Embed Size (px)

Citation preview

SAN MIGUEL CORPORATION

Shelf Registration in the Philippines of

up to 975,571,800 Series “2” Preferred Shares

to be offered within a period of three (3) years

at an Offer Price of ₱75.00 per Preferred Share

to be listed and traded on the Main Board

of The Philippine Stock Exchange, Inc.

THE SECURITIES AND EXCHANGE COMMISSION HAS NOT APPROVED THESE

SECURITIES OR DETERMINED IF THIS PROSPECTUS IS ACCURATE OR

COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE

AND SHOULD BE REPORTED IMMEDIATELY TO THE SECURITIES AND EXCHANGE

COMMISSION.

This Prospectus is dated March 9, 2016

2

SAN MIGUEL CORPORATION 40 San Miguel Avenue Mandaluyong City 1550 Philippines Telephone number (632) 632-3000 http://www.sanmiguel.com.ph This Prospectus relates to the shelf registration and continuous offer by way of sale in the Philippines (the “Offer”) of up to 975,571,800 cumulative, non-voting, non-participating, non-convertible Peso-denominated Series “2” Preferred Shares (the “Offer Shares”) of San Miguel Corporation (“SMC”, the “Company”, the “Parent Company” or the “Issuer”), a corporation duly organized and existing under Philippine law, subject to the registration requirements of the Securities and Exchange Commission of the Philippines (the “SEC”). The Offer Shares will be sold at a subscription price of ₱75.00 per share (the “Offer Price”), or for a total offer size of up to Seventy-Three Billion One Hundred Sixty-Seven Million Eight Hundred Eighty-Five Thousand Pesos (₱73,167,885,000.00). The Offer Shares shall be issued in tranches within a period of three (3) years (the “Shelf Period”), at an offer price of ₱75.00 per share. The Offer Shares will be issued from the (a) treasury shares of the Company and (b) unissued Series “2” Preferred Shares of the Company. The specific terms of the Offer Shares with respect to each issue tranche thereof shall be determined by the Company taking into account prevailing market conditions and shall be provided at the time of the relevant offering. The Offer Shares are being offered for subscription solely in the Philippines. On January 15, 2016, the Board of Directors of the Company (the “Board of Directors”) authorized the sale and offer of up to Eighty Billion Pesos (₱80,000,000,000.00) of Series “2” Preferred Shares, at an offer price of ₱75.00 per share, or 1,066,000,000 Series “2” Preferred Shares, under a shelf registration to be issued within a period of three (3) years from the date of effectivity of the Registration Statement, under such terms and conditions as the management of SMC may deem advantageous to it (the “Enabling Resolutions”). On June 9, 2015, the stockholders of SMC approved the issuance of Series “2” Preferred Shares and delegated to the Board of Directors the authority to determine the terms and conditions of the issuance of the Offer Shares through the approval of the relevant enabling resolutions. Dividends may be declared at the discretion of the Board of Directors and will depend upon the future results of operations and general financial condition and capital requirements of SMC; its ability to receive dividends and other distributions and payments from its subsidiaries; foreign exchange rates, legal, regulatory and contractual restrictions, loan obligations (both at the parent and subsidiary levels) and other factors the Board of Directors may deem relevant. While there is no assurance that SMC will declare dividends on the Offer Shares in the future, SMC has consistently paid quarterly cash dividends to both its common and preferred shareholders, details of which are found on page 154. The date of declaration of cash dividends on the Offer Shares will be subject to the discretion of the Board of Directors to the extent permitted by law. The declaration and payment of dividends (except stock dividends) do not require any further approval from the shareholders of SMC. As and if cash dividends are declared by the Board of Directors, and in accordance with the Enabling Resolutions, cash dividends on the Offer Shares shall be set out in the Offer Supplement, as defined in this Prospectus, in all cases calculated for each share by reference to the Offer Price thereof in respect of each Dividend Period (each, the “Dividend Rate” for the relevant subseries). Subject to limitations on the payment of cash dividends as described in the section on the “Terms of the Offer”, dividends on the Offer Shares will be payable once for every Dividend Period on such date set by the Board of Directors at the time of declaration of such dividends (each a “Dividend Payment Date”), which date shall be any day within the period commencing on (and including) the last date of a Dividend Period and 15 calendar days from the end of the relevant Dividend Period. A “Dividend Period” shall be the period commencing on the relevant Issue Date, as defined in the section on “Terms of the Offer”, and having a duration of three (3) months, and thereafter, each of the successive periods of three (3) months commencing on the last day of the immediately preceding Dividend Period up to, but excluding the first day of, the immediately succeeding Dividend Period; provided that the first Dividend Period of the Offer Shares shall be the period commencing on the relevant Issue Date and ending on the last day of the then current dividend period for the outstanding

3

Preferred Shares. If a Dividend Payment Date occurs after the end of a Dividend Period, there shall be no adjustment as to the amount of dividends to be paid. The dividends on the Offer Shares will be calculated on a 30/360-day basis. If the Dividend Payment Date is not a Banking Day, dividends will be paid on the next succeeding Banking Day, without adjustment as to the amount of dividends to be paid. For the purpose of the first dividend payment of the Offer Shares, the same will be paid on such date as to synchronize with the payment of dividends for the outstanding Preferred Shares. The Board of Directors will not declare and pay cash dividends on any Dividend Payment Date where (a) payment of the cash dividend would cause SMC to breach any of its financial covenants or (b) the profits available to SMC to distribute as cash dividends are not sufficient to enable SMC to pay in full both the cash dividends on the Series “2” Preferred Shares and the dividends on all other classes of the shares of SMC that are scheduled to be paid on or before the same date as the cash dividends on the Series “2” Preferred Shares and that have an equal right to dividends as the Series “2” Preferred Shares. Upon listing of the Offer Shares on The Philippine Stock Exchange, Inc. (“PSE”), SMC may purchase the Offer Shares which are then currently tradeable at any time in the open market or by public tender or by private contract at any price through the PSE without any obligation to purchase or redeem the other outstanding preferred shares of the Company. The use of proceeds for each tranche of the Offer will be set out in the relevant Offer Supplement. No dealer, salesman or any other person has been authorized to give any information or to make any representation not contained in this Prospectus. If given or made, any such information or representation must not be relied upon as having been authorized by the Company or any of the underwriters that may be engaged by the Company for each tranche of the Offer (the “Underwriters”). The distribution of this Prospectus and the offer and sale of the Offer Shares may, in certain jurisdictions, be restricted by law. The Company and the Underwriters require persons into whose possession this Prospectus comes, to inform themselves of the applicable legal requirements under the laws and regulations of the countries of their nationality, residence or domicile, and as to any relevant tax or foreign exchange control laws and regulations affecting them personally. This Prospectus does not constitute an offer of any securities, or any offer to sell, or a solicitation of any offer to buy any securities of the Company in any jurisdiction, to or from any person whom it is unlawful to make such offer in such jurisdiction. Unless otherwise stated, the information contained in this Prospectus has been supplied by the Company. The Company (which has taken all reasonable care to ensure that such is the case) confirms that the information contained in this Prospectus is correct, and that there is no material misstatement or omission of fact which would make any statement in this Prospectus misleading in any material respect. Unless otherwise indicated, all information in the Prospectus is as of the date hereof. Neither the delivery of this Prospectus nor any sale made pursuant to this Prospectus shall, under any circumstances, create any implication that the information contained herein is correct as of any date subsequent to the date hereof or that there has been no change in the affairs of the Company and its subsidiaries since such date. Market data and certain industry forecasts used throughout this Prospectus were obtained from internal surveys, market research, publicly available information and industry publications. Industry publications generally state that the information contained therein has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Similarly, internal surveys, industry forecasts and market research, while believed to be reliable, have not been independently verified, the Company does not make any representation, undertaking or other assurance as to the accuracy or completeness of such information or that any projections will be achieved, or in relation to any other matter, information, opinion or statements in relation to the Offer. Any reliance placed on any projections or forecasts is a matter of commercial judgment. Certain agreements are referred to in this Prospectus in summary form. Any such summary does not purport to be a complete or accurate description of the agreement and prospective investors are expected to independently review such agreements in full. This Prospectus is not intended to provide the basis of any credit or other evaluation nor should it be considered as a recommendation by either the Issuer, the Underwriters or their respective affiliates or legal advisers that any recipient of this Prospectus should purchase the Offer Shares. Each person contemplating an investment in the Offer Shares should make his own investigation and analysis of the creditworthiness of

4

SMC and his own determination of the suitability of any such investment. The risk disclosure herein does not purport to disclose all the risks and other significant aspects of investing in the Offer Shares. A person contemplating an investment in the Offer Shares should seek professional advice if he or she is uncertain of, or has not understood any aspect of the securities to invest in or the nature of risks involved in trading of securities, especially those high-risk securities. Investing in the Offer Shares involves a higher degree of risk compared to debt instruments. For a discussion of certain factors to be considered in respect of an investment in the Offer Shares, see the section on “Risks Factors” starting on page 39. The Company owns land as identified in the section on Description of Property on page 150. In connection with the ownership of private land, the Philippine Constitution states that no private land shall be transferred or conveyed except to citizens of the Philippines or to corporations or associations organized under the laws of the Philippines at least 60.0% of whose capital is owned by such citizens. For as long as the percentage of Filipino ownership of the capital stock of the Company is at least 60.0% of the total shares outstanding and voting, the corporation shall be considered as a 100.0% Filipino-owned corporation. The listing of the Offer Shares is subject to the approval of the Board of Directors of the PSE. An application to list the Offer Shares has been filed with the PSE, but has not yet been approved by the Board of Directors of the PSE. If approved by the PSE, such approval for listing is permissive only and does not constitute a recommendation or endorsement of the Offer Shares by the PSE. The PSE assumes no responsibility for the correctness of any statements made or opinions expressed in this Prospectus. The PSE makes no representation as to its completeness and expressly disclaims any liability whatsoever for any loss arising from reliance on the entire or any part of the Prospectus.

6

Table of Contents

TABLE OF CONTENTS .................................................................................................................................... 6

FORWARD-LOOKING STATEMENTS ............................................................................................................ 7

DEFINITION OF TERMS .................................................................................................................................. 8

EXECUTIVE SUMMARY ................................................................................................................................ 12

SUMMARY OF FINANCIAL INFORMATION ................................................................................................. 23

CAPITALIZATION .......................................................................................................................................... 25

TERMS OF THE OFFER ................................................................................................................................ 26

DESCRIPTION OF THE OFFER SHARES .................................................................................................... 34

RISK FACTORS ............................................................................................................................................. 39

USE OF PROCEEDS ...................................................................................................................................... 59

DETERMINATION OF OFFER PRICE ........................................................................................................... 60

DILUTION........................................................................................................................................................ 61

PLAN OF DISTRIBUTION .............................................................................................................................. 62

THE COMPANY .............................................................................................................................................. 65

DESCRIPTION OF PROPERTY ................................................................................................................... 150

LEGAL PROCEEDINGS ............................................................................................................................... 151

OWNERSHIP AND CAPITALIZATION ........................................................................................................ 152

MARKET PRICE OF AND DIVIDENDS ON THE EQUITY OF SMC AND RELATED SHAREHOLDER MATTERS ..................................................................................................................................................... 154

DIRECTORS AND EXECUTIVE OFFICERS ................................................................................................ 160

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS ............................................................... 170

SELECTED FINANCIAL INFORMATION AND OTHER DATA ................................................................... 172

MANAGEMENT’S DISCUSSION AND ANALYSIS OF RESULTS OF OPERATIONS AND FINANCIAL CONDITION .................................................................................................................................................. 174

EXTERNAL AUDIT FEES AND SERVICES ................................................................................................ 188

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE ............................................................................................................................................... 189

INTEREST OF NAMED EXPERTS AND COUNSEL ................................................................................... 190

TAXATION .................................................................................................................................................... 191

REGULATORY FRAMEWORK .................................................................................................................... 195

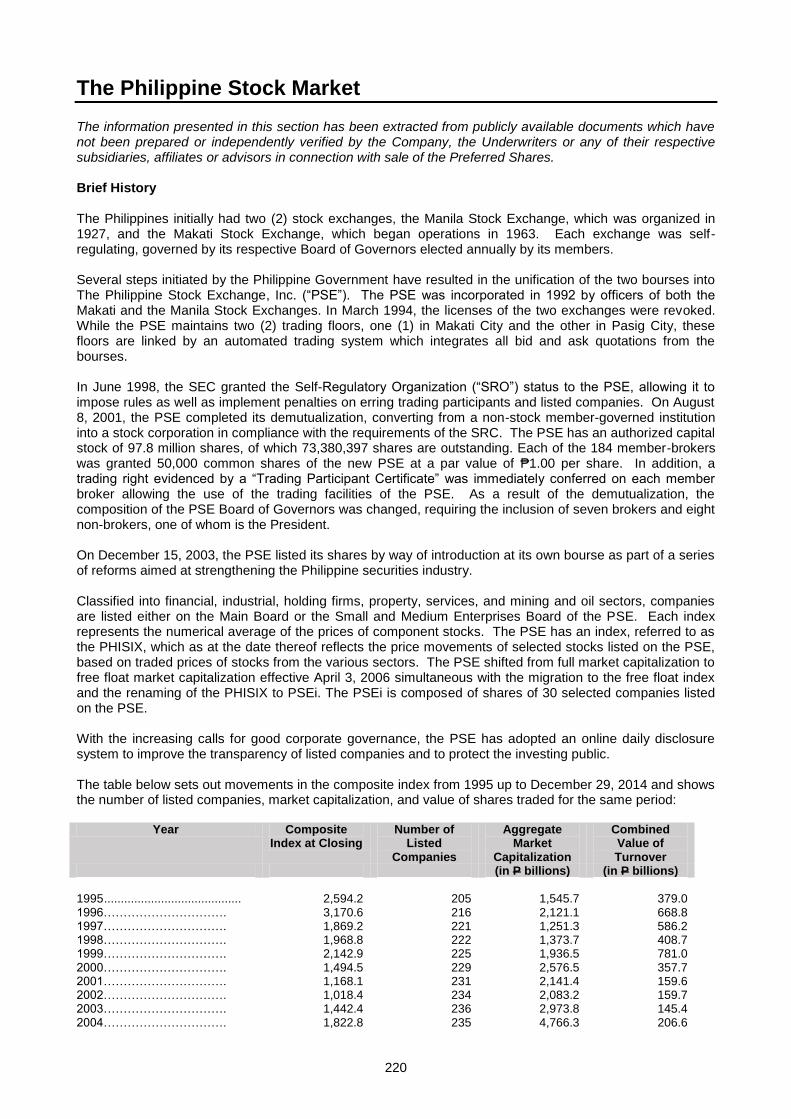

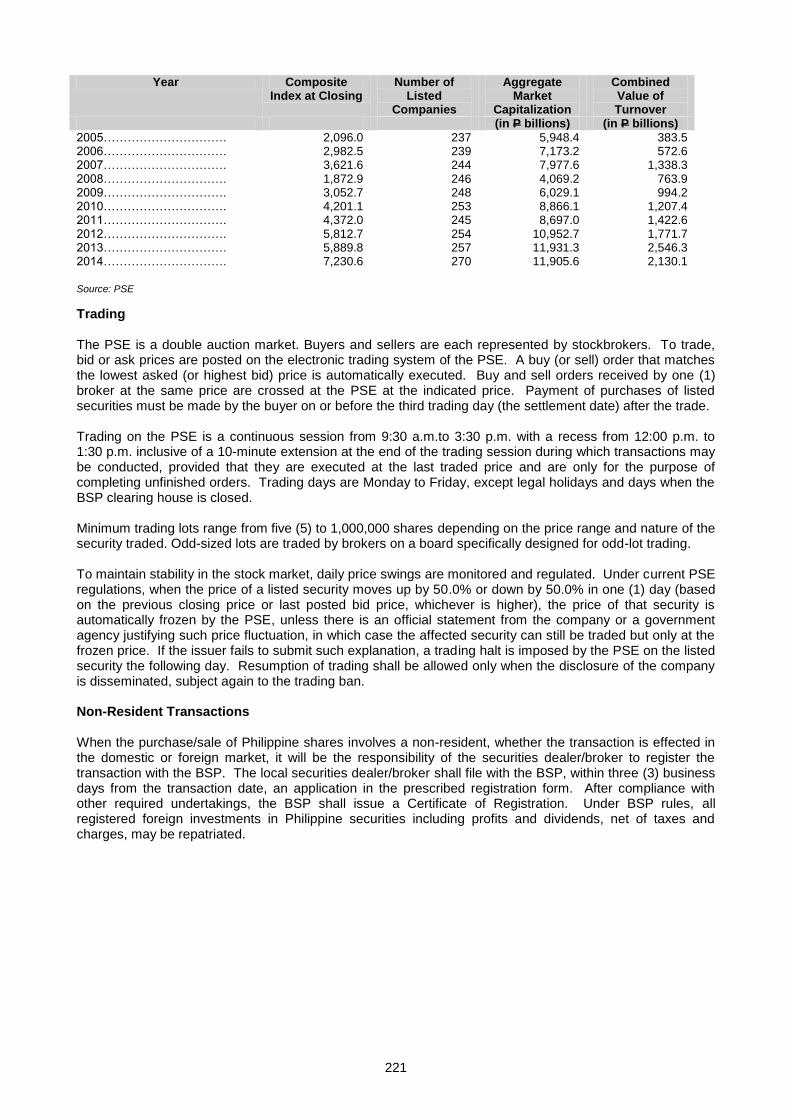

THE PHILIPPINE STOCK MARKET ............................................................................................................ 220

APPENDIX .................................................................................................................................................... 225

7

Forward-looking Statements

This Prospectus contains forward-looking statements that are, by their nature, subject to significant risks and uncertainties. These forward-looking statements include, without limitation, statements relating to:

known and unknown risks;

uncertainties and other factors which may cause actual results, performance or achievements of SMC to be materially different from any future results; and

performance or achievements expressed or implied by forward-looking statements. Such forward-looking statements are based on assumptions regarding the present and future business strategies and the environment in which SMC will operate in the future. Important factors that could cause some or all of the assumptions not to occur or cause actual results, performance or achievements to differ materially from those in the forward-looking statements include, among other things:

the ability of SMC to successfully implement its strategies;

the ability of SMC to anticipate and respond to consumer trends;

changes in availability of raw materials used in the production processes of the SMC Group;

the ability of the SMC Group to successfully manage its growth;

the condition and changes in the Philippines, Asian or global economies;

any future political instability in the Philippines, Asia or other regions;

changes in interest rates, inflation rates and the value of the Peso against the U.S. Dollar and other currencies;

changes in government regulations, including tax laws, or licensing requirements in the Philippines, Asia or other regions; and

competition in the beer, liquor, food, packaging, power, fuel and oil, telecommunications, and infrastructure industries in the Philippines and globally.

Additional factors that could cause actual results, performance or achievements of SMC to differ materially include, but are not limited to, those disclosed under “Risk Factors” and elsewhere in this Prospectus.

These forward-looking statements speak only as of the date of this Prospectus. SMC and the Underwriters expressly disclaim any obligation or undertaking to release, publicly or otherwise, any updates or revisions to any forward-looking statement contained herein to reflect any change in the expectations of SMC with regard thereto or any change in events, conditions, assumptions or circumstances on which any statement is based. This Prospectus includes forward-looking statements, including statements regarding the expectations and projections of the Issuer for future operating performance and business prospects. The words “believe”, “expect”, “anticipate”, “estimate”, “project”, “may”, “plan”, “intend”, “will”, “shall”, “should”, “would” and similar words identify forward-looking statements. In addition, all statements other than statements of historical facts included in this Prospectus are forward-looking statements. Statements in this Prospectus as to the opinions, beliefs and intentions of the Issuer accurately reflect in all material respects the opinions, beliefs and intentions of the management of SMC as to such matters at the date of this Prospectus, although the Issuer can give no assurance that such opinions or beliefs will prove to be correct or that such intentions will not change. This Prospectus discloses, under the section “Risk Factors” and elsewhere, important factors that could cause actual results to differ materially from the expectation of the Issuer. All subsequent written and oral forward-looking statements attributable to either the Issuer or persons acting on behalf of the Issuer are expressly qualified in their entirety by cautionary statements.

8

Definition of Terms

In this Prospectus, unless the context otherwise requires, the following terms shall have the meanings set forth below. AAIBV…………………………………………….. Atlantic Aurum Investments B.V. including as the context requires, its subsidiaries

AAIPC……………………………………………. Atlantic Aurum Investments Philippines Corporation

AGNP……………………………………………… A. G. N. Philippines, Inc.

AHC……………………………………………….. Angat Hydropower Corporation

AHEPP……………………………………………. Angat Hydroelectric Power Plant

ALECO……………………………………………. Albay Electric Cooperative

APEC………………………………………………. Albay Power and Energy Corp.

ASEAN……………………………………………..

The Association of Southeast Asian Nations, consisting of Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand and Vietnam

BellTel………………………………………………

Bell Telecommunication Philippines, Inc.

BIR………………………………………………….

Bureau of Internal Revenue of the Philippines

Board of Directors ………………………………… Board of Directors of SMC

Bonanza Energy…………………………………. Bonanza Energy Resources, Inc

BGTOM……………………………………………. Build-Gradual Transfer-Operate-Maintain

BOT………………………………………………...

Build-Operate-Transfer

BOC……………………………………………….. Bank of Commerce

BPG……………………………………………….. Business Procurement Group

BROT……………………………………………… Build-Rehabilitate-Operate-Transfer

BTO………………………………………………… Build-Transfer-Operate

BSP………………………………………………..

Bangko Sentral ng Pilipinas

CCEC……………………………………………… Citra Central Expressway Corp.

Clean Air Act………………………………………

The Philippine Clean Air Act of 1999

Clean Water Act…………………………………..

The Philippine Clean Water Act of 2004

CMMTC……………………………………………. Citra Metro Manila Tollways Corporation

Corporation Code ……………………………….. Batas Pambansa Blg. 68, otherwise known as the Corporation Code of the Philippines, as amended

CTCII……………………………………………… Cypress Tree Capital Investments, Inc.

DA………………………………………………….

Department of Agriculture of the Philippines

Daguma…………………………………………… Daguma Agro Minerals, Inc.

DENR………………………………………………

Department of Environment and Natural Resources of the Philippines

Distribution Code ………………………………… The Philippine Distribution Code

DOE………………………………………………..

Department of Energy of the Philippines

DOH………………………………………………..

Department of Health of the Philippines, including the FDA

DOTC……………………………………………… Department of Transportation and Communications of the Philippines

DPWH…………………………………………….. Department of Public Works and Highways of the Philippines

DTI………………………………………………… Department of Trade and Industry of the Philippines

9

EBITDA……………………………………………. Earnings before interest, taxes, depreciation and amortizations

ECA…………………………………………………

Energy conversion agreement

ECC…………………………………………………

Environmental Compliance Certificate

EIS………………………………………………….

Environmental Impact Statement

EMEPMI…………………………………………… ExxonMobil Exploration and Production Malaysia, Inc.

EPIRA………………………………………………

Electric Power Industry Reform Act of 2001

ERC…………………………………………………

Energy Regulatory Commission of the Philippines

Fahrenheit Research…………………………….. Fahrenheit Research (M) Sdn. Bhd

FDA………………………………………………..

The Food and Drug Administration of the Philippines

FDDC Act………………………………………….

The Philippine Foods, Drugs and Devices, and Cosmetics Act, as amended by the Food and Drug Administration Act of 2009

FIA………………………………………………….

Foreign Investment Act of 1991

Grid Code………………………………………….

The Philippine Grid Code

Ginebra……………………………………………. Ginebra San Miguel Inc., including as the context requires, its subsidiaries

GWh………………………………………….……. Giga-watt hours

IMF………………………………………………… International Monetary Fund

IPP………………………………………………….

Independent Power Producer

IPPA……………………………………………….

Independent Power Producer Administrator

ISO…………………………………………………

International Organization for Standardization

K-Water…………………………………………… Korea Water Resources Corporation

Kirin……………………………………………….. Kirin Holdings Company, Limited

LGU…………………………………………………

Local government unit

Liberty Telecom……………………………………

Liberty Telecoms Holdings, Inc.

Livestock and Poultry Feeds Act………………..

The Philippine Livestock and Poultry Feeds Act, including its implementing rules and regulations

LPG………………………………………………..

Liquefied petroleum gas

Magnolia……………………………………………

Magnolia Inc.

MNHPI…………………………………………….. Manila North Harbour Port, Inc.

MARINA…………………………………………… Maritime Industry Authority of the Philippines

Meat Inspection Code…………………………….

The Meat Inspection Code of the Philippines

Meralco…………………………………………….

Manila Electric Company

Metrix……………………………………………… Metrix Research Sdn. Bhd.

Mincorr……………………………………………. Mindanao Corrugated Fibreboard, Inc

MRT-7………………………………………………

Metro Rail Transit Line 7

MTDME……………………………………………. MTD Manila Expressways, Inc.

MW…………………………………………………

Mega-watt

NAIAx……………………………………………… NAIA Expressway

NCR ………………………………………………. National Capital Region of the Philippines

NGCP……………………………………………… National Grid Corporation of the Philippines

NPC………………………………………………… National Power Corporation of the Philippines

10

NVRC………………………………………………

New Ventures Realty Corporation

NYG…………………………………………………

Nihon Yamamura Glass Company, Ltd.

Oil Deregulation Act………………………………

The Philippine Republic Act No. 8479, otherwise known as the Downstream Oil Industry Deregulation Act of 1998

Offer Supplement………………………………….. The document which sets out the terms and conditions for each tranche of the Offer Shares

Packaging Group ………………………………… San Miguel Yamamura Packaging Corporation, San Miguel Yamamura Packaging International Limited and its subsidiaries, San Miguel Yamamura Asia Corporation and Mindanao Corrugated Fibreboard Inc.

Padma…………………………………………….. Padma Fund L.P.

PDTC……………………………………………….

The Philippine Depository & Trust Corporation

PEMC………………………………………………

Philippine Electricity Market Corporation

Penderyn………………………………………….. Penderyn Pte Ltd.

Peso or P………………………………………….. Philippine Peso, the lawful currency of the Republic of the Philippines

PET………………………………………………...

Polyethylene Terephthalate

Petron………………………………………………

Petron Corporation including as the context requires, its subsidiaries

PFRS……………………………………………….

Philippine Financial Reporting Standards

PIDC……………………………………………….

Private Infra Dev Corporation

PNCC……………………………………………… Philippine National Construction Company

PNOC……………………………………………… Philippine National Oil Company

PPA…………………………………………………

Power purchase agreement

PPP………………………………………………….

Public-Private Partnership

Price Act……………………………………………

The Price Act

Privado…………………………………………….. Privado Holdings Corp.

PSALM………………………………………………

Power Sector Assets and Liabilities Management Corporation

PSC………………………………………………….

Power supply contract

PSE………………………………………………….

The Philippine Stock Exchange, Inc.

PVEI……………………………………………….. PowerOne Ventures Energy Inc.

Rapid………………………………………………. Rapid Thoroughfares, Inc.

RCOA……………………………………………… Retail Competition and Open Access

RMP-2………………………………………………

Petron Bataan Refinery Master Plan Phase -2 Upgrade

S3HC………………………………………………. Stage 3 Connector Tollways Holdings Corp.

San Miguel Pure Foods …………………………. San Miguel Pure Foods Company, Inc., including as the context requires, its subsidiaries

Saudi Aramco……………………………………..

Saudi Arabian Oil Company

SCCP……………………………………………….

The Securities Clearing Corporation of the Philippines

SEC…………………………………………………

Securities and Exchange Commission of the Philippines

SIDC………………………………………………… Star Infrastructure Development Corporation

SLEX……………………………………………….. South Luzon Expressway

SMB…………………………………………………

San Miguel Brewery Inc., including as the context requires, its subsidiaries

SMBIL……………………………………………….

San Miguel Brewing International, Ltd.

11

SMC, the Company, the Parent Company or the Issuer………………

San Miguel Corporation, a corporation incorporated under the laws of the Republic of the Philippines

SMC Global Power………………………………. SMC Global Power Holdings Corp. including as the context requires, its subsidiaries

SMC Group……………………………………….. SMC and its subsidiaries

SMEC……………………………………………….

San Miguel Energy Corporation

SMEII………………………………………………. San Miguel Equity Investments Inc.

SMELC…………………………………………….. San Miguel Electric Corp.

SMESI……………………………………………… San Miguel Equity Securities, Inc.

SMHC………………………………………………. San Miguel Holdings Corp., including as the context requires, its subsidiaries

SMMI………………………………………………. San Miguel Mills, Inc.

SMPI………………………………………………. San Miguel Properties, Inc., including as the context requires, its subsidiaries

SMYAC…………………………………………….

San Miguel Yamamura Asia Corporation

SMYPC…………………………………………….

San Miguel Yamamura Packaging Corporation, including as the context requires, its subsidiaries

SMYPIL……………………………………………

San Miguel Yamamura Packaging Internation Limited

SPDC……………………………………………….

Strategic Power Dev. Corp.

SPI…………………………………………………. SMC Powergen Inc.

SPPC………………………………………………..

South Premiere Power Corp.

SRC………………………………………………… Securities Regulation Code of the Philippines

SRPC……………………………………………….

San Roque Power Corporation

SSS…………………………………………………

Social Security System of the Philippines

STAR………………………………………………. Southern Tagalog Arterial Road

Sultan Energy……………………………………… Sultan Energy Philippines Corp.

TADHC…………………………………………….. Trans Aire Development Holdings Corp.

Tax Code………………………………………….. The Philippine National Internal Revenue Code of 1997, as amended

Top Frontier……………………………………….. Top Frontier Investment Holdings, Inc.

TPLEX………………………………………………

Tarlac–Pangasinan–La Union Expressway

TransCo…………………………………………….

National Transmission Corporation

TRB………………………………………………… Toll Regulatory Board of the Philippines

Underwriters………………………………………..

Underwriters that may be engaged by the Company for each tranche of the Offer

Universal LRT……………………………………..

Universal LRT Corporation (BVI) Limited

VAT………………………………………………….

Value added tax

Vega………………………………………………… Vega Telecom Inc.

Vertex……………………………………………….. Vertex Tollways Devt. Inc.

WESM……………………………………………….

Philippine Wholesale Electricity Spot Market

12

Executive Summary

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information and audited financial statements, including notes thereto, found in the appendices of this Prospectus. Prospective investors should read this entire Prospectus fully and carefully, including the section on “Risk Factors”. In case of any inconsistency between this summary and the more detailed information in this Prospectus, then the more detailed portions, as the case may be, shall at all times prevail.

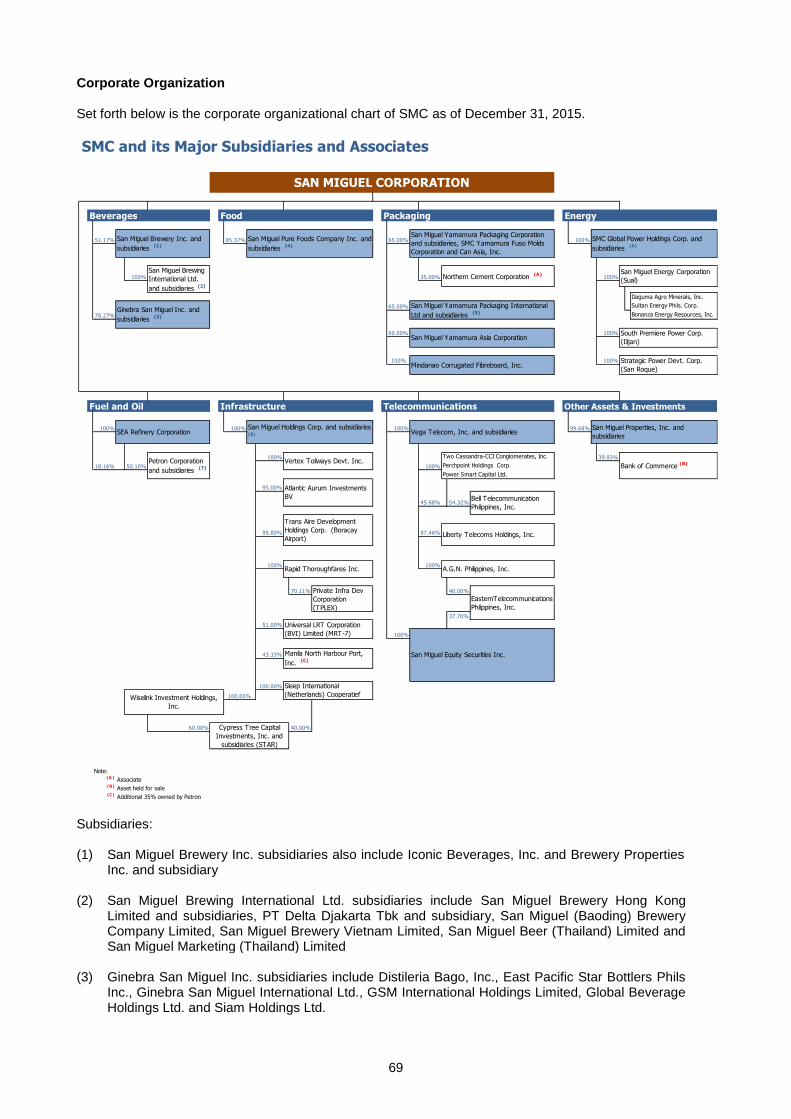

Brief Background on the Company San Miguel Corporation (“SMC”, the “Company”, the “Parent Company”, or the “Issuer”), together with its subsidiaries (collectively with the Company referred to as the “SMC Group”), is one of the largest and most diversified conglomerates in the Philippines by revenues and total assets, with sales of about 6.2% of the Philippine gross domestic product in 2014. Originally founded in 1890 as a single brewery in the Philippines, SMC has transformed itself from a market-leading beverage, food and packaging business with a globally recognized beer brand, into a diversified conglomerate with market-leading businesses and investments in the fuel and oil, energy, infrastructure, telecommunications and banking industries. SMC owns a portfolio of companies that is tightly interwoven into the economic fabric of its home market, benefiting from and contributing to the development and economic progress of the Philippines. The common shares of SMC were listed on November 5, 1948 at the Manila Stock Exchange, now The Philippine Stock Exchange, Inc. In 2007, in light of the opportunities presented by the global financial crisis, the ongoing program of asset and industry privatization of the Philippine government, the strong cash position of SMC enhanced by recent divestments and the strong cash flow generated by its established businesses, SMC adopted an aggressive business diversification program. The program channeled the resources of SMC into what it believes were attractive growth sectors, aligned with the development and growth of the Philippine economy. SMC believes this strategy will achieve a more diverse mix of sales and operating income, and better position for SMC to access capital, present different growth opportunities and mitigate the impact of downturns and business cycles. Since January 2008 up to the third quarter of 2015, SMC has either directly or through its subsidiaries, made a series of acquisitions in the fuel and oil, energy, infrastructure, telecommunications and banking industries. A summary of these transactions is set forth below:

acquired 68.26% equity interest in Petron Corporation (“Petron”)

acquired the rights, pursuant to Independent Power Producer Administrator (“IPPA”) agreements with Power Sector Assets and Liabilities Management Corporation (“PSALM”) to administer three (3) power plants in Sual and San Roque in Pangasinan and Ilijan in Batangas

made the following infrastructure acquisitions:

– initial 35.0% equity interest in Private Infra Dev Corporation (“PIDC”), which is now at 70.11%

– initial 93.4% equity interest in Trans Aire Development Holdings Corp. (“TADHC”, formerly known

as Caticlan International Airport Development Corporation), which is now at 99.80% of the total

outstanding common shares of TADHC

– 51.0% equity interest In Universal LRT Corporation (BVI) Limited (“Universal LRT”)

– initial 46.53% equity interest In Atlantic Aurum Investments BV (“AAIBV”), which is now at 95.0%

made the following telecommunications acquisitions:

– initial 41.48% equity interest in Liberty Telecommunications Holdings, Inc. (“Liberty Telecom”),

which is now at 97.46% of the total issued and outstanding shares of Liberty Telecom

13

– 100.0% equity interest in Bell Telecommunication Philippines, Inc. (“BellTel”), a 100.0% equity

interest in A.G.N. Philippines, Inc. (“AGNP”), which holds 40.0% interest in Eastern

Telecommunications Philippines, Inc. (“Eastern Telecom”) and 37.7% equity interest in Eastern

Telecom through its wholly-owned subsidiary, San Miguel Equity Securities, Inc. (“SMESI”),

bringing its total indirect equity interest in Eastern Telecom to 77.7%

acquired 100.0% equity interest in each of the three (3) concession holders of coal deposits in the

Southern Mindanao region – namely, Daguma Agro Minerals, Inc. (“Daguma”), Bonanza Energy

Resources, Inc. (“Bonanza Energy”) and Sultan Energy Phils. Corp. (“Sultan Energy”)

acquired initially 30.0% in Bank of Commerce (“BOC”), which is now at 39.93%

SMC, through its subsidiaries and affiliates, has become a Philippine market leader in its businesses with 20,488 regular employees and more than 100 production facilities in the Asia-Pacific region as of September 30, 2015. The extensive portfolio of SMC products includes beer, liquor, non-alcoholic beverages, poultry, animal feeds, flour, fresh and processed meats, dairy products, coffee, various packaging products and a full range of refined petroleum products, most of which are market leaders in their respective markets. In addition, the SMC Group contributes to the growth of downstream industries and sustains a network of hundreds of third party suppliers.

Through the partnerships it has forged with major international companies, the SMC Group has gained access to the latest technologies and expertise, thereby enhancing its status as a world-class organization.

SMC has strategic partnerships with international companies, among them are Kirin Holdings Company, Limited (“Kirin”) for beer, Hormel Foods International Corporation (“Hormel”) for processed meats, Nihon Yamamura Glass Company, Ltd. (“NYG”) for packaging products, Padma Fund L.P. (“Padma”) for toll roads and Super Coffee Corporation Pte Ltd for coffee. Major developments in the SMC Group are discussed in Management’s Discussion and Analysis of Financial Position and Performance, found on page 174.

Core Businesses Beverages San Miguel Brewery Inc. (“SMB”) is primarily engaged in the manufacture and sale of fermented and malt-based beverages, particularly beer of all kinds and classes. SMB has six (6) production facilities in the Philippines strategically located in Luzon, Visayas and Mindanao and operates one (1) brewery each in Hong Kong, Indonesia, Vietnam, Thailand, and two (2) breweries in China. In addition, SMB has recently acquired the non-alcoholic beverage business. The SMC Group also produces hard liquor through its majority-owned subsidiary, Ginebra San Miguel, Inc. (“Ginebra”). Ginebra is one of the largest gin producers in the world by volume with some of the most recognizable brands in the Philippine liquor market. It operates one (1) distillery, five (5) liquor bottling plants and one (1) cassava starch milk plant, and has engaged two (2) toll bottlers strategically located throughout the Philippines and one (1) bottling and distillery plant in Thailand. Food The food operations of SMC holds numerous market-leading positions in the Philippine food industry, offering a wide range of high-quality food products and services to household, institutional and foodservice customers. The food business is conducted through San Miguel Pure Foods Company, Inc. (“San Miguel Pure Foods”). In addition to its Philippine operations, the food business also has a presence in Indonesia and Vietnam. San Miguel Pure Foods has some of the most recognizable brands in the Philippine food industry, including Magnolia for chicken, ice cream and dairy products, Monterey for fresh and marinated meats, Purefoods for refrigerated processed meats and canned meats, Star and Dari Crème for margarine, San Mig Super Coffee for coffee, La Pacita for biscuits and B-Meg for animal feeds.

14

Packaging The packaging business is a total packaging solutions business servicing many of the leading food, pharmaceutical, chemical, beverages, spirits and personal care manufacturers in the region. The packaging business is comprised of San Miguel Yamamura Packaging Corporation (“SMYPC”), San Miguel Yamamura Packaging International Limited (“SMYPIL”), San Miguel Yamamura Asia Corporation (“SMYAC”), SMC Yamamura Fuso Molds Inc. (“SYMFC”), Can Asia, Inc. (“CAI”) and Mindanao Corrugated Fibreboard, Inc (“Mincorr”), collectively referred to as the Packaging Group. The Packaging Group has one of the largest packaging operations in the Philippines, producing glass, metal, plastic, aluminum cans, paper, flexibles, PET (Polyethylene Terephthalate) and other packaging products and services such as beverage tolling for PET bottles and aluminum cans. The packaging business is the major source of packaging requirements of the other business units of SMC. It also supplies its products to customers across the Asia-Pacific region, the United States, South Africa, Australia and the Middle East, as well as to major multinational corporations in the Philippines, including Coca-Cola Femsa Philippines, Inc., Nestle Philippines and Pepsi Cola Products Philippines, Inc. The Packaging Group has 13 international packaging facilities located in China (glass, plastic and paper packaging products), Vietnam (glass and metal), Malaysia (composite, plastic films, woven bags and a packaging research center) and Australia (glass, trading, wine closures and bottle caps) and New Zealand (plastics and trading). Aside from extending the reach of the packaging business overseas, these facilities also allow the Packaging Group to serve the packaging requirements of SMB breweries in China, Vietnam, Indonesia and Thailand. Properties San Miguel Properties Inc. (“SMPI”) was created in 1990 initially as the corporate real estate arm of SMC. It is the primary property subsidiary of the SMC Group, currently 99.68% owned by SMC. SMPI is presently engaged in commercial property development, sale and lease of real properties, management of strategic real estate ventures and corporate real estate services.

New Businesses Fuel and Oil SMC operates its fuel and oil business through Petron, which is involved in refining crude oil and marketing and distribution of refined petroleum products mainly in the Philippines and Malaysia. Petron is the number one integrated oil refining and marketing company in the Philippines, with a market share of 35.4% as of December 2014, according to the Department of Energy of the Philippines (“DOE”). Petron participates in the reseller (service station), industrial, lube and liquified petroleum gas (“LPG”) sectors. In addition, Petron is also engaged in non-fuels business by earning income from billboards and locators, which are largely situated within the premises of the service stations. In Malaysia, Petron holds a 17.1% share of the retail market as of September 30, 2015, based on Petron estimates and information from Fahrenheit Research (M) Sdn. Bhd (“Fahrenheit Research”), the market research consultant appointed by Malaysian retail market participants to compile industry data. Petron owns and manages the most extensive oil distribution infrastructure with 30 depots, terminals and airport installations and approximately 2,200 retail service stations in the Philippines and ten (10) product terminals and more than 560 retail service stations in Malaysia. Petron also exports various petroleum products and petrochemical feedstock, including naphtha, mixed xylene, benzene, toluene and propylene, to customers in the Asia-Pacific region. Petron owns and operates a petroleum refining complex, with a capacity of 180,000 barrels per day located in Limay, Bataan Philippines. The refinery has its own piers and two (2) offshore berthing facilities. In 2010, Petron upgraded its refinery by undertaking the Petron Bataan Refinery Master Plan Phase-2 Upgrade (“RMP-2”) which was completed in 2014. RMP-2 upgraded the Petron Bataan Refinery to a full conversion refining complex, where all its fuel oil production is converted to higher value products – gasoline, diesel, jet fuel and petrochemicals, making it comparable to highly complex refineries worldwide. The completion of RMP-2 made Petron the only oil company in the Philippines capable of producing Euro IV-standard fuels,

15

the global clean air standards for fuels. Petron also has a refinery in Malaysia with a capacity of 88,000 barrels per day. Energy The energy business, which is conducted through SMC Global Power Holdings Corp. (“SMC Global Power”), is one of the leaders in the Philippine power generation industry in terms of installed capacity. SMC Global Power administers three (3) power plants, located in Sual, Pangasinan (coal), Ilijan, Batangas (natural gas) and San Roque, Pangasinan (hydroelectric), with a combined capacity of 2,545 MW, pursuant to the IPPA agreements with PSALM and National Power Corporation of the Philippines (“NPC”). SMC Global Power began acting as an IPPA of the Sual power plant in November 2009, the San Roque power plant in January 2010 and the Ilijan power plant in June 2010. SMC Global Power sells power through off take agreements either directly to customers, including Manila Electric Company and other distribution utilities, electric cooperatives and industrial customers, or through the Philippine Wholesale Electricity Spot Market (“WESM”).

In September 2013, SMC Powergen Inc. (“SPI”), a subsidiary of SMC Global Power, acquired the 2 x 35 MW co-generation solid fuel fired plant of Petron located in Limay, Bataan. The plant added 140 MW to the total capacity of SMC Global Power. During the same period, SMC Global Power was awarded the winning concessionaire for the rehabilitation, operations and maintenance of Albay Electric Cooperative (“ALECO”), located in Albay, Bicol. A new subsidiary, Albay Power and Energy Corp. (“APEC”) was created for this purpose. In 2013, San Miguel Consolidated Power Corporation broke ground on the new coal-fired power plant in Malita, Davao and SMC Consolidated Power Corporation on another coal-fired power plant in Limay, Bataan, both of which will have an initial capacity of 300 MW each. These power plants are expected to be commercially available by 2016. In 2014, PowerOne Ventures Energy Inc. (“PVEI”), a subsidiary of SMC Global Power, and Korea Water Resources Corporation (“K-Water”) entered into a joint venture partnership for the acquisition, rehabilitation, operation and maintenance of the 218 MW Angat Hydroelectric Power Plant (“AHEPP”) awarded by PSALM to K-Water. This brought total installed capacity of SMC Global Power to 2,903 MW. As of September 30, 2015, SMC Global Power is one of the largest power companies in the Philippines, which holds a 22.2% market share of the total installed power generation capacity for the Luzon power grid and a 16.5% market share of the national grid according to the Energy Regulatory Commission of the Philippines (“ERC”). SMC Global Power, through San Miguel Energy Corporation (“SMEC”), likewise owns three (3) coal mining companies which are concession holders of coal deposits in Southern Mindanao. Infrastructure The infrastructure business, conducted through San Miguel Holdings Corp. (“SMHC”), consists of investments in companies that hold long-term concessions in the infrastructure sector in the Philippines. Current operating tollroads include the Tarlac-Pangasinan-La Union Toll Expressway (“TPLEX”), South Luzon Expressway (“SLEX”), Skyway Stage 1 and 2 and the Southern Tagalog Arterial Road (“STAR”) tollways and ongoing tollroad projects are the NAIA Expressway (“NAIAx”) and the Skyway Stage 3. It also operates and is currently expanding Boracay Airport. In addition, it has the concession right to construct, operate and maintain the Mass Rail Transit Line 7 (“MRT-7”). TPLEX SMHC, through its subsidiary, Rapid Thoroughfares, Inc. (“Rapid”), owns a 70.11% equity interest in PIDC. PIDC is a company which holds a 35-year Build-Transfer-Operate (“BTO”) concession rights to construct, operate and maintain an 88.85 km toll expressway from La Paz, Tarlac, through Pangasinan, to Rosario, La Union.

16

Boracay Airport SMC, through the 99.80% interest of SMHC in TADHC, is undertaking the expansion of Boracay Airport under a 25-year Build-Rehabilitate-Operate-Transfer (“BROT”) concession granted by the Republic of the Philippines (“ROP”), through the Department of Transportation and Communications of the Philippines (“DOTC”). STAR Tollway SMHC, through Cypress Tree Capital Investments, Inc. (“CTCII”) has an effective 100.0% interest in Star Infrastructure Development Corporation (“SIDC”). SIDC holds the 30-year BTO concession rights of the STAR Project consisting of: Stage 1 - operation and maintenance of the 22.16 km toll road from Sto. Tomas to Lipa City; and Stage 2 - financing, design, construction, operation and maintenance of the 19.74 km toll road from Lipa City to Batangas City.

NAIAx

On May 31, 2013, SMHC incorporated Vertex Tollways Devt. Inc. (“Vertex”), a company that holds the 30-year BTO concession rights for the construction and operation of the NAIA Expressway (“NAIAx”) – a four (4) lane elevated expressway with end-to-end distance of 5.4 km that will provide access to NAIA Terminals 1, 2 and 3. NAIAx will connect to the Skyway system, the Manila-Cavite Toll Expressway (“CAVITEX”) and the Entertainment City of the Philippine Amusement and Gaming Corporation (“PAGCOR”). SLEX / Skyway Stage 1 and 2 On March 5, 2015, SMHC increased its shareholdings in AAIBV to 95.0% stake in AAIBV. AAIBV has the following shareholdings:

80.0% stake in South Luzon Tollway Corporation (“SLTC”), through MTD Manila Expressways, Inc. (“MTDME”), a wholly-owned subsidiary of AAIBV. SLTC holds a 30-year concession rights to operate the 36.1 km South Luzon Expressway (“SLEX”), one of the three (3) major expressways that link Metro Manila to Southern Luzon;

87.84% beneficial ownership in Citra Metro Manila Tollways Corporation (“CMMTC”), through Atlantic Aurum Investments Philippines Corporation (“AAIPC”), a wholly-owned subsidiary of AAIBV. CMMTC holds a 30-year concession to construct, operate and maintain the 29.59 km Skyway Stage 1 and 2 Project.

Skyway Stage 3

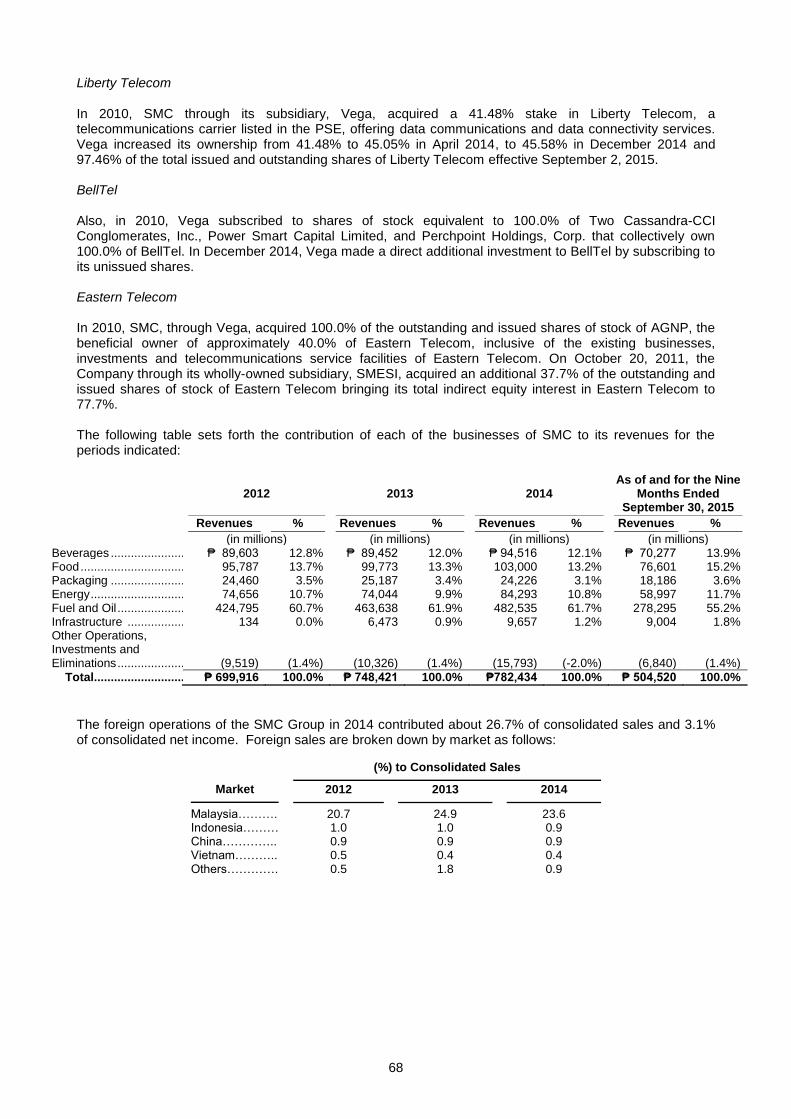

On February 28, 2014, SMHC through AAIBV incorporated Stage 3 Connector Tollways Holdings Corp. (“S3HC”), which holds an 80.0% ownership interest in Citra Central Expressway Corp. (“CCEC”). CCEC holds a 30-year concession to construct, operate, and maintain the Skyway Stage 3, an elevated roadway with the entire length of approximately 14.82 km from Buendia Avenue in Makati to Balintawak, Quezon City and will connect to the existing Skyway Stage 1 and 2. This is envisioned to inter-connect the southern and northern areas of Metro Manila to help decongest traffic in Metro Manila and stimulate the growth of trade and industry in Luzon, outside of Metro Manila. MRT-7 In October 2010, SMC, through SMHC, acquired a 51.0% stake in Universal LRT, which holds the 25-year Build-Gradual Transfer-Operate-Maintain (“BGTOM”) concession for MRT-7. MRT-7 is a planned expansion of the metro rail system in Manila which mainly involves the construction of 22 km mass rail transit system with 14 stations that will start from San Jose del Monte City and end at the integrated LRT-1 / MRT-3 / MRT-7 station at North EDSA and a 22 km six (6) lane asphalt highway that will connect the North Luzon Expressway to the intermodal transport terminal in San Jose del Monte City, Bulacan and a 22-km road component from San Jose del Monte City, Bulacan to the Bocaue exit of the NLEX. Telecom SMC has made investments in the telecommunications sector in the Philippines through acquisitions of stakes in Liberty Telecom, BellTel and Eastern Telecom.

17

Liberty Telecom

In 2010, SMC through its subsidiary, Vega Telecom Inc. (“Vega”), owns a 41.48% stake in Liberty Telecom, a telecommunications carrier listed in The Philippine Stock Exchange, Inc., offering data communications and data connectivity services. Vega increased its ownership from 41.48% to 45.05% in April 2014,to 45.58% in December 2014 and 97.46% of the total issued and outstanding shares of Liberty Telecom effective September 2, 2015. BellTel Also, in 2010, Vega subscribed to the shares of stock equivalent to 100.0% of Two Cassandra-CCI Conglomerates, Inc., Power Smart Capital Limited, and Perchpoint Holdings, Corp. that collectively owns 100.0% of BellTel. In December 2014, Vega made a direct additional investment to BellTel by subscribing to its unissued shares.

BellTel, which began commercial operations in 2002, offers an integrated package of services, including local and long distance telephony, high speed data connectivity and Internet. It has various licenses that include local exchange carrier, international gateway facility, inter-exchange carrier, very small aperture terminal, internet service provider, and wireless local loop telephone systems in various cities and municipalities in the National Capital Region of the Philippines (“NCR”). It is authorized to provide the full range of services throughout the Philippines. In 2014, BellTel acquired 100.0% of Dominer Pointe, Inc. and Somete Logistics & Dev’t. Corp. from various individuals. Both tower companies are engaged in the business of conceptualization, construction, installation, establishment, operation, leasing, sale and maintenance, and rendering of specialty technical services for tower infrastructures to be utilized by telecommunication companies.

Eastern Telecom

In 2010, SMC, through Vega, acquired 100.0% of the outstanding and issued shares of stock of AGNP, the beneficial owner of approximately 40.0% of Eastern Telecom, inclusive of the existing businesses, investments and telecommunications service facilities of Eastern Telecom. On October 20, 2011, the Parent Company through its wholly-owned subsidiary, SMESI, acquired an additional 37.7% of the outstanding and issued shares of stock of Eastern Telecom bringing its total indirect equity interest in Eastern Telecom to 77.7%.

Established more than 130 years ago, Eastern Telecom offers a full range of telecommunication services, including internet, data, voice and certain value added services. Eastern Telecom is a provider of voice, data and internet services to the business process outsourcing market.

Competitive Strengths SMC believes that its principal strengths include the following: Diversified platform with broad exposure to the Philippine economy The Philippines has become one of the fastest growing economies in Asia, with consecutive annual positive gross domestic product growth since 1999. According to the Association of South East Asian Nations (“ASEAN”) briefing, the Philippines announced a gross domestic product growth of 6.1% in 2014, the second (2

nd) highest in the Asia-Pacific region. According to the International Monetary Fund (“IMF”), the Philippines

is expected to experience gross domestic product growth at the rate of 6.0% and 6.2% for 2016 and 2017, respectively. In addition, the Philippine population is young, comparably literate and growing, which provides the Philippine economy with favorable demographics for further growth. As one of the largest conglomerates in the Philippines by revenues and total assets, with sales of about 6.2% of the Philippine gross domestic product in 2014, the SMC Group is broadly exposed to the Philippine economy through its diverse range of businesses spanning the beverage, food, packaging, fuel and oil, energy, infrastructure, telecommunication, property, and banking industries. This diversified portfolio aligns SMC to key sectors that it believes will benefit from the forecast growth of the Philippine economy.

18

Market leading positions in key Philippine industries Many of the businesses of SMC are leaders in their domestic markets.

Beverages: The domestic beer business of SMC has consistently dominated the Philippine beer market, with a market share of 90.0% by volume in 2012, according to Canadean data, with no significant changes thereafter. SMB has held this position since 1999. SMC also produces some of the most recognizable brands in the Philippine liquor market. It also has a growing non-alcoholic beverage business which produces non-carbonated ready to drink teas, fruit juices and water. Food: San Miguel Pure Foods is a leading Philippine food company with market-leading positions in key food categories and offers a broad range of high-quality food products and services to household, institutional and foodservice customers. Based on data from certain Philippine government agencies and its own internal assumptions and calculations, San Miguel Pure Foods believes it has market shares of 38.0% for poultry, 40.0% for fresh meats (based on sow population of large commercial farms), and 43.0% for animal feeds, in each case as of December 2014 and 16.0% for flour as of September 30, 2015. According to Kantar Worldpanel, San Miguel Pure Foods has a market share of 58.0% for hotdogs sold in Philippine supermarkets, 84.0% in the chicken nugget product category, and market shares of 42.0% for butter, 97.0% for refrigerated margarine, in each case based on value as of September 2015. According to Nielsen, San Miguel Pure Foods has a 97.0% market share for non-refrigerated margarine and 20.0% market share for cheese as of August 2015. San Miguel Pure Foods has continuously enhanced brand recognition and trust with consumers by consistently maintaining high product quality, as well as through active and targeted advertising and promotional campaigns. Packaging: The packaging business is one of the largest packaging operations in the Philippines, producing glass, metal, plastic, aluminum cans, paper, flexibles, PET and other packaging products. The packaging business is the major source of packaging requirements of the other businesses of SMC. It also supplies its products to major multinational corporations in the Philippines and customers across the Asia-Pacific region, the United States, Africa, Australia and the Middle East. Fuel and oil: Petron refines crude oil and markets and distributes refined petroleum products in the Philippines and Malaysia. In the Philippines, Petron is the number one integrated oil refining and marketing company, with an overall market share of 35.4% of the Philippine oil market in terms of sales volume based on industry data from the DOE as of December 2014. Petron also has a 17.1% share of the Malaysian retail market as of September 30, 2015, according to Petron and Farenheit Research estimates. Energy: SMC Global Power is one of the largest IPPAs in the Philippines, holding a 22.2% market share of the total installed capacity of the Luzon power grid and a 16.5% market share of the national grid as of September 30, 2015, according to the ERC. SMC Global Power administers three (3) power plants, located in Sual, Pangasinan (coal-fired), Ilijan, Batangas (natural gas) and San Roque, Pangasinan (hydroelectric) and owns the power plant in Limay, Bataan (coal co-generation). In addition, SMC also owns 60.0% interest in the AHEPP. This brings total combined capacity of SMC Global Power to 2,903 MW. The energy trading team of SMC comprises of pioneers in WESM trading. Infrastructure: SMHC has become one of the major infrastructure companies in the country, with concessions in toll roads, airport and mass rail transit. SMHC has rights to about 52.7% of the total road length of awarded toll road projects. This includes operating toll roads such as TPLEX, SLEX, Skyway Stages 1 and 2 and STAR tollways while ongoing projects include NAIAx and Skyway Stage 3. SMHC also operates the Boracay Airport which is currently doing improvement and expansion activities that will take advantage of the growing number of tourists in the area. In addition, SMHC holds the concession to construct, operate and maintain the MRT-7 project, a 22-km rapid mass rail transit system, which spans from North EDSA to San Jose del Monte City, Bulacan, and a 22-km road component from San Jose del Monte City, Bulacan to the Bocaue exit of the NLEX.

Experienced management team SMC has an extensive pool of experienced managers who have been with SMC for more than 20 years. The management team has a deep knowledge and understanding of the Philippine operating environment and has been able to effectively manage SMC through periods of crisis and instability in the Philippines. In addition, the management team has successfully directed the diversification strategy of SMC, including retaining key management personnel from acquired companies in order to maintain their expertise and leverage their industry experience.

19

Operating businesses provide sustainable stream of income and cash flows The beverage, food and packaging businesses provide SMC with a sustainable stream of income. These businesses demonstrated resilience during the global financial crisis and provided SMC with a strong financial base from which to pursue its recent diversification strategy. In 2014, the core businesses of beverage, food and packaging businesses provided 28.3% of total SMC sales and 43.9% of total SMC EBITDA. For the period ending September 30, 2015, core businesses provided 32.2% of total SMC sales and 37.6% of total SMC EBITDA. For the period ending September 30, 2015, SMC generated ₱77,466 million of EBITDA and ₱6,167 million of net income attributable to the Parent Company with ₱43,983 million of capital expenditure. In 2014, SMC generated ₱88,096 million of EBITDA and ₱14,692 million of net income attributable to the Parent Company with ₱38,951 million of capital expenditure. In 2013, it generated ₱77,283 million of EBITDA and ₱38,053 million of net income attributable to the Parent Company with ₱65,865 million of capital expenditure. In 2012, it generated ₱76,626 million of EBITDA and ₱26,806 million of net income attributable to the Parent Company with ₱52,917 million of capital expenditure. Well-positioned for significant future growth SMC is well-positioned for significant future growth. The established businesses of SMC in beverage, food and packaging continue to provide stable cash flow, while its new businesses have enabled the Company to expand its ability to generate higher returns.

Beverage: The beverage business is well-positioned to benefit from the increasing affluence and population growth in the Philippines, which the Company believes present significant opportunities in the premium beer market. In addition, the international beer business of SMC is experiencing increased sales through growing brand recognition in selected overseas markets such as Indonesia, Thailand, Singapore, Hong Kong, the Middle East, US and Asia-Pacific region. SMC is expanding its liquor business throughout the Philippines and internationally. SMC plans to create rapid deployment task forces, particularly in the southern Philippines, where market penetration is low and where there is no existing dealership system. With the transfer of the non-alcoholic beverage business from Ginebra to SMB, SMC believes that the strong distribution infrastructure of SMB will be able to increase margins and improve profitability of the beverage business as a whole. The beverage business continues to introduce new products and new package formats to increase consumer interest and overall market size, as well as address the needs of an increasingly fragmenting market, especially in high growth segments. Food: The food business aims to become the least-cost producer through its vertically-integrated meats business model, which allows it to secure stable raw material supply and develop cheaper alternative raw materials. San Miguel Pure Foods is also streamlining its operations to improve the profitability of its established business segments, such as poultry, feeds, meats and flour, maximize synergies across operations, and improve margins by shifting to stable-priced and value-added products. Packaging: The packaging business aims to provide a total packaging solution to be able to serve a wide spectrum of customers thereby increasing its potential for higher growth. It also aims to benefit from trade liberalization and globalization in the ASEAN region as it further expands its exports market. The rising environmental awareness also provides opportunities for the production of more environmentally friendly products such as heavy metal-free paint glass and recycled PET resin. The packaging business plans to improve margins by developing alternative sources of raw materials and optimizing recycling efforts to lower its material costs. Fuel and Oil: Petron operates as an integrated oil refining and marketing company in the Philippines and Malaysia, both of which it believes have favorable oil industry dynamics. The Philippines operates under a free market scheme with movements in regional prices and foreign exchange reflected in the pump prices on a weekly basis. Malaysia, on the other hand, operates under a regulated environment and implements an automatic pricing mechanism that provides stable returns to fuel retailers. Petron owns refineries, in both the Philippines and Malaysia, capable of producing finished petroleum products. Petron believes it has the competitive advantage against other oil players that only import finished petroleum products. Petron plans to continue its service station network expansion and seek growth in complementary non-fuel businesses. Petron also increased its production of higher margin

20

products with the completion of RMP-2. The RMP-2 is the second phase of a refinery expansion project, which includes further enhancements to its operational efficiencies, increase in conversion capability and reduce production of lower-value products. In addition to RMP-2 and the expansion of the service station network, Petron is operating the new coal Co-generation power plant to supply the power requirements of the Limay Refinery that replaced some of the existing turbo and steam generators. The new coal Co-generation power plant is utilizing more efficient technology and generating power at lower costs. Energy: SMC Global Power is expanding its power generating capacity over the next five (5) years and believes its energy business will benefit from growing demand for electricity in the Philippines, which is forecasted to exceed the growth rates of the Philippine gross domestic product, and the shortage in electricity supply, with the industry constrained by aging power generation assets and minimal additional capacities. Also, if spot electricity rates move higher as a result of increased demand, the margins of SMC Global Power are expected to increase. Infrastructure: SMHC believes there are significant opportunities in building or acquiring infrastructure assets in a growing economy that has historically under-invested in infrastructure. In addition, concession agreements for the various projects will provide strong and stable long-term income streams, as well as serve as a barrier to entry to new players to the business. Telecom: SMC believes its investments in the telecommunications industry provide the Company with an opportunity to participate in a high growth industry as the Philippine population becomes more affluent and spends more on higher margin services. In particular, SMC is currently refining its telecommunications business strategy, where it plans to take advantage of opportunities in digitization of businesses, the emergence of mobile platforms for businesses and the provision of services to consumers. Moreover, the three (3) telecom companies of SMC have a wide bandwidth of spectrum that would enable SMC to be competitive in both current (2G/3G/4G) and future technologies.

Synergies across businesses SMC expects significant opportunities to develop and increase synergies across many of its businesses, including:

Ancillary business opportunities: SMC believes it has opportunities within its existing businesses to secure growth in its new businesses by using the relevant areas to conduct business and activities. Potential initiatives of this type include installing SMC Group advertisements, building service stations, retail outlets, rest stops and kiosks along toll roads.

Immediate distribution channel: The extensive retail distribution network of SMC provides an effective platform for roll-out of new products and services. For example, the network of Petron service stations provides an immediate distribution channel for retail sales for the beverage and food products of SMC. Economies of scale: SMC believes the size and scale of its distribution network operations will provide significant economies of scale and synergies in production, research and development, distribution, management and marketing. The size and scale of SMC should also result in substantial leverage and bargaining power with suppliers and retailers. Integration: SMC plans to continue pursuing vertical integration across the established and strategic businesses, such as supplying the fuel and oil and power requirements of its businesses internally.

Business Strategies of SMC The principal strategies of SMC include the following: Enhance value of established businesses SMC aims to enhance the value of its established businesses by pursuing operational excellence, brand enhancement, improving product visibility, targeting regions where SMC has lower market share, implementing pricing strategies and pursuing efficiencies.

21

Continue to diversify into industries that underpin the development and growth of the Philippine economy In addition to organic growth, SMC intends to continue to seek strategic acquisition opportunities to position itself for the economic growth and industrial development of the Philippines. Identify and pursue synergies across businesses through vertical integration, platform matching and channel management SMC intends to create an even broader distribution network for its products and expand its customer base by identifying synergies across its various businesses. In addition, SMC is pursuing plans to integrate its production and distribution facilities for its established and newly acquired businesses to enable additional cost savings and efficiencies. Invest in and develop businesses with leading market positions SMC intends to further enhance its market position in the Philippines by leveraging its financial resources and experience to continue introducing innovative products and services. Potential investments to develop existing businesses include constructing new power plants and expanding its power generation portfolio, building additional service and micro-filling stations and expanding distribution networks for its beverage and food products. SMC believes its strong domestic market position and brand recognition provide an effective platform to develop markets for its expanding product portfolio. SMC plans to continue to invest in and develop businesses it believes have the potential to gain leading positions in their respective markets. Adopt world-leading practices and joint development of businesses SMC continues to develop strategic partnerships with global industry leaders, such as Kirin for beer, Hormel for processed meats and NYG for packaging products. These partnerships provide marketing and expansion opportunities.

Risks of Investing Prospective investors should also consider the following risks of investing in the Offer Shares: 1. Macroeconomic risks, including the current and immediate political and economic factors in the

Philippines and the experience of the country with natural catastrophes, as a principal risk for investing in general;

2. Risks relating to SMC, its subsidiaries and their business and operations; and

3. The nature of the Offer Shares as perpetual securities, the absence of a liquid secondary market and volatility of the Offer Shares and other risks relating to the Offer Shares.

(For a more detailed discussion, see “Risk Factors” on page 39)

Use of Proceeds The Offer Price shall be at ₱75.00. Out of the gross proceeds, SMC shall deduct fees, commissions, and expenses, for each tranche of the Offer. The use of proceeds for each tranche of the Offer will be set out in the relevant Offer Supplement.

Offer Supplement

For each tranche of the Offer, the Company shall distribute a supplement (the “Offer Supplement”) which shall be disclosed to the public through the filing with the SEC and the PSE and made available for download from the website of SMC specifically, in http://www.sanmiguel.com.ph.

The Offer Supplement shall contain the following information: (a) timetable, offer size of the specific offering, the applicable dividend rate and the mode of

settlement of the offering; (b) capital structure of the Company after the offering; (c) any changes to the risk factors and tax consequences of the offering;

22

(d) description of the specific distribution and underwriting arrangements; and (e) amount and use of proceeds.

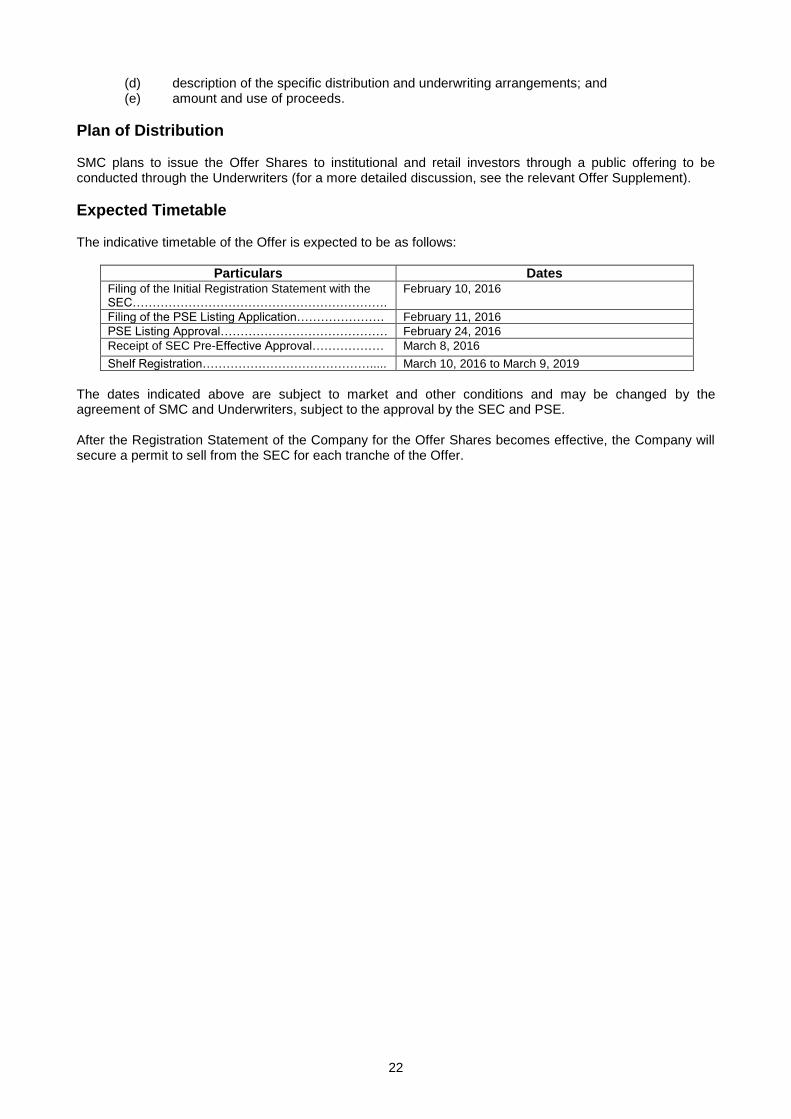

Plan of Distribution SMC plans to issue the Offer Shares to institutional and retail investors through a public offering to be conducted through the Underwriters (for a more detailed discussion, see the relevant Offer Supplement).

Expected Timetable The indicative timetable of the Offer is expected to be as follows:

Particulars Dates Filing of the Initial Registration Statement with the SEC……………………………………………………….

February 10, 2016

Filing of the PSE Listing Application…………………. February 11, 2016

PSE Listing Approval…………………………………… February 24, 2016

Receipt of SEC Pre-Effective Approval……………… March 8, 2016

Shelf Registration……………………………………..... March 10, 2016 to March 9, 2019

The dates indicated above are subject to market and other conditions and may be changed by the agreement of SMC and Underwriters, subject to the approval by the SEC and PSE. After the Registration Statement of the Company for the Offer Shares becomes effective, the Company will secure a permit to sell from the SEC for each tranche of the Offer.

23

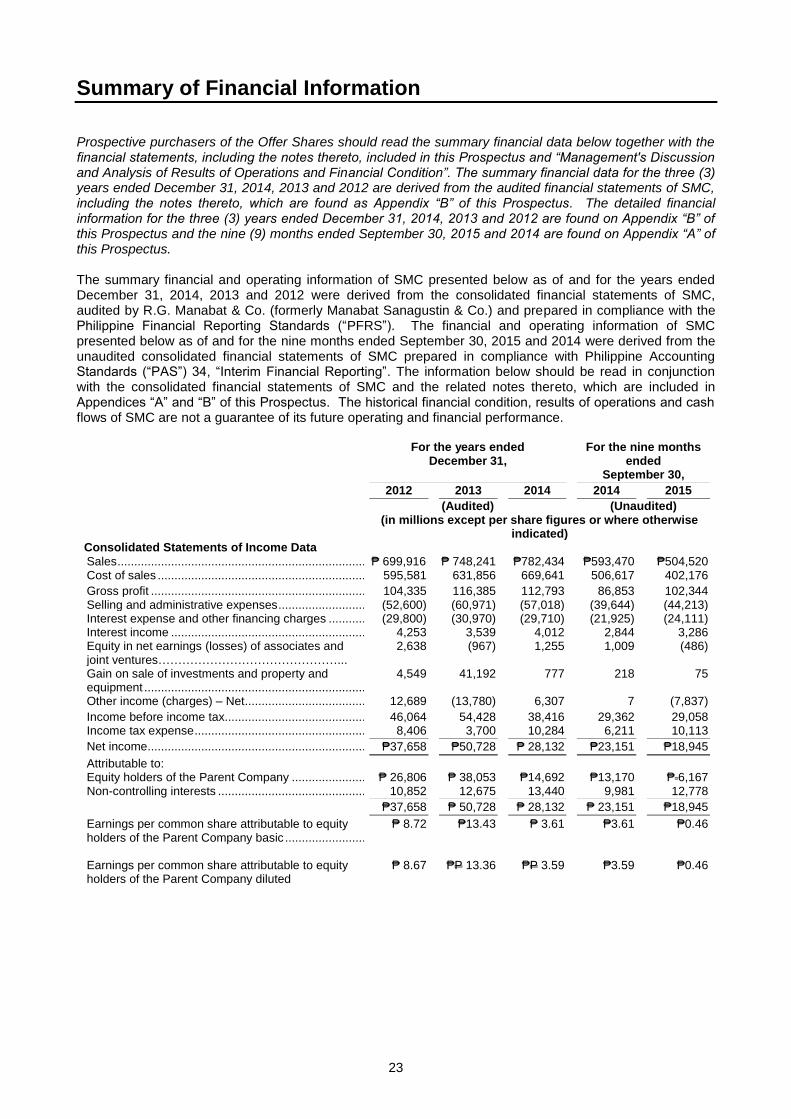

Summary of Financial Information

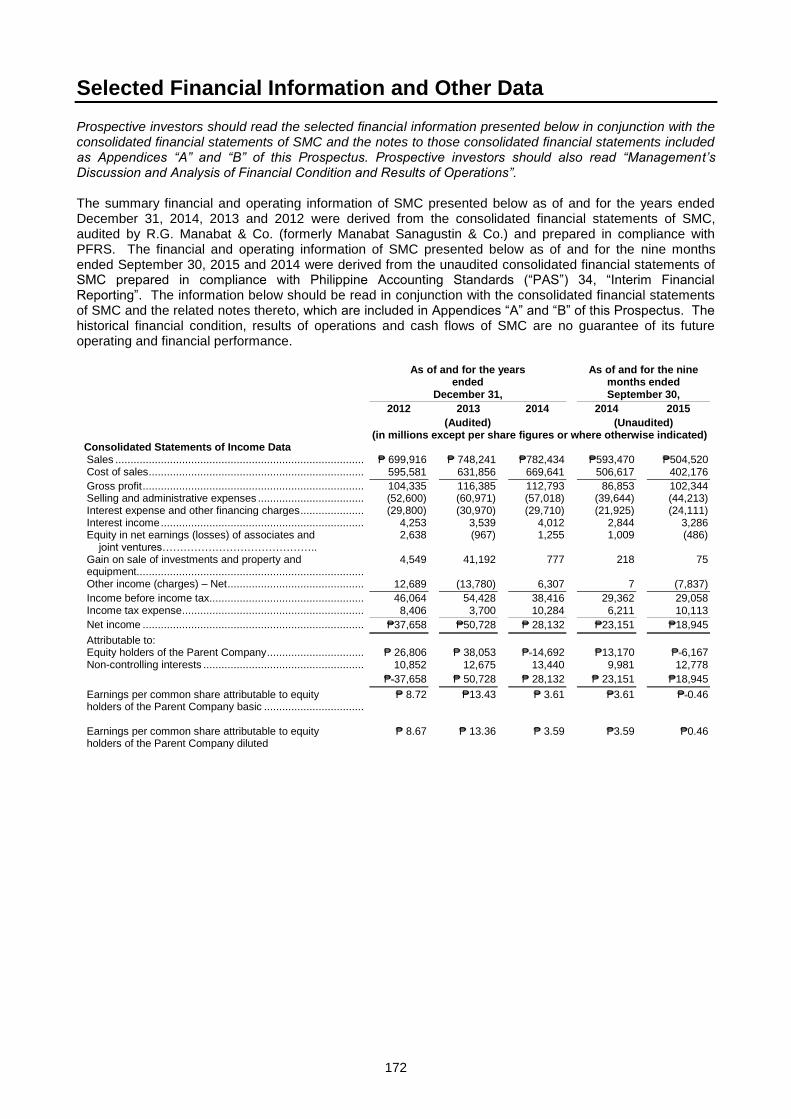

Prospective purchasers of the Offer Shares should read the summary financial data below together with the financial statements, including the notes thereto, included in this Prospectus and “Management's Discussion and Analysis of Results of Operations and Financial Condition”. The summary financial data for the three (3) years ended December 31, 2014, 2013 and 2012 are derived from the audited financial statements of SMC, including the notes thereto, which are found as Appendix “B” of this Prospectus. The detailed financial information for the three (3) years ended December 31, 2014, 2013 and 2012 are found on Appendix “B” of this Prospectus and the nine (9) months ended September 30, 2015 and 2014 are found on Appendix “A” of this Prospectus. The summary financial and operating information of SMC presented below as of and for the years ended December 31, 2014, 2013 and 2012 were derived from the consolidated financial statements of SMC, audited by R.G. Manabat & Co. (formerly Manabat Sanagustin & Co.) and prepared in compliance with the Philippine Financial Reporting Standards (“PFRS”). The financial and operating information of SMC presented below as of and for the nine months ended September 30, 2015 and 2014 were derived from the unaudited consolidated financial statements of SMC prepared in compliance with Philippine Accounting Standards (“PAS”) 34, “Interim Financial Reporting”. The information below should be read in conjunction with the consolidated financial statements of SMC and the related notes thereto, which are included in Appendices “A” and “B” of this Prospectus. The historical financial condition, results of operations and cash flows of SMC are not a guarantee of its future operating and financial performance.

For the years ended December 31,

For the nine months ended

September 30,

2012 2013 2014 2014 2015

(Audited) (Unaudited)

(in millions except per share figures or where otherwise indicated)

Consolidated Statements of Income Data Sales ........................................................................................... ₱ 699,916 ₱ 748,241 ₱782,434 ₱593,470 ₱504,520 Cost of sales ............................................................................... 595,581 631,856 669,641 506,617 402,176

Gross profit ................................................................................. 104,335 116,385 112,793 86,853 102,344 Selling and administrative expenses ........................................... (52,600) (60,971) (57,018) (39,644) (44,213) Interest expense and other financing charges ............................ (29,800) (30,970) (29,710) (21,925) (24,111) Interest income ........................................................................... 4,253 3,539 4,012 2,844 3,286 Equity in net earnings (losses) of associates and joint ventures………………………………………...

2,638 (967) 1,255 1,009 (486)

Gain on sale of investments and property and equipment ...................................................................................

4,549 41,192 777 218 75

Other income (charges) – Net ..................................................... 12,689 (13,780) 6,307 7 (7,837)

Income before income tax ........................................................... 46,064 54,428 38,416 29,362 29,058 Income tax expense .................................................................... 8,406 3,700 10,284 6,211 10,113

Net income .................................................................................. ₱37,658 ₱50,728 ₱ 28,132 ₱23,151 ₱18,945

Attributable to: Equity holders of the Parent Company ....................................... ₱ 26,806 ₱ 38,053 ₱14,692 ₱13,170 ₱ 6,167 Non-controlling interests ............................................................. 10,852 12,675 13,440 9,981 12,778

₱37,658 ₱ 50,728 ₱ 28,132 ₱ 23,151 ₱18,945

Earnings per common share attributable to equity holders of the Parent Company basic .........................................

₱ 8.72 ₱13.43

₱ 3.61

₱3.61

₱0.46

Earnings per common share attributable to equity holders of the Parent Company diluted

₱ 8.67 ₱P 13.36 ₱P 3.59 ₱3.59 ₱0.46

24

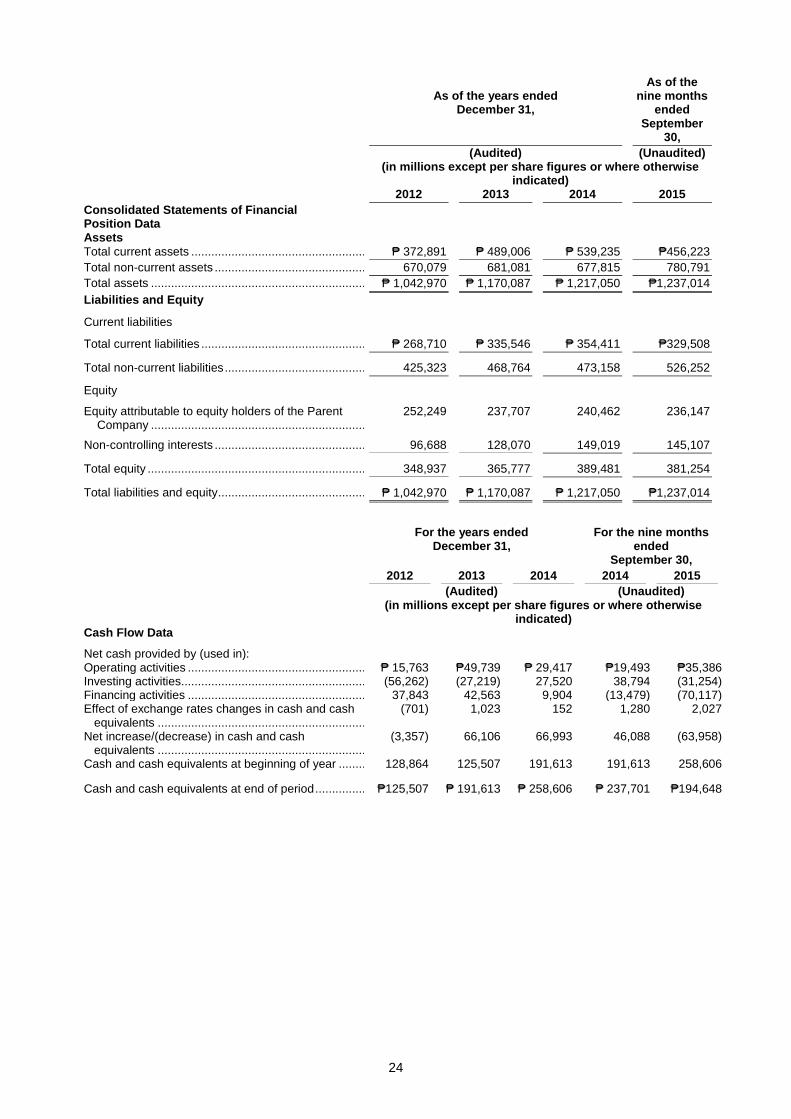

As of the years ended

December 31,

As of the nine months

ended September

30,

(Audited) (Unaudited)

(in millions except per share figures or where otherwise indicated)

2012 2013 2014 2015

Consolidated Statements of Financial Position Data

Assets Total current assets ..................................................................... ₱ 372,891 ₱ 489,006 ₱ 539,235 ₱456,223

Total non-current assets ................................................ 670,079 681,081 677,815 780,791

Total assets ................................................................... ₱ 1,042,970 ₱ 1,170,087 ₱ 1,217,050 ₱1,237,014

Liabilities and Equity

Current liabilities

Total current liabilities .................................................... ₱ 268,710 ₱ 335,546 ₱ 354,411 ₱329,508