Embed Size (px)

Citation preview

25 October 2011 Credit Research

Sector Report

UniCredit Research page 1 See last pages for disclaimer.

Sector Report United Kingdom ■ Considerable healthy balance sheet restructuring, clarity about its future

regulatory path and its interesting spread environment, currently make the UK an attractive country for investors.

■ Economy: Moving into 2012, we expect GDP growth to accelerate as financial market tensions gradually subside and the downward trend in global growth indicators flattens out. In addition, the effect of the BoE’s asset purchases should boost growth. We expect GDP to increase by 0.8% in 2011 and 1.5% in 2012. The UK is likely to benefit from a recov-ery in its main trading partners which should spur exports and, in turn, business confidence and thus investment. In addition, the squeeze in real household disposable income seen in 2011 should moderate, as the temporary effect of the factors pushing up prices begins to wane and in-flation decelerates. As a result, we expect growth to be driven by a mod-erate acceleration in consumption and a more marked recovery in ex-ports and investment.

■ Sector drivers: The UK banking system features five major players: Bar-clays, HSBC, Lloyds, Royal Bank of Scotland and Santander UK. In some business segments, such as current accounts or SME banking, these five institutions have a combined market share of 85% to 90%. Furthermore, there are a number of banks that operate on a local or na-tional level, such as Clydesdale, or building societies, e.g. Coventry Building Society or Yorkshire Building Society. The latter are institutions that specialize in mortgage lending. On 12 September 2011, the UK In-dependent Commission on Banking (ICB) published its recommenda-tions for a reform of the British financial system. The core measure to achieve these aims is setting up a ring-fence around business entities such as retail banking in order to protect them from losses generated by other units, such as investment banking. Only ring-fenced banks shall be allowed to take deposits and provide overdrafts, purportedly with an im-plementation deadline until 2019. Moreover, while the report does not re-quire a full separation of retail and investment banking business, the ICB recommends increasing capital requirements for large ring-fenced banks. We will look into the differentiated impact of these recommendations on the individual banking segments.

■ Covered Bonds: The UK covered bond market came into existence in 2003. This market has since constantly grown, reaching a total volume of EUR 209bn as at the end of 2010. However, only around 40% is related to EUR-denominated benchmark bonds, which currently amount to EUR 85bn from eleven issuers. In March 2008, a specific UK covered bond legislation was implemented.

■ We believe that the recent spread widening is fundamentally exagger-ated. With the right timing and a focus on liquid bonds, it may be worth considering specific trades in UK bank bonds. The large UK banking groups are solidly rooted in retail business and/or part of a mutual sys-tem. As soon as market fears wane, the fundamental strength of UK banks will likely be mirrored in tighter spreads.

Contents UK Economic Outlook ________________________ 2UK Housing Market __________________________ 4UK Banking Sector___________________________ 5

Introduction, Crisis, Recovery & the ICB_________ 5A Comparison of the big 5 UK Banks_____________ 9Overview – Investment Metrics ________________ 12The Stress-Robustness of major UK Banks_______ 16Regulation ________________________________ 22The UK Covered Bond Legislation ______________ 23Overview of the UK Covered Bond Market________ 26Snapshot – UK Bank Profiles__________________ 29

Abbey/Santander _________________________ 29Abbey/Santander UK's Cover Pool Details ______ 30Barclays ________________________________ 36Barclays' Cover Pool Details_________________ 37Clydesdale ______________________________ 44Clydesdale's Cover Pool Details______________ 45Coventry Building Society___________________ 49Coventry's Cover Pool Details _______________ 50HSBC __________________________________ 54HSBC's Cover Pool Details__________________ 55Lloyds Banking Group______________________ 62Lloyds' Cover Pool Details __________________ 63Nationwide Building Society _________________ 69Nationwide's Cover Pool Details______________ 70Royal Bank of Scotland_____________________ 75RBS' Cover Pool Details ____________________ 76Standard Chartered _______________________ 82Yorkshire Building Society __________________ 88YBS' Cover Pool Details ____________________ 89

Spread Overview ___________________________ 93Investment Considerations____________________ 99

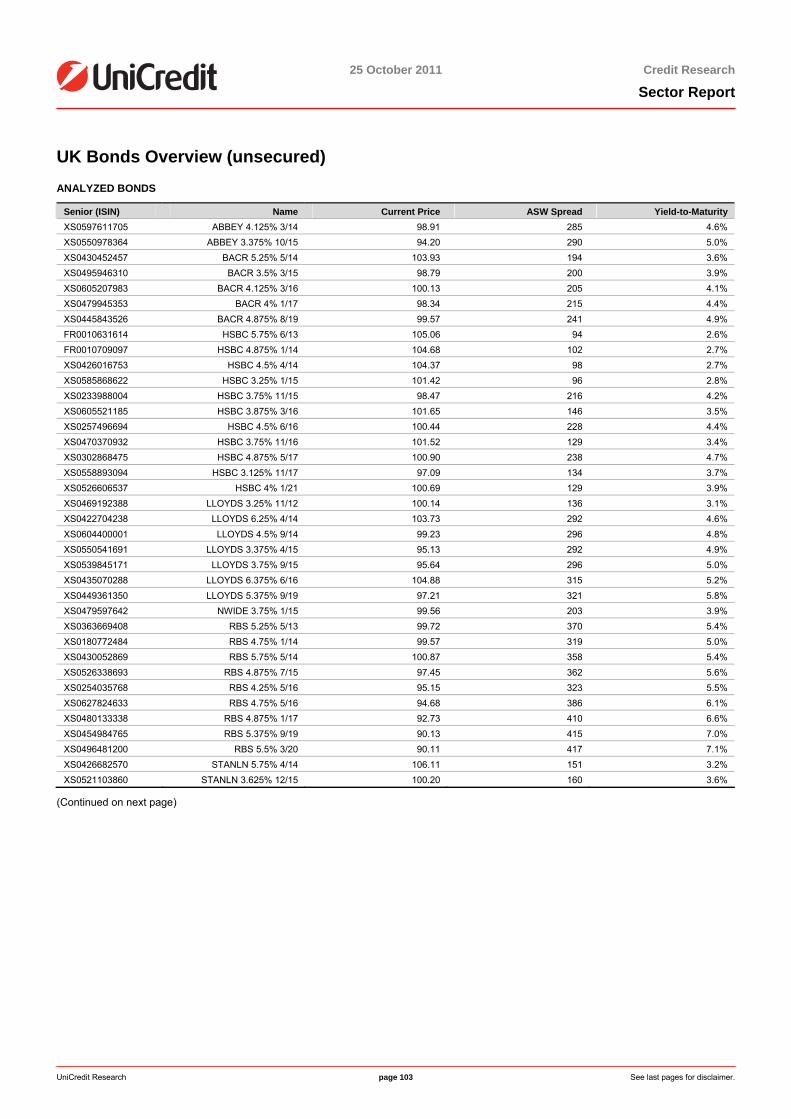

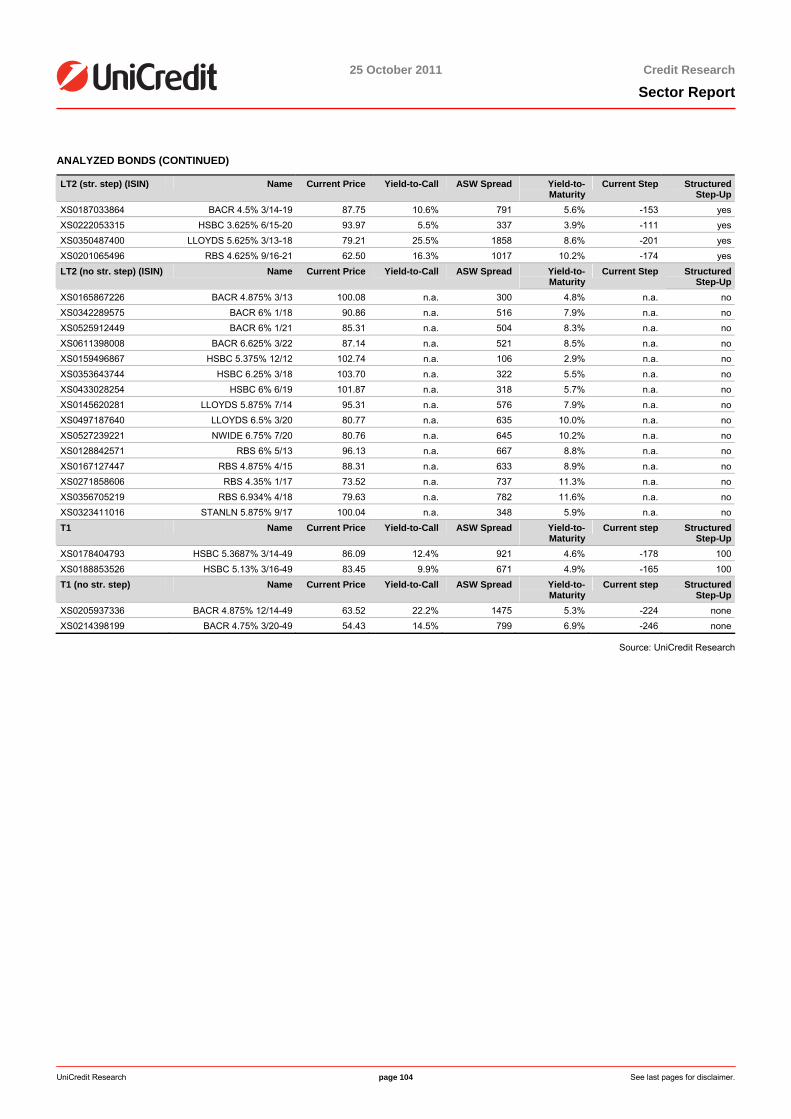

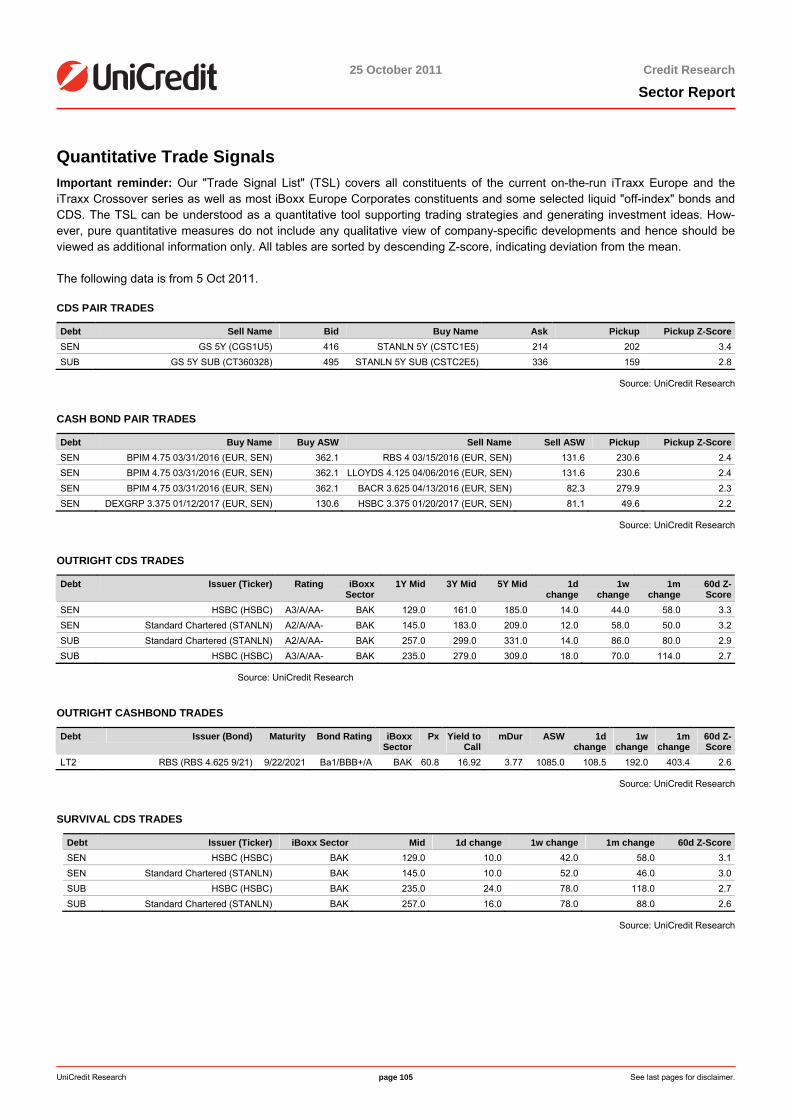

Analysis of secondary Market Spreads_________ 99Trade Ideas_____________________________ 100UK Bonds Overview (unsecured) ____________ 103Quantitative Trade Signals _________________ 105

Company websites www.santander.co.uk www.barclays.com www.cbonline.co.uk www.coventrybuildingsociety.co.uk www.hsbc.com www.lloydsbankinggroup.com www.nationwide.co.uk www.rbs.com www.standardchartered.com www.ybs.co.uk

Authors Dr. Tilo Höpker (UniCredit Bank) +49 89 378-12960 [email protected] Franz Rudolf, CEFA (UniCredit Bank) +49 89 378-12449 [email protected] Mauro Giorgio Marrano (UniCredit Bank) +39 02 88628222 [email protected] Bloomberg UCCR Internet www.research.unicreditgroup.eu

25 October 2011 Credit Research

Sector Report

UniCredit Research page 2 See last pages for disclaimer.

UK Economic Outlook Summary Moving into 2012, we expect GDP growth to accelerate as financial market tensions

gradually subside and the downward trend in global growth indicators flattens out. Inaddition, the effect of the BoE’s asset purchases should boost growth. We expect GDPto increase by 0.8% in 2011 and 1.5% in 2012. Inflation reached 5.2% in Septemberdriven by increases in utility charges, but should fall sharply in forthcoming years asthe effect of the temporary factors pushing up prices wane. The outlook for the UK economy has worsened over the summer due to the deterioration of the global eco-nomic outlook, rising financial market tensions, and the sustained weakness of thedomestic economy. Recent data and indicators point to continued weak growth in 3Qand 4Q. On the back of the deterioration of the outlook, at the October meeting the Bank of England resumed asset purchases, increasing the size of the stock of pur-chases by GBP 75bn to a total of GBP 275bn. We expect an additional increase of GBP50bn in 1Q12.

GDP growth to remain weak in 3Q and 4Q

Following very modest growth in 2Q, with the preliminary GDP reading revised down from0.2% qoq to 0.1%, data available for 3Q point to continued weak growth. Both PMIs deterio-rated in 3Q compared to 2Q (the manufacturing index fell from 52.7 to 50.0, while the servicesindex dropped from 58.7 to 53.1). Industrial production for July and August suggests that the production sector will grow 0.2% qoq, providing a positive, but modest, contribution to GDPgrowth in 3Q. On the expenditure side, consumer spending indicators remained weak, with 3Q retail sales falling 0.2% qoq compared to 2Q. On a positive note, trade data suggest that net exports are likely to provide a positive contribution to 3Q GDP growth. On the basis ofavailable data and information, we expect GDP to grow 0.2% qoq in 3Q. Regarding 4Q, weexpect GDP growth to slow to 0.1%, with growth suffering from the slowdown in the globaleconomy, particularly in the UK’s main trade partners such as the euro area. GDP shouldgrow 0.8% overall in 2011.

Growth will begin to recover in 2012

Moving into 2012, we expect GDP growth to accelerate as financial market tensions graduallysubside and the downward trend in global growth indicators flattens out. Furthermore, the effect of asset purchases should boost growth. The UK is likely to benefit from a recovery in its main trading partners (especially in the euro area, where we expect growth to start accel-erating at the beginning of 2012 and to reach its potential around the middle of the year)which should spur exports and, in turn, business confidence and thus investment. In addition, the squeeze in real household disposable income seen in 2011 should moderate, as the tem-porary effect of the factors pushing up prices (higher commodity prices, VAT increase and higher imports) begins to wane and inflation decelerates. As a result, we expect growth to be driven by a moderate acceleration in consumption and a more marked recovery in exports and investment. We expect GDP to grow 1.5% in 2012.

Labor market conditions are worsening

After having improved since mid-2010, labor market indicators began to deteriorate in 3Q. In the three months to August, employment fell by 178,000 as job creation in the private sectorwas unable to offset the fall in public sector employment, while unemployment increased by 114,000. For both indicators, these are the poorest performances since mid-2009. The unem-ployment rate increased from 7.9% to 8.1%. Due to the deterioration of the growth outlook seen over the summer, we expect labor market conditions to worsen in the remainder of theyear, before stabilizing in 1Q12 and starting to improve in 2Q12 as growth accelerates andeconomic prospects improve.

Inflation should have peaked in September

Inflation has been increasing since the end of 2009, mainly driven by higher commodity andimport prices, and VAT increases. Headline inflation accelerated from 4.5% to 5.2% in Sep-tember driven by utility charges. Such an increase was already factored in by the Bank ofEngland that had been warning in the preceding months about inflation going above 5% andtherefore it should not change the Bank’s view on QE. We expect inflation to have peaked in

25 October 2011 Credit Research

Sector Report

UniCredit Research page 3 See last pages for disclaimer.

September and we see it beginning to gradually slow down by the end of the year, and more sharply in 2012 when the effect of the temporary factors pushing up prices wane (VAT in-creases, commodity and import prices). We expect inflation to average 4.3% in 2011 and2.4% in 2012.

BoE: more QE in 1Q12 On the back of the deterioration of the outlook, at the October meeting the Bank of England resumed asset purchases, increasing the size of the stock of purchases by GBP 75bn to atotal of GBP 275bn. As in the first round, the BoE will purchase gilts with a maturity greaterthan three years in a timeframe of four months. The minutes of the meeting showed that thedecision was unanimous and the MPC hinted that the Bank of England could announce more purchases if needed. We expect the BoE to announce an additional increase of GBP 50bn in1Q12, bringing the stock of purchases to GBP 325bn. As for the Bank rate, we do not expectthe first hike until 1Q13.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 4 See last pages for disclaimer.

UK Housing Market Summary The housing market remains weak. The recovery is likely to be very gradual, reflecting

a weak demand for housing due to credit constraints, squeezed household incomes, and uncertainty over the economic outlook. However, historically low Bank rates andthe resumption of quantitative easing, should provide some support to the housingmarket.

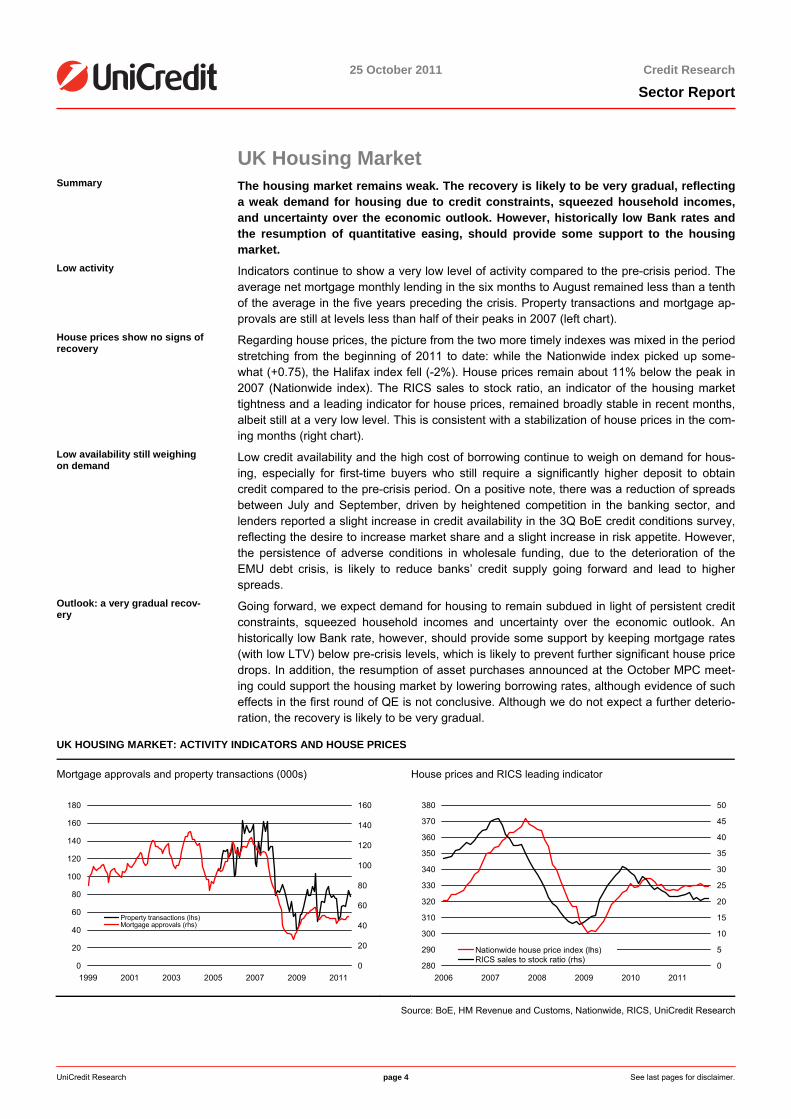

Low activity Indicators continue to show a very low level of activity compared to the pre-crisis period. The average net mortgage monthly lending in the six months to August remained less than a tenth of the average in the five years preceding the crisis. Property transactions and mortgage ap-provals are still at levels less than half of their peaks in 2007 (left chart).

House prices show no signs of recovery

Regarding house prices, the picture from the two more timely indexes was mixed in the period stretching from the beginning of 2011 to date: while the Nationwide index picked up some-what (+0.75), the Halifax index fell (-2%). House prices remain about 11% below the peak in 2007 (Nationwide index). The RICS sales to stock ratio, an indicator of the housing markettightness and a leading indicator for house prices, remained broadly stable in recent months,albeit still at a very low level. This is consistent with a stabilization of house prices in the com-ing months (right chart).

Low availability still weighing on demand

Low credit availability and the high cost of borrowing continue to weigh on demand for hous-ing, especially for first-time buyers who still require a significantly higher deposit to obtain credit compared to the pre-crisis period. On a positive note, there was a reduction of spreads between July and September, driven by heightened competition in the banking sector, andlenders reported a slight increase in credit availability in the 3Q BoE credit conditions survey,reflecting the desire to increase market share and a slight increase in risk appetite. However, the persistence of adverse conditions in wholesale funding, due to the deterioration of theEMU debt crisis, is likely to reduce banks’ credit supply going forward and lead to higherspreads.

Outlook: a very gradual recov-ery

Going forward, we expect demand for housing to remain subdued in light of persistent creditconstraints, squeezed household incomes and uncertainty over the economic outlook. Anhistorically low Bank rate, however, should provide some support by keeping mortgage rates (with low LTV) below pre-crisis levels, which is likely to prevent further significant house pricedrops. In addition, the resumption of asset purchases announced at the October MPC meet-ing could support the housing market by lowering borrowing rates, although evidence of such effects in the first round of QE is not conclusive. Although we do not expect a further deterio-ration, the recovery is likely to be very gradual.

UK HOUSING MARKET: ACTIVITY INDICATORS AND HOUSE PRICES

Mortgage approvals and property transactions (000s) House prices and RICS leading indicator

0

20

40

60

80

100

120

140

160

180

1999 2001 2003 2005 2007 2009 20110

20

40

60

80

100

120

140

160

Property transactions (lhs)Mortgage approvals (rhs)

280

290

300

310

320

330

340

350

360

370

380

2006 2007 2008 2009 2010 20110

5

10

15

20

25

30

35

40

45

50

Nationwide house price index (lhs)RICS sales to stock ratio (rhs)

Source: BoE, HM Revenue and Customs, Nationwide, RICS, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 5 See last pages for disclaimer.

UK Banking Sector

Introduction, Crisis, Recovery & the ICB Five major banks with com-bined market shares of up to 90%

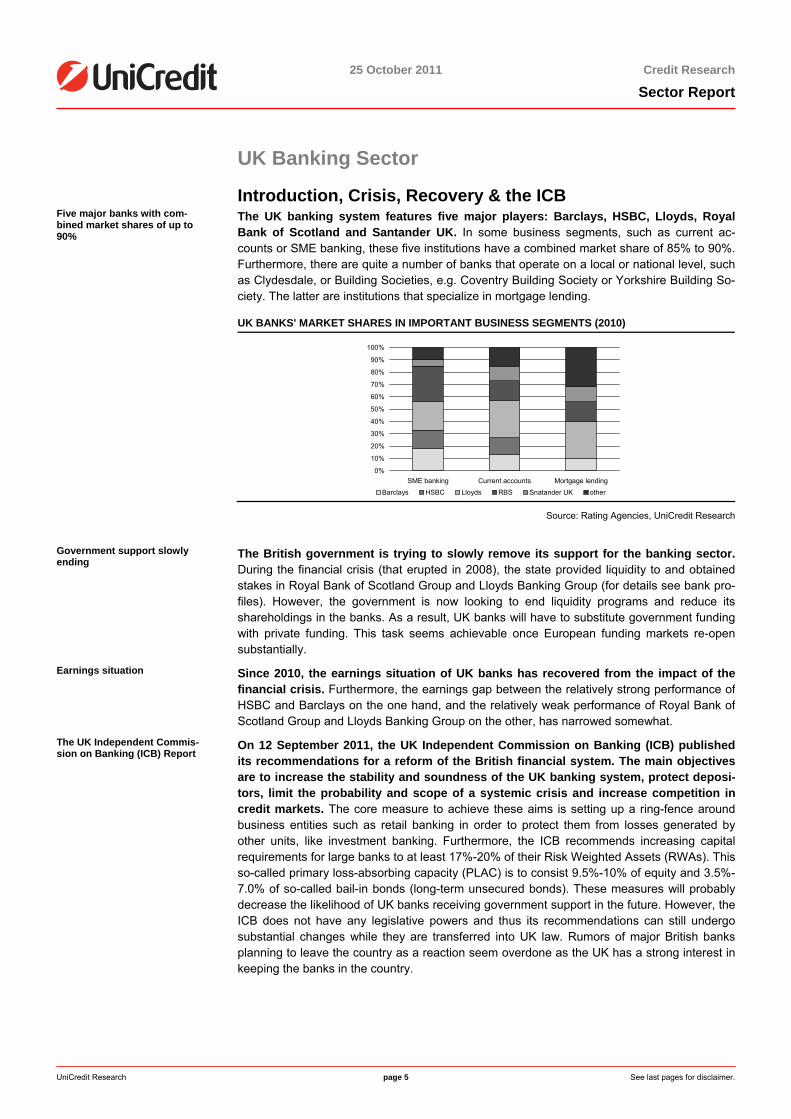

The UK banking system features five major players: Barclays, HSBC, Lloyds, Royal Bank of Scotland and Santander UK. In some business segments, such as current ac-counts or SME banking, these five institutions have a combined market share of 85% to 90%. Furthermore, there are quite a number of banks that operate on a local or national level, such as Clydesdale, or Building Societies, e.g. Coventry Building Society or Yorkshire Building So-ciety. The latter are institutions that specialize in mortgage lending.

UK BANKS' MARKET SHARES IN IMPORTANT BUSINESS SEGMENTS (2010)

0%

10%

20%

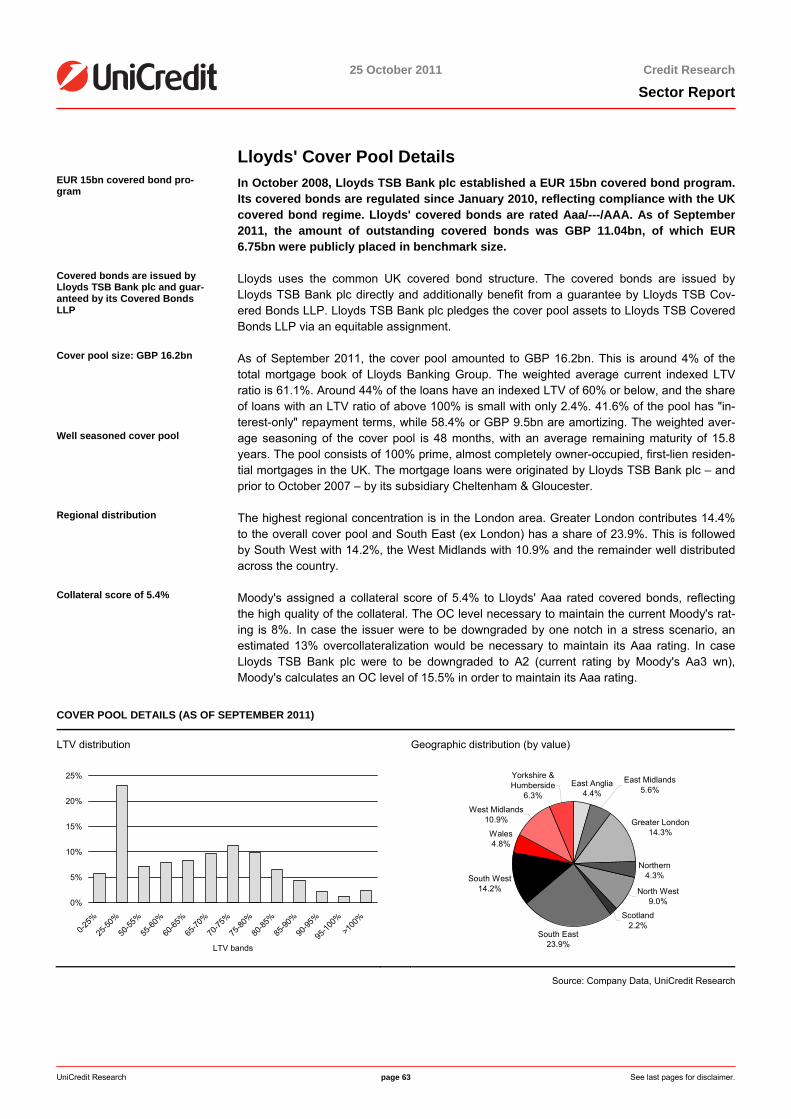

30%

40%

50%

60%

70%

80%

90%

100%

SME banking Current accounts Mortgage lending

Barclays HSBC Lloyds RBS Snatander UK other Source: Rating Agencies, UniCredit Research

Government support slowly ending

The British government is trying to slowly remove its support for the banking sector.During the financial crisis (that erupted in 2008), the state provided liquidity to and obtained stakes in Royal Bank of Scotland Group and Lloyds Banking Group (for details see bank pro-files). However, the government is now looking to end liquidity programs and reduce its shareholdings in the banks. As a result, UK banks will have to substitute government funding with private funding. This task seems achievable once European funding markets re-open substantially.

Earnings situation Since 2010, the earnings situation of UK banks has recovered from the impact of the financial crisis. Furthermore, the earnings gap between the relatively strong performance ofHSBC and Barclays on the one hand, and the relatively weak performance of Royal Bank of Scotland Group and Lloyds Banking Group on the other, has narrowed somewhat.

The UK Independent Commis-sion on Banking (ICB) Report

On 12 September 2011, the UK Independent Commission on Banking (ICB) published its recommendations for a reform of the British financial system. The main objectives are to increase the stability and soundness of the UK banking system, protect deposi-tors, limit the probability and scope of a systemic crisis and increase competition incredit markets. The core measure to achieve these aims is setting up a ring-fence around business entities such as retail banking in order to protect them from losses generated byother units, like investment banking. Furthermore, the ICB recommends increasing capital requirements for large banks to at least 17%-20% of their Risk Weighted Assets (RWAs). This so-called primary loss-absorbing capacity (PLAC) is to consist 9.5%-10% of equity and 3.5%-7.0% of so-called bail-in bonds (long-term unsecured bonds). These measures will probably decrease the likelihood of UK banks receiving government support in the future. However, the ICB does not have any legislative powers and thus its recommendations can still undergo substantial changes while they are transferred into UK law. Rumors of major British banks planning to leave the country as a reaction seem overdone as the UK has a strong interest in keeping the banks in the country.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 6 See last pages for disclaimer.

Sector wrap-up and latest events

On 7 October 2011, Moody's downgraded the senior debt and deposit ratings of 12 UK finan-cial institutions and confirmed the rating of 1 institution, concluding its review of UK systemic support started on 24 May: ■ The downgrades reflect Moody's re-assessment of the UK's support environment, leading

it to remove the assumption of systemic support for seven smaller institutions and to lower systemic support by one-to-three notches for five larger financial groups.

■ Moody's ascribes these to the announcements and actions made by British authorities, which it believes will lower the predictability of support in the medium to long run.

■ The agency also said that the UK government remains likely to offer some form of supportto systemically important financial institutions still having up to three notches of uplift.

■ Moody's said it is more probable that there will be no support for smaller institutions.

■ The rating actions were not caused by worsening financial strength of the banking systemnor of the UK government.

■ Moreover, Moody's has a negative outlook on the senior debt and deposit ratings of banks with still two or more notches of systemic support. This is due to the possibility of a further lowering of systemic support over the medium-to-long term.

■ The specific downgrades for individual banks were as follows: a one-notch downgrade of Lloyds TSB Bank plc (to A1 from Aa3), Santander UK plc (to A1 from Aa3), Cooperative Bank plc (to A3 from A2), a two-notch downgrade of RBS plc (to A2 from Aa3) and Nation-wide Building Society (to A2 from Aa3); and downgrades by one to five notches for seven smaller building societies. Clydesdale Bank's ratings were confirmed at A2, with a negativeoutlook.

■ Regarding standalone rating actions (which preceded the debt rating actions), the following banks were upgraded: Cooperative Bank, Santander UK, Nationwide, Yorkshire, and Prin-cipality Building Society.

To put this into context: On 12 September 2011, the UK's government-appointed Inde-pendent Commission on Banking (ICB) released its final recommendations on reformsto improve stability and competition in the UK banking. These are the main recommenda-tions and points:

■ Only ring-fenced banks shall be allowed to take deposits and provide overdrafts, with animplementation deadline until 2019 and purportedly (i) slowly enough to avoid undermining the economy and (ii) to prevent UK retail banks from leaving the country.

■ The report does not require a full separation of retail and investment banking business butrecommends that riskier business should be done at non-ring-fenced banks and not benefit from explicit government support. That a total separation was not recommended wasdriven by concerns about: (i) higher economic expense (loss of synergies), (ii) potentialconflicts with European law and (iii) precluding support for troubled retail banks from else-where in banking groups.

■ Large ring-fenced banks (RWAs/GDP of >3%: Barclays, HSBC, Lloyds Banking Group,Nationwide, RBS, Santander UK) are faced with a minimum equity-RWA ratio of 10%, banks with RWAs/GDP of 1%-3% (Co-op, Verde, Clydesdale) face a 7% + ring-fence buffer of 3/2x (RWAs/GDP-1%) – yielding a buffer of max. 10% – and all other banks (RWAs/GDP of <1%) a 7% buffer.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 7 See last pages for disclaimer.

■ Retail and other activities of large UK banking groups should have a primary loss-absorbing capacity of 17%-20% (equity and other capital that also includes long-term un-secured debt, which may bear losses in resolution [bail-in bonds] and could also include contingent capital ["CoCos"]).

■ Reform costs are estimated at GBP 4bn-7bn p.a. for the aggregate of UK banks and will affect around a third of UK banks' balance sheets or up to GBP 2.3tn.

■ The implementation and final decision on the recommendations rests with the Chancellor of the Exchequer, Osborne, who supports ring-fencing and wants the necessary legislation in place "while this parliament is sitting".

■ Ring-fencing was to be expected, as was the response by the British Bankers’ Association(BBA). The BBA stated that UK banks were already implementing “sweeping reforms” andthat the "ICB’s recommendations cover the same important issues. Any further reform measures adopted by the UK authorities need to be carefully analyzed and compared withthose agreed internationally. It is vital that the full impact any further reforms will have onthe economy, the recovery and banks’ ability to support their customers in the UK is under-stood”.

■ Also, as expected, the report provides relief for taxpayers but leaves enough time for UK banks to adapt to the new rules and not to be as harsh (full separation, immediate imple-mentation, etc.) as to trigger a re-location of UK banks (somewhat unrealistic) or an imme-diate drop in profits/capitalization levels. Also, given Basel III, the discussion of extra capi-tal buffers for systemically important banks and the general trend to make banks suppos-edly safer but also less "sexy" (resolution schemes, ring-fencing discussions in other coun-tries, stress tests, EC imposed de-risking in return for state aid, "voluntary" rights issues and disposal of non-core assets, staff cuts, etc.), the recommendations do not come as asurprise really.

■ On 14 September (in contrast to its rating action on 7 October), Moody's stated that theICB report has no immediate rating impact for UK banks, but is credit-negative overall for bondholders of the largest UK banking groups due to following:

– The UK government still needs to formally accept the ICB recommendations and legislation will likely require a lengthy drafting process and a longer-than-expected implementation period, which may extend until 2019. This would in-crease the probability that the final decisions may differ from the current rec-ommendations.

– Over the longer term, the ICB proposals could be credit-negative for bondhold-ers of the largest UK banks due to enhanced resolution powers, including the ability to bail-in senior unsecured bondholders and possibly higher funding and operating costs.

– On the other hand, the high capital requirements imposed by the ICB's recom-mendations and the simpler structure regarding ring-fenced banking entities are credit-positive and could be a mitigating factor, at least for the ring-fenced bank-ing units.

– Moody's has pointed to three aspects in the ICB's recommendations that mighthave the greatest importance for bondholders:

25 October 2011 Credit Research

Sector Report

UniCredit Research page 8 See last pages for disclaimer.

■ Moody's said that it would assign separate standalone ratings to Ring-Fenced Banks (RFBs) and Non-Ring-Fenced Banks (NRFBs), and that the recommendations would probably affect the rating agency's evaluation of franchise value, funding, prof-itability and capital adequacy. Despite keeping the overall group risk profile, Moody's expects the recommendations to be positive for the standalone rating of RFBs due to more stable earnings. They would be negative for the standalone ratings of NRFBs thanks to more volatile earnings and possibly higher funding costs.

■ Regarding capital, the core capital ratios required by the ICB's recommendations will be slightly higher for the RFBs of the large UK banks than Basel III for G-SIB banksand would therefore be credit-positive. However, the additional loss-absorbing ca-pacity will highly depend on its specific composition of equity, contingent capital instruments or loss-absorbing debt.

■ Concerning resolution tools, the ICB's recommendations regarding depositor prefer-ence for insured depositors and statutory bail-in powers to impose losses on senior unsecured debt are in the same vein as the long-term international and EU plans on bank resolution and are credit negative. The capital and loss-absorbing requirementsfor the largest banks are negative if they rely mainly on allowing senior unse-cured debt to be bailed in. Moody's also expects the recommendations to lead to an overall further lessening in systemic support in Moody's senior debt ratings both for RFBs and NRFBs.

■ The rating considerations above were followed by Fitch's lowering of the UK support ratingfloors on 13 October, cutting Lloyds Banking Group plc's long-term IDR to A from AA-, placing Barclays IDR on watch negative and RBS Group's long-term IDR on A from AA-.

To conclude, the above-mentioned fits into the larger European context as follows. Wethink the pessimistic market view will continue to predominate in the near future. The Euro-pean sovereign crisis remains center-stage, and as long as this issue has not been resolved, tightening potential is limited. Moreover, there is no new positive investment trigger on the horizon that could divert investors' attention. Hence, the many investment opportunities that make sense fundamentally and are highly attractive following the re-pricing will become even more attractive in the next few weeks before we return to tighter, justified levels. However, at some point, market participants will perceive spread levels as sufficiently attractive and thenegative story as priced in – and start buying again. Finding this optimal entry point is impos-sible to predict, especially due to the large carry that is lost when not being invested, meaninginvestors will return to financials credit before positive news kicks in. While September was another challenging month for financials credit markets, with spreads widening across the board, there was some relief at the end of the month following political support for the EFSFenlargement.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 9 See last pages for disclaimer.

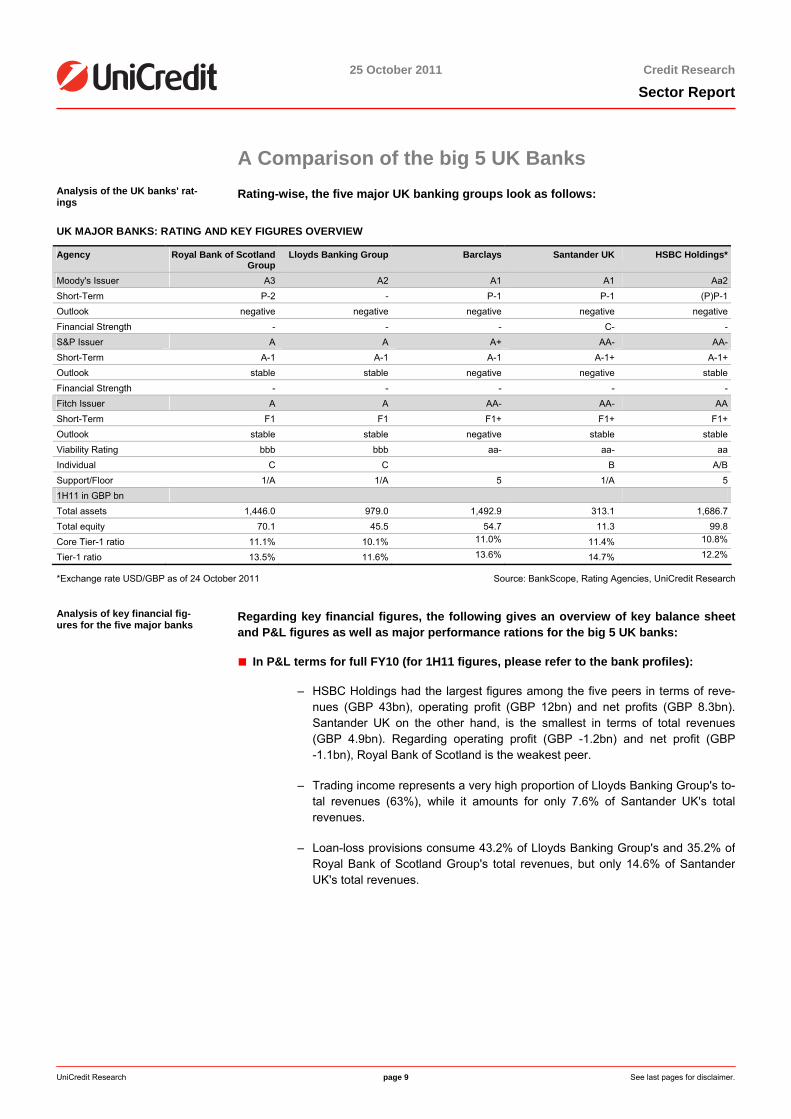

A Comparison of the big 5 UK Banks Analysis of the UK banks' rat-ings

Rating-wise, the five major UK banking groups look as follows:

UK MAJOR BANKS: RATING AND KEY FIGURES OVERVIEW

Agency Royal Bank of Scotland Group

Lloyds Banking Group Barclays Santander UK HSBC Holdings*

Moody's Issuer A3 A2 A1 A1 Aa2Short-Term P-2 - P-1 P-1 (P)P-1Outlook negative negative negative negative negativeFinancial Strength - - - C- -S&P Issuer A A A+ AA- AA-Short-Term A-1 A-1 A-1 A-1+ A-1+Outlook stable stable negative negative stableFinancial Strength - - - - -Fitch Issuer A A AA- AA- AAShort-Term F1 F1 F1+ F1+ F1+Outlook stable stable negative stable stableViability Rating bbb bbb aa- aa- aaIndividual C C B A/BSupport/Floor 1/A 1/A 5 1/A 51H11 in GBP bn Total assets 1,446.0 979.0 1,492.9 313.1 1,686.7Total equity 70.1 45.5 54.7 11.3 99.8Core Tier-1 ratio 11.1% 10.1% 11.0% 11.4% 10.8%

Tier-1 ratio 13.5% 11.6% 13.6% 14.7% 12.2%

*Exchange rate USD/GBP as of 24 October 2011 Source: BankScope, Rating Agencies, UniCredit Research

Analysis of key financial fig-ures for the five major banks

Regarding key financial figures, the following gives an overview of key balance sheet and P&L figures as well as major performance rations for the big 5 UK banks:

■ In P&L terms for full FY10 (for 1H11 figures, please refer to the bank profiles):

– HSBC Holdings had the largest figures among the five peers in terms of reve-nues (GBP 43bn), operating profit (GBP 12bn) and net profits (GBP 8.3bn).Santander UK on the other hand, is the smallest in terms of total revenues(GBP 4.9bn). Regarding operating profit (GBP -1.2bn) and net profit (GBP-1.1bn), Royal Bank of Scotland is the weakest peer.

– Trading income represents a very high proportion of Lloyds Banking Group's to-tal revenues (63%), while it amounts for only 7.6% of Santander UK's total revenues.

– Loan-loss provisions consume 43.2% of Lloyds Banking Group's and 35.2% of Royal Bank of Scotland Group's total revenues, but only 14.6% of SantanderUK's total revenues.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 10 See last pages for disclaimer.

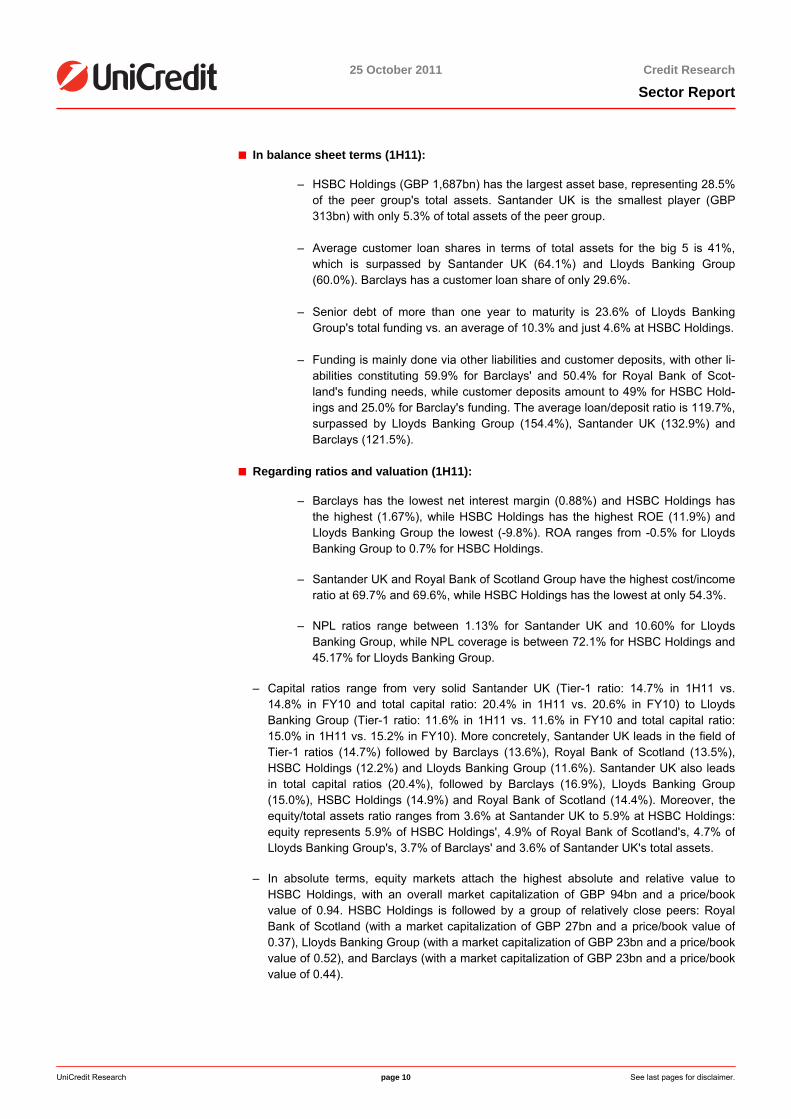

■ In balance sheet terms (1H11):

– HSBC Holdings (GBP 1,687bn) has the largest asset base, representing 28.5%of the peer group's total assets. Santander UK is the smallest player (GBP313bn) with only 5.3% of total assets of the peer group.

– Average customer loan shares in terms of total assets for the big 5 is 41%,which is surpassed by Santander UK (64.1%) and Lloyds Banking Group (60.0%). Barclays has a customer loan share of only 29.6%.

– Senior debt of more than one year to maturity is 23.6% of Lloyds BankingGroup's total funding vs. an average of 10.3% and just 4.6% at HSBC Holdings.

– Funding is mainly done via other liabilities and customer deposits, with other li-abilities constituting 59.9% for Barclays' and 50.4% for Royal Bank of Scot-land's funding needs, while customer deposits amount to 49% for HSBC Hold-ings and 25.0% for Barclay's funding. The average loan/deposit ratio is 119.7%, surpassed by Lloyds Banking Group (154.4%), Santander UK (132.9%) andBarclays (121.5%).

■ Regarding ratios and valuation (1H11):

– Barclays has the lowest net interest margin (0.88%) and HSBC Holdings hasthe highest (1.67%), while HSBC Holdings has the highest ROE (11.9%) and Lloyds Banking Group the lowest (-9.8%). ROA ranges from -0.5% for Lloyds Banking Group to 0.7% for HSBC Holdings.

– Santander UK and Royal Bank of Scotland Group have the highest cost/income ratio at 69.7% and 69.6%, while HSBC Holdings has the lowest at only 54.3%.

– NPL ratios range between 1.13% for Santander UK and 10.60% for LloydsBanking Group, while NPL coverage is between 72.1% for HSBC Holdings and45.17% for Lloyds Banking Group.

– Capital ratios range from very solid Santander UK (Tier-1 ratio: 14.7% in 1H11 vs. 14.8% in FY10 and total capital ratio: 20.4% in 1H11 vs. 20.6% in FY10) to LloydsBanking Group (Tier-1 ratio: 11.6% in 1H11 vs. 11.6% in FY10 and total capital ratio:15.0% in 1H11 vs. 15.2% in FY10). More concretely, Santander UK leads in the field of Tier-1 ratios (14.7%) followed by Barclays (13.6%), Royal Bank of Scotland (13.5%),HSBC Holdings (12.2%) and Lloyds Banking Group (11.6%). Santander UK also leadsin total capital ratios (20.4%), followed by Barclays (16.9%), Lloyds Banking Group (15.0%), HSBC Holdings (14.9%) and Royal Bank of Scotland (14.4%). Moreover, theequity/total assets ratio ranges from 3.6% at Santander UK to 5.9% at HSBC Holdings:equity represents 5.9% of HSBC Holdings', 4.9% of Royal Bank of Scotland's, 4.7% ofLloyds Banking Group's, 3.7% of Barclays' and 3.6% of Santander UK's total assets.

– In absolute terms, equity markets attach the highest absolute and relative value toHSBC Holdings, with an overall market capitalization of GBP 94bn and a price/book value of 0.94. HSBC Holdings is followed by a group of relatively close peers: RoyalBank of Scotland (with a market capitalization of GBP 27bn and a price/book value of0.37), Lloyds Banking Group (with a market capitalization of GBP 23bn and a price/book value of 0.52), and Barclays (with a market capitalization of GBP 23bn and a price/bookvalue of 0.44).

25 October 2011 Credit Research

Sector Report

UniCredit Research page 11 See last pages for disclaimer.

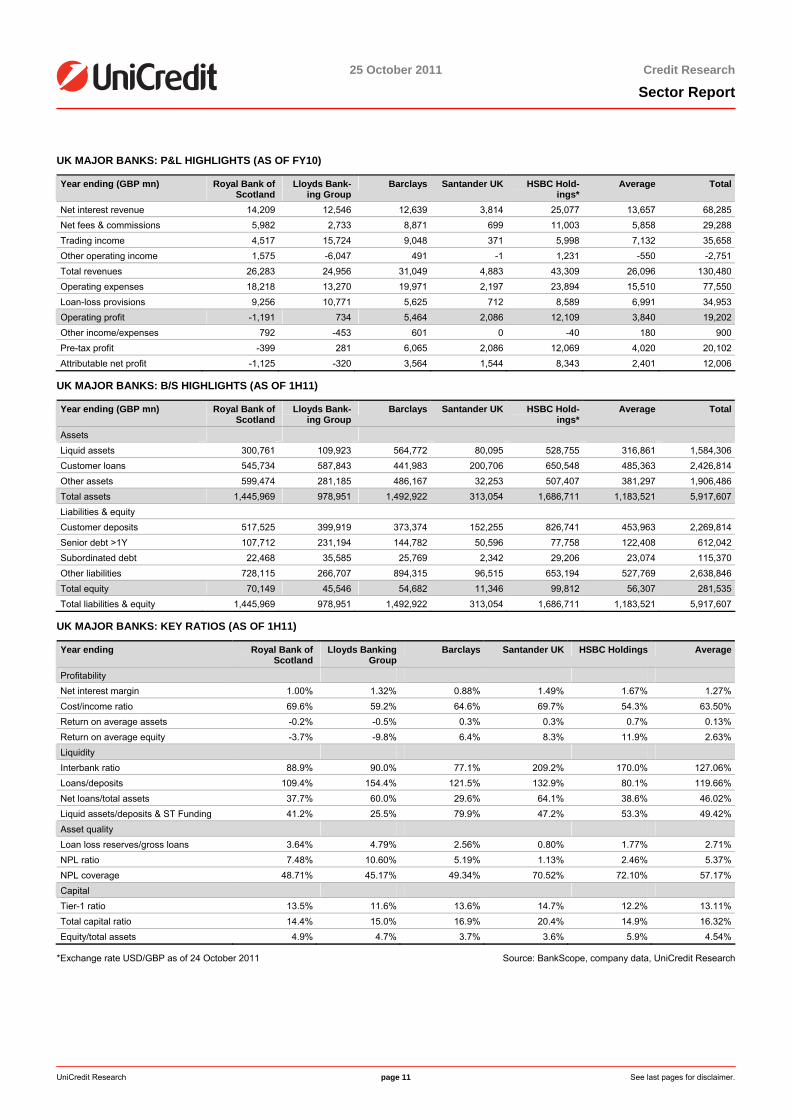

UK MAJOR BANKS: P&L HIGHLIGHTS (AS OF FY10)

Year ending (GBP mn) Royal Bank of Scotland

Lloyds Bank-ing Group

Barclays Santander UK HSBC Hold-ings*

Average Total

Net interest revenue 14,209 12,546 12,639 3,814 25,077 13,657 68,285Net fees & commissions 5,982 2,733 8,871 699 11,003 5,858 29,288Trading income 4,517 15,724 9,048 371 5,998 7,132 35,658Other operating income 1,575 -6,047 491 -1 1,231 -550 -2,751Total revenues 26,283 24,956 31,049 4,883 43,309 26,096 130,480Operating expenses 18,218 13,270 19,971 2,197 23,894 15,510 77,550Loan-loss provisions 9,256 10,771 5,625 712 8,589 6,991 34,953Operating profit -1,191 734 5,464 2,086 12,109 3,840 19,202Other income/expenses 792 -453 601 0 -40 180 900Pre-tax profit -399 281 6,065 2,086 12,069 4,020 20,102Attributable net profit -1,125 -320 3,564 1,544 8,343 2,401 12,006

UK MAJOR BANKS: B/S HIGHLIGHTS (AS OF 1H11)

Year ending (GBP mn) Royal Bank of Scotland

Lloyds Bank-ing Group

Barclays Santander UK HSBC Hold-ings*

Average Total

Assets Liquid assets 300,761 109,923 564,772 80,095 528,755 316,861 1,584,306Customer loans 545,734 587,843 441,983 200,706 650,548 485,363 2,426,814Other assets 599,474 281,185 486,167 32,253 507,407 381,297 1,906,486Total assets 1,445,969 978,951 1,492,922 313,054 1,686,711 1,183,521 5,917,607Liabilities & equity Customer deposits 517,525 399,919 373,374 152,255 826,741 453,963 2,269,814Senior debt >1Y 107,712 231,194 144,782 50,596 77,758 122,408 612,042Subordinated debt 22,468 35,585 25,769 2,342 29,206 23,074 115,370Other liabilities 728,115 266,707 894,315 96,515 653,194 527,769 2,638,846Total equity 70,149 45,546 54,682 11,346 99,812 56,307 281,535Total liabilities & equity 1,445,969 978,951 1,492,922 313,054 1,686,711 1,183,521 5,917,607

UK MAJOR BANKS: KEY RATIOS (AS OF 1H11)

Year ending Royal Bank of Scotland

Lloyds Banking Group

Barclays Santander UK HSBC Holdings Average

Profitability Net interest margin 1.00% 1.32% 0.88% 1.49% 1.67% 1.27%Cost/income ratio 69.6% 59.2% 64.6% 69.7% 54.3% 63.50%Return on average assets -0.2% -0.5% 0.3% 0.3% 0.7% 0.13%Return on average equity -3.7% -9.8% 6.4% 8.3% 11.9% 2.63%Liquidity Interbank ratio 88.9% 90.0% 77.1% 209.2% 170.0% 127.06%Loans/deposits 109.4% 154.4% 121.5% 132.9% 80.1% 119.66%Net loans/total assets 37.7% 60.0% 29.6% 64.1% 38.6% 46.02%Liquid assets/deposits & ST Funding 41.2% 25.5% 79.9% 47.2% 53.3% 49.42%Asset quality Loan loss reserves/gross loans 3.64% 4.79% 2.56% 0.80% 1.77% 2.71%NPL ratio 7.48% 10.60% 5.19% 1.13% 2.46% 5.37%NPL coverage 48.71% 45.17% 49.34% 70.52% 72.10% 57.17%Capital Tier-1 ratio 13.5% 11.6% 13.6% 14.7% 12.2% 13.11%Total capital ratio 14.4% 15.0% 16.9% 20.4% 14.9% 16.32%Equity/total assets 4.9% 4.7% 3.7% 3.6% 5.9% 4.54%

*Exchange rate USD/GBP as of 24 October 2011 Source: BankScope, company data, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 12 See last pages for disclaimer.

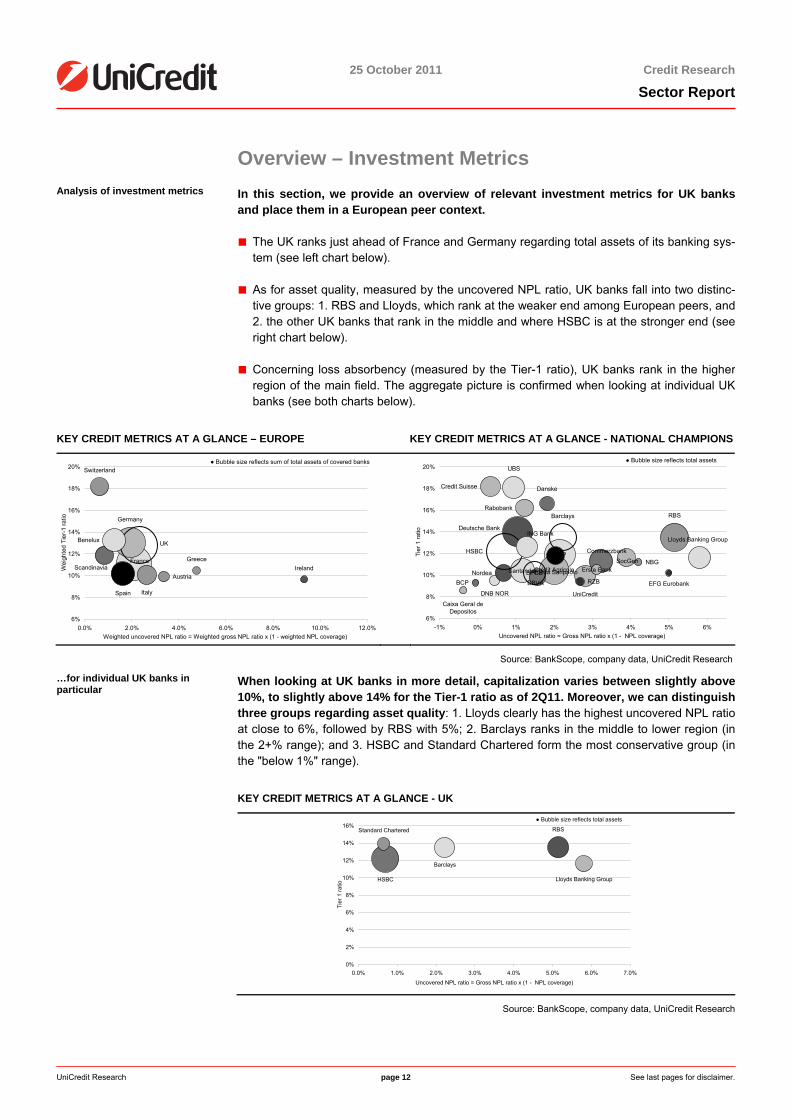

Overview – Investment Metrics Analysis of investment metrics In this section, we provide an overview of relevant investment metrics for UK banks

and place them in a European peer context.

■ The UK ranks just ahead of France and Germany regarding total assets of its banking sys-tem (see left chart below).

■ As for asset quality, measured by the uncovered NPL ratio, UK banks fall into two distinc-tive groups: 1. RBS and Lloyds, which rank at the weaker end among European peers, and 2. the other UK banks that rank in the middle and where HSBC is at the stronger end (see right chart below).

■ Concerning loss absorbency (measured by the Tier-1 ratio), UK banks rank in the higher region of the main field. The aggregate picture is confirmed when looking at individual UKbanks (see both charts below).

KEY CREDIT METRICS AT A GLANCE – EUROPE KEY CREDIT METRICS AT A GLANCE - NATIONAL CHAMPIONS

IrelandFrance

Germany

Greece

Italy

Scandinavia

Spain

Switzerland

UK

Austria

Benelux

6%

8%

10%

12%

14%

16%

18%

20%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0%Weighted uncovered NPL ratio = Weighted gross NPL ratio x (1 - weighted NPL coverage)

Wei

ghte

d Ti

er-1

ratio

● Bubble size reflects sum of total assets of covered banks

BNPSocGen

Crédit Agricole

Deutsche Bank

Intesa Sanpaolo

UniCreditCaixa Geral de

Depositos

BCP

Danske

DNB NOR

Nordea Santander

BBVA

Barclays

HSBC

Lloyds Banking Group

RBS

Credit Suisse

UBS

Commerzbank

NBG

EFG Eurobank

ING Bank

Rabobank

Erste Bank

RZBBPCE

6%

8%

10%

12%

14%

16%

18%

20%

-1% 0% 1% 2% 3% 4% 5% 6%Uncovered NPL ratio = Gross NPL ratio x (1 - NPL coverage)

Tier

1 ra

tio

● Bubble size reflects total assets

Source: BankScope, company data, UniCredit Research

…for individual UK banks in particular

When looking at UK banks in more detail, capitalization varies between slightly above 10%, to slightly above 14% for the Tier-1 ratio as of 2Q11. Moreover, we can distinguish three groups regarding asset quality: 1. Lloyds clearly has the highest uncovered NPL ratio at close to 6%, followed by RBS with 5%; 2. Barclays ranks in the middle to lower region (in the 2+% range); and 3. HSBC and Standard Chartered form the most conservative group (in the "below 1%" range).

KEY CREDIT METRICS AT A GLANCE - UK

Barclays

HSBC Lloyds Banking Group

RBSStandard Chartered

0%

2%

4%

6%

8%

10%

12%

14%

16%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0%

Uncovered NPL ratio = Gross NPL ratio x (1 - NPL coverage)

Tier

1 ra

tio

● Bubble size reflects total assets

Source: BankScope, company data, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 13 See last pages for disclaimer.

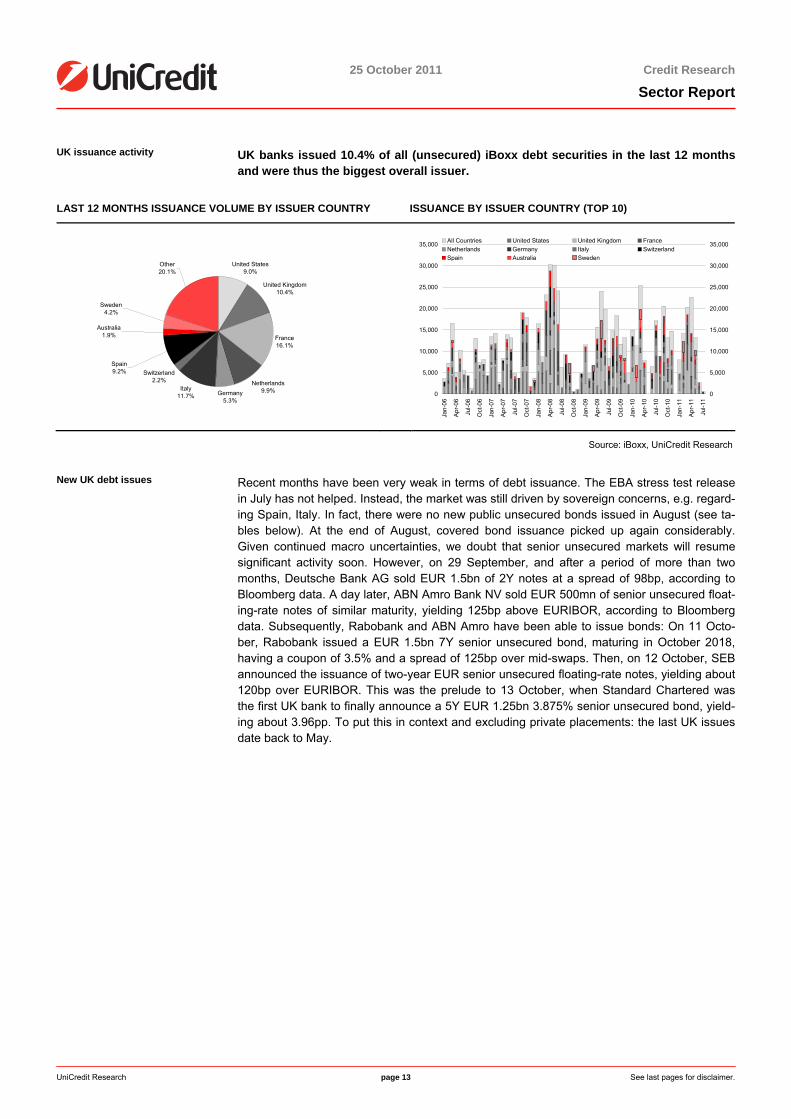

UK issuance activity UK banks issued 10.4% of all (unsecured) iBoxx debt securities in the last 12 months and were thus the biggest overall issuer.

LAST 12 MONTHS ISSUANCE VOLUME BY ISSUER COUNTRY ISSUANCE BY ISSUER COUNTRY (TOP 10)

United States9.0%

United Kingdom10.4%

France16.1%

Netherlands9.9%Germany

5.3%

Italy11.7%

Switzerland2.2%

Other20.1%

Spain9.2%

Australia1.9%

Sweden4.2%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000All Countries United States United Kingdom FranceNetherlands Germany Italy SwitzerlandSpain Australia Sweden

Source: iBoxx, UniCredit Research

New UK debt issues Recent months have been very weak in terms of debt issuance. The EBA stress test release in July has not helped. Instead, the market was still driven by sovereign concerns, e.g. regard-ing Spain, Italy. In fact, there were no new public unsecured bonds issued in August (see ta-bles below). At the end of August, covered bond issuance picked up again considerably.Given continued macro uncertainties, we doubt that senior unsecured markets will resumesignificant activity soon. However, on 29 September, and after a period of more than twomonths, Deutsche Bank AG sold EUR 1.5bn of 2Y notes at a spread of 98bp, according toBloomberg data. A day later, ABN Amro Bank NV sold EUR 500mn of senior unsecured float-ing-rate notes of similar maturity, yielding 125bp above EURIBOR, according to Bloombergdata. Subsequently, Rabobank and ABN Amro have been able to issue bonds: On 11 Octo-ber, Rabobank issued a EUR 1.5bn 7Y senior unsecured bond, maturing in October 2018, having a coupon of 3.5% and a spread of 125bp over mid-swaps. Then, on 12 October, SEB announced the issuance of two-year EUR senior unsecured floating-rate notes, yielding about 120bp over EURIBOR. This was the prelude to 13 October, when Standard Chartered was the first UK bank to finally announce a 5Y EUR 1.25bn 3.875% senior unsecured bond, yield-ing about 3.96pp. To put this in context and excluding private placements: the last UK issues date back to May.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 14 See last pages for disclaimer.

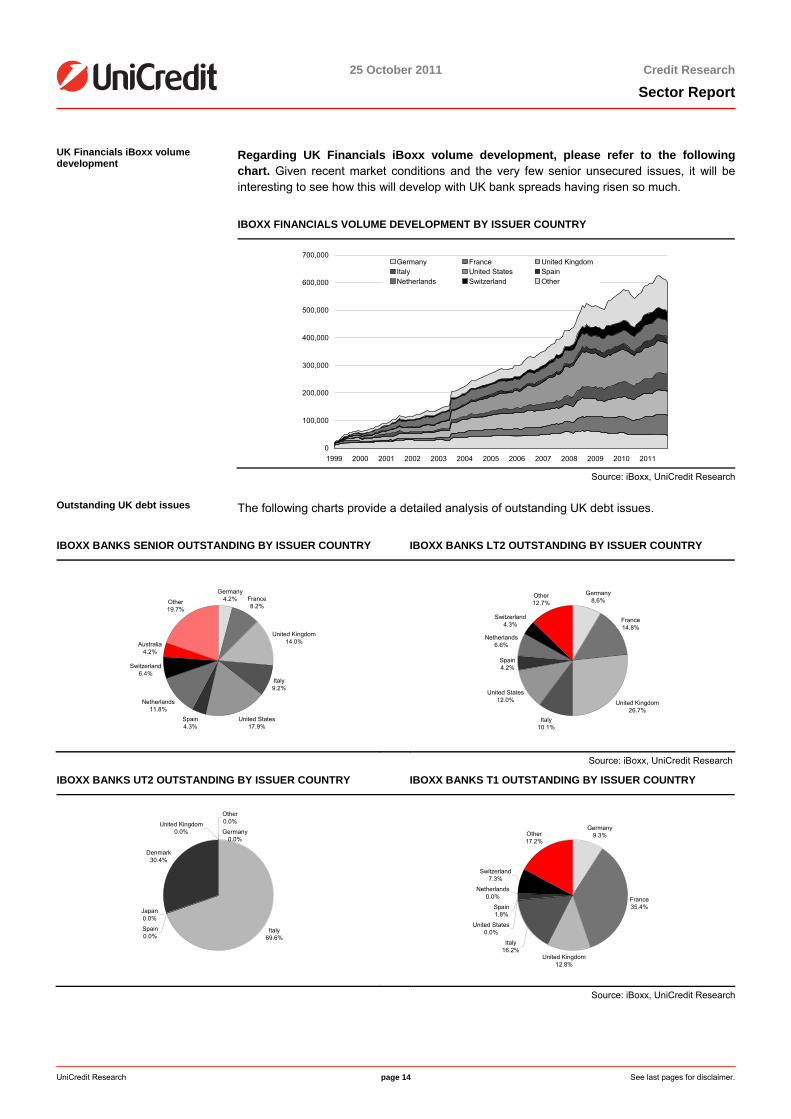

UK Financials iBoxx volume development

Regarding UK Financials iBoxx volume development, please refer to the following chart. Given recent market conditions and the very few senior unsecured issues, it will be interesting to see how this will develop with UK bank spreads having risen so much.

IBOXX FINANCIALS VOLUME DEVELOPMENT BY ISSUER COUNTRY

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Germany France United KingdomItaly United States SpainNetherlands Switzerland Other

Source: iBoxx, UniCredit Research

Outstanding UK debt issues The following charts provide a detailed analysis of outstanding UK debt issues.

IBOXX BANKS SENIOR OUTSTANDING BY ISSUER COUNTRY IBOXX BANKS LT2 OUTSTANDING BY ISSUER COUNTRY

Germany4.2% France

8.2%

United Kingdom14.0%

Italy9.2%

United States17.9%

Spain4.3%

Netherlands11.8%

Switzerland6.4%

Australia4.2%

Other19.7%

Germany8.6%

France14.8%

United Kingdom26.7%

Italy10.1%

United States12.0%

Spain4.2%

Netherlands6.6%

Switzerland4.3%

Other12.7%

Source: iBoxx, UniCredit Research

IBOXX BANKS UT2 OUTSTANDING BY ISSUER COUNTRY IBOXX BANKS T1 OUTSTANDING BY ISSUER COUNTRY

Germany0.0%

Italy69.6%

Spain0.0%

Japan0.0%

Denmark30.4%

Other0.0%United Kingdom

0.0%

Germany9.3%

France35.4%

United Kingdom12.8%

Italy16.2%

United States0.0%

Spain1.8%

Netherlands0.0%

Switzerland7.3%

Other17.2%

Source: iBoxx, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 15 See last pages for disclaimer.

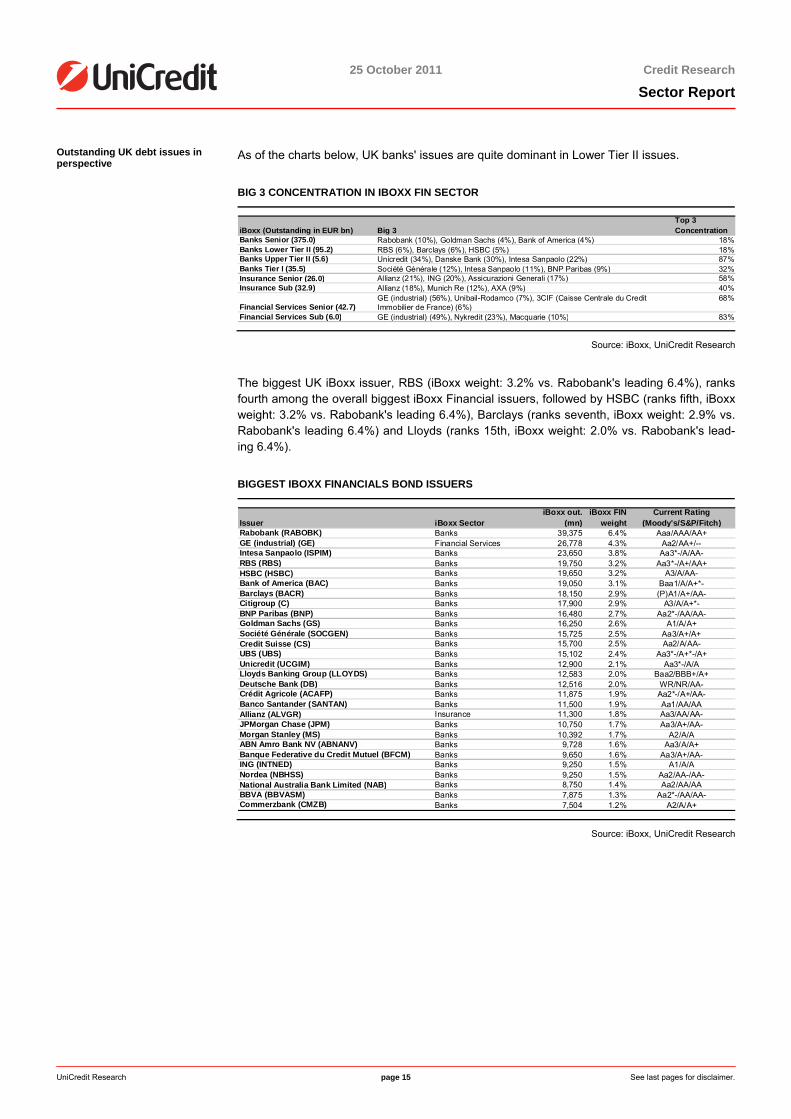

Outstanding UK debt issues in perspective

As of the charts below, UK banks' issues are quite dominant in Lower Tier II issues.

BIG 3 CONCENTRATION IN IBOXX FIN SECTOR

iBoxx (Outstanding in EUR bn) Big 3Top 3 Concentration

Banks Senior (375.0) Rabobank (10%), Goldman Sachs (4%), Bank of America (4%) 18%Banks Lower Tier II (95.2) RBS (6%), Barclays (6%), HSBC (5%) 18%Banks Upper Tier II (5.6) Unicredit (34%), Danske Bank (30%), Intesa Sanpaolo (22%) 87%Banks Tier I (35.5) Société Générale (12%), Intesa Sanpaolo (11%), BNP Paribas (9%) 32%Insurance Senior (26.0) Allianz (21%), ING (20%), Assicurazioni Generali (17%) 58%Insurance Sub (32.9) Allianz (18%), Munich Re (12%), AXA (9%) 40%

Financial Services Senior (42.7)GE (industrial) (56%), Unibail-Rodamco (7%), 3CIF (Caisse Centrale du Credit Immobilier de France) (6%)

68%

Financial Services Sub (6.0) GE (industrial) (49%), Nykredit (23%), Macquarie (10%) 83%

Source: iBoxx, UniCredit Research

The biggest UK iBoxx issuer, RBS (iBoxx weight: 3.2% vs. Rabobank's leading 6.4%), ranks fourth among the overall biggest iBoxx Financial issuers, followed by HSBC (ranks fifth, iBoxx weight: 3.2% vs. Rabobank's leading 6.4%), Barclays (ranks seventh, iBoxx weight: 2.9% vs. Rabobank's leading 6.4%) and Lloyds (ranks 15th, iBoxx weight: 2.0% vs. Rabobank's lead-ing 6.4%).

BIGGEST IBOXX FINANCIALS BOND ISSUERS

Issuer iBoxx SectoriBoxx out.

(mn)iBoxx FIN

weightCurrent Rating

(Moody's/S&P/Fitch)Rabobank (RABOBK) Banks 39,375 6.4% Aaa/AAA/AA+GE (industrial) (GE) Financial Services 26,778 4.3% Aa2/AA+/--Intesa Sanpaolo (ISPIM) Banks 23,650 3.8% Aa3*-/A/AA-RBS (RBS) Banks 19,750 3.2% Aa3*-/A+/AA+HSBC (HSBC) Banks 19,650 3.2% A3/A/AA-Bank of America (BAC) Banks 19,050 3.1% Baa1/A/A+*-Barclays (BACR) Banks 18,150 2.9% (P)A1/A+/AA-Citigroup (C) Banks 17,900 2.9% A3/A/A+*-BNP Paribas (BNP) Banks 16,480 2.7% Aa2*-/AA/AA-Goldman Sachs (GS) Banks 16,250 2.6% A1/A/A+Société Générale (SOCGEN) Banks 15,725 2.5% Aa3/A+/A+Credit Suisse (CS) Banks 15,700 2.5% Aa2/A/AA-UBS (UBS) Banks 15,102 2.4% Aa3*-/A+*-/A+Unicredit (UCGIM) Banks 12,900 2.1% Aa3*-/A/ALloyds Banking Group (LLOYDS) Banks 12,583 2.0% Baa2/BBB+/A+Deutsche Bank (DB) Banks 12,516 2.0% WR/NR/AA-Crédit Agricole (ACAFP) Banks 11,875 1.9% Aa2*-/A+/AA-Banco Santander (SANTAN) Banks 11,500 1.9% Aa1/AA/AAAllianz (ALVGR) Insurance 11,300 1.8% Aa3/AA/AA-JPMorgan Chase (JPM) Banks 10,750 1.7% Aa3/A+/AA-Morgan Stanley (MS) Banks 10,392 1.7% A2/A/AABN Amro Bank NV (ABNANV) Banks 9,728 1.6% Aa3/A/A+Banque Federative du Credit Mutuel (BFCM) Banks 9,650 1.6% Aa3/A+/AA-ING (INTNED) Banks 9,250 1.5% A1/A/ANordea (NBHSS) Banks 9,250 1.5% Aa2/AA-/AA-National Australia Bank Limited (NAB) Banks 8,750 1.4% Aa2/AA/AABBVA (BBVASM) Banks 7,875 1.3% Aa2*-/AA/AA-Commerzbank (CMZB) Banks 7,504 1.2% A2/A/A+

Source: iBoxx, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 16 See last pages for disclaimer.

The Stress-Robustness of major UK Banks Analysis of the UK banks' stress resilience

Stress-wise, the major individual UK banking groups showed the following overall ex-posure to periphery countries, according to EBA's 15 July stress test.

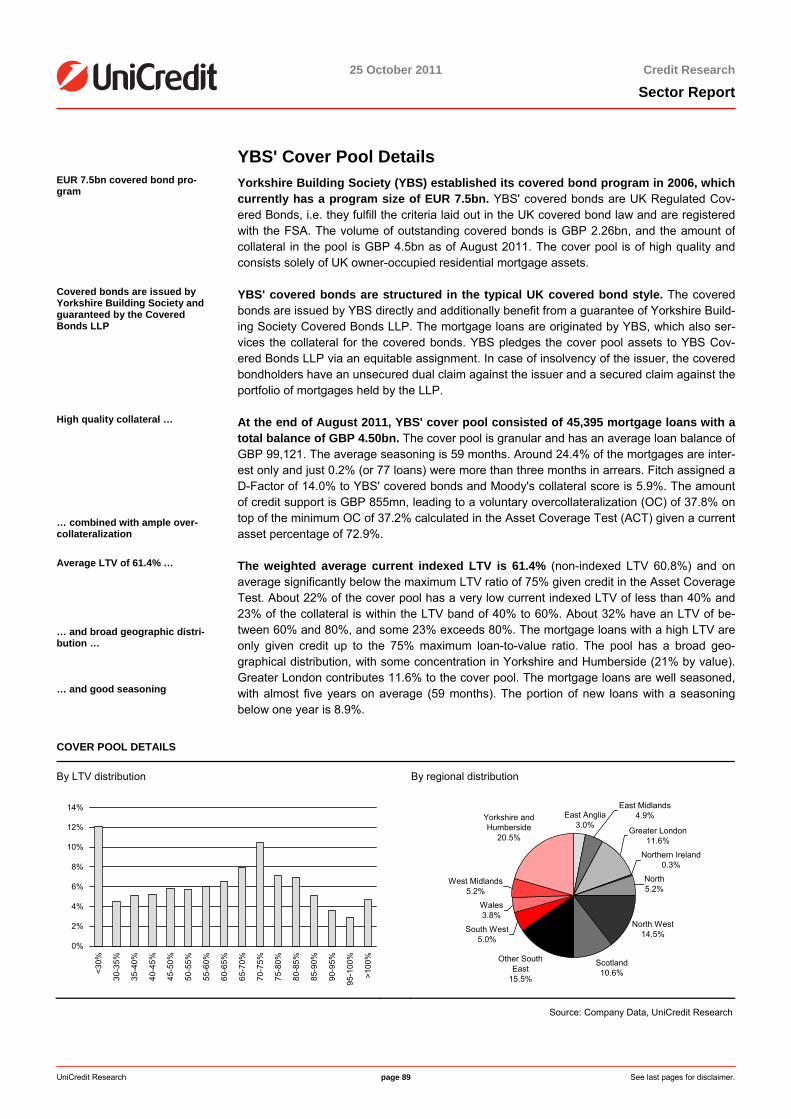

UK BANKS' EXPOSURE TO OVERALL TOTAL PERIPHERY COUNTRIES AS OF FY10 CT1

NB: Lloyds does not have any exposure to periphery countries according to EBA data. Source: EBA, UniCredit Research

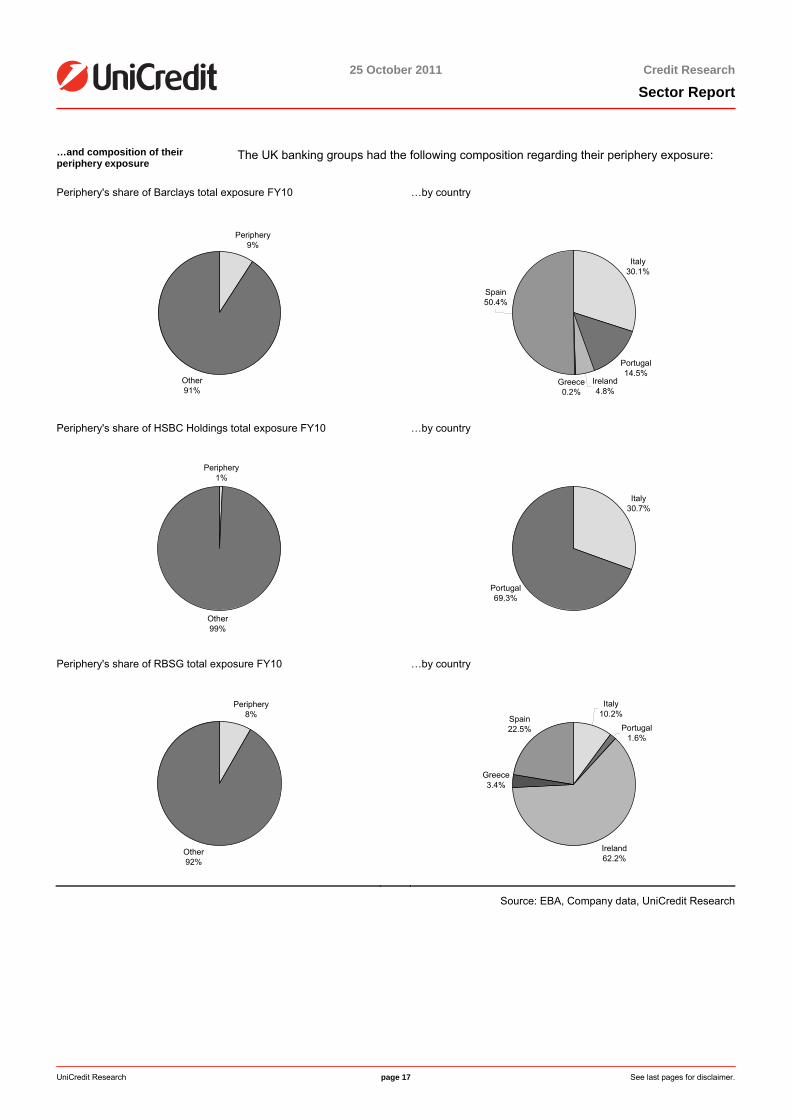

…and composition of their periphery exposure

The major individual UK banking groups had the following composition regarding their periph-ery exposure, according to EBA's 15 July stress test.

UK BANKS' SHARE OF INDIVIDUAL OVERALL TOTAL PERIPHERAL COUNTRY EXPOSURE AS OF FY10

Periphery's share as of FY10 Periphery's share of FY10 CT1 capital by country

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Barclays HSBC Holdings Lloyds BankingGroup

RBS Group

Italy Portugal Ireland Greece Spain

0%

20%

40%

60%

80%

100%

120%

Barclays HSBC Holdings Lloyds BankingGroup

RBS Group

Greece Ireland Italy Portugal Spain

NB: Lloyds does not have any exposure to periphery countries according to EBA data Source: EBA, Company data, UniCredit Research

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

Barclays HSBC Holdings Lloyds BankingGroup

RBS Group

25 October 2011 Credit Research

Sector Report

UniCredit Research page 17 See last pages for disclaimer.

…and composition of their periphery exposure

The UK banking groups had the following composition regarding their periphery exposure:

Periphery's share of Barclays total exposure FY10 …by country

Periphery9%

Other91%

Italy30.1%

Portugal14.5%

Ireland4.8%

Greece0.2%

Spain50.4%

Periphery's share of HSBC Holdings total exposure FY10 …by country

Periphery1%

Other99%

Italy30.7%

Portugal69.3%

Periphery's share of RBSG total exposure FY10 …by country

Periphery8%

Other92%

Italy10.2%

Portugal1.6%

Ireland62.2%

Greece3.4%

Spain22.5%

Source: EBA, Company data, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 18 See last pages for disclaimer.

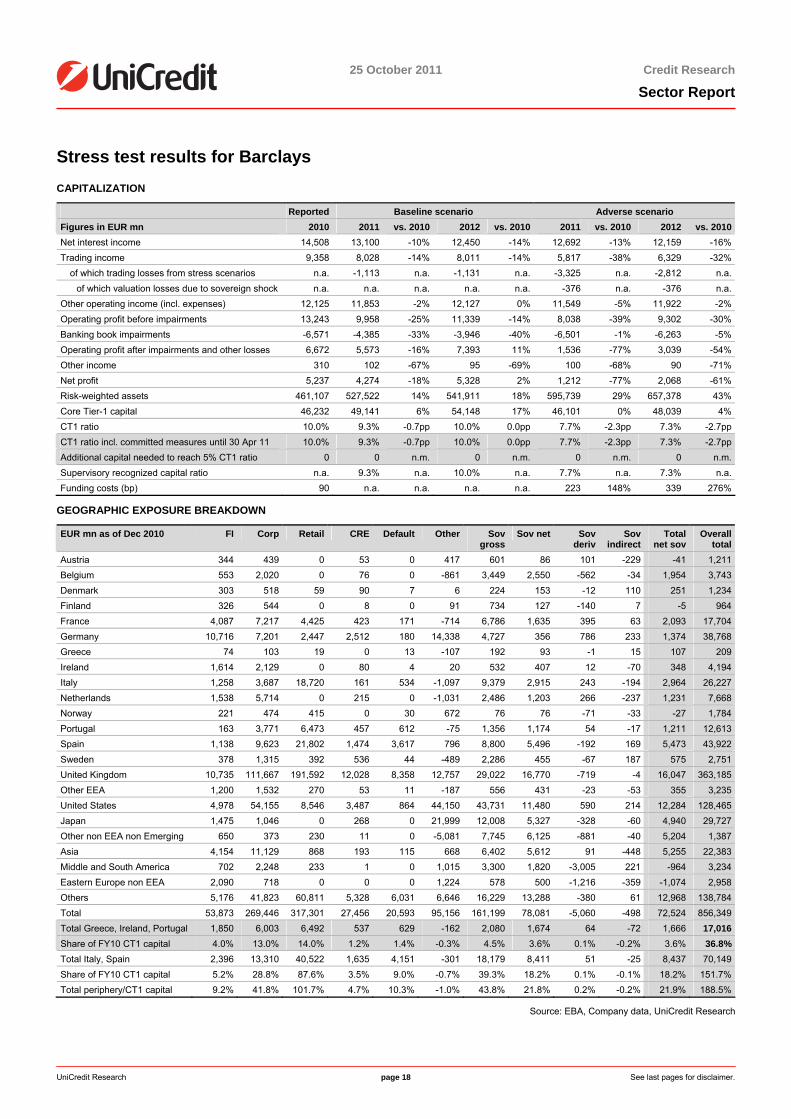

Stress test results for Barclays CAPITALIZATION

Reported Baseline scenario Adverse scenario Figures in EUR mn 2010 2011 vs. 2010 2012 vs. 2010 2011 vs. 2010 2012 vs. 2010Net interest income 14,508 13,100 -10% 12,450 -14% 12,692 -13% 12,159 -16%Trading income 9,358 8,028 -14% 8,011 -14% 5,817 -38% 6,329 -32%

of which trading losses from stress scenarios n.a. -1,113 n.a. -1,131 n.a. -3,325 n.a. -2,812 n.a.of which valuation losses due to sovereign shock n.a. n.a. n.a. n.a. n.a. -376 n.a. -376 n.a.

Other operating income (incl. expenses) 12,125 11,853 -2% 12,127 0% 11,549 -5% 11,922 -2%Operating profit before impairments 13,243 9,958 -25% 11,339 -14% 8,038 -39% 9,302 -30%Banking book impairments -6,571 -4,385 -33% -3,946 -40% -6,501 -1% -6,263 -5%Operating profit after impairments and other losses 6,672 5,573 -16% 7,393 11% 1,536 -77% 3,039 -54%Other income 310 102 -67% 95 -69% 100 -68% 90 -71%Net profit 5,237 4,274 -18% 5,328 2% 1,212 -77% 2,068 -61%Risk-weighted assets 461,107 527,522 14% 541,911 18% 595,739 29% 657,378 43%Core Tier-1 capital 46,232 49,141 6% 54,148 17% 46,101 0% 48,039 4%CT1 ratio 10.0% 9.3% -0.7pp 10.0% 0.0pp 7.7% -2.3pp 7.3% -2.7ppCT1 ratio incl. committed measures until 30 Apr 11 10.0% 9.3% -0.7pp 10.0% 0.0pp 7.7% -2.3pp 7.3% -2.7ppAdditional capital needed to reach 5% CT1 ratio 0 0 n.m. 0 n.m. 0 n.m. 0 n.m.Supervisory recognized capital ratio n.a. 9.3% n.a. 10.0% n.a. 7.7% n.a. 7.3% n.a.Funding costs (bp) 90 n.a. n.a. n.a. n.a. 223 148% 339 276%

GEOGRAPHIC EXPOSURE BREAKDOWN

EUR mn as of Dec 2010 FI Corp Retail CRE Default Other Sov gross

Sov net Sov deriv

Sov indirect

Total net sov

Overall total

Austria 344 439 0 53 0 417 601 86 101 -229 -41 1,211Belgium 553 2,020 0 76 0 -861 3,449 2,550 -562 -34 1,954 3,743Denmark 303 518 59 90 7 6 224 153 -12 110 251 1,234Finland 326 544 0 8 0 91 734 127 -140 7 -5 964France 4,087 7,217 4,425 423 171 -714 6,786 1,635 395 63 2,093 17,704Germany 10,716 7,201 2,447 2,512 180 14,338 4,727 356 786 233 1,374 38,768Greece 74 103 19 0 13 -107 192 93 -1 15 107 209Ireland 1,614 2,129 0 80 4 20 532 407 12 -70 348 4,194Italy 1,258 3,687 18,720 161 534 -1,097 9,379 2,915 243 -194 2,964 26,227Netherlands 1,538 5,714 0 215 0 -1,031 2,486 1,203 266 -237 1,231 7,668Norway 221 474 415 0 30 672 76 76 -71 -33 -27 1,784Portugal 163 3,771 6,473 457 612 -75 1,356 1,174 54 -17 1,211 12,613Spain 1,138 9,623 21,802 1,474 3,617 796 8,800 5,496 -192 169 5,473 43,922Sweden 378 1,315 392 536 44 -489 2,286 455 -67 187 575 2,751United Kingdom 10,735 111,667 191,592 12,028 8,358 12,757 29,022 16,770 -719 -4 16,047 363,185Other EEA 1,200 1,532 270 53 11 -187 556 431 -23 -53 355 3,235United States 4,978 54,155 8,546 3,487 864 44,150 43,731 11,480 590 214 12,284 128,465Japan 1,475 1,046 0 268 0 21,999 12,008 5,327 -328 -60 4,940 29,727Other non EEA non Emerging 650 373 230 11 0 -5,081 7,745 6,125 -881 -40 5,204 1,387Asia 4,154 11,129 868 193 115 668 6,402 5,612 91 -448 5,255 22,383Middle and South America 702 2,248 233 1 0 1,015 3,300 1,820 -3,005 221 -964 3,234Eastern Europe non EEA 2,090 718 0 0 0 1,224 578 500 -1,216 -359 -1,074 2,958Others 5,176 41,823 60,811 5,328 6,031 6,646 16,229 13,288 -380 61 12,968 138,784Total 53,873 269,446 317,301 27,456 20,593 95,156 161,199 78,081 -5,060 -498 72,524 856,349Total Greece, Ireland, Portugal 1,850 6,003 6,492 537 629 -162 2,080 1,674 64 -72 1,666 17,016Share of FY10 CT1 capital 4.0% 13.0% 14.0% 1.2% 1.4% -0.3% 4.5% 3.6% 0.1% -0.2% 3.6% 36.8%Total Italy, Spain 2,396 13,310 40,522 1,635 4,151 -301 18,179 8,411 51 -25 8,437 70,149Share of FY10 CT1 capital 5.2% 28.8% 87.6% 3.5% 9.0% -0.7% 39.3% 18.2% 0.1% -0.1% 18.2% 151.7%Total periphery/CT1 capital 9.2% 41.8% 101.7% 4.7% 10.3% -1.0% 43.8% 21.8% 0.2% -0.2% 21.9% 188.5%

Source: EBA, Company data, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 19 See last pages for disclaimer.

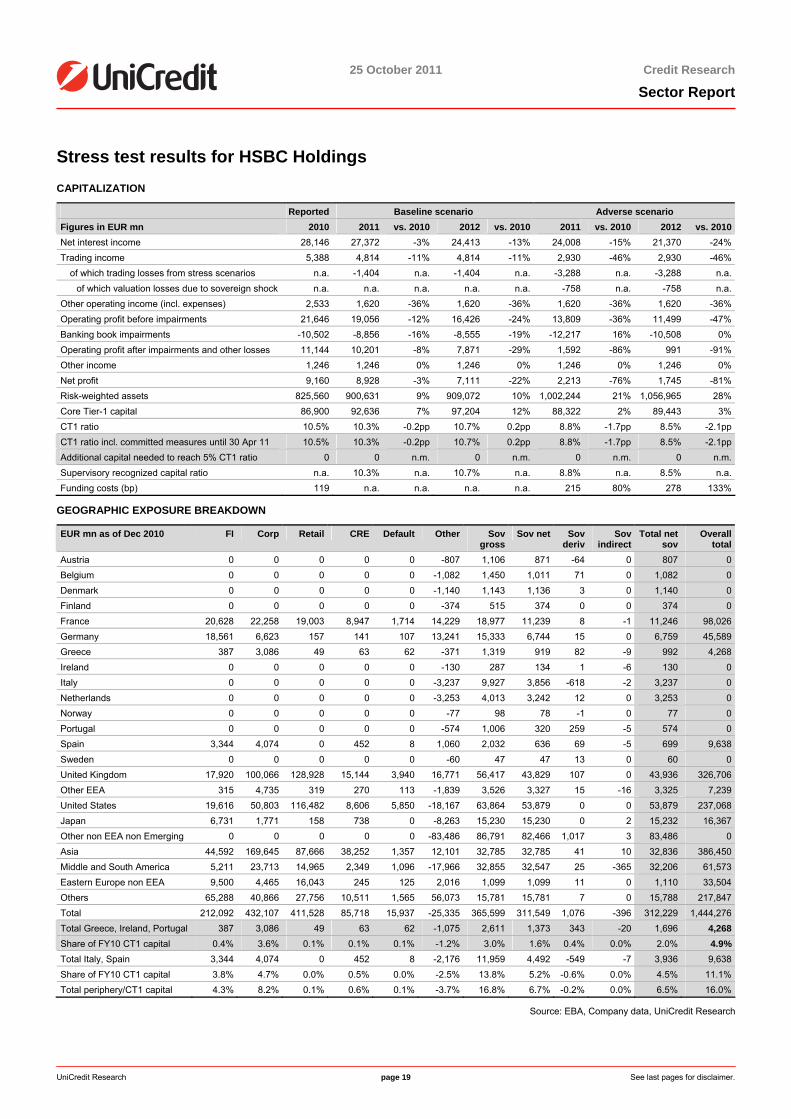

Stress test results for HSBC Holdings CAPITALIZATION

Reported Baseline scenario Adverse scenario Figures in EUR mn 2010 2011 vs. 2010 2012 vs. 2010 2011 vs. 2010 2012 vs. 2010Net interest income 28,146 27,372 -3% 24,413 -13% 24,008 -15% 21,370 -24%Trading income 5,388 4,814 -11% 4,814 -11% 2,930 -46% 2,930 -46%

of which trading losses from stress scenarios n.a. -1,404 n.a. -1,404 n.a. -3,288 n.a. -3,288 n.a.of which valuation losses due to sovereign shock n.a. n.a. n.a. n.a. n.a. -758 n.a. -758 n.a.

Other operating income (incl. expenses) 2,533 1,620 -36% 1,620 -36% 1,620 -36% 1,620 -36%Operating profit before impairments 21,646 19,056 -12% 16,426 -24% 13,809 -36% 11,499 -47%Banking book impairments -10,502 -8,856 -16% -8,555 -19% -12,217 16% -10,508 0%Operating profit after impairments and other losses 11,144 10,201 -8% 7,871 -29% 1,592 -86% 991 -91%Other income 1,246 1,246 0% 1,246 0% 1,246 0% 1,246 0%Net profit 9,160 8,928 -3% 7,111 -22% 2,213 -76% 1,745 -81%Risk-weighted assets 825,560 900,631 9% 909,072 10% 1,002,244 21% 1,056,965 28%Core Tier-1 capital 86,900 92,636 7% 97,204 12% 88,322 2% 89,443 3%CT1 ratio 10.5% 10.3% -0.2pp 10.7% 0.2pp 8.8% -1.7pp 8.5% -2.1ppCT1 ratio incl. committed measures until 30 Apr 11 10.5% 10.3% -0.2pp 10.7% 0.2pp 8.8% -1.7pp 8.5% -2.1ppAdditional capital needed to reach 5% CT1 ratio 0 0 n.m. 0 n.m. 0 n.m. 0 n.m.Supervisory recognized capital ratio n.a. 10.3% n.a. 10.7% n.a. 8.8% n.a. 8.5% n.a.Funding costs (bp) 119 n.a. n.a. n.a. n.a. 215 80% 278 133%

GEOGRAPHIC EXPOSURE BREAKDOWN

EUR mn as of Dec 2010 FI Corp Retail CRE Default Other Sov gross

Sov net Sov deriv

Sov indirect

Total net sov

Overall total

Austria 0 0 0 0 0 -807 1,106 871 -64 0 807 0Belgium 0 0 0 0 0 -1,082 1,450 1,011 71 0 1,082 0Denmark 0 0 0 0 0 -1,140 1,143 1,136 3 0 1,140 0Finland 0 0 0 0 0 -374 515 374 0 0 374 0France 20,628 22,258 19,003 8,947 1,714 14,229 18,977 11,239 8 -1 11,246 98,026Germany 18,561 6,623 157 141 107 13,241 15,333 6,744 15 0 6,759 45,589Greece 387 3,086 49 63 62 -371 1,319 919 82 -9 992 4,268Ireland 0 0 0 0 0 -130 287 134 1 -6 130 0Italy 0 0 0 0 0 -3,237 9,927 3,856 -618 -2 3,237 0Netherlands 0 0 0 0 0 -3,253 4,013 3,242 12 0 3,253 0Norway 0 0 0 0 0 -77 98 78 -1 0 77 0Portugal 0 0 0 0 0 -574 1,006 320 259 -5 574 0Spain 3,344 4,074 0 452 8 1,060 2,032 636 69 -5 699 9,638Sweden 0 0 0 0 0 -60 47 47 13 0 60 0United Kingdom 17,920 100,066 128,928 15,144 3,940 16,771 56,417 43,829 107 0 43,936 326,706Other EEA 315 4,735 319 270 113 -1,839 3,526 3,327 15 -16 3,325 7,239United States 19,616 50,803 116,482 8,606 5,850 -18,167 63,864 53,879 0 0 53,879 237,068Japan 6,731 1,771 158 738 0 -8,263 15,230 15,230 0 2 15,232 16,367Other non EEA non Emerging 0 0 0 0 0 -83,486 86,791 82,466 1,017 3 83,486 0Asia 44,592 169,645 87,666 38,252 1,357 12,101 32,785 32,785 41 10 32,836 386,450Middle and South America 5,211 23,713 14,965 2,349 1,096 -17,966 32,855 32,547 25 -365 32,206 61,573Eastern Europe non EEA 9,500 4,465 16,043 245 125 2,016 1,099 1,099 11 0 1,110 33,504Others 65,288 40,866 27,756 10,511 1,565 56,073 15,781 15,781 7 0 15,788 217,847Total 212,092 432,107 411,528 85,718 15,937 -25,335 365,599 311,549 1,076 -396 312,229 1,444,276Total Greece, Ireland, Portugal 387 3,086 49 63 62 -1,075 2,611 1,373 343 -20 1,696 4,268Share of FY10 CT1 capital 0.4% 3.6% 0.1% 0.1% 0.1% -1.2% 3.0% 1.6% 0.4% 0.0% 2.0% 4.9%Total Italy, Spain 3,344 4,074 0 452 8 -2,176 11,959 4,492 -549 -7 3,936 9,638Share of FY10 CT1 capital 3.8% 4.7% 0.0% 0.5% 0.0% -2.5% 13.8% 5.2% -0.6% 0.0% 4.5% 11.1%Total periphery/CT1 capital 4.3% 8.2% 0.1% 0.6% 0.1% -3.7% 16.8% 6.7% -0.2% 0.0% 6.5% 16.0%

Source: EBA, Company data, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 20 See last pages for disclaimer.

Stress test results for Lloyds Banking Group CAPITALIZATION

Reported Baseline scenario Adverse scenario Figures in EUR mn 2010 2011 vs. 2010 2012 vs. 2010 2011 vs. 2010 2012 vs. 2010Net interest income 16,363 16,012 -2% 15,030 -8% 14,759 -10% 14,589 -11%Trading income 374 307 -18% 307 -18% 132 -65% 132 -65%

of which trading losses from stress scenarios n.a. -18 n.a. -18 n.a. -194 n.a. -194 n.a.of which valuation losses due to sovereign shock n.a. n.a. n.a. n.a. n.a. -30 n.a. -30 n.a.

Other operating income (incl. expenses) 8,161 4,158 -49% 7,409 -9% 4,114 -50% 7,336 -10%Operating profit before impairments 13,022 9,182 -29% 12,084 -7% 7,717 -41% 11,380 -13%Banking book impairments -15,313 -8,681 -43% -5,164 -66% -20,145 32% -11,399 -26%Operating profit after impairments and other losses -2,292 501 -122% 6,920 -402% -12,428 442% -19 -99%Other income 980 -1,679 -271% 1,097 12% 1,919 96% -646 -166%Net profit -1,938 -1,246 -36% 5,772 -398% -8,104 318% -653 -66%Risk-weighted assets 472,114 483,304 2% 484,176 3% 520,087 10% 548,300 16%Core Tier-1 capital 47,984 48,044 0% 53,127 11% 41,193 -14% 39,851 -17%CT1 ratio 10.2% 9.9% -0.2pp 11.0% 0.8pp 7.9% -2.2pp 7.3% -2.9ppCT1 ratio incl. committed measures until 30 Apr 11 10.2% 10.2% 0.0pp 11.7% 1.5pp 8.1% -2.1pp 7.7% -2.4ppAdditional capital needed to reach 5% CT1 ratio 0 0 n.m. 0 n.m. 0 n.m. 0 n.m.Supervisory recognized capital ratio n.a. 10.2% n.a. 11.7% n.a. 8.1% n.a. 7.7% n.a.Funding costs (bp) 143 n.a. n.a. n.a. n.a. 262 84% 368 158%

GEOGRAPHIC EXPOSURE BREAKDOWN

EUR mn as of Dec 2010 FI Corp Retail CRE Default Other Sov gross

Sov net Sov deriv

Sov indirect

Total net sov

Overall total

Austria 0 0 0 0 0 -1 1 1 0 0 1 0Belgium 0 0 0 0 0 -5 0 0 5 0 5 0Denmark 0 0 0 0 0 -2 2 2 0 0 2 0Finland 0 0 0 0 0 0 0 0 0 0 0 0France 0 0 0 0 0 -765 765 765 0 0 765 0Germany 0 0 0 0 0 -1,911 1,911 1,911 0 0 1,911 0Greece 0 0 0 0 0 0 0 0 0 0 0 0Ireland 0 0 0 0 0 0 0 0 0 0 0 0Italy 0 0 0 0 0 -17 32 32 0 -15 17 0Netherlands 0 0 0 0 0 0 0 0 0 0 0 0Norway 0 0 0 0 0 0 0 0 0 0 0 0Portugal 0 0 0 0 0 0 0 0 0 0 0 0Spain 0 0 0 0 0 -62 62 62 0 0 62 0Sweden 0 0 0 0 0 0 0 0 0 0 0 0United Kingdom 7,173 116,550 504,795 47,870 37,661 87,216 15,143 15,143 1 0 15,143 816,409Other EEA 0 0 0 0 0 -505 502 502 2 0 505 0United States 5,214 19,518 103 23 1,258 28,481 12,253 12,253 0 1 12,254 66,852Japan 0 0 0 0 0 0 0 0 0 0 0 0Other non EEA non Emerging 0 0 0 0 0 -498 2,043 499 -1 0 498 0Asia 0 0 0 0 0 -26 0 0 26 0 26 0Middle and South America 0 0 0 0 0 0 0 0 0 0 0 0Eastern Europe non EEA 0 0 0 0 0 0 0 0 0 0 0 0Others 16,846 45,872 24,780 8,345 18,366 47,244 0 0 0 0 0 161,452Total 29,233 181,940 529,679 56,238 57,285 159,149 32,715 31,171 32 -14 31,189 1,044,713Total Greece, Ireland, Portugal 0 0 0 0 0 0 0 0 0 0 0 0Share of FY10 CT1 capital 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%Total Italy, Spain 0 0 0 0 0 -79 94 94 0 -15 79 0Share of FY10 CT1 capital 0.0% 0.0% 0.0% 0.0% 0.0% -0.2% 0.2% 0.2% 0.0% 0.0% 0.2% 0.0%Total periphery/CT1 capital 0.0% 0.0% 0.0% 0.0% 0.0% -0.2% 0.2% 0.2% 0.0% 0.0% 0.2% 0.0%

Source: EBA, Company data, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 21 See last pages for disclaimer.

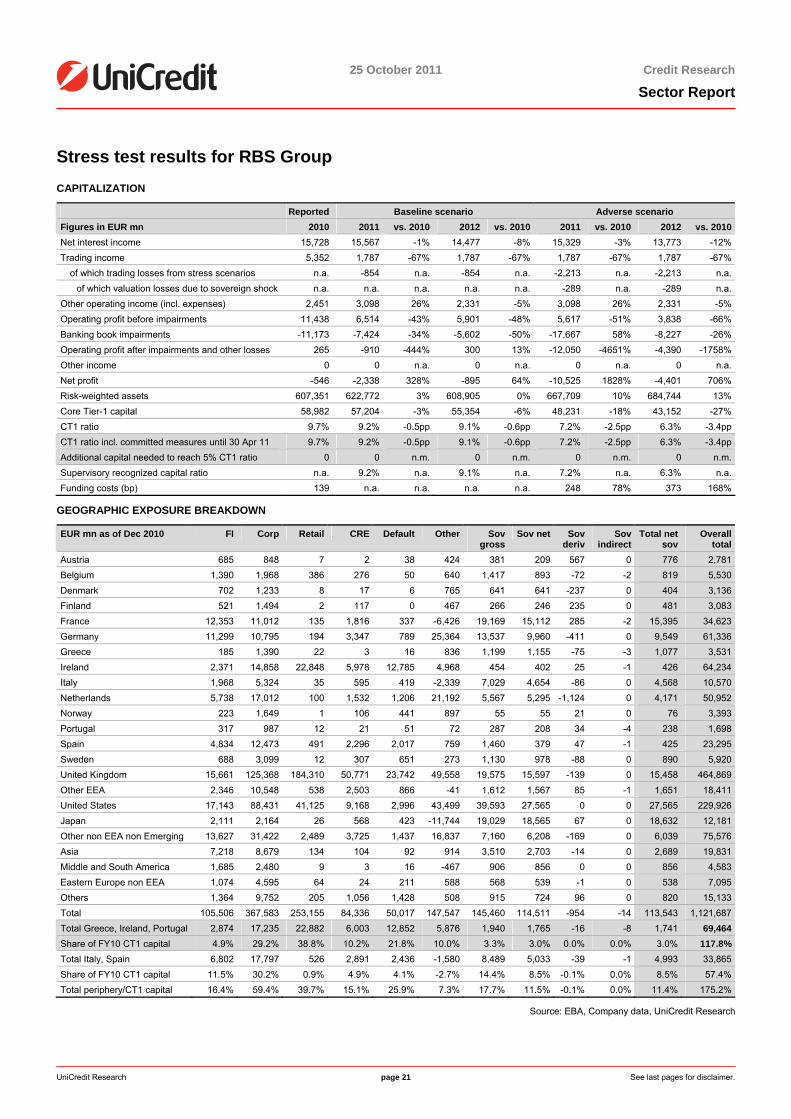

Stress test results for RBS Group CAPITALIZATION

Reported Baseline scenario Adverse scenario Figures in EUR mn 2010 2011 vs. 2010 2012 vs. 2010 2011 vs. 2010 2012 vs. 2010Net interest income 15,728 15,567 -1% 14,477 -8% 15,329 -3% 13,773 -12%Trading income 5,352 1,787 -67% 1,787 -67% 1,787 -67% 1,787 -67%

of which trading losses from stress scenarios n.a. -854 n.a. -854 n.a. -2,213 n.a. -2,213 n.a.of which valuation losses due to sovereign shock n.a. n.a. n.a. n.a. n.a. -289 n.a. -289 n.a.

Other operating income (incl. expenses) 2,451 3,098 26% 2,331 -5% 3,098 26% 2,331 -5%Operating profit before impairments 11,438 6,514 -43% 5,901 -48% 5,617 -51% 3,838 -66%Banking book impairments -11,173 -7,424 -34% -5,602 -50% -17,667 58% -8,227 -26%Operating profit after impairments and other losses 265 -910 -444% 300 13% -12,050 -4651% -4,390 -1758%Other income 0 0 n.a. 0 n.a. 0 n.a. 0 n.a.Net profit -546 -2,338 328% -895 64% -10,525 1828% -4,401 706%Risk-weighted assets 607,351 622,772 3% 608,905 0% 667,709 10% 684,744 13%Core Tier-1 capital 58,982 57,204 -3% 55,354 -6% 48,231 -18% 43,152 -27%CT1 ratio 9.7% 9.2% -0.5pp 9.1% -0.6pp 7.2% -2.5pp 6.3% -3.4ppCT1 ratio incl. committed measures until 30 Apr 11 9.7% 9.2% -0.5pp 9.1% -0.6pp 7.2% -2.5pp 6.3% -3.4ppAdditional capital needed to reach 5% CT1 ratio 0 0 n.m. 0 n.m. 0 n.m. 0 n.m.Supervisory recognized capital ratio n.a. 9.2% n.a. 9.1% n.a. 7.2% n.a. 6.3% n.a.Funding costs (bp) 139 n.a. n.a. n.a. n.a. 248 78% 373 168%

GEOGRAPHIC EXPOSURE BREAKDOWN

EUR mn as of Dec 2010 FI Corp Retail CRE Default Other Sov gross

Sov net Sov deriv

Sov indirect

Total net sov

Overall total

Austria 685 848 7 2 38 424 381 209 567 0 776 2,781Belgium 1,390 1,968 386 276 50 640 1,417 893 -72 -2 819 5,530Denmark 702 1,233 8 17 6 765 641 641 -237 0 404 3,136Finland 521 1,494 2 117 0 467 266 246 235 0 481 3,083France 12,353 11,012 135 1,816 337 -6,426 19,169 15,112 285 -2 15,395 34,623Germany 11,299 10,795 194 3,347 789 25,364 13,537 9,960 -411 0 9,549 61,336Greece 185 1,390 22 3 16 836 1,199 1,155 -75 -3 1,077 3,531Ireland 2,371 14,858 22,848 5,978 12,785 4,968 454 402 25 -1 426 64,234Italy 1,968 5,324 35 595 419 -2,339 7,029 4,654 -86 0 4,568 10,570Netherlands 5,738 17,012 100 1,532 1,206 21,192 5,567 5,295 -1,124 0 4,171 50,952Norway 223 1,649 1 106 441 897 55 55 21 0 76 3,393Portugal 317 987 12 21 51 72 287 208 34 -4 238 1,698Spain 4,834 12,473 491 2,296 2,017 759 1,460 379 47 -1 425 23,295Sweden 688 3,099 12 307 651 273 1,130 978 -88 0 890 5,920United Kingdom 15,661 125,368 184,310 50,771 23,742 49,558 19,575 15,597 -139 0 15,458 464,869Other EEA 2,346 10,548 538 2,503 866 -41 1,612 1,567 85 -1 1,651 18,411United States 17,143 88,431 41,125 9,168 2,996 43,499 39,593 27,565 0 0 27,565 229,926Japan 2,111 2,164 26 568 423 -11,744 19,029 18,565 67 0 18,632 12,181Other non EEA non Emerging 13,627 31,422 2,489 3,725 1,437 16,837 7,160 6,208 -169 0 6,039 75,576Asia 7,218 8,679 134 104 92 914 3,510 2,703 -14 0 2,689 19,831Middle and South America 1,685 2,480 9 3 16 -467 906 856 0 0 856 4,583Eastern Europe non EEA 1,074 4,595 64 24 211 588 568 539 -1 0 538 7,095Others 1,364 9,752 205 1,056 1,428 508 915 724 96 0 820 15,133Total 105,506 367,583 253,155 84,336 50,017 147,547 145,460 114,511 -954 -14 113,543 1,121,687Total Greece, Ireland, Portugal 2,874 17,235 22,882 6,003 12,852 5,876 1,940 1,765 -16 -8 1,741 69,464Share of FY10 CT1 capital 4.9% 29.2% 38.8% 10.2% 21.8% 10.0% 3.3% 3.0% 0.0% 0.0% 3.0% 117.8%Total Italy, Spain 6,802 17,797 526 2,891 2,436 -1,580 8,489 5,033 -39 -1 4,993 33,865Share of FY10 CT1 capital 11.5% 30.2% 0.9% 4.9% 4.1% -2.7% 14.4% 8.5% -0.1% 0.0% 8.5% 57.4%Total periphery/CT1 capital 16.4% 59.4% 39.7% 15.1% 25.9% 7.3% 17.7% 11.5% -0.1% 0.0% 11.4% 175.2%

Source: EBA, Company data, UniCredit Research

25 October 2011 Credit Research

Sector Report

UniCredit Research page 22 See last pages for disclaimer.

Regulation Overview Banking regulation in the UK is currently based on a three-pillar system consisting of

the Financial Services Authority (FSA), the Bank of England and HM Treasury. Together these three institutions are known as the UK Authorities. However, the three-pillar system will cease to exist by the end of 2012, with major responsibilities being shifted from the FSA to the Bank of England.

HM Treasury Her Majesty's Treasury (HM Treasury) is the British finance ministry. Led by the Chan-cellor of the Exchequer, it represents the political branch of the UK Authorities, with responsi-bility for the design of the overall legal and regulatory framework, which constrains and con-trols the operations of financial businesses within the UK.

Financial Services Authority (FSA)

The Financial Services Authority (FSA) regulates and supervises financial markets andfirms (including mortgage businesses, insurance companies, banks and building so-cieties) within a framework set by the British government through HM Treasury. The Financial Services and Markets Act 2000 provides the legal basis for FSA's operations. The FSA is an organization entirely funded by the institutions it supervises, yet it is still account-able to HM Treasury and to Parliament. The framework underlying FSA's regulatory activity isthe Advanced Risk-Responsive Operating Framework (ARROW), with its current form (AR-ROW II) having been introduced in 2006. Its methodology tries to asses the risk caused by single firms as well as sectors or even market risk. The FSA undertakes some basic risk as-sessment (overseeing the company's financial situation and compliance standards) for allfirms independent of the risk they bare for financial markets as a whole. In addition, the FSA maintains close contact to the management of firms, which bare a higher risk for financialmarkets. Furthermore, the FSA is responsible for preventing financial crimes, such as moneylaundering, fraud or market abuse. However, key competencies will be shifted from the FSA to the Bank of England as part of a reform of the British financial regulatory bodies.

The Bank of England The Bank of England's objective is to contribute to stability and soundness within the British financial system by monitoring financial institutions, overseeing payments, and functioning as a lender of last resort if needed. So, in comparison to the FSA, which fo-cuses on assessing the risk individual firms have on the financial system, the Bank of England screens financial and money markets as a whole for potential disruptions. The Bank of Eng-land is also responsible for ensuring the availability of funds for lending businesses and actsas a lender of last resort in times of crises.

Future developments The British government plans to undertake a reform of the financial sector regulatory body, which will shift competencies to the Bank of England and abolish the FSA. In-stead, a Financial Policy Committee (FPC) will be created within the Bank of England, which will be responsible for risk management in the financial sector from a macro point of view.Furthermore, a so-called Prudential Regulation Authority (PRA) will be established, with the task of assessing the soundness of financial institutions, including the assessment of their business models. Furthermore, a Financial Conduct Authority (FCA) will be created, ensuringproper conduct of financial service providers and protecting the interests of consumers. Thisreform aims at centralizing competencies and resources at the Bank of England in order to create a single institution, being able to control the financial system. According to HM Treas-ury, the new regulatory framework will take effect in late 2012.

Special Resolution Regime The Special Resolution Regime (SRR) gives the British financial authorities specialcompetences to deal with financial institutions that are in distress. The authorities can select from a wide range of possible measures taking into account the specific situation of the distressed institution. These measures include nationalizing banks for a limited amount of time, selling banks' assets or initiating insolvency proceedings. In order to put a bank under SRR, approval from all three UK authorities is needed, with HM Treasury being responsible for the potential nationalization of a bank's assets.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 23 See last pages for disclaimer.

The UK Covered Bond Legislation UK covered bond legislation is in place since 2008 …

In March 2008, the UK covered bond legislation came into force and on 6 April 2011, HM Treasury and the FSA published its "Review of the UK's regulatory framework for cov-ered bonds". The legislation is a principle-based framework. Issuers of covered bonds can have their covered-bond programs registered with the Financial Services Authority (FSA) inorder to receive regulated covered bond status – but are not required to do so. The FSA pub-lishes the issuers of regulated covered bonds as well as a list of regulated covered bonds per issuer on their website (http://www.fsa.gov.uk/Pages/Register/rcb_register/index.shtml). Cur-rently, there are eleven issuers with regulated covered bonds in the UK: Abbey NationalTreasury Services, Bank of Scotland, Barclays, Clydesdale Bank, Coventry Building Society, HSBC Bank, Leeds Building Society, Lloyds TSB Bank, Nationwide Building Society, RoyalBank of Scotland, and Yorkshire Building Society.

… and was built around already existing programs

The UK covered bond legislation was built around already existing covered bond pro-grams and structures. Hence, certain elements of UK regulated covered bonds are alsosubject to common law, i.e. the segregation of assets via equitable assignment to a specialpurpose vehicle. The key elements of the UK covered bond legislation are:

Key aspects ■ Issuers: Issuance of covered bonds is restricted to UK authorized credit institutions.

■ Priority claim: The regulated covered bonds are direct, unconditional obligations of theissuer, but have also a priority claim over the cover pool in case of the insolvency of the is-suer.

■ Asset pool and eligible property: The definition of eligible assets is, in general, based on the CRD (Directive 2006/48/EC §68 of Annex VI), thus permitting residential and commer-cial mortgages, public sector loans, and shipping mortgages. However, in respect to publicsector debt, HMT limited exposures to Credit Step 1 bodies only (while the CRD also al-lows for Credit Step 2 bodies up to 20% of covered bonds). Social housing and loans re-lated to Public Partnership Projects, where these are secured by a public body with step-in rights, is explicitly mentioned as eligible property.

■ Use of RMBS/CMBS: The use of RMBS and of CMBS as collateral is defined narrower than in the CRD, limiting the range of eligible securities to residential real estate or com-mercial real estate exposures which were originated or acquired by the issuer, and only if the senior units have an AAA rating.

■ Regional scope: The regional scope of eligible property is restricted to property located inan EEA state, Switzerland, the US, Japan, Canada, Australia, New Zealand, the ChannelIslands or the Isle of Man.

■ Overcollateralization: UK legislation does not stipulate a minimum level of overcollaterali-zation, but requires sufficient collateral at all times. The level of overcollateralization is thussubject to the respective covered bond programs.

■ Register: A special record has to be kept of each asset in the asset pool.

■ Regular reporting: In order to ensure the quality of the cover pool, a report to the FSA isstipulated in the law. The issuer has to provide information regarding the assets in the rele-vant asset pool and the quality of these assets, as well as the capability of coverage, andtimely payment of claims. The frequency of reporting can be determined by the FSA.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 24 See last pages for disclaimer.

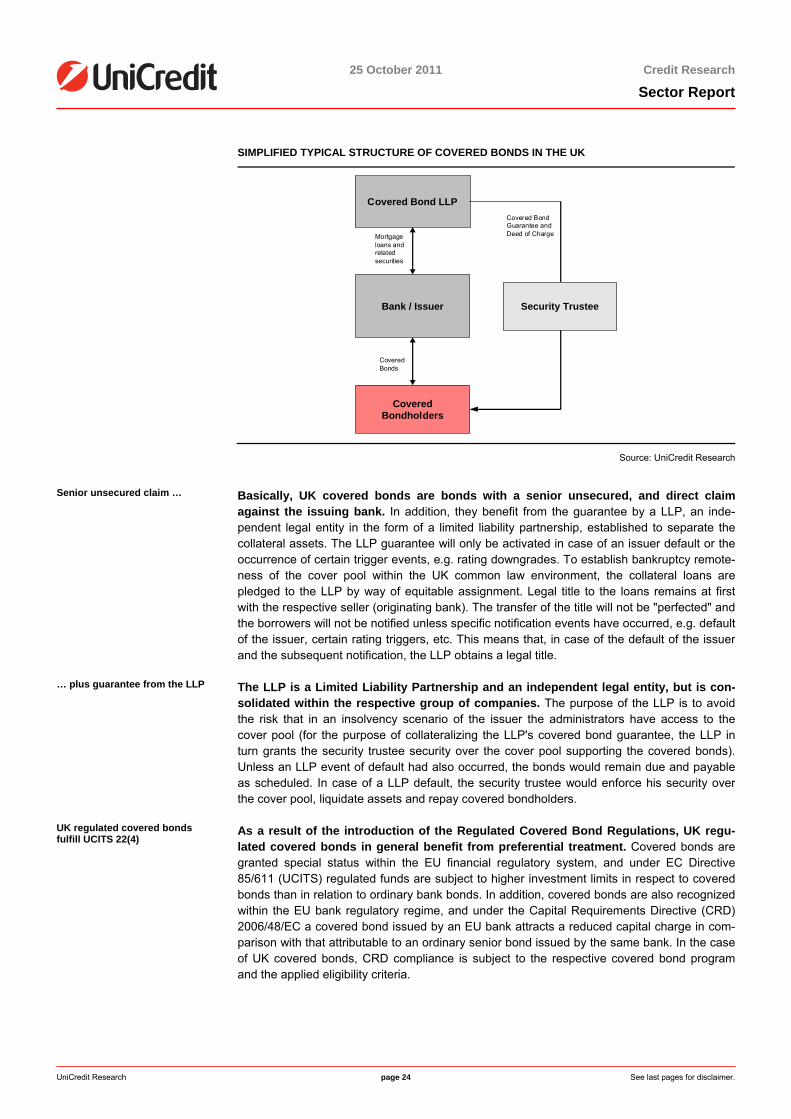

SIMPLIFIED TYPICAL STRUCTURE OF COVERED BONDS IN THE UK

Bank / Issuer

CoveredBondholders

Mortgage loans and related securities

Covered Bond LLP

Covered Bonds

Covered Bond Guarantee and Deed of Charge

Security Trustee

Source: UniCredit Research

Senior unsecured claim … Basically, UK covered bonds are bonds with a senior unsecured, and direct claim against the issuing bank. In addition, they benefit from the guarantee by a LLP, an inde-pendent legal entity in the form of a limited liability partnership, established to separate the collateral assets. The LLP guarantee will only be activated in case of an issuer default or theoccurrence of certain trigger events, e.g. rating downgrades. To establish bankruptcy remote-ness of the cover pool within the UK common law environment, the collateral loans arepledged to the LLP by way of equitable assignment. Legal title to the loans remains at firstwith the respective seller (originating bank). The transfer of the title will not be "perfected" andthe borrowers will not be notified unless specific notification events have occurred, e.g. defaultof the issuer, certain rating triggers, etc. This means that, in case of the default of the issuerand the subsequent notification, the LLP obtains a legal title.

… plus guarantee from the LLP The LLP is a Limited Liability Partnership and an independent legal entity, but is con-solidated within the respective group of companies. The purpose of the LLP is to avoid the risk that in an insolvency scenario of the issuer the administrators have access to the cover pool (for the purpose of collateralizing the LLP's covered bond guarantee, the LLP inturn grants the security trustee security over the cover pool supporting the covered bonds).Unless an LLP event of default had also occurred, the bonds would remain due and payableas scheduled. In case of a LLP default, the security trustee would enforce his security over the cover pool, liquidate assets and repay covered bondholders.

UK regulated covered bonds fulfill UCITS 22(4)

As a result of the introduction of the Regulated Covered Bond Regulations, UK regu-lated covered bonds in general benefit from preferential treatment. Covered bonds are granted special status within the EU financial regulatory system, and under EC Directive 85/611 (UCITS) regulated funds are subject to higher investment limits in respect to coveredbonds than in relation to ordinary bank bonds. In addition, covered bonds are also recognizedwithin the EU bank regulatory regime, and under the Capital Requirements Directive (CRD) 2006/48/EC a covered bond issued by an EU bank attracts a reduced capital charge in com-parison with that attributable to an ordinary senior bond issued by the same bank. In the caseof UK covered bonds, CRD compliance is subject to the respective covered bond program and the applied eligibility criteria.

25 October 2011 Credit Research

Sector Report

UniCredit Research page 25 See last pages for disclaimer.

Review of the regulatory framework

On 6 April, HM Treasury and the FSA published its "Review of the UK's regulatory framework for covered bonds". The Government and the regulator ask for feedback on the proposed changes to the UK Covered Bond Law until 1 July 2011. Following the consultation,it is intended to set out later in 2011 the final changes to the legislation which will then come into force at the end of 2012.

Key changes proposed In order to further strengthen the UK Covered Bond legislation and to increase the awareness of a prudential covered bond regulation, the following changes are proposed:

■ Designation of the regulated covered bond program to a specific collateral type, i.e. residential mortgages, commercial mortgages, public sector loans (including UK privatesector housing associations and public-private partnerships), or mixed collateral. Although the range of eligible assets according to the current legal framework is broader, UK issuersare currently only using residential mortgages in their programs. This could, however, change over time due to the dynamic structure of the pools. Thus, the changes target to make the identification of the underlying collateral more transparent to investors by clearlystating what kind of assets, e.g. residential or commercial mortgages are in the pool be-sides substitute collateral.

■ Exclusion of securitization as eligible assets. While the current legislation allows for the inclusion of securitization (as defined by the CRD), none of the issuers makes use of it. Inorder to draw a clear line between covered bonds and securitization, the proposal narrows down the definition of eligible assets and thus excludes securitizations from cover pools in the future.

■ Stipulation of a fixed minimum overcollateralization level. Although the level of over-collateralization (OC) has not been determined yet, the FSA acknowledged the European standard to implement a certain minimum OC by law. Although this minimum OC level willstill be significantly below the current OC levels, the levels required by the FSA stress test-ing, as well as below the levels required by rating agencies to achieve a triple A rating, itwill align the UK covered bond law with other European covered bond laws, e.g. the Ger-man legislation.

■ Introduction of an asset pool monitor. In order to provide an extra layer of control, issu-ers must appoint an independent asset monitor for each asset pool. The asset monitormust conduct a biannual inspection to ensure the compliance of the cover pool with regula-tions.