Embed Size (px)

Citation preview

RUSSIAN SHOPPERS IN NEW ECONOMIC ENVIRONMENT

RESEARCH FINDINGS

SEPTEMBER 2014

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

2

The Client is not authorised to publish and/or adapt this research report,

whether in whole or in part(s), in the press, on the radio, on television, in

leaflets, data search systems, litigations etc. without prior written consent of

Nielsen .

Consent for publication should be sought from Nielsen each time.

CONFIDENTIALITY

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

3

THE CONTENT

RESEARCH DESIGN 4

MAIN FINDINGS 5

SHOPPER IN NEW ECONOMIC ENVIRONMENT 8

PURCHASE BEHAVIOUR BY CATEGORIES 14

SHOPPER UNDER IMPORT EMBARGO 26

SHOPPER PROFILE 37

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

4

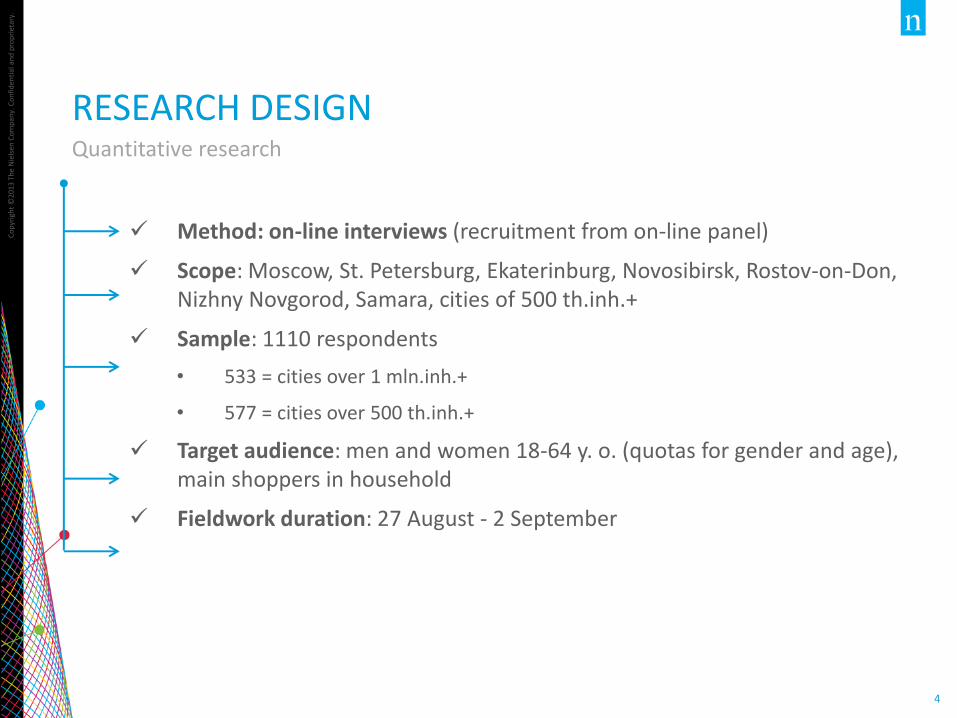

RESEARCH DESIGN Quantitative research

Method: on-line interviews (recruitment from on-line panel)

Scope: Moscow, St. Petersburg, Ekaterinburg, Novosibirsk, Rostov-on-Don, Nizhny Novgorod, Samara, cities of 500 th.inh.+

Sample: 1110 respondents

• 533 = cities over 1 mln.inh.+

• 577 = cities over 500 th.inh.+

Target audience: men and women 18-64 y. o. (quotas for gender and age), main shoppers in household

Fieldwork duration: 27 August - 2 September

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

5

MAIN FINDINGS Level of shopper optimism

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

6

MAIN FINDINGS Changes in FMCG consumption

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

7

MAIN FINDINGS Consumption under import embargo

SHOPPER IN NEW ECONOMIC ENVIRONMENT

• LEVEL OF SHOPPER OPTIMISM • INCOME AND SAVINGS • CHANGE IN CONSUMER BEHAVIOUR • STRATEGIES OF SAVING • CHANGES OF CONSUMER BEHAVIOUR BY CHANNELS

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

9

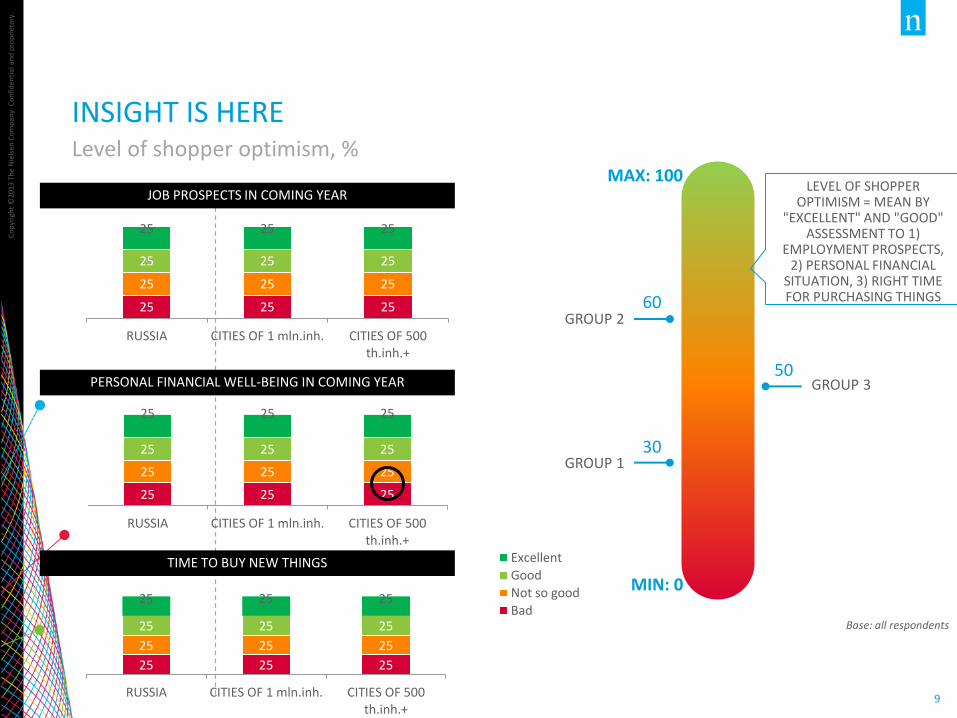

INSIGHT IS HERE Level of shopper optimism, %

25 25 25

25 25 25

25 25 25

25 25 25

RUSSIA CITIES OF 1 mln.inh. CITIES OF 500th.inh.+

JOB PROSPECTS IN COMING YEAR

25 25 25

25 25 25

25 25 25

25 25 25

RUSSIA CITIES OF 1 mln.inh. CITIES OF 500th.inh.+

Excellent

Good

Not so good

Bad

25 25 25

25 25 25

25 25 25

25 25 25

RUSSIA CITIES OF 1 mln.inh. CITIES OF 500th.inh.+

PERSONAL FINANCIAL WELL-BEING IN COMING YEAR

Base: all respondents

TIME TO BUY NEW THINGS

GROUP 3

GROUP 1

MAX: 100

MIN: 0

LEVEL OF SHOPPER OPTIMISM = MEAN BY

"EXCELLENT" AND "GOOD" ASSESSMENT TO 1)

EMPLOYMENT PROSPECTS, 2) PERSONAL FINANCIAL

SITUATION, 3) RIGHT TIME FOR PURCHASING THINGS

50

GROUP 2 60

30

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

10

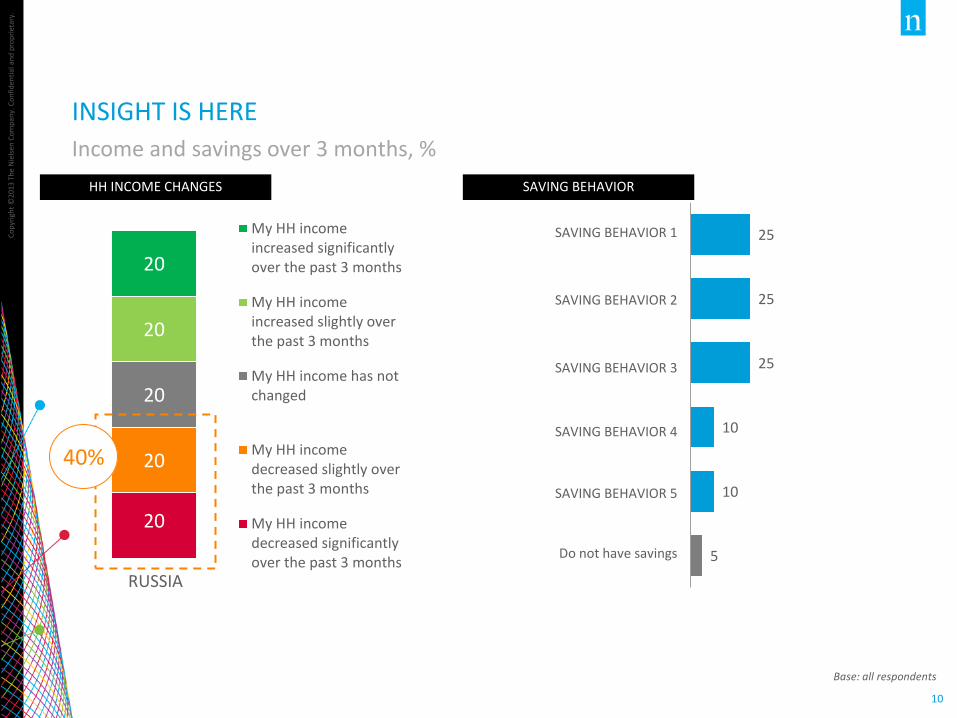

20

20

20

20

20

My HH incomeincreased significantlyover the past 3 months

My HH incomeincreased slightly overthe past 3 months

My HH income has notchanged

My HH incomedecreased slightly overthe past 3 months

My HH incomedecreased significantlyover the past 3 months

25

25

25

10

10

5

INSIGHT IS HERE

Income and savings over 3 months, %

Base: all respondents

HH INCOME CHANGES SAVING BEHAVIOR

SAVING BEHAVIOR 1

SAVING BEHAVIOR 2

SAVING BEHAVIOR 3

SAVING BEHAVIOR 4

SAVING BEHAVIOR 5

Do not have savings

RUSSIA

40%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

11

25 25 25 25

Definitely yes Probably yes Probably no Definitely no

INSIGHT IS HERE

Overall changes in consumer behavior over 3 months, %

33

33

34

Buy less FMCG

Buy the same amount of FMCG

Buy more FMCG

CHANGES IN FMCG-CONSUMPTION

CHANGE IN SPENDING

Base: all respondents

XX %

XX %

Base: n=241

Base: n=625

% AVERAGE CHANGES

20

20

20

20

20

Spend significantly more money

Spend slightly more money

Spend the same amount of money

Spend slightly less money

Spend significantly less money

33

33

34

Less 16% 16%-25% More 25%

BECAME MORE THRIFTY? 50%

33

33

34

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

12

10

10

10

10

10

10

10

10

10

INSIGHT IS HERE

Overall changes in consumer behavior over 3 months, %

Base: all respondents

20

20

20

20

20

Prices increased significantly

Prices increased slightly

Prices have not changed

Prices decreased slightly

Prices decreased significantly

CHANGES IN PRICES XX %

20

20

20

20

20

Range of products grown significantly

Range of products grown slightly

Range of products has not changed

Range of products decreased slightly

Range of products decreased significantly

CHANGES IN ASSORTMENT

AVERAGE % OF PRICE CHANGE

40%

40%

STRATEGY 1

STRATEGY 2

STRATEGY 3

STRATEGY 4

STRATEGY 5

STRATEGY 6

STRATEGY 7

STRATEGY 8

No action

STRATEGIES OF SAVING

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

13

33

33

33

33

33

33

33

33

33

33

33

33

33

33

33

33

34

34

34

34

34

34

34

34

DISCOUNTERS

HYPERMARKETS

OPEN MARKETS

CASH&CARRY

SUPERMARKETS

MINIMARKETS

TT STORES

KIOSKS/PAVILIONS

Has started to buy more than 3 months ago The same as 3 months ago

Has started to buy less than 3 months ago

INSIGHT IS HERE Changes in consumption by channels over 3 months, %

Base: all visitors of channels

PURCHASE BEHAVIOUR BY CATEGORIES

• CHANGES IN CONSUMER BEHAVIOUR BY CATEGORIES • REASONS FOR CHANGES IN CONSUMER BEHAVIOUR • PRICE CHANGE BY CATEGORY • SAVING STRATEGIES BY CATEGORY • CATEGORIES-INDICATORS OF PRICE LEVEL

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

15

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

Beer

Bottled / mineral water

Boxes of chocolate pralines

Carbonated soft drinks

Cereals, pasta

Cheese

Chips, crackers, and other snacks

Chocolate

Coffee

Fresh fruit and vegetables

Fresh meat, poultry, fish

Frozen food

Fruit juices

Meat products, sausages

Modern dairy

Packed sweets

Pet food

Premium alcohol

Tea

Traditional dairy

Vodka

Have stopped buying now Buy less than 3 months ago Buy the same as 3 months ago Buy more than 3 months ago

Changes in consumption by categories over 3 months (food products), %

INSIGHT IS HERE

Base: category shoppers

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

16

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

Diapers

Feminine products

Hair care

Household cleaners

Laundry detergents

Paper products

Personal care

Have stopped buying now Buy less than 3 months ago Buy the same as 3 months ago Buy more than 3 months ago

Changes in consumption by categories over 3 months (non-food products), %

INSIGHT IS HERE

Base: category shoppers

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

17

50

50

50

50

50

50

50

50

50

50

50

50

50

50

50

50

50

50

50

50

50

Beer

Bottled / mineral water

Boxes of chocolate pralines

Carbonated soft drinks

Cereals, pasta

Cheese

Chips, crackers, and other snacks

Chocolate

Coffee

Expensive alcohol

Forage for animals

Fresh fruit and vegetables

Fresh meat, poultry, fish

Frozen foods

Fruit juices

Meat products, sausages

Modern dairy products

Packaged candy

Tea

Traditional dairy products

Vodka

25

25

25

25

25

25

25 25

25

25

25

25

25

25

25

25 25

25

25

25

25

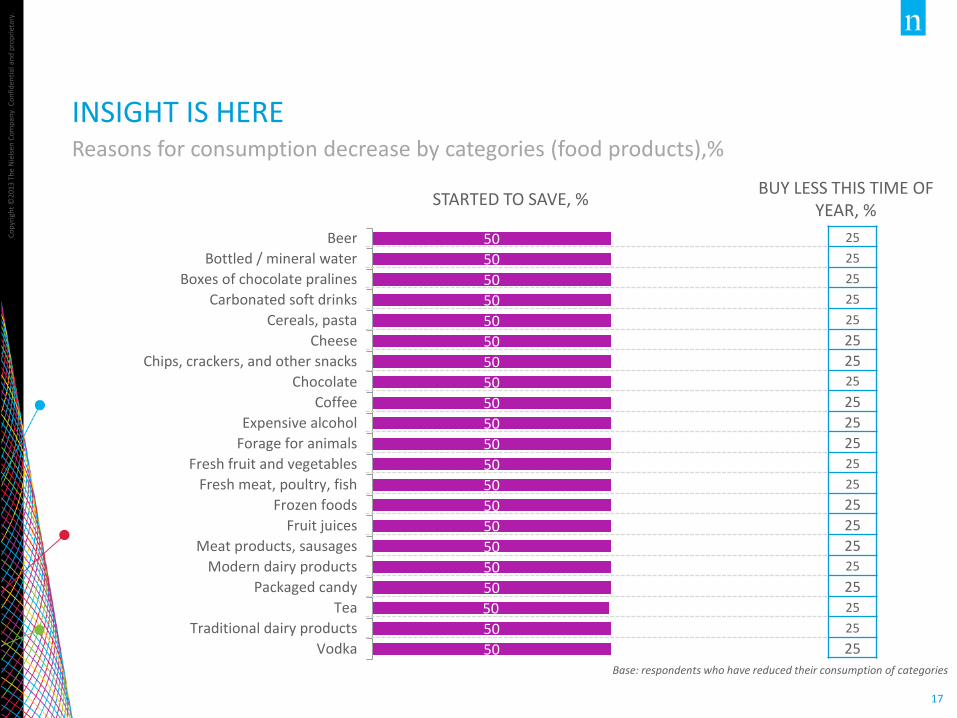

INSIGHT IS HERE Reasons for consumption decrease by categories (food products),%

Base: respondents who have reduced their consumption of categories

STARTED TO SAVE, % BUY LESS THIS TIME OF

YEAR, %

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

18

50

50

50

50

50

50

50

50

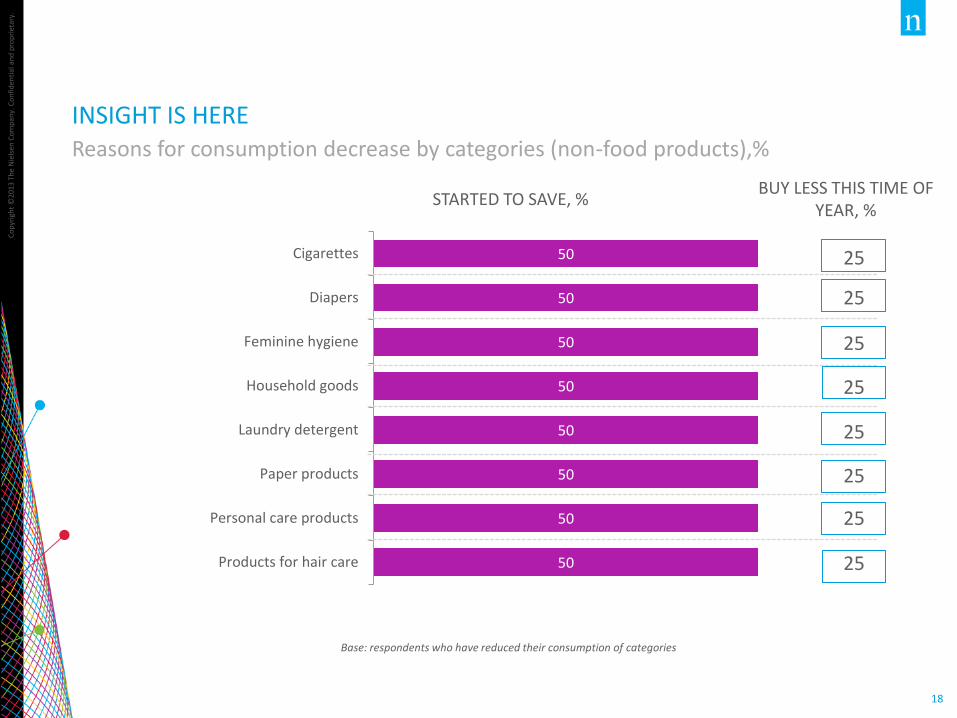

Cigarettes

Diapers

Feminine hygiene

Household goods

Laundry detergent

Paper products

Personal care products

Products for hair care

INSIGHT IS HERE Reasons for consumption decrease by categories (non-food products),%

25

25

25

25

25

25

25

25

STARTED TO SAVE, % BUY LESS THIS TIME OF

YEAR, %

Base: respondents who have reduced their consumption of categories

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

19

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

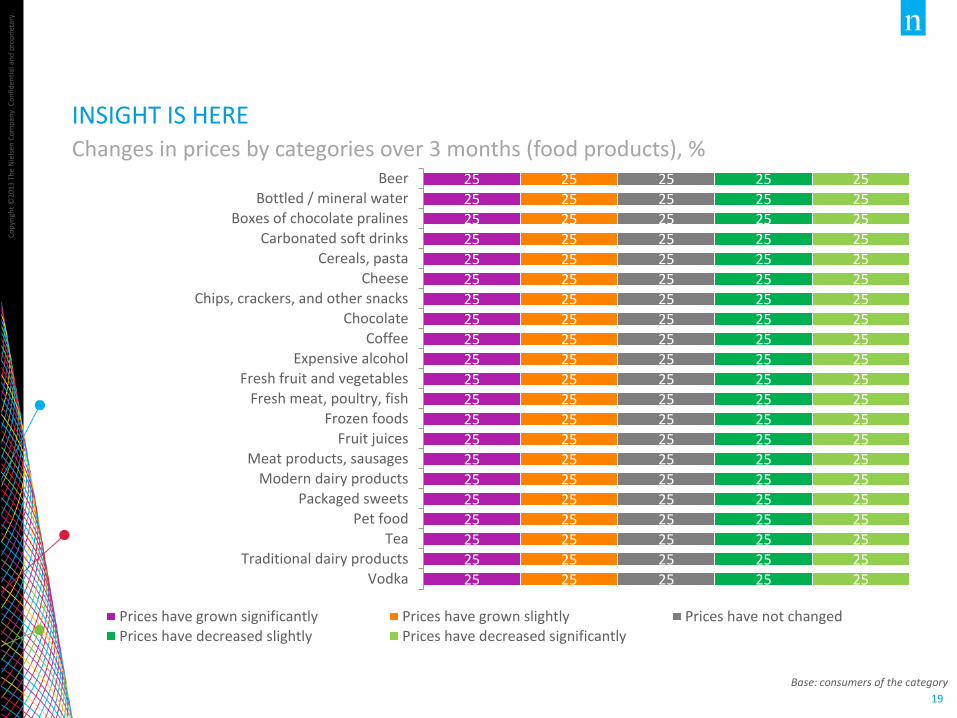

Beer

Bottled / mineral water

Boxes of chocolate pralines

Carbonated soft drinks

Cereals, pasta

Cheese

Chips, crackers, and other snacks

Chocolate

Coffee

Expensive alcohol

Fresh fruit and vegetables

Fresh meat, poultry, fish

Frozen foods

Fruit juices

Meat products, sausages

Modern dairy products

Packaged sweets

Pet food

Tea

Traditional dairy products

Vodka

Prices have grown significantly Prices have grown slightly Prices have not changedPrices have decreased slightly Prices have decreased significantly

INSIGHT IS HERE Changes in prices by categories over 3 months (food products), %

Base: consumers of the category

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

20

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

25

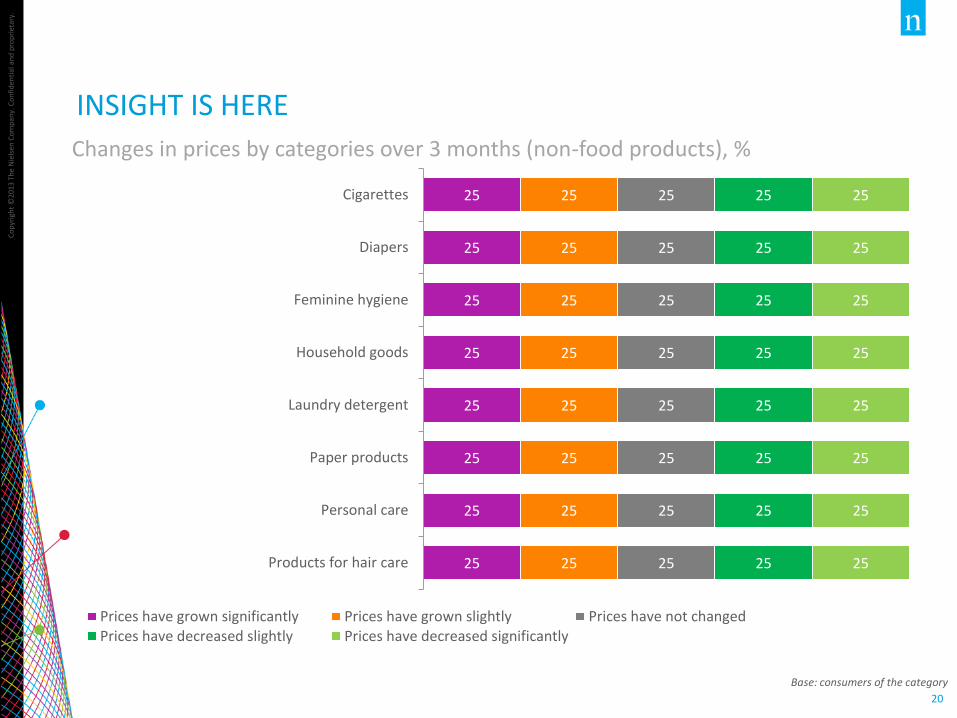

Cigarettes

Diapers

Feminine hygiene

Household goods

Laundry detergent

Paper products

Personal care

Products for hair care

Prices have grown significantly Prices have grown slightly Prices have not changedPrices have decreased slightly Prices have decreased significantly

INSIGHT IS HERE

Changes in prices by categories over 3 months (non-food products), %

Base: consumers of the category

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

21

FRESH FOOD PRODUCTS DAIRY CATEGORIES

Fresh vegetables and fruit

Fresh meat, poultry, fish

Traditional dairy products

Modern dairy products

Cheese

n= n= n= n= n=

INSIGHT IS HERE

Saving strategies by category, in 3 months (food products), % Base: consumers of the category, who noticed an increase in prices

Strategy 1 30 30 30 30 30

Strategy 2 25 25

25 25 25

Strategy 3 20 20 20 20 20

Strategy 4 20 20 20 20 20

Strategy 5 15 15 15 15 15

Strategy 6 15 15

15 15 15

Strategy 7 10 10 10 10 10

Strategy 8 10 10 10 10 10

Strategy 9 5 5 5 5 5

Nothing has changed 25 25 25 25 25

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

22

OTHER FOOD CATEGORIES

Meat products, sausages

Chips, crackers,

and other snacks

Boxes of chocolate pralines

Packaged sweets

Chocolate Cereals,

pasta Frozen food

Pet food Tea Coffee

n= n= n= n= n= n= n= n= n= n=

INSIGHT IS HERE Saving strategies by category, in 3 months (food products), % Base: consumers of the category, who noticed an increase in prices

Strategy 1 30 30 30 30 30 30 30 30 30 30

Strategy 2 25 25 25 25 25 25 25 25 25 25

Strategy 3 20 20 20 20 20 20 20 20 20 20

Strategy 4 20 20 20 20 20 20 20 20 20 20

Strategy 5 15 15 15 15 15 15 15 15 15 15

Strategy 6 15 15 15 15 15 15 15 15 15 15

Strategy 7 10 10 10 10 10 10 10 10 10 10

Strategy 8 10 10 10 10 10 10 10 10 10 10

Strategy 9 5 5 5 5 5 5 5 5 5 5

Nothing has changed 25 25 25 25 25 25 25 25 25 25

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

23

DRINKS

Carbonated soft drinks

Fruit juices Bottled water/

mineral water Beer

Premium alcohol

Vodka

n= n= n= n= n= n=

INSIGHT IS HERE Saving strategy by categories in 3 months (drinks), % Base: consumers of the category, who noticed an increase in prices

Strategy 1 30 30 30 30 30 30

Strategy 2 25 25 25 25 25 25

Strategy 3 20 20 20 20 20 20

Strategy 4 20 20 20 20 20 20

Strategy 5 15 15 15 15 15 15

Strategy 6 15 15 15 15 15 15

Strategy 7 10 10 10 10 10 10

Strategy 8 10 10 10 10 10 10

Strategy 9 5 5 5 5 5 5

Nothing has changed 25 25 25 25 25 25

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

24

NON-FOOD PRODUCTS

Paper products

Personal hygiene products

Products for hair care

Laundry detergents

Household goods

Feminine hygiene products

Diapers Cigarettes

n= n= n= n= n= n= n= n=

INSIGHT IS HERE Saving strategies by category, in 3 months (non-food products), % Base: consumers of the category, who noticed an increase in prices

Strategy 1 30 30 30 30 30 30 30 30

Strategy 2 25 25 25 25 25 25 25 25

Strategy 3 20 20 20 20 20 20 20 20

Strategy 4 20 20 20 20 20 20 20 20

Strategy 5 15 15 15 15 15 15 15 15

Strategy 6 15 15 15 15 15 15 15 15

Strategy 7 10 10 10 10 10 10 10 10

Strategy 8 10 10 10 10 10 10 10 10

Strategy 9 5 5 5 5 5 5 5 5

Nothing has changed 25 25 25 25 25 25 25 25

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

25

10

10

10

10

10

10

10

10

10

10

Cereals, pasta

Cheese

Coffee

Fresh fruit and vegetables

Fresh meat, poultry, fish

Household goods

Meat products, sausages

Modern dairy products

Tea

Traditional dairy products

INSIGHT IS HERE Indicators of store price level (TOP 10), %

Base: all respondents

1 0

-1 1

-1 1

1 -1

1 -1

-1 1

1 -1

0 0

-1 1

-1 1

CITIES OF 1 MLN. INH CITIES OF 500 TH.+ INH

* DIFFERENCE FROM RUSSIA LEVEL

SHOPPER UNDER IMPORT EMBARGO

• CONCERNS ABOUT EMBARGO • POSITIVE AND NEGATIVE EFFECTS • OBSERVED CHANGES AND STRATEGIES OF SAVING • POSSIBLE RESULT OF IMPORT EMBARGO • CATEGORIES OF CONSUMPTION • CATEGORIES OF CONCERN • STRATEGIES FOR SAVING IN BANNED CATEGORIES • POSSIBLE STRATEGIES FOR SAVING IN BANNED CATEGORIES • OOS CONSUMPTION

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

27

20 20 20 20 20

Much concernedSlightly concernedNeutralRather not concernedAbsolutely not concerned

Base: all respondents

INSIGHT IS HERE Concern about embargo, %

AWARENESS OF IMPORT EMBARGO

CONCERN ABOUT IMPORT EMBARGO

50 50 Aware

Unaware 10

10

10

10

10

1

2

3

4

5

WHAT GIVES RISE TO CONCERN (TOP 5)

Base: respondents concerned about import embargo

40%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

28

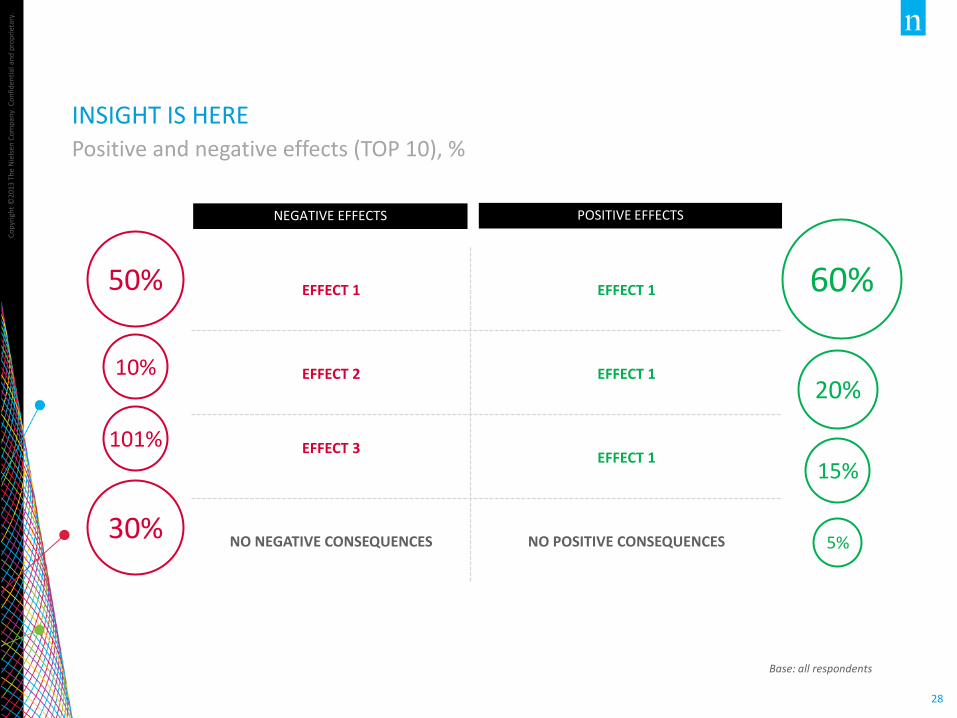

INSIGHT IS HERE Positive and negative effects (TOP 10), %

Base: all respondents

EFFECT 1 EFFECT 1

EFFECT 2 EFFECT 1

EFFECT 3

EFFECT 1

NO NEGATIVE CONSEQUENCES NO POSITIVE CONSEQUENCES

POSITIVE EFFECTS NEGATIVE EFFECTS

50%

30%

10%

101%

60%

20%

15%

5%

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

29

30

25

20

15

10

5

5

50

INSIGHT IS HERE Observed changes, strategies of saving, %

Base: all respondents

STRATEGIES OF SAVING

30

25

20

15

10

5

5

5

50

OBSERVED CHANGES

Strategy 1

Strategy 2

Strategy 3

Strategy 4

Strategy 5

Strategy 6

Strategy 7

Strategy 8

No any strategy

Strategy 1

Strategy 2

Strategy 3

Strategy 4

Strategy 5

Strategy 6

Strategy 7

No any strategy

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

30

20 20 20 20 20

Will affect very significantly

Will affect significantly

Will affect slightly

Will have no effect, probably

Will have no effect at all

20 20 20 20

Prices will rise significantly

Prices will rise slightly

No changes

Prices wiil decrease slightly

Prices will drop significantly

INSIGHT IS HERE Possible consequences of the sanctions, %

15 15 15 15 20 20

Necessary products will not be available

Range of products will decrease considerably

Range of products will decrease slightly

No changes

Range of products will grow slightly

Range of products will grow significantly

CHANGES IN ASSORTMENT

20 20 20 20 20

Quality of products will significantly deteriorate

Product quality will deteriorate slightly

No changes

Quality of products will slightly improve

Quality of products will significantly improve

CHANGES IN PRICES

CHANGES IN PRODUCTS QUALITY

Base: all respondents Base:

Base: Base:

IMPACT ON REGION ECONOMY

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

31

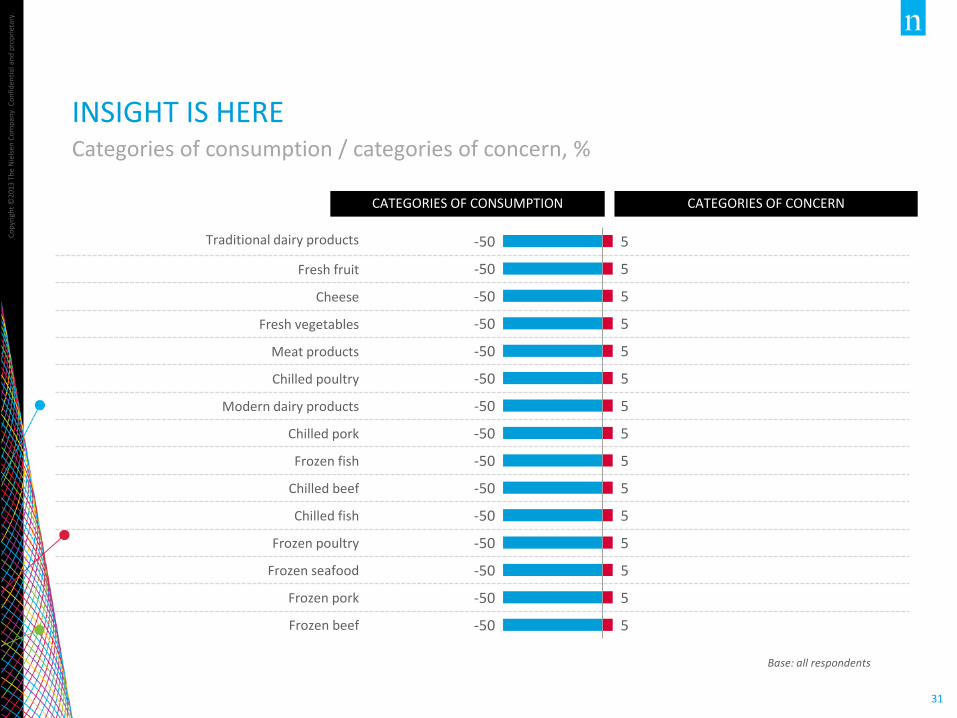

Traditional dairy products

Fresh fruit

Cheese

Fresh vegetables

Meat products

Chilled poultry

Modern dairy products

Chilled pork

Frozen fish

Chilled beef

Chilled fish

Frozen poultry

Frozen seafood

Frozen pork

Frozen beef

INSIGHT IS HERE Categories of consumption / categories of concern, %

Base: all respondents

CATEGORIES OF CONCERN

-50

-50

-50

-50

-50

-50

-50

-50

-50

-50

-50

-50

-50

-50

-50

5

5

5

5

5

5

5

5

5

5

5

5

5

5

5

CATEGORIES OF CONSUMPTION

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

32

FRESH FOOD PRODUCTS DAIRY CATEGORIES

Fresh vegetables Fresh fruit Traditional dairy

products Modern dairy

products Cheese

n= n= n= n= n=

INSIGHT IS HERE Strategies of saving by categories, % Base: consumers of the category

Strategy 1 30 30 30 30 30

Strategy 2 25 25 25 25 25

Strategy 3 20 20 20 20 20

Strategy 4 20 20 20 20 20

Strategy 5 15 15 15 15 15

Strategy 6 15 15 15 15 15

Strategy 7 10 10 10 10 10

Strategy 8 10 10 10 10 10

Strategy 9 5 5 5 5 5

Strategy 10 5 5 5 5 5

I buy the same as before 50 50 50 50 50

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

33

MEAT / MEAT PRODUCTS

Chilled pork Chilled beef Chilled poultry Meat

products Chilled fish Frozen fish

n= n= n= n= n= n=

INSIGHT IS HERE Strategies of saving by categories, %

FISH Base: consumers of the category

Strategy 1 30 30 30 30 30 30

Strategy 2 25 25 25 25 25 25

Strategy 3 20 20 20 20 20 20

Strategy 4 20 20 20 20 20 20

Strategy 5 15 15 15 15 15 15

Strategy 6 15 15 15 15 15 15

Strategy 7 10 10 10 10 10 10

Strategy 8 10 10 10 10 10 10

Strategy 9 5 5 5 5 5 5

Strategy 10 5 5 5 5 5 5

I buy the same as before 50 50 50 50 50 50

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

34

FRESH FOOD PRODUCTS DAIRY CATEGORIES

Fresh vegetables Fresh fruit Traditional dairy

products Modern dairy

products Cheese

n= n= n= n= n=

INSIGHT IS HERE Possible strategies of saving by categories, % Base: consumers of the category

Strategy 1 30 30 30 30 30

Strategy 2 20 20 20 20 20

Strategy 3 20 20 20 20 20

Strategy 4 15 15 15 15 15

Strategy 5 15 15 15 15 15

Strategy 6 10 10 10 10 10

Strategy 7 10 10 10 10 10

Strategy 8 5 5 5 5 5

Strategy 9 5 5 5 5 5

I will buy the same way as before 50 50 50 50 50

Co

pyr

igh

t ©

2012

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

35

MEAT / MEAT PRODUCTS

Chilled pork Chilled beef Chilled poultry Meat

products Chilled fish Frozen fish

n= n= n= n= n= n=

INSIGHT IS HERE Possible strategies of saving by categories, %

FISH Base: consumers of the category

Strategy 1 30 30 30 30 30 30

Strategy 2 20 20 20 20 20 20

Strategy 3 20 20 20 20 20 20

Strategy 4 15 15 15 15 15 15

Strategy 5 15 15 15 15 15 15

Strategy 6 10 10 10 10 10 10

Strategy 7 10 10 10 10 10 10

Strategy 8 5 5 5 5 5 5

Strategy 9 5 5 5 5 5 5

I will buy the same way as before 50 50 50 50 50 50

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

36

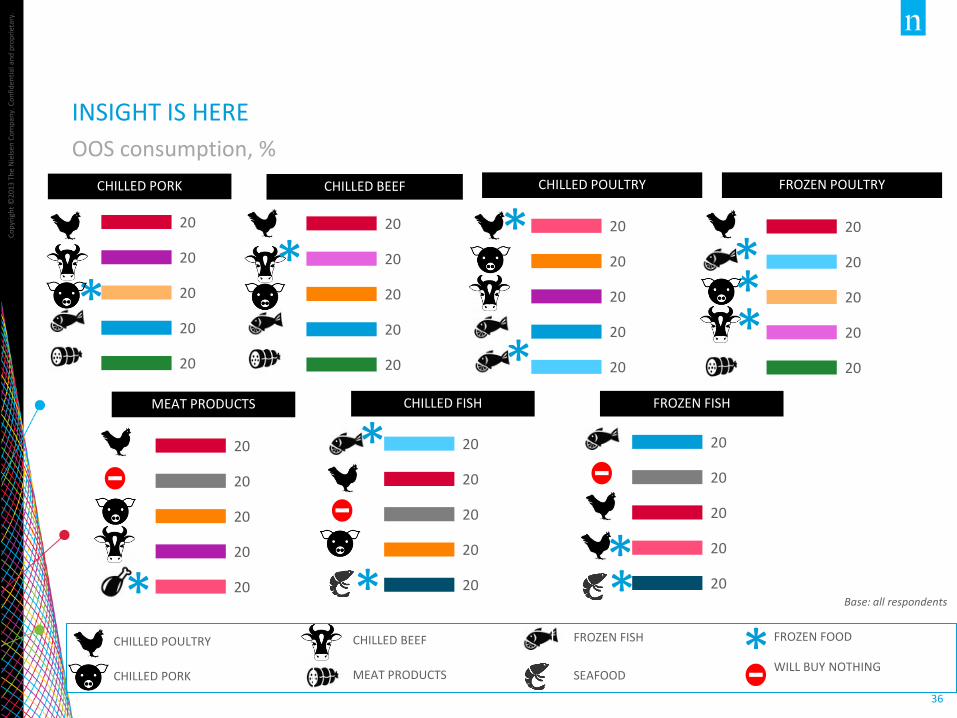

FROZEN FOOD

WILL BUY NOTHING

FROZEN FISH

SEAFOOD

INSIGHT IS HERE

OOS consumption, %

Base: all respondents

20

20

20

20

20

CHILLED PORK

20

20

20

20

20

CHILLED BEEF

20

20

20

20

20

CHILLED POULTRY

*

*

20

20

20

20

20

FROZEN POULTRY

20

20

20

20

20

MEAT PRODUCTS

*

20

20

20

20

20

CHILLED FISH

*

* 20

20

20

20

20

FROZEN FISH

* *

CHILLED BEEF

MEAT PRODUCTS

CHILLED POULTRY

CHILLED PORK *

* *

* * *

SHOPPERS' PROFILE

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

38

20

20

20

20

20 18 – 24

25 – 34

35 – 44

45 – 54

55 – 64

SHOPPERS' PROFILE

Base: all respondents

50% 50%

25%

25%

25%

25% +

Average age XX

Number of family members AGE

GENDER

Co

pyr

igh

t ©

2013

Th

e N

iels

en C

om

pan

y. C

on

fid

enti

al a

nd

pro

pri

etar

y.

39

15

15

15

15

20

20

Higher

Professional trainingat technical college

Incomplete higher

Secondary - highschool, vocationalschoolIncompletesecondary

MBA

SHOPPERS' PROFILE

Base: all respondents

10

10

10

10

10

10

10

10

10

10

Specialist with highereducation, without…

Head of the department,division

Temporarily not working,unemployed, looking for…

Worker

Employee without highereducation

Non-working pensioner

Business owner /entrepreneur

A student (full-time)

Domestic service staff

Managing employee of acompany, institution