Embed Size (px)

Citation preview

Single Assessment Framework –Business Case Guidance Notes (all tiers) Page 1

ContentsThe Capital Framework (TCF).................................................................................................................1

Single Assessment Framework...............................................................................................................1

Contents.................................................................................................................................................2

A. Introduction....................................................................................................................................4

i) Background.................................................................................................................................4

ii) Objectives...................................................................................................................................5

iii) Policy Statement.........................................................................................................................6

B. Business Case Preparation..............................................................................................................7

1. Executive Summary........................................................................................................................9

2. Project Outline.............................................................................................................................10

2.1 Description of the Project.....................................................................................................10

2.2 Review 1 (PCW): Status of Functional Brief/Output Specification........................................10

3. Needs Analysis..............................................................................................................................12

3.1 Problem................................................................................................................................12

3.2 Benefits.................................................................................................................................13

3.3 Options Analysis...................................................................................................................14

3.4 Review 2 (Treasury): Needs Analysis....................................................................................15

4. Cost and Contingency...................................................................................................................17

4.1 Preliminary Cost Estimate.....................................................................................................17

4.2 Contingency..........................................................................................................................18

4.3 Whole of Life........................................................................................................................21

4.4 Budget / Funding Strategy....................................................................................................24

5. Cost and Economic Analysis.........................................................................................................25

Purpose............................................................................................................................................25

Framework.......................................................................................................................................25

5.1 Cost-Benefit Analysis (Economic Efficiency Analysis)............................................................25

5.2 Wider Economic Benefits (where applicable).......................................................................30

5.3 Cost-Effectiveness Analysis...................................................................................................31

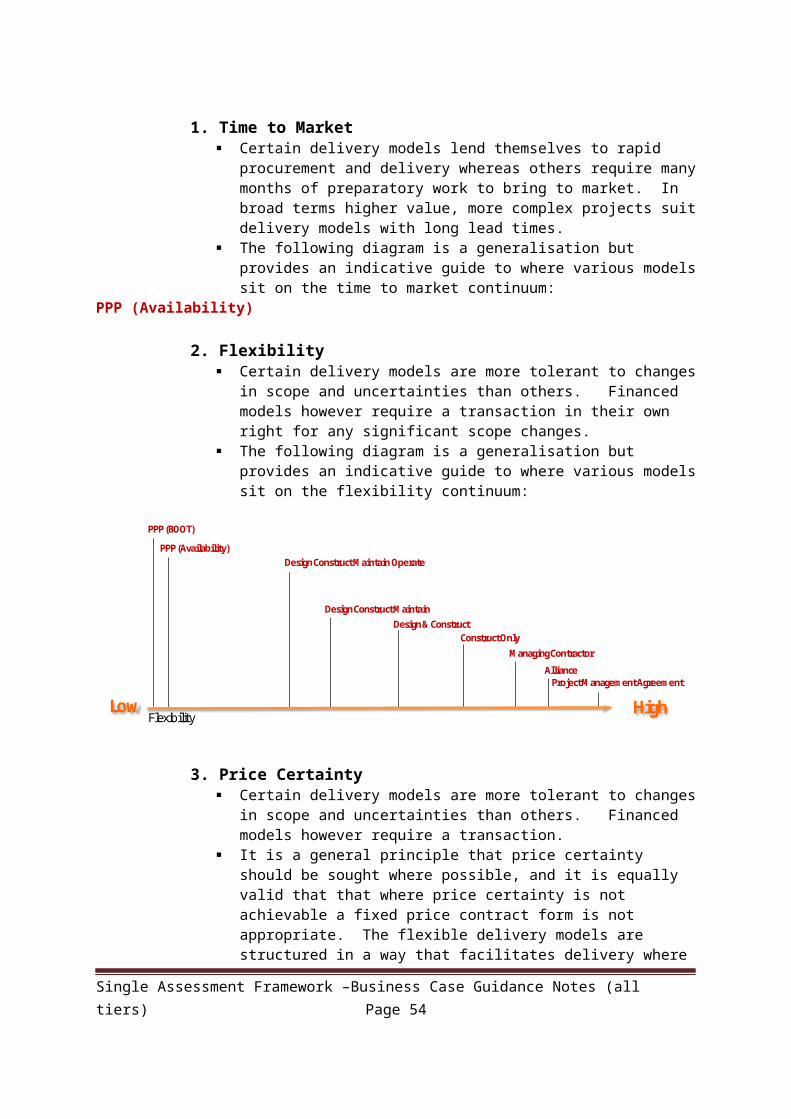

6. Delivery Model Analysis...............................................................................................................32

6.1 Outline of Delivery Models...................................................................................................32

6.2 Outline of Key Risks..............................................................................................................38

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 2

6.3 Commercial Principles..........................................................................................................38

6.4 Delivery Model Assessment..................................................................................................41

6.5 Recommended Delivery Model............................................................................................44

6.6 Review 3 (PCW): Delivery Model Selection...........................................................................46

7. Financial Analysis (PPP & DCMO only)..........................................................................................47

Economic Infrastructure...................................................................................................................47

Social infrastructure.........................................................................................................................49

7.1 Financing Assumptions.........................................................................................................51

7.2 PPP/DCMO Payment Stream................................................................................................51

7.3 Incremental Procurement/Transaction Costs.......................................................................52

7.4 Public Sector Comparator (“PSC”)........................................................................................52

7.5 Review 4 (Treasury): Financial..............................................................................................53

8. Project Governance......................................................................................................................55

8.1 Governance and Stakeholder Management.........................................................................55

8.2 Key Roles & Responsibilities.................................................................................................55

8.3 Typical Governance Structure for Tier 1 Projects.................................................................58

8.4 Typical Governance Structure for Tier 2 Projects.................................................................59

9. Stakeholder Engagement Plan......................................................................................................60

9.1 Stakeholder Identification....................................................................................................60

9.2 Stakeholder Involvement and Interest.................................................................................60

9.3 Stakeholder Engagement Plan..............................................................................................61

10. Advisor Engagement Plan.........................................................................................................63

10.1 Proposed Advisors Roles.......................................................................................................63

11. Timelines..................................................................................................................................67

11.1 Project Timetable.................................................................................................................67

Appendix A: Economic Analysis Guidelines..........................................................................................68

Appendix B: Risk & Contingency Management....................................................................................73

i) Risk Management Process........................................................................................................73

ii) Risk Workshops........................................................................................................................74

iii) Risk Management.....................................................................................................................77

iv) Contingency Management.......................................................................................................77

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 3

A. Introduction

i) Background

The ACT Government (“the Territory”) has developed The Capital Framework (“TCF”), which outlines the capital works review process. Stage 3 (Prove) of TCF includes a pre-funding business case review referred to as the Single Assessment Framework (“SAF”). This provides a structured basis for the review of capital works projects prior to funding. This framework does not intend to replicate the complex “multi-gate” capital works review processes utilised by other jurisdictions, however it aims to develop a streamlined and fit –for-purpose review process with a single “gate” prior to funding. The new business case process is a critical part of TCF.

The business case process is designed to achieve a number of practical outcomes. These are:

Prevent poorly developed output specifications/functional briefs going to market Ensure risks are allocated to the party that can best manage them Embrace a broader range of delivery models Realise improved value for money outcomes in capital works procurement

The SAF will enable the Territory to embrace a broader range of delivery models and facilitate a more appropriate allocation of risk. The level of analysis required escalates in complexity based on the value and risk profile of the project in accordance with the following three tiers. The tiers are indicative only and flexible based on risk and scope of the particular project. The three tiers are:

Tier 1: >$50mTier 2: $10m - $50mTier 3: <$10m

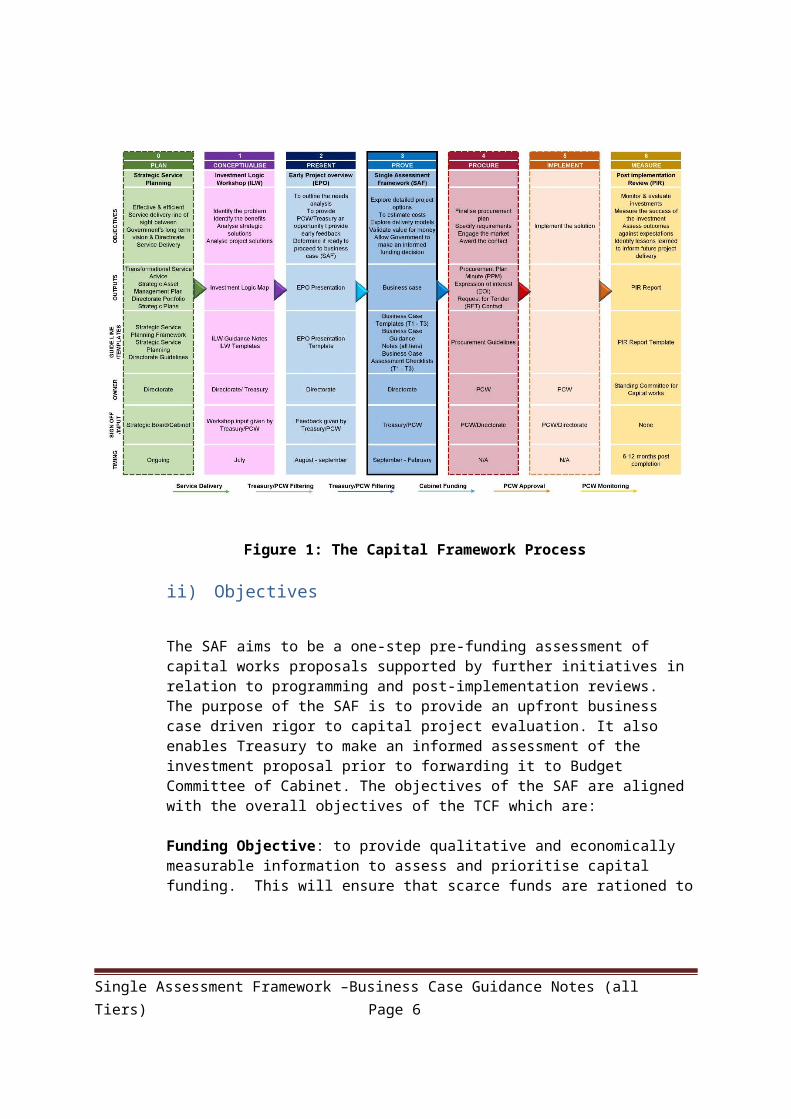

Each tier has an associated template and each template contains a series of questions under each section of this guide. It is important that each of the questions in the template is addressed when preparing the full Business Case. An overview of the TCF is provided in Figure 1:

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 4

Figure 1: The Capital Framework Process

ii) Objectives

The SAF aims to be a one-step pre-funding assessment of capital works proposals supported by further initiatives in relation to programming and post-implementation reviews. The purpose of the SAF is to provide an upfront business case driven rigor to capital project evaluation. It also enables Treasury to make an informed assessment of the investment proposal prior to forwarding it to Budget Committee of Cabinet. The objectives of the SAF are aligned with the overall objectives of the TCF which are:

Funding Objective: to provide qualitative and economically measurable information to assess and prioritise capital funding. This will ensure that scarce funds are rationed to projects in order of economic merit. This is primarily defined through needs analysis and economic assessment.

Spending Objective: to place a far greater emphasis on up-front analysis where savings per dollar spent are greatest. A formalised and consistent approach will be applied to:

Risk assessment; Risk quantification; Development of commercial principles; and

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 5

Delivery model selection.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 6

This will ensure that scarce funds are spent in a manner that optimises value for money outcomes by allocating risk to the party than can best manage it.

Process Objective: to be fit-for-purpose to meet the Funding and Spending objectives. The proposed three tiered approach helps ensure that the level of analysis is proportional to scale of the project.

iii) Policy Statement

The SAF will operate in, and support, the existing legislative and policy parameters of Territory Procurement. The primary legislation is the Government Procurement Act 2001 which defines and requires adherence to the procurement principle – value for money. At section 22A (3) that Act requires regard be given to probity and ethical behaviour; management of risk; open and effective competition; and optimising whole of life costs. A suite of other Territory enactments are relevant to interpreting this requirement, including:

1. The Financial Management Act 1996, which requires at section 31 that the director-general of a directorate is accountable to the Minister of the directorate for the efficient and effective financial management of the directorate;

2. The Public Sector Management Act 1994 which at Part 2 sets out the operating values and principles of the ACT Public Services, including at sections 6 accountability to the government for the ways in which functions are performed, fairness and integrity and efficiency and effectiveness;

3. The Environment Protection Act 1997, the objects of which include to achieve effective integration of environmental, economic and social considerations in decision-making processes; and

4. The Work Health Safety Act 2011, the object of which is to provide for a balanced and nationally consistent framework to secure the health and safety of workers and workplaces.

In line with optimising whole of life costs, consideration needs to be given to the medium and longer term costs of maintenance and major upgrades. Consideration also should be given to the broader economic costs of carbon emissions. The Government's stated targets for greenhouse reduction also need to be accounted for in the cost and design of these assets. Often this will mean examining a suite of environmentally sustainable features, and appropriate cost to benefit analysis being undertaken to determine the least-cost path to achieving the government stated green building standard.

The SAF is consistent with the goals set out in the overarching policy direction of the Territory as set out in The Canberra Plan: Towards Our Second Century. The Canberra Plan's vision is that Canberra will be recognised as:

A truly sustainable and creative city; An inclusive community that supports its vulnerable people and enables all to reach

their potential; A centre of economic growth and innovation;

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 7

The proud capital of the nation and home of its pre-eminent cultural institutions; and A place of natural beauty.

The SAF will provide a structured system to help meet the Government’s priorities with rigorous risk assessment, prioritisation and optimal management of the Government’s resources.

The SAF is also consistent with the ACT Government Infrastructure Plan: 2011–2021, which identifies a series of future directions in the strategic infrastructure planning and prioritisation processes including:1. Implementing strategic asset management and service planning across Government

agencies;2. Exploring strategic opportunities across all agencies to support innovation and quality

infrastructure design;3. Consulting on the need for a climate change vulnerability assessment framework for ACT

Government infrastructure;4. Strengthening strategic infrastructure planning by developing closer links with

Government prioritisation processes; and5. Engaging in continuous improvement of the planning and delivery of new infrastructure

investment in the Territory.

The SAF is consistent with the objectives of this Plan.

B. Business Case Preparation

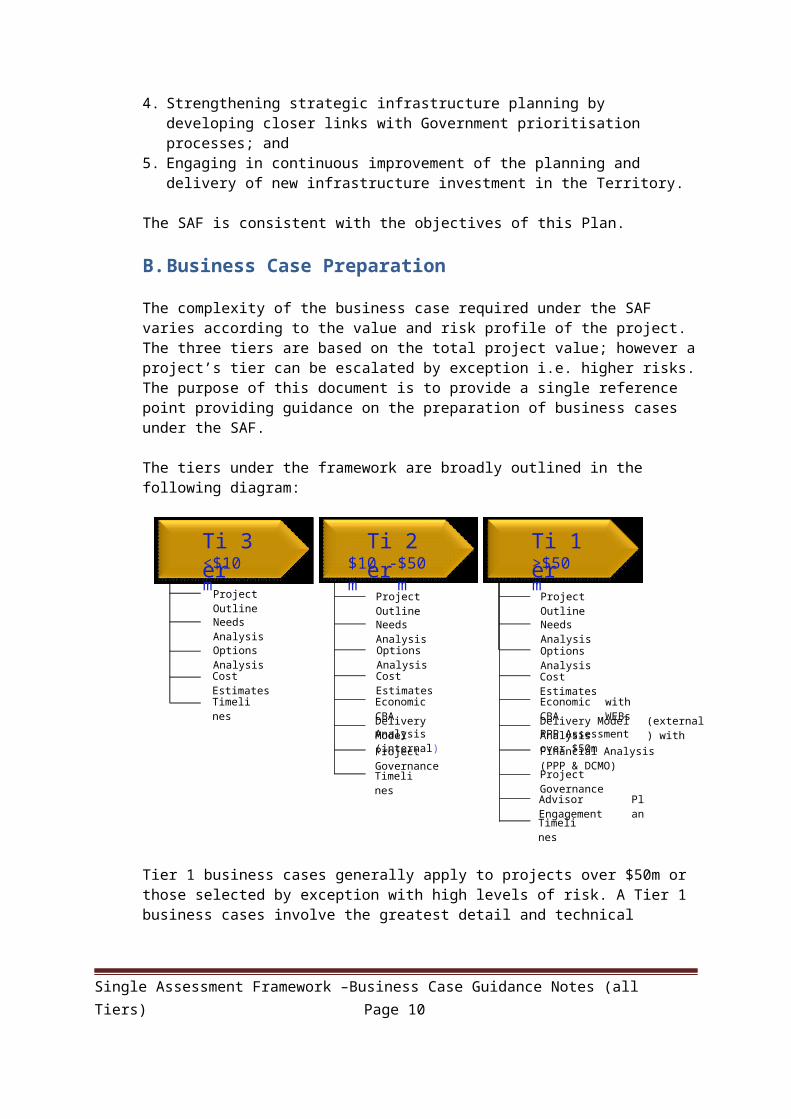

The complexity of the business case required under the SAF varies according to the value and risk profile of the project. The three tiers are based on the total project value; however a project’s tier can be escalated by exception i.e. higher risks. The purpose of this document is to provide a single reference point providing guidance on the preparation of business cases under the SAF.

The tiers under the framework are broadly outlined in the following diagram:

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 8

Financial Analysis (PPP & DCMO)

Tier 3<$10m

Tier 2$10m - $50m

Tier 1>$50m

Project Outline

Needs Analysis

Options Analysis

Cost Estimates

Project Outline

Needs Analysis

Economic CBA

Delivery Model Analysis (internal)

Project Governance

Project Outline

Needs Analysis

Economic CBA with WEBs

Delivery Model Analysis (external) with PPP Assessment over $50m

Project Governance

Advisor Engagement Plan

Options Analysis

Cost Estimates

Timelines

Options Analysis

Cost Estimates

Timelines

Timelines

1 2 3

1 2 3

Tiers 1 and 2Applicable

1 2 3

Tier 1 business cases generally apply to projects over $50m or those selected by exception with high levels of risk. A Tier 1 business cases involve the greatest detail and technical complexity. It is strongly recommended that Tier 1 business cases involve the use of external advisors to assist in completion. The Procurement and Capital Works (PCW) maintains a panel of infrastructure commercial advisors to provide assistance in this area. This can be located at:

http://www.procurement.act.gov.au/contracts/contracts_register/contracts_register_functionality/panel_contract_search?queries_pcs_query=20254.110

The following icons advise which sections of these guidelines are applicable to the project tier.

These Guidelines are particularly tailored to support directorates in the internal development of business cases for Tier 2 and 3 projects.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 9

All TiersApplicable 1 2 3

Template Instructions

For Tier 1 and High Risk Projects- Complete all sections of the consolidated Tier 1 and Tier 2 Template. For Tier 2 Projects - Complete all sections of the consolidated Tier 1 and Tier 2 Template except.

Section 5.2 Wider Economic Benefits, Section 7 Financial Analysis (PPP and DCMO only) Section 9 Stakeholder Engagement Plan Section 10 Advisor Engagement Plan

For Tier 3 Projects - Complete all sections of the Recurrent/ Capital/ICT Template- Read this guidance in conjunction with guidance provided for the above Template

1. Executive Summary

The Executive Summary should provide a concise overview of the entire Business Case drawing on the most significant points from each section, rather than only providing a description of the scope of the project. The Executive Summary should be the last part of the business case to be completed and should not introduce new information.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 10

All TiersApplicable 1 2 3

2. Project Outline

2.1 Description of the Project

2.1.1. Overview This section should provide a background to the project and outline any prior

work or studies previously undertaken. A description of the project and a summary of the project’s objectives should be

included here.

2.1.2. Scope of Works Outline the scope of the capital works to be undertaken including location,

nature of construction, known issues and risks, and nature of work environment.

2.1.3. Scope of Services Where services are included in the specification such as for DCM, DCMO and PPP

delivery models, list out what services will be included in the procured outcome. These services will need to be included in any modelled financial outcomes. Services are defined as services delivered by the project (e.g. education for

students aged 12 to 16). The scope of services is not referring to the services required to deliver the project (e.g. architects).

2.2 Review 1 (PCW): Status of Functional Brief/Output Specification

This is the first review point for PCW and is an assessment of the status of the functional brief/output specification.

Sign off should only occur if the PCW officer is confident that the functional brief/output specifications are sufficiently progressed in order to go to market under the delivery model selected, and within the procurement timeline outlined in the business case.

If not, an alternative delivery model should be selected or the business case should be returned to the Directorate.

Risk workshops and quantification of project risks is mandatory for Tier 1 and 2 projects.

Disclaimer: This review does not represent an endorsement or agreement by the signing officer as to the contents of the section or a certification that the work was correctly performed.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 11

PurposeThe Functional Brief/Output Specification is prepared when a Directorate has identified the need for a potential capital works project. A Functional Brief/Output Specification is a summary of the needs and outcomes that the Directorate is seeking to achieve from their project, and as such, is a key element in the successful outcome of capital works projects. It is not relevant for projects where detailed design has already been completed (Construct Only).

The Functional Brief/Output Specification is a written statement of the functions to be accommodated and the inter-relationships of these functions for a proposed capital works project. This document should be in sufficient detail to both facilitate procurement and initiate the design process.

The Functional Brief/Output Specification outlines the Government’s design principles for the project and the understanding of, and approach to, design that forms the basis of the design requirements.

It should establish the optimum solution to meet service requirements and outline the total scope of works to be undertaken. It should describe the services to be provided, activities to be performed and clearly identify how the project meets the organisation’s objectives and policies.

Wherever possible, the Functional Brief/Output Specification should also be supported by any specific directorate design guidelines, policy documents and other relevant information pertaining to the project.

The Directorates are responsible for preparing a Functional Brief/Output Specification but where necessary, may be assisted by an external Consultant.

RequirementsA Functional Brief/Output Specification needs to be prepared prior to commencement of a Feasibility Study. The Functional Brief/Output Specification is the basis from which the time and costing data are prepared and a Feasibility Study is completed.

The document should contain sufficient detail to initiate the design process. A Functional Brief/Output Specification for any capital works project should include, but not limited to the following information:

Directorate or agency role statement Directorate or agency expectations and user requirements An estimated program schedule and timeframe / key milestone dates Details of any proposed staging or phasing Required deliverables Management and operational policies Type and level of facilities or services to be provided Existing and future trends Overall project objective Project background (including Master Plan outcomes) Description of any existing facilities, use and current condition

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 12

All TiersApplicable 1 2 3

Departmental functions associated with the project Departmental and functional relationships – “bubble diagrams” Accommodation requirements on a departmental or functional area basis General design considerations, “generic layouts” and “room data sheets” Equipment needs FF&E requirements Services facilities & services management Recurrent cost statement if applicable

The review should ensure the list of requirements (relevant to the size/scale of the project) is included in the Functional Brief/Output Specification. The review should also ensure that the Functional Brief and Output Specification are sufficiently progressed in order to go to market under the delivery model selected, and within the procurement timeline outlined in the business case.

3. Needs Analysis

This section should present the outcomes of the Investment Logic Workshop (“ILW”) (if one was undertaken).

Please detail all participants who attended the workshop and attach a copy of the Investment Logic Map (“the Map”) produced as an Appendix to the Business Case.

Ensure that feedback from Procurement and Treasury officials from the ILW workshop(s) is addressed in this section.

3.1 Problem

This section should outline the problem that you are aiming to address. The “3 Problem Questions” below should be answered in this section:

What is the problem? What is the evidence to confirm there is a problem? Does the problem need to be addressed now?

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 13

For example, in relation to a hypothetical set of problems in the justice sector:

1. Problem 1: Extensive delays at the Magistrates Court are undermining access to justice: The demand for justice exceeds the capacity of the current court facilities.

2. Problem 2: A lack of modern justice services is driving recidivism and the high cost of justice: The design and functionality of the heritage listed Courts does not‐ support modern justice standards, operational efficiency and current user needs.

3. Problem 3: All court users face safety risks because of the out dated design of ‐the court rooms: The heritage listed Court fails to meet current court health and ‐safety standards leading to increased risk of assault and unnecessary strain on the health of the public and judiciary.

This section should include the evidence to support the existence of the problem. The evidence should draw on experience of interventions in other jurisdictions or pilots. Remember to show how and why the problem exists.

3.2 Benefits

3.2.1. Benefits to be DeliveredThis section should outline the benefits you are trying to achieve by addressing the problem. The “3 Benefits Questions” should be answered in this section:

What are the benefits of addressing the problem? Are the benefits of high value to the Territory? Are there measurement mechanisms (KPIs) to provide evidence that the benefits

have been delivered?

The benefits need to be realistic and achievable.

For example, if the problem were those above in the justice sector, benefits could be:

1. Cost savings for courts and the public: Cost savings will be achieved through a reduction in rescheduling and transfer to other courts and the use of alternative justice services.

2. Increased effectiveness of justice system: Reduced delay in justice services measured by the waiting time for cases heard being reduced.

3. Safety of all court users: would improve with a decrease in the incidents of violence and improved security reflected in the willingness of witnesses to attend hearings.

3.2.2. Importance of benefits for GovernmentThis section should outline why the benefits are important to the Territory. Some questions to ask:

How does this proposal align with strategic objectives and priorities of the Territory?

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 14

How does the proposal enhance existing Territory policies or programs or deliver new ones?

Is this proposal associated with a Government election commitment or legislation change?

3.3 Options Analysis

3.3.1. Strategic Solutions AnalysisThis section should address the strategic solutions explored to address the problem and deliver the benefits. Strategic solutions are about differing approaches to solving the problem. It should be noted that Strategic Solutions are different to Project Solution Analysis in section 3.3.3 of this guide.

For example, if the problem was a regional water shortage the strategic solutions could look like:

1. Build a water pipeline to the region2. Build a desalination plant3. Provide water grants to enhance storage and conservation

The “3 Strategic solutions analysis questions” should be answered in this section:

What different approaches to the problem have been identified? What is the evidence to demonstrate that the strategic options are feasible? Is the preferred strategic option the most effective way to address the problem

and deliver the benefits?

3.3.2. Recommended Strategic SolutionThis section should outline the recommended strategic solution and provide justification as to why this solution has the most merit.

3.3.3. Project Solutions AnalysisThis section should address the project options explored to address the problem and deliver the benefits. The Project Solution Analysis should outline the different ways in which the Recommended Strategic Solution can be implemented successfully. Note: Options should also give consideration to non-infrastructure based solutions.

For example, if the problem was a regional water shortage and the preferred strategic solutions was option 1 (build a water pipeline) then the project solutions could look like:

1. Build a water pipeline from location X or Y to the region2. Build a water pipeline with or without a local reservoir 3. Build a water pipeline using material A, B, or C

The “3 Project solutions analysis questions” should be answered in this section:

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 15

What different approaches to the solution have been identified? Quantify the costs and benefits of each option Demonstrate exploration of alternative options All realistic options should be considered including:

o Refurbishing existing facility/assetso Private sector involvement, rental optionso Various locations/shared facilities

Link suitable options to the business case need identified as listed above Identify the preferred option including the preferred physical location Outline key advantages and disadvantages, and identify all whole-of-life

benefits and costs of each option Is the recommended project option the best value for money way to address the

problem and deliver the results? Can the recommended project option be delivered (cost, risk, timeframe etc)?

Note: Consideration should be given to immediate project requirements versus those components of the project that could be done later in the project timeline.

3.3.4. Base CaseThis section should outline the do nothing/do minimum option. In some cases “do nothing” may be a viable option. In some cases, however, a “do minimum” option is the more realistic approach.

For example, a building is at the end of its useful life and the proposal is to build its replacement. The Base Case may well be a do minimum option with a combination of:

Building a limited extension to the existing building Enhanced periodic maintenance program Refurbish existing facilities Modify rostering and usage to enhance capacity

The Base Case as such is therefore likely to involve a combination of interim and partial solutions that would likely have to be put in place if the proposed solution was not undertaken. The Base Case should consider public and workplace safety issues and how these might be addressed if capital funding is not made available.

3.3.5. Recommended Project SolutionThis section should outline the recommended project solution.

3.4 Review 2 (Treasury): Needs Analysis

This is the first review point for Treasury and is assessment of the needs analysis. Sign off should only occur if the Treasury officer is confident that the needs analysis is

robust, is based on evidence and an Investment Logic Workshop (ILW) has been undertaken (if applicable).

Note that Tier 1 business cases anticipate review and signoff by the Under Treasurer. An assessment of the needs analysis should be undertaken here

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 16

Procurement will provide feedback to Treasury on the needs analysis and the merit of the Recommended Project Solution.

The documentation should only proceed to the next part of the process if the Treasury officer is confident that the needs analysis is robust and is based on evidence

Disclaimer: This review does not represent an endorsement or agreement by the signing officer as to the contents of the section or a certification that the work was correctly performed.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 17

All TiersApplicable 1 2 3

4. Cost and ContingencyThe scope, risk and delivery model of the Recommended Project Solution will have a bearing on the cost and associated need for contingency funding. This section will assist both Treasury and Procurement to understand the funding implications, and assess the Value for Money, of the Recommended Project Solution and its proposed Delivery Model (see Sections 4.2.2 and 6).

4.1 Preliminary Cost Estimate

The business case should present a preliminary cost estimate prepared by an appropriately qualified technical advisor / quantity surveyor. When providing cost estimates please ensure you provide both the source of the costing and the year the costing occurred.

o Note that in Tier 3, or where appropriate this may be an internal estimate or be based on real cost analysis from completed projects of a similar nature.

The preliminary cost estimate should include any line item contingencies. It should also include the Shared Services Management Fee (four per cent of capital

cost), Insurance (one per cent of capital cost) and all costs managed by the Directorate.

Note that advice on the development of design and construction cost estimates is NOT within the scope of the business case guidance material.

For example, a preliminary cost estimate would be derived on the basis of: Benchmarking with similar sized facilities based on likely scope of the

project. Contingencies and Directorate costs included within each cost line. Costs set out in nominal dollar terms and include additional ongoing

operational costs.

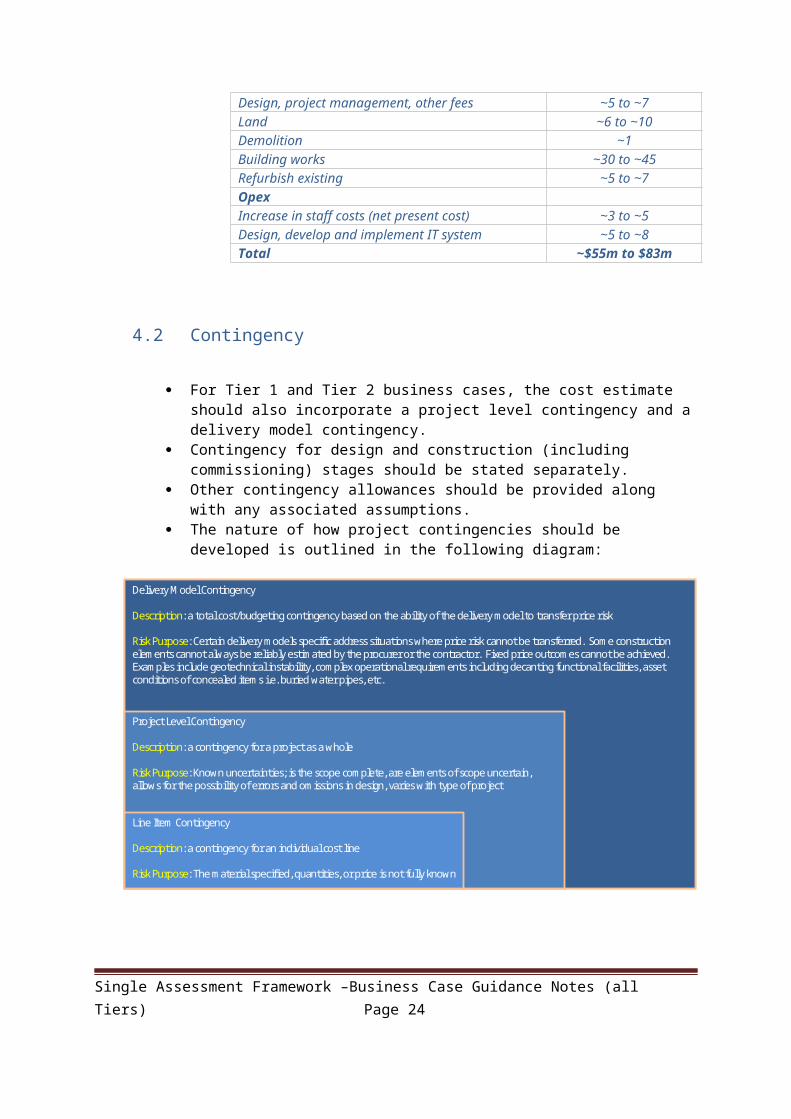

Item Estimated Cost ($m)CapexDesign, project management, other fees ~5 to ~7Land ~6 to ~10Demolition ~1Building works ~30 to ~45Refurbish existing ~5 to ~7OpexIncrease in staff costs (net present cost) ~3 to ~5Design, develop and implement IT system ~5 to ~8Total ~$55m to $83m

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 18

4.2 Contingency

For Tier 1 and Tier 2 business cases, the cost estimate should also incorporate a project level contingency and a delivery model contingency.

Contingency for design and construction (including commissioning) stages should be stated separately.

Other contingency allowances should be provided along with any associated assumptions.

The nature of how project contingencies should be developed is outlined in the following diagram:

Delivery Model Contingency

Description: a total cost/budgeting contingency based on the ability of the delivery model to transfer price risk

Risk Purpose: Certain delivery models specific address situations where price risk cannot be transferred. Some construction elements cannot always be reliably estimated by the procurer or the contractor. Fixed price outcomes cannot be achieved. Examples include geotechnical instability, complex operational requirements including decanting functional facilities, asset conditions of concealed items i.e. buried water pipes, etc.

Project Level Contingency

Description: a contingency for a project as a whole

Risk Purpose: Known uncertainties; is the scope complete, are elements of scope uncertain, allows for the possibility of errors and omissions in design, varies with type of project

Line Item Contingency

Description: a contingency for an individual cost line

Risk Purpose: The material specified, quantities, or price is not fully known

Delivery Model Contingency

Description: a total cost/budgeting contingency based on the ability of the delivery model to transfer price risk

Risk Purpose: Certain delivery models specific address situations where price risk cannot be transferred. Some construction elements cannot always be reliably estimated by the procurer or the contractor. Fixed price outcomes cannot be achieved. Examples include geotechnical instability, complex operational requirements including decanting functional facilities, asset conditions of concealed items i.e. buried water pipes, etc.

Project Level Contingency

Description: a contingency for a project as a whole

Risk Purpose: Known uncertainties; is the scope complete, are elements of scope uncertain, allows for the possibility of errors and omissions in design, varies with type of project

Line Item Contingency

Description: a contingency for an individual cost line

Risk Purpose: The material specified, quantities, or price is not fully known

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 19

All Tiers All Tiers Applicable 1 2 3

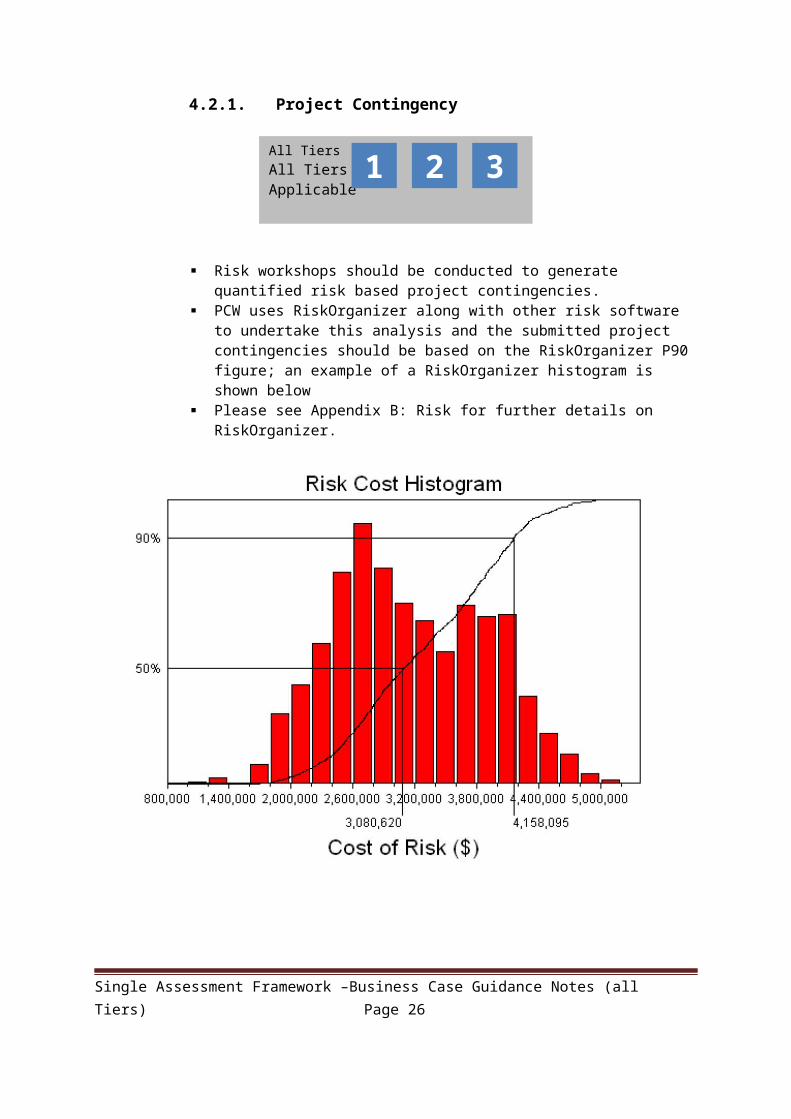

4.2.1. Project Contingency

Risk workshops should be conducted to generate quantified risk based project contingencies.

PCW uses RiskOrganizer along with other risk software to undertake this analysis and the submitted project contingencies should be based on the RiskOrganizer P90 figure; an example of a RiskOrganizer histogram is shown below

Please see Appendix B: Risk for further details on RiskOrganizer.

If a commercial advisor has been engaged to undertake risk analysis, the methodology and tools used to quantify the risk contingency should be outlined.

The project contingency is managed by the PCW project officer in consultation with project sponsor Directorates.

Risk workshop documents should be attached to the final business case (see Appendix B)

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 20

Tiers 1 and 2Applicable 1 2 3

4.2.2. Delivery Model Contingency

Under the SAF process, certain flexible delivery (relationship contracting) models are required to have contingencies in addition to line item and project level contingencies to reflect delivery models where price certainty cannot be achieved.

The specified flexible delivery models for use have delivery model contingencies of: Managing Contractor 30% Alliance 50% PMA

o Fixed scope 5%o Open scope 40%

Whilst there have been some studies into project overruns under varying delivery models 1, these figures are largely heuristic and intended to address uncertainty (“unknown unknowns”) in providing delivery where there may be issues such as:

Latent asset condition issues Complex operation requirements Geotechnical uncertainty Incomplete scope

Where commercial factors justify higher or lower delivery model contingencies to the default these should be outlined here.

Delivery Model Contingency is managed by Treasury. Access would need to be applied for through Treasury under the existing process for supplementary budget appropriations and released based on forecasts.

Please see Appendix B: Risk for further details.

1 The three notable studies in this area are: In Pursuit of Additional Value: A benchmarking study into alliancing in the Australian Public Sector. Department of Treasury and

Finance, Victoria, October 2009. Performance of PPPs and Traditional Procurement in Australia, Infrastructure Partnerships Australia, 2008. National PPP Forum – Benchmarking Study, Phase II. Report on the performance of PPP projects in Australia when compared

with a representative sample of traditionally procured infrastructure projects. Assoc Prof Colin Duffield. The University of Melbourne, December 2008.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 21

4.3 Whole of Life

The business case should include a financial evaluation of the whole of life costs of the options. This section provides guidance on the importance of assessing the whole of life financial impacts and how whole of life cash flows can be calculated and evaluated. The section concludes by providing guidance in relation to analysing the sensitivity of the evaluation to changes in key assumptions and variables.

While it is important to evaluate the level and timing of the project’s up-front capital investment cost, often the operating and maintenance costs for the life of the asset have an equally large financial cost. Indeed an option with a larger up-front investment cost may result in reduced whole of life costs.

The purpose of this whole of life financial evaluation is to: Assess the incremental whole of life financial value or cost of the shortlisted

project options when compared to the base case Assess any funding requirements or subsidies from other Government bodies Assess the commercial viability of the shortlisted project options (where

applicable) Assess the affordability of the shortlisted options.

The financial analysis provides a set of baseline whole of life cash flows (including for the base case). This can be used in the development of cost comparators which are used in the value for money assessment.

For further information on best practice in determining the Whole of Life Cost or Life Cycle Cost of an asset, please refer to:

Life-Cycle Costing – Better Practice Guide, Australian National Audit Office, 2001

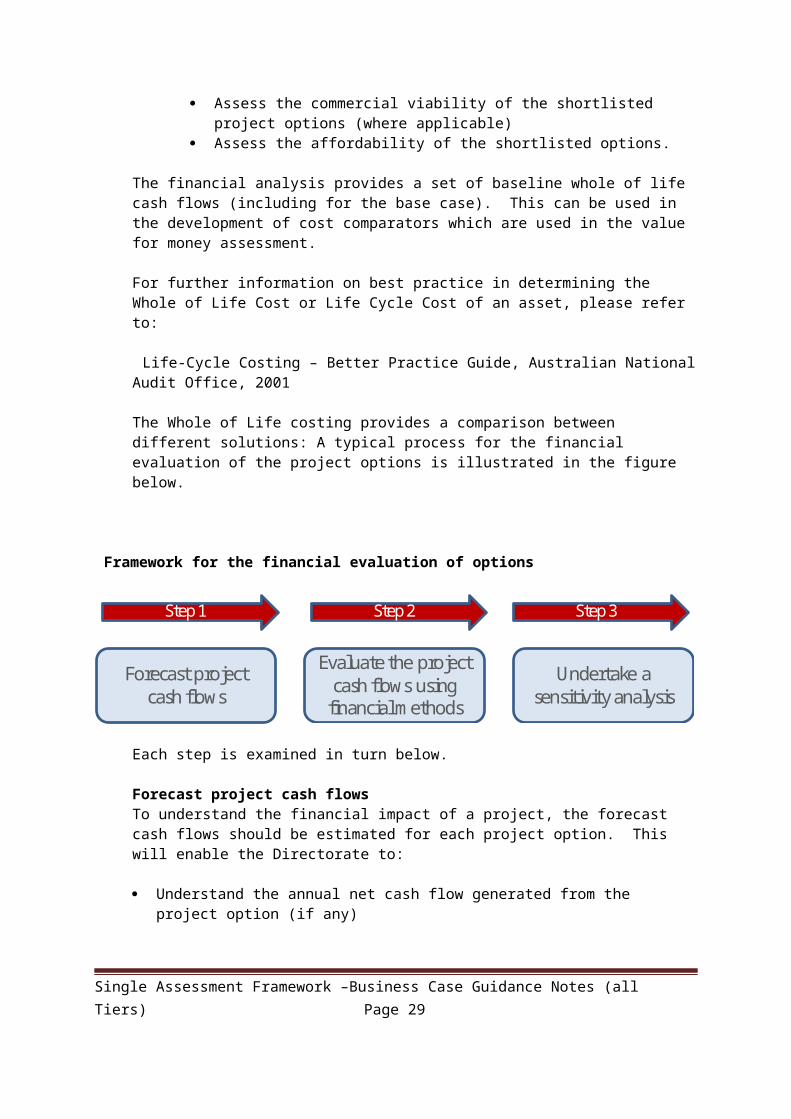

The Whole of Life costing provides a comparison between different solutions: A typical process for the financial evaluation of the project options is illustrated in the figure below.

Framework for the financial evaluation of options

Forecast project cash flows

Evaluate the project cash flows using

financial methods

Undertake a sensitivity analysis

Step 1 Step 2 Step 3

Each step is examined in turn below.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 22

Forecast project cash flowsTo understand the financial impact of a project, the forecast cash flows should be estimated for each project option. This will enable the Directorate to:

Understand the annual net cash flow generated from the project option (if any) Identify the net financial cost or benefit of the project option in present value terms

Cash flows for the shortlisted options should comprise only those things which are an incremental result of the option when compared with the base case - they do not include the cash flow associated with the base case. Types of cash inflows include revenues, avoided cash flows, productivity savings, residual value and release of capital. Types of cash outflows include capital expenditure, operating expenditure and one-off costs.

The typical components of a forecast cash flow for a capital project are outlined in the Table below:

Table: Components of a project cash flowComponents DescriptionEstimated capital cost The cash outflows associated with the capital development phase of

the project option, including expected risks or contingencies.Forecast revenue generated

The revenue expected to be generated from the project option. Some project options may leverage revenue to the ACT Government. The increase in expected revenue should be captured as part of the financial analysis.

Forecast operating expenditure incurred

The operating expenditure to be incurred as a result of the investment made, including staff costs, direct operating costs, overheads, and operating risk adjustments.

Annual net cash flow Represents the sum of all cash outflows and inflows for a particular year.

Key assumptions Assumptions are used to project the capital cost, revenue and operating expenditure of the project option. They may include activity growth assumptions, price indexation rates and timing assumptions.

Key considerations when developing a cash flow forecast are:

o Forecast period: The forecast period of cash flow may vary. It is recommended the forecast cash flow period reflects the ACT Government’s investment horizon, as long as it does not exceed the life of the asset.

o Impact on existing revenue and expenditure: It is important to consider the impact that a proposed capital investment will have on existing services.

o Cash flow period adopted: Depending on the degree of accuracy required in the analysis, cash flows may be forecast on a monthly, quarterly or annual basis.

All modelling prepared to the forecast project cash flows should be included as an attachment to the business case.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 23

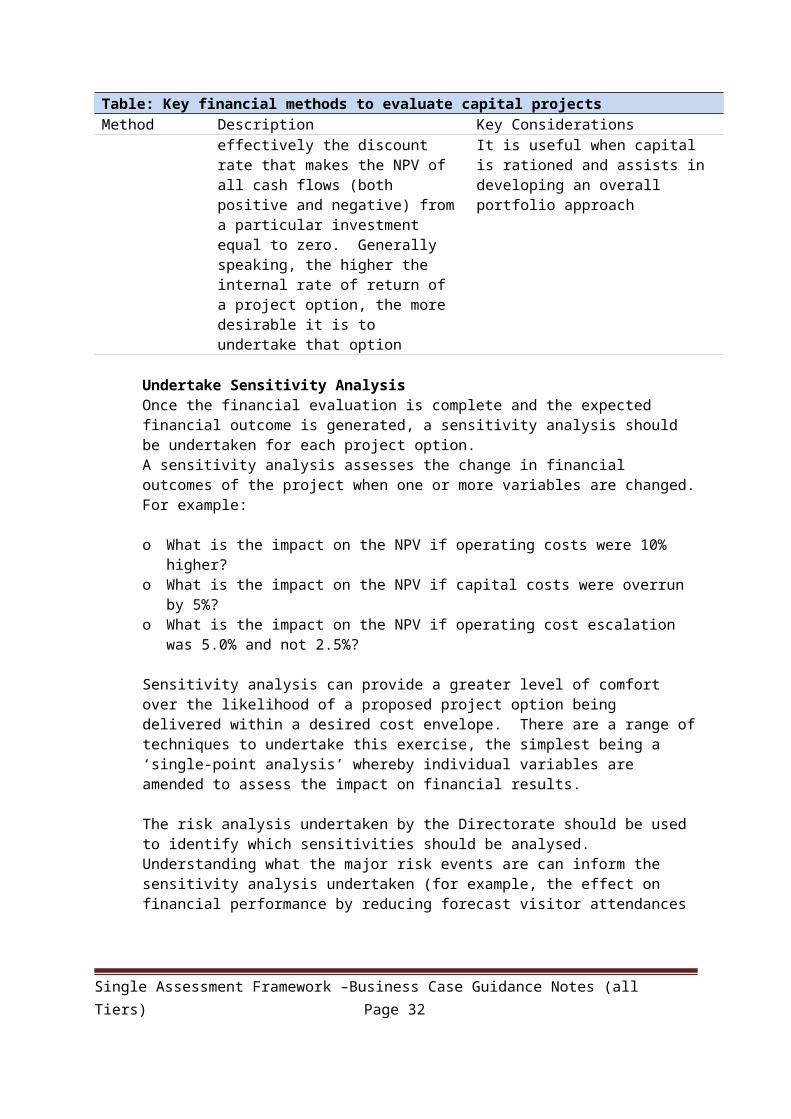

Evaluate project cash flowsAn evaluation method needs to be applied to each of the shortlisted project options. The table below provides an overview of the two financial methods required to evaluate a capital investment: net present value and internal rate of return.

Table: Key financial methods to evaluate capital projectsMethod Description Key ConsiderationsDiscounted cash flow methodsNet Present Value (NPV)

The NPV is the present value of an investment's future net cash flows minus the initial investmentA positive NPV represents the immediate increase in financial value to the ACT Government. A negative NPV indicates that a project option will result in a net cost to the ACT Government.

An NPV can be generated from projected cash flowsThe NPV is dependent on the ACT Government discount rate, which will generally reflect the long term bond rate and can be obtained from Treasury.

Internal Rate of Return (IRR)

The IRR is a rate of return used in capital budgeting to measure and compare the implied or intrinsic profitability of investments. It is effectively the discount rate that makes the NPV of all cash flows (both positive and negative) from a particular investment equal to zero. Generally speaking, the higher the internal rate of return of a project option, the more desirable it is to undertake that option

An IRR can be determined from projected cash flowsWhen cash flows are volatile it can generate multiple IRRs which may confuse the analysisIt is useful when capital is rationed and assists in developing an overall portfolio approach

Undertake Sensitivity AnalysisOnce the financial evaluation is complete and the expected financial outcome is generated, a sensitivity analysis should be undertaken for each project option.A sensitivity analysis assesses the change in financial outcomes of the project when one or more variables are changed. For example:

o What is the impact on the NPV if operating costs were 10% higher?o What is the impact on the NPV if capital costs were overrun by 5%?o What is the impact on the NPV if operating cost escalation was 5.0% and not 2.5%?

Sensitivity analysis can provide a greater level of comfort over the likelihood of a proposed project option being delivered within a desired cost envelope. There are a range of techniques to undertake this exercise, the simplest being a ‘single-point analysis’ whereby individual variables are amended to assess the impact on financial results.

The risk analysis undertaken by the Directorate should be used to identify which sensitivities should be analysed. Understanding what the major risk events are can inform the sensitivity analysis undertaken (for example, the effect on financial performance by reducing forecast

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 24

All TiersApplicable 1 2 3

visitor attendances by 10%). In this way the expected impact on results can be determined (for example a decrease in the revenue generation).

4.4 Budget / Funding Strategy

The purpose of this section is to set out the budget impacts of the preferred option.A budget impact statement analyses the budget impact of the proposed project (savings and costs) and implications for the Directorate, such as additional staff, equipment or any financial impacts on other Directorates where there is a joint proposal.

The Treasury budget summary requires the identification of capital and recurrent costs and also incremental staffing impacts across the budget forward estimate period.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 25

Tiers 1 and 2Applicable 1 2 3

Tiers 1 and 2Applicable 1 2 3

5. Cost and Economic Analysis

The business case for Tier 1 and Tier 2 projects must also consider the broader non-financial impacts of an investment upon the ACT community. These broader considerations include all relevant economic, social and environmental factors (collectively 'non-financial factors') that are of significance in making an investment decision and selecting the preferred project option.

Purpose

Like the financial analysis, the purpose of the non-financial analysis of options is to assess and compare the incremental impacts of each shortlisted project option over and above the base case.

The non-financial evaluation is required to identify and estimate all the likely impacts of a project to the community as a whole.

Framework

The scope of the non-financial evaluation undertaken will vary depending upon the nature of the project, the likely impacts and the level of expenditure involved. The depth of analysis and detail of reporting is expected to be greater for proposals involving significant expenditure or with significant impacts. It also depends on the availability of data and the agreed scope of the analysis (including time, budget and appropriateness) of all three elements. The quantifiable and non-quantifiable costs and benefits of the economic, social and environmental impacts should be addressed in the business case report to fully inform decision making.

The financial analysis is solely quantitative. For non-financial impacts, a range of analysis techniques may be adopted ranging from:

A monetised economic analysis – cost benefit analysis; and An analysis of non-monetised but quantifiable measures – economic impact analysis.

5.1 Cost-Benefit Analysis (Economic Efficiency Analysis)

A cost-benefit analysis is an assessment tool used to determine whether an option is beneficial relative to the base case. The key principle of cost-benefit analyses is to convert the costs and benefits into dollar terms, allowing them to be weighed up against each other. An option will be considered more desirable if it delivers benefits over and above its costs, which is typically expressed in net present value (“NPV”) terms.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 26

The cost-benefit analysis differs from traditional financial analysis in that it is performed from the viewpoint of society; specifically the community of the ACT. For example, it considers the road safety benefits of a road improvement project. It goes beyond just looking at just the fiscal impacts by examining social welfare impacts too.

A Cost Benefit Analysis (“CBA”) quantifies (in monetary terms) all the major costs and benefits of project options. Thus the outcomes for a range of options are translated into comparable terms to facilitate evaluation and decision making. The technique also makes explicit allowance for the many costs and benefits which cannot be valued.

Where supporting data is available, every effort should be made to put a value on the monetary or quantifiable benefits and impacts. For some projects, a combination of the three evaluation techniques (monetary, quantitative and qualitative) may be adopted requiring a weighting of impacts to be applied across the three types of analysis. This enables the complete merits of an investment ranging from financial quantitative impacts to qualitative non-financial impacts to be considered.

Given the role and functions of Government, many proposed projects will be non-revenue generating or revenue-generating proposals which will not reflect positive net present values on the basis of their cash flows alone, but are undertaken to deliver other significant benefits to the community.

The business case should seek to place a quantifiable value on the extent of project benefits as much as feasible. That said, it’s acknowledged that some non-financial costs, benefits and risks are difficult to measure given their subjective nature and it’s not expected that all will be quantified or capable of being translated into monetary terms. All significant non-monetary and non-quantifiable costs, benefits and risks relating to each project option should be reported upon in an appropriate form in the business case.

The non-financial evaluation of a project option can be a complex process. Whilst in some instances the Directorate will have the requisite skills to undertake its own evaluation, some project options will require the services of an external consultant. As a minimum the project team should be in a position to identify the type and nature of the likely non-financial impacts which may result from each project option prior to engaging an external consultant.

A suggested framework for the non-financial analysis for a Tier 1 and Tier 2 project is illustrated below.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 27

Framework for non-financial analysis of options

Identify and classify non financial impacts (environmental, social

or environmental)

Review non financial impacts to detect

duplication

Select and apply a tool for the assessment of non-financial impacts

and apply

Step 1 Step 2 Step 3

Guidance on each step is provided in the following sections:

Identifying and classifying non-financial impactsNon-financial analysis in a general sense covers three broad areas: economic, social and environmental impacts. The first step in the non-financial analysis involves the project team identifying and classifying the impacts. This includes the following tasks:

Identify non-financial impacts: Identify all potentially significant non-financial impacts (economic, social and environmental) of each project option should be identified; regardless of how difficult they may be to measure (otherwise only a partial evaluation may be carried out). A further task is assessing the extent to which a project option achieves the broad objectives.

Classify impacts: Allocate all impacts under either an economic, social or environmental impact and further identify under each category whether the impact is a cost or a benefit to the broader community.

The following sections provide an overview of the economic, social and environmental areas of impacts.

5.1.1. Economic A project option may not be seen as 'financially' viable (with a positive net present value) but it may still be 'economically' viable to execute it. On this basis, the option will deliver a return from the perspective of the community. Two key economic considerations for a project option are:

o Whether it is economically efficient (whether the economic benefits of an option exceed the costs)

o The extent to which it contributes to Gross Regional Product (or its impact on the regional economy)

The economic analysis should demonstrate which option offers a greater economic return to the ACT community.

Identify quantifiable costs All economic appraisals should be based on incremental costs and benefits associated with a particular project. Changes which would have occurred anyway should be excluded.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 28

Assumptions underlying all capital and recurrent cost estimates should be made explicit in the evaluation.

The degree of accuracy desirable will vary with the significance of the project, data availability and cost of obtaining missing data. Best estimates are often sufficient but if there is doubt as to whether such will be acceptable, advice should be sought from Treasury.

Identify quantifiable benefits The following may be relevant: Avoided costs-incremental costs which are unavoidable if nothing is done, but may be

avoided if action is taken; Cost savings-verifiable reductions in existing levels of expenditure if a program proceeds; Revenues-incremental revenues from introduction of the project; Benefits to project beneficiaries not reflected in revenue flows-while difficult, attempts

should be made to quantify these, with assumptions and methodologies clearly explained; and

Residual value of asset (if any).

Calculate net benefits Quantifiable costs and benefits over the project life - a 20 year analysis period is recommended for consistency - are expressed in Net Present Value terms.

Costs and benefits should be valued in real terms over the 20 years: that is, they should be expressed in constant dollar terms and not include nominal increases due to inflation. The stream of costs and benefits should then be discounted by a real discount rate of 7%, with sensitivity testing using discount rates of 4% and 10%.

The discounting process takes account of the fact that initial investment costs are borne up-front, while benefits or operating costs may extend far into the future. Discounting the value of future costs and benefits brings these back to a common time dimension - present value - for the purpose of comparison. The process of discounting is simply a compound interest calculation worked backwards.

The process of discounting real costs and benefit values reflects, even in the absence of inflation, the concept of time preference for money. People normally prefer to receive cash sooner rather than later and pay bills later rather than sooner. The existence of real interest rates also reflects this time preference.

Using the discounted stream of costs and benefits the following decision measures should be calculated:

o Net Present Value (NPV)-the sum of benefits minus costs; a project is potentially worthwhile (subject to the availability of funds) if the NPV is greater than zero.

o Net Present Value per $ of capital investment (NPV/I)-the highest NPV may involve very high capital expenditure and capital availability is normally constrained. Projects with the highest ratios would be potentially worthwhile.

o Benefit Cost Ratio-a project is potentially worthwhile if the BCR is greater than 1 i.e., the present value of benefits exceeds the present value of costs). It has become

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 29

conventional to deduct ongoing costs from benefits to produce a net benefit stream, and to use initial capital costs as the denominator. This is the required basis on which results should be provided. In cases where BCR calculations are done on another basis, for example to satisfy requirements of other Governments for jointly funded projects, results should be shown on the two bases and clearly identified.

o Internal Rate of Return (IRR)-this is the discount rate at which the Net Present Value of a project is equal to zero (i.e. discounted benefits equal discounted costs). A project is worthwhile if the IRR is greater than the test discount rate.

o Sensitivity analysis should be undertaken to test the robustness of results under different scenarios, using different assumptions about some or all of the key variables.

Identify qualitative factors and summarise results Quantifiable costs and benefits are only part of an economic appraisal. Other aspects such as environmental considerations, social or regional impacts, resource availability, funding, distribution of benefits and costs, etc, will also have to be taken into account in choosing between competing options and projects.

Some of these may be quantifiable to some extent but where they are not, qualitative aspects of options or projects should be discussed in the appraisal.

The report on the appraisal should include a clear summary of results, and indicate the preferred option.

Sensitivity testingSensitivity testing of the cost benefit analysis is a key element of risk assessment. The purpose of the sensitivity analysis is to acknowledge that there is always a degree of uncertainty and ultimately risk surrounding a proposal. Typically there are four sources of uncertainty surrounding a proposal:

o Capital costs; o Construction duration and therefore opening date; o Operating (including maintenance) costs; and o Under and over estimation of the benefits (typically demand for the service).

A risk assessment should be undertaken to estimate the typical variations around these inputs with the sensitivity testing undertaken based on the variations.

5.1.2. Social AnalysisMost investments are undertaken to deliver services and, as a result, will have some social consequences. The business case should analyse social outcomes, unless it is clear that the external impacts are minimal.

Social analysis identifies and quantifies social issues and opportunities arising from a project option. The analysis should explain the nature and extent of the social impact (and, where possible, quantify them). This might include:

Policy implications;

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 30

Tier 1Applicable

Employment opportunities or likely redundancies/termination of existing contracts; and

Community.

5.1.3. Environmental AnalysisLegislative requirements and community concerns drive the need for an environmental analysis. The environmental analysis should assess the extent and nature of environmental consequences and opportunities surrounding each project option. Issues include:

The extent to which a project option requires a departure from the ACT Government’s environmental policies;

Known environmental issues arising from the option (e.g. contaminated site); Consents or approvals required; and Whether an Environmental Effects Statement (EES) or a Commonwealth

Environmental Impact Statement (EIS) is required and issues arising from such requirements.

Tools for assessing non-financial impactsThe second step of the financial analysis requires the project team to select a tool for assessment of the non-financial impacts of each project option. An overview of three such assessment tools is set out below.

Further technical guidance on undertaking a CBA is provided in Appendix A: Economic Analysis Guidelines.

Additional guidance material on how to undertake cost benefit analysis can be found at the following links:

o the Department of Finance and Deregulation website at http://www.finance.gov.au/obpr/cost-benefit-analysis.html

o Department of Finance, Handbook of Cost Benefit Analysis, January 2006 which can be found at: http://www.finance.gov.au/publications/finance-circulars/2006/01.html

o Department of Finance, Introduction to Cost Benefit Analysis and Alternative Evaluation Methodologies, January 2006 : http://www.finance.gov.au/publications/finance-circulars/2006/docs/Intro_to_CB_analysis.pdf

o The Green Book – Appraisal and Evaluation in Central Government, Treasury Guidance, London 2004 : http://www.hm-treasury.gov.uk/data_greenbook_index.htm

5.2 Wider Economic Benefits (where applicable)

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 31

Tiers 1 and 2Applicable 1 2 3

Wider economic impact studies look at the impact of a project option in terms of changes to macroeconomic aggregates such as Gross Regional Product, Gross State Product or Gross Domestic Product and employment – that is the ‘economic impacts’. Economic impacts should not be confused with economic costs and benefits described above.

5.3 Cost-Effectiveness Analysis

Cost effectiveness analysis is used to compare the costs of alternate ways of delivering the same project, whereas cost-benefit analysis are used to quantify the costs and benefits of a proposal including where those costs and benefits are not necessarily market based.

A cost effectiveness analysis is applicable to projects that have strong social welfare objectives or where the benefit of building an asset has already been established, or cannot be established, and the information being required relates more to the different delivery options (ie the objectives of the project are the same but there are different ways to deliver the outcome).

For example, this may be used for schools, where the benefits of education have been established as part of broader public policy efforts, and the decision to construct a school is based more on demand modelling. Unlike health, there is a greater homogeneity of service in a school, and costs are much less sensitive to “models of care”.

In these cases, what needs to be established is the most cost-effective option, based on scenarios where differing methods/options can be used to deliver broadly the same outcome.

While Cost Effectiveness Analysis is a valid option for agencies, agreement from Treasury should first be obtained before it is used instead of a cost-benefit analysis. Treasury would need to be assured that either:

the benefits have already been sufficiently decided on or understood; or the benefits cannot be reliably measured with enough confidence to make a CBA

reliable.

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 32

Tiers 1 and 2Applicable 1 2 3

6. Delivery Model Analysis

The business case needs to justify the procurement decision based on facts and analysis. For Tier 1 and Tier 2 projects this includes a procurement options analysis, which should demonstrate how the recommended procurement approach represents value for money. It would be beneficial to contact PCW for early input in selecting a suitable delivery model.

When evaluating different procurement options, the Directorate should:

Develop a framework for the comparative analysis of the different procurement options, which incorporates evaluation criteria and a system for rating each option against the criteria

Identify the different procurement options to be considered Identify key project risks and desired risk allocations Set timeframes associated with each procurement option and provide an assessment of their

achievability Engage the market through market soundings to:

- Identify key players;- Determine market capacity;- Determine market appetite; and- Consider whether there is sufficient competition to drive value for money outcomes.

Assess the potential value for money associated with each procurement option Assess and rank each of the procurement options against the evaluation criteria Recommend the preferred procurement approach Identify potential commercial structure and associated issues related to the recommended

procurement approach.

6.1 Outline of Delivery Models

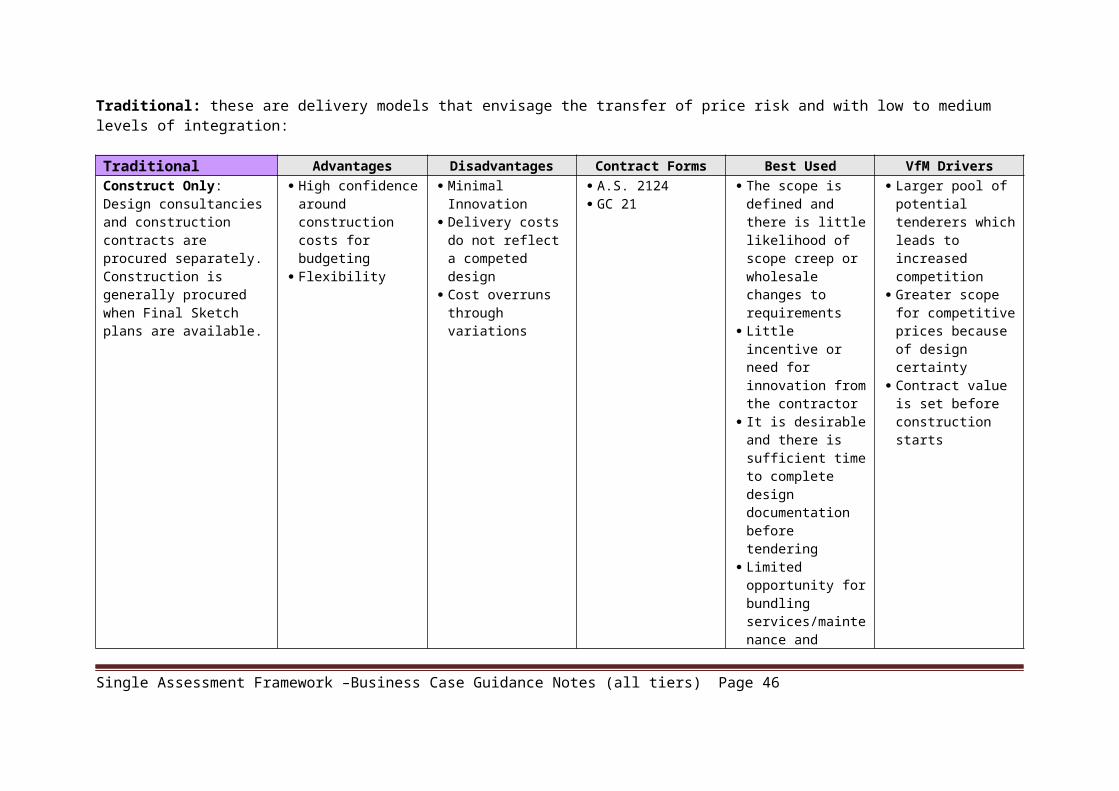

There are a broad range of delivery models available for capital works projects. The suitability of any one model will be driven by the project’s risk profile and characteristics. Under the SAF there are nine prescribed delivery models for use. This does not preclude other delivery models being used; however the nine proposed should be sufficient to deal with most project risk profiles. It’s anticipated that existing models will still be used for Tier 3 projects. Tiers 1 and 2 offer a broader range of models.

The following graph approximates where the various models sit against an axis of integration and risk transfer (note Government Works is provided for explanatory purposes only – it is not an option for delivery outside Property Group small value works):

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 33

These models can be broken down into three classes as outlined in the following table (note that “Flexible” delivery models are also referred to as relationship contracting models):

Single Assessment Framework –Business Case Guidance Notes (all Tiers) Page 34

Inte

grati

on

Risk TransferConstruct Only

Managing Contractor

AllianceDesign & Construct

Design Construct Maintain

Design Construct Maintain Operate

BOOT PPPAvail. PPP

PMA

Govt. Works

Traditional: these are delivery models that envisage the transfer of price risk and with low to medium levels of integration:

Traditional Advantages Disadvantages Contract Forms Best Used VfM DriversConstruct Only: Design consultancies and construction contracts are procured separately. Construction is generally procured when Final Sketch plans are available.

High confidence around construction costs for budgeting

Flexibility

Minimal Innovation Delivery costs do not

reflect a competed design

Cost overruns through variations

A.S. 2124 GC 21

The scope is defined and there is little likelihood of scope creep or wholesale changes to requirements

Little incentive or need for innovation from the contractor

It is desirable and there is sufficient time to complete design documentation before tendering

Limited opportunity for bundling services/maintenance and creating whole-of-life efficiencies

Larger pool of potential tenderers which leads to increased competition

Greater scope for competitive prices because of design certainty

Contract value is set before construction starts

Design & Construct (D&C): An integrated design and construction outcome is simultaneously procured. Generally at Preliminary Sketch Plan.

Delivery cost reflects a competed design

Innovation Improved VfM Contractor motivated

for earliest completion

Competition may drive reduced quality of finish and durability

More emphasis on upfront specifications required to ensure the asset is fit for purpose

A.S. 4300 GC 21

The Government’s requirements are tightly specified before tender or do not change

Government is seeking cost effective designs.

Limited opportunity for bundling services/maintenance and creating whole-

Single point of accountability for design and construction

Fixed price contract Potentially, reduced

overall project cost because the Contractor has the opportunity to contribute construction

Single Assessment Framework –Business Case Guidance Notes (all tiers) Page 35

Traditional Advantages Disadvantages Contract Forms Best Used VfM Driversof-life efficiencies experience into the

design, resulting in innovation and efficiencies.

Design Construct Maintain:A Design & Construct with an integrated maintenance contract.Maintenance contracts are typically 5 to 15 years.

Certainty of maintenance outcomes

Maintenance contract can prevent poor finish and fittings

More emphasis on upfront specifications

Higher procurement and bid costs

GC 21 Scope for bundling maintenance with the design and construction contract and creating whole-of-life efficiencies

As with D&C with the additional benefits of greater durability and better whole of life cost outcomes

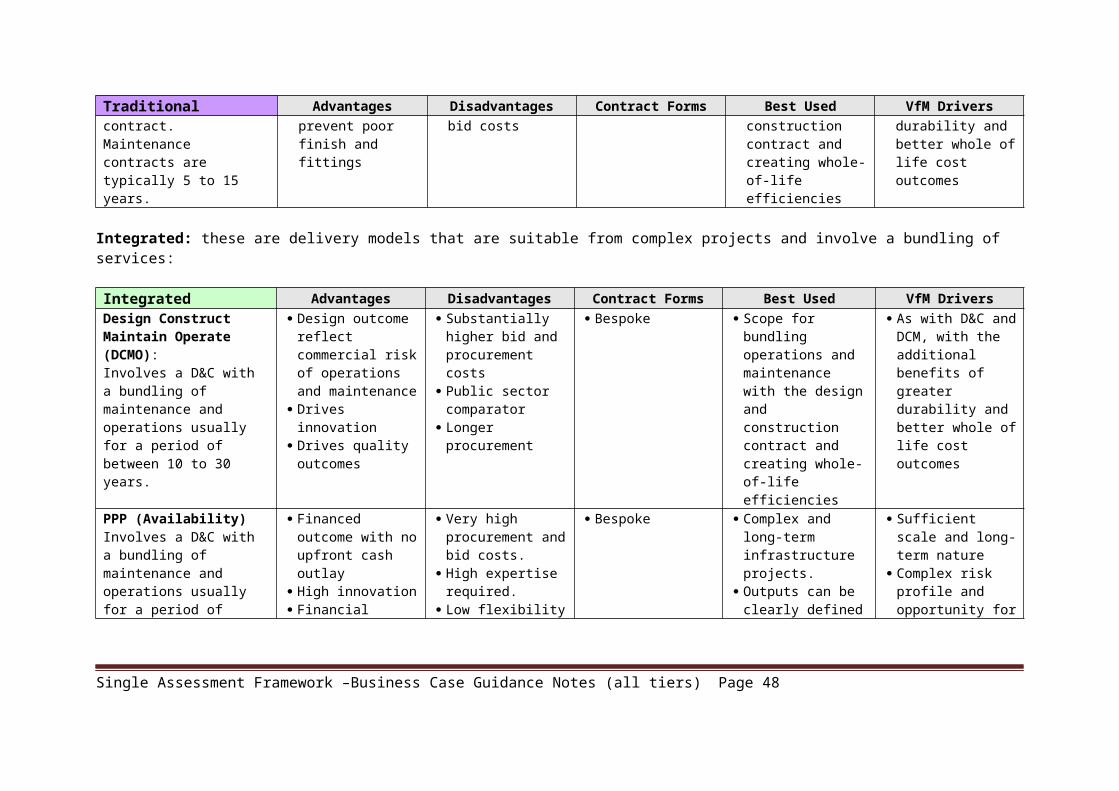

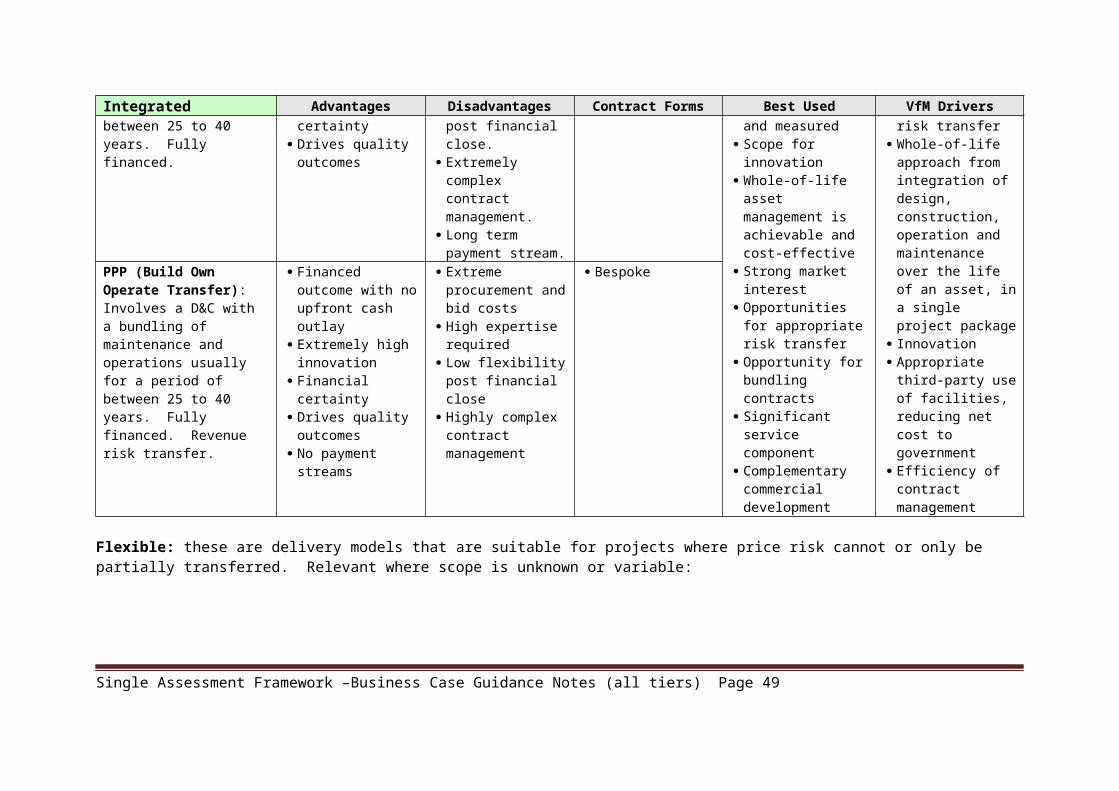

Integrated: these are delivery models that are suitable from complex projects and involve a bundling of services:

Integrated Advantages Disadvantages Contract Forms Best Used VfM DriversDesign Construct Maintain Operate (DCMO): Involves a D&C with a bundling of maintenance and operations usually for a period of between 10 to 30 years.

Design outcome reflect commercial risk of operations and maintenance

Drives innovation Drives quality

outcomes

Substantially higher bid and procurement costs

Public sector comparator

Longer procurement

Bespoke Scope for bundling operations and maintenance with the design and construction contract and creating whole-of-life efficiencies

As with D&C and DCM, with the additional benefits of greater durability and better whole of life cost outcomes

PPP (Availability) Involves a D&C with a bundling of maintenance and operations usually for a period of between 25 to 40 years. Fully financed.

Financed outcome with no upfront cash outlay

High innovation Financial certainty Drives quality

outcomes

Very high procurement and bid costs.

High expertise required.

Low flexibility post financial close.

Extremely complex contract management.

Bespoke Complex and long-term infrastructure projects.

Outputs can be clearly defined and measured

Scope for innovation Whole-of-life asset

management is achievable and cost-effective

Sufficient scale and long-term nature

Complex risk profile and opportunity for risk transfer

Whole-of-life approach from integration of design, construction, operation and

Single Assessment Framework –Business Case Guidance Notes (all tiers) Page 36

Integrated Advantages Disadvantages Contract Forms Best Used VfM Drivers Long term payment

stream. Strong market interest Opportunities for

appropriate risk transfer

Opportunity for bundling contracts

Significant service component

Complementary commercial development

maintenance over the life of an asset, in a single project package

Innovation Appropriate third-

party use of facilities, reducing net cost to government

Efficiency of contract management

PPP (Build Own Operate Transfer): Involves a D&C with a bundling of maintenance and operations usually for a period of between 25 to 40 years. Fully financed. Revenue risk transfer.

Financed outcome with no upfront cash outlay

Extremely high innovation

Financial certainty Drives quality

outcomes No payment streams

Extreme procurement and bid costs

High expertise required

Low flexibility post financial close

Highly complex contract management

Bespoke

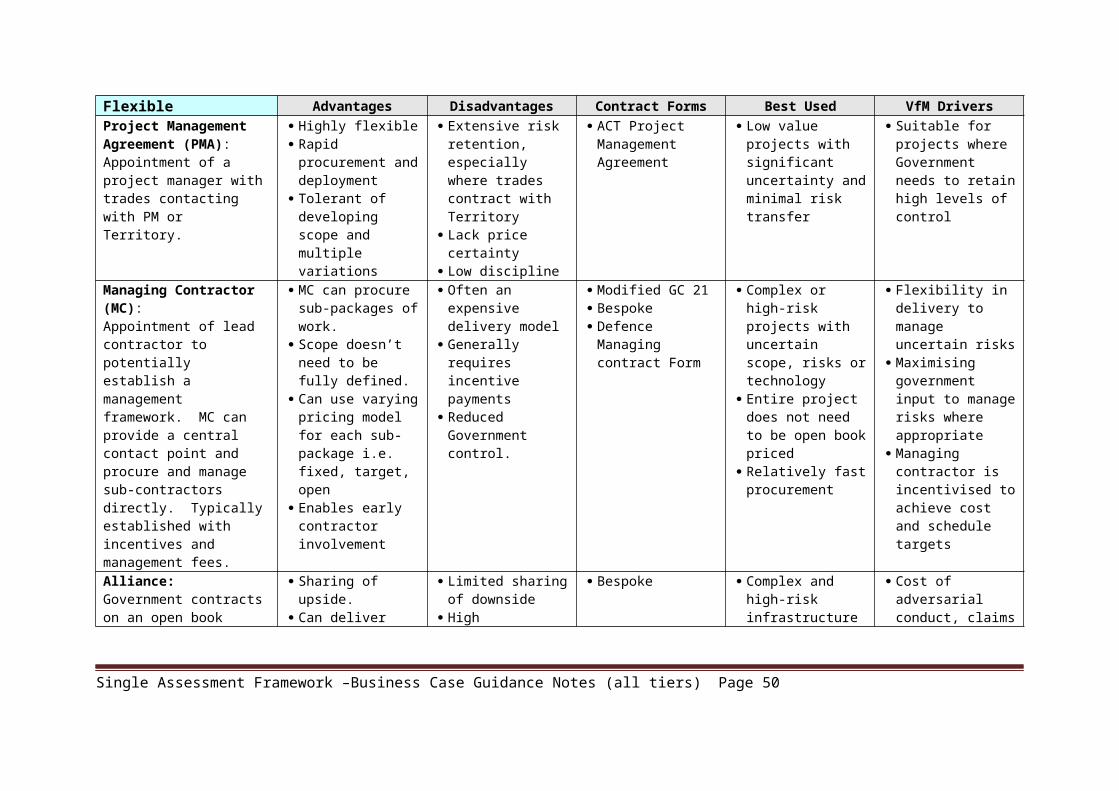

Flexible: these are delivery models that are suitable for projects where price risk cannot or only be partially transferred. Relevant where scope is unknown or variable:

Flexible Advantages Disadvantages Contract Forms Best Used VfM DriversProject Management Agreement (PMA): Appointment of a project manager with trades contacting with PM or Territory.

Highly flexible Rapid procurement

and deployment Tolerant of

developing scope and multiple variations

Extensive risk retention, especially where trades contract with Territory

Lack price certainty Low discipline

ACT Project Management Agreement

Low value projects with significant uncertainty and minimal risk transfer

Suitable for projects where Government needs to retain high levels of control

Managing Contractor (MC):Appointment of lead contractor to potentially establish a management framework. MC can provide a central contact point and procure and manage sub-contractors directly. Typically established with incentives

MC can procure sub-packages of work.

Scope doesn’t need to be fully defined.

Can use varying pricing model for each sub-package i.e. fixed, target, open

Enables early

Often an expensive delivery model

Generally requires incentive payments

Reduced Government control.

Modified GC 21 Bespoke Defence Managing

contract Form

Complex or high-risk projects with uncertain scope, risks or technology

Entire project does not need to be open book priced

Relatively fast procurement

Flexibility in delivery to manage uncertain risks

Maximising government input to manage risks where appropriate

Managing contractor is incentivised to

Single Assessment Framework –Business Case Guidance Notes (all tiers) Page 37

Flexible Advantages Disadvantages Contract Forms Best Used VfM Driversand management fees. contractor

involvementachieve cost and schedule targets

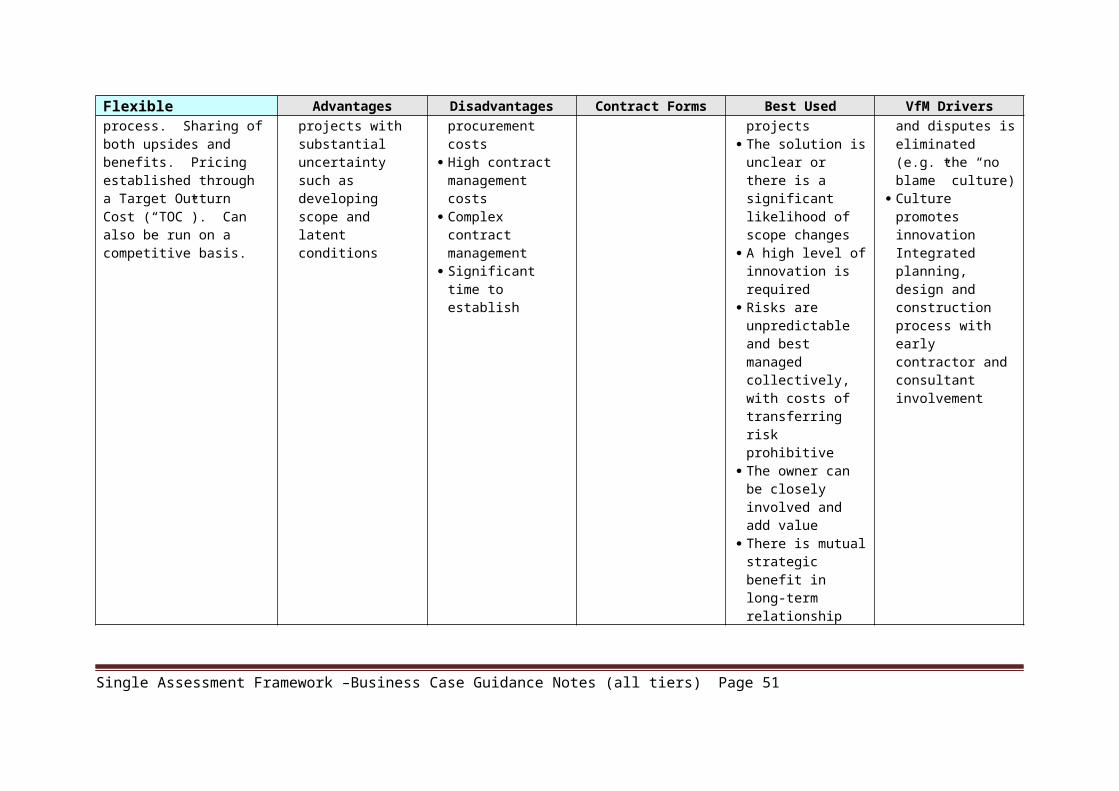

Alliance: Government contracts on an open book process. Sharing of both upsides and benefits. Pricing established through a Target Outturn Cost (“TOC”). Can also be run on a competitive basis.

Sharing of upside. Can deliver projects

with substantial uncertainty such as developing scope and latent conditions

Limited sharing of downside

High procurement costs

High contract management costs

Complex contract management

Significant time to establish

Bespoke Complex and high-risk infrastructure projects

The solution is unclear or there is a significant likelihood of scope changes

A high level of innovation is required

Risks are unpredictable and best managed collectively, with costs of transferring risk prohibitive

The owner can be closely involved and add value

There is mutual strategic benefit in long-term relationship building between the parties

Cost of adversarial conduct, claims and disputes is eliminated (e.g. the “no blame” culture)

Culture promotes innovation Integrated planning, design and construction process with early contractor and consultant involvement

Single Assessment Framework –Business Case Guidance Notes (all tiers) Page 38

6.2 Outline of Key Risks

• Outline process undertaken for risk management. • Has a RiskOrganizer (or equivalent) workshop been undertaken? If not, was any Risk

Workshop undertaken? • Please attach a copy of your Risk Register in an Appendix to the Business Case.• Please attach a Risk Management Plan which highlights the process to identify, assess,

allocate and monitor current, anticipated and emerging risks? Please note if utilising the RiskOrganizer tool, outline how often risk workshops will be held and who will be managing the process. Please see Appendix B: Risk of the Guidelines for further information on how to develop a Risk Management Plan.

6.3 Commercial Principles

Commercial principles provide a link between the project risk and the delivery model. These reflect how project risk will be dealt with.