Embed Size (px)

Citation preview

© SAIC. All rights reserved.

Science Applications International Corporation (SAIC)[NYSE: SAIC]

June 2015 Investor Presentation

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Forward-Looking Statements

Certain statements in this release contain or are based on "forward-looking" information within the meaning of the Private Securities Litigation Reform Act of 1995. In some cases, you can identify forward-looking statements by words such as "expects," "intends," "plans," "anticipates," "believes," "estimates," and similar words or phrases. Forward-looking statements in this release include, among others, statements regarding benefits of the proposed acquisition (including anticipated future financial operating performance and results), estimates of future revenues, operating income, earnings, earnings per share, charges, backlog, outstanding shares and cash flows, as well as statements about future dividends, share repurchases and other capital deployment plans. These statements reflect our belief and assumptions as to future events that may not prove to be accurate. Actual performance and results may differ materially from the forward-looking statements made in this release depending on a variety of factors, including: the risk that Scitor will not be integrated successfully into SAIC following the consummation of the acquisition and the risk that revenue opportunities, cost savings, synergies and other anticipated benefits from the merger may not be fully realized or may take longer to realize than expected, diversion of management’s attention from normal daily operations of the business and the challenges of managing larger and more widespread operations resulting from the acquisition, difficulties in entering markets in which we have previously had limited direct prior experience, the potential loss of key employees, customers, and other business partners following announcement of the acquisition, use of a substantial portion of our existing cash resources, incurrence of a substantial amount of debt with increased interest expense and amortization demands, compliance with new bank financial and other covenants, assumption of the known and unknown liabilities of the acquired company, recordation of goodwill and nonamortizable intangible assets subject to regular impairment testing and potential impairment charges, incurrence of amortization expenses related to certain intangible assets, assumption that we will enjoy material future tax benefits acquired in connection with the acquisition, developments in the U.S. government defense and intelligence community budgets, including budget reductions, implementation of spending cuts (sequestration) or changes in budgetary priorities; delays in the U.S. government budget process or approval to raise the U.S. debt ceiling; delays in the U.S. government contract procurement process or the award of contracts; delays or loss of contracts as result of competitor protests; changes in U.S. government procurement rules, regulations and practices; our compliance with various U.S. government and other government procurement rules and regulations; governmental reviews, audits and investigations of our company; our ability to effectively compete and win contracts with the U.S. government and other customers; our ability to attract, train and retain skilled employees, including our management team, and to retain and obtain security clearances for our employees; our ability to accurately estimate costs associated with our firm-fixed-price and other contracts; cybersecurity, data security or other security threats, systems failures or other disruptions of our business; resolution of legal and other disputes with our customers and others or legal or regulatory compliance issues; our ability to effectively deploy capital and make investments in our business; our ability to maintain relationships with prime contractors, subcontractors and joint venture partners; our ability to manage performance and other risks related to customer contracts; the adequacy of our insurance programs designed to protect us from significant product or other liability claims; our ability to declare future dividends based on our earnings, financial condition, capital requirements and other factors, including compliance with applicable laws and contractual agreements; risks associated with our completed spin-off transaction from our former parent, such as disruption to business operations, unanticipated expenses or a failure to realize the expected benefits of the spin-off; and our ability to execute our business plan and long-term management initiatives effectively and to overcome these and other known and unknown risks that we face. These are only some of the factors that may affect the forward-looking statements contained in this release. For further information concerning risks and uncertainties associated with our business, please refer to the filings we make from time to time with the U.S. Securities and Exchange Commission, including the "Risk Factors," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Legal Proceedings" sections of our Annual Report on Form 10-K which may be viewed or obtained through the Investor Relations section of our web site at www.saic.com.

All information in this presentation is as of June 9, 2015. SAIC expressly disclaims any duty to update any forward-looking statement provided in this release to reflect subsequent events, actual results or changes in SAIC's expectations. SAIC also disclaims any duty to comment upon or correct information that may be contained in reports published by investment analysts or others.

In addition, these slides should be read in conjunction with our press release dated June 9, 2015 along with listening to or reading a transcript of the comments of our management delivered in a conference call held on June 9, 2015.

2

Company Overview

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

SAIC Overview

4

• Leading technology integrator specializing in technical, engineering and enterprise IT services to the U.S. government

• 46-year history of mission service delivery and customer relationships

• Significant scale of about $4.4 billion with diversified contract base

• Highly skilled workforce of about 15,000 employees

• Strong and predictable cash flow

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Investment Highlights

Focused on serving our customers leveraging both deep mission domain knowledge and the breadth of enabling IT solutions

Enduring Customer Relationships and Mission-Orientation

Technical Experts Led by Experienced Management

Tailored Operational Model and Competitive Structure

Over 65% of workforce hold a security clearance and work at customer locations

Efficient corporate structure and effective account management and service lines for critical mission delivery

Solid Financial Position Strong cash flow generation from recurring revenue base with margin expansion potential

Full Lifecycle Offerings End-to-end services and solutions support entire mission and enterprise lifecycles

Significant Scale and Diversified Contract Base

One of the largest pure play technical services providers to the U.S. Government; about $4.4B in annual revenues

Offering a compelling value proposition to all stakeholders5

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

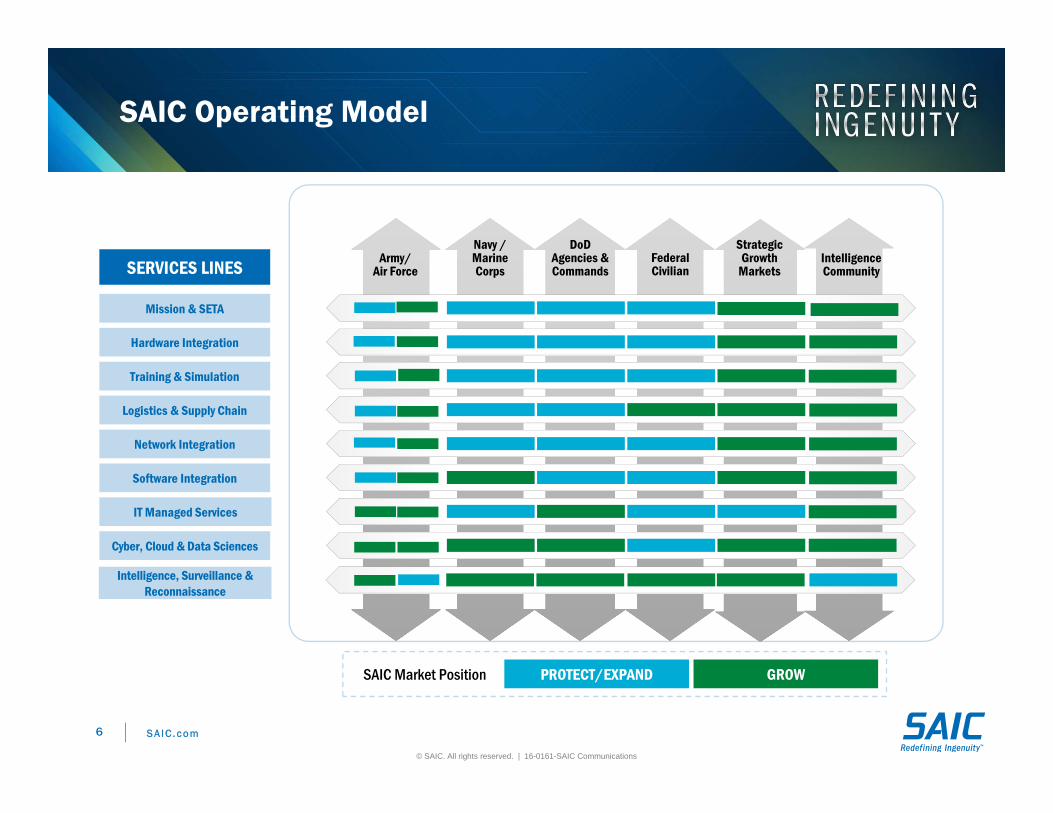

Intelligence, Surveillance & Reconnaissance

SAIC Operating Model

Navy / Marine Corps

DoD Agencies & Commands

Federal Civilian

Strategic Growth

MarketsArmy/

Air ForceIntelligence CommunitySERVICES LINES

Mission & SETA

Hardware Integration

Training & Simulation

Logistics & Supply Chain

Network Integration

Software Integration

IT Managed Services

Cyber, Cloud & Data Sciences

SAIC Market Position GROW PROTECT/EXPAND

6

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

We Are Providing

Full Lifecycle Services & Solutions

7

HardwareIntegration

IT ManagedServices

SoftwareIntegration

Logistics & Supply Chain

Mission & SETA

Cyber, Cloud & Data Science

Network Integration

Training & Simulation

Intelligence, Surveillance, and Reconnaissance

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

• Unified communications• Network core

• Network access, infrastructure & management

• Network security

• Application development and maintenance

• Rapid legacy system modernization• Service-oriented architecture design

• Mobile application development and management

• ERP & COTS integration

• Data center management• End-User & help desk support services• Managed services management

• Operations management services• Network & Security Operations

Center services

• Cloud and virtualized computing infrastructure

• Data science

• Cyber security• Business transformation

Enterprise Information Technology Offerings

Network Integration

Software Integration

Cyber, Cloud &Data Science

IT Managed Services

8

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

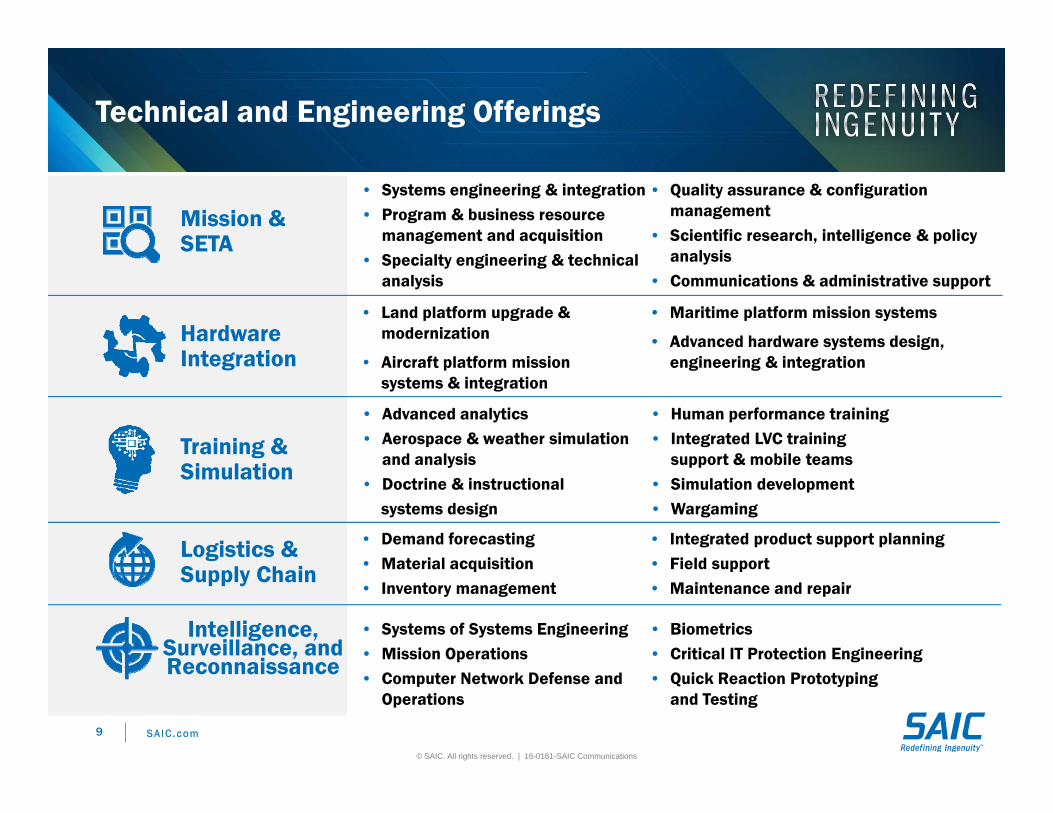

Technical and Engineering Offerings

• Land platform upgrade & modernization

• Aircraft platform mission systems & integration

• Demand forecasting• Material acquisition• Inventory management

• Integrated product support planning• Field support• Maintenance and repair

• Maritime platform mission systems

• Advanced hardware systems design, engineering & integration

Mission &SETA

HardwareIntegration

Logistics & Supply Chain

Training & Simulation

• Systems engineering & integration• Program & business resource

management and acquisition• Specialty engineering & technical

analysis

• Quality assurance & configuration management

• Scientific research, intelligence & policy analysis

• Communications & administrative support

• Advanced analytics• Aerospace & weather simulation

and analysis• Doctrine & instructional

systems design

• Human performance training• Integrated LVC training

support & mobile teams• Simulation development• Wargaming

9

Intelligence, Surveillance, and Reconnaissance

• Systems of Systems Engineering• Mission Operations• Computer Network Defense and

Operations

• Biometrics• Critical IT Protection Engineering• Quick Reaction Prototyping

and Testing

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

SAIC Competitive Landscape

OEM DefenseContractors

Pure Play SETA & Government Services

Diversified IT Services

SAIC competes effectively across this landscape

10

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Employee Demographics

Deployed at customer sites

26%

68%

70%

~ 15,000 E M P L O Y E E S

Hold a security clearance

Protected Veterans status workforce

Employees by Service

Line

Mission & SETA19%

IT ManagedServices17%

SoftwareIntegration14%

HardwareIntegration11%

Training & Simulation8%

Logistics & Supply Chain9%

Cyber, Cloud & Data Science5%

Network Integration5%

11

ISR*12%

*ISR service line expected to be implemented in fall 2015

Company Overview

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Revenue Profile*

Customer Mix

Contract Type

Revenue Mix

DoD Agencies & Commands24%

Navy/Marine Corps25%

Army /Air Force25%

Federal Civilian23%

State/Local/Commercial3%Cost

Reimbursable37%

Time & Materials29%

Fixed PriceSupply Chain Materials15%

SAIC Labor45%

Subcontractor32%

Supply Chain Materials16%

Other Materials7%

~85% IDIQ Revenue; 90%+ recompete win rate*As of SAIC FY2015 ended January 30, 2015

Fixed Price Services19%

13

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

First Quarter Fiscal Year 2016 Results

14(1) Results of Science Applications International Corporation and its consolidated subsidiaries for the first quarter ended May 1, 2015 and May 2, 2014; excludes revenues performed by former

parent company.(2) Adjusted operating income, adjusted EBITDA and free cash flow are non-GAAP financial measures as defined and reconciled in the appendix of this presentation.(3) Excludes $3 million dollars of acquisition and integration costs.

($ in millions; except per share data) FY16 Q1(1)

FY15 Q1(1)

Change

Revenue $998 $961 4%

Operating Income $57 $59 -3%

Operating Income % 5.7% 6.1% -40 bps

Adj. Operating Income %(2)

6.0% 6.1% -10 bps

Adj. EBITDA %(2)

6.5% 6.7% -20 bps

Effective Tax Rate 38.0% 37.9% -10 bps

Diluted EPS(3)

$0.69 $0.69 0%

Operating Cash Flow $29 $34

Free Cash Flow (2)

$28 $27

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Capital Deployment

$13MDividends

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$-

$5

$10

$15

Q1 FY2016**

Dividends

Cash From OperationsLess Capital ExpendituresFree Cash Flow (FCF)*

$29M($1M)$28M

*See Appendix for non-GAAP Measures**First quarter fiscal year 2016 ending May 1, 2015

($M)

Total Cash Deployed(% of FCF*)

46%

15

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Annual Internal Revenue Growth Low single-digit growth

Operating Margin 10 to 20 bps annual improvement

Maximize cash flow generation, free cash flow to exceed net income

Return of capital in excess of operating needs, absent expected higher return capital

deployment opportunities

Leverage (debt to EBITDA) Financial leverage appropriate for SAIC’s

investment requirements and cash generating characteristics

Long Term Financial Targets (on average and over time)

Our forward guidance practice is limited to these long-term targets

16

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

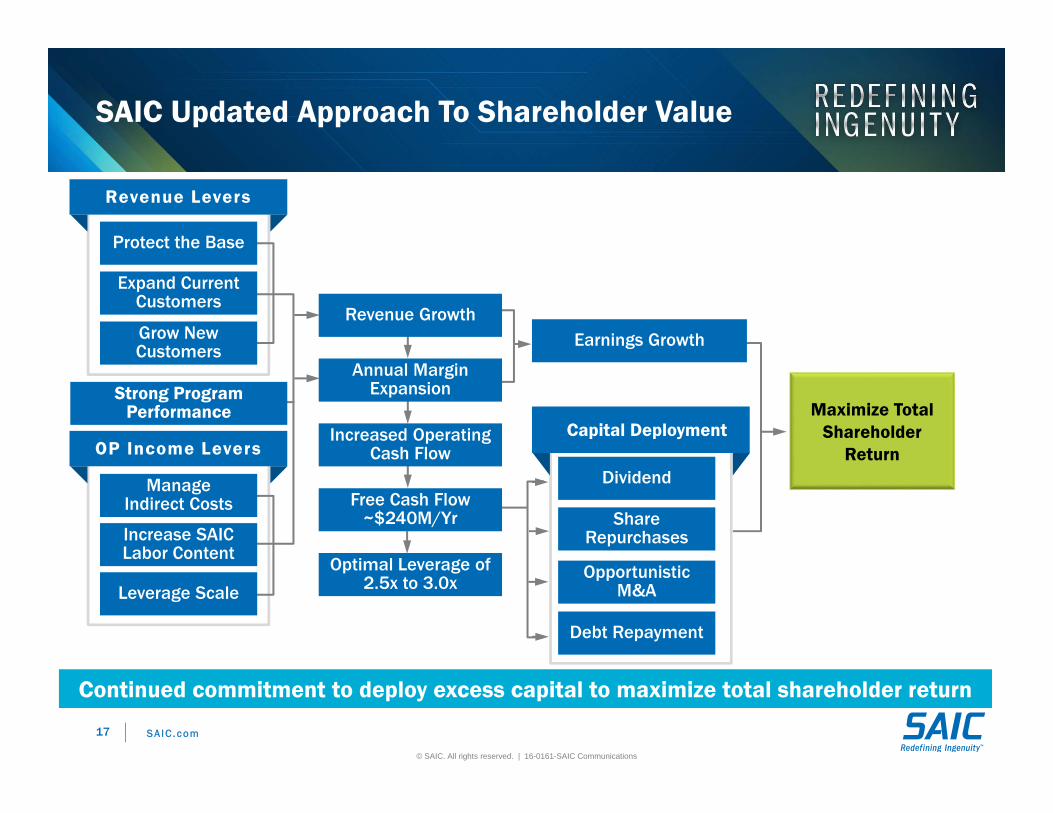

OP Income Levers

SAIC Updated Approach To Shareholder Value

Continued commitment to deploy excess capital to maximize total shareholder return

Revenue Levers

Leverage Scale

Protect the Base

Grow New Customers

Strong Program Performance

Manage Indirect Costs

Expand Current Customers

Increase SAIC Labor Content

Revenue Growth

Annual Margin Expansion

Increased Operating Cash Flow

Free Cash Flow ~$240M/Yr

Optimal Leverage of 2.5x to 3.0x

Maximize Total Shareholder

Return

Earnings Growth

Capital Deployment

Dividend

Share Repurchases

Opportunistic M&A

Debt Repayment

17

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

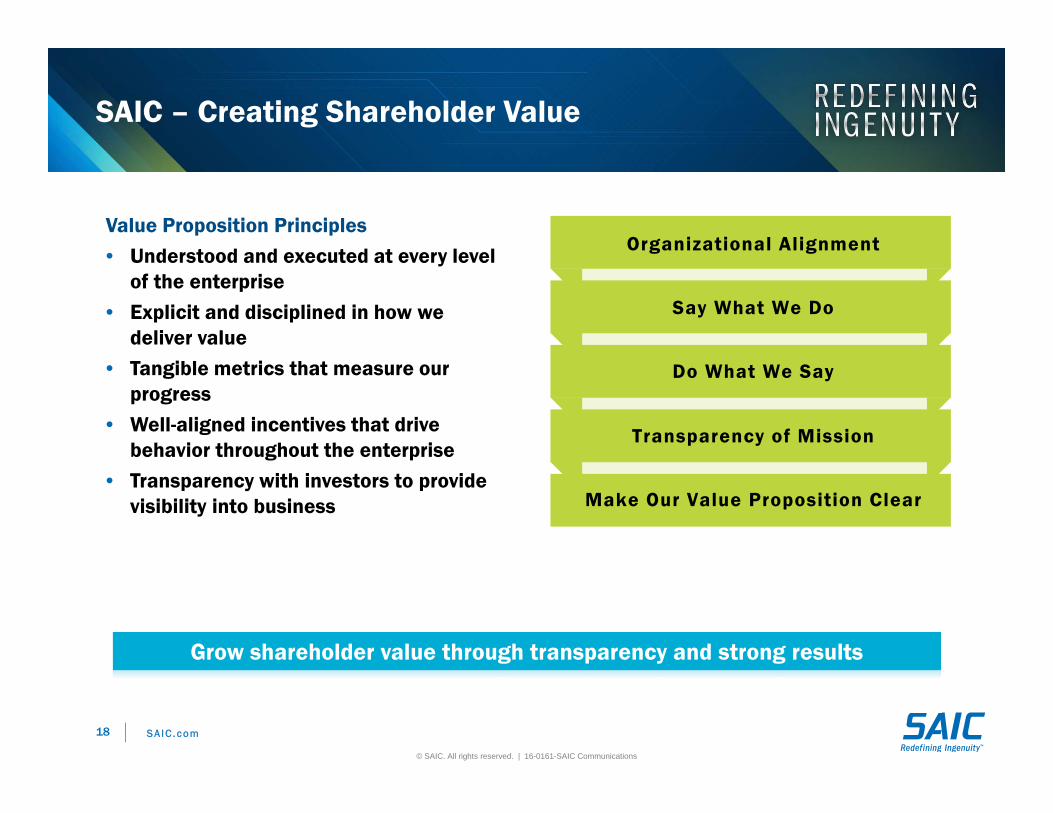

SAIC – Creating Shareholder Value

Value Proposition Principles• Understood and executed at every level

of the enterprise• Explicit and disciplined in how we

deliver value• Tangible metrics that measure our

progress • Well-aligned incentives that drive

behavior throughout the enterprise• Transparency with investors to provide

visibility into business

Grow shareholder value through transparency and strong results

Organizational Alignment

Say What We Do

Do What We Say

Transparency of Mission

Make Our Value Proposition Clear

18

Appendix

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

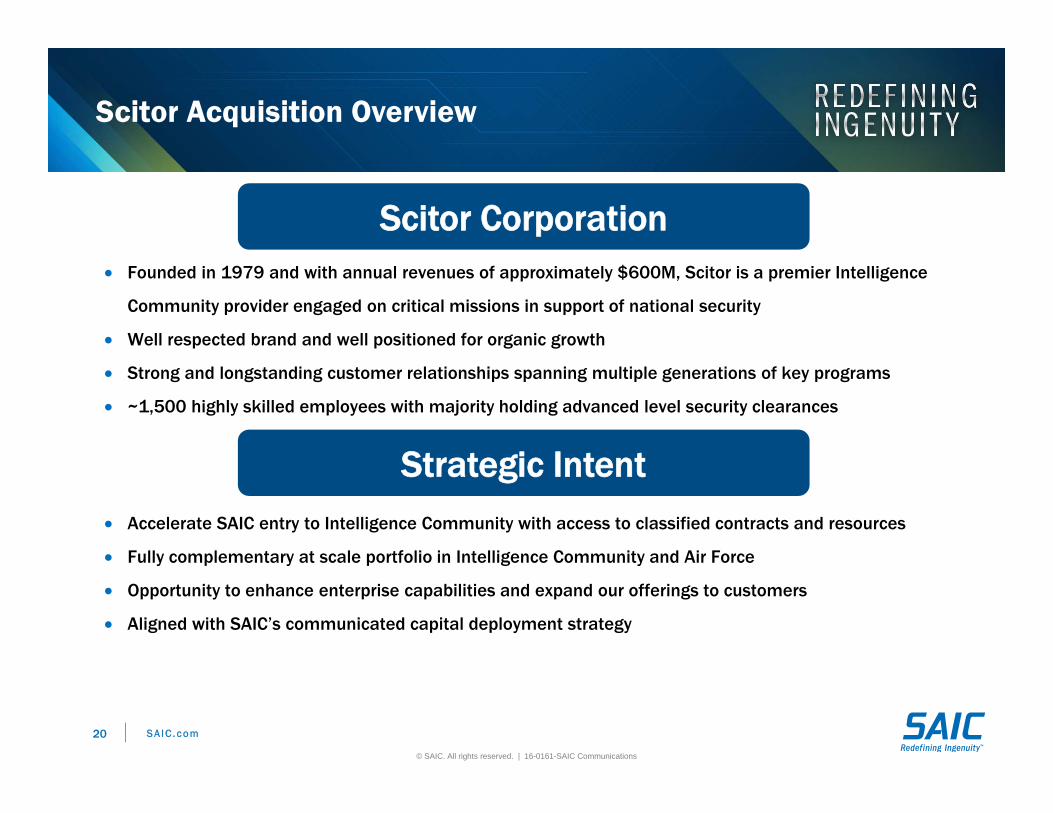

Scitor Acquisition Overview

20

Founded in 1979 and with annual revenues of approximately $600M, Scitor is a premier Intelligence

Community provider engaged on critical missions in support of national security

Well respected brand and well positioned for organic growth

Strong and longstanding customer relationships spanning multiple generations of key programs

~1,500 highly skilled employees with majority holding advanced level security clearances

Scitor Corporation

Accelerate SAIC entry to Intelligence Community with access to classified contracts and resources

Fully complementary at scale portfolio in Intelligence Community and Air Force

Opportunity to enhance enterprise capabilities and expand our offerings to customers

Aligned with SAIC’s communicated capital deployment strategy

Strategic Intent

20

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

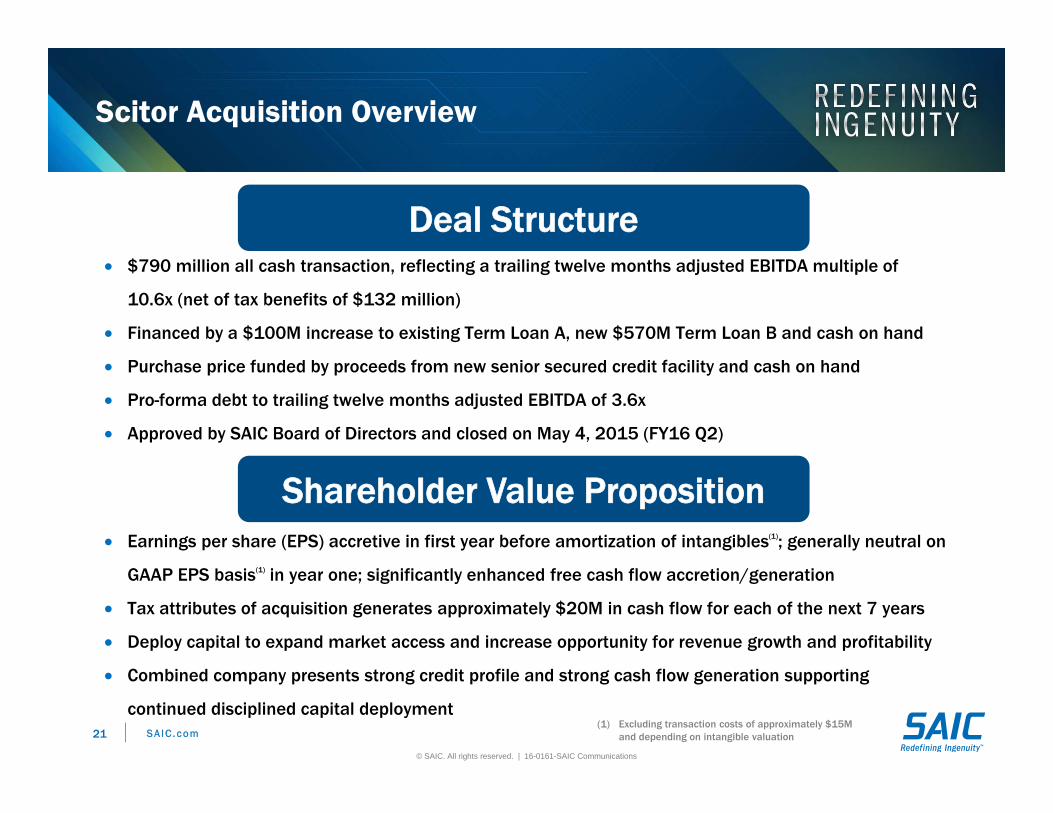

Scitor Acquisition Overview

21

$790 million all cash transaction, reflecting a trailing twelve months adjusted EBITDA multiple of

10.6x (net of tax benefits of $132 million)

Financed by a $100M increase to existing Term Loan A, new $570M Term Loan B and cash on hand

Purchase price funded by proceeds from new senior secured credit facility and cash on hand

Pro-forma debt to trailing twelve months adjusted EBITDA of 3.6x

Approved by SAIC Board of Directors and closed on May 4, 2015 (FY16 Q2)

Deal Structure

Shareholder Value Proposition Earnings per share (EPS) accretive in first year before amortization of intangibles(1); generally neutral on

GAAP EPS basis(1) in year one; significantly enhanced free cash flow accretion/generation

Tax attributes of acquisition generates approximately $20M in cash flow for each of the next 7 years

Deploy capital to expand market access and increase opportunity for revenue growth and profitability

Combined company presents strong credit profile and strong cash flow generation supporting

continued disciplined capital deployment(1) Excluding transaction costs of approximately $15M

and depending on intangible valuation21

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

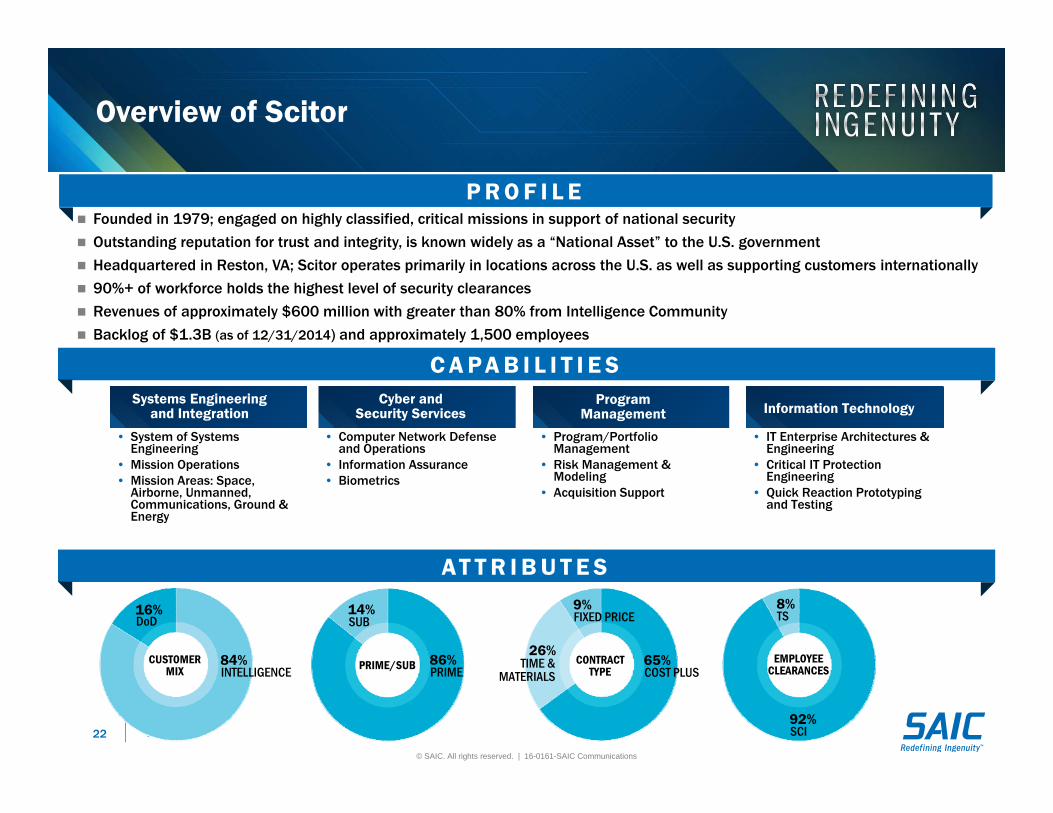

Overview of Scitor

6

Founded in 1979; engaged on highly classified, critical missions in support of national security

Outstanding reputation for trust and integrity, is known widely as a “National Asset” to the U.S. government

Headquartered in Reston, VA; Scitor operates primarily in locations across the U.S. as well as supporting customers internationally

90%+ of workforce holds the highest level of security clearances

Revenues of approximately $600 million with greater than 80% from Intelligence Community

Backlog of $1.3B (as of 12/31/2014) and approximately 1,500 employees

Cyber and Security Services

Systems Engineering and Integration Information Technology

Program Management

• System of Systems Engineering

• Mission Operations• Mission Areas: Space,

Airborne, Unmanned, Communications, Ground & Energy

• Computer Network Defense and Operations

• Information Assurance• Biometrics

• Program/Portfolio Management

• Risk Management & Modeling

• Acquisition Support

• IT Enterprise Architectures & Engineering

• Critical IT Protection Engineering

• Quick Reaction Prototyping and Testing

C A P A B I L I T I E S

P R O F I L E

AT T R I B U T E S

CUSTOMERMIX PRIME/SUB CONTRACT

TYPEEMPLOYEE

CLEARANCES84%INTELLIGENCE

16%DoD

14%SUB

86%PRIME

9%FIXED PRICE

65%COST PLUS

26%TIME &

MATERIALS

92%SCI

8%TS

22

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Overview of Scitor

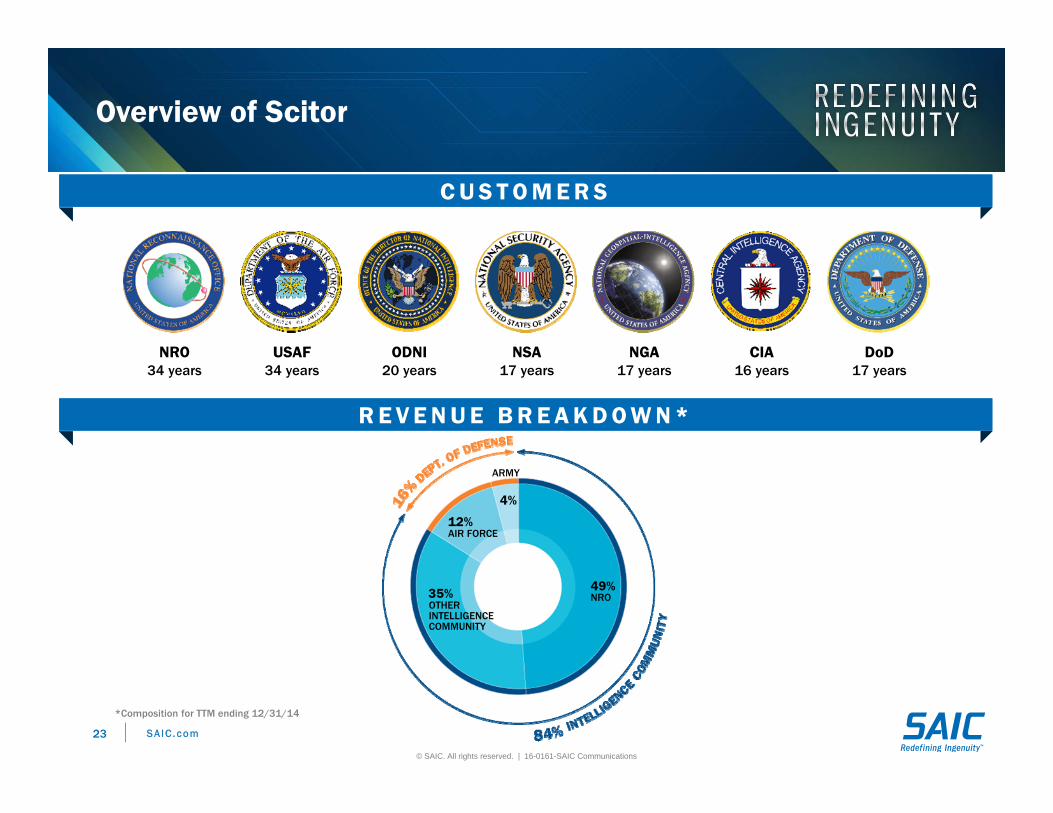

DoD17 years

NGA17 years

NSA17 years

CIA16 years

NRO34 years

ODNI20 years

USAF34 years

*Composition for TTM ending 12/31/14

49%35%

12%

4%

NROOTHER INTELLIGENCE COMMUNITY

AIR FORCE

ARMY

R E V E N U E B R E A K D O W N *

C U S T O M E R S

23

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Scitor Strategic Differentiators

24

Intelligence Community Focus

Focused on highly classified Intelligence Community programs

Capabilities leveraged to broader defense and national security customers

Highest-End / Highest-Value Solutions

Capstone, multi-generational programs of a protected nature

Focus on strategic mission-critical Cyber, C5ISR(1) and Information Sciences

Selective and Sought-After Employer

Scitor’s reputation and strong presence attracts impactful leaders

Limited turnover drives strength and tenure of client relationships

Reputation / Brand Highly respected in Intelligence Community for quality and consistent high performance

High Quality Portfolio withStrong Mission Delivery

Management of contract portfolio emphasizes financial performance,

long-term sustainability and growth

A Leading, Large National Security Provider(1) Command, Control, Communications, Computers, Combat Systems, Intelligence, Surveillance, and Reconnaissance

S T R AT E G I C P O S I T I O N I N G

24

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Strategic Rationale for Acquiring Scitor

25

• Highly complementary acquisition that aligns with our previously communicated strategy to gain access to Intelligence and Air Force markets

• Creates opportunity to deliver existing SAIC technology integration services into a market with similar mission requirements

• Recognized leader within the Intelligence Community; acquisition facilitates expansion into classified contracts, personnel and infrastructure

• Pure-play intelligence asset with key prime contracts well positioned for organic growth

• Enables SAIC to “stand up” an Intelligence business with limited integration risk

• Maximizes new customer and contract vehicle access without paying for overlap

• Business model compatible with current services portfolio; low capital requirements and steady cash flows

• Strong cultural alignment with shared values and mission focus

Scitor Represents an Opportunity to Position SAIC as a Leading, Trusted Service Provider to the Intelligence Community

25

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

+ =

Combined Company Revenue Profile(1)

26

26%FEDERAL CIVILIAN

70%DoD

84%INTELLIGENCE

16%DoD

63%DoD

11%INTELLIGENCE

22%

Revenue of $3.8B Revenue of ~$600M Revenue of $4.4B

PRO FORMA

(1) For SAIC, financial metrics represent FYE 1/30/15 and for Scitor represent TTM 12/31/14.

*Includes state and local, commercial and international customers.

Combined Company More Diversified at Scale

FEDERAL CIVILIAN

4%

OTHER*

4%

OTHER*

26

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Financial Rationale

27

• Combined company will have ~$4.4 billion of annual revenues(1)

• Combined company adjusted EBITDA of ~$361 million(1) or 8.1% margin after inclusion of Scitor’s adjusted EBITDA(1)

• EPS accretive in first year before amortization of intangibles(2); generally neutral on GAAP EPS basis(2) ; significantly enhanced free cash flow generation

• Estimated value of tax attributes in the acquisition of $132 million generates approximately $20 million of cash flow for the next 7 years

• Identified potential annual cost synergies of at least $20 million realized by year 3

• Combined company presents strong credit profile and strong cash flow for continued disciplined capital deployment

Disciplined Deployment of Capital for Shareholder Value Creation

(2) Excluding transaction costs and depending on intangible valuations

(1) Pro-forma trailing twelve months; see reconciliation in appendix

27

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Non-GAAP Reconciliation –Adjusted Operating Income

($ in millions)

“Adjusted operating income” and “Adjusted operating margin” are non-GAAP financial measures that are reconciled in this schedule to the most directly comparable GAAP financial measures. These non-GAAP financial measures provide investors with greater visibility into operating income and cash flows provided by operating activities, but they are not meant to be considered in isolation or as a substitute for comparable GAAP measures and should be read only in conjunction with SAIC's consolidated financial statements prepared in accordance with GAAP. The methods used to calculate these non-GAAP financial measures may differ from the methods used by other companies and so similarly titled non-GAAP financial measures presented by other companies may not be comparable to those provided in this schedule.

Three Months Ended Three Months Ended($ in mil l ions) May 1, 2015 May 2, 2014

Operating Income 57$ 59$ Acquisition and integration costs 3 ‐ Adjusted Operating Income 60$ 59$

Operating Margin 5.7% 6.1%Adjusted Operating Margin 6.0% 6.1%

28

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

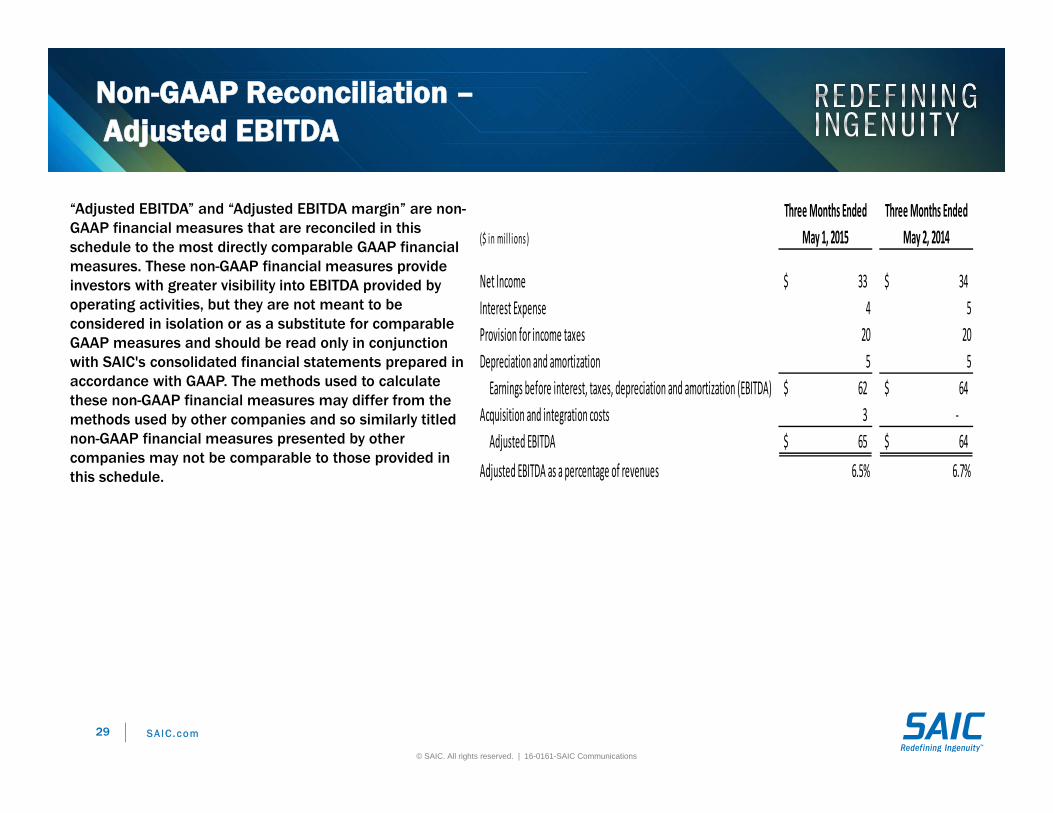

Non-GAAP Reconciliation –Adjusted EBITDA

($ in millions)

“Adjusted EBITDA” and “Adjusted EBITDA margin” are non-GAAP financial measures that are reconciled in this schedule to the most directly comparable GAAP financial measures. These non-GAAP financial measures provide investors with greater visibility into EBITDA provided by operating activities, but they are not meant to be considered in isolation or as a substitute for comparable GAAP measures and should be read only in conjunction with SAIC's consolidated financial statements prepared in accordance with GAAP. The methods used to calculate these non-GAAP financial measures may differ from the methods used by other companies and so similarly titled non-GAAP financial measures presented by other companies may not be comparable to those provided in this schedule.

Three Months Ended Three Months Ended($ in mil l ions ) May 1, 2015 May 2, 2014

Net Income 33$ 34$ Interest Expense 4 5Provision for income taxes 20 20Depreciation and amortization 5 5 Earnings before interest, taxes, depreciation and amortization (EBITDA) 62$ 64$ Acquisition and integration costs 3 ‐ Adjusted EBITDA 65$ 64$ Adjusted EBITDA as a percentage of revenues 6.5% 6.7%

29

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Non-GAAP Reconciliation –Free Cash Flow

($ in millions)

“Free cash flow” is a non-GAAP financial measure that is reconciled in this schedule to the most directly comparable GAAP financial measures. These non-GAAP financial measures provide investors with greater visibility into operating income and cash flows provided by operating activities, but they are not meant to be considered in isolation or as a substitute for comparable GAAP measures and should be read only in conjunction with SAIC's consolidated financial statements prepared in accordance with GAAP. The methods used to calculate these non-GAAP financial measures may differ from the methods used by other companies and so similarly titled non-GAAP financial measures presented by other companies may not be comparable to those provided in this schedule.

Three Months Ended Three Months Ended($ in mil l ions) May 1, 2015 May 2, 2014

Total cash flows provided by operating activities, as reported 29$ 34$ Expenditures for property, plant and equipment (1) (7) Free cash flow 28$ 27$

30

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Shareholder and Stock Information

► Initial Public Offering: Science Applications International Corporation (SAIC) common stock began trading on the New York Stock Exchange (NYSE) on September 30, 2013.

► Fiscal Year 2015: SAIC’s fiscal year starts on February 1, 2014 and ends on January 30, 2015.

► Share Price Information: SAIC’s common stock is listed on the NYSE under ticker symbol SAIC. Share price information can be found at http://investors.saic.com/stock-information

► State of Incorporation: SAIC is incorporated in the state of Delaware

► Dividends: SAIC expects to declare and pay regular quarterly cash dividends in the future; however, the actual declaration of any such future dividends and the establishment of the per share amount, record dates and payment dates for any such future dividends are subject to the discretion of the Board. The table below lists SAIC’s dividends for the past 12 months:

Declaration Date Record Date Payable Date Amount Type

06/03/15 07/15/15 07/30/15 $0.31 Cash, Quarterly

03/25/15 04/15/15 04/30/15 $0.28 Cash, Quarterly

12/03/14 01/15/15 01/30/15 $0.28 Cash, Quarterly

09/03/14 10/15/14 10/30/14 $0.28 Cash, Quarterly

06/04/14 07/15/14 04/30/14 $0.28 Cash, Quarterly

03/20/14 04/15/14 04/30/14 $0.28 Cash, Quarterly

12/12/13 01/15/14 01/30/14 $0.28 Cash, Quarterly

10/03/13 10/15/13 10/30/13 $0.28 Cash. Quarterly

31

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Shareholder and Stock Information (continued)

► Annual Stockholder Meeting : Stockholders attended SAIC’s annual meeting of stockholders on June 3, 2015 at SAIC facilities located at 1710 SAIC Drive, McLean VA. At the annual meeting, stockholders acted upon the matters set forth in the notice of meeting, including the election of certain directors and the selection of the Company’s independent registered public accounting firm. SAIC’s senior management presented information about performance during fiscal year 2015 and were available to answer questions from stockholders.

► Transfer Agent :

Computershare

PO Box 43078

Providence, RI 02940-3078

1-866-400-7242

www.computershare.com/saic

► Independent Registered Public Accounting Firm:

Deloitte & Touch LLP

McLean, VA

32

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Shareholder and Stock Information (continued)

► Executive Leadership:

― Anthony J. Moraco, Chief Executive Officer

― John R. Hartley, Chief Financial Officer

― Nazzic S. Keene, Sector President

― Doug Wagoner, Sector President

► Board of Directors:

― Edward Sanderson Jr., Chairman

― Anthony J. Moraco, Chief Executive Officer

― Bob Bedingfield, Independent Director

― Deborah Dunie, Independent Director

― Tommy Frist, Independent Director

― John Hamre, Independent Director

― Tim Mayopoulus, Independent Director

― Donna Morea, Independent Director

― Steven Shane, Independent Director

33

SA IC . com

© SAIC. All rights reserved. | 16-0161-SAIC Communications

Shareholder and Stock Information (continued)

► Website: www.saic.com

► Inquiries from securities analysts, portfolio managers, institutional investors and other interested investors in SAIC should be directed to:

Paul E. Levi

Director of Investor Relations

(703) 676-2283

► Inquiries from media should de directed to:

Lauren A. Presti

(703) 676-8982

► Inquiries regarding corporate governance should de directed to:

Paul H. Greiner

(858) 826-7360

![Science Applications International Corporation (SAIC ... · PDF fileScience Applications International Corporation (SAIC) [NYSE: SAIC] ... Science Applications International Corporation](https://img.pdfslide.us/doc/110x75/5ab54bee7f8b9a6e1c8ca2a2/science-applications-international-corporation-saic-applications-international.jpg)