Embed Size (px)

Citation preview

M&A International™ – the world's leading M&A alliance

Selling Your Company

June 2012

Howard E. Johnson MBA, FCA, FCMA, CBV, CPA, CFA, ASA, CF, C.DIR

1

M&A International™ – the world's leading M&A alliance

Speaker

Howard E. Johnson MBA, FCA, FCMA, CBV, CPA, CFA, ASA, CF, C.Dir Managing Director, Veracap Corporate Finance Limited (416) 597-4500; [email protected] Howard is a Managing Director of Veracap Corporate Finance and its affiliate, Campbell Valuation Partners Limited. He advises business owners and executives of mid-sized and large public and private companies on business valuation, acquisitions, divestitures, and value maximization strategies. Howard is the author of several texts on the subjects of business valuation and corporate finance, and has acted as an expert witness on valuation matters before the courts.

2

M&A International™ – the world's leading M&A alliance

About Veracap

Veracap Corporate Finance Limited helps business owners and executives to maximize shareholder value through acquisitions, divestitures, private equity financing and shareholder value advisory services. Veracap is an affiliate of Campbell Valuation Partners, Canada’s longest established independent business valuation firm. Veracap is a member of M&A International, the world’s leading affiliation of M&A advisors, with over 500 professionals in 41 countries.

www.veracap.com 3

M&A International™ – the world's leading M&A alliance

Disclaimer

This material is for educational purposes only. It deals with technical matters which have broad application and may not be applicable to a particular set of circumstances and facts. As well, the course material and references contained therein reflect laws and practices which are subject to change. For these reasons, the course material should not be relied upon as a substitute for specialized advice in connection with any particular matter. Although the course material has been carefully prepared, the author does not accept any legal responsibility for its contents or for any consequences arising from its use. © Howard E. Johnson, 2012

4

M&A International™ – the world's leading M&A alliance

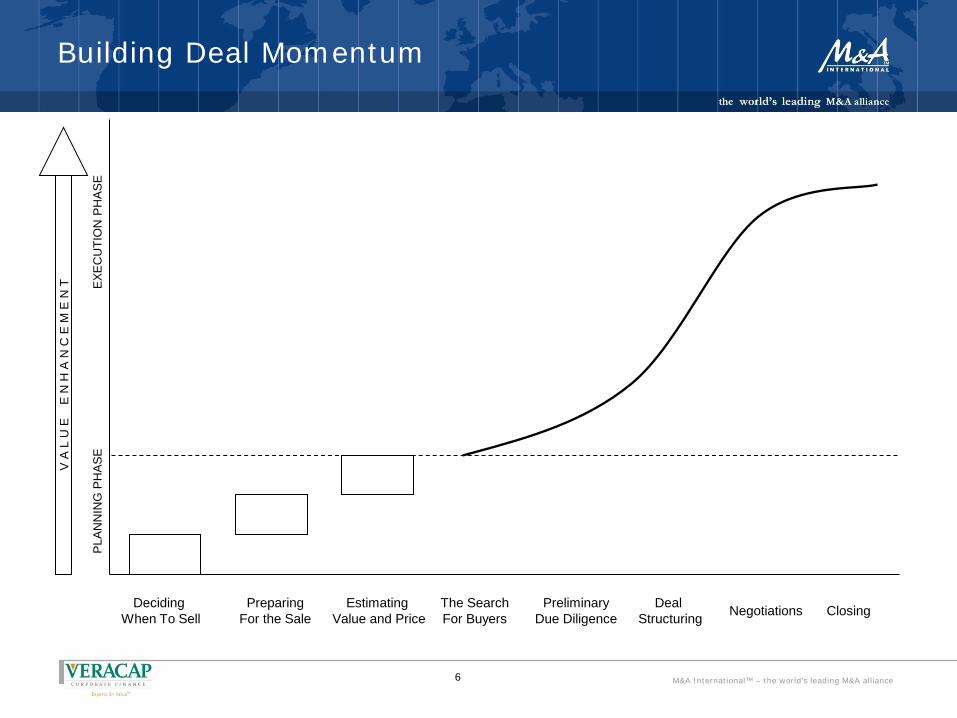

The Private Company Sale Process 1. Deciding When to Sell 2. Preparing for the Sale 3. Estimating Value & Price 4. Search for Buyers 5. Preliminary Due Diligence 6. Deal Structuring 7. Negotiations 8. Closing

5

M&A International™ – the world's leading M&A alliance

Deciding When To Sell

Preparing For the Sale

The Search For Buyers

Estimating Value and Price

Preliminary Due Diligence

PLA

NN

ING

PH

AS

E

E

XEC

UTI

ON

PH

AS

E

Negotiations Deal Structuring Closing

V A

L U

E

E N

H A

N C

E M

E N

T

Building Deal Momentum

6

M&A International™ – the world's leading M&A alliance

Deciding When to Sell

Situation analysis – owner or parent co. Economic and industry conditions

Company performance and prospects

Key = Time the sale to coincide with favourable personal and business conditions

7

M&A International™ – the world's leading M&A alliance

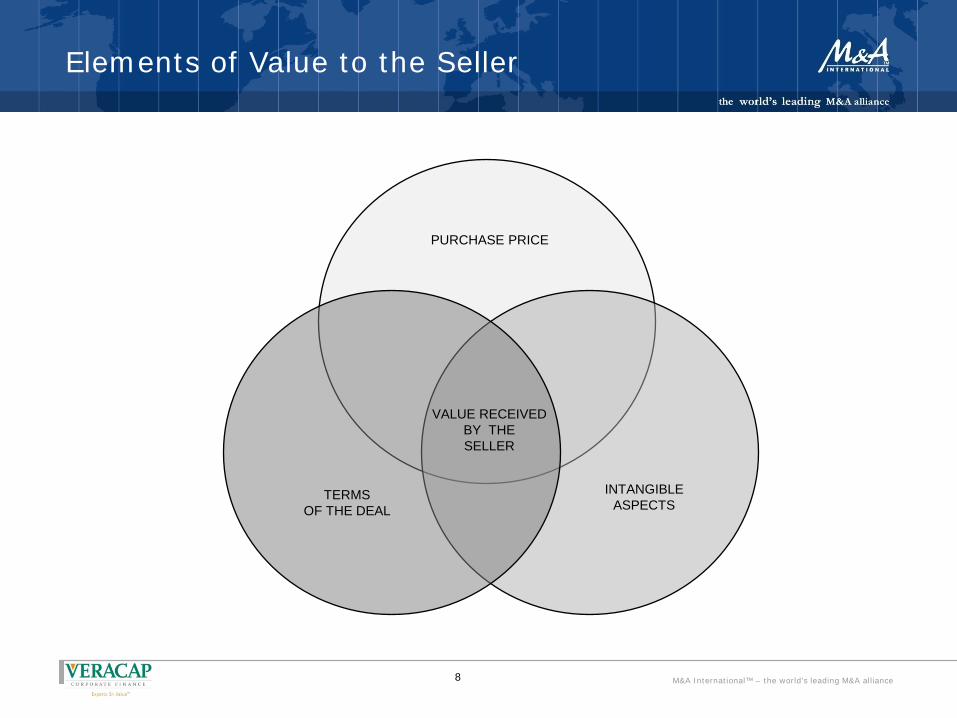

VALUE RECEIVED BY THE SELLER

TERMS OF THE DEAL

INTANGIBLE ASPECTS

PURCHASE PRICE

Elements of Value to the Seller

8

M&A International™ – the world's leading M&A alliance

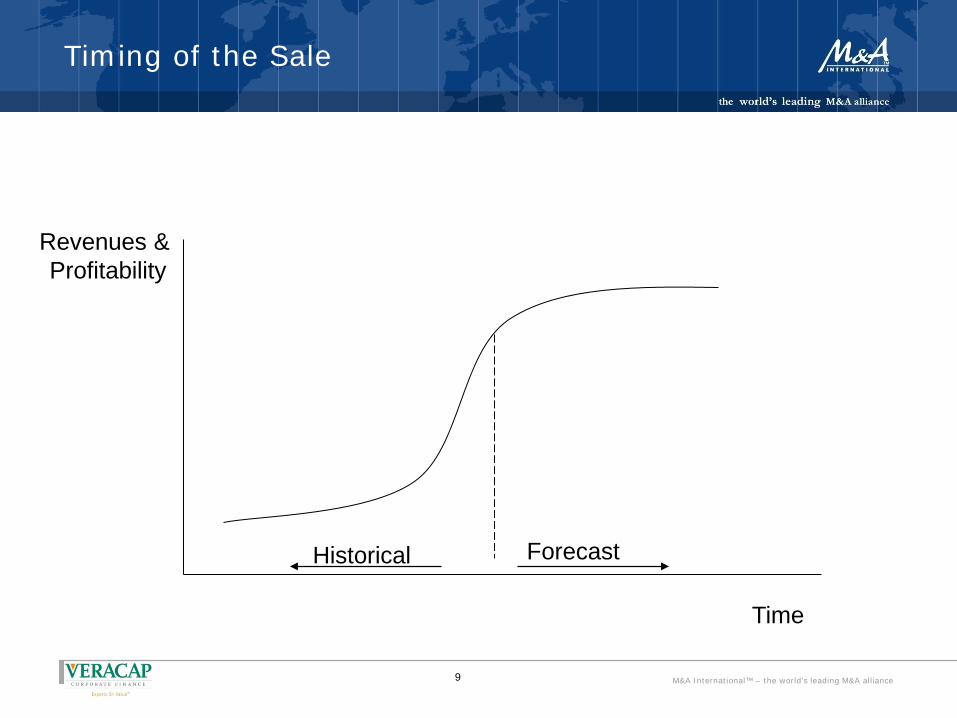

Timing of the Sale

Revenues & Profitability

Time

Historical Forecast

9

M&A International™ – the world's leading M&A alliance

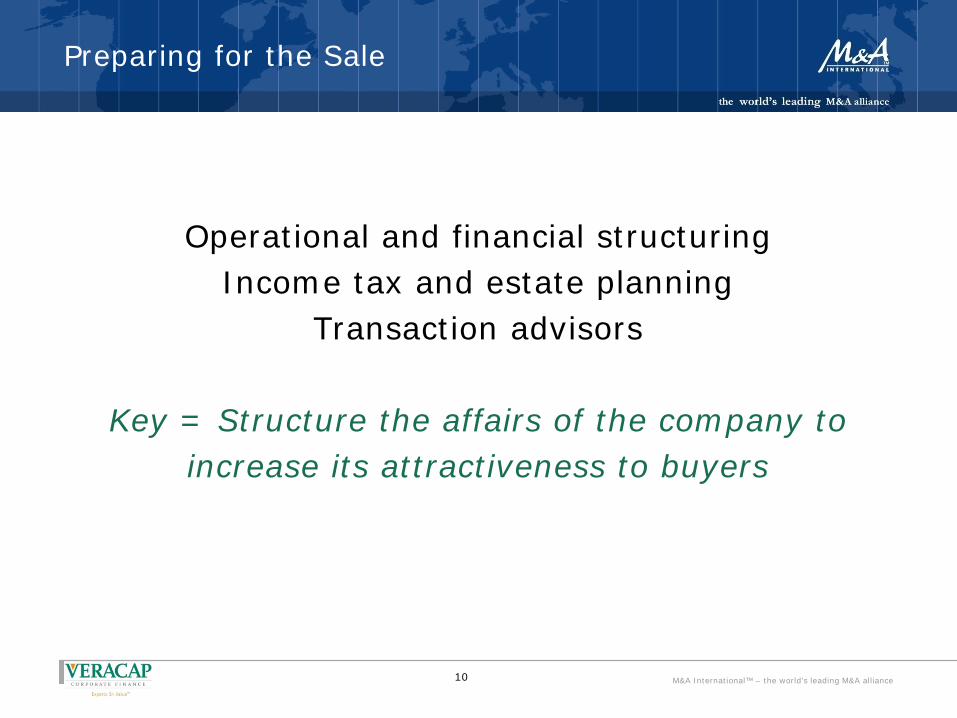

Preparing for the Sale

Operational and financial structuring Income tax and estate planning

Transaction advisors

Key = Structure the affairs of the company to increase its attractiveness to buyers

10

M&A International™ – the world's leading M&A alliance

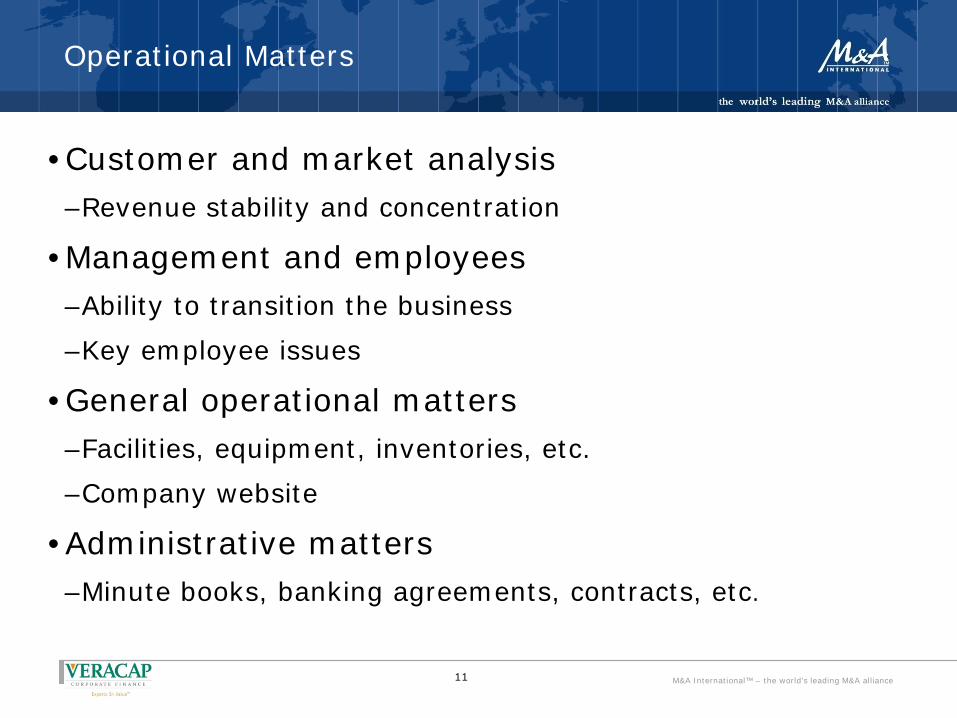

Operational Matters

•Customer and market analysis –Revenue stability and concentration

•Management and employees –Ability to transition the business –Key employee issues

•General operational matters –Facilities, equipment, inventories, etc. –Company website

•Administrative matters –Minute books, banking agreements, contracts, etc.

11

M&A International™ – the world's leading M&A alliance

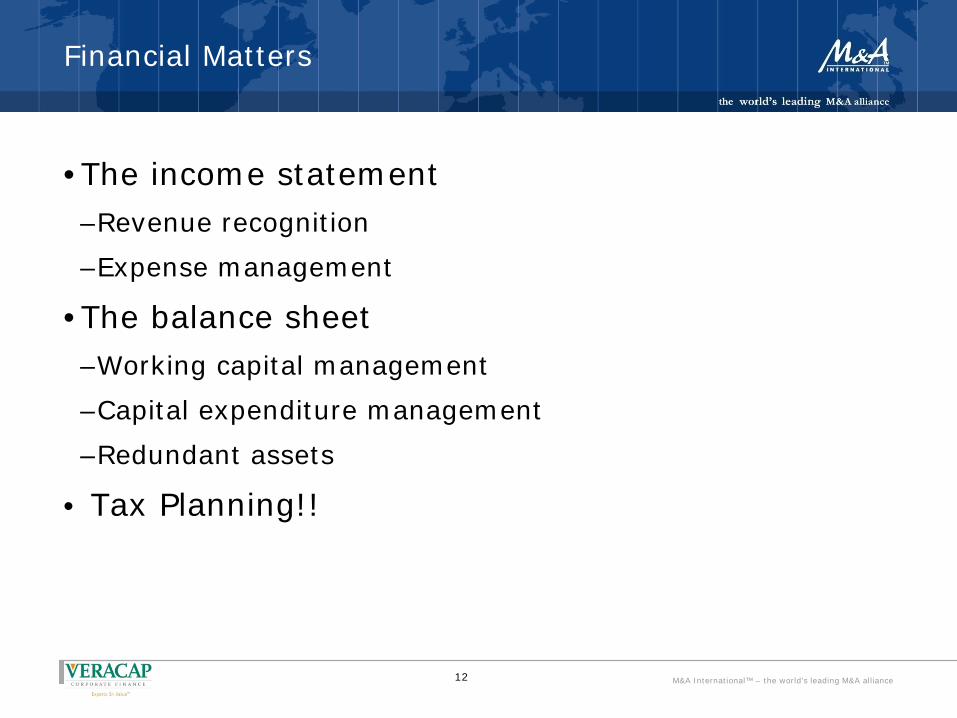

Financial Matters

•The income statement –Revenue recognition –Expense management

•The balance sheet –Working capital management –Capital expenditure management –Redundant assets

• Tax Planning!!

12

M&A International™ – the world's leading M&A alliance

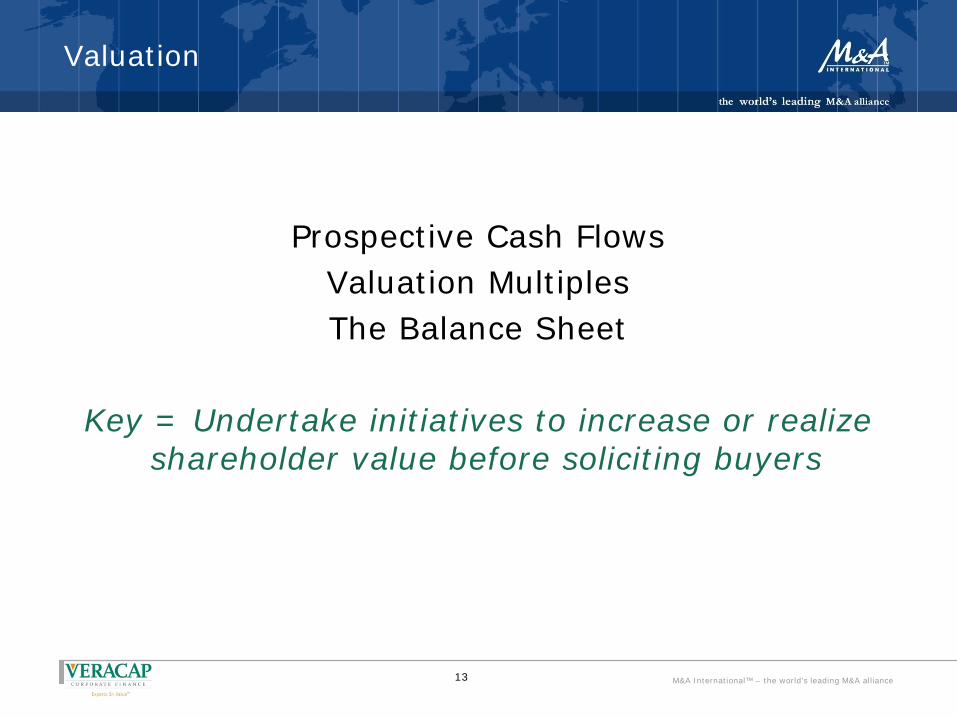

Valuation

Prospective Cash Flows Valuation Multiples The Balance Sheet

Key = Undertake initiatives to increase or realize

shareholder value before soliciting buyers

13

M&A International™ – the world's leading M&A alliance

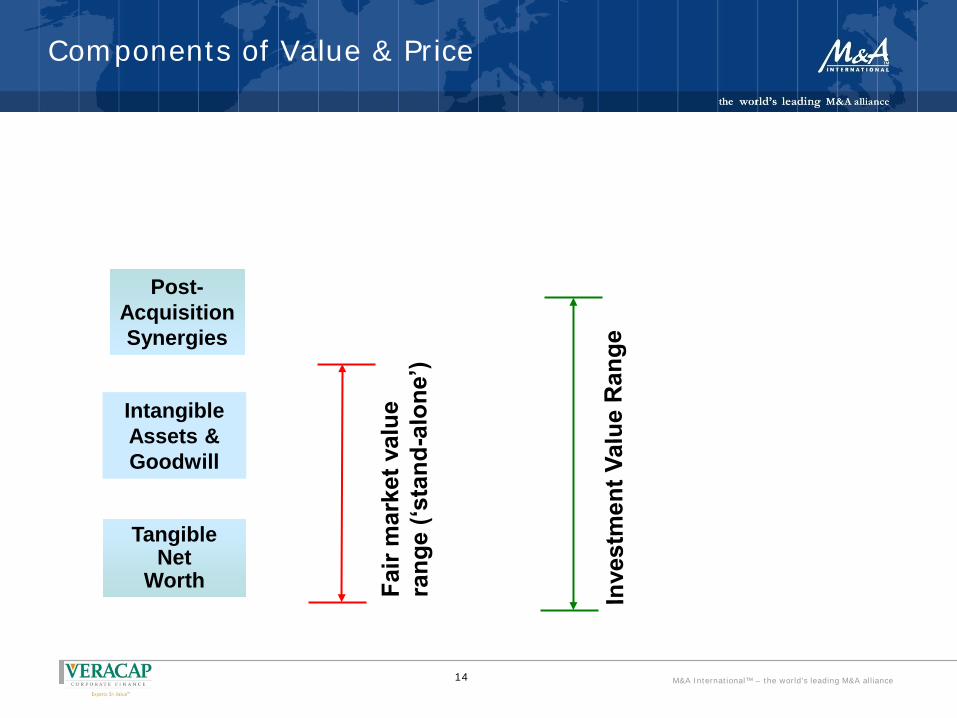

Components of Value & Price

Post-Acquisition Synergies

Intangible Assets & Goodwill

Tangible Net

Worth

14

M&A International™ – the world's leading M&A alliance

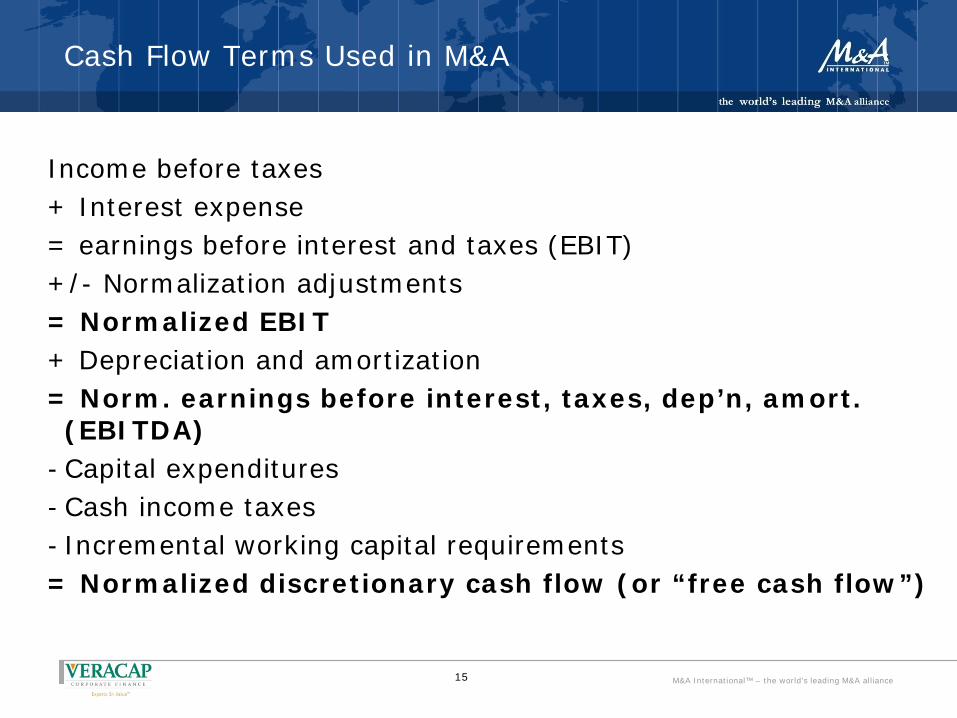

Cash Flow Terms Used in M&A

Income before taxes + Interest expense = earnings before interest and taxes (EBIT) +/- Normalization adjustments = Normalized EBIT + Depreciation and amortization = Norm. earnings before interest, taxes, dep’n, amort. (EBITDA)

- Capital expenditures - Cash income taxes - Incremental working capital requirements = Normalized discretionary cash flow (or “free cash flow”)

15

M&A International™ – the world's leading M&A alliance

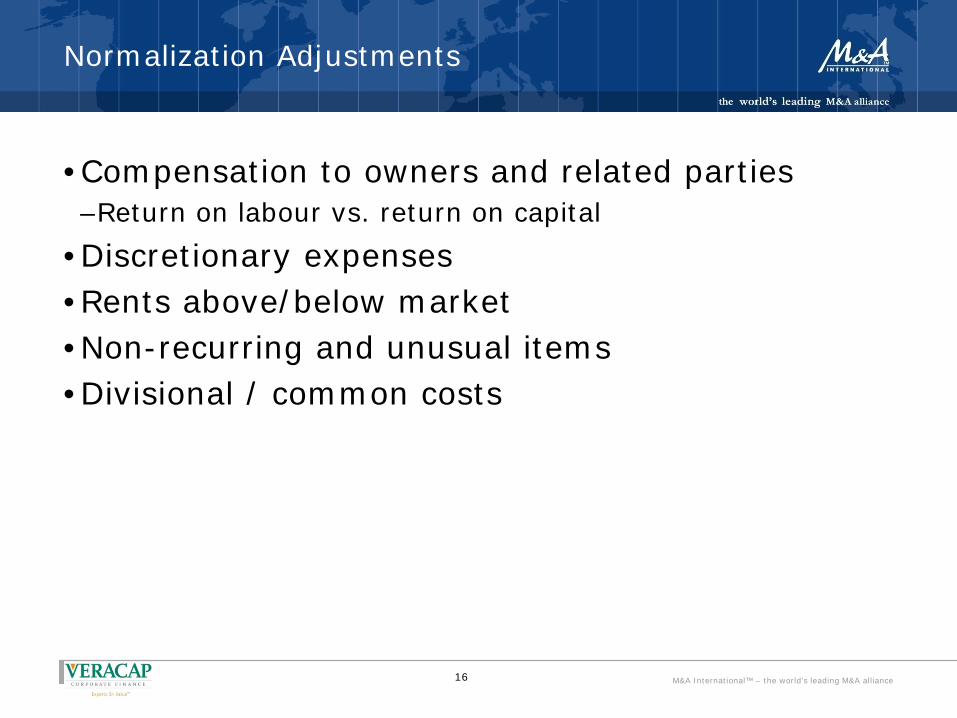

Normalization Adjustments

•Compensation to owners and related parties –Return on labour vs. return on capital

•Discretionary expenses •Rents above/below market •Non-recurring and unusual items •Divisional / common costs

16

M&A International™ – the world's leading M&A alliance

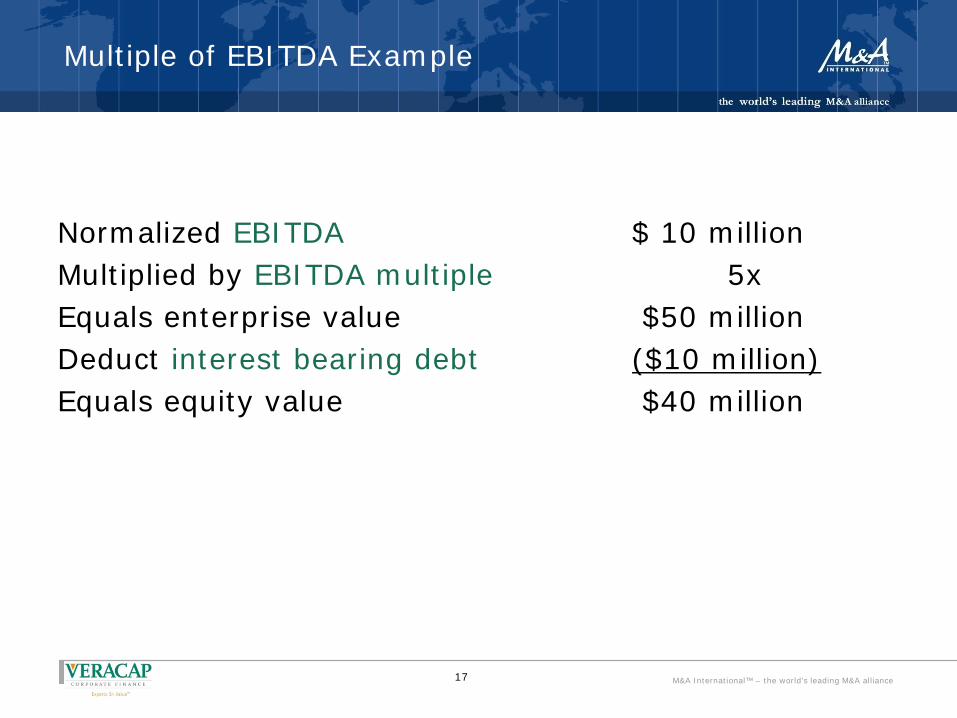

Multiple of EBITDA Example

Normalized EBITDA $ 10 million Multiplied by EBITDA multiple 5x Equals enterprise value $50 million Deduct interest bearing debt ($10 million) Equals equity value $40 million

17

M&A International™ – the world's leading M&A alliance

Determinants of Valuation Multiples

•Company size •Revenue stability and concentration •Proprietary products and services •Management and employees •Growth potential •Capital expenditure requirements •Buyer synergy expectations •Terms of the transaction •Comparable transactions

18

M&A International™ – the world's leading M&A alliance

Rates of Return & Multiples

Return Multiple EBITDA $10,000 20% 5x Depreciation 2,800 EBIT $7,200 14% 7x Income taxes 2,200 After-tax cash flow $5,000 10% 10x All results lead to $50 million (enterprise value)

19

M&A International™ – the world's leading M&A alliance

What about the Balance Sheet?

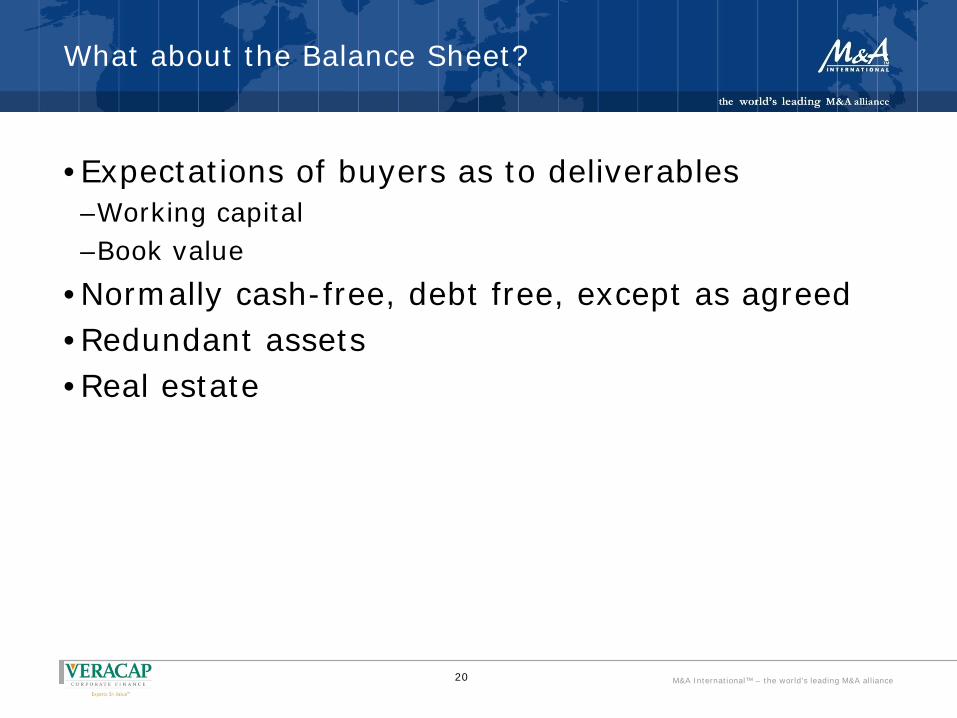

•Expectations of buyers as to deliverables –Working capital –Book value

•Normally cash-free, debt free, except as agreed •Redundant assets •Real estate

20

M&A International™ – the world's leading M&A alliance

Search for Buyers

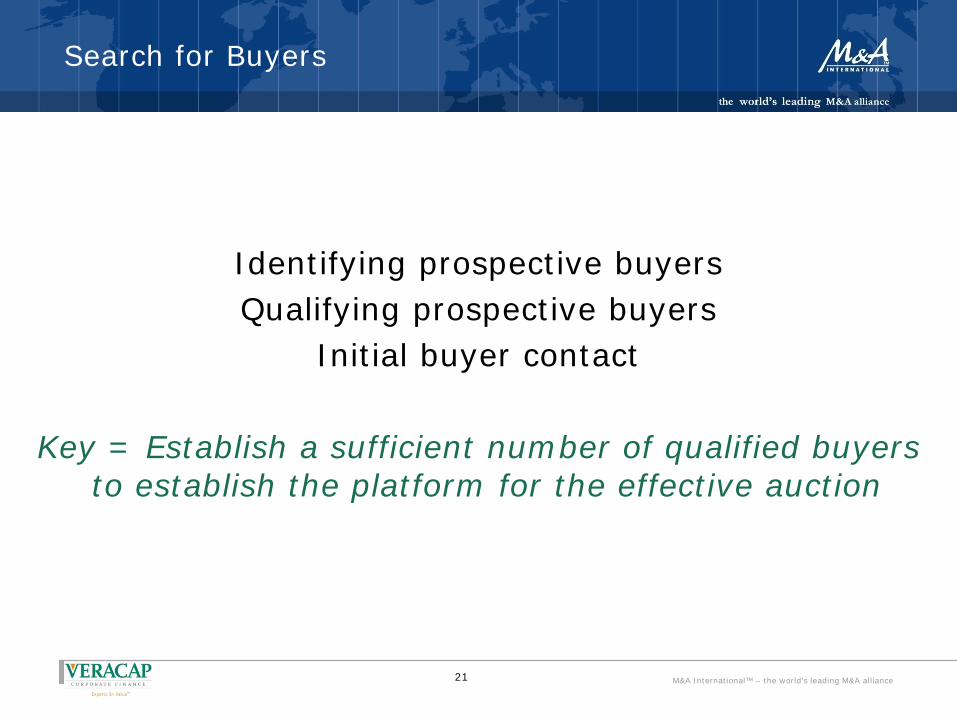

Identifying prospective buyers Qualifying prospective buyers

Initial buyer contact

Key = Establish a sufficient number of qualified buyers to establish the platform for the effective auction

21

M&A International™ – the world's leading M&A alliance

Types of Prospective Buyers

•Strategic •Non-strategic •Small corporate / individuals •Financial •Management and employees

Finding the “Platform Buyer”

22

M&A International™ – the world's leading M&A alliance

The MBO Opportunity

•Availability of capital coupled with a lack of quality opportunities for investment –Financial investors becoming more aggressive

•Speed & confidentiality vs. strategic buyers •Deal structuring opportunities –Tax efficient transaction and availability of cash

•Possible lucrative upside for seller and management

But - beware the conflict of interest

23

M&A International™ – the world's leading M&A alliance

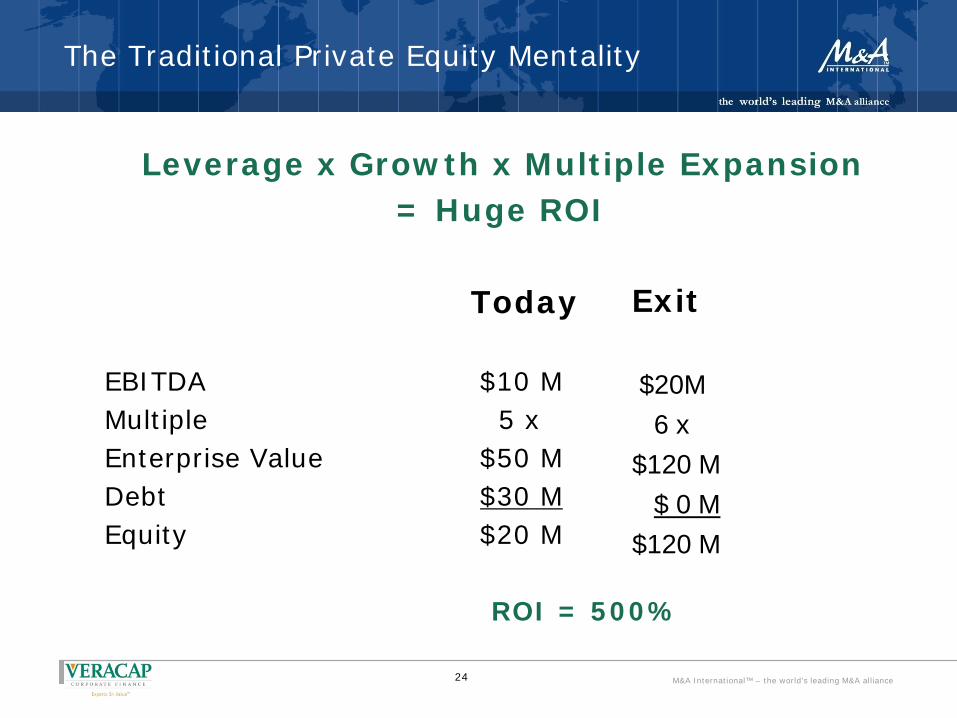

The Traditional Private Equity Mentality

Leverage x Growth x Multiple Expansion = Huge ROI

Today EBITDA $10 M Multiple 5 x Enterprise Value $50 M Debt $30 M Equity $20 M

ROI = 500%

Exit

$20M 6 x $120 M $ 0 M $120 M

24

M&A International™ – the world's leading M&A alliance

Preliminary Due Diligence

The Confidential Information Memorandum Initial buyer meetings

Other information and procedures

Key = Control the flow of information to increase the perceived value among buyers

25

M&A International™ – the world's leading M&A alliance

Transaction Structuring

Assets vs. shares Forms and terms of payment The Management Contract

Key = Evaluate each proposal based on its risk-

reward parameters and income tax efficiency

26

M&A International™ – the world's leading M&A alliance

Forms of Consideration

•Cash at closing •Holdback •Seller take-back / Promissory Notes •Share exchange •Earn-out

27

M&A International™ – the world's leading M&A alliance

Negotiations

Preparing for negotiations Negotiating strategies and tactics

The Letter of Intent

Key = Secure a comprehensive letter of intent that offers the best value to the business owner

28

M&A International™ – the world's leading M&A alliance

Negotiating Principles

•Information is key •Credibility –Information provided –Changes in stated positions

•Alternatives –Number and quality of buyers

•Price and terms are important –When / how paid –Conditions for payment –Tax issues

29

M&A International™ – the world's leading M&A alliance

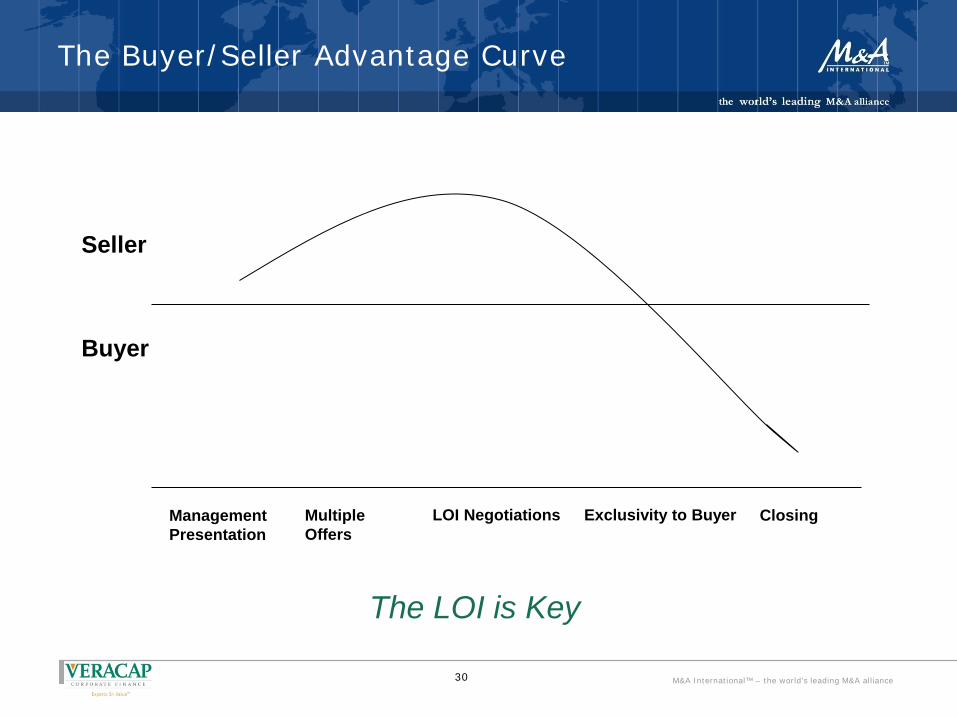

The Buyer/Seller Advantage Curve

Management Presentation

Multiple Offers

LOI Negotiations Exclusivity to Buyer Closing

Seller

Buyer

30

The LOI is Key

M&A International™ – the world's leading M&A alliance

Closing

Detailed due diligence The purchase agreement

Final closing

Key = Stay focused on running the business

31

M&A International™ – the world's leading M&A alliance

Why Deals Fail to Close

• Buyer and seller have different expectations – Secure a comprehensive, unambiguous LOI / term

sheet • New issues uncovered in detailed due diligence

– Ensure full disclosure of major issues prior to the LOI / term sheet

• Material adverse change in the company’s operations – Adopt a ‘business as usual’ attitude during closing

• External circumstances – Negotiate a relatively short exclusivity period

32

M&A International™ – the world's leading M&A alliance

The CFO as Quarterback

• Before the Process – Business readiness (financial and operational) – Organizing the transaction team (internal & external) – Tax planning

• During the Process – Coordinating with advisors – Information management – Assessing offers against objectives

• After the Process – Transition management – Integration issues

33

M&A International™ – the world's leading M&A alliance

Concluding Comments

• Presale planning and preparation are essential • Understand the components of value • Minimize the buyer’s perceived “transition risk” • Stay in control of the process • Terms and price are equally important • The LOI is a critical document • Stay the course through closing

34

M&A International™ – the world's leading M&A alliance

Resources

35

![[Howard Johnson, Martin Graham] High Speed Digital(BookSee.org)](https://img.pdfslide.us/doc/110x75/5695d0011a28ab9b02908771/howard-johnson-martin-graham-high-speed-digitalbookseeorg.jpg)