Embed Size (px)

Citation preview

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 1/14

1

L&T Infra

Infra Project Finance Financial Advisory ServicesStructured Products

Enablers for Infra Finance

ADB Workshop in Manila, Philippines30 September 2011

L&T Infrastructure Finance Co LtdRamesh M. Bhujang

Vice President - Corporate & Strategic Affairs

The views expressed in these presentations are the views of the author and do not necessarily reflect the views or policies of the Asian Development

Bank (ADB), or its Board of Directors or the governments they represent. ADB does not guarantee the source, originality, accuracy, completeness or

reliability of any statement, information, data, finding, interpretation, advice, opinion, or view presented, nor does it make any representation concerning

the same.

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 2/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

2

Agenda

Definition of Infra

Clarity in regulation & rationalization of stamp duties

Modifying Investment criteria for investment companies

Investment criteria for banks

Guidelines/ regulations Taxation

Annex

Infra enablers in recent years

Key issues for Infra projects

Sources

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 3/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

3

Common definition of “Infra”

Could facilitate(1) insurance companies channelize funds to Infra

(2) assist in designing fiscal incentives for infra

(3) assist consistent tracking of progress in Infra

(4) improve trading in infra papers or bonds

Area Action required (Broad

level) Action required (Specific)

Definition of

Infrastructure

Harmonising the definition

by RBI, IRDA, Income

Tax, ECB etc

RBI's definition could be uniformly

assumed; Principle of "Transferability" and"Natural Monopoly" could be the basic

principles for classification as "Infra". (For

example, Cement and steel can be imported

and exported i.e. transferred and would not

form a part of "Infra"; road, power plant,

telecom network, pipeline network etc

cannot be transferred and would form a part

of "Infra")

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 4/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

4

Clarity in regulation & rationalization of stamp duties

Area Action required (Broad

level) Action required (Specific)

Advantage of such

action

Clarity in

regulation

Implementation of the RHPatil Committee

recommendations

Several areas including

consolidation of all regulations on

issuance of corporate debt

securities under SEBI

Single regulator and

clarity

Corporatebonds Rationalise stamp dutiesacross states

Implementation of the Indian

Stamp Amendment Bill 2011 mayenable rationalisation of stamp

dueties across states.

Help in the

development of avibrant debt market

•Slow progress has been made towards rationalization of stamp duties across various

states in India

•Complete implementation of the RH Patil Committee Recommendations (2005/06) ispending

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 5/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

5

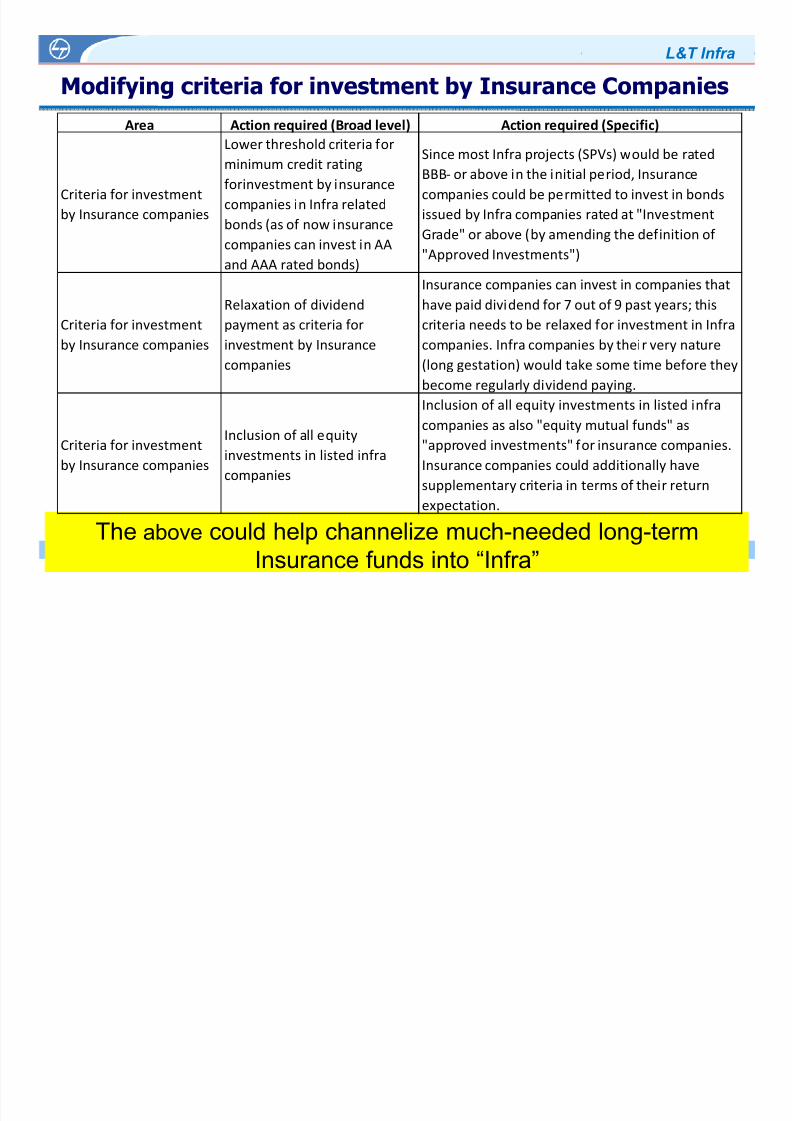

The above could help channelize much-needed long-termInsurance funds into “Infra”

Modifying criteria for investment by Insurance Companies

Area Action required (Broad level) Action required (Specific)

Criteria for investment

by Insurance companies

Lower threshold criteria for

minimum credit rating

forinvestment by insurance

companies in Infra related

bonds (as of now insurance

companies can invest in AA

and AAA rated bonds)

Since most Infra projects (SPVs) would be rated

BBB- or above in the initial period, Insurance

companies could be permitted to invest in bonds

issued by Infra companies rated at "InvestmentGrade" or above (by amending the definition of

"Approved Investments")

Criteria for investment

by Insurance companies

Relaxation of dividend

payment as criteria for

investment by Insurance

companies

Insurance companies can invest in companies that

have paid dividend for 7 out of 9 past years; this

criteria needs to be relaxed for investment in Infra

companies. Infra companies by their very nature

(long gestation) would take some time before they

become regularly dividend paying.

Criteria for investment

by Insurance companies

Inclusion of all equity

investments in listed infra

companies

Inclusion of all equity investments in listed infra

companies as also "equity mutual funds" as"approved investments" for insurance companies.

Insurance companies could additionally have

supplementary criteria in terms of their return

expectation.

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 6/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

6

The above could enable larger flow of funds from Banks to “infra”

Modifying criteria for investment by Banks

Area Action required (Broad

level) Action required (Specific)

Advantage of such

action

Underwrittenexposures for banks

Exclusion of underwritten

exposures from the definition

of "Infra"

Underwritten exposures could be excluded from

the definition of Infra (with a limit of say 5% of

NOF) where the stated intention is to sell-off theasset in 6 months. In case this does not

happen in 6 months, the Bank/ NBFC / IFC

would have to bring in additional capital

Banks can take a

higher exposure toInfra and manage ALM

mismatches

Definition of "Group"

exposure

In case of lending to SPVs on

non-recorse basis, the SPV

need not be included under

"Group" exposure

SPVs that do not have recourse to parent

companies/ Group need to be at differentiated

wrt "Concentration Risk"

Banks can take higher

exposures to "Infra"

Risk weight for

Takeout Financing

As on date, the takeout

financier as well as the initial

financier need to set aside

capital (risk weightage 100%,

capital conversion).

Both initial lender and takeout financier currently

set aside capital from day 1 although takeout

may happen only after 5 years. Proposed that

the capital conversion and risk weightage could

be 0% till such time the asset is transferred to

the books of the takeout financier

Encouragement to

takout financing

SLR requirement for

banks

Lower SLR requirement for

banks for their investments

in "Infra"

Lower SLR requirement for banks for their

investments in "Infra"

Banks can take higher

exposures to "Infra"

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 7/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

7

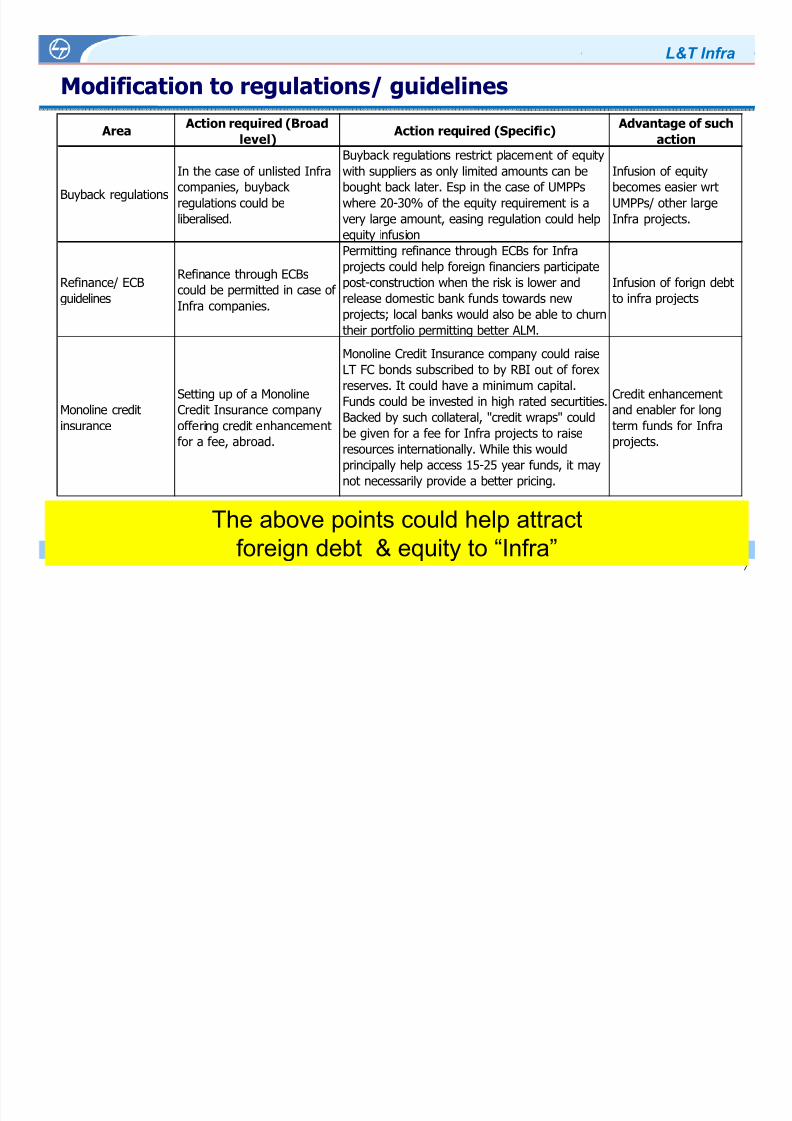

The above points could help attract

foreign debt & equity to “Infra”

Modification to regulations/ guidelines

Area Action required (Broad

level) Action required (Specific)

Advantage of such

action

Buyback regulations

In the case of unlisted Infra

companies, buyback

regulations could be

liberalised.

Buyback regulations restrict placement of equity

with suppliers as only limited amounts can be

bought back later. Esp in the case of UMPPs

where 20-30% of the equity requirement is a

very large amount, easing regulation could helpequity infusion

Infusion of equity

becomes easier wrt

UMPPs/ other large

Infra projects.

Refinance/ ECB

guidelines

Refinance through ECBs

could be permitted in case of

Infra companies.

Permitting refinance through ECBs for Infra

projects could help foreign financiers participate

post-construction when the risk is lower and

release domestic bank funds towards new

projects; local banks would also be able to churn

their portfolio permitting better ALM.

Infusion of forign debt

to infra projects

Monoline credit

insurance

Setting up of a Monoline

Credit Insurance company

offering credit enhancementfor a fee, abroad.

Monoline Credit Insurance company could raise

LT FC bonds subscribed to by RBI out of forex

reserves. It could have a minimum capital.

Funds could be invested in high rated securtities.

Backed by such collateral, "credit wraps" could

be given for a fee for Infra projects to raise

resources internationally. While this would

principally help access 15-25 year funds, it may

not necessarily provide a better pricing.

Credit enhancement

and enabler for long

term funds for Infraprojects.

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 8/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

8

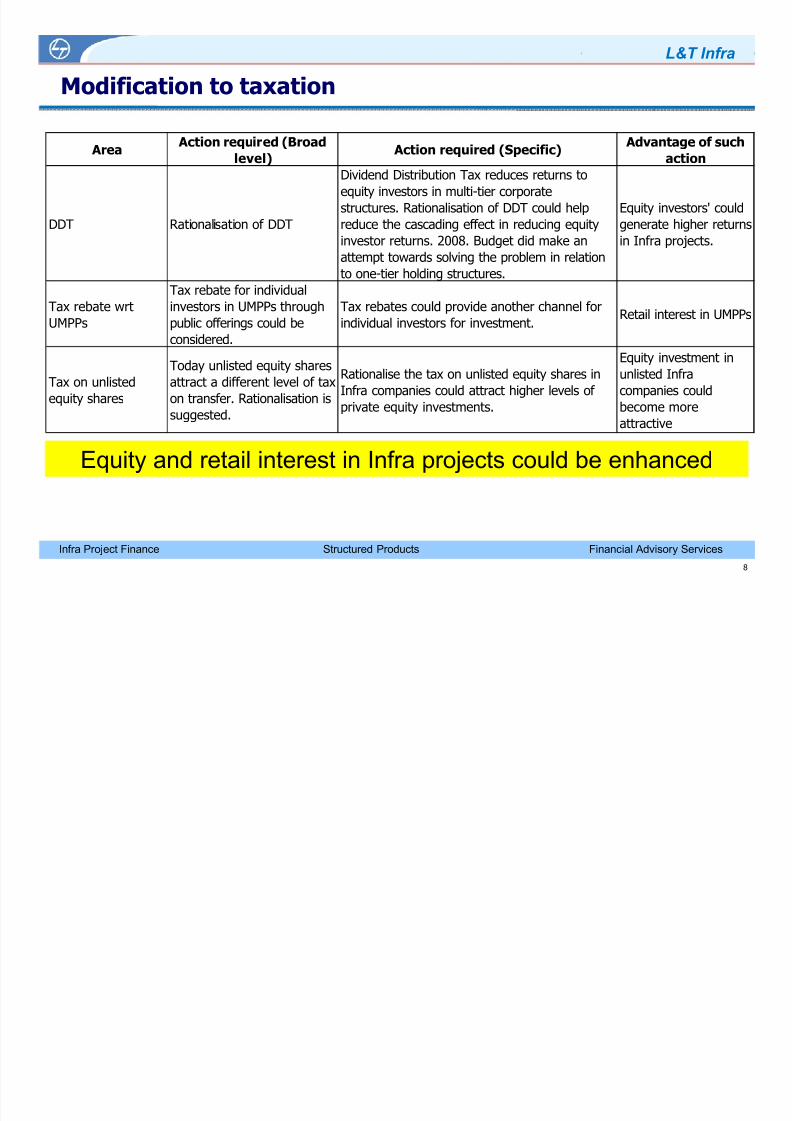

Equity and retail interest in Infra projects could be enhanced

Modification to taxation

Area Action required (Broad

level) Action required (Specific)

Advantage of such

action

DDT Rationalisation of DDT

Dividend Distribution Tax reduces returns to

equity investors in multi-tier corporate

structures. Rationalisation of DDT could helpreduce the cascading effect in reducing equity

investor returns. 2008. Budget did make an

attempt towards solving the problem in relation

to one-tier holding structures.

Equity investors' couldgenerate higher returns

in Infra projects.

Tax rebate wrt

UMPPs

Tax rebate for individual

investors in UMPPs through

public offerings could beconsidered.

Tax rebates could provide another channel for

individual investors for investment.Retail interest in UMPPs

Tax on unlisted

equity shares

Today unlisted equity shares

attract a different level of tax

on transfer. Rationalisation is

suggested.

Rationalise the tax on unlisted equity shares in

Infra companies could attract higher levels of

private equity investments.

Equity investment in

unlisted Infra

companies could

become more

attractive

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 9/14

9

L&T Infra

Infra Project Finance Financial Advisory ServicesStructured Products

Annex

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 10/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

10

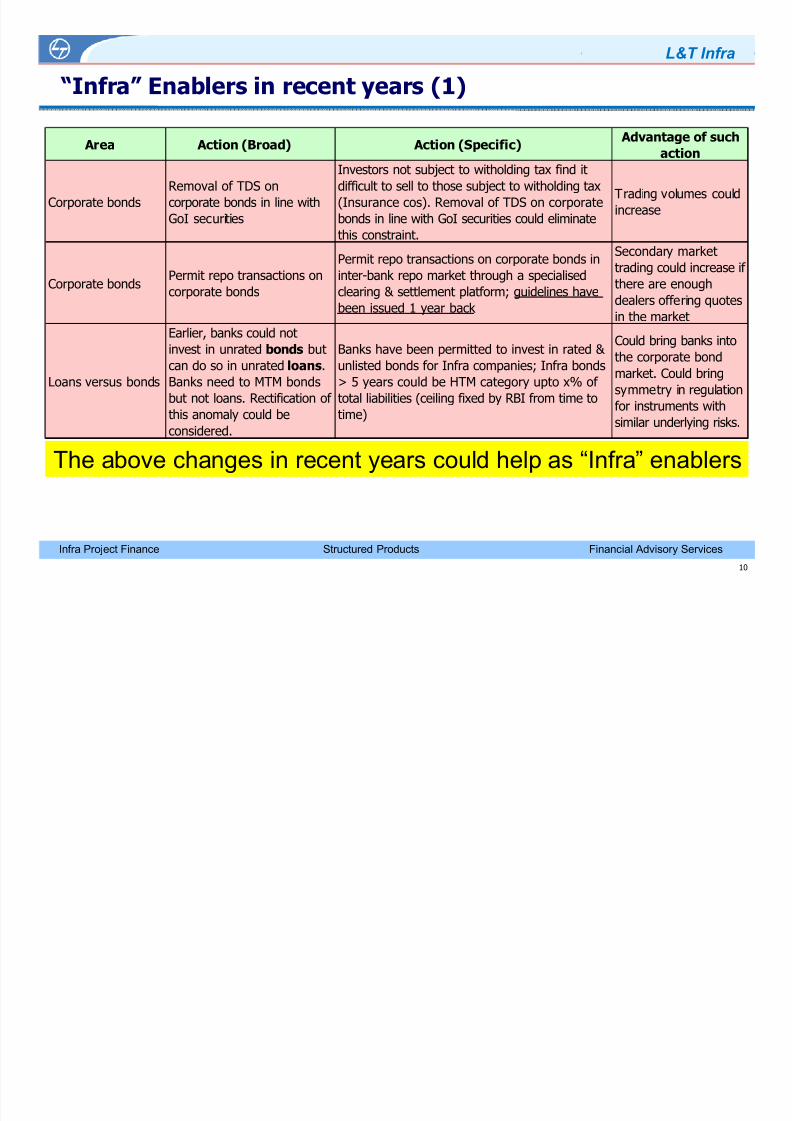

The above changes in recent years could help as “Infra” enablers

“Infra” Enablers in recent years (1)

Area Action (Broad) Action (Specific) Advantage of such

action

Corporate bonds

Removal of TDS on

corporate bonds in line with

GoI securities

Investors not subject to witholding tax find it

difficult to sell to those subject to witholding tax

(Insurance cos). Removal of TDS on corporate

bonds in line with GoI securities could eliminatethis constraint.

Trading volumes could

increase

Corporate bondsPermit repo transactions on

corporate bonds

Permit repo transactions on corporate bonds in

inter-bank repo market through a specialised

clearing & settlement platform; guidelines have

been issued 1 year back

Secondary market

trading could increase if

there are enough

dealers offering quotes

in the market

Loans versus bonds

Earlier, banks could not

invest in unrated bonds but

can do so in unrated loans.

Banks need to MTM bonds

but not loans. Rectification of

this anomaly could be

considered.

Banks have been permitted to invest in rated &

unlisted bonds for Infra companies; Infra bonds

> 5 years could be HTM category upto x% of

total liabilities (ceiling fixed by RBI from time to

time)

Could bring banks into

the corporate bond

market. Could bring

symmetry in regulation

for instruments with

similar underlying risks.

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 11/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

11

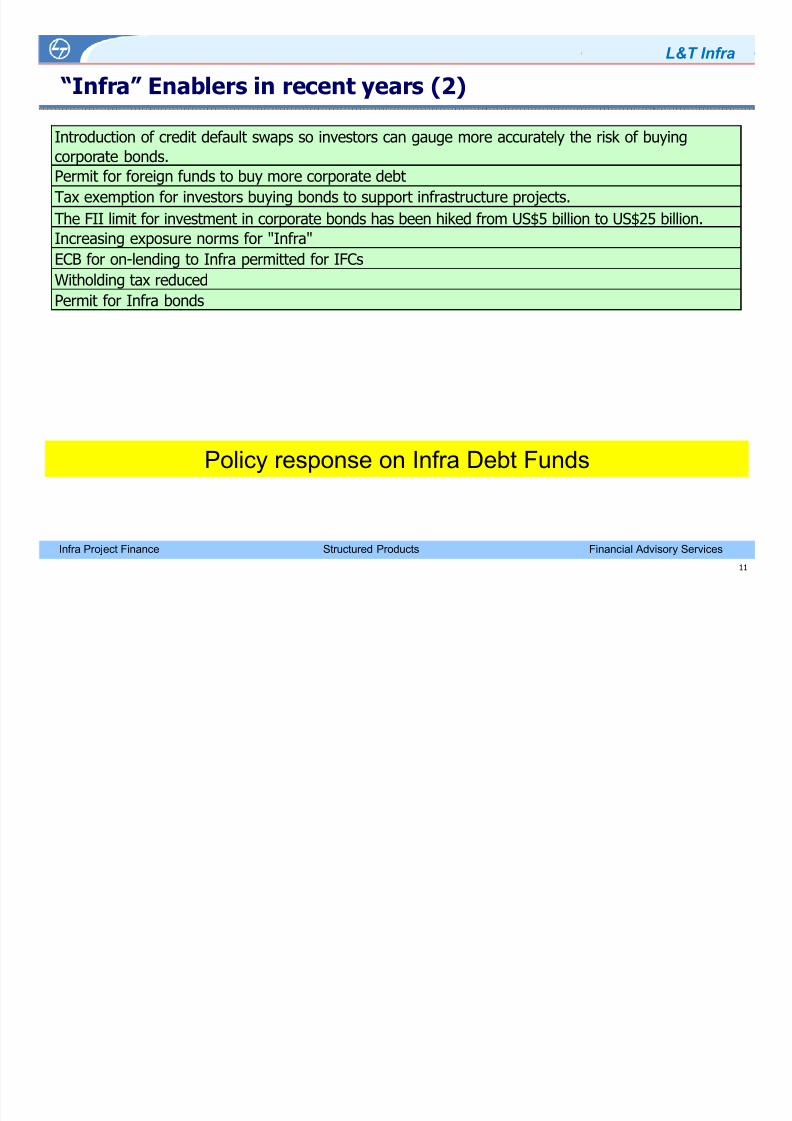

Introduction of credit default swaps so investors can gauge more accurately the risk of buying

corporate bonds.

Permit for foreign funds to buy more corporate debt

Tax exemption for investors buying bonds to support infrastructure projects.

The FII limit for investment in corporate bonds has been hiked from US$5 billion to US$25 billion.Increasing exposure norms for "Infra"

ECB for on-lending to Infra permitted for IFCs

Witholding tax reduced

Permit for Infra bonds

“Infra” Enablers in recent years (2)

Policy response on Infra Debt Funds

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 12/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

12

Key issues for Infra projects (1)

Land acquisition

Environmental regulations/ guidelines

Fuel linkages Project execution capacity issues due to non-availability

of skilled labour

Policy clarity in telecom/ litigation Power evacuation Infra

Import of coal – port inadequacies

Availability of railway rakes

Water availability for projects

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 13/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

13

Key issues for Infra projects (2)

Financial losses of distribution entities

Aggressive bids in solar, roads

Mining – Bellary issues – Iron Ore Port connectivity and deep draft

Subdued equity market conditions

Low liquidity of corporate bond markets

Low levels of credit enhancement due to lack of credit

enhancers

8/3/2019 S5_110930 PPP Presn_Ramesh Bhujang_Infra Finance

http://slidepdf.com/reader/full/s5110930-ppp-presnramesh-bhujanginfra-finance 14/14

Infra Project Finance Financial Advisory ServicesStructured Products

L&T Infra

14

Sources

Secondary sources/ Annual Report/ Press articles

Government Committee Reports

SEBI/ FII/ IFCs IBEF/ RBI Annual Report/ BK Chaturvedi report

RBI Governors’ speeches