Embed Size (px)

Citation preview

1

Centre for Science & Security Studies

Sanctions and the Insurance Industry

Challenges and Opportunities

Matthew Moran and Daniel Salisbury

September 2013

CSSS Occasional Papers 2/2013

About the Centre for Science and Security Studies

The Centre for Science and Security Studies (CSSS) is a multi-disciplinary research group in

the Department of War Studies at King’s College London. CSSS was created by a grant from

the John D. and Catherine C. MacArthur Foundation in 2003 and brings together scientific

experts with specialists in politics, international relations and history. Members of the

Centre conduct scholarly and policy-relevant research on weapons proliferation, non-

proliferation, verification and disarmament, space security and mass effect terrorism

including the CBRN (chemical, biological, radiological and nuclear) dimension.

About the CSSS Occasional Papers Series

The CSSS Occasional Paper Series aims to provide an insight into some of the research

being conducted at the Centre for Science and Security Studies

Acknowledgements

This paper was prepared as part of a project funded by the Economic and Social Research

Council (ESRC), AXA, Freshfields Bruckhaus Deringer LLP, Marsh & McLennan Companies,

Lloyd’s, and Swiss Re .

Copyright 2013 King’s College London

The information in this report may be used for educational purposes. All material

reproduced should clearly cite the source: Matthew Moran and Daniel Salisbury,

“Sanctions and the Insurance Industry: Challenges and Opportunities”, CSSS Occasional

Paper Series, (London: King’s College London, 2013).

Cover Image

Image ‘Container Port, Cape Town’, by Flickr user Delgoff licensed under a Creative

Commons Licence.

ISBN 978-1-908951-05-2

© 2013 King’s College London

Sanctions and the Insurance Industry:

Challenges and Opportunities

Table of Contents

About the Authors 4

Sponsors 5

Acknowledgements 6

Abbreviations 7

Introduction 9

Part One: Sanctions on Iran: Policy Goals 11

and Latest Developments

Part Two: The Challenges of Sanctions Legislation 23

Part Three: Compliance and Enforcement 31

Part Four: Promoting Coherence between Policy Makers 39

and Practitioners

Conclusion 47

Annex 1: Project Alpha 49

4

About the Authors

Matthew Moran is Deputy Director for Research Development at the Centre for Science and

Security Studies at King’s College London. He studied for a BA (Hons) and MA at the

National University of Ireland, Galway and holds a PhD from University College London. His

research interests include nuclear non-proliferation and sanctions. His latest book, Exploring

Regional Responses to a Nuclear Iran: Nuclear Dominoes?, will be published by Palgrave

Macmillan in October 2013.

Daniel Salisbury is Researcher at the Centre for Science and Security Studies at King’s

College London. His work focuses on proliferation and illicit trade. He holds a BA in War

Studies, an MA in Science and Security, and is currently completing a PhD at King’s College

London.

5

Sponsors

6

Acknowledgements

The authors would like to thank Andrew Bardot, Jonathan Brewer, David Brummond,

Christopher Pickup, Ian Stewart and Andy Wragg for their comments on earlier drafts of this

report. It should be noted that the report does not necessarily reflect the views of these

individuals or their organisations. Any faults in the text, and the arguments presented, are

the sole responsibility of the authors.

Abbreviations

Bpd Barrels per day CISADA Comprehensive Iran Sanctions, Accountability, and Divestment Act EU European Union IAEA International Atomic Energy Agency IFCA Iran Freedom and Counterproliferation Act IRGC Islamic Revolutionary Guards Corps IRISL Islamic Republic of Iran Shipping Lines ISA Iran Sanctions Act TRA Iran Threat Reduction and Syrian Human Rights Act NDAA National Defence Authorisation Act NPT Treaty on the Non-Proliferation of Nuclear Weapons NITC National Iranian Tanker Company OFAC Office of Foreign Assets Control P&I Protection and Indemnity Insurance SDN Specially Designated Nationals UANI United Against a Nuclear Iran UK United Kingdom UN United Nations UNSC United Nations Security Council US United States USD United States Dollar

7

8

Introduction Since December 2006 four sets of UN Security Council sanctions have been imposed on Iran over its nuclear programme, with Tehran still yet to satisfy the international community that its intentions are solely peaceful. UN sanctions have been augmented by unilateral sanctions (particularly on the part of the United States) and sanctions imposed by the European Union. The various regimes target multiple economic sectors. However, while sanctions constitute a valuable tool for the international community to apply pressure on Iran to negotiate over its nuclear programme, the wide range and scope of the various regimes, and in many cases a lack of detailed guidance on implementation, mean that there can be uncertainty within industry with regard to their implementation.

Much attention has been focused on the banking sector in recent years as policy-makers have adapted tools initially designed to target the assets and money-laundering capabilities of terrorist organisations and organised crime to meet the needs of non-proliferation sanctions. This focus on the banking sector has forced banks and financial institutions to enhance greatly their compliance capabilities and procedures. However, other financial service sectors, such as the insurance industry, have not been subject to similar attention and, consequently, have faced difficulties in developing similarly sophisticated compliance capabilities. This position has changed somewhat in recent years, primarily due to the increasing scope of Iran sanctions, but challenges remain. Moreover, the rapidly-evolving sanctions environment has added an additional layer of complexity to compliance efforts within those industries already attempting to make up ground.

The obligation to comply with sanctions extends to a range of insurance products and activities, especially where these relate to commerce. Insurance companies have taken significant steps to adapt to the restrictions imposed by sanctions, such as putting standardised sanctions clauses in insurance contracts, for example. However, sanctions implementation can be costly and complex and it can be difficult to determine whether compliance policies and procedures meet the challenges.

In the context of reinsurance, for example, ensuring compliance on broad-based, multi-activity coverage has become an important challenge for reinsurers. The shipping industry has been dramatically affected due to the implications of the sanctions both property underwriters (hull and machinery and cargo) and protection and indemnity (marine liability) insurance coverage. Unusual measures have in some cases been adopted. The government of Japan, for example, has extended sovereign insurance coverage to Japanese tankers whose insurance is affected by the EU and US measures on Iran to allow them to continue importing Iranian oil permitted under US waivers.

Of course, the challenges associated with sanctions and their implementation are not limited to industry practitioners. Sanctions are as much a political tool as an economic one and policy-makers are often required to develop and legislate on sanctions without having adequate time to fully consider the range of challenges and difficulties that these measures will pose to commercial stakeholders. This means that policy makers have faced difficulties in making sure that new sanctions measures may be developed and implemented with minimum risk to commercial activities and to the interests of third parties who may suffer as a consequence of such measures.

9

In this context, King’s College London hosted a two-day expert workshop entitled ‘Sanctions and the Insurance Industry’ on 4-5 June 2013. Focusing primarily on Iran sanctions and their impact, this workshop brought together practitioners from major global insurance and reinsurance providers and brokers (compliance officers, etc.), representatives from industries covered by relevant insurance policies, representatives from the policy community (UK Treasury, US Treasury, the UN Panel of Experts on Iran, and the European External Action Service) and academics, for a frank discussion under the Chatham House rule.

The aims of the workshop were twofold:

• To contribute to the effective implementation of sanctions in the insurance industry by addressing directly the risks and challenges faced by industry practitioners, particularly those working in the area of compliance, and facilitating a dialogue between practitioners and policy-makers on how best to overcome, or at least mitigate these challenges.

• To offer policy-makers the opportunity to engage with industry on the subject of sanctions and better understand the particular sanctions-related challenges that the insurance industry faces. A number of initiatives aimed at exploring the impact of sanctions across different industries have taken place at the regional level; however the lack of sector-specific initiatives means that policy-makers have few opportunities to engage with practitioners in a focused and targeted manner.

In broader terms, the workshop aimed to make a contribution to strengthening the resilience of the insurance industry, both in the United Kingdom and beyond, in the face of complex and rapidly-evolving sanctions regimes. In particular, the workshop was intended to enhance the ability of policy-makers to translate the political need for sanctions into robust and effective legislative measures that do not unnecessarily hinder commercial activities.

The workshop was generously funded by a number of partners:

• The Economic and Social Research Council (ESRC) • AXA • Freshfields Bruckhaus Deringer LLP • Lloyd’s • Marsh & McLennan Companies • Swiss Re

The following report brings together the key points of discussion and the conclusions reached during the workshop. The report also includes a number of recommendations relevant to the effective implementation of sanctions in the insurance industry. Given that the workshop was held under the Chatham House Rule, all points and information arising from participants contributions have been anonymised. The report largely mirrors the workshop agenda, beginning with a broader discussion of the policy goals and objectives of sanctions, particularly with respect to Iran, before moving to look at the practical challenges faced by the insurance industry. The final section focuses on ways and means of promoting coherence between policy-makers and practitioners with a view to facilitating the successful implementation of sanctions with minimum risk to industry.

10

PART ONE:

SANCTIONS ON IRAN: POLICY GOALS AND LATEST DEVELOPMENTS

11

Sanctions on Iran Sanctions on Iran are not new; the country has lived with US sanctions in some shape or form since the 1979 takeover of the US embassy in Tehran when US diplomats were detained for 444 days. In recent years, however, and particularly since the first round of UN sanctions was imposed in 2006, sanctions have gained unprecedented momentum and visibility in the context of international efforts to halt or even reverse Iran’s nuclear trajectory.

‘Sanctions’ is a term used to describe a range of punitive legislative provisions that are put in place with a view to altering political and/or military behaviour. A distinction can be made between ‘targeted’ or ‘smart’ sanctions and ‘comprehensive’ sanctions. Targeted sanctions are “directed at leaders, their core allies in the regime’s hierarchy, and/or specific enterprises and agencies engaged in the proscribed behaviour”.1 The aim here is to “minimise unintended, undesirable, or indiscriminate consequences for the broader public”.2 Sanctions have provoked controversy in the past in this regard, being cited as responsible for civilian suffering in Iraq in the early 1990s for example.

Comprehensive economic sanctions, however, target “both the macro-economy and macro-politics of states, so that punishments [...] are extended over wide segments of the population”.3 The distinction here is important since sanctions on Iran have evolved in recent years from a targeted approach to what is now a wide-ranging, comprehensive sanctions regime. More than this, the current mosaic of sanctions regimes imposed upon Iran is breaking new ground. On one hand, “the U.S. has used its leverage over the international financial system to create the most comprehensive unilateral sanctions regime in history”.4 On the other, the 2012 EU oil embargo signalled the emergence of an unprecedented international coalition around sanctions on Iran and marked a significant escalation in the punitive measures being applied to the country.

Sanctions have, apparently, thus far failed to change Iran’s nuclear calculus; however they have placed considerable strain on the Iranian economy. In January 2012, for example, the announcement of additional EU sanctions caused the value of the Iranian Rial to plummet as Iranians rushed to convert their currency into US dollars. And recent research reveals that the value of the Rial has continued to fall: “the unofficial value of the Rial has gone from Rial 20,000 to the US dollar in January 2012 to Rial 33,000 in January 2013”.5

In this context, and before beginning to explore the practical challenges associated with sanctions in the specific context of the insurance industry, it is thus useful to set out the policy goals and objectives of sanctions and how they these translate into practice, as well as highlighting potential future developments. The following section approaches these issues from the perspective of the United Nations Security Council (UNSC), the United States, the United Kingdom and the European Union (EU).

1 Etel Solingen (ed.), Sanctions, Statecraft, and Nuclear Proliferation (Cambridge & New York: Cambridge University Press, 2012), p.19. 2 Ibid. 3 Ibid. 4 Bijan Khajehpour, Reza Marashi and Trita Parsi, “‘Never give in and never give up’: The Impact of Sanctions on Tehran’s Nuclear Calculations”, (Washington, DC: National Iranian American Council, 2013), p.3. 5 Ibid., p.21.

12

Policy Goals and Objectives While there are some differences between the objectives of various state actors and international organisations, all share the broader goal of impeding Iran’s nuclear progress.6 Sanctions regimes thus target, to varying degrees, individuals and organisations that support the country’s work in the area of nuclear and ballistic missile development. Unilateral sanctions have also targeted key sectors of the Iranian economy, such as the automobile industry, in a bid to affect Iranian decision making.

Iran’s nuclear programme was propelled to the top of the international security agenda in 2002, following revelations of a number of undeclared nuclear facilities. In 2005, the IAEA Board of Governors found Iran to be in non-compliance with its NPT safeguards obligations and, in 2006, referred Iran to the United Nations Security Council (UNSC). Since this point, sanctions have been imposed upon Iran have been imposed in an increasing number of areas by a range of actors.

A first round of sanctions was imposed on Iran by the UNSC in December 2006 under Resolution 1737. This was followed by the imposition of additional sanctions in 2007 (Resolution 1747), 2008 (Resolution 1803), and 2010 (Resolution 1929). These measures constitute a direct response to Iran’s non-compliance with its NPT safeguards obligations. The primary policy objective is to impede the progress of Iran’s nuclear and ballistic missile programmes and force Tehran to comply with requirements of the IAEA, and this is reflected in their comparatively limited scope. UN sanctions are focused on technologies and entities directly associated with Iran’s nuclear and missile programmes. UNSC resolutions are binding on all UN member states under international law.

US, UK and EU sanctions go beyond the scope and reach of UN sanctions. Indeed, it has been pointed out that “UN sanctions were seen - at least by the EU, the United States, and others - as an international imprimatur for additional sanctions to be enacted by regional bodies or individual countries after UN action”.7 The sanctions which have had the largest impact on the insurance industry are those put in place by US and EU legislation.

UK and US policy towards Iran’s nuclear programme has been broadly based on a dual-track approach that comprises diplomatic engagement and pressure. In a recent statement to accompany the announcement of additional US sanctions related to Iran, for example, the Office of the Press Secretary reiterated that sanctions “are part of President Obama’s commitment to prevent Iran from acquiring a nuclear weapon, by raising the cost of Iran’s defiance of the international community. Even as we intensify our pressure on the Iranian

6 It should be noted that sanctions have also been imposed on Iran by the EU, among others, on human rights grounds. In the EU these take the form of asset freezes against some individuals and trade restrictions relating to telecoms/internet intercept and monitoring equipment, including restrictions on insurance and reinsurance. See “Financial sanctions, Iran (human rights)”, HM Treasury <https://www.gov.uk/government/organisations/hm-treasury/series/financial-sanctions-regime-specific-consolidated-lists-and-releases>. 7 Meghan L. O’Sullivan, “Iran and the Great Sanctions Debate”, The Washington Quarterly (2010), Vol.33, No.4, p.12.

13

government, we hold the door open to a diplomatic solution that allows Iran to rejoin the community of nations if they meet their obligations”.8

However, with Iran moving closer to a nuclear weapons capability and the threat of Israeli military action ever-present, recent years have seen a steady increase of punitive pressure on Iran as the international community seeks to secure a peaceful solution to the Iranian nuclear challenge.

In the case of the European Union, prominent members such as the UK, France and Germany have, for some time, lobbied for more punitive sanctions on Iran. These efforts played a significant role in the 2012 decision by the European Union to impose a phased oil embargo on Iran. The push for stronger sanctions is unsurprising; European powers have played an important role in negotiations with Iran since 2003, when the Foreign Ministers of the E3 (France, Germany and the United Kingdom) attempted to negotiate a halt to Iran’s work on enrichment as well as seeking transparency over its nuclear activities past and present. The broader EU engagement that followed was motivated both by a desire to avoid a potential military conflict between Iran and Israel and by a wish to play a more prominent role in nonproliferation issues.

In official terms, the objective of the EU continues to be “a comprehensive, negotiated, long-term settlement, which would build international confidence in the exclusively peaceful nature of the Iranian nuclear programme, while respecting Iran’s legitimate right to the peaceful use of nuclear energy in conformity with the Non Proliferation Treaty and fully taking into account UN Security Council and IAEA Board of Governors resolutions”.9

In terms of policy objectives, then, US, UK and EU goals overlap significantly. However, in terms of legislation, the United States has imposed the most stringent and wide-ranging sanctions upon the Islamic Republic. Consequently, the objectives and goals of other sanctions efforts are, to a large extent, overshadowed by the weight of the US sanctions regime.

US sanctions have, for example, long incorporated an ‘extraterritorial’ element – the Iran and Libya Sanctions Act of 1996 (later the Iran Sanctions Act) placed restrictions on “the activities of foreign nationals who have neither personal nor territorial connections with the United States”.10 However, the extraterritorial scope of economic sanctions against Iran was significantly expanded with the Comprehensive Iran Sanctions, Accountability, and Divestment Act of 2010 (CISADA). The objective here has been to force a choice on private sector actors around the world: individuals and organisations can either do business with the United States or Iran, but not with both.

8 “Statement by the Press Secretary on the Announcement of Additional Sanctions Related to Iran”, The Office of the Press Secretary, The White House, 3 June 2013 <http://www.whitehouse.gov/the-press-office/2013/06/03/statement-press-secretary-announcement-additional-sanctions-related-iran>. 9 European Union, “Factsheet: The European Union and Iran”, 6 June 2013 <http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/EN/foraff/129724.pdf>. 10 Matthias Herdegen, Principles of International Economic Law (Oxford: Oxford University Press, 2013), p.79.

14

There are also elements of the US political establishment that regard sanctions as having the broader and more extreme objective of regime change.11 However, it is important to note that such a position contrasts starkly with the official policy of the Obama administration, the UK government and other countries around the world.

Current State of Play and Recent Developments The sanctions environment is a fluid and fast-changing one. In recent years, a host of new, more restrictive measures have been introduced in the Iranian context, presenting a considerable challenge to private sector firms as they attempt to stay abreast of compliance requirements. This section will offer an insight into the state of play with regard to sanctions on Iran as of July 2013, setting out key legislative developments and what these entail, particularly with regard to the insurance industry.

Recent UN Developments Only two UN resolutions make explicit reference to insurance (see 1929 and 1803 in the table below), however, all place prohibitions on certain activities which impact upon the insurance industry. There have been no developments in UN sanctions legislation since the passing of UNSCR1929 in June 2010. The UN Panel of Experts established pursuant to resolution 1929 is monitoring implementation and recently had its mandate extended until summer 2014.

Table 1: UNSC Resolutions imposing sanctions on Iran

Date Resolution Summary of selected provisions

9 June 2010

UNSC Resolution

1929

• Prevents Iran from acquiring commercial interests in Uranium mining

• Effectively imposes an arms embargo • Prohibits ballistic missile activities • Directs states to take actions to prohibit designated

individuals from entering or transiting through • Calls upon states to inspect cargo in certain circumstances • Prohibits the provision of fuel or supplies, or other servicing

of vessels, to Iranian-owned or -contracted vessels • Expands certain provisions of previous resolutions to apply

to IRISL and the IRGC • Puts certain prohibitions on Iranian banking operations • Prohibits the provision of financial services, including

insurance or re-insurance, if those services could contribute to Iran’s proliferation-sensitive nuclear activities, or the development of nuclear weapon delivery systems

3 March 2008

UNSC Resolution

1803

• Asks states to exercise vigilance and restraint regarding the entry into or transit through their territories of individuals who are engaged in Iran’s nuclear and missile activities

• Revises export restrictions of sensitive technologies • Calls on states to exercise vigilance regarding the activities

11 See for example Kate Gould, “Iran Leak Reveals Senate Push for Regime Change”, The Huffington Post, 10 May 2013 <http://www.huffingtonpost.com/kate-gould/iran-sanctions-bill_b_3244329.html>.

15

of Iranian banks in particular with Bank Melli and Bank Saderat

• Calls upon states to inspect Iranian vessels and planes when they suspect breaches of resolutions

• Calls upon all States to exercise vigilance in entering into commitments for public provided financial support for trade with Iran, including the granting of export credits, guarantees or insurance, in order to avoid such financial support contributing to the proliferation sensitive nuclear activities

24 March 2007

UNSC Resolution

1747

• Iran shall not supply aircraft any arms or related materiel, and that all States shall prohibit the procurement of such items from Iran by their nationals

• States should exercise vigilance and restraint in supplying arms or related services to Iran in order to prevent a destabilising accumulation of arms

• Prohibits states and international financial institutions not to entering into new commitments for grants, financial assistance, and concessional loans, to the government of the Islamic Republic of Iran, except for humanitarian and developmental purposes

23 December

2006

UNSC Resolution

1737

• Prohibits the transfer of certain listed sensitive technologies • Directs states to take the measures to prevent the provision

to Iran of any technical assistance or training, financial assistance, investment, brokering or other services

• Ask states to exercise vigilance regarding the entry into or transit through their territories of individuals who are related to nuclear and missile activities

• Imposes an asset freeze on listed individuals

Recent EU Developments Since 2007, the European Union has introduced a range of sanctions on Iran. These sanctions constitute a response to Iran's proliferation-sensitive nuclear activities, and both work to implement UN decisions and include additional measures adopted independently by the European Union.

EU sanctions were last substantially strengthened on 15 October 2012 under Council Decision 2012/635/CFSP. The Council of the European Union also agreed to adopt a number of additional designations on 21 December (Council Decision 2012/829/CFSP).12 Additional designations were also agreed on 6 June 2013 (Council Decision 2013/270/CFSP).13

These Decisions took effect through a number of Council Regulations that amended or implemented the landmark Council Regulation (EU) No 267/2012 under which the EU oil embargo was imposed upon Iran.

12 “The European Union and Iran - Factsheet”, Council of the European Union, 6 June 2013 <http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/EN/foraff/129724.pdf>. 13 “Decisions”, Official Journal of the European Union, 8 June 2013 <http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2013:156:0010:0014:EN:PDF>.

16

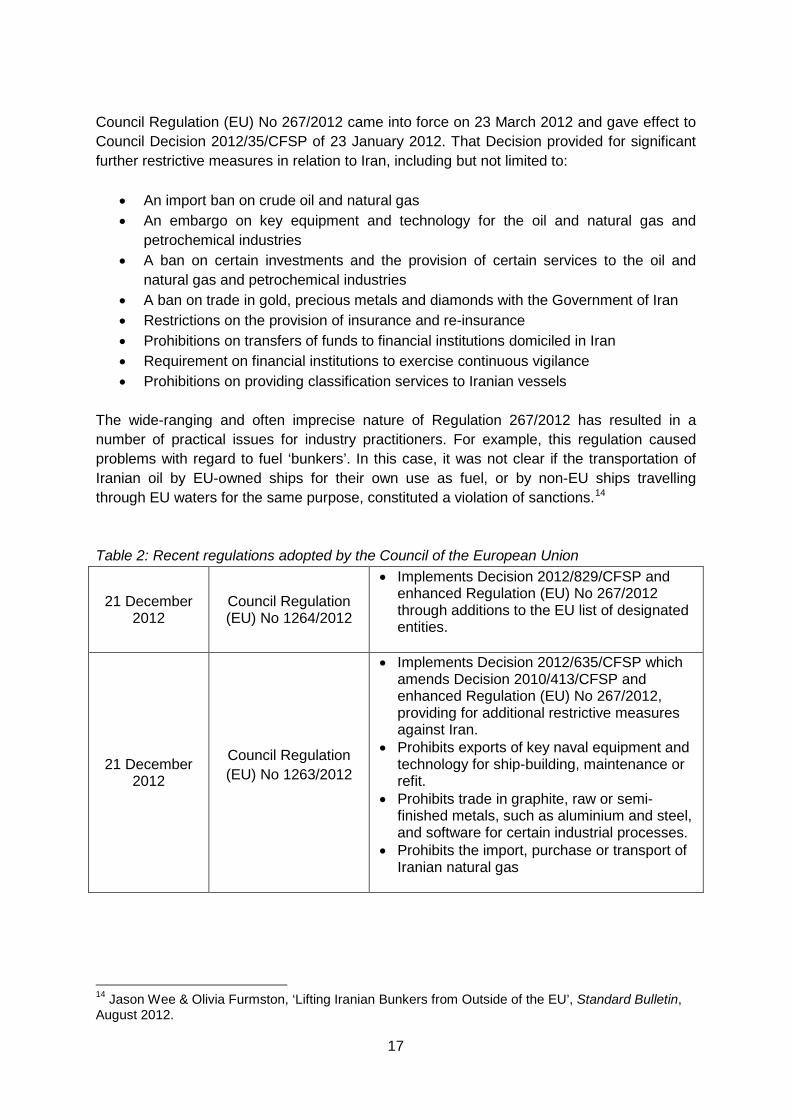

Council Regulation (EU) No 267/2012 came into force on 23 March 2012 and gave effect to Council Decision 2012/35/CFSP of 23 January 2012. That Decision provided for significant further restrictive measures in relation to Iran, including but not limited to:

• An import ban on crude oil and natural gas • An embargo on key equipment and technology for the oil and natural gas and

petrochemical industries • A ban on certain investments and the provision of certain services to the oil and

natural gas and petrochemical industries • A ban on trade in gold, precious metals and diamonds with the Government of Iran • Restrictions on the provision of insurance and re-insurance • Prohibitions on transfers of funds to financial institutions domiciled in Iran • Requirement on financial institutions to exercise continuous vigilance • Prohibitions on providing classification services to Iranian vessels

The wide-ranging and often imprecise nature of Regulation 267/2012 has resulted in a number of practical issues for industry practitioners. For example, this regulation caused problems with regard to fuel ‘bunkers’. In this case, it was not clear if the transportation of Iranian oil by EU-owned ships for their own use as fuel, or by non-EU ships travelling through EU waters for the same purpose, constituted a violation of sanctions.14 Table 2: Recent regulations adopted by the Council of the European Union

21 December 2012

Council Regulation (EU) No 1264/2012

• Implements Decision 2012/829/CFSP and enhanced Regulation (EU) No 267/2012 through additions to the EU list of designated entities.

21 December 2012

Council Regulation (EU) No 1263/2012

• Implements Decision 2012/635/CFSP which amends Decision 2010/413/CFSP and enhanced Regulation (EU) No 267/2012, providing for additional restrictive measures against Iran.

• Prohibits exports of key naval equipment and technology for ship-building, maintenance or refit.

• Prohibits trade in graphite, raw or semi-finished metals, such as aluminium and steel, and software for certain industrial processes.

• Prohibits the import, purchase or transport of Iranian natural gas

14 Jason Wee & Olivia Furmston, ‘Lifting Iranian Bunkers from Outside of the EU’, Standard Bulletin, August 2012.

17

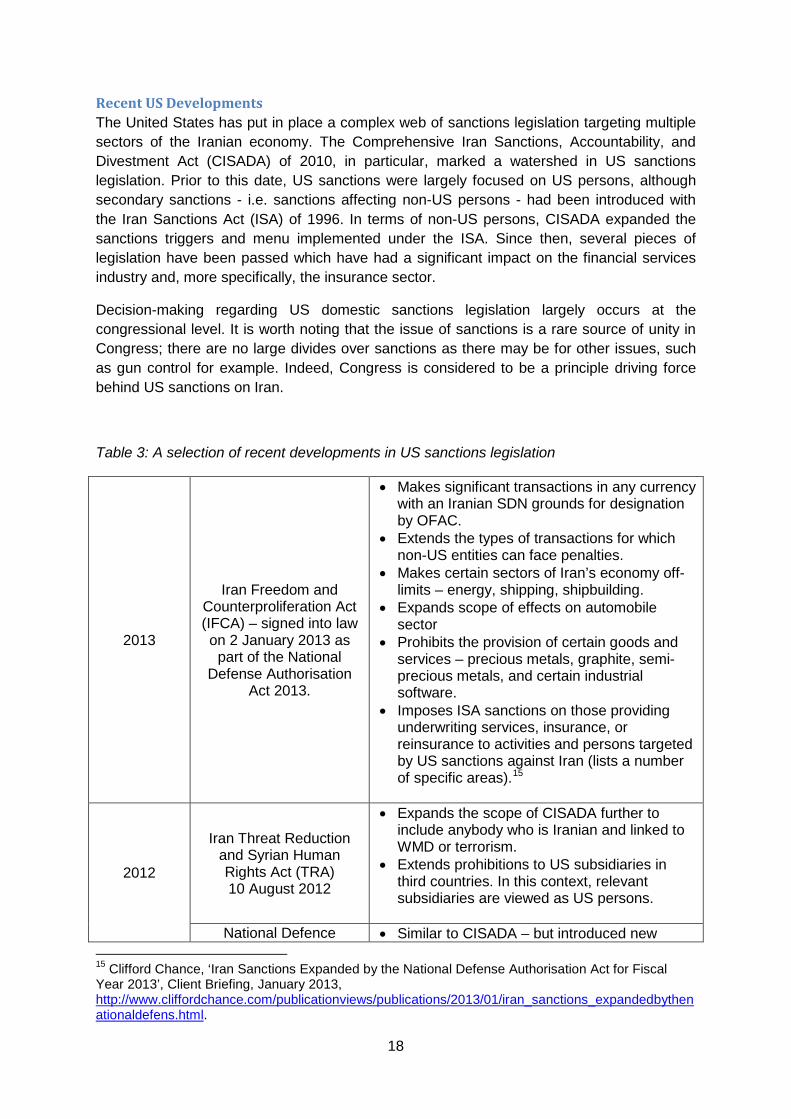

Recent US Developments The United States has put in place a complex web of sanctions legislation targeting multiple sectors of the Iranian economy. The Comprehensive Iran Sanctions, Accountability, and Divestment Act (CISADA) of 2010, in particular, marked a watershed in US sanctions legislation. Prior to this date, US sanctions were largely focused on US persons, although secondary sanctions - i.e. sanctions affecting non-US persons - had been introduced with the Iran Sanctions Act (ISA) of 1996. In terms of non-US persons, CISADA expanded the sanctions triggers and menu implemented under the ISA. Since then, several pieces of legislation have been passed which have had a significant impact on the financial services industry and, more specifically, the insurance sector.

Decision-making regarding US domestic sanctions legislation largely occurs at the congressional level. It is worth noting that the issue of sanctions is a rare source of unity in Congress; there are no large divides over sanctions as there may be for other issues, such as gun control for example. Indeed, Congress is considered to be a principle driving force behind US sanctions on Iran.

Table 3: A selection of recent developments in US sanctions legislation

2013

Iran Freedom and Counterproliferation Act (IFCA) – signed into law on 2 January 2013 as

part of the National Defense Authorisation

Act 2013.

• Makes significant transactions in any currency with an Iranian SDN grounds for designation by OFAC.

• Extends the types of transactions for which non-US entities can face penalties.

• Makes certain sectors of Iran’s economy off-limits – energy, shipping, shipbuilding.

• Expands scope of effects on automobile sector

• Prohibits the provision of certain goods and services – precious metals, graphite, semi-precious metals, and certain industrial software.

• Imposes ISA sanctions on those providing underwriting services, insurance, or reinsurance to activities and persons targeted by US sanctions against Iran (lists a number of specific areas).15

2012

Iran Threat Reduction and Syrian Human Rights Act (TRA) 10 August 2012

• Expands the scope of CISADA further to include anybody who is Iranian and linked to WMD or terrorism.

• Extends prohibitions to US subsidiaries in third countries. In this context, relevant subsidiaries are viewed as US persons.

National Defence • Similar to CISADA – but introduced new

15 Clifford Chance, ‘Iran Sanctions Expanded by the National Defense Authorisation Act for Fiscal Year 2013’, Client Briefing, January 2013, http://www.cliffordchance.com/publicationviews/publications/2013/01/iran_sanctions_expandedbythenationaldefens.html.

18

Authorisation Act (NDAA)

31 December 2011

restrictive measures regarding business with the Central Bank of Iran based on money laundering concerns.

• Set up provisions for states to gradually reduce their dependency on crude oil, sanctions waivers and triggers.

2010

Comprehensive Iran Sanctions,

Accountability, and Divestment Act

(CISADA) 1 July 2010

• Broadened the triggers and the consequences of the Iran Sanctions Act.

• Expanded the definition of US entities. • Expanded the ISA trigger and menu relating

to non-US entities.

Legislation passed by Congress is often complemented by Executive Orders and guidance which seeks to clarify some of the details of the sanctions in question. This is often in response to issues which have been identified after an Act has been passed or has entered into force.

Most recently, in June 2013 for example, President Obama signed Executive Order 13645 which significantly expands the jurisdictional reach of US sanctions against Iran.16 The Executive Order has two principal objectives:

• It implements certain sections of the Iran Freedom and Counter-Proliferation Act of 2012 (IFCA)

• It authorises additional sanctions against Iran, primarily targeting certain transactions and activities related to the Iranian rial, Iran’s automotive sector, and persons who materially assist Iranian persons on the list of Specially Designated Nationals and Blocked Persons

All in all, the multiple formats through which restrictive measures find expression combine to create a complex, multi-layered body of legislation that presents significant challenges to industry practitioners responsible for compliance.

Recent UK Developments Much of UK sanctions legislation and related provisions revolves around the obligatory implementation of EU and UN legislation. The UK government website provides a summary of sanctions measures that currently apply in the UK.17

16 Stephen M. McNabb, Marsha Z. Gerber, Stefan Reisinger, Kimberly Hope Caine, “Expansive executive order tightens Iran sanctions as labyrinth of front companies surfaces”, Norton Rose Fulbright, 18 June 2013 <http://www.nortonrosefulbright.com/knowledge/publications/99884/expansive-executive-order-tightens-iran-sanctions-as-labyrinth-of-front-companies-surfaces>. 17 See ‘Financial Sanctions, Iran (nuclear proliferation)’, UK gov.uk Website, <https://www.gov.uk/government/publications/financial-sanctions-iran-nuclear-proliferation>; and, more generally, “Financial sanctions: Regime-specific lists and releases”, HM Treasury <https://www.gov.uk/government/organisations/hm-treasury/series/financial-sanctions-regime-specific-consolidated-lists-and-releases>.

19

At the same time, however, the UK government has implemented additional, independent measures. For example, the Financial Restrictions (Iran) Order 2012 came into force on 21 November 2012. This order added the Central Bank of Iran to the Iran (proliferation) specific list of the ‘Consolidated List of Financial Sanctions Targets in the UK’.18

Future Developments in Sanctions Legislation At the UN level there are unlikely to be further sanctions on Iran passed by the Security Council in the immediate future. This relates to current difficulties in securing a consensus within the UNSC. Russia and China, in particular, are opposed to further sanctions and both countries have powers of veto.

The potential for further sanctions at the EU level depends upon the interests of EU member states. The current EU focus is on implementation of the sanctions already in place, however, further sanctions should not be ruled out, particularly if there is a lack of progress in talks with Iran. In this context, the UK position mirrors that of the EU.

In the US, it is likely that further measures against Iran will be introduced, largely due to concentrated efforts within US Congress to enhance the current Iran sanctions regime. On 1 August 2013, the House of Representatives passed a new bill, entitled the “Nuclear Iran Prevention Act”, which seeks to impose a near-total oil embargo on Iran as well as expanding restrictions on commercial activities. This bill is due to be voted upon by the Senate in September.19

A Bird’s Eye View: Assessing the Current Sanctions Landscape The sanctions landscape constitutes a complex mosaic of restrictive measures imposed by national and international authorities. For the most part, the different sanctions regimes share common policy objectives. Broadly speaking, the different law-makers agree on the goals that they are seeking to achieve in the Iranian context.

However, the practical legislative measures that different authorities adopt in pursuit of these objectives, as well as the rate at which they are imposed, differ significantly. The United States, for example, has imposed a sanctions regime that far surpasses those imposed by the European Union or the United Kingdom in terms of extraterritoriality and severity. Moreover, a considerable political appetite for sanctions within US Congress has meant that sanctions legislation has been passed at a considerable rate in the in recent years.

Navigating this sanctions landscape presents a number of risks and difficulties for industry. Inevitably, the rapidly-changing nature of the legislation poses challenges in terms of the compliance efforts of multinational organisations operating in multiple jurisdictions. The need for quick implementation of shock asset freeze measures by industry, for example, means that compliance teams have to respond to new measures almost instantly. Those responsible for compliance are forced to operate in a fluid, rapidly-evolving sanctions environment where there is often a lack of clarity regarding certain aspects of the legislation.

18 “The Financial Restrictions (Iran) Order 2012”, 20 November 2012, available from Legislation.gov Website, <http://www.legislation.gov.uk/uksi/2012/2904/introduction/made>. This Order was revoked on 31 January 2013 after a similar prohibition was introduced at EU level. 19 “Iran Sanctions Bill on Oil Passed By US House”, BBC, 1 August 2013, <http://www.bbc.co.uk/news/world-middle-east-23530245>.

20

The challenges here are compounded by a lack of dialogue between policy-makers and industry practitioners. The unforeseen consequences of legislation mean that there is significant exposure to risk for industry stakeholders. However, while industry experts have much to contribute in terms of identifying potential problems with proposed legislation, there is an absence of regular communication. Consequently, the relationship between industry and the policy community is best described as a reactive one, with both sides constantly playing catch-up as problems are encountered and must be resolved.

Finally, in terms of how the insurance industry interprets the sanctions landscape, it is clear that US sanctions represent the benchmark for compliance efforts. The dominant role occupied by the United States and the US dollar (USD) in the global economy means that multinational companies cannot afford to be found in non-compliance with US sanctions. It is thus US legislation that acts as the principal driver of compliance efforts, although this is not to say that firms are not also keen to comply with other sanctions regimes.

21

22

PART TWO:

THE CHALLENGES OF SANCTIONS LEGISLATION

23

Practical Challenges of Sanctions Legislation This section will explore some of the practical challenges posed to industry by sanctions legislation. The analysis will use the particular example of marine insurance, a significant sub-section of the insurance industry, to illustrate the nature and scope of some of the problems encountered by industry practitioners. The section will also briefly explore the issue of blocking legislation as another discrete legislative issue with the potential to cause significant problems for businesses operating across multiple jurisdictions.

Legislation Challenges: Marine considerations The contribution of shipping to global trade across a range of industries is enormous. In the energy sector alone, more than two-thirds of oil consumed worldwide is transported by sea since shipping offers the most economical means of transportation in bulk. This is particularly important in the Iranian context. Prior to the imposition of the EU oil embargo, Iran was OPEC’s second-largest producer and exported most of its 2.2 million barrels of oil per day.20 Through the imposition of an oil embargo on Iran, the US and the EU have thus used sanctions to target Iran's largest single source of revenue.

Supporting global shipping activities is the marine insurance sector. The availability of adequate insurance cover, and in particular marine liability insurance cover, is of fundamental importance to the global shipping industry. Protection and Indemnity (P&I) Insurance is third party liability insurance cover taken out by ship owners to protect against such liabilities as oil pollution, loss of life and personal injury, wreck removal and damage to other vessels and property. In some cases, for example oil pollution and loss of life or injury to passengers, such liabilities are governed by international maritime conventions which mandate the existence of adequate insurance cover or other financial security to very high limits in order to protect third party victims. Such liabilities can run to hundreds of millions or, in the case of passengers and crew liabilities, billions of dollars.

It is for this reason that US and EU sanctions targeting maritime trade with Iran have focused on the provision of insurance to ship operators transporting Iranian oil. For while Iran still has a number of willing buyers of oil, petrochemical products and gas, including China, Japan and India, some ninety per cent of the world's tanker insurance is based in the West and the lack of access to this market constitutes a major obstacle to those wishing to transport Iranian cargoes. In this regard, marine insurance has been termed, the “stranglehold on Iran”.21

Moreover, while the prohibition preventing US and EU P&I insurers from providing cover has caused shippers wishing to carry Iranian oil as cargo to turn to alternative sources of P&I - such as the Kish P&I club in Iran, or even national governments - these alternative sources providers are untested in terms of their ability to respond to claims arising and the levels of cover available, thus raising some significant questions regarding the viability of coverage and the risks involved.

20 Clare Baldwin and Osamu Tsukimori, “Analysis: Marine insurance: the stranglehold on Iran?”, Reuters, 17 April 2012. 21 Ibid.

24

The Difficulties and Costs of Compliance for Marine Insurers The prohibition on the provision of insurance to ship owners transporting Iranian oil has indeed served to significantly reduce Iran’s oil market. In June 2013, Reuters reported that Iran's crude exports had dropped to some 700,000 barrels per day (bpd).22 At the same time, however, it also poses a number of practical difficulties and costs to marine insurance providers. Clearly, the difficulties faced by individual organisations vary according to the nature and scope of their particular business. This said, there are a number of challenges that are common to firms across the marine insurance sector.

First, it is often difficult for insurers who are far removed from the commercial activities of insured parties to be confident that sanctions are being complied with. Consider, for example, a P&I insurer of commercial vessels. It is not practical for the insurer, whether it be a mutual club or commercial insurer, to be continuously aware of the exact location of each and every vessel it insures. Consequently, this is not a requirement of the coverage provided. In any case, the continuous monitoring of vessel movements would require considerable resources. In the majority of cases, ship operators will only likely contact the insurer if something goes wrong, and, even in these cases, it is not uncommon for the insurer to hear about potentially sanctions-breaching activity through the press or from governments rather than the operator.

Some of the risk here can be mitigated by measures taken by the insurer as part of a comprehensive compliance programme. For example, commercial intelligence can be used to raise a red-flag when an insured ship enters an Iranian port. Once this occurs, a dialogue can begin between the operator and the insurer, and the insurer can take steps to safeguard its commercial and reputational interests. However, incorporating measures such as commercial intelligence into a compliance programme do not come without cost for insurance industry stakeholders.

Second, sanctions legislation is often rolled out quickly in response to political drivers. Consequently, legislation can be vague and leave room for conflicting interpretations. For example, if a non-Iranian ship is carrying Iranian oil to a country which possesses an NDAA waiver, it is unlawful for an EU insurer to provide coverage to the vessel.23 Should the insurer then terminate all coverage for the ship in question, or simply withdraw coverage for the particular voyage that violates sanctions? While this is unlikely to be necessary, it still puts the insurer in a difficult situation, not least in reputational terms. Whilst legislative ambiguities such as this are usually resolved by the relevant authorities, this can take time leaving a period of uncertainty for commercial actors.

Third, as with other sectors, the marine sector feels the effects of sanctions on Iran in more general terms. For example, the financial costs of concluding operations in Iran, as many shipping companies have, can be significant and the process can be complex. Issues here include the costs of closing offices, or the challenges associated with making payments to

22 Alex Lawler and Nidhi Verma, “Sanctions push Iran's oil exports to lowest in decades”, 5 June 2013 <http://uk.reuters.com/article/2013/06/05/us-asia-iran-oil-idUSBRE9540FV20130605>. 23 Under Article 49(d) of EU Regulation 267/2012, EU sanctions apply to all EU companies in respect of all their business worldwide. EU sanctions prohibit the provision, directly or indirectly, of "financial assistance" for the transport of crude oil (and petroleum products) of Iranian origin. Under Article 11(1)(d) of Regulation 267/2012, "Financial assistance" is expressly stated to include insurance (and reinsurance).

25

local staff through Iranian banks. On the other hand, continuing legitimate commercial operations in Iran, however limited, poses a reputational risk to an international organisation. The situation is made more complex by the fact that many organisations have invested considerable time and effort in establishing good business relations in Iran, a country renowned for its bureaucracy and factionalism.

Lost Business and Emerging Markets Other important consequences of Iran sanctions relate to lost business and the growth of alternative sources of insurance and reinsurance. While the impact here is difficult to quantify, the fact that US and European P&I insurers can no longer provide insurance to entities such as the Islamic Republic of Iran Shipping Lines (IRISL) and the Iranian National Tanker Company (NITC), or to other non-Iranian shipping companies which can quite legitimately and lawfully continue to trade with Iran, translates as a loss of potential revenue.

Moreover, sanctions on Iran have led to the further development of the Iranian insurance market. Without the ability to procure P&I cover from the leading P&I clubs, Iranian ship operators have turned to the domestic insurance market, including the Kish P&I club. This, in turn, has facilitated the development of the industry in Iran. Iranian media have claimed that these developments have saved Iranian shipping companies millions of dollars, however this reliance on alternative and less established sources of P&I cover raises a number of important questions (see section below on broader risks).24

Sanctions have also provided an opportunity for other marine insurance markets to grow around the world. In October 2009, for example, the UK Treasury prohibited business with Iranian state shipping company IRISL, prompting coverage to be withdrawn from UK insurers. IRISL subsequently secured temporary cover from a Bermuda-based provider, and following the passage of legislation in Bermuda in 2010, took cover from an Iranian provider.25 In broader terms, a number of key growth markets may be identified, including China, India, Japan and Russia. Russia, in particular, has been identified as “a good example of how quickly a major market can develop”.26

Despite the emergence of new markets in an uncertain landscape, however, the competitive advantages of UK and US markets should not be forgotten. It is widely accepted that the UK and US insurance markets are well-established, better regulated and more comprehensive than the markets emerging as a response to sanctions.

The impact of sanctions on insurance coverage has also resulted in state actors providing sovereign cover. For example, after the EU regulations came into effect in July 2012, the cover that the Japan Ship Owners’ Mutual P&I Club could provide to ships transporting Iranian oil dropped from $7.6 billion to just $8 million (US $9 million with effect from 20 February 2013).27 Japan responded to this by passing a bill which would allow for $7.6 billion

24 “Insurance Bans on Oil Tankers Save Iran $700m: Official”, Press TV, 10 September 2012 <http://www.presstv.com/detail/2012/09/10/260871/insurance-bans-save-iran-700m/>. 25 Luke Hunt, “Maritime Disaster waiting to Happen”, The Diplomat, 22 August 2011 <http://thediplomat.com/2011/08/22/maritime-disaster-waiting-to-happen/2/>. 26 Workshop participant, 4-5 June 2013. 27 Takeo Kumagai, “Japan Caught between the Insurance Trap and EU sanctions on Iran oil”, The Barrel Blog, 5 June 2012 <http://blogs.platts.com/2012/06/05/japan_caught/>.

26

of sovereign cover to ships importing Iranian oil, allowing imports to continue.28 India has also provided state backed insurance to allow shipments of Iranian oil to continue, although with much lower limits of liability than would be provided by a conventional P & I insurer.29

P&I and Broader Risks The risks associated with prohibitions on P&I cover need to be carefully considered. As already mentioned, P&I insurers play a crucial role due to their ability to provide significant levels of coverage in the event of serious incidents at sea. This includes circumstances where a ship has become a casualty and salvage is required; perhaps where a ship has caught fire, grounded or has been lost at sea. P&I cover is in place to pay for the consequential liabilities, including oil pollution and consequential loss and damage claims, loss of life and personal injury wreck removal amongst others, that the casualty may have caused. Given that 90% of global shipping is insured by the London-based International Group of P&I Clubs, and in turn reinsured by the global reinsurance markets, the restrictions placed on the established US and European insurers, including the P&I clubs have serious implications.30

Potential Accidents With sanctions preventing P&I insurers from covering Iranian shipping or ships carrying Iranian oil, Iranian and other ship operators have been forced to look elsewhere for their coverage. Clubs such as Iran’s Kish P&I club claim that they would be able to provide the equivalent of USD 1 billion in coverage.31 However, there are questions regarding the ability of the Kish club to pay out, particularly in light of the payment restrictions arising under financial sanctions measures imposed on dealings with Iran.32 Only a serious accident at sea involving a vessel with coverage by Kish or another club would test these claims, with the consequent risk of non-payment falling on innocent third-party victims of the maritime casualty.

There are a number of different scenarios which could potentially arise involving a vessel with inadequate P&I coverage. Many vessels believed to be covered by Iranian P&I are those conducting trade with East Asia, including those countries which have been granted waivers from US sanctions on the purchase of Iranian oil. If a vessel carrying Iranian oil, for example, was to become a casualty and to spill its cargo along the coastline of a small state located between Iran and East Asia, would the clean-up be covered? If coverage was disputed, would Iran be liable for cleanup costs, and would the government have the political will or the funds to pay out? Would there be a need to use Iranian banks, and if so, how would this sit with current sanctions regimes? There a large number of variables which make

28 Yuji Okada, “Japan set to load first Iran Crude with Sovereign Insurance”, Bloomberg News, 13 July 2012 <http://www.bloomberg.com/news/2012-07-13/japan-set-to-load-first-iran-crude-with-sovereign-insurance-1-.html>. 29 Pratish Narayanan & Karthikeyan Sundaram, “Iran Oil Shipping to Resume as Insurers Step in: Corporate India”, Bloomberg, 2 August 2012 <http://www.bloomberg.com/news/2012-08-01/iran-oil-shipping-to-resume-as-insurers-step-in-corporate-india.html>. 30 Website of the International Group of P&I Clubs, 10 June 2013 <http://www.igpandi.org/>. 31 Website of Kish P&I Club, “About Kish P&I”, 8 July 2013 <http://www.kishpandi.com/LNGen/About.aspx>. 32 See for example Emanuele Ottolenghi and Mark Dubowitz, “Is Iran Resorting to an Insurance Scam to Keep Oil Exports Flowing”, Forbes, 15 November 2012 <http://www.forbes.com/sites/energysource/2012/11/15/is-iran-resorting-to-an-insurance-scam-to-keep-oil-exports-going/>.

27

the consequences of a potential accident uncertain: something that insurance is usually in place to prevent.

Safety Concerns Sanctions also have important implications in terms of their effect on classification societies. These are organisations which maintain standards on safety and the maintenance of ships, and work to verify these standards on board individual vessels around the world. A valid classification is typically required by a ship to enter ports around the world. Sanctions and related concerns regarding potential reputational risks have prompted these societies to halt their business in Iran.33 The EU has since imposed a specific prohibition on the provision of classification and other similar services to, in broad terms, Iranian oil tankers and cargo vessels.34

The effects of this move on the safety of vessels at sea must be considered, particularly in the context of concerns regarding the viability of Iranian P&I clubs and possible casualty situations. An impact assessment of these combined effects of sanctions could serve to highlight to policy-makers some of the risks associated with sanctions.

Intended vs. Unintended Consequences? The above-mentioned risks are commonly perceived to be ‘unintended consequences’ by stakeholders in the insurance industry; effectively the collateral damage of sanctioned business. However, this is not necessarily the case. For while the risk of a potential accident, for example, is problematic and undesireable, it may also be interpreted as simply another cost that a nuclearizing Iran brings to bear on the international community. In this context, it is worth emphasising that the view of what is an intentional effect or consequence of sanctions differs between industry and government.

In general terms, it is clear that sanctions on Iran have had significant and wide ranging effects on the marine insurance industry. Moreover, the difficulties experienced within this sector, especially in terms of the lack of coherence between the relevant authorities and the marine insurance industry, are often symptomatic of broader issues across the wider insurance industry.

Dealing with Blocking Legislation Another good example of the challenges posed to industry by sanctions legislation stems from the issue of blocking legislation. Sanctions, by their very nature, are political instruments; through restrictive economic measures, states attempt to achieve their foreign policy goals and objectives. However, elements of one state’s foreign policy may adversely affect the perceived national interests of another state and this may be reflected in conflicting sanctions legislation.

Blocking legislation refers to legislation that has been put in place by a number of jurisdictions to block the effects of extraterritorial sanctions and protect the trading interests

33 “Classification Societies Pulling Back from Iran as Sanctions Heat Up”, Maritime Connector, 19 June 2012 <http://maritime-connector.com/news/general/classification-societies-pulling-back-from-iran-as-sanctions-heat-up/>. 34 Council Regulation (EU) No 1263/2012 of 21 December 2012, Official Journal of the European Union, 22 December 2012 <http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2012:356:0034:0054:EN:PDF>.

28

of the entities based in these jurisdictions. Blocking legislation typically includes a prohibition against domestic individuals and organisations complying with certain extraterritorial measures imposed by another nation making compliance a mutually exclusive activity.

The most commonly cited legislation in this context is the 1996 EU blocking regulation (Council Regulation (EC) No 2271/96). This was put in place to protect EU trading interests and counter the measures first introduced under the Torricelli Law (1992), the Helms-Burton or Libertad Act (1996) and the Iran and Libya Sanctions Act (1996).35 These three pieces of US legislation feature dimensions that are (or were) directed at the activities of non-US companies based in third countries. Simply put, the EU objected to the restrictions imposed upon its members by US legislation and took action to neutralise these restrictions. EU blocking legislation works to counter certain elements of US sanctions legislation, protecting the actions of EU businesses.

While the EU blocking regulation is perhaps the best known, there are also other relevant pieces of blocking legislation, including various national laws within the EU. For example, UK measures in 1980 and 1993 form a somewhat lighter version of the EU blocking legislation, creating powers for the UK authorities to intervene to protect UK commercial interests where appropriate. More recent legislation, which has similar objectives, is also in place in countries as diverse as Germany, Canada, Mexico, Australia, Argentina and Israel.

When businesses find themselves affected by blocking legislation, there is often uncertainty regarding which legislation they must comply with. The difficulty is often compounded by the multiple national bases of different actors: an example here would be a situation involving underwriters from countries A and B, reinsurers from countries C and D, a broker from country E, as well as insured party from country F perhaps owned by an entity in country G making a claim following an incident in Jurisdiction H.

In particular, concerns have been raised over whether compliance with the extraterritorial element of CISADA by EU members would leave them in breach of EU laws, or indeed their own national laws.

Moreover, while a particular transaction or commercial activity may not directly involve a US entity or US dollar transaction, there is often an entity somewhere down the chain that would need to make or receive a payment in US dollars.

There are few cases involving blocking legislation where enforcement actions have been taken. A single case of an Austrian bank involving actions to cancel the accounts of Cuban nationals in 2007 provides the only example in the public domain.36 This makes it difficult for companies’ compliance and risk management programmes to conceptualise the risks.

In the insurance industry, it appears that in cases where there is no obligation to comply with US sanctions or where blocking legislation counters US sanctions legislation, international organisations will often choose to comply with US sanctions. There are two principal reasons for this:

35 Nicholas Davidson, “U.S. Secondary Sanctions: The U.S. and the E.U. Response”, Stetson Law Review (1998), Vol.XXVII, available from http://www.law.stetson.edu/lawreview/media/u-s-secondary-sanctions-the-u-k-and-e-u-response.pdf. 36 George Jahn, “Austrian Bank Won’t Serve Cubans”, The Washington Post, 13 April 2007 <http://www.washingtonpost.com/wp-dyn/content/article/2007/04/13/AR2007041301357.html>.

29

• While following US sanctions may place an organisation at risk of non-compliance with EU legislation, there are questions regarding the EU authorities’ will to pursue the case in this context. The US authorities are considerably more active in this regard.

• The role and influence of the US market and currency in the global economy means that company policy may give priority to compliance with US sanctions. The costs of being found in non-compliance by US authorities are significant. This point is linked to the ‘risk appetite’ of international organisations and how this finds expression in company compliance policies.

In general terms, the issue of blocking legislation has been the subject of conflicting legal interpretations and continues to lack clarity. At present, transactions or activities that involve a conflict between different sanctions regimes need to be considered on a case-by-case basis and pose a significant challenge to those responsible for compliance.

30

PART THREE:

COMPLIANCE AND ENFORCEMENT

31

Managing Compliance Requirements: A Successful Framework

In recent years, sanctions have emerged as a key tool in efforts to achieve foreign policy goals with regard to Iran. Organisations have had to rapidly respond to sanctions developments to ensure that they have adequate compliance systems and processes in place to prevent non-compliance and the associated financial, legal and reputational risks. It is thus important to consider the nature and demands of successful compliance frameworks within the insurance industry. While the specific systems in place in different companies are largely dependent on a variety of business, operational and historic factors, much can be gained from exploring the general approaches adopted by different organisations.

Compliance Systems It is no surprise that both industry practitioners and policy-makers agree on the need for a systematic approach to compliance. In terms of the implementation and enforcement of sanctions, the response of relevant authorities to sanctions violations is heavily influenced by the compliance system that an organisation has in place.

Across UK, US and EU sanctions regimes, competent authorities attach considerable importance to the nature and extent of an organisation’s compliance systems and processes when making judgements regarding a firm’s compliance or non-compliance with the law and any resultant actions. For example, the rigour of an insurer’s compliance programme is a General Factor to be considered by the US Office of Foreign Assets Control (OFAC) in the overall assessment of the appropriate enforcement response to an apparent sanctions violation.37

In this context, it should be noted that in the late 2000s, many of the large fines arising from sanctions violations - primarily by banks - related to failures or inadequacies in the organisation’s compliance system. In many of these cases, violations were extensive, systematic, and often related to multiple sanctioned countries and entities.

At the expert workshop, Industry representatives presented some examples of how their businesses approach the issue of compliance. Discussions here addressed a range of topics including approaches to the broader organisation of the system, how specific components are managed, and how systems are kept up-to-date and relevant. Industry participants also discussed some of the difficulties associated with compliance systems and management. Some discussion points reflected the operating procedures of individual businesses and have been omitted from the report, however details of some of the more general points are set out in the following sections.

Screening Systems All major insurance companies have put in place IT systems to automatically screen existing and potential customers and business partners on a periodic basis. These automated systems screen entities against all major lists of designated entities and sanctioned parties, and raise a red-flag when matches are found.

One major challenge associated with screening systems relates to ‘false positives’. This refers to occasions when the system flags entities which have similar details (for example

37 See Federal Register, Rules and Regulations, Vol. 74, No. 215, 9 November 2009 <http://www.treasury.gov/resource-center/sanctions/Documents/fr74_57593.pdf>.

32

name, location, address, date of birth) as a listed entity. These possible matches must then be assessed manually by a compliance team before a decision is made to proceed with business or not.

The rate of ‘positive hits’, false or otherwise, varies across organisations and between software. In general terms, however, workshop participants had experienced few actual positive hits. This is partly due to the relatively low number of designated entities and individuals, however, deception plays a major role. Listed individuals and organisations are usually aware of their status as designated entities and are unlikely to use their true names and/or details to conduct business, often using proxies to avoid detection.

Another challenge associated with assessing screening systems and their results relates to the unlogged number of inquiries that are rejected before reaching the screening stage. These can be rejected for a number of reasons, such as originating in an area that the organisation does not conduct business in, for example.

Finally, screening often takes place after much initial time and effort has been spent on a prospective deal. Consequently, a key issue to consider is how compliance functions within firms can raise awareness with underwriters and other relevant parties and assist them in rapidly identifying instances where business may not be possible.

In this context, it is crucial to have software that is fit-for-purpose, incorporating effective and efficient algorithms. This software should also be supported by secondary, independent testing measures, and incorporated into the business in a manner which maximises efficiency.

Advances in the technology mean that screening systems constitute an important and valuable tool supporting compliance efforts within organisations. However, challenges such as those mentioned above mean that, at present, technology and screening systems serve as the second line of defence rather than the first. Emphasis remains on the importance of human resources, promoting awareness of sanctions-related issues and, where possible and appropriate, training for underwriters and brokers.

Education and Training Finding effective ways to educate employees or, indeed customers regarding sanctions and their impact is central to a robust and comprehensive compliance system. However, this also poses a number of challenges. These challenges relate less to the general understanding of stakeholders in cases where the risks are clear and alarms are likely to be raised, and more to awareness of the specifics of sanctions legislation.

For example, any business involving Iran or Syria or is likely to be quickly flagged by underwriters. Similarly, practitioners and customers will quickly become aware of higher-profile issues, such as ‘bunkering’ for example, especially when coverage providers make efforts to provide them with guidance to mitigate the risk of misunderstanding.

However, education and training for stakeholders on the specifics of sanctions legislation constitutes a more problematic issue. Large insurance and reinsurance organisations often operate across multiple jurisdictions, and employees must therefore understand and reconcile the complexities of different regimes and legislative frameworks, as well as how these apply to specific cases.

33

In this context, it is common practice to rely on legal counsel or compliance officers to interpret legislative measures and their potential impact. This is due to two interlinked factors. First, a lack of understanding on the part of employees and, second, a desire to shift the burden of responsibility.38 However, while this does mitigate the risk of sanctions violations, it also places considerable, and perhaps excessive, pressure on legal or compliance officers, thus reducing their capacity for other work.

Education and training offer a means of easing the pressure on legal counsels and compliance officers without exposing the organisation to undue risk. In the workshop, for example, participants discussed the training that their organisations provide to underwriters and other employees. The discussion highlighted the value of tools such as intranet feeds to post updates and straightforward summaries of legislative changes for employees. In terms of the customer, the value of email alerts to update customers and policy holders was also highlighted. Another key issue relates to the importance of having clear routes of escalation, and guidance on what kind of further questions to ask regarding commercial activities.

Due Diligence: How Much is Enough?

Due diligence constitutes a cornerstone of a sanctions compliance programme in any industry. Insurance providers, reinsurance companies and brokers (among others) can all play a role in an insurance-related transaction. Each of these stakeholders will have different views of potential customers and their connections and attribute different levels of priority to the entities and facts involved in any prospective deal.

Having in place processes and guidelines which inform employees as to how much due diligence is enough – or, indeed, how much is too much – is an important part of an organisation’s approach to risk and compliance. However, competent authorities and enforcement agencies are reluctant to provide concrete opinions or comprehensive guidance on the matter. It is thus left to firms to develop their own interpretation of how much due diligence is needed based on their ‘risk appetite’.

The area of due diligence presents many difficulties in the compliance context. Some challenges include the long-standing nature of agreements or contracts; the need to verify details multiple times at different points during a transaction, such as when business is written or when a claim is made; and the difficulties of determining whether certain activities carried out by a customer were prohibited, thus nullifying contracts.

Some guidance has been provided in this area by The Corporation of Lloyd’s which provides oversight and support to the Lloyd’s Market in the UK. The due diligence guidance provided, Sanctions Due Diligence Guidance for the Lloyds Market,39 was prepared by Lloyds and in part ‘reviewed’ by the UK Treasury.40 It should be noted that the guidance is ‘not prescriptive

38 Note that the desire to shift responsibility often stems from the lack of understanding regarding sanctions legislation and its potential impact. 39 “Sanctions Due Diligence Guidance for the Lloyd’s Market”, Lloyd’s, 6 February 2012 <http://www.lloyds.com/~/media/Files/The%20Market/Communications/Key%20regulatory%20projects/Financial%20Crime/20120206_Sanctions_due_diligence_guidance.pdf>. 40 “Sanctions Compliance – Due Diligence Guidance for the Lloyd’s Market”, Market Bulletin Y4560, 6 February 2012 <http://www.lloyds.com/~/media/Files/The%20Market/Communications/Market%20Bulletins/2012/02/Y4560.pdf>.

34

but does set down a framework to which managing agents should refer when assessing their procedures’.41

Government Guidance: A Factor in Enforcement The extent to which firms conduct due diligence plays a significant role in judgements relating to sanctions violations. If firms have appropriate due diligence processes in place, there may be ‘exceptions’, meaning that penalties will not be imposed, or that a company’s efforts may be considered as mitigating circumstances by prosecutors.

CISADA (2010) provides an example here, factoring due diligence into enforcement actions. An exception is provided for firms engaging in sanctionable activity related to the provision of underwriting, insurance or reinsurance if “the President determines that the person has exercised due diligence in establishing and enforcing official policies, procedures, and controls to ensure that the person does not provide” prohibited services.42 Similar clauses are included in related more recent legislation.43

However, while due diligence is said to be an important factor, the lack of detailed official guidance regarding how much due diligence is appropriate presents a significant challenge to industry. Official guidance is limited in terms of the specifics here. Take for example, the guidance issued by the US State Department in 2012 which notes:

“All persons involved in activities in high-risk sectors should consider implementing enhanced due diligence in order to minimize the risks of inadvertently becoming engaged in a sanctionable transaction. This could include, but is not limited to, confirming that transactions in these sectors do not involve an entity owned or controlled by Iran or that Iran is not otherwise connected to any entities in the commercial transactions, including by reviewing the Office of Foreign Assets Control's Specially Designated Nationals and Blocked Persons (SDN) List; searching commercial databases and verifying ownership structures of unknown companies; and, in the case of transportation or insurance of crude oil and petroleum products, verifying that Iran is not the origin of the cargo”.44

It is a widely held view in industry that while due diligence can serve as a mitigating factor in OFAC enforcement actions, there is often a lack of clarity regarding what exactly is expected by the authorities. It is also accepted that while a comprehensive due diligence system can serve as a mitigating factor, it does not constitute a ‘get-out-of-jail-free’ card.

41 Ibid. 42 See 5(a)(9) of the ‘Iran Sanctions Act’ (1996), available at <http://www.house.gov/legcoun/Comps/Iran%20Sanctions%20Act%20Of%201996.pdf> 43 See for example the clause in IFCA as brought in by the 2013 NDAA. Clifford Chance, “Iran Sanctions Expanded by the National Defense Authorisation Act for Fiscal Year 2013”, Client Briefing, January 2013 <http://www.cliffordchance.com/publicationviews/publications/2013/01/iran_sanctions_expandedbythenationaldefens.html>. 44 “State Department Sanctions Information and Guidance”, US Department of State Website, 8 November 2012 <http://www.state.gov/e/eb/tfs/spi/iran/fs/200316.htm>.

35

Due Diligence: A Risk-based Approach Given the dearth of official guidance on due diligence, it is left to individual organisations to determine what they see as an appropriate level of due diligence. Workshop participants agreed that the issue of due diligence largely relates to the judgement of individual companies in terms of how they balance risks and where they draw the line when it comes to conducting due diligence. This, in turn, is based on the ‘risk appetite’ of the company, the type of business pursued, the regulatory environment and different business cultures.

Determining the appropriate level of due diligence is a complex process due to the large number of unknowns and uncertainties in this area of business. The long term nature of contracts and business poses particular problems. The simple fact that ship operators may change while the owner remains the same serves to illustrate this point. While it is possible to mitigate certain risks with an exclusion clause, which are now commonplace in the industry, problems remain.

Beyond determining the risk appetite of the company, it is also crucial to ensure that others – both those within the organisation (underwriters, etc.) and those without (brokers, etc.) are aware of company policy and approach to these issues. In this context, relationships with brokers are often highlighted as a particular challenge. The difficulty here lies in ensuring that brokers are adequately informed of a particular insurance or reinsurance company’s sanctions and risk policy, that they are asking the appropriate questions and that they are aware of red flags.

Of course, there are other difficulties associated with a risk-based approach. The question of resources, for example, weighs heavily on policy considerations within an organisation. In cases where firms feel that the costs of determining the integrity of parties to be insured and their activities, they may be inclined to reject the business outright. This is an often unconsidered cost of compliance and effect of sanctions.

Take for example a prospective deal to insure a particular shipment for a small business; a low value transaction, yet for a valued and long-term customer. If for example on this occasion, the customer is planning to purchase goods from Iran. If there are questions that are difficult to answer regarding the exact nature of the goods, shipment routes and the entities from which the goods are being purchased, business sense and risk appetite may dictate that the potential business be turned down.

These dilemmas are particularly acute in areas where there is a lack of clarity in the information provided or acquired, or where there is a specific risk which could be difficult to gauge. For example, if a company was to insure a shipment which could be composed of sensitive goods such as chemicals, or potentially dual-use technologies. Without knowledge regarding the specifics of the transaction it is difficult to assess the risk.

Furthermore, there are a number of ethical and business issues at stake here. If the customer is a long term customer, there would be little reason to doubt that their request was for genuine legitimate business. Turning it down would likely prove to be the end of the business relationship. This type of situation also shifts the impact of sanctions towards smaller business rather than of larger companies pursuing higher-value transactions and more easily verifiable bonafides.

36