Embed Size (px)

Citation preview

Session 03

Project Appraisals

Programme : Executive Diploma in Accounting, Business & Strategy

(EDABS 2017)

Course : Corporate Financial Management (EDABS 202)

Lecturer : Mr. Asanka Ranasinghe

MBA (Colombo), BBA (Finance), ACMA, CGMA

Contact : [email protected]

Learning Outcomes

• Identify and apply relevant and incremental cash flows in net

present value calculations

• Recognise and deal with sunk costs, incidental costs and

allocated overheads

• The replacement decision/the replacement cycle

• The calculation of annual equivalent annuities

• The make or buy decision

• Optimal timing of investment

• Fluctuating output situations

Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA2

Project Cashflows

• Cash (not accounting income) flows

• Operating (not financing) flows

• After-tax flows

• Incremental flows

• Ignore sunk costs

• Include opportunity costs

• Include project-driven changes in working capital net of

spontaneous changes in current liabilities

• Include effects of inflation

Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA3

Depreciation

4Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA

Depreciation represents the systematic allocation of the cost of a

capital asset over a period of time for financial reporting purposes,

tax purposes, or both.

Accounting profit is calculated after deducting depreciation

Depreciation should not be deducted to calculate net cash inflows

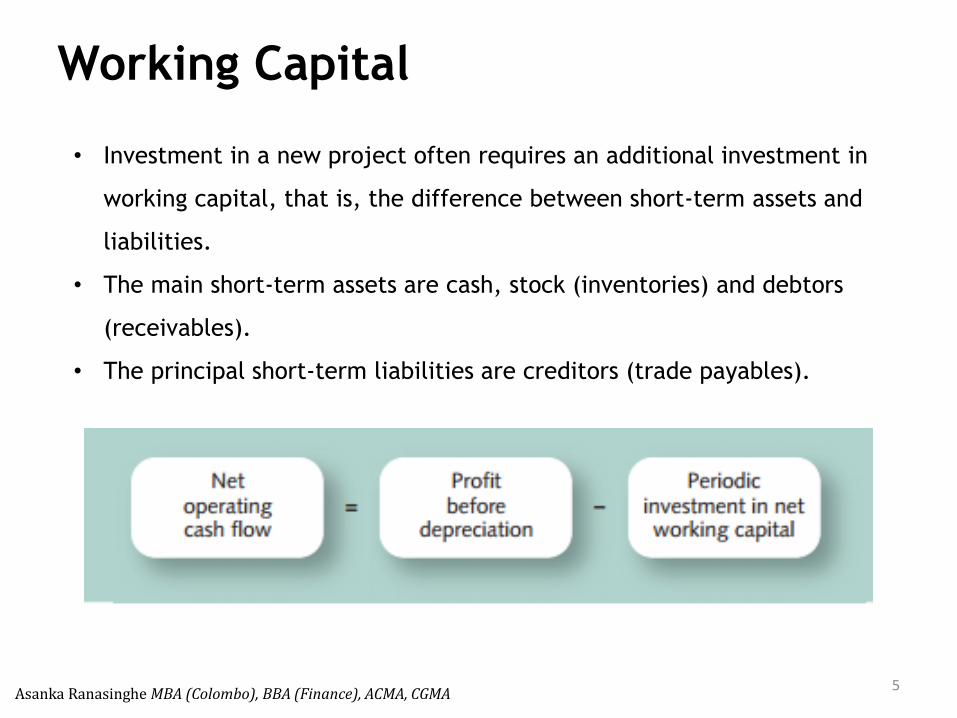

Working Capital

5Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA

• Investment in a new project often requires an additional investment in

working capital, that is, the difference between short-term assets and

liabilities.

• The main short-term assets are cash, stock (inventories) and debtors

(receivables).

• The principal short-term liabilities are creditors (trade payables).

Incremental Cash flows

6Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA

Three steps are involved in the evaluation of an investment:

• Estimation of cash flows

• Estimation of the required rate of return (the opportunity cost

of capital)

• Application of a decision rule for making the choice

Asset Replacement

7Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA

In making a replacement decision the increased costs associated

with the purchase and installation of the new machine have to be

weighed against the savings from switching to the new method of

production.

Replacement Cycles :

Depending on the comparison between the benefit to be derived by

delaying the replacement decision (that is, the postponed cash

outflow associated with the purchase of new assets) and the cost in

terms of higher maintenance costs (and lower secondhand value

achieved with the sale of the used asset).

Annual Equivalent Annuities

8Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA

Suppose the firm Brrum has to decide between two machines, A and B, to

replace an old worn-out one. Whichever new machine is chosen it will be

replaced on a regular cycle. Both machines produce the same level of output.

Because they produce exactly the same output we do not need to examine

the cash inflows at all to choose between the machines; we can concentrate

solely on establishing the lower-cost machine. Assume cost of capital of 6%.

Brrum plc

• Machine A costs £30m, lasts three years and costs £8m a year to run

• Machine B costs £20m, lasts two years and costs £12m a year to run

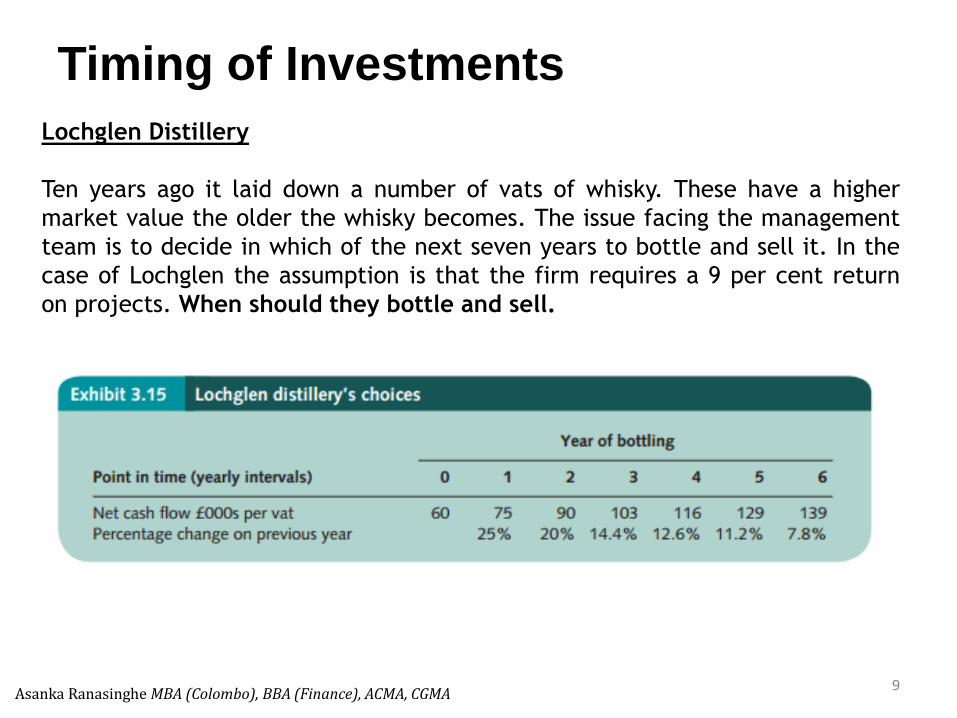

Timing of Investments

9Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA

Lochglen Distillery

Ten years ago it laid down a number of vats of whisky. These have a higher

market value the older the whisky becomes. The issue facing the management

team is to decide in which of the next seven years to bottle and sell it. In the

case of Lochglen the assumption is that the firm requires a 9 per cent return

on projects. When should they bottle and sell.

Make or Buy Decision

10Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA

We need to establish the difference between the costs of set-up and

production in-house and the costs of purchase.

Davis and Davies were to produce their own ‘eyes’ they would have to spend

£40,000 immediately on machinery, setting up and training. The machinery

will have a life of four years and the annual cost of production of 100,000

sets will be £80,000, £85,000, £92,000 and £100,000 respectively. The cost of

bought-in components is not expected to remain at £1 per set. The more

realistic estimates are £105,000 for year 1, followed by £120,000, £128,000

and £132,000 for years 2 to 4 respectively, for 100,000 sets per year. The new

machinery will be installed in an empty factory the open market rental value

of which is £20,000 per annum and the firm’s cost of capital is 11 per cent.

Fluctuating Output

11Asanka Ranasinghe MBA (Colombo), BBA (Finance), ACMA, CGMA

A Potato Sorting Company, which grades and bags potatoes in terms of size

and quality. During the summer and autumn its two machines work at full

capacity, which is the equivalent of 20,000 bags per machine per year.

However, in the six months of the winter and spring the machines work at

half capacity because fewer home grown potatoes need to be sorted. The

operating cost of the machine per bag is 20 pence. The machines were

installed over 50 years ago and can be regarded as still having a very long

productive life. Despite this they have no secondhand value because

modern machines called Fastsort now dominate the market. Fastsort has

an identical capacity to the old machine but its running cost is only 10

pence per bag. These machines are also expected to be productive

indefinitely, but they cost £12,000 each to purchase and install. The new

production manager is keen on getting rid of the two old machines and

replacing them with two Fastsort machines.

Cost of capital of 10 per cent.

Asanka Ranasinghe BBA (Finance), ACMA, CGMA12