Embed Size (px)

Citation preview

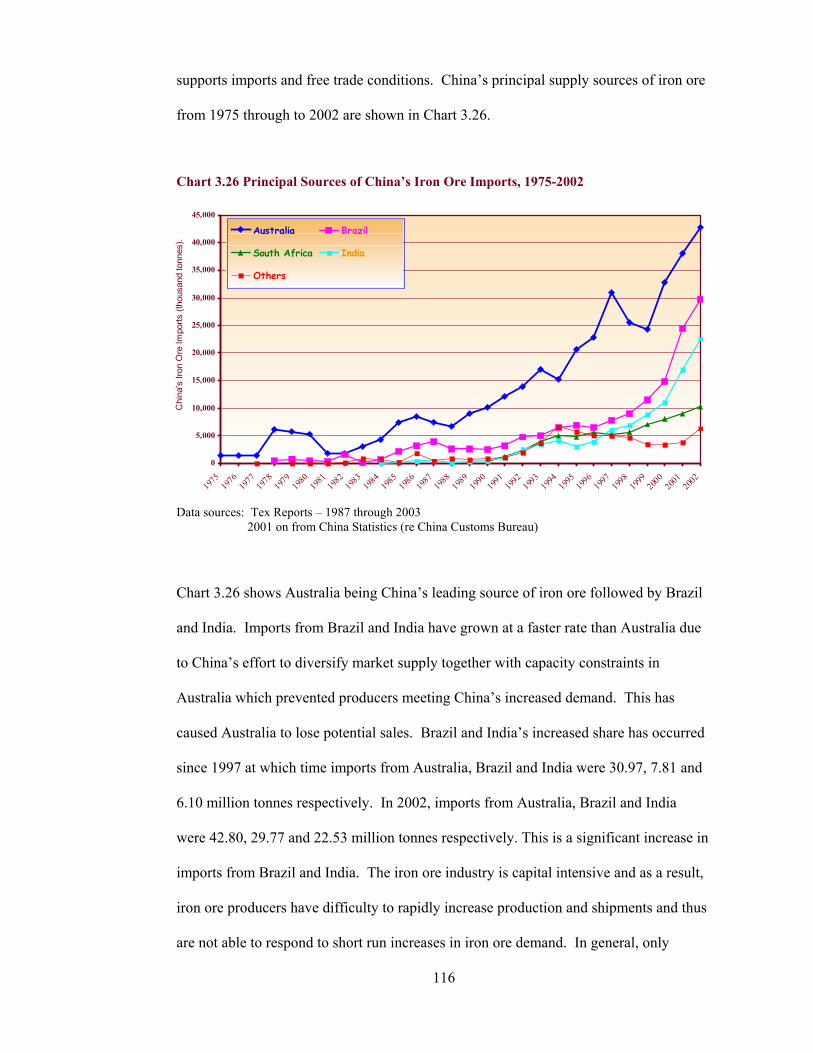

Role of the Chinese Steel Industry in the Economic Development of China and

Australia’s Contribution to the Industry as a Supplier of Raw Materials

By

James G. Trench MSc, Grad Dip, BSc Hons

This Thesis is presented for the degree of

Doctor of Philosophy of Murdoch University

- 2004 -

ii

Declaration

I declare that this thesis is my own account of my research and contains as its main

content work that has not previously been submitted for a degree at any tertiary

education institution.

James G. Trench

iii

Abstract

The objective of this thesis is to examine the extent to which the iron and steel industry

in China has been a major contributor to the recent economic development and growth

of the Chinese economy and whether this will continue. Key elements of China’s

economic development model – THE CHINESE MODEL - based on the steel industry

are presented and demonstrate the impact of China taking “great leaps forward” in its

steel production capacity to become the world’s leading steel producer and one of the

fastest growing economies. This bold step was undertaken at times when the global

steel industry was burdened with overcapacity and economic pressures. At the same

time, this thesis examines the role played by the Australian iron ore industry in

supporting the Chinese steel industry through its iron ore trade with China and how this

role will evolve.

The development of the iron and steel industry in China reflects not just the role played

in the overall expansion of the Chinese economy through technical input-output

relationships, but it also reflects control and historical characteristics taken from China's

social and political context. Starting from the views of Sun Yat Sen, and flowing

through Mao Zedong, and then into later leaders, the steel industry was always intended

to be the basis for the modernisation of the Chinese economy. The Great Leap Forward

of the 1950s was an ill-founded reflection of that fundamental view, but the failure in

that case did not cause a shift away from that basic perspective. Instead a more

comprehensive perspective was provided and this came to the fore at the start of the

reform process in the early 1980s.

iv

The role of the steel industry in the recent modernisation of China is traced using the

policy foundations and directions that were adopted combined with empirical data on

the investment and growth in the industry, as well as the role of the output of the steel

industry in the expansion of other industries in China. To the extent that conditions in

China may be replicated in other countries, the Chinese experience using the iron and

steel industry as the key element in the industrialisation of that economy will have

important lessons.

At the same time, this thesis demonstrates weaknesses in a development model that has

the iron and steel industry as the leading sector. One major weakness is the reliance on

imported raw materials and at this point the Chinese experience with Australia as a

source of raw materials becomes relevant. Australia’s role as a reliable supplier and

partner for the steel industry enabled the steel industry to expand in a low risk

environment with respect to the price and availability of raw materials.

v

Contents

1 INTRODUCTION...................................................................................................1

1.1 THE OBJECTIVE OF THIS THESIS .........................................................................3 1.2 ACADEMIC REVIEW............................................................................................4 1.3 RESEARCH METHODOLOGY ...............................................................................8 1.4 OVERVIEW OF CHAPTERS.................................................................................10

2 OVERVIEW OF THE GLOBAL IRON AND STEEL INDUSTRY ...............13

2.1 STEEL INDUSTRY - DRIVER OF THE ECONOMY .................................................14 2.2 INDUSTRY STRUCTURE AND BEHAVIOUR - BARRIERS TO ENTRY .....................21 2.3 ECONOMICS OF THE STEEL INDUSTRY - FACTORS OF PRODUCTION..................22

2.3.1 Iron Ore - Principal Input Material to the Steel Industry ......................28 2.4 LEADING STEEL PRODUCING COUNTRIES ........................................................29 2.5 STEEL PRODUCTION PROCESSES FOR THE TOP SIX PRODUCING COUNTRIES....31

2.5.1 Continuous Cast Steel Making Process ..................................................31 2.5.2 Steel Production in Electric Arc Furnaces .............................................33 2.5.3 Production of Steel in Oxygen Blown Converters ..................................35 2.5.4 Steel Production in Open Hearth Furnaces............................................36 2.5.5 Summary of Global Supply .....................................................................37

2.6 STEEL DEMAND ...............................................................................................37 2.6.1 World Apparent Crude Steel Consumption.............................................38 2.6.2 Per Capita Steel Demand - Six Leading Producer Countries ................40 2.6.3 Summary of Global Demand...................................................................41

2.7 EMPLOYMENT IN THE STEEL INDUSTRY ...........................................................42 2.8 DISCUSSION .....................................................................................................43 2.9 CONCLUSION....................................................................................................45

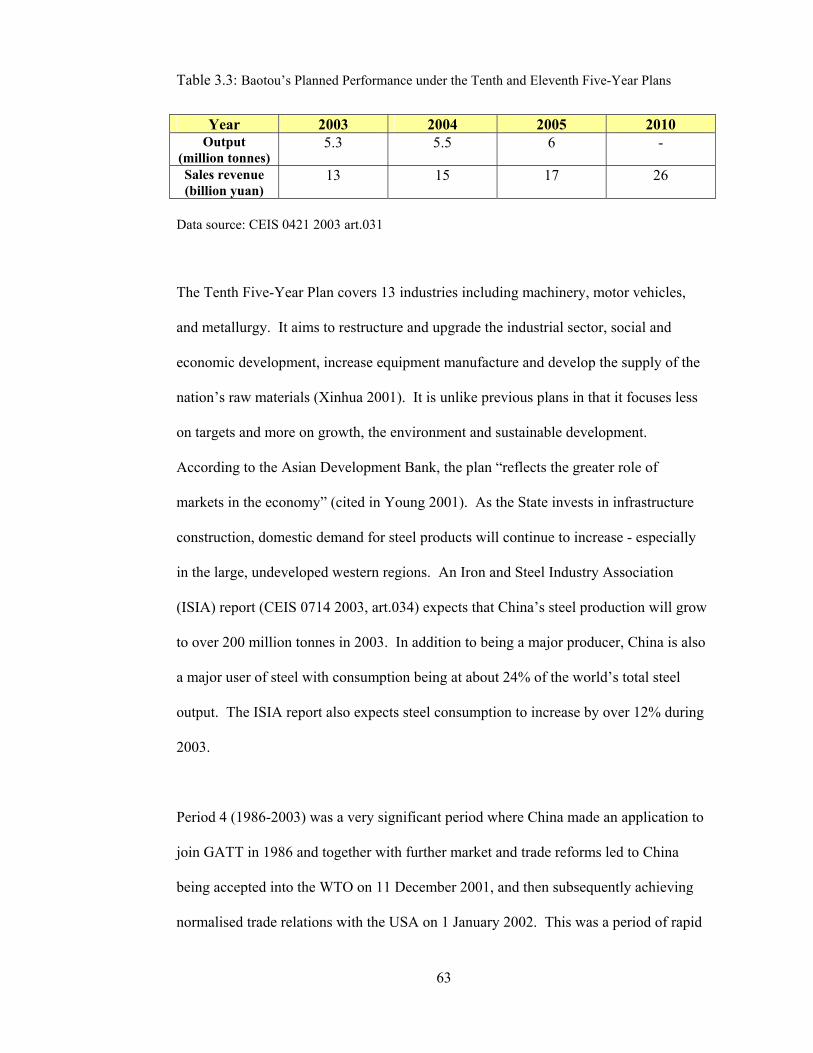

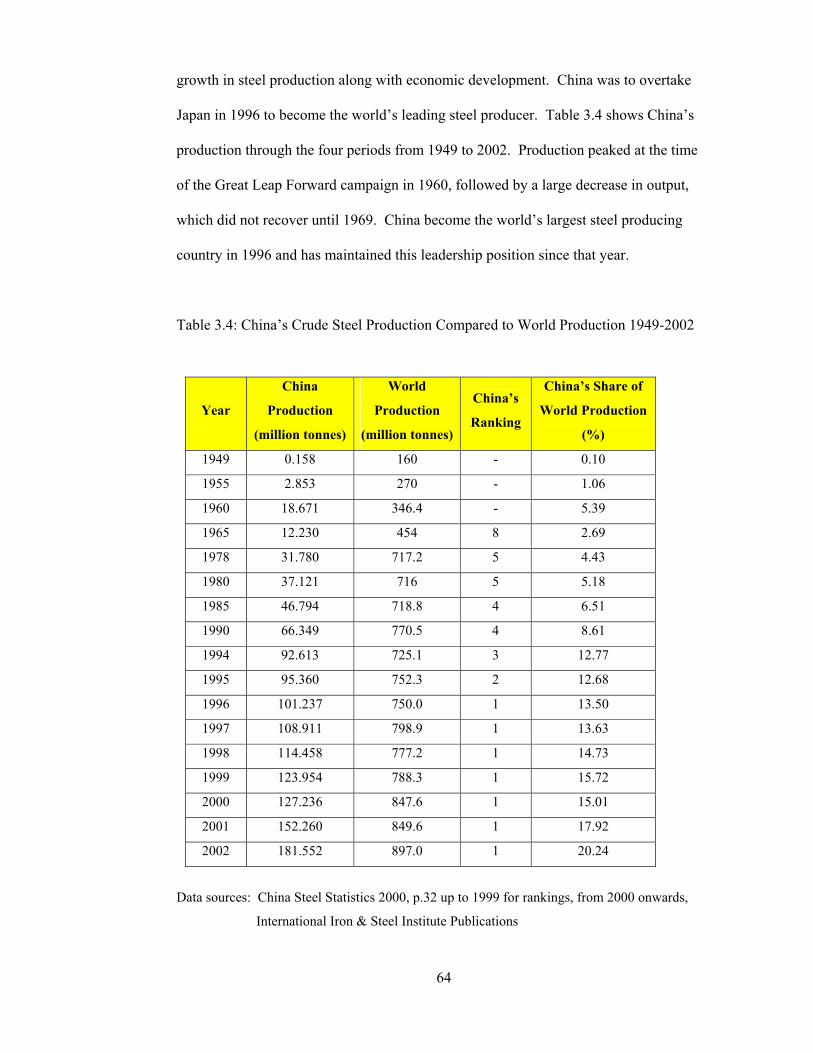

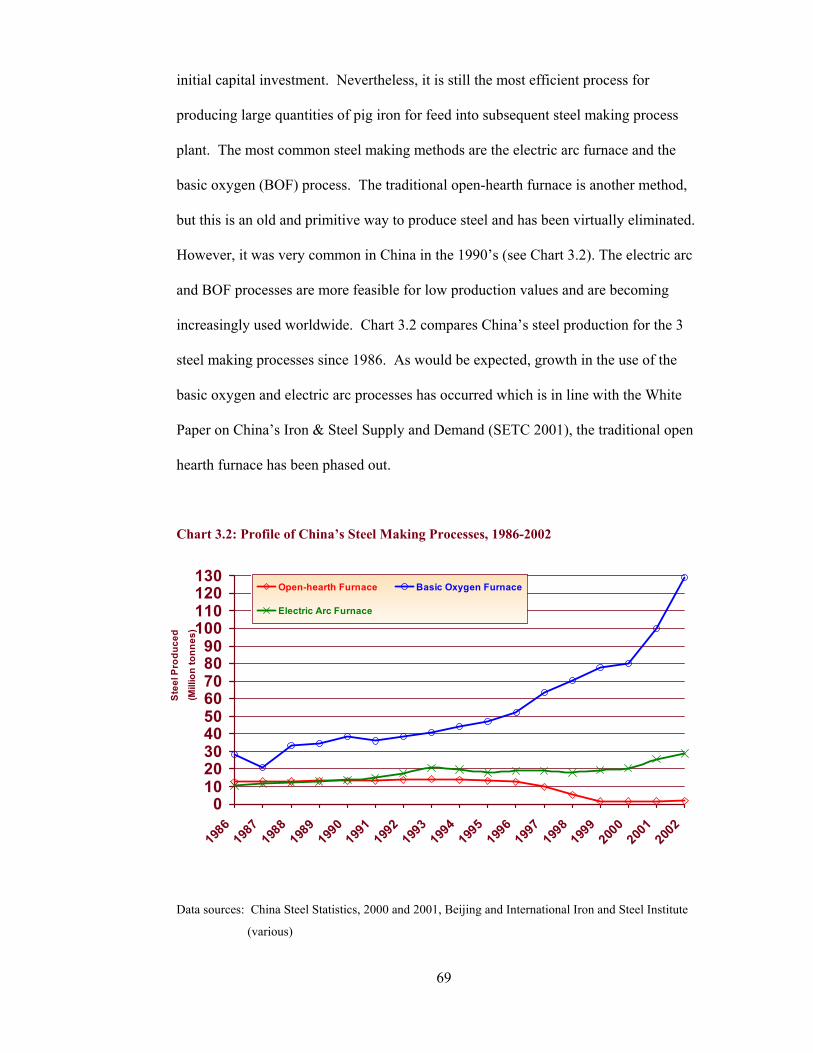

3 CHINESE IRON AND STEEL INDUSTRY–MARSHALL OF INDUSTRY 46

3.1 HISTORY OF CHINA’S IRON AND STEEL INDUSTRY...........................................47 3.2 PROFILE OF CHINA’S TOP 10 STEEL PRODUCERS...............................................65 3.3 CRUDE STEEL PRODUCTION BY STEEL MAKING PROCESS ...............................68 3.4 CONTINUOUSLY CAST STEEL DEVELOPMENT ..................................................70 3.5 STEEL PRODUCTION AND ECONOMIC GROWTH................................................71

3.5.1 Gross Domestic Product .........................................................................75 3.5.2 Agriculture & Industrial Production ......................................................78 3.5.3 Money Supply ..........................................................................................82

3.6 PRODUCTIVITY AND ECONOMIC EFFICIENCY ...................................................85 3.6.1 Iron Ore Production – Principal Input Factor .......................................89 3.6.2 Energy Consumption - Input Factor 3 ....................................................91

3.7 TRADE DEVELOPMENT - STEEL AND IRON ORE ................................................97 3.8 CHINA’S IRON ORE DEMAND .........................................................................100

3.8.1 Elasticity of Demand for Steel and Iron Ore ........................................105 3.8.2 Intensity of Demand ..............................................................................107 3.8.3 Automobile Production and Steel Demand...........................................111 3.8.4 Shipbuilding and Steel Demand............................................................113

3.9 IRON ORE SUPPLY CHARACTERISTICS............................................................115 3.9.1 Iron Ore Supply Elasticity.....................................................................117

4 AUSTRALIA’S ROLE SUPPLYING CHINA’S STEEL INDUSTRY..........120

vi

4.1 AUSTRALIA’S ROLE IN SUPPORTING CHINA’S ECONOMIC DEVELOPMENT .....120 4.1.1 Trade between China and Australia .....................................................120

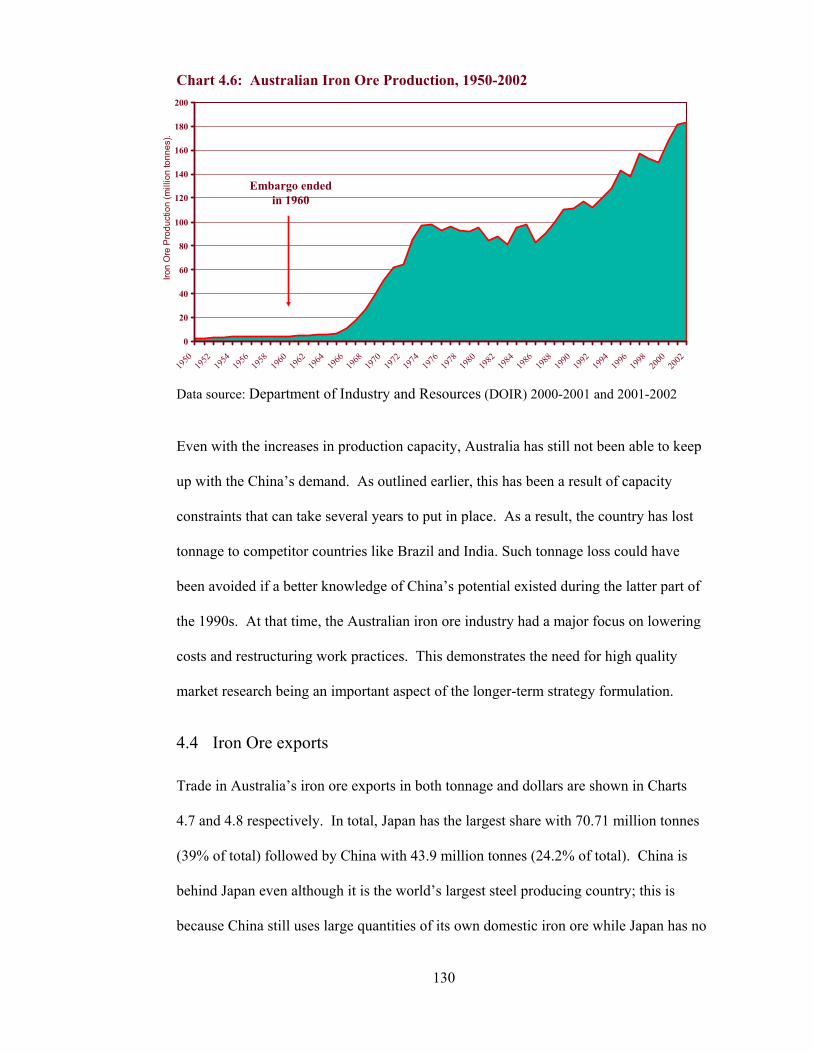

4.2 COMPARATIVE ADVANTAGE..........................................................................127 4.3 IRON ORE PRODUCTION .................................................................................129 4.4 IRON ORE EXPORTS ........................................................................................130

4.4.1 Outlook for Australia’s Iron Ore Production .......................................133 4.4.2 Pricing of Iron Ore - Setters or Takers.................................................134 4.4.3 Economics of Iron Ore Sea Borne Trade..............................................137 4.4.4 Outlook for Australian Iron Ore Trade.................................................140

5 CHINA’S TRADE DEVELOPMENT...............................................................142

5.1 CHINA’S INTERNATIONAL TRADE ..................................................................143 5.1.1 China’s approach to trade ....................................................................148

5.2 TRADE WITH JAPAN AND THE USA ................................................................150 5.3 CHINA’S FUTURE TRADE OUTLOOK - FACTORS INPUTS AND EFFICIENCY......152

5.3.1 How China develops trading strategy – Buying and Selling ................153 5.3.2 Olympics 2008 and Shanghai World Fair 2010 ...................................154 5.3.3 Infrastructure development ...................................................................155

5.4 FREE TRADE AND TARIFFS .............................................................................157 5.5 WORLD TRADE ORGANISATION (WTO) ENTRY.............................................165 5.6 FOREIGN TRADE POLICY................................................................................170

5.6.1 Foreign Investment in China.................................................................171 5.7 FUTURE OF CHINA’S STEEL INDUSTRY...........................................................180

5.7.1 Outlook for steel production .................................................................181 5.7.2 Research, Development and Sustainability...........................................184 5.7.3 Environmental Issues ............................................................................187 5.7.4 China’s Economic Development ...........................................................188

5.8 STRUCTURAL WEAKNESSES IN ECONOMY .....................................................191 5.8.1 China’s Currency..................................................................................191 5.8.2 Finance - debt levels .............................................................................196 5.8.3 Reform Generated Unemployment – Threat to Economic Stability......205

6 FINDINGS ...........................................................................................................209

6.1.1 Key Research Findings .........................................................................210

7 RECOMMENDATION AND CONCLUSION ................................................238

7.1 SUMMARY OF FINDINGS .................................................................................239 7.2 RECOMMENDATIONS......................................................................................242

7.2.1 China.....................................................................................................242 7.2.2 Australia................................................................................................243 7.2.3 Other Countries.....................................................................................244

7.3 FURTHER RESEARCH......................................................................................244 7.4 CONCLUSION..................................................................................................245

8 REFERENCES....................................................................................................248

9 APPENDICES .....................................................................................................275

9.1 GLOBAL IRON & STEEL INDUSTRY DATA ......................................................275 9.1.1 China Steel Balance ..............................................................................275 9.1.2 Japan Steel Balance ..............................................................................276

vii

9.1.3 Global Steel Production, 1900-2002 ....................................................277 9.1.4 Summary-Crude Steel Production ........................................................278 9.1.5 China Steel Growth Predictions ...........................................................279 9.1.6 Summary-Continuously Cast Steel Production.....................................280 9.1.7 Summary-Production of Steel in Oxygen Blown Converters ................281 9.1.8 Summary-Production of Steel in Electric Arc Furnaces.......................282 9.1.9 Summary-Production of Steel in Open Hearth Furnaces .....................283 9.1.10 Summary-Apparent Crude Steel Consumption .....................................284 9.1.11 Summary-Apparent Crude Steel Consumption per Capita ...................285 9.1.12 Productivity of Top 6 Crude Steel Producers .......................................286 9.1.13 Ranking of Steel Producing Countries, 1993-2002 ..............................287 9.1.14 Top 50 Steel Producing Companies, 1999-2002 ..................................289

9.2 CHINA AND GLOBAL IRON ORE DATA ...........................................................291 9.2.1 World and China’s Historical Iron Ore Production.............................291 9.2.2 Australian Historical Iron Ore Production, 1950-2002 .......................292 9.2.3 Australian Exports of Iron Ore, 2000-2002..........................................293 9.2.4 China Iron Ore Imports and GDP, 1981-2002.....................................294 9.2.5 Iron Ore Fines Pricing into Asia, 1973-2002 .......................................295 9.2.6 Composition of Iron Ore Imports to China, 1975-2002 .......................296 9.2.7 Composition of Australian Iron Ore Exports, 1975-2002 ....................297

9.3 KEY PHASES OF CHINA’S REFORM..................................................................298 9.4 CHINA STEEL INDUSTRY ................................................................................299

9.4.1 Steel products supply in 2002 with forecast for 2003...........................299 9.4.2 China's output of major steel products, 2002 .......................................299 9.4.3 Import and export of major steel products, 2002..................................300 9.4.4 Output of Non Ferrous metals, 2002 ....................................................301 9.4.5 Import and Export of Major Metals, 2002............................................302 9.4.6 Import Value of Major Commodities, 2002 ..........................................303 9.4.7 China’s Import Volume of Major Commodities, 2002..........................303 9.4.8 Automobile Makes, Output and Sales in China, 2002 ..........................304 9.4.9 Automobile Output by Region, 2002 .....................................................305

9.5 SELECTED CHINA ECONOMIC INDICATORS.....................................................306 9.5.1 Economic Data Base.............................................................................306 9.5.2 China’s GDP, Trade and Output, 1981-2002.......................................307 9.5.3 China’s Money Supply, 1981-2002.......................................................308 9.5.4 Debt Level Comparisons, 1981-2002....................................................309 9.5.5 Intensity of Steel Demand, 1952-2002 ..................................................310 9.5.6 China’s Trade with Australia, 1982-2002 ............................................311 9.5.7 Industrial Added Value by China’s Regions, 2002 ...............................312

9.6 CHINA MAP - STEEL AND IRON ORE REGIONS................................................313 9.7 AUSTRALIA – CHINA SHIPPING MAP ..............................................................314 9.8 DEVELOPMENTS IN CHINA’S IRON & STEEL INDUSTRY..................................315 9.9 EXTRACT FROM ZHU RONGJI’S GOVERNMENT WORK REPORT ......................316 9.10 COMPOSITION OF CHINA'S EXPORTS TO USA, 2002.......................................317 9.11 COMPOSITION OF CHINA'S IMPORT FROM USA, 2002 ....................................318 9.12 STEEL FOR THE BEIJING OLYMPICS ................................................................319 9.13 FIXED ASSET INVESTMENT IN CHINA 2002 ....................................................320 9.14 AUSTRALIA CHINA TRADE.............................................................................321

9.14.1 Summary of Australian Trade with Top 5 Countries, 2000-2002.........321 9.14.2 Australian Merchandise Trade by Country, 2000-2002 .......................322

viii

9.14.3 Australia’s Top Trades with China, 1996-2002....................................323 9.14.4 Australia – China Trade breakdown, 2002...........................................324

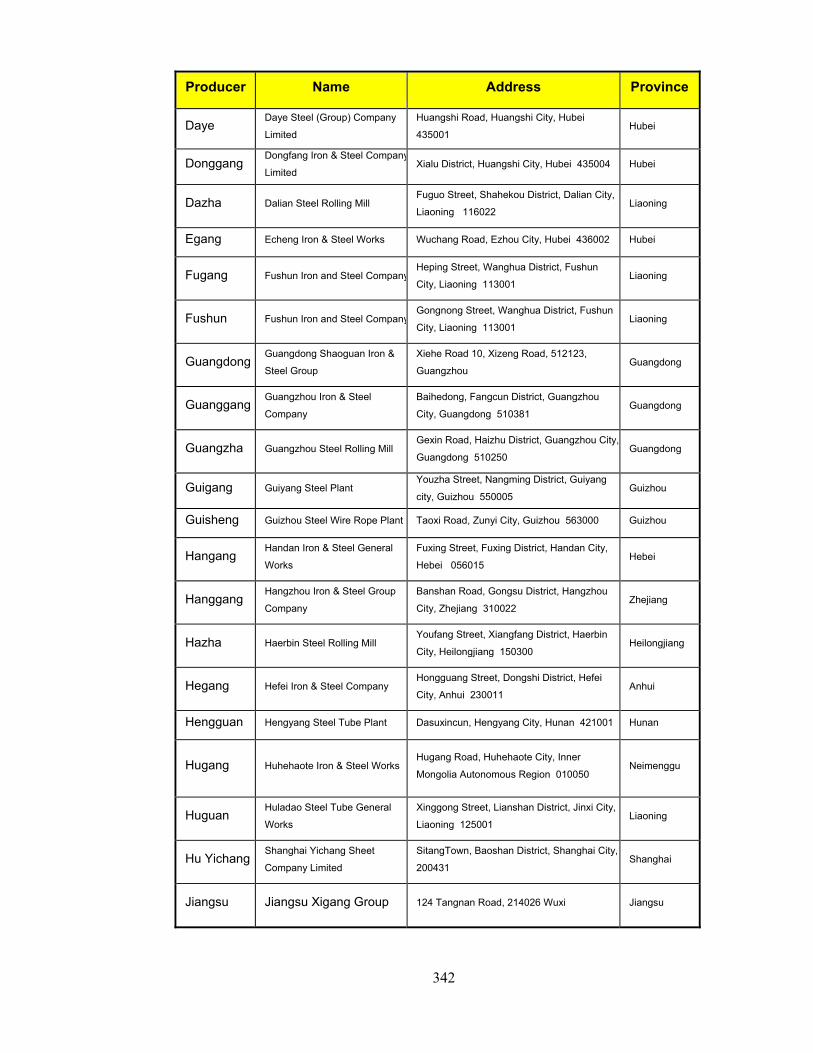

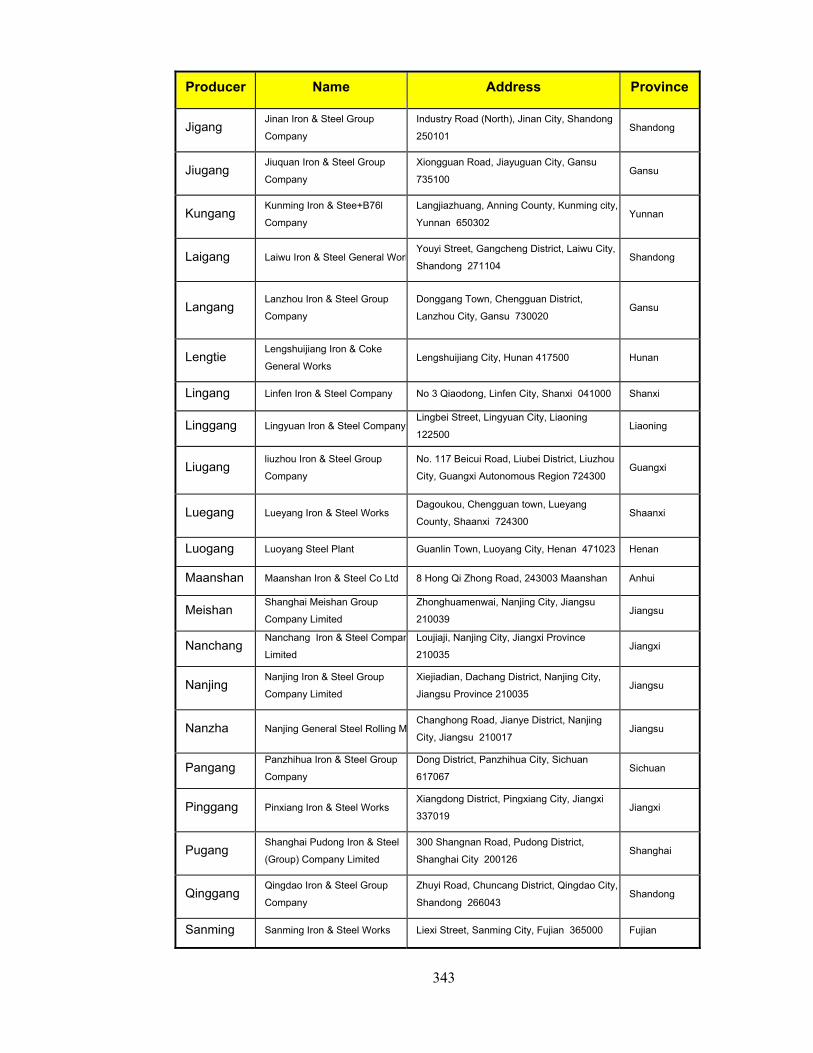

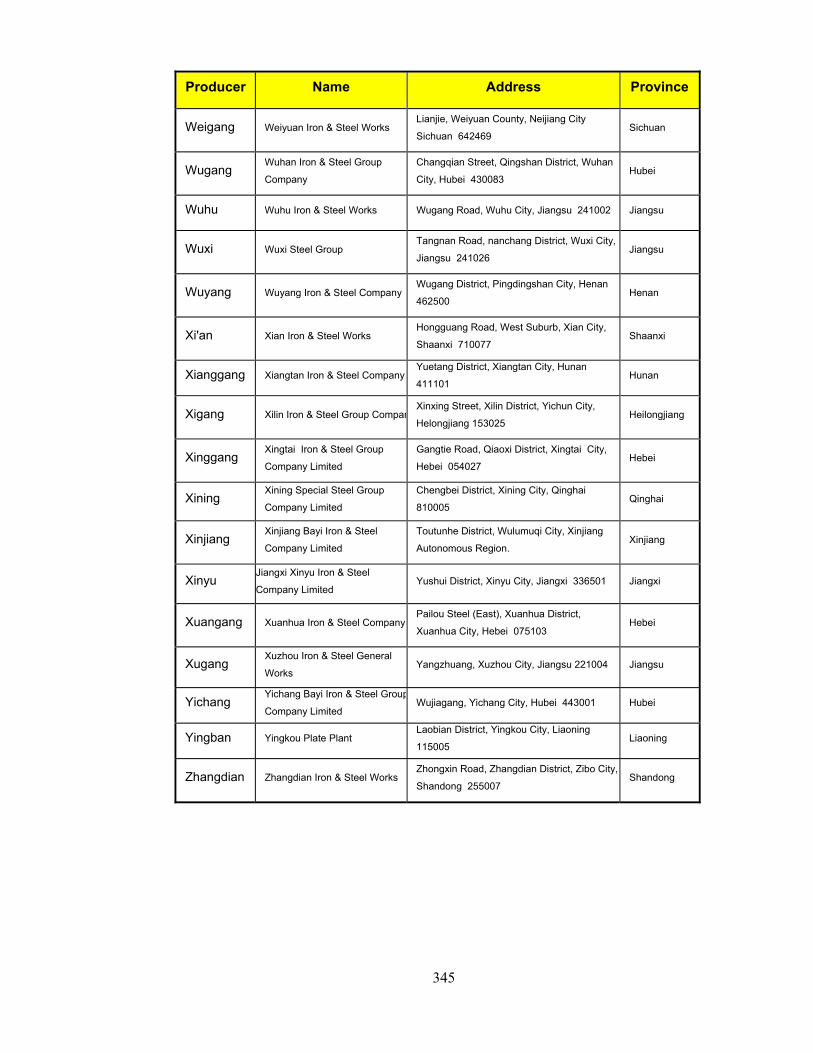

9.15 CHINA’S TOP ELEVEN IMPORT COMMODITIES, 2000 AND 2001 .....................325 9.16 MAP SHOWING AUSTRALIA’S IRON ORE MINES ............................................326 9.17 STEEL TARIFF CHANGES FOLLOWING WTO MEMBERSHIP ............................327 9.18 CHINA STEEL COMPANIES DATA BASE ...........................................................341 9.19 STATE COUNCIL .............................................................................................346

ix

Acknowledgements

I extend my gratitude to Murdoch University which provided financial and professional

support for this research programme and also supported me in presenting papers at

international conferences.

I also extend my thanks to my employer BHP Billiton Marketing Asia Pte Ltd, Minister

Song Ruixiang, Head of China’s Seismological Bureau, Professor Herb Thompson who

had the task of helping me develop my initial research programme and Dr Frank

Harman who subsequently edited my initial drafts.

A special thanks is given to Dr Dora Marinova who had the task of supervising me

during the latter and most demanding part of my research. Her experience and wisdom

were very helpful in enabling me to put my research thesis into its final form.

I specially acknowledge the excellent publications issued by the China Economic

Information Service (a Xinhua news agency publication), the Asian Development Bank,

the International Iron and Steel Institute, the World Trade Organisation, CRU

International (which publishes a wide range of journals on the metals industry). Each

one of these organisations produces many useful publications and information, which

was helpful to me during my research.

Last and not least is to thank my dear wife, Dr Gaomai Trench, who endlessly provided

moral support during many intense study periods both overseas and in

Australia. She is my inspiration.

1

1 Introduction

From the age of 12 and as a young martial arts enthusiast, I had an intense interest in

Asian culture. Then as a young professional engineer, I witnessed the emergence of

Asian industry at the expense of western industry. Japan emerged as the world’s

leading steel making country. It seemed that no country could possibly compete with

such a culture and strengthening economy. It was not until I became involved in the

iron and steel industry in the early 80s, that my interest started to focus on China. By

the early 90s, I could see an eclipse of Japan’s unbeatable rising sun was occurring.

China through its market and social reform programmes was emerging on the horizon

and was soon to become the leading steel making country.

China had indeed begun its journey in becoming a significant trading nation. Industrial

output was increasing, infrastructure was being improved, steel demand was increasing

and most importantly the iron and steel industry was modernising and growing. In

1996, crude steel production from China overtook Japan’s iron and steel industry (101.2

cf 98.8 million tonnes) and has continued to do so. It seems that China’s miraculous

development is now unbeatable. At the same time, and resulting from China’s reliance

on imports of raw materials, Australia was playing an ever-increasing role in China’s

economic development and China had become one of its leading trading partners. How

such a transformation could occur intrigued many. Working in the Australian iron ore

industry highlighted that China’s iron and steel industry had an important role to play in

China’s economic development, but this was not enough to enable an understanding of

what was really behind such development, its drivers and where it would lead to. It was

not until after studying Chinese language, culture and history followed by a Masters

2

programme in Mineral Economics that I started to take great interest in not only the

significant role that the iron and steel industry had played in China’s economic

development, but also in the role that history and culture played in this development.

With a view to understanding and subsequently documenting the model behind China’s

success, this research programme was undertaken.

In Chinese culture, historical events are to be understood as determinants for the future.

The view of the importance of nationally developing the iron and steel industry can be

traced back to Dr Sun Yat Sen and subsequently maintained by Mao Zedong even

though his Great Leap Forward campaign was a complete failure. In the last quarter of

the 20th century, China started to achieve enormous success in its efforts to modernise

its industrial capability. Towards the end of the century, the centralised planning

system was replaced by a transitional and now market economy. By exploring the

development of China’s economy and by examining historical and cultural

characteristics behind that development, this thesis will attempt to give answers to the

main research question which is: What role did the Chinese iron and steel industry play

in the economic development of China? In order to answer it, the following sub-

questions are addressed:

• Did the industry support the building of a more prosperous society or did people

have to pay for wrong decisions?

• Can the industry sustain China’s economic development?

• Being a major supplier of raw materials (iron ore in particular), what role has

Australia played and will continue to play in supporting China’s development?

• What are the lessons for the future or for any other countries?

3

1.1 The Objective of this Thesis

The specific aims of the study are to:

• Analyse trends in the development of the Chinese iron and steel industry

including Australia’s contribution

• Examine previous literature analysing this development

• Draw an understanding of the development model

• Identify weaknesses in the model

• Make recommendations.

To do this, the research explores, examines and documents the characteristics behind a

long-standing view held in China that steel industry development and subsequent

industrialisation of the country would be a successful model for the economic

modernisation of China and that it would also lead to achieving the status of being a

modern world power. At the same time, the thesis outlines China’s iron and steel

industry development relative to the global iron and steel industry and the role that

Australia plays in supplying the principal raw material input, iron ore, to China.

The research also exposes weaknesses in China’s modernisation model based on the

expansion of the steel industry and industrial reform. Examples of these are social

pressures arising from higher unemployment and increasing financial instability seen

from the high level of non-performing loans that exist particularly in state owned

enterprises that have undergone significant reform. Whether growth in steelmaking

capacity can be sustained after domestic consumption demand cools off is examined.

The importance of China’s currency for the steel industry and continued economic

development is also considered.

4

1.2 Academic Review

Extensive studies have been published about China’s economy, but not so much work

undertaken in relation to the Chinese Steel Industry and its role as a model in

developing the Chinese economy. Jefferson (1990) examined sources of enterprise

efficiency and productivity growth in China’s steel industry. His work showed that

during the years following the Great Leap Forward, productivity performance was poor

but improved significantly as a result of the reforms that took place in the 1980s.

Following Feng’s (1994a) study on restructuring of the international steel industry and

changing comparative advantage and Labson et al’s (1995) publication on China’s

emerging steel industry and its impact on world iron ore and steel market, much of the

academic China steel industry research has been undertaken by Yanrui Wu. His work

includes a 2000 paper outlining recent developments and prospects for the Chinese steel

industry (Wu 2000) and a 1998 study on the economics of the East Asia steel industries

in which a chapter was dedicated to China’s iron and steel industry (Wu 1998). In other

work on the productive efficiency and performance in Chinese enterprises, he illustrates

that China’s iron and steel industry is only achieving around 60% of its potential output

and that this is typical of a developing economy (Wu 1995 and 1996).

Tcha and Wright (1999) present results of analysis of their model for determining

China’s demand for importing Australian iron ore. Crompton and Wu (2000) further

examine features of Chinese steel consumption demand. Greig’s (1997) discussion

paper on emerging trends, issues and policies in metals markets and East Asia is a

convenient collection of several University of Western Australia’s discussion papers in

which Wu also provides input. In relation to China’s iron and steel industry, the paper

covers supply and demand characteristics. It also briefly looks at Western Australia as

5

a supply source of iron ore. Extending to Wu’s work is Xiao-Guang Zhang & Siqi

Zhang (2001) who further discuss technical efficiency in China’s iron and steel

industry.

With regards to reform and economic growth, Wu and Ye (1998) as editors present a

selection of papers that were given at the International Conference on the Economies of

Greater China, held at the University of Western Australia in 1997. The papers include

macroeconomic policy and reforms; trade reform and economic growth and regional

development. Bell et al (1993) in their book on China’s market reforms outline

developments since China’s 1949 revolution - embarking on a strategy of socialist

economic development based on self reliance, central planning and directed allocation

of resources. They illustrate by the 1970s the economy through trade and investment

was opened up, but still contained a large proportion of public ownership. The authors

show how China’s reform was unlike other centrally planned economies of Eastern

Europe in that the process was gradual and not “big bang”. A summary of the reform

phases is outlined in Appendix 9.3.

The World Bank has produced many papers on China. Two such papers on China’s

comparative advantage (Yeats 1991) and foreign trade reform (World Bank 1994) were

found particularly useful. In the comparative advantage paper, tables on comparative

advantage indices are compared with Japan and other Asian countries between 1970 and

1987. It concludes that China’s main advantage is with its huge pool of low cost labour

resources and that the country has large potential in expanding its international trade as

it builds on this advantage. In the China foreign trade reform paper, a detailed overview

of China’s reform process is outlined. It is interesting to note that with regards to

6

inefficiency in the country’s steel industry due to fragmentation of production facilities,

in 1989 it was estimated that as much as 95% of enterprises were operating below

optimum.

Feng (1994b) in his article on China’s steel industry suggests that a clear trend in

developing economies attracting steel industry at the expense of industrialised countries

exists. He outlines this is attributed to increased national demand in developing

economies which in turn facilitates supply side capital stocks and economic reforms.

This then promotes technical efficiency and resource allocation improvements.

For understanding the history that shaped the Chinese psychology and attitude that

enabled economic reforms to be effective, cultural literature works were found very

useful. Wagner’s (1997) study of the traditional Chinese iron industry and how it

changed was useful from a historical perspective of the country’s steel industry

development.

Most of the iron and steel statistical data came from Chinese Government Departments

(their publications, internet websites and people) and the International Iron & Steel

Institute (their publications and internet website)1. Economic data were collected from

the Asian Development Bank (their internet website and publications). Much of the

current financial and economic news was obtained from the Asian media during regular

searches. The China Economic Information Service (CEIS) was monitored over several

years and was found to be one of the best sources of information on China’s steel

industry, mineral resources activity and general economic news.

1 Also documents searched for and found hidden away in old library files-discarded as being too old.

7

In relation to the actual role played by China’s steel industry on the country’s economic

development, apart from in depth academic analysis of aspects, which generally related

to efficiency, it was found that much of the published work available tended to be rather

old and did not articulate or examine the history behind the role played by the industry

in China’s economic development and its industrialisation programme. This research

was needed to bring together the history behind the development of an industry that was

intended to be the country’s major driver towards industrialisation and how it compared

with the global industry. This being particularly significant since during a large

proportion of China’s period of rapid economic development, the global iron and steel

industry suffered from overcapacity and inefficiency.

Very little academic work has been done that takes a forward looking perspective in

examining how such an industry being a key driver of Chinese economic development

will develop. As conditions change in China, weaknesses in a model based on

industrialisation are sure to emerge. In order that both China and those engaging in

trade with the country better understand risks, it is useful to openly discuss these

weaknesses. It is considered necessary in a study researching the role played by a major

industry sector, to examine whether the viability of the industry can be sustained as the

country develops and its exposure to strategic issues increases.

8

1.3 Research Methodology

The research was conducted over several years in Australia, China and Singapore. It

consisted of reviewing Asian media, literature and databases held by international

organisations like the International Iron & Steel Institute, the Asian Development Bank,

the World Bank, the International Monetary Fund and Chinese Government

Departments. Several research visits were made to China where discussions were held

with Chinese Government Departments and Universities in both Beijing and Tianjin. A

trip was also made to the United Kingdom (a country that formerly had a strong iron

and steel industry). Support for the research was initially given by Rio Tinto Pty

Limited and subsequently by BHP Billiton Pty Ltd, two of the world’s largest mineral

resources companies and leading iron ore producers and suppliers to the Chinese steel

industry.

Several presentations and papers on this research were given. The most significant

were at the 2001 Global Iron Ore Conference in London, the 2002 Global Iron Ore &

Steel Forecast Conference in Australia and at a 2002 Hi-Tech trade presentation in

Tianjin, China. Participation in these events helped develop important contacts in

China which were helpful in providing further insight into the key features of steel

industry development that helped transform China’s economy and restore national

pride.

Economic and steel industry data were collected and stored in databases much of which

has been shown in the Appendices. The research focuses on China’s economic

development and examines the following hypothesis in relation to that development:

9

From a long-standing national development perspective, a firmly based indigenous

steel industry not relying on imported steel provides a secure base for modernisation

and economic development through industrialisation and international trade.

This research tests this hypothesis by examining in detail the following:

• In view of the importance of culture and history behind the drive towards

modernisation and industrialisation, Chinese literature going back to Sun Yat

Sen (1866-1925) - who led the first Chinese Republic in 1911

• An analysis of the failure of the Great Leap Forward campaign which started in

the early part of 1958, officially ended in December 1958, but many of the

programmes still continued through to 1963 (the end of the second five year

planning period in which the campaign was to modernise China’s economy)

• The details of the modernisation programme during and post Mao Zedong – this

covers his first Five-Year Plan (1953-1957) and subsequent plans. Post Mao

reforms started with Deng Xiaoping just prior to Mao Zedong’s death in 1976

• An outline of the growth of the Chinese steel industry (relative to the global

industry) from the middle of the 20th century

• How the iron and steel industry contributed to enhancing other industries

through increasing the production of exports and also reducing reliance on

imports

• The most important input raw material required for the production of iron and

steel is iron ore. This is a resource that China lacks; so having access to a

reliable source of this principal input is essential for sustaining the industry.

Australia is a key source for this raw material, and therefore Australia’s

10

contribution to China’s iron and steel industry as a supplier of raw materials is

examined

• Structural weaknesses, that may just be a part of the economic cycle, that

threaten the ability of the iron and steel industry to continue developing and

which in turn could lead to the industry being a drain on the economy.

1.4 Overview of Chapters

Before one can quantify the role China’s iron and steel industry has had on the

development of the country’s economy, it is necessary to understand the relative

position within the global iron and steel industry. This thesis starts with an in depth

look at the global iron and steel industry in Chapter 2. This is to provide an

understanding of the industry and enable one to better quantify and put into context the

importance of the steel industry as a key economic driver. In order to subsequently be

able to quantify the relative magnitude of China’s iron and steel industry development

and its corresponding rankings, global historical industry production data up to the end

of 2002 are presented along with selected detailed industry data and trends for the

world’s leading steel producing countries.

Chapter 3 follows with a historical review and detailed examination of the Chinese iron

and steel industry. This outlines the significant milestones in China’s history that had a

bearing on the philosophy behind developing an iron and steel industry to be a key

factor in rebuilding the country and driving the economy. Reforms in both political

ideology and economic management that put in place the appropriate framework for

iron and steel production are discussed in detail. The significant developments since the

birth of the People’s Republic in 1949 are highlighted along with changes in the

11

industry’s characteristics which are shown and discussed along with economic data and

trends. The country’s comparative advantage in a range of steel production processes

along with improvements in economic efficiency in relation to factors of production and

resource allocation are considered. These demonstrate and quantify the nature and

importance of the role played by the industry on the country’s economic development

and modernisation at the same time providing a detailed assessment of China’s iron and

steel industry in relation to the global iron and steel industry.

Chapter 4 presents an outline of Australia’s role in supporting China’s iron and steel

industry and the country’s economic development. Australia’s endowment of iron ore

reserves gives it a comparative advantage and this makes it the source of choice for

China and has elevated Australia to being China’s principle supplier of iron ore. Iron

ore production and supply economics are examined and discussed. The potential for

future trade developments between Australia and China is also assessed.

Chapter 5 outlines China’s economic development and its approach to international

trade. As the relationship between the nation’s steel industry and economy develops,

the appeal of international trade and foreign investment, which were found to be

increasing, is looked at with a view to impact on iron and steel demand and the nature

of its trade. The effects of China being a member of the World Trade Organisation, the

Beijing Olympics 2008, Shanghai World Expo and further trade reform together with

changing approaches to trade are discussed. The research discovered mid to longer-

term inherent risks and exposures for both China and international suppliers or

investors. With this in mind, steel industry, trade development and structural

weaknesses associated with exchange rate policy, integrity of the financial system in

12

relation to debt and reform generated unemployment giving rise to social tensions are

highlighted.

Chapter 6 outlines and discusses the findings of this research project and assesses

whether the decision to build an iron and steel industry, which supported

industrialisation as a basis for modernisation and economic development, was a good

choice. The work looks at the results of increased exposure to international markets and

resulting trade, whether they have improved the living standards of the Chinese,

whether the steel industry will continue to play as significant role in the future as the

economy develops and how the nature of demand, factors of production and

comparative advantage may change.

Chapter 7 summarises the findings and key issues that are relevant to China,

Australia and other countries. Conclusions, recommendations and further research

directions are also presented.

13

2 Overview of the Global Iron and Steel Industry

To help understand China’s relative ranking and position in the global iron and steel

industry both now and in the past, this Chapter presents an overview of the industry. It

gives an outline of the key elements and measurements that enable assessment of the

steel industry’s economic contribution.

Throughout this and following chapters, a great deal of reference is made to crude steel

making, manufacturing processes and product types. To help understand the

terminology and measures that are referred to in this thesis, the diagram on Figure 2.1

has been developed. It presents the key elements of total crude steel production. A

breakdown of the key elements of the crude steel making processes is shown in brown

and the key elements of steel product processes are shown in blue.

Figure 2.1: Crude Steel Production Breakdown

Abvn: HR: Hot rolled Coil (steel strip); CR: Cold Rolled Coil; HDG: Hot Dipped Galvanised

Stock

Rebar Merchant Bar Sections

WireRod

Billets & Blooms Slabs

Longs Sheet/Flat

Plate

HR Coil

HDG

CR Coil

Total Crude Steel Production

Oxy Blown Converter Electric Arc Furnace Other

Steel Products

Crude Steel Ingots Continuously Cast Steel Liquid Steel for casting

Open Hearth Furnace

Scrap

Tubes & Fittings Other Products

Rail Track Scrap

Abvn: HR: Hot rolled Coil (steel strip); CR: Cold Rolled Coil; HDG: Hot Dipped Galvanised

Stock

Rebar Merchant Bar Sections

WireRod

Billets & Blooms Slabs

Longs Sheet/Flat

Plate

HR Coil

HDG

CR Coil

Total Crude Steel Production

Oxy Blown Converter Electric Arc Furnace Other

Steel Products

Crude Steel Ingots Continuously Cast Steel Liquid Steel for casting

Open Hearth Furnace

Scrap

Tubes & Fittings Other Products

Rail Track Scrap

14

2.1 Steel Industry - Driver of the Economy

A key principle in growth theory is the important roles played by industry and

manufacturing in that they are considered as being “Engines of Growth” (Kaldor 1996

cited in Bramall 2000). The global steel industry developed from the heavily

industrialised Europe and USA. These regions had industries in place prior to the

Second World War between 1939 and 1945. It was not until after the war that

production capacity started to rapidly increase (refer to Chart 2.1). However, during the

latter half of the 20th century, developments in other manufacturing sectors introduced

substitutes (for example, plastics and aluminium) and these have contributed to lower

demand and lessened the steel industry’s dominance in the global economy. The

industry has been faced with oversupply problems for most of the second half of the

20th century. Threats to oil supplies and environmental concerns also contributed to

many western countries reducing investment in the industry.

However, steel is a material that is difficult to do without and less developed countries

demand more as they embark on development programmes as occurred in the last

quarter of the 20th century when Asian countries increased their appetite for steel. So as

western countries downgraded supply side economics, Asian economies (first Japan,

then Korea and China) with their lower input factor costs, moved in and captured steel

production market share. This was done during periods of significant economic

development for these countries that in effect used the steel industry as a model to

utilise resources, reduce reliance on imports and at the same time increase their

15

industrial base and capability. Correspondingly, this growth has been positively

reflected in GDP statistics.2

The iron and steel industry is very resource hungry and factors of production

incorporate a large proportion of a country’s energy, minerals and labour. In relation to

economic significance, the World Trade Organisation (2002) reports that global trade in

the iron and steel industry in 2001 was US$130 billion. Allowing for related industries

Marsh (2003a, p.i) considers the iron and steel industry to be worth over US$300 billion

annually to the global economy.

Chart 2.1 shows world steel production which following World War 2 was driven by

large demand growth in the industrialised countries and regions of Europe and North

America. The most rapid growth phase was from the late 1940s through late 1970s

when production increased from 111.6 million tonnes in 1946 to 746.4 million tonnes in

1979. From this time, as traditional industrial nations like USA and the European

countries reduced demand growth, Asian economies started their development, which

maintained increased demand.

2 Both Japan and Korea subsequently had economic issues that arose from weaknesses in their economic structures.

16

Chart 2.1: World Steel Production, 1900-2002

Data sources: From 1990 to 2001(inclusive) - Steel Statistical Yearbooks

For 2002 - CRU Monitor Bulk Ferroalloys (March 2003)

The major challenges affecting the industry are slowing down of world economic

growth, excess steelmaking capacity, input factor logistics/economics, oil price and US

dollar value. The slow down in world economic growth at a time when many countries

added to their steel production capacity has contributed to global excess steelmaking

capacity. This excess capacity is causing older, less efficient plants (like many in the

USA) to close, this in turn is causing domestic political pressures in the USA to impose

punitive tariffs and impact world trade and prices. The oil price has a significant impact

on regional economies in that as it increases, demand and economic growth suffer. In

addition, as factor input prices increase, steel production costs increase, which lower

profit margins for the industry. These lower margins cannot be recovered in the market

place due to the excess supply of steel causing product prices to remain low. Oil

markets have been very volatile in recent years as a result of regional insecurity and

threats of terrorism. Most countries trade in US dollars, so as the dollar weakens, to

maintain local costs, sellers tend to increase prices. During 2002 and 2003, the US

0

100

200

300

400

500

600

700

800

900

1000

1900

1905

1910

1915

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

Wor

ld S

teel

Pro

duct

ion

(Mill

ion

tonn

es

2002

17

dollar has depreciated by over 20% against several currencies. It appears unlikely in the

short term that the US dollar will recover to its pre 2002 high values. The producers

who can best manage the above challenges will be the ones that will better survive in a

tough global marketplace.

To show the world steel production, Chart 2.2 shows the regional comparisons since

1989. Regional groupings are: Europe (all of Europe); former USSR3; North America

(Canada, USA, Mexico, Trinidad & Tobago, Cuba, Dominican Republic, Guatemala

and El Salvador); South America (Argentina, Brazil, Chile, Colombia, Ecuador,

Paraguay, Peru, Uruguay and Venezuela); Africa and Middle East; China; Japan; South

Korea and other Asian countries plus Oceania (Australia and New Zealand).

Chart 2.2: Regional World Steel Production, 1989 – 2002

Data source: International Iron and Steel Institute

From Chart 2.2, the reducing trend in steel production in the former USSR can be seen.

Notwithstanding industry restructuring which involved closing many inefficient plants,

0

50

100

150

200

250

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002year

Reg

iona

l Ste

el P

rodu

ctio

n (th

ousa

nd to

nnes

)

All Europe Former USSR North America

South America Africa and Middle East China

Japan Korea Asia and Oceania

18

North America still maintained a modest increase in production output. This results

from continued investment in modern steel making processes such as the lower capital-

intensive electric arc process. China’s production output grew steadily from 1989

through to 2000 from 61.59 to 127.24 million tonnes, an average annual increase of 6

million tonnes. From 2000 to the end of 2002, production output increased from 127.24

to 181.56 million tonnes, an increase of 42.7%. Since 1989, China has had the highest

growth in steel production in the world. Japan (formerly the world’s largest

steelmaking country up until1996), produced 107.91 million tonnes of steel in 1989 and

in 2002 produced 107.75 million tonnes. Its output has remained reasonably constant.

This is mainly due to the higher technical quality steels being produced there. These

groupings are shown in Chart 2.3 for 2000, 2001 and 2002.

From Chart 2.3, it can be seen that global crude steel production did not change much

from 2000 to 2001 then increased moderately in 2002. In comparison, China’s crude

steel production increased from 127.2 million tonnes in 2000 to 152.3 million tonnes in

2001 and then to 181.6 million tonnes in 2002. This represents 15%, 17.9% and 20.5%

of the world’s total production respectively. Europe has remained steady at around 206

million tonnes. China (the world’s largest steel making country) is catching up with

181.6 million tonnes and has the potential to exceed the steel production of all of

Europe within the next few years. Particularly, with oversupply resulting from excess

capacity in both Europe and North America, these regions are under pressure to

rationalise their industries by closing down older plants and ones with lower efficiency4

(in the mid to longer term, this will lead to considerably less supply in these regions).

3 Former USSR consists of: Russia, Ukraine, Kazakhstan, Byelorussia, Moldova, Latvia, Uzbekistan, Azerbaijan, Georgia, Estonia, Latvia and Lithuania.

19

China has undoubtedly become one of the top steel producers in the world. Details of

world production (supply) and world steel consumption (demand) of crude steel are

shown in Appendices 9.1.3 and 9.1.10 respectively.

4 China has been selectively purchasing redundant plant mainly from Germany and has then with the help of German expertise used this plant in expansions and upgrades to some of the older Chinese plants.

20

Chart 2.3: Regional World Steel Production 2000, 2001 & 2002

Data source: International Iron and Steel Institute (all units in million tonnes)

World steel (2000)Total 847 million tonnes

62.943.1

106.4

127.2

24.639.1 135.2

98.6

209.8

15%15%

World steel (2001)Total 849 million tonnes

204.6

100.1

119.737.4

26.8152.3

102.9

43.962.1

Europe

Former USSR

North America

South America

Africa & Middle East

China

Japan

South Korea

Other Asia & Oceania

17.9%17.9%

World steel (2002)Total 887 million tonnes

55.245.4

107.7

181.6

26.6 40.8123.9

99.9

205.6

20.5%20.5%

21

2.2 Industry Structure and Behaviour - Barriers to Entry

The iron and steel industry is very capital intensive, requires long factory construction

and upgrade times and access to low cost factor inputs (iron ore, energy and labour).

These features make it difficult for new companies to enter the industry and in effect are

natural barriers of entry. In addition, returns on investment have traditionally been low,

which also does not encourage new entrants. Many of the Chinese producers initially

had their factories close to iron ore and coal mines (to lower the major factor input

costs), but many also found that the quality of their iron ore was too low (30-35% iron

content compared with Australia at 60-63%) and environmental problems arose from

coal burning.

Due to the high costs and low returns, many of the traditional steel making factories in

the USA closed (Marsh 2003a). The United Kingdom was one of the first industrialised

nations to see its steel industry being cut back. In the 1970s, crude steel production in

the United Kingdom was 28 million tonnes (IISI 1974, p.5) compared to 2002 when

production was only 11.6 million tonnes (IISI 2002a). Closing down and rehabilitation

costs also tend to encourage older less efficient plants5 to continue production beyond

their economic lives, this adds to the oversupply situation of steel products, which

continues to maintain downward pressure on steel prices.

In 2002, the top 5 world’s leading steel countries (China, Japan, USA, Russia and South

Korea) produced 54.8% of the world’s steel output, and then when one examines the top

5 of the world’s steel makers (Arcelor, LNM Group, Nippon Steel, Posco and Baosteel),

one sees that they only produce 17.6% of total world output. This is less industry

22

concentration compared to other industries like cement, aluminium and copper where it

is more than 40% (Marsh 2003a, p2). The steel production figures show that the

potential for further consolidation in the industry is likely and necessary. Further

examination of the iron ore industry (being the principal raw material input) showed

that predominantly 3 large companies control the majority of global production

(Australia’s Rio Tinto and BHP Billiton and Brazil’s CVRD).

To restore some measure of profitability to the industry and ensure that it can be

sustained in the longer term, pressure for more consolidation through mergers and

acquisitions is mounting (Alden & Marsh 2002, p3). This is an attempt by the major

players to increase industry concentration, which will in turn tilt playing fields and

enable higher market prices. As suggested above, this trend in industry concentration is

likely to increase barriers to entry, but will also increase a move towards monopolistic

behaviour, which together with high barriers to entry will increase the returns on capital

being achieved. In addition to high capital investment costs, other factor of production

characteristics impact entrants’ willingness to enter the industry. Examples of these

follow.

2.3 Economics of the Steel Industry - Factors of Production

To understand how China has emerged from being an insignificant player in the global

steel industry to being the world’s largest producer, it is useful to consider economic

aspects of the steel industry. These relate to the principal factors of production: energy,

raw materials (iron ore being the principal input), technology, vintage of plant, location

of labour and comparative advantage.

5 Environmental impact, energy efficiency and costs per tonne are key measures impacting plant efficiency.

23

A major factor of production is operating costs. These costs consist of feedstock raw

materials (iron ore, coking coal, magnesium, nickel and other minor additives), energy,

labour, services, and interest charges. With China starting steel industry development

in its communist era of the 1950s, these production costs had been artificially low and

centrally planned economies have shown that factors of production were not efficiently

allocated. This will be discussed in more detail in Chapter 3.

Steel industry start up costs are high due to the capital required for the high costs of the

steel making plant. However, with rationalisation in both the European and North

American steel industries underway, China has been able to purchase redundant steel

plant at low costs. For example in 1998, Thyssen Krupp Stahl (TKS) sold its 1.5

million tonne per year blast furnace from its Dortmund-Horde plant to China’s Handan

Iron and Steel Works (CRU 1998, Industry developments, p.3). Then in 2001, TKS

sold the Jiangsu Shagang Group most of the 4 million tonnes per year Dortmund steel

plant. When operational, this will increase Shagang’s total steel production capacity

from 4.5 to 8.5 million tonnes per year (CRU 2002a, Industry developments, p.10). In

2002, China’s Xiyang Group purchased two flat product mills, one from ISG’s

Cleveland West operations and the other from ISG’s Sparrow Point Mill. With the

collapse of Enron, the Chongqing Iron and Steel Company purchased a cold rolling mill

previously owned by them (CRU 2003a, Industry news in brief, p.10).

Due to the lower start up costs, many modern plants are being constructed as mini steel

mills. This type of plant uses the electric arc steel production process to produce long

products (refer to Figure 2.1 which shows the other two processes, oxygen blown

24

converter and open hearth furnace and also charts later in this chapter which show

increasing use of the lower capital cost electric arc production process). A typical

breakdown of costs associated with mini steel mills is shown in Table 2.1.

Table 2.1: Comparison of Average Mini Steel Plant (long products) Costs as at 2000

Country

(averages)

Feedstock Energy Refractories Fluxes &

Alloys

Direct

labour Electrodes Other

China 63% 18% 4% 5% 1% 3% 6%

Japan,

Korea,

Taiwan

56% 23% 5% 4% 3% 3% 6%

North

America 56% 17% 6% 5% 7% 4% 5%

Data source: AME Mineral Economics Steel, 2001, pp.26-33

The above table confirms that notwithstanding China’s comparative advantage of low

labour and energy costs, feedstock costs are higher. In this regard, it is worth taking a

detailed look at one of China’s steelworks, see Table 2.2. It shows costs in US$/tonne

against the world average costs for Shanghai No.5, long products mill in 2002.

25

Table 2.2: Comparison of Selected World Average Costs with Shanghai No.5 Long

Products Mill as at 2000

Costs (US$/tonne)

Average Feedstoc

k Energy

Direct

labour

Refractories, Fluxes,

Alloys,

Electrodes & Other

Shanghai No. 5

Long Products Mill

Year 2000

120.2 36.9 2.0 35.9

World average

(from samples) 97.3 31.5 6.8 35.9

Data source: AME Mineral Economics Steel, 2001, p.A-3

China’s main feedstock raw material is iron ore. As the country’s reserves of these are

of low quality, it is cost effective to use only part of the domestic production and import

the rest. Shanghai No 5’s feedstock cost of US$120.2 per tonne is 23.5% higher than

the world average of US$97.3 per tonne and energy costs of US$36.9 per tonne are

17.1% higher than the world average value of US$31.5 per tonne. This research

identified that China’s feedstock costs are increasing (mainly as a result of the country’s

own demand) and as the country relies on energy imports, it is likely that energy costs

will continue to be higher than world average. This shows that China’s low labour cost

is giving the country a competitive advantage. As the country’s economic development

continues, labour costs are likely to increase; this suggests that in the long run, China

could lose its international competitiveness. This situation will occur sooner if its

currency appreciates in value which will make imports cheaper and exports more

expensive.

26

As stated above, the principal feedstock raw material in the steel making process is iron

ore. Details of domestic reserves, production and imports are presented in Chapter 3.

This is an area where Australia with its abundant iron ore resources and a direct reduced

iron production facility will play a major role in China’s continued development of both

its iron and steel industry and its economy. Australia’s contribution is outlined in detail

in Chapter 4. Feedstock inputs (energy and iron ore) are major risk exposures that

China faces in maintaining the steel industry’s momentum in driving the economy.

With direct labour cost of US$2 per tonne, comparative advantage in low labour cost

inputs is evident from Table 2.2. This is confirmed by the World Bank’s research on

China’s comparative advantage, which concluded that China had developed

comparative advantage in a relatively broad base of labour intensive industries (Yeats

1991). China has a large supply of labour that is willing to work for low wages in

generally poor working environments. Factories take advantage of this and to some

extent exploit workers in that safety and health in the workplace is not high on their

agendas.

Location is an important factor contributing to production costs. China’s industrial

development has been helped by the development of large production facilities located

at coastal cities. Improved infrastructure has enabled improved transport efficiency of

the commodities for export and for those required for industrial inputs. Unfortunately,

in a country as large as China, this has given rise to large disparities in regional

development and efficiencies. So in the short term, this increases the efficiency of

production, but in the longer term, will introduce social problems as state workers are

27

laid off and locals cannot get work. This leads to an important finding and is discussed

in more detail in Chapter 5.

Important features of the productive efficiency of steel producing plants are age,

technical and commercial ability. Newer and higher technical level steel making

facilities require lower maintenance and operate using lower energy consumption.

Environmental pollution is also lower. How well the factories manage the supply -

demand balance, negotiate raw material supply contracts and markets their products

impacts input/output efficiency. In relation to sustainability, China has recently started

to pay more attention to improving environmental externalities. The China Economic

Information Service reported (CEIS 0401 2003, art.043) that Shougang steelworks will

reduce production capacity by 2 million tonnes by closing down one of their converters

to reduce pollution. A new production facility is being built in Hebei, closer to

Shougang’s mining operations. The plant is expected to be operational by mid 2004.

According to Zhu Jimin, Board Chairman of Shougang (CEIS 0128 2003, art.040) “no

out-of-date production techniques and equipment formerly used by Shougang would be

transferred to the new base. Instead new and environmentally friendly technology and

equipment would be installed to build a modern steel plant”. In the past few years,

Shougang is reported to have spent 241 million yuan (US$29 million) in financing 33

projects relating to environmental protection (CEIS 0117 2003). It is expected that

many other steel facilities will close down as the Central Government continues in its

endeavours to reduce pollution.

28

2.3.1 Iron Ore - Principal Input Material to the Steel Industry

Chart 2.4: World Production of Iron Ore, 1948 - 2002

Data sources: American Iron Ore Association (1996), International Iron and Steel Institute

AME Mineral Economics, January 2003 (for 2002 data only)

Iron ore is the principal raw material input required in the steel making process. In

many countries, the industry is considered a labour intensive factor input. In relation to

China, it is a resource that was traditionally sourced domestically, but now increasingly

relying on imports due to cost effectiveness of using higher quality material than what is

available domestically. The growth in world iron ore production since 1948 is shown in

Chart 2.4 and is directly related to steel production, which in turn is determined by

global demand for steel products. Within 50 years, we have seen production increase

from under 200 to just over 1,000 million tonnes (annual average 16 million tonnes).

Most of the growth occurred between 1950 and early 1970s – from just over 200 to

approx 900 million tonnes (annual average 35 million tonnes). Growth slowed after

mid 1970s, not starting its modest recovery (in relative terms) until early 1980s when

China’s demand increased. The Asian economic crisis in the early 1990s stalled the

growth rate for a few years.

0

200

400

600

800

1000

120019

48

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Iron

Ore

Pro

duct

ion

(milli

on to

nnes

)

29

China has taken advantage of the key factors of production to develop its steel industry.

Iron ore and coal (coking and energy) have been relatively low cost; prices for these key

inputs are increasing as a result of the country’s high demand. The country is

maintaining its comparative advantage through its low cost labour. This is under threat

as labour costs increase with increasing economic development. Increasing demand and

in turn increased costs of steel will impact the country’s continued economic

development. This finding will be discussed in more detail in Chapter 6.

2.4 Leading Steel Producing Countries

Table 2.3 shows the top ten steel producing countries (ranked on 2002 output) and the

corresponding production output from 1998 to 2002.

Table 2.3 Steel Output of the Top Ten Producing Countries (million tonnes), 1998 - 2002

Countries 1998 1999 2000 2001 2002

China 114.1 123.3 126.3 150.9 181.6

Japan 93.5 94.2 106.4 102.9 107.7

USA 97.3 96.1 100.7 90.1 92.4

Russia 41.8 49.8 57.6 57.5 58.6

Korea 39.9 41.0 43.1 43.9 45.4

Germany 44.0 42.1 46.4 44.8 45.0

Ukraine 23.5 26.8 31.3 33.1 34.1

Brazil 25.8 25.0 27.8 26.8 29.6

India 23.5 24.3 26.9 27.3 28.8

Italy 25.8 25.0 26.5 26.5 26

Data sources: International Iron and Steel Institute, Iron & Steel Monthly report December

1999 for 1999 & 1998; Iron & Steel Monthly report December 2001 for 2000; Iron

& Steel Monthly report December 2002 for 2001 and 2002

30

Since 1998, not much change has occurred with the main exception being China

increasing production by the highest margin and Korea edging ahead of Germany in

2002. Rankings since 1991 are in Appendix 9.1.13.

Chart 2.5 shows the 6 leading steel producing countries since 1972. These are China,

Japan, Germany, USA, Russia and South Korea. The chart shows that only China and

Korea are experiencing growth, which is occurring at the expense of the others.

Between 1972 and 2002, China increased from 23.4 to 181.5 million tonnes, Korea

from 2 to 45.4 million tonnes and the USA, actually decreased from 120.9 to 92.4

million tonnes. This shows the shift in steel production from the west to Asia.

Although Japan is losing market share to China, it still is a significant producing

country.

Chart 2.5: Six Leading Producer Countries' Steel Production, 1972 - 2002

Data sources: International Iron and Steel Institute up to 2000 and Russia 2001

CRU Monitor Bulk Ferroalloys, March 2003, p.2 for 2001 and 2002

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

year

Maj

or P

rodu

cers

' Ste

el P

rodu

ctio

n S

ince

197

2(th

ousa

nd to

nnes

)

PR China USA

Japan Russia

Germany Korea

31

2.5 Steel Production Processes for the Top Six Producing Countries

A useful way to quantify a country’s efficiency and technical development is to

examine the change in steel production from the traditional steel making processes.

Figure 2.1 outlined the steel production processes and resulting products. The main

steel making processes are oxygen blown converter, electric arc furnace and the open-

hearth furnace. The final casting methods used can be very energy and labour intensive,

the most technically advanced approach is to use the continuous casting process. The

continuous casting process uses less energy (it processes the material directly before it

cools thus eliminating the need for additional heat energy). Many producers have been

upgrading plants to use this method.

Chart 2.6 shows the development in continuously cast steel for the 6 leading producer

countries. A higher level of usage of continuous casting is a key industry performance

measure. Charts 2.7, 2.8 and 2.9 illustrate the changes in the major crude steel

production processes (this is the stage before shaping the steel into billets, blooms or

slabs either by continuous casting or in separate stages) for the 6 leading producing

countries since 1972.

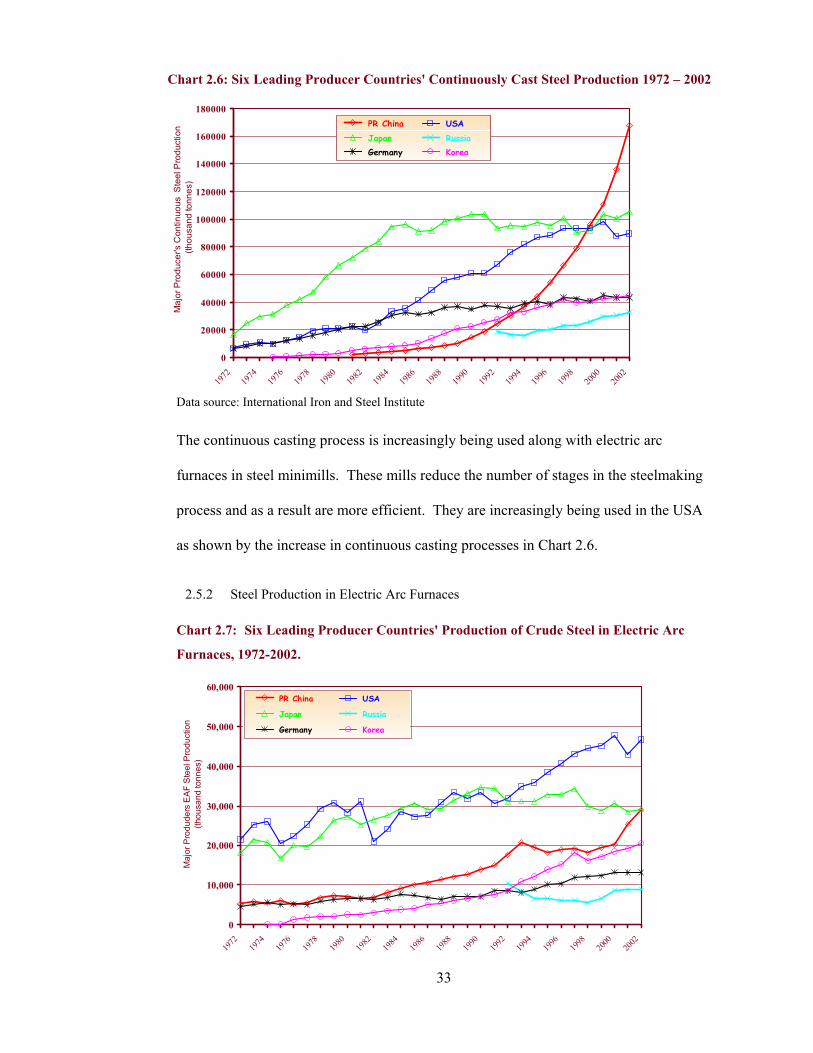

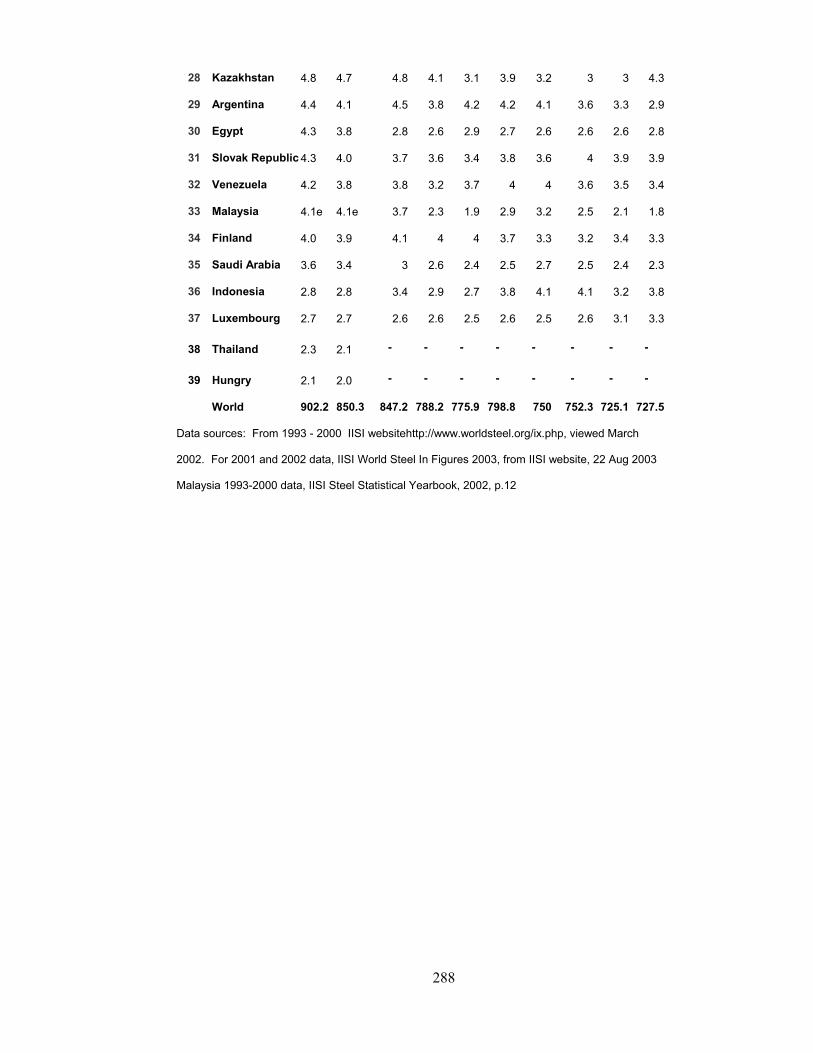

2.5.1 Continuous Cast Steel Making Process Chart 2.6 shows that between 1982 and 2002, China’s continuous cast steel production

has increased from just under 3 to 168 million tonnes; Korea from just over 6 to just

under 45 million tonnes. Between 1982 and 2002, the USA increased continuous cast

32

steel production from 19.6 to 89.5 million tonnes dropping to 87.3 million tonnes in

2001 as the industry faced overcapacity in steel production.

33

Chart 2.6: Six Leading Producer Countries' Continuously Cast Steel Production 1972 – 2002 Data source: International Iron and Steel Institute

The continuous casting process is increasingly being used along with electric arc

furnaces in steel minimills. These mills reduce the number of stages in the steelmaking

process and as a result are more efficient. They are increasingly being used in the USA

as shown by the increase in continuous casting processes in Chart 2.6.

2.5.2 Steel Production in Electric Arc Furnaces

Chart 2.7: Six Leading Producer Countries' Production of Crude Steel in Electric Arc

Furnaces, 1972-2002.

Source: International Iron and Steel Institute

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Maj

or P

rodu

cer's

Con

tinuo

us S

teel

Pro

duct

ion

(tho

usan

d to

nnes

)

PR China USA Japan Russia Germany Korea

0

10,000

20,000

30,000

40,000

50,000

60,000

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Maj

or P

rodu

ders

EA

F S

teel

Pro

duct

ion

(thou

sand

tonn

es)

PR China USA

Japan Russia

Germany Korea

34

Data source: International Iron and Steel Institute

Since it was very effective at reducing the ingress of impurities into the steelmaking

process, the electric arc furnace was originally designed for making high grade alloy

steels. It was also found to be very effective at removing sulphur from the steelmaking

process when scrap was being used and for this reason, electric arc furnace steelmaking

plant became more attractive from an investment perspective in that lower capital is

required and the process is simpler. Chart 2.7 shows the growth in the electric arc

furnace process. Between 1972 and 2002, Japan’s growth has been from 18 to 28.2

million tonnes, the USA from 21.5 to 46.7 million tonnes and China from 5.2 to 29

million tonnes. Korea has quietly been increasing from 0 in 1974 to 20.5 million tonnes

in 2002. The electric arc furnace can use direct reduced iron (DRI) products and scrap

metal directly. This type of plant is very suitable for minimills where they are more

suited to rolled rather than flat products. It is however heavily reliant on the cost of

electrical power.

35

2.5.3 Production of Steel in Oxygen Blown Converters

Chart 2.8: Six Leading Producer Countries' Production of Crude Steel in Oxygen Blown

Converters, 1972 - 2002

Data source: International Iron and Steel Institute

Chart 2.8 shows the production of steel in oxygen blown converters. Oxygen blown

converters include blast furnace steel making processes which have a jet of pure oxygen

injected onto the surface of the molten iron. These furnaces prefer lump product or

agglomerated (sinter) products being fed into the furnace. Unfortunately, they have

high initial capital outlays. The chart shows that only China and Korea invested in

growth of the use of oxygen blown converters. The USA closed down plants of this

type in the early 1980s in an effort to reduce the country’s oversupply capacity while

endeavouring to increase its more cost effective electric arc furnace steel producing

plant together with continuous casting processes in minimills.

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Maj

or P

rodu

cers

BO

F S

teel

Pro

duct

ion

. (t

hous

and

tonn

es)

PR China USA

Japan Russia

Germany Korea

36

2.5.4 Steel Production in Open Hearth Furnaces Chart 2.9 shows the traditional inefficient open-hearth furnace. The open-hearth

furnace is the oldest method and was primarily used in the early days of steel making.

As can be seen, its use is diminishing as older plants are closed down.

Chart 2.9: Six Leading Producer Countries' Production of Crude Steel in Open Hearth

Furnaces, 1972 – 2002.

Data source: International Iron and Steel Institute

Following the forming of the People’s Republic, the open-hearth furnace was China’s

principal steel making process. It continued growing until the mid 1990s when as part

of the country’s steel industry reform, the central government closed many steel

producing plants that used this type of equipment. The chart shows that long before

China’s reform, other leading countries such as Japan, Germany and USA had been

moving away from the open-hearth steel making process replacing it with more efficient

alternatives.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

Ste

el P

rodu

ctio

n in

Ope

n H

earth

Fur

nace

s (th

ousa

nd to

nnes

)

PR China USA

Japan Russia

Germany Korea

37

2.5.5 Summary of Global Supply

Regionally, notwithstanding a potential increase in Russian crude steel production, the

trend for the European steel production is moderately downwards, this being somewhat

dependent on German industry consolidation. Asia’s competitive advantage through

factor of production inputs of lower labour costs and plant locations (principally

supplying domestic markets) should result in Asia’s upward trend continuing. This

upward trend will be underpinned and sustained by China, Korea and India’s supply

growth. North America’s long-term trend is upwards. This has the potential to

significantly level off and may even trend downwards as older plants (which are

continuing beyond their economic lives) close down and the industry continues to both

restructure and consolidate. However, it is not all negative, as the North American steel

industry consolidates and increases its use of higher level of technical processes, its

operating efficiencies will increase. The increasing use of lower capital intensive and

mini steel mills using electric arc furnaces and continuous casting steel making

processes will improve the competitive position of the its steel industry.

2.6 Steel Demand

The previous sections outlined supply characteristics, this section outlines demand

characteristics. The International Institute of Steel’s standard methodology (IISI 2002b,