Embed Size (px)

Citation preview

Securities Regulation Summary

General Introduction

Definition: The point of securities law is to govern the capital raising process. It is the body of law that governs how a business can raise money. It governs how a stock is traded, and provides for the ongoing disclosure requirements.

Securities Law has two concerns:(a) Protecting investors(b) Ensuring efficiency

…and possibly a third concern—confidence in markets

Three Approaches to Security Law

1. Neoclassical Law and EconomicsIndividuals should be left alone to bargain. If someone accepts to buy X security at Y price that is because they want; they are best situated to know that that is a good bargain, not a third party. Voluntary exchanges are the best way to ensure proper distribution as everyone pursues his or her self-interest. Neoclassical economists are skeptical as to the ability of government to control regulatory exchanges efficiently. Where there is a goal, it should be efficiency. Efficiency is defined as where at least one party, if not both are better off by the exchange. Where a party is worse off, inefficiency has resulted. Some role for government where the market does not work best (i.e. in disclosing information).

2. Behavioural FinanceQuestions the view that people are rational actors. Believes legal rules should respond it irrational behaviour. Examples include that people will often prefer the status quo, even if the quo is not efficient, that people will get rid of good investments too early, will keep bad investments too long and deal with all bad problems at once.

3. Socio-legal PositionFocuses on the regulators. Wonders about who the winners and losers are when the rules are made. Scholars try to calculate who wins and who loses when issuers are required to issue 100 page prospectuses.

Sources of Security Law

StatuteOntario Securities Act

National Instruments- Issued by the X, these are not binding but most provinces choose to follow them- Require ratification from the provincial government

Local Rules- Can be issued by the regulator without comment from the provincial government

Policies- Not binding- Often issued in conjunction w/ NIs to act as a guideline or explanation

Admin Law Note:

Rules are subject to a notice and comment procedure

HistorySecurities law has moved away form its caveat emptor roots. In the early 20th century, Canada introduced “blue sky” legislation, meaning to focus on the sellers and on fraud issues. Later, regulators realized that they needed to do more front-end and back-end. In the mid 40s and mid 60s as a result of the Kimber committee, security regulation moves from front end concern with initial offering information but with ongoing release disclosure requirements. Today, securities regulation is marked by vigorous front- and back-end securities regulation.

Our Federal System

Provinces have clamed authority for securities regulation under s. 92, while the federal government makes claims under . 91

Feds as trade and commerce Provinces as property and civil rights History shows the provinces asserting their authorities

Mayland and Mercury Oils Limited v. Lymburn and Frawley (1932)

The defendant argued that it would be difficult for federally incorporated companies to operate under various provincial regimes and that such authority was ultra vires. The Privy Council confirms that regulating securities is within the provincial government’s powers.

IRWIN LAW says: “…the PC held that properly crafted provincial securities laws could indeed apply to federal companies. Specifically, such laws are valid as long as they do not require federal companies to register provincially before they sell securities.”

R v. Smith (1960)

The defendant was charged w/ issuing a false prospectus. The defendant argued that the provincial sanctions were too similar to criminal charges and were therefore ultra vires. The SCC ruled that this was complementary, not contradictory. The Criminal Code had no provisions for what a prospectus should contain, whereas the provincial code did. The

SCC affirms the province’s authority to regulate securities and to sanction violations under s. 92.

IRWIN LAW says: “In Smith, the court determined that there was “no repugnancy” between what is now section 400 of the Criminal Code and the legislative predecessor to what is now section 122 of the OSA….the OSA and the Criminal Code provisions could continue to co-exist because the provincial provision was not one “the pith and substance of what is to prohibit an act with penal consequences.” The main purpose of the provincial enactment was instead “to ensure the registration of persons and companies before they are permitted to trade in securities themselves.”

R. v. W. McKenzie Securities Limited 1966

Ontario broker solicits sales in Manitoba via mail. Manitoban teacher purchases, complains and ultimately buys more. Purchaser took action against said broker for not registering in Manitoba. The defendant argued that Manitoba would be overstepping its authority by regulating an Ontario broker, which maintained no Manitoba office. The Court of Appeal rules that by soliciting and selling securities to Manitobans, the defendant was subject to Manitoban security regulation. Evidence that the court is going to broadly define working within a province. NOTE: A broker, not an issuer. Multiple Access Ltd. v. McCutcheon (1982)

Ruled that federal and provincial regime need not be exclusive. As long as compliance with one does not put one at odds with the other, there is no conflict or authority. Duplication in laws is defined as acceptable. Thus, regulators have a variety of remedial options available.

Irwin Law quotes: “Parliament has not yet enacted any comprehensive scheme of securities legislation. To date the Canadian experience has been that the provinces have taken control of the marketing of securities, differing in this respect from the U.S. where the Securities and Exchange Commission has regulated trading and primary distribution of securities. I should not wish by anything said in this case to affect prejudicially the constitutional right of Parliament to enact a general scheme of securities legislation pursuant to its power to make laws in relation to interprovincial and export trade and commerce. This is of particular significance considering the interprovincial and indeed international nature of the securities industry.

Quebec (Sa Majeste du Chef) v. Ontario Securities Commission SCC [Asbestos]

American company took over the defendant by agreement. Minority shareholders, however, did not get an offer for their shares. Ontario minority shareholders sued. Question: Was the fact that some of the shareholders were Ontarians enough to warrant OSC involvement?

The SCC rules that by selling shares to Ontario purchasers, the Quebec defendant had brought itself within the ambit of OSC regulation. NOTE: This case is perhaps on the outer limit. Raises questions as to how many Ontario purchasers need to be involved and concerns for extra-national corporations.

Irwin Law says: “The court ruled that not even a transactional nexus to Ontario is required to trigger Ontario’s constitutional jurisdiction. All that is required to invoke the public interest powers, as a matter of constitutional law, is that the transaction have an effect on Ontario shareholders sufficiently to prejudice the public interest.”

“It appears that the public interest sanctions in the OSA may be invoked even where there is no security, and even where the transaction in question takes place outside the jurisdiction, so long as the transaction has a prejudicial impact on Ontario security holders.”

CRITICISM OF THIS DECISION:

“Briefly, critics were concerned that the court sanctioned the application of provincial securities laws to extraprovincial actions in circumstances where such actions had, at most, an indirect effect on Ontario residents (in this case, those minority shareholders of ACL who resided in Ontario).” Says two problems:

“First, it could seriously erode the traditional Canadian constitutional division of powers. [i.e. when things cross provincial borders, the feds take over; however, any such transaction has a tangential effect on any province it steps into]”“Second, the same transaction may have indirect effects on the residents of several provinces, thus exposing market actors to several different, and perhaps contradictory, provincial regulatory schemes.”

Global Securities Corp v. British Columbia (Securities Commission)

B.C. securities regulator provided information on an issuer to the S.E.C. Q: Was providing data on an issuer to the American regulator ultra vires? The SCC rules that it is necessary for Canadian regulators work with each other and with foreign regulators to ensure the efficiency and stability of the securities market. The SCC emphasizes the minor role of helping the U.S. and pays less attention to the matter of “due administration of securities law in B.C.”

Irwin Law says: OSC has the power to both order an investigation and examination not only to enforce Ontario securities law, but also “to assist in the due administration of the securities laws or the regulation of the capital markets in another jurisdiction.”

“The constitutional validity of this extraterritorial aspect of the comparable investigation power in the B.C. Securities Act was recently upheld by the SCC in Global…”

“Going Federal”: can we and should we?

Pro: Governor of the Bank of Canada, most issuers, foreign trading partners and economists. Con: Quebec and B.C.

Several reports and studies on this topic. Most famous include the Porter Report and the Wise Persons Committee. All have recommended a federal system. While many have issued legal opinions that it is possible, the concerns are that constitutional challenges may prevent the federal government from assuming this power and the provinces, with 70 years of jurisprudence affirming their authority in securities matters, may fight it to continue garnering revenue. Some argue that were the Federal government to create a federal regulator, it could assume dominance through the doctrine of primacy to render the existing legal framework inoperable.

Why Provincial? Opportunities for complaints

being filed in separate markets Avoids the Toronto-centric

approach a federal regulator would likely adopt

Being new might result in a painful transition period

Why Federal? Ease of markets Harmony of practices and

efficient markets Increased foreign involvement by

issuers and purchasers skeptical of Canada’s varying jurisdictions

Costly and inefficient duplication Inconsistency of prov. schemes

Markets

The primary market is for the initial offering of securities, whether in an IPO or a PO

The secondary market is for the trading of seasoned securities among investors

The involved parties are the issuers, the purchasers and the intermediaries (underwriters).

“issuer” means a person or company who has outstanding, issues or proposes to issue, a security; (“émetteur”)

“underwriter” means a person or company who, as principal, agrees to purchase securities with a view to distribution or who, as agent, offers for sale or sells securities in connection with a distribution and includes a person or company who has a direct or indirect participation in any such distribution, but does not include,

(a) a person or company whose interest in the transaction is limited to receiving the usual and customary distributor’s or seller’s commission payable by an underwriter or issuer,

(b) a mutual fund that, under the laws of the jurisdiction to which it is subject, accepts its shares or units for surrender and resells them,

(c) a company that, under the laws of the jurisdiction to which it is subject, purchases its shares and resells them, or

(d) a bank listed in Schedule I, II or III to the Bank Act (Canada) with respect to securities described in paragraph 1 of subsection 35 (2) or to such banking transactions as are designated by the regulations; (“souscripteur à forfait”)

Canada’s Markets

Canada has a variety of markets. However, there is a general trend toward competition and consolidation (including privatization).

Exchanges are different from electronic trading systems.

Exchanges guarantee the execution of a sale according to its listed price. Consequently, exchanges have a listing component. If the exchange cannot find a buyer or a seller, they will act as a principle to do so themselves. In practice, this means various dealers take on the responsibility to fulfill this function with various securities as buyers/sellers of last resort.

TSX (Toronto)Canada’s largest and most seasoned market, dealing in blue chip companies. Canada’s largest issuers, senior equities, rely on this exchange. The TSX is privatized. It is regulated by RS (Market Regulation Services), of which it is a major shareholder.

TSX Venture (Calgary)

Handles junior equities and is considered a specialized market for oil, gas and resource corporations. Has less onerous listing requirements and often features that do not yet qualify for TSX. Micro-cap issuers represent 76 percent of issuers and small-cap 23 percent.

NGX

A TSX exchange market for the trading and clearing of natural gas and electricity contracts.

CNQ

A new (2004) CDN stock exchange specializing in equity securities for emerging companies using innovative trading technologies. It is web-based. Offers issuers reduced costs in raising capital, streamlined regulatory process and a market model that maximizes liquidity by offering features of an auction market and dealer market.

Bourse de Montreal (Montreal)

The Montreal Exchange trades in derivatives, which are securities, such as an option or futures contract, whose value depends on the performance of an underlying security or asset. Considered a risky but essential part of the modern market. Prices are usually determined by supply and demand and most commonly, futures and options are traded.

WHAT IS THE DIFFERENCE BETWEEN DERIVATIVES AND SHARES?

The subtle, but crucial, difference is that while shares are assets, derivatives are usually contracts (the major exception to this are warrants and convertible bonds, which are similar to shares in that they are assets).

So what? Well, we can define financial assets (e.g. shares, bonds) as: claims on another person or corporation; they will usually be fairly standardised and governed by the property or securities laws in an appropriate country.

On the other hand, a contract is merely: an agreement between two parties, where the contract details may not be standardised.

Possibly because it is thought that investors may be wary of the woolly definition of derivatives, one frequently comes across references to "derivatives securities" or "derivatives products". These "securities" and "products" sound fairly solid, tangible things. But in many cases these terms are rather inappropriately applied to what are really contracts.

An option contract allows the holder to buy (call option) or sell (put option) a specified underlying asset by a specified date at a specified price.

A futures contract requires the seller to deliver a specific asset (or cash equivalent) to the buyer on the specified date for a predetermined price.

Irwin Law says: “In fact, every derivative security, no matter how complex, can be characterized as either an option contract, a future (or forward) contract, or a (frequently elaborate) combination of the two. The term derivative security is an umbrella term used to refer to a vast range of different types of financial instruments whose values vary with the underlying interests.”

Canadian Derivatives Clearing Corporation

The issuer, clearinghouse, and guarantor of interest rate, equity and index derivative contracts on the Bouse (as well as other markets on a contractual basis). Members must maintain margin deposits to cover market risk.

Winnipeg Commodity Exchange

The national commodities futures and option exchange.

NASDAQ Canada

America’s largest electronic stock market in the world. Entered the CDN market to link CDN issuers and institutional investors w/ a global trading network. NOTE: NASDAQ runs all of its operations in the U.S. and seems to have had limited success in Canada.

Issuers

“issuer” means a person or company who has outstanding, issues or proposes to issue, a security; (“émetteur”)

Canada has only a small group of issuers that are national and international in scope. Indeed, only 100 CDN sellers are cross-listed w/ U.S. markets. There are roughly 777 companies w/ a market capitalization above $500 mil.

Issuers flock to certain markets based on area of specialty. Alberta—oil and gas and mining; B.C.—micro-cap issuers looking for less than $300,000; Ontario—financial expertise.

Broker

“dealer” means a person or company who trades in securities in the capacity of principal or agent; (“courtier”)

This is the intermediary who assists in the trade. On the purchaser’s behalf, the broker buys or sells a security on the market. Online brokerages do not trade on the market; rather, they do your trade on your behalf at a third-party market. The law requires that they be registered, which requires a minimum of tested competence.

There is a distinction between a full service brokerage which offers competent financial advice and charges a premium on trades and discount brokerages which hold out their services as nothing beyond effecting trades.

Pearson v. Boliden (2002)

Albertan purchasers wished to sue under Ontario law (preferable to Albertan laws) w/ a class of Ontarian plaintiffs. The court ruled that purchasers must sue under their own provincial regime. The real answer to this problem is to instigate national standards.

Mutual Reliance (National Policy 43-201)

Ostensibly, an issuer would only have to seek approval from home province regulator and other provincial regulators would rubberstamp approval. In practice, however, provinces could opt out, causing delays to the issuer. This could add serious transaction costs to the issuer as well as resulting in the issuer missing a window of opportunity (capital markets are time sensitive). This led to the passport system.

The Passport System

The Passport System is a response to the criticisms of the Wise Persons Committee. This results from NI 11-101. The province of the head office of each issuer would become its

principle regulator. All provinces who have ratified NI 11-101 would accept the approval of the regulatory province.

Ontario has refused to participate, noting that this system does move toward a unilateral federal system.

Consequently, Ontario issuers have, until the near future, had to seek approval by either B.C. or Quebec, depending on the issue. As of March 2008, if your principle regulator is Ontario, Ontario is the only province from which an issuer needs approval. Cynics are concerned that this move will prevent a future national security scheme from being implemented.

Enforcement concerns

RCMP has authority to persecute securities violations under the Criminal Code.

The Ontario Securities Act includes offences in s. 122: 122. (1) Every person or company that,

(a) makes a statement in any material, evidence or information submitted to the Commission, a Director, any person acting under the authority of the Commission or the Executive Director or any person appointed to make an investigation or examination under this Act that, in a material respect and at the time and in the light of the circumstances under which it is made, is misleading or untrue or does not state a fact that is required to be stated or that is necessary to make the statement not misleading;

(b) makes a statement in any application, release, report, preliminary prospectus, prospectus, return, financial statement, information circular, take-over bid circular, issuer bid circular or other document required to be filed or furnished under Ontario securities law that, in a material respect and at the time and in the light of the circumstances under which it is made, is misleading or untrue or does not state a fact that is required to be stated or that is necessary to make the statement not misleading; or

(c) contravenes Ontario securities law,

is guilty of an offence and on conviction is liable to a fine of not more than $5 million or to imprisonment for a term of not more than five years less a day, or to both. 1994, c. 11, s. 373; 2002, c. 22, s. 181 (1).

Exemption

(1.1) Clauses (1) (a) and (b) do not apply to a statement made or given to the Commission in a submission in respect of a proposed rule or policy. 1994, c. 33, s. 7.

Defence

(2) Without limiting the availability of other defences, no person or company is guilty of an offence under clause (1) (a) or (b) if the person or company did not know and in the exercise of reasonable diligence could not have known that the statement was misleading or untrue or that it omitted to state a fact that was required to be stated or that was necessary to make the statement not misleading in light of the circumstances in which it was made. 1994, c. 11, s. 373.

Directors and officers

(3) Every director or officer of a company or of a person other than an individual who authorizes, permits or acquiesces in the commission of an offence under subsection (1) by the company or person, whether or not a charge has been laid or a finding of guilt has been made against the company or person in respect of the offence under subsection (1), is guilty of an offence and is liable on conviction to a fine of not more than $5 million or to imprisonment for a term of not more than five years less a day, or to both. 1994, c. 11, s. 373; 2002, c. 22, s. 181 (2).

Fine for contravention of s. 76

(4) Despite subsection (1) and in addition to any imprisonment imposed under subsection (1), a person or company who is convicted of contravening subsection 76 (1), (2) or (3) is liable to a minimum fine equal to the profit made or the loss avoided by the person or company by reason of the contravention and a maximum fine equal to the greater of,

(a) $5 million; and

(b) the amount equal to triple the amount of the profit made or the loss avoided by the person or company by reason of the contravention. 2002, c. 18, Sched. H, s. 11; 2002, c. 22, s. 181 (3); 2002, c. 22, s. 188 (3).

Same

(5) If it is not possible to determine the profit made or loss avoided by the person or company by reason of the contravention, subsection (4) does not apply but subsection (1) continues to apply. 1994, c. 11, s. 373.

Definitions: “loss avoided”, “profit made”

(6) In subsections (4) and (5),

“loss avoided” means the amount by which the amount received for the security sold in contravention of subsection 76 (1) exceeds the average trading price of the security in the twenty trading days following general disclosure of the material fact or the material change; (“perte évitée”)

“profit made” means,

(a) the amount by which the average trading price of the security in the twenty trading days following general disclosure of the material fact or the material change exceeds the amount paid for the security purchased in contravention of subsection 76 (1),

(b) in respect of a short sale, the amount by which the amount received for the security sold in contravention of subsection 76 (1) exceeds the average trading price of the security in the twenty trading days following general disclosure of the material fact or the material change, or

(c) the value of any consideration received for informing another person or company of a material fact or material change with respect to the reporting issuer in contravention of subsection 76 (2) or (3). (“profit réalisé”) 1994, c. 11, s. 373.

Consent of Commission

(7) No proceeding under this section shall be commenced except with the consent of the Commission. 1994, c. 11, s. 373.

Trial by provincial judge

(8) The Commission or an agent for the Commission may by notice to the clerk of the court having jurisdiction in respect of an offence under this Act require that a provincial judge preside over the proceeding. 1994, c. 11, s. 373.

Additional remedies

122.1 (1) If a person or company is convicted of an offence under this Act, the court may, in addition to any penalty, order the convicted person or company to make restitution or pay compensation in relation to the offence to an aggrieved person or company. 2006, c. 33, Sched. Z.5, s. 12.

Notice

(2) If a court makes an order for restitution or compensation, it shall cause a copy of the order or a notice of the content of the order to be given to the person or company to whom the restitution or compensation is ordered to be paid. 2006, c. 33, Sched. Z.5, s. 12.

Filing

(3) An order for restitution or compensation may be filed with a local registrar of the Superior Court of Justice and the responsibility for filing shall be on the person or company to whom the restitution or compensation is ordered to be paid. 2006, c. 33, Sched. Z.5, s. 12.

Enforcement

(4) An order for restitution or compensation filed under subsection (3) may be enforced as if it were an order of the court. 2006, c. 33, Sched. Z.5, s. 12.

Postjudgment interest

(5) Section 129 of the Courts of Justice Act applies in respect of an order for restitution or compensation filed under subsection (3) and, for that purpose, the date of filing shall be deemed to be the date of the order. 2006, c. 33, Sched. Z.5, s. 12.

Limitation

(6) A person or company is not entitled to participate in a proceeding in which an order may be made under this section solely on the basis that the person or company has a right of action against a defendant to the proceeding or that the person or company may be entitled to receive an amount under the order. 2006, c. 33, Sched. Z.5, s. 12.

Civil remedies protected

(7) A civil remedy for an act or omission is not affected by reason only that an order for restitution or compensation under this section

has been made in respect of that act or omission. 2006, c. 33, Sched. Z.5, s. 12.

The Ontario Securities Act grants authority to punish under s. 127:

Orders in the public interest

127. (1) The Commission may make one or more of the following orders if in its opinion it is in the public interest to make the order or orders:

1. An order that the registration or recognition granted to a person or company under Ontario securities law be suspended or restricted for such period as is specified in the order or be terminated, or that terms and conditions be imposed on the registration or recognition.

2. An order that trading in any securities by or of a person or company cease permanently or for such period as is specified in the order.

2.1 An order that acquisition of any securities by a particular person or company is prohibited, permanently or for the period specified in the order.

3. An order that any exemptions contained in Ontario securities law do not apply to a person or company permanently or for such period as is specified in the order.

4. An order that a market participant submit to a review of his, her or its practices and procedures and institute such changes as may be ordered by the Commission.

5. If the Commission is satisfied that Ontario securities law has not been complied with, an order that a release, report, preliminary prospectus, prospectus, return, financial statement, information circular, take-over bid circular, issuer bid circular, offering memorandum, proxy solicitation or any other document described in the order,

i. be provided by a market participant to a person or company,

ii. not be provided by a market participant to a person or company, or

iii. be amended by a market participant to the extent that amendment is practicable.

6. An order that a person or company be reprimanded.

7. An order that a person resign one or more positions that the person holds as a director or officer of an issuer.

8. An order that a person is prohibited from becoming or acting as a director or officer of any issuer.

8.1 An order that a person resign one or more positions that the persons holds as a director or officer of a registrant.

8.2 An order that a person is prohibited from becoming or acting as a director or officer of a registrant.

8.3 An order that a person resign one or more positions that the person holds as a director or officer of an investment fund manager.

8.4 An order that a person is prohibited from becoming or acting as a director or officer of an investment fund manager.

8.5 An order that a person or company is prohibited from becoming or acting as a registrant, as an investment fund manager or as a promoter.

9. If a person or company has not complied with Ontario securities law, an order requiring the person or company to pay an administrative penalty of not more than $1 million for each failure to comply.

10. If a person or company has not complied with Ontario securities law, an order requiring the person or company to disgorge to the Commission any amounts obtained as a result of the non-compliance. 1994, c. 11, s. 375; 1999, c. 9, s. 215; 2002, c. 22, s. 183 (1); 2005, c. 31, Sched. 20, s. 8.

Terms and conditions

(2) An order under this section may be subject to such terms and conditions as the Commission may impose. 1994, c. 11, s. 375.

Cease trading order

(3) The Commission may make an order under paragraph 2 of subsection (1) despite the delivery of a report to it under subsection 75 (3). 1994, c. 11, s. 375.

Exception

(3.1) A person or company is not entitled to participate in a proceeding in which an order may be made under paragraph 9 or 10 of subsection (1) solely on the basis that the person or company may be entitled to receive any amount paid under the order. 2004, c. 31, Sched. 34, s. 5.

Hearing requirement

(4) No order shall be made under this section without a hearing, subject to section 4 of the Statutory Powers Procedure Act. 1994, c. 11, s. 375.

Temporary orders

(5) Despite subsection (4), if in the opinion of the Commission the length of time required to conclude a hearing could be prejudicial to the public interest, the Commission may make a temporary order under paragraph 1, 2 or 3 of subsection (1) or subparagraph ii of paragraph 5 of subsection (1). 1994, c. 11, s. 375.

Period of temporary order

(6) The temporary order shall take effect immediately and shall expire on the fifteenth day after its making unless extended by the Commission. 1994, c. 11, s. 375.

Extension of temporary order

(7) The Commission may extend a temporary order until the hearing is concluded if a hearing is commenced within the fifteen-day period. 1994, c. 11, s. 375.

Same

(8) Despite subsection (7), the Commission may extend a temporary order under paragraph 2 of subsection (1) for such period as it considers necessary if satisfactory information is not provided to the Commission within the fifteen-day period. 1994, c. 11, s. 375.

Notice of temporary order

(9) The Commission shall give written notice of every temporary order made under subsection (5), together with a notice of hearing, to any person or company directly affected by the temporary order. 1994, c. 11, s. 375.

The OSC hears these matters at its own board. However, fines are issued by the Courts, not by administrative bodies. This is controversial as the Board drafts rules, investigates offences, prosecutes offences and judicially decides the matter. Studies have shown that people view a lack of apparent fairness in the way OSC pursues violations (due to lack of division of powers).

The OSC is however limited in its jurisdiction by the Statutory Powers and Procedures Act.

The OSC consists of a commission level, which includes 8-10 commissioners, two vice-chars, and a single chair, staff (hundreds, divided among different divisions), and enforcement. The enforcement division consists of litigators, former RCMP and police officers, forensic accountants, who prepare files, investigate, compel witnesses and issue statements of violations.

Committee for the Equal Treatment of Asbestos Minority Shareholders v. Ontario (Securities Commission) 2001 SCC

Held: The appeal should be dismissed.

Pursuant to s. 127(1) of the Securities Act, the OSC has the jurisdiction and a broad discretion to intervene in Ontario capital markets if it is in the public interest to do so. The permissive language of s. 127(1) expresses an intent to leave it to the OSC to determine whether and how to intervene in a particular case. In exercising its discretion, the OSC should consider the protection of investors and the efficiency of, and public confidence in, capital markets generally. In addition, s. 127(1) is a regulatory provision. The sanctions under the section are preventive in nature and prospective in orientation. Therefore, s. 127 cannot be used in response to Securities Act misconduct alleged to have caused harm or damages to private parties or individuals.

The standard of review applicable in this case is one of reasonableness. The OSC is a specialized tribunal with a wide discretion to intervene in the public interest and the protection of the public interest is a matter falling within the core of the OSC’s expertise. Therefore, although there is no privative clause shielding the decisions of the OSC from review by the courts, taking into consideration that body’s relative expertise in the regulation of the capital markets, the purpose of the Act as a whole and s. 127(1) in particular, and the nature of the problem before the OSC, those factors all militate in favour of a high degree of curial deference. However, as there is a statutory right of appeal from the decision of the OSC to the courts, when this factor is considered with all the other factors, an intermediate standard of review is indicated.

Condon: The courts have proven less willing to intervene, largely due to a lack of expertise. Iacobucci was the securities expert, and since his retirement, the SCC has been reluctant to get involved.

Irwin Law says: “The SCC upheld the OSC’s decision not to make an order pursuant to its ‘public interest’ jurisdiction under section 127 of the OSA…OSC decisions still should be accorded a ‘high degree of curial deference’ because of the OSC’s specialized expertise, the purpose of the statute, and the nature of the problem before the OSC.”

The STNDRD of RVW: “intermediate” lying between the extremes of correctness on the one hand and patently unreasonable on the other.

Re: Cartaway Resources Corp. 2004

Brokers had taken Cartway, a garbage removal company, and turned it into a mining co. They persuaded several of the brokerage clients to purchase shares. They did not update the purchasers that Cartaway had changed its business to mining. The B.C. securities regulator was outraged and levied an administrative fine, citing future deterrence as its motivation.

Q: Could the B.C. Reg. issue a fine for purposes of deterrence (is that not too similar to criminal law? HELD: The appeal should be allowed and the Commission’s order restored.

The balance of factors in the pragmatic and functional analysis pointed towards the reasonableness standard of review and away from the more exacting standard of correctness. STD of RVW: Was it rational for the Reg. to issue this fine?General deterrence is an appropriate factor to consider, albeit not the only one, in formulating a penalty in the public interest. Since general deterrence is both prospective and preventative in orientation, it falls squarely within the public interest jurisdiction of securities commissions to maintain investor confidence in the capital markets.No one factor should be considered in isolation because to do so would skew the textured and nuanced evaluation conducted by the Commission in crafting an order in the public interest. Here, the imposition of the maximum penalty was rationally connected to the respondents’ conduct globally.

Investment Dealers Association (IDA)

Takes the role of defining detailed roles and record keeping for broker’s investment requirements. However, it also acts as a lobby group for brokers, raising concerns as to how it can both regulate brokers and lobby for them.

Market Regulation Services (RS)

Wholly owned subsidiary of the TSX, RS regulates the trading process, including monitoring ongoing trades. Watches for such violations as front-running (a broker dealing w/ his brokerage’s accounts prior to his clients), taking advantage of the market, and empty trading (making non-existent trades to generate market excitement). Uses complex computer programs to watch for anomalies and deviations from trading patterns. Plans for RS to merge w/ IDA, as both monitor the same individual.

Mutual Fund-Dealers Organization

Ensure ethical conduct by mutual fund dealers, especially as mutual funds are targeted at non-sophisticated retail-end investors. The TSX imposes listing requirements as well; consequently, the TS ensures that listers follow listing requirements.

Security: Definitions

“security” includes,

(a) any document, instrument or writing commonly known as a security,

(b) any document constituting evidence of title to or interest in the capital, assets, property, profits, earnings or royalties of any person or company,

(c) any document constituting evidence of an interest in an association of legatees or heirs,

(d) any document constituting evidence of an option, subscription or other interest in or to a security,

(e) any bond, debenture, note or other evidence of indebtedness, share, stock, unit, unit certificate, participation certificate, certificate of share or interest, preorganization certificate or subscription other than a contract of insurance issued by an insurance company licensed under the Insurance Act and an evidence of deposit issued by a bank listed in Schedule I or II to the Bank Act (Canada), by a

credit union or league to which the Credit Unions and Caisses Populaires Act, 1994 applies or by a loan corporation or trust corporation registered under the Loan and Trust Corporations Act,

(f) any agreement under which the interest of the purchaser is valued for purposes of conversion or surrender by reference to the value of a proportionate interest in a specified portfolio of assets, except a contract issued by an insurance company licensed under the Insurance Act which provides for payment at maturity of an amount not less than three quarters of the premiums paid by the purchaser for a benefit payable at maturity,

(g) any agreement providing that money received will be repaid or treated as a subscription to shares, stock, units or interests at the option of the recipient or of any person or company,

(h) any certificate of share or interest in a trust, estate or association,

(i) any profit-sharing agreement or certificate,

(j) any certificate of interest in an oil, natural gas or mining lease, claim or royalty voting trust certificate,

(k) any oil or natural gas royalties or leases or fractional or other interest therein,

(l) any collateral trust certificate,

(m) any income or annuity contract not issued by an insurance company,

(n) any investment contract,

(o) any document constituting evidence of an interest in a scholarship or educational plan or trust, and

(p) any commodity futures contract or any commodity futures option that is not traded on a commodity futures exchange registered with or recognized by the Commission under the Commodity Futures Act or the form of which is not accepted by the Director under that Act,

whether any of the foregoing relate to an issuer or proposed issuer; (“valeur mobilière”)

We are most concerned with def. E. However, note that “commonly known” is commonly known by investors and market experts.

Irwin Law says: “The first thing to note about this definition is that it states that the term security “includes” the various enumerations. The definition is not exhaustive: things other than those appearing on the list may also be found to be securities. It is unlikely that any court or securities regulator would have to venture outside of the list, however, because the various terms are ‘catchalls.’ Designed to cast the net as wide as possible. In fact, the definition of security is so wide that it can be reasonably asserted that only the common sense of securities regulators and the courts places limits on what will be regulated as a security.”

Factors the court considers: (1) Investor Protection: If the court perceives that the purchaser of an interest is an investor in need of legislative protection, it is likely that the interest will be defined a security. If the investor is protected by another act or is situated to protect own interests, the court is less likely to see it as a security.

(2) Expectation of profit: Where one secures money from another one the promise of profit, expect a security, especially where the expected return is to exceed the initial value of the investment

(3) Risk factor: Need not be speculative, as even some risk is sufficient (though increased risk, increased likelihood of being considered a security).

(4) Purchaser’s degree of control: less control of an investor of the money invested, the increased likelihood of legislative protection.

(5) Independent value: if there is value in the subject matter independent of the success of the enterprise, may be characterized (such as selling an interest in a real estate transaction). Does not matter that an item may have value external (i.e. land can be sold on its own).

(6) Substance over form: court cares less about what something is touted as and cares more about what it is. Does not matter if something says it is not a security.

(7) Overlap in definition: remember that the OSA’s definition includes “any investment contract”. Thus wide, wide, wide definition.

(8) U.S. caselaw: U.S. cases are usefully cited.

(9) Explicit exclusions: the act specifically excludes contracts of insurance, as well as evidence of a deposit issued by a bank (these are essentially dealt w/ under the Ban Act.

Definitions:

Bond—debt security issued by a business where there is an obligation to pay the face value of the instrument and the interest (principle is returned).

Share—an equitable interest (with an open-ended return) that can be traded on the seasoned market. If designed as such, may involve voting rights , dividends, and/or rights to assets on dissolution.

Option—Right to buy or sell a specified item at a specified price at a specified time. Risky, often given to management to motivate and reward performance.

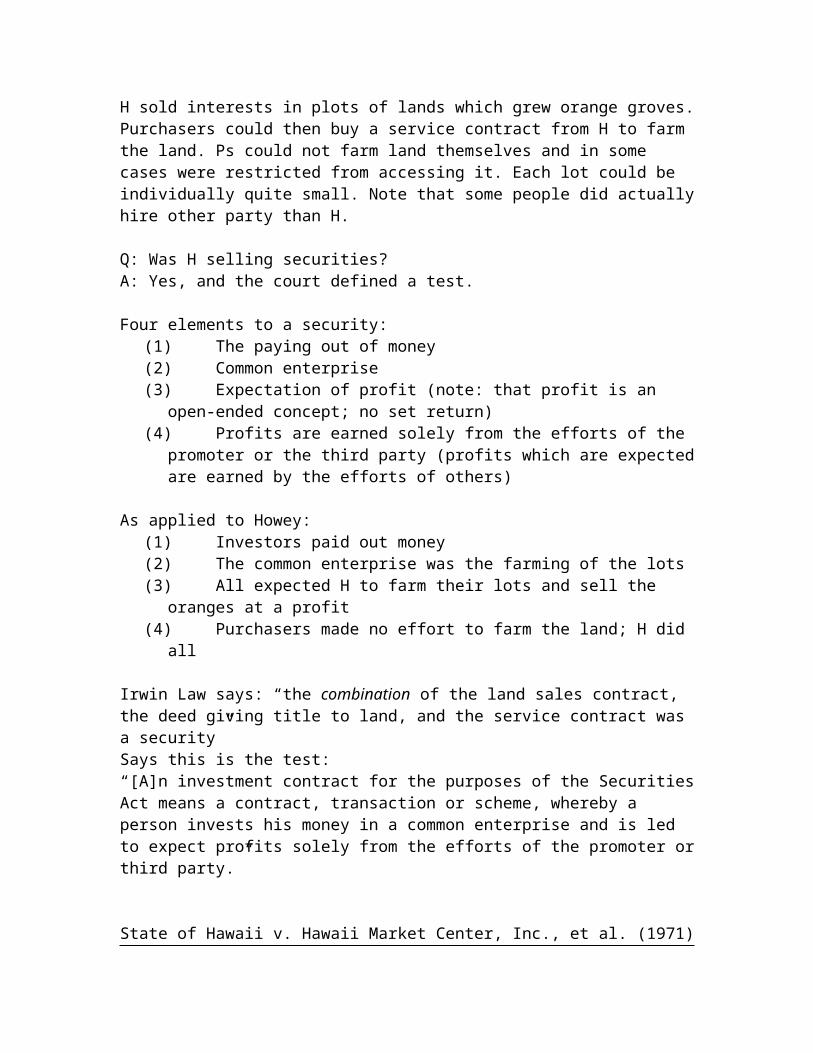

Securities and Exchange Commission v. W.J. Howey Co. et al. (1946)

H sold interests in plots of lands which grew orange groves. Purchasers could then buy a service contract from H to farm the land. Ps could not farm land themselves and in some cases were restricted from accessing it. Each lot could be individually quite small. Note that some people did actually hire other party than H.

Q: Was H selling securities? A: Yes, and the court defined a test.

Four elements to a security:(1) The paying out of money(2) Common enterprise(3) Expectation of profit (note: that profit is an open-ended concept; no set return)

(4) Profits are earned solely from the efforts of the promoter or the third party (profits which are expected are earned by the efforts of others)

As applied to Howey:(1) Investors paid out money(2) The common enterprise was the farming of the lots(3) All expected H to farm their lots and sell the oranges at a profit(4) Purchasers made no effort to farm the land; H did all

Irwin Law says: “the combination of the land sales contract, the deed giving title to land, and the service contract was a security”Says this is the test:“[A]n investment contract for the purposes of the Securities Act means a contract, transaction or scheme, whereby a person invests his money in a common enterprise and is led to expect profits solely from the efforts of the promoter or third party.”

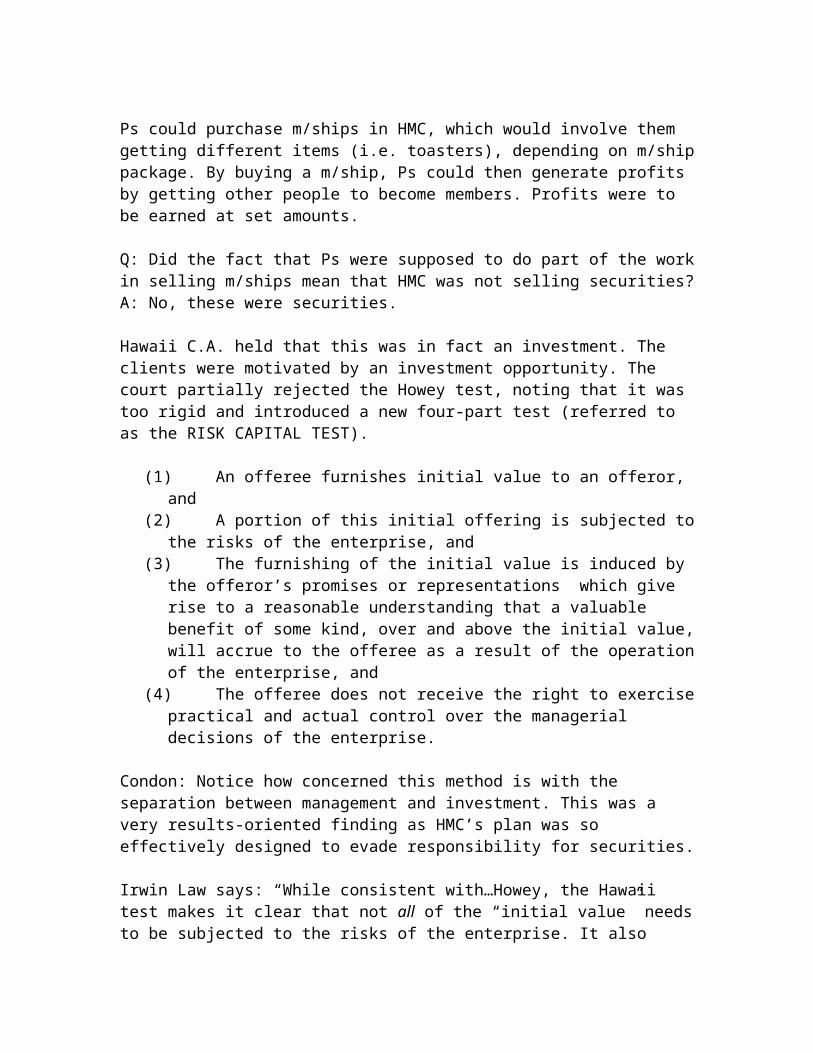

State of Hawaii v. Hawaii Market Center, Inc., et al. (1971)

Ps could purchase m/ships in HMC, which would involve them getting different items (i.e. toasters), depending on m/ship package. By buying a m/ship, Ps could then generate profits by getting other people to become members. Profits were to be earned at set amounts.

Q: Did the fact that Ps were supposed to do part of the work in selling m/ships mean that HMC was not selling securities? A: No, these were securities.

Hawaii C.A. held that this was in fact an investment. The clients were motivated by an investment opportunity. The court partially rejected the Howey test, noting that it was too rigid and introduced a new four-part test (referred to as the RISK CAPITAL TEST).

(1) An offeree furnishes initial value to an offeror, and(2) A portion of this initial offering is subjected to the risks of the enterprise, and(3) The furnishing of the initial value is induced by the offeror’s promises or

representations which give rise to a reasonable understanding that a valuable benefit of some kind, over and above the initial value, will accrue to the offeree as a result of the operation of the enterprise, and

(4) The offeree does not receive the right to exercise practical and actual control over the managerial decisions of the enterprise.

Condon: Notice how concerned this method is with the separation between management and investment. This was a very results-oriented finding as HMC’s plan was so effectively designed to evade responsibility for securities.

Irwin Law says: “While consistent with…Howey, the Hawaii test makes it clear that not all of the “initial value” needs to be subjected to the risks of the enterprise. It also sidesteps the problem created by Howey’s requirement that the purchaser be led to expect profits “solely” from the efforts of a third party, by requiring only that the purchaser have no “practical and actual control” over management decisions.”

Pacific Coast Coin Exchange of Canada v. Ontario (Securities Commission) 1978 SCC

D sells options to buy bags of silver coins to investors. Investors have choice to either buy a legit bag for full price, or could simply make a down payment of only 35 percent. Purchasers in effect acquired an option to purchase silver whenever they wanted (and would have to pay the remainder if bought on margin) provided PCC had received 48 hour notice. Clear theory is that this an investment scheme with futures overtone. D holds out bags as good investment, “a good hedge against inflation.” Moreover, D emphasizes its expert knowledge of silver market, and when necessary to enter the futures market. Like Hawaii, there is a dependence on the expertise of the offeror to guarantee a profit for all concerned parties. DISTINCTION: whereas everyone involved in Howey was involved for a common reason, here they find that everyone is interested in making money (note that this is a much lesser example of commonality as some bought silver for the sake of owning silver). The court here waters down the test element significantly. The majority in this case adopts a HOLISTISTIC approach, concerning itself with the goal of the legislature (investor protection, which is obvious where sellers are doing margin transactions). The court holds that a strict test approach does not best protect investors.

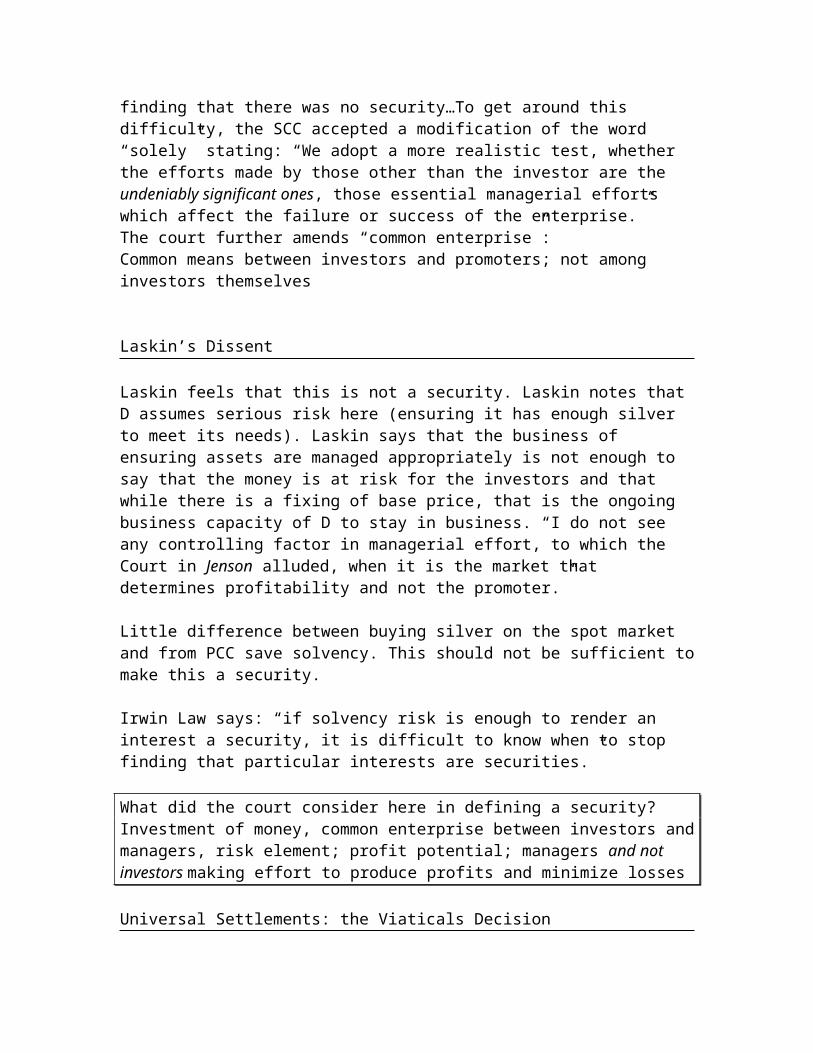

Irwin Law says: “The PCC turned on whether the interests sold by PCCE constituted ‘investment contracts.” In finding that the interests were indeed investment contracts, the SCC purported to adopt the Howey test. However, applying the Howey test literally would likely have resulted in the finding that there was no security…To get around this difficulty, the SCC accepted a modification of the word “solely” stating: “We adopt a more realistic test, whether the efforts made by those other than the investor are the undeniably significant ones, those essential managerial efforts which affect the failure or success of the enterprise.” The court further amends “common enterprise”:Common means between investors and promoters; not among investors themselves

Laskin’s Dissent

Laskin feels that this is not a security. Laskin notes that D assumes serious risk here (ensuring it has enough silver to meet its needs). Laskin says that the business of ensuring assets are managed appropriately is not enough to say that the money is at risk for the investors and that while there is a fixing of base price, that is the ongoing business capacity of D to stay in business. “I do not see any controlling factor in managerial effort,

to which the Court in Jenson alluded, when it is the market that determines profitability and not the promoter.”

Little difference between buying silver on the spot market and from PCC save solvency. This should not be sufficient to make this a security.

Irwin Law says: “if solvency risk is enough to render an interest a security, it is difficult to know when to stop finding that particular interests are securities.”

What did the court consider here in defining a security? Investment of money, common enterprise between investors and managers, risk element; profit potential; managers and not investors making effort to produce profits and minimize losses

Universal Settlements: the Viaticals Decision

Terminally ill patients would sell their life insurance policies to a company that would then partially pay out to the survivor, based on the notion it will realize a profit on the plan. The other party then continues to pay the premiums.

Q: Are viaticals a security?

Factors: There is a core contract; UniS is acting as a promoter (a recognized security role) by putting terminally ill in contact w/ investor pools; investors invest by paying for life insurance contract, risk that the party will not predecease the profitability point, managers do the research into the terminally ill;

The Court had to differentiate from Life Partners, which was not found to be a security. Key difference: in Life Partners, investors were brought on after the work was complete. Here, investors were on board and then the ill were sought. NOTE: buyers could have contact w/ the ill if they wished.

Found: Universal Settlements is a security for the above reasons.

Albino Decision

An Ontario natural resource company was compensating employees with incentive units (part of an award plan). Mr. Albino, an employee of Rio Algom was given an incentive plan whereby he would be paid the difference between the price at which the stock of RA was trading on its award, and the price at which it was trading when encashed. This was a phantom stock option (PSO) as Albino was never awarded the actual common share, just the difference in price from when he was granted the PSO and when he chose to cash it. He was charged w/ insider trading but it first had to be proved said PSO was a security, as per the act.

Q: Are PSOs recognized securities?

Held: Three judgments!!!

PM1: Not a security Not commonly recognized as such by the security experts PSOs are akin to employment contracts w/ interest in performance of the comp. Executive paid no money, was not allowed to trade, and no stock changed hands Also, only specific windows of time in which A could cash option (lim. liquidity)

PM2: Yes a security Applied dicta from Pacific Coast, and said law had to be read broadly and

purposively Relevant provision was the prohibition against insider trading, which A did PSOs are akin to derivative securities (which draw value from underlying

security) Encashing awards was a “constructive sale” Sanctions should be applied and objectives relating to insider trading would be

awarded

PM3: Refused to decide, but said OSC had jurisdiction. Refused to decide Found sufficient nexus between PSOs and capital markets for OSC to regulate Also, found A’s behaviour was “seriously prejudicial to public confidence in the

capital markets” A’s abuse of insider knowledge in encashing the awards was exactly what the law

was made to prevent

Irwin Law says: “the jurisdictional test for the issuance of a public interest order is not whether there is a security, but whether the transaction exhibits a significant connection to the capital markets of Ontario.”

While this does seem broad, Irwin Law cites Asbestos as proof the courts agree.

Trade and Distributions

A trade is:

“trade” or “trading” includes,

(a) any sale or disposition of a security for valuable consideration, whether the terms of payment be on margin, instalment or otherwise, but does not include a purchase of a security or, except as provided in clause (d), a transfer, pledge or encumbrance of securities for the purpose of giving collateral for a debt made in good faith,

(b) any participation as a trader in any transaction in a security through the facilities of any stock exchange or quotation and trade reporting system,

(c) any receipt by a registrant of an order to buy or sell a security,

(d) any transfer, pledge or encumbrancing of securities of an issuer from the holdings of any person or company or combination of persons or companies described in clause (c) of the definition of “distribution” for the purpose of giving collateral for a debt made in good faith, and

(e) any act, advertisement, solicitation, conduct or negotiation directly or indirectly in furtherance of any of the foregoing; (“opération”)

For the purposes of insider trading, trading includes purchasing and selling. For a “trade,” it is only selling, but for insider “trades” it can include the buyer.

Why worry about regulators/registrants/brokers?

They can easily manipulate customers and for the Securities Act to be triggered, it is necessary to label such actors as “trading in securities.” Most trades are conducted through brokers, with the exception of a discount brokerage.

Irwin Law notes five key points:

(1) Any sale or disposition for valuable considerationa. Gifts are excludedb. Valuable consideration can be widely defined

(2) Excludes (most) share pledgesa. Share pledges (generally as loan collateral) are excluded save in two

cases:i. The debt must have been incurred in ‘good faith’ (i.e. cannot use

this exception to avoid securities regulationii. A pledge is a ‘trade’ if the grantor is a control person

(3) Participation as a trader: receipt of an order by a registranta. Principle: Activities of professional traders can have a critical impact on

the functioning of the capital markets and must be regulated to protect investors

b. “any participation by a trader in any transaction in a security through the facilities of any stock exchange or quotation and trade reporting system” and “any receipt by registrant of an order to buy or sell a security”

(4) Acts in furtherance of a trade

a. “any act, advertisement, solicitation, conduct or negotiation directly or indirectly in furtherance of’ any of the other activities constituting a trade’

b. The law is not simply reactive, it is preventative as well(5) Trades that are not distributions

a. A trade that is not a distribution can still be regulatedb. Traders must register w/ regulators either as dealers or as advisersc. This is to ensure minimum levels of integrity, competence and financial

soundness

Re World Stock Exchange (2000) Alberta Securities Commission

Q: Does a stock offering not based in Alberta trigger Albertan securities regulation? Held: It does unless…

Factors: An offeror / broker must include disclaimers that it is clearly not part of said province’s jurisdiction and that it is limiting its business to Z jurisdiction.

POINT: Even if you are trading in a way that does not amount to a distribution, regulators are zealous enforcers of their authority.

For the relevance of the OSC’s powers, see below:

3. (1) The Ontario Securities Commission is continued as a corporation without share capital under the name Ontario Securities Commission in English and Commission des valeurs mobilières de l’Ontario in French. 1997, c. 10, s. 37.

Composition

(2) The Commission is composed of at least nine and not more than 14 members. 1997, c. 10, s. 37.

Deficiency in number

(3) If there are fewer than nine but at least two members in office, the Commission shall be deemed to be properly constituted for a period not exceeding 90 days after the deficiency in the number of members first occurs. 1997, c. 10, s. 37.

Appointment

(4) The members shall be appointed by the Lieutenant Governor in Council for such term of office not exceeding five years as the Lieutenant Governor in Council determines. A member may be reappointed. 1997, c. 10, s. 37.

Chair and Vice-Chairs

(5) The Lieutenant Governor in Council shall, by order, designate a member of the Commission as Chair and may designate one or two members as Vice-Chairs. 1997, c. 10, s. 37.

Same

(6) The Chair and each Vice-Chair holds office for the term specified by the Lieutenant Governor in Council which shall not exceed his or her term as a member of the Commission. 1997, c. 10, s. 37.

Duties of Chair

(7) The Chair is the chief executive officer of the Commission and shall devote his or her full time to the work of the Commission. 1997, c. 10, s. 37.

Duties of members

(8) The members (other than the Chair) shall devote such time as may be necessary for the due performance of their duties as members. 1997, c. 10, s. 37.

Protection from liability

(9) A member is not liable for an act, an omission, an obligation or a liability of the Commission or its employees. A member is not liable for any act that in good faith is done or omitted in the performance or intended performance of his or her duties as a member of the Commission under this or any other Act. 1997, c. 10, s. 37.

Acting Chair

(10) If the office of Chair is vacant or if the Chair is absent or is unable to act for any reason, a Vice-Chair shall act as Chair. 1997, c. 10, s. 37.

Quorum

(11) Two members of the Commission constitute a quorum. 1997, c. 10, s. 37.

Crown agency

(12) The Commission is an agent of Her Majesty in right of Ontario, and its powers may be exercised only as an agent of Her Majesty. 1997, c. 10, s. 37.

Distribution: A distribution occurs when an issuer makes a public offering of a security that has not previously been traded. The first distribution by an issuer is an initial public offering (IPO); however, subsequent issues are still labeled distribution.

“distribution”, where used in relation to trading in securities, means,

(a) a trade in securities of an issuer that have not been previously issued,

(b) a trade by or on behalf of an issuer in previously issued securities of that issuer that have been redeemed or purchased by or donated to that issuer,

(c) a trade in previously issued securities of an issuer from the holdings of any control person,

(d) a trade by or on behalf of an underwriter in securities which were acquired by that underwriter, acting as underwriter, prior to the 15th day of September, 1979 if those securities continued on that date to be owned by or for that underwriter, so acting,

(e) a trade by or on behalf of an underwriter in securities which were acquired by that underwriter, acting as underwriter, within eighteen months after the 15th day of September, 1979, if the trade took place during that eighteen months, and

(f) any trade that is a distribution under the regulations,

and on and after the 15th day of March, 1981, includes a distribution as referred to in subsections 72 (4), (5), (6) and (7), and also includes any transaction or series of transactions involving a purchase and sale or a repurchase and resale in the course of or incidental to a distribution and “distribute”, “distributed” and “distributing” have a corresponding meaning; (“placement”, “placer”, “placé”)

“distribution company” means a person or company distributing securities under a distribution contract; (“compagnie de placement”)

“distribution contract” means a contract between a mutual fund or its trustees or other legal representative and a person or company under which that person or company is granted the right to purchase the shares or units of the mutual fund for distribution or to distribute the shares or units of the mutual fund on behalf of the mutual fund; (“contrat de placement”)

“distribution to the public”, where used in relation to trading in securities, means a distribution that is made for the purpose of distributing to the public securities issued by an issuer, whether such trades are made directly or indirectly to the public through an underwriter or otherwise; (“placement dans le public”)

Distribution is triggered in three situations: (1) trade by issuers, (2) trades by control persons, and (3) sales of restricted securities held by exempt purchasers.

Canada Business Corporations Act holds that were an issuer to purchase its shares, it extinguishes said shares. A corporation cannot, according to the CBCA, hold shares in itself.

Adjustment of stated capital account

39. (1) On a purchase, redemption or other acquisition by a corporation under section 34, 35, 36, 45 or 190 or paragraph 241(3)(f), of shares or fractions thereof issued by it, the corporation shall deduct from the stated capital account maintained for the class or series of shares of which the shares purchased, redeemed or otherwise acquired form a part an amount equal to the result obtained by multiplying the stated capital of the shares of that class or series by the number of shares of that class or series or fractions thereof purchased, redeemed or otherwise acquired, divided by the number of issued shares of that class or series immediately before the purchase, redemption or other acquisition.

Cancellation or restoration of shares

(6) Shares or fractions thereof of any class or series of shares issued by a corporation and purchased, redeemed or otherwise acquired by it shall be cancelled or, if the articles limit the number of authorized shares, may be restored to the status of authorized but unissued shares of the class.

Exception

(7) For the purposes of this section, a corporation holding shares in itself as permitted by subsections 31(1) and (2) is deemed not to have purchased, redeemed or otherwise acquired such shares.

Idem

(8) For the purposes of this section, a corporation holding shares in itself as permitted by paragraph 32(1)(a) is deemed not to have purchased, redeemed or otherwise acquired the shares at the time they were acquired, but

(a) any of those shares that are held by the corporation at the expiration of two years, and

(b) any shares into which any of those shares were converted by the corporation and held under paragraph 32(1)(b) that are held by the corporation at the expiration of two years after the shares from which they were converted were acquired

are deemed to have been acquired at the expiration of the two years.

Controlled Companies: A controlled company is one in which more than 50 percent of the shares are owned by one entity (an investor or a company) or where voting rights are such that one party has the right to elect the entire board.

DEFINITIONS: 1(3) A company shall be deemed to be controlled by another person or company or by two or more companies if,

Note: On a day to be named by proclamation of the Lieutenant Governor, subsection (3) is amended by the Statutes of Ontario, 2007, chapter 7, Schedule 38, subsection 1 (4) by adding at the beginning “Except for the purposes of Part XX”. See: 2007, c. 7, Sched. 38, ss. 1 (4), 15 (2).

(a) voting securities of the first-mentioned company carrying more than 50 per cent of the votes for the election of directors are held, otherwise than by way of security only, by or for the benefit of the other person or company or by or for the benefit of the other companies; and

(b) the votes carried by such securities are entitled, if exercised, to elect a majority of the board of directors of the first-mentioned company. R.S.O. 1990, c. S.5, s. 1 (3).

For a definition of a control person see below. The bright line test prima facie holds an investor with a 20 percent or greater share a control person by default. This presumption is rebuttable where a party can show that others have greater influence. That same test, however, can find a shareholder w/ less 20 percent a control person if said investor’s influence is such that it can affect material control.

Note that through (b), where an agreement exists, a combination of persons can be deemed controlling persons if their influence is such to trigger for all effects and purposes control person status. For the most part, reporting issuers start as issuers. In the past, a commonly exploited loophole allowed parties listed on other Canadian exchanges to transfer to the TSX. However, said loophole is now gone.

“control person” means,

(a) a person or company who holds a sufficient number of the voting rights attached to all outstanding voting securities of an issuer to affect materially the control of the issuer, and, if a person or company holds more than 20 per cent of the voting rights attached to all outstanding voting securities of an issuer, the person or company is deemed, in the absence of evidence to the contrary, to hold a sufficient number of the voting rights to affect materially the control of the issuer, or

(b) each person or company in a combination of persons or companies, acting in concert by virtue of an agreement, arrangement, commitment or understanding, which holds in total a sufficient number of the voting rights attached to all outstanding voting securities of an issuer to affect materially the control of the issuer, and, if a combination of persons or companies holds more than 20 per cent of the voting rights attached to all outstanding voting securities of an issuer, the combination of persons or companies is deemed, in the absence of evidence to the contrary, to hold a sufficient number of the voting rights to affect materially the control of the issuer; (“personne qui a le contrôle”)

Reporting issuer is any issuer who has at one point issued securities after March 1, 1967, has filed a prospectus, has filed a take-over bid, has had securities listed on an Ontario stock exchange, is offering securities and is recognized by the CBCA, is the continuance of another company that was previously listed, etc.

“reporting issuer” means an issuer,

(a) that has issued voting securities on or after the 1st day of May, 1967 in respect of which a prospectus was filed and a receipt therefor obtained under a predecessor of this Act or in respect of which a securities exchange take-over bid circular was filed under a predecessor of this Act,

(b) that has filed a prospectus and for which the Director has issued a receipt under this Act,

(b.1) that has filed a securities exchange take-over bid circular under this Act before December 14, 1999,

(c) any of whose securities have been at any time since the 15th day of September, 1979 listed and posted for trading on any stock exchange in Ontario recognized by the Commission, regardless of when such listing and posting for trading commenced,

(d) to which the Business Corporations Act applies and which, for the purposes of that Act, is offering its securities to the public,

(e) that is the company whose existence continues following the exchange of securities of a company by or for the account of such company with another company or the holders of the securities of that other company in connection with,

(i) a statutory amalgamation or arrangement, or

(ii) a statutory procedure under which one company takes title to the assets of the other company that in turn loses its existence by operation of law, or under which the existing companies merge into a new company,

where one of the amalgamating or merged companies or the continuing company has been a reporting issuer for at least twelve months, or

(f) that is designated as a reporting issuer in an order made under subsection 1 (11); (“émetteur assujetti”)

Preparing, filing and offering a prospectus

Short-form regime covered by NI 44-101

Why go public?

More flexible than working w/ banks Shareholders better able to retain control Private owners can diversify their wealth (without going public, the corporation is

dependant on their continued investment) Can capitalize future plans Ongoing visibility for public company (analysts follow the stock) Can acquire other corporations through stocks (which are not taxed until cashed)

versus cash (which is taxed immediately)

Use the trading market for the securities to offer the owner of an asset securities of one’s own company as opposed to cash for consideration on the transaction

Create a base for future capital needs Attractive for investors as their investments gain liquidity

Alternatives?

Banking debt (which must a. must be paid back and b. often involves acquiescing to banking decisions)

Private placement, i.e. seeking private equityo Priced less competitivelyo Buyer wants a price that reflects their increased interest (they can liquidate

their investment as readily)o Actual restrictions on when a party can private placement

What are the negatives?

Expensive: requires ongoing costs w/ accountants, securities lawyers, etc. Increased scrutiny

o Shareholders and competitors alike can monitor reportso Information maintained on SEDR (system for electronic disclosure and

retrieval) Certain groups of shareholders expect immediate returns and have little concern

for long-term strategy Taxes on equity Potential for loss of control Reduced flexibility

Security Process

There are four stages: pre-filing, waiting period, pre-closing and post-closing. In pre-filing, the issuer files a preliminary prospectus. During the waiting period, the issuer waits for approval from the regulator. The issuer can advertise the shares during this period. The OSC does not simply approve/disapprove; there is room for negotiation. Issuers can also distribute copies of the preliminary prospectus at so-called road shows (note: obligations flow from distributing these documents; issuers must keep a record of to whom they are issued). The issuer must also practice due-diligence and inspect the prospectus (do not want to trigger s. 130). Once the prospectus has been approved, the issuer enters the pre-closing stage and can print copies of final prospectus. The cooling-off period begins to run. Finally, at post-closing, money and securities change hands. The underwriter will advise the issuer when the distribution is complete.

Prospectus required

53. (1) No person or company shall trade in a security on his, her or its own account or on behalf of any other person or company if the trade would be a distribution of the security, unless a preliminary prospectus and a prospectus have been filed and receipts have been issued fofailry onerous requirements r them by the Director. 2006, c. 33, Sched. Z.5, s. 2.

Filing without distribution

(2) A preliminary prospectus and a prospectus may be filed in accordance with this Part to enable the issuer to become a reporting issuer, despite the fact that no distribution is contemplated. R.S.O. 1990, c. S.5, s. 53 (2).

Underwriting

The underwriter sells the issuer’s securities. Why employ an underwriter?

Extensive capital markets experience Ability to assess market demand for an issuer’s securities Knowledge regarding setting the terms of the offering Providing advice w/ respect to business management, and ownership structure

changes that may be necessary to make investment more attractive

An underwriter is defined as:

“underwriter” means a person or company who, as principal, agrees to purchase securities with a view to distribution or who, as agent, offers for sale or sells securities in connection with a distribution and includes a person or company who has a direct or indirect participation in any such distribution, but does not include,

(a) a person or company whose interest in the transaction is limited to receiving the usual and customary distributor’s or seller’s commission payable by an underwriter or issuer,

(b) a mutual fund that, under the laws of the jurisdiction to which it is subject, accepts its shares or units for surrender and resells them,

(c) a company that, under the laws of the jurisdiction to which it is subject, purchases its shares and resells them, or

(d) a bank listed in Schedule I, II or III to the Bank Act (Canada) with respect to securities described in paragraph 1 of subsection 35 (2) or to such banking transactions as are designated by the regulations; (“souscripteur à forfait”)

The underwriter has a precarious position. On the one hand, they are an interested financial party with a clear stake in the issue. On the other, they have a fiduciary duty as a “gatekeeper” and is expected to assume an “adversarial” role to ensure the issue is legitimate. The underwriter is expected to act as a third-party.

YBM Magnex International Inc. OSCBC 2003

YBM was initially a magnet company that shifted industries. In this instance, YBM stands for the principle that underwriters can be pursued as well. The court noted that “The phrase “to the best of our knowledge, information and belief” carries with it a requirement to obtain information before an underwriter can make that affirmation…An underwriter must go beyond the statements of the issuer’s directors, officers and counsel and must avoid automatic reliance.” However, this is to be balanced against their limited access.

Types of Underwriter / Issuer Relationships

Issuers and underwriters can have four relationships: direct issue, “best efforts” underwriting, firm commitment and bought deal.

Direct Issue: In a direct issue, there is no underwriter (such as occurred in Google’s IPO). This rarely occurs as underwriters are the parties experienced w/ capital markets and it is often their reputation which helps ensure the success of the offering.

“Best Efforts” Underwriting: The underwriter makes no agreement to purchase offering as a principle. This is governed by NI 41-101 part 8. The underwriter is only undertaking to make the best effort to sell the securities on the issuer’s behalf. The underwriter in effect is acting as an agent for the issuer. The risk of unsold securities is strictly that of the issuer. The underwriter has 90 days to distribute the security, at which point, the distribution ends. Underwriter only collects commission on securities sold.

Firm Commitment: The underwriter makes an agreement to purchase the securities and resell them. The undertaker likely is confident that the s/he can realize a profit on the sale of the securities to the capital market, the difference being the underwriter’s spread. An example of a firm commitment is the bought deal (see below). The issuer can also agree to sell the issue at the agreed price and instead charge an underwriting fee linked to the issue price.

NOTE: An underwriter can use “market out” clauses as a way to limit liability for sales here but must contract to do so. These occur generally in unstable markets and are often contingent on some unforeseen crisis (i.e. tsunami). Indemnity clauses will allow the underwriter to indemnify if there is a mistake in the prospectus. Not clear if the court will enforce these.

Bought Deal: A form of firm commitment in which the underwriter agrees to buy all shares. These are made before the preliminary prospectus is filed. These are more common in Canadian distributions than in the U.S. These generally occur where the underwriter has lined up an institutional investor who is interested in the issue. Retail investors complain because these are often attractive issues to which they have no access (rather than the normally speculative shares aimed at the retail investor).

COIs and Underwriting

Underwriting COIs are governed by NI 33-105.

The law recognizes three potential levels of COIs:

Low Level: The underwriter and issuer are not related but are connected (the test being would a reasonable investor be right to ask if the two are independent)

Medium Level: Issuer has a relation to the underwriter.

High Level: Bank is both issuing and underwriting the security

What kind of relationships are we discussing?

Imagine an issuer who has a loan w/ BMO. Said issuer wants to reduce loan and goes to Nesbitt Burns. NB is likely to have a COI w/ BMO.

The regulator has responded by requiring such relationships be made explicit and evident to investors. Also, where the underwriter is related, a portion of the underwriting work must go to an independent underwriter. Major underwriters complained that this was simply a hand-out of work to smaller underwriters, but the government did not care.

Preliminary Prospectus

Preliminary prospectus

54. (1) A preliminary prospectus shall substantially comply with the requirements of Ontario securities law respecting the form and content of a prospectus, except that the report or reports of the auditor or accountant required by the regulations need not be included. R.S.O. 1990, c. S.5, s. 54 (1); 1994, c. 11, s. 366.

Idem

(2) A preliminary prospectus may exclude information with respect to the price to the underwriter and offering price of any securities and other matters dependent upon or relating to such prices. R.S.O. 1990, c. S.5, s. 54 (2).

As per s. 54, a preliminary prospectus is not a draft.

Receipt for preliminary prospectus

55. The Director shall issue a receipt for a preliminary prospectus forthwith upon the filing thereof. R.S.O. 1990, c. S.5, s. 55.