Embed Size (px)

Citation preview

FAC2601/201/1/2010 SCHOOL OF ACCOUNTING SCIENCES

DEPARTMENT OF FINANCIAL ACCOUNTING

FINANCIAL ACCOUNTING FOR COMPANIES

TUTORIAL LETTER 201/1/2010 FOR FAC2601 (FIRST SEMESTER)

Dear Student Enclosed please find information regarding the examination as well as the solutions to assignments 01/2010 – 03/2010. Yours faithfully Mr GJ Steyn Tel: (012) 429-4343 [email protected] Ms N Passier Tel: (012) 429-3932 [email protected] LECTURERS: ACCOUNTING II (FAC2601) Ms D Kruger Tel: (012) 429-4596 ADMINISTRATIVE PERSONNEL PLEASE NOTE THAT THE NEW EXAMINATION DATE IS 12 MAY 2010. ANNEXURE A: EXAMINATION ANNEXURE B: SOLUTION TO ASSIGNMENT 01/2/2010 ANNEXURE C: SOLUTION TO ASSIGNMENT 02/2/2010 ANNEXURE D: SOLUTION TO ASSIGNMENT 03/2/2010 ANNEXURE E: PREVIOUS EXAMINATION PAPER AND SOLUTION

2 ANNEXURE A: EXAMINATION (i) We would like to draw your attention once more to tutorial letter 301 on examination

technique and we would like to stress a few items:

- Number all your answers clearly. - Answer each question on a new page. Please do not answer two questions on the

same page. - Keep to the time table. When the time for a question is over you must carry on with the

next question. You cannot afford to leave out a question. - Write neatly and structure your work so that it is easy to read. - It is important to do what is asked of you to do so that you do not do unnecessary work

and thus waist valuable time. - Work though all your study material and do not just concentrate on old exam papers.

(ii) The examination consists of a two hour paper counting a total of 100 marks. The whole syllabus can be tested in this paper. Here are some tips to improve your future studies (these tips are based on what the students did wrong in previous exams). Remember this is not a summary of what to study, it is just guidelines for the examinations:

1. Statement of comprehensive income (SoCI):

- Know how to do calculations on finance cost and show CALCULATIONS clearly. - Remember to show/calculate other comprehensive income. - Note on profit before tax: Know how to disclose different disclosable items on this note

and show calculations in brackets.

2. Statement of financial position (SoFP):

- Show all calculations. This can be done in brackets next to the item or reference it back to your calculation on another page, but remember to reference your work.

- Study how the notes on financial statements are disclosed and show calculations separately on these notes if necessary. Notes are not just calculations, it is extra information for the users of the statements and is disclosable.

- Property, plant and equipment (PPE) is always one entry in the SoFP. The total you get in the note on PPE must be the same as the total in the SoFP. You get a principal mark for having the same amount. Remember to give the extra information regarding the description of the property just underneath the note on PPE.

3. Statement of changes in equity:

- Know how to calculate opening balances. You can only improve by exercising this type

of questions under examination conditions. - Please note that dividends are declared at the end or the beginning of the financial

year after all relevant transactions are accounted for. Read what the question asks you to do and always show all your calculations with specific reference to all the types of dividends (eg. ordinary dividends, cumulative preference dividends and preference dividends).

4. Theory:

Please study all relevant questions in assignment 3 and study guide, refer to text book as well where necessary.

FAC2601/201/1 3

ANNEXURE B: SOLUTION ASSIGNMENT 01/2010 – FIRST SEMESTER UNIQUE NUMBER: 844292 ANSWERS 1. 3 2. 1 3. 1 4. 3 5. 4 6. 2 7. 4 8. 3 9. 2 10. 3 MARKING PLAN Marks 2 marks each 20

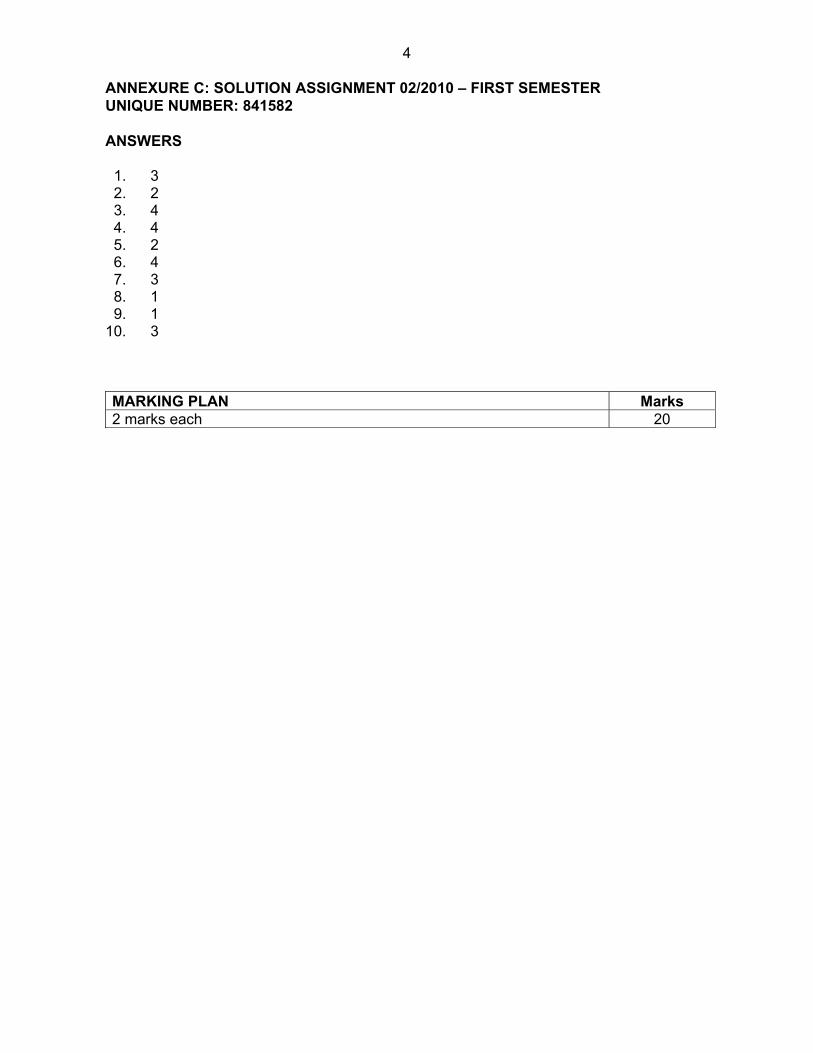

4 ANNEXURE C: SOLUTION ASSIGNMENT 02/2010 – FIRST SEMESTER UNIQUE NUMBER: 841582 ANSWERS 1. 3 2. 2 3. 4 4. 4 5. 2 6. 4 7. 3 8. 1 9. 1 10. 3 MARKING PLAN Marks 2 marks each 20

FAC2601/201/1 5

ANNEXURE D: SOLUTION ASSIGNMENT 03/2010 SOLUTION 1 1.1 Capital redemption reserve fund A capital redemption reserve fund is created when redeemable preference shares are redeemed out of profits available for distribution. According to Section 98(1)(b) of the Companies Act, 1973, where any such shares are redeemed otherwise than out of the proceeds of a new issue, there shall, out of profits which would otherwise have been available for dividends, be transferred to a reserve fund, to be called the capital redemption reserve fund, a sum equal to the nominal amount of the shares redeemed. Share premium A share premium account is created when shares are issued for an amount exceeding nominal or par value. Stated capital Stated capital represents issued no par value shares 1.2 Application of share premium According to Section 76(3) of the Companies Act, the share premium may be applied by the company for the following: - For issuing unissued shares as fully paid capitalisation shares. - For writing off preliminary expenses or expenses of, or commission paid or discount

allowed on the issue of any shares of the company. - For providing the premium payable on redemption of any redeemable preference shares

of the company. - For the payment of the premium over the par value in the case of an acquisition of shares

in accordance with section 85.

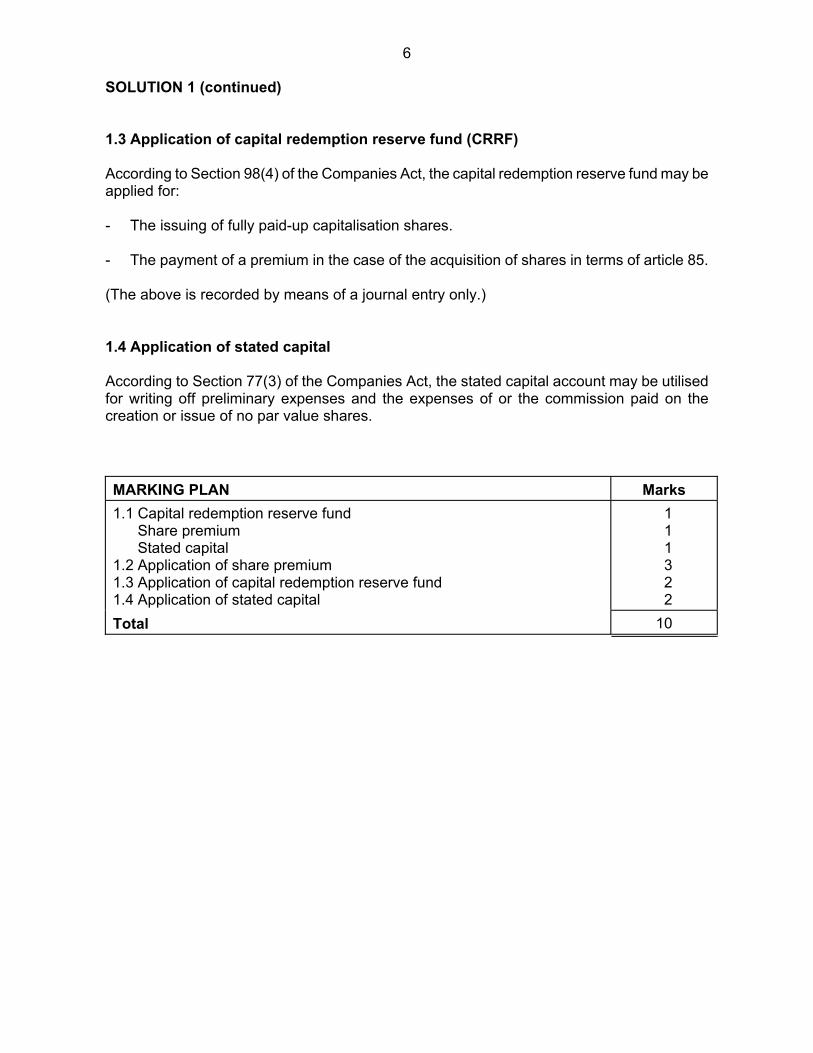

6 SOLUTION 1 (continued) 1.3 Application of capital redemption reserve fund (CRRF) According to Section 98(4) of the Companies Act, the capital redemption reserve fund may be applied for: - The issuing of fully paid-up capitalisation shares. - The payment of a premium in the case of the acquisition of shares in terms of article 85. (The above is recorded by means of a journal entry only.) 1.4 Application of stated capital According to Section 77(3) of the Companies Act, the stated capital account may be utilised for writing off preliminary expenses and the expenses of or the commission paid on the creation or issue of no par value shares. MARKING PLAN

Marks

1.1 Capital redemption reserve fund Share premium Stated capital

1.2 Application of share premium 1.3 Application of capital redemption reserve fund 1.4 Application of stated capital

1 1 1 3 2 2

Total

10

FAC2601/201/1 7

SOLUTION 2 VULA LIMITED EXTRACT FROM THE STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2006

Notes RRevenue Cost of sales

12 000 000 (5 000 000)

Gross profit Other operating income Distribution cost Administrative expenses Other operating expenses (1 025 000 – 255 000) Finance cost [(1 800 000 x 15% x 6/12) + (1 600 000 x 15% x 6/12)] (Calculation 2)

7 000 000 245 000

(1 200 000) (3 000 000) (770 000)

(255 000)Profit before tax 1 Income tax expense

2 020 000 (585 800)

Profit for the year 1 434 200 VULA LIMITED NOTE FOR THE YEAR ENDED 28 FEBRUARY 2006 1. Profit before tax is disclosed after taking the following items into account,

amongst others:

Income Profit on sale of non-current asset

R

10 000 Income from subsidiaries - Dividends - Interest

90 000 45 000

Income from other financial assets - Listed investments - Dividends - Unlisted investments - Dividends

40 000 60 000

Expenses Directors’ remuneration Executive directors

781 000

- Emoluments (766 000 + 5 200) - Less: Paid by subsidiary

771 200 (5 200)

Total paid by company 766 000 Non-executive directors - Emoluments (15 000 + 418 400) - Less: Paid by subsidiary

433 400 (418 400)

Total paid by company 15 000

8 SOLUTION 2 (continued)

Depreciation (36 000 + 525 000 + 66 500) R

627 500

Auditors’ remuneration - Fees for audit - Expenses

75 000 15 000

Loss on sale of non-current asset 14 000

Calculations 1. Directors’ remuneration

Executive Non-executive

Vula Ltd R

Bolo Ltd

R

Vula Ltd

R

Bolo Ltd

R A Salary

Entertainment allowance Fees for attending meetings

7 000

200 000 12 000 3 200

B Salary

Entertainment allowance Fees for attending meetings

300 000 24 000 4 000

C Salary

Fees for attending meetings

180 000 4 000

D Fees for attending meetings

4 000

E Fees for attending meetings Salary

4 000

3 200 200 000

G Salary Fees for attending meetings

250 000 4 000

5 200

766 000 5 200 15 000 418 400

FAC2601/201/1 9

SOLUTION 2 (continued) 2. Finance cost

Longterm loan Total payments payable (according to question (note 10)) 10 Less: Payments made up to 28/02/2006 2 Payments outstanding 8

R Outstanding loan as per list of balances 1 600 000 R1 600 000 = 8 payments One payment is thus R1 600 000 / 8 200 000 Loan at end of year 1 600 000 Plus: One payment made during the year 200 000 Loan at beginning of year 1 800 000 Outstanding amount 1/3/2005 – 31/8/2005 1 800 000 Outstanding amount 1/9/2005 – 28/2/2006 1 600 000 Finance charges is calculated at 15% on the above two amounts

3. Depreciation R 3.1 Buildings Cost price 1 800 000 Depreciation R1 800 000 @ 2% p.a. 36 000

3.2 Plant and machinery Cost price 3 500 000 Depreciation R3 500 000 @ 15% p.a. 525 000

3.3 Furniture and equipment Carrying amount 28/2/2006 (R700 000 – R101 500) 598 500 Cost price 100/90 x R598 500 665 000 Depreciation 10% x R665 000 66 500

or Cost price 1/9/2004 700 000 Less: Depreciation 10% x 700 000 x 6/12 35 000 Carrying amount 28/2/2005 665 000

10 SOLUTION 2 (continued) MARKING PLAN Marks Statement of comprehensive income Revenue Cost of sales Other operating income Distribution cost Administrative expenses Other operating expenses Finance cost Income tax expense Note Profit on sale of non-current asset Income from subsidiary Income from other financial assets Executive directors’ remuneration Emoluments Paid by subsidiary Non-executive directors’ remuneration Emoluments Paid by subsidiary Depreciation Auditors’ remuneration Fees for audit Expenses Loss on sale of non-current asset

1 1 1 1 1 2 2 1 1 2 3

31/2 1

21/2 1 3 1 1 1

Total 30

FAC2601/201/1 11

SOLUTION 3 LAST RESORT LIMITED EXTRACT FROM THE STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 29 FEBRUARY 2008

Notes R Revenue (7 980 000 x 100 / 114) Cost of sales

7 000 000 (2 800 000)

Gross profit Other income (38 000 + 50 000 + 13 000) Administrative expenses Distribution cost Other operating expenses [370 000 – (15% x 120 000 x 6/12) – (15% x 90 000 x 6/12)] Finance cost (9 000 + 6 750)

4 200 000 101 000 2 170 000

(268 000) (354 250)

(15 750)

Profit before tax 1 Income tax expense

1 493 000 (421 950)

Profit for the period 1 071 050 LAST RESORT LIMITED NOTE FOR THE YEAR ENDED 29 FEBRUARY 2008 1. Profit before tax is disclosed after taking the following, amongst others, into

account:

Income Fair value adjustment [100 000 x ,50(R3,00 – R2,50)] Profit on sale of non-current asset [85 000 – (80 000 – 8 000)]

R

50 000 13 000

Income from subsidiary - Dividends - Interest

12 000 6 000

Income from other financial assets - Listed investments - Dividends 20 000 Expenses Directors’ remuneration Executive directors 486 000 - Emoluments [240 000 + 200 000 + 12 000 + (2 x 5 000)] - Pension (managing director)

462 000 24 000

Non-executive directors 137 000 - Emoluments [120 000 + (1 x 5 000)] - Pension (chairman)

125 000 12 000

Auditors’ remuneration 48 000 - Fees for audit - Expenses

40 000 8 000

Depreciation (calculation 1) 59 000

12 SOLUTION 3 (continued) Calculations: 1. Depreciation 1.1 Depreciation on equipment

Carrying amount 28/2/2008 Cost price (48 000 x 100 / 40) or (48 000 x 5/2) Depreciation (20% x 120 000)

R

48 000 120 000 24 000

1.2 Depreciation on motor vehicles 1.2.1 Vehicle sold

Carrying amount 28/2/2007 Depreciation 1/3/2007 – 31/8/2007 (20% x R80 000 x 6/12) Carrying amount 31/8/2007

80 000 8 000 72 000

1.2.2 Rest of vehicles

Carrying amount 29/2/2008 (240 000 – 60 000 – 72 000) Carrying amount 1/3/2007 (100/80 x 108 000) Depreciation 1/3/2007 – 29/2/2008 (20% x 135 000)

108 000 135 000 27 000

1.3 Total depreciation (24 000 + 8 000 + 27 000) 59 000 MARKING PLAN Marks Statement of comprehensive income Revenue Cost of sales Other income Administrative expenses Distribution expenses Other operating expenses Finance cost Income tax expense Note Fair value adjustment Profit on sale on non-current asset Income from subsidiary Income from financial assets Director’s remuneration Auditor’s remuneration Depreciation

2 1 3 1 1 2 2 1 1 1 2 1 3 1 3

Total 25

FAC2601/201/1 13

SOLUTION 4 VISION LIMITED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 28 FEBRUARY 2006

Stated capital - ordinary shares

R

10% Cumulative preference

share capital

R

12% Non-cumulativepreference

share capital

R

Share premium

R

Surplus onrevaluationof assets

R

Capital redemptio

n reserve

fund R

Reserve for

increased replace-

ment cost of non-current assets

R

Retained earnings

R Total

R Balance 1 March 2005 1 500 000 300 000 550 000 50 000 500 000 180 000 250 000 350 000 3 680 000 Comprehensive Income for the year Dividends (calculation 1) Preference – cumulative Preference – non-cumulative Ordinary Capitalisation shares issued (1 200 000/6) x R1,25 Share issue expenses written off Transfer to reserve

250 000

(25 000)

(50 000)

1 000 000

(180 000)

90 000

800 000

(60 000)

(66 000)(140 000) (20 000)

(90 000)

1 800 000

(60 000)

(66 000) (140 000)

-

(25 000)-

Balance 28 February 2006 1 725 000 300 000 550 000 - 1 500 000 - 340 000 774 000 5 189 000

Calculation 1 Dividends

R 266 000

Cumulative preference (R300 000 x 10% x 2 years) Non-cumulative preference (R550 000 x 12%) Ordinary (1 400 000 x 10c)

60 00066 000

140 000 Note 1. Calculation of dividends in cents is done on the number of shares while the calculation

of dividends as a percentage (%) is done on rand (R) values. 2. Par value of shares is R1,25 and not R1,00. MARKING PLAN Marks Statement of changes in equity Stated capital – ordinary shares Share premium 12% Non-cumulative preference share capital 10% Cumulative preference share capital Surplus on revaluation of assets Capital redemption reserve fund Reserve for increased replacement cost of non-current assets Retained earnings

3½ 1½ ½ ½ 1½ 1½ 1½ 9½

Total 20

14 SOLUTION 5 TRIO LIMITED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2006

Ordinary share capital

R

Share premium

R

Stated capital

– ordinar

y shares

R

12% Cumula-tive pre-ference share capital

R

Surplus on

Revalua-tion of assets

R

Capital redemption

reserve fund

R

Reserve for

replace-ment of assets

R

Retainedearnings

R Total

R Balance 1 July 2005 432 000 27 000 - 150 000 - 60 000 20 000 80 000 769 000 Comprehensive income for the year Shares issued 1 January 2006 Shares issued 31 March 2006 Capitalisation shares issued Share issue expenses written off Transfer to replacement reserve Conversion of shares Dividends declared* Preference shares Ordinary shares

48 000 60 000

(540 000)

1 000 8 000

(16 000)

(20 000)

560 000

50 000

50 000

(60 000)

70 000

200 000

(70 000)

(39 000) (90 000)

250 000 51 000 56 000

- (16 000)

- -

(39 000) (90 000)

Balance 30 June 2006 - - 560 000 200 000 50 000 - 90 000 81 000 981 000

*Dividends Preference

R 39 000

(12% x R150 000 x 2 years) (12% x R50 000 x 6 months)

36 0003 000

Ordinary (360 000 + 40 000 + 50 000) shares x 20c 90 000 Note 1. Calculation of dividends in cents is done on the number of shares while the calculation

of dividends as a percentage (%) is done on rand (R) values. 2. Par value of shares is R1,20 and not R1,00. MARKING PLAN Marks Statement of changes in equity Ordinary share capital Share premium Stated capital – ordinary shares 12% Cumulative preference share capital Surplus on revaluation of assets Capital redemption reserve fund Reserve for replacement of assets Retained earnings

5 5 1 3 1 2 2 7

Total 26

FAC2601/201/1 15

SOLUTION 6 6.1 TRIO LIMITED NOTES FOR THE YEAR ENDED 30 JUNE 2006 6. NON-CURRENT LIABILITIES

Long-term liability Secured 12% Long-term loan Less: Short-term portion transferred to current liabilities

R

80 000 (20 000)

60 000

The loan is secured by a first mortgage bond over fixed property. Interest is calculated at 12% per annum. The capital portion is repayable in five equal annual instalments from 30 April 2006.

6.2 TRIO LIMITED NOTES FOR THE YEAR ENDED 30 JUNE 2006 1. Property, plant and equipment

Land R

BuildingsR

MachineryR

Furniture and

equipment R

Total R

Carrying amount 1 July 2005 100 000 480 000 300 000 62 000 942 000 Cost Accumulated depreciation

100 000-

500 000 (20 000)

400 000 (100 000)

90 000 (28 000)

1 090 000 (148 000)

Revaluation Disposal at carrying amount Additions at cost Depreciation

50 000- - -

- - -

(10 000)

- - -

(75 000)

- (1 250) 15 000 (18 350)

50 000 (1 250) 15 000

(103 350)Carrying amount 30 June 2006 150 000 470 000 225 000 57 400 902 400 Valuation/Cost Accumulated depreciation

150 000-

500 000 (30 000)

400 000 (175 000)

100 000 (42 600)

1 150 000 (247 600)

Land and buildings are situated on erf 3510, George and consist of an office block. It was revalued on 31 October 2005 by mr Black, a sworn appraiser, at replacement value of R150 000.

16 SOLUTION 6 (continued) 6.3 TRIO LIMITED EXTRACT FROM THE STATEMENT OF FINANCIAL POSITION AS AT

30 JUNE 2006 Notes R

ASSETS Non-current assets

962 400

Property, plant and equipment 1 Investment in subsidiary

902 400 60 000

Current assets

276 600

Inventory Trade and other receivables Other financial assets Cash and cash equivalents

80 200 65 400 60 000 71 000

Total assets 1 239 000 Calculations:

1. Property, plant and equipment 1.1 Buildings Depreciation – current year (2% x R500 000)

R

10 000 1.2 Machinery

Carrying amount 30 June 2006 – given Carrying amount 30 June 2005 (R225 000 x 100/75) Cost 30 June 2004 (R300 000 x 100/75) Depreciation – current year (R300 000 x 25%) Depreciation – previous year (R400 000 x 25%)

225 000 300 000 400 000 75 000

100 000 1.3 Furniture and equipment

Cost 30 June 2006 – given Cost of addition 31 March 2006 Cost of disposal 31 March 2006

100 000 (15 000)

5 000 Cost 30 June 2005 90 000

Depreciation – current year New computer [R(15 000 – 3 000) x 20% x 3/12] Computer sold (R5 000 x 20% x 9/12) Remaining equipment (R85 000 x 20%)

600 750

17 000 Total 18 350 Accumulated depreciation on disposal (R3 000 + 750) 3 750 Carrying amount of disposal (R5 000 – 3 750) 1 250

Accumulated depreciation 30 June 2005 (R42 600 + 3 750 – 18 350) 28 000

FAC2601/201/1 17

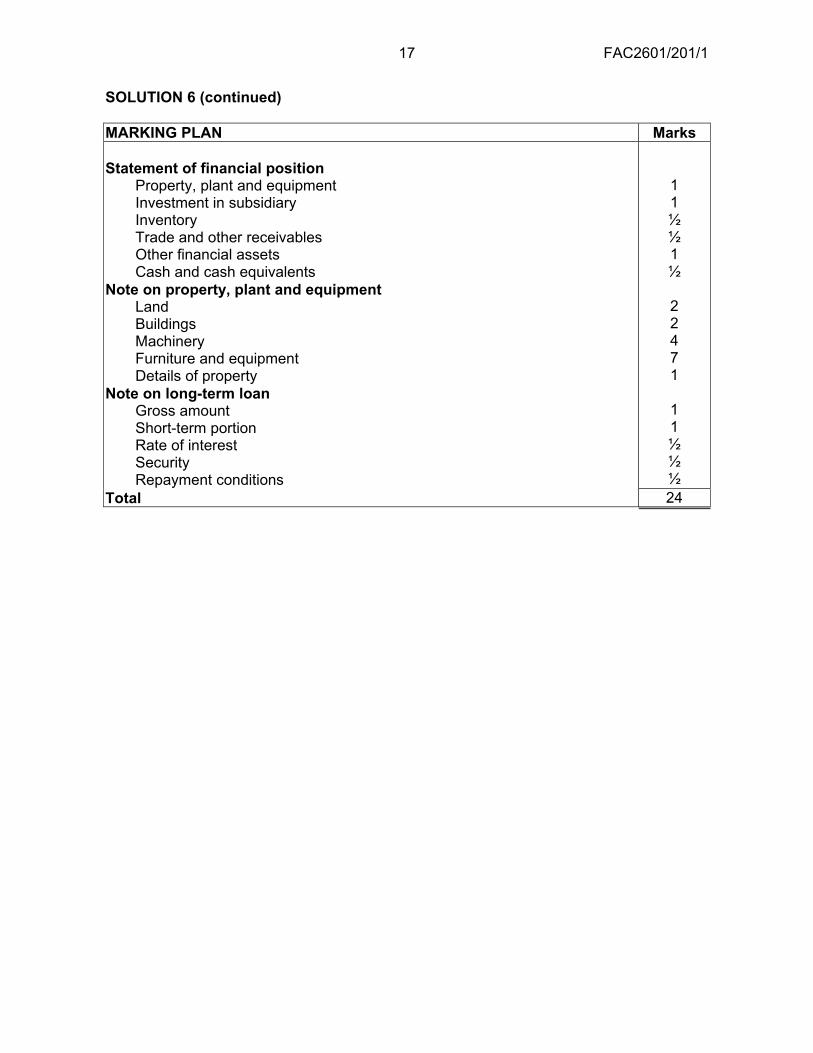

SOLUTION 6 (continued) MARKING PLAN Marks Statement of financial position

Property, plant and equipment Investment in subsidiary Inventory Trade and other receivables Other financial assets Cash and cash equivalents

Note on property, plant and equipment Land Buildings Machinery Furniture and equipment Details of property

Note on long-term loan Gross amount Short-term portion Rate of interest Security Repayment conditions

1 1 ½ ½ 1 ½

2 2 4 7 1

1 1 ½ ½ ½

Total 24

18 SOLUTION 7 PURCO LIMITED EXTRACT FROM THE STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2006 ASSETS Notes Non-current assets

R 6 143 600

Property, plant and equipment 1 Investment in subsidiary 2

5 793 600 350 000

Current assets 1 898 500Inventories 3 Trade and other receivables Other current assets 4

950 000 748 500 200 000

Total assets 8 042 100 PURCO LIMITED NOTES FOR THE YEAR ENDED 30 JUNE 2006 1. Property, plant and equipment

Land R

Buildings R

Plant and machinery

R

Furniture and

equipment R

Total R

Carrying amount 1 July 2005 1 000 000 - 2 432 000 400 000 3 832 000 Cost Accumulated depreciation

1 000 000 -

- -

3 200 000 (768 000)

600 000 (200 000)

4 800 000 (968 000)

Revaluation Additions at cost (1 878 400 + 121 600) Disposals at carrying amount Depreciation capitalised Depreciation

500 000 - - - -

- 2 000 000

- -

(20 000)

- - -

(121 600) (364 800)

- 80 000

(52 500)

- (59 500)

500 000 2 080 000

(52 500) (121 600) (444 300)

Carrying amount 30 June 2006 1 500 000 1 980 000 1 945 600 368 000 5 793 600Valuation/cost Accumulated depreciation

1 500 000 -

2 000 000 (20 000)

3 200 000 (1 254 400)

580 000 (212 000)

7 280 000 (1 486 400)

Land and buildings comprise erf 323, Sunward Park, with factory buildings and an office block. The land was revalued during 2006 by mr Value, a sworn appraiser, at replacement value.

FAC2601/201/1 19

SOLUTION 7 (continued) 2. Investment in subsidiary

R 350 000

Shares at cost Loan to subsidiary

200 000150 000

3. Inventories

Consist of 950 000Raw materials Work in progress Finished goods

300 000400 000250 000

4. Other current assets

Listed investments 200 00020 000 Preference shares of R2 each in Thakalaka Ltd at fair value 70 000 Ordinary shares of R1 each in Sugar Ltd at fair value

60 000140 000

Calculations 1. Buildings 1.1 Additions

R

2 000 000Direct cost – given Depreciation capitalised

1 878 400121 600

1.2 Depreciation – current year (R2 000 000 x 2% x 6/12) 20 000 2. Plant and machinery 2.1 Cost – opening balance (R2 432 000 + 768 000) 3 200 000 2.2 Depreciation – current year (R2 432 000 x 20%) 486 400 2.3 Depreciation capitalised (R486 400 x 3/12) 121 600 2.4 Accumulated depreciation – closing balance (R768 000 + 121 600 + 364 800)

1 254 400

3. Furniture and equipment 3.1 Depreciation on machinery traded in – current year (R100 000 x 10% x 9/12) 7 500 3.2 Accumulated depreciation on machinery traded in (R40 000 + 7 500) 47 500 3.3 Carrying amount of machinery traded in (R100 000 – 47 500) 52 500

20 SOLUTION 7 (continued)

R 3.4 Depreciation of equipment on hand – current year [(R500 000 x 10%) + (80 000 x 10% x 3/12)]

52 000

3.5 Total depreciation – current year (R7 500 + 52 000) 59 500 3.6 Cost – closing balance (R600 000 – 100 000 + 80 000) 580 000 3.7 Accumulated depreciation – closing balance (R200 000 – 47 500 + 59 500) 212 000 MARKING PLAN Marks Statement of financial position Property, plant and equipment Investment in subsidiary Inventories Trade and other receivables Other current assets Notes Property, plant and equipment

Revaluation of land Additions to buildings Depreciation - buildings Plant and machinery at cost - opening balance Depreciation capitalised Depreciation - plant and machinery Accumulated depreciation plant and machinery - closing balance Additions to furniture and equipment Disposals of furniture and equipment Depreciation - furniture and equipment Furniture and equipment at cost - closing balance Accumulated depreciation furniture and equipment - closing balance Note on situation of land and buildings

Investment in subsidiary Shares Loan

Inventories Raw materials Work in progress Finished goods

Other current assets Listed Unlisted

1 1 1 1 1

1 2 1 1 2 2 1 1 2 2 1 1 1

1 1

1 2

Total 30

FAC2601/201/1 21

SOLUTION 8 PURCO LIMITED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2006

Ordinary share capital

R

6% Cumulative preference

share capital

R

8% Non-cumulative preference

share capital

R

Share premium

R

Surplus onrevaluation

of non-current assets

R

Capital Redemp-

tion reserve

fund R

Retained earnings

R Total

R Balance 1 July 2005 Ordinary share issued on 31 March 2006 Non-cumulative preference shares issued on 1 April 2006

2 000 000

1 000 000

500 000 -

300 000

50 000

50 000

-

600 000 800 000 3 950 000

1 050 000

300 000Preliminary expenses written off Share issue expenses written off Capitalisation shares issued [(1 500 000/10) x R2] Comprehensive income for the year (1 000 000 – 444 300 – 161 150) Dividends declared: Cumulative preference shares (6% x 500 000 x 2 years) Non-cumulative preference shares (8% x 300 000 x 3/12) Ordinary shares (1 650 000 x 5c)

300 000

(30 000) (12 000)

500 000

(300 000)

394 550

(60 000)

(6 000)

(82 500)

(30 000)

(12 000)

-

894 550

(60 000)

(6 000)

(82 500)

Balance 30 June 2006 3 300 000 500 000 300 000 58 000 500 000 300 000 1 046 050 6 004 050 MARKING PLAN Marks Statement of changes in equity Ordinary share capital 6% Cumulative preference share capital 8% Non-cumulative preference share capital Share premium Surplus on revaluation of non-current assets Capital redemption reserve fund Retained earnings

4 2 2 5 1 2 10

Total 26

22 SOLUTIONS 9-37 9. Elements of cost The cost of a PPE-item comprises: (a) its purchase price, including import duties and non-refundable purchase taxes, after

deducting trade discounts and rebates. (b) any costs directly attributable to bringing the asset to the location and condition necessary

for it to be capable of operating in the manner intended by management. (c) the initial estimate of the costs of dismantling and removing the item and restoring the site

on which it is located. This obligation can arise either when the item is acquired or as a consequence of having used the item during a particular period for purposes other than to produce inventories during that period.

10. Examples of costs that are not costs of a PPE-item are: (a) costs of opening a new facility; (b) costs of introducing a new product or service (including costs of advertising and

promotional activities); (c) costs of conducting business in a new location or with a new class of customer (including

costs of staff training); and (d) administration and other general overhead costs. 11. Impairment loss An impairment loss is the amount by which the carrying amount of an asset exceeds its recoverable amount. 12. Compensation for impairment Monetary or non-monetary compensation for impairment that an entity may receive from third parties may include: (a) reimbursement by insurance companies after an impairment or loss of PPE-items, e.g.

due to natural disasters, theft or mishandling; (b) indemnities by the government for PPE-items that were expropriated; (c) compensation related to the involuntary convertion of PPE-items, e.g. relocation of

facilities from a designated urban area to a non-urban area in accordance with a national land policy;

(d) or physical replacement in whole or in part of an impaired or lost asset. 13. Derecognition The carrying amount of a PPE-item shall be derecognised: (a) on disposal; or (b) when no future economic benefits are expected from its use or disposal. The gain or loss arising from the derecognition of a PPE-item shall be included in profit or loss when the item is derecognised. Gains shall not be classified as revenue from the sale of goods and services.

FAC2601/201/1 23SOLUTIONS 9-37 (continued) 14. (a) Change in accounting policy When an item of PPE is revalued for the first time it is considered to be a change in accounting policy. It is therefore treated as a normal revaluation. Only the effect of the change on the figures for the current year is shown, as replacement values applicable to previous years are not readily available. (b) Residual value Residual values of assets should be reviewed at least at each financial year-end. If necessary the residual values should be adjusted and the disclosure requirements with regard to a change in accounting estimate should be complied with. (c) Estimated useful life If necessary the amended remaining useful life should be used and the disclosure requirements with regard to a change in accounting estimate should be complied with. (d) Determination of replacement value Assets can be revalued according to the net replacement value or the gross replacement value. Gross replacement value is the replacement cost (market value) of a similar, new asset. Net replacement value is the equivalent fair market value of a similar asset of the same age and/or condition. 15. Change in fair value of a financial asset A gain or loss arising from a change in the fair value of a financial asset or financial liability that is not part of a hedging relationship shall be recognised as follows: (a) A gain or loss on a financial asset or financial liability classified as at fair value

through profit or loss shall be recognised in profit or loss. Profit or loss

Debit – Investment Profit Credit – Fair value adjustment

Debit – Fair value adjustment Loss Credit – Investment

24 SOLUTIONS 9-37 (continued) (b) A gain or loss on an available-for-sale financial asset shall be recognised directly in

equity through the statement of changes in equity. Profit or loss

Debit – Investment Profit Credit – Mark-to-market reserve

Debit – Mark-to-market reserve Loss Credit – Investment 16. Revaluation of an asset – net replacement value basis

Carrying amount end of 20.1 Net replacement value

R 80 000

120 000Revaluation surplus 40 000

Journal

Dr R

Cr R

Accumulated depreciation Equipment at cost

20 000 100 000

Equipment at revaluation Revaluation surplus

Revaluation of equipment on the net replacement value vasis

120 000 40 000

17. Net replacement value basis Step 1: The net replacement value of R90 000 is regarded as the cost to replace the asset

currently with a similar asset of the same age and condition. Step 2: Calculate the amount that must be transferred to the revaluation surplus (revalued

amount – carrying amount of asset on revaluation date).

Net replacement value Carrying amount

R 90 00060 000

Revaluation surplus 30 000

FAC2601/201/1 25SOLUTIONS 9-37 (continued) Step 3: Journalise the revaluation Journals

Dr R

Cr R

Asset at revaluation Asset at cost

90 000 100 000

Accumulated depreciation Revaluation surplus

Revaluation of asset on net replacement value basis

40 000 30 000

Depreciation (90 000/6)

Accumulated depreciation Depreciation for the year based on revalued amount

15 000

15 000

18. Revaluation date: 1 January 20.3 Net replacement value: R160 000 The asset is 1 year old at 1 January 20.3 (180 000/6 = 30 000; 30 000/30 000 = 1 year) or 1 January 20.2 – 1 January 20.3 = 1 year The revaluation surplus at this date is:

Cost Accumulated depreciation

R 180 000 (30 000)

Carrying amount at 1 January 20.3 Net replacement value 1 January 20.3

150 000 (160 000)

Revaluation surplus at 1 January 20.3 10 000 The accumulated depreciation and cost of the asset is written back and the asset is

shown at the revalued amount. Journals

Dr R

Cr R

Accumulated depreciation Asset at revaluation

Asset at cost Revaluation surplus

Revaluation of asset on the net replacement value basis

30 000 160 000

180 00010 000

Depreciation (160 000/5)

Accumulated depreciation Depreciation for the year based on revalued amount

32 000

32 000

26 SOLUTIONS 9-37 (continued) 19. Investment property Property held (by the owner or by the lessee under a finance lease) to earn rentals or for capital appreciation or both, rather than for: (a) use in the production or supply of goods or services or for administrative purposes; or (b) sale in the ordinary course of business. Owner-occupied property Property held (by the owner or by the lessee under a finance lease) for use in the production or supply of goods or services or for administrative purposes. Examples of investment properties: (Name any two of the following) (a) land held for long-term capital appreciation rather than for short-term sale in the ordinary

course of business. (b) land held for a currently undetermined future use. (If an entity has not determined that it

will use the land as owner-occupied property or for short-term sale in the ordinary course of business, the land is regarded as held for capital appreciation.)

(c) a building owned by the entity (or held by the entity under a finance lease) and leased out under one or more operating leases.

(d) a building that is vacant but is held to be leased out under one or more operating leases. Examples of items that are not investment property: (Name any two of the following) (a) property intended for sale in the ordinary course of business or in the process of

construction or development for such sale, for example, property acquired exclusively with a view to subsequent disposal in the near future or for development and resale.

(b) property being constructed or developed on behalf of third parties. (c) owner-occupied property, including: (i) property held for future use as owner-occupied property. (ii) property held for future development and subsequent use as owner-occupied

property. (iii) property occupied by employees (whether or not the employees pay rent at market

rates) and (iv) owner-occupied property awaiting disposal. (d) property that is being constructed or developed for future use as investment property. (e) property that is leased to another entity under a finance lease.

FAC2601/201/1 27SOLUTIONS 9-37 (continued) 20. Accounting policy on investment property An entity shall choose either - the fair value model or - the cost model as its accounting policy and shall apply that policy to all of its investment property. Fair value model After initial recognition, an entity that chooses the fair value model shall measure all of its investment property at fair value, except when there is clear evidence when an entity first acquires an investment property that the entity will not be able to determine the fair value of the investment property reliably on a continuing basis. A gain or loss arising from a change in the fair value of investment property shall be recognised in profit or loss for the period in which it arises. Cost model After initial recognition, an entity that chooses the cost model shall measure all of its investment property at cost less accumulated depreciation and accumulated impairment losses. 21. What is impairment? Impairment will occur when the carrying amount of the asset in the books of the entity exceeds the asset’s recoverable amount. This will lead to an impairment loss. The impairment loss may be reversed if there is any indication that an impairment loss recognised for an asset in prior years may no longer exist or may have decreased. When does impairment take place? An asset is impaired when the carrying amount of the asset exceeds its recoverable amount. An entity should assess at each reporting date (balance sheet date) whether or not there is any indication that an asset may be impaired. If any such indication exists, the entity should estimate the recoverable amount of the asset. If there is no indication of a potential impairment loss then the statement does not require an entity to make a formal estimate of the recoverable amount.

28 SOLUTIONS 9-37 (continued) 22. Definitions (i) Provision A provision is a liability of uncertain timing or amount. (ii) Liability A present obligation of the entity arising from past events, the settlement of which is

expected to result in an outflow from the entity of resources embodying economic benefits. (iii) Obligating event An event that creates a legal or constructive obligation that results in an entity having no

realistic alternative to settling that obligation. (iv) Legal obligation An obligation that derives from: (a) a contract (through its explicit or implicit terms); (b) legislation; or (c) other operation of law. (v) Constructive obligation An obligation that derives from an entity’s actions where: (a) by an established pattern of past practice, published policies or a sufficiently specific

current statement, the entity has indicated to other parties that it will accept certain responsibilities; and

(b) as a result, the entity has created a valid expectation on the part of those other parties that it will discharge those responsibilities.

(vi) Contingent liability A contingent liability is: (a) a possible obligation that arises from past events and whose existence will be

confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity; or

(b) a present obligation that arises from past events but is not recognised because: it is not probable that an outflow of resources embodying economic benefits will be

required to settle the obligation; or the amount of the obligation cannot be measured with sufficient reliability.

FAC2601/201/1 29SOLUTIONS 9-37 (continued) In a general sense, all provisions are contingent because they are uncertain in timing or

amount. The difference between a provision and contingent liability is that there is more uncertainty i.r.o. a contingent liability with regard to the possibility of an outflow of economic resources or the estimate of the amount of the outflow of the economic resources.

(vii) Contingent asset A possible asset that arises from past events and whose existence will be confirmed only

by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity.

(viii) Onerous contract A contract which the unavoidable costs of meeting the obligations under the contract

exceed the economic benefits to be received under it. 23. Provisions - recognition A provision should be recognised when: (a) an entity has a present obligation (legal or constructive) as a result of a past event; and (b) it is probable that an outflow of resources embodying economic benefits will be required to

settle the obligation; and (c) a reliable estimate can be made of the amount of the obligation. If all these conditions are not met, no provision should be recognised. 24. Provisions - categories Provisions are divided into two categories, namely legal obligations; and constructive obligations.

Legal obligations

This category of obligations means that another party has the right to summons the entity

to perform. Such obligations are applicable, for example, when warranties are given to customers, when it results from litigation and when self-insurance is applied, as well as in the case of onerous contracts. The essential element in such cases is therefore an obligation that can be enforced by law.

30 SOLUTIONS 9-37 (continued) Constructive obligations

Constructive obligations are those obligations that are not legally enforceable, but are

inescapable as a result of external factors or management policy and decisions. This means that the entity is left no other realistic alternative than to incur the obligation. Constructive obligations therefore emanate from circumstances, in contrast to legal obligations that arise from the operation of the law. If it is the policy of a trader to exchange products within three days of the sale thereof if the customer is not completely satisfied, this policy brings about a constructive obligation for the entity, because its name can be brought into disrepute by the non-fulfilment of the undertaking. Although the customer cannot necessarily institute a legal action for the enforcement of the policy, and in this sense no legal obligation can therefore arise, the obligation is nevertheless such that the entity will want to fulfil it: it is therefore a constructive obligation. Another example of a constructive obligation is that of contaminated ground around a factory plant. Public opposition to such contamination may be such that it is obligatory for the entity to incur costs to remove the contamination, even if it does not necessarily have a legal obligation to do so. The mere presence of environmental pollution does not, however, give rise to an obligation, even if it is caused by the entity’s activities. Only when there is no realistic alternative to rehabilitation does the obligation arise. This can be on the date that the board makes a public announcement that cleaning up will take place, or when production is inhibited by the pollution to such an extent that cleaning up can no longer be postponed.

25. Contingent liability An entity should not recognise a contingent liability. A contingent liability should however be disclosed unless the possibility of an outflow of resources embodying economic benefits is remote. Where an entity is jointly and severally liable for an obligation, the part of the obligation that is expected to be met by other parties is treated as a contingent liability. 26. Contingent assets An entity should not recognise a contingent asset. A contingent asset is disclosed where an inflow of economic benefits is probable. However, when the realisation of income is virtually certain, the related asset is not a contingent asset and its recognition is appropriate. Contingent assets usually arise from unplanned or other unexpected events that give rise to the possibility of an inflow of economic benefits to the entity. An example is a claim that an entity is pursuing through legal processes, where the outcome is uncertain. Contingent assets are assessed continually to ensure that development are appropriately reflected in the financial statements. If it has become virtually certain that an inflow of economic benefits will arise, the asset and the related income are recognised in the financial statements of the period in which the change occurs.

FAC2601/201/1 31SOLUTIONS 9-37 (continued) 27. Events after the reporting period Events after the reporting date are those events, both favourable and unfavourable, that occur between the date and the date when the financial statements are authorised for issue. Two types of events can be identified: (a) those that provide evidence of conditions that existed at the date (adjusting events after

balance sheet date); and (b) those that are indicative of conditions that arose after the date (non-adjusting events

after date). 28. Adjusting events after the reporting period An entity should adjust the amounts recognised in its financial statements to reflect adjusting events after the date. The following are examples of adjusting events after the date that require an entity to adjust the amounts recognised in its financial statements, or to recognise items that were not previously recognised: (a) The resolution after the date of a court case which, because it confirms that an entity

already had a present obligation at the date, requires the entity to adjust a provision already recognised, or to recognise a provision instead of merely disclosing a contingent liability.

(b) The receipt of information after the date indicating that an asset was impaired at the date,

or that the amount of a previously recognised impairment loss for that asset needs to be adjusted. For example:

(i) the bankruptcy of a customer which occurs after the date usually confirms that a loss

already existed at the date on a trade receivable account and that the entity needs to adjust the carrying amount of the trade receivable account; and

(ii) the sale of inventories after the date may give evidence about their net realisable value at the date.

(c) The determination after the date of the cost of assets purchased, or the proceeds from

assets sold, before the date. (d) The determination after the date of the amount of profit sharing or bonus payments, if the

entity had a present legal or constructive obligation at the date to make such payments as a result of events before that date.

(e) The discovery of fraud or errors that show that the financial statements were incorrect.

32 SOLUTIONS 9-37 (continued) 29. Non-adjusting events after the reporting period An entity should not adjust the amounts recognised in its financial statements to reflect non-adjusting events after the date. An example of a non-adjusting event after the date is a decline in market value of investments between the date and the date when the financial statements are authorised for issue. The fall in market value does not normally relate to the condition of the investments at the date, but reflects circumstances that have arisen in the following period. Therefore, an entity does not adjust the amounts recognised in its financial statements for the investments. Similarly, the entity does not update the amounts disclosed for the investments as at the date, although it may need to give additional disclosure (see the paragraph dealing with disclosure). The following are examples of non-adjusting events after the date that may be of such importance that non-disclosure would affect the ability of the users of the financial statements to make proper evaluation and decisions: (a) A major business combination after the date (business combinations, requires specific

disclosures in such cases – not part of this module) or disposing of major subsidiary. (b) Announcing a plan to discontinue operation, disposing of assets or settling liabilities

attributable to a discontinuing operation or entering into binding agreements to sell such assets or settle such liabilities.

(c) Major purchases and disposals of assets, or expropriation of major assets by government. (d) The destruction of a major production plant by a fire after the date. (e) Announcing, or commencing the implementation of, a major restructuring. (f) Major ordinary share transactions and potential ordinary share transactions after the date. (g) Abnormally large changes after the date in asset prices or foreign exchange rates. (h) Changes in tax rates or tax laws enacted or announced after the date that have a

significant effect on current and deferred tax assets and liabilities. (i) Entering into significant commitments or contingent liabilities, for example, by issuing

significant guarantees. (j) Commencing major litigation arising solely out of events that occurred after the date. 30. Disclosure – Non-adjusting events after the reporting period Where not-adjusting events after the date are of such importance that non-disclosure would affect the ability of the users of the financial statements to make proper evaluations and decisions, an entity should disclose the following information for each significant category of non-adjusting event after the date: (a) the nature of the event; and (b) an estimate of its financial effect, or a statement that such an estimate cannot be made.

FAC2601/201/1 33SOLUTIONS 9-37 (continued) 31. Definition - Revenue Revenue is: the gross inflow of economic benefits during the period arising in the course of the ordinary activities of an entity that results in increases in equity, excluding the contributions of equity participants.

32. Disclosure in respect of revenue The following should be disclosed in the financial statements: The accounting policies adopted for the recognition of revenue, including the methods

adopted to determine the stage of completion of transactions involving the rendering of services.

The amount of each significant category of revenue recognised during the period, including revenue arising from:

- the sale of goods; - the rendering of services; - interest; - royalties; - dividends. The amount of revenue arising from the exchange of goods or services included in each

significant category of revenue. In terms of the Fourth Schedule to the Companies Act, the following items should be disclosed separately: income from investments, distinguishing between listed and unlisted investments and

between interest, dividends and other specified income; the aggregate amount of income from subsidiaries, stating whether dividends, interest,

fees or other specified income; and the aggregate amount of turnover for the accounting period and the basis upon which

turnover has been determined. 33. Measurement - Revenue Revenue will be measured as follows: At fair value of the consideration received or receivable. At fair value which is the amount for which an asset could be exchanged or a liability

settled, between knowledgeable willing parties in arms length transaction.

34 SOLUTIONS 9-37 (continued) 34. Recognition - Revenue Revenue will be recognised when it is probable that future economic benefits will flow to the entity and it can be measured reliably. 35. Sale of goods (i) Bill and Hold sales: Revenue recognised when buyer takes title and it is probable

that delivery will be made. (ii) Goods shipped subject to conditions: (a) Installation and inspection: Revenue recognised when buyer accepts delivery

and installation and inspection process are complete or immediately upon delivery when installation process is simple.

(b) Consignment sales: Revenue recognised when goods are sold by the recipient to a third party.

(c) COD: Revenue recognised when delivery has been made and cash is received. (iii) Lay away sales: Revenue recognised when buyer makes final payment or significant

deposit is received. (iv) Order when payment is received in advance for goods not presently held in

inventory: Revenue recognised when goods are delivered to buyer. (v) Sale and repurchase agreements: The terms of agreement need to be analysed

to determine if the seller has transferred the risks and rewards of ownership. (vi) Sales to intermediate parties: Revenue recognised when risks and rewards of

ownership have passed to buyer. (vii) Subscriptions: Revenue recognised on a straight-line basis over the period of the

agreement. (viii) Instalment sales: Revenue attributable to sales price, exclusive of interest

recognised on date of sale. Interest element recognised on time proportion basis. (ix) Real estate sales: Revenue recognised when legal title passes to the buyer. 36. Rendering of services (i) Installation fees: Revenue recognised by reference to stage of completion unless

incidental; then recognised when goods are sold. (ii) Service fees included in price of product: Service fees is deferred and

recognised over the period during which the service is performed. (iii) Advertising commissions: Revenue recognised when advertisement appears before

public. Production commissions recognised by reference to the stage of completion of project.

(iv) Insurance agency commissions: Revenue recognised on the effective commencement or renewal dates of the related policies.

(v) Admission fees: Revenue recognised when the event takes place.

FAC2601/201/1 35

SOLUTIONS 9-37 (continued) (vi) Tuition fees: Revenue recognised over the period of instruction. (vii) Initiation, entrance and membership fees: Revenue recognition depends on the

nature of the service provided, for example if the fee permits only membership or include other services as well.

(viii) Franchise fees: Revenue recognised on a basis that reflects the purpose for which the fees were charged.

(ix) Development of customised software: Revenue recognised by reference to stage of completion.

37. License fees and royalties: Revenue recognised in accordance with the substance of

the agreement, this may be on straight-line basis over the live of the agreement.

36 SOLUTIONS 9-37 (continued) MARKING PLAN Marks

9 10 11 12 13 14

15 16 17 18 19

20 21 22

23 24 25 26 27 28 29 30 31 32 33 34 35 36 37

Elements of cost Examples of cost not cost of PPE Impairment loss Compensation for impairment Derecognition (a) Change in accounting policy (b) Residual value (c) Estimated useful life (d) Determination of replacement value Change in fair value of a financial asset Revaluation of an asset Determination of replacement value Determination of replacement value Investment property Owner-occupied property Accounting policy on investment property Impairment of an asset Definitions Provision Liability Obligating event Legal obligation Constructive obligation Contingent liability Contingent asset Onerous contracts Provisions – recognition Provisions – categories Contingent liability Contingent asset Events after reporting period Adjusting events after reporting date Non-adjusting events after reporting date Events after reporting date – disclosure Revenue – definition Revenue – disclosure Revenue –measurement Revenue – recognition Revenue recognition – sale of goods Revenue recognition – rendering of services Revenue recognition – other

6 6 2 4 4 2 2 2 4 8

10 10 12 2 1 6 4 1 2 1 3 3 4 2 2 4 6 2 4 4 8 5 3 3 4 2 2

12 10 2

Total 174

FAC2601/201/1 37

SOLUTION 38 (20 marks) (24 minutes) a) MALEMOME LIMITED STATEMENT OF FINANCIAL POSITION AS AT 30 SEPTEMBER 2008

R Assets Non-current assets .................................................................................... 3 124 000 Property, plant and equipment (2 600 000 + 360 000) ............................. 2 960 000 Intangible assets ...................................................................................... 100 000 Available-for-sale financial assets ............................................................ 64 000 Current assets............................................................................................ 2 799 000 Inventories ............................................................................................... 1 750 000 Trade and other receivables (870 000 – 50 000) ..................................... 820 000 Financial assets at fair value through profit or loss held for trading ......... 89 000 Cash and cash equivalents ...................................................................... 140 000 Total assets ................................................................................................ 5 923 000 Equity and liabilities Total equity ................................................................................................. 3 233 000 Share capital and -premium (700 000 + 268 000) .................................... 968 000 Retained earnings (2 200 000 – 50 000 – 200 000 – 100 000) ................ 1 850 000 Other components of equity (270 000 + 145 000) .................................... 415 000 Total liabilities ............................................................................................ 2 690 000 Non-current liabilities ............................................................................ 970 000 Long-term borrowings ........................................................................... 970 000

Current liabilities ................................................................................... 1 720 000 Trade and other payables (670 000 + 600 000 + 200 000 + 100 000) .. 1 570 000 Dividends payable ................................................................................. 150 000

Total equity and liabilities ......................................................................... 5 923 000

(15) b) Notes to annual financial statements Notes for the year ended 30 September 2008 Non-adjusting events after the reporting period

1) Dividends

An ordinary dividend of 20 cents per share was declared after the reporting date for share holders registered on reporting date. Total dividend declared is R140 000 (700 000 x 20c). (3)

38 SOLUTIONS 38 (continued)

2) Fire damage

On 27 October 2008, a fire destroyed a furnace and caused damages of R300 000. The effect is that profit after tax for 2009 will be reduced by R206 000. (2)

MARKING PLAN Marks a) Statement of financial position Property, plant and equipment Intangible assets Available-for-sale financial asset Inventory Trade and other receivables Other financial assets Financial assets at fair value Cash and cash equivalents Share capital and premium Retained earnings Other components of equity Long-term borrowings Trade and other payables Shareholders for dividends b) Notes Non-adjusting events after reporting period

1. Dividends 2. Fire damage

1½ ½ ½ ½ 1½ ½ ½ ½ 1½ 2½ 1½ ½ 2½ ½

3 2

Total 20

FAC2601/201/1 39

ANNEXURE E: PREVIOUS EXAMINATION PAPER AND SOLUTION May 2009 This paper consists of 7 pages N.B.: 1. This paper consists of FOUR (4) questions. 2. Basic workings, where applicable, must be shown. 3. Ensure that you are handed the correct examination answer book (blue colour for

accounting) by the invigilator. 4. Each question attempted must be commenced on a new (separate) page. 5. The pass rate for this course is 50%. 6. PROPOSED TIMETABLE: Question

No Subject Marks Time in

minutes1 Statement of comprehensive income (Income statement) 31 37 2 Statement of changes in equity 16 19 3 Statement of financial position - Assets (Balance sheet) 33 40 4 Theory 20 24 100 120

40 USE THIS INFORMATION TO ANSWER THE FOLLOWING THREE QUESTIONS The following list of balances was extracted from the books of Winners Limited for the year ended 28 February 2009: Ordinary share capital ........................................................................................ 10% Preference share capital ............................................................................ Share premium – ordinary shares ...................................................................... Proceeds of 100 000 new no par value shares issued ...................................... Share issue expenses incurred on the above shares issued ............................. Preliminary expenses ......................................................................................... Debenture issue expenses ................................................................................ Land at cost ....................................................................................................... Buildings at cost ................................................................................................. Investments ....................................................................................................... Long-term loan from Losers (Pty) Ltd ................................................................ Loans to staff ..................................................................................................... Profit before tax ................................................................................................. Retained earnings – 1 March 2008 .................................................................... Trade and other receivables .............................................................................. Inventories – raw material .................................................................................. Inventories – finished goods .............................................................................. Machinery and equipment at cost ...................................................................... Accumulated depreciation – 28 February 2009

Machinery and equipment ........................................................................... Buildings ......................................................................................................

Provisional tax payments ................................................................................... Motor cycle at cost ............................................................................................. 10% Debentures of R100 each (secured by a first mortgage bond over land and buildings) ................................................................................................... Dividends receivable (except from subsidiary)

Blocks Limited ............................................................................................. Crocs (Pty) Ltd ............................................................................................

R 1 000 000

200 000210 000210 000

4 0003 0002 000

100 0001 000 000

172 000100 000

9 000107 00093 80086 000

8 00092 000

1 600 000

800 00037 00016 200

?

200 000

1 800800

Additional information: 1. Winners Limited was incorporated with an authorised share capital of: 800 000 Ordinary shares of R2 each 100 000 10% Preference shares of R5 each 2. On 1 March 2008 the directors of Winners Limited decided on the following which must

still be accounted for in the following order: 2.1 To make a capitalisation issue to existing shareholders in the ratio of 1 share for every

5 ordinary shares held. The capitalisation issue must not be made out of retained earnings.

FAC2601/201/1 41

2.2 To convert the ordinary par value shares into no par value shares. 2.3 To write off all share issue expenses, preliminary expenses and debenture issue

expenses with the minimum effect towards distributable reserves. 3. The existing land (owner occupied and situated at erf 10, Rietbron) was purchased on

1 March 2006 for R100 000. Buildings at a cost of R900 000 were completed on 1 March 2007. On 1 March 2008 the land was revalued by a sworn appraiser, Mr Right, for R400 000 on the replacement basis. No entry to record the revaluation was done. Since then a modernising program of R300 000 was approved by the directors. Work to the amount of R100 000 was completed and paid for at 31 August 2008 while contracts to the value of R100 000 were already entered into for the following accounting period.

4. Investments consist of the following: 4.1 4.2 4.3

Allout Limited 20 000 Ordinary shares of R3 each ...................................................... The authorised share capital of Allout Ltd is 50 000 shares of which 30 000 were issued. Blocks Limited – listed on the Johannesburg Securities Exchange (bought for speculative purposes): 2 000 Ordinary shares of R40 each ...................................................... Market value on 28 February 2009 was R50 per share. Crocs (Pty) Limited – unlisted company (designated as available-for-sale): 400 Ordinary shares of R80 each ......................................................... Directors’ valuation on 28 February 2009 amounts to R40 000. In previous years the fair value of all the investments above was equal to their cost prices.

R 60 000

80 000

32 000

172 000 4.4

The fair value of the above investment in the previous years were the same as the cost price of the investments.

5. The unsecured long-term loan originated on 1 March 2008 and is repayable in equal

annual instalments of R20 000 on 1 March every year. Interest for the current year at the rate of 10% must still be provided for and is payable on 5 March 2009. Winners Ltd uses the settlement basis of accounting to account for its financial instruments.

6. Loans to personnel consist of: 6.1 A loan of R6 000 to Mr Grog, the marketing manager. No repayment was made during

the current year. 6.2 R3 000 owing by Mr Traus, the company secretary. The original advance on

1 June 2008 amounted to R6 000. Both these loans are short-term and interest free.

42 7. Profit before tax for the year was determined after taking the following into account,

amongst others:

Income from subsidiary: Dividends .................................................................................................. Administration fees ...................................................................................Profit on sale of delivery motor cycle ..........................................................Auditors’ remuneration (including R800 travelling expenses) .....................Travelling and entertainment allowance of the managing director ..............Directors’ remuneration for attendance of meetings - Managing director .....................................................................................- Non-executive directors ............................................................................ (An additional R4 000 was paid by the subsidiary to the managing director who acts as chairman for the subsidiary) Salaries (including R140 000 paid to the managing director, as well as the company’s pension fund contributions of 5% on all salaries) ................Bank charges ..............................................................................................Depreciation - Machinery and equipment ........................................................................- Buildings ...................................................................................................Interest on overdraft ....................................................................................Interest on debentures ................................................................................

R

1 0007 0001 5004 0006 800

3 6003 600

400 0001 400

200 00019 00013 80016 000

No entry has yet been made in respect of the depreciation on the new motor cycle

purchased on 1 September 2008 (refer note 9). 8. Normal company taxation of R20 972 and dividends on ordinary shares of 5c per share

must still be provided for. 9. Winners Limited’s only delivery motor cycle was sold on 1 March 2008. The transaction

was entered correctly in the books. The original cost price of this asset was R20 000 and the carrying amount at date of sale was R4 000. It was replaced on 1 September 2008 with a new motor cycle costing R91 200 (including VAT at 14%). It is Winners Limited’s policy to write off depreciation on their motor cycle at 20% p.a. on the straight-line basis. Depreciation for this year must still be provided on the new motor cycle.

10. It is Winners Limited’s policy to write off depreciation on machinery and equipment at

20% per annum according to the diminishing balance method. No purchase or sale of machinery took place during the year.

11. Revenue for the year amounted to R10 260 000 and represents net sales to third

parties (including VAT at 14%) of goods purchased for resale. Winners Limited maintained a 40% gross profit percentage throughout the year.

12. Buildings are depreciated at 2% per annum on the straight-line basis.

FAC2601/201/1 43

13. Included in profit before tax are distribution expenses amounting to R53 600 and

administrative expenses of R3 421 700 (before adjustments). QUESTION 1 (31 marks) (37 minutes) REQUIRED: Use the above information to prepare the statement of comprehensive income (Income statement) and the relevant notes thereto of Winners Limited for the year ended 28 February 2009 according to the requirements of the Companies Act, 1973 as amended and Generally Accepted Accounting Practice. (Ignore accounting policy notes and comparative figures. Show all calculations.) QUESTION 2 (16 marks) (19 minutes) REQUIRED: Use the above information to prepare the statement of changes in equity of Winners Limited for the year ended 28 February 2009 according to the requirements of the Companies Act, 1973 as amended and Generally Accepted Accounting Practice. (Show all calculations.) QUESTION 3 (33 marks) (40 minutes) REQUIRED: Use the above information to prepare the “Asset” side of the statement of financial position (balance sheet) and the relevant notes at 28 February 2009 according to the requirements of the Companies Act, 1973 as amended and Generally Accepted Accounting Practice. (Ignore accounting policy notes and comparative figures. Show all calculations.)

44 QUESTION 4 (20 marks)(24 minutes) 1. Which of the following will you classify as a non-adjusting event after reporting date? (A) The bankruptcy of a customer which occurs one month after the reporting date (B) The discovery of fraud or errors that show that the financial statements were

incorrect (C) Entering into a binding agreement to sell major assets of the company two months

after reporting date (D) None of the above 2. XYZ Limited issued 2 000 redeemable preference shares on 1 January 2002. The shares

are redeemable in cash at the option of the company before 31 December 2012. How will you disclose the preference shares in the financial statements of XYZ Limited on 30 June 2008?

(A) Financial liability (B) Equity (C) Contingent liability (D) None of the above 3. Which of the following costs is NOT regarded as a directly attributable cost of an item of

property, plant and equipment? (A) Professional fees (B) Cost of site preparation (C) All of the above (D) None of the above 4. Revenue attributable to instalment sales (excluding interest) is recognised: (A) When the buyer makes a final payment (B) When a significant deposit is received (C) A or B (D) None of the above 5. A building owned by the entity and leased out under an operating lease is regarded as: (A) Owner occupied property (B) Investment property (C) A contingent asset (D) None of the above

FAC2601/201/1 45QUESTION 4 (continued) 6. A provision should be recognised when: (A) An enterprise has a present obligation as a result of a past event (B) It is probable that an outflow of resources embodying economic benefits will be

required to settle the obligation (C) A reliable estimate can be made of the amount of the obligation (D) All of the above 7. The Standard on Impairment of assets (IAS36/AC128) shall be applied to the following: (A) Inventories (B) Non-current assets classified as held for sale (C) Investment in subsidiaries (D) None of the above 8. A gain or loss on an available-for-sale financial asset shall be recognised: (A) Directly in equity (B) In profit and loss (C) A or B (D) None of the above 9. A provision will not be provided at reporting date in the following cases: (A) Staff training cost to be incurred in the next financial year after significant changes

to the Income Tax Act. (B) Accumulated unused leave by employees of the company to be paid out on

retirement or resignation (C) Goods sold by a company under warranties whereby the company undertakes to

make good, repair or replace goods with manufacturing defects that become apparent within two years from date of sale. Previous experience shows that about 5% of sales are returned with a claim against the warranty.

(D) None of the above 10. Which of the following statements are true? (A) The carrying amount of inventory purchased must be recognised as an expense in

the relevant period. (B) Any amount which arises when inventory is written off to net realisable value and

any loss of inventory should be recognised as an expense in the period in which the write-off took place

(C) A and B (D) None of the above

© UNISA 2009

46

MEMORANDUM

ACN201Q

MAY/JUNE 2009

FAC2601/201/1 47

SOLUTION 1 WINNERS LIMITED STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 28 FEBRUARY 2009

Notes R Revenue Cost of sales (9 000 000 – 3 600 000)

9 000 000 5 400 000

Gross profit (40% x 9 000 000) Other income (1 800 + 800 + 1 000 + 7 000 + 1 500 + 20 000) Distribution expenses Administration expenses (3 421 700 + 8 000 + 2 000) Finance cost (13 800 + 16 000 + 10 000)

3 600 000 32 100

(53 600) (3 431 700) (39 800)

Profit before tax 9 Income tax expense 10

107 000 (20 972)

PROFIT FOR THE YEAR Other comprehensive income:

86 028 308 000

Gain on available-for-sale financial assets (40 000 – 32 000) Gain on property revaluation (400 000 – 100 000)

8 000 300 000

TOTAL COMPREHENSIVE INCOME FOR THE YEAR 394 028 Profit attributable to: Owners 86 028 Total comprehensive income attributable to: Owners 308 000 Profit before tax is disclosed after taking the following disclosable items into account

RIncome Revenue consists of sales of goods Profit on sale of non-current asset Fair value adjustment – financial asset at fair value through profit or loss Dividend income

9 000 000 1 500 20 000 2 600

- Financial asset at fair value through profit or loss – listed investment - Available-for-sale financial assets – unlisted investment

1 800 800

Income from subsidiary 8 000 - Dividends - Administration fee

1 000 7 000

Expenses Directors’ remuneration

161 000 Executive directors 157 400 - Emoluments [6 800 + 3 600 + 4 000 + 140 000 + 5% x 140 000)] - Less: Paid by subsidiary

161 400 4 000

Non-executive directors - Emoluments

3 600

Auditors’ remuneration 4 000 Audit fees Expenses

2 400 1 600

Depreciation (200 000 + 19 000 + 8 000) Write-off of debenture issue expenses

227 000 4 000

48 SOLUTION 1 (continued) Income tax expense R SA Normal taxation – Current 20 972 Calculations 1. Sales Less: VAT (14/114 x 10 260 000)

10 260 000 (1 260 000)

9 000 000 2. Depreciation on motor cycle Total cost price Less: VAT (14/114 x R91 200)

91 000 (11 200)

Depreciation 20/100 x 80 000 x 6/12 8 000 MARKING PLAN Marks Statement of comprehensive income Revenue Cost of sales Gross profit Other income Distribution expenses Administration expenses Finance cost Income tax expense Gain on available-for-sale financial assets Gain on property revaluation Note on profit before tax Revenue Profit on sale of non-current asset Fair value adjustment Dividend income Income from subsidiary Directors remuneration Auditors remuneration Depreciation SA Normal taxation

1½ 1 1 3 1

1½ 2 1 1 1

1½ 1 2 2 2

3½ 2 2 1

Total 31

FAC2601/201/1 49

SOLUTION 2 WINNERS LIMITED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 28 FEBRUARY 2009

Ordinary share capital

R

Stated capital – ordinary shares

R

Pre-ference share capital

R

Share premium

R

Reva-luation surplus

R

Mark-to-

market reserve

R

Retained earnings

R Total

R Balance at 1 March 2008 Total comprehensive income for the year Issue of capitalisation shares Conversion of par value shares and premium Issue of no par value shares Share issue expenses written off Preliminary expenses written off Dividends preference (R200 000 x 10%) ordinary (700 000 x 5c) (500 000 + 100 000 + 100 000) shares

1 000 000

200 000

(1 200 000)

-

1 210 000

210 000

(4 000)

(3 000)

200 000 210 000

(200 000)

(10 000)

-

300 000

-

8 000

93 800

86 028

(20 000)

(35 000)

1 503 800

394 028

210 000

(4 000)

(3 000)

(20 000)

(35 000)Balance 28 February 2009 - 1 413 000 200 000 - 300 000 8 000 124 828 2 045 828 MARKING PLAN Marks Statement of changes of equity Ordinary share capital Stated capital Preference share capital Share premium Revaluation surplus Mark-to-market reserve Retained earnings

2½ 4 ½

2½ 1

1½ 4

Total 16

50 QUESTION 3 WINNERS LIMITED STATEMENT OF FINANCIAL POSITION AS AT 28 FEBRUARY 2009 ASSETS Notes Non-current assets

R 2 335 000

Property, plant and equipment 1 Investment in subsidiary 2 Available-for-sale financial assets 3

2 235 000 60 000 40 000

Current assets 297 600Inventory 4 Trade and other receivables (86 000 + 1 800 + 800) 3 Other financial assets (9 000 + 100 000) 3

100 000 88 600 109 000

Total assets 2 632 600 WINNERS LIMITED NOTES FOR THE YEAR ENDED 28 FEBRUARY 2008 1. Property, plant and equipment

BuildingsR

Land R

Machineryand

equipmentR

Delivery vehicle

R Total

R Carrying amount 1 March 2008 882 000 100 000 11 000 000 4 000 1 986 000 Gross carrying amount or cost Accumulated depreciation

900 000 (18 000)

100 000 -

1 600 000 (600 000)

40 000 (36 000)

2 640 000 (654 000)

Revaluation surplus for the year Depreciation for the year Additions Disposals

- (19 000) 100 000

-

300 000 - - -

- (200 000)

- -

- (8 000) 80 000

(4 000)

300 000 (227 000) 180 000

(4 000)Carrying amount 28 February 2009 963 000 400 000 800 000 72 000 2 235 000 Gross carrying amount or cost Accumulated depreciation

1 000 000 (37 000)

400 000 -

1 600 000 (800 000)

80 000 (8 000)

3 080 000 (845 000)

1 100 000 x 100/80 = 1 000 000 On 1 March 2008 land, with a building, situated at erf 10 Rietbron was revalued by Mr Right, a sworn appraiser according to the replacement basis for R400 000. Additions during the year amounted to R100 000. The land and buildings serve as security for the debentures.

FAC2601/201/1 51

SOLUTION 3 (continued) 2. Investment in subsidiary

R

Shares at cost 60 000 3. Financial assets

Non-current financial assets at fair value Available-for-sale

40 000

Unlisted investment – 400 Ordinary shares of R80 each (cost R32 000) 40 000 Current financial assets 98 800Trade receivables (86 000 + 1 800 + 800) Loans and receivables

88 6009 000

Staff loans (The loans are interest free and repayable in the following year) 9 000Financial assets at fair value through profit or loss – held for trading Listed investment – 2 000 Ordinary shares of R40 in Blocks Ltd (cost R80 000) 100 000

237 600 4. Inventories

Finished goods Raw materials

R

92 000 8 000

100 000 MARKING PLAN Marks Statement of financial position Property, plant and equipment Investment in subsidiary Available-for-sale financial assets Inventory Trade and other receivables Other financial assets Notes Buildings Land Machinery and equipment Delivery vehicle Note on property Investment in subsidiary Financial assets Inventories

1 1 1 1

1½ 1 4

1½ 2 6 4 1 6 2

Total 33

52 SOLUTION 4 1. C 2. B 3. D 4. D 5. B 6. D 7. C 8. A 9. A 10. C MARKING PLAN Marks 2 Marks per question – 10 x 2

20

Total 20 FAC2601_2010_TL_201_1_E.doc