Embed Size (px)

Citation preview

Section 2Analyzing Sales Transactions

Section 2Analyzing Sales TransactionsWhat You’ll Learn

How to record the sale of merchandise on account.

How to use the accounts receivable subsidiary ledger.

How to post to the accounts receivable subsidiary ledger.

The use of the Sales Tax Payable account, and its rules of debit and credit.

The use of the Sales Returns and Allowances account, and its rules of debit and credit.

What You’ll Learn How to record the sale of merchandise

on account. How to use the accounts receivable

subsidiary ledger. How to post to the accounts receivable

subsidiary ledger. The use of the Sales Tax Payable

account, and its rules of debit and credit. The use of the Sales Returns and

Allowances account, and its rules of debit and credit.

Why It’s ImportantIt is essential to record sales

transactions correctly as they reflect the revenue of the business.

Why It’s ImportantIt is essential to record sales

transactions correctly as they reflect the revenue of the business.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Key Terms sale on account charge customer credit cards sales slip sales tax credit terms accounts receivable subsidiary ledger

Key Terms sale on account charge customer credit cards sales slip sales tax credit terms accounts receivable subsidiary ledger

subsidiary ledger controlling account sales return sales allowance credit memorandum contra account

subsidiary ledger controlling account sales return sales allowance credit memorandum contra account

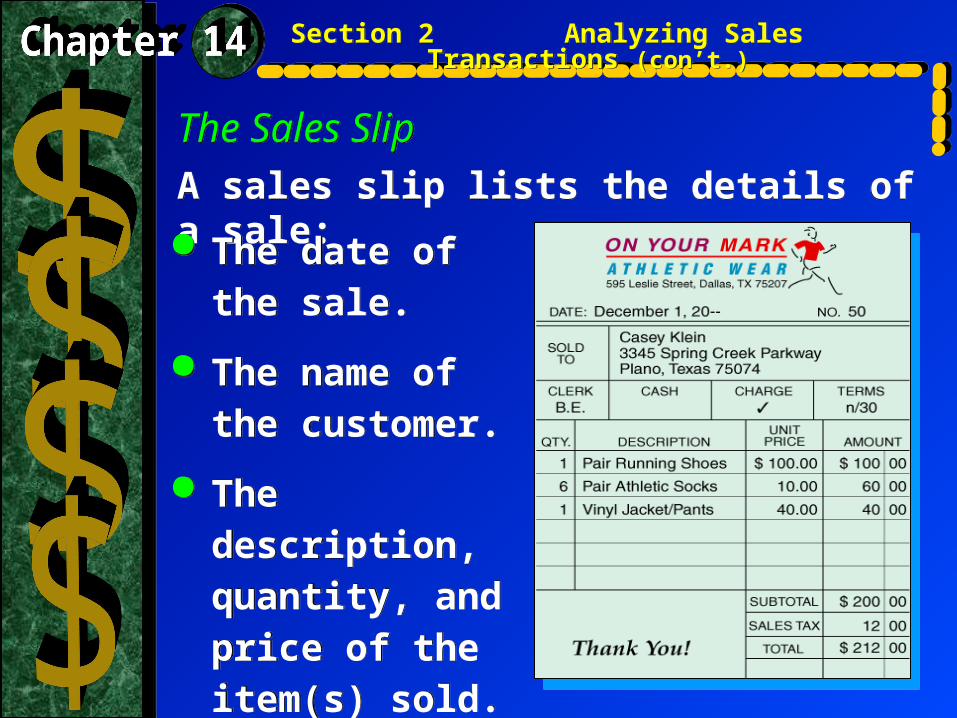

The Sales SlipA sales slip lists the details of a sale:

The Sales SlipA sales slip lists the details of a sale:

The date of the sale.

The name of the customer.

The description, quantity, and price of the item(s) sold.

The date of the sale.

The name of the customer.

The description, quantity, and price of the item(s) sold.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

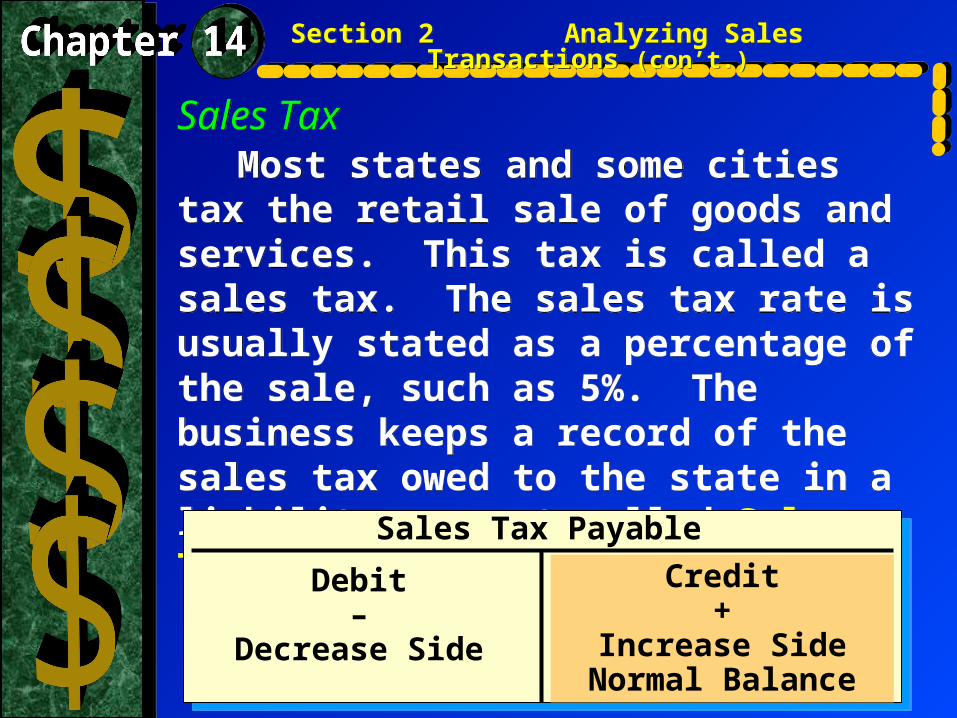

Sales TaxSales TaxMost states and some cities tax the

retail sale of goods and services. This tax is called a sales tax. The sales tax rate is usually stated as a percentage of the sale, such as 5%. The business keeps a record of the sales tax owed to the state in a liability account called Sales Tax Payable.

Most states and some cities tax the retail sale of goods and services. This tax is called a sales tax. The sales tax rate is usually stated as a percentage of the sale, such as 5%. The business keeps a record of the sales tax owed to the state in a liability account called Sales Tax Payable.

Sales Tax Payable

Debit–

Decrease Side

Credit+

Increase SideNormal Balance

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Credit TermsCredit Terms

Credit terms state the time allowed for

payment.

The credit terms for the sale to Casey

Klein are n/30.

The “n” stands for the net, or total,

amount of the sale.

The “30” stands for the number of

days the customer has to pay for the

merchandise.

Credit terms state the time allowed for

payment.

The credit terms for the sale to Casey

Klein are n/30.

The “n” stands for the net, or total,

amount of the sale.

The “30” stands for the number of

days the customer has to pay for the

merchandise.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

The Accounts Receivable LedgerThe Accounts Receivable LedgerThe accounts receivable subsidiary

ledger contains an account for each charge customer.

The accounts receivable subsidiary ledger contains an account for each charge customer.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

General Ledger

Accounts Receivable—controlling account $10,000

Accounts Receivable Subsidiary Ledger

Individual Accounts Within Ledger:

Brown, Joshua $2,000

Clark, Gillian 3,000

Greene, Jason 1,000

Perez, Sarita 4,000

Total $10,000

General Ledger

Accounts Receivable—controlling account $10,000

Accounts Receivable Subsidiary Ledger

Individual Accounts Within Ledger:

Brown, Joshua $2,000

Clark, Gillian 3,000

Greene, Jason 1,000

Perez, Sarita 4,000

Total $10,000

Controlling account balance equals total of accounts in subsidiary ledger.

Controlling account balance equals total of accounts in subsidiary ledger.

The Accounts Receivable Subsidiary Ledger FormThe Accounts Receivable Subsidiary Ledger Form

The subsidiary ledger account form

has lines at the top for the name and

address of the customer.

The subsidiary ledger account form

has lines at the top for the name and

address of the customer.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

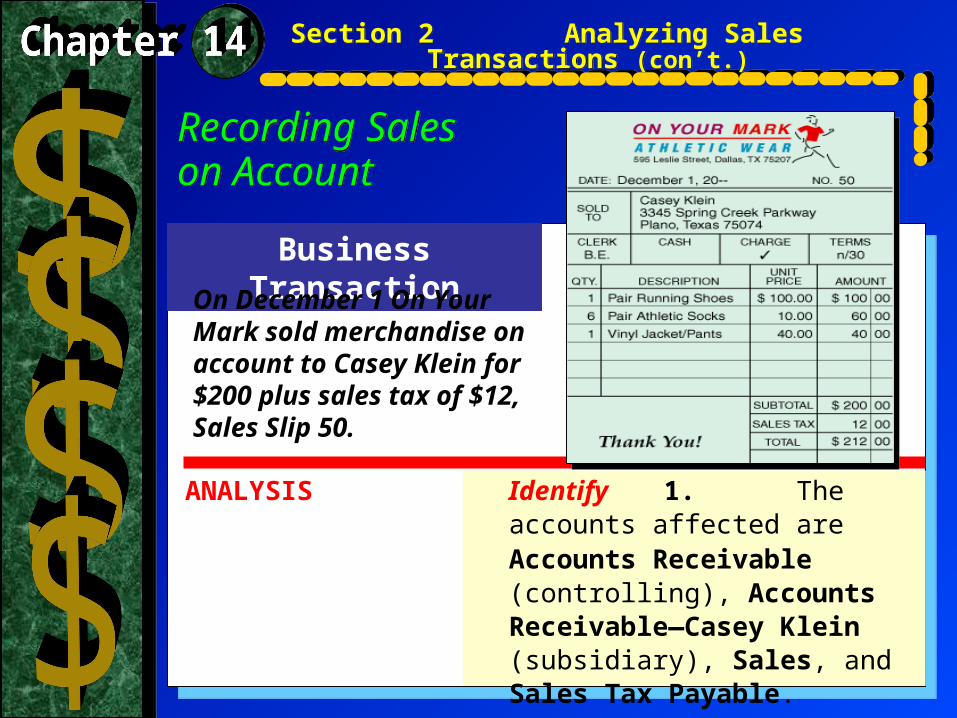

Business Transaction

ANALYSIS Identify 1. The accounts affected are Accounts Receivable (controlling), Accounts Receivable—Casey Klein (subsidiary), Sales, and Sales Tax Payable.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Recording Sales on AccountRecording Sales on Account

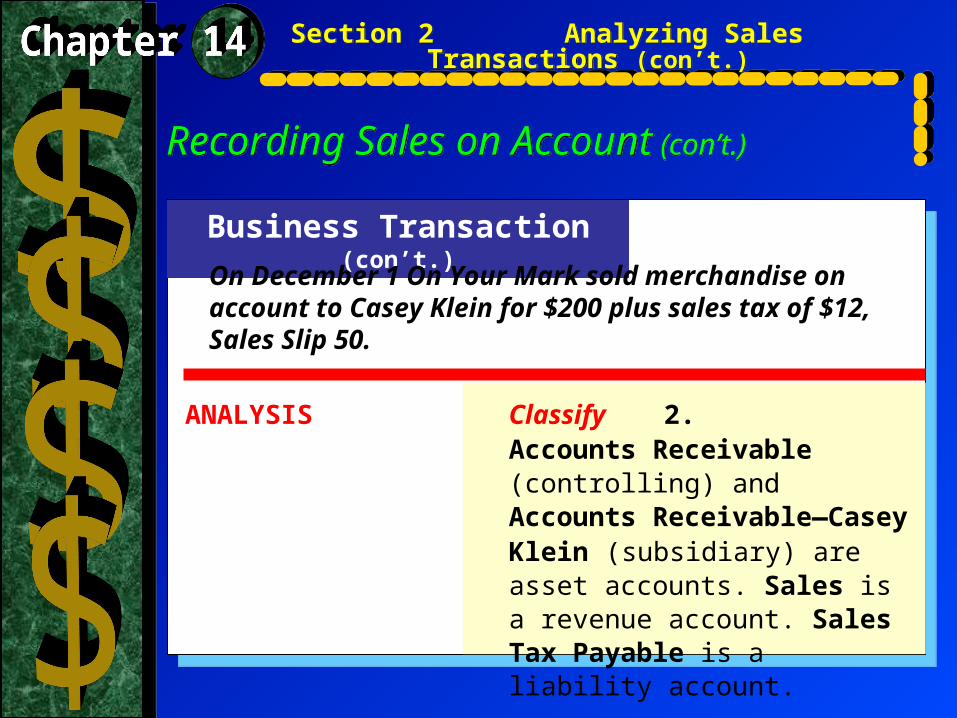

On December 1 On Your Mark sold merchandise on account to Casey Klein for $200 plus sales tax of $12, Sales Slip 50.

Business Transaction (con’t.)

ANALYSIS Classify 2.Accounts Receivable (controlling) and Accounts Receivable—Casey Klein (subsidiary) are asset accounts. Sales is a revenue account. Sales Tax Payable is a liability account.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Recording Sales on Account (con’t.)Recording Sales on Account (con’t.)

On December 1 On Your Mark sold merchandise on account to Casey Klein for $200 plus sales tax of $12, Sales Slip 50.

Business Transaction (con’t.)

ANALYSIS + / – 3.Accounts Receivable (controlling) and Accounts Receivable—Casey Klein (subsidiary) are increased by the total amount, $212 (dollar amount of merchandise sold plus sales tax). Sales is increased by the dollar amount of merchandise sold, $200. Sales Tax Payable is increased by the amount of sales tax charged, $12.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Recording Sales on Account (con’t.)Recording Sales on Account (con’t.)

On December 1 On Your Mark sold merchandise on account to Casey Klein for $200 plus sales tax of $12, Sales Slip 50.

Business Transaction (con’t.)

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Recording Sales on Account (con’t.)Recording Sales on Account (con’t.)

On December 1 On Your Mark sold merchandise on account to Casey Klein for $200 plus sales tax of $12, Sales Slip 50.

DEBIT-CREDIT RULE 4.Increases to asset accounts are recorded as debits. Debit Accounts Receivable (controlling) for $212. Also debit Accounts Receivable—Casey Klein (subsidiary) for $212.

5.Increases to revenue and liability accounts are recorded as credits. Credit Sales for $200 and Sales Tax Payable for $12.

T ACCOUNTS 6.Accounts Receivable Sales

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Recording Sales on Account (con’t.)Recording Sales on Account (con’t.)Business Transaction (con’t.)

On December 1 On Your Mark sold merchandise on account to Casey Klein for $200 plus sales tax of $12, Sales Slip 50.

Debit+

212

Credit+

200

Credit–

Debit–

Accounts ReceivableSubsidiary Ledger Sales Tax

Casey Klein Payable

Debit+

212

Credit–

Debit–

Credit+

200

Business Transaction (con’t.)

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Recording Sales on Account (con’t.)Recording Sales on Account (con’t.)

On December 1 On Your Mark sold merchandise on account to Casey Klein for $200 plus sales tax of $12, Sales Slip 50.

JOURNAL ENTRY 7.

Sales Returns and AllowancesSales Returns and Allowances

Any merchandise returned for

credit or a cash refund is called a

sales return.

A price reduction granted for

damaged goods kept by the

customer is called a sales

allowance.

Any merchandise returned for

credit or a cash refund is called a

sales return.

A price reduction granted for

damaged goods kept by the

customer is called a sales

allowance.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

Sales Returns and Allowances (con’t.)Sales Returns and Allowances (con’t.)

A credit memorandum lists the details of a sales return or allowance.

A credit memorandum lists the details of a sales return or allowance.

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

The Sales Returns and Allowances AccountThe Sales Returns and Allowances Account decreases the total revenue earned

by a business; summarizes the total returns and

allowances for damaged, defective, or other otherwise unsatisfactory merchandise;

is a contra account.

decreases the total revenue earned by a business;

summarizes the total returns and allowances for damaged, defective, or other otherwise unsatisfactory merchandise;

is a contra account.

Sales Returns and Allowances

Debit+

Increase SideNormal Balance

Credit–

Decrease Side

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

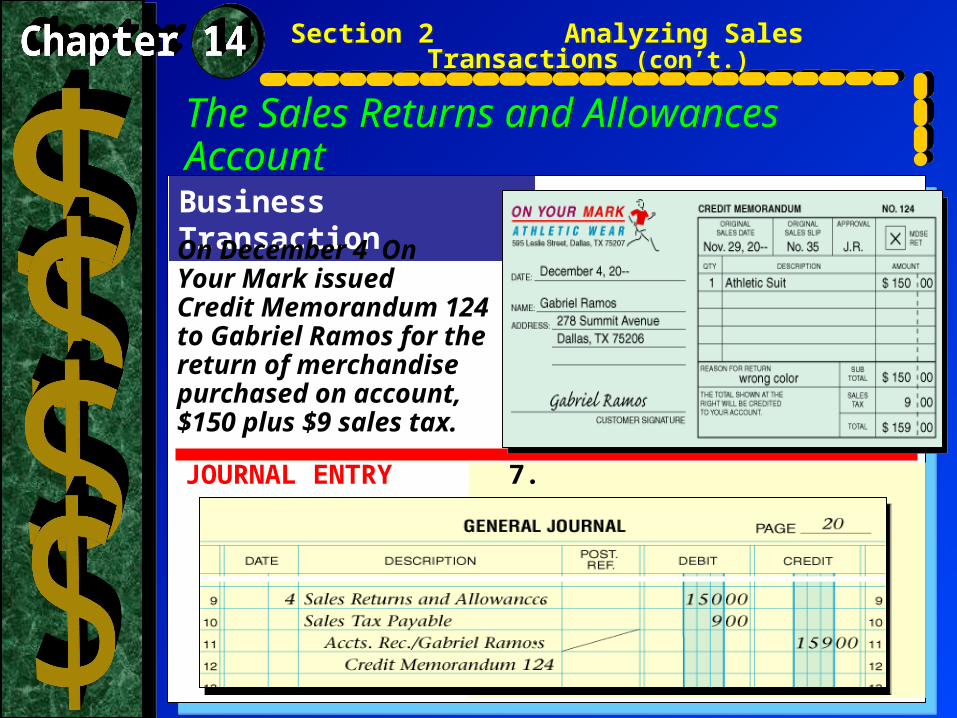

Business Transaction

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

On December 4 OnYour Mark issued Credit Memorandum 124 to Gabriel Ramos for the return of merchandise purchased on account, $150 plus $9 sales tax.

JOURNAL ENTRY 7.

The Sales Returns and Allowances AccountThe Sales Returns and Allowances Account

Check Your UnderstandingCheck Your Understanding

Businesses collect sales tax

from customers. In what account is

the sales tax recorded?

Businesses collect sales tax

from customers. In what account is

the sales tax recorded?

Section 2 Analyzing Sales Transactions (con’t.)Section 2 Analyzing Sales Transactions (con’t.)

![How to extend a Note Receivable - RIMSS · Note Receivable: C] Select All Loan Details Note Receivable -11 10/30/2018 $2,056.58 Check DC": Date 10/30/2018 10/30/2018 10/26/2016 12/1/2016](https://img.pdfslide.us/doc/110x75/60af4231804ddb489a2cde92/how-to-extend-a-note-receivable-rimss-note-receivable-c-select-all-loan-details.jpg)