Embed Size (px)

Citation preview

SEARS – THE NEXT ZERO BY 2020

THE OPEN UNIVERSITY OF HONG KONG

TONG CHO YI JOEL

WAN FUNG STEPHEN

WONG SUN WING SIMON

FEBRUARY 20, 2015

1

Table of Contents

Introduction .................................................................................................................... 2

Ways to survive ............................................................................................................... 4

1.1 Transformation to brick-and-click retailing helps Sears? ................................ 4

1.2 Transformation to member-centric retailing helps Sears? ............................... 5

1.3 Can Sears survive in brick-and-mortar retailing industry? .............................. 6

1.4 Can we trust Sears corporate leaders in bringing the company to survive? .... 7

1.5 Can Sears bring in the right management talents? ......................................... 10

Financial Analysis ........................................................................................................ 11

2.1 Liquidity ......................................................................................................... 12

2.2 Profitability .................................................................................................... 14

2.3 Long-term Solvency....................................................................................... 16

Why Sears will not be acquired by others? .................................................................. 18

Conclusion ................................................................................................................... 20

Appendix ...................................................................................................................... 24

2

Introduction

Sears Holdings, one of the largest department stores retailers in the past, is now facing

a potential bankruptcy. A growing number of reports and commentaries in the past

discussed the possibility for Sears to be filed for Chapter 11. However, Sears seems

immortal and has been surviving until now, which has disappointed a number of

financial analysts. Can Sears keep running until 2020 and after?

In our report, we will explore the possible ways for a traditional retailer to survive in

the new and ever-changing business environment, and then point out the infeasibility

of those ways for Sears by studying its company strategies and organizational

structure. A brief financial analysis also provided to show the solvency problem of the

firm. Lastly, a study on Sears’ financing policy will be used to illustrate the reason

why Sears will become zero value in 5 years.

3

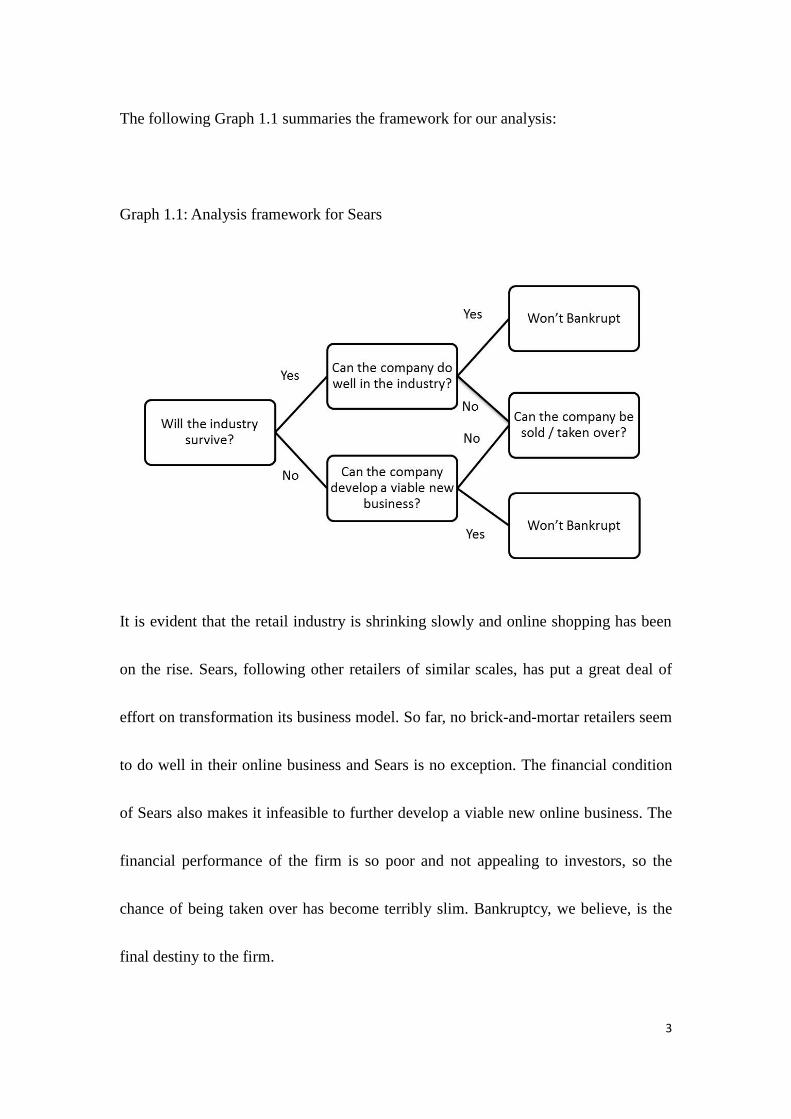

The following Graph 1.1 summaries the framework for our analysis:

Graph 1.1: Analysis framework for Sears

It is evident that the retail industry is shrinking slowly and online shopping has been

on the rise. Sears, following other retailers of similar scales, has put a great deal of

effort on transformation its business model. So far, no brick-and-mortar retailers seem

to do well in their online business and Sears is no exception. The financial condition

of Sears also makes it infeasible to further develop a viable new online business. The

financial performance of the firm is so poor and not appealing to investors, so the

chance of being taken over has become terribly slim. Bankruptcy, we believe, is the

final destiny to the firm.

4

Ways to survive

1.1 Transformation to brick-and-click retailing helps Sears?

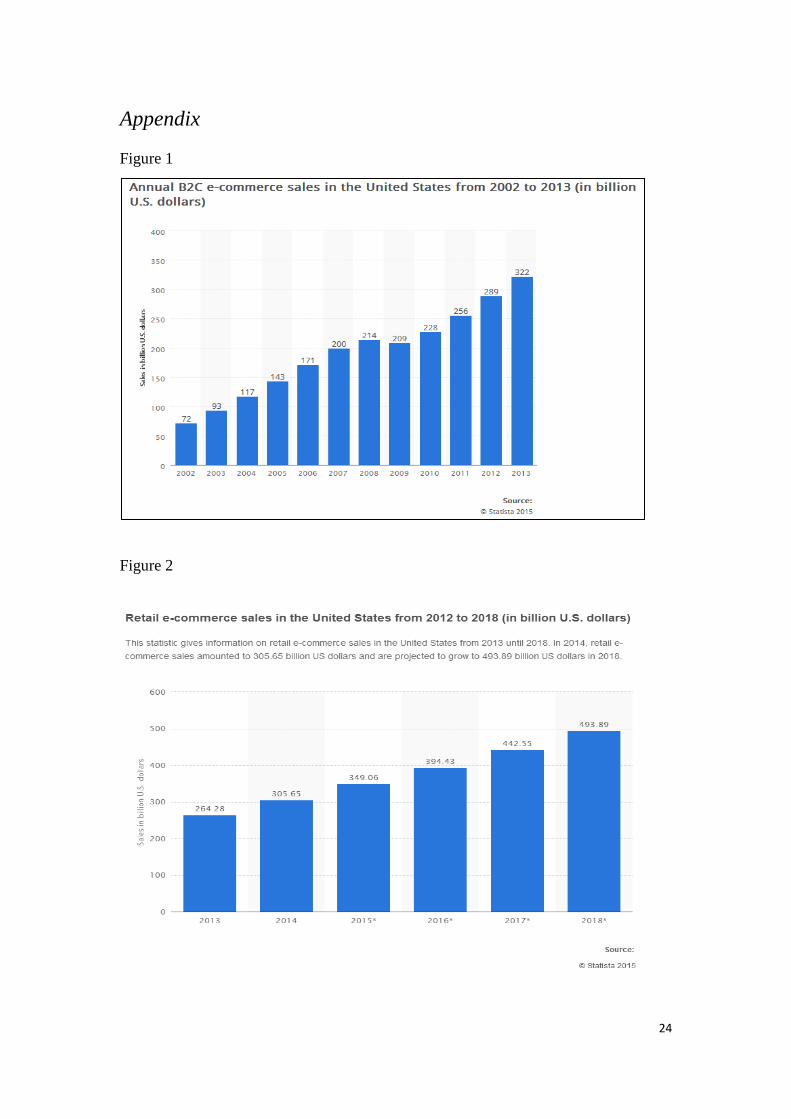

E-commerce has been growing quickly. According to the findings from Statista,

e-commerce sales in U.S. has an upward trend from 2000 to 2013 (Figure 1) and it

will continue in future (Figure 2). The rapid development of e-commerce has eaten

traditional retail market and many retailers are considering switching to e-commerce

to survive. Sears has a strategy of shifting its massive brick-and-mortar presence to

e-commerce since 1999.

Argument

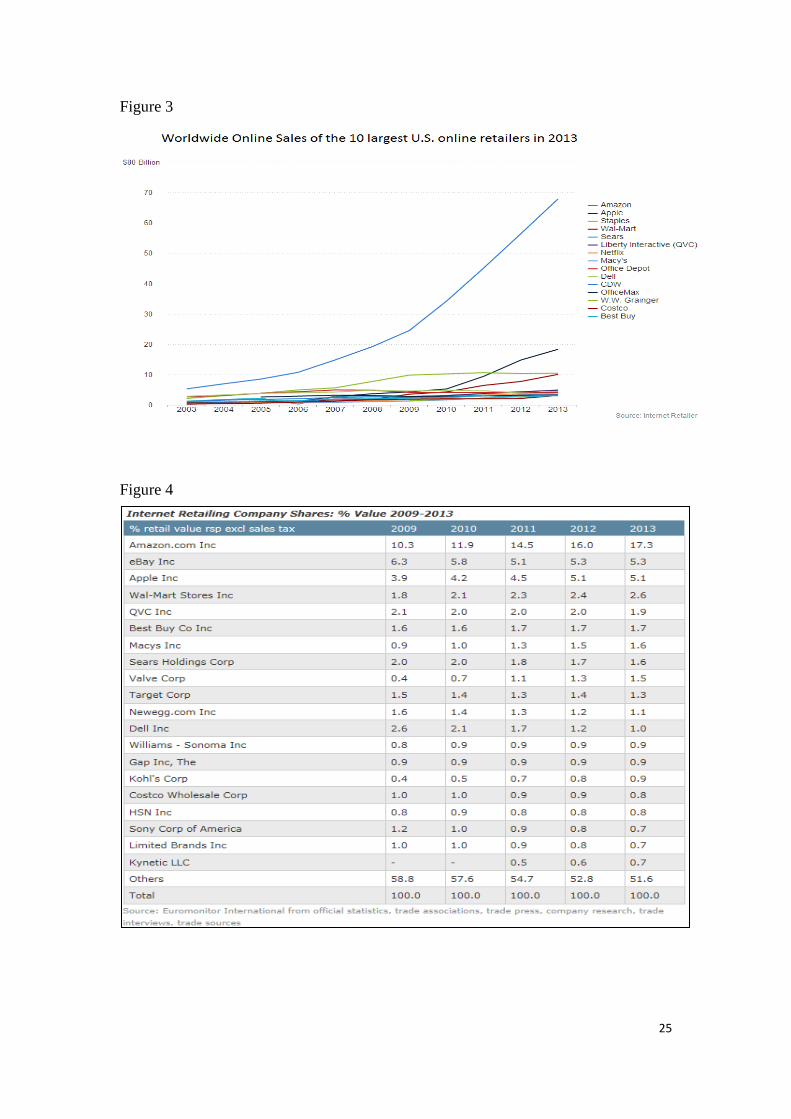

It is not easy for companies to turn store-based into brick-and-click retailing

successfully. According to research from Internet Retailer, no brick-and-mortar

retailer, including Staples, Wal-Mart and Sears, has substantial growth in online sales

after their transformation. Only Amazon, the traditional e-commerce company, has

rapid growth in online sales. (Figure 3)

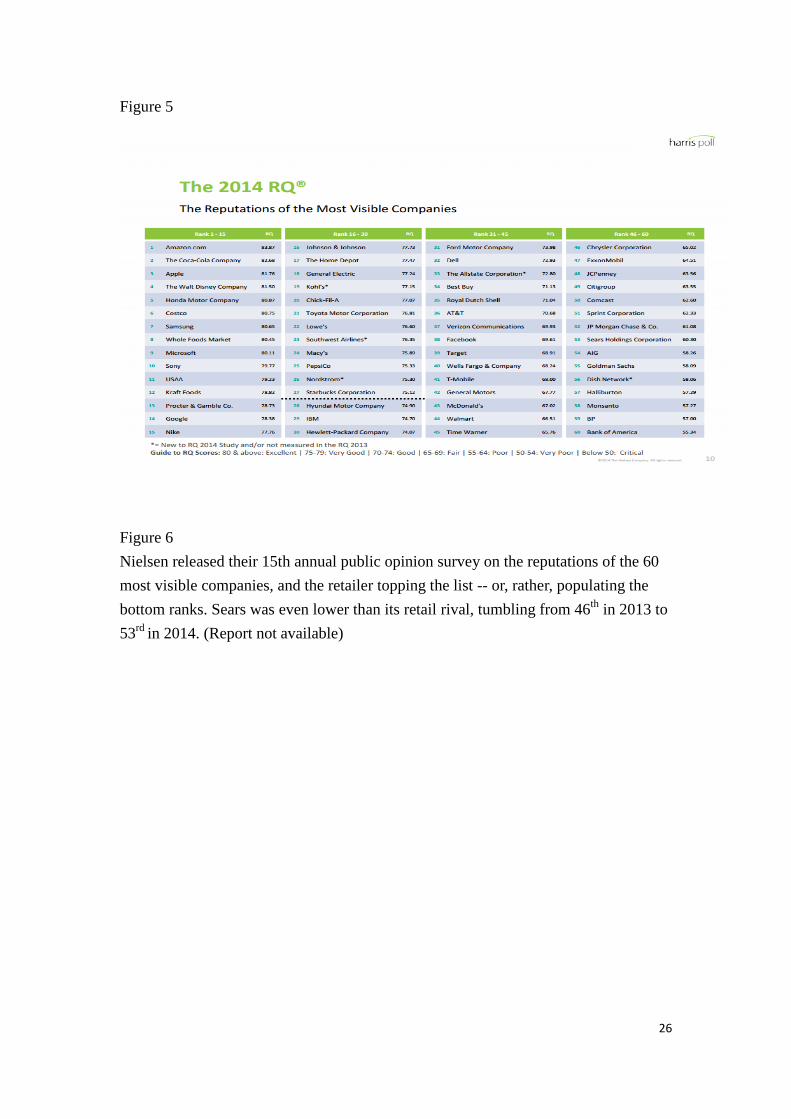

The reason why traditional retailers fail to compete in the cyber frontier is that

e-giants like Amazon has strong brand loyalty in the e-commence area. They create

customer value, from reliable and stable site to user-friendly interface, which

5

traditional retailers are hard to complete. Besides, Amazon has a strong e-commence

network and links itself to Yahoo!, Excite and AOL.com and patent on ‘one-click’

shipping procedure. As a result, traditional retailers like Sears faces difficulty in

gaining on-line retail market share. The dominating market share in internet retailing

captured by Amazon support our argument (Figure 4).

1.2 Transformation to member-centric retailing helps Sears?

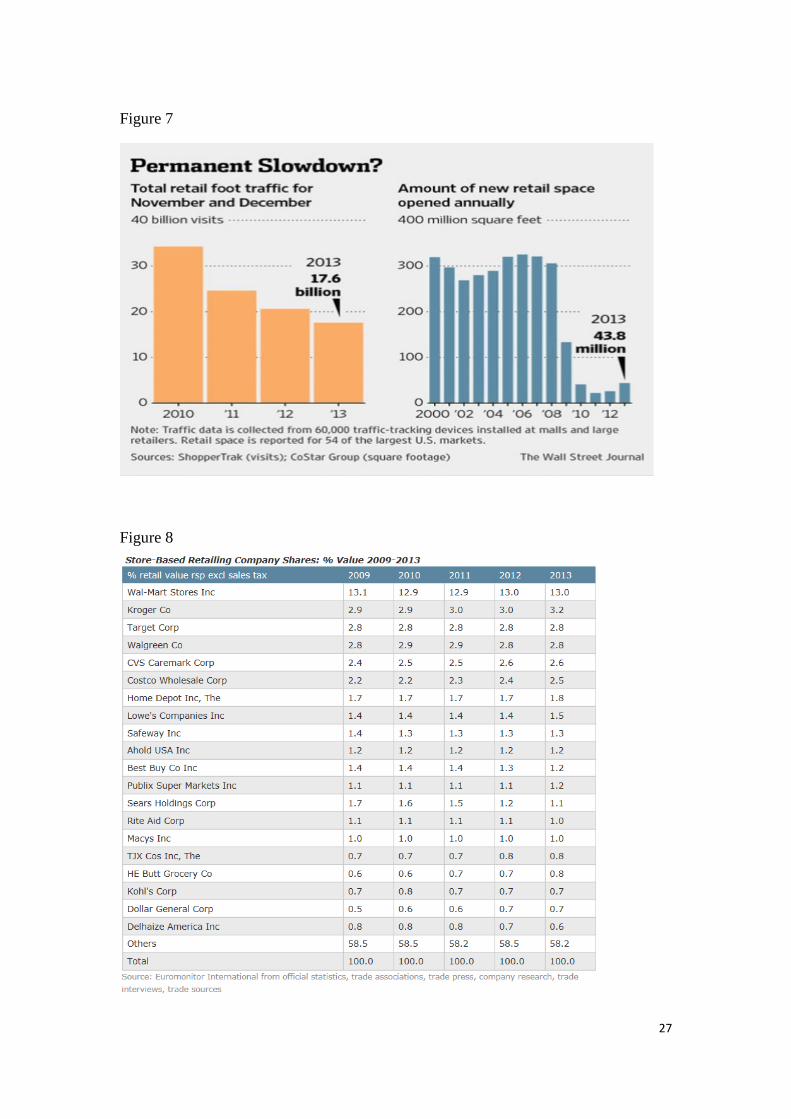

Sears is losing its reputation, according to Nielsen 15th annual public opinion survey

in 2014 (Figure 5 and 6). Customer-centric, which detects the customers need and

uses the resources according, is one of the successful factors of Amazon’s good

reputations according to the survey. If Sears can develop a differentiated

member-centric approach, it may survive. Therefore, Sears is moving away from

product-centric to a member-centric business model, which focuses on providing

benefits to members.

Argument

To achieve customer oriented strategy, Sears has launched Shop Your Way loyalty

program to develop a member-driven social commerce platform across web and

mobile channels. However, the characteristics of Shop Your Way program fail to

6

differentiate itself from others loyalty program such as Target’s RED card and Macy's

Star Rewards.

According to Sears’ FY2013 fourth-quarter report, the firm has its twenty-eighth

consecutive quarter decline in sales, even though it attempted a turnaround by its Shop

Your Way loyalty program in 2009. This shows that the loyalty program cannot turn

the company around.

Member-centric retailing emphasizes building long-term relationship with shoppers.

However, Sears had low credibility that it alleged in selling the private information of

the credit card customers to third party vendors such as Memberworks, Cendent and

Encore Marketing for profit (Bovay et al. v. Sears, Roebuck & Co). The incident

caused a reduction in the number of loyal customers and undermined Sears’

competitiveness.

1.3 Can Sears survive in brick-and-mortar retailing industry?

Sears can no longer grow in brick-and-mortar retailing industry following to the

general declining trend in retail business. Store-based retailers are facing challenges

from e-retailing. According to ShopperTrak, foot traffic in stores has declined from

7

2010 to 2013 (Figure 7). Based on Euromonitor International statistics, companies in

brick-and-mortar retailing industry have no significant growth. Some retailers like

Sears has a drop in retailing shares from 2009 to 2013 (Figure 8).

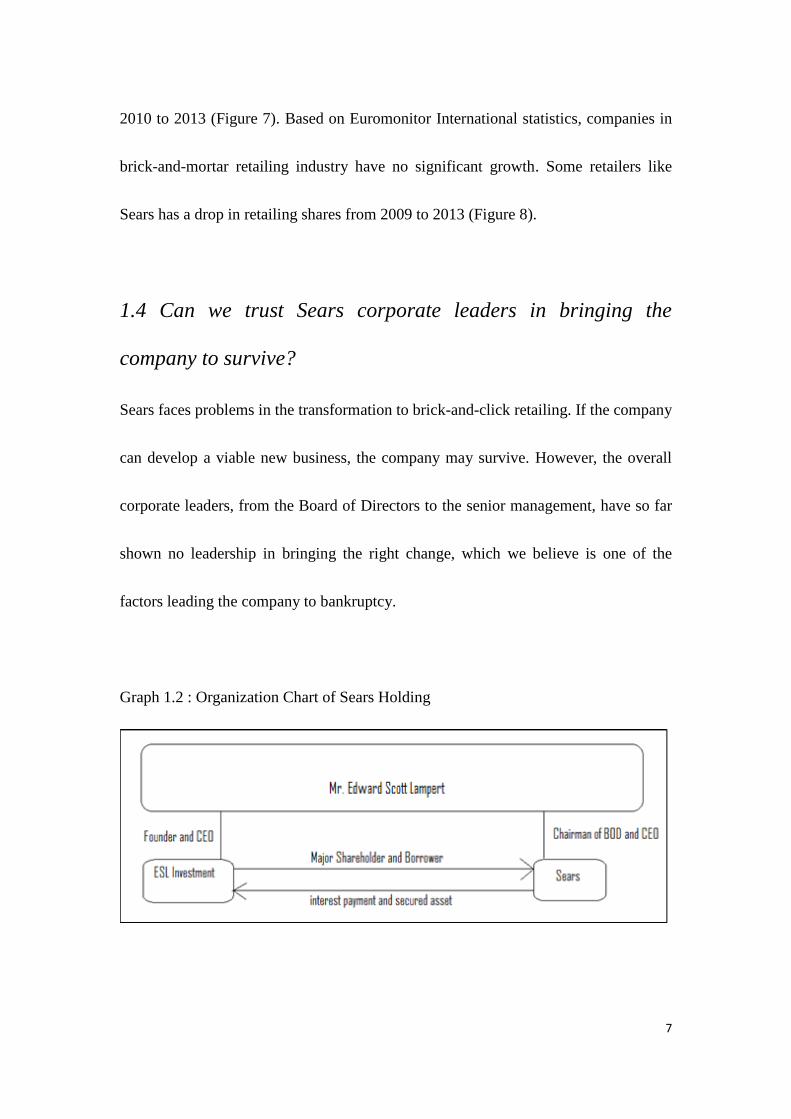

1.4 Can we trust Sears corporate leaders in bringing the

company to survive?

Sears faces problems in the transformation to brick-and-click retailing. If the company

can develop a viable new business, the company may survive. However, the overall

corporate leaders, from the Board of Directors to the senior management, have so far

shown no leadership in bringing the right change, which we believe is one of the

factors leading the company to bankruptcy.

Graph 1.2 : Organization Chart of Sears Holding

8

1.4.1 Potential Conflict of Interest

From the Board of Directors, the dual status of Edward S. Lampert enables him to

operate Sears for his own interest rather than the long-term benefit of the company

(Graph 1.2). Being the major shareholder and the main source of funding of Sears,

Edward S. Lampert, who acts as the Chairman of the Board of the Directors and the

CEO of Sears, is also the founder and CEO of ESL Investment.

In the latest $400 million borrowing, the estimate value of the secured asset for such

borrowing is much more than $400 million. In other words, this is unlikely to be an

arm-length transaction, and Mr. Lampert is expected to gain a lot if Sears defaults on

repayment. Besides, starting from last year, Edward S. Lampert changed the form of

his loan to the company, from unsecured to secure. This change may imply loss of

confidence of Lampert in the Company.

1.4.2 Change for Worse

For the senior management, the co-operate leaders of Sears are short-sighted, which

limits the profitability of the company. The competitive advantage of Sears depends

on the value creation of exclusive brand and valuable real estate. However, the

management makes the wrong decision that allows the products of profitable and

9

exclusive brands like Kenmore and Craftsman sold in other retail stores, which has

weakened the competitiveness of Sears.

Besides, Sears sold most of its beneficial company real estate including the valuable

stores in Cupertino, California which cost$102.5 million and left very few other assets

to sell. Sears lost its strong pillars to generate the cash flow in the long term.

Sears management lacks the vision for the future development. The declining

operation performance can be regarded as the indicator for the above analysis.

1.4.3 High Turnover of Senior Management

The rapid replacement of key senior executives makes Sears face the difficulty in

setting goals and strategic direction, which affects the consistency of strategy and

creation of the long term planning. For Instance, Imran Jooma, who acted as the

Executive Vice President in charge of online, marketing, pricing and financial services

from 2011, left the company in February 2015.Employees need to modify themselves

for the new organizational behaviors, which may lead to the negative impact on the

employee morale and the performance.

To conclude, the incapacity of the corporate leaders and the frequency change in key

10

management personnel limits the company to develop a viable new business.

1.5 Can Sears bring in the right management talents?

Evidence has shown that it is difficult for Sears to attract talented business leaders in

order to change.

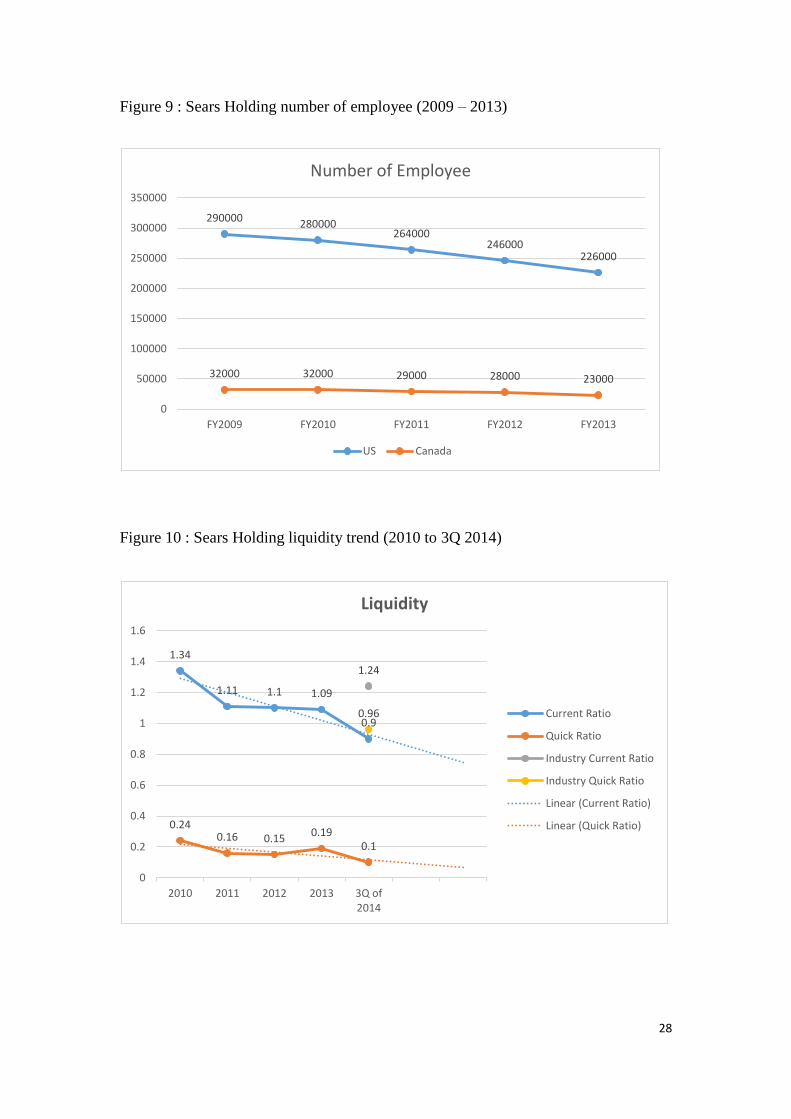

According to the annual report, Sears faces the decline of employees in both the

United States territories and Sears Canada (Figure 9). The number had dropped 22%

from 2010 to 2014. The annual report also reveals that most of the executive officers

were appointed within the last 5 years. This reflects that the turnover rate of staff has

been relatively high.

Sears faces the serious debt problem and it is difficult for the company to offer

attractive packages for talented business leaders to join.

On the other hand, the new talented business leaders find themselves difficult to

develop their career as the continuous shrinkage of store network and the integration

of the online operations.

11

In short, the declining reputation of Sears greatly reduces its appeal to potential talents.

This causes the vicious cycle.

Financial Analysis

In this part, we will use financial statements’ figures to assess the probability of

bankruptcy for Sears. Trend analysis will be used for future performance prediction

and industry average data will be used to evaluate the performance of Sears in the

industry.

To achieve a more comprehensive conclusion, we will focus on 3 aspects:

(1) Liquidity : to assess company’s ability to repay current debt

(2) Profitability : to assess the ability in generating profits

(3) Long-Term Solvency : to assess the future financial burden of the company

12

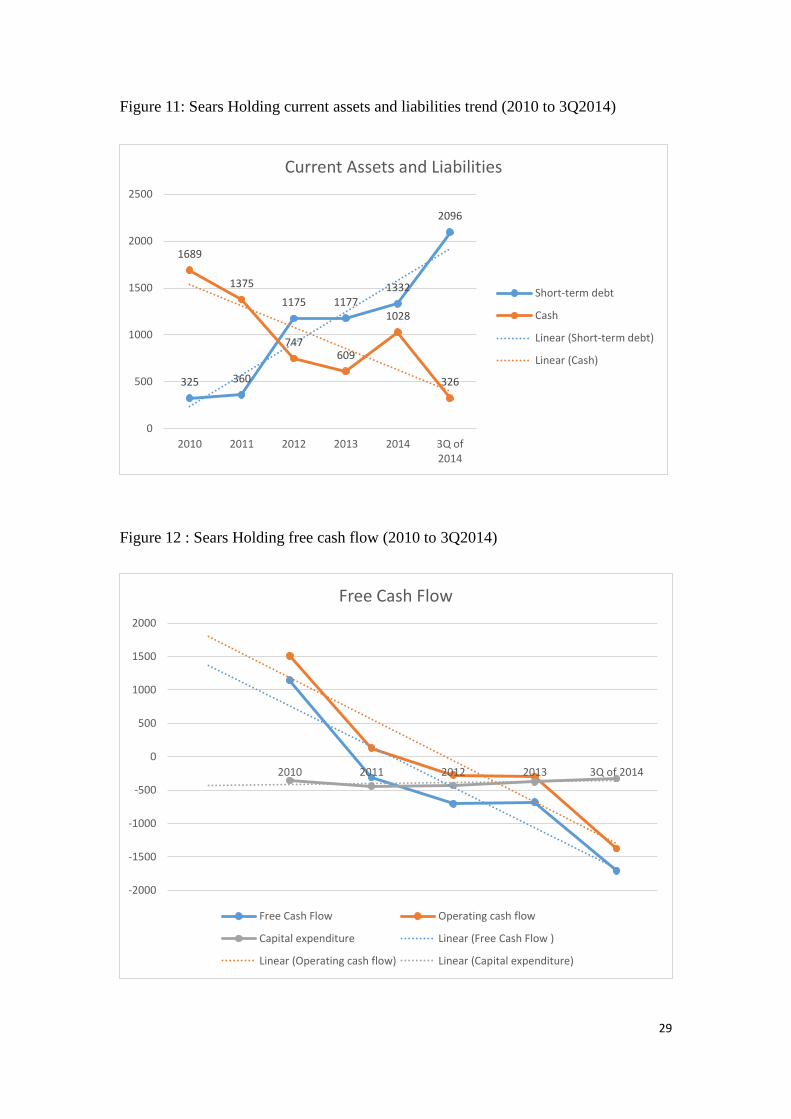

2.1 Liquidity

Current ratio: A dynamic drop about 30% from 1.3 in FY2010 to 0.96 in 3rd

quarter

2014 (Figure 10), which is much lower than 1.24 industry average. The decrease is

due to the huge increase in short-term debt, from USD$869 million in FY2010 to

USD$2,171 million in latest quarter(Figure 11), 140% on average for each year,

resulting in an upward trend in borrowing but a downward trend in cash, from

USD$1,689 million in FY2010 to USD$326 million in latest quarter (Figure 11). One

possible reason for the inverse relationship is the continuous yearly loss, and the

company seems to fail in generating cash-flow from operating activities so the

company initiates cash flow from investing or financing activities, such as the

$USD994 million from short-term borrowing and $USD996 million from disposal of

PPE in FY2013. It implies that the current assets of the company are insufficient to

cover current liabilities, and Sears needs to borrow to finance its operation. That

create huge pressure to the firm in handling debt repayment and Sear may choose to

default its debt in the end.

Quick Ratio: It decreases from 0.24 in FY2010 to 0.1 in 3th

quarter 2014 (Figure 10),

and the performance is below the industry average of 0.9. The decrease due to the

cash burn under decreasing losses, and the divergence between quick ratio and current

13

ratio may be the result of the high stock level which is 85% of all current assets. Such

poor quick ratio put Sears’s liquidity in a very dangerous position.

Stock turnover rate: With 85% of the current assets as inventory, the company has a

lower stock turnover ratio of 3.38, which is lower than the 9.32 industry average. It

indicates the lower efficiency to turn inventory into more liquid assets such as account

receivables or cash, and this further lower the liquidity position.

Receivables and Payables Period: During the recent years, both receivables and

payables remind stable at around 60 days and 35 days respectively. However, a

company with receivable period longer than its payable period implies an inefficient

credit policy. When the rate of cash paid faster than that of those received, the

liquidity level is worsened.

The above ratios analysis show problems in company’s liquidity, which is a

detrimental factor lead to bankruptcy.

Cash flow: The company suffered from a huge decrease in free cash flow, from

USD$1,146 million in FY2010 to negative USD$1,709 million FY2013 (Figure 12).

14

The downward trend is mainly due to the increasing operation losses, from USD$297

million in FY2009 to negative USD$1,116 million in FY2013. The poor operating

efficiency pushes the company to sell its assets and raise debts to generate enough

cash for its daily operation, such as the large cash inflow from disposal of assets of

$USD995 million and long-term borrowing of $USD994 million in FY2013 (Figure

13).

To conclude, we are pessimistic about the liquidity of Sears and expect the ability in

repayment of debt is much lower than the acceptable level, increasing the risk of

bankruptcy.

2.2 Profitability

Revenue growth: There is a decreasing trend for the revenue (Figure 14), from

$USD44,043 million in FY2010 to $USD36,188 million in FY2013, negative 3.6%

per year on average. This result shows that the transformation of Sears is not

successful, and the decrease in revenue may continue if there is no turnaround

strategy to improve the situation.

The gross profit margin deceases from 27.7% in FY2011 to 24.2% in FY2013, which

15

match with the decreasing trend of the industry and indicate that the market is

shrinking. In the annual report, the company further states the decrease is also due to

theextra discount for customer under the new customer-oriented program. Thus, under

this new strategy, a lower gross profit margin is expected since the revenue per good

decreases, unless the company has a greater cost control.

The negative net profit margin is increasing from -2.33% in FY2012 of total revenue

to -5.6% in the travelling twelve months ended Feb 2015. When comparing with the

industry average of 4.71%, the performance of Sears is much worse than its

competitors. Moreover, the selling and administrative cost is still at around 27-28% of

sales. This is unfavorable since Sears has tried to lower these costs by shutting down

stores and labor cut, and it seems the cost control is not as effective as expected.

Moreover, Sears has declared dividend of $USD 476 million in the FY2013 even the

company was making since FY2011. This may shows that the management is not

acting at the interest of Sears.

The downward trend of revenue and profit shows that the new strategies of Sears are

16

not as successful as expected. There is also a doubt that whether the business can be

sustained.

2.3 Long-term Solvency

The unusual gearing ratio of 41.17 of the latest quarter indicates the company highly

relies on debt financing. There will then be problems of large interest payment and

debt repayment. This problem is also reflected on the negative interest coverage of

-9.19 in the travelling twelve months.

In FY2009, total assets value was $USD 24,808 million while the total liabilities

amount to $USD15,712 million, with assets to liabilities ratio of 1:58 to 1. However,

as the company keeps selling the PPE, the assets value records a decreasing trend and

declines by about 26% to $USD18,261 million in FY2013, while the total liabilities

increases to $USD16,522 million, resulting in a ratio of 1.11 to 1. With the lower asset

to liabilities ratio, the assets may not cover the liabilities in future, especially when

there are impairment for intangible assets and the continuous disposal of PPE.

Price to book ratio: The ratio in FY2013 is 33.2, showing that the valuation is much

higher than the book value of the company. This situation is unusual especially for a

17

retailing company recorded losses in the recent years. That reflects Sears is much

expensive than its retail peers such as Wal-Mart and Costco.

The above financial analysis shows that Sear is facing a serious problem in current

debt repayment. This problem cannot be easily solved since there is a trend of

decreasing profit margin and revenue, which indicates the company cannot generate

profit. More importantly, the over-dependence on debt financing creates a huge

amount of future repayment of debt, which will negatively affect the liquidity.

Therefore, if the profitability cannot be improved as predicted in the opening section,

the chance of Sear’s bankruptcy will increase,

18

Why Sears will not be acquired by others?

In fact, even for some companies which did not operate well, they still avoided

bankruptcy because of acquisition. However, we do not expect it will take place in

Sears due to several reasons.

Firstly, the company keeps making loss starting from 2012, and this loss is expected

to be long-lasting due to the trend and the business environment. For a company that

cannot bring profit, acquisition seldom takes place since the acquirers always look for

an expected positive return from the action.

Secondly, there is not much valuable intangible asset left in Sears. Some acquisitions

may still take place even if the acquiree was making a loss, since there are valuable

assets remaining which can bring competitive advantages. For example, Motorola’s

patents helped finalize the acquisition from Lenovo. However, in Sears, the main

intangible asset came from the Kmart’s acquisition, which was impaired in the recent

years, and there are not many unique intangible assets, which can bring benefits to the

acquirer, in Sears.

Thirdly, the gearing ratio is extremely high. For acquisition to take place, the

19

company should not bear much debt. Otherwise, the other interested companies may

not take the step since there are high risks to take a huge amount of debts.

Can new financing be obtained?

Companies which keep making loss may still stay alive by borrowing money to

finance and last for several more years. However, for Sears, we do not expect this

situation since there is a doubt whether it can obtain sufficient funding to finance the

debt repayment and operation, due to the over-dependence on the shareholders and the

low creditability, and, more importantly, a substantial amount of repayment in 2018.

In order to achieve the $1 billion additional capital target for 2014, the company had

to borrow $400 million from the major shareholder, ESL Investment, while another

$665 million comes from the spin-off the business and selling of assets. On the other

hand, the credit rating of the company has been downgraded from CC to CCC in

2014.

Moreover, a huge amount of long-term debt has been issued during the year, resulting

in a future repayment of above $2 billion due 2018, which is just 3 years away from

now. There is then a hard situation for Sears to pass in 2018.

20

To conclude, the above facts show that there is problem on credibility for the company.

Along with the analysis showing the declining profitability and liquidity, Sears may

be unable to repay the short-term debt, especially a huge amount of $USD2.2 billion

in 2018.

Conclusion

Bankruptcy is the only fate for Sear and it is very likely to take place no later than

2020.

21

Reference

Tears for Sears: American icon in trouble (2012). CNN Money. Retrieved February 19,

2015 from

http://money.cnn.com/2012/01/12/markets/thebuzz/

Berr, J. (2013). Five Companies That May Not Survive Past 2014.In The Fiscal Times.

Retrieved February 19, 2015 from

http://www.thefiscaltimes.com/Articles/2013/12/27/Five-Companies-May-Not-Surviv

e-Past-2014

Retail e-commerce sales in the United States from 2012 to 2018 (in billion U.S.

dollars) (2015). Statista. Retrieved February 18, 2015 from

http://www.statista.com/statistics/183750/us-retail-e-commerce-sales-figures/

Annual B2C e-commerce sales in the United States from 2002 to 2013 (in billion U.S.

dollars) (2015). Statista. Retrieved February 18, 2015 from

http://www.statista.com/statistics/271449/annual-b2c-e-commerce-sales-in-the-united-

states/

Amazon Bests Competitors in Online Slaes (2013).The Wall Street Journal. Retrieved

February 20, 2015 from

http://www.wsj.com/news/interactive/WEBFAILB050214?ref=SB1000142405270230

3417104579544080308837964

Internet Retailing in the US (2014). Euromonitor International. Retrieved February 18,

2015 from

http://www.portal.euromonitor.com.ezproxy.lib.ouhk.edu.hk/portal/analysis/tab

The Harris Poll 2014 A Survey of the U.S. General Public Using the Reputation

Quotient (2014). The Nielsen Company. Retrieved February 19, 2015 from

http://www.nielsen.com/content/dam/corporate/us/en/reports-downloads/2014%20Re

ports/harris-poll-2014-rq-summary-report.pdf

Ries, A. (2012). The Best Bet for Sears? Ditch Its Softer Side. In Advertising Age.

Retrieved February 18, 2015 from

http://adage.com/article/al-ries/bet-sears-ditch-softer-side/232678/

22

Retailing in the US (2014). Euromonitor International. Retrieved February 18, 2015

from http://www.portal.euromonitor.com.ezproxy.lib.ouhk.edu.hk/portal/analysis/tab

Reents, R. (2014). Closing Up Shop: Sears Has No Brand Identity. In CBD Marketing.

Retrieved February 18, 2015 from

http://www.cbdmarketing.com/about/blog/sears-has-no-brand-identity/#sthash.Ngy1

MK29.hvEyjnuy.dpbs

Wahba, P. (2014). Sears CEO Lampert explains why he closed 200 stores. In Fortune.

Retrieved February 18, 2015 from http://fortune.com/2014/12/15/sears-ceo-lampert/

Kenneally, I. (2014). Sears Q4: 28th Consecutive Quarterly Loss; Cost-Cuts and Asset

Sales Soften the Blow. In Sourcing Journal. Retrieved February 18, 2015 from

https://www.sourcingjournalonline.com/sears-q4-28th-consecutive-quarterly-loss-cost

-cuts-asset-sales-soften-blow-ik/

eCommerce Disruption: A Global Theme / Transforming Traditional Retail (2013).

MORGAN STANLEY RESEARCH Global. Retrieved February 20, 2015 from

http://www.academia.edu/6554203/eCommerce_Disruption_A_Global_Theme_Trans

forming_Traditional_Retail

Sears CEO Lampert has failed to revive dying company

The Buffalo News. Retrieved February 20, 2015 from

http://www.buffalonews.com/business/sears-ceo-lampert-has-failed-to-revive-dying-c

ompany-20141116

Sears Privacy Litigation

http://www.searsprivacyclassaction.com/

Sears shares plunge after it borrows $400M from its own CEO

CBC News. Retrieved September 17, 2014 from

http://www.cbc.ca/news/business/sears-shares-plunge-after-it-borrows-400m-from-its-

own-ceo-1.2769407

23

Sears Holdings' marketing president to resign

Direct Marketing News. Retrieved November 03, 2011 from

http://www.dmnews.com/sears-holdings-marketing-president-to-resign/article/215953

/

Leader of Online Operations for Sears Holdings Resigns

The New York Times. Retrieved December 24, 2014 from

http://www.nytimes.com/2014/12/25/business/leader-of-online-operations-for-sears-h

oldings-resigns.html?_r=1

Sears holdings corporation.

Annual report

http://searsholdings.com/invest/financial_info.htm

Growth, Profitability, and Financial Ratios for Sears Holdings Corp (SHLD) from

Morningstar.com

http://financials.morningstar.com/ratios/r.html?t=SHLD

Sears Holdings Corp (SHLD.O) Analysts.

Reuters.com.

http://www.reuters.com/finance/stocks/analyst?symbol=SHLD.O

24

Appendix

Figure 1

Figure 2

25

Figure 3

Figure 4

26

Figure 5

Figure 6

Nielsen released their 15th annual public opinion survey on the reputations of the 60

most visible companies, and the retailer topping the list -- or, rather, populating the

bottom ranks. Sears was even lower than its retail rival, tumbling from 46th

in 2013 to

53rd

in 2014. (Report not available)

27

Figure 7

Figure 8

28

Figure 9 : Sears Holding number of employee (2009 – 2013)

Figure 10 : Sears Holding liquidity trend (2010 to 3Q 2014)

290000 280000

264000 246000

226000

32000 32000 29000 28000 23000

0

50000

100000

150000

200000

250000

300000

350000

FY2009 FY2010 FY2011 FY2012 FY2013

Number of Employee

US Canada

1.34

1.11 1.1 1.09

0.9

0.24 0.16 0.15

0.19 0.1

1.24

0.96

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

2010 2011 2012 2013 3Q of2014

Liquidity

Current Ratio

Quick Ratio

Industry Current Ratio

Industry Quick Ratio

Linear (Current Ratio)

Linear (Quick Ratio)

29

Figure 11: Sears Holding current assets and liabilities trend (2010 to 3Q2014)

Figure 12 : Sears Holding free cash flow (2010 to 3Q2014)

325 360

1175 1177 1332

2096

1689

1375

747 609

1028

326

0

500

1000

1500

2000

2500

2010 2011 2012 2013 2014 3Q of2014

Current Assets and Liabilities

Short-term debt

Cash

Linear (Short-term debt)

Linear (Cash)

-2000

-1500

-1000

-500

0

500

1000

1500

2000

2010 2011 2012 2013 3Q of 2014

Free Cash Flow

Free Cash Flow Operating cash flow

Capital expenditure Linear (Free Cash Flow )

Linear (Operating cash flow) Linear (Capital expenditure)

30

Figure 13: Sears Holding cash flow components (2010 to 2014)

Figure 14: Sears Holding revenue trend (2010 to 2014)

-4000

-3000

-2000

-1000

0

1000

2000

2010 2011 2012 2013 2014

Cash Flow Components

Net income Cash flow from PPE Long-term debt issued Cash dividends

44043 43326

41567

39854

36188

30000

32000

34000

36000

38000

40000

42000

44000

46000

2010 2011 2012 2013 2014

Revenue