled content, and lower basis weights

Global supply of softwood pulp is expected to remain relatively flat • New mills are overwhelmingly hardwood pulp and management believes any increases in

softwood supply should be more than offset by capacity closuresMercer benefits from favourable green energy rates and related government incentives

• Climate change is making the cost curve of pulp and paper steeper, significantly disadvantaging inefficient and environmentally unsound operations and benefitting world class operations, such as Mercer’s

10

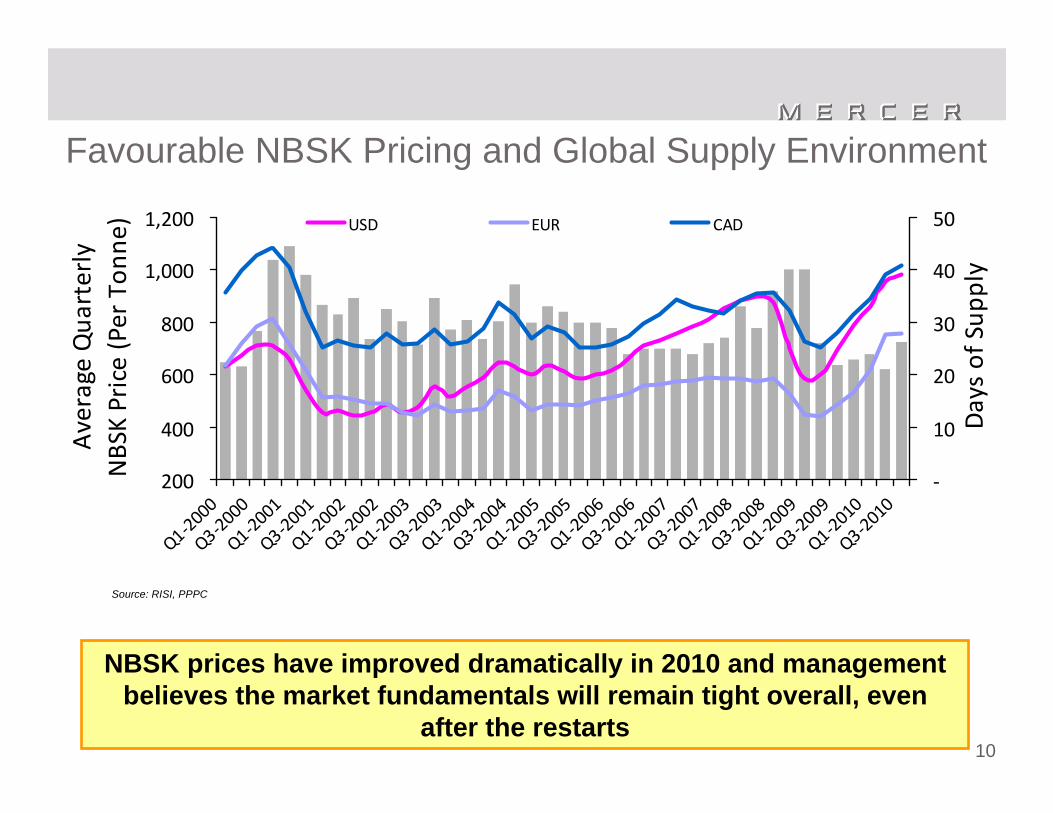

Favourable NBSK Pricing and Global Supply Environment

NBSK prices have improved dramatically in 2010 and management believes the market fundamentals will remain tight overall, even

after the restarts

Source: RISI, PPPC

200

400

600

800

1,000

1,200

Q1‐2000

Q3‐2000

Q1‐2001

Q3‐2001

Q1‐2002

Q3‐2002

Q1‐2003

Q3‐2003

Q1‐2004

Q3‐2004

Q1‐2005

Q3‐2005

Q1‐2006

Q3‐2006

Q1‐2007

Q3‐2007

Q1‐2008

Q3‐2008

Q1‐2009

Q3‐2009

Q1‐2010

Q3‐2010

Average Qua

rterly

NBSK Price (Per Ton

ne)

‐

10

20

30

40

50

Days of Sup

ply

USD EUR CAD

11

Overview of Operations

12

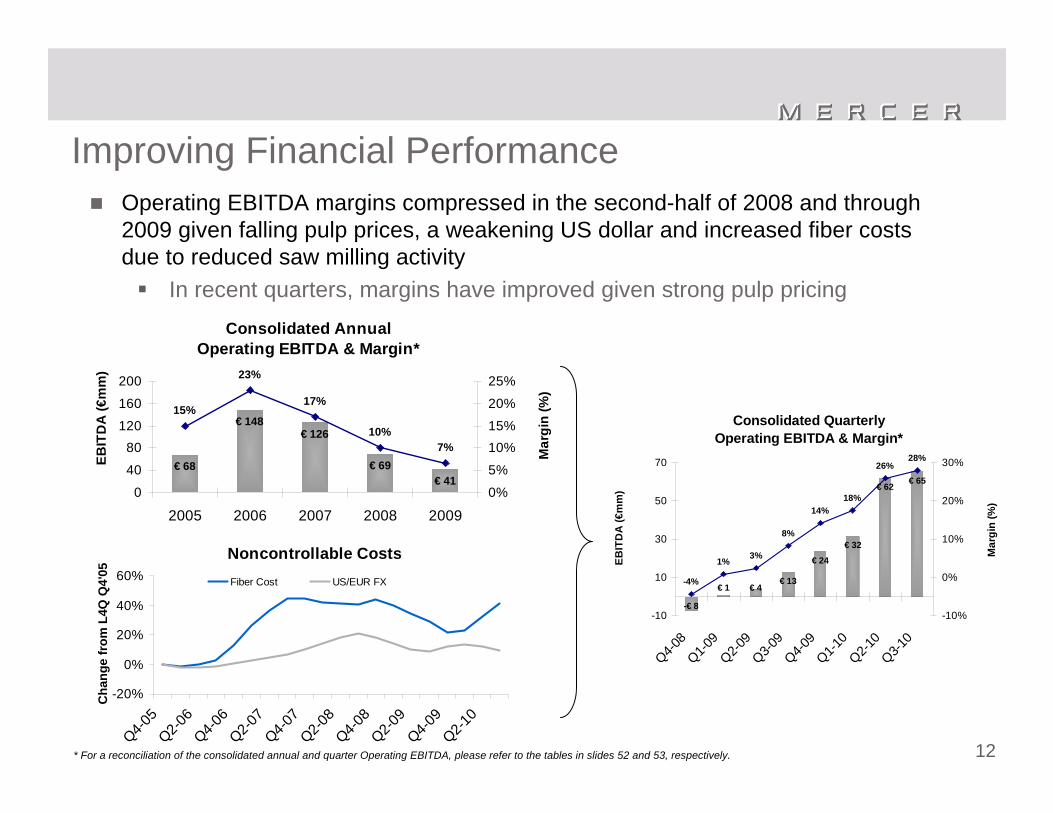

Operating EBITDA margins compressed in the second-half of 2008 and through 2009 given falling pulp prices, a weakening US dollar and increased fiber costs due to reduced saw milling activity

In recent quarters, margins have improved given strong pulp pricing

Improving Financial Performance

Consolidated Quarterly Operating EBITDA & Margin*

-€ 8

€ 1 € 4€ 13

€ 24

€ 32

€ 62 € 65

-4%

1% 3%

8%

14%18%

26%28%

-10

10

30

50

70

Q4-08

Q1-09

Q2-09

Q3-09

Q4-09

Q1-10

Q2-10

Q3-10

EBIT

DA

(€m

m)

-10%

0%

10%

20%

30%

Mar

gin

(%)

Consolidated Annual Operating EBITDA & Margin*

€ 68

€ 148€ 126

€ 69€ 41

15%

23%

17%

10%7%

0

40

80120

160

200

2005 2006 2007 2008 2009

EBIT

DA

(€m

m)

0%

5%

10%15%

20%

25%

Mar

gin

(%)

Noncontrollable Costs

-20%

0%

20%

40%

60%

Q4-05

Q2-06

Q4-06

Q2-07

Q4-07

Q2-08

Q4-08

Q2-09

Q4-09

Q2-10

Cha

nge

from

L4Q

Q4'

05

Fiber Cost US/EUR FX

* For a reconciliation of the consolidated annual and quarter Operating EBITDA, please refer to the tables in slides 52 and 53, respectively.

13

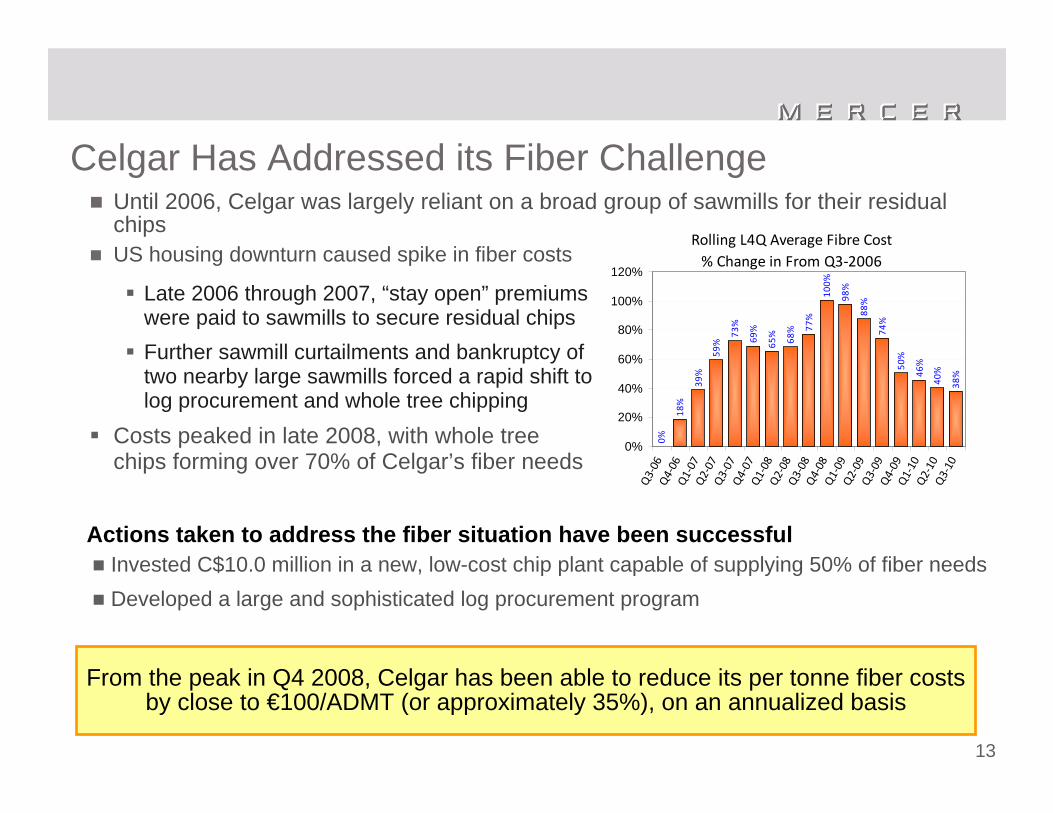

Until 2006, Celgar was largely reliant on a broad group of sawmills for their residual chips US housing downturn caused spike in fiber costs

From the peak in Q4 2008, Celgar has been able to reduce its per tonne fiber costs by close to €100/ADMT (or approximately 35%), on an annualized basis

Celgar Has Addressed its Fiber Challenge

Actions taken to address the fiber situation have been successfulInvested C$10.0 million in a new, low-cost chip plant capable of supplying 50% of fiber needs Developed a large and sophisticated log procurement program

Late 2006 through 2007, “stay open” premiums were paid to sawmills to secure residual chips Further sawmill curtailments and bankruptcy of two nearby large sawmills forced a rapid shift to log procurement and whole tree chipping

Costs peaked in late 2008, with whole tree chips forming over 70% of Celgar’s fiber needs

Rolling L4Q Average Fibre Cost % Change in From Q3‐2006

0%

18%

39%

59%

73%

69%

65%

68% 77

%

100%

98%

88%

74%

50%

46%

40%

38%

0%

20%

40%

60%

80%

100%

120%

Q3‐06

Q4‐06

Q1‐07

Q2‐07

Q3‐07

Q4‐07

Q1‐08

Q2‐08

Q3‐08

Q4‐08

Q1‐09

Q2‐09

Q3‐09

Q4‐09

Q1‐10

Q2‐10

Q3‐10

14

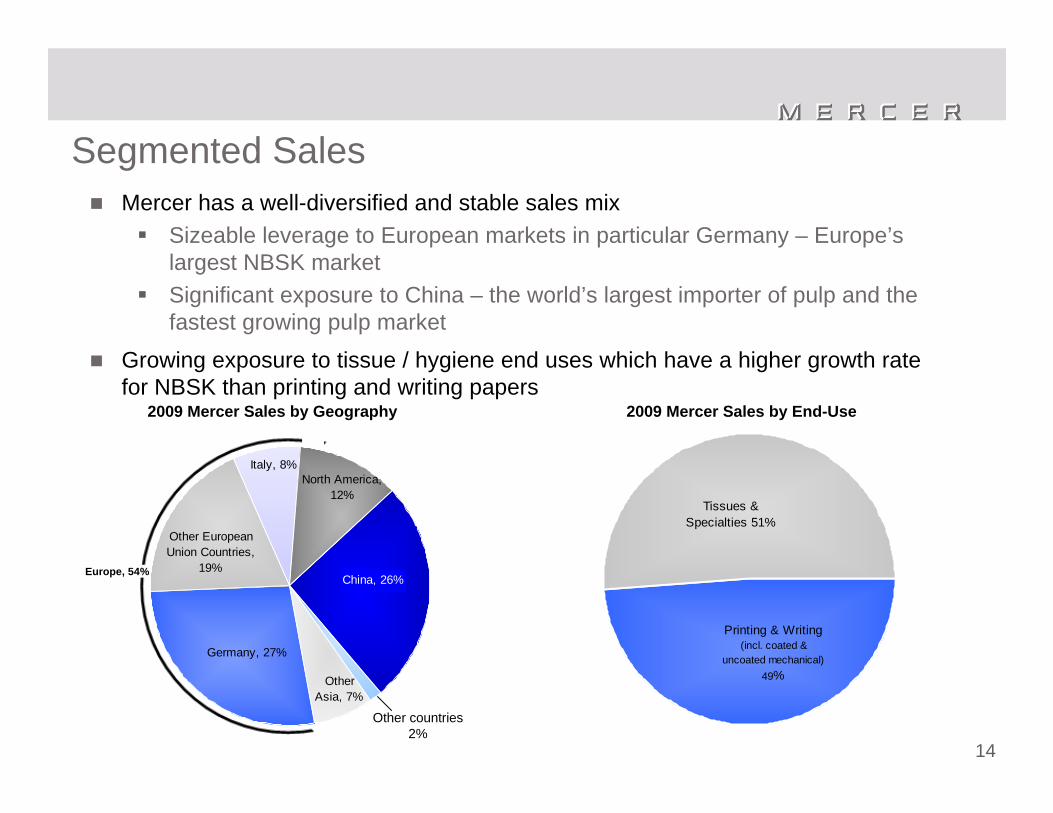

Mercer has a well-diversified and stable sales mixSizeable leverage to European markets in particular Germany – Europe’s largest NBSK marketSignificant exposure to China – the world’s largest importer of pulp and the fastest growing pulp market

Growing exposure to tissue / hygiene end uses which have a higher growth rate for NBSK than printing and writing papers

Segmented Sales

2009 Mercer Sales by End-Use2009 Mercer Sales by Geography

Other countries2%

Printing & Writing(incl. coated &

uncoated mechanical) 49%

Tissues & Specialties 51%

Europe, 54%

Germany, 27%

Other European Union Countries,

19%

Italy, 8%North America,

12%

China, 26%

Other Asia, 7%

15

Financial Review

16

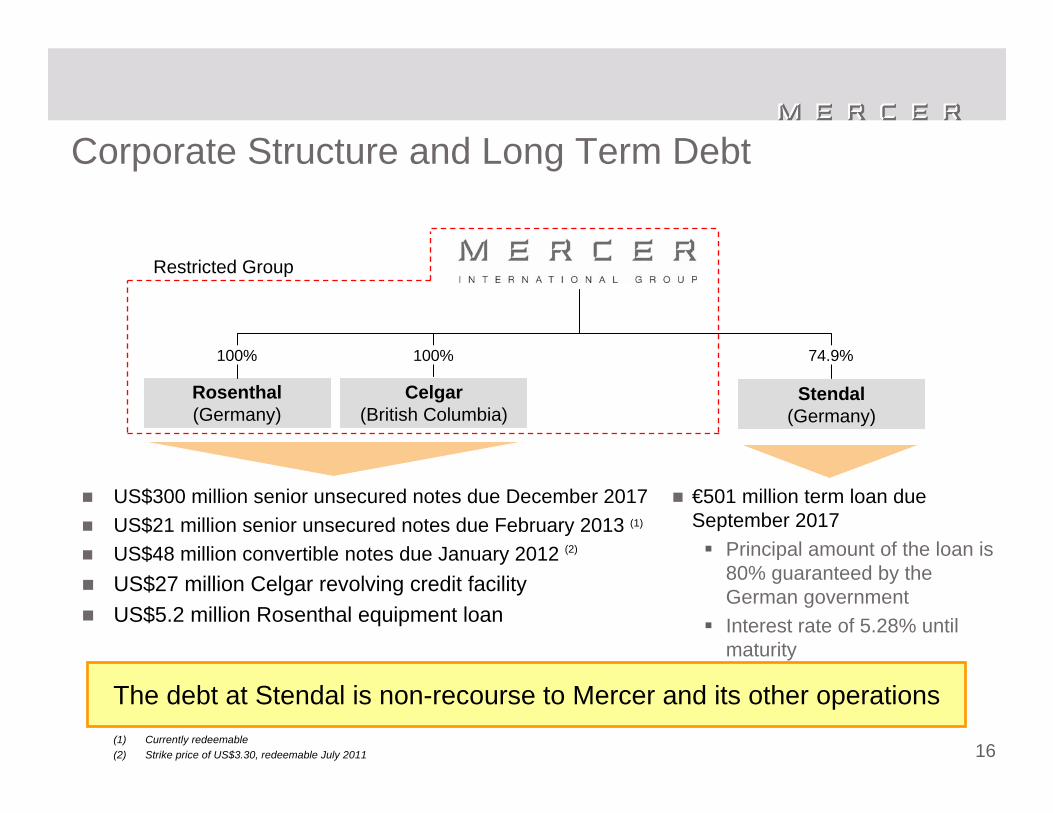

Corporate Structure and Long Term Debt

Rosenthal(Germany)

Celgar(British Columbia)

Stendal(Germany)

74.9%

US$300 million senior unsecured notes due December 2017US$21 million senior unsecured notes due February 2013 (1)

US$48 million convertible notes due January 2012 (2)

US$27 million Celgar revolving credit facilityUS$5.2 million Rosenthal equipment loan

€501 million term loan due September 2017

Principal amount of the loan is 80% guaranteed by the German governmentInterest rate of 5.28% until maturity

Restricted Group

100% 100%

The debt at Stendal is non-recourse to Mercer and its other operations (1) Currently redeemable(2) Strike price of US$3.30, redeemable July 2011

17

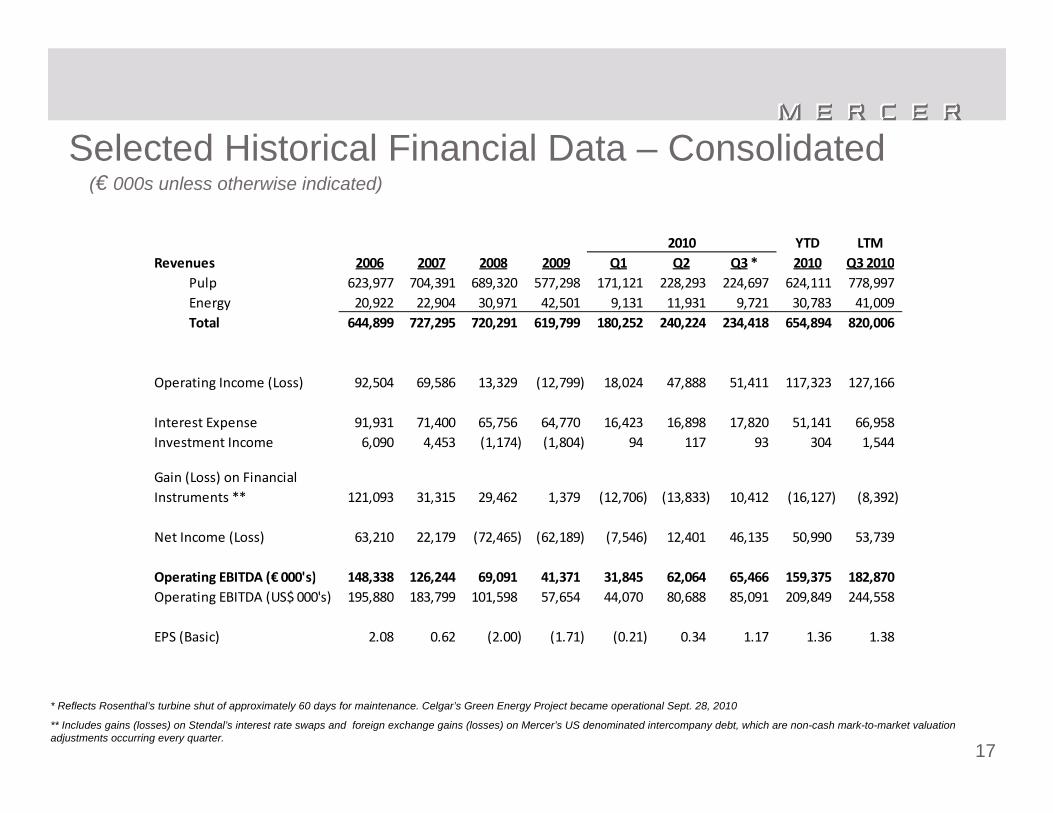

Selected Historical Financial Data – Consolidated(€ 000s unless otherwise indicated)

* Reflects Rosenthal’s turbine shut of approximately 60 days for maintenance. Celgar’s Green Energy Project became operational Sept. 28, 2010

** Includes gains (losses) on Stendal’s interest rate swaps and foreign exchange gains (losses) on Mercer’s US denominated intercompany debt, which are non-cash mark-to-market valuation adjustments occurring every quarter.

YTD LTMRevenues 2006 2007 2008 2009 Q1 Q2 Q3* 2010 Q3 2010

Pulp 623,977 704,391 689,320 577,298 171,121 228,293 224,697 624,111 778,997 Energy 20,922 22,904 30,971 42,501 9,131 11,931 9,721 30,783 41,009 Total 644,899 727,295 720,291 619,799 180,252 240,224 234,418 654,894 820,006

Operating Income (Loss) 92,504 69,586 13,329 (12,799) 18,024 47,888 51,411 117,323 127,166

Interest Expense 91,931 71,400 65,756 64,770 16,423 16,898 17,820 51,141 66,958 Investment Income 6,090 4,453 (1,174) (1,804) 94 117 93 304 1,544

121,093 31,315 29,462 1,379 (12,706) (13,833) 10,412 (16,127) (8,392)

Net Income (Loss) 63,210 22,179 (72,465) (62,189) (7,546) 12,401 46,135 50,990 53,739

Operating EBITDA (€ 000's)*** 148,338 126,244 69,091 41,371 31,845 62,064 65,466 159,375 182,870 Operating EBITDA (US$ 000's) 195,880 183,799 101,598 57,654 44,070 80,688 85,091 209,849 244,558

EPS (Basic) 2.08 0.62 (2.00) (1.71) (0.21) 0.34 1.17 1.36 1.38

Gain (Loss) on Financial Instruments **

2010

18

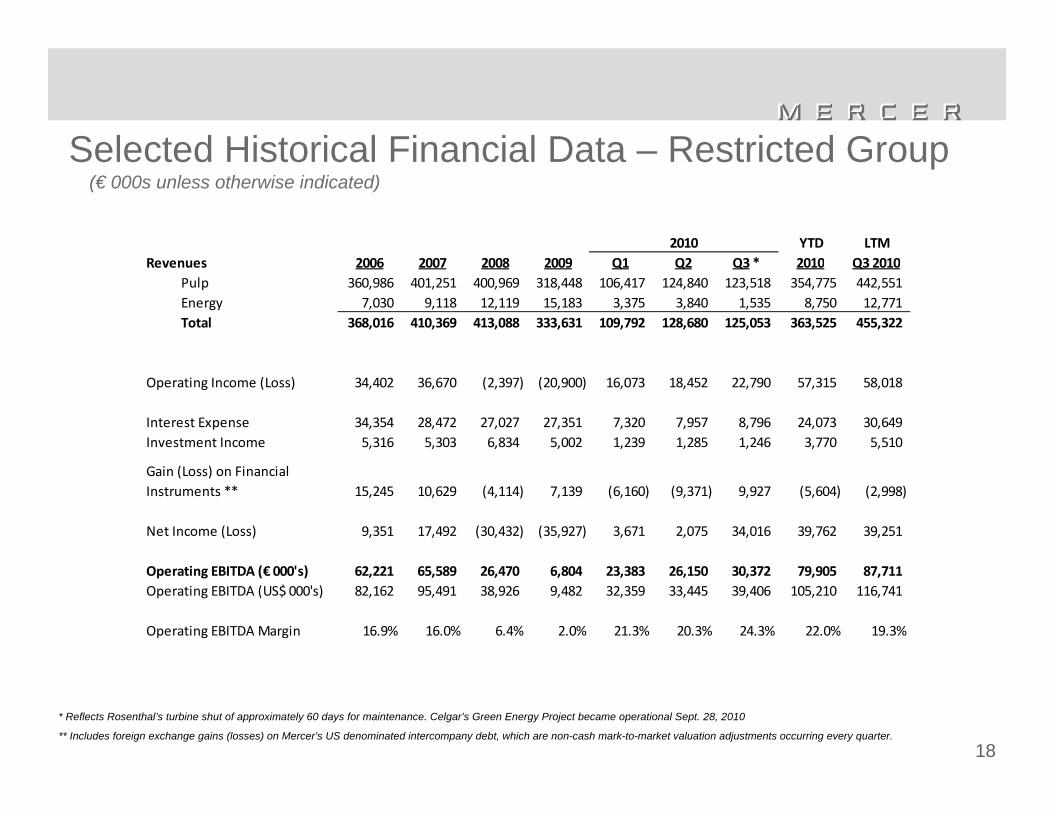

YTD LTMRevenues 2006 2007 2008 2009 Q1 Q2 Q3* 2010 Q3 2010

Pulp 360,986 401,251 400,969 318,448 106,417 124,840 123,518 354,775 442,551 Energy 7,030 9,118 12,119 15,183 3,375 3,840 1,535 8,750 12,771 Total 368,016 410,369 413,088 333,631 109,792 128,680 125,053 363,525 455,322

Operating Income (Loss) 34,402 36,670 (2,397) (20,900) 16,073 18,452 22,790 57,315 58,018

Interest Expense 34,354 28,472 27,027 27,351 7,320 7,957 8,796 24,073 30,649 Investment Income 5,316 5,303 6,834 5,002 1,239 1,285 1,246 3,770 5,510

15,245 10,629 (4,114) 7,139 (6,160) (9,371) 9,927 (5,604) (2,998)

Net Income (Loss) 9,351 17,492 (30,432) (35,927) 3,671 2,075 34,016 39,762 39,251

Operating EBITDA (€ 000's) *** 62,221 65,589 26,470 6,804 23,383 26,150 30,372 79,905 87,711 Operating EBITDA (US$ 000's) 82,162 95,491 38,926 9,482 32,359 33,445 39,406 105,210 116,741

Operating EBITDA Margin 16.9% 16.0% 6.4% 2.0% 21.3% 20.3% 24.3% 22.0% 19.3%

Gain (Loss) on Financial Instruments **

2010

Selected Historical Financial Data – Restricted Group(€ 000s unless otherwise indicated)

* Reflects Rosenthal’s turbine shut of approximately 60 days for maintenance. Celgar’s Green Energy Project became operational Sept. 28, 2010

** Includes foreign exchange gains (losses) on Mercer’s US denominated intercompany debt, which are non-cash mark-to-market valuation adjustments occurring every quarter.

19

Balance SheetAs at September 30, 2010 (in €000s) Restricted

Group

Unrestricted Subsidiaries (Stendal) Eliminations

Consolidated Group

ASSETSCash and cash equivalents 48,411 36,715 85,126 Receivables 51,792 50,128 101,920 Note Receivable, current portion 1,609 ‐ 1,609 Inventories 68,257 44,128 112,385 Prepaid expenses and other 4,870 5,507 10,377

174,939 136,478 ‐ 311,417

Property, plant and equipment 363,758 487,978 851,736 Other 2,608 4,333 6,941 Deferred income tax 12,990 ‐ 12,990 Due from unrestricted group 78,177 (78,177) ‐ Note Receivable, long‐term portion 1,723 ‐ 1,723

TOTAL ASSETS 634,195 628,789 (78,177) 1,184,807

LIABILITIESAccounts payable and accrued exp. 64,669 43,461 108,130 Pension (current portion) 608 ‐ 608 Debt, current portion 2,761 23,167 25,928

68,038 66,628 ‐ 134,666

Debt, less current portion 282,335 477,490 759,825 Loan, minority shareholders ‐ 30,925 30,925 Due to restricted group ‐ 78,177 (78,177) ‐ Unrealized derivative loss ‐ 63,396 63,396 Pension (long term) 19,581 ‐ 19,581 Capital leases and other 6,616 3,942 10,558 Deferred tax payable ‐ ‐ ‐

TOTAL LIABILITIES 376,570 720,558 (78,177) 1,018,951

TOTAL EQUITY (DEFICIT) 257,625 (91,769) 165,856 TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY 634,195 628,789 (78,177) 1,184,807

20

Capital Structure“Restricted Group” structure was used to protect Mercer from the high leverage of the Stendal project

The Restricted Group - created at the time of issuing US$310 million Notes - is supported by the Celgar and Rosenthal operations (recently replaced by a US$300 million issue due December 2017)

Together, the mills provide approximately 830,000 tonnes of pulp production capacity Now that Celgar’s Green Energy Project is online, the Restricted Group is expected to generate approximately US$40 million in annual electricity revenues

Since energy production is a by-product of our pulp production, there are minimal incremental costs and our energy sales are highly profitable

Mercer’s operations have benefitted from the heavy involvement of governments in the form of non-repayable grants for the construction of its mills in Germany

Mercer has received €410 million in government grants for the construction of the Rosenthal, Stendal, and Celgar Green Energy Project

These grants reduce the cost basis of the assets purchased and are not reported in our incomeThe Stendal debt of €501 million is guaranteed to 80% by the German government and isnon-recourse to the rest of Mercer

Stendal’s debt is amortizing and has a sinking fund account to support debt amortization and interest payments during weaker periods

Stendal’s balance sheet is complicated by its deeply subordinated shareholder loans and a quarterly mark-to-market, non-cash valuation adjustment relating to its fixed interest rate swaps

21

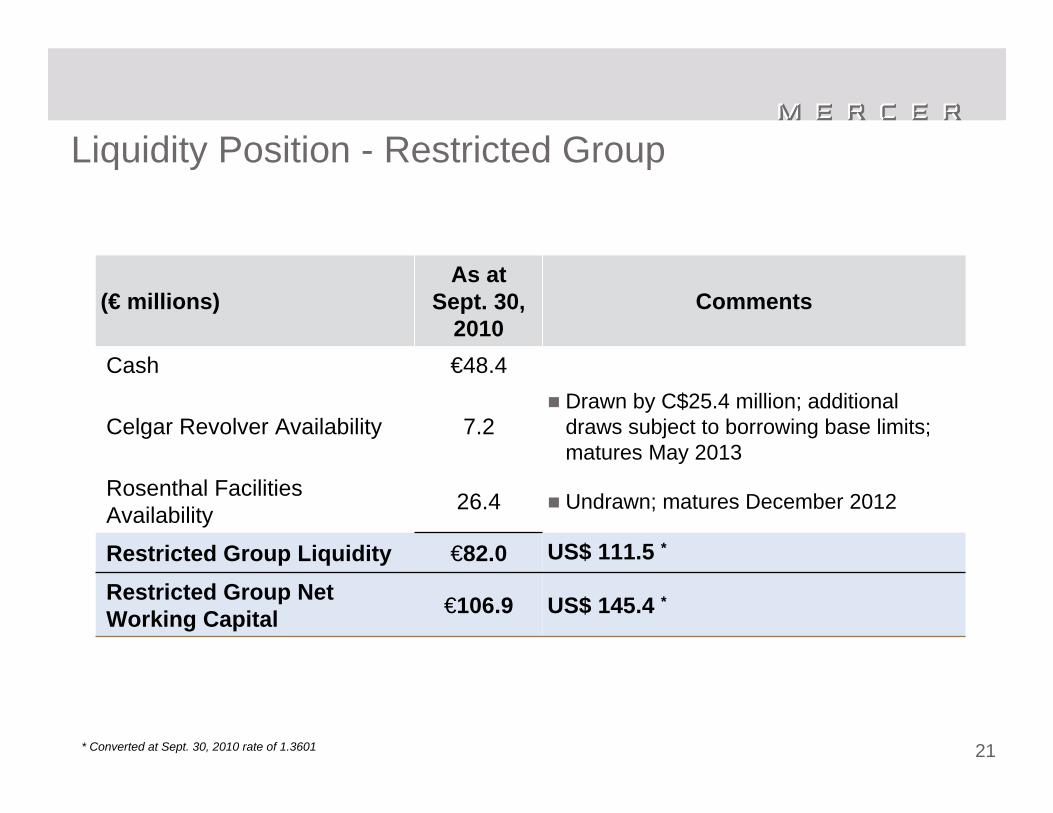

Liquidity Position - Restricted Group

US$ 111.5 *€82.0Restricted Group Liquidity

US$ 145.4 *€106.9Restricted Group Net Working Capital

(€ millions)As at

Sept. 30, 2010

Comments

Cash €48.4

Celgar Revolver Availability 7.2Drawn by C$25.4 million; additional draws subject to borrowing base limits; matures May 2013

Rosenthal Facilities Availability 26.4 Undrawn; matures December 2012

* Converted at Sept. 30, 2010 rate of 1.3601

22

Investment Highlights

23

It’s Been a Transitional Year for MercerThe financial crisis of 2009 has resulted in the closure of a significant volume of NBSK capacity

Celgar’s new wood room has reduced its fiber cost by close to €100 / Admtfrom the peak in Q4 2008

Celgar’s new turbine was commissioned in September 2010 and will add another C$20-25 million to the company’s existing electricity revenue base of €43 million

Mercer has extended the maturity of its convertible debentures to 2012 and its senior notes to 2017

24

Key Investment HighlightsOperates world-class, large, modern mills that produce high-quality NBSK pulp which is a premium grade of kraft pulp

Strategically located mills, with excellent fiber baskets, in close proximity to key global markets

Strong, long-term forecast supply/demand outlook for NBSK

Significant and growing revenue from sale of excess renewable, carbon-neutral electricity

Financial structure offers very high leverage to the pulp cycle

Experienced, shareholder-focused management team and board of directors

Improved liquidity performance

25

Appendix

26

Current Industry Environment

27

NBSK is Needed for StrengthManagement believes demand for NBSK will remain strong over the long term

Reinforcing properties needed by modern production technology make NBSK an essential component in a wide range of paper, tissue and hygiene products

Producers have generally substituted as much lower cost hardwood and recycled pulp into their products as possible, so any demand growth in their products should translate directly into demand growth for NBSK

Demand for most paper grades in which NBSK is used, such as tissue, is forecasted to continue growing

Improving global standards of living in countries such as China, aging populations, and growing interest in health and cleanliness are increasing demand for tissue and hygiene products

For example, in China, tissue consumption increased by approximately 2.5 million tonnesbetween 2000 and 20091, and production volumes of fine paper and pulp based tissue areforecasted to grow at respective average annual rates of 13% and 10% from 2009 to 2013 2

Supply of NBSK is forecasted to remain flat or decreaseThe vast majority of the new pulp capacity that is coming online is hardwoodThere have been significant permanent softwood closures in recent years and global pulp inventories remain at near record lows

The long term supply / demand fundamentals for NBSK pulp currently remain strong

1 Tissue PPI Annual Review, Income - McKinsey Institute, TerraChoice MSI; 2 Hawkins Wright – Defining the China Market (October 2009)

28

Annual World Tissue Output(millions of tonnes)

10

14

18

22

26

30

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

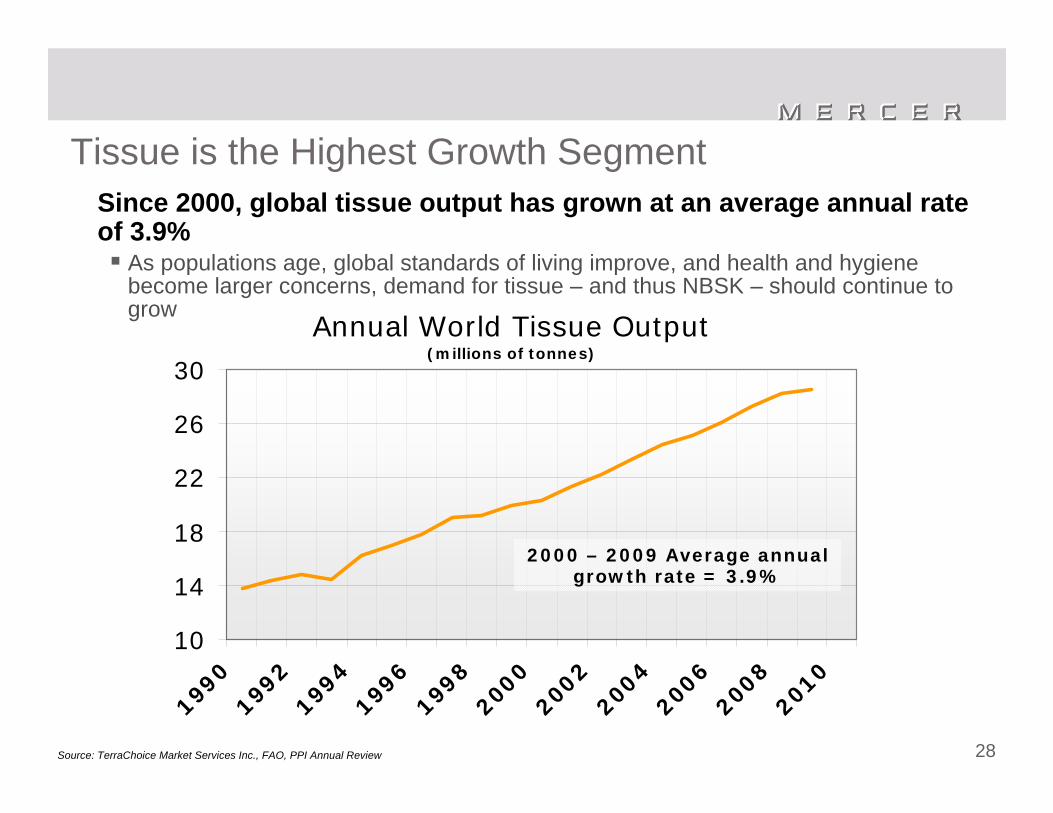

Tissue is the Highest Growth SegmentSince 2000, global tissue output has grown at an average annual rate of 3.9%

As populations age, global standards of living improve, and health and hygiene become larger concerns, demand for tissue – and thus NBSK – should continue to grow

Source: TerraChoice Market Services Inc., FAO, PPI Annual Review

2000 – 2009 Average annual growth rate = 3.9%

29

0.6

2.6

4.6

6.6

8.6

10.6

12.6

14.6

19901994

19982002

20062010

20142018

2022

mill

ions

of to

nnes

0%

20%

40%

60%

80%

100%

% o

f popula

tion n

ot

poor

Consumption

Production

(%) of population

not poor (McKinsey)

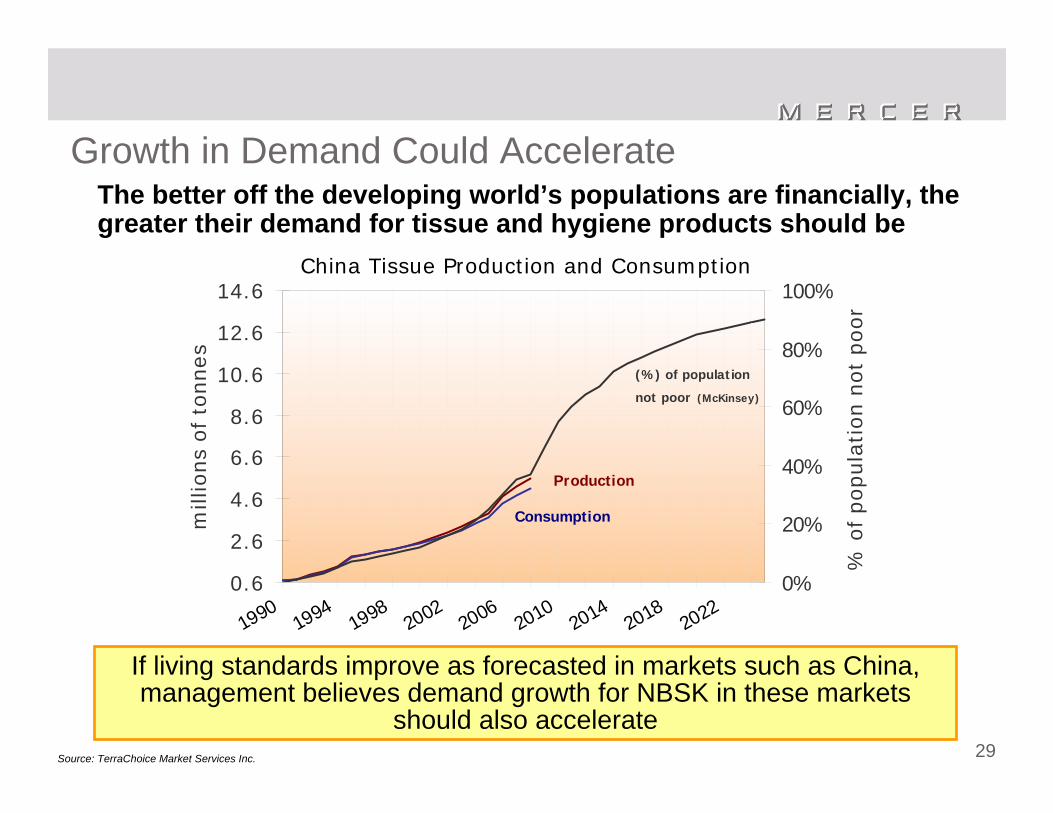

Growth in Demand Could AccelerateThe better off the developing world’s populations are financially, the greater their demand for tissue and hygiene products should be

Source: TerraChoice Market Services Inc.

If living standards improve as forecasted in markets such as China, management believes demand growth for NBSK in these markets

should also accelerate

China Tissue Production and Consumption

30

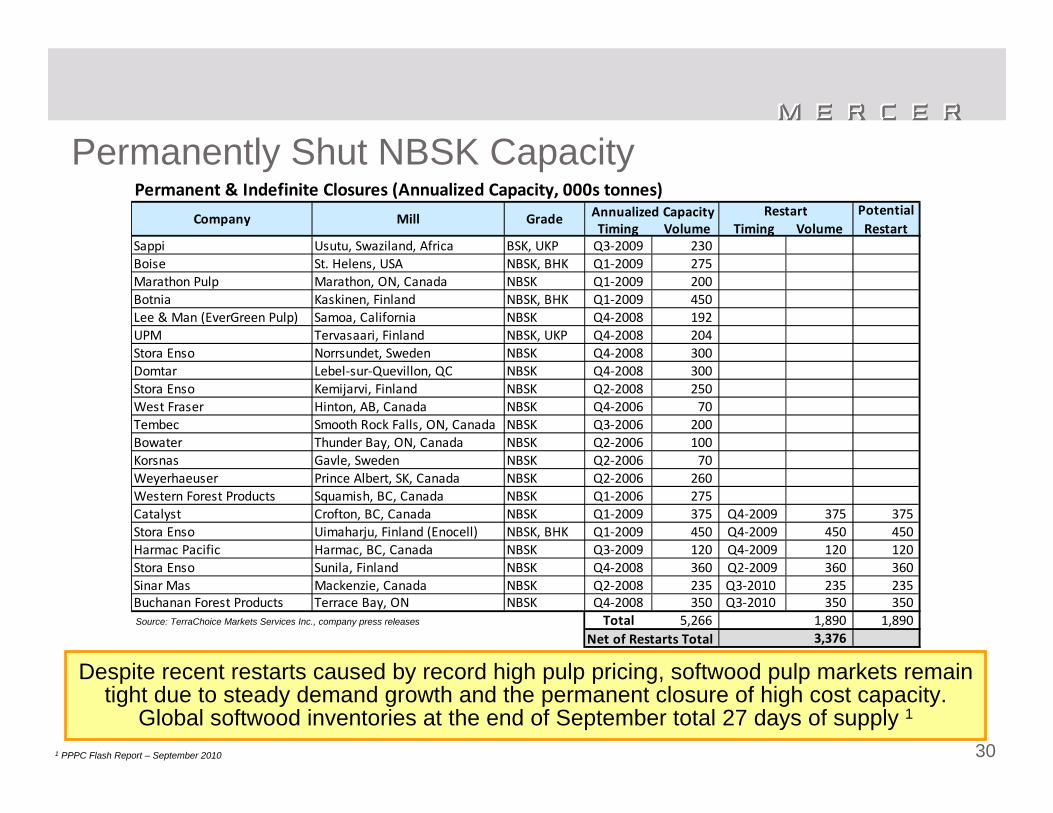

Permanent & Indefinite Closures (Annualized Capacity, 000s tonnes)

Timing Volume Timing VolumeSappi Usutu, Swaziland, Africa BSK, UKP Q3‐2009 230 Boise St. Helens, USA NBSK, BHK Q1‐2009 275 Marathon Pulp Marathon, ON, Canada NBSK Q1‐2009 200 Botnia Kaskinen, Finland NBSK, BHK Q1‐2009 450 Lee & Man (EverGreen Pulp) Samoa, California NBSK Q4‐2008 192 UPM Tervasaari, Finland NBSK, UKP Q4‐2008 204 Stora Enso Norrsundet, Sweden NBSK Q4‐2008 300 Domtar Lebel‐sur‐Quevillon, QC NBSK Q4‐2008 300 Stora Enso Kemijarvi, Finland NBSK Q2‐2008 250 West Fraser Hinton, AB, Canada NBSK Q4‐2006 70 Tembec Smooth Rock Falls, ON, Canada NBSK Q3‐2006 200 Bowater Thunder Bay, ON, Canada NBSK Q2‐2006 100 Korsnas Gavle, Sweden NBSK Q2‐2006 70 Weyerhaeuser Prince Albert, SK, Canada NBSK Q2‐2006 260 Western Forest Products Squamish, BC, Canada NBSK Q1‐2006 275 Catalyst Crofton, BC, Canada NBSK Q1‐2009 375 Q4‐2009 375 375 Stora Enso Uimaharju, Finland (Enocell) NBSK, BHK Q1‐2009 450 Q4‐2009 450 450 Harmac Pacific Harmac, BC, Canada NBSK Q3‐2009 120 Q4‐2009 120 120 Stora Enso Sunila, Finland NBSK Q4‐2008 360 Q2‐2009 360 360 Sinar Mas Mackenzie, Canada NBSK Q2‐2008 235 Q3‐2010 235 235 Buchanan Forest Products Terrace Bay, ON NBSK Q4‐2008 350 Q3‐2010 350 350

Total 5,266 1,890 1,890 Net of Restarts Total 3,376

MillCompanyPotential Restart

Annualized Capacity RestartGrade

1 PPPC Flash Report – September 2010

Permanently Shut NBSK Capacity

Despite recent restarts caused by record high pulp pricing, softwood pulp markets remain tight due to steady demand growth and the permanent closure of high cost capacity.

Global softwood inventories at the end of September total 27 days of supply 1

Source: TerraChoice Markets Services Inc., company press releases

31

10 12 14 16 18 20 22 24 26 28 30 32 34

mill

ions

tonnes

Bleached Softwood Kraft(-0.5% aagr 2008-2014)

Bleached Hardwood Kraft(2.7% aagr 2008-2014)

World Market Pulp Capacity

Global Supply of BSK

Source: TerraChoice Markets Services Inc.

Most of the new pulp capacity that is coming online is hardwood pulp capacity. Total global softwood pulp capacity is expected to remain flat as only one new softwood

mill is being built (Ilim) to replace the old, high cost softwood mills being shut

32

Climate Change Presents Mercer with OpportunitiesClimate change has emerged as a very significant issue and Mercer is well positioned to benefit from the changes that are expected to result

Both Canadian and German governments provide support and incentives for green initiatives and energy production

• Our German operations receive superior energy rates for selling their generation under the green tariff structure of the German Renewable Energy Act (EEG)

• In 2009, Celgar was awarded C$57.7 million under the Canadian government’s Green Transformation Program

• Celgar signed a long term energy purchase agreement with the local utility, delivering 238,000 MWh of bioenergyannually to the grid at higher green rates

• Became operational on Sept. 28th, 2010

Mercer has already garnered significant benefits in the emerging carbon economy and we remain actively engaged with policy makers to maximize these benefits

going forward

Changes we see coming from climate change include:

Full utilization of forestsIncreased silviculture / thinningIncreased cogenerationTechnologies for bioproductsand the markets for these bioproducts will develop

33

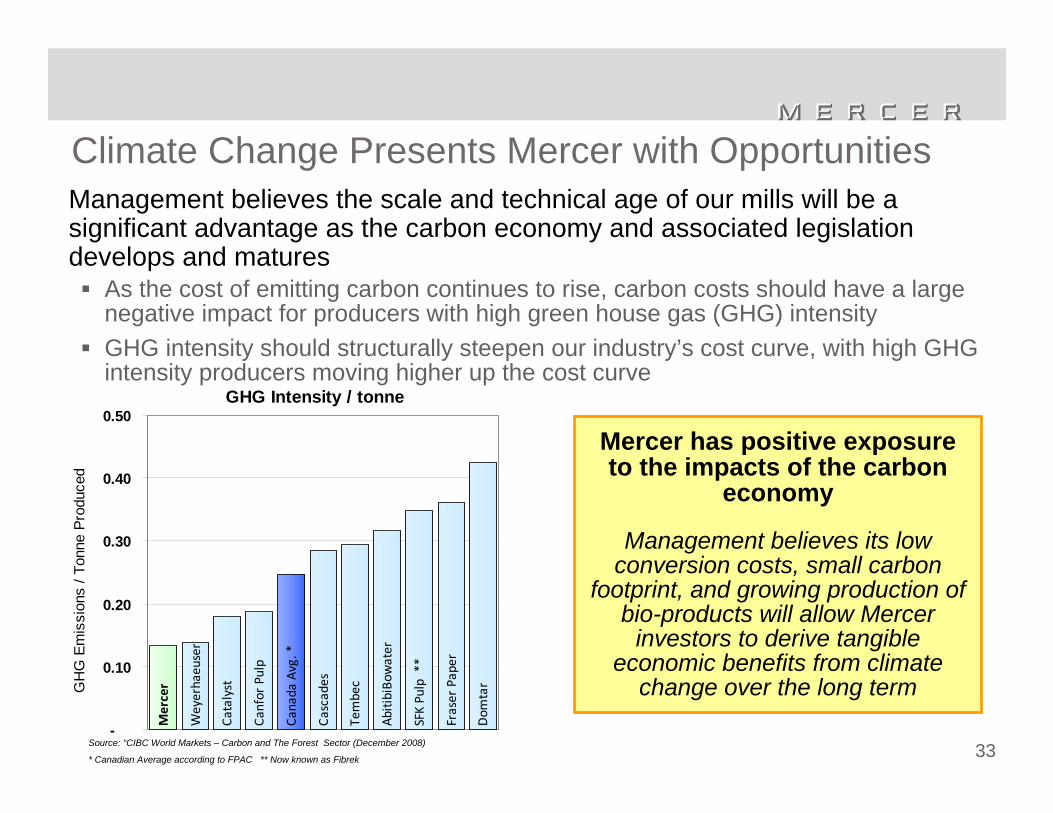

GHG Intensity / tonne

Weyerhaeuser

Catalyst

Canfor Pulp

Cascades

Tembec

SFK Pulp **

Fraser Paper

Dom

tar

Mercer

Canada

Avg. *

AbitibiBo

water

-

0.10

0.20

0.30

0.40

0.50

GH

G E

mis

sion

s / T

onne

Pro

duce

d

Management believes the scale and technical age of our mills will be a significant advantage as the carbon economy and associated legislation develops and matures

As the cost of emitting carbon continues to rise, carbon costs should have a large negative impact for producers with high green house gas (GHG) intensityGHG intensity should structurally steepen our industry’s cost curve, with high GHG intensity producers moving higher up the cost curve

Climate Change Presents Mercer with Opportunities

Source: “CIBC World Markets – Carbon and The Forest Sector (December 2008)

* Canadian Average according to FPAC ** Now known as Fibrek

Mercer has positive exposure to the impacts of the carbon

economy

Management believes its low conversion costs, small carbon

footprint, and growing production of bio-products will allow Mercer

investors to derive tangible economic benefits from climate

change over the long term

34

Operations

35

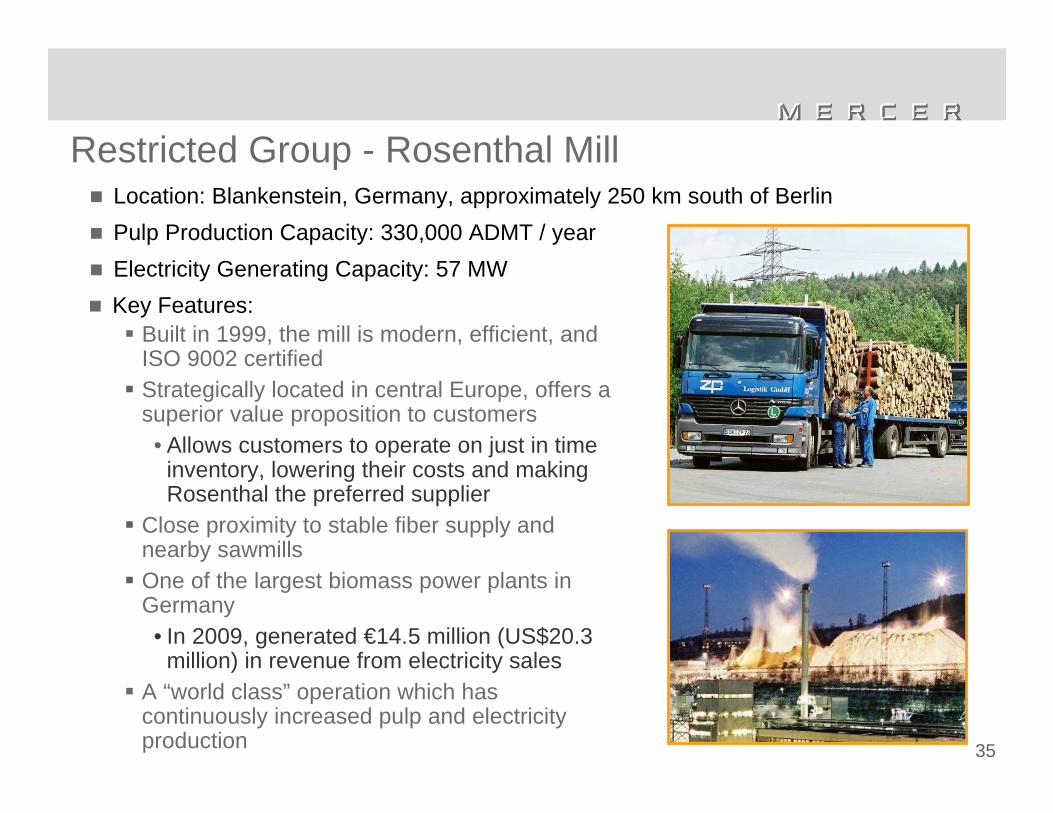

Restricted Group - Rosenthal MillLocation: Blankenstein, Germany, approximately 250 km south of BerlinPulp Production Capacity: 330,000 ADMT / yearElectricity Generating Capacity: 57 MWKey Features:

Built in 1999, the mill is modern, efficient, and ISO 9002 certifiedStrategically located in central Europe, offers a superior value proposition to customers• Allows customers to operate on just in time

inventory, lowering their costs and making Rosenthal the preferred supplier

Close proximity to stable fiber supply and nearby sawmillsOne of the largest biomass power plants in Germany • In 2009, generated €14.5 million (US$20.3

million) in revenue from electricity salesA “world class” operation which has continuously increased pulp and electricity production

36

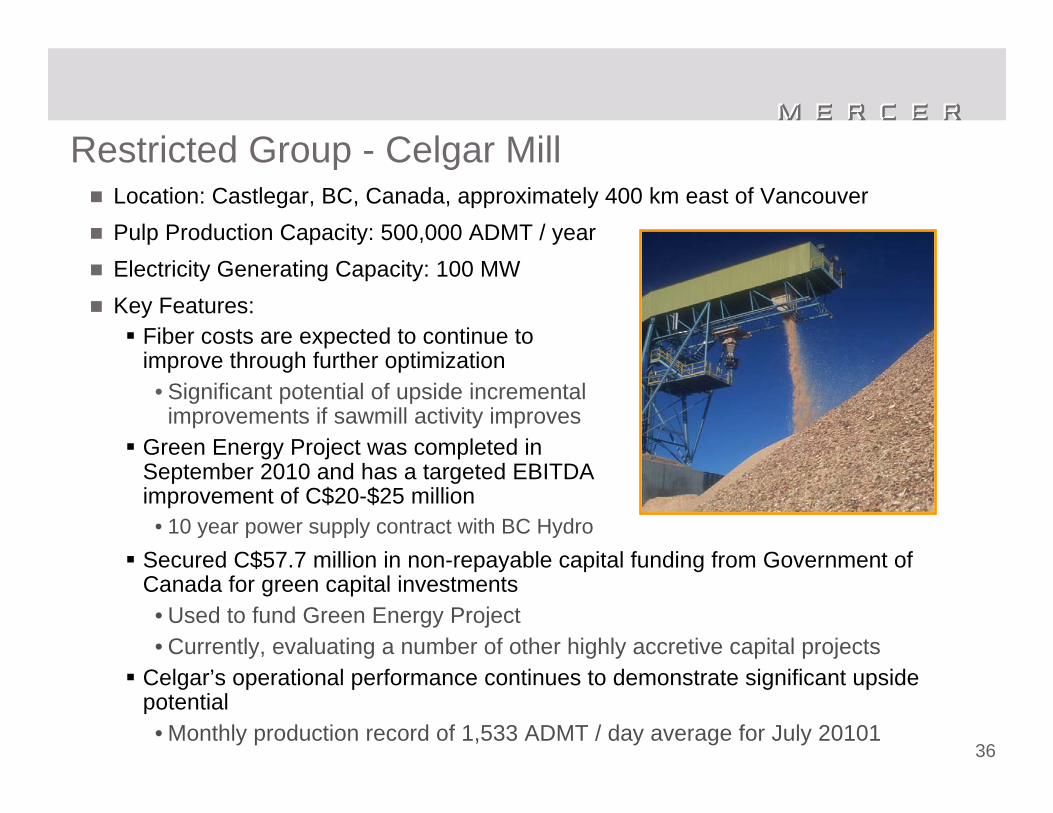

Restricted Group - Celgar MillLocation: Castlegar, BC, Canada, approximately 400 km east of VancouverPulp Production Capacity: 500,000 ADMT / yearElectricity Generating Capacity: 100 MWKey Features:

Fiber costs are expected to continue to improve through further optimization• Significant potential of upside incremental

improvements if sawmill activity improvesGreen Energy Project was completed in September 2010 and has a targeted EBITDA improvement of C$20-$25 million

• 10 year power supply contract with BC HydroSecured C$57.7 million in non-repayable capital funding from Government of Canada for green capital investments• Used to fund Green Energy Project• Currently, evaluating a number of other highly accretive capital projects

Celgar’s operational performance continues to demonstrate significant upside potential• Monthly production record of 1,533 ADMT / day average for July 20101

37

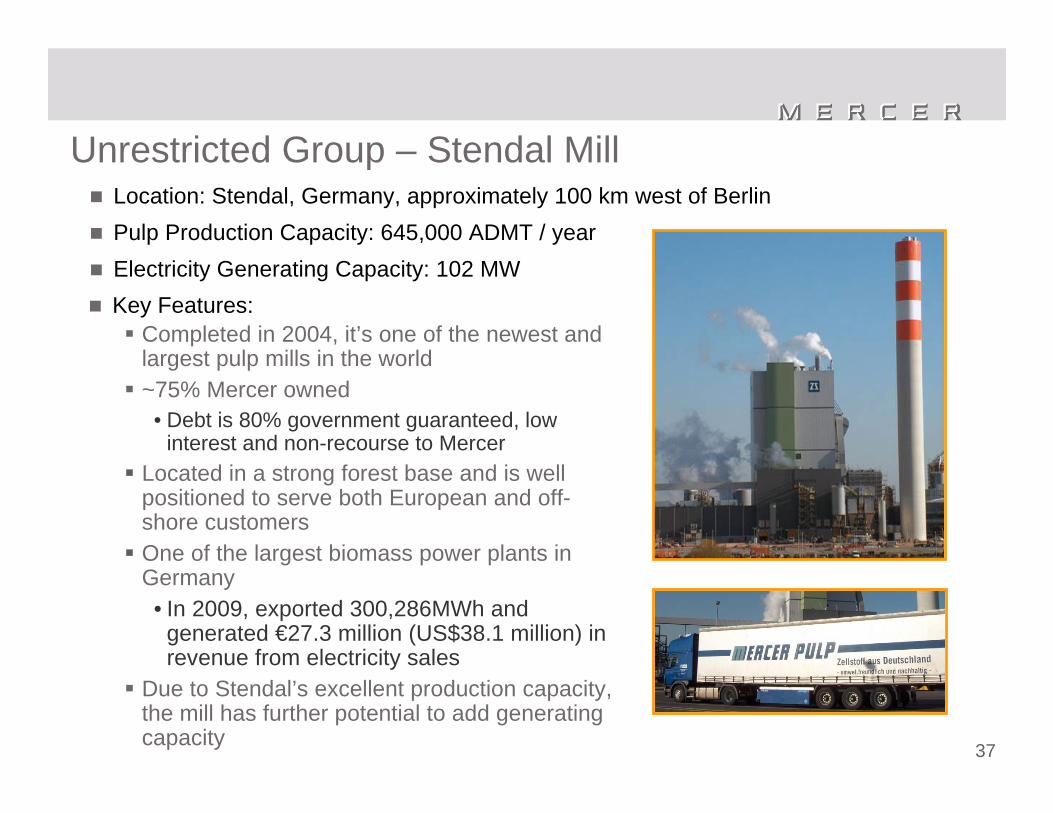

Unrestricted Group – Stendal MillLocation: Stendal, Germany, approximately 100 km west of BerlinPulp Production Capacity: 645,000 ADMT / yearElectricity Generating Capacity: 102 MWKey Features:

Completed in 2004, it’s one of the newest and largest pulp mills in the world~75% Mercer owned

• Debt is 80% government guaranteed, low interest and non-recourse to Mercer

Located in a strong forest base and is well positioned to serve both European and off-shore customersOne of the largest biomass power plants in Germany • In 2009, exported 300,286MWh and

generated €27.3 million (US$38.1 million) in revenue from electricity sales

Due to Stendal’s excellent production capacity, the mill has further potential to add generating capacity