Embed Size (px)

Citation preview

Role of Deposit Insurance in Bank Resolution Framework – Lessons from the Financial Crisis

Session III – Lessons from Financial Crisis for Bank Resolution: US and European Experience

Jerzy Pruski – President of the Bank Guarantee Fund

Jodhpur, INDIA, 14th November 2011

Jodhpur 13-16th November 2011 22

Market experience regarding resolution

Jodhpur 13-16th November 2011 3

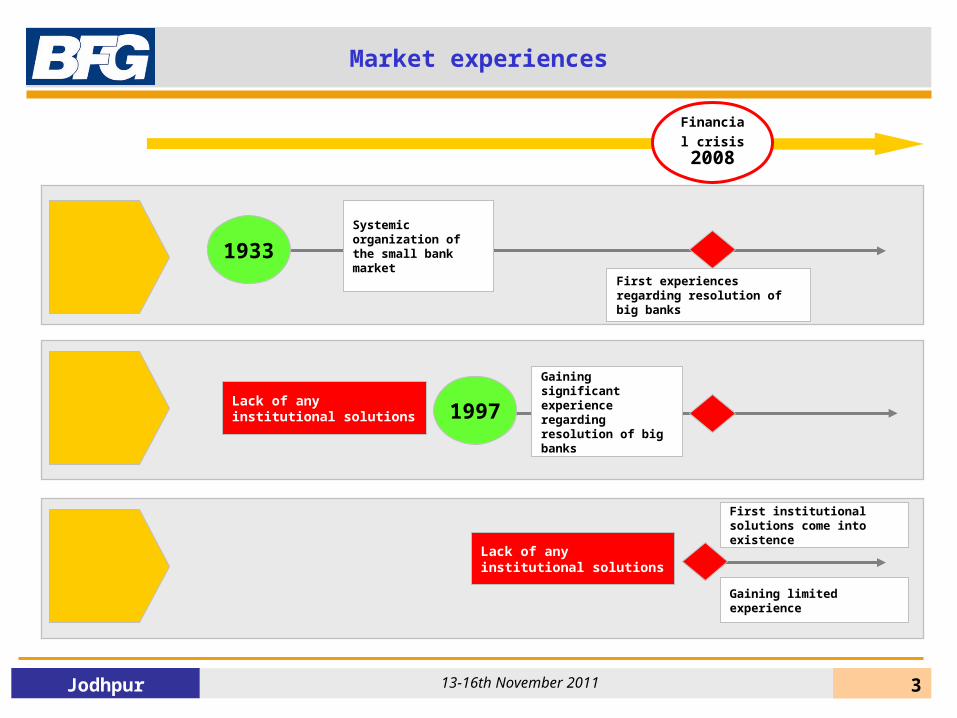

USA

Europe

3

Market experiences

1933Systemic organization of the small bank market

First experiences regarding resolution of big banks

Financial

crisis 2008

Lack of any institutional solutions

First institutional solutions come into existence

Gaining limited experience

Asia 1997Lack of any institutional solutions

Gaining significant experience regarding resolution of big banks

Jodhpur 13-16th November 2011 4

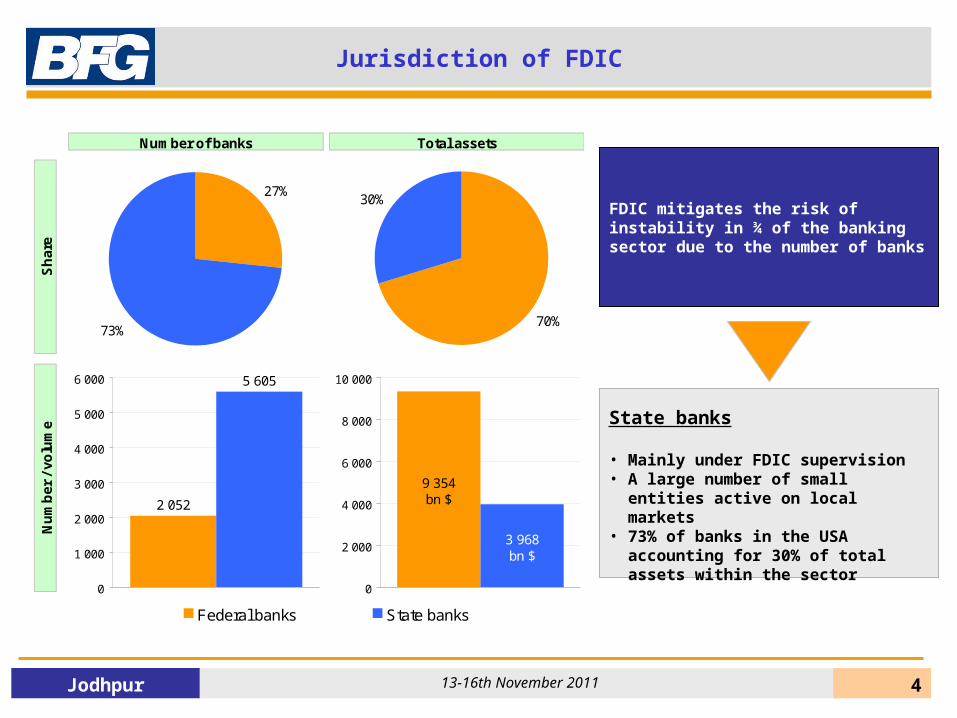

Jurisdiction of FDIC

State banks

• Mainly under FDIC supervision• A large number of small entities active

on local markets• 73% of banks in the USA accounting

for 30% of total assets within the sector

FDIC mitigates the risk of instability in ¾ of the banking sector due to the number of banks

Number of banks Total assets

Sh

are

Nu

mb

er /

volu

me

27%

73%70%

30%

Federal banks State banks

2 052

5 605

0

1 000

2 000

3 000

4 000

5 000

6 000

9 354 bn $

3 968 bn $

0

2 000

4 000

6 000

8 000

10 000

Jodhpur 13-16th November 2011 5

150,8

70,3

62,5

57,7

38,9

32,3

30,9

29,9

29,5

22,4

0 20 40 60 80 100 120 140 160

Suma bilansowa w mld $

4 705 banków

...

1 631,6

1 482,3

1 154,3

1 102,3

302,3

256,6

196,7

181,9

181,1

168,7

0 200 400 600 800 1 000 1 200 1 400 1 600 1 800

Suma bilansowa w mld $

... 2 932 banki

0,5%

0,2%

5,0%

10,0%

2,0%

2 932 banks

Total assets in bn $

5

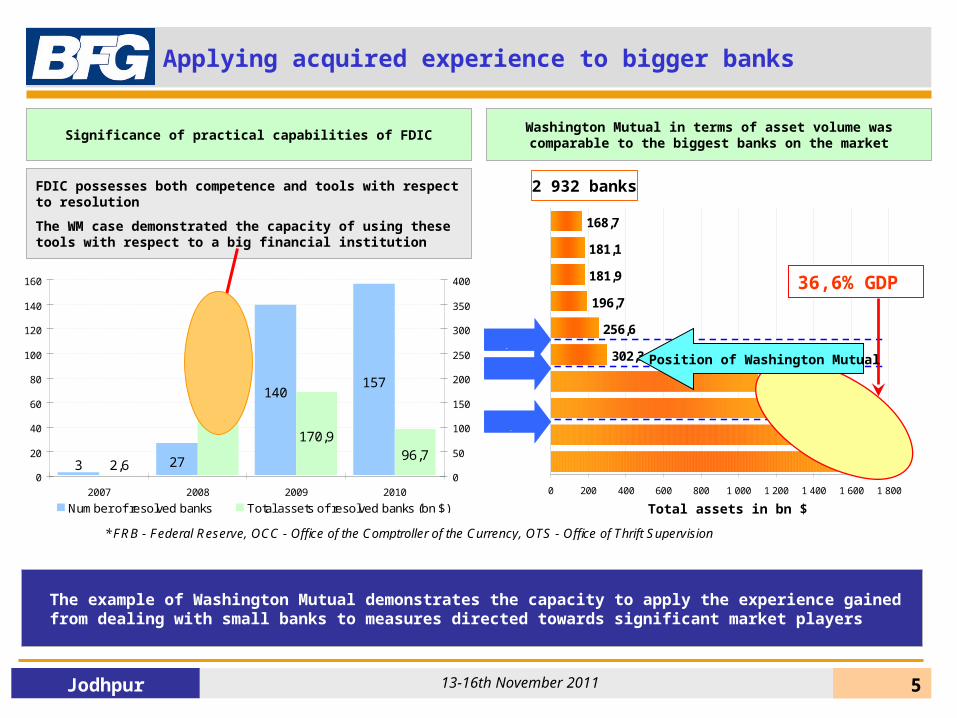

Applying acquired experience to bigger banks

5

* FRB - Federal Reserve, OCC - Office of the Comptroller of the Currency, OTS - Office of Thrift Supervision

36,6% GDP

1,0% PKB USA

Największe banki stanowe(pod nadzorem FDIC)

Washington Mutual in terms of asset volume was comparable to the biggest banks on the market

The example of Washington Mutual demonstrates the capacity to apply the experience gained from dealing with small banks to measures directed towards significant market players

Resolution średnie aktywa 0,9 mld $

FDIC possesses both competence and tools with respect to resolution

The WM case demonstrated the capacity of using these tools with respect to a big financial institution

Significance of practical capabilities of FDIC

3 27

140157

341,6

170,996,7

2,60

20

40

60

80

100

120

140

160

2007 2008 2009 2010

0

50

100

150

200

250

300

350

400

Number of resolved banks Total assets of resolved banks (bn $)

Position of Washington Mutual

Jodhpur 13-16th November 2011 66

Risks connected with the structure of the banking sectorEuropean examples

Jodhpur 13-16th November 2011 7

Belgium

France

Austria

Estonia

Slovakia

SloveniaBulgaria

Malta

Latvia

RomaniaCzech Rep.

Greece

Lithuania

Portugal

Denmark

Sweden

Hungary

UK

Netherlands

Spain

Finland

Ireland

Poland

Italy

Germany

0

5

10

15

20

25

30

35

0 10 000 20 000 30 000 40 000 50 000

GDP per capita (EUR)

Luxem. (28,4; 82 100)

outside the scale

outside the scale

Cyprus (72,7; 21 700)

Number of banks per 10 bn EUR of

GDP

Belgium

Cyprus

France

Austria

Estonia Slovakia Slovenia

BulgariaMalta

Latvia

Romania Czech Rep.

Greece

Lithuania

Portugal DenmarkSweden

HungaryUK

NetherlandsSpain

Finland

Ireland

Poland Italy

0

100

200

300

400

500

600

700

800

900

1000

0 10 000 20 000 30 000 40 000 50 000

GDP per capita (EUR)

Number of banks

Germany (1819; 30 600)

Luxem.(118; 82 100)

outside the scale

outside the scale

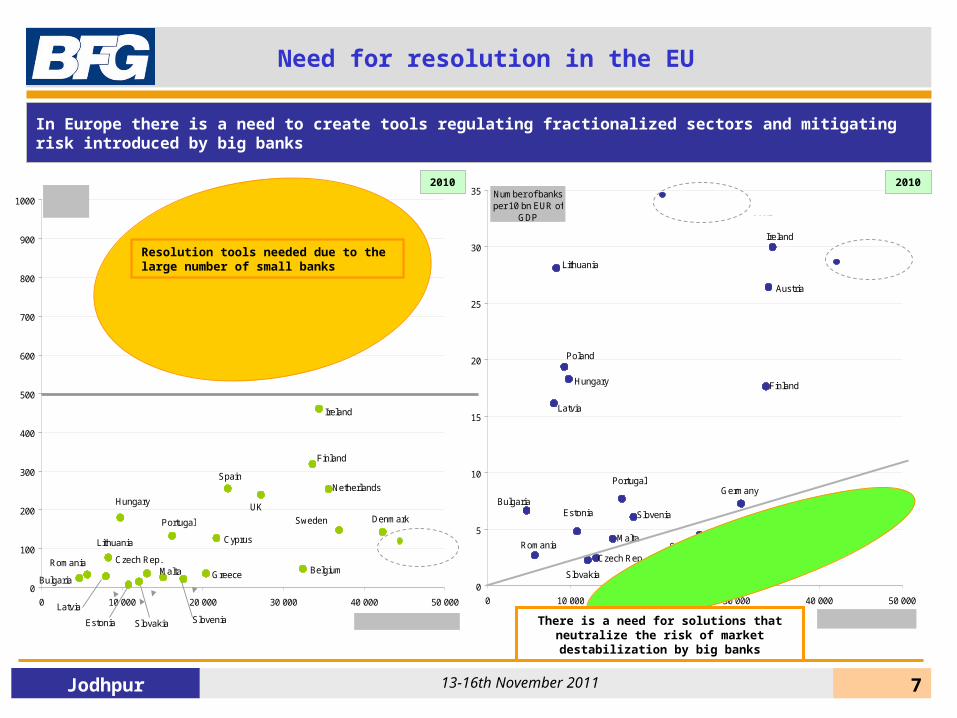

Need for resolution in the EU

In Europe there is a need to create tools regulating fractionalized sectors and mitigating risk introduced by big banks

Resolution tools needed due to the large number of small banks

There is a need for solutions that neutralize the risk of market destabilization by big banks

2010 2010

Jodhpur 13-16th November 2011 8

38

2

74

2

1 0

02

1 1

11

1 1

65

1 5

00

1 5

75

2 4

39

3 4

82

3 6

75

4 5

71

4 7

17

6 0

72

7 4

06

10

10

7

13

61

3

13

80

3

24

79

93

1 8

53

8 1

14

2 8

61

1 7

72

34

9 2 5

69

3 9

54

9 5

70

3 6

98

0

10 000

20 000

30 000

40 000

Lithuania

Pola

nd

Hungary

Latv

ia

Cypru

s

Fin

land

Austr

ia

Malta

Bulg

aria

Rom

ania

Slo

venia

Irela

nd

Slo

vakia

Port

ugal

Italy

Czech R

ep.

Germ

any

Esto

nia

Denm

ark

Luxem

.

Sw

eden

Fra

nce

Neth

erlands

Gre

ece

Spain

Belg

ium

UK

15 22 24 26 29 33 36 48

127

133

180 23

925

425

5

635

685

697

750

1819

143

461

148

77

7 36

118

318

0

500

1 000

1 500

2 000

Est

onia

Slo

vaki

a

Slo

veni

a

Bul

garia

Mal

ta

Latv

ia

Rom

ania

Cze

ch R

ep.

Gre

ece

Bel

gium

Lith

uani

a

Luxe

m.

Cyp

rus

Por

tuga

l

Den

mar

k

Sw

eden

Hun

gary UK

Net

herla

nds

Spa

in

Fin

land

Irel

and

Fra

nce

Pol

and

Ital

y

Aus

tria

Ger

man

y

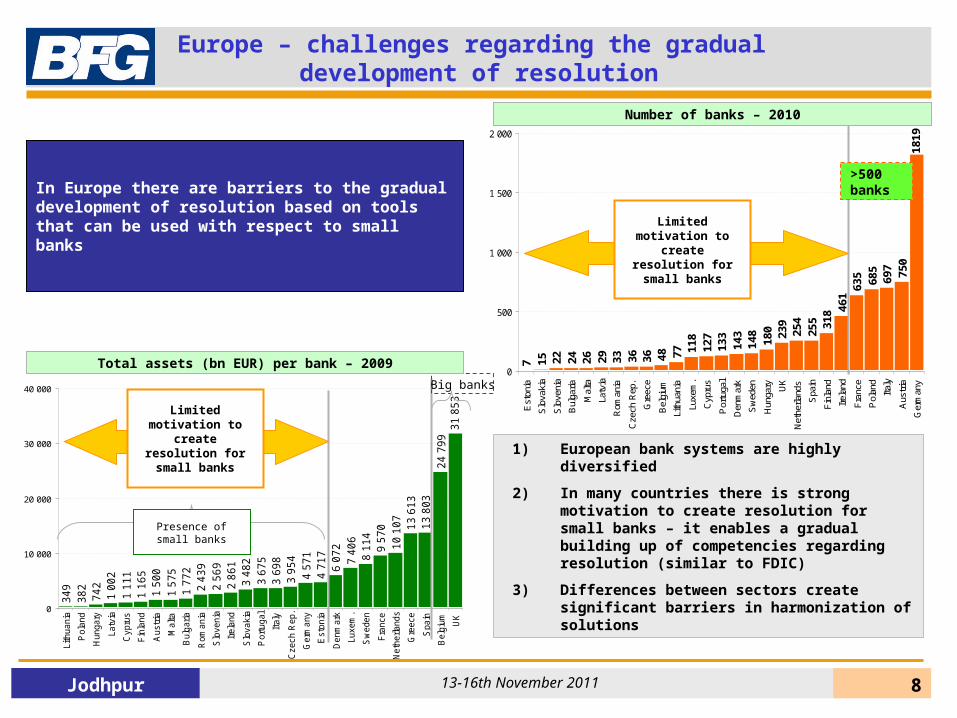

Europe – challenges regarding the gradual development of resolution

>500 banks

1) European bank systems are highly diversified

2) In many countries there is strong motivation to create resolution for small banks – it enables a gradual building up of competencies regarding resolution (similar to FDIC)

3) Differences between sectors create significant barriers in harmonization of solutions

Big banks

Number of banks – 2010

Total assets (bn EUR) per bank – 2009

Limited motivation to create resolution

for small banks

Presence of small banks

Limited motivation to create resolution

for small banks

In Europe there are barriers to the gradual development of resolution based on tools that can be used with respect to small banks

Jodhpur 13-16th November 2011 99

Cross-border problemsEuropean examples

Jodhpur 13-16th November 2011 1010

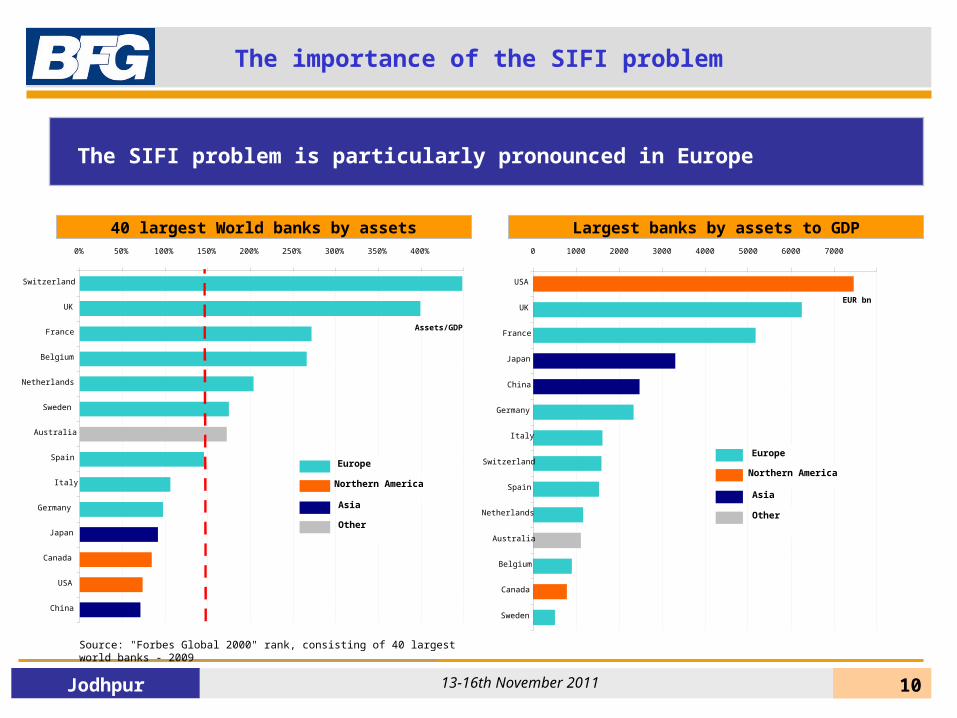

The SIFI problem is particularly pronounced in Europe

The importance of the SIFI problem

0 1000 2000 3000 4000 5000 6000 7000

USA

UK

France

Japan

China

Germany

Italy

Switzerland

Spain

Netherlands

Australia

Belgium

Canada

Sweden

EUR bn

Europe

Northern America

Asia

Other

Source: "Forbes Global 2000" rank, consisting of 40 largest world banks - 2009

0% 50% 100% 150% 200% 250% 300% 350% 400%

Switzerland

UK

France

Belgium

Netherlands

Sweden

Australia

Spain

Italy

Germany

Japan

Canada

USA

China

Assets/GDP

Europe

Northern America

Asia

Other

40 largest World banks by assets Largest banks by assets to GDP

Jodhpur 13-16th November 2011 1111

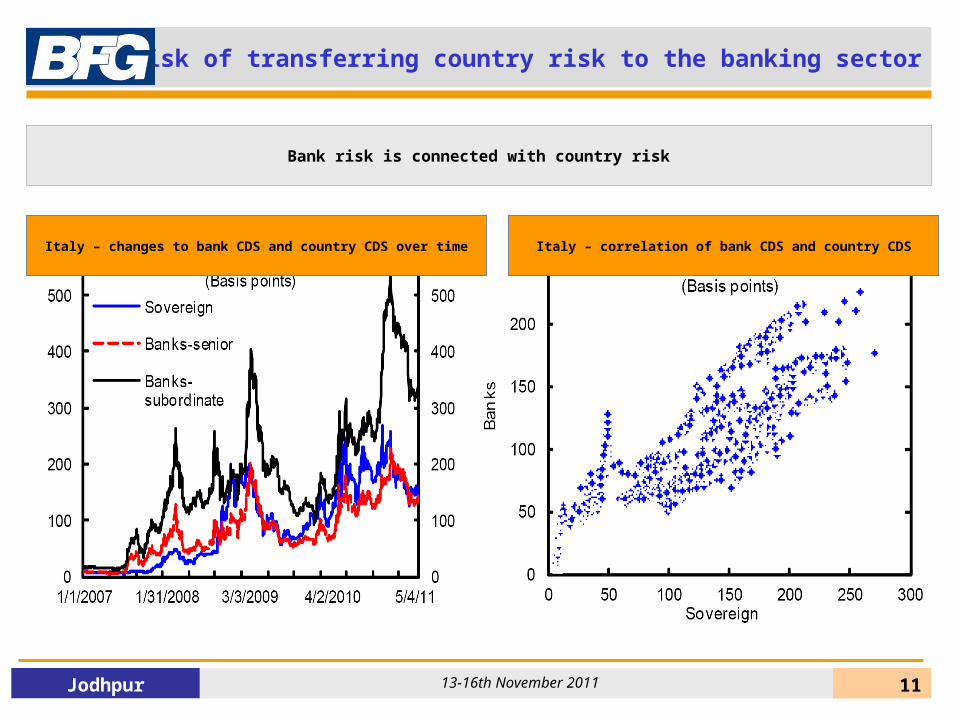

Risk of transferring country risk to the banking sector

Italy – correlation of bank CDS and country CDSItaly – changes to bank CDS and country CDS over time

Bank risk is connected with country risk

Jodhpur 13-16th November 2011 1212

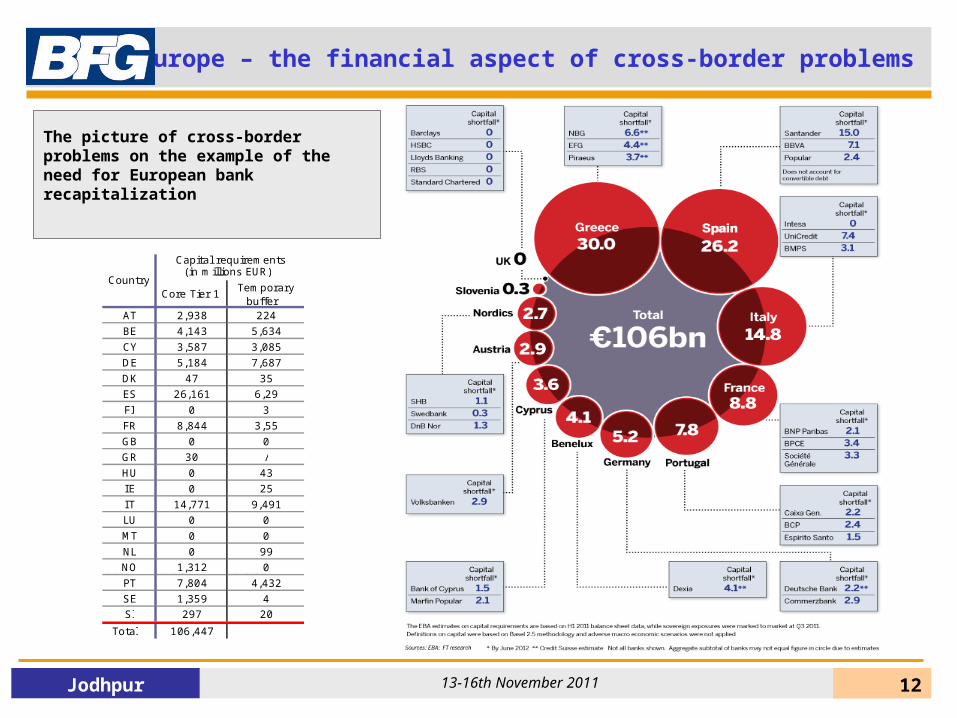

Europe – the financial aspect of cross-border problems

The picture of cross-border problems on the example of the need for European bank recapitalization

Core Tier 1 Temporary buffer

AT 2,938 224 BE 4,143 5,634 CY 3,587 3,085 DE 5,184 7,687 DK 47 35 ES 26,161 6,29 FI 0 3 FR 8,844 3,55 GB 0 0 GR 30 / HU 0 43 IE 0 25 I T 14,771 9,491 LU 0 0 MT 0 0 NL 0 99 NO 1,312 0 PT 7,804 4,432 SE 1,359 4 Sl 297 20

Total 106,447

Country Capital requirements

(in millions EUR)

Jodhpur 13-16th November 2011 1313

www.bfg.pl