Embed Size (px)

Citation preview

Saudi Arabia

Executive Summary

This country fact sheet provides key trade and investment related statistics for Saudi Arabia. Specifically, it shows

Saudi Arabia’s trade and investment flows including an analysis of top markets and products with South Africa and

the Western Cape highlighting the largest and fastest growing products and subsectors. The key highlights in the

Saudi Arabia country fact sheet are provided below:

Economy In 2015, Saudi Arabia’s GDP (PPP) was estimated at USD1.7trn, making Saudi Arabia the world's 15th

largest economy.

In 2015, Saudi Arabia’s GDP growth was at 3.4%.

Trade Global exports from Saudi Arabia in 2014 were valued at ZAR3.8trn compared to ZAR3.6trn in 2013,

increasing by 6.6%.

China was the leading import market in 2014 valued at ZAR223bn.

South Africa exported goods to Saudi Arabia valued at ZAR4.8bn in 2014 compared to ZAR2.6bn in

2013, representing an increase of 83%

The leading export product to Saudi Arabia from South Africa was motor vehicles for the transport of

goods and valued at ZAR819m, followed by citrus fruit (ZAR754m)

The province exported goods to Saudi Arabia valued at ZAR893m in 2014

Citrus fruit was the leading export product category to Saudi Arabia from the Western Cape in 2014,

valued at ZAR398m. This is followed by flat-rolled products of iron or non-alloy steel, valued at

ZAR160m.

Investment Between January 2003 and July 2015 a total of 1,217 FDI projects were recorded into Saudi Arabia.

These projects represent a total capital investment of ZAR1,785.79bn

Between January 2003 and July 2015 a total of 534 FDI projects were recorded from Saudi Arabia.

These projects represent a total capital investment of ZAR487.47bn

Between January 2003 and July 2015 a total of 2 FDI projects were recorded from South Africa to Saudi

Arabia. These projects represent a total capital investment of ZAR399.55m

Between January 2003 and July 2015 a total of 5 FDI projects were recorded from Saudi Arabia to

South Africa. These projects represent a total capital investment of ZAR20.70bn

Tourism Outbound tourism is expected to increase significantly over the next five years through to 2020 with

outbound travel increasing from 11.7mn in 2016 to 14.8mn in 2020.

Saudi Arabian tourist arrivals into South Africa increased by 5% from 6 251 tourists in 2013 to 6 545

tourists in 2014.

2

Table of Contents

1. General Information ....................................................................................................... 3

2. Economic Overview ....................................................................................................... 3

2.1 Doing Business in Saudi Arabia .............................................................................. 6

3. Trade ............................................................................................................................. 7

3.1 Saudi Arabia’s Global Trade in Services ................................................................. 7

3.2 Saudi Arabia’s Global Trade in Products ................................................................. 8

3.3 Trade with South Africa ......................................................................................... 11

3.4 Trade with the Western Cape ............................................................................... 12

3.5 Saudi Arabia’s Trade Agreements ........................................................................ 13

3.6 Port to Port ........................................................................................................... 14

3.7 Tariffs.................................................................................................................... 14

4. FDI ............................................................................................................................... 17

4.1 Inward FDI to Saudi Arabia ................................................................................... 17

4.2 Outward FDI from Saudi Arabia ............................................................................ 20

4.3 South African FDI with Saudi Arabia ..................................................................... 24

5. Tourism ........................................................................................................................ 25

5.1 Saudi Arabia Trends and Travel Patterns ............................................................. 25

5.2 Saudi Arabian Tourist Arrivals into South Africa .................................................... 25

3

1. General Information

Saudi Arabia is the largest Arab state in Western Asia by land area (approximately 2,150,000 km2 and the second-

largest in the Arab world after Algeria). It is bordered by Jordan and Iraq to the north, Kuwait to the northeast,

Qatar, Bahrain and the United Arab Emirates to the east, Oman to the southeast, and Yemen in the south. It is the

only nation with both a Red Sea coast and a Persian Gulf coast.

Saudi Arabia is an absolute monarchy and the king combines legislative, executive, and judicial functions. It is an

active member of the Organisation of Islamic Cooperation, Arab League, Gulf Cooperation Council, Organisation

of Islamic Cooperation and OPEC.

GENERAL INFORMATION

Population 27,752,316

Capital Riyadh

Chief of state King and Prime Minister SALMAN bin Abd

al-Aziz Al Saud

Official language(s) Arabic (official)

Ethnic group(s) Arab 90%, Afro-Asian 10%

Religion(s)

Muslim (official; citizens are 85-90% Sunni

and 10-15% Shia), other (includes Eastern

Orthodox, Protestant, Roman Catholic,

Jewish, Hindu, Buddhist, and Sikh

Life expectancy 75.05 years

Literacy rate 94.7%

HDI (2015) 0.837 (Ranked 39th)

Source: CIA World Factbook, 2016

2. Economic Overview

Saudi Arabia has an oil-based economy with strong government controls over major economic activities. It

possesses about 16% of the world's proven petroleum reserves, ranks as the largest exporter of petroleum, and

plays a leading role in OPEC. The petroleum sector accounts for roughly 80% of budget revenues, 45% of GDP,

and 90% of export earnings. Saudi Arabia officially has about 260 billion barrels (4.1×1010m3) of oil reserves,

comprising about one-fifth of the world's proven total petroleum reserves.

Saudi Arabia is encouraging the growth of the private sector in order to diversify its economy and to employ more

Saudi nationals. Diversification efforts are focusing on power generation, telecommunications, natural gas

exploration, and petrochemical sectors.

In 2015, Saudi Arabia’s GDP (PPP) was estimated at USD1.7trn, making Saudi Arabia the world's 15th largest

economy. In 2015, Saudi Arabia’s GDP growth was at 3.4%. On a per capita income basis, Saudi Arabia’s is ranked

21st with a GDP per capita of USD54,600 according to the International Monetary Fund (IMF).

ECONOMIC INFORMATION

GDP (PPP) (2015 est.) USD1.681trn

GDP growth (2015 est.) 3.4%

GDP per capita (2015 est.) USD54,600

Inflation (2015 est.) 2.3%

Interest rate (31 December 2015 est.) 6.7%

Unemployment rate (2015 est.) 11.4%

Exports (2014) ZAR3.8trn

Imports (2014) ZAR1.7trn

Doing Business in...(2016 ranking) 82

Source: Ease of Doing Business, 2016; CIA World Factbook, 2016

4

The figure below illustrates the GDP value and growth for Saudi Arabia’s economy for the period 2012 to 2020.

The economy will experience a steady increase in GDP value during the forecast period with GDP increasing from

SAR2.3trn in 2012 to SAR2.9trn in 2020. Growth in Saudi Arabia will slow sharply over the next couple of years as

the government embarks on fiscal consolidation and oil production flattens. GDP average annual growth is forecast

at 2.9% for 2016 to 2020.

Source: IMF, 2016

According to the figure below, Saudi Arabia’s largest sector was crude petroleum and natural gas sector at 46%

share of GDP in 2014. Manufacturing accounted for 13% share of GDP, followed by finance insurance real estate

and business services with 11% share of GDP.

Key industries: in Saudi Arabia the key industries are crude oil production, petroleum refining, basic

petrochemicals, ammonia, industrial gases, sodium hydroxide (caustic soda), cement, fertilizer, plastics, metals,

commercial ship repair, commercial aircraft repair and construction. The main agricultural products produced in

Saudi Arabia are wheat, barley, tomatoes, melons, dates, citrus; mutton, chickens, eggs, milk.

Some key sectors in Saudi Arabia are highlighted below:

Petroleum: Saudi oil reserves are the 2nd largest in the world, and Saudi Arabia is the world's leading oil producer

and exporter. Oil accounts for more than 90% of the country's exports and nearly 75% of government revenues.

The petrochemicals sector is the largest non-oil sector in Saudi Arabia. Saudi Arabia is the world’s 11th largest

petrochemicals supplier, accounting for 7-8% of total supply. While the nation’s current strengths lie in the

production of basic petrochemical building blocks such as ethylene and methanol, there are plans to diversify its

petrochemical portfolio into more complex, distinctive products such as specialty chemicals and engineering

thermoplastics.

ICT: With over 27 million consumers and a number of global enterprises, Saudi Arabia is the largest ICT market by

far in the Middle East. For example, the Saudi Arabian telecommunications and information technology industries

represent over 55% and 51% of the total Middle East markets, respectively.

Transport and logistics: Saudi Arabia’s strategic location and large-scale infrastructure development will position

KSA as one of the world’s leading transport and logistics hubs. The transport and logistics sector in Saudi is

supporting a population of 27.14 million (2010), and within only 3 hours flying radius, this sector can serve both

cargo and passengers of more than 250 million inhabitants in neighbouring countries

2012 2013 2014 2015 2016f 2017f 2018f 2019f 2020f

Value (SARbn) 2 289 2 350 2 432 2 515 2 571 2 645 2 725 2 809 2 898

Growth 5.4% 2.7% 3.5% 3.4% 2.2% 2.9% 3.0% 3.1% 3.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0

500

1 000

1 500

2 000

2 500

3 000

3 500

Gro

wth

Valu

e (

SA

Rbn)

SAUDIA ARABIAN GDP, 2012-2020

5

Source: Central Department of Statistics & Information, 2016

The table below lists Saudi Arabia’s top 20 companies on the Forbes List in 2015.

TOP 10 SAUDI ARABIAN COMPANIES ON FORBES TOP 2000 COMPANIES IN THE WORLD, 2015

FORBES RANK

COMPANY SECTOR SALES

(USDbn) PROFITS (USDbn)

ASSETS (USDbn)

MARKET VALUE

(USDbn)

#116 Saudi Basic Industries Chemicals 50.4 6.2 90.9 64

#405 Saudi Telecom Telecommunications 12.3 2.9 24.2 32.8

#474 Saudi Electricity Energy 10.3 0.963 84.7 18.8

#488 National Commercial Bank

Banking 5 2.3 115.9 31.9

#597 Al Rajhi Bank Banking 3.7 1.8 82 24.5

#754 Samba Financial Group Banking 2.1 1.3 57.9 13.4

#771 Riyad Bank Banking 2.4 1.2 57.2 13.5

#782 Saudi British Bank Banking 1.9 1.1 50 13.1

#849 Banque Saudi Fransi Banking 1.7 0.938 50.3 11

#971 Arab National Bank Banking 1.6 0.767 43.9 8.7

#1289 Savola Group Food processing 7.3 0.553 7.1 9.7

#1290 Saudi Arabian Mining Minerals & mining 2.9 0.362 22.5 11.7

#1311 Saudi Arabian Fertilizers Chemicals 1.2 0.846 2.4 13.3

#1412 Saudi Hollandi Bank Banking 0.987 0.486 25.7 6.2

#1495 Alinma Bank Banking 0.755 0.337 21.5 8.6

#1527 Kingdom Holding Investment Services 0.896 0.232 12.5 19.6

#1554 Almarai Food processing 3.4 0.446 6.4 13.6

#1641 Petro Rabigh Chemicals 14.5 0.182 10.9 4.8

#1672 Saudi Investment Bank Banking 842 0.383 25 3.8

#1826 Jabal Omar Development Banking 0.197 0.154 5 18.8

Source: Forbes 2000, 2016

Agriculture , Forestry & Fishing2.4%

Crude Petroleum & Natural Gas

46.1%

Other mining & quarry0.4%

Manufacturing13.4%

Electricity , Gas and Water1.5%

Construction5.8%

Wholesale & Retail Trade, Restaurants &

hotels10.8%

Transport , Storage & Communication

6.5%

Finance , Insurance , Real Estate &

business services 10.8%

Community , Social & Personal Services

2.3%

SAUDI ARABIA SECTOR CONTRIBUTION TO GDP, 2014

6

2.1 Doing Business in Saudi Arabia

According to the World Bank’s Doing Business 2016 report, Saudi Arabia is ranked 82 out of 189 countries in

terms of ease of doing business. Saudi Arabia’s ease of doing business is evident in terms of paying taxes (3rd);

dealing with Construction Permits (17th) and getting electricity (24th).

SAUDI ARABIA EASE OF DOING BUSINESS, 2016

TOPIC RANKING RANKING OUT OF 189

COUNTRIES, 2016

Starting a Business 130

Dealing with Construction Permits 17

Getting Electricity 24

Registering Property 31

Getting Credit 79

Protecting Investors 99

Paying Taxes 3

Trading Across Borders 150

Enforcing Contracts 86

Resolving Insolvency 189

Doing Business 2016 82

Source: Cost of Doing Business, 2016

2.2 Saudi Arabia Risk Ratings

The table below shows Saudi Arabia’s sovereign risk and it indicates very strong capacity to meet financial

commitments. The decline in oil prices will have a marked and lasting impact on Saudi Arabia's fiscal and economic

indicators given its high dependence on oil. According to Moodys, Saudi Arabia's (Aa3 stable) fiscal position is

weakening but is still relatively strong. Volatile oil prices will continue to weigh on the government's balance sheet.

It expects that lower oil revenues will result in continued large budget deficits, a drawdown in reserves, and

increased sovereign debt issuance

Saudi Arabia is currently facing a huge budget deficit which is expected to reach USD87bn in 2016 according

official government numbers. However, the actual figure is expected to be much higher as the IMF estimated last

year's deficit at USD140bn. The kingdom’s oil sales account for almost 80% of the country’s revenues.

SAUDI ARABIA’S COUNTRY RATINGS

STANDARD & POORS SOVEREIGN RATINGS FITCH RATING MOODY'S RATINGS

Local Currency

Rating

Foreign Currency

Rating T&C Assessment Credit Rating Credit Rating

A- A- A- AA Aa3

Source: Standard & Poors, 2016

The table below shows Saudi Arabia’s risk assessment in terms of export transactions and direct investments.

Ratings are between 1 and 7, and between A and C, with 7 and C being the maximum risk indicators. The political

risk in Saudi Arabia is low in the short term and medium to long-term. Special transaction risk is moderate together

with some categories of direct investment risk, i.e. risk of expropriation and government action(3) and transfer

risk(3).

SAUDI ARABIA RISK ASSESSMENT

EXPORT TRANSACTIONS

Political Risks

Short Term 2

Medium-Long term 2

Special Transactions 2

Commercial Risk B

DIRECT INVESTMENTS

War risk 4

Risk of expropriation and government action 3

Transfer risk 3

Source: ONDD, 2016

7

3. Trade

3.1 Saudi Arabia’s Global Trade in Services

In 2014 Saudi Arabia experienced the highest trade in services both in terms of exports and imports over the ten

year period. Saudi Arabia’s exports of services increased by 16% in 2014 to reach ZAR132bn, while imports

increased by 43% in 2014 to reach ZAR1trn. From 2005 to 2014 a negative trade balance was experienced by

Saudi Arabia.

Source: TradeMap, 2016

The table below shows Saudi Arabia’s trade in services for the period 2014. Travel was the largest services export

valued at ZAR89bn followed by transportation valued at ZAR30bn. Government services was the largest import

service into Saudi Arabia valued at ZAR410bn followed by travel and transport services valued at ZAR261bn and

ZAR216bn respectively.

SAUDI ARABIA’S TOP 10 EXPORTS OF SERVICES, 2014 SAUDI ARABIA’S TOP 10 IMPORTS OF SERVICES, 2014

Code SERVICE VALUE

2014 (ZARbn)

% GROWTH 2010-2014

Code SERVICE VALUE

2014 (ZARbn)

% GROWTH 2010-2014

'4 Travel 89.2 12.99% '12 Government goods and services n.i.e.

410 16.20%

'3 Transport 29.7 14.47% '4 Travel 261 11.89%

'12 Government goods and services n.i.e. 6.0 19.09% '3 Transport 216 18.54%

'7 Financial services 2.3 11.13% '10 Other business services 72 9.52%

'9 Telecommunications, computer, and information services

2.2 7.78% '5 Construction 34 8.27%

'6 Insurance and pension services 1.9 2.92% '9 Telecommunications, computer, and information services

24 10.04%

'10 Other business services 1.0 16.99% '6 Insurance and pension services 22 13.45%

TOTAL EXPORTS 132.3 10.79% TOTAL IMPORTS 1 049 12.48%

Source: TradeMap, 2016

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports (ZARbn) 72 95 115 76 81 78 83 90 114 132

Imports (ZARbn) 210 332 443 610 622 560 561 600 736 1 049

Trade balance (ZARbn) -137 -237 -328 -534 -541 -482 -478 -510 -622 -917

-1 500

-1 000

-500

0

500

1 000

1 500

Valu

e (

ZA

Rbn)

SAUDI ARABIA SERVICES TRADE, 2005-2014

8

3.2 Saudi Arabia’s Global Trade in Products

In 2014 Saudi Arabia experienced the highest trade value both in terms of exports and imports over the ten year

period. Global exports from Saudi Arabia in 2014 were valued at ZAR3.8trn compared to ZAR3.6trn in 2013,

increasing by 6.6%. Global imports into Saudi Arabia were valued at ZAR1.7trn in 2014 compared to ZAR1.5trn in

2013, increasing by 15%. The trade balance over the period has been consistently positive as Saudi Arabia is a

net exporter.

Source: TradeMap, 2016

China was the leading export market for Saudi Arabia with a value of ZAR525bn. Japan and the United States

ranked second and third valued at ZAR513bn and ZAR509bn respectively. Other top destination markets were

Republic of Korea (ZAR398bn); India (ZAR354bn) and Singapore (ZAR158bn).

TOP 10 DESTINATION MARKETS FOR EXPORTS FROM

SAUDI ARABIA, 2014

RANK MARKET

VALUE

2014

(ZARbn)

%

GROWTH

2010-2014

%

SHARE

2014

1 China 525 22.73% 13.87%

2 Japan 513 16.89% 13.56%

3 United States 509 22.58% 13.45%

4 Korea, Republic

of 398 19.78% 10.50%

5 India 354 24.83% 9.35%

6 Singapore 158 20.70% 4.18%

7 Taipei, Chinese 148 15.86% 3.91%

8 France 102 33.67% 2.69%

9 Bahrain 91 561.53% 2.39%

10 Thailand 85 21.00% 2.24%

11 South Africa 77 29.24% 2.04%

TOTAL EXPORTS 3 786 20.92% 100%

Source: TradeMap, 2016

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports (ZARbn) 1 049 1 381 1 545 2 654 1 503 1 755 2 529 3 087 3 553 3 786

Imports (ZARbn) 330 415 565 821 679 690 834 1 134 1 466 1 684

Trade balance (ZARbn) 719 966 980 1 832 824 1 065 1 695 1 953 2 088 2 102

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

Valu

e (

ZA

Rbn)

GLOBAL FDI INTO SAUDI ARABIA, 2005-2014

9

China was the leading import market in 2014 valued at ZAR223bn. The United States and India were ranked

second and third valued at ZAR203bn and ZAR141bn respectively. Other top import markets were Germany

(ZAR129bn); the Republic of Korea (ZAR90bn) and Japan (ZAR82bn).

TOP 10 SOURCE MARKETS FOR IMPORTS TO SAUDI ARABIA, 2014

RANK MARKET VALUE

2014 (ZARbn)

% GROWTH 2010-2014

% SHARE

2014

1 China 223 25.43% 13.23%

2 United States 203 18.97% 12.03%

3 India 141 38.63% 8.40%

4 Germany 129 18.89% 7.65%

5 Korea, Republic of 90 24.60% 5.33%

6 Japan 82 14.32% 4.89%

7 United Kingdom 74 17.91% 4.42%

8 Italy 69 21.15% 4.11%

9 Switzerland 54 42.78% 3.22%

10 France 42 9.35% 2.52%

47 South Africa 4.8 17.97% 0.28%

TOTAL IMPORTS 1 684 20.51% 100.00%

Source: TradeMap, 2016

In 2014 Saudi Arabia was the 16th largest exporter of

global goods at ZAR3.8trn and the 30th largest importer of

global goods at ZAR1.7trn.

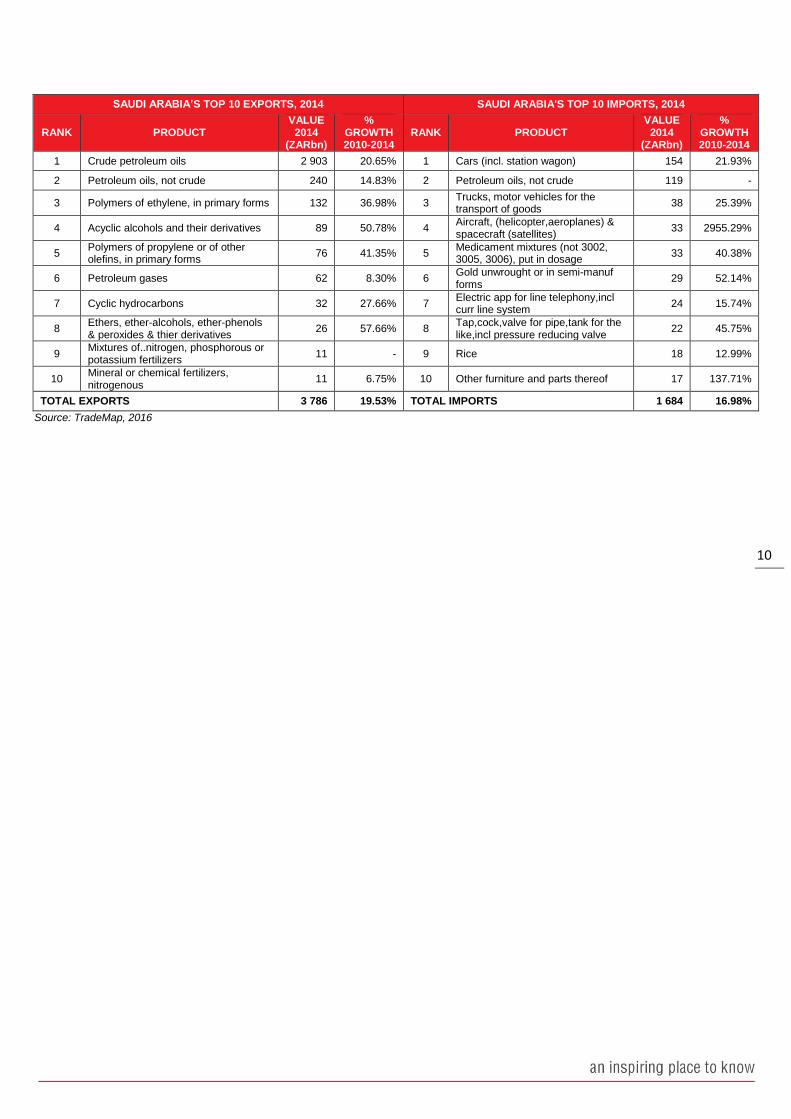

Crude petroleum was the leading export product valued at ZAR2.9trn. Refined petroleum (ZAR240bn) and

polymers of ethylene, in primary forms (ZAR132bn) were ranked second and third respectively. Other top exports

were acyclic alcohols and their derivatives (ZAR89bn); petroleum gases (ZAR62bn) and cyclic hydrocarbons

(ZAR32bn).

In 2014, cars was the leading import product by Saudi Arabia, valued at ZAR154bn. Refined petroleum and trucks

were ranked second and third at ZAR119bn and ZAR38bn respectively. Other top imports aircraft (ZAR33bn) and

medicaments (ZAR33m).

2nd Global Exporter of

Mineral fuels, oils, distillation products

5thGlobal Importer for

Cereals

9th Global Exporter of Fertilizers

2nd Global Importer for Arms and

ammunition, parts and

accessories

6th Global Importer for

Ceramic products

8th Global Exporter

Plastics and articles thereof

10

SAUDI ARABIA’S TOP 10 EXPORTS, 2014 SAUDI ARABIA'S TOP 10 IMPORTS, 2014

RANK PRODUCT VALUE

2014 (ZARbn)

% GROWTH 2010-2014

RANK PRODUCT VALUE

2014 (ZARbn)

% GROWTH 2010-2014

1 Crude petroleum oils 2 903 20.65% 1 Cars (incl. station wagon) 154 21.93%

2 Petroleum oils, not crude 240 14.83% 2 Petroleum oils, not crude 119 -

3 Polymers of ethylene, in primary forms 132 36.98% 3 Trucks, motor vehicles for the transport of goods

38 25.39%

4 Acyclic alcohols and their derivatives 89 50.78% 4 Aircraft, (helicopter,aeroplanes) & spacecraft (satellites)

33 2955.29%

5 Polymers of propylene or of other olefins, in primary forms

76 41.35% 5 Medicament mixtures (not 3002, 3005, 3006), put in dosage

33 40.38%

6 Petroleum gases 62 8.30% 6 Gold unwrought or in semi-manuf forms

29 52.14%

7 Cyclic hydrocarbons 32 27.66% 7 Electric app for line telephony,incl curr line system

24 15.74%

8 Ethers, ether-alcohols, ether-phenols & peroxides & thier derivatives

26 57.66% 8 Tap,cock,valve for pipe,tank for the like,incl pressure reducing valve

22 45.75%

9 Mixtures of..nitrogen, phosphorous or potassium fertilizers

11 - 9 Rice 18 12.99%

10 Mineral or chemical fertilizers, nitrogenous

11 6.75% 10 Other furniture and parts thereof 17 137.71%

TOTAL EXPORTS 3 786 19.53% TOTAL IMPORTS 1 684 16.98%

Source: TradeMap, 2016

11

3.3 Trade with South Africa

South Africa exported goods to Saudi Arabia valued at ZAR4.8bn in 2014 compared to ZAR2.6bn in 2013,

representing an increase of 83%, while imported goods were valued at ZAR77.3bn in 2014 compared to ZAR77.4bn

in 2013, decreasing by 0.15%. South Africa had a constant trade deficit with Saudi Arabia, with imports exceeding

exports over the ten year period.

Source: Quantec, 2016

The leading export product to Saudi Arabia from South Africa was motor vehicles for the transport of goods valued

at ZAR819m, followed by citrus fruit (ZAR754m) and aluminium plates (ZAR410m). Flat-rolled products of iron or

non-alloy steel was the fastest growing export product over the five year period.

The leading imported product from Saudi Arabia into South Africa was crude petroleum valued at ZAR67bn,

followed by refined petroleum (ZAR4.5bn) and Polymers of ethylene, in primary forms (ZAR1.2bn). The import of

Sulphur was the fastest growing import into South Africa from Saudi Arabia over the five year period.

SOUTH AFRICA'S TOP 10 EXPORTS TO SAUDI ARABIA’S, 2014 SOUTH AFRICA'S TOP 10 IMPORTS FROM SAUDI ARABIA’S, 2014

RANK PRODUCT VALUE

2014 (ZARm)

% GROWTH 2010-2014

RANK PRODUCT VALUE

2014 (ZARm)

% GROWTH 2010-2014

1 Motor vehicles for the transport of goods.

819 - 1 Crude petroleum oils 66 976 30.83%

2 Citrus fruit, fresh or dried. 754 19.7% 2 Refined Petroleum oils 4 505 173.94%

3 Aluminium plates, sheets and strip, of a thickness exceeding 0.2 mm.

410 18.5% 3 Polymers of ethylene, in primary forms.

1 229 20.99%

4 Titanium ores and concentrates. 313 - 4 Acyclic alcohols and their halogenated, sulphonated, nitrated or nitrosated derivatives.

780 34.13%

5 Manganese ores and concentrates, 251 42.4% 5 Mineral or chemical fertilisers, nitrogenous.

748 4.87%

6 Iron ores and concentrates, including roasted iron pyrites.

175 - 6 Cyclic hydrocarbons. 690 40.80%

7 Flat-rolled products of other alloy steel, of a width of 600 mm or more.

168 - 7 Acyclic hydrocarbons. 549 31.74%

8 Flat-rolled products of iron or non-alloy steel, of a width of 600 mm or more

160 195.6% 8 Mixed alkylbenzenes and mixed alkylnaphthalenes

393 44.94%

9 Copper powders and flakes. 115 - 9 Sulphur of all kinds, other than sublimed sulphur

222 1058.38%

10 Maize (corn). 104 - 10

Mineral or chemical fertilisers containing two or three of the fertilising elements nitrogen, phosphorus and potassium

175 -

TOTAL EXPORTS 4 789 17.9% TOTAL IMPORTS 77 327 29.14%

Source: Quantec, 2016

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports (ZARm) 1 496 1 715 1 651 2 279 2 720 2 488 2 653 2 588 2 919 2 620 4 789

Imports (ZARm) 17 086 19 408 24 545 25 360 45 958 26 651 23 674 32 295 65 148 77 440 77 327

Trade balance (ZARm) -15 590-17 693-22 894-23 081-43 237-24 163-21 022-29 707-62 229-74 820-72 539

-100 000

-80 000

-60 000

-40 000

-20 000

0

20 000

40 000

60 000

80 000

100 000

Valu

e (

ZA

Rm

)

SOUTH AFRICA TRADE WITH SAUDI ARABIA, 2004-2014

12

3.4 Trade with the Western Cape

The province exported goods to the value of ZAR893m in 2014 compared to ZAR718m in 2013, representing a

decrease of 24%, while imported goods were valued at ZAR46bn in 2014 compared to ZAR49bn in 2013,

increasing by 6.1%.

Source: Quantec, 2016

Citrus fruit was the leading export product category to Saudi Arabia from the Western Cape in 2014, valued at

ZAR398m. This is followed by flat-rolled products of iron or non-alloy steel, valued at ZAR160m. Half of the top ten

products exported by the Western Cape include agro-processing products revealing a high demand for these

products. The leading import products into the Western Cape from Saudi Arabia include crude petroleum valued

at ZAR43bn, followed by refined petroleum valued at ZAR2.2bn.

WESTERN CAPE’S TOP 10 EXPORTS TO SAUDI ARABIA’S, 2014 WESTERN CAPE’S TOP 10 IMPORTS FROM SAUDI ARABIA’S, 2014

RANK PRODUCT VALUE

2014 (ZARm)

% GROWTH 2010-2014

RANK PRODUCT VALUE,

2014 (ZARm)

% GROWTH 2010-2014

1 Citrus fruit, fresh or dried. 397.8 9.78% 1 Crude Petroleum oils 42 725.6 33.66%

2 Flat-rolled products of iron or non-alloy steel

160.3 - 2 Refined Petroleum oils 2 157.8 229.66%

3 Apples, pears and quinces, fresh. 72.1 27.86% 3 Acyclic alcohols and their halogenated, sulphonated, nitrated

574.6 -

4 Apricots, cherries, peaches (including nectarines), plums and sloes, fresh.

59.9 23.23% 4 Mixed alkylbenzenes and mixed alkylnaphthalenes.

393.2 -

5 Grapes, fresh or dried. 52.4 22.49% 5 Cyclic hydrocarbons. 51.2 -

6 Transfers (decalcomanias). 42.1 20.43% 6 Coal; briquettes, ovoids and similar solid fuels manufactured from coal.

26.3 -

7 Other plates, sheets, film, foil and strip, of plastics, non-cellular

23.9 10.50% 7 Saturated acyclic monocarboxylic acids

14.6 -

8 Parts suitable for use solely or principally with the machinery of headings 84.25 to 84.30.

12.9 - 8 Polyacetals, other polyethers and epoxide resins, in primary forms

8.3 -

9 Fruit, nuts and other edible parts of plants

11.0 - 9 Carboys, bottles, flasks, jars, pots, phials, ampoules and other containers, of glass

7.0 -22.21%

10 Other live plants (including their roots), cuttings and slips; mushroom spawn.

6.9 - 10 Polymers of ethylene, in primary forms.

6.2 -

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Exports (ZARm) 4.5 396 351 396 446 520 622 750 1 094 718 893

Imports (ZARm) 11 526 13 507 17 134 15 882 26 454 13 677 12 476 17 154 38 682 48 855 45 978

Trade balance (ZARm) -11 521 -13 111 -16 783 -15 486 -26 008 -13 157 -11 854 -16 403 -37 589 -48 137 -45 085

-60 000

-40 000

-20 000

0

20 000

40 000

60 000

Valu

e (

ZA

Rm

)

SAUDI ARABIA FDI TO WESTERN CAPE, 2004-2014

13

WESTERN CAPE’S TOP 10 EXPORTS TO SAUDI ARABIA’S, 2014 WESTERN CAPE’S TOP 10 IMPORTS FROM SAUDI ARABIA’S, 2014

RANK PRODUCT VALUE

2014 (ZARm)

% GROWTH 2010-2014

RANK PRODUCT VALUE,

2014 (ZARm)

% GROWTH 2010-2014

TOTAL EXPORTS 893.2 15.19% TOTAL IMPORTS 45 978.4 34.93%

Source: Quantec, 2016

Western Cape trade with Saudi Arabia by sector is shown below. The largest share of exports to Saudi Arabia

were:

Printing, publishing & recorded media sector accounting for 24%,

Machinery and equipment (21%),

Plastic products (13%) and

Basic iron and steel (9%).

Source: Quantec, 2014

3.5 Saudi Arabia’s Trade Agreements

Saudi Arabia is a member of the key trade agreements below:

International Economic Cooperation: Saudi Arabia is a main player in the commercial life around the world. By

signing agreements with world trade organizations and many European and Asian countries, Saudi Arabia has

created a powerful cooperation within the world economy.

0.1%

0.1%

0.2%

0.2%

0.6%

0.8%

1.1%

1.6%

2.1%

2.1%

2.8%

6.6%

7.7%

8.2%

8.6%

12.8%

20.8%

23.5%

0% 5% 10% 15% 20% 25%

Furniture

Coke & refined petroleum products

Textiles

Electrical machinery

Metal products excluding machinery

Tobacco

Other transport equipment

Wearing apparel

Television, radio & communication equipment

Basic chemicals

Motor vehicles, parts & accessories

Other chemicals & man-made fibres

Food

Professional & scientific equipment

Basic iron & steel

Plastic products

Machinery & equipment

Printing, publishing & recorded media

WESTERN CAPE EXPORTS SAUDI ARABIA BY SECTOR, (% SHARE), 2013

% share

14

Gulf Cooperation Council : The Gulf Cooperation Council (GCC) was founded in May 1981, by the leaders of the

United Arab Emirates, the Kingdom of Bahrain, the Kingdom of Saudi Arabia, the Sultanate of Oman, the State of

Qatar and the State of Kuwait. The GCC Charter documents the special relations of the six states, their common

qualities and similar systems founded on the creed of Islam, and their faith in a common destiny.

3.6 Port to Port

The table below shows the distance and time it takes goods to travel from Cape Town Port terminal to Saudi Arabia:

CAPE TOWN PORT TERMINAL TO SAUDI ARABIA’S MAIN SEA PORTS

SEA PORTS DISTANCE TRANSIT TIME

Dammam Terminal 9388.15km 15 days 2 hours

Dhuba 9464.47km 15 days 5 hours

Dhuba Bulk Plant Terminal 9444.08km 15 days 4 hours

Gizan 8170.51km 13 days 3 hours

Jeddah Terminal 8793.88km 14 days 3 hours

Jubail Terminal 9450.76km 15 days 4 hours

Qadhimah 8895.86km 14 days 7 hours

Rabigh 8941.34km 14 days 8 hours

Ras al Mishab 9572.02km 15 days 9 hours

Ras Tanura 9391.26km 15 days 2 hours

Source: Sea-Rates, 2016

3.7 Tariffs

Saudi Arabia’s tariffs imposed on South Africa’s export products (HS2) are shown in the table below.

SAUDI ARABIA’S TARIFF IMPOSED ON SOUTH AFRICAN EXPORTS (HS2), 2014

HS CODE

PRODUCT

Total ad valorem

equivalent tariff (%)

HS CODE

PRODUCT

Total ad valorem

equivalent tariff (%)

HS CODE

PRODUCT

Total ad valorem

equivalent tariff (%)

01 Live animals 0 34 Soaps, lubricants, waxes, candles, modelling pastes

5 67 Bird skin, feathers, artificial flowers, human hair

5

02 Meat and edible meat offal 4.3 35 Albuminoidal substances; modified starches; glues; enzymes

5 68 Stone, plaster, cement, asbestos, mica, articles

5

03 Fish, crustaceans, molluscs, aquatic invertebrates

2.9 36 Explosives, pyrotechnics, matches, pyrophorics

5 69 Ceramic products 5

04 Dairy products, eggs, honey, edible animal product

4.9 37 Photographic or cinematographic goods

5 70 Glass and glassware 5

05 Products of animal origin, not elsewhere specified or included

5 38 Miscellaneous chemical products

4.7 71 Pearls, precious stones, metals, coins

3.7

06 Live trees, plants, bulbs, roots, cut flowers

3.5 39 Plastics and articles thereof 5 72 Iron and steel 5

07 Edible vegetables and certain roots and tubers

2.4 40 Rubber and articles thereof 5 73 Articles of iron or steel 5

08 Edible fruit and nuts; peel of citrus fruits or melons

1.4 41 Raw hides and skins (other than furskins) and leather

5 74 Copper and articles thereof

5

09 Coffee, tea, maté and spices

1.2 42 Articles of leather, animal gut, harness, travel goods

5 75 Nickel and articles thereof

5

10 Cereals 0 43 Furskins and artificial fur; manufactures thereof

5 76 Aluminium and articles thereof

5

11 Products of the milling industry; malt; starches; inulin; wheat gluten

2.3 44 Wood and articles of wood; wood charcoal

5 78 Lead and articles thereof

5

12 Oil seed, oleagic fruits, grain, seed, fruit

2 45 Cork and articles of cork 5 79 Zinc and articles thereof

5

15

SAUDI ARABIA’S TARIFF IMPOSED ON SOUTH AFRICAN EXPORTS (HS2), 2014

HS CODE

PRODUCT

Total ad valorem

equivalent tariff (%)

HS CODE

PRODUCT

Total ad valorem

equivalent tariff (%)

HS CODE

PRODUCT

Total ad valorem

equivalent tariff (%)

13 Lac; gums, resins and other vegetable saps and extracts

5 46 Manufactures of plaiting material, basketwork,

5 80 Tin and articles thereof

5

14 Vegetable plaiting materials, vegetable products

5 47 Pulp of wood, fibrous cellulosic material, waste

5 81 Other base metals; cermets; articles thereof

5

15 Animal, vegetable fats and oils, cleavage products

5 48 Paper and paperboard; articles of paper pulp, of paper or of paperboard

5 82 Tools, implements, cutlery, of base metal

5

16 Meat, fish and seafood food preparations

5 49 Printed books, newspapers, pictures

5 83 Miscellaneous articles of base metal

5

17 Sugars and sugar confectionery

0.4 50 Silk 5 84

Nuclear reactors, boilers, machinery and mechanical appliances; parts thereof

4.1

18 Cocoa and cocoa preparations

5 51 Wool, fine or coarse animal hair; horsehair yarn and woven fabric

5 85 Electrical, electronic equipment

2.6

19 Preparations of cereals, flour, starch or milk; pastrycooks' products

3.5 52 Cotton 4.7 86 Railway, tramway locomotives, rolling stock, equipment

5

20 Preparations of vegetables, fruit, nuts or other parts of plants

5 53 Other vegetable textile fibres; paper yarn and woven fabrics of paper yarn

5 87 Vehicles other than railway, tramway

5

21 Miscellaneous edible preparations

4.8 54 Man-made filaments 5 88 Aircraft, spacecraft, and parts thereof

2.1

22 Beverages, spirits and vinegar

4.9 55 Man-made staple fibres 5 89 Ships, boats and floating structures

0.3

23 Residues and waste from the food industries; prepared animal fodder

1.6 56 Wadding, felt, nonwovens, yarns, twine, cordage

5 90 Optical, photo, technical, medical, apparatus

4.1

24 Tobacco and manufactured tobacco substitutes

115.7 57 Carpets and other textile floor coverings

5 91 Clocks and watches and parts thereof

5

25 Salt; sulphur; earths and stone; plastering materials, lime and cement

5 58 Special woven or tufted fabric, lace, tapestry

5 92 Musical instruments; parts and accessories of such articles

5

26 Ores, slag and ash 5 59 Impregnated, coated or laminated textile fabric

5 93 Arms and ammunition; parts and accessories thereof

-

27 Mineral fuels, oils, distillation products

5 60 Knitted or crocheted fabrics 5 94 Furniture, lighting, signs, prefabricated buildings

5

28 Inorganic chemicals, precious metal compound, isotopes

5 61 Articles of apparel and clothing accessories, knitted or crocheted

5 95 Toys, games, sports requisites

5

29 Organic chemicals 3.4 62 Articles of apparel and clothing accessories, not knitted or crocheted

5 96 Miscellaneous manufactured articles

5

30 Pharmaceutical products 0 63 Other made textile articles, sets, worn clothing

5 97 Works of art, collectors' pieces and antiques

5

31 Fertilizers 5 64 Footwear, gaiters and the like; parts of such articles

5 - -

32 Tanning, dyeing extracts, tannins, derivatives, pigments

5 65 Headgear and parts thereof 5 - -

33 Essential oils, perfumes, cosmetics, toiletries

5 66 Umbrellas, walking-sticks, seat-sticks, whips

4.7 - -

Source: Market Access Map, 2016

NOTE: Exporters should not take the HS2 tariff as conclusive and as the actual tariff that will be applied to the exported product.

The tariffs indicated above are average tariffs and for products within the category it may be higher or lower than indicated. Where

the tariff is zero it can be assumed that there is zero tariff applicable to all products within that HS code. Tariffs are determined

according to the importing country’s national tariff line from the HS6 level and upwards. Exporters are advised to visit

www.macmap.org to determine the exact tariff applicable to the product at HS6.

16

3.8 Trade regulations, Customs and Standards

Import Requirements and Documentation

Under its WTO obligations, Saudi Arabia has committed to implement a transparent and predictable import

licensing system. The following documents are required for exporting goods to Saudi Arabia:

certificate of origin;

commercial invoice (in triplicate) which must state the country of origin, name of the carrier, brand and

number of goods, and description of the goods including weight and value;

a clean bill of lading or airway bill;

documents indicating compliance with health regulations, if applicable;

insurance documents, if shipments are sent CIF;

packing list; and

certificate of conformity with applicable Saudi Arabian standards, if available.

The original documents must be accompanied by an Arabic translation of a radiation certificate, if applicable.

Labelling and Marking

Labelling and marking requirements are compulsory for any products exported to Saudi Arabia. Labelling is

particularly important for companies marketing food products, personal care products, health care products, and

pharmaceuticals. Labels must be in Arabic for any imported foodstuff item, which should basically reveal the same

information on the container as in the foreign language.

The product(s) must have a label or sticker showing the statutory information such as

product name,

country of origin,

producer’s name and address,

production and expiry/use by dates,

in Arabic and English languages (samples imported must be labelled at least in English).

Product Certification

The Saudi Arabian Standards Organization SASO has its own certification organization for locally manufactured

products, as several SASO employees have been certified to work as professional auditors in conformance with

ISO 9000 series standards. For imported products, the Ministry of Commerce and Industry will implement the CoC

program, which should be abolished under Saudi Arabia’s WTO accession commitments.

Prohibited and Restricted Imports

There are health and sanitation regulations for all imported foods. Importing the following products requires special

approval by Saudi Arabian authorities: agriculture seeds, live animals, books, periodicals, movies, and tapes;

religious books and tapes; chemicals and harmful materials; pharmaceutical products; wireless equipment, and

radio controlled model airplanes; horses; products containing alcohol (e.g., perfume); natural asphalt; and

archaeological artifacts.

Saudi law prohibits importation of the following products:

weapons,

alcohol,

narcotics,

pork,

pornographic materials,

distillery equipment,

retreaded or used tires,

used clothing and

certain sculptures.

17

4. FDI

4.1 Inward FDI to Saudi Arabia

Between January 2003 and July 2015 a total of 1,217 FDI projects were recorded into Saudi Arabia. These projects

represent a total capital investment of ZAR1,785.79bn which is an average investment of ZAR1,466.98m per

project. During the period, a total of 169,392 jobs were created.

Source: FDI Intelligence, 2016

The figures below shows Saudi Arabia’s sector global inward FDI for the period 2003 to July 2015 by number of

projects and capex. In terms of sectors by projects most investments were in the following:

Business services sector received the largest share in terms of projects accounting for 11%,

Financial services sector 9% of projects and,

Textiles accounting for 8.7% of projects.

In terms of sectors capex most investments were in the following:

Chemicals sector received the largest share in terms of capex accounting for 31%,

Coal, oil and natural gas sector accounting for 25%, and

Real estate accounting for 13% capex.

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capex (ZARm) 21 223 160 09 36 312 226 36 99 748 435 43 170 85 97 430 189 25 91 911 74 535 116 85 65 776

Projects 31 35 58 95 56 109 144 120 167 138 127 88 49

20

40

60

80

100

120

140

160

180

0

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

450 000

500 000

Pro

jects

Valu

e (

ZA

Rm

)

INWARD FDI INTO SAUDI ARABIA, 2003-JULY 2015

18

Source: FDI Intelligence, 2016

The United States was the largest source market for inward FDI into Saudi Arabia in terms of projects, with 232

investment projects, accounting for 19% between 2003 and July 2015. The UAE and the United Kingdom were

ranked second and third accounting for 212% and 90% respectively. Other top markets are France, India and

Japan.

TOP SOURCE MARKETS FOR FDI TO SAUDI ARABIA’S, 2003-JULY 2015

RANK SOURCE

COUNTRY PROJECTS

% PROJECTS

CAPEX (ZARm)

% CAPEX COMPANIES % COMPANIES

1 United States 232 19.06% 452 519.7 25.3% 182 20.16%

2 UAE 212 17.42% 158 981.7 8.9% 138 15.28%

3 UK 90 7.40% 36 259.6 2.0% 75 8.31%

4 France 69 5.67% 236 697.4 13.3% 44 4.87%

5 India 63 5.18% 73 460.1 4.1% 52 5.76%

6 Japan 47 3.86% 186 460.5 10.4% 37 4.10%

7 Germany 42 3.45% 45 662.5 2.6% 35 3.88%

8 Netherlands 37 3.04% 91 605.1 5.1% 20 2.21%

9 Spain 36 2.96% 3 790.5 0.2% 26 2.88%

10 Switzerland 35 2.88% 22 169.8 1.2% 24 2.66%

TOTAL 1 217 100.00% 1 785 791.7 100.00% 903 100.00%

Source: FDI Intelligence, 2014

Business Services11.3% Financial

Services9.2%

Textiles8.7%

Industrial Machinery,

Equipment & Tools7.9%

Hotels & Tourism

6.4%

Software & IT services

5.8%

Consumer Products

5.6%

Real Estate5.3%

Communications

4.4%

Chemicals4.3%

Other sectors31.1%

INWARD FDI INTO SAUDI ARABIA SECTORS BY PROJECTS, 2003-JULY 2015

Chemicals30.7%

Coal, Oil and Natural Gas

25.3%Real Estate

12.7%

Hotels & Tourism

8.0%

Metals7.9%

Automotive OEM2.2%

Plastics1.7%

Financial Services

1.3%

Industrial Machinery, Equipment & Tools

1.1%

Building & Construction

Materials1.0%

Other sectors8.1%

INWARD FDI INTO SAUDI ARABIA SECTORS BY CAPEX, 2003-JULY 2015

19

The top 20 global companies investing into Saudi Arabia by projects from 2003 to July 2015 are shown below.

COMPANIES INVESTING INTO SAUDI ARABIA, 2003-JULY 2015

RANK INVESTING COMPANY

SECTORS PROJECTS CAPEX (ZARm)

1 TNT Express Transportation 11 7 029

2 Carrefour Food & Tobacco 10 1 476

3 Redtag Group Textiles 8 337

4 AXA Cooperative Financial Services 7 1 870

5 LuLu Food & Tobacco 7 928

6 Millennium & Copthorne Hotels

Hotels & Tourism 7 18 692

7 Rotana Hotels Hotels & Tourism 6 13 683

8 Saudi Hollandi Bank

Banking 6 1 062

9 Alshaya International

Retail 5 260

10 Ascott Group Apartments 5 45 743

11 Cellucom Wireless Products 5 375

12 Corp Executive Hotels

Hotels 5 13 352

13 DHL Express Transportation 5 1 023

14 Dow Chemical Chemicals 5 248 621

15 Giordano Textiles 5 211

16 Hewlett-Packard (HP)

Business Machines & Equipment

5 907

17 3M Mining & Manufacturing 4 278

18 Al Danube Building Materials

Building & Construction Materials

4 2 050

19 Asteco Real Estate 4 1 463

20 ATS Transportation 4 717

Source: FDI Intelligence, 2016

20

4.2 Outward FDI from Saudi Arabia

Between January 2003 and July 2015 a total of 534 FDI projects were recorded from Saudi Arabia. These projects

represent a total capital investment of ZAR487.47bn which is an average investment of ZAR912.76m per project.

During the period, a total of 97,525 jobs were created.

Source: FDI Intelligence, 2016

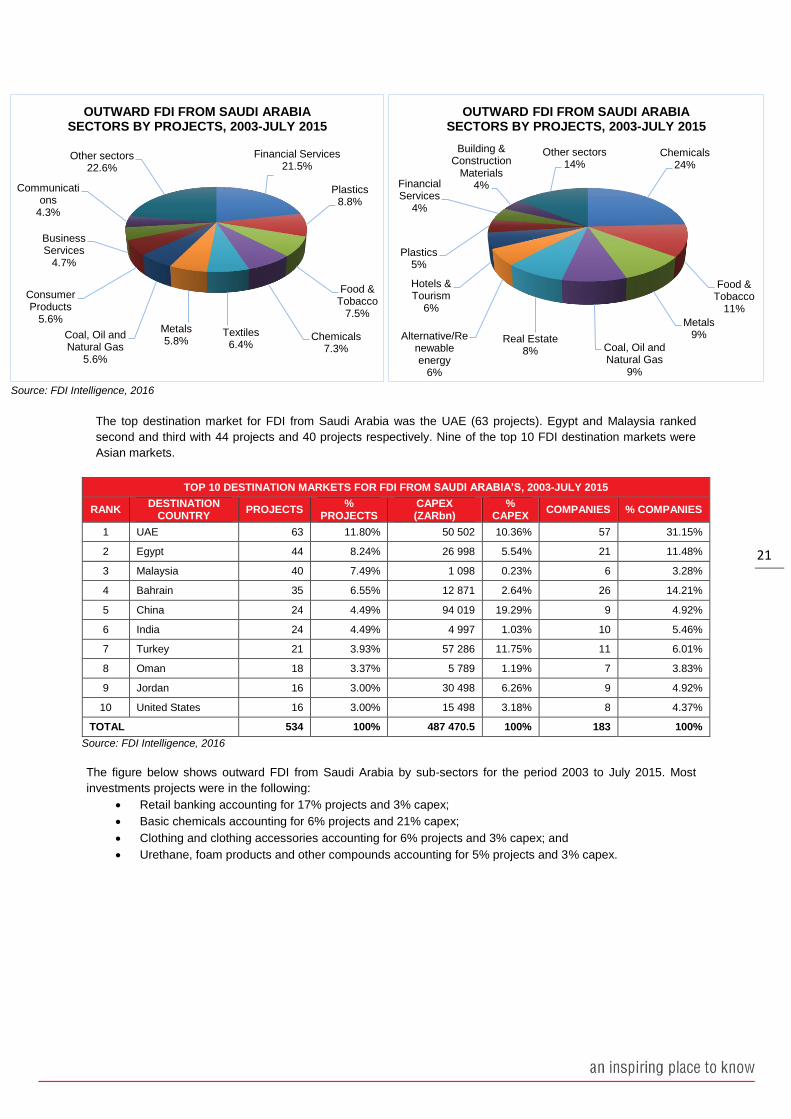

The figure below shows Saudi Arabia’s global outward FDI by sector for the period 2003 to July 2015. In terms of

projects the most investments were in the following:

Financial services sector received the largest share accounting for 21%,

Plastics 9% of projects,

Food and tobacco sector accounting for 8% projects.

In terms of capex, the most investments were in the following:

Chemicals sector received the largest share in terms of capex accounting for 24%,

Food and tobacco accounting for 11% of capex,

Coal, oil and natural gas sector accounting for 9% of capex.

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Capex (ZARm) 10 663 65 593 21 474 62 768 22 047 57 371 69 671 16 814 65 928 23 817 32 235 22 571 16 519

Projects 15 22 17 60 55 52 32 39 70 80 39 43 10

10

20

30

40

50

60

70

80

90

0

10 000

20 000

30 000

40 000

50 000

60 000

70 000

80 000

Pro

jects

Valu

e (

ZA

Rm

)

OUTWARD FDI FROM SAUDI ARABIA, 2003-JULY 2015

21

Source: FDI Intelligence, 2016

The top destination market for FDI from Saudi Arabia was the UAE (63 projects). Egypt and Malaysia ranked

second and third with 44 projects and 40 projects respectively. Nine of the top 10 FDI destination markets were

Asian markets.

TOP 10 DESTINATION MARKETS FOR FDI FROM SAUDI ARABIA’S, 2003-JULY 2015

RANK DESTINATION

COUNTRY PROJECTS

% PROJECTS

CAPEX (ZARbn)

% CAPEX

COMPANIES % COMPANIES

1 UAE 63 11.80% 50 502 10.36% 57 31.15%

2 Egypt 44 8.24% 26 998 5.54% 21 11.48%

3 Malaysia 40 7.49% 1 098 0.23% 6 3.28%

4 Bahrain 35 6.55% 12 871 2.64% 26 14.21%

5 China 24 4.49% 94 019 19.29% 9 4.92%

6 India 24 4.49% 4 997 1.03% 10 5.46%

7 Turkey 21 3.93% 57 286 11.75% 11 6.01%

8 Oman 18 3.37% 5 789 1.19% 7 3.83%

9 Jordan 16 3.00% 30 498 6.26% 9 4.92%

10 United States 16 3.00% 15 498 3.18% 8 4.37%

TOTAL 534 100% 487 470.5 100% 183 100%

Source: FDI Intelligence, 2016

The figure below shows outward FDI from Saudi Arabia by sub-sectors for the period 2003 to July 2015. Most

investments projects were in the following:

Retail banking accounting for 17% projects and 3% capex;

Basic chemicals accounting for 6% projects and 21% capex;

Clothing and clothing accessories accounting for 6% projects and 3% capex; and

Urethane, foam products and other compounds accounting for 5% projects and 3% capex.

Financial Services21.5%

Plastics8.8%

Food & Tobacco

7.5%

Chemicals7.3%

Textiles6.4%

Metals5.8%

Coal, Oil and Natural Gas

5.6%

Consumer Products

5.6%

Business Services

4.7%

Communications

4.3%

Other sectors22.6%

OUTWARD FDI FROM SAUDI ARABIA SECTORS BY PROJECTS, 2003-JULY 2015

Chemicals24%

Food & Tobacco

11%

Metals9%

Coal, Oil and Natural Gas

9%

Real Estate8%

Alternative/Renewable energy

6%

Hotels & Tourism

6%

Plastics5%

Financial Services

4%

Building & Construction

Materials4%

Other sectors14%

OUTWARD FDI FROM SAUDI ARABIA SECTORS BY PROJECTS, 2003-JULY 2015

22

Source: FDI Intelligence, 2016

The top 20 global companies investing from Saudi Arabia by projects from 2003 to 2013 are shown below.

COMPANIES INVESTING FROM SAUDI ARABIA, 2003-2013

RANK INVESTING COMPANY

SECTOR PROJECTS CAPEX (ZARm)

1 Saudi Basic Industries (SABIC)

Plastics 42 57 764

2 Fawaz Alhokair Group Textiles 38 525

3 Al Rajhi Bank Financial Services 33 9 299

4 SABIC Innovative Plastics

Plastics 19 6 238

5 Albaraka Banking Group (ABG)

Financial Services 13 2 016

6 Albaraka Turk Financial Services

13 8 895

7 Saudi Aramco Coal, Oil and Natural Gas

12 2 107

8 Shifa Al Jazeera Medical Group

Medical 11 7 045

9 Construction Products Holding Company (CPC)

Construction 11 60

10 E-Holidays Hotels & Tourism 9 1 729

11 Islamic Development Bank (IDB)

Banking 8 601.3

12 Albaraka Bank Egypt Financial Services

8 5 262.00

17.8%

6.4%

6.2%

5.1%

4.1%

3.2%

2.6%

2.2%

2.2%

2.2%

2.1%

1.9%

1.5%

3.1%

20.6%

3.4%

3.1%

1.3%

1.0%

0.5%

1.2%

1.0%

1.4%

0.3%

0.4%

4.9%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Retail banking

Basic chemicals

Clothing & clothing accessories

Urethane, foam products & other compounds

Other petroleum & coal products

Corporate & investment banking

Travel arrangement & reservation services

Architectural & structured metals

Cosmetics, perfume, personal care & householdproducts

Wireless telecommunication carriers

Sporting goods, hobby, books & music

Food & Beverage Stores (Food & Tobacco)

Accommodation

SAUDI ARABIA OUTWARD FDI BY SUBSECTORS (% SHARE), 2003-JULY 2015

% Capex % Projects

23

COMPANIES INVESTING FROM SAUDI ARABIA, 2003-2013

RANK INVESTING COMPANY

SECTOR PROJECTS CAPEX (ZARm)

13 Al-Tuwairqi Group (ATG)

Metals 8 2 183.80

14 Amouage (Oman Perfumery)

Consumer Products 8 3 715.00

15 Aramco Overseas Coal, Oil and Natural Gas

8 18 110.60

16 Savola Financial Services 7 2 016.40

17 Bintel Communications 6 4 576.00

18 Al Hokair Food & Tobacco 5 393.6

19 Albaraka Bank Algeria Financial Services 5 597.2

20 Amiantit Materials 5 2 323.20

Total 477 261 549

Source: FDI Intelligence, 2016

24

4.3 South African FDI with Saudi Arabia

Between January 2003 and July 2015 a total of 2 FDI projects were recorded from South Africa to Saudi Arabia.

These projects represent a total capital investment of ZAR399.55m which is an average investment of ZAR200.36m

per project. During the period, a total of 39 jobs were created.

SOUTH AFRICA FDI TO SAUDI ARABIA, 2003-JULY 2015

DATE INVESTING

COMPANY

SOURCE

STATE INDUSTRY SECTOR

SUB-SECTOR INDUSTRY

ACTIVITY

CAPEX

(ZARm) JOBS

Nov 2007 Dimension Data

Holdings (DiData) Gauteng

Software & IT services

Computer facilities

management services

Sales, Marketing &

Support 68 21

Jul 2006 Gensec Property

Services Gauteng Real Estate Real estate services

Sales, Marketing &

Support 332 18

TOTAL 400 39

Source: FDI Intelligence, 2016

Between January 2003 and July 2015 a total of 5 FDI projects were recorded from Saudi Arabia to South Africa.

These projects represent a total capital investment of ZAR20.70bn which is an average investment of

ZAR4,140.81m per project. During the period, a total of 385 jobs were created.

In 2010 - Saudi Basic Industries (SABIC) a plastics manufacturer from Saudi Arabia invested in the city of Cape

Town in the plastics sector in a sales, marketing and support project valued at ZAR23bn.The facility will allow the

company to strengthen its existing operations locally and improve its sales in neighbouring countries, bringing

SABIC closer to its customers. It will also support the company's existing distribution centre in the country.

SAUDI ARABIA FDI TO SOUTH AFRICA, 2003-JULY 2015

DATE INVESTING

COMPANY

DESTINATION

STATE INDUSTRY SECTOR SUB-SECTOR

INDUSTRY

ACTIVITY

CAPEX

(ZARm) JOBS

Jan 2015 ACWA Power

International Northern Cape

Alternative/Renewable energy

Solar electric power Electricity 14 060 216

Jun 2014

Altaaqa Global

CAT Rental

Power

Gauteng Industrial Machinery, Equipment & Tools

Power transmission

equipment

Sales, Marketing &

Support 34 17

Sep 2013 ACWA Power International

Northern Cape Alternative/Renewable energy

Solar electric power Electricity 6 151 60

Sep 2010 Saudi Basic Industries (SABIC)

Western Cape Plastics Urethane, foam products & other compounds

Sales, Marketing & Support

23 12

Apr 2008 I2 (IICC) Gauteng

Communications Wireless telecommunication carriers

Headquarters

432 80

TOTAL 20 702 385

Source: FDI Intelligence, 2016

25

5. Tourism

5.1 Saudi Arabia Trends and Travel Patterns

Saudi Arabia has a relatively large population of around 27.7 million and there is a strong tradition of domestic

travel in the country. Saudi travellers are lauded as amongst the highest spending globally, with government reports

stating that Saudi travellers spend over USD14bn overseas annually. The government is keen to keep more of this

spending at home and has some USD11.6bn of tourist projects planned or underway in order to encourage more

local travel.

Outbound tourism is expected to increase significantly over the next five years through to 2020 with outbound travel

increasing from 11.7mn in 2016 to 14.8mn in 2020.

5.2 Saudi Arabian Tourist Arrivals into South Africa

The graph below depicts total tourist arrivals from Saudi Arabia into South Africa from 2013 to 2014. Saudi Arabia

tourist arrivals into South Africa increased by 5% from 6251 tourists in 2013 to 6 545 tourists in 2014. No data is

available for Saudi Arabian tourist arrivals into the Western Cape due to an insufficient sample size.

Source: SATourism, 2016

*Note: Statistics SA made changes to the release of its Tourism & Migration reports in 2014 and now no longer report on transit

arrivals. As a result of this change, the weighting methodology has been revised and the results are now not comparable to

data prior to 2013. 2014 represents the beginning of a new series of data.

For more information on this publication and other Wesgro publications please contact [email protected]. For more

publications like this visit the Wesgro publications portal on our website at http://wesgro.co.za/publications

2013 2014

Tourist Arrivals 6 251 6 545

6 100

6 150

6 200

6 250

6 300

6 350

6 400

6 450

6 500

6 550

6 600

Tourist A

rriv

als

SAUDI ARABIA TOURIST ARRIVALS TO SOUTH AFRICA, 2013-2014