Embed Size (px)

Citation preview

Russia, a promising and exciting business environment

ABN AMRO Group Public Affairs: Economics Department: Marijke Zewuster, [email protected] Sector Research: Jan van den Berg, [email protected] Thijs Pons, [email protected] Commissioned by: Sector Advisory NL: Willem Rol Commercial Client Segment / IDCC: Nico Overwijn Finalised: September 2007

Russia

2 Economics Department/Sector Research, September 2007

Introduction When evaluating Russia, from whatever perspective, there are usually two extremes: from very sceptical or even unfavourable to nearly euphoric. From the perspective of a foreigner who has spent some three and a half very bright and intense years in the country, I can confirm the saying by the Russian poet Tutchev that there is no intellectual understanding of Russia, nor can it be measured with a standard arshin (old Russian measure that equals 0.711 metre). It can indeed be anything, but never dull. Russia is unique, diverse, challenging, exciting and promising. I could extend this list of epithets further, but the incontestable facts about Russia’s current economic situation and its potential, analysed in detail in this report, speak for themselves. The fundamentals are very strong. Russia’s GDP growth rate for the last five years has substantially exceeded that of most industrially developed countries. Growth is driven by high commodity prices and booming domestic consumer demand. Favourable prices for commodities, such as oil, gas, gold, nickel and many others that Russia has in abundance, have created excess cash in both the public and private sectors and a positive current account balance. Russian currency and gold reserves – the world’s third-largest – reached historical highs of over USD 420 bn in mid-September 2007. Inflation is coming down, the rouble is quickly becoming a currency to be reckoned with and the sovereign rating has increased to well beyond investment grade level. In summary, the Russian economy has transformed to become one of the largest (ranking ninth) and most important economies in the world. And I am convinced that this is only the beginning, given all the potential (size of the market, availability of high-quality labour, growth potential, etc.) that is yet to be tapped. The Russian Government is putting a lot of effort into attracting more investment into the country and improving the investment climate in general. It has created investment institutions such as the Investment Fund and the Development Bank to ensure investments in all sectors of the economy as well as infrastructure projects. “I want to note that 300 billion rubles [currently about USD12 bn] have been allocated to these institutions this year alone. Moreover, we have put in place a mechanism that ensures that these funds will increase each year, but only so long as they are used effectively”, - stated President Putin during his opening remarks at the International Investment Forum in Sochi (September 24, 2007). There is a clear willingness on the part of the government and the business community to develop a relationship, as long as it is based on mutual interests and benefits. International business and foreign investors are striving to increase their market share, strengthen their financial position, broaden their product range, ensure stability and find the best talent. Russia provides a solid basis for this. It may not happen overnight, but surely in the somewhat longer term. The coming year will be an exciting one for the country in general and the business community in particular, with parliamentary elections scheduled in December 2007 and presidential elections in early 2008. However, we all witnessed the local market’s rather limited reaction to the recent and sudden changes in the Russian Government. The market overall is very focused on

Russia

3 Economics Department/Sector Research, September 2007

business and trusts that the new government will continue the on-going projects, policies and reforms. The liquidity crisis in the international financial markets is having a much greater impact on the Russian business environment. Until now the country has been enjoying a boom in the capital markets across all sectors, with one of the fastest growing equity markets in the world (up over 1000% during the “Putin era”), and stable growth in the fixed income market. Further developments in that area will greatly depend on overall international market conditions. But of course this by no means stops many foreign companies from coming to Russia as they see much greater opportunities here than elsewhere in the world. And bear in mind that of all the BRIC countries, Russia enjoys the highest percentage of satisfied foreign investors. Over 80% of foreign businesses indicate that they are generating very attractive returns on their investments in Russia, a statistic that cannot be matched by other countries. Russia should be more and better promoted. I trust this report will give you valuable insight into the country from which it is sometimes argued that doing business is, despite its challenges, the best kept secret in the world. Henk Paardekooper, Country Executive Russia

Russia

4 Economics Department/Sector Research, September 2007

Contents

Introduction......................................................................................2

Chapter 1: Economic Overview .......................................................6 Economic structure and trade....................................................................................... 6 Economic developments .............................................................................................. 9 SWOT analysis ........................................................................................................... 13

Chapter 2: Russia’s Minerals & Mining Industry............................18 The importance of the sector to the Russian economy .............................................. 18 Exploration spending in the global mining sector ....................................................... 19 Growing demand for mining equipment...................................................................... 20 Medium-term outlook.................................................................................................. 20 Opportunities in mining equipment, services and systems......................................... 21

Chapter 3: The Russian Oil Industry .............................................22 Oil reserves ................................................................................................................ 22 Oil production ............................................................................................................. 22 Oil exports .................................................................................................................. 22 Oil production and export outlook............................................................................... 23

Chapter 4: The Russian Natural Gas Sector .................................25 Natural gas reserves .................................................................................................. 25 Natural gas production ............................................................................................... 25 Natural gas exports .................................................................................................... 26 Natural gas production and export outlook................................................................. 27 The China option ........................................................................................................ 29

Chapter 5: Opportunities in Russian Oil and Gas..........................31 Investment climate...................................................................................................... 31 Resource nationalism increasing................................................................................ 31 High investments needed ........................................................................................... 32 The E&P momentum .................................................................................................. 33

Chapter 6: Agrifood .......................................................................35 Exports from the Netherlands to Russia..................................................................... 35 Dutch companies are investing in Russia................................................................... 37

Chapter 7: “Doing Business is People’s Business” .......................39 1. Campina in Russia: ‘Ask for support from the local authorities’ ‘Establish a good relationship with the local authorities’ ......................................................................... 39 2. Jørgen de Ree, Managing Director of De Ree Holland BV ‘The Russians are loyal, reliable customers’...................................................................................................... 41 3. Mammoet in Russia A good business contact is based on friendship................... 43 4. Ottevanger Milling Engineers is successful on the Russian market ....................... 45 5. Gebroeders Van den Berk B.V. ‘With patience and respect, you can do good business in Russia’..................................................................................................... 47 6. For Econosto, Russia is a top market in the making .............................................. 49

Russia

5 Economics Department/Sector Research, September 2007

Russia

6 Economics Department/Sector Research, September 2007

Chapter 1: Economic Overview After the roaring nineties, which began with the collapse of the Soviet Union in 1991 and ended with the rouble crisis in 1998, the start of this century was characterised by a much more stable and prosperous development. The year 1999 was one of adjustment, and since president Putin took power in 2000 the Russian economy has shown an outstanding performance. The period of uninterrupted decline over the first eight years of the transition period were followed by a period of prolonged strong growth following the rouble crisis. And in fact, the end of this sustained growth is not yet in sight. The year 2006 was a milestone as it was the first year in which Russia was able to make up for the large decline in the real value of GDP during the years of transition prior to the rouble crisis. 1 With a population of over 140 million people, a nominal GDP of almost one trillion USD and rising wealth levels, Russia is not only attractive because of its rich natural resource base and related industrial investments and services, but has also become an interesting consumer market with a rising middle class. Although the positive economic developments since 1999 are mostly attributable to high energy prices and the much improved competitive position due to the sharp fall in the rouble at the end of 1998, sound macroeconomic management also played an important role. Fiscal surpluses became the rule and debt levels were reduced to the point that the government became a net creditor. The currency started to strengthen and inflation was brought under control. The much improved macroeconomic stability also enhanced the inflow of foreign investment, which rose considerably over recent years. There is, however, a flipside to these strong growth levels and the inflow of foreign capital. The central bank is having a hard time balancing the need to keep inflation in check and the risk of a strong loss in competitiveness due to the resulting strong currency. A loosening of fiscal policy in the run-up to the parliamentary elections at the end of 2007 and the presidential elections in March 2008 makes this balancing act even more difficult. Economic structure and trade Service sector has become more important The transition from a centrally planned economy towards a more market-oriented economy has led to far-reaching changes in the country’s economic structure. During the Soviet era, the focus was on heavy industry which was where most people were employed, while the service sector was underdeveloped. Already in the first years after the collapse of the Soviet Union, the economic structure changed dramatically. The share of agriculture in GDP fell from 17% in 1990 to 7% in 1995 and continued its gradual decline in the years thereafter to a current share of 5%. At the same time, the agricultural sector’s productivity declined strongly, as is evident by the fact that while its share in GDP has declined, the share in total employment has hardly changed and now stands at around 12%, against 13% in 1990. Furthermore, much of the activity in the informal economy likely takes place in the agricultural sector, which implies that even more people are making a living of farming as the statistics indicate. Estimates for the informal economy vary between 25% and 40% of GDP.

1 The cumulative decline in GDP in the period from 1991 to 1998 was 52%, while the cumulative growth in the period 1999 up to 2006 was 54%.

Russia 2006 2007 2008 % changes GDP 6.7 7.3 6.5 Inflation (average) 9.7 8.2 8.0 levels Current account (% GDP) 9.6 5.9 4.9 Budget balance (% GDP) 7.4 6.0 2.5 Government debt (% GDP) 9.0 5.0 5.0 Foreign debt (% GDP) 29 28 24 year-end Short interest rate (3m) 11.0 10.0 9.0 RUB per USD 26.3 25.3 25.5 RUB per EUR 34.6 36.7 34.4 Forecasts ABN AMRO Economics Department

Strong growth and… % GDP

-8

-4

0

4

8

12

1995 1997 1999 2001 2003 2005 2007

Source: Thomson Financial

…a strong rouble

24

28

32

36

40

Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07

—— RUB per EUR RUB per USD

Source: Thomson Financial

Russia

7 Economics Department/Sector Research, September 2007

The share of industry also showed a declining trend, with the share of industry to GDP falling from 48% in 1990 to 38% in 1995, where it still stands. Sixty percent of this continues to be heavy industry, the sector is dominated by large industrial enterprises. These statistics are not completely reliable, however. During the Soviet era, output figures were more likely overestimated while now, given the fact that tax evasion is considerable, output figures are likely to be underestimated. Services, on the other hand, increased its share from 35% of GDP in 1990 to 55% in 1995, and has remained around this level ever since. If we look at the other sectors, employment has developed more in line with the contribution of these sectors to total production. Industry’s share in employment fell from 42% in 1990 to 30% currently, while services increased its share in that period from 42% to 55%. The oil and gas sector contributes over 50% of industrial output and represents around 25% of GDP, including other oil and gas-related activities. It also generates 65% of total exports and 35% of state revenues. Due to the concentration of economic activity in the capital intensive energy sector, the current government has dedicated various measures to stimulating investments outside the resources-based industries. These measures include special zones, tax incentives, and export promotion. Meanwhile, the government is concentrating its own influence on what are called the strategic sectors of the economy, of which the oil and gas sector is obviously the most important component. Strategic sectors At the start of 2007 the Russian government finally published the long-awaited draft law on the limitation of foreign investment in the country. The law designates 40 industries as "strategic" for Russian development. Predictably, the list includes the production of military equipment, aircraft, spacecraft, ciphering tools, treatment and trade of radioactive and nuclear materials. This "strategic" status will also be assigned to fields highly endowed with natural resources, with thresholds of some 70 million tonnes for oil, 50 billion cubic metres for gas, 50 tonnes for gold and 500,000 tonnes for copper. The list of strategic industries also includes natural monopolies and arms-related metallurgy. Moreover, the regulation stipulates eight criteria for evaluating any particular company, which effectively enables any type of production to be classified as "strategic". The regulation sets up a special inter-departmental commission uniting economic and security officials to approve deals involving "strategic" companies. Its permission will be necessary for purchases and other deals related to the controlling shares of strategic companies, even if they do not belong to the state. Foreign states, their subsidiaries or international organisations will have to seek approval for deals above the 25% share threshold, and will be completely prohibited from acquiring control over "strategic"' companies. The long list of strategic industries and the provisos for potentially classifying companies beyond them as strategic, reflects the government’s increasing control over economic issues. On the other hand, the fact that there is now a policy for considering foreign involvement could lead to less uncertainty and is hence an improvement over the earlier non-transparent ad-hoc decisions.

Economic Structure Share of GDP

IndustryServices

Agriculture

Source: EIU

…real growth agriculture and industry

-20

-10

0

10

20

1996 1998 2000 2002 2004 2006 2008

—— Industry Agricutture

Source EIU

Savings and investment rate % GDP

10152025303540

1993 1995 1997 1999 2001 2003 2005 2007

—— Investment rate Savings rate

Source: Thomson Financial

Russia

8 Economics Department/Sector Research, September 2007

EU most important trading partner Since the collapse of the Soviet Union, Russia’s imports from non-CIS countries have grown rapidly, with especially strong growth in trade with the EU. The EU is by far Russia's main trading partner, accounting for around 50% of its overall trade. Total exports from Russia to the EU amounted to USD 177 billion in 2006. Of this total, around 65% involved energy and fuels, making Russia the EU’s single most important energy supplier. Imports from the EU amount to USD 61 billion. They include machinery (36%), chemicals (14%), manufactured goods (11%), transport equipment (10%), food and live animals (7%). Although the EU is clearly the most important trading partner, trade with China is quickly increasing in importance. China is now Russia’s fourth export market and the second most important source of imports. And Russia is China’s 10th leading trading partner. For the EU, however, trade with Russia is less important, given that most trade is of an intra-regional trade. Exports to Russia account for less than 5% of total EU exports, comparable to the share of exports from the EU to China. Exports to the Netherlands have also grown strongly. In 2006, exports to the Netherlands accounted for 12.3% of total exports, while this was only 4% in the period from 1995 to 2000. This makes the Netherlands Russia’s largest export destination. If we look at the import side, Germany is still number one, with a share of 14% of total imports. However, China is catching up quickly and has become the second largest supplier of imported goods, with a share of almost 10%, while the Netherlands doesn’t even appear in the top 10. However, if we take a closer look at the figures regarding trade between Russia and the Netherlands, there is a huge gap between the figures the IMF provides for Russia and those provided by the IMF for the Netherlands. According to IMF statistics for Russia, the value of imports from the Netherlands is just USD 2.7 billion, representing a share of 2% of total imports. However, if we take the same statistics for the Netherlands, the value of Dutch exports to Russia amounted to USD 7 billion. This would mean the Netherlands takes fifth position as a source of imports for Russia. The same discrepancy can be seen if we compare Dutch imports from Russia (USD 21 billion) with exports from Russia to the Netherlands (USD 36 billion). According to the IMF, the principal reason for this is related to differences in 1) classification concepts and detail, 2) time of recording, 3) valuation, 4) coverage, and 5) processing errors. Relations with both EU and US remain difficult Given the growing importance of trade relations and because they have become neighbours, both the EU and Russia have a shared interest in a stable and prosperous Europe. So far, however, the EU and Russia have not found a way of working together constructively. In fact, collaboration between Russia, the EU and the US seems to have become even more problematic. EU policy towards the east currently consists of three types of strategy; the enlargement process, the European Neighbourhood policy (ENP) and the Four Common Spaces with Russia. Plans to build the four 'common spaces' [in economics, education and research and internal and external security have made little headway. The EU-Russia summit in

Major exports (ITS) Agricultural products 6.1% Fuels and mining products 67.7% Manufactures 23.2% Source WTO

Main import markets (2006) USD bln % of total EU-25 61.3 46 o.w Netherlands 2.7 2 Germany 18.4 14 US 6.4 5 China 12.9 10 Ukraine 9.2 7 Total 132.5 Source Datastream/IMFdirection of trade statistics

Major imports (ITS) Agricultural products 15.4% Fuels and mining products 3.9% Manufactures 80.2% Source WTO

Value of import and export

USD bln

0

100

200

300

400

1993 1995 1997 1999 2001 2003 2005 2007

—— Import Export Source: EIU

Main export markets (2006) USD bln % of total EU-25 177.2 61 o.w Netherlands 35.9 12 Germany 24.5 8 USA 8.9 3 China 15.7 5 Ukraine 15.0 5 Total 291.3 Source Datastream/IMF direction of trade statistics

Russia

9 Economics Department/Sector Research, September 2007

Samara on 18 May on a new EU-Russia treaty failed to achieve a breakthrough. The summit underlined that further delays should be expected to the start of talks on replacing the partnership and co-operation agreement (PCA) that is due to expire at the end of 2007. The failure to reach an agreement has a great deal to do with political tensions and differing values. Where Russia insists on strategic partnerships among peers, the EU aims at making the country more responsive to EU standards and values with respect to issues like democracy and human rights. The EU is also concerned about Russia's autocratic tendencies, its use of energy resources for political purposes and its bullying of smaller neighbours, but has so far not been able to formulate a common policy. Moscow, on the other hand, sees this as unacceptable interference in its domestic affairs and prefers to work directly with the big member-states like Germany. The ENP, the vehicle for stronger engagement of the EU with the CIS member countries, is also a source of tension between the EU and Russia. This is especially true for the relations with Georgia, Ukraine, Azerbaijan and Moldova – the so-called GUAM countries – which seek a closer connection with the EU but are seen by Russia as the “near abroad”. Furthermore, although many former CIS countries would like to be absolutely independent from Russia, they are not prepared to lose the economic benefits, such as cheap gas, which they continue to enjoy. This has resulted in the “gas wars” with Ukraine, Georgia and Belarus, for example. On the one hand, the EU supports the more independent position of these countries while on the other, it is concerned about the security of its own oil and gas supplies. Energy is hence one of the most pressing topics for discussion between the EU and Russia. Strong economic differences also play a role in explaining the difficulties in achieving economic and political cooperation. Despite Russia’s current strong economic performance, the EU is still far larger than Russia in terms of economic size, population and wealth. In fact for Russia, even trade with the EU is much more important as a share of total trade than it is for the EU. Nevertheless, now that its economic situation has improved on the back of high oil prices, Russia's international political interest has become increasingly geared towards renewing its status as a world power, which doesn’t make cooperation any easier. In addition, the forthcoming Duma elections (December 2007) and presidential elections (March 2008) cast further uncertainty on future relations, as is evidenced by the increased rhetoric from Moscow concerning both the EU and the US. Examples are the strong negative statements from Moscow regarding the US ambition to implement a military missile defence shield in Poland and the Czech Republic, and its reaction to the request by the UK to extradite the main suspect sought by the UK in the Litvinenko murder case. Given all this, we therefore expect that relations between Russia, the EU and the US will remain wobbly in the coming years. Economic developments Domestic demand will remain the sole driver behind economic growth, while the contribution of the external sector will become increasingly negative. A looser fiscal stance in the run-up to the presidential elections in March 2008 will further add to

Different in size US EU-25 Russia Nominal GDP (USD bln)

13247

14550

985

Population (mln) 299 490 142 GDP per capita (PPP) 44244 28420 12162 Source EIU

Russia

10 Economics Department/Sector Research, September 2007

growth. Higher import demand will only partly offset the increase in domestic demand. We therefore predict that although the high growth level of 7.8% seen in the first half of 2007 might not be sustained, growth for the full year will remain robust at 7.3%, up from 6.7% in 2006. In 2008 we expect growth to remain strong, albeit slightly lower, at around 6.5%. 2000-2006, years of rising prosperity The strong growth performance over the last eight years has resulted in an even stronger increase in per-capita GDP. Measured at purchasing power parity, per-capita GDP fell from USD 8,400 in 1991 to a low of 5,800 in 1998 and has since risen to over 12,000. Driven by domestic demand, the economy grew by an average of 6.7% per year between 2000 and 2006. Consumer demand is fuelled by a strong increase in disposable income. Real wages have increased by more than 10% a year since president Putin came to power. This has given rise to a consumption boom and a rapid growth in the retail sector. Private consumption grew by 9.5% annually between 2000 and 2006. Investments accelerated by no less than 12.6% per year. The growth in domestic spending drove up import demand by over 20% a year, while export demand jumped by an average of just 9% per year. Despite the strong growth in the value of imports, the current account remained in surplus thanks to the high oil prices. Windfall oil revenues were channelled into a stabilisation fund, which was used in 2005 to repay the IMF obligations and the former Soviet debt to the Paris Club (the club of debtor nations). Despite the debt repayments, the fund now has a balance of over USD 100 billion. The Stabilisation Fund was also an important tool of macroeconomic policy, as it helped prevent an even stronger appreciation of the rouble and kept the economy from overheating. Recent developments 2006-2007 Gross investments, which dipped below 10% growth in 2005, bounced back strongly in 2006. In the first quarter of this year, gross fixed capital formation was up 19.8% yoy, compared to 17.4% in the last quarter of 2006 and just 5.7% in the first quarter of last year. Including inventories, the rise was even more impressive, amounting to 34.2% in the first quarter, against 19.7% in the last quarter of 2006 and 4% in the first quarter of 2006. Foreign direct investment increased by USD 16 bn to a total of USD 81 bn. This contradicts fears that investment would suffer from the government’s renationalisation efforts and a worsening political climate. The bulk of investments, both domestic and foreign, is directed to the energy sector, construction, transportation and services. Foreign direct investment is also increasingly directed towards the financial sector. Private consumer demand also remained robust, growing 10.9% in 2006. Private consumption growth accelerated during the second half of last year to 12.6% in the final quarter of 2006, slowing slightly in the first quarter of 2007 to 11.9%. Domestic demand is not only stimulated by the continuing increase in real disposable income but also by increased access to consumer credit. Overall credit rose 46% in 2006. Loans to individuals were up 75% during that year, while credit to the corporate sector increased by 39%.

Government debt

% GDP

020406080

100120140

1995 1998 2001 2004 2007

Source: EIU/Economics Department

GDP per capita at PPP

4000

6000

8000

10000

12000

14000

1991 1995 1999 2003 2007

Source: EIU

Growth of real disposable income

%

-15-10

-505

1015

1996 1998 2000 2002 2004 2006 2008

Source: EIU

Russia

11 Economics Department/Sector Research, September 2007

Booming consumption market Table: Top 20 of private consumption expenditure, at current market prices in billion US dollar ranked by 2008 Country 2000 2001 2002 2003 2004 2005 2006 2007 2008 placeUNITED STATES 6739 7055 7351 7704 8211 8742 9271 9640 10087 1JAPAN 2624 2340 2259 2431 2629 2600 2495 2814 3102 2GERMANY 1122 1127 1194 1451 1621 1644 1684 1878 1924 3UNITED KINGDOM 944 946 1035 1183 1394 1439 1520 1689 1731 4FRANCE 743 751 819 1019 1166 1213 1279 1439 1483 5CHINA 554 595 635 687 771 865 988 1146 1294 6ITALY 656 657 715 888 1007 1032 1075 1193 1226 7SPAIN 347 360 402 510 605 652 713 815 847 8CANADA 401 401 418 490 553 627 709 719 758 9RUSSIAN FEDERATION 120 151 177 218 289 367 476 594 688 10INDIA 296 308 318 371 419 474 536 601 666 11MEXICO 389 433 448 439 465 525 570 596 613 12KOREA, REP. OF 276 266 305 327 351 415 474 530 592 13BRAZIL 366 309 267 287 333 442 533 563 585 14AUSTRALIA 228 218 244 308 374 407 421 428 418 15NETHERLANDS 185 201 220 270 300 308 321 362 371 16TURKEY 143 105 122 160 200 245 265 281 295 17INDONESIA 102 101 132 160 171 184 229 253 276 18TAIWAN 195 181 181 183 198 215 220 236 259 19SWITZERLAND 148 151 166 195 216 221 224 250 258 20

Total top 20 16579 16656 17408 19280 21274 22617 24002 26028 27471Total World 19279 19374 20145 22437 24903 26652 28448 31056 32824as % of total world 86 86 86 86 85 85 84 84 84 source EIU

Not only has private consumption shown remarkable increases in recent years compared to the pre-Putin era, but is also impressive when compared to other countries. This is illustrated in the table above, showing the nominal amount of national income spent on private consumption from 2000 to 2008. These countries rank as the top 20 in 2008 and, over the years, have represented around 85% of total global private consumption expenditure. Given current growth prospects, Russia is expected to move from 19th place in 2000 to 10th in 2008, outranking countries like India, Mexico, South Korea and Brazil. This will make Russia an increasingly attractive market for both retail and other consumer-related activities. Construction and manufacturing show strongest growth Looking at the supply side, it is the construction and retail sectors that showed the strongest growth. In the second quarter of this year, growth in the construction sector was 22% yoy. Overall GDP grew by 7.8% yoy in the second quarter, just below the 7.9% growth level recorded in the first quarter. Other sectors registering growth above the GDP average are trade, financial activities, real estate and transport and communication. The state administration sub-sector also showed remarkable Q2 growth at 8.1%. This merely reflects sharp increases in public sector salaries in the run-up to the elections. Growth in the manufacturing sector was below average at 6.2% following a very strong performance of 11.8% in the first quarter. Resource extraction remains sluggish due to a lack of investment in new fields and infrastructure. The sector grew by just 1.4% in the second quarter, after recording a lacklustre 2.4% growth in the first quarter. Another sector which continues to underperform is the agriculture sector, which grew 2.6% in the second quarter and 2.9% in the first quarter.

Real import and export growth % yoy

-40

-20

0

20

40

1991 1995 1999 2003 2007

—— Export Import Source: EIU

Industrial production growth % yoy

-10

-5

0

5

10

15

1996 1998 2000 2002 2004 2006 2008

Source: EIU

Russia

12 Economics Department/Sector Research, September 2007

The construction and retail sectors are expected to continue to outperform due to further increases in overall wealth levels. The manufacturing sector might slow down furhter over the coming period, as the sector will eventually be negatively impacted by the loss in competitiveness caused by the continuous strengthening of the rouble. This will particularly affect those areas of manufacturing that are oriented to the export market or compete on the domestic market with imported goods. Current account surplus will diminish Despite strong import growth and a slight decline in oil prices in the second half of last year, the current account surplus rose further in 2006 to USD 94.5 billion, compared with USD 83.3 billion in 2005. For 2007 we expect a small decline in the nominal value of the surplus as imports continue to swell. This trend will continue in the coming years, but we do not foresee a current account deficit, at least up until 2010. Strong inflows of foreign capital will more than compensate for the lower current account surplus and foreign reserves will hence continue to swell. Figures for the first half of 2007 indicate that foreign capital continues to pour into the country. To a large extent, this is related to foreign borrowing by Russian corporates, but foreign direct investments are also surging. Total FDI inflows more than doubled in the first half of 2007 compared to the year-earlier period. FDI inflows amounted to USD 16 billion2, bringing the total amount of FDI to USD 81 billion. The Netherlands is the most important source of direct foreign investment with over USD 30 billion invested in Russia. Most of this is invested in the extraction industries. Cyprus, which is the major offshore banking centre for Russian corporates, is the second largest source of FDI. Rouble remains strong and inflation subdued The net capital inflow has led to a continuous strengthening of the rouble, which had a dampening effect on inflation, despite strong consumer demand. In March 2006, inflation fell below 10% for the first time since the start of the rouble crisis in August 1998. Inflation ended 2006 at 9%, precisely at the upper end of the central bank’s target. It fell to a low of 7.4% in March, but has since risen above 8%. We expect inflation to end 2007 around 8.5%, above the official inflation target, which is set between 6.5-8.0%. Interest rates were lowered by 50 basis points in mid-June to 10%, but there is little room for further cuts. In July 2006, the rouble became fully convertible, meaning that the remaining restrictions on capital account transactions were removed. As the balance of payments (current account plus capital balance) will remain in surplus, there will be continuous upward pressure on the exchange rate. Therefore, the central bank needs to continue maintaining a balance between efforts to reach its inflation target and heeding political pressure to keep appreciation of the currency in check. Clearly this is a difficult balancing act. Raising interest rates to stem inflation will only lead to more capital inflow and hence probably to even stronger upward pressure on the currency. The appreciation of the currency itself also attracts additional capital inflows and could thus lead to further appreciation. Another option is to further increase its reserve requirements as a loosening of fiscal policy in the run-up to elections makes it even more difficult for the central bank to achieve its inflationary targets. The one thing that

2 According to figures from RosStat

Real effective exchange rate against USD 1997=100

40

60

80

100

120

1995 1998 2001 2004 2007

Source: EIU

Inflation % yoy

0255075

100125150

1995 1998 2001 2004 2007

Source: EIU

Current account % GDP

0

5

10

15

20

25

1993 1997 2001 2005

Trade balance Current account Source: EIU/Economics Department

Russia

13 Economics Department/Sector Research, September 2007

could exert downward pressure on the currency could be political uncertainty in the period surrounding the coming elections. However, the chances that this will lead to strong and prolonged currency volatility are small given the country’s huge international reserves and substantial current account surplus. Elections could pose some risks to our positive outlook Uncertainty about Russia’s political outlook after President Putin steps down at the end of his second term in 2008 represents a major threat to our forecast for the coming two years. Infighting among rival factions in the Kremlin that are competing for influence could give rise to political turbulence, and might even trigger some capital flight. However, the most probable scenario, given Putin’s formidable power base and his tremendous popularity, is that whoever he appoints will win the elections and carry on his policies. Although it is unclear whether this new president will be able to maintain the same powerbase as Putin, the very favourable current economic developments –particularly the extremely favourable external liquidity position – strongly mitigate the political risks. Therefore, as long as the oil price continues to prop up the economy and create growing prosperity among broader sections of the population, the current power base in the Kremlin is unlikely to be seriously threatened. The more relevant vulnerability, in our view, is therefore the fact that the government is using its oil wealth to avoid painful reforms and to expand its presence in the economy. Given the inefficiency of state-owned firms, this could constitute a long-term structural constraint on growth. Further, because both the institutions and the legal framework are very weak, many approved reforms are not being implemented. This, together with high and increasing levels of corruption, could become a serious constraint to further investments. SWOT analysis Though Russia is an extremely attractive market for investors, it is also fraught with pitfalls. The most common problems concern the complexity of the tax system, corruption, regulatory volatility, the lack of regulatory transparency, government bureaucracy, weak contract legislation, the absence of a commercial market and business ethos as well as the absence of a commercial law system. This means that deals must often be made on the basis of trust. Investors also frequently encounter financing difficulties and have problems obtaining payment from Russian companies3. Despite these problems, businesses and investors are increasingly finding their way to Russia. Western exports to and investments in Russia are steadily rising. Every day, new products and services are launched in the Russian market. The most important reason for this is the tremendous scope for entrepreneurship in this country. In the table below we have summarised the most important strengths and weaknesses as well as the respective opportunities and threats these may give rise to. As the economic strengths have already been addressed in our outline on the current economic situation and prospects, we will only very briefly summarise the strengths and emphasise the risks to our overall very benign picture of the Russian economy.

3 The Institute of Direct Investments Foundation has been set up by the Russian government to assist investors in Russia.

Short term interest rate year-end

010203040506070

1996 1999 2002 2005 2008

Source: EIU

Russia

14 Economics Department/Sector Research, September 2007

Table : SWOT analyses of Russia

Strength: Weakness:

rich resource base

growing wealth

large domestic market

sound economic policy

Low sovereign debt levels

Sound external liquidity situation

fragile political situation

state interventionism

weak institutions and corruption

demographics, infrastructure,

education, and health

low degree of diversification

Opportunity: Threat:

deepening of financial markets

diversification of the economic base

development of SME sector

to improve transparency and corporate

governance

losing competitiveness

Lower oil prices

shrinking population

Source: ABN AMRO

Strengths Russia’s current strength is related to the fact that its rich resource base and favourable commodity prices – in combination with sound economic policies – have enabled the country to lower its sovereign debt to less than 10% of GDP and dramatically improve the external liquidity situation. This makes the country much less vulnerable to adverse internal or external developments. Although we expect that both the fiscal and the current account surplus will diminish rapidly in the coming years, the low levels of government debt and huge international reserves will cushion the economy for a long time from a possible change in investor sentiment. The oil boom has also led to a strong increase in wealth, which, given the size of the population, also makes Russia very attractive as a retail market. Weaknesses Fragile political situation The country’s present political stability has, in part, been achieved at the expense of progress in democratic development, which could in turn set the stage for longer-term instability. The biggest short-term threat to the benign risk environment is related to the question of what will happen after president Putin's second term ends in 2008. The concentration and centralisation of power in the hands of the president could result in instability in the longer run, regardless of who wins the elections. This is even more likely if the relationship between politicians and the private corporate sector further deteriorates as this could hamper future investment growth. This scenario could also have a strong negative impact on the allocation of scarce resources, impeding healthy economic development and leading to strong inefficiencies. But as we stated previously, as long as oil prices stay high and the economy continues to grow, the political risks are strongly mitigated. Another risk related to the concentration of power among only a few individuals is that the sudden death of the president could have a strong negative impact, especially if it leads to political infighting among different factions in the Duma and the country’s different regions, which now are firmly under state control. These risks range from increased fiscal instability in the regions to a rise in terrorist activities.

Russia

15 Economics Department/Sector Research, September 2007

State interventionism In the long run, the increasing discretionary role of the state in society and the economy has several distortionary impacts. Inefficiencies in state-controlled sectors are likely to grow and corruption will rise. In addition, private business that is no longer supported by the government could suffer strongly. Weak political, legal, and economic institutions There has been rapid legislative reform since the election of President Putin, but enforcement is still a major problem due to weak institutions and a weak legal framework. This is also true for the intellectual property legislation that was passed in 2002 as Russia makes its bid to join the WTO. The lack of enforcement severely hinders the investment climate, which is also negatively impacted by the high and rising corruption levels. Russia currently ranks 121 out of 158 countries in the Transparency International Corruption index 2006. Demographics, education, health, housing and infrastructure Years of underinvestment have resulted in a dilapidated infrastructure and inadequate education and health system. Decent, affordable housing remains an important issue as well, as it hampers the movement of labour from the agricultural sector to more productive sectors of the economy. Government investments are still clearly insufficient, and increased spending in these areas is urgently needed in order to maintain a strong human capital base. This should diminish the risks related to the negative demographic trend of a rapidly declining, and rapidly aging, population. Now that the foreign sovereign debt levels have declined to the extent that Russia has become a net creditor, it could be argued that part of the stabilisation fund could be used for such government investments. This would help further bolster political stability. Russia’s poor infrastructure is a major impediment to trade. Several major projects are being carried out to improve its infrastructure with financial support from the World Bank and the European Bank for Reconstruction and Development (EBRD). The aim is to upgrade the road network as well as modernise the ports and airports. Only 9 per cent of the total freight volume is transported by road, as most of the reasonably good roads are located in the European part of Russia and only in the proximity of its larger cities. In the rest of the country, the road network is less developed. Nearly 40 per cent of the villages have no access via paved roads. The rail network is also in very poor technical condition, while the numerous ports and waterways are often poorly located or lack facilities for the transshipment of large volumes of goods4. Opportunities Deepening of financial markets The financial sector is developing rapidly. The market for consumer credit and mortgages as well as the rise of the corporate bond market are particularly encouraging. The reduction in borrowing costs was very helpful in enhancing credit growth as were improvements in the regulation of the banking sector in recent years and the introduction of deposit insurance. Nevertheless, the sector is still far from

4 For example a large portion of agri-food products destined for West Russia is transported via ports in Western Europe or the Baltic states because the ports in Russia lack the required facilities.

Russia

16 Economics Department/Sector Research, September 2007

offering the full range of modern instruments needed to support a dynamic corporate sector. The Russian banking sector also remains relatively small, weak, and segmented. Given continued scarcity of skilled bank personnel and substantial non-transparency with respect to the operation and ownership of domestic corporations, there is inadequate means to assess the creditworthiness of clients. This increases the share of bad loans. There is no legislation to protect the banks against delinquent customers. Meanwhile, the public—the potential customers—still distrust banks, but instead prefer to keep their savings in cash. This hampers the proper working of financial intermediation in the economy. Development of the sector would clearly further enhance the economy’s growth prospects. The development could be facilitated by eliminating inconsistencies among different laws and codes, and clarifying responsibilities among the various agencies charged with overseeing the sector. Diversify the economic base To further broaden the base of economic development it is important to stimulate investments in other sectors as well as development of the SME sector. The latter is especially important, as a well-developed SME sector increases competition and is an important source of jobs and a generator of innovations. This would also be a better stimulus for achieving the government’s aim of stimulating innovation than the current trend towards more centralisation. Improve transparency and corporate governance More and more Russian companies are listed abroad. Although there are no guarantees, this will very likely expose Russia more to "international" standards (including increasing transparency and corporate governance) and will create a certain integration between Russian and Western(-European) Financial Markets. Threats Sharp fall in world oil prices A sharp drop in world market oil prices would severely slow the pace of the Russian economy’s expansion and increase all other risks. But as long as oil prices remain high and above USD 40 a barrel, most short and medium-term risks remain limited. Dutch disease development A sharp fall in the oil price is not the only risk; high oil prices also pose a threat to sound future economic development. Oil dependence makes the country vulnerable and creates uneven development. During the Soviet era the economy was relatively well diversified. But since the fall of the centrally planned communist system, import demand has started to rise at the expense of domestic production. This process accelerated when the oil boom began. Russia’s strong currency has worsened its competitive position, which was greatly enhanced by the mega rouble devaluation in 1998. As a consequence, diversification has diminished at the expense of the energy sector. So far, the shift in concentration of economic activity out of the labour-intensive manufacturing sector into the capital-intensive oil and gas sector has largely been compensated by strong employment growth in the services sector and construction, but this could come to an end when the country’s development reaches a more mature stage.

Russia

17 Economics Department/Sector Research, September 2007

Demographics The Russian population is dwindling and – due to low birth rates in the late Soviet and transition eras – is rapidly aging as well. This could lead to labour shortages and pension problems. In addition to this negative demographic trend, the technological basis of higher education has been depleted since the fall of the Soviet Union, resulting in a lack of good technically skilled employees.

Russia

18 Economics Department/Sector Research, September 2007

Chapter 2: Russia’s Minerals & Mining Industry This chapter describes Russia’s non-fuel mining industry, i.e. excluding coal, oil, natural gas and uranium mining. Oil and natural gas will be discussed in the next chapters. The importance of the sector to the Russian economy The non-fuel mining industry (including the further processing of ores) is of vital importance to Russia’s economy. Russia has a long mining tradition and is currently one of the world’s leading producers and exporters of minerals and mineral-based products. Blessed with vast resources, the country is a major producer of aluminium, cobalt, copper, diamonds, gold, iron ore, mica, nickel, platinum, potash, tin, titanium and zinc. In addition, many other metals and various industrial minerals are mined. The country’s most important regions for metals mining are East Siberia, the Kola Peninsula, the North Caucasus, the Russian Far East and the Urals. Mining conditions in some of these regions are harsh. Following the collapse of the Soviet Union in 1991, it became clear that the Russian mining industry – which is almost exclusively state-owned – was in a poor state due to years of underinvestment and lack of maintenance. Low labour productivity, high energy use and, at times, low product quality resulted in decreasing competitiveness in the world market. The transition from a centrally planned economy to a free market system in the early 1990s affected domestic demand for many basic metals and industrial minerals. By 1998, Russia’s industrial production had fallen to 45% of its level in 1990. One positive effect of the slump in domestic demand was that substantial volumes became available for export, resulting in a rapid increase in the export of minerals and metals. The sector’s poor performance and the free market economy caused the collapse of several large state mining companies, while private mining companies began to emerge. Meanwhile, small mining and metals companies closed down or merged, thereby creating larger and financially stronger companies. This reconstruction was necessary in order to survive against a backdrop of lower global commodity prices at the end of the 1990s and the 60% depreciation of the Rouble in 1998. However, the resulting capacity rationalisation was a major positive effect of the turmoil hitting the industry. The transition of the Russian mining industry also brought about major job losses and many miners left their regions to find work elsewhere. Privatisation was used to bring in Western know-how, technology and the much-needed foreign capital to upgrade the industry. However, many Western companies were still reluctant to invest in the Russian mining sector as a result of its negative image due to the unreliable legal system, problems with subsoil licensing, doubtful reserve classification and high federal and local taxes. Although some of the problems were overstated by the media, the Russian Government has recognised the need to improve foreign investment conditions and bring legislation up to world standards.

Russia

19 Economics Department/Sector Research, September 2007

Exploration spending in the global mining sector Exploration is the key element in unlocking new reserves and increasing a mining company’s reserve base. Data from the Metals Economics Group (MEG)5 show that, after the peak in 1997, global exploration spending in the non-ferrous mining sector started to decline. The reasons for this decline were the low price environment and falling investor confidence in the mining sector. As a result, less capital was available for the mining sector while the more promising dot.com sector attracted huge capital flows. At the turn of the century, the combined market value of quoted mining and metals companies (representing real ‘bricks and mortar’) is said to have fallen to only about half the value of Microsoft. After bottoming out in 2002, global exploration spending began to boom once again from 2004. This type of boom-to-bust cycle is typical for the mining sector. Key drivers for the sector are global economic growth and, in particular, demand growth in the manufacturing, construction and infrastructure sectors. The current boom is based on a combination of: • years of underinvestment since the Asian crisis in 1998; • lagging reserve replacement, a key issue for the mining industry; • surging demand, particularly from the emerging economies of India and China. Metals and minerals consumption per capita in India, China and other developing countries is still low compared to consumption levels in developed countries. This implies that there is considerable scope for sustained high demand growth over the medium term as long as economic growth in these countries remains relatively high. Total global exploration spending was estimated at USD 7.13 billion in 2006, up by USD 2.2 billion (45%) from 2005. Although gold and diamond exploration spending still represents a major part of total spending, most of the increase can be attributed to base metals exploration spending. Canada, Australia and the US traditionally head the list of top ten countries, together accounting for 38% of total global exploration budgets. Since 2004, Russia has quickly moved up the top ten list, jumping from seventh place in 2005 to its current fourth place spot. In 2006, Russia accounted for 5% of global exploration spending. Expansions are usually the preferred method of reserve replacement over grassroots discoveries. A major reason for this is that grassroots projects take an average of 7-10 years from initial discovery to production. According to MEG’s survey, there is currently a clear trend towards late-stage/feasibility exploration budgets, which outpace the increases in grassroots projects. In the present price environment, with most metals at 15 to 20-year highs, several dormant, abandoned or technically difficult projects are now being re-assessed for near-term development.

5 The 2006 data collected by MEG are based on an analysis of 1,624 international nonferrous mining companies with exploration budgets of at least USD 100,000. MEG is a world leader in mining industry intelligence and a provider of information and analysis on global nonferrous metals exploration, development and production. MEG’s data are widely used by the mining industry and by governments to analyse trends and formulate policies.

Distribution of worldwide exploration budgets in 2006, USD 7.13 billion

Canada

Australia

United States

Russia

Others

MexicoBrazil

MongoliaChina

South Africa Peru

Source: Metals Economics Group

Worldwide nonferrous exploration spending USD bln, 1994-2006

0

2

4

6

8

1995 2000 2005

Source: Metals Economics Group

Russia

20 Economics Department/Sector Research, September 2007

The data collected by MEG show that over the past few years the so called ‘junior exploration companies’6 have significantly outpaced larger mining companies in exploration spending growth. Although this can partially be explained by the focus of junior exploration companies on gold mining, they are also looking for opportunities in other commodities. In 2006, the junior exploration companies accounted for about 50% of total global exploration spending. It is becoming increasingly difficult to find economically viable metal ore and mineral deposits as most of the ‘low-hanging fruit’ has already been discovered and developed. Therefore, it will take considerably more capex to discover, explore and develop new grassroots deposits than in the past, particularly when local infrastructure is lacking. As a result, the expansion of supply will continue to struggle to keep pace with the expected continuing growth in demand. Growing demand for mining equipment MEG’s survey of exploration budgets indicates a sustainable revival of the global mining industry. However, one should realize that a substantial part of the increase in exploration spending over the past few years can be attributed to cost inflation. Since the trough in 2002, there have been significant cost increases in wages, services and mining equipment. Therefore, the amount of real capital invested in 2006 may be much smaller than the survey indicates. The revival of the exploration market and the development of new deposits will be key drivers for mining and processing equipment market. According to a recent study7 by The Freedonia Group, global demand for specialised mining machinery and equipment is forecast to increase 9.3% per year through 2009 to USD 27.5 billion. Freedonia expects Eastern Europe to offer the best regional prospects due to the long period of underinvestment and the region’s extensive mineral resources. Despite the recent turnaround in the fortunes of the global mining industry, the sector still faces many challenges. Considerable equipment cost inflation and the lack of human resources are not the only problems hindering production and capacity growth. Some projects are encountering environmental oppositions, technical problems or cost overruns. In addition, the availability of equipment is currently causing stress in the mining sector, leading to project delays. Medium-term outlook The medium-term outlook for Russia’s minerals and mining industry looks rather promising, considering the global supply/demand trends. The industry has profited from increasing global demand and rising prices since 2002, which has stimulated increased production.

6 Junior exploration/mining companies are small to medium-sized companies involved in early-stage mining projects. Their exploration expenditures vary from USD 50,000 to 1,000,000. Because they have no cash flow (i.e. no income from an operating mine) and their assets consist of exploration properties, their capital needs cannot be satisfied through normal financing channels. The capital for mineral properties, exploration, plant and equipment is raised through the issuing of shares. Investors consider junior mining companies ‘high-risk/high-reward plays’. Many are listed on the Canadian TSX Venture (TSX-V) Exchange or London’s Alternative Investment Market (AIM). 7 World Mining Equipment, World Industry Study with Forecasts to 2009 & 2014. The Freedonia Group, Inc., April 2006.

Acute shortages constrain the equipment supply side

Item Normal delivery time (months)

Current delivery time (months)

Grinding mills 20 44 Draglines 18 36 Barges 24 32 Locomotives 12 26 Power generation 12 24 Wagons 12 24 Rope shovels 9 24 Reclaimers 18 24 Tyres 0-6 24 Large haul trucks 0-6 24 Crushers 15 24 Ship Loaders 8 22 Source: Rio Tinto, Outlook for Metals and Minerals

Russia

21 Economics Department/Sector Research, September 2007

Like many of their competitors elsewhere, Russian companies are also being confronted with the depletion of their high-grade ore deposits. They will have to develop new deposits in order to meet both increasing indigenous demand from the manufacturing sector and from exports. The potential for mineral exploration in Russia has been recognised by several large Western companies, such as Anglo American, AngloGold Ashanti, BHP Billiton and Rio Tinto. In recent years, several alliances and joint ventures have been announced with Russian companies to explore and develop attractive mineral deposits. Most of these joint ventures will develop greenfield mineral deposits in certain areas, such as western Siberia and the north-western part of Russia. Junior exploration companies are also likely to play a role in the development of these deposits. The successful development of a deposit could make these junior mining companies more attractive for acquisition by larger (‘senior’) mining companies, as this increases their reserves and production base. Opportunities in mining equipment, services and systems Despite its production potential, the Russian minerals and mining sector still faces major problems, such as ageing equipment. In 2000, about 80% of Russia’s mining machinery was near the end of its operable life and in need of urgent replacement. Although there have been some improvements since, many mining companies are still using outdated technologies from the Soviet era. According to estimates, 30-70% of Russia’s minerals reserves are not economically exploitable. Major investments will be needed to reach Western standards of product quality, pollution control, energy use per unit of output and labour productivity. Moreover, new mineral deposits will have to be developed to meet the ever-increasing demand and compensate for the depletion of existing deposits. Vast investments will therefore be required in the coming decade, offering significant opportunities for Western companies involved in exploration and development, and for suppliers of control systems, logistics, mining technology or mining equipment. Medium-sized companies will be particularly interested in optimising mining and plant operations through advanced process control systems, and minimising the idle time of mining equipment through better coordination with the transport system. Even large mining companies tend to contract specialised companies for services that require certain expertise. Automation of mining equipment is also an important issue in modern mining operations, particularly in underground mining. Automation considerably improves both productivity and safety. Some Russian mining companies have poor safety and environmental records, and automation could surely help them improve safety, health and environmental (SHE) conditions. A consistently good SHE performance is increasingly becoming a prerequisite to sell to Western customers.

Russia

22 Economics Department/Sector Research, September 2007

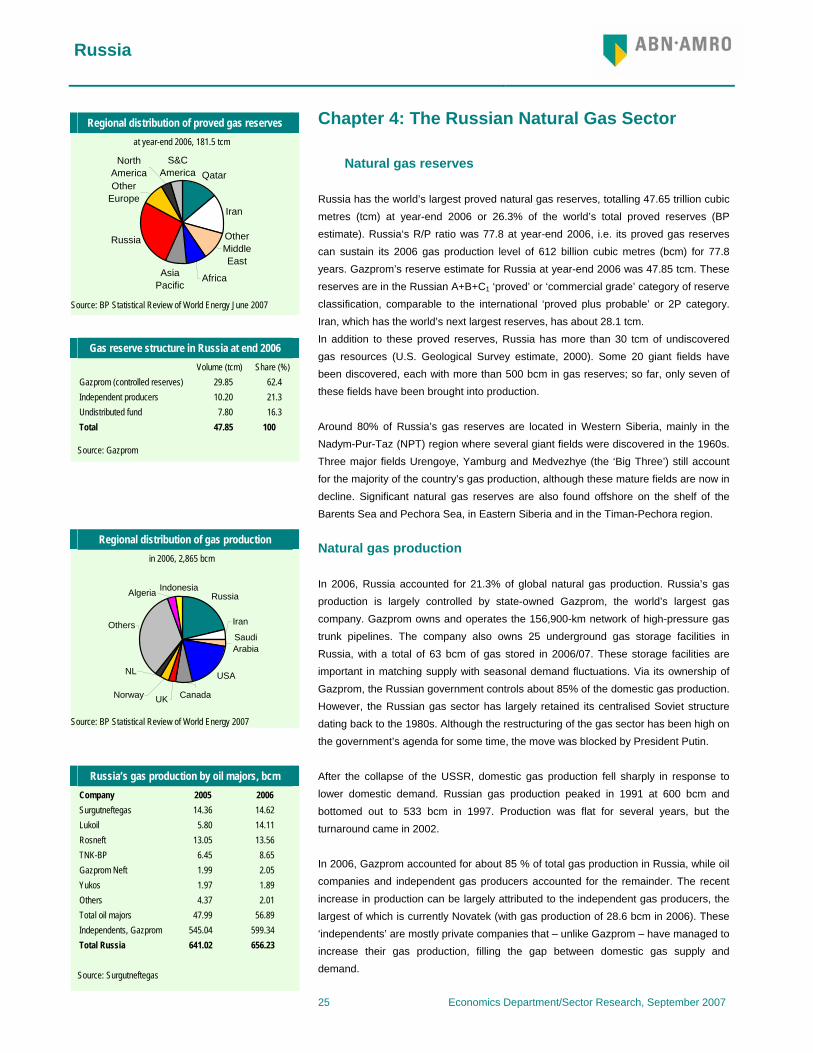

Chapter 3: The Russian Oil Industry Oil reserves Russia’s proved oil reserves amounted to about 79.5 billion barrels as at year-end 2006, accounting for 6.6% of the world’s total proved reserves (BP estimate). Most of these oil reserves are located in four oil provinces: Western Siberia, Volga-Ural, Timan-Pechora and Northern Caucasus. In addition, the country has roughly the same level of probable and possible oil reserves, putting this non-OPEC country in the top league of oil-producing nations that includes OPEC members like Saudi Arabia, Iran, the UAE and Venezuela. According to BP, Russia’s R/P ratio was 22.3 at year-end 2006, i.e. its proved reserves can sustain its 2006 production level of 9.77 million bpd for 22.3 years. Oil production In the 1980s, the Soviet Union became a major world oil producer due to the development of the Western Siberia region (also known as the ‘Russian Core’). Peak production reached 11.4 million bpd (barrels per day) in 1987. Following the disintegration of the Soviet Union in 1991, Russian oil production fell over the subsequent years to bottom out at 6.1 million bpd in 1996. Oil production then stabilised at this level for several years. The production decline can be attributed to several factors: the collapse of the central planning system, the depletion of major fields due to excessive production targets and insufficient attention to matters such as infrastructural development, enhanced oil recovery techniques, maintenance and energy-saving measures. The turnaround for Russia’s oil production came in 1999. In 2000, Russian oil production showed an increase of almost 360,000 bpd, a rise of 5.8% over the previous year. This turnaround can be attributed to the introduction of Western technologies and the re-engineering of oil fields in Western Siberia. Another driver was the sector’s privatisation, leading to better management and new field developments. Yukos and Sibneft played an important role in the production increase by using Western-style production methods. Russia’s oil production (crude oil plus condensates) amounted to 9.77 million bpd in 2006, with the ‘big four’ Lukoil, Rosneft, TNK-BP and Surgutneftegaz accounting for 64.5% of total production. Oil production in 2006 showed an increase of 2.2% over 2005, the lowest growth rate seen since 1999 when oil was still at USD 10 per bbl (barrel). This represents a marked slowdown from the 8-10% annual growth rate seen in the 2001-2004 period. In fact, Russia was the motor for global oil supply growth in 2001-2004, accounting for 50-75% of non-OPEC supply growth during those years. Oil exports Russia has a vast integrated oil transportation system, which handles both crude oil (mostly Urals blend) and refined products. The pipelines, which were in urgent need of repair in the 1990s, have since been substantially upgraded. The pipeline network consists of more than 60,000 km of long-distance pipelines, local oil pipeline networks and several export pipelines, the most important of which are ‘Druzhba-1’ and ‘Druzhba-2’.

Russia’s major oil producers (production x mln tons)*

Company 2005 2006 Lukoil 87.81 90.42 Rosneft 74.42 81.71 TNK-BP 75.35 72.42 Surgutneftegas 63.86 65.55 Gazprom Neft 33.04 32.72 Tatneft 25.33 25.41 Slavneft 24.16 23.30 Yukos 24.52 21.53 Russneft 12.18 14.76 Gazprom 12.79 13.40 Others 36.44 39.31 Total 469.90 480.53 * incl. gas condensates Source: Gazprom Neft

Regional distribution of proved oil reserves at year-end 2006, 1,208 bln bbl

Saudi Arabia

Other Middle EastS&C

America

Africa

Russia

Other Europe

IranNorth

America

Asia Pacific

Source: BP Statistical Review of World Energy June 2007

Regional distribution of oil production in 2006 81.66 mln bpd

Saudi Arabia

Iran

Other Middle East

North AmericaRussia

Other Europe

Africa

S&C America

Asia Pacific

Source: BP Statistical Review of World Energy June 2007

Oil production and consumption in the Russian Federation (mln bpd)

0

3

6

9

12

1985 1990 1995 2000 2005

—— Production Consumption

Source: BP Statistical Review of World Energy

Russia

23 Economics Department/Sector Research, September 2007

Over 70% of Russia’s crude oil production is directly exported, while the remaining 30% is refined locally. Most of Russia’s oil exports are transported via pipelines (overland to other countries or to export terminals at ports). About 35% of Russia’s crude oil exports are still shipped via higher-cost railroad tankers and river barges due to pipeline bottlenecks. Some of the crude oil export capacity deficit is handled by exporting refined petroleum products to Europe, mostly fuel oil and diesel fuel. Traditionally, exports are primarily transported overland via the Druzhba trunk pipelines into Central Europe and by sea via the Black Sea ports of Novorossiysk, Tuapse and Odessa, and via the Baltic port of Ventspils and several other ports in the Gulf of Finland. The Baltic Pipeline System (BPS), which came on stream in December 2001, transports oil from the West Siberian and Timan-Pechora oil fields westward to a new terminal at the Russian Baltic port of Primorsk, diverting the flow from the Latvian port of Ventspils. The final stage of the BPS was completed in 2006. In 2006, about 85% of Russian crude oil exports went to non-CIS countries. Major destinations were Germany, Italy, France and the Netherlands. The remaining 15% mainly went to CIS countries. The Russian oil pipeline system is very inefficient due to inept management, and is often troubled by reliability and environmental problems. Over 90% of the system is owned and managed by Russia’s state-owned monopoly Transneft. The tariffs charged by Transneft for use of its pipelines are based on distance. In order to maintain control over oil exports, Transneft has so far opposed deregulation of the pipelines. In October 2005, a new export tax system was introduced to stimulate crude oil production growth by capping the export tariff rate. The unintended side-effect was a shift toward exports of refined products at the expense of crude oil exports. This was mainly due to the fact that under the new tax system, the tax on refined products has declined relative to the crude oil tax. For Urals at USD 40/bbl the difference for light products is about USD 2.8/bbl, but for Urals at USD 60/bbl, the difference is about USD 7/bbl. The differences in taxation have more than offset the higher transportation and other costs involved in the export of refined products. Oil production and export outlook Russia’s oil production is forecast to continue its upward trend. The International Energy Agency (IEA) expects Russia’s oil production to rise by 2.4% in 2007, slightly higher than the production growth of 2.2% seen in 2006. For the medium term (2007-2012), the IEA expects Russian oil production to continue to grow, albeit at a slower pace compared to the period 2001-2006. This lower growth rate reflects the fact that several major oil fields are showing signs of maturity as well as the difficulties encountered in compensating for the decline by developing new fields. As domestic demand is expected to increase less rapidly than production, this leaves room for increasing exports of crude oil and refined products. According to the IEA, Russia’s exports will start to gradually decline soon after 2010 when domestic demand outstrips the increase in production. IEA’s overall conclusion is that these production and export trends will remain highly sensitive to politics and taxes and may, therefore, differ substantially from the current scenario.

FSU net exports* of crude oil and petroleum products (million bpd)

2004 2005 2006 Crude oil seaborne 3.96 4.05 4.07 Druzhba pipelines 1.10 1.15 1.20 Other pipelines 0.23 0.25 0.38 Total crude exports 5.29 5.45 5.64 - of which Transneft 3.76 4.04 4.09 Exports petroleum products 2.19 2.38 2.51 Total exports 7.48 7.83 8.16 Source: IEA Monthly Oil Market Report

Sources of crude oil exports in 2006 38.81 mln bpd

Middle East

North America

S&C America

FSU

Other Europe

Africa

Rest of world

Source: BP Statistical Review of World Energy June 2007

Differential Crude oil Urals Med. vs dated Brent USD per bbl

-8

-6

-4

-2

0

2

00 01 02 03 04 05 06 07

Source: Thomson Financial

Russia

24 Economics Department/Sector Research, September 2007

The medium-term outlook for Russia’s oil production growth is highly uncertain, mainly due to the fact that seismic data are neither transparent nor made externally available. Oil analysts have also pointed out the lack of exploration in potential production areas over the last decade. The key factor determining Russia’s future level of oil production essentially depends on how long Western Siberia’s current production can be maintained while new reserves are meanwhile put into production to offset the decline in maturing or post-peak fields. According to a study by John Grace ‘Russian Oil Supply’ (Oxford Institute of Energy Studies) about 20% (1.8 million bpd) of Russia’s oil production in 2004 came from fields that had cumulatively produced 80% of their total recoverable reserves. Attention is therefore likely to shift to less mature basins such as Timan-Pechora, and to frontier areas such as Eastern Siberia and Sakhalin. However, the development and production costs for such ‘greenfield projects’ are expected to be much higher than for existing ‘brownfield projects’ in Western Siberia. Government taxation and the lack of clarity regarding subsoil resources ownership will continue to create uncertainties. In this type of environment, it will be quite difficult to achieve sustained production growth. The key to Russia’s future oil production growth will be the availability of viable export routes via pipelines. Alternative methods of exporting oil (by rail or barge) are far more costly than shipment via pipelines. Both Transneft and the Russian government have acknowledged the future capacity problem and have introduced incentives to develop new export infrastructure. This export infrastructure will also take into account the growing demand for oil in the North East Asian market, which has so far been a limited target for Russian oil exports. A major project aimed at increasing oil exports to the North East Asian market will be the 4,200-km Eastern Siberia-Pacific Ocean (ESPO) pipeline, which was approved in December 2004. Many problems had to be solved before construction could start, such as the possible connection with China, the sourcing of the oil and the financing of the pipeline with an estimated cost of USD 7.0 billion for the first section and USD 6.0 billion for the second section. There were also environmental concerns related to Lake Baikal (a UNESCO-protected site) and Perevoznaya Bay (a sensitive area for whales). In the meantime, environmental and safety problems have been solved, but total construction costs may be double the initial estimate when both sections are completed. The first 2,800-km section of the ESPO pipeline, owned by Transneft, is expected to be completed by December 2008, with the second section to be finished in 2010. The route has been amended and the pipeline now passes 200 km from Lake Baikal. The pipeline is designed to deliver 80 million tons/year (1.6 million bpd) of Siberian oil to China and Asia-Pacific countries.

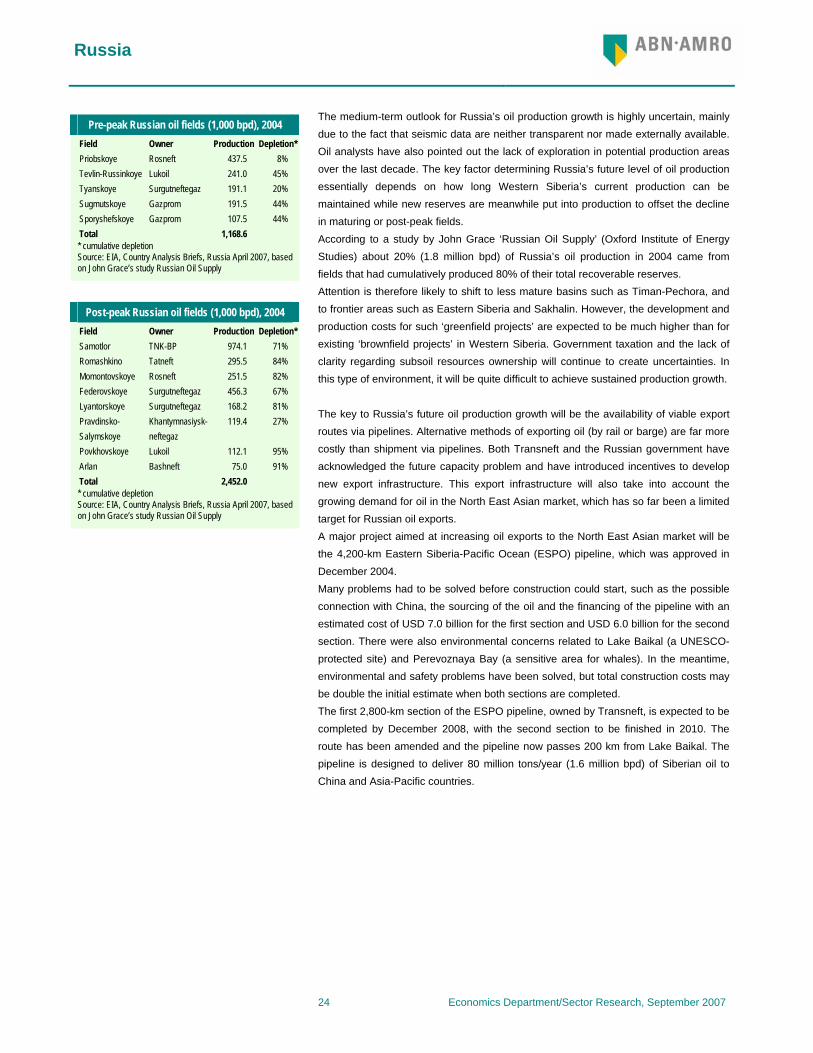

Pre-peak Russian oil fields (1,000 bpd), 2004 Field Owner Production Depletion* Priobskoye Rosneft 437.5 8% Tevlin-Russinkoye Lukoil 241.0 45% Tyanskoye Surgutneftegaz 191.1 20% Sugmutskoye Gazprom 191.5 44% Sporyshefskoye Gazprom 107.5 44% Total 1,168.6 * cumulative depletion Source: EIA, Country Analysis Briefs, Russia April 2007, based on John Grace’s study Russian Oil Supply

Post-peak Russian oil fields (1,000 bpd), 2004 Field Owner Production Depletion* Samotlor TNK-BP 974.1 71% Romashkino Tatneft 295.5 84% Momontovskoye Rosneft 251.5 82% Federovskoye Surgutneftegaz 456.3 67% Lyantorskoye Surgutneftegaz 168.2 81% Pravdinsko-Salymskoye

Khantymnasiysk-neftegaz

119.4 27%

Povkhovskoye Lukoil 112.1 95% Arlan Bashneft 75.0 91% Total 2,452.0 * cumulative depletion Source: EIA, Country Analysis Briefs, Russia April 2007, based on John Grace’s study Russian Oil Supply

Russia

25 Economics Department/Sector Research, September 2007