Embed Size (px)

Citation preview

2012Integrated Annual Report for the year ended 31 March

This report provides an overview of

Telkom’s business activities including

all operating subsidiaries, based on

reporting segments for the year ended

31 March 2012. It details the Group’s

fi nancial statements and looks ahead

at the Group’s prospects for the next

fi nancial year. The previous reporting

period for the period ended 31 March

2011 was covered in the 2011 Telkom

Integrated Annual Report.

This report includes an overview of

the business operations as well as

the fi nancial statements relating to

the Group’s activities over the period.

It has been prepared in accordance

with the Global Reporting Initiative 3

guidelines and represents a balanced

and reasonable presentation of Telkom’s

economic, environmental and social

performance.

While this document is designed to be

an integrated report, a more focused

description of Telkom’s sustainable

development activities can be found

on pages 68 to 111 for easier access

and increased clarity on certain of our

core sustainability issues. This section

includes data and information based

only on operations within the Republic of

South Africa for the year ended 31 March

2012. The South African operating

subsidiaries Swiftnet (Pty) Limited

(trading as Fastnet Wireless Service) and

Trudon (Pty) Limited have been included

in the 2012 sustainability section of this

report with respect to information relating

to climate change and greenhouse gas

emissions, water consumption, human

capital management, and occupational

health and safety.

The data relating to the Broad-Based

Black Economic Empowerment

(B-BBEE) score card also refl ects data

from the previous reporting cycle as the

current BEE review and certifi cation will

only take place following the completion

of the 2012 reporting period.

SCOPE OF REPORT

Integ

rated A

nn

ual R

epo

rt for th

e y

ea

r en

de

d 3

1 M

arc

h 2

01

2

PAPERSTOCK

COVER: PRINTED ON

Magno Satin 350gsm

INTERNAL PAGES

Printed front 135gsm Triple Green Silk

Printed back 115gsm Triple Green Silk

www.telkom.co.za

GRI and King III

1 Connecting with our stakeholders

2 Mission, vision and values

3 Strategy for 2012 – 2013

4 The year at a glance

6 Telkom shareholding at

31 March 2012

7 Telkom Group segment structure

8 Chairman’s message

12 Message from the Group Chief

Executive Offi cer

16 Board of Directors

18 Executive Committee

20 Industry overview

22 Business review

31 Awards and achievements

32 Integrated performance indicators

36 Financial overview

49 Governance

58 Enterprise risk management

66 Risk factors

68 Sustainability review

70 Group value added statement

72 Stakeholder engagement

76 Material sustainability issues

80 Human capital/our people

88 Occupational health and safety

95 Empowerment

96 Procurement

97 The Telkom Foundation

100 Environmental management

104 Product responsibility

113 Group fi nancial statements

280 Shareholders’ analysis

282 Defi nitions

283 Administration

CONTENTS

MA

KIN

G I

T SI

MPL

E

Forward looking statements

Many of the statements included in this document, as well as oral statements that may be made by us or by offi cers,

directors, prescribed offi cers or employees acting on behalf of us, constitute or are based on forward looking

statements.

All statements, other than statements of historical facts, including, among others, statements regarding our mobile

and other strategies, future fi nancial position and plans, objectives, capital expenditures, projected costs and

anticipated cost savings and fi nancing plans, as well as projected levels of growth in the communications market,

are forward looking statements. Forward looking statements can generally be identifi ed by the use of terminology

such as “may”, “will”, “should”, “expect”, “envisage”, “intend”, “plan”, “project”, “estimate”, “anticipate”, “believe”,

“hope”, “can”, “is designed to” or similar phrases, although the absence of such words does not necessarily mean

that a statement is not forward looking. These forward looking statements involve a number of known and unknown

risks, uncertainties and other factors that could cause our actual results and outcomes to be materially different

from historical results or from any future results expressed or implied by such forward looking statements. The

factors that could cause our actual results or outcomes to differ materially from our expectations include, but are not

limited to those risks identifi ed on page 66.

We caution you not to place undue reliance on these forward looking statements. All written and oral forward looking

statements attributable to us, or persons acting on our behalf, are qualifi ed in their entirety by these cautionary

statements. Moreover, unless we are required by law to update these statements, we will not necessarily update

any of these statements after the date of this document, either to conform them to actual results or to changes in

our expectations.

This is Telkom’s second integrated report and we continue to be guided

by the best practise offered to us in terms of compliance with the

Companies Act and King III. Telkom is aware of the need to improve

the service experience at every level and, since this report is one way

of doing just that, we hope to have provided you with a transparent

document that lays out the risks and opportunities that lie ahead as well

as a clear picture of how we are shaping and fulfi lling our strategies to

fi t an ever-evolving telecoms environment.

The guidance set out by King III states that companies should openly

portray the relevant risks, opportunities, governance processes and

strategies so that stakeholders can make better informed choices in

their dealings with the Company. We could not agree more and hence

we have laid out a clear structure and easy way for you to use this report

by referring to the sections listed on the inside fl ap of the cover.

There are also a number of references that we have included to make

it easier for you to refer to places of interest elsewhere in the report, or

ways in which you can access additional information.

Telkom SA Limited is the registered name of the organisation, however,

for ease of reference we have used either Telkom or “the Group” to

represent the Company and its group entities. All subsidiaries, business

divisions and products are referred to by their branded names for easy

recognition.

If you have any recommendations or suggestions as to how we can

improve on our reporting, please refer to the inside back cover of the

2012 Integrated Report for the appropriate contact details.

GRI and King III: refers the reader to an indicator used

in the application of the Global Reporting Initiative (GRI)

guidelines and King III

About this report

Connecting with our stakeholders

Organised labour

Dedicated forums to proactively and

continuously discuss and resolve issues relating

to our workforce.

We add signifi cant value to the South African

society and engage with our respective

stakeholders to ensure they are up to date

with developments in the Group while

simultaneously obtaining their feedback.

InvestorsKeeping investors

informed of the strategy, corporate governance,

operational and fi nancial performance as well as to gain

an understanding of their requirements and

expectations.

GovernorsBriefed regularly on issues of strategy

and Corporate Governance.

CustomersEnhance customer

satisfaction, retention and loyalty.

GovernmentRegular engagement

on policy issues.

Suppliers/partners

Regular meetings focusing onimproving the sourcing and

procurement process to ensure transparency

and fairness.

EmployeesDaily communications

regarding strategic, tacticaland operational issues.

The mediaNumerous briefi ng

sessions to inform the media and thus

the public.

Civil societyDedicated partnership programme funding or

sponsoring various projects across the country.

Telkom Integrated Annual Report 2012 1

2 Telkom Integrated Annual Report 2012

✔

Mission and vision

Connecting

NetworkingRelationshipsTechnologyCommunity

Personal applicationsMachines

People

Putting people fi rstCaring

CommunityEmployees

ShareholdersCustomers

(Business and consumers)

Seamlessly

Customer serviceConvenience

One-stopSimple

Cross-silo

To a better life

ProsperityCommerce/trade

EntertainmentEducation/health

EnvironmentGrowth and renewal

OUR VALUES

C ontinues improvement – Listen, act, learn, innovate.

H onesty – Be real, be open, be truthful.

A ccoutability – If it’s to be, it’s up to me.

R espect – Ensure dignity to all. Protect the environment.

T eamwork – Together we win.

VISION

Leading in the converged ICT market through deep and credible relationships and a distinctive customer experience.

Our vision includes:• Leading the provision of converged solutions.

• Providing a quality network with reach that is unmatched.

• Maintaining our leading brand promise in the business community.

• Creating innovative and pervasive broadband consumer services.

• Being the wholesale provider of choice in selected areas.

• Being the best place to work for, for committed and accountable people.

MISSIONSeamlessly

connecting people to a better life

2 Telkom Integrated Annual Report 2012

Telkom is one of Africa’s largest telecommunications companies, providing integrated communication solutions to both the business and consumer markets. We operate in nine different countries across Africa, with South Africa making up 98.9% of Telkom’s total revenue. We offer fi xed-line, mobile, ICT and data services and provide a wide range of products to suit our customers’ needs.

GRI and King III

Strategy for 2012 – 2013

Telkom Integrated Annual Report 2012 3

Strategy for 2012 – 2013

SHARP AND CLEAR STRATEGIC FOCUS

• Growing and defending profi table

Telkom Business revenues through

entry into high-growth adjacencies

focusing on convergence, value added

services and ICT offerings.

• Delivering on our investment in

Telkom Mobile by meeting the growing

data demand in South Africa and

providing a unique converged offering.

• Growing and defending profi table

revenues in Telkom Consumer Services

and Retail by increasing broadband

penetration in South Africa; while

strengthening our role as a content

aggregator.

• Transforming and upgrading the Telkom

network through the successful rollout of a

commercially-led, IP enabled network.

4 Telkom Integrated Annual Report 2012

The year at a glance

Our results for the year include an R896 million loss relating to the disposal of Multi-Links and an impairment loss of R569 million relating to iWayAfrica. Headline earnings per share declined 33.0% from the prior year. This is mainly as a result of the investment made in our mobile business as well as R605 million additional depreciation as a result of the review of the useful lives of existing network equipment as we invest to transform to a commercially led next generation network. This was partially offset by R739 million voluntary employee severance package costs included in the prior year.

Read more: for information on our fi nancial performance please see page 36

WEB: please visit www.telkom.co.za/ir

GRI and King III

Operating revenue (R million)

5 000

10 000

15 000

20 000

25 000

30 000

35 000

20122011

33 308 33 079

ADSL subscribers

200 000

400 000

600 000

800 000

1 000 000

20122011

751,625827,091

Cash flows from operating activities (R million)

5 188

5 892

1 000

2 000

3 000

4 000

5 000

6 000

20122011

Revenue generating mobile subscribers

300 000

600 000

900 000

1 200 000

1 500 000

20122011

473,604

1,483,401

Share performance 2011 2012 %

Number of ordinary share in issue shares 520,783,900 520,783,900 –

Weighted number of ordinary shares in issue shares 509,311,296 510,593,816 0.3

Headline earnings per share cents 484.8 324.7 (33.0)

Dividends per share cents 300.0 – (100.0)

Ordinary cents 125.0 145.0 16.0

Special cents 175.0 – (100.0)

Market capitalisation Rm 19,269 12,499 (35.1)

Number of ordinary shares traded ('000) 377,766 290,691 (23.1)

Highest price traded cents 39.10 38.49 (1.6)

Lowest price traded cents 32.85 24.00 (26.9)

Closing price at 31 March cents 37.00 24.00 (35.1)

Telkom Integrated Annual Report 2012 5

Revenue from mobile operations (R million)

200

400

600

800

1 000

1 200

20122011

81

1,200

Number of days lost due to injuries

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

20122011

6 970

3 505

Group revenue

Subscriptions and connections

Voice 34%

32%

21%

5%

4%

4%

Interconnection

Data

Mobile

Other and eliminations

EBITDA loss – mobile operations (R million)

1.1

2.2

0.5

1.0

1.5

2.0

2.5

20122011

Skills development (Points)

Achievable weighting

2008 2009 2010 2011

2

4

6

8

10

12

14

16 15

10.489.36 9.65

10.41

6 Telkom Integrated Annual Report 2012

Telkom shareholding at 31 March 2012

Government

39.8%The Government of the

Republic of South Africa is the largest shareholder in

Telkom.

Allan Gray

5.4%

Free fl oat

42.3%The free fl oat makes up the

remainder of the Group’s issued share capital and includes 11,573,158 shares held by 78,918 retail shareholders representing 2.2% of the

Group’s share capital.

Public Investment Corporation

10.5%The Public Investment Corporation (PIC) is an

investment management company wholly owned by the Government. It invests funds on behalf of public

sector entities.

Telkom treasury stock

2.0%Rossal No 65 (Pty) Limited and Acajou Investments

(Pty) Limited hold 2,046,528 shares (0.4%) and 8,143,556 shares (1.6%), respectively.

Read more: for the shareholder analysis please see page 280

GRI and King III

Telkom Integrated Annual Report 2012 7

Telkom operates in nine different countries across Africa, however, our core market is South Africa, contributing 98.9% in revenues.

The fi xed-line is our largest segment and consists of fi xed-line subscription and connection, traffi c, interconnection, data and internet services.

• Telkom Consumer Serving residential customers across South Africa, Telkom Consumer is a dedicated business unit within the Telkom Group. We provide voice and data services to customers in their homes, using Telkom’s national fi xed-line network.

• Telkom Business Telkom Business is the business unit dedicated to serving businesses of every type, industry and size in and outside South Africa. The businesses that we serve range from small and medium enterprises (SMEs) to large corporations, Government organisations and global enterprises. Positioned as the industry leader in telecommunications and ICT in South Africa, Telkom Business offers capability solutions across the technology spectrum.

• Telkom Wholesale and Networks Telkom Wholesale is South Africa’s leading provider of ICT wholesale facilities, services and solutions through our world-class network and ICT expertise. Telkom Wholesale enables customers to grow businesses by offering a variety of ICT wholesale products and solutions that are tailor-made to suit their needs.

We service any intermediary, which is licensed to provide ICT services to a third party. Our current client base includes mobile cellular operators, international ICT companies, services providers, fi xed-line operators and broadcasters, both locally and internationally.

The networks section provide and maintain all the required infrastructure which supports the revenue generating capability of the company.

• 8•ta 8•ta is an innovative mobile service provider that provides South African consumers and enterprises the ability to communicate wherever they are. Launched in October 2010, 8•ta uses state of the art Radio Access Network (RAN), core and IT technology to deliver products that are of high value, simple to use and of high quality.

• Telkom Business Mobile Telkom Business Mobile offers voice, data, messaging and value-added services to business customers.

Telkom Group segment structure

Telkom fi xed-line (revenue contribution: R30.6 billion)

Mobile (revenue contribution: R1.2 billion)

Other

South Africa International

• Trudon (64.9%) (revenue contribution: R1.2 billion) Trudon (Pty) Limited provides yellow and white page directory services, an electronic directory service, 10118 ‘The Talking Yellow Pages’ and an online web directory service.

• Swiftnet (wholly-owned subsidiary) (revenue contribution: R128 million) Swiftnet (Pty) Limited trades under the name FastNet Wireless Data Service. The FastNet suite of services include traditional connectivity services for point-of-sale, managed SIM services and customised wireless and wired Virtual Private Network Services which provide secure data transfer and backup to existing communication links at broadband speeds.

• Cybernest (revenue contribution: R1.4 billion) Our data centre offering consists of basic hosting where customers receive server rack and fl oor space, as well as cooling, power and backup power, managed and fully managed hosting and disaster recovery.

• Corporate Centre (revenue contribution: R78 million) This includes the Group’s human resources, procurement, legal, Corporate Governance, risk management, compliance, regulatory and fi nance functions. The revenue contribution relates mainly to revenue received by the Telkom Foundation from Telkom, that is eliminated on consolidation, as well as revenue from sale of materials.

• iWayAfrica Group (wholly-owned subsidiary) (revenue contribution: R368 million) iWayAfrica Group is an integration of Africa Online Limited and MWEB Africa Limited. With points of presence throughout sub-Saharan Africa, iWayAfrica Group provides customised solutions to Africa’s local, national, pan-African and multinational enterprises. iWayAfrica Group offers a hybrid of access solutions, specialising in both satellite and terrestrial access services to keep businesses connected to the world.

• Telkom International The Telkom International business unit is responsible for managing all subsidiaries.

Read more: for information on the business review please see page 22

WEB: please visit www.telkom.co.za

GRI and King III

Read more: for information on our fi nancial performance please see page 36

8 Telkom Integrated Annual Report 2012

Chairman’s message

It is an honour to be appointed as Chairman of the Telkom Board for a second term. I take the role of providing support and guidance to our stakeholders and to management very seriously. Integrating the desires of our stakeholders with the broader goals of the Group is of particular importance and, in order to achieve this, strong governance principles are required. It is therefore important that all our stakeholders be given a transparent view of how the Board’s role is best utilised to meet the needs of the organisation and the communities within which it operates.

South Africa relies on a stable Telkom that will be around for years to come. For this reason we must pursue the most suitable and sustainable course of action that enriches the lives of our customers. I believe that Telkom has, at its disposal, the ability to provide industry-leading service to its customers, but making this a reality will require hard work and a keen sense of the opportunities and challenges that lie ahead.

THE OVERALL HEALTH OF THE ORGANISATIONThe broader global economic outlook is stormy to say the least and consumers continue to feel fi nancial pressure. The macro-economic environment is tough and the overall health of Telkom must remain our primary focus going forward. Management has put strategies in place to retire legacy technologies and offer new products – such as mobile and converged data offerings – on a transformed Next Generation Network to ensure that Telkom is in the best position possible to meet the future needs of our customers. This must be accomplished in an environment that is seeing increasing pressure on traditional telecoms-related revenue streams and an increased need to invest in newer integrated communication technologies in order to meet the demand for faster, better-quality ICT products that provide better value for money.

While the picture painted of the past year may appear to have presented a Telkom struggling to hold its own in the

face of considerable external pressures, in truth, it has been a year of introspection and serious work having taken place at the Group’s core. Much of the work took place behind the scenes at both a Board level as well as at management level, which the Group Chief Executive Offi cer will speak to later in this report. While certain issues may continue to pose challenges on us for some time still, I am confi dent that the issues around regulatory risk, the burden of increased competition and contracting revenue trends are being handled with the utmost care and effi ciency by Telkom’s management team.

As a whole, the views of management are now better aligned with those of the Board and strategies have been put in place to grow shareholder value and embark on a new journey of ICT delivery.

The Board is aware of the increased capital requirements that will be needed to build Telkom’s Next Generation Network into a competitive, commercially viable investment. It is important to note that, while we are committed to growing shareholder value, we will need to take into consideration the longer-term benefi t of an improved network as the business enters its next phase.

Another key strategic focus area is that of Telkom Mobile. We are the fourth entrant in the mobile space and our competitors have had over 16 years’ experience in the sector. It is essential that Telkom’s mobile offering is sustainable over the long term and to this end it must complement the other strengths and core competencies of the business. Making Telkom Mobile a success is a focused priority for Telkom and will continue to be so in the year ahead.

Telkom’s focus on these two strategic pillars is imperative to ensure sustainability and growth of the Group and will require signifi cant capital investment over the next few years. With due consideration of Telkom’s growth requirements and current capital structure, the Board has decided it would be prudent not to declare a dividend for the 2012 fi nancial year.

Polelo Lazarus ZimNon-executive Chairman

GRI and King III

Telkom Integrated Annual Report 2012 9

The fi nalisation of the sale of our Nigeria operations – Multi-Links – in October 2011 is indeed a signifi cant milestone. We have now successfully curtailed the adverse impact that the investment has had on Telkom’s profi t and cash fl ow levels in recent years and management can now focus on its very clear strategic objectives, unencumbered by further distractions.

Progress has been made with regard to the industry regulator’s process of unbundling the local loop. The Independent Communications Authority of South Africa (ICASA) has clearly laid out what the next steps are in unpacking the issue. The reduction in Telkom’s IP Connect rates demonstrates the Group’s commitment towards playing its role in fi nding solutions in this regard.

The two important matters of independence and sustainability will be dealt with in more detail below.

CORPORATE GOVERNANCE We introduced a number of measures to strengthen the overall governance of the Board during the past year. Two Board sub-committees were established, partly to ensure independence levels were in keeping with King III, while a new Memorandum of Incorporation has been drafted in order to replace the existing version. The latter also takes into consideration the changes in relation to the shareholders’ rights pertaining to Government and the Public Investment Corporation as the class A and class B shareholders, respectively.

The Board approved the revised Business Code of Ethics in 2011 and is committed to conducting the business in an ethical manner based on an ethical foundation.

A full report on our Corporate Governance structures and processes and our governance and enterprise risk profi le can be found on pages 49 and 58 respectively.

INCREASING INDEPENDENCEUpon my re-appointment as Chairman, the question of the overall independence of the Board of Directors was brought to the fore, largely as a result of certain rights held by the Government of South Africa (as the class A shareholder) having expired on 5 March 2011. Under the existing Memorandum of Incorporation, the class A shareholder was, up until the lapsing date, entitled to appoint fi ve directors – including the Chairman – to the Telkom Board.

In response to the need to align the Group with international best practise and the King III guidelines, I am pleased to report that the Board now consists of an increased number of independent directors. The measures taken to ensure the Board is in line with international best practise, JSE Listings Requirements and King III in terms of independence are as follows:

1. The Board was previously limited to a maximum of 12 Board members; this has been increased to 14; six of whom are now independent non-executive directors, six of whom are non-executive directors and two executive directors.

2. Four additional independent non-executive directors were appointed over the course of the year, thus increasing overall independence and bringing valuable new skills and experience to the Board.

3. An Independent Directors’ Committee has been formed to assist with shareholder-related matters in which the Chairman may be confl icted – the Lead Independent Director’s effectiveness was successfully tested during the appointment of the Chairman in February.

4. Mr Sibusiso Luthuli has been appointed as lead independent director and Chairman of the Independent Directors’ Committee. Mr Luthuli’s training as a chartered accountant and his experience as a businessman, coupled with his extensive experience on the Telkom Board, will stand him in good stead as he takes up this vital role.

Those directors presently sitting on the Board, who were appointed by the class A shareholder, will be placed on rotation for re-election as and when their three-year tenure comes to an end.

STRENGTHENING THE BOARDIn addition to the newly upgraded level of independence on the Telkom Board, I am confi dent that the range of skills amongst its members will allow the Board to continue to provide focused support to management when it is required. Five of the present Board members have extensive experience in telecommunications and ICT, including academic experience, policy creation and hands-on industry experience, while the remaining Board members bring necessary skills and experience in accounting, fi nance and corporate action, law, and Corporate Governance as well as executive level experience.

I would like to welcome Dr Sibusiso Sibisi, Ms Nomavuso Mnxasana, Ms Neo Dongwana and Mr Itumeleng Kgaboesele. The Board is grateful to have their skills and I look forward to working with them going forward.

Mr Kgaboesele has taken over as Chairman of the Investment and Transaction sub-committee. As a chartered accountant with several years of investment banking experience, he brings signifi cant expertise and entrepreneurial skills which will greatly contribute to the strength of this committee and of the Board.

DRIVING SUSTAINABILITYIt is important to take into consideration the overarching role that the Group plays in South Africa’s broader economy. We touch many people’s lives on a daily basis and for this reason sustainability is of core importance to the manner in which we put our strategies into practise.

The Social, Ethics and Sustainability Committee was formed during the course of the year to ensure that matters pertaining to the long-term sustainability of the Group, as well as how it conducts itself in relation to the environments within which it operates, be given the utmost attention. The committee is accountable to both the Board and broader stakeholders of Telkom and reports to shareholders at the Company’s Annual General Meeting. This sub-committee was formed to comply with the Companies Act as well as meet the recommendations made by King III and we look forward to reporting on these pertinent issues going forward. The committee is chaired by Ms Julia Hope, a telecoms engineer with extensive experience in broadcasting and telecommunications, as well as ICT regulatory policy formulation and implementation.

10 Telkom Integrated Annual Report 2012

REGULATORY ENVIRONMENTWhile Telkom is committed to playing its part in providing broadband services to all South Africans, it must come with a balanced approach that is not onerous to the Group and its broader stakeholder community.

In order to be sustainable and effective as a group we are committed to building stronger relationships with Government – as the policy maker – as well as the industry regulator ICASA to ensure that the broader social needs are met without placing unnecessary strain or unfair disadvantages on the Telkom Group. We need to work hard at understanding the needs of Government, while putting forward our own requirements as an industry player in an increasingly liberalised market.

Telkom is entering its second decade as a publicly-listed company and has operated as a liberalised entity since 1991. There is a growing sense that the scales have been tipped in favour of Telkom’s competitors for long enough. Telkom management feels it is essential that the regulatory framework be re-assessed to refl ect the current competitive situation in order to ensure that the long-term success of the industry as a whole does not come at Telkom’s expense.

As a Board, we are committed to lending support where necessary towards ensuring that Telkom continues to contribute towards a levelled playing fi eld at all times but that the framework under which we operate is fair to all.

CONCLUSIONIn conclusion I would like to thank the members of the Board for their hard work over the past year and would also like to take this opportunity to welcome our new Board members. Mr Peter Joubert resigned from the Telkom Board in August 2011 – I would like to thank him for his valuable contribution to the Company over the past years.

Our broader stakeholders – especially our customers and our investors – are vital to the health of the organisation and we welcome any suggestions and thoughts on how we can make your Telkom experience more fulfi lling – your steadfast loyalty is greatly appreciated. Lastly I would like to thank Telkom management as well as all our employees for the hard work and dedication to the Group during what has been a very diffi cult year.

The year ahead will be diffi cult for Telkom as we continue to streamline operations and position the Group for fl exibility in the face of a changing telecoms environment. However, it is evident to me that the Group is well on its way to execute on the strategies put in place to ensure we deliver on our promise of seamlessly connecting our customers to a better life.

Lazarus ZimChairman of the Telkom Board

Chairman’s letter (continued)

Telkom Integrated Annual Report 2012 11

12 Telkom Integrated Annual Report 2012

Message from the Group Chief Executive Offi cer

Dear Stakeholder,To summarise the year under review, I would call it a year of clean-up and consolidation across the Telkom Group.

Over the past year we have placed extensive effort on the aligning and streamlining of the Group’s strategies and operations in order to better deliver value going forward. It has been a diffi cult year but one that has been hugely necessary to the future stability of the Group. Much has been accomplished in terms of realising the broader strategy and consolidating our operations but there is much that still needs to be done.

The Group faced continued erosion of the traditional fi xed-line business, while simultaneously bearing the burden of increased costs associated with positioning the Group to meet the growing broadband and mobility needs of our consumers. Demand for faster products at lower prices continues to put the Company under pressure and the impending notion of a recession means that our larger consumers are stockpiling resources somewhat and are hesitant to invest in telecoms services.

Fixed-line continues to be under pressure from competition and substitution by mobile, especially in terms of voice minutes. Data, however, continues to be an area of growth and we believe the point at which the contributions of data and of voice will be one-to-one is not far off.

FINANCIAL HIGHLIGHTSOur results for the year include an R896 million loss relating to the disposal of Multi-Links and an impairment loss of R569 million relating to the goodwill and assets of the Telkom International subsidiary iWayAfrica. Headline earnings per share declined 33.0% from the prior year. This is mainly as a result of the investment made in our mobile business as well as additional depreciation of R605 million as a result of a review of the existing network equipment in terms of its useful life as we invest to transform to a commercially-led, Next Generation Network. This was partially offset by R739 million

voluntary employee severance package costs included in the prior year. Overall, we have managed to contain operating costs – excluding depreciation, amortisation impairments and write-offs – to below infl ationary increases.

The Group faced continued erosion of the traditional fi xed-line business with fi xed-line traffi c revenue decreasing by 8.0%. Despite the decline in traffi c volumes and pricing pressure we managed to limit the fi xed-line revenue decline to 2.8%. The Group generated R2.1 billion free cash fl ow for the year under review.

Demand for faster products at lower prices continued to put our data revenue under pressure.

DIVIDENDTelkom decided not to declare a dividend in respect of the fi nancial year ended 31 March 2012. While our current fi nancial position should allow us to fund network transformation and build our data driven mobile offering, the Board has decided that it is prudent to allow for more internally generated funding for the capital expenditures planned over the next three years. This will better position Telkom to weather uncertainties as we advance our value building strategy.

Telkom’s strategic objectives of network transformation and the building of its mobile business will see dividends being considered on an annual basis based on the performance of the Group.

MULTI-LINKS SALE CONCLUDEDThe sale of Telkom’s Nigerian operation Multi-Links was concluded in October 2011. While the process faced more challenges than we were anticipating, management is satisfi ed that Telkom is now better positioned to focus on delivering better results in its core business without further distraction from non-aligned operations. We believe that the negative fi nancial and legal ramifi cations associated with retaining Multi-Links would have had a far more

Nombulelo MoholiGroup Chief Executive Offi cer

GRI and King III

Telkom Integrated Annual Report 2012 13

negative impact on the Group than divesting as quickly and profi ciently as we did.

TELKOM MOBILETelkom Mobile has been well-received by the market and the acquisition of customers has exceeded expectations. Converting these numbers into strong revenue has been somewhat disappointing, especially in the pre-paid segment. This was largely due to an under-estimation of the deep relationships that some of our competitors have with certain distributors. We have prioritised the need to improve our distribution network and have already seen an increase in distribution using larger retail channels. We also intend increasing our direct channel footprint up to threefold by the end of the year and develop effective channel mix capacity for main target segments.

The overall roll-out has been slower than we originally anticipated, primarily because the current strategy depends largely on acquiring base stations from our competitors, with varying degrees of co-operation. Early indications are that we may need to invest further in our base station coverage to meet growing data needs and provide better coverage. We are, however, already utilising our own network for the majority of our data delivery.

Going forward, we intend to focus on areas in which Telkom Business Mobile and 8•ta can differentiate their brands and provide further value-added services to customers.

TRUDONTelkom holds 64.9% of the printing and electronic directory listing group Trudon with the remainder held by Belgium’s Truvo.

Trudon continues to follow its consumers online as print readership continues to face decline. New product offerings from the likes of Google are adding additional pressure to the Group with free listing opportunities and the like. However, there is still potential upside in the medium term and Telkom has taken the decision to invest further in this asset going forward.

SWIFTNETSwiftnet continues to offer valuable services in the credit clearance and debit card market. We are embarking on a major technology refresh programme away from the radio-based X.25 technology towards mobile technology to offer a better service to our customers in the point-of-sale verifi cation, security and fl eet management services.

ALIGNING LEADERSHIP GOALSI am pleased to report that the extensive time spent balancing the views of the Telkom Board with that of management has paid off. There is a new energy within the management team and I am satisfi ed that Telkom’s leadership is committed to taking the Group to the next level.

We continue to be dogged by the historical perceptions of poor delivery and, being acutely aware of this, have now put measures in place to ensure leadership development is a priority.

A NEW SET OF VALUESWe are beginning to see improvements in overall morale and attitude across the Group. Changing the culture of an organisation is not easy and will take years to get to a point that I would believe is satisfactory. However, it is essential that we foster a culture that champions customer service at every level. I take great pride in knowing that our employees themselves came up with the values with which we will take the Company forward, those of continuous improvement, honesty, accountability, respect and teamwork. These values form the foundation of our business code of ethics, which sets out Telkom’s standards for ethical behaviour. We are committed to conducting our business in an ethical manner and I personally commit to the standards outlined in our code of ethics.

STRATEGIC PARTNERSHIPSOn 8 May 2012, Telkom announced that it had reached an in-principle agreement with Korea’s KT Corporation regarding the terms of a potential strategic venture that would, if implemented, have resulted in KT acquiring a strategic equity shareholding of 20% in the post-issue ordinary share capital of Telkom. Telkom and KT would also have entered into a fi ve-year co-source management services agreement to identify areas of mutual strategic and business co-operation.

On 30 May 2012, Telkom was informed by the Honourable Minister of Communications that the proposed transaction between the companies had been presented to the cabinet of the South African Government and that cabinet had taken the decision not to support the transaction as proposed. Telkom will continue to engage the South African Government further.

THE REGULATORY ENVIRONMENTThe telecoms and ICT environment has changed signifi cantly from where it was 10 years ago and we would like to see a full review of the industry regulations. For example, it is not sustainable for one company in an open market to continue to be under price control in perpetuity. Also, the roll-out and maintenance strategy for public payphones that Telkom must carry in line with its operating licence is unnecessarily burdensome on the Company in our view.

I would ultimately like to see a scenario in which all wholesale operations are regulated while the retail operations remain open to free-market principles. In my view, this would allow for a greater uptake of broadband services while fostering

This is our second integrated annual report. We have, once again, been guided by King III governance principles to deliver a transparent, user-friendly and accessible document to you. We are making every effort to allow the integrated approach to infuse the way we talk to our stakeholders.

We would value any feedback from you in this regard, please refer to the front of the report for information on how you can help us to get better insight into what you want to read in future reports.

This is our second integrated annual report. We have,once again, been guided by King III governanceprinciples to deliver a transparent, user-friendly andaccessible document to you. We are making everyeffort to allow the integrated approach to infuse theway we talk to our stakeholders.

We would value any feedback from you in this regard,please refer to the front of the report for informationon how you can help us to get better insight into whatyou want to read in future reports.

14 Telkom Integrated Annual Report 2012

Message from the Group Chief Executive Offi cer (continued)

an environment that will increase competition and decrease the costs of telecommunications and ICT services to for the end-user.

Local loop unbundling (LLU)We continue as Telkom to be fi rm that discussions around LLU should not be seen in isolation but rather in terms of what we want to achieve in terms of broadband penetration as a country. We believe that fi xed-line broadband, as it is the case today, has already been overtaken by mobile broadband in terms of the numbers of subscribers and therefore the fi xation with local loop unbundling may have been overtaken by time. Telkom believes that the regulatory burden placed on Telkom is not sustainable for Telkom or the country.

We will continue to engage with the industry regulator on matters affecting Telkom’s strategy.

Increasing broadband penetration and meeting Government’s ICT targetsThe Group is focused and willing to assist the South African Government with its vision to create higher broadband penetration in South Africa by 2020. We look forward to exploring future public-private partnerships in order to assist Government in achieving its objectives. In our view, the fastest and most viable means of ensuring broadband accessibility is using wireless technology and we look forward to engaging with Government to fi nd meaningful means of rolling out this technology.

Taking Telkom forward – unpacking the Group strategyWe have reviewed and refi ned Telkom’s strategic intent across the various key business areas as follows:

Growing and defending profi table Telkom Business revenues Telkom Business aims to become the industry leader in fi xed and converged communication services as well as a serious contender in cloud-related and services to the South African business market, within the next fi ve years. In order to achieve this, it is essential that we utilise the services offered across the Telkom network, leveraging off our broader Telkom network while making use of data centre services spearheaded by Cybernest as well as Telkom Mobile to provide relevant fi xed-mobile convergence (FMC) and unifi ed communication services to South African businesses.

Delivering on our investment in Telkom MobileThe broader mobile business strategy to defend erosion in our fi xed-line business while growing converged delivery channels to our customers is a key priority. We are committed to ensuring that all investments deliver value to our shareholders, and to this end we will focus closely on our mobile business strategy to ensure that it aligns to this outcome.

Meeting the growing data demand in South Africa is a core feature of our mobile strategy and it is essential that this be done in such a way that it does not lead to cannibalisation of our other services. Instead, we must offer services that reward

the customer for using Telkom’s products with varying levels of incentives depending on the customers’ level of loyalty.

Growing and defending profi table revenues in Telkom Consumer Services and RetailGlobally, our peers in the fi xed-line and broader telecoms space are battling the same dwindling revenue streams and the same unyielding demand for lower prices as we are. Consumers are entering a new era, in which they will be less tolerant of the boundaries between communication channels and more demanding in terms of their data needs. In short, consumers require a seamless communication connection to complement their everyday lives.

Using Telkom’s extensive network and integrating this with consumer related products such as mobile we are uniquely positioned to meet the future demand for converged communications and increased broadband needs.

We intend to work more closely with partners to offer value-added broadband services. The products that we would look at investigating are those that are bandwidth intensive. As an example, Telecoms companies worldwide continue to exploit video-on-demand services and Telkom would look into this as a potential future value-added service. The group recently signed an agreement with electronics manufacturer Samsung to provide entry-level Smart TV services to consumers and we expect further innovations in this regard going forward.

Transforming and upgrading the Telkom network The democratisation of information is upon us and ICT players will have to keep up in order to survive. Telkom’s investment in the Next Generation Network will enable the local loop to offer speeds of 10 Mbps and higher in selected areas to allow us to offer new services and better quality products.

In moving toward becoming a true data provider we will need to make use of the entire spectrum of services across the network. In order to achieve this we will need to ensure that our network upgrade is rolled out profi ciently, on a commercially viable basis.

Following a year of extensive planning, the implementation of the network transformation process will come online during the course of this year. There is much that needs to take place in terms of upgrading our network to meet tomorrow’s needs, however, the process has kicked off successfully with clear deliverables in place and we have since achieved major traction against these plans as we work towards delivering an all-IP (internet protocol) network, designed to enable fi xed-mobile convergence and truly differentiated high-speed broadband.

The network transformation intent is to take our fi bre deeper into the network and smartly leverage a mix of high-speed broadband access technologies. Our aggregation network is increasingly able to support super-fast transmission and enable a superior browsing experience. We have already evolved our national and regional transmission network from carrying Gbps to Tbps with great resilience and manageability. Our international connectivity has received a major boost to ensure worldwide reach with superb capacity and resilience.

Telkom’s network transformation is bound to change the face of broadband capability in South Africa.

Sustainability and environmental approach Perhaps no other sector besides telecommunications is better positioned to facilitate the shift towards sustainable,

A detailed breakdown of the fi nancial performance of our various business segments can be found on page 36, while strategic information relating to the Group’s business divisions can be found on page 22.

A detailed breakdown of the fi nancialperformance of our various business segmentscan be found on page 36, while strategicinformation relating to the Group’s businessdivisions can be found on page 22.

less energy-intensive business practices. But like most of our peers in this ‘low-to-medium impact sector’ we are still in the early stages of developing our strategy to embed sustainability practices in all aspects of our business operations.

Our approach to sustainability has been guided by the fact that we operate in a resource constrained world where responsible corporate citizens need to fi nd initiatives for the more effi cient use of natural resources such as energy and water. Telkom is involved in a range of activities to reduce energy consumption through more intelligent usage as well as investment in more energy effi cient infrastructure. We continue to invest in better monitoring systems to understand and improve our water usage. Although no targets have been set, Telkom is currently in the process of developing them for these priority areas.

The Telkom sustainability strategy, which is expected to be formally approved by the Telkom Board during the second half of 2012, seeks to ensure the integration of sustainability considerations into our business plans, decision-making processes and our operations.

We recognise that sustained investment in the skills and wellness of our staff is necessary to achieve a competitive advantage over the longer term. Thus, it is with great sadness that I must report the death of two colleagues while on duty. No fatality is acceptable and we will continue to invest in measures that reduce workplace risks for our workforce. In this context it is pleasing to note that over the past fi ve years our interventions have led to a steady, if gradual, decline in the lost time injury frequency rate as well as more than a 50% decline in the number of days lost per employee as a result of safety incidents. This indicates a signifi cant overall reduction in the severity of workplace incidents.

Going forward we will continue to target interventions at priority risk areas and achieving our performance targets developed by Telkom’s various business units. This will be done through the setting of long-term performance targets and developing the systems that will allow us to report more formally on our progress against the Global Reporting Initiative (GRI) guidelines for sustainability reporting.

OUTLOOK AND CONCLUSIONTelkom faces many challenges at the moment but we will advance calmly and in a determined manner while remaining focused on delivering on the promise of our business and strategy going forward. Group fi nancial results for the year under review have refl ected the challenges that we are currently facing as a Company but we have taken a number of signifi cant steps towards securing a successful future for Telkom and have begun casting the foundation that will allow the Group to compete well against its peers and build value in the future. Our strategy going forward is clear and focused.

The Group is now more stable and more accountable from a management perspective and we are committed to increasing our productivity levels in order to facilitate the seamless delivery of connectivity to all our customers.

In conclusion I would like to thank the Telkom employees for your hard work over the year as well as our other stakeholders for your loyalty and support. We are committed to growing value for all our stakeholders and I look forward to continuing this journey with you.

Nombulelo MoholiGroup Chief Executive Offi cer

Telkom Integrated Annual Report 2012 15

16 Telkom Integrated Annual Report 2012

Board of Directors

1 2 3

4 5 6

7 8 9

10 11 12

13 14

Telkom Integrated Annual Report 2012 17

1. LAZARUS ZIMNon-executive Chairman

Age: 51

One years service on Telkom BoardQualifi cations: MComMember of the following Board committees:Human Resources Review and Remuneration Committee; andNominations CommitteeOther external boards:Chairman of Afripalm Resources;Chairman of Zim Capital; andChairman of Northam Platinum

2. NOMBULELO MOHOLI Group Chief Executive Officer

and Executive DirectorAge: 52

Fourteen years service at TelkomQualifi cations: BSc (Eng) (Electrical and Electronic)Member of the following Board committees:Executive Committee; andHuman Resources Review and Remuneration Committee

3. JACQUES SCHINDEHÜTTE Chief Financial Officer and Executive DirectorAge: 53

Appointed August 2011Qualifi cations: CA(SA), BCom (Hons), Higher Diploma in TaxationMember of the following committee:Executive CommitteeOther non-executive director appointments:JD Group Limited; andAvusa Limited

4. ITUMELENG KGABOESELEIndependent non-executive directorAge: 40

Appointed July 2011Qualifi cations: CA(SA), BCom, Post Graduate Diploma in AccountingMember of the following Board committees:Chairman of the Investment and Transaction Committee; Audit and Risk Committee; andIndependent Directors’ CommitteeOther external boards:Sphere Holdings (Pty) Limited;Old Mutual Investment Group (South Africa); Holdings (Pty) Limited; andStudent Sponsorship Programme

5. BRAHM DU PLESSISIndependent non-executive directorAge: 57

Seven years service on Telkom BoardQualifi cations: BA, LLB, LLMMember of the following Board committees:Audit and Risk Committee;Nominations Committee;Human Resources Review and Remuneration Committee; andIndependent Directors’ CommitteeOther external boards:Member of Advocates for Transformation

6. JACKIE HUNTLEYNon-executive directorAge: 49

Four years service on Telkom BoardQualifi cations: BProc, LLBMember of the following Board committees:Chairman of the Human Resources Review and Remuneration Committee;Social, Ethics and Sustainability Committee; andInvestment and Transactions CommitteeOther external boards:Mkhabela Huntley Adekeye Inc; Rorisang Basadi Investments (Pty) Limited; Kutana Investment Group Limited; Capitec Bank Limited

7. SIBUSISO LUTHULILead independent non-executive directorAge: 38

Six years service on Telkom BoardQualifi cations: CA(SA), BCom (Hons)Member of the following Board committees:Independent Directors’ Committee;Chairman of the Audit and Risk Committee;Nominations Committee; andInvestment and Transactions CommitteeOther external boards:Chairman of Cipla Medpro SA Limited

8. JEFF MOLOBELANon-executive directorAge: 56

Two years service on Telkom BoardQualifi cations: BSc (Eng) Hons, MBAMember of the following Board committees:Nominations Committee; andHuman Resources Review and Remuneration CommitteeOther external board:N3 Toll Consertion (Pty) Limited; andZimele Investment Enterprise Company (Pty) Limited

9. JULIA HOPENon-executive directorAge: 49

Two years service on Telkom BoardQualifi cations: MSc (Eng. Telecommunications)Member of the following Board committees:Nominations Committee;Investments and Transactions Committee;Human Resources Review and Remuneration Committee; andSocial, Ethics and Sustainability CommitteeOther external boards:Rovusa Trading Enterprise; Hopelafl eur Communications Networks (HCN).

10. NAVIN KAPILANon-executive directorAge: 58

One year service on Telkom BoardMember of the following Board committee:Investment and Transactions Committee

11. YOUNAID WAJANon-executive directorAge: 60

Two years service on Telkom BoardQualifi cations: CA(SA), BCom (Hons), HDip Tax LawMember of the following Board committees:Social, Ethics and Sustainability Committee; andInvestment and Transactions CommitteeOther external boards:Blue IQ Limited;Imperial Holdings Limited;Pareto Limited;Diablo Share Trust;Public Investment Corporation;APF Chartered Accountant Inc; andIncome Tax Special Court

12. DR SIBUSISO SIBISIIndependent non-executive directorAge: 56

Appointed February 2012 Qualifi cations: BSc (Physics), PhD (Applied Mathematics and Theoretical Physics)Member of the following Board committee:Independent Directors’ CommitteeOther external boards:CEO of the Council for Scientifi c and Industrial Research (CSIR, SA);Murray & Roberts;Liberty Life; andMapungubwe Institute

13. NOMAVUSO MNXASANAIndependent non-executive directorAge: 55

Appointed February 2012Qualifi cations: CA(SA), BCompt (Hons)Member of the following Board committees:Audit and Risk Committee; andIndependent Directors’ CommitteeOther external boards:Land Bank;Winhold Limited;AIH;Pareto Limited;Nedbank Limited;Optimum Coal Limited; andSchindler (Pty) Limited

14. NEO DONGWANA Independent non-executive directorAge: 40

Appointed February 2012Qualifi cations: CA(SA), BCom (Hons)Member of the following Board committees:Independent Directors’ Committee; andAudit and Risk CommitteeOther external boards:AVI Limited;Mpact Limited; andEnterprise Development Fund of PPC Limited

WEB: Comprehensive CVs of the directors are available

at www.telkom.co.za.

GRI and King III

18 Telkom Integrated Annual Report 2012

6. THAMI MSUBOChief of Human ResourcesAge: 46

Years of service at Telkom: 1BA Public Management (Hons), Bachelors of Economics in Public Management

Executive Committee

1. MOTLATSI NZEKU Managing Director: Telkom International

and SubsidiariesAge: 51

Years of service at Telkom: 16

BSc Mathematics and Physics, BEng (Hons)

3. BASHIER SALLIE Managing Director of Wholesale

and NetworksAge: 44

Years of service at Telkom: 26

MDP

5. NOMBULELO MOHOLI Group Chief Executive Officer and

Executive DirectorAge: 52

Years of service at Telkom: 14Qualifi cations: BSc (Eng) (Electrical and Electronic)

2. DEON FREDERICKSDeputy Chief Financial OfficerAge: 51

Years of service at Telkom: 18

CA(SA), BCom Business Management (Hons)

4. JACQUES SCHINDEHÜTTE Chief Financial Officer

and Executive DirectorAge: 53

Years of service at Telkom: 1

Qualifi cations: CA(SA), BCom (Hons), Higher Diploma in Taxation

Telkom Integrated Annual Report 2012 19

8. DR BRIAN ARMSTRONGManaging Director of Telkom BusinessAge: 51

Years of service at Telkom: 2

PhD, MSc (Eng) (Electrical), BSc (Eng) (Electrical)

7. OUMA RASETHABAChief of Corporate GovernanceAge: 51

Years of service at Telkom: 6

BProc, LLB (Hons), higher diploma in Company Law, LLM

9. MANELISA MAVUSO Managing Director of Consumer Services

and RetailAge: 41

Years of service at Telkom: 2

BEcon

WEB: Comprehensive CVs of the directors are available

at www.telkom.co.za.

GRI and King III

20 Telkom Integrated Annual Report 2012

Industry overview

THE REGULATORY ENVIRONMENTThe regulatory environment has seen much activity over the past year. Telkom continues to engage with the Independent Communications Authority of SA (ICASA) on a variety of issues including local loop unbundling, the access line defi cit, interconnection rates and spectrum fees.

Self-provision and fi xed-line voice competitionAs the incumbent fi xed-line operator in South Africa, fi xed-line voice revenue is and has been at the core of our business. The playing fi eld was changed with the introduction of Neotel, which competes with us in all markets, and the granting of an electronic communications network service (ECNS) licences to the state-owned Broadband Infraco (Pty) Limited, whose main objective is the provision of wholesale bandwidth to other licensees at cost-based prices. Other licensees, including the mobile operators, who used to obtain their core transmission infrastructure from us, are now adequately licensed to provide their own infrastructure and also to provide it to other licensees, in competition with Telkom’s network services.

Spectrum licence fees and accessAdministrative incentive pricing (AIP) of spectrum was introduced through regulation by ICASA in 2010 to incentivise spectrum users to make the most effective and effi cient use of the radio frequency spectrum, specifi cally with regard to spectrum use in rural areas. Although implementation of these regulations was initially deferred to 1 April 2012, there remains a level of uncertainty regarding the implementation of the various formulae and data tables and we continue to engage with ICASA to clarify the situation. As previously reported, while we expect the proposed fee structure to increase our spectrum fees, we are looking at various options to reduce this amount.

Review of universal service obligationsIn August 2010, ICASA issued a discussion document on the review of universal service and access obligations (USAOs). As indicated in the previous year’s report, we have submitted our views on the proposed USAO model to ICASA but no further progress has taken place. We are still of the belief that there will need to be further consultations with ICASA before the regulations are fi nalised.

Price controlsWe have fi led our retail tariffs in accordance with the regulations governing the standard terms and conditions for individual licences, which contemplate that such tariffs be fi led with ICASA, seven days before they become effective, but does not require ICASA approval of those tariffs.

Local loop unbundlingLocal loop unbundling (LLU) in its original form is a regulatory mandated process that enables multiple telecommunications operators to access and provide services over the ‘last mile’ infrastructure – from the local exchange to the customer’s premises – that is traditionally owned by the incumbent operator. There are other forms of wholesale services, including that known as BitStream, which could give operators access to our broadband infrastructure without requiring the physical unbundling of the loop.

After a fairly lengthy consultation process ICASA has come to the conclusion that LLU is a fairly complex and costly process that will require the conduct a regulatory impact analysis before it is mandated by regulation, as well as a market review to determine the necessity and scope of any LLU regulation. On this basis, ICASA has suggested that in the interim BitStream should be offered by Telkom from November 2012.

Mobile and fi xed-line termination ratesICASA has imposed new termination rates, which came into effect on 1 March 2010. Our two larger competitors – Vodacom and MTN – are required to reduce their termination rates, in step measures, from R0.89 to R0.40 by 1 March 2013. Also from 2013 there will be no difference between peak and off-peak rates for call termination services.

The smaller players – being ourselves (8•ta) and Cell C – are entitled to charge up to 20% more than MTN and Vodacom for calls terminated on each of our respective networks between 1 March 2011 and 28 February 2012. After that date, the maximum premium charged would fall to 15% and then to 10% in March 2013.

COMPETITION – VOICE REVENUES WILL CONTINUE TO BE ERODEDAs an integrated communications service provider, Telkom offers packaged fi xed and mobile voice, data, broadband and internet services to business and residential customers, mostly in South Africa. As a result of the Electronic Communications Act, the licensing framework has resulted in a more horizontally layered market with a large number of electronic communications and broadcasting licences issued, This has led to increased competition in our industry.

Our competitors continue to self-provide in the infrastructure development space and this trend is unlikely to abate anytime soon. Demand for faster services at cheaper rates is driving the aggressive rollout of fi bre and infrastructure services. The introduction of the planned upgrade to

The South African market has felt the effects of slowing voice and mobile revenues and there has been an increased level of competition from local telecoms companies defending their own interests. Added to this, there is a promulgation of non-traditional players in the internet space now joining the fray with their own inexpensive communications solutions.

Telecoms operators will have to look at new, adjacent offerings in order to grow their revenues. The upside is that with the introduction of new technologies and services, such as fi xed-mobile convergence, there is the potential that the existing revenue streams may be protected by an increased desire for high-speed, quality data.

Telkom Integrated Annual Report 2012 21

our network will go a long way to ensuring that we can provide our own unique offering in this regard and entice other mobile operators to utilise our network services. A commercially-led and viable pricing model in this regard will further enhance our capabilities.

An increase in the use of voice over IP (VoIP) technology is a further threat to our voice revenues and the best way to mitigate this risk is to ensure that we are competing with an upgraded and transformed, all-IP network as quickly as possible. In addition, we will continue to offer suitable products and services that grow our share of the data market in both fi xed-broadband ADSL and mobile.

The introduction of 8•ta in the mobile space has certainly increased competition in the sector. The existing major players have responded with aggressive deals and this is likely to continue. Although customer growth rates may slow over the medium term, we believe there are suffi cient credible opportunities to ensure that Telkom creates a niche for itself in the broader industry. Fixed-mobile convergence (FMC) and unifi ed communications are likely to become more important from a long-term perspective, while faster mobile data and content are likely to be at the top of the consumer’s medium-term telecommunications needs.

It is likely that telecommunications operators will focus on extracting as much value out of their existing clients resulting in an increased battle to secure the customer’s loyalty going forward.

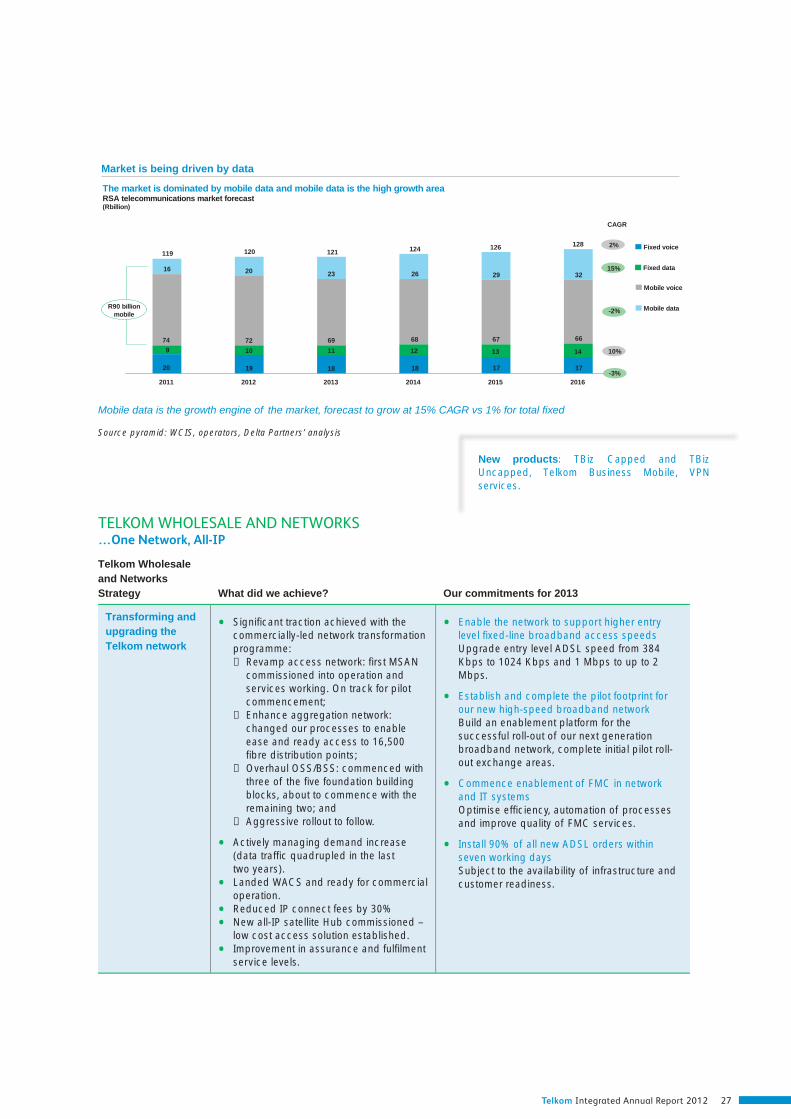

DATA DEMAND WILL CONTINUE TO INCREASEThe South African consumer is becoming increasingly more aware of global trends in ICT and data consumption and continues to demand a faster, more stable data service at a lower price. Data, and in particular mobile data, is expected to see substantial growth in future. We have already begun the process of increasing the minimum speeds of our fi xed-line ADSL network and recently increased our minimum ADSL speed from 384 Kbps to up to 1 Mbps. Further improvement in this area is reliant on the speed at which we can action the network transformation and upgrade. We are also aware of the opportunities surrounding content delivery – that is more bandwidth intensive – and will be focusing on unlocking potential avenues that will enable consumers to use our data products and network services more effectively.

FMC as well as unifi ed communications and cloud computing will present further opportunities for Telkom to take advantage of potential adjacent revenue streams. We intend to consolidate our position in this regard and accelerate our data offerings to take a leading role in bringing these services to the market.

Actual and forecasted broadband subscribers

00

1616

010

5747

1639

187133

43131

421247

64353

832

Bro

adb

and

su

bsc

rib

ers

(’00

0)

415

82

509

1 172

582

83

721

1 671

867

90

856

2 417

1 472

97

979

3 405

2 329

108 116

1 331

3 858

5 305

1 180

4 489

3 202

122

1 444

5 914

4 349

128

1 568

6 585

4 889

126

1 520

6 326

4 680

1 000

2 000

3 000

4 000

5 000

6 000

7 000

Dec 2016Dec 2015Dec 2014Dec 2013Dec 2012Dec 2011Dec 2010Dec 2009Dec 2008Dec 2007Dec 2006Dec 2005Dec 2004Dec 2003

Fixed Nomadic Mobile Total market

Fixed-line technology market share (Voice channels)

Mar

ket s

har

e (%

)

11

100 100 100 100 100 99 98 97 96 95 94 92 91 89

986543210000010

20

30

40

50

60

70

80

90

100

Dec 2016Dec 2015Dec 2014Dec 2013Dec 2012Dec 2011Dec 2010Dec 2009Dec 2008Dec 2007Dec 2006Dec 2005Dec 2004Dec 2003

VoIP PSTN

Source: Africa Analysis: SA Telecoms model

22 Telkom Integrated Annual Report 2012

Business review

Telkom’s South African operations contributes 98.9% towards Telkom’s total revenues. It is made up of a number of consumer- and business-focused operations in voice and data across both fi xed-line and mobile. The divisions (detailed below) are largely cross-functional and share services wherever possible. Telkom South Africa is constantly looking for fresh opportunities to grow its revenue streams beyond that of traditional fi xed-line voice and has made aggressive forays into mobile and data to position Telkom for better future growth.

Below is a breakdown of the various business segments, their product offering and growth prospects; as well as the general outlook for the year ahead:

Telkom Business provides services to approximately 330,000 registered businesses in South Africa. A massive portion of the economy is reliant on Telkom services and we are well positioned to leverage off this existing client base by providing further ICT solutions to assist these businesses with their everyday requirements and to meet expected bandwidth demand growth.

We have made good progress on the uptake of voice discount plans, specifi cally by winning back business lost to least cost routing in the past; this is helping to mitigate the downward pressures on fi xed voice revenues. Overall revenues from data products showed modest yet encouraging growth over the period indicating that the strategy of managing price declined in concert with volume growth is effective. There is, however, a need to rapidly evolve our portfolio to meet the demands of the market for increased bandwidth, greatly reduced unit cost, and technology substitution, as well as to transform our sales channels to become sellers of ICT services rather than purely sellers of fi xed-lines.

Telkom Business Mobile was launched during the course of the year. The overall response from the market in terms of the features and overall quality of our products has been positive. We are now placing strong emphasis on securing stable distribution channels and re-skilling existing direct sales channels such as Telkom Direct Stores and Telkom Business client services staff. The introduction of the next generation network (NGN) will underpin the next generation

broadband, fi bre and cloud products we will begin to offer across Telkom Business customer segments, as well as enable evolution of the Telkom Business Mobile portfolio and continued progress with fi xed-mobile convergence (FMC) and Unifi ed Communications offerings.

Overall customer satisfaction levels are positive, especially so in our largest customer segment – the larger South African corporates. In terms of customer relationship leadership, we continue to make good progress, a fact that can be seen in the Telkom Business brand survey results, which have been most encouraging. Compared to our competitors we have by far the highest level of bonding. In terms of service levels, our managed services show very good and continually improving results, and our large project implementation teams are delivering exceptional performance.

Overall service improvements were as follows:

• 98.7% of Telkom Business customer SLAs met or exceeded;

• 99.2% on time delivery on large customer project implementation;

• 14% improvement in Enterprise/Wholesale broadband delivery;

• Top 2 box scores for quality to corporates 57% to 60%;

• Top 2 box scores for quality to wholesale 51% to 58%; and

• 11.2% improvement on consumer broadband delivery.

TELKOM BUSINESS…Data driven, we will continue to build on our strengths

Telkom strategy What did we achieve this year? Our commitments for 2013

• Leading the market in the provisioning of fi xed and converged communications services

• Transforming the way IT is delivered, through the Cloud

• Successfully defended our number one position in the business market.

• Secured strategic growth deals with clients including Old Mutual, Nedbank, Department of Communications and Standard Bank.

• Succeeding with fi xed-to-mobile win-back initiatives.

• Launched Telkom Business Mobile.

• Launched Telkom Business uncapped internet.

• Progressed our FMC and unifi ed communications capability.

• Further improved excellent managed services delivery and project implementation performance.

• Improvement in Telkom Business brand and reputation.

• Delivered 12% year-on-year revenue growth in Cybernest, our data centre offering.

• Launch productised cloud services Supplement existing, bespoke services with

an initial tranche of productised cloud-based services primarily aimed at the SMB segment including Hosted Exchange; Backup-as-a-Service; Payroll-as-a-Service and CRM-as-a-Service.

• Launch pre-packaged and tailor-made FMC bundles

Launch fi xed-mobile bundles. Allow customers to choose between basic, advanced, premium or customised converged voice and data deals with a compelling value proposition.

• Re-positioning our fi bre portfolio Make it easier and cheaper for our customers

to access fi bre services to satisfy their ever increasing demand for bandwidth.

Telkom Integrated Annual Report 2012 23

We are working on providing a more focused level of customer care at small business level to foster the similar levels experienced amongst our larger corporates, which tend to have dedicated client services personnel. This will, however, take time to implement.

The public sector has been a challenge; while we have made progress in terms of slightly increased revenues in the last year, sales cycles for new contracts have taken longer than expected to complete. This may be symptomatic of the sector but could also be an early warning sign of changing public sector market dynamics and downward pressure on revenues going forward. We are working hard to align the strategic intent between ourselves and Government, for example the role of Telkom where local authorities plan to deploy their own fi bre telecommunications infrastructure, and how Telkom can support Government’s broadband aspirations.

Our core product innovations and launch performance has improved substantially over the past year. Whereas two years ago we were taking far too long to get new products to the market, we have been ahead of the curve in many instances and continue to reshape and innovate our offerings to allow for further demand-driven products to enter the market.

Telkom Business has placed signifi cant effort on evolving its metro-Ethernet fi bre product portfolio. On the broadband side we have responded well to market demands by launching uncapped ADSL, high-speed ADSL and a number of bundled products. We also launched our Offi ce Link products to suit the needs of the small- and medium- sized business. We will also continue with the evolution of our Virtual Private Network (VPN) Supreme portfolio, which we believe is a world-class, market leading product in South Africa, in terms of access options, quality of service options and value-added benefi ts. We intend to grow our share of the VPN market into the medium business sector as well as continue to grow ADSL in the small business category.

ICT is expected to be the biggest growth sector in South Africa over next fi ve years and we intend to capitalise on this growth in an effi cient and sustainable manner. We are pursuing a joint organic and inorganic approach to this opportunity, and as we have reported, we continue to explore acquisition opportunities in the ICT sector.

We will consistently focus on maximising the performance of our existing products to retain customers and ensure we offer the best value proposition in the market. We will continue to seek new revenue streams from adjacent areas in ICT as well as the opportunities arising in FMC. Fast growing adjacencies that Telkom Business will be pursuing in ICT services include Unifi ed Communications, cloud services (specifi cally infrastructure as a service (IaaS) and software as a service (SaaS)), IS Outsourcing and LAN Management, which will be offered in conjunction with managed data network services and managed hosting and managed infrastructure services hosted by Cybernest.