Embed Size (px)

Citation preview

Shea & Company, LLC

Business Intelligence and Analytics Platforms Market Map

F E B R U A R Y 2 0 1 6

Agenda

1

Outlook & Key Themes

Business Intelligence & Analytics Technology Stack and Landscape

Transaction & Acquisition Landscape

Shea & Company Firm Overview

Copyright © 2016 Shea & Company, LLC

Outlook & Key Themes

Key Themes for Business Intelligence & Analytics in 2016

Business intelligence (BI) sector growth

remains strong and consistent

Enterprises are moving away from legacy solutions and towards a growing

crop of disruptive vendors (e.g. Tableau, GoodData) addressing a new set of BI

needs such as mobile, BigData, cloud and social

BI remains a top priority for IT, but rising

business user demands are shifting the BI

landscape

Enterprises are refocusing on growth initiatives and upgrading to more robust

BI solutions

New cloud-based solutions touting ease-of-use will also extend the appeal of

BI solutions to the mid-market, who will play a major role in overall market

growth

Difference in BI firm approaches and

evolution – components vs. platforms

The current market features BI “1.0” and “2.0” vendors fall on a spectrum of

providing components of the BI & analytics stack or platforms with

functionalities that cross the stack layers

There are constraints and opportunities

caused by the reality of multiple BI tools in

the organization

Organizations will use multiple BI solutions to accommodate different needs

Emerging BI players tend to address enterprise departmental needs in the

enterprise and mid-market cases, and incumbent BI vendors have provided

the oversight and control that traditional IT seeks

Investors have made bets at all layers of

the stack that enables BI, with more

immediate opportunity in the middle

Top-of-stack visualization is becoming relatively commoditized functionality

and the bottom-of--stack data infrastructure is well-funded and maturing

Investors will find immediate opportunity at the middle of stack, as much

effort in BI is spent indexing, discovering, integrating and preparing extant

data for analysis

1.

2.

4.

5.

3.

The BI analytics market is quickly moving within the “2.0” phase of its lifecycle which we believe will

usher in a wave of investment and consolidation activity

Legacy BI will respond to the current

market evolution with M&A

Larger legacy players (SAP, Oracle, IBM, etc.) will inevitably look to acquire

more nimble independent vendors in an effort to keep pace with the rapid

evolution of the BI analytics market

6.

Key Themes for 2015-16

2

Copyright © 2016 Shea & Company, LLC

The BI analytics market is anticipated to grow at 6% annually as BI continues to be a top IT spending

priority and as legacy solutions are upgraded

Outlook & Key Themes

Theme #1: Growing Market

Source: Gartner, IDC

Trends Forcing Market Evolution

Rise of Business User

The analytics user in the organization is shifting from IT and analytics

experts to the business users, empowered by more intuitive solutions

and new visualization and analytics tools tailored to them

Growth of the user base within the organization increases 3.5x

Enhanced Access

Data across the organization is being made available to users,

allowing for more complex, cross-functional analyses; analysis is no

longer limited to a siloed data set

Self-Service Functionality

Users now expect the ability to access and analyze enterprise data

without the need for extensive IT intervention

Collaboration

Users expect the ability to share insights across teams within and,

increasingly, outside the organization in the cloud via both desktop

and mobile

Proliferation of Data Sources and Methods

Enterprises are adopting more applications generating exponential

amounts of data; additionally, unstructured data is becoming a key

input into analysis, particularly for marketing and commerce

applications

Technological advancements such as in-memory databases are

enabling real-time, next-generation capabilities such as predictive

analytics and event processing of this diverse data

Vendors are exploring and commercially offering tools for advanced

analytics such as machine learning

Business Intelligence and Analytics Market Size ($ billions)

$13 $14

$15 $16

$17 $18

$19 $20

$-

$5

$10

$15

$20

$25

2012 2013 2014 2015 2016 2017 2018 2019

7% CAGR

Market Share, Top Vendors

6% CAGR

SAP

20.4%

Oracle

13.1%

SAS

11.6%IBM

11.1%

Microsoft

10.0%

Qlik

3.4%

MicroStrategy

2.8%

Tableau

2.7%

FICO

2.6%

Information

Builders

1.3%

Others

21.0%

3

Copyright © 2016 Shea & Company, LLC

Decentralized data discovery deployments

that enable easier and broader use without

the assistance of IT

Investing in enterprise features for

governance, administration, embeddability

and scalability; but still works in progress

Key vendors:

An ideal architecture where both IT and

business users have easy access to each

stack subject to their needs and sufficient

tools to perform various tasks with different

complexity levels

To date, no vendor in the market has been

able to provide such a platform

Legacy BI vendors, emerging BI platforms, as

well as component players are all racing

towards this “Ultimate” BI standard

Still best-suited for enterprises’ standard

system-of-record reporting provisioning

Wants to deliver on rising business user

demands without sacrificing governance

Investing aggressively to support

decentralized, governed data discovery and

OEM/embedded BI use cases, but limited

success to date

Key vendors:

4

Outlook & Key Themes

Theme #2: Rising Business User Demands Shifting the BI Landscape

Traditional IT-Led Full-Stacked BI Platform

Business Intelligence, Analytics

& Visualization

Next-Generation BI Platform

Data (IT-Supplied)

Data Warehouse / Marts

ETLIT

Data

Scientist

Business Intelligence, Analytics

& Visualization

Self-Service Data Prep

(Governed)

Data Warehouse / Marts

ETLIT

Business

User

CR

M

ER

P

SC

M

Un

stru

ctu

red

CR

M

ER

P

SC

M

Un

stru

ctu

red

Emerging Business-Driven Decentralized BI Platform

Business Intelligence, Analytics

& Visualization

Self-Service Data Prep

Business

User

CR

M

ER

P

SC

M

Un

stru

ctu

red

The decentralized BI model is taking market share from traditional centralized BI platforms by

effectively delivering for the rising line-of-business demands in enterprises and SMBs

APIs APIs APIs

Copyright © 2016 Shea & Company, LLC

Outlook & Key Themes

Theme #3: Different Approaches in the Evolution – Platform vs. Components

Emerging Decentralized BI Platforms

Da

ta D

isco

very

an

d A

na

lyti

csD

ata

Infr

ast

ruct

ure

Da

ta A

ssem

bly

an

d P

rep

Traditional Full-Stacked BI PlatformsFragmented Component Vendors

Continue to shift the focus of new product

investment and platform emphasis from IT-

authored production reporting to governed,

business-user-driven data discovery and

analysis tools

Investing aggressively in next-generation,

smart data discovery experience (self-

service data preparation, automated

pattern detection, etc.)

Trying to differentiate through integration

with the rest of their enterprise platforms

to support governed data discovery, but

have had limited adoption to date

Running against time to close gaps with

emerging platform leaders and regain

momentum and differentiation

Large legacy vendors:

Cloud BI continues to grow as data gravity

shifts to the cloud; new challengers:

Recent BI players continue to invest in

making their platforms easier to use for a

broader range of users, yet less emphasis

on emerging growth areas

Others are trying to accommodate

emerging requirements such as smart

data discovery, self-service data

preparation, embedded advanced

analytics and big data capabilities to

differentiate themselves

Unclear the new platform vendors will

extend into the data infrastructure layer

A number of vendors provide access to

sophisticated, yet business-user-

accessible, data preparation tools:

The ever-increasing amount and diversity

of data has given rise to the use of NoSQL

databases, such as Hadoop, and thus

Hadoop-based data discovery specialists:

Though general visualization still

dominates new investment, new

requirements are occurring on the data

discovery and advanced analytics level

Smart data discovery players emerged to

further “democratize” data analytics:

Vendors focusing on governed data

discovery found their spot trying to balance

between business users demands and

data governance requirements from IT:

A mature market with several clear, large

leaders and significant funding for each

Emerging demand for multi-structure data

capabilities, especially NoSQL

5

Copyright © 2016 Shea & Company, LLC

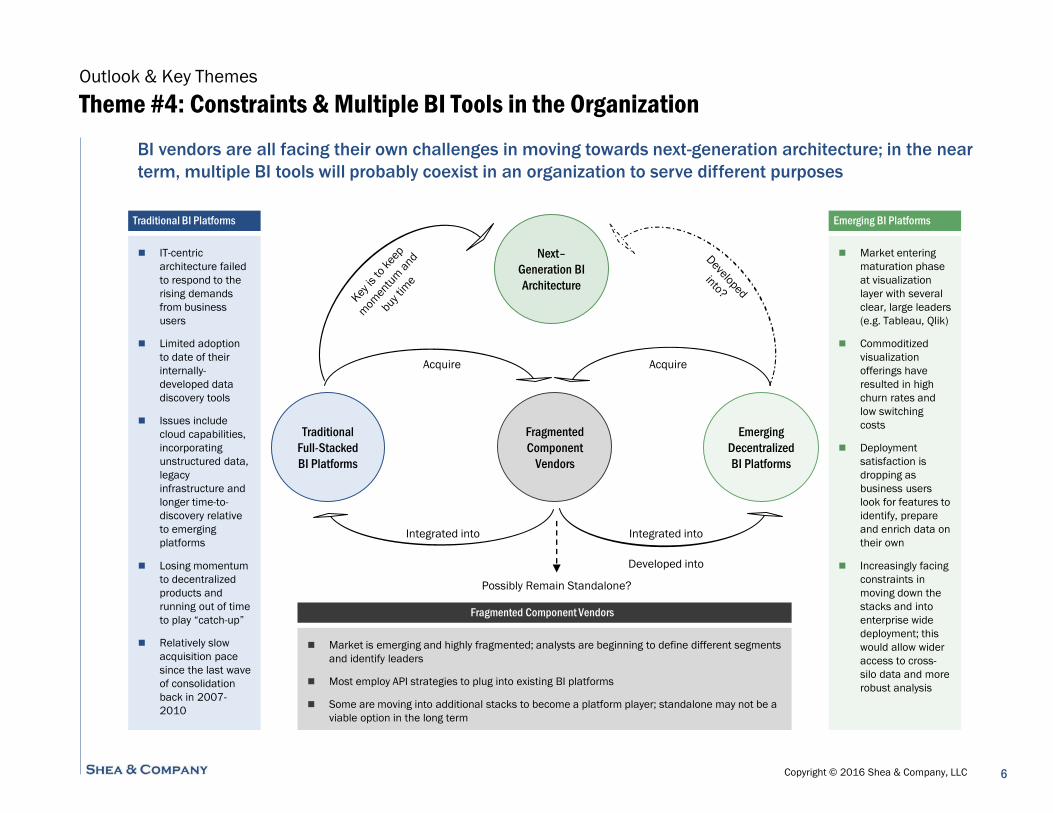

Market entering

maturation phase

at visualization

layer with several

clear, large leaders

(e.g. Tableau, Qlik)

Commoditized

visualization

offerings have

resulted in high

churn rates and

low switching

costs

Deployment

satisfaction is

dropping as

business users

look for features to

identify, prepare

and enrich data on

their own

Increasingly facing

constraints in

moving down the

stacks and into

enterprise wide

deployment; this

would allow wider

access to cross-

silo data and more

robust analysis

6

Outlook & Key Themes

Theme #4: Constraints & Multiple BI Tools in the Organization

Fragmented

Component

Vendors

Emerging

Decentralized

BI Platforms

Traditional

Full-Stacked

BI Platforms

Integrated into

Acquire

Integrated into

Developed into

Acquire

Possibly Remain Standalone?

Next–

Generation BI

Architecture

BI vendors are all facing their own challenges in moving towards next-generation architecture; in the near

term, multiple BI tools will probably coexist in an organization to serve different purposes

Traditional BI Platforms

IT-centric

architecture failed

to respond to the

rising demands

from business

users

Limited adoption

to date of their

internally-

developed data

discovery tools

Issues include

cloud capabilities,

incorporating

unstructured data,

legacy

infrastructure and

longer time-to-

discovery relative

to emerging

platforms

Losing momentum

to decentralized

products and

running out of time

to play “catch-up”

Relatively slow

acquisition pace

since the last wave

of consolidation

back in 2007-

2010

Emerging BI Platforms

Market is emerging and highly fragmented; analysts are beginning to define different segments

and identify leaders

Most employ API strategies to plug into existing BI platforms

Some are moving into additional stacks to become a platform player; standalone may not be a

viable option in the long term

Fragmented Component Vendors

Copyright © 2016 Shea & Company, LLC 7

Outlook & Key Themes

Theme #5: Bets Placed at All Layers, With Immediate Opportunity in the Middle

An

aly

tics

& V

isu

ali

zati

on

Da

ta A

ssem

bly

an

d P

rep

Da

ta In

fra

stru

ctu

re

Public$100m Raised Public$156m Raised $250m Raised

According to a 2013 Forrester survey, only 17% of information workers used a data dashboard or BI tools as part of their job

Multiple public competitors exist in this space already, with companies like Tableau trading at around 10x CY15E Revenue multiple

A new group of leaders is emerging and have raised significant amounts of capital

Self-service platforms are in the early stage of market evolution and will be used to accelerate a shift toward the business user by lowering complex analysis

Most platforms integrate with the likes of Tableau and Qlik, filling the gaps for data preparation and analytics features

Only now finding defined, repeatable use cases

Various segments of the data infrastructure market are very mature with clear leaders and large contenders raising large amounts of capital

The market for Hadoop-centric products alone is also believed to grow at a 64% CAGR from $4.2bn to $50bn by 2020; and existing companies have major partnerships

across the software realm

Source: Gartner, Forrester

$1,042m RaisedPublic PublicPublic $174m Raised$47m Raised

$51m Raised$23m Raised

$65m Raised$32m Raised

$108m Raised

$28m Raised$78m Raised$77m Raised $39m Raised$49m Raised

$208m Raised $28m Raised

Platforms

$24m Raised

Component

Copyright © 2016 Shea & Company, LLC 8

Outlook & Key Themes

Theme #6: How We See the Market Playing Out

The BI market will undergo a paradigm shift over the next few years as emerging players seek to gain

further market share and larger players look to play catch-up

Continued Acceleration of

Emerging Vendors

Legacy Vendors will

Maintain a Foothold

Solutions More

Widely Adopted

at SMB Level

Next Wave of

Consolidation Starts

Well-funded, disruptive independent vendors focused on the top stack (Birst, Tableau,

GoodData) continue to take share from legacy solutions and move down stack

Vendors see use at the departmental level as more than just a complement to the standard BI

infrastructure in enterprises

Established vendors with existing footprints continue to control the “plumbing” and basic

reporting function of BI

Vendors will look to maintain a foothold by upgrading product offerings through both in-house

innovation (Amazon developing QuickSight) and through acquisition

SaaS-based, easy-to-use solutions extend the appeal and value to the mid-market, who will

increasingly drive growth of the overall market

Emerging vendors will control the majority of the share in these markets given their value

proposition

Legacy players (SAP, Oracle, IBM, etc.) acquire established platforms and smaller component

players to upgrade platforms

Growing next-generation vendors (TIBCO, Qlik, etc.) acquire rising technologies to extend their

lead

Copyright © 2016 Shea & Company, LLC 9

Outlook & Key Themes

Theme #6 (Cont’d): M&A Interest Comes from Several Angles

Diversified Technology Platforms

Diversified technology vendors offering

solutions across the BI stack, from

hardware to applications

Will look to do technology tuck-ins as

well as acquire platforms

Independent BI vendors of scale

looking to build BI product offering

across the technology stack

More focused on tuck-in technology /

functionality acquisitions

Vendors controlling the data and

infrastructure layer

Focused on platform acquisitions to

move up the technology stack towards

the application layer

Pure-Play BI Vendors Data & Infrastructure

Copyright © 2016 Shea & Company, LLC

Outlook & Key Themes

Theme #6 (Cont’d): Time to Action for Legacy Players

10

Since a strong consolidation period starting in 2007 amongst BI 1.0 solutions, legacy solution vendors

have been slow to react in the past few years and are now running against time to catch up in the

significant shift of the BI landscape

Source: 451 Group

Acquirer Data Infrastructure Data Assembly and Prep Analytics and Visualization

in 2010 for

$1.8bn

in 2010 for

undisclosed

amount

in 2014 for

undisclosed

amount

in 2015 for

undisclosed

amount in 2007 for $170m in 2009 for $12m

in 2013 for

undisclosed

amount in 2007 for $5bn

in 2009 for

$1.2bn

in 2007 for

undisclosed

amount in 2008 for $250m

in 2011 for

undisclosed

amount

in 2011 for

$27.5m in 2006 for $40m in 2008 for $1.2bn in 2014 for $115m

in 2015 for

undisclosed

amount

in 2006 for $60m in 2007 for $60m in 2009 for $7.4bn

in 2009 for

undisclosed

amount in 2006 for $45m

in 2009 for

undisclosed

amount in 2006 for $5.9bn in 2007 for $3.3bn in 2009 for $1.1bn

in 2005 for

undisclosed

amount in 2010 for $6.1bn

in 2012 for

undisclosed

amount in 2007 for $490m in 2007 for $490m in 2008 for $6.8bn in 2013 for $40m

in 2008 for

undisclosed

amount

in 2010 for

undisclosed

amount

in 2011 for

undisclosed

amount

in 2012 for

undisclosed

amount

(assets)

Agenda

11

Outlook & Key Themes

Business Intelligence & Analytics Technology Stack and Landscape

Transaction & Acquisition Landscape

Shea & Company Firm Overview

Copyright © 2016 Shea & Company, LLC

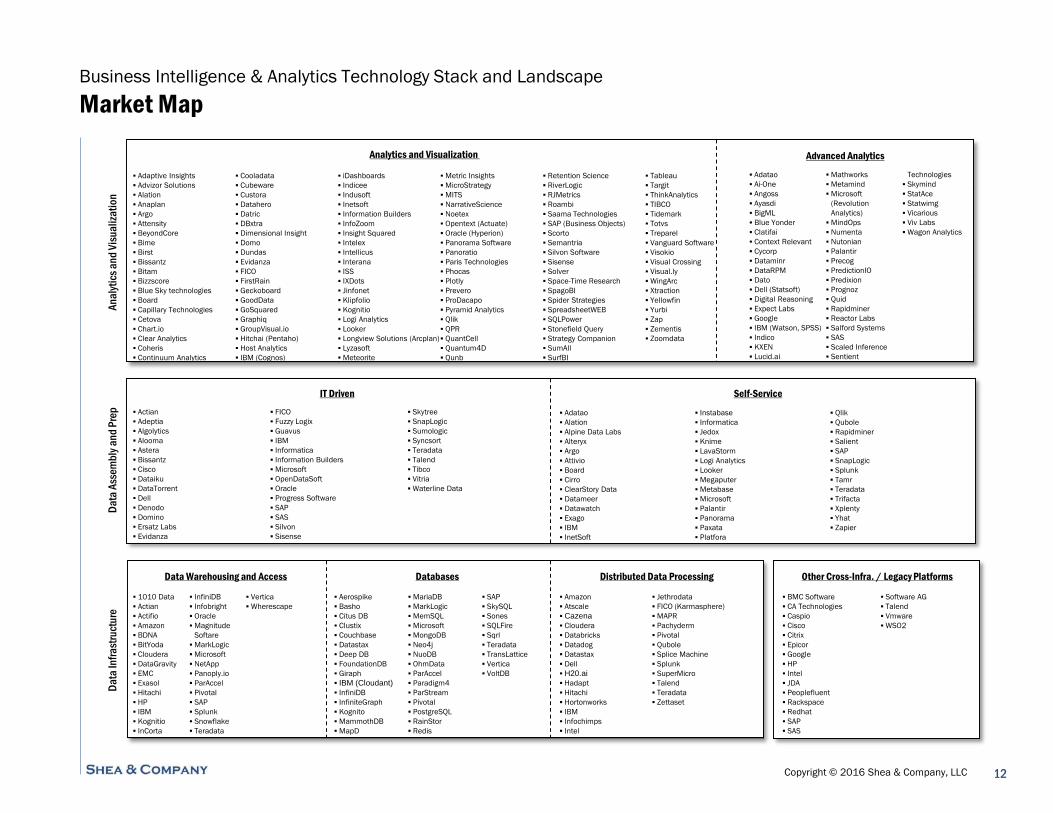

Business Intelligence & Analytics Technology Stack and Landscape

Market Map

Data Warehousing and Access Databases

Advanced AnalyticsAnalytics and Visualization

1010 Data

Actian

Actifio

Amazon

BDNA

BitYoda

Cloudera

DataGravity

EMC

Exasol

Hitachi

HP

IBM

Kognitio

InCorta

InfiniDB

Infobright

Oracle

Magnitude

Softare

MarkLogic

Microsoft

NetApp

Panoply.io

ParAccel

Pivotal

SAP

Splunk

Snowflake

Teradata

Vertica

Wherescape

Distributed Data Processing

BMC Software

CA Technologies

Caspio

Cisco

Citrix

Epicor

HP

Intel

JDA

Peoplefluent

Rackspace

Redhat

SAP

SAS

Software AG

Talend

Vmware

WSO2

Aerospike

Basho

Citus DB

Clustix

Couchbase

Datastax

Deep DB

FoundationDB

Giraph

IBM (Cloudant)

InfiniDB

InfiniteGraph

Kognito

MammothDB

MapD

MariaDB

MarkLogic

MemSQL

Microsoft

MongoDB

Neo4j

NuoDB

OhmData

ParAccel

Paradigm4

ParStream

Pivotal

PostgreSQL

RainStor

Redis

SAP

SkySQL

Sones

SQLFire

Sqrl

Teradata

TransLattice

Vertica

VoltDB

Amazon

Atscale

Cazena

Cloudera

Databricks

Datadog

Datastax

Dell

H20.ai

Hadapt

Hitachi

Hortonworks

IBM

Infochimps

Intel

Jethrodata

FICO (Karmasphere)

MAPR

Pachyderm

Pivotal

Qubole

Splice Machine

Splunk

SuperMicro

Talend

Teradata

Zettaset

Adatao

Ai-One

Angoss

Ayasdi

BigML

Blue Yonder

Clatifai

Context Relevant

Cycorp

Dataminr

DataRPM

Dato

Dell (Statsoft)

Digital Reasoning

Expect Labs

IBM (Watson, SPSS)

Indico

KXEN

Lucid.ai

Mathworks

Metamind

Microsoft

(Revolution

Analytics)

MindOps

Numenta

Nutonian

Palantir

Precog

PredictionIO

Predixion

Prognoz

Quid

Rapidminer

Reactor Labs

Salford Systems

SAS

Scaled Inference

Sentient

Technologies

Skymind

StatAce

Statwimg

Vicarious

Viv Labs

Wagon Analytics

An

aly

tics

an

d V

isu

ali

zati

on

Actian

Adeptia

Algolytics

Alooma

Astera

Bissantz

Cisco

Dataiku

DataTorrent

Dell

Denodo

Domino

Ersatz Labs

Evidanza

FICO

Fuzzy Logix

Guavus

IBM

Informatica

Information Builders

Microsoft

OpenDataSoft

Oracle

Progress Software

SAP

SAS

Silvon

Sisense

Skytree

SnapLogic

Sumologic

Syncsort

Teradata

Talend

Tibco

Vitria

Waterline Data

IT Driven Self-Service

Adatao

Alation

Alpine Data Labs

Alteryx

Argo

Attivio

Board

Cirro

ClearStory Data

Datameer

Datawatch

Exago

IBM

InetSoft

Instabase

Informatica

Jedox

Knime

LavaStorm

Logi Analytics

Looker

Megaputer

Metabase

Microsoft

Palantir

Panorama

Paxata

Platfora

Qlik

Qubole

Rapidminer

Salient

SAP

SnapLogic

Splunk

Tamr

Teradata

Trifacta

Xplenty

Yhat

Zapier

Da

ta A

ssem

bly

an

d P

rep

Da

ta In

fra

stru

ctu

re

Adaptive Insights

Advizor Solutions

Alation

Anaplan

Argo

Attensity

BeyondCore

Bime

Birst

Bissantz

Bitam

Bizzscore

Blue Sky technologies

Board

Capillary Technologies

Cetova

Chart.io

Clear Analytics

Coheris

Continuum Analytics

Cooladata

Cubeware

Custora

Datahero

Datric

DBxtra

Dimensional Insight

Domo

Dundas

Evidanza

FICO

FirstRain

Geckoboard

GoodData

GoSquared

Graphiq

GroupVisual.io

Hitchai (Pentaho)

Host Analytics

IBM (Cognos)

iDashboards

Indicee

Indusoft

Inetsoft

Information Builders

InfoZoom

Insight Squared

Intelex

Intellicus

Interana

ISS

IXDots

Jinfonet

Klipfolio

Kognitio

Logi Analytics

Looker

Longview Solutions (Arcplan)

Lyzasoft

Meteorite

Metric Insights

MicroStrategy

MITS

NarrativeScience

Noetex

Opentext (Actuate)

Oracle (Hyperion)

Panorama Software

Panoratio

Paris Technologies

Phocas

Plotly

Prevero

ProDacapo

Pyramid Analytics

Qlik

QPR

QuantCell

Quantum4D

Qunb

Retention Science

RiverLogic

RJMetrics

Roambi

Saama Technologies

SAP (Business Objects)

Scorto

Semantria

Silvon Software

Sisense

Solver

Space-Time Research

SpagoBI

Spider Strategies

SpreadsheetWEB

SQLPower

Stonefield Query

Strategy Companion

SumAll

SurfBI

Tableau

Targit

ThinkAnalytics

TIBCO

Tidemark

Totvs

Treparel

Vanguard Software

Visokio

Visual Crossing

Visual.ly

WingArc

Xtraction

Yellowfin

Yurbi

Zap

Zementis

Zoomdata

Other Cross-Infra. / Legacy Platforms

12

Copyright © 2016 Shea & Company, LLC

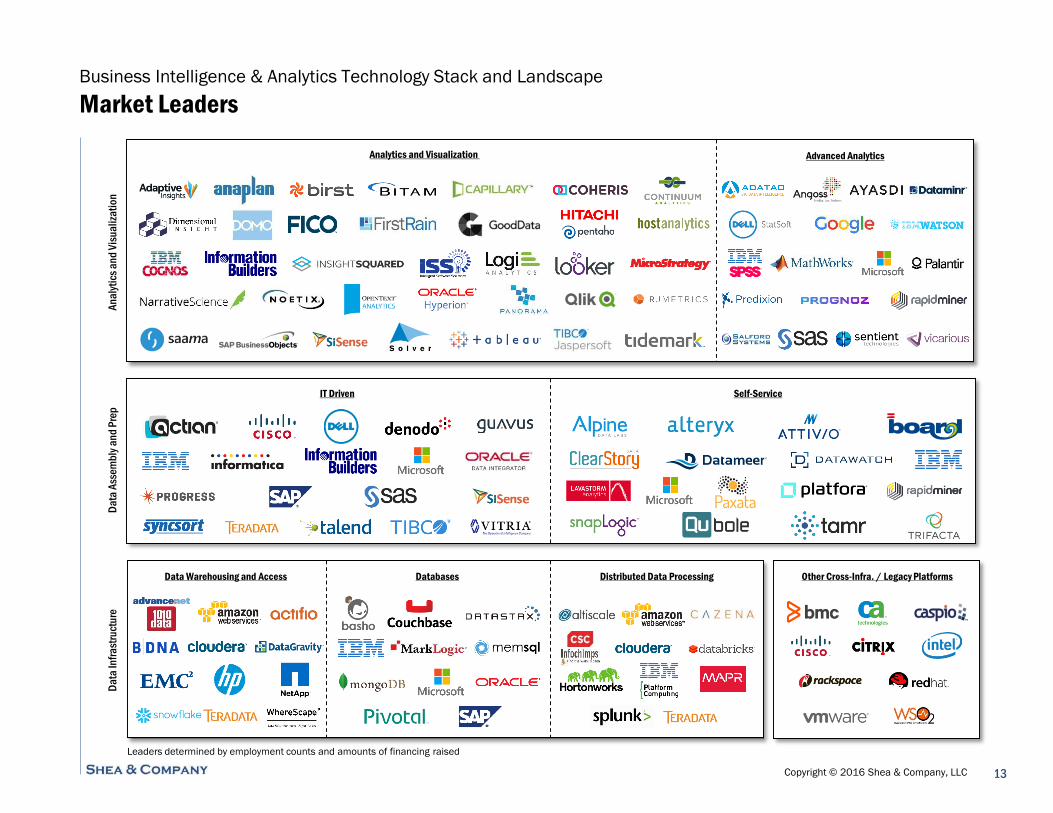

Business Intelligence & Analytics Technology Stack and Landscape

Market LeadersD

ata

Ass

emb

ly a

nd

Pre

pD

ata

Infr

ast

ruct

ure

Leaders determined by employment counts and amounts of financing raised

An

aly

tics

an

d V

isu

ali

zati

on

13

Data Warehousing and Access Databases

Advanced AnalyticsAnalytics and Visualization

Distributed Data Processing

IT Driven Self-Service

Other Cross-Infra. / Legacy Platforms

Agenda

14

Outlook & Key Themes

Business Intelligence & Analytics Technology Stack and Landscape

Transaction & Acquisition Landscape

Shea & Company Firm Overview

Copyright © 2016 Shea & Company, LLC

Latest Round Date 06/12/14 09/09/14 09/15/14 03/17/15 07/22/15 10/28/15 01/14/16

Amount Raised $30 $26 $16 $65 $235 $85 $48

Post-Money, Latest Round n/a $276 $64 $500 $2,035 $765 n/a

Total Raised to Date $54 $100 $24 $156 $484 $163 $96

Transaction & Acquisition Landscape

Recent Capital Raise Activity

Source: PitchBook and other publicly available sources

($ millions)

15

Close Date Company Participating Investor(s) Description Amount Post Val

01/14/16 Looker KPCB, Meritech, Redpoint, Sapphire Ventures Web-based relational querying tools 48$ n/a

10/28/15 Alteryx Insight, Iconiq Capital Data pulling, cleaning, management and overlay 85 765

10/20/15 Pyramid Analytics Sequoia, Viola Group Integrated, scalable dashboards and analytics 30 n/a

09/09/15 Paxata Accel, EDBI, Walden Riverwood Ventures, Toba Capital Analyst-centric data preparation 18 72

09/02/15 Capillary Technologies Sequoia, Warburg Pincus, Norwest Venture Partners End-to-end, multichannel customer engagement, BI and social CRM 45 181

08/12/15 Datameer Citi Ventures, KPCB, Next World Capital, Redpoint, Top Tier Capital Partners, Workday Self-service data integration, analytics and visualization 40 224

07/23/15 Continuum Analytics BuildGroup, Defense Advanced Research Projects Agency, General Catalyst, Various Angels Scientific computing, analysis, visualization and reporting 24 n/a

07/22/15 Cazena Andreessen Horowitz, Formation 8, North Bridge Venture Partners On-demand big data platform for improved data access 28 88

07/22/15 Domo Glynn Capital, GGV Capital, and The Capital Group Companies Executive business management platform 235 2,035

06/23/15 Snowflake Computing Altimeter Capital, Redpoint, Sutter Hill, Wing Venture Partners Cloud data warehousing 45 274

06/09/15 Saama Technologies Carrick Capital Partners Machine learning and big data analysis tools 36 n/a

03/25/15 Ayasdi Bullpen, Centerview Capital, Citi Ventures, Draper Nexus, FLOODGATE, GE Ventures, IVP, Khosla, KPCB Machine intelligence platform for topological data analysis 55 n/a

03/19/15 Quid Artis, Atomico, Endeavour Vision, Founders Fund, Infocomm, Liberty Interactive, Subtraction, T.H. Lee Decision making optimization and data capturing and management 39 n/a

03/17/15 Birst DAG Ventures, Hummer Winblad, Northgate, Sequoia, Wellington Automated data warehousing and visual analytics 65 500

03/17/15 DataMinr Credit Suisse, Deep Fork, Expansion Venture, Glynn, Goldman, GSV, IVP, Venrock, Wellington, Wharton Equity Real-time social media analytics 130 700

02/18/15 RapidMiner Ascent Venture Partners, Earlybird Venture Capital, Longworth Venture Partners, Open Ocean Capital Open stack predictive dashboards, metrics and reporting 15 28

01/21/15 Interana AME Cloud, Battery, FUEL Capital, Index, Data Collective Real-time mass data interpretation 20 n/a

12/12/14 Hortonworks n/a Data storage, management and analytics 100 n/a

11/17/14 InsightSquared Atlas Venture, DFJ, NextView Ventures, Two Sigma Investments Employee activity tracking, sales forecasting and win loss analysis 14 85

10/06/14 Zoomdata Accel, B7 Ventures, Columbus Nova Technology, NEA, Razor's Edge Ventures Data analytics and visualization platform 17 52

09/29/14 Qubit Accel, Balderton Capital, Salesforce.com Website optimization, CRM, web personalization and testing 26 n/a

09/23/14 Radius Intelligence BlueRun, Formation 8, Founders Fund, Glynn Capital, Slow Ventures, Western Technology Investment Sales and marketing intelligence and insights 55 n/a

09/15/14 RjMetrics August, SoftTech VC, Trinity Ventures E-commerce analytics platform 17 64

09/09/14 GoodData Andreessen Horowitz, General Catalyst, Intel Capital, NWC, Pharus Capital, Tenaya, TOTVS, Windcrest Business intelligence and dashboard reporting tools 26 276

07/08/14 RetailNext Activant, American Express, August, Commerce Ventures, Nokia Growth, Qualcomm Ventures, StarVest, Tyco In-store business intelligence and data visualization 30 184

06/30/14 MapR Google Capital, Lightspeed, Mayfield, NEA, Qualcomm Ventures Data protection and business continuity for big data processes 110 583

06/12/14 SiSense Battery, DFJ Growth, Genesis Partners, Opus Capital Data analytics and reports sharing 30 n/a

05/29/14 Trifacta Accel, Greylock, Ignition Productivity platform for simplifying raw data into actionable form 25 133

05/08/14 Tidemark Systems Andreessen Horowitz, Greylock, Redpoint, SVB, Tenaya Enterprise performance management 32 250

03/19/14 Cloudera DAG Ventures, Google Ventures, Intel Capital, MSD Capital, T. Rowe Price Data management and enterprise Hadoop infrastructure 900 4,111

Copyright © 2016 Shea & Company, LLC

[b] Source: The 451 Group

Note: EV / Revenue multiples greater than 20x and EV / EBITDA multiples greater than 50x are considered to be not meaningful

($ millions)

16

Transaction & Acquisition Landscape

Recent M&A Activity

Consideration Equity Enterprise EV / Revenue EV / EBITDA EV / EBITDA

Announced Target Acquirer % Cash % Stock Value Value Current yr Forward yr Current yr Forward yr

10/13/15 We Are Cloud (BIME) Zendesk 100.0% 0 0.0% 0 - 0 $45 0 - - 0 - -

08/03/15 1010data Advance Publications 100.0% 0 0.0% 0 - 0 $500 0 10.0x [b] - 0 - -

06/01/15 Maxifier Cxense ASA 0.0% 0 100.0% 0 - 0 $4 0 1.2x - 0 - -

05/21/15 Troux Technologies Planview 100.0% [b] 0.0% [b] - 0 $40 [b] 1.3x [b] - 0 - -

05/05/15 ColdLight Solutions PTC 100.0% 0 0.0% 0 - 0 $100 0 13.8x [b] - 0 - -

04/27/15 Applied Predictive Technologies MasterCard - 0 - 0 - 0 $600 0 - - 0 - -

03/05/15 Appfluent Attunity 61.0% 0 39.0% 0 - 0 $18 0 5.5x 2.4x 0 - -

02/26/15 Prelytix First Derivatives 80.0% 0 20.0% 0 - 0 $8 0 3.8x - 0 nm -

02/10/15 Pentaho Hitachi Data Systems 100.0% [b] 0.0% [b] - 0 $530 [b] 13.3x [b] - 0 - -

01/23/15 Revolution Analytics Microsoft 100.0% 0 0.0% 0 - 0 $115 [b] nm - 0 - -

12/05/14 Actuate OpenText 100.0% 0 0.0% 0 $330 0 $272 0 2.7x 3.0x 0 nm -

11/05/14 Dealogic Carlyle Group - 0 - 0 - 0 $700 0 5.0x - 0 - -

10/14/14 CQuotient Demandware 100.0% 0 0.0% 0 - 0 $22 0 - - 0 - -

07/08/14 Social Solutions Vista Equity Partners 100.0% 0 0.0% 0 - 0 $125 [b] 6.3x [b] - 0 - -

05/06/14 Adometry Google 100.0% [b] 0.0% [b] - 0 $150 [b] 7.5x [b] - 0 - -

04/28/14 Jaspersoft TIBCO Software - 0 - 0 - 0 $185 0 6.2x [b] - 0 - -

03/14/14 InfoCentricity Fair Isaac 100.0% 0 0.0% 0 - 0 $8 0 - - 0 - -

01/22/14 Scout Analytics ServiceSource International 100.0% 0 0.0% 0 - 0 $32 0 5.9x - 0 - -

12/16/13 SignalDemand PROS Holdings 100.0% 0 0.0% 0 - 0 $14 0 - - 0 - -

09/18/13 Extended Results TIBCO Software - 0 - 0 - 0 $21 0 - - 0 - -

09/10/13 KXEN SAP 100.0% [b] 0.0% [b] - 0 $40 [b] 3.3x [b] - 0 - -

08/22/13 Jackbe Software AG 100.0% [b] 0.0% [b] - 0 $40 [b] 4.0x [b] - 0 - -

08/06/13 Infochimps Computer Sciences 100.0% [b] 0.0% [b] - 0 $25 [b] 12.5x [b] - 0 - -

06/27/13 Visual Analytics Raytheon 100.0% 0 0.0% 0 - 0 $14 0 - - 0 - -

06/17/13 Panopticon Software AB Datawatch 0.0% 0 100.0% 0 - 0 $31 0 6.3x - 0 - -

06/11/13 StreamBase Systems TIBCO Software 100.0% 0 0.0% 0 - 0 $52 0 2.6x [b] - 0 - -

06/07/13 EdgeSpring Salesforce.com 47.0% 0 53.0% 0 - 0 $134 0 - - 0 - -

05/06/13 NComVA AB QlikTech 100.0% 0 0.0% 0 - 0 $8 0 - - 0 - -

03/01/13 Altosoft Kofax 100.0% 0 0.0% 0 $14 0 $14 0 4.0x - 0 27.0x -

01/28/13 Angoss Software Corporation Peterson Partners 100.0% 0 0.0% 0 $5 0 $6 0 0.9x - 0 - -

01/28/13 Pervasive Software Actian 100.0% 0 0.0% 0 $162 0 $119 0 2.4x 2.3x 0 24.8x 22.5x

01/16/13 Cogility Software Drumright Group - 0 - 0 $7 0 $7 0 - - 0 - -

12/19/12 StoredIQ IBM - 0 - 0 - 0 - 0 - [b] - 0 - -

11/19/12 AltoStor WANdisco International Ltd. - 0 - 0 $4 0 $4 0 - - 0 - -

10/22/12 Quiterian Actuate 100.0% 0 0.0% 0 - 0 $5 0 - - 0 - -

09/04/12 Prelytis SA Access UK Ltd. - 0 - 0 - 0 $5 0 - - 0 - -

08/07/12 Xformity Altametrics 100.0% 0 0.0% 0 $1 0 $1 0 - - 0 - -

04/26/12 Torex Retail Holdings MICROS Systems 100.0% 0 0.0% 0 $107 0 $185 0 - - 0 - -

Mean 89.6% 10.4% $78.7 $112.9 5.6x 2.6x 25.9x 22.5x

Median $10.3 $32.0 5.0x 2.4x 25.9x 22.5x

Agenda

17

Outlook & Key Themes

Business Intelligence & Analytics Technology Stack and Landscape

Transaction & Acquisition Landscape

Shea & Company Firm Overview

Copyright © 2016 Shea & Company, LLC

Advisory Services and Selected Transactions

18

Mergers & Acquisitions

Buy-side and sell-side M&A advisory

Divestitures

Restructuring

Private Placements & Capital Raising

Late-stage venture and growth equity

Recapitalizations

IPO advisory

Corporate Strategy

Corporate development advisory

Fairness opinions

Selected TransactionsShea & Company has advised on billions of dollars of software M&A and capital raise transactions

Shea & Company Firm Overview

Introduction to Shea & Company

Shea & Company served as the exclusive

financial advisor to Mimecast

has received an investment from

Shea & Company served as the exclusive

financial advisor to Lacoon

has been acquired by

Shea & Company served as the exclusive

financial advisor to Bronto

has been acquired by by

Shea & Company served as the exclusive

financial advisor to TA Associates

has acquired

Shea & Company served as the exclusive

financial advisor to Bomgar Corporation

has received a majority investment from

Shea & Company served as the exclusive

financial advisor to SeeWhy

has been acquired by

Shea & Company served as the exclusive

financial advisor to MRI Software

has been acquired by

Shea & Company served as the exclusive

financial advisor to LastPass

has been acquired by

Shea & Company served as the exclusive

financial advisor to Secure Islands

has been acquired by

People ▪ Industry Expertise ▪ Process Excellence

Shea & Company served as the exclusive

financial advisor to HP

has been acquired by

Shea & Company served as the exclusive

placement agent for the transaction

has received an investment from

Shea & Company served as the exclusive

financial advisor to Sovos Compliance

has received a majority investment from