Embed Size (px)

Citation preview

Authors: Uma Ayyer, Sajid Husain, Tao Jiang, Srdjan Petrovic, Anand Tolani

Self-Driving Cars: Disruptive vs Incremental

This work was created in an open classroom environment as part of the Engineering Leadership Professional Program (ELPP) developed and led by Prof. Ikhlaq Sidhu at UC Berkeley. There should be no proprietary informaEon contained in this work. No informaEon contained in this work is intended to affect or influence public relaEons with any firm affiliated with any of the authors. The views represented are those of the authors alone and do not reflect those of the University of California Berkeley.

“Autonomous Drive is about relieving motorists of everyday tasks, par9cularly in congested or long-‐distance situa9ons. The driver remains in control, at the wheel, of a car that is capable of doing more things automa9cally. Self-‐driving cars, by comparison, don’t require any human interven9on – and remain a long-‐way from commercial reality. They are suitable only for 9ghtly-‐controlled road environments, at slow speeds, and face a regulatory minefield.”

-‐ Carlos Ghosn, CEO of Nissan Motor Co, Ltd.

INCREM

ENTAL VS D

ISRUPTIVE STRATEGY

Automakers Google

Cars that assist humans while driving. Cars that taxi humans around.

TECHNOLO

GY DIFFEREN

CES Automakers Google

● Pre-‐mapped world: observing deltas.

● High-‐precision lidar technology. ($$$)

● RealEme view of the world. ● Sonar, radar, and camera

technology.

BU

SIN

ES

S SU

MM

AR

Y/TE

CH

NIC

AL E

NV

IRO

NM

EN

T

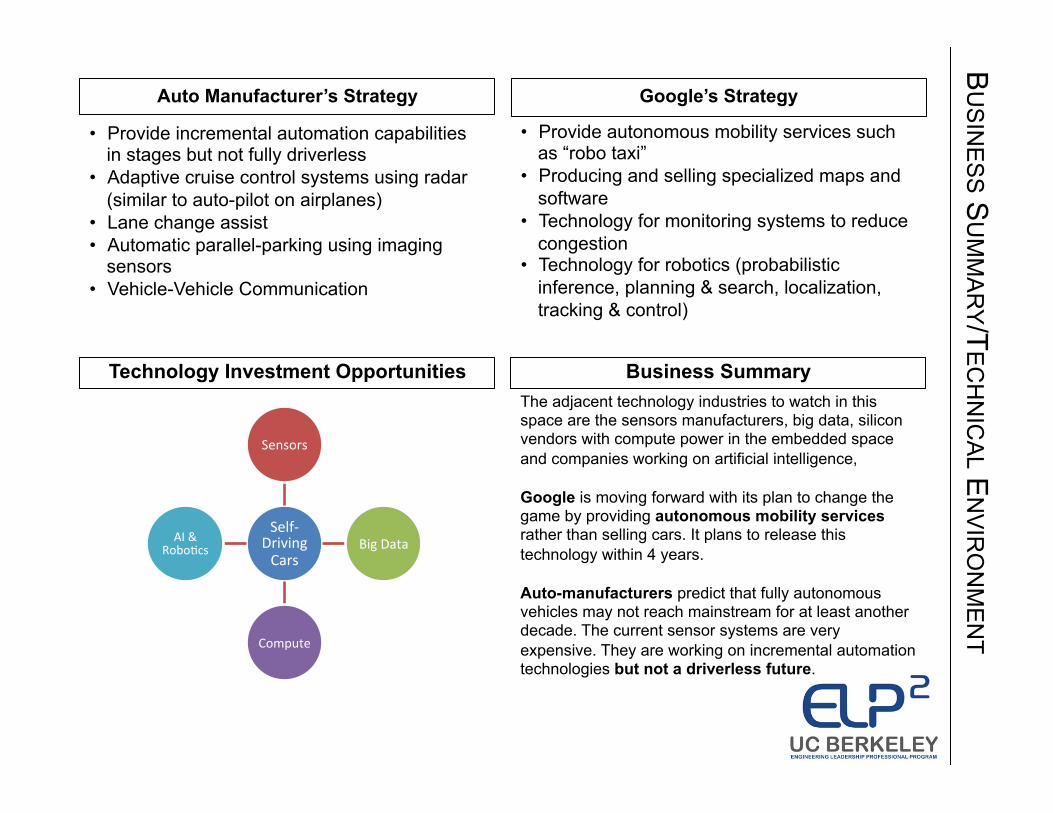

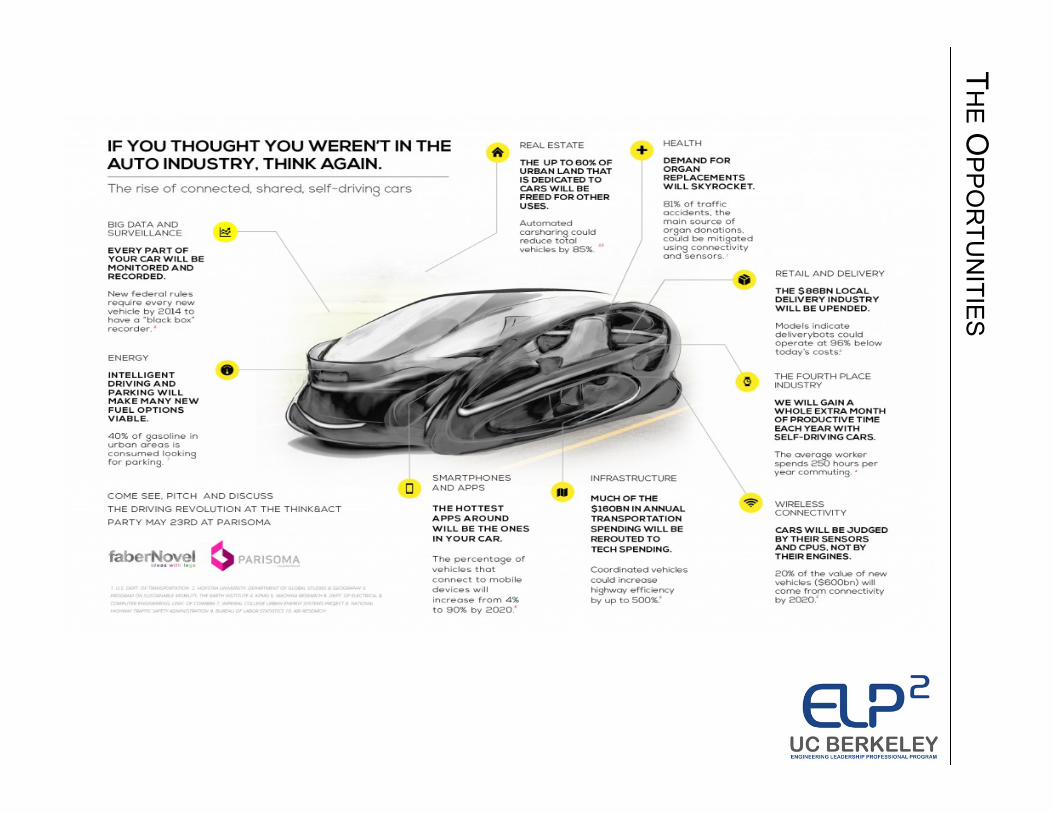

The adjacent technology industries to watch in this space are the sensors manufacturers, big data, silicon vendors with compute power in the embedded space and companies working on artificial intelligence, Google is moving forward with its plan to change the game by providing autonomous mobility services rather than selling cars. It plans to release this technology within 4 years. Auto-manufacturers predict that fully autonomous vehicles may not reach mainstream for at least another decade. The current sensor systems are very expensive. They are working on incremental automation technologies but not a driverless future.

Business Summary Technology Investment Opportunities

Google’s Strategy Auto Manufacturer’s Strategy

Self-‐Driving Cars

Sensors

Big Data

Compute

AI & RoboEcs

• Provide autonomous mobility services such as “robo taxi”

• Producing and selling specialized maps and software

• Technology for monitoring systems to reduce congestion

• Technology for robotics (probabilistic inference, planning & search, localization, tracking & control)

• Provide incremental automation capabilities in stages but not fully driverless

• Adaptive cruise control systems using radar (similar to auto-pilot on airplanes)

• Lane change assist • Automatic parallel-parking using imaging

sensors • Vehicle-Vehicle Communication

AUTOMATED PARKING ASSIST (Now) Toyota, Ford, Mercedes-‐Benz, Volkswagen,

Tesla

AdapFve Cruise Control(2016) BMW, GM, Volkswagen, Mercedes-‐Benz, Toyota

Highway Assist (2018) Nissan, Mercedes-‐Benz, GM

Driverless Car (2030) Nissan, Mercedes-‐Benz

Highway Auto Driving (2020) Nissan, Mercedes-‐Benz

ROADM

AP Google Automakers

Driverless Car (Now to 2020)

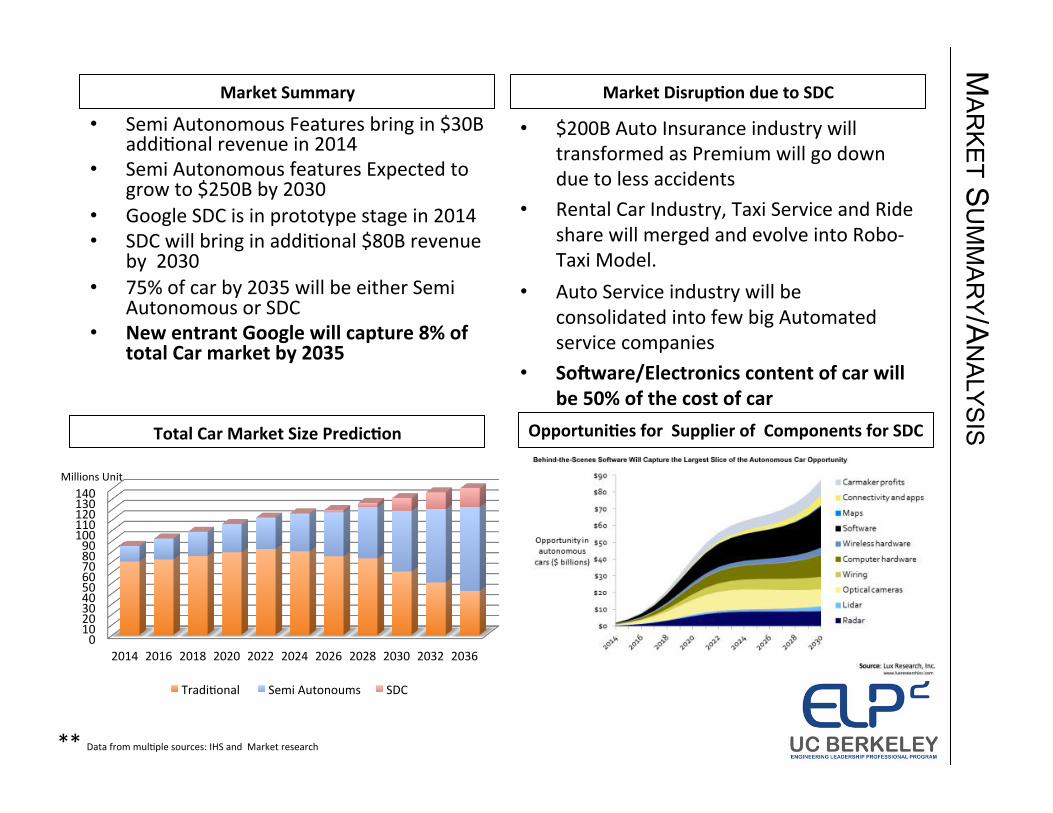

Market DisrupFon due to SDC Market Summary

Total Car Market Size PredicFon

MA

RK

ET S

UM

MA

RY/A

NA

LYS

IS

0 10 20 30 40 50 60 70 80 90

100 110 120 130 140

2014 2016 2018 2020 2022 2024 2026 2028 2030 2032 2036

TradiEonal Semi Autonoums SDC

• Semi Autonomous Features bring in $30B addiEonal revenue in 2014

• Semi Autonomous features Expected to grow to $250B by 2030

• Google SDC is in prototype stage in 2014 • SDC will bring in addiEonal $80B revenue

by 2030 • 75% of car by 2035 will be either Semi

Autonomous or SDC • New entrant Google will capture 8% of

total Car market by 2035

• $200B Auto Insurance industry will transformed as Premium will go down due to less accidents

• Rental Car Industry, Taxi Service and Ride share will merged and evolve into Robo-‐Taxi Model.

• Auto Service industry will be consolidated into few big Automated service companies

• SoVware/Electronics content of car will be 50% of the cost of car

Millions Unit

OpportuniFes for Supplier of Components for SDC

** Data from mulEple sources: IHS and Market research

RE

GU

LATOR

Y FA

CTO

RS: S

TATE AN

D FE

DE

RA

L Bill Year License Routes Driver’s Seat

Occupant(1) Distracted

Driving Ban(2) Vehicle OEM

Liability Safety & OperaFng Standards

NV AB 511 SB 140

✓ 2011 TesEng for now Designated state highways

Lic driver & passenger req.

exempt when autonomous

exempt TBD by NV DOT

CA SB 1298 ✓ 2012 Mandate for tesEng and public operaFon

Not explicitly restricted

Lic. driver req. exempt when autonomous

not exempt Due from CA DMV before Jan 2015(3)

FL HB 1207 SB 1768

2012 TesEng only Not explicitly restricted

Lic. driver req. exempt Draier report was due Feb 2014

MI SB 169 ✗ 2013 TesEng only Not explicitly restricted

Lic. driver req. MI DOT to submit report by Feb 2016

CO SB 13-‐016 ✗ 2013 TesEng only Lic. driver req. with kill switch

exempt when autonomous

Bill indefinitely tabled by Sen. Brophy ciEng transportaEon commijee opposiEon

(1) Driver’s seat occupant must be a licensed driver with access to steering, throale, and brake controls. (2) Ban on use of cell phones and texFng while driver is operaFng the vehicle. (3) Intent for public operaFon by Jun 2015.

State Legislation

• “Preliminary Statement of Policy” 14-13 released May 30th, 2013. • Begun 4 year safety standards study, 1st phase to be completed in 2017. • Research includes “vehicle to vehicle” communication technology. • Encourages states to allow testing of self-driving. • Does NOT recommend states currently allow public operation. • Else, licensed occupant in driver’s seat should be required. • Suggests operators have special training and licensing

Federal : NHTSA

Level DefiniFon Example / ExplanaFon

Level 0 No AutomaEon driver always in complete control

Level 1 FuncEon-‐specific AutomaEon e.g. stability control or brake assist

Level 2 Combined FuncEon AutomaEon two or more automated funcEons

Level 3 Limited Self-‐Driving AutomaEon “the Google car” 2013, BMW X5

Level 4 Full Self-‐Driving AutomaEon driver not available at any Eme hjp://cyberlaw.stanford.edu/wiki/index.php/Automated_Driving:_LegislaEve_and_Regulatory_AcEon

Federal : NTSB

• Require EDRs (event data recorders, i.e. “black boxes”).

LEGAL ISSUES Automakers Google

● States currently allow only tesFng of self-‐driving vehicles.

● Federal government study completes only in 2017.

● California most likely state to allow public operaFon.

● NaEonwide support for assisFve technology (e.g, adapEve cruise control).

● Future technology can follow law changes hand-‐in-‐hand.

LIA

BILITY A

ND E

THIC

S Auto Insurance Industry

• Consumer Watchdog society to CA DMV on proposed regulations (03/11/2013) – “… gather only the data necessary to operate the vehicle and retain that data only as long

as necessary for the vehicle’s operation”.

• Poll conducted by Alliance of Automobile Manufacturers in 06/2013 highlighted the following consumer concerns: – 75% : operating software will be used to collect personal data – 70% : data will be shared with the government – 81% : hackers may gain control of vehicle

• FBI Strategic Issues Groups – report obtained 07/2014 – “get away” vehicles – Terrorist attacks – Criminal “multi-tasking”

Privacy & Security Concerns

~$200B : 2013 US Auto Insurance Premiums (Private & Commercial)

• Traditional insurance law – vehicles are insured not drivers.

• For Level 4 vehicles, does Private Motor Vehicle Insurance è Manufacturer Product Liability Insurance?

• Black Boxes è Easier fault determination?

13%

87%

2013 Premiums

Commercial

Private

5%

68%

25% 2%

2013 Costs & Profit

Profit

Claims

Overhead

Taxes

Source: The Insurance InformaEon InsEtute

Source: NaEonal AssociaEon of Insurance Comissioners

Can the auto insurance industry survive a 90/90 world?

90% fewer private cars è 90% drop in private premiums è $53B industry?

90% fewer accidents è 90% fewer costs in claims è 90% drop in premiums è$20B industry?

Source: The Eno TransportaEon FoundaEon

WIN

NE

RS / LO

SE

RS

** Data from mulEple sources: IHS and Market research

Losers Winners

Intelligent Traffic Highway & Mapping Ø IBM Ø Google

SDC Adopters Ø Google Ø Nissan Ø Audi Ø Mercedes Ø Toyota Ø Tesla

Integrated Component Suppliers

Ø BOSCH Ø ConEnental Ø Denso

Rental & Ride Sharing Companies

Ø AVIS, Hertz Ø UBER, LYFT

Auto Manufacturer Ø Reduce car sales Ø Low Margins

Taxi Services

Auto Insurance Companies Ø Reduce Premiums Ø New model for collision

coverage

Auto Service Industry Ø ConsolidaEon with few

survivors

Summary

BACKUP SLIDES

TH

E OP

PO

RTU

NITIE

S

TH

E EC

ON

OM

IC IM

PAC

T

Morgan Stanley esEmates that self-‐driving vehicles could deliver the following: Ø $1.3 Trillion in annual savings to the

U.S.Economy Ø $507 Billion in annual producEvity gains Ø $488 Billion in annual accident cost

reducEon savings Ø $158 Billion in annual fuel cost savings Ø $138 Billion in annual producEvity

savings from less congesEon

BE

NE

FITS O

F SE

LF-DR

IVIN

G C

AR

S

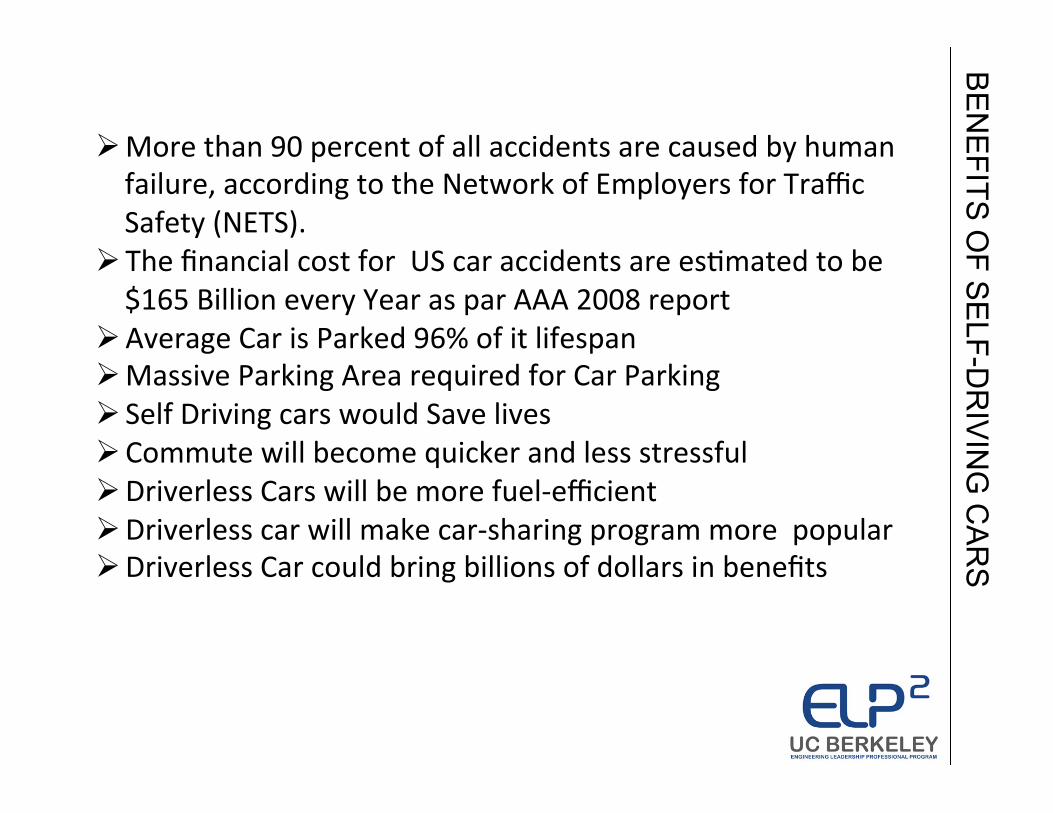

Ø More than 90 percent of all accidents are caused by human failure, according to the Network of Employers for Traffic Safety (NETS).

Ø The financial cost for US car accidents are esEmated to be $165 Billion every Year as par AAA 2008 report

Ø Average Car is Parked 96% of it lifespan Ø Massive Parking Area required for Car Parking Ø Self Driving cars would Save lives Ø Commute will become quicker and less stressful Ø Driverless Cars will be more fuel-‐efficient Ø Driverless car will make car-‐sharing program more popular Ø Driverless Car could bring billions of dollars in benefits

Self Driving Car Market Forecast

-‐2000000

0

2000000

4000000

6000000

8000000

10000000

12000000

14000000

2015 2020 2025 2030 2035 2040

SDC Volume forcast by IHS

SDC Volume forcast

$50,000.00

$10,000.00 $7,000.00

$1,000.00 $0.00

$10,000.00

$20,000.00

$30,000.00

$40,000.00

$50,000.00

$60,000.00

2010 2015 2020 2025 2030 2035

Cost of SDC Feature Add By IHS

Cost of SDC Feature Add

29%

20% 24%

27%

SDC Market Share Forcast by Region by IHS (2030)

USA

Europe

China

Others

RO

AD

MA

P