Embed Size (px)

Citation preview

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent.

Milano, July 1st 2014

Shale Gas: impacts on the Value Chain

Tiziano Rivolta*

*Bain & Company Italy, Inc.

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 2

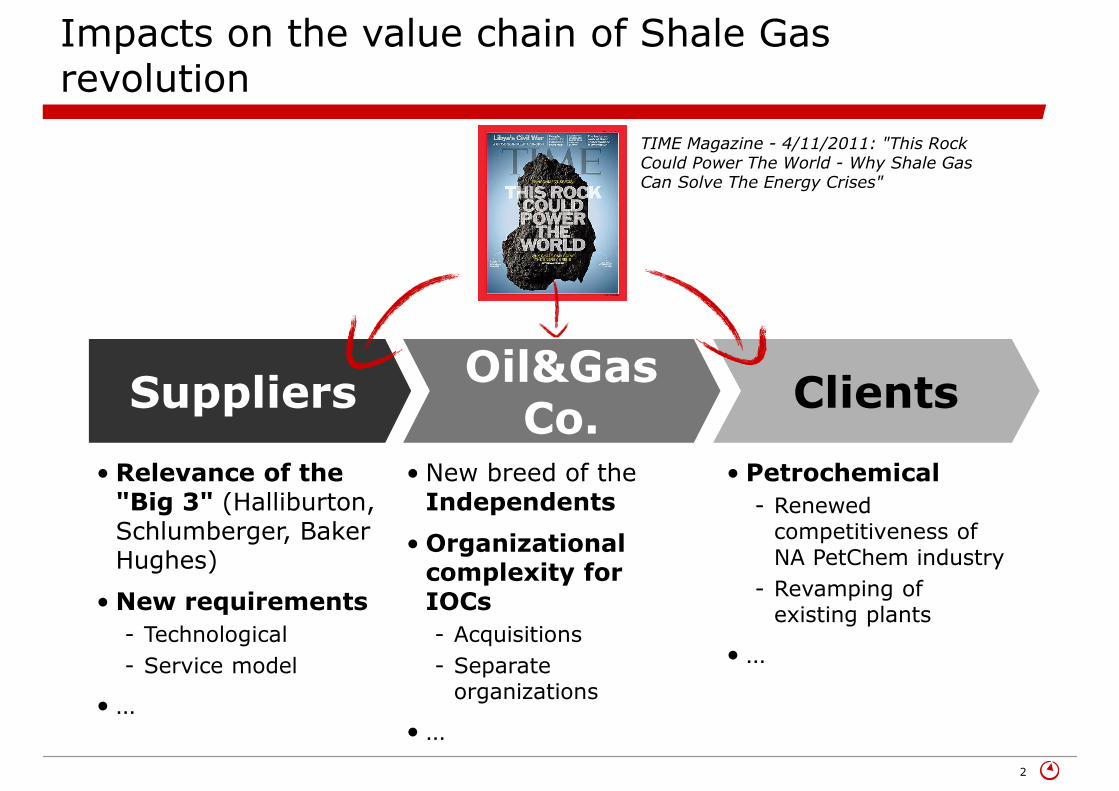

Impacts on the value chain of Shale Gas revolution

ClientsOil&Gas

Co.Suppliers

• Relevance of the "Big 3" (Halliburton, Schlumberger, Baker Hughes)

• New requirements

- Technological

- Service model

• …

• New breed of the Independents

• Organizational complexity for IOCs

- Acquisitions

- Separate organizations

• …

• Petrochemical

- Renewed competitiveness of NA PetChem industry

- Revamping of existing plants

• …

TIME Magazine - 4/11/2011: "This Rock Could Power The World - Why Shale Gas Can Solve The Energy Crises"

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 3

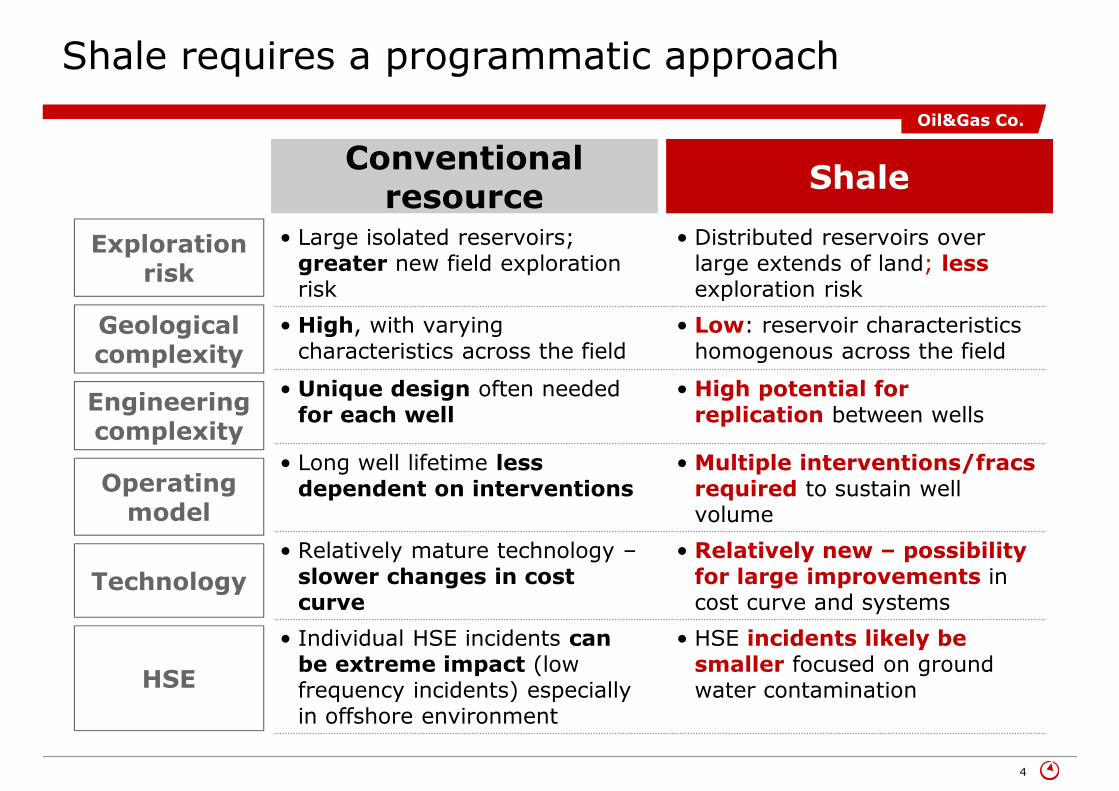

Shale plays differ significantly from conventional resources

Conventional resource Shale

Oil&Gas Co.

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 4

Shale requires a programmatic approach

• Large isolated reservoirs; greater new field exploration risk

• Distributed reservoirs over large extends of land; less exploration risk

• High, with varying characteristics across the field

• Low: reservoir characteristics homogenous across the field

• Unique design often needed for each well

• High potential for replication between wells

• Long well lifetime less dependent on interventions

• Multiple interventions/fracsrequired to sustain well volume

• Relatively mature technology –slower changes in cost curve

• Relatively new – possibility for large improvements in cost curve and systems

• Individual HSE incidents can be extreme impact (low frequency incidents) especially in offshore environment

• HSE incidents likely be smaller focused on ground water contamination

Conventional resource

Exploration risk

Geological complexity

Engineering complexity

Operating model

Technology

HSE

Shale

Oil&Gas Co.

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 5

Companies need to develop or acquire a number of shale-specific skills in each phase of the value chain

•Fast acquisition of small land tracts based on limited info (e.g. 2D logs)

•Rapid piloting and high-grading of technical solutions

•Factory process to minimize down-time and accelerate development

•Down-spacing and multilateral wells to maximize pad utilization

•Coordination of fracing stages for existing wells to optimize well life and balance field production

•Sophisticated O&M logistics

•On time development of gathering lines and processing facilities

•Capacity sizing and utilization linked to field development plan

Access & exploration

Drilling & completions

Production Midstream

Technology

Support functions

• Multilateral fracturing• Hydraulic fracturing

• Sophisticated sand and water logistics

• Large volume of data collection and information processing

• Debottlenecking support services to process high volume of repeatable tasks

Oil&Gas Co.

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 6

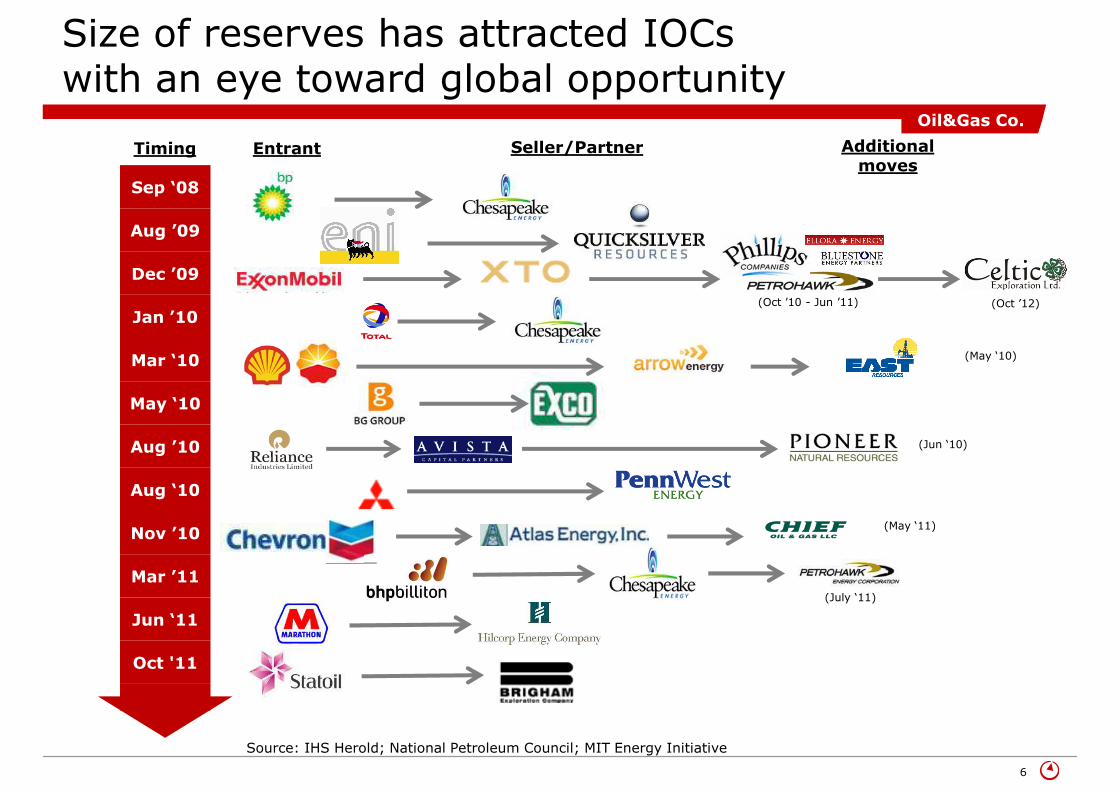

Size of reserves has attracted IOCs with an eye toward global opportunity

Source: IHS Herold; National Petroleum Council; MIT Energy Initiative

Sep ‘08

Aug ’09

Dec ’09

Jan ’10

Mar ‘10

May ‘10

Aug ’10

Aug ‘10

Nov ’10

Mar ’11

Jun ‘11

Oct '11

Timing Entrant Seller/Partner Additional moves

(Oct ’10 - Jun ’11)

(May ‘10)

(Jun ‘10)

(May ‘11)

(July ‘11)

Oil&Gas Co.

(Oct ’12)

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 7

0

20

40

60

80

100%

Barnett

CHK

Southwestern

EOG

Total

SmallINDs

Pioneer

Exxo

n

BHP

Exxo

n

BP

Haynesville

EOG

Devon

Plains

CHK

Encana

Ana

dark

o

Exxon

BHP

BG

SmallINDs

ConocoChevronTotal SA

Marcellus

TailsmanUPL

SouthwesternEOG

Range

CHK

Anadarko

Noble

BG

Gail

Reliance

Small INDs

Chevron

Shell

StatOil

Exxon

Utica

Hess

Anad

arko

CHK

Devon

Small

INDsExxon

Che

vron

Eagleford

PioneerMurphy

Hess

BHPTailsman

CHK

EOG

Newfield

Anadarko

Apache

Reliance

CNOOC

KNOC

SmallINDs

StatOil

Shell

Marathon

ConocoExxon

Bakkens area

EOG

Newfield

Whiting

Continental

Hess

StatOil

Small INDs

Marathon

Conoco*

Exxon

Niobrara

Devon

EOG

Anadarko

CHK

Noble

Continental

CNOOC

SmallINDs

Marathon

Whiting

Shell

Approximate U.S. shale positions by major play(~38M acres held)

Fayetteville

Rapid consolidation amongst operators is taking place, increasing importance of IOCs and large Independents

*Note: ConocoPhillips data from firm website and includes entire Williston Basin (N.Dakota, Montana, and Canada). Positions are an approximate view of most major acreage holders in Q4-2011 in selected basins only. Utica positions are approximate as majority of acquisitions are in last six months

Source: Operator investor relations presentations; literature search; Bain analysis

Dry gas NGL Shale/tight oil

Oil&Gas Co.

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 8

Traditional E&P functional model unlikely to be appropriate for shale gas operations

•Ability to leverage technical expertise across entire business

•Technical skills needed for shale unique

•Focus on optimizing capital allocation& resources across global project portfolio

• Less need to analyze economics of individual projects – need to focus on system and program economics

•Common processes drive consistency across the organization (e.g. well delivery, safety response)

•Common processes may be over engineered for shale gas, introducing unnecessary costs into system

• Increased efficiency in project execution and use of resources

•Repetitive processes necessary to drive down costs

•Focus on quality of functional performance globally

•Speedy cross-functional issue resolution and local optimization needed

Functional model typically adopted for specific benefits…

…that are not applicable in shale operations

Oil&Gas Co.

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 9

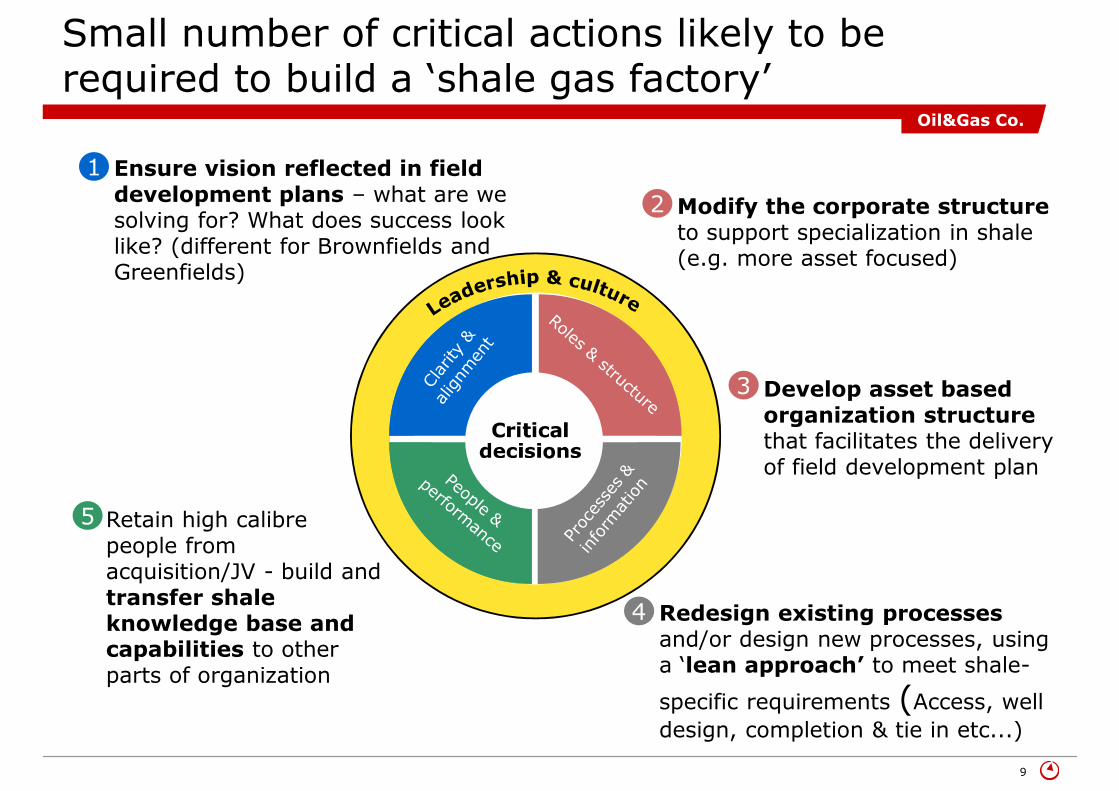

Small number of critical actions likely to be required to build a ‘shale gas factory’

• Ensure vision reflected in field development plans – what are we solving for? What does success look like? (different for Brownfields and Greenfields)

• Develop asset based organization structure that facilitates the delivery of field development plan

1

• Modify the corporate structureto support specialization in shale (e.g. more asset focused)

2

3

• Retain high calibre people from acquisition/JV - build and transfer shale knowledge base and capabilities to other parts of organization

5

• Redesign existing processes and/or design new processes, using a ‘lean approach’ to meet shale-

specific requirements (Access, well

design, completion & tie in etc...)

4

Oil&Gas Co.

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 10

Key players are carving out separate organizations to develop their shale skillset

• ExxonMobil acquired XTO Energy in early 2010

• XTO continues to operate as a wholly-owned subsidiary of XOM

• Use of remote monitoring and operating centers: “information to make decisions is at fingertips, and replaces need for multiple meetings”

• In May 2008 EnCana announced that it was spinning into two companies:

- EnCana, focused on development of unconventional natural gas

- Cenovus Energy, an integrated oil company focused on tar sands assets

• “We will be better equipped to direct their strategies and operations towards building value by tailoring practices and execution to fit the unique nature of their assets” – Randy Eresman, EnCana CEO

• In late 2009, Talisman Energy reorganized its North American operations to clearly focus on shale vs. conventional assets

• Focused on optimizing key value levers for unconventional gas (lean well delivery, zipper fracs and supply chain optimization)

• As a result investment break-even cost reduced from $6.5/Mcf in 2009 to expected ~$3/Mcf range in 2011

• “It's all about what we call lean manufacturing processes within North America, which continuously work to drive down the operating costs” - John Manzoni, 2011, President

Source: companies’ webpages, analyst presentations and press releases

Oil&Gas Co.

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 11

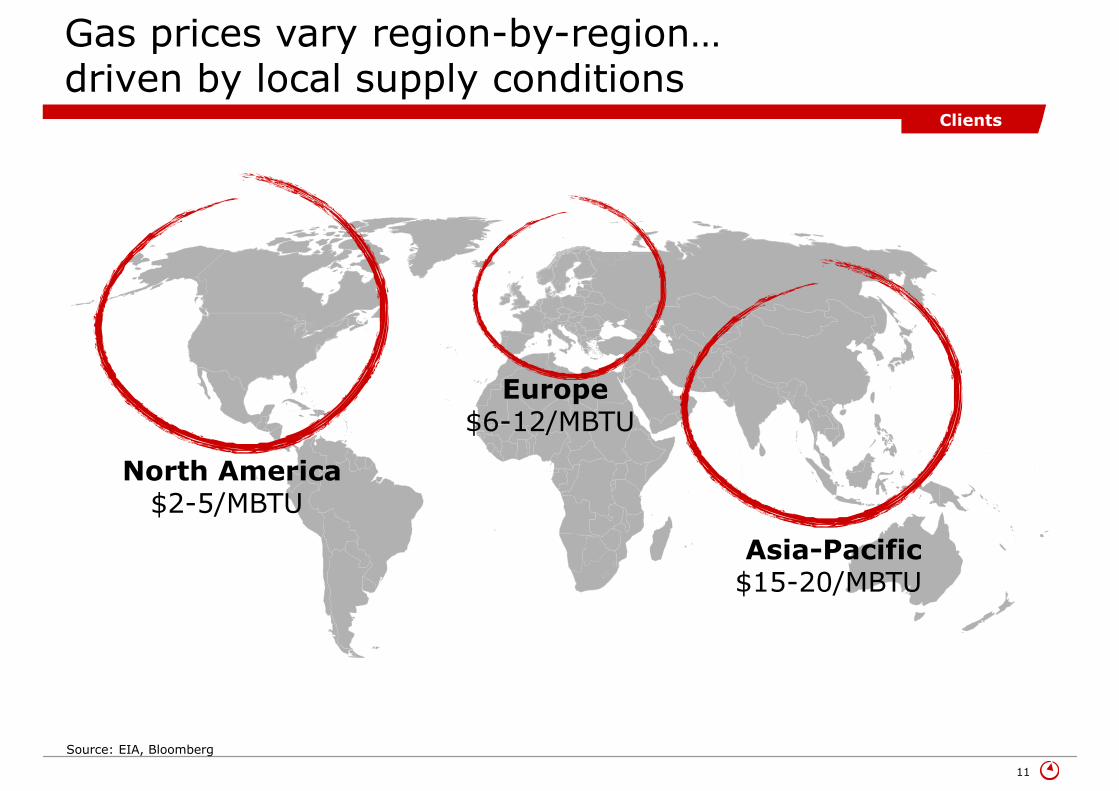

Gas prices vary region-by-region… driven by local supply conditions

Asia-Pacific$15-20/MBTU

Europe$6-12/MBTU

North America$2-5/MBTU

Source: EIA, Bloomberg

Clients

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 12

0

200

400

600

800

$1,000

2000 Ethylene average production

cash cost, U$/MT

US E

thane

US ethylene is - for example - now more cost competitive compared to other regions

0

200

400

600

800

$1,000

2011 Ethylene average production

cash cost, February, U$/MT

US E

thane

Source: CMAI presentation to SW chemical association, Feb 2011; KB Consulting Cost Model

Clients

YESTERDAY (2000) TODAY (2011)

Bren

t cru

de:

U$30/B

BL

Natu

ral

Gas:

U$4/M

MBTU

Bren

t cru

de:

U$94/B

BL

Natu

ral

Gas:

U$4.3

5/M

MBTU

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 13

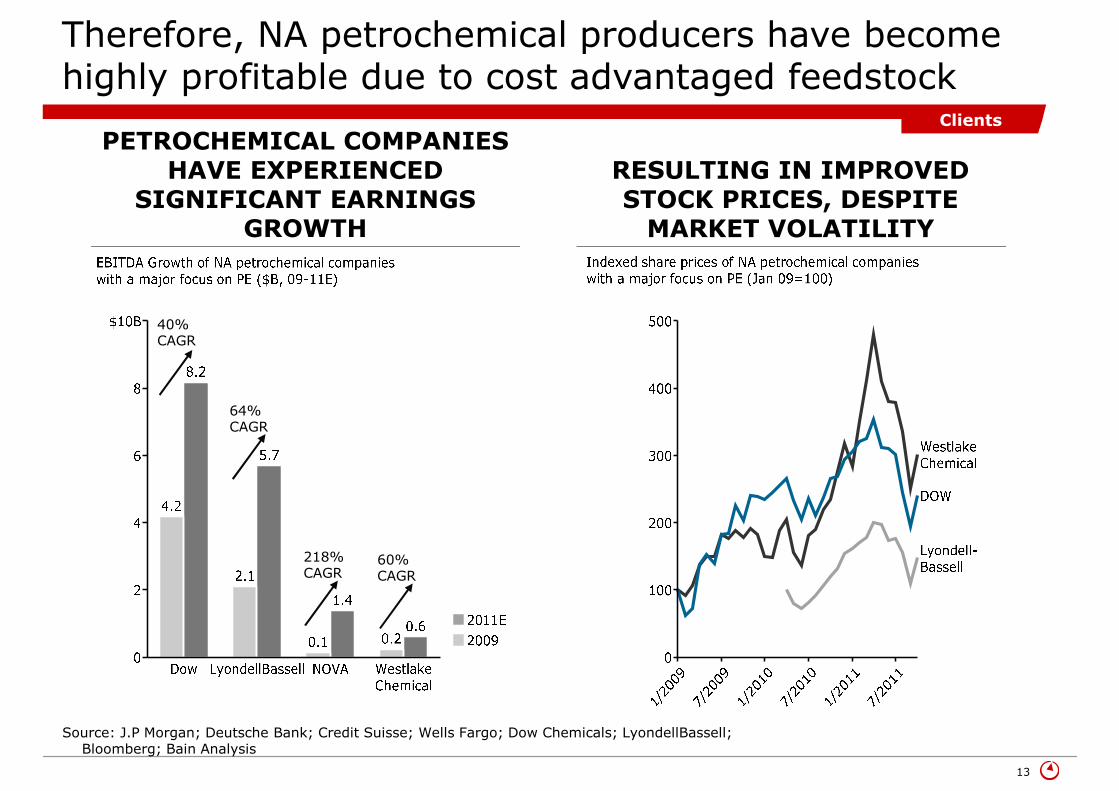

Therefore, NA petrochemical producers have become highly profitable due to cost advantaged feedstock

Source: J.P Morgan; Deutsche Bank; Credit Suisse; Wells Fargo; Dow Chemicals; LyondellBassell; Bloomberg; Bain Analysis

40%CAGR

64%CAGR

218%CAGR

60%CAGR

RESULTING IN IMPROVED STOCK PRICES, DESPITE

MARKET VOLATILITY

PETROCHEMICAL COMPANIES HAVE EXPERIENCED

SIGNIFICANT EARNINGS GROWTH

Clients

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 14

2000

6

2005

13

2011

Halliburton

Schlumberger

BakerHughes

Others

40

Explosive growth has opened opportunities for niche providers but ‘Big 3’ best positioned to meet emerging needs

Source: Bain analysis

"Big 3"

Suppliers

PRESSURE PUMPING REVENUE BY COMPANY ($B)

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 15

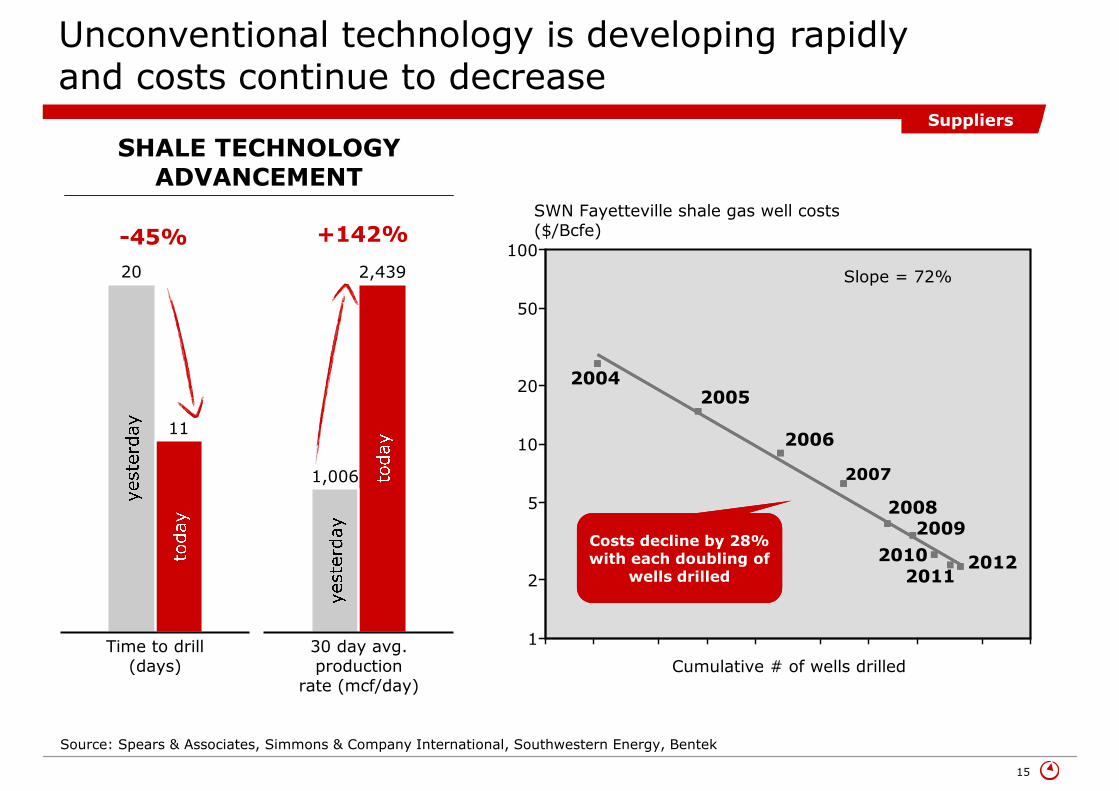

Unconventional technology is developing rapidly and costs continue to decrease

Time to drill(days)

20

11

30 day avg.production

rate (mcf/day)

1,006

2,439

+142%

SHALE TECHNOLOGY ADVANCEMENT

1

2

5

10

20

50

100

Cumulative # of wells drilled

SWN Fayetteville shale gas well costs($/Bcfe)

20122011

2010

20092008

2007

2006

20052004

Slope = 72%

Costs decline by 28% with each doubling of

wells drilled

Costs decline by 28% with each doubling of

wells drilled

-45%

Source: Spears & Associates, Simmons & Company International, Southwestern Energy, Bentek

Suppliers

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 16

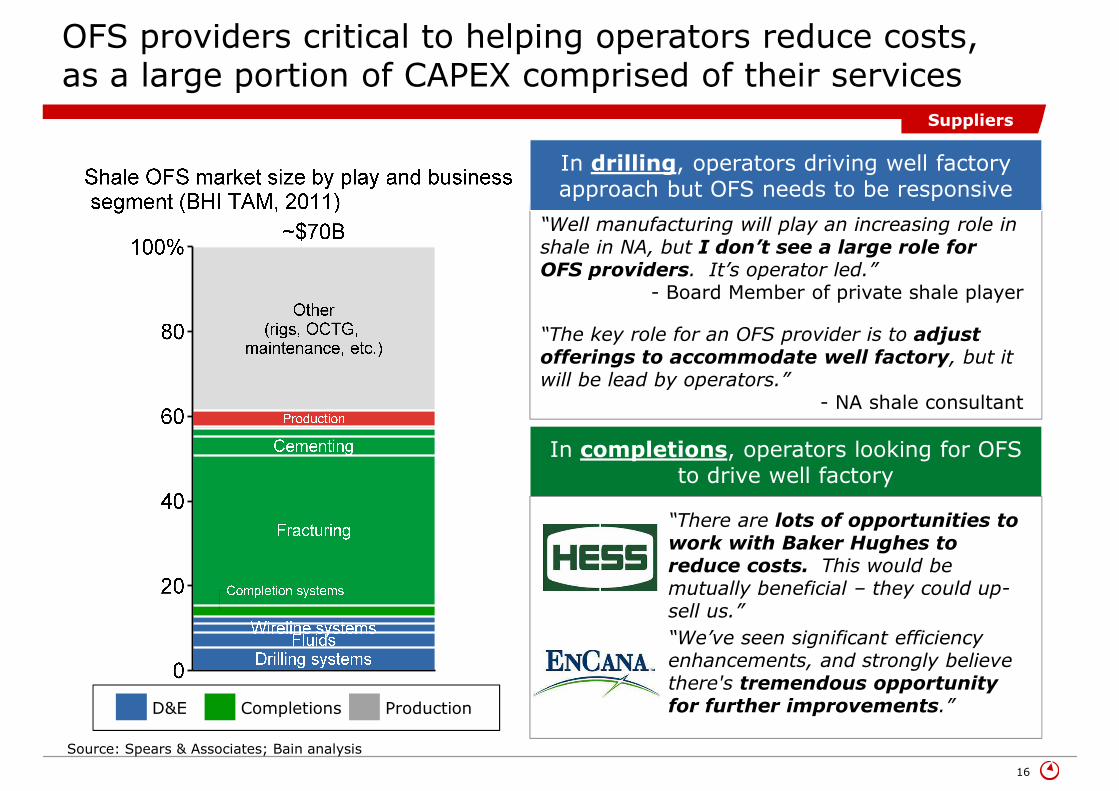

OFS providers critical to helping operators reduce costs, as a large portion of CAPEX comprised of their services

“Well manufacturing will play an increasing role in shale in NA, but I don’t see a large role for OFS providers. It’s operator led.”

- Board Member of private shale player

In completions, operators looking for OFS to drive well factory

“The key role for an OFS provider is to adjust offerings to accommodate well factory, but it will be lead by operators.”

- NA shale consultant

D&E Completions Production

“There are lots of opportunities to work with Baker Hughes to reduce costs. This would be mutually beneficial – they could up-sell us.”

“We’ve seen significant efficiency enhancements, and strongly believe there's tremendous opportunity for further improvements.”

Source: Spears & Associates; Bain analysis

Suppliers

In drilling, operators driving well factory approach but OFS needs to be responsive

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 17

Reward

Production Enhancement

Contract

Mature field management

•Fees based on tariff per barrel

•Value added through:

- Apply sub-surface capabilities to increase production

Production Sharing

Agreement

Risk Service Contract

Build, operate, transfer

•Fees based on KPIs

•Value added through:- Innovative design

- Cost effective execution

Field development and operation

•Fees based on share of production

•Value added through:

- Fast track delivery with early production

- End-to-end field management

- Apply sub-surface capabilities to identify by-passed resources

Risk

Fee for Service

Provision of discrete services

•Fees based on nature of services rendered

•Value added through:

- Technical innovation

- Low cost

- Degree of integration

Potential also exists to move towards more outcome-based pricing (as is happening in conventional)

Shale today

Future?

Suppliers

This information is confidential and was prepared by Bain & Company solely for training purposes; it is not to be relied on by any 3rd party without Bain's prior written consent. 18

To conclude

•Shale gas has transformed global gas industrygenerating profound industry consequences, severe disruptions along the natural gas value chain and, on the other hand, tremendous opportunities

•Shale gas is different to conventional resources and the traditional E&P functional model does not work effectively

•A new operating model is required in order to succeed in shale gas with a small number of critical actions needed to build a ‘shale gas factory’

•Service providers and components manufacturers have to evolve too in order to develop effective relationships with producers focusing more on true results delivery (price effectiveness and technology innovation)