Embed Size (px)

Citation preview

Investor presentation September 2017

CONTENT

p.3 THE PROMOTERS

p .5 Spactiv

p .8 Promoters’ Track Record

p.11 Key Terms and Investor Return Profile

APPENDIX

p.17 Details on Promoters’ Profiles

p .25 SPAC: General Overview

3 Strictly private and confidential

THE PROMOTERS

2006 – to date: Founding Partner of

Borletti Group

2016 – to date: Chairman

and leading investor in Grandi Stazioni

2006 – 2013: Honorary Chairman and

leading investor in Printemps

2006 – 2012: Member of Steering

Committee of EuroCommerce,

Board of Federdistribuzione

2005 – 2011: Chairman and leading

investor in laRinascente

1994 – 2000: Owner and CEO of Christofle

2006 – to date: Founding Partner of

Borletti Group; Board member of

Printemps, Grandi Stazioni Retail,

Highstreet

2002 – 2006: CEO of Ungaro,

senior manager at Ferragamo

1999 – 2002: Founder and CEO of

international food retail chain

1988 – 1998: M&A advisor with

Deutsche Bank

2016 – to date: Founder and Managing

Director of Milano Capital

2014 – 2016: Managing Director at Idea

Capital Funds; Board member of

La Piadineria

2007 – 2014: Partner at McKinsey&Co.

1997 – 2007: Strategy consultant at

McKinsey&Co.; M&A Advisor with

Morgan Stanley

MAURIZIO BORLETTI PAOLO DE SPIRT GABRIELE BAVAGNOLI

BORLETTI GROUP is a privately-owned investment group with offices in London and

Luxembourg. Borletti Group’s Private Equity division is a team of successful managers with

entrepreneurial, industrial and financial backgrounds. Over the last 12 years, it has led or co-led

successful transactions for a total amount of over € 7 bn.

MILANO CAPITAL combines Principal

Investing and Strategic Advisory and

operates alongside leading Italian and

international Private Equity investors.

CONTENT

p.3 The Promoters

p .5 SPACTIV

p .8 Promoters’ Track Record

p.11 Key Terms and Investor Return Profile

APPENDIX

p.17 Details on Promoters’ Profiles

p .25 SPAC: General Overview

5 Strictly private and

confidential

SPACTIV - Transaction Highlights

An Italian or permanently established in Italy (PIR-compliant) mid-cap company, with high

growth potential; Equity Value indicatively between €100m and €400m

Qualified minority or majority investment in shares

Industry focus (not exclusive) on Lifestyle : Food, Fashion, Design, Other Consumer

Goods, Health care, Wellness, Tourism. Whole industry value chain: manufacturing, retail,

services

To fund Spactiv, a SPAC that will merge with an Italian or permanently established in Italy

(anyhow PIR-compliant) mid-cap company, with high growth potential

Spactiv S.p.A., a joint-stock company under the Italian Law

Maurizio Borletti, Paolo De Spirt, Gabriele Bavagnoli

Objective1: €60m - €80m

THE OPPORTUNITY

ISSUER

PROMOTERS

SIZE

TARGET

PROMOTERS’ FUNDS

TIMING

MARKET

SYNDICATE

AIM Italia - Italian Stock Exchange

Global Coordinators & Joint Bookrunners: Mediobanca, UBI Banca.

Nomad and Specialist: UBI Banca

Special Shares (convertible into Ordinary Shares) subscribed by Promoters for an

amount of €2.5 - €3.0m, depending on the final offer size

Second Half of 2017

1 up to a maximum of €100 m

•

•

•

6 Strictly private and confidential

SPACTIV – Key Distinctiveness

1 4

+ 2

3

Experienced team with proven

Private Equity, M&A, and Value

Creation track-record and years

of fruitful collaboration

Proprietary deal flow focused on

Lifestyle industries, constituting an

Italian excellence, with strong growth

fundamentals

Active approach to value

creation, in line with Promoters’

track record

• Family-owned business background,

with longstanding exposure to typical

family- business issues.

• Strong personal network and

operational experience, underpinning

value creation capabilities.

• Italian roots coupled with international

footprint and track record, implying

ability to serve as catalysts for

international expansion.

• Modus Operandi based on supporting

and empowering entrepreneurs and

management teams while keeping

proper “investor distance”.

Promoters’ appeal for Italian

entrepreneurs

CONTENT

p.3 The Promoters

p .5 Spactiv

p .8 PROMOTERS’ TRACK RECORD

p.11 Key Terms and Investor Return Profile

APPENDIX

p.17 Details on Promoters’ Profiles

p .25 SPAC: General Overview

8 Strictly private and confidential

BORLETTI GROUP - Track Record

1 Combined equity returns. 2 Real Estate.

3 Start up

Over the last 12 years, the Borletti Group has led or co-led five acquisitions for a total

invested capital of over €7bn

ACQUISITION

DATE

EXIT

YEARS COMPANY

ENTERPRISE

VALUE RETURNS

2005 2011

(IT)

€0.8bn

> 5x MoM1

2006

2013

(FR)

€0.9bn

2008

CURRENT

(DE)

€4.5bn2

CURRENT

2016

CURRENT

€1.0bn

CURRENT

2017 CURRENT

(SM) tbd3 ONGOING

(IT)

9 Strictly private and confidential

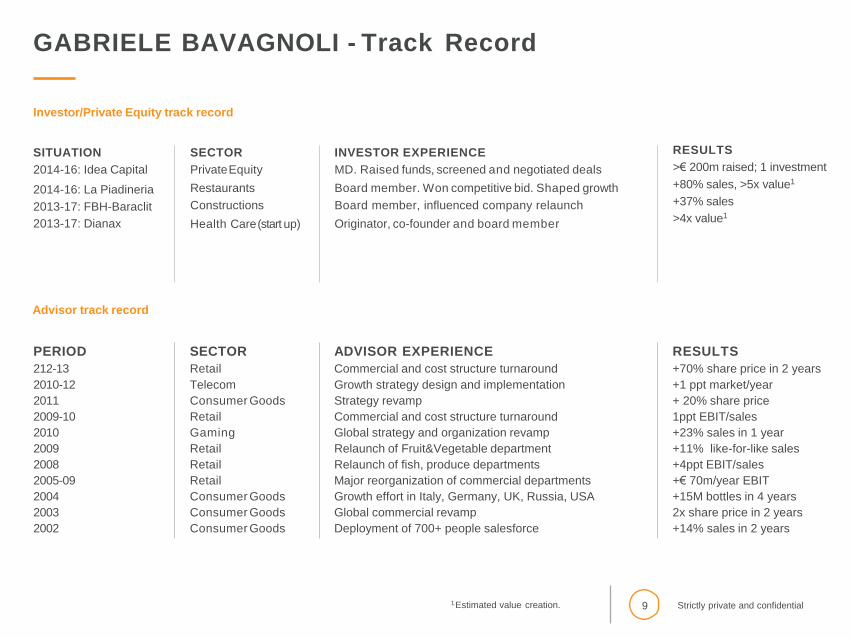

GABRIELE BAVAGNOLI - Track Record

1. Estimated value creation.

Investor/Private Equity track record

SITUATION

2014-16: Idea Capital

2014-16: La Piadineria

2013-17: FBH-Baraclit

2013-17: Dianax

SECTOR

Private Equity

Restaurants

Constructions

Health Care (start up)

RESULTS

>€ 200m raised; 1 investment

+80% sales, >5x value1

+37% sales

>4x value1

INVESTOR EXPERIENCE

MD. Raised funds, screened and negotiated deals

Board member. Won competitive bid. Shaped growth

Board member, influenced company relaunch

Originator, co-founder and board member

Advisor track record

PERIOD SECTOR ADVISOR EXPERIENCE RESULTS

212-13 Retail Commercial and cost structure turnaround +70% share price in 2 years

2010-12 Telecom Growth strategy design and implementation +1 ppt market/year

2011 Consumer Goods Strategy revamp + 20% share price

2009-10 Retail Commercial and cost structure turnaround 1ppt EBIT/sales

2010 Gaming Global strategy and organization revamp +23% sales in 1 year

2009 Retail Relaunch of Fruit&Vegetable department +11% like-for-like sales

2008 Retail Relaunch of fish, produce departments +4ppt EBIT/sales

2005-09 Retail Major reorganization of commercial departments +€ 70m/year EBIT

2004 Consumer Goods Growth effort in Italy, Germany, UK, Russia, USA +15M bottles in 4 years

2003 Consumer Goods Global commercial revamp 2x share price in 2 years

2002 Consumer Goods Deployment of 700+ people salesforce +14% sales in 2 years

CONTENT

p.3 The Promoters

p .5 Spactiv

p .8 Promoters’ Track Record

p.11 KEY TERMS AND INVESTOR RETURN PROFILE

APPENDIX

p.17 Details on Promoters’ Profiles

p .25 SPAC: General Overview

11 Strictly private and confidential

SPACTIV - Head of Terms 1 / 2

ISSUER

PROMOTERS

OFFER SIZE

INVESTMENT

FEATURES

WARRANTS

TARGET

MARKET

• Spactiv S.p.A. a joint-stock company under the Italian Law

• Maurizio Borletti, Paolo De Spirt, Gabriele Bavagnoli

• Objective1: €60m - €80m

• 6 - 8m2 A Shares at € 10 per share

• 2 free Warrants each 10 A Shares at the IPO; 3 free Warrants each 10 A Shares at the Business

Combination for Investors who do not exercise their withdrawal rights

• Virtually cashless conversion (€ 0.10 per new share). Each warrant entitles investors to receive a formula-

based3 number of new Ordinary Shares in the combined entity at a Strike Price of € 9.50

• Warrants to be exercised within 5 years from the Business Combination

• Compulsory conversion when Ordinary Share price equals or exceeds € 13.304

• An Italian or permanently established in Italy (PIR-compliant) mid-cap company, with high growth potential;

Equity Value indicatively between €100m and €400m

• Qualified minority or majority investment in shares

• Industry focus (not exclusive) on Lifestyle sectors: Food, Fashion, Design, Other Consumer Goods,

Health care, Wellness, Tourism. Whole value chain: manufacturing, distribution, services.

• Excluded sectors: Banking, Energy, Real Estate

• Excluded deal types: start-ups and financial turnarounds (i.e. “procedure concorsuali”)

• Transaction: merger, share purchase, share capital increase or similar transactions

• AIM Italia – Italian Stock Exchange, with the objective of listing on the main market (MTA or STAR

Segment) shortly after Business Combination

1 up to a maximum of € 100m 2 up to maximum of 10m, depending on the size of the offer 3 Formula: number of new shares per warrant = (avg. monthly share price

– strike price) / (avg. monthly share price – share subscription price)

4 In the event that the official price of the ordinary

shares traded for at least 15 days out of 30 days of

consecutive open stock market is greater or equal

than € 13.30

12 Strictly private and confidential

SPACTIV - Head of Terms 2 / 2

TIMEFRAME

INVESTOR

PROTECTION

PROMOTERS’

SHARES

PROMOTERS’

LOCK-UP

24 months from the IPO to approve the Business Combination5

100% of investors’ proceeds are placed into an escrow account

After use of promoters’ funds and interests on proceeds, up to 1% of proceeds, subject to BoD resolution,

may be used to finance working capital requirements of the SPAC

Withdrawal right for investors who do not attend the shareholders meeting called to resolve upon the

Business Combination, abstain or vote against.

Investors who exercise the withdrawal right at the time of the Business Combination will receive the pro-quota net

asset value of the company represented by their shares

The Business Combination will take place only if the net cash out to serve withdrawals

does not exceed 30% of the amount raised in the offer

In case of liquidation, proceeds will be allocated only to Investors until they receive at least 99%

of their invested capital. Promoters start to receive their pro-quota of proceeds only thereafter.

For conversions of Special Shares (i), (ii) and (iii), 12 months after each conversion, up to 4 years after the

Business Combination

•

•

•

•

•

•

•

• €2.5 - €3.0m, depending on the final size of the offer

• Up to 300.000 Class – B Shares:

•

- reserved to Promoters, non-listed, subordinated, not voting for Business Combination and non-

transferrable; entitled with certain veto rights and with the right to appoint BoD members with certain

veto rights

- issued at €10 per share and fully paid upfront;

- convertible into Class – A Shares at a 1 to 6 ratio: (i) 35% at Business Combination, (ii) 25% when share

price reaches €11.006, (iii) 20% when share price reaches €12.006, (iv) 20% when share price reaches

€13.306 within a period of 36 months from the effective date of the Business Combination. In case the share

price reaches €13.306 within a period of 36 months, the last 20% of B Shares will be converted in A Shares at

the 48th month from Business Combination. After that, any remaining class - A shares will then be converted

into class - B, at 1 to 1 ratio.

5 The duration will be extended for other 6 months if an

agreement on the Business Combination is reached and

communicated within 24 months

6 In the event that the official price of the ordinary shares traded

for at least 15 days out of 30 days of consecutive open stock

market is greater or equal than € 11, € 12 and € 13.30

13 Strictly private and confidential

SPACTIV – Illustrative Potential Investor Returns - 1 / 2

Solely for illustration purposes. This chart is not a representation or warranty of future return prospects,

which could be different from what shown below. Accordingly, no reliance should be placed on the illustration

below and recipients of this presentation must make their own independent analysis and calculations.

3 additional warrants

to existing shareholders

every 10 Ordinary Shares 35% of Class – B Shares

converted into Class –

A Shares

Investor return: 17,5% (assuming the exercise of all market warrants; excluding additional return from dividend)

Investor return: 52,0% (assuming the exercise of all market warrants; excluding additional return from dividend)

12

16

15

14

13

10

0

@€11

25% of Class - B Shares

converted into Class -

A Shares

@€12

20% of Class - B Shares

converted into Class - A

Shares

@€13,3

Compulsory conversion of

warrants into Ordinary

shares and 20% of Class -

B Shares converted

into Class - A Shares

Price per Share (€)

Assumption

Timeline

•

•

@ BUSINESS

COMBINATION

Investor return: 32,5% (assuming the exercise of all market warrants; excluding additional return from dividend)

14 Strictly private and confidential

SPACTIV – Illustrative Potential Investor Returns - 2 / 2

“Cashless” warrants may leverage investors’ return

FORMULA =

FORMULA

COMPUTATION

RETURN ON

100€1

INVESTMENT

PERCENTAGE

RETURN

AVG. MONTHLY SHARE

PRICE = €11

1.376 NEW SHARES

EACH

10.000 WARRANT

2.101 NEW SHARES

EACH

10.000 WARRANT

2.879 NEW SHARES

EACH 10.000 WARRANT

AVG. MONTHLY SHARE

PRICE = €12

AVG. MONTHLY SHARE

PRICE = €13,3

Avg. Monthly Share Price - Strike Price (€9,50)

Avg. Monthly Share Price - Share Subscription Price (€0,1)

€ 10*(11-10)+5*0,1376*(11- 0,1) =

= €17,50

€ 10*(12-10)+5*0,2101*(12-0,1) =

= €32,50

€ 10*(13,3-10)+5*0,2879*(13,3-0,1) =

= € 52,00

17,5% 32,5% 52,0%

1 Assuming 2 warrants each 10 Class – A Shares at the IPO and 3 warrants each 10 Class – A

Shares post Business Combination, for a total of 5 warrants each 10 Class – A Shares.

€11-9,50 =

€1,5

€11 - €0,1 €10,9 =

0,1376 new shares

from each warrant

€12-€9,50 €2,5

€12 - €0,1 €11,9 =

0,2101 new shares

from each warrant

=

€13,3-9,50 =

€3,8

€13,3 - €0,1 €13,2 =

0,2879 new shares

from each warrant

15 Strictly private and confidential

SPACTIV’S LIQUIDATION SCHEME

In case of liquidation of Spactiv, the net proceeds will be

allocated as follows:

Initially, funds will be allocated only to Investors (and

not to Promoters) until they receive 99% of the amount

they provided in the IPO to subscribe class – A shares;

Then, if any cash or other assets still remain, Promoters

will receive up to 99% of the amount they provided to

subscribe class - B shares;

Finally, any remaining cash or other assets will

be allocated among Investors and Promoters,

according to the share of capital owned.

HYPOTHESES

Investors’ Fund

€80.000.000

1,0%

€80.800.000

Funds at IPO

R e t u r n o n

f u n d s 1

Funds with accrued

interest

0 , 0 %

€3.000.000

Investors’ Funds

€3.000.000

Total Funds

€83.800.000

Scenario 1

Total Cost

€1 . 0 0 0 . 0 0 0

€82.800.000

€79.807.229

€2.992.771

Scenario 1

Total Cost € 3 . 0 0 0 . 0 0 0

€80.800.000

€79.200.229

€1.600.000

Scenario 1

Total Cost € 3 . 8 0 0 . 0 0 0

€80.800.000

€79.200.000

€800.000

99%2

€80.000.000

99% x €80.000.000

+

(80/83) x (€82.800.000-99% x

€83.000.000)

1 The hypothesis about the return on the escrow account (i.e. 1%) serves only for illustrative purposes. In any case, it cannot be

considered a proxy of the actual return on the escrow account.

2 In this illustrative example, in case of total costs or losses above € 4,6 mln (€3 mln +1 % of return on escrow account + 1% of investors’

fund utilization), investors’ proceeds at liquidation would be lower than 99% of the initial investment.

Total Fund at Liquidation

Investors’ Fund at Liquidation

Promoters’ Fund at Liquidation

•

•

•

CONTENT

p.3 The Promoters

p .5 Spactiv

p .8 Promoters’ Track Record

p.11 Key Terms and Investor Return Profile

APPENDIX

p.17 DETAILS ON PROMOTERS’ PROFILES

p .25 SPAC: General Overview

17 Strictly private and confidential

DETAILS ON PROMOTER PROFILE

MAURIZIO BORLETTI Founding Partner – Borletti Group

PAOLO DE SPIRT Founding Partner – Borletti Group

GABRIELE BAVAGNOLI Founder - Milano Capital

Experience and Management

Christofle, laRinascente, Printemps, Borletti

Family Office, Swedish Match

Board Membership

Altagamma, Comité Colbert,

Confcommercio, Confindustria,

EuroCommerce, Federdistribuzione IADS,

IGDS, Grandi Stazioni Retail, Santa

Margherita, The Market

Education

Bocconi University

Experience and Management

Grandi Stazioni Retail, Printemps, Ungaro,

Ferragamo, Dunkin’ Donuts, Deutsche

Bank, Morgan Grenfell

Board Membership

Grandi Stazioni Retail, Printemps,

Highstreet, Borletti Group,

S&C Germany

Advisory

Sanson, Benetton, Prenatal, Mannesman,

Perini, Ducati, Lamborghini

Education

University of Buckingham

Experience and Management

McKinsey & Company, Milano Capital, Idea

Capital, Morgan Stanley

Board Membership

FBH, Gruppo La Piadineria, ToI Uno, Dianax

Advisory

Several global industrial groups and

financial investors

Education

Politecnico Milano, Columbia University

18 Strictly private and confidential

MAURIZIO BORLETTI

Since the creation of the Borletti Group, Maurizio

has been active together with Paolo De Spirt in

building its team, sourcing and analysing

investment opportunities.

In 2016, he participated to the acquisition of

Grandi Stazioni Retail, in which he currently

serves as Chairman.

Maurizio has been involved in the target industries

for over 20 years, holding board memberships of

organisations such as Federdistribuzione (Italian

Multiple Retailers’ Association), EuroCommerce

(European Association of Retailers), IADS and IGDS

(the two major department store associations),

Comité Colbert (premium brands association in

France), Altagamma (premium brands association in

Italy), Logo International (O’Neill, WE, van Gils

brands), Santa Margherita (wines), Inalternative SGR

(Fund of Hedge Funds) and Confindustria

(Confederation of Italian industrial companies).

In 2006, he was lead investor in the acquisition of

Printemps, where he served as Honorary Chairman

until 2013.

In 2005, Maurizio founded Borletti Group: an

independent investment firm focused on

Private Equity. He also promoted and

participated as investor to the consortium for

the acquisition of laRinascente where he

served as Chairman between 2005 and 2011,

when it was successfully divested.

In 1993, he left Amministrazione Borletti - one of the

oldest and most relevant Italian family offices

founded in 1865 - to acquire the French luxury

company Christofle, where he led the company

turnaround as CEO until 2003.

During his academic years, he founded three

successive start ups and in 1989 he succeeded

his late father in Amministrazione Borletti.

He reorganised its holdings and in 1991 and

pursued his first take-over as part of the

consortium purchaser of Swedish Match.

Maurizio graduated from Bocconi University with a

post-graduate academic experience in Japan. He is

fluent in Italian, English, French, Spanish and

Portuguese.

19 Strictly private and confidential

PAOLO DE SPIRT

Paolo co-founded Borletti Group where he has

been active in deal sourcing, in managing the

acquisition processes and in monitoring

investments.

In 2016, he participated to the acquisition of

Grandi Stazioni Retail, in which he serves as

Board member.

In 2006, he participated to the acquisition of

Printemps in France and of Highstreet

(Karstadt’s real estate portfolio) in Germany.

He has been a board member of Printemps

since 2006 and served as board member in

Highstreet from 2006 to 2011.

In 2003, he was asked by Ferragamo to

restructure and divest the Luxury ready-to-

wear brand Emmanuel Ungaro, where he

served as CEO until its sale in 2006.

In 2002, he joined the Ferragamo Family

holding company where he served as Group

Business Development Director at Salvatore Ferragamo.

In 1999, he left investment banking to found

Dunkin’ Donuts Germany & Italy (franchise of

the US company). He was CEO until 2002 and

then served as Chairman from 2002 to

2008. He was backed in his venture by private

investors and major hedge funds.

Paolo started his career as an investment banker

at Deutsche Bank where he grew to the position

of Director. He worked on key assignments with

Audi/Lamborghini, TPG/ Ducati, Roeber/Perini,

Artsana/Prenatal, Benetton, Del Vecchio/Sanson

Beatrice Foods, Ansaldo, Mannesman/Olivetti.

Paolo pursued his studies in Italy and the

United kingdom. He is a graduate from the

University of Buckingham. He is fluent in

Italian, English, German, and French.

20 Strictly private and confidential

GABRIELE BAVAGNOLI

Gabriele is Founder and Managing Director of

Milano Capital, combining Principal Investing and

Strategic Advisory and working alongside large

Italian and international Private Equity firms. He

has been cooperating with Maurizio Borletti and

Paolo De Spirt since Borletti Group’s acquisition of

Grandi Stazioni Retail.

From 2014 to 2016 he was Managing Director at

Idea Capital – a leading Italian Private Equity Firm

with more than € 1.5b assets under management –

where he co-led the creation of a € 200+ m Private

Equity Fund focused on Food & Beverage, and

carried out the leveraged buy-out of Gruppo La

Piadineria, a fast-growing restaurant chain, in

which he served as Board member.

From 1997 to 2014 he has been at McKinsey &

Company, where he became Partner in the

Milan Office and shareholder of the firm in 2007

and served as co-Chairman of the

Knowledge Committee of the Europe Middle East

and Africa Consumer Practice.

Within McKinsey, he advised global Retail,

Consumer Goods and Telecom groups in Italy,

UK, US, the Netherlands, Eastern Europe, and

Egypt on strategy, finance, and commercial

topics, with a focus on boosting top-line growth.

He also advised several Private Equity firms in

due diligence and portfolio work.

He is board member and shareholder at FBH,

leading Italian manufacturer of prefabricated

buildings and of Dianax, a Biotech company he

co-founded in 2013.

He holds a Master of Business Administration

from Columbia University, New York, and a

Laurea cum laude in Management Engineering

from Politecnico di Milano.

21 Strictly private and confidential

BORLETTI GROUP –

laRinascente

BACKGROUND

March 2005: Acquisition of laRinascente from IFIL / Auchan

Leading Italian department store with over €300m sales,

5,500 employees and a prime real estate portfolio

Competitive auction with over 35 participants

Borletti Group’s equity partners: Deutsche Bank, Pirelli,

Investitori Associati

2005-2011: successful repositioning of the store chain through

revamping of the stores, with major investments and product

category reallocation

June 2011: Sale of laRinascente to Central Retail Corporation

(Thai retail group)

RESULTS

• Repositioning of the flagship stores and the group towards a

different brand strategy (unsuccessful own brands were replaced

by A-brands)

• Operational improvements:

Same Store Sales 4-year CAGR of +3.5% in a global

crisis context

Flagship store sales: +70%

EBITDA CAGR of 71%

+4 points increase in profitability

•

•

•

•

•

•

•

•

•

•

22 Strictly private and confidential

BORLETTI GROUP –

Printemps

•

•

October 2006: Acquisition of “Printemps” from PPR Group

Leading French department store chain with € 950m sales, over

5,000 employees and a prime real estate portfolio

Restricted acquisition process with only three participants

Borletti Group’s equity partner: Deutsche Bank.

2006-2013: Major investments to revamp the stores and

product category reallocation leading to a successful

repositioning of the group

July 2013: Sale of Printemps to a Qatari investor (sales having

reached €1.3bn)

Successful repositioning leading to a significant increase in

sales productivity per sqm

Operational improvements:

• Same Store Sales 5-year CAGR of +4% in a global crisis

context

• Flagship store sales: +43%

• +3 points increase in profitability

• EBITDAR CAGR of +10%

BACKGROUND

RESULTS

•

•

•

•

•

•

23 Strictly private and confidential

BORLETTI GROUP –

Grandi Stazioni Retail

In early 2015, the shareholders of Grandi Stazioni decided to

demerge retail activities from facility management and

transport-related services.

The concession on the retail activities has been transferred into a

new company, Grandi Stazioni Retail, to be sold through a auction

process

In September 2015, the auction started and BG with 2 partners

(Antin and ICAMAP), decided to participate as a Consortium

In June 2016, Grandi Stazioni Retail has been awarded to the

Consortium, for an enterprise value of €953m

Concession expiration: 20401

Stations: 14 of the largest Italian train stations: Roma Termini, Roma

Tiburtina, Milano Centrale, Torino Porta Nuova, Genova Principe,

Genova Brignole, Verona Porta Nuova, Venezia Mestre, Venezia

Santa Lucia, Bologna Centrale, Firenze Santa Maria Novella, Napoli

Centrale, Bari centrale, Palermo Centrale.

Visitors ’14:750m

Leased areas ’14: ~ 95k sqm

•

•

•

•

•

•

•

•

BACKGROUND

RESULTS

CONTENT

p.3 The Promoters

p .5 Spactiv

p .8 Promoters’ Track Record

p.11 Key Terms and Investor Return Profile

APPENDIX

p.17 Details On Promoters’ Profiles

p .25 SPAC: GENERAL OVERVIEW

25 Strictly private and confidential

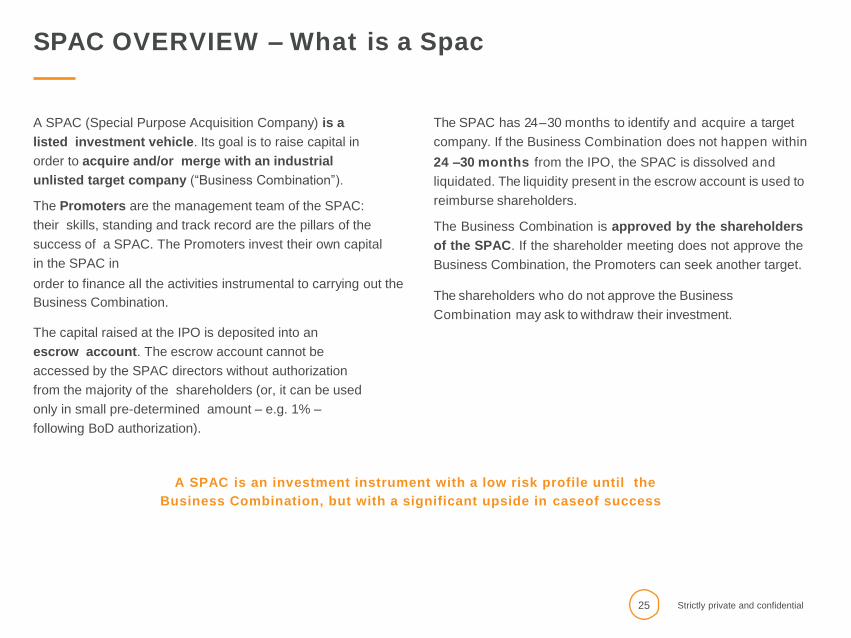

SPAC OVERVIEW – What is a Spac

A SPAC (Special Purpose Acquisition Company) is a

listed investment vehicle. Its goal is to raise capital in

order to acquire and/or merge with an industrial

unlisted target company (“Business Combination”).

The Promoters are the management team of the SPAC:

their skills, standing and track record are the pillars of the

success of a SPAC. The Promoters invest their own capital

in the SPAC in

order to finance all the activities instrumental to carrying out the

Business Combination.

The capital raised at the IPO is deposited into an

escrow account. The escrow account cannot be

accessed by the SPAC directors without authorization

from the majority of the shareholders (or, it can be used

only in small pre-determined amount – e.g. 1% –

following BoD authorization).

The SPAC has 24 – 30 months to identify and acquire a target

company. If the Business Combination does not happen within

24 –30 months from the IPO, the SPAC is dissolved and

liquidated. The liquidity present in the escrow account is used to

reimburse shareholders.

The Business Combination is approved by the shareholders

of the SPAC. If the shareholder meeting does not approve the

Business Combination, the Promoters can seek another target.

The shareholders who do not approve the Business

Combination may ask to withdraw their investment.

A SPAC is an investment instrument with a low risk profile until the

Business Combination, but with a significant upside in caseof success

26 Strictly private and confidential

SPAC OVERVIEW – Italian Mid Caps and Spacs

ITALY HAS MANY

SUCCESSFUL

MID-CAP COMPANIES

Italy has many successful, privately-owned, mid-size companies. Several of them are

champions in profitable, export-driven markets: from Apparel to Food, from Pharma to

Mechanical Manufacturing, from Automotive to Sustainable Energy.

They often combine agility with technical excellence, superior design with deep understanding of

the needs of their customers. In many cases, they dominate global niche markets.

•

•

SPACS ARE THE

SIMPLEST AND

MOST CERTAIN

ROUTE TO

LISTING FOR MID-

CAP COMPANIES

• Family-owned mid-caps are looking at SPACs with increasing interest as a way to list their

shares and raise capital, since a transaction with a SPAC minimizes the time, burden and

uncertainties of listing. They particularly appreciate the fact that the valuation is negotiated with

Promoters, not the result of an uncertain fundraising process.

• Also, SPACs are often seen as more entrepreneur-friendly than private equity funds, since

SPACs do not require the entrepreneurs to give up control, neither immediately nor in 5 years,

as PE funds typically require.

SPACS

CONSTITUTE AN

OPPORTUNITY

FOR INVESTORS

As a result of all of the above, SPACs offer investors the opportunity to acquire equity interests

in attractive Italian mid-size companies.

As of today, the return on Italian SPACs have been consistently attractive

•

•

27 Strictly private and confidential

SPAC OVERVIEW – Pros for Spac Investors

INVESTOR AT

THE CENTRE

ACCESS TO AN

EXPERIENCED

AND COMMITTED

TEAM

LIQUIDITY OF THE

INVESTIMENT

WITHDRAWAL

RIGHTS AND

PROTECTION

SPACs place investors at the very center: shareholders are to be informed and vote on any

proposed merger, with the option to exit given to dissenting investors.

Investors benefit from the capabilities of a strong and committed team, with experience in the

selection and acquisition of non-listed companies.

The payoff for the Promoters is linked to the performance of the company post Business Combination.

Stocks and warrants of the SPAC trade on the stock market from the IPO; therefore, the investment

is liquid since the first day of trading.

Warrants give investors the chance to realise an extra upside on the investment.

Investors dissenting on the proposed business combination, can withdraw their investment, even if

the transaction is approved by the majority of shareholders and go through. Similarly, in case the SPAC

is unable to approve a transaction in two years, the company is liquidated and investors receive their

share of proceeds, protected in the escrow account.

28 Strictly private and confidential

SPAC OVERVIEW – Lifecycle of a Spac

SPAC

IPO

TARGET

SEARCH AND

NEGOTIATIONS

BUSINESS

COMBINATION

ANNOUNCEMENT

SHAREHOLDER

MEETING

APPROVAL

OF THE BUSINESS

COMBINATION

Business

Combination

(SPAC

shareholders

become

shareholders

of the target

company)

Reimbursement

to the SPAC

shareholders

of their quota

Reimbursement to shareholders of

the liquidity in the escrow account

BUSINESS

COMBINATION NOT

APPROVED

NO TRANSACTION

SPAC DISSOLUTION

Shareholders that voted YES or didn’t withdraw

New target search

Shareholders that voted NO and withdrew

24 - 30 month

Capital raise in

SPAC IPO

Promoters’

investment

Target search

Due diligence

Transaction

negotiations

Presentation of the

target company

Withdrawal right

for investors not

approving the

Business Combination

Shareholder

approval of

the Business

Combination

Minimum requirements for approval:

• Majority vote

• Cash outflow as a consequence of withdrawals accounting for less

than 30% of the amount raised in the IPO

In case the Business Combination is not approved, the Promoters can seek a

new target (within the time limit)

DISCLAMER

This document (the “Document”) has been prepared solely for information purposes; a limited number of copies of the Document have been made and are strictly reserved for the person to

whom they are addressed: for this reason the information contained herein is confidential and must not be used, in whole or in part, or disclosed to third parties or copied, distributed,

transmitted or reproduced.

The Document is aimed at (i) a selected and limited number of “qualified investors” as defined in art. 100 of D.Lgs. No. 58/1998 and art. 34-ter of Consob Regulation No. 11971/1999, with the

experience and know-how needed to adequately understand and evaluate the risks inherent in any potential investment in the project described in this Document (the “Project”) relating

to the above-mentioned Italian SPAC named “Spactiv” (Special Purpose Acquisition Company) (the “Company”); and (ii) a limited number of investors, other than those aforementioned

under point (i), who will be able to participate in the Project in such manner, in terms of quality and/or quantity, to let the Company be included in the cases of inapplicability of the

regulations relating to the offer of securities to the public set forth by the aforementioned regulations.

The description of the Project characteristics contained in the Document is not intended and does not constitute in any way an investment advice or a solicitation to purchase securities,

nor is it an offer, or invitation, or promotional message for the purchase, sale or underwriting by any person in any jurisdiction or country where such activities are unlawful or unauthorized

according to the applicable law or regulation, except for the exemptions provided for by the applicable laws.

The terms, data and information contained in the Document are subject to revision and update; the Company and , its Promoters and their consultants assume no responsibility for the

communication, in advance or subsequently, of such revisions and updates should they become necessary or opportune, nor for any damages that may result from improper use of the

information (including communications of revisions and updates) included in the Document.. Within the limits set forth by law, the Company, its Promoters, corporate executives,

managers, employees, and consultants make no statement, give no guarantee and assume no responsibility, express or implied, regarding the accuracy, the adequacy, completeness

and up to date nature of the information contained in the Document, nor regarding any possible error, omission, inaccuracy or oversight contained herein. All prices mentioned in the

Document are indicative and dependent upon market conditions and the terms are liable to change and completion in the final documentation. The document does not attempt to

describe all terms and conditions that will pertain to the proposed transaction nor does it set forth the specific phrasing to be used in the documentation.

The distribution of the Document and information on the Project may be subject to restrictions in certain jurisdictions. It is recommended that any potential investment decision regarding a possible investment in the Project be based on the formal offering documents prepared by the Company as part of

the listing of the Company shares on the AIM Italia /Mercato Alternativo del Capitale organized and managed by Borsa Italiana S.p.A and on the audit by the investors own independent

and professional financial, legal and fiscal advisers.

Any expected return from the Project is not guaranteed and is based on data shown in Euro. The Document may contain “forward-looking” information which is based upon

certain assumptions about future events or conditions and is intended only to illustrate hypothetical results under those assumptions (not all of which are specified herein).

Actual events or conditions are unlikely to be consistent with, and may differ materially from, those assumed. In addition, not all relevant events or conditions may have been considered

in developing such assumptions. Accordingly, actual results will vary and the variations may be material. Prospective investors should understand such assumptions and evaluate whether

they are appropriate for their purposes. Any data on past performance, modelling, scenario analysis or back-testing contained herein is no indication as to future performance. No

representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any modelling, scenario analysis or back- testing;. for investors

resident in EC countries that are not part of the Eurozone these returns can increase or decrease due to exchange rate movements.

The tax consequences of an investment depend on the individual circumstances of each investor and may be subject to change in the future; therefore, this Document may not be

considered to have been prepared in order to offer an opinion, legal advice or tax opinion regarding the possible tax consequences of the Project. Every prospective investor is invited to

evaluate any potential investment in the Project on the basis of independent accounting, fiscal and legal advice and should also obtain from its own financial advisors

analyses of the adequacy of the transaction, the risks, the protection and the cash flows associated with the transaction, insofar as such analyses are appropriate for ascertaining the risks

and benefits of the transaction.

Each prospective investor is responsible for its own evaluation that a potential investment in the Project described herein does not contravene the laws and regulations of the

country of residence of the investor and is also responsible for obtaining any prior authorization that might be required to make the investment.

Mediobanca – Banca di Credito Finanziario S.p.A. (“Mediobanca”) and UBI Banca S.p.A. (“Ubi Banca”) will act as a global coordinators and joint bookrunners in the context of the listing

of the Company shares on the AIM Italia /Mercato Alternativo del Capitale. Mediobanca and Ubi Banca are respectively the parent company of the Mediobanca Banking Group and

the Ubi Banca Group, the companies of which are involved in a wide range of financial transactions, both on a proprietary basis and on behalf of clients. It is possible that Mediobanca and

Ubi Banca, or any one of their subsidiaries or associate companies, or any one of the clients of Mediobanca or Ubi Banca or the Group headed up by them, may have entered into

agreements with or hold investments in, or may execute or have executed transactions, which could lead to a situation of potential conflict of interests vis-à-vis the transactions described in

the Document. Mediobanca and Ubi Banca declare that, in line with their policy for managing conflicts of interest, they have implemented appropriate measures to ensure that the risk of

conflicts of interests that may damage the client’s interest is properly managed, as required by Directive 2004/39/CE and the related second-level provisions and by the respective regulations

transposing and implementing such provisions in Italy.

Acceptance of delivery of the Document by the recipient constitutes acceptance of the terms and conditions set out in this Disclaimer.