Embed Size (px)

Citation preview

R.I.P brick & mortar retail? Not so fast

CRISIL Insight

September 2015

CRISIL Insight

2

Analytical Contacts

Anuj Sethi Director, CRISIL Ratings Email: [email protected] Amit Bhave Director, CRISIL Ratings Email: [email protected] Sushant Sarode Manager, CRISIL Ratings Email: [email protected] Aditya Nori Senior Analyst, CRISIL Ratings Email: [email protected]

3

R.I.P brick & mortar retail? Not so fast

Laser focus on profitability, revisiting strategies help organised retail do well But sales growth will moderate to 13-15% over the medium term as e-tailing explodes CRISIL sees credit quality of large retailers stable in the next 2-3 years

Cassandras would have us believe cut-throat competition from online retailers in a subdued macroeconomic environment would imperil organised brick & mortar (B&M; estimated revenues of ~Rs.2.4 trillion in fiscal 2015) rivals. That refrain, to paraphrase Mark Twain, seems exaggerated, if an analysis of the financials of 24 large B&M retailers in India – 18 of them rated by CRISIL – is any yardstick. Our study shows revenues have leaped at a very healthy 24% compound annual growth rate to Rs. 0.7 trillion in the last five years to fiscal 2015 for these two dozen retailers, despite the headwinds. That compares with about 60% for online retailers (estimated gross merchandise value of ~Rs.0.4 trillion in fiscal 2015), or e-tailers, driven by large discounts and shopping convenience. Just what is helping this club? Unprecedented, relentless focus on profitability, even if it means in some cases, a moderation in revenue growth. A combination of initiatives are being deployed to ensure improvement in operating efficiency – including exiting unviable product categories, rightsizing stores, increasing focus on private labels and undertaking cluster-based store expansion. Many are revisiting business strategy, which include adopting an omni-channel approach – which is about pushing both physical and online sales -- in an attempt to protect turf, focusing on Tier II and Tier III cities for expansion. What’s more, there is a considerable spurt in consolidation among these retailers as they look to use scale of operations and extent of reach to take on competition. All this has helped boost the resilience of CRISIL-rated large retailers to online retail and other external challenges, and led to improvements in their financial risk profiles. CRISIL believes this realignment of business model will continue over the medium term, helped along by an expected improvement in the macroeconomic environment. Prudent store addition and debt accretion, along with strong promoter support, are likely to help organised B&M retailers sustain credit quality.

CRISIL Insight

4

Realigning business model to take on competition

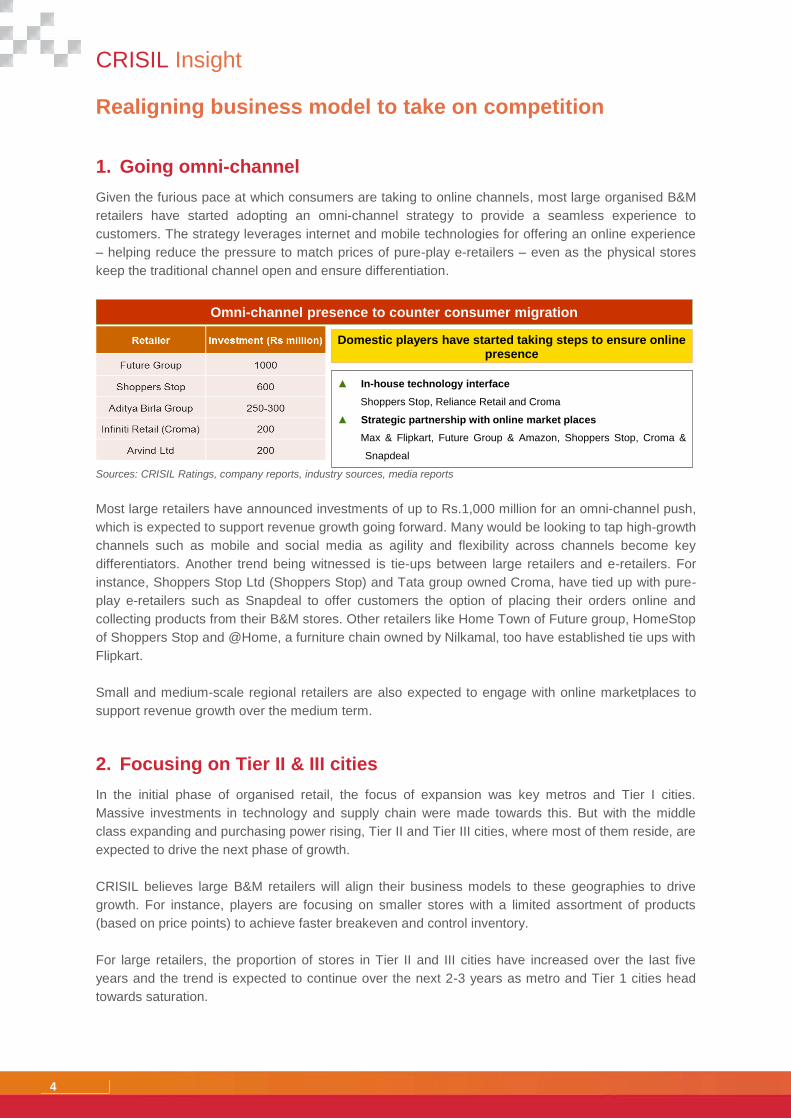

1. Going omni-channel Given the furious pace at which consumers are taking to online channels, most large organised B&M retailers have started adopting an omni-channel strategy to provide a seamless experience to customers. The strategy leverages internet and mobile technologies for offering an online experience – helping reduce the pressure to match prices of pure-play e-retailers – even as the physical stores keep the traditional channel open and ensure differentiation.

Sources: CRISIL Ratings, company reports, industry sources, media reports Most large retailers have announced investments of up to Rs.1,000 million for an omni-channel push, which is expected to support revenue growth going forward. Many would be looking to tap high-growth channels such as mobile and social media as agility and flexibility across channels become key differentiators. Another trend being witnessed is tie-ups between large retailers and e-retailers. For instance, Shoppers Stop Ltd (Shoppers Stop) and Tata group owned Croma, have tied up with pure-play e-retailers such as Snapdeal to offer customers the option of placing their orders online and collecting products from their B&M stores. Other retailers like Home Town of Future group, HomeStop of Shoppers Stop and @Home, a furniture chain owned by Nilkamal, too have established tie ups with Flipkart. Small and medium-scale regional retailers are also expected to engage with online marketplaces to support revenue growth over the medium term.

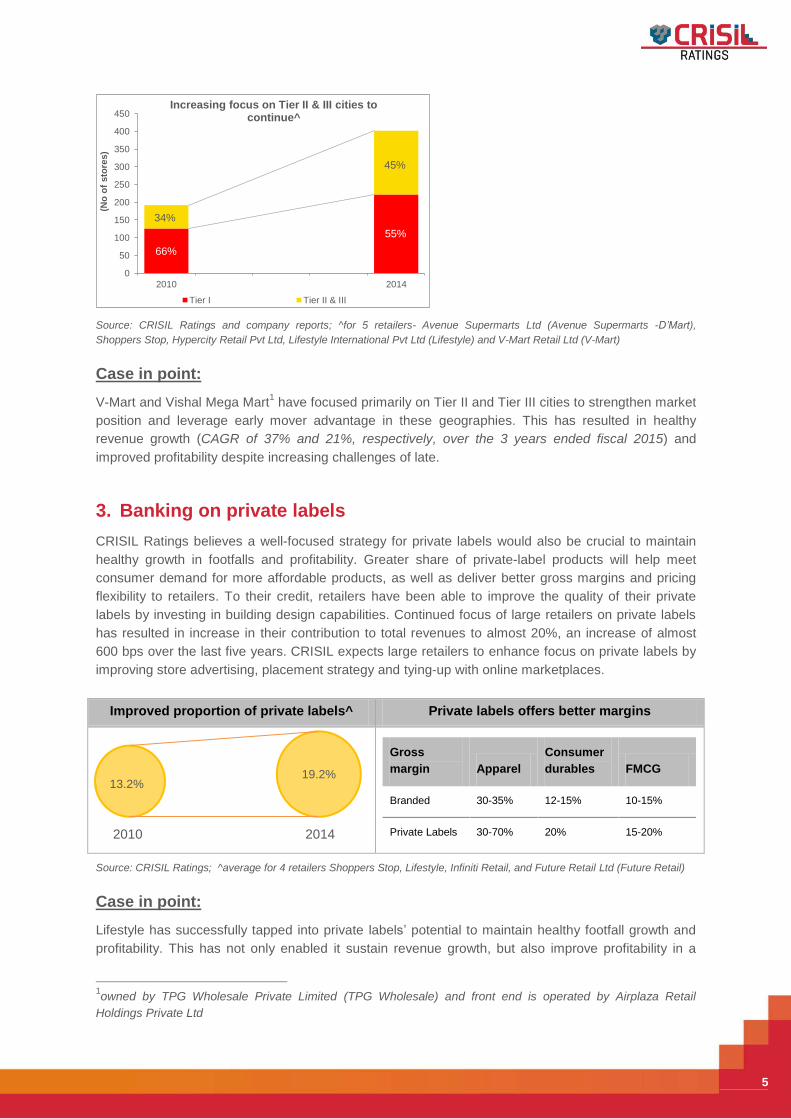

2. Focusing on Tier II & III cities In the initial phase of organised retail, the focus of expansion was key metros and Tier I cities. Massive investments in technology and supply chain were made towards this. But with the middle class expanding and purchasing power rising, Tier II and Tier III cities, where most of them reside, are expected to drive the next phase of growth. CRISIL believes large B&M retailers will align their business models to these geographies to drive growth. For instance, players are focusing on smaller stores with a limited assortment of products (based on price points) to achieve faster breakeven and control inventory. For large retailers, the proportion of stores in Tier II and III cities have increased over the last five years and the trend is expected to continue over the next 2-3 years as metro and Tier 1 cities head towards saturation.

Omni-channel presence to counter consumer migration

▲ In-house technology interfaceShoppers Stop, Reliance Retail and Croma

▲ Strategic partnership with online market placesMax & Flipkart, Future Group & Amazon, Shoppers Stop, Croma &

Snapdeal

Domestic players have started taking steps to ensure online presence

5

Source: CRISIL Ratings and company reports; ^for 5 retailers- Avenue Supermarts Ltd (Avenue Supermarts -D’Mart), Shoppers Stop, Hypercity Retail Pvt Ltd, Lifestyle International Pvt Ltd (Lifestyle) and V-Mart Retail Ltd (V-Mart)

Case in point: V-Mart and Vishal Mega Mart1 have focused primarily on Tier II and Tier III cities to strengthen market position and leverage early mover advantage in these geographies. This has resulted in healthy revenue growth (CAGR of 37% and 21%, respectively, over the 3 years ended fiscal 2015) and improved profitability despite increasing challenges of late.

3. Banking on private labels CRISIL Ratings believes a well-focused strategy for private labels would also be crucial to maintain healthy growth in footfalls and profitability. Greater share of private-label products will help meet consumer demand for more affordable products, as well as deliver better gross margins and pricing flexibility to retailers. To their credit, retailers have been able to improve the quality of their private labels by investing in building design capabilities. Continued focus of large retailers on private labels has resulted in increase in their contribution to total revenues to almost 20%, an increase of almost 600 bps over the last five years. CRISIL expects large retailers to enhance focus on private labels by improving store advertising, placement strategy and tying-up with online marketplaces.

Improved proportion of private labels^ Private labels offers better margins

2010 2014

Gross margin Apparel

Consumer durables FMCG

Branded 30-35% 12-15% 10-15%

Private Labels 30-70% 20% 15-20%

Source: CRISIL Ratings; ^average for 4 retailers Shoppers Stop, Lifestyle, Infiniti Retail, and Future Retail Ltd (Future Retail)

Case in point: Lifestyle has successfully tapped into private labels’ potential to maintain healthy footfall growth and profitability. This has not only enabled it sustain revenue growth, but also improve profitability in a

1owned by TPG Wholesale Private Limited (TPG Wholesale) and front end is operated by Airplaza Retail Holdings Private Ltd

0

50

100

150

200

250

300

350

400

450

2010 2014

(No

of s

tore

s)Increasing focus on Tier II & III cities to

continue^

Tier I Tier II & III

45%

55%66%

34%

19.2% 13.2%

CRISIL Insight

6

challenging environment. Moreover, Lifestyle is looking at private labels as an entry strategy for expanding into Tier II and Tier III markets where the average transaction size is lower.

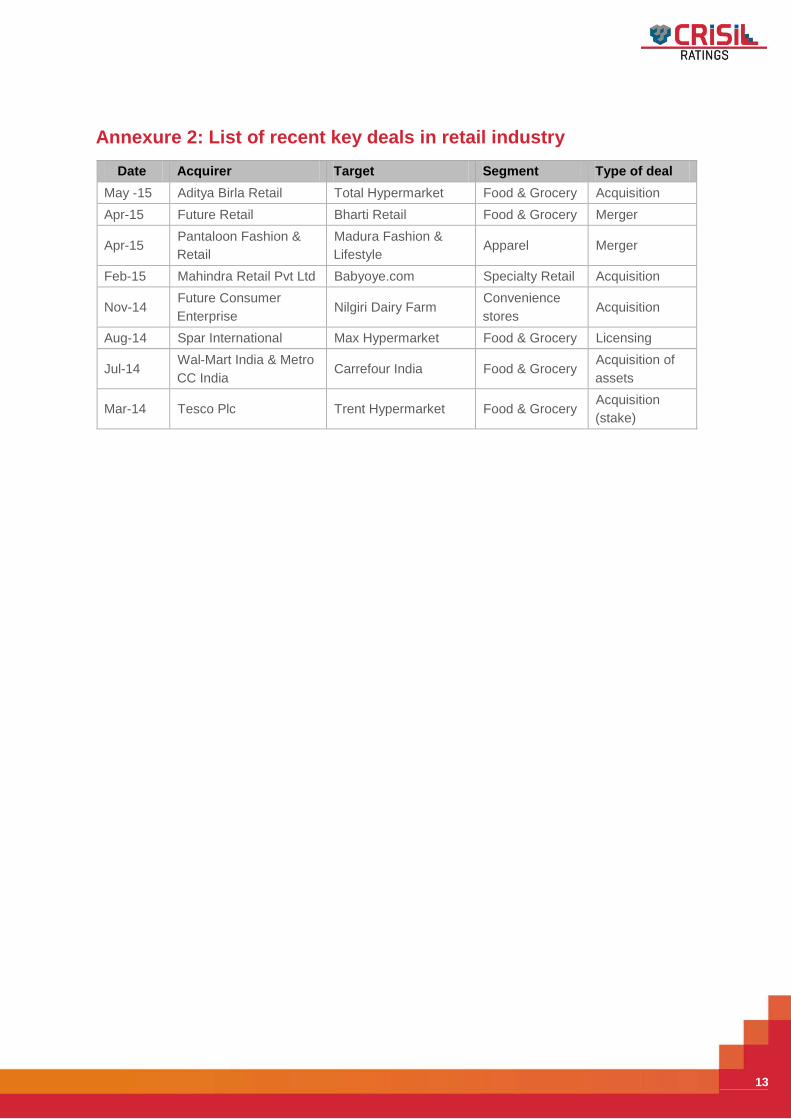

4. Consolidation time Increased consolidation in the sector has been witnessed in the last 2 years as players seek to achieve scale through inorganic means. Acquisitions (refer to Annexure 2) have broadly been undertaken as a means of entry into newer geographies where the target retailer has an established market presence and the acquirer can maximise utilisation of back-end infrastructure. Consolidation has also been witnessed among players operating in the same vertical as a means to achieve scale, besides improved operating efficiencies. CRISIL Ratings believes large retailers with strong backend infrastructure will increasingly take the inorganic route to enhance their market position and achieve synergistic growth.

7

Credit quality of large retailers to remain stable over the medium term An analysis of 24 large B&M retailers2 (18 rated by CRISIL) shows that store productivity has seen sustained improvement over the last five years ended fiscal 2015. This has reflected in improvement in operating level profitability and cash generation for these players. CRISIL believes these retailers will also benefit from an expected recovery in consumer sentiment and the broader economy.

1. Going ahead, revenue growth will be function of product category

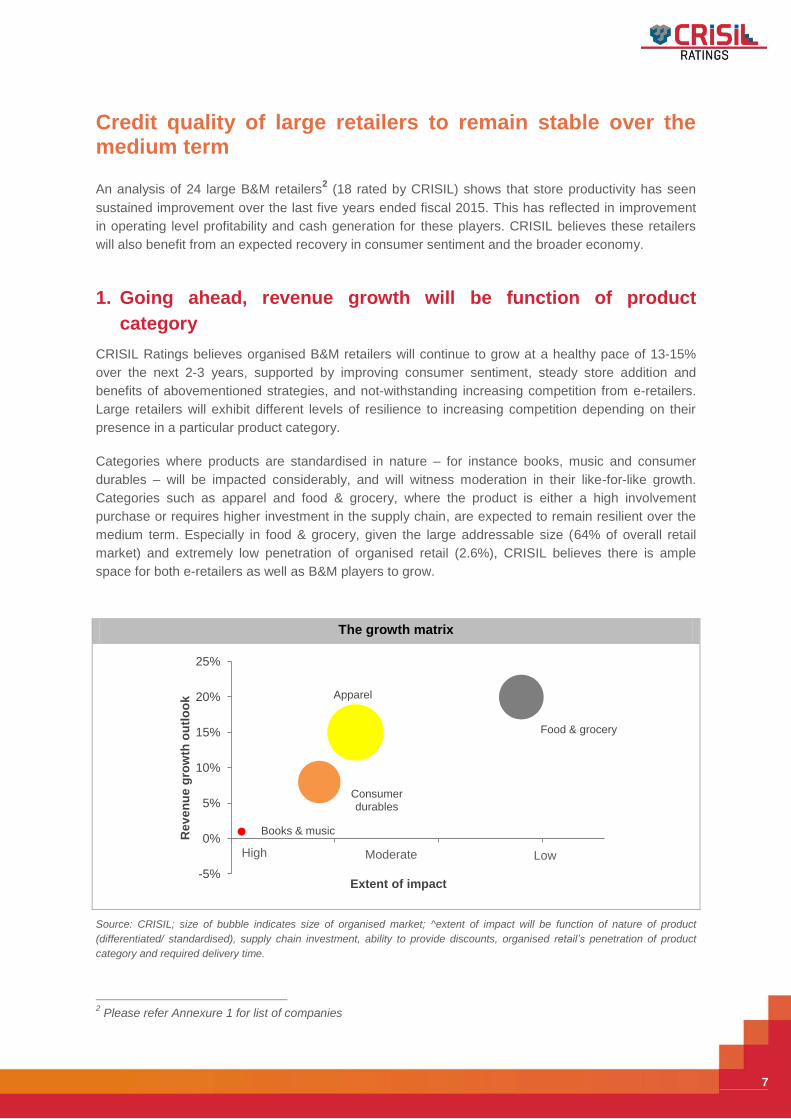

CRISIL Ratings believes organised B&M retailers will continue to grow at a healthy pace of 13-15% over the next 2-3 years, supported by improving consumer sentiment, steady store addition and benefits of abovementioned strategies, and not-withstanding increasing competition from e-retailers. Large retailers will exhibit different levels of resilience to increasing competition depending on their presence in a particular product category. Categories where products are standardised in nature – for instance books, music and consumer durables – will be impacted considerably, and will witness moderation in their like-for-like growth. Categories such as apparel and food & grocery, where the product is either a high involvement purchase or requires higher investment in the supply chain, are expected to remain resilient over the medium term. Especially in food & grocery, given the large addressable size (64% of overall retail market) and extremely low penetration of organised retail (2.6%), CRISIL believes there is ample space for both e-retailers as well as B&M players to grow.

The growth matrix

Source: CRISIL; size of bubble indicates size of organised market; ^extent of impact will be function of nature of product (differentiated/ standardised), supply chain investment, ability to provide discounts, organised retail’s penetration of product category and required delivery time.

2 Please refer Annexure 1 for list of companies

Food & grocery

Apparel

Consumer durables

Books & music

-5%

0%

5%

10%

15%

20%

25%

Rev

enue

gro

wth

out

look

Extent of impact

LowHigh Moderate

CRISIL Insight

8

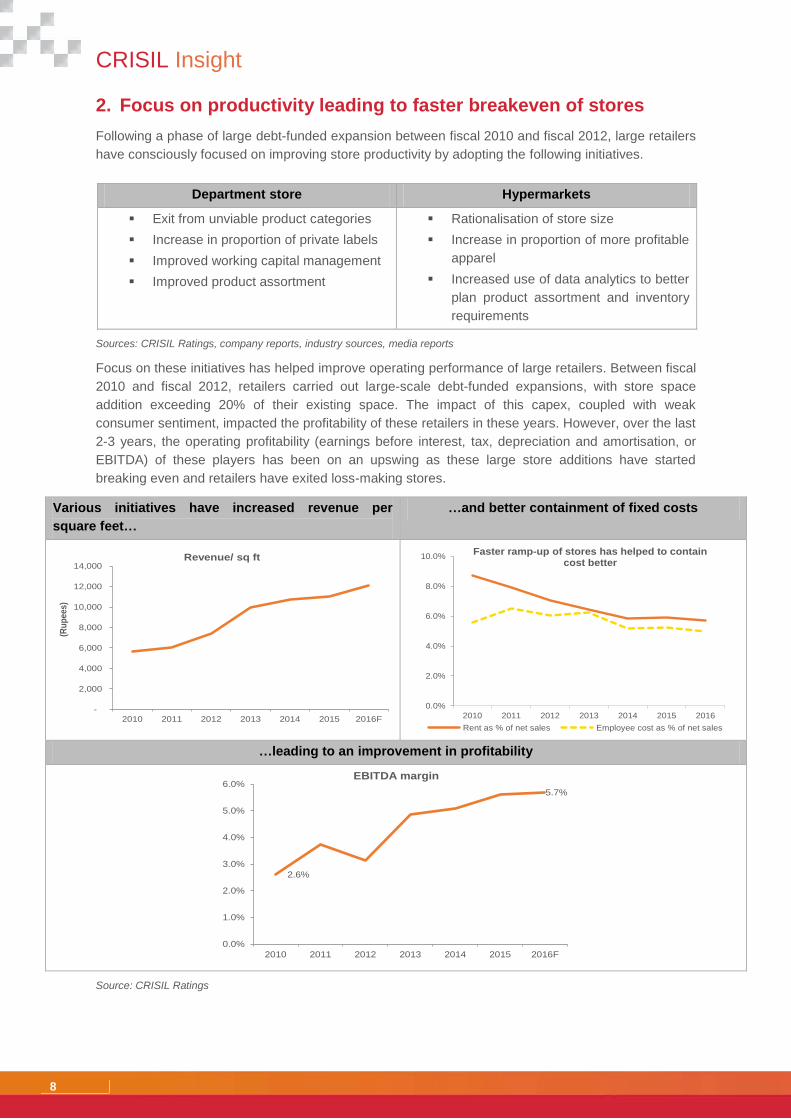

2. Focus on productivity leading to faster breakeven of stores Following a phase of large debt-funded expansion between fiscal 2010 and fiscal 2012, large retailers have consciously focused on improving store productivity by adopting the following initiatives.

Department store Hypermarkets

Exit from unviable product categories Increase in proportion of private labels Improved working capital management Improved product assortment

Rationalisation of store size Increase in proportion of more profitable

apparel Increased use of data analytics to better

plan product assortment and inventory requirements

Sources: CRISIL Ratings, company reports, industry sources, media reports

Focus on these initiatives has helped improve operating performance of large retailers. Between fiscal 2010 and fiscal 2012, retailers carried out large-scale debt-funded expansions, with store space addition exceeding 20% of their existing space. The impact of this capex, coupled with weak consumer sentiment, impacted the profitability of these retailers in these years. However, over the last 2-3 years, the operating profitability (earnings before interest, tax, depreciation and amortisation, or EBITDA) of these players has been on an upswing as these large store additions have started breaking even and retailers have exited loss-making stores.

Various initiatives have increased revenue per square feet…

…and better containment of fixed costs

…leading to an improvement in profitability

Source: CRISIL Ratings

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2010 2011 2012 2013 2014 2015 2016F

(Rup

ees)

Revenue/ sq ft

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2010 2011 2012 2013 2014 2015 2016

Faster ramp-up of stores has helped to contain cost better

Rent as % of net sales Employee cost as % of net sales

2.6%

5.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2010 2011 2012 2013 2014 2015 2016F

EBITDA margin

9

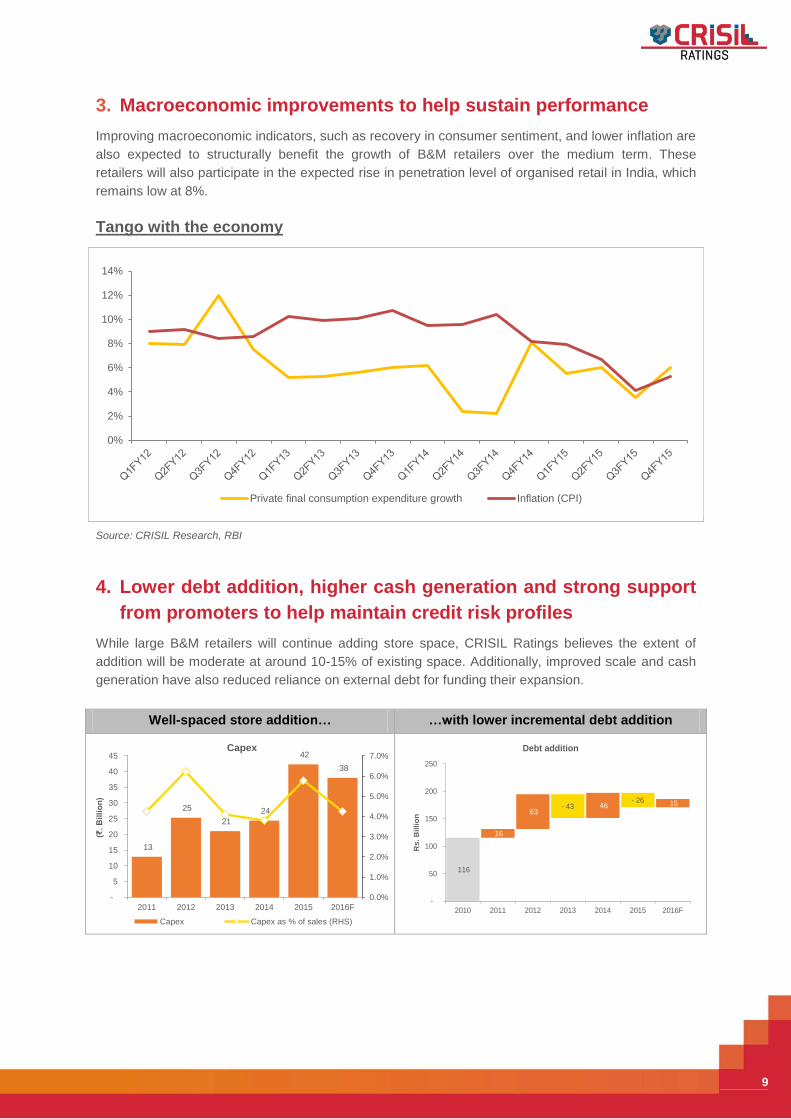

3. Macroeconomic improvements to help sustain performance Improving macroeconomic indicators, such as recovery in consumer sentiment, and lower inflation are also expected to structurally benefit the growth of B&M retailers over the medium term. These retailers will also participate in the expected rise in penetration level of organised retail in India, which remains low at 8%.

Tango with the economy

Source: CRISIL Research, RBI

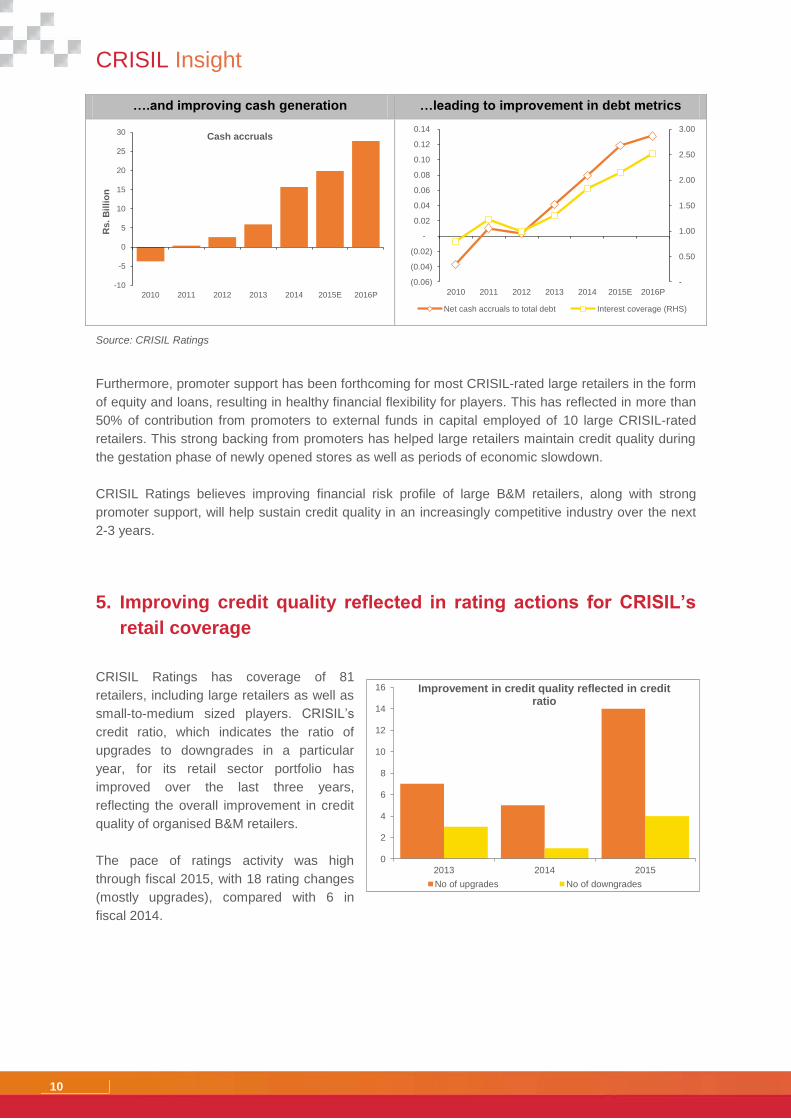

4. Lower debt addition, higher cash generation and strong support from promoters to help maintain credit risk profiles

While large B&M retailers will continue adding store space, CRISIL Ratings believes the extent of addition will be moderate at around 10-15% of existing space. Additionally, improved scale and cash generation have also reduced reliance on external debt for funding their expansion.

Well-spaced store addition… …with lower incremental debt addition

0%

2%

4%

6%

8%

10%

12%

14%

Private final consumption expenditure growth Inflation (CPI)

13

25 21

24

42 38

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

-

5

10

15

20

25

30

35

40

45

2011 2012 2013 2014 2015 2016F

(₹. B

illio

n)

Capex

Capex Capex as % of sales (RHS)

116

16

63 - 43 46

- 26 15

-

50

100

150

200

250

2010 2011 2012 2013 2014 2015 2016F

Rs.

Bill

ion

Debt addition

CRISIL Insight

10

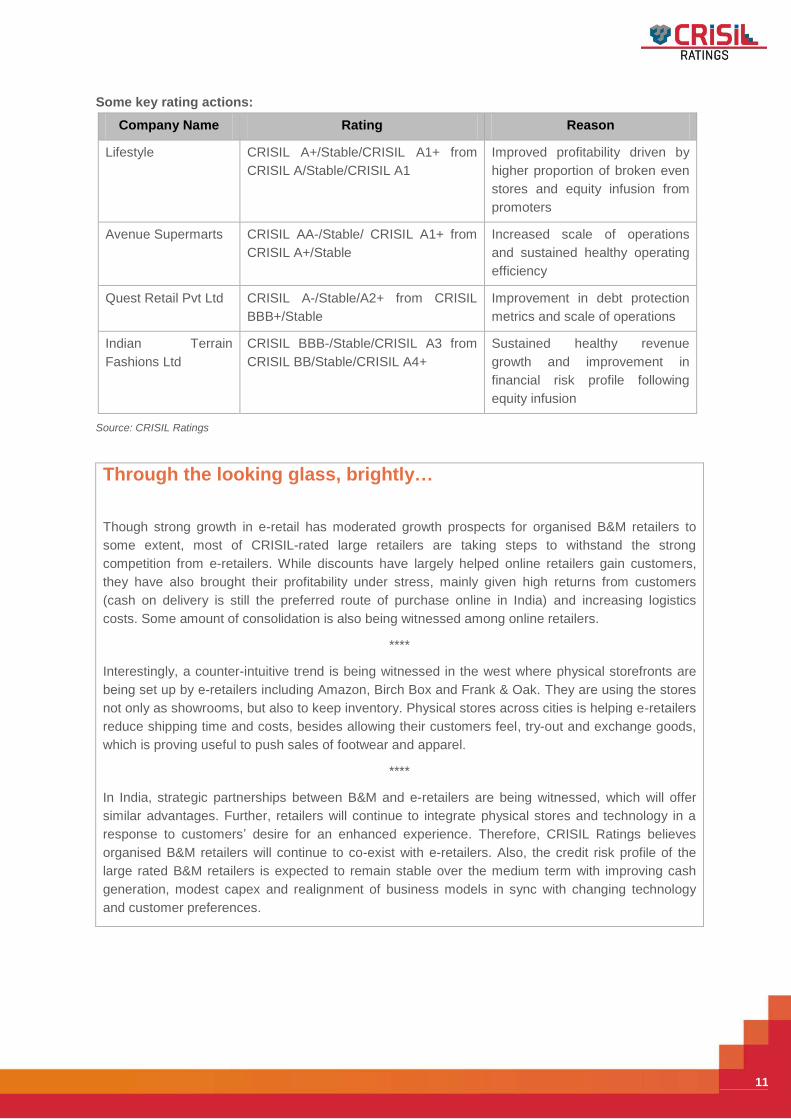

….and improving cash generation …leading to improvement in debt metrics

Source: CRISIL Ratings

Furthermore, promoter support has been forthcoming for most CRISIL-rated large retailers in the form of equity and loans, resulting in healthy financial flexibility for players. This has reflected in more than 50% of contribution from promoters to external funds in capital employed of 10 large CRISIL-rated retailers. This strong backing from promoters has helped large retailers maintain credit quality during the gestation phase of newly opened stores as well as periods of economic slowdown. CRISIL Ratings believes improving financial risk profile of large B&M retailers, along with strong promoter support, will help sustain credit quality in an increasingly competitive industry over the next 2-3 years.

5. Improving credit quality reflected in rating actions for CRISIL’s retail coverage

CRISIL Ratings has coverage of 81 retailers, including large retailers as well as small-to-medium sized players. CRISIL’s credit ratio, which indicates the ratio of upgrades to downgrades in a particular year, for its retail sector portfolio has improved over the last three years, reflecting the overall improvement in credit quality of organised B&M retailers. The pace of ratings activity was high through fiscal 2015, with 18 rating changes (mostly upgrades), compared with 6 in fiscal 2014.

-10

-5

0

5

10

15

20

25

30

2010 2011 2012 2013 2014 2015E 2016P

Cash accruals

Rs.

Bill

ion

-

0.50

1.00

1.50

2.00

2.50

3.00

(0.06)

(0.04)

(0.02)

-

0.02

0.04

0.06

0.08

0.10

0.12

0.14

2010 2011 2012 2013 2014 2015E 2016P

Net cash accruals to total debt Interest coverage (RHS)

0

2

4

6

8

10

12

14

16

2013 2014 2015

Improvement in credit quality reflected in credit ratio

No of upgrades No of downgrades

11

Some key rating actions: Company Name Rating Reason

Lifestyle CRISIL A+/Stable/CRISIL A1+ from CRISIL A/Stable/CRISIL A1

Improved profitability driven by higher proportion of broken even stores and equity infusion from promoters

Avenue Supermarts CRISIL AA-/Stable/ CRISIL A1+ from CRISIL A+/Stable

Increased scale of operations and sustained healthy operating efficiency

Quest Retail Pvt Ltd CRISIL A-/Stable/A2+ from CRISIL BBB+/Stable

Improvement in debt protection metrics and scale of operations

Indian Terrain Fashions Ltd

CRISIL BBB-/Stable/CRISIL A3 from CRISIL BB/Stable/CRISIL A4+

Sustained healthy revenue growth and improvement in financial risk profile following equity infusion

Source: CRISIL Ratings

Through the looking glass, brightly…

Though strong growth in e-retail has moderated growth prospects for organised B&M retailers to some extent, most of CRISIL-rated large retailers are taking steps to withstand the strong competition from e-retailers. While discounts have largely helped online retailers gain customers, they have also brought their profitability under stress, mainly given high returns from customers (cash on delivery is still the preferred route of purchase online in India) and increasing logistics costs. Some amount of consolidation is also being witnessed among online retailers.

****

Interestingly, a counter-intuitive trend is being witnessed in the west where physical storefronts are being set up by e-retailers including Amazon, Birch Box and Frank & Oak. They are using the stores not only as showrooms, but also to keep inventory. Physical stores across cities is helping e-retailers reduce shipping time and costs, besides allowing their customers feel, try-out and exchange goods, which is proving useful to push sales of footwear and apparel.

****

In India, strategic partnerships between B&M and e-retailers are being witnessed, which will offer similar advantages. Further, retailers will continue to integrate physical stores and technology in a response to customers’ desire for an enhanced experience. Therefore, CRISIL Ratings believes organised B&M retailers will continue to co-exist with e-retailers. Also, the credit risk profile of the large rated B&M retailers is expected to remain stable over the medium term with improving cash generation, modest capex and realignment of business models in sync with changing technology and customer preferences.

CRISIL Insight

12

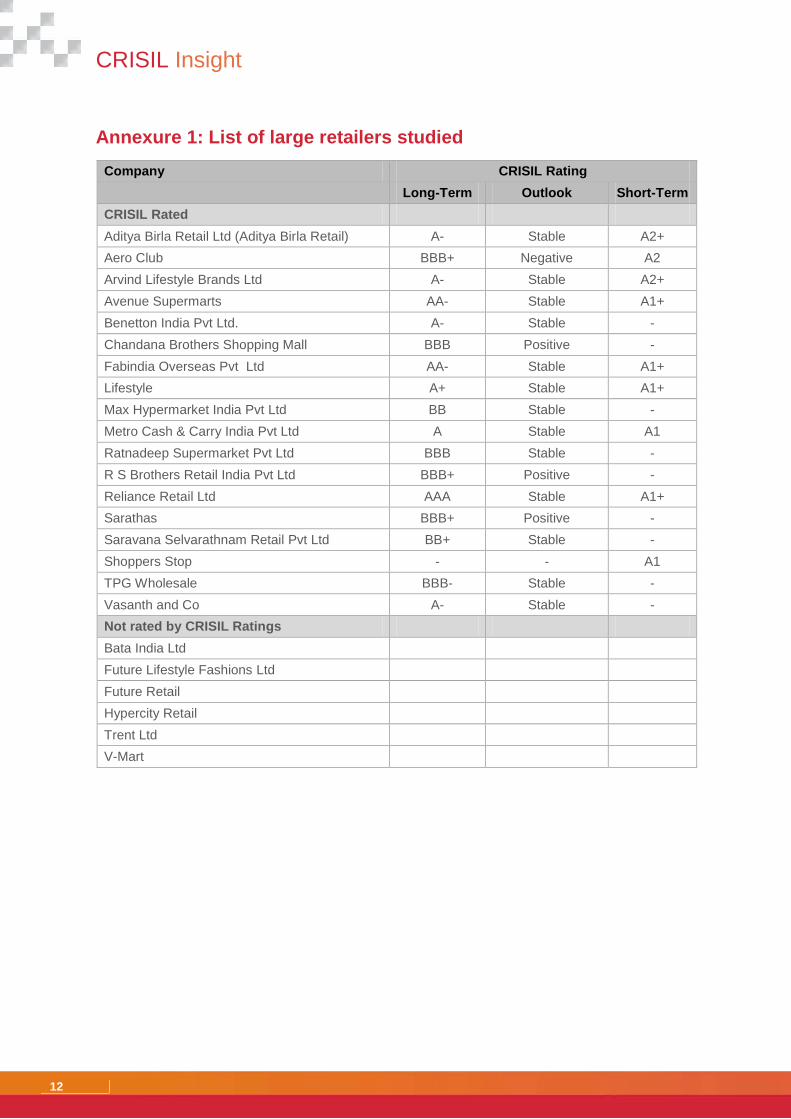

Annexure 1: List of large retailers studied Company CRISIL Rating

Long-Term Outlook Short-Term

CRISIL Rated Aditya Birla Retail Ltd (Aditya Birla Retail) A- Stable A2+ Aero Club BBB+ Negative A2 Arvind Lifestyle Brands Ltd A- Stable A2+ Avenue Supermarts AA- Stable A1+ Benetton India Pvt Ltd. A- Stable - Chandana Brothers Shopping Mall BBB Positive - Fabindia Overseas Pvt Ltd AA- Stable A1+ Lifestyle A+ Stable A1+ Max Hypermarket India Pvt Ltd BB Stable - Metro Cash & Carry India Pvt Ltd A Stable A1 Ratnadeep Supermarket Pvt Ltd BBB Stable - R S Brothers Retail India Pvt Ltd BBB+ Positive - Reliance Retail Ltd AAA Stable A1+ Sarathas BBB+ Positive - Saravana Selvarathnam Retail Pvt Ltd BB+ Stable - Shoppers Stop - - A1 TPG Wholesale BBB- Stable - Vasanth and Co A- Stable - Not rated by CRISIL Ratings Bata India Ltd Future Lifestyle Fashions Ltd Future Retail Hypercity Retail Trent Ltd V-Mart

13

Annexure 2: List of recent key deals in retail industry Date Acquirer Target Segment Type of deal

May -15 Aditya Birla Retail Total Hypermarket Food & Grocery Acquisition Apr-15 Future Retail Bharti Retail Food & Grocery Merger

Apr-15 Pantaloon Fashion & Retail

Madura Fashion & Lifestyle

Apparel Merger

Feb-15 Mahindra Retail Pvt Ltd Babyoye.com Specialty Retail Acquisition

Nov-14 Future Consumer Enterprise

Nilgiri Dairy Farm Convenience stores

Acquisition

Aug-14 Spar International Max Hypermarket Food & Grocery Licensing

Jul-14 Wal-Mart India & Metro CC India

Carrefour India Food & Grocery Acquisition of assets

Mar-14 Tesco Plc Trent Hypermarket Food & Grocery Acquisition (stake)

CRISIL Insight

14

This page is intentionally left blank

15

About CRISIL Limited

CRISIL is a global analytical company providing ratings, research, and risk and policy advisory services. We are India's leading ratings agency. We are also the foremost provider of high-end research to the world's largest banks and leading corporations. About CRISIL Ratings

CRISIL Ratings is India's leading rating agency. We pioneered the concept of credit rating in India in 1987. With a tradition of independence, analytical rigour and innovation, we have a leadership position. We have rated over 95,000 entities, by far the largest number in India. We are a full-service rating agency. We rate the entire range of debt instruments: bank loans, certificates of deposit, commercial paper, non-convertible debentures, bank hybrid capital instruments, asset-backed securities, mortgage-backed securities, perpetual bonds, and partial guarantees. CRISIL sets the standards in every aspect of the credit rating business. We have instituted several innovations in India including rating municipal bonds, partially guaranteed instruments, microfinance institutions and voluntary organizations. We pioneered a globally unique and affordable rating service for Small and Medium Enterprises (SMEs).This has significantly expanded the market for ratings and is improving SMEs' access to affordable finance. We have an active outreach programme with issuers, investors and regulators to maintain a high level of transparency regarding our rating criteria and to disseminate our analytical insights and knowledge. CRISIL Privacy CRISIL respects your privacy. We use your contact information, such as your name, address, and email id, to fulfil your request and service your account and to provide you with additional information from CRISIL and other parts of McGraw Hill Financial you may find of interest. For further information, or to let us know your preferences with respect to receiving marketing materials, please visit www.crisil.com/privacy. You can view McGraw Hill Financial’s Customer Privacy Policy at http://www.mhfi.com/privacy.

Last updated: August, 2014

Our Office

Ahmedabad Unit No. 706, 7th Floor, Venus Atlantis, Prahladnagar, Satellite, Ahmedabad - 380015 India Phone : +91 79 4024 4500 Fax : +91 79 4024 4520

Bengaluru W - 101, 1st floor, Sunrise Chambers, 22, Ulsoor Road, Bengaluru - 560042, India Phone: +91 80 4244 5399 Fax: +91 80 4244 5300

Chennai Thapar House, Mezzanine Floor, No. 37 Montieth Road, Egmore, Chennai - 600 008 India Phone : +91 44 2854 6205 - 06 /

+91 44 854 6093 Fax : +91 44 2854 7531

Gurgaon CRISIL House Plot No. 46, Sector 44, Opp PF Office, Gurgaon, Haryana, India Phone : +91 0124 672 2000

Hyderabad Uma Chambers, 3rd Floor Plot No. 9&10, Nagarjuna Hills Near Punjagutta Cross Road Hyderabad - 500 082, India Phone: +91 40 2335 8103/05 Fax: +91 40 2335 7507 Kolkata Convergence Building 3rd Floor, D2/2, EPGP Block Sector V, Salt Lake City Kolkata - 700 091, India Phone: +91 33 4011 8200 Fax: +91 33 4011 8250 Pune 1187/17, Ghole Road, Shivaji Nagar, Pune - 411 005, India Phone: +91 20 4018 1900 Fax: +91 20 4018 1930

Stay Connected | CRISIL Website |

Twitter |

LinkedIn |

YouTube |

CRISIL Limited CRISIL House, Central Avenue, Hiranandani Business Park, Powai, Mumbai – 400076. India Phone: + 91 22 3342 3000 | Fax: + 91 22 3342 3001 www.crisil.com