Embed Size (px)

Citation preview

Transform Milwaukee 4-1 Entrepreneurs and Entrepreneurship

Section 4 – Entrepreneurs and Entrepreneurship Developing and supporting entrepreneurs is a foundational economic development strategy; one that is

increasingly receiving consideration from communities and regions. Of particular interest is how economic

development organizations and local governments can effectively develop strategies that stimulate growth

among existing and latent business owners. Despite this recent attention, entrepreneurship frequently

remains misunderstood by policy analysts, economic development practitioners, and elected officials. Too

often, the result is nominal efforts to support entrepreneurs. Section 4 serves as a starting point for

overcoming these challenges by considering entrepreneurs and entrepreneurship in the context of

Milwaukee’s Industrial Corridor. The objectives are to understand the rationale for entrepreneurship as an

economic development strategy; measure entrepreneurial activity in the Milwaukee area; and identify

opportunities for rethinking local entrepreneurship policies.

Entrepreneurship as an Economic Development Strategy

Entrepreneurs and entrepreneurship have long been areas of interest among economic development

practitioners, academics and policy analysts. Regions and communities increasingly consider entrepreneurs to

be local assets that can be leveraged to produce economic growth.1 In the United States, much of this interest

has been driven by the domestic employment consequences arising from globalization and the decline of

traditional, mature industries such as manufacturing (Goetz and Freshwater, 2001). Even so, communities

have struggled with what level of importance to place on entrepreneurs within the customary economic

development disciplines of asset attraction, retention and expansion.

Traditionally, many communities and regions have focused on industry attraction as their primary economic

development strategy. These efforts often include providing economic enticements in an attempt to lure firms

to a community. The roots of this focus began with Mississippi’s Balancing Agriculture with Industry (BAWI)

policies enacted in the 1930’s. BAWI is often identified with the beginning of the industrial recruiting era as the

initiative sought to attract manufacturing to Mississippi by offering firms various financial incentives. While

BAWI was initially praised as a successful strategy for growing Mississippi’s economy, eighty years later

Mississippi is at or near the bottom of national rankings for state per capita income, unemployment rates, and

poverty levels. 2

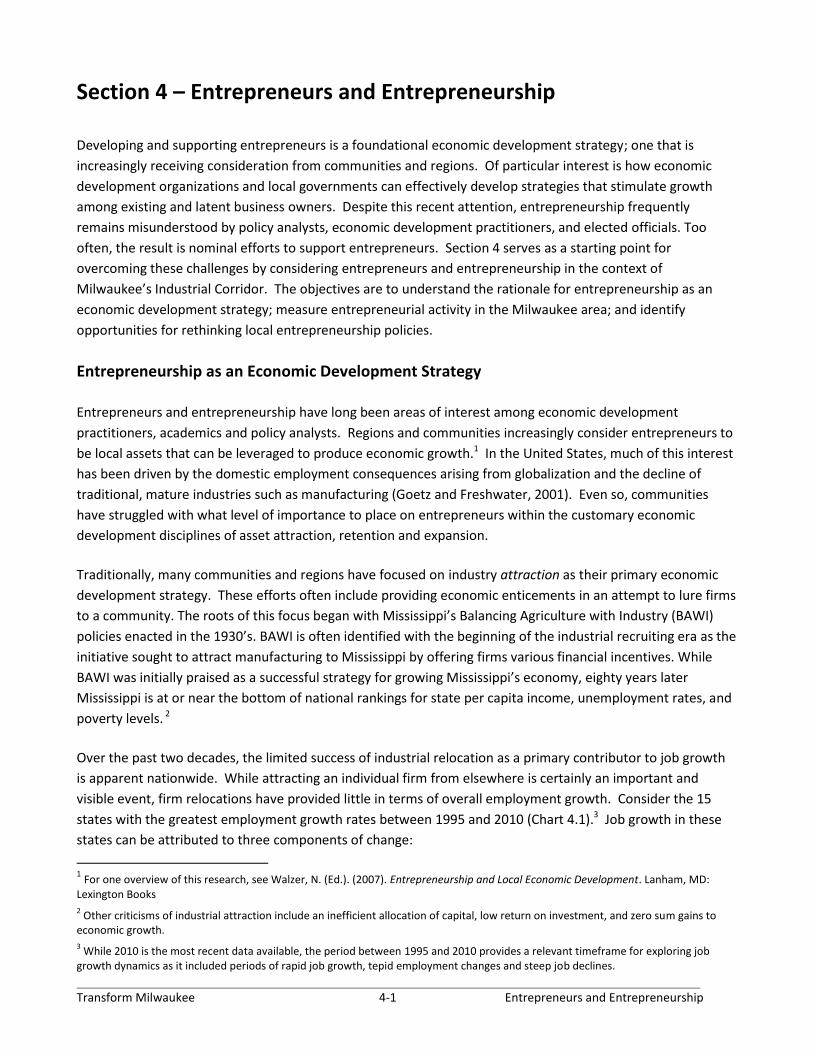

Over the past two decades, the limited success of industrial relocation as a primary contributor to job growth

is apparent nationwide. While attracting an individual firm from elsewhere is certainly an important and

visible event, firm relocations have provided little in terms of overall employment growth. Consider the 15

states with the greatest employment growth rates between 1995 and 2010 (Chart 4.1).3 Job growth in these

states can be attributed to three components of change:

1 For one overview of this research, see Walzer, N. (Ed.). (2007). Entrepreneurship and Local Economic Development. Lanham, MD:

Lexington Books

2 Other criticisms of industrial attraction include an inefficient allocation of capital, low return on investment, and zero sum gains to

economic growth.

3 While 2010 is the most recent data available, the period between 1995 and 2010 provides a relevant timeframe for exploring job

growth dynamics as it included periods of rapid job growth, tepid employment changes and steep job declines.

Transform Milwaukee 4-2 Entrepreneurs and Entrepreneurship

1. Net establishment openings - Jobs in establishment openings minus jobs in establishment closings;

2. Net establishment expansions - Jobs in establishment expansions minus jobs in establishment contractions;

3. Net establishment relocations - Jobs in establishments moving into a region minus jobs in establishments

moving out of a region;

Chart 4.1 shows that job contributions from establishment expansions provide by far the greatest shares of

new jobs in most of the top 15 states.4 Furthermore, jobs from net openings tend to provide the second

largest source of job growth in most states. While net openings do involve some level of industry attraction, a

large share is from endogenous new startups. Net relocations, the remaining component of job growth,

provide only minor influences on new employment in some states, with no contributions in others. While

these figures provide just one perspective, additional research shows similar connections between economic

growth and business start-ups and expansions at a variety of geographic scales, both urban and rural.5

Chart 4.1 – Components of Job Growth among the 15 States with Greatest Employment Growth Rates (1995 to 2010)

Sources: YourEconomy.org and UW-Extension Center for Community and Economic Development

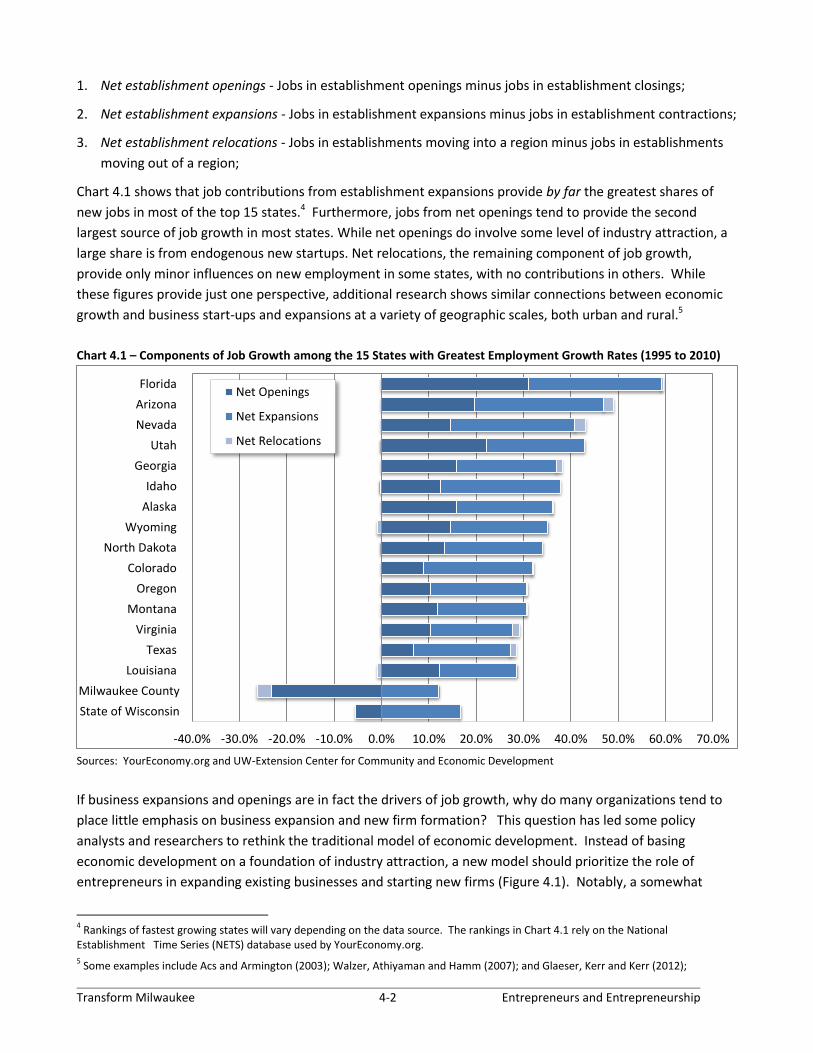

If business expansions and openings are in fact the drivers of job growth, why do many organizations tend to

place little emphasis on business expansion and new firm formation? This question has led some policy

analysts and researchers to rethink the traditional model of economic development. Instead of basing

economic development on a foundation of industry attraction, a new model should prioritize the role of

entrepreneurs in expanding existing businesses and starting new firms (Figure 4.1). Notably, a somewhat

4 Rankings of fastest growing states will vary depending on the data source. The rankings in Chart 4.1 rely on the National

Establishment Time Series (NETS) database used by YourEconomy.org.

5 Some examples include Acs and Armington (2003); Walzer, Athiyaman and Hamm (2007); and Glaeser, Kerr and Kerr (2012);

-40.0% -30.0% -20.0% -10.0% 0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Florida

Arizona

Nevada

Utah

Georgia

Idaho

Alaska

Wyoming

North Dakota

Colorado

Oregon

Montana

Virginia

Texas

Louisiana

Milwaukee County

State of Wisconsin

Net Openings

Net Expansions

Net Relocations

Transform Milwaukee 4-3 Entrepreneurs and Entrepreneurship

Traditional Model

Industrial Recruitment

Small Business Startups

Expansion

New Model

Attraction

Entrepreneurship

Retention

Figure 4.1 – Traditional and New Models of Economic Development

Source: Dabson (2003)

similar conclusion was drawn by a 2011 Public Policy Forum report looking at Milwaukee’s economic

development landscape:6

“In contrast to business attraction and financing, the resources dedicated to business

development and assistance are limited. Only three of the eight participants focus on business

development services targeted at start-ups and small/micro businesses, and those

organizations operate with relatively low budgets overall. BizStarts Milwaukee, for example,

had an operating budget of $389,805 in 2011—one of the lowest budgets of any organization

included on the map. WWBIC, an organization dedicated to providing both technical and

financial assistance to small and micro businesses, had a 2011 operating budget of slightly

more than $3.6 million, with one-third of the organization’s activities occurring outside of

southeast Wisconsin. In interviews conducted for this report, some participants suggested that

the resource discrepancy between business attraction and real estate financing on the one

hand, and support for start-ups and small business expansion on the other, should be

revisited.” (pg. 46).

Implementing a new model for local economic development can be challenging. Understandably, political

pressure, reduced visibility, and loss of funding are concerns facing organizations considering a new approach.

The challenges facing an increased emphasis on entrepreneurship in Milwaukee’s Industrial Corridor are likely

no different. Some of these apprehensions can be eased by noting that industry attraction is not abandoned in

the new model of economic development.7 In fact, the job growth trends and economic conditions noted in

the introduction to this report suggest attraction, retention and expansion all have necessary roles. However,

the largest challenge in adopting this new model may lie in understanding entrepreneurs and

entrepreneurship.

6 See: Helpap, D., Henken, R. and Peterangelo, J. (2011) Assembling the Parts: An examination of Milwaukee’s economic development

landscape. Public Policy Forum. Milwaukee, WI. 7 However, attraction in the new model is modified somewhat as it applies not only to the attraction of industries, but also the

attraction of new human, financial and social capital.

Transform Milwaukee 4-4 Entrepreneurs and Entrepreneurship

Defining Entrepreneurs

As entrepreneurship has become a somewhat recent emphasis of economic development efforts, policies and

strategies that effectively encourage the development of entrepreneurs are well not understood, particularly

at the local level. Some of this confusion arises from loosely-defined characterizations of an “entrepreneur.”

This is understandable. After all, researchers and academics in economics, sociology, psychology and political

science do not have consensus as to what constitutes an entrepreneur. While the debate over definitions

need not be repeated as part of this analysis, developing entrepreneurship strategies in Milwaukee’s Industrial

Corridor does require aligning policies with some formal perspectives on entrepreneurs and entrepreneurial

ventures.8

Ahmed and Hoffman (2008) define entrepreneurs as “people who design, produce and generate value through

the creation or expansion of economic activity.” This definition, or a similar one, is significant for two reasons.

First, the focus of the definition is on people and not economic institutions. Consequently, a primary strategy

for fostering entrepreneurs should be developing people, not merely enhancing infrastructure and business

climate. Second, Ahmed and Hoffman’s definition encompasses all economic activity and is not restricted to

the creation or expansion of businesses. As noted by Drucker (1985), entrepreneurial ventures are not limited

to businesses, but can include non-profits, universities and government institutions. While the creation and

expansion of new businesses will be the focus of this analysis, the development of entrepreneurial institutions

also will be considered.

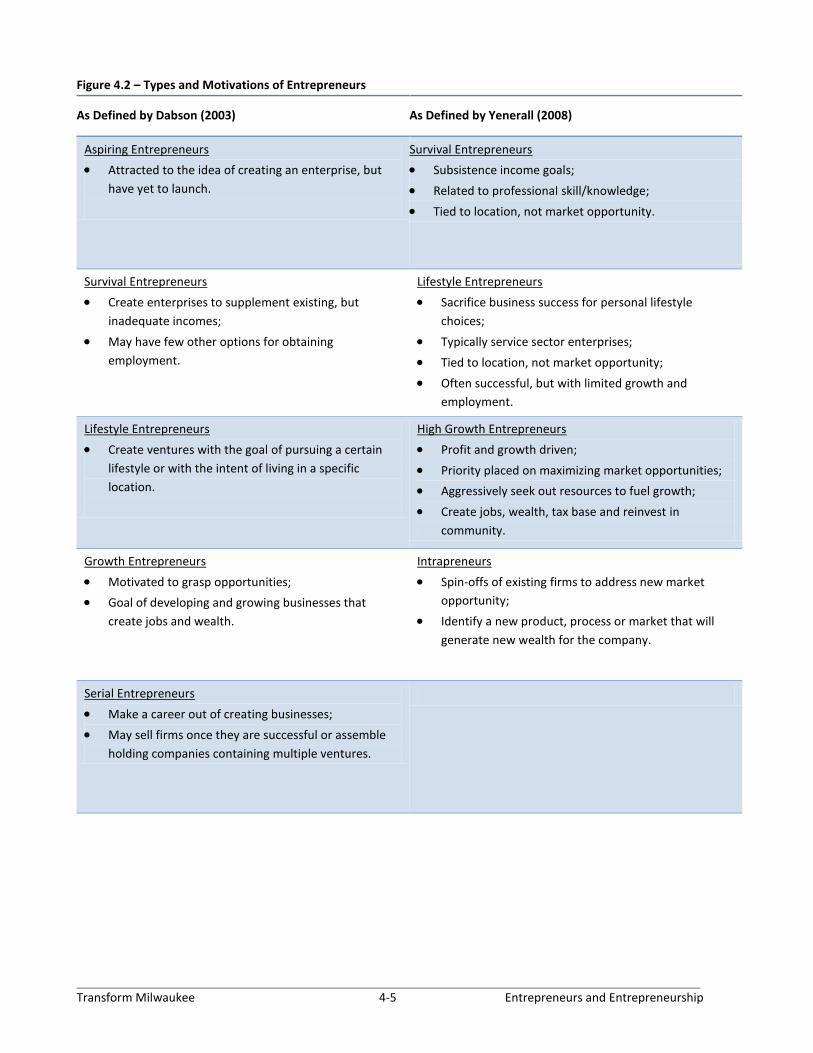

Understanding entrepreneurs also requires knowing an individual’s motives and goals (Figure 4.2). Some

people become entrepreneurs out of necessity. They form a venture to create economic opportunities where

few may exist. Others are driven by growth and look to create firms that generate jobs and wealth. These

varying entrepreneurial types will have different impacts on a community. Furthermore, diversity among

entrepreneurs suggests that entrepreneurship should not be conflated with small business development.

While entrepreneurial endeavors are often small in scale, they can include large and multiple ventures.

When considering the different types of entrepreneurs in Figure 4.2, it may be tempting from a policy

perspective to dismiss survival and lifestyle entrepreneurs and focus on growth or serial entrepreneurs.

Relatively few survival and lifestyle entrepreneurs will evolve into larger drivers of the local economy, whereas

growth and serial entrepreneurs may generate a larger return on public support or investment. However, all

types of entrepreneurs add to the local economy and contribute to the overall entrepreneurial culture in a

community (Dabson, 2007). Moreover, policies designed to support and develop these individuals need to

vary. For instance, a survival entrepreneur has different capital and technical assistance needs than does a

growth or serial entrepreneur.

8 For more on defining entrepreneurs, see Dabson, B. (2007) Entrepreneurship as a Rural Economic Development Policy: A Changing

Paradigm. In Walzer, N (Ed), Entrepreneurship and Local Economic Development (pp. 81-102). Lanham, MD: Lexington Books

Transform Milwaukee 4-5 Entrepreneurs and Entrepreneurship

Figure 4.2 – Types and Motivations of Entrepreneurs

As Defined by Dabson (2003) As Defined by Yenerall (2008)

Aspiring Entrepreneurs

Attracted to the idea of creating an enterprise, but

have yet to launch.

Survival Entrepreneurs

Subsistence income goals;

Related to professional skill/knowledge;

Tied to location, not market opportunity.

Survival Entrepreneurs

Create enterprises to supplement existing, but

inadequate incomes;

May have few other options for obtaining

employment.

Lifestyle Entrepreneurs

Sacrifice business success for personal lifestyle

choices;

Typically service sector enterprises;

Tied to location, not market opportunity;

Often successful, but with limited growth and

employment.

Lifestyle Entrepreneurs

Create ventures with the goal of pursuing a certain

lifestyle or with the intent of living in a specific

location.

High Growth Entrepreneurs

Profit and growth driven;

Priority placed on maximizing market opportunities;

Aggressively seek out resources to fuel growth;

Create jobs, wealth, tax base and reinvest in

community.

Growth Entrepreneurs

Motivated to grasp opportunities;

Goal of developing and growing businesses that

create jobs and wealth.

Intrapreneurs

Spin-offs of existing firms to address new market

opportunity;

Identify a new product, process or market that will

generate new wealth for the company.

Serial Entrepreneurs

Make a career out of creating businesses;

May sell firms once they are successful or assemble

holding companies containing multiple ventures.

Transform Milwaukee 4-6 Entrepreneurs and Entrepreneurship

Measuring Entrepreneurial Activity in the Milwaukee Region

Measuring entrepreneurial activity provides insights into the current intensity of the so-called entrepreneurial

“seed bed” in Milwaukee. That is, knowing levels of entrepreneurship potentially can guide efforts to identify

and develop supportive strategies. Just as defining “entrepreneurs” is challenging, it is also difficult to

measure entrepreneurial activity. Researchers and policy analysts have used a variety of metrics including:

new business formations; employment growth in startups; self-employment; proprietor or self-employment

income; initial public offerings; and investment activity (such as angel capital and venture capital). As no one

measure is comprehensive, a variety of metrics are used in this analysis:

Non-farm proprietors as a share of employment;

Household self-employment income;

Business births and deaths;

Employment and establishments by business

stage;

Minority-business enterprises.

Note that most of these measures are only available at either the county or regional level. Still, statistics for

Milwaukee County, the Milwaukee-Waukesha-West Allis MSA or the M7 Region are useful as they provide

perspectives on broader entrepreneurial culture in the region. Potential entrepreneurs throughout the region

also may provide opportunities for developing enterprises in Milwaukee’s Industrial Corridor.

Non-Farm Proprietors

Non-farm proprietor figures from the Bureau of Economic Analysis measure levels of non-farm self-

employment. These include sole-proprietors (e.g. non-employers) and individual business partners not

assumed to be limited partners. Self-employment estimates differ somewhat from other employment figures

as they are mostly reported by place-of-residence, rather than place-of-work. Furthermore, self-employment

estimates reflect the total number of sole proprietorships or partnerships active at any time during the year,

rather than the annual averages used for other measures of employment in this study.

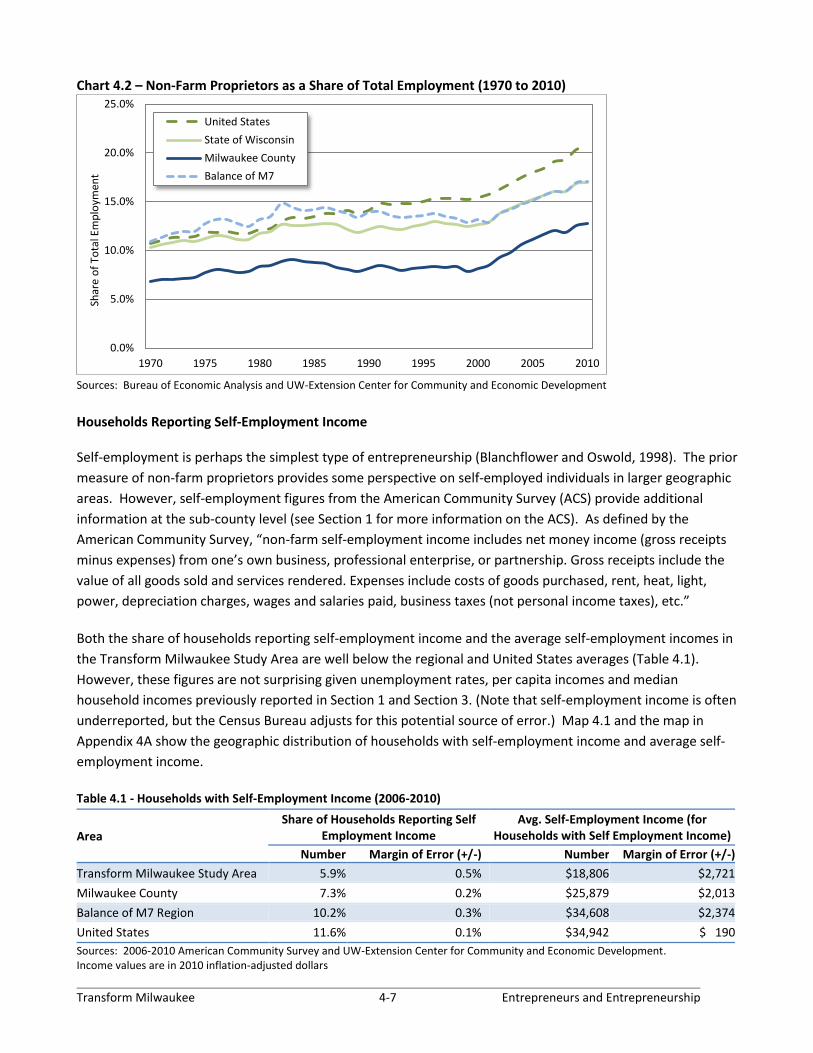

Non-farm proprietors are measured here as a percent of total employment in an area (Chart 4.2). Also called

entrepreneurship breadth, self-employment as a share of total employment provides perspective on the broad

propensity for entrepreneurial activity in an area.9 Despite similar growth trends, Milwaukee County, the

Balance of the M7 Region and the State of Wisconsin all have trailed the nation’s rate of entrepreneurship

breadth since the late 1980’s. Speculations for these lower levels throughout Wisconsin have been made, but

no definitive conclusion is available. In fact, the values are likely a combination of reasons. One specific factor

deserving further research is the state’s historical reliance on manufacturing, as the past availability of well-

paying jobs (many of them with benefits) may have reduced an individual’s incentive to be entrepreneurial.10

The increasing shares of self-employed individuals between 2000 and 2010 should be noted for all areas

depicted on Chart 4.2. While self-employment increased over this time, wage and salary employment growth

declined in Milwaukee County and was relatively flat in the U.S., Wisconsin and the Balance of the M7 Region.

Consequently, the increasing shares in the last decade largely are explained by other forms of employment not

keeping pace with the growth in self-employment.

9 For more on entrepreneurial breadth, see Henderson, J., Low, S.A., and Weiler, S. (2007) The Drivers of Regional Entrepreneurship in Rural and Metro Areas. In Walzer, N (Ed), Entrepreneurship and Local Economic Development (pp. 81-102). Lanham, MD: Lexington Books 10 A related hypothesis was first suggested by Chinitz (1961) and was recently expanded upon by Glaeser, Kerr and Kerr (2012).

Transform Milwaukee 4-7 Entrepreneurs and Entrepreneurship

Chart 4.2 – Non-Farm Proprietors as a Share of Total Employment (1970 to 2010)

Sources: Bureau of Economic Analysis and UW-Extension Center for Community and Economic Development

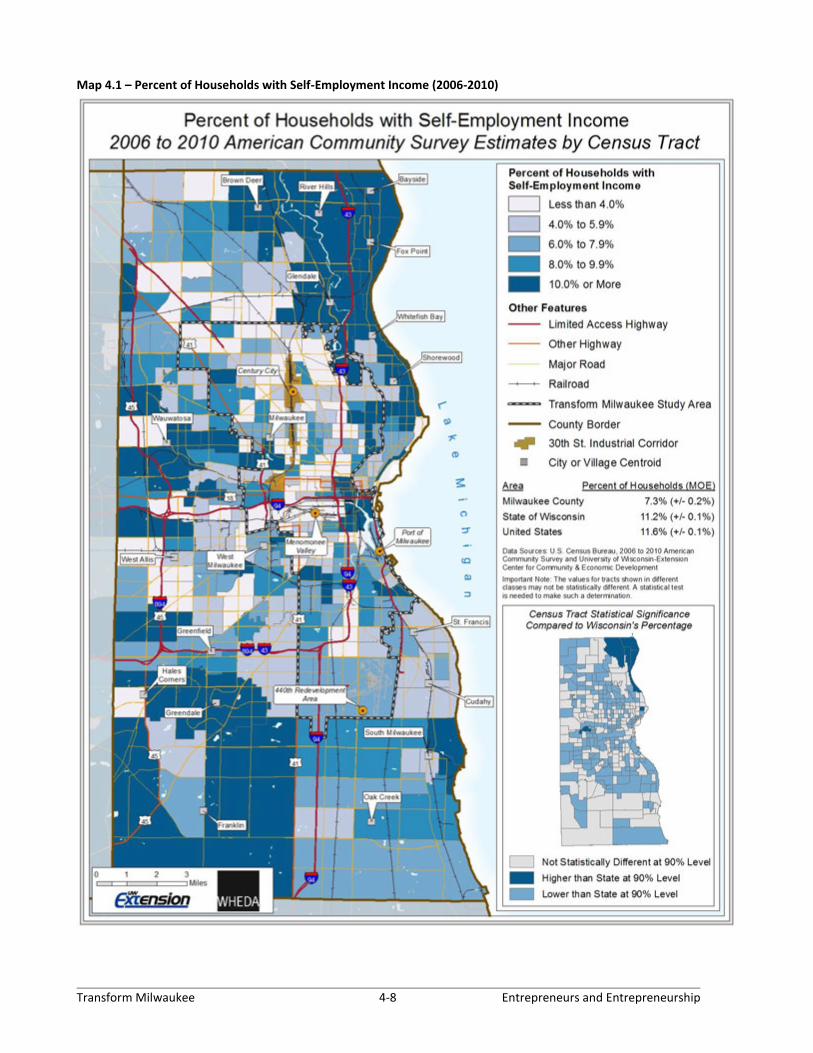

Households Reporting Self-Employment Income

Self-employment is perhaps the simplest type of entrepreneurship (Blanchflower and Oswold, 1998). The prior

measure of non-farm proprietors provides some perspective on self-employed individuals in larger geographic

areas. However, self-employment figures from the American Community Survey (ACS) provide additional

information at the sub-county level (see Section 1 for more information on the ACS). As defined by the

American Community Survey, “non-farm self-employment income includes net money income (gross receipts

minus expenses) from one’s own business, professional enterprise, or partnership. Gross receipts include the

value of all goods sold and services rendered. Expenses include costs of goods purchased, rent, heat, light,

power, depreciation charges, wages and salaries paid, business taxes (not personal income taxes), etc.”

Both the share of households reporting self-employment income and the average self-employment incomes in

the Transform Milwaukee Study Area are well below the regional and United States averages (Table 4.1).

However, these figures are not surprising given unemployment rates, per capita incomes and median

household incomes previously reported in Section 1 and Section 3. (Note that self-employment income is often

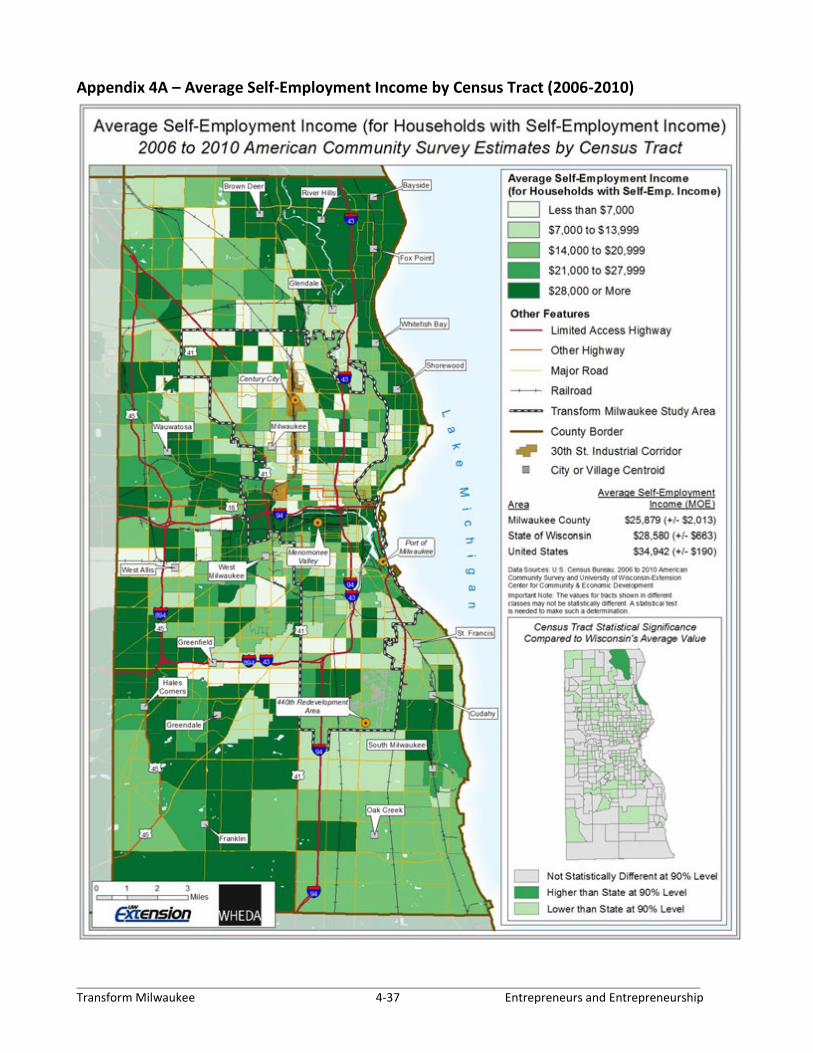

underreported, but the Census Bureau adjusts for this potential source of error.) Map 4.1 and the map in

Appendix 4A show the geographic distribution of households with self-employment income and average self-

employment income.

Table 4.1 - Households with Self-Employment Income (2006-2010)

Area

Share of Households Reporting Self Employment Income

Avg. Self-Employment Income (for Households with Self Employment Income)

Number Margin of Error (+/-) Number Margin of Error (+/-)

Transform Milwaukee Study Area 5.9% 0.5% $18,806 $2,721

Milwaukee County 7.3% 0.2% $25,879 $2,013

Balance of M7 Region 10.2% 0.3% $34,608 $2,374

United States 11.6% 0.1% $34,942 $ 190

Sources: 2006-2010 American Community Survey and UW-Extension Center for Community and Economic Development. Income values are in 2010 inflation-adjusted dollars

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1970 1975 1980 1985 1990 1995 2000 2005 2010

Shar

e o

f To

tal E

mp

loym

ent

United States

State of Wisconsin

Milwaukee County

Balance of M7

Transform Milwaukee 4-8 Entrepreneurs and Entrepreneurship

Map 4.1 – Percent of Households with Self-Employment Income (2006-2010)

Transform Milwaukee 4-9 Entrepreneurs and Entrepreneurship

Establishment Births and Deaths

A popular view is that small businesses create most of the jobs in the United States. However, the exact role of

small businesses in job creation has been subject to much debate concerning: 1) the definition of a small

business; 2) the migration of firms between large and small employment categories; and 3) the time-frame

used to measure job growth (Davis, Haltiwanger and Schuh, 1996). Recently, research rooted in longitudinal

databases suggests that young businesses, not necessarily small businesses, are a better predictor of job

growth (Haltiwanger, Jarmin and Miranda, 2010; Haltiwanger, Hyatt, McEntarfer and Sousa, 2012). While not

all young firms are the same, these studies suggest that business births are an active component of job

creation. The employment contributions of business births in the form of net openings also were apparent

when considering the job creation dynamics previously reported in Chart 4.1.

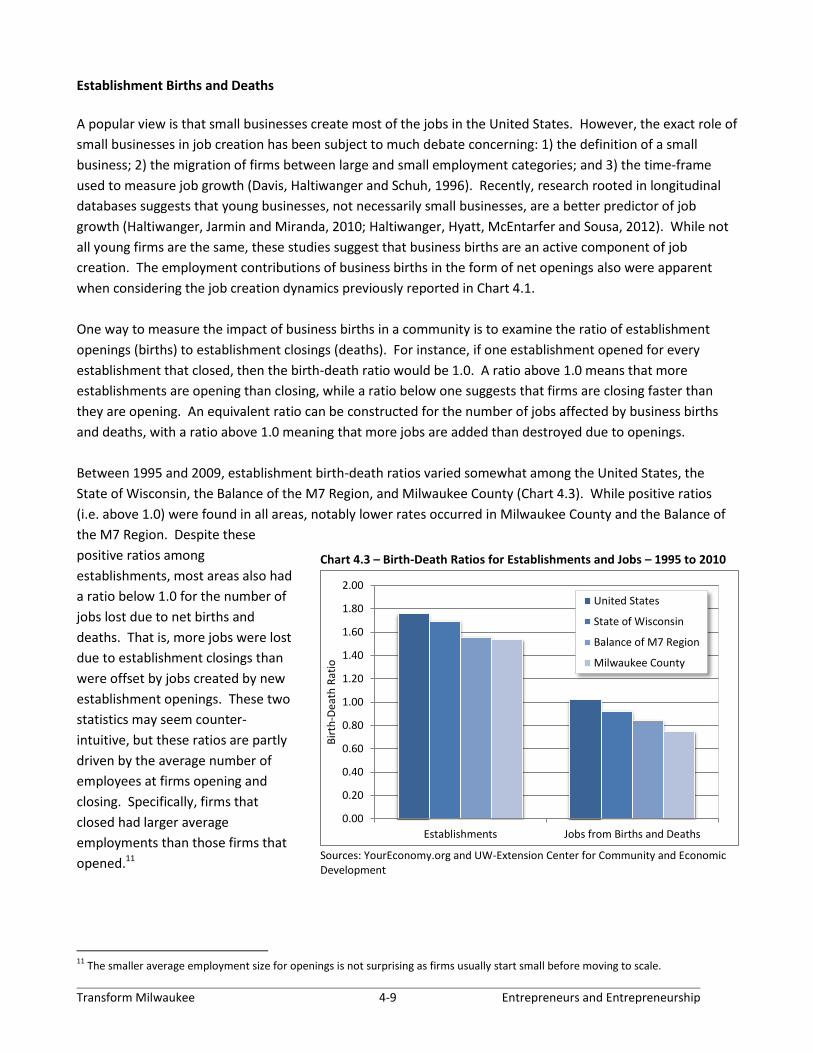

One way to measure the impact of business births in a community is to examine the ratio of establishment

openings (births) to establishment closings (deaths). For instance, if one establishment opened for every

establishment that closed, then the birth-death ratio would be 1.0. A ratio above 1.0 means that more

establishments are opening than closing, while a ratio below one suggests that firms are closing faster than

they are opening. An equivalent ratio can be constructed for the number of jobs affected by business births

and deaths, with a ratio above 1.0 meaning that more jobs are added than destroyed due to openings.

Between 1995 and 2009, establishment birth-death ratios varied somewhat among the United States, the

State of Wisconsin, the Balance of the M7 Region, and Milwaukee County (Chart 4.3). While positive ratios

(i.e. above 1.0) were found in all areas, notably lower rates occurred in Milwaukee County and the Balance of

the M7 Region. Despite these

positive ratios among

establishments, most areas also had

a ratio below 1.0 for the number of

jobs lost due to net births and

deaths. That is, more jobs were lost

due to establishment closings than

were offset by jobs created by new

establishment openings. These two

statistics may seem counter-

intuitive, but these ratios are partly

driven by the average number of

employees at firms opening and

closing. Specifically, firms that

closed had larger average

employments than those firms that

opened.11

11

The smaller average employment size for openings is not surprising as firms usually start small before moving to scale.

Chart 4.3 – Birth-Death Ratios for Establishments and Jobs – 1995 to 2010

Sources: YourEconomy.org and UW-Extension Center for Community and Economic Development

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

Establishments Jobs from Births and Deaths

Bir

th-D

eath

Rat

io

United States

State of Wisconsin

Balance of M7 Region

Milwaukee County

Transform Milwaukee 4-10 Entrepreneurs and Entrepreneurship

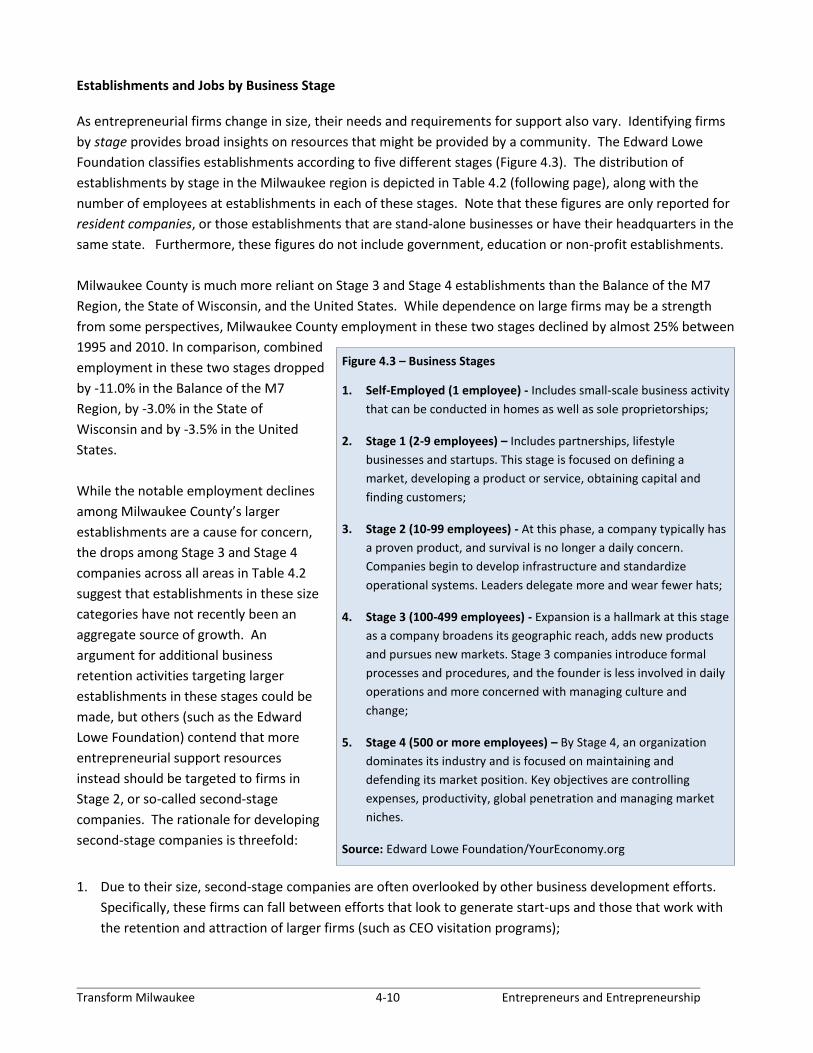

Figure 4.3 – Business Stages

1. Self-Employed (1 employee) - Includes small-scale business activity

that can be conducted in homes as well as sole proprietorships;

2. Stage 1 (2-9 employees) – Includes partnerships, lifestyle

businesses and startups. This stage is focused on defining a

market, developing a product or service, obtaining capital and

finding customers;

3. Stage 2 (10-99 employees) - At this phase, a company typically has

a proven product, and survival is no longer a daily concern.

Companies begin to develop infrastructure and standardize

operational systems. Leaders delegate more and wear fewer hats;

4. Stage 3 (100-499 employees) - Expansion is a hallmark at this stage

as a company broadens its geographic reach, adds new products

and pursues new markets. Stage 3 companies introduce formal

processes and procedures, and the founder is less involved in daily

operations and more concerned with managing culture and

change;

5. Stage 4 (500 or more employees) – By Stage 4, an organization

dominates its industry and is focused on maintaining and

defending its market position. Key objectives are controlling

expenses, productivity, global penetration and managing market

niches.

Source: Edward Lowe Foundation/YourEconomy.org

Establishments and Jobs by Business Stage As entrepreneurial firms change in size, their needs and requirements for support also vary. Identifying firms

by stage provides broad insights on resources that might be provided by a community. The Edward Lowe

Foundation classifies establishments according to five different stages (Figure 4.3). The distribution of

establishments by stage in the Milwaukee region is depicted in Table 4.2 (following page), along with the

number of employees at establishments in each of these stages. Note that these figures are only reported for

resident companies, or those establishments that are stand-alone businesses or have their headquarters in the

same state. Furthermore, these figures do not include government, education or non-profit establishments.

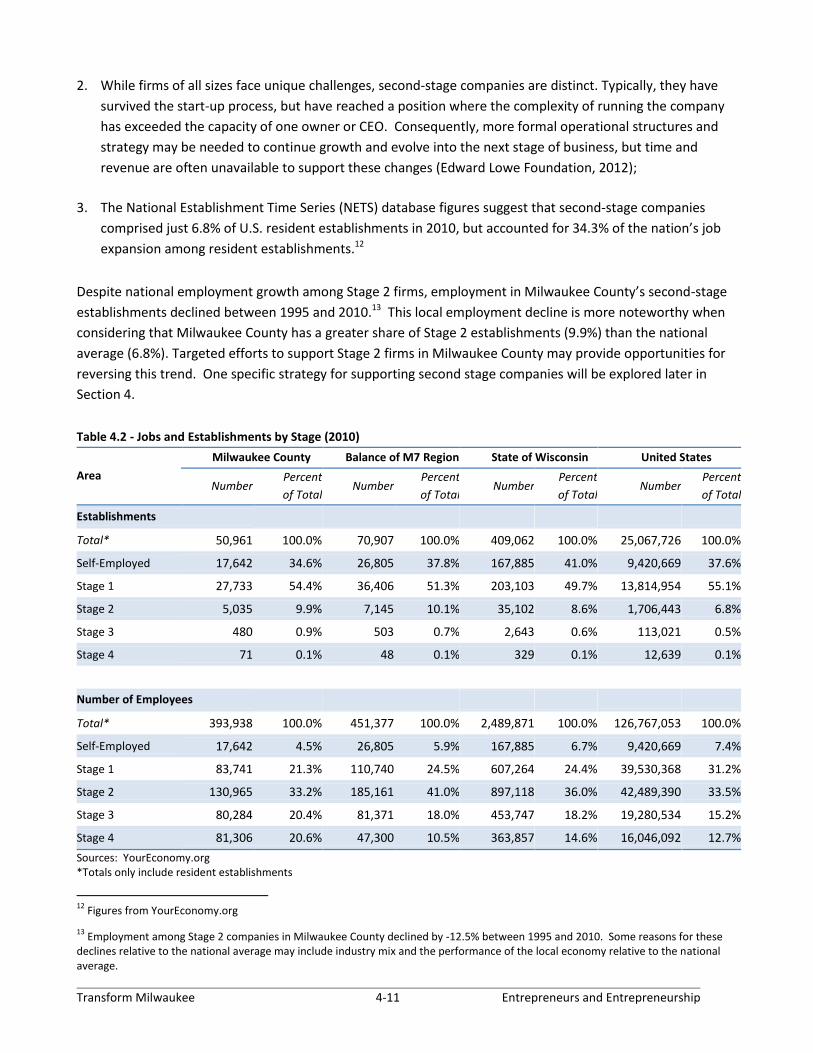

Milwaukee County is much more reliant on Stage 3 and Stage 4 establishments than the Balance of the M7

Region, the State of Wisconsin, and the United States. While dependence on large firms may be a strength

from some perspectives, Milwaukee County employment in these two stages declined by almost 25% between

1995 and 2010. In comparison, combined

employment in these two stages dropped

by -11.0% in the Balance of the M7

Region, by -3.0% in the State of

Wisconsin and by -3.5% in the United

States.

While the notable employment declines

among Milwaukee County’s larger

establishments are a cause for concern,

the drops among Stage 3 and Stage 4

companies across all areas in Table 4.2

suggest that establishments in these size

categories have not recently been an

aggregate source of growth. An

argument for additional business

retention activities targeting larger

establishments in these stages could be

made, but others (such as the Edward

Lowe Foundation) contend that more

entrepreneurial support resources

instead should be targeted to firms in

Stage 2, or so-called second-stage

companies. The rationale for developing

second-stage companies is threefold:

1. Due to their size, second-stage companies are often overlooked by other business development efforts.

Specifically, these firms can fall between efforts that look to generate start-ups and those that work with

the retention and attraction of larger firms (such as CEO visitation programs);

Transform Milwaukee 4-11 Entrepreneurs and Entrepreneurship

2. While firms of all sizes face unique challenges, second-stage companies are distinct. Typically, they have

survived the start-up process, but have reached a position where the complexity of running the company

has exceeded the capacity of one owner or CEO. Consequently, more formal operational structures and

strategy may be needed to continue growth and evolve into the next stage of business, but time and

revenue are often unavailable to support these changes (Edward Lowe Foundation, 2012);

3. The National Establishment Time Series (NETS) database figures suggest that second-stage companies

comprised just 6.8% of U.S. resident establishments in 2010, but accounted for 34.3% of the nation’s job

expansion among resident establishments.12

Despite national employment growth among Stage 2 firms, employment in Milwaukee County’s second-stage

establishments declined between 1995 and 2010.13 This local employment decline is more noteworthy when

considering that Milwaukee County has a greater share of Stage 2 establishments (9.9%) than the national

average (6.8%). Targeted efforts to support Stage 2 firms in Milwaukee County may provide opportunities for

reversing this trend. One specific strategy for supporting second stage companies will be explored later in

Section 4.

Table 4.2 - Jobs and Establishments by Stage (2010)

Area

Milwaukee County Balance of M7 Region State of Wisconsin United States

Number Percent

of Total Number

Percent

of Total Number

Percent

of Total Number

Percent

of Total

Establishments

Total* 50,961 100.0% 70,907 100.0% 409,062 100.0% 25,067,726 100.0%

Self-Employed 17,642 34.6% 26,805 37.8% 167,885 41.0% 9,420,669 37.6%

Stage 1 27,733 54.4% 36,406 51.3% 203,103 49.7% 13,814,954 55.1%

Stage 2 5,035 9.9% 7,145 10.1% 35,102 8.6% 1,706,443 6.8%

Stage 3 480 0.9% 503 0.7% 2,643 0.6% 113,021 0.5%

Stage 4 71 0.1% 48 0.1% 329 0.1% 12,639 0.1%

Number of Employees

Total* 393,938 100.0% 451,377 100.0% 2,489,871 100.0% 126,767,053 100.0%

Self-Employed 17,642 4.5% 26,805 5.9% 167,885 6.7% 9,420,669 7.4%

Stage 1 83,741 21.3% 110,740 24.5% 607,264 24.4% 39,530,368 31.2%

Stage 2 130,965 33.2% 185,161 41.0% 897,118 36.0% 42,489,390 33.5%

Stage 3 80,284 20.4% 81,371 18.0% 453,747 18.2% 19,280,534 15.2%

Stage 4 81,306 20.6% 47,300 10.5% 363,857 14.6% 16,046,092 12.7%

Sources: YourEconomy.org *Totals only include resident establishments

12

Figures from YourEconomy.org 13

Employment among Stage 2 companies in Milwaukee County declined by -12.5% between 1995 and 2010. Some reasons for these declines relative to the national average may include industry mix and the performance of the local economy relative to the national average.

Transform Milwaukee 4-12 Entrepreneurs and Entrepreneurship

Minority-Business Enterprises

Creating and developing successful entrepreneurs has long been encouraged as a strategy for promoting

economic advancement among minority groups. In particular, the creation of Minority Business Enterprises

(MBEs) has been suggested as an alternative route to employment, a means to escape poverty, and a strategy

for combating high unemployment rates among minorities (such as those rates found in the Transform

Milwaukee Study Area). Certainly, starting a business creates an employment opportunity for the proprietor,

but research also suggests that larger MBEs also produce additional employment opportunities in minority

communities. Specifically, MBEs are more likely to locate in urban minority communities and employ minority

workers from low income areas than non-minority owned businesses (Bates 2006).14

MBEs face a number of challenges that often result in smaller, less profitable and less viable firms (Bates, 1997;

Smith, 2005). A large body of research has been devoted to understanding these challenges, including

variations in success and formation rates across the United States. Commonly identified factors include: lower

levels of educational attainment; poor access to financial capital and management expertise; smaller

probabilities of having self-employed parents; experience levels; household characteristics; discrimination and

segregation; demographic trends; and the influence of historical events such as the Great Migration (Bates,

Lofstrom and Servon, 2011; Bogan and Darity, 2007; Boston and Boston, 2007; Smith, 2005). However, the

influence of these factors on MBE formation and success rates can vary among minority groups and business

types. For instance, Bates et al (2011) find that financial constraints may have little effect on entrepreneurial

entry to industries with low human capital requirements.

Minority business enterprises have been measured previously in Milwaukee, but deserve additional research.15

To analyze the ownership rates and types of minority businesses enterprises in Milwaukee, figures are

summarized from the 2007 Survey of Business Owners (SBO). Conducted every five years by the Census

Bureau, the SBO reports business ownership by gender, ethnicity, race, and veteran status. Survey coverage

encompasses non-farm businesses with receipts of $1,000 or more that filed Internal Revenue Service tax

forms as individual proprietorships, partnerships, or any type of corporation. Note that the 2012 SBO is

currently underway, but the results are not scheduled to be released until 2015.

The Survey of Business Owners is conducted on a company or firm basis, rather than an establishment basis,

and includes firms with paid employees and firms without paid employees. Business ownership is defined as

having 51 percent or more of the stock or equity in the business.16 Businesses may also be classified in more

than one racial group if the sole owner reported to be of more than one race; the majority owner was

reported to be of more than one race; or a majority combination of owners was reported to be of more than

one race. While data are available for Milwaukee County, the analysis relies on figures reported for the

Milwaukee-Waukesha-West Allis MSA as much of the information at the county level is suppressed due to

confidentiality considerations. Even so, a large percentage of the MBEs in the metropolitan area are located in

Milwaukee County.

14 Construction firms are the most likely to actively hire workers in low-income minority communities. 15 See: Minority Business Ownership in Metropolitan Milwaukee in the 1990s: Some Statistical Indicators and Comparisons to the Nation's Largest Metropolitan Areas. May 14, 2001. Marc V. Levine and Lisa Heuler Williams. 16 Minority-owned firms are those where Blacks or African Americans, American Indians and Alaska Natives, Asians, Native Hawaiians and Other Pacific Islanders, and/or Hispanics own 51 percent or more of the equity, interest, or stock of the business.

Transform Milwaukee 4-13 Entrepreneurs and Entrepreneurship

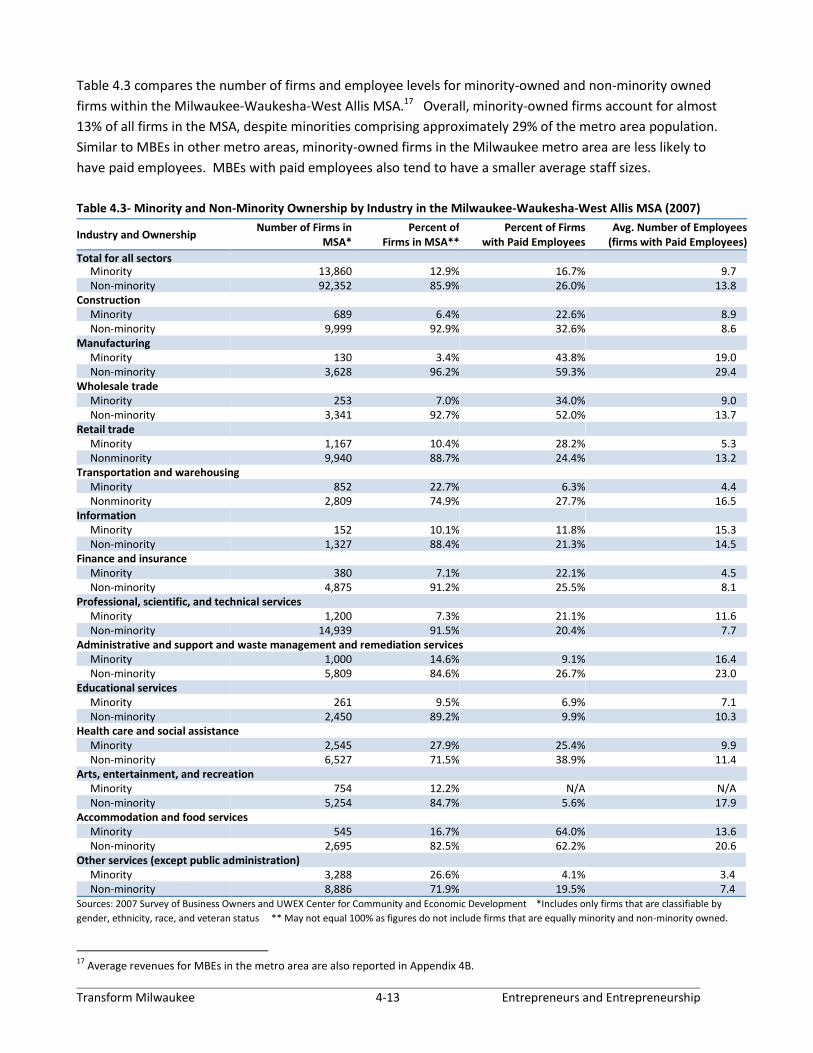

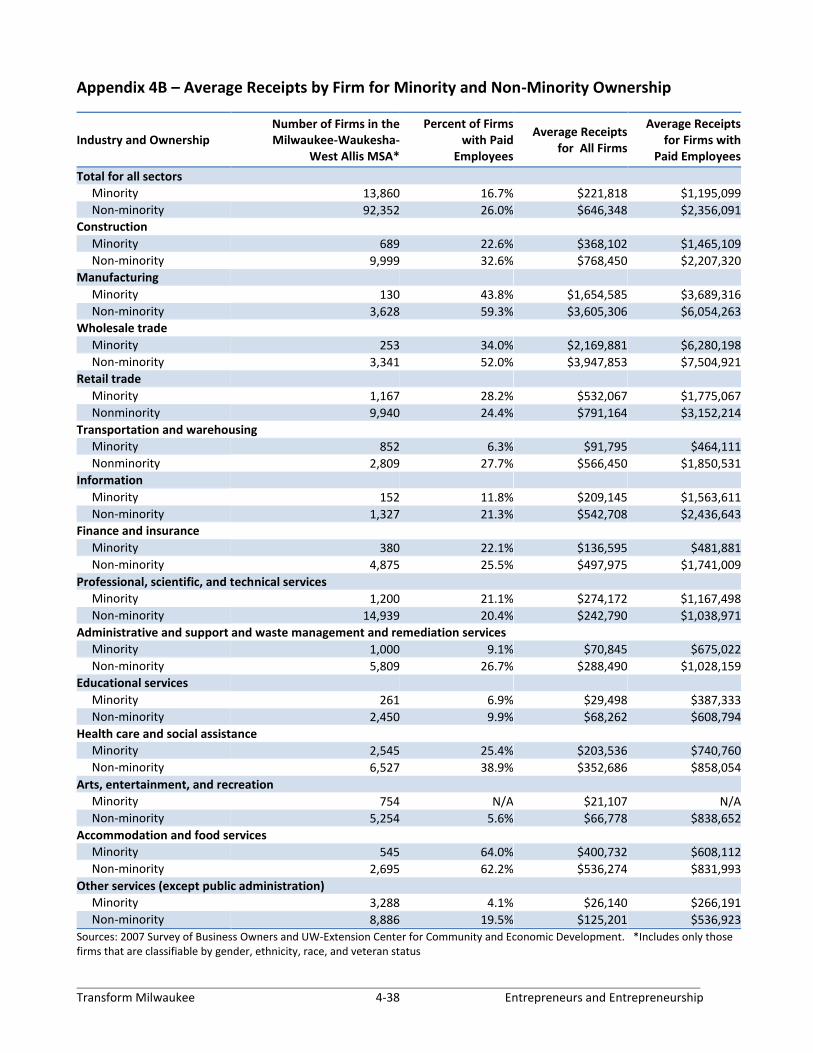

Table 4.3 compares the number of firms and employee levels for minority-owned and non-minority owned

firms within the Milwaukee-Waukesha-West Allis MSA.17 Overall, minority-owned firms account for almost

13% of all firms in the MSA, despite minorities comprising approximately 29% of the metro area population.

Similar to MBEs in other metro areas, minority-owned firms in the Milwaukee metro area are less likely to

have paid employees. MBEs with paid employees also tend to have a smaller average staff sizes.

Table 4.3- Minority and Non-Minority Ownership by Industry in the Milwaukee-Waukesha-West Allis MSA (2007)

Industry and Ownership Number of Firms in

MSA* Percent of

Firms in MSA** Percent of Firms

with Paid Employees Avg. Number of Employees

(firms with Paid Employees)

Total for all sectors Minority 13,860 12.9% 16.7% 9.7 Non-minority 92,352 85.9% 26.0% 13.8 Construction Minority 689 6.4% 22.6% 8.9 Non-minority 9,999 92.9% 32.6% 8.6 Manufacturing Minority 130 3.4% 43.8% 19.0 Non-minority 3,628 96.2% 59.3% 29.4 Wholesale trade Minority 253 7.0% 34.0% 9.0 Non-minority 3,341 92.7% 52.0% 13.7 Retail trade Minority 1,167 10.4% 28.2% 5.3 Nonminority 9,940 88.7% 24.4% 13.2 Transportation and warehousing Minority 852 22.7% 6.3% 4.4 Nonminority 2,809 74.9% 27.7% 16.5 Information Minority 152 10.1% 11.8% 15.3 Non-minority 1,327 88.4% 21.3% 14.5 Finance and insurance Minority 380 7.1% 22.1% 4.5 Non-minority 4,875 91.2% 25.5% 8.1 Professional, scientific, and technical services Minority 1,200 7.3% 21.1% 11.6 Non-minority 14,939 91.5% 20.4% 7.7 Administrative and support and waste management and remediation services Minority 1,000 14.6% 9.1% 16.4 Non-minority 5,809 84.6% 26.7% 23.0 Educational services Minority 261 9.5% 6.9% 7.1 Non-minority 2,450 89.2% 9.9% 10.3 Health care and social assistance Minority 2,545 27.9% 25.4% 9.9 Non-minority 6,527 71.5% 38.9% 11.4 Arts, entertainment, and recreation Minority 754 12.2% N/A N/A Non-minority 5,254 84.7% 5.6% 17.9 Accommodation and food services Minority 545 16.7% 64.0% 13.6 Non-minority 2,695 82.5% 62.2% 20.6 Other services (except public administration) Minority 3,288 26.6% 4.1% 3.4 Non-minority 8,886 71.9% 19.5% 7.4 Sources: 2007 Survey of Business Owners and UWEX Center for Community and Economic Development *Includes only firms that are classifiable by

gender, ethnicity, race, and veteran status ** May not equal 100% as figures do not include firms that are equally minority and non-minority owned.

17

Average revenues for MBEs in the metro area are also reported in Appendix 4B.

Transform Milwaukee 4-14 Entrepreneurs and Entrepreneurship

The Milwaukee metro area’s overall minority ownership rate of 12.9% is low compared to its total share of

minority residents. However, minority ownership rates in the metro area are even lower among so-called high

barrier industries. As defined by Bates et al (2011), a high-barrier industry is one defined by advanced

educational requirements and/or large levels of startup capital. Examples of high-barrier industries with small

relative levels of minority ownership in the Milwaukee-Waukesha-West Allis MSA include professional,

scientific and professional services (7.3% of firms); finance and insurance (7.1%); and wholesale trade (7.0%).

The share of MBEs in manufacturing (another high barrier industry) is especially surprising with minority-

ownership accounting for just 3.4% of firms in the metro area.

In contrast, MBEs in the Milwaukee MSA have higher shares of firms in low-barrier industries, or industries

relatively accessible to individuals with less than a college education and without large financial capital

requirements. Not unlike other large metropolitan areas, minority ownership rates in the Milwaukee metro

area tend to be the greatest in low-barrier industries including administrative and support services (14.6%);

accommodations and food services (16.7%); transportation and warehousing (22.7%) and other services

(26.6%). The one key exception in this low barrier distribution is construction, where minority-owned firms

only account for 6.4% of all firms in the MSA.18

While MBEs are important across all ethnicities and racial categories, this analysis primarily considers

ownership rates among Black or African American residents and Hispanic or Latino residents. Ownership

within these two groups in the Milwaukee-Waukesha-West Allis MSA is compared to MBEs in the 51 other U.S.

metro areas with a population of one-million or more. While this study is not intended to be a benchmarking

analysis, these comparisons provide perspectives and updates on past statistics suggesting that the Milwaukee

metro area has some of the lowest minority business ownership rates in the nation.19

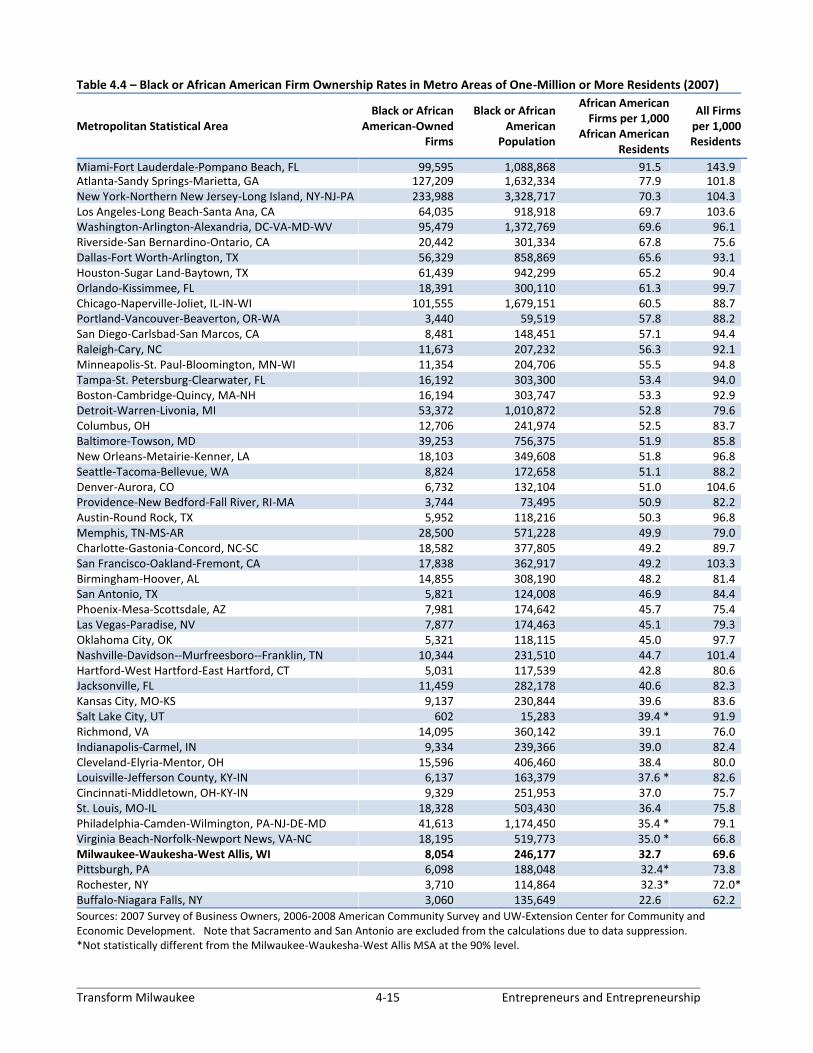

Black or African American MBE figures are reported in Table 4.4 with rates measured as the number of firms

per 1,000 Black or African American residents in each respective metropolitan area. Similarly, Hispanic or

Latino ownership rates are listed in Table 4.5. Each table compares these rates to the overall number of firms

per 1,000 residents in a metro area, regardless of race or ethnicity. Based on these measures, it is clear that

the Milwaukee-Waukesha-West Allis MSA has among the lowest ownership rates for Black or African

American-owned firms and Hispanic or Latino firms. Reasons for these low rates in Milwaukee have been

hypothesized, but definitive answers will require a detailed econometric study.

While not ranked on Table 4.4 or Table 4.5, it is important to note that the Milwaukee MSA also has one of the

lowest rates of firms per 1,000 residents for the total population. The overall rate is important as it suggests

that low business ownership rates in the Milwaukee metro area are not necessarily exclusive to minority-owned

firms. Instead, low ownership rates may be a function of overall entrepreneurial propensity in the region. Some

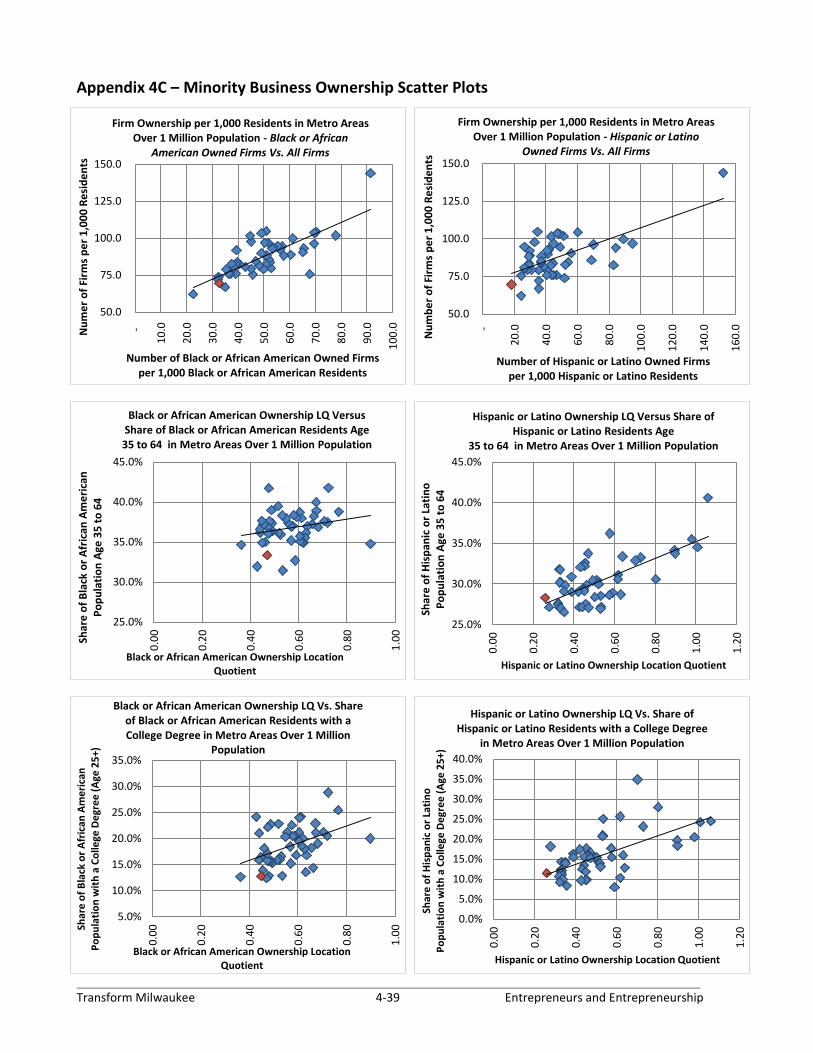

statistical evidence in this observation is present as well. Measuring the correlation between the overall

number of firms per 1,000 residents in an MSA and the number of Black or African American firms per 1,000

residents shows a strong positive relationship. Specifically, Pearson’s correlation coefficient between African

American firms per capita and overall firms per capita is 0.764 (or 0.688 when removing the Miami-Fort

Lauderdale-Pompano Beach, FL MSA, which is somewhat of an outlier).

18 Construction and MBEs will be further considered in Section 9. 19 The aforementioned study from the University of Wisconsin-Milwaukee’s Center for Economic Development showed Milwaukee as having low minority-ownership rates among large metro areas. Furthermore, Forbes sponsored research conducted by Cox and Ozuna in 2011 ranked Milwaukee as the worst large metro area for minority entrepreneurs.

Transform Milwaukee 4-15 Entrepreneurs and Entrepreneurship

Table 4.4 – Black or African American Firm Ownership Rates in Metro Areas of One-Million or More Residents (2007)

Metropolitan Statistical Area Black or African

American-Owned Firms

Black or African American

Population

African American Firms per 1,000

African American Residents

All Firms per 1,000 Residents

Miami-Fort Lauderdale-Pompano Beach, FL 99,595 1,088,868 91.5 143.9 Atlanta-Sandy Springs-Marietta, GA 127,209 1,632,334 77.9 101.8 New York-Northern New Jersey-Long Island, NY-NJ-PA 233,988 3,328,717 70.3 104.3 Los Angeles-Long Beach-Santa Ana, CA 64,035 918,918 69.7 103.6 Washington-Arlington-Alexandria, DC-VA-MD-WV 95,479 1,372,769 69.6 96.1 Riverside-San Bernardino-Ontario, CA 20,442 301,334 67.8 75.6 Dallas-Fort Worth-Arlington, TX 56,329 858,869 65.6 93.1 Houston-Sugar Land-Baytown, TX 61,439 942,299 65.2 90.4 Orlando-Kissimmee, FL 18,391 300,110 61.3 99.7 Chicago-Naperville-Joliet, IL-IN-WI 101,555 1,679,151 60.5 88.7 Portland-Vancouver-Beaverton, OR-WA 3,440 59,519 57.8 88.2 San Diego-Carlsbad-San Marcos, CA 8,481 148,451 57.1 94.4 Raleigh-Cary, NC 11,673 207,232 56.3 92.1 Minneapolis-St. Paul-Bloomington, MN-WI 11,354 204,706 55.5 94.8 Tampa-St. Petersburg-Clearwater, FL 16,192 303,300 53.4 94.0 Boston-Cambridge-Quincy, MA-NH 16,194 303,747 53.3 92.9 Detroit-Warren-Livonia, MI 53,372 1,010,872 52.8 79.6 Columbus, OH 12,706 241,974 52.5 83.7 Baltimore-Towson, MD 39,253 756,375 51.9 85.8 New Orleans-Metairie-Kenner, LA 18,103 349,608 51.8 96.8 Seattle-Tacoma-Bellevue, WA 8,824 172,658 51.1 88.2 Denver-Aurora, CO 6,732 132,104 51.0 104.6 Providence-New Bedford-Fall River, RI-MA 3,744 73,495 50.9 82.2 Austin-Round Rock, TX 5,952 118,216 50.3 96.8 Memphis, TN-MS-AR 28,500 571,228 49.9 79.0 Charlotte-Gastonia-Concord, NC-SC 18,582 377,805 49.2 89.7 San Francisco-Oakland-Fremont, CA 17,838 362,917 49.2 103.3 Birmingham-Hoover, AL 14,855 308,190 48.2 81.4 San Antonio, TX 5,821 124,008 46.9 84.4 Phoenix-Mesa-Scottsdale, AZ 7,981 174,642 45.7 75.4 Las Vegas-Paradise, NV 7,877 174,463 45.1 79.3 Oklahoma City, OK 5,321 118,115 45.0 97.7 Nashville-Davidson--Murfreesboro--Franklin, TN 10,344 231,510 44.7 101.4 Hartford-West Hartford-East Hartford, CT 5,031 117,539 42.8 80.6 Jacksonville, FL 11,459 282,178 40.6 82.3 Kansas City, MO-KS 9,137 230,844 39.6 83.6 Salt Lake City, UT 602 15,283 39.4 * 91.9 Richmond, VA 14,095 360,142 39.1 76.0 Indianapolis-Carmel, IN 9,334 239,366 39.0 82.4 Cleveland-Elyria-Mentor, OH 15,596 406,460 38.4 80.0 Louisville-Jefferson County, KY-IN 6,137 163,379 37.6 * 82.6 Cincinnati-Middletown, OH-KY-IN 9,329 251,953 37.0 75.7 St. Louis, MO-IL 18,328 503,430 36.4 75.8 Philadelphia-Camden-Wilmington, PA-NJ-DE-MD 41,613 1,174,450 35.4 * 79.1 Virginia Beach-Norfolk-Newport News, VA-NC 18,195 519,773 35.0 * 66.8 Milwaukee-Waukesha-West Allis, WI 8,054 246,177 32.7 69.6 Pittsburgh, PA 6,098 188,048 32.4* 73.8 Rochester, NY 3,710 114,864 32.3* 72.0* Buffalo-Niagara Falls, NY 3,060 135,649 22.6 62.2

Sources: 2007 Survey of Business Owners, 2006-2008 American Community Survey and UW-Extension Center for Community and Economic Development. Note that Sacramento and San Antonio are excluded from the calculations due to data suppression. *Not statistically different from the Milwaukee-Waukesha-West Allis MSA at the 90% level.

Transform Milwaukee 4-16 Entrepreneurs and Entrepreneurship

Table 4.5 – Hispanic or Latino Firm Ownership Rates in Metro Areas of One-Million or More Residents (2007)

Metropolitan Statistical Area Hispanic or

Latino-Owned Firms

Hispanic or Latino

Population

Hispanic or Latino Firms per 1,000

Hispanic or Latino Residents

All Firms per 1,000 Residents

Miami-Fort Lauderdale-Pompano Beach, FL 320,083 2,099,334 152.5 143.9 New Orleans-Metairie-Kenner, LA 6,290 66,294 94.9 96.8 Orlando-Kissimmee, FL 40,509 453,773 89.3 99.7 Tampa-St. Petersburg-Clearwater, FL 32,402 383,757 84.4 94.0 Jacksonville, FL 6,119 73,708 83.0 82.3 Washington-Arlington-Alexandria, DC-VA-MD-WV 44,456 633,399 70.2 96.1 Baltimore-Towson, MD 5,815 84,274 69.0 85.8 New York-Northern New Jersey-Long Island, NY-NJ-PA 242,939 4,036,076 60.2 104.3 Houston-Sugar Land-Baytown, TX 104,368 1,865,649 55.9 90.4 San Antonio, TX 56,644 1,047,746 54.1 84.4 Louisville-Jefferson County, KY-IN 1,731 33,147 52.2 82.6 Pittsburgh, PA 1,319 25,418 51.9 73.8 Atlanta-Sandy Springs-Marietta, GA 25,030 487,984 51.3 101.8 San Diego-Carlsbad-San Marcos, CA 44,156 901,183 49.0 94.4 San Francisco-Oakland-Fremont, CA 41,207 847,595 48.6 103.3 Los Angeles-Long Beach-Santa Ana, CA 266,582 5,645,374 47.2 103.6 St. Louis, MO-IL 2,819 60,218 46.8 75.8 Austin-Round Rock, TX 21,255 473,084 44.9 96.8 Riverside-San Bernardino-Ontario, CA 81,178 1,819,809 44.6 75.6 Columbus, OH 2,257 50,708 44.5 83.7 Richmond, VA 2,005 45,950 43.6 76.0 Nashville-Davidson--Murfreesboro--Franklin, TN 3,473 80,018 43.4 101.4 Providence-New Bedford-Fall River, RI-MA 6,264 145,927 42.9 82.2 Boston-Cambridge-Quincy, MA-NH 14,919 354,702 42.1 92.9 Dallas-Fort Worth-Arlington, TX 69,265 1,650,317 42.0 93.1 Charlotte-Gastonia-Concord, NC-SC 5,675 137,936 41.1 89.7 Raleigh-Cary, NC 3,677 90,290 40.7 92.1 Philadelphia-Camden-Wilmington, PA-NJ-DE-MD 15,444 380,066 40.6 79.1 Cincinnati-Middletown, OH-KY-IN 1,598 39,417 40.5 75.7 Birmingham-Hoover, AL 1,315 34,144 38.5 81.4 Seattle-Tacoma-Bellevue, WA 9,001 242,065 37.2 88.2 Sacramento--Arden-Arcade--Roseville, CA 14,362 387,122 37.1 83.8 San Jose-Sunnyvale-Santa Clara, CA 17,499 473,795 36.9 85.1 Virginia Beach-Norfolk-Newport News, VA-NC 2,484 69,777 35.6 66.8 Memphis, TN-MS-AR 1,725 48,482 35.6 79.0 Rochester, NY 1,867 52,485 35.6 72.0* Denver-Aurora, CO 18,804 541,716 34.7 104.6 Oklahoma City, OK 3,633 110,533 32.9 97.7 Detroit-Warren-Livonia, MI 5,045 162,931 31.0 79.6 Chicago-Naperville-Joliet, IL-IN-WI 55,086 1,849,486 29.8 88.7 Salt Lake City, UT 4,892 165,002 29.6 91.9 Kansas City, MO-KS 4,070 138,913 29.3 83.6 Portland-Vancouver-Beaverton, OR-WA 6,373 218,823 29.1 88.2 Indianapolis-Carmel, IN 2,286 78,860 29.0 82.4 Las Vegas-Paradise, NV 14,310 505,213 28.3 79.3 Cleveland-Elyria-Mentor, OH 2,321 87,267 26.6 80.0 Minneapolis-St. Paul-Bloomington, MN-WI 3,926 148,404 26.5 94.8 Hartford-West Hartford-East Hartford, CT 3,450 130,527 26.4 80.6 Phoenix-Mesa-Scottsdale, AZ 30,677 1,258,721 24.4 75.4 Buffalo-Niagara Falls, NY 927 38,265 24.2 * 62.2 Milwaukee-Waukesha-West Allis, WI 2,296 127,265 18.0 69.6 Sources: 2007 Survey of Business Owners, 2006-2008 American Community Survey and UW-Extension Center for Community and Economic Development *Not statistically different from the Milwaukee-Waukesha-West Allis MSA at the 90% level.

Transform Milwaukee 4-17 Entrepreneurs and Entrepreneurship

Somewhat lesser, but positive relationships (ρ = 0.642) are also found among Hispanic or Latino ownership

rates (ρ = 0.393 with the Miami metro area removed). These correlation coefficients recognize the dictum that

correlation does not mean causality, but there is some parallel between overall ownership rates and minority

ownership rates. These coefficients are summarized in Table 4.6 and scatterplots for ownership rates are also

available in Appendix 4C.

Minority and overall ownership rates among metro areas also can be normalized using location quotients. The

location quotient (LQ) is calculated by dividing a metropolitan area’s minority-owned firms per capita by its

overall firms per capita (See Section 2 for more on LQs). If a metro area has the same minority ownership rate

as its overall ownership rate, then the corresponding LQ would be 1.0. Location quotients with values below

1.0 show lower relative ownership rates among minority residents in a metro area, while values above 1.0

show higher rates. Accordingly, the measures control somewhat for metro areas that have high overall

ownership rates.

Comparing location quotients for Black or African American ownership rates, Milwaukee’s position improves

somewhat in that the metro area either ranks above, or is not statistically different from 21 other large

metropolitan areas (Table 4.7). Nonetheless, this figure remains well below those metro areas with the highest

location quotients. Furthermore, comparing location quotients for Hispanic or Latino ownership provides little

change in Milwaukee’s overall position (Table 4.8). Consequently, other factors beyond overall ownership

rates likely are contributing to the lower rates found in the Milwaukee metro area.

As mentioned earlier, a detailed econometric study would help to identify local factors contributing to MBE

formation rates in the Milwaukee metro area. Two factors that should be considered in this analysis are age

structure and educational attainment. Data suggest that entrepreneurial rates increase dramatically between

the ages of 35 and 64 and among persons with a bachelor’s degree or higher.20 However, when compared to

other large metropolitan areas, the Milwaukee MSA has one of the smallest shares of Black or African

American residents ages 35 to 64 and one of the lowest rates of Black or African American residents age 25 or

over with a college degree. Further, the Milwaukee MSA is in the bottom third of large metro areas for both

its share of Hispanic or Latino residents ages 35 to 64 and its share of Hispanic or Latino residents with a

bachelor’s degree or higher.

While the influences of age and education on entrepreneurial propensity are not necessarily specific to Black

or Hispanic entrepreneurs, there is some modest to strong correlation between these factors and minority

ownership rates in the nation’s largest metro areas. The scatterplots in Appendix 4C and the Pearson’s

correlation coefficients in Table 4.6 show moderate positive correlations between Black or African American

ownership rates and levels of Black or African American educational attainment in the nation’s largest metro

areas. A somewhat smaller, but positive correlation is found between Black or African American ownership

rates and the share of the population between the ages of 35 and 64. Even stronger correlations are seen

between Hispanic or Latino ownership rates and age and educational attainment.

20

Acs and Armington (2003) find that human capital affects firm formation rates. However, for other perspectives again see: Henderson, J., Low, S.A., and Weiler, S. (2007) and Yenerall (2008).

Transform Milwaukee 4-18 Entrepreneurs and Entrepreneurship

Table 4.6 – Selected Measures of Business Ownership Correlation in Large Metropolitan Areas

Variables Measured Correlation Coefficient (ρ)

Black or African American Ownership Rate and

Overall Ownership Rate 0.764 *

Hispanic or Latino Ownership Rate and

Overall Ownership Rate 0.642 **

Black or African American Ownership LQ and Share of Black or African

American Residents Ages 35 to 64 0.228

Correlation between Black or African American Ownership LQ and

Share of Black or African American Residents with a College Degree 0.444

Correlation between Hispanic or Latino Ownership LQ and Share of

Hispanic or Latino Residents Ages 35 to 64 0.689

Correlation between Hispanic or Latino Ownership LQ and Share of

Hispanic or Latino Residents with a College Degree 0.616

Sources: Source: 2007 Survey of Business Owners, 2006-2008 American Community Survey and Author’s Calculations * 0.688 with the Miami-Fort Lauderdale-Pompano Beach, FL MSA removed

** 0.393 with Miami-Fort Lauderdale-Pompano Beach, FL MSA removed

Again, these correlations are not evidence that minority business ownership rates in the Milwaukee-

Waukesha-West Allis MSA are necessarily attributed to age or education levels. Nonetheless, we know that

these two demographic categories are among the most entrepreneurial and are underrepresented in

Milwaukee’s Black or African residents and Hispanic or Latino residents relative to other metro areas. While

some public policy officials might view these figures as a challenge, Milwaukee’s demographics may actually

provide an opportunity in the coming decade. Specifically, the large number of young Black and African

American residents and younger Hispanic and Latino residents offers great potential for future MBEs in

Milwaukee. These potential entrepreneurs will need to be encouraged to create these opportunities. Levels

of human capital also will need to be increased. Strategies for developing these future potential business

owners will be examined later in this section.

Transform Milwaukee 4-19 Entrepreneurs and Entrepreneurship

Table 4.7 – Selected Demographic Characteristics and Ownership LQs for Black or African American Residents (2007)

Metropolitan Statistical Area African American

Owned Firm Location Quotient

African American Firms per 1,000

African American Residents

African American Residents –

% Age 35 to 64

African American Residents Age 25 and Over- % with

College Degree

Riverside-San Bernardino-Ontario, CA 0.90 67.8 34.7% 20.0% Atlanta-Sandy Springs-Marietta, GA 0.77 77.9 38.7% 25.4%

Washington-Arlington-Alexandria, DC-VA-MD-WV 0.72 69.6 41.8% 28.8%

Houston-Sugar Land-Baytown, TX 0.72 65.2 37.4% 20.5%

Dallas-Fort Worth-Arlington, TX 0.70 65.6 37.6% 21.2%

Chicago-Naperville-Joliet, IL-IN-WI 0.68 60.5 36.8% 19.0%

New York-Northern New Jersey-Long Island, NY-NJ-PA 0.67 70.3 38.9% 21.1%

Los Angeles-Long Beach-Santa Ana, CA 0.67 69.7 39.9% 22.9%

Detroit-Warren-Livonia, MI 0.66 52.8 38.2% 14.3%

Portland-Vancouver-Beaverton, OR-WA 0.66 57.8 37.2% 18.2%

Miami-Fort Lauderdale-Pompano Beach, FL 0.64 91.5 36.9% 16.8%

Memphis, TN-MS-AR 0.63 49.9 36.1% 13.5%

Columbus, OH 0.63 52.5 35.5% 18.0%

Providence-New Bedford-Fall River, RI-MA 0.62 50.9 34.9% 20.0%

Orlando-Kissimmee, FL 0.61 61.3 35.0% 18.6%

Raleigh-Cary, NC 0.61 56.3 38.0% 24.2%

Phoenix-Mesa-Scottsdale, AZ 0.61 45.7 35.1% 24.0%

San Diego-Carlsbad-San Marcos, CA 0.61 57.1 35.7% 21.1%

Baltimore-Towson, MD 0.60 51.9 38.7% 19.5%

Birmingham-Hoover, AL 0.59 48.2 38.1% 16.8%

Minneapolis-St. Paul-Bloomington, MN-WI 0.59 55.5 32.7% 20.5%

Seattle-Tacoma-Bellevue, WA 0.58 51.1 38.4% 20.4%

Boston-Cambridge-Quincy, MA-NH 0.57 53.3 37.0% 22.5%

Las Vegas-Paradise, NV 0.57 45.1 36.9% 15.2%

Tampa-St. Petersburg-Clearwater, FL 0.57 53.4 35.2% 18.4%

San Antonio, TX 0.56 * 46.9 37.4% 21.2%

Charlotte-Gastonia-Concord, NC-SC 0.55 49.2 37.9% 20.3%

New Orleans-Metairie-Kenner, LA 0.53 51.8 31.4% 12.8% *

Hartford-West Hartford-East Hartford, CT 0.53 * 42.8 38.3% 16.6%

Virginia Beach-Norfolk-Newport News, VA-NC 0.52 35.0 * 35.9% 15.9%

Austin-Round Rock, TX 0.52 * 50.3 36.1% 22.8%

Richmond, VA 0.51 * 39.1 39.5% 15.8%

Jacksonville, FL 0.49 * 40.6 36.4% 15.2%

Cincinnati-Middletown, OH-KY-IN 0.49 * 37.0 37.3% 15.7%

Denver-Aurora, CO 0.49 * 51.0 39.0% 22.7%

St. Louis, MO-IL 0.48 * 36.4 36.2% 15.7%

Cleveland-Elyria-Mentor, OH 0.48 * 38.4 37.5% 12.8% *

San Francisco-Oakland-Fremont, CA 0.48 * 49.2 41.7% 22.2%

Kansas City, MO-KS 0.47 * 39.6 36.8% 15.7%

Indianapolis-Carmel, IN 0.47 * 39.0 36.1% 17.1%

Milwaukee-Waukesha-West Allis, WI 0.47 32.7 33.4% 12.4%

Oklahoma City, OK 0.46 * 45.0 35.0% 18.1%

Louisville-Jefferson County, KY-IN 0.45 * 37.6 * 37.2% 13.9%

Rochester, NY 0.45 * 32.3 34.9% 12.8% *

Philadelphia-Camden-Wilmington, PA-NJ-DE-MD 0.45 * 35.4 * 37.7% 16.4%

Nashville-Davidson--Murfreesboro--Franklin, TN 0.44 * 44.7 36.1% 21.0%

Pittsburgh, PA 0.44 * 32.4 * 36.6% 15.9%

Salt Lake City, UT 0.43 * 39.4 * 31.9%* 24.1%

Buffalo-Niagara Falls, NY 0.36 22.6 34.6% 12.6% *

Sources: Source: 2007 Survey of Business Owners, 2006-2008 American Community Survey and UW-Extension Center for Community and Economic Development. Note that Sacramento and San Antonio are excluded from the calculations due to data suppression. *Not statistically different from the Milwaukee-Waukesha-West Allis MSA at the 90% level

Transform Milwaukee 4-20 Entrepreneurs and Entrepreneurship

Table 4.8 – Hispanic or Latino Ownership LQs, Residents Age 35 to 64, and Residents with a College Degree (2007)

Metropolitan Statistical Area

Hispanic or Latino Owned Firm Location

Quotient

Hispanic or Latino Firms per 1,000

Hispanic or Latino Residents

Hispanic or Latino Population –

% Age 35 to 64

Hispanic or Latino Population – Percent with

College Degree

Miami-Fort Lauderdale-Pompano Beach, FL 1.06 152.47 40.6% 24.4% Jacksonville, FL 1.01 83.02 34.5% 24.1% New Orleans-Metairie-Kenner, LA 0.98 94.88 35.5% 20.4% Tampa-St. Petersburg-Clearwater, FL 0.90 84.43 33.7% 18.3% Orlando-Kissimmee, FL 0.90 89.27 34.2% 19.7% Baltimore-Towson, MD 0.80 69.00 30.6% 27.9% Washington-Arlington-Alexandria, DC-VA-MD-WV 0.73 70.19 33.2% 23.1% Pittsburgh, PA 0.70 51.89 32.9% 34.9% San Antonio, TX 0.64 54.06 33.4% 12.8% Louisville-Jefferson County, KY-IN 0.63 52.22 28.7% * 15.9% Houston-Sugar Land-Baytown, TX 0.62 55.94 31.1% 10.3%* St. Louis, MO-IL 0.62 46.81 30.6% 25.6% Riverside-San Bernardino-Ontario, CA 0.59 44.61 28.9% 7.9% New York-Northern New Jersey-Long Island, NY-NJ-PA 0.58 60.19 36.2% 15.4% Richmond, VA 0.57 43.63 28.6% * 17.7% Cincinnati-Middletown, OH-KY-IN 0.54 40.54 27.2% * 25.0% Virginia Beach-Norfolk-Newport News, VA-NC 0.53 35.60 28.5% * 20.9% Columbus, OH 0.53 44.51 26.9% 20.6% Providence-New Bedford-Fall River, RI-MA 0.52 42.93 29.9% 13.0%* San Diego-Carlsbad-San Marcos, CA 0.52 49.00 30.1% 13.9% Philadelphia-Camden-Wilmington, PA-NJ-DE-MD 0.51 40.64 30.5% 14.0% Atlanta-Sandy Springs-Marietta, GA 0.50 51.29 28.4% * 15.3% Rochester, NY 0.49 35.57 30.4% 15.4% Birmingham-Hoover, AL 0.47 38.51 27.1% * 15.2% San Francisco-Oakland-Fremont, CA 0.47 48.62 33.7% 16.6% Austin-Round Rock, TX 0.46 44.93 29.9% 15.9% Charlotte-Gastonia-Concord, NC-SC 0.46 41.14 27.5% 15.6% Los Angeles-Long Beach-Santa Ana, CA 0.46 47.22 32.6% 9.8% Boston-Cambridge-Quincy, MA-NH 0.45 42.06 32.2% 17.6% Dallas-Fort Worth-Arlington, TX 0.45 41.97 29.1% 9.7% Memphis, TN-MS-AR 0.45 35.58 29.3% 11.7%* Sacramento--Arden-Arcade--Roseville, CA 0.44 37.10 29.4% 13.5% Raleigh-Cary, NC 0.44 40.72 27.1% 15.5% San Jose-Sunnyvale-Santa Clara, CA 0.43 36.93 32.0% 12.5% Nashville-Davidson--Murfreesboro--Franklin, TN 0.43 43.40 27.1% 9.6% Seattle-Tacoma-Bellevue, WA 0.42 37.18 29.0% 17.4% Buffalo-Niagara Falls, NY 0.39 * 24.23* 29.0% 15.4% Detroit-Warren-Livonia, MI 0.39 30.96 30.9% 16.3% Las Vegas-Paradise, NV 0.36 28.32 29.8% 8.3% Indianapolis-Carmel, IN 0.35 * 28.99 26.5% 13.9% Kansas City, MO-KS 0.35 29.30 29.1% 14.3% Oklahoma City, OK 0.34 * 32.87 26.9% 9.8%* Chicago-Naperville-Joliet, IL-IN-WI 0.34 29.78 30.2% 11.0%* Cleveland-Elyria-Mentor, OH 0.33 * 26.60 31.7% 14.3% Denver-Aurora, CO 0.33 34.71 30.1% 12.1%* Portland-Vancouver-Beaverton, OR-WA 0.33 29.12 27.1% 12.3%* Hartford-West Hartford-East Hartford, CT 0.33 * 26.43 31.8% 11.7%* Phoenix-Mesa-Scottsdale, AZ 0.32 * 24.37 27.6% 9.2% Salt Lake City, UT 0.32 * 29.65 27.5% 10.6%* Minneapolis-St. Paul-Bloomington, MN-WI 0.28 * 26.45 27.1% 18.1% Milwaukee-Waukesha-West Allis, WI 0.26 18.04 28.3% 11.5% Sources: Source: 2007 Survey of Business Owners, 2006-2008 American Community Survey and UW-Extension Center for Community and Economic Development *Not statistically different from the Milwaukee-Waukesha-West Allis MSA at the 90% level

Transform Milwaukee 4-21 Entrepreneurs and Entrepreneurship

Assessing Entrepreneurship Policy and Strategy for Milwaukee’s Industrial Corridor

Entrepreneurship is not a panacea for growing the local economy; however, the preceding metrics and

discussion suggest that entrepreneurial activity in the Milwaukee region is lacking. The factors driving these

measures are likely a combination of industrial legacy, human capital levels, demographic characteristics and

other dynamics. If entrepreneurship is to become a successful economic development strategy for

Milwaukee’s Industrial Corridor, then additional efforts are needed to cultivate entrepreneurs of all types.

However, developing initiatives and policies to further entrepreneurship will entail significant challenges.

Specific concerns to be addressed include those outlined by Markely et al (2005):

Reluctance of practitioners to abandon traditional strategies;

Shortage of institutional support for an entrepreneurship strategy;

Lack of community leaders’ familiarity with entrepreneurship;

Recognition that the outcomes of entrepreneurship are incremental;

Acceptance that there currently are limited examples of state and local strategies to provide guidance and

support.

Consequently, embracing entrepreneurship may require a sort of “leap of faith.” Success is unlikely to be swift.

Community leaders and economic developers need to learn more about entrepreneurship. Existing

entrepreneurial support organizations need to be included. Outcomes need to be measured and institutional

champions need to emerge. Ultimately, creating entrepreneurial strategies for Milwaukee’s Industrial Corridor

requires understanding best practices and tools that can be adapted to a breadth of entrepreneurial types. In

fact, several of these tools may be considered to be entrepreneurial themselves. Keeping these challenges in

mind, the following discussion considers five areas of entrepreneurial development strategy:

1. Increasing support for minority business enterprises;

2. Enhancing the entrepreneurial culture in the Transform Milwaukee Study Area and the broader region;

3. Understanding and rethinking the role of universities in entrepreneurship;

4. Connecting existing entrepreneurial support systems;

5. Developing support for second-stage companies.

Supporting Minority Business Enterprises

Improving minority ownership rates should be considered as a worthwhile strategy to create economic

opportunities in the Transform Milwaukee Study Area and beyond. Developing MBEs in manufacturing and

construction may be of particular interest given the region’s industrial base; the low number of MBEs in these

industries; and the propensity for minority owners in construction and manufacturing to hire within low

income areas. 21 However, impacts on unemployment rates resulting from increased numbers MBEs should be

tempered somewhat. As identified by Levine (2007), even in those metropolitan areas with high rates of

21

Expansion of MBEs beyond the Transform Milwaukee Study Area also may be important for improving minority employment prospects as an owner’s race often is a larger factor in predicting the racial composition of the small-business labor force (Bates 2006; Boston & Ross 1997).

Transform Milwaukee 4-22 Entrepreneurs and Entrepreneurship

minority business ownership, these firms only account for a small share of overall employment. Consequently,

a dramatic increase in MBEs could potentially have a small impact on employment conditions in the Transform

Milwaukee Study Area. Given this dynamic, the development of minority businesses should be viewed as one

among many strategies for improving local employment opportunities.

When considering strategies for the formation and development of MBEs in Milwaukee, there is little research

specific to the community to draw upon. However, research related to the support of small and minority-

owned businesses in other communities provides some context. One comprehensive analysis conducted in

New York suggests five “gaps” facing entrepreneurs in a metropolitan setting, many of whom were

disadvantaged (Servon, Fairlie, Rastello and Seely, 2010). These gaps involve both financial and non-financial

difficulties and include: 1) the information gap; 2) an institutional capacity and service delivery gap; 3) a capital

gap; 4) an asset gap; and 5) the transitional gap.

The first two gaps are unrelated to an entrepreneur’s financial resources. The information gap suggests that

cultural and language barriers; lack of awareness of resources; poor financial literacy; and lack of business

acumen all hinder informed business decision making. The institutional capacity and service delivery gap

suggests that small business support organizations often face capacity issues related to high levels of

fragmentation and inefficiency; duplication of services; inadequate staffing and resources; and slow

incorporation of emerging best practices. These two gaps will be addressed later in Section 4.

The remaining three gaps are related to financing, which has been the subject of significant research related to

MBEs and entrepreneurial development.22 First, the capital gap points to a lack of available financing both

before and after startup. Many entrepreneurs require very little capital for startup, often below the lending

threshold requirements of traditional lenders. Microloan funds and peer-to-peer lending networks provide

some opportunities for addressing this gap, as should the African American Chamber of Commerce’s revolving

loan fund (targeting start-up lending between $1,500 and $25,000). However, Servon et al (2010) suggest that

somewhat larger loan amounts between $50,000 and $100,000 are commonly unavailable to firms looking to

start or expand.

Second, the asset gap faces entrepreneurs without the necessary assets needed to secure loans, such as home

equity and a good credit history. In economically-challenged communities, such as the Transform Milwaukee

Study Area, this gap is particularly prevalent due to lower home ownership rates and property values. If

friends and families of entrepreneurs face similar economic conditions, the asset gap may be more extensive.

Specifically, friends and families without appropriate assets may not be able to serve as loan co-signers or

provide informal sources of lending

Finally, the transitional gap refers to challenges related to moving from non-traditional lines of credit to more

formal financing. As mentioned, microcredit resources are available to some entrepreneurs. However, these

sources may be offered a limited amount of times and are rarely applied to credit history. Consequently, once

microcredit sources subside, graduating to traditional financing may not be a viable step. Activities to

overcome these issues include identifying other sources of collateral and helping entrepreneurs to develop

22

A comprehensive review on the issues facing MBEs, including financing, is outside the scope of this analysis. However, Bates (2010) provides one overview of these issues.

Transform Milwaukee 4-23 Entrepreneurs and Entrepreneurship

richer credit histories (by documenting experiences with non-traditional lending sources that often do not

report to credit bureaus).

Lenders are concerned, of course, with financial gaps facing minority entrepreneurs and have explored ways to

address these issues. In a review of inner city lending strategies, Bates (2010) found mixed results among

models used over the past few decades including Minority Enterprise Small Business Investment Companies

(MESBICs); Specialized Small Business Investment Companies (SSBICs); community development financial

institution funds; private venture capital (VC) funds; Medallion Funding; and microenterprise programs. Bates

concludes that regardless of the model, publicly-subsidized business lenders must meet several well-

established preconditions for success. While these may seem intuitive to experienced lenders, they can be

difficult to operationalize in a central city environment.

First, the portfolio must be large enough to achieve scale economies in loan processing and servicing.

However, many subsidized inner-city lenders operate below the $2 million threshold. This affects viability as

lenders’ operating costs are too high. Inflated operating costs also may preclude a program’s ability to employ

a full-time professional manager with expertise to evaluate borrower creditworthiness.

Second, business lenders must be able to properly manage loan default risks, both by diversifying those risks

and by having the ability to recoup loan principal in the event of default. The latter has been achieved through

loan collateral requirements (such as those required by Medallion Funding) and loan guarantees from entities

such as the Small Business Administration. However, diversifying risks may also require lending outside a

limited geographic area in the inner city. Bates points to examples from ICV Partners and Chicago’s Shorebank

Neighborhood Fund, which made VC investments in Chicago’s inner city until the mid-1990s.23 Despite

managerial expertise and the level of financing necessary, ICV Partners’ equity investments in inner-city

ventures failed to generate competitive financial returns, while ICV Partners’ non-inner city investments

produced very high returns. While this dichotomy may not prove viable for a private for-profit investment

enterprise, it does suggest that balancing investments across geographic areas could provide one model for

diversifying risk in publically-subsidized central city investments. That is, lending programs that target the

Transform Milwaukee Initiative may need to spread risk by pooling investments across a broader geographic

area. This finding is reinforced by the Shorebank Neighborhood Fund, as targeting a limited geographic area

was one of the cited reasons for its failure.

An additional insight on microenterprise financing is provided by Bates et al (2011). They conclude that

microenterprise lending programs have been largely ineffective for both high and low barrier businesses. As

noted earlier, high barrier industries typically require advanced education and training and/or large scale

capital investments. Low barrier businesses are not capital intensive, but education and skill level play an

important role in access and success. In short, entry into low barrier industries typically is not constrained by

wealth and microloans often are not as critical. That is, aspiring minority entrepreneurs possessing few

personal assets are just as likely to become self-employed in low barrier industries as those with a net worth of

$25,000 to $50,000. Instead, education and training may be the most important factors in supporting

entrepreneurs entering low barrier enterprises. The authors conclude that microloan programs may better

23

ICV Partners is a for-profit venture capital fund operated by Michael Porter’s Initiative for a Competitive Inner City and American Securities.

Transform Milwaukee 4-24 Entrepreneurs and Entrepreneurship

serve existing small businesses needing to finance expansion and continuation of operations, rather than those

seeking start-up funding. In turn, these findings suggest that new models of targeted capital sources may be

needed for minority entrepreneurs looking to enter high barrier industries (such as improved inner-city VC

funds), rather than funds for low-barrier industries.

Other opportunities for supporting minority business enterprises include procurement contracting

requirements with local governments. These programs are largely in place, but should be approached with

some caution for MBEs. Specifically, MBEs obtaining 25% or more of revenues from public sector sources have

notably higher failure rates when compared to other non-minority and minority firms with government

procurement contracts. The reasons for these failure rates are attributed to MBEs often being younger,

smaller and undercapitalized relative to other government contractors (Bates, 1997; Bates, 2009).

Accordingly, government assistance directed at developing strong MBEs should target entrepreneurs with the

necessary resources and skills (Bates, 2006; Bates and Bradford, 2008). If WHEDA pursues contracting with

MBEs as part of the Transform Milwaukee Initiative, then practices such as unbundling of large contracts or

connecting smaller MBEs with larger, established minority business owners should be considered.

Furthermore, MBEs should seek to develop non-local and non-government revenue sources.

Enhancing the Entrepreneurial Culture

Entrepreneurship as an economic development strategy is not limited to minority business development and

should include the entire community. However, it is important to note that entrepreneurship has cultural

elements. Economic environments, family backgrounds, employment histories, organizational experiences,

social networks, and personality traits all affect the probability of someone acting entrepreneurially (Rauch

and Frese, 2000). Some of these factors are deeply engrained in individuals and in societies; therefore, pools

of potential entrepreneurs may vary in size from region to region. Other elements, such as organizational

experiences and social networks, can be changed and influenced to develop and grow a community’s pipeline

of entrepreneurs. In other words, communities are not locked into current levels of entrepreneurial activity

and can take steps to create an entrepreneurial culture.

A community’s culture as a factor influencing its economic opportunities may seem somewhat “fluffy” to

elected officials and economic development practitioners. Creating an entrepreneurial culture is not concrete

like designating a new TIF district. However, if we look deeper, a community’s culture is an integral part of

economic development. For instance, Shaffer, Deller and Marcouiller (2004) note that some communities have

cultures where people feel victimized by external forces (such as a factory closing), while other communities

instead build on these forces (coalescing around, say, a similar factory closing) and adapt to create new

economic opportunities. Other communities may fail to recognize a culture that maintains the status quo,

such as Appalachian entrepreneurs who feel a perceived negative attitude in the community toward success

(Taylor et al, 2003). Accordingly, a community culture that focuses on failures rather than opportunities may

not recognize assets available for development.24

24

Hustedde (2007) provides an in-depth overview of entrepreneurial culture.

Transform Milwaukee 4-25 Entrepreneurs and Entrepreneurship

So what characteristics of a community constitute an entrepreneurial culture? From a broad perspective, an

entrepreneurial culture is one in which a community is aware of the importance of entrepreneurs to the local

economy. It is open to new and different ideas and it accepts failure. It is willing to experiment. It encourages

and supports entrepreneurs. More specifically, Hustedde (2007) maintains that an entrepreneurial culture is

fostered by:

Creating opportunities to learn, question and think differently about entrepreneurship;

Welcoming fresh voices and embracing diversity;

Mobilizing resources for entrepreneurs;

Cultivating networks for entrepreneurs to thrive;

Focusing on assets instead of deficits;