Embed Size (px)

Citation preview

1

2

Roche

2012 results

January 30, 2013

3

This presentation contains certain forward-looking statements. These forward-looking statements may be identified by words such as ‘believes’, ‘expects’, ‘anticipates’, ‘projects’, ‘intends’, ‘should’, ‘seeks’, ‘estimates’, ‘future’ or similar expressions or by discussion of, among other things, strategy, goals, plans or intentions. Various factors may cause actual results to differ materially in the future from those reflected in forward-looking statements contained in this presentation, among others:1 pricing and product initiatives of competitors;2 legislative and regulatory developments and economic conditions; 3 delay or inability in obtaining regulatory approvals or bringing products to market; 4 fluctuations in currency exchange rates and general financial market conditions; 5 uncertainties in the discovery, development or marketing of new products or new uses of existing

products, including without limitation negative results of clinical trials or research projects, unexpected side-effects of pipeline or marketed products;

6 increased government pricing pressures; 7 interruptions in production; 8 loss of or inability to obtain adequate protection for intellectual property rights; 9 litigation;10 loss of key executives or other employees; and11 adverse publicity and news coverage.

Any statements regarding earnings per share growth is not a profit forecast and should not be interpreted to mean that Roche’s earnings or earnings per share for this year or any subsequent period will necessarily match or exceed the historical published earnings or earnings per share of Roche.

For marketed products discussed in this presentation, please see full prescribing information on our website – www.roche.com

All mentioned trademarks are legally protected

4

GroupSeverin SchwanChief Executive Officer

5

Solid results 2012

Outlook

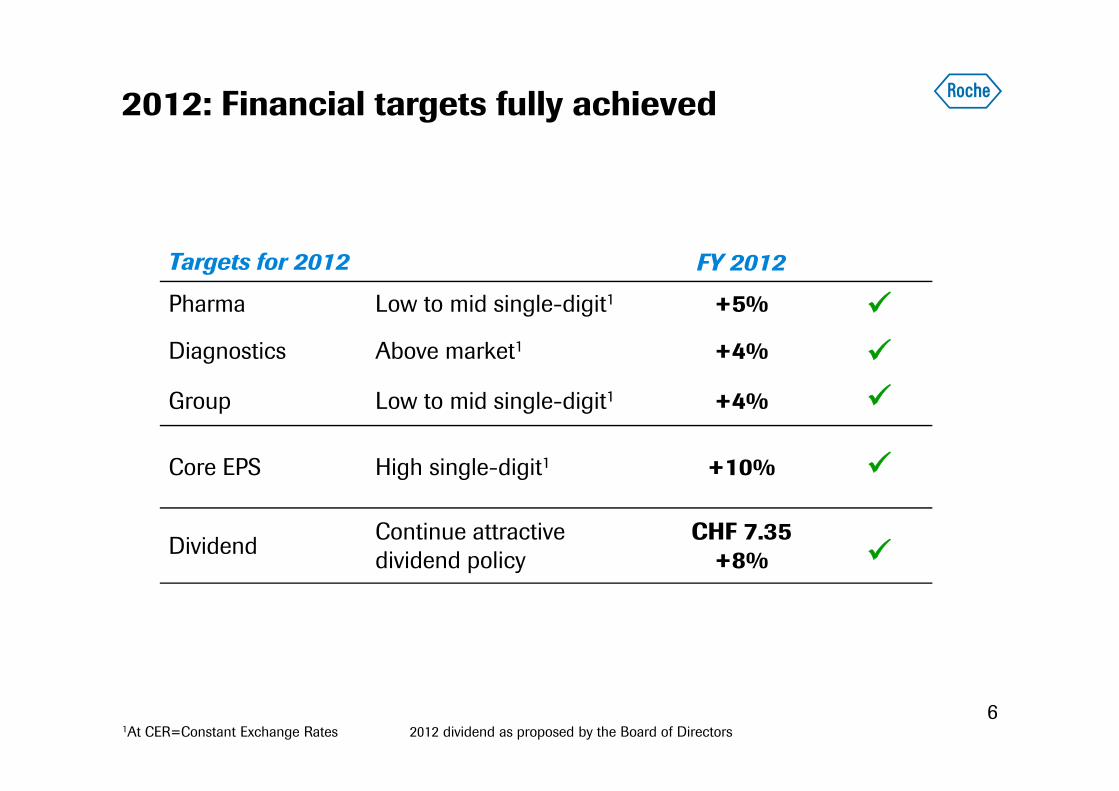

2012: Financial targets fully achieved

6

Targets for 2012 FY 2012

Pharma Low to mid single-digit1 +5%

Diagnostics Above market1 +4%

Group Low to mid single-digit1 +4%

Core EPS High single-digit1 +10%

Dividend Continue attractive dividend policy

CHF 7.35 +8%

1At CER=Constant Exchange Rates 2012 dividend as proposed by the Board of Directors

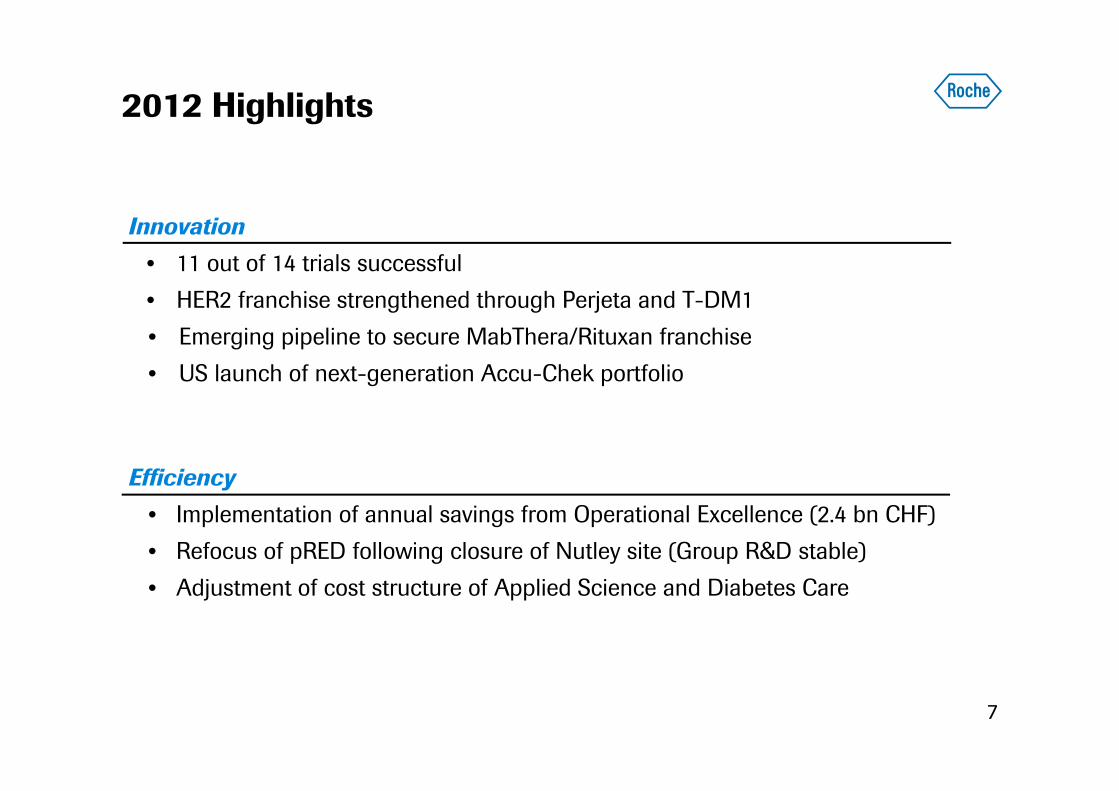

2012 Highlights

7

Efficiency• Implementation of annual savings from Operational Excellence (2.4 bn CHF) • Refocus of pRED following closure of Nutley site (Group R&D stable)• Adjustment of cost structure of Applied Science and Diabetes Care

Innovation • 11 out of 14 trials successful • HER2 franchise strengthened through Perjeta and T-DM1• Emerging pipeline to secure MabThera/Rituxan franchise• US launch of next-generation Accu-Chek portfolio

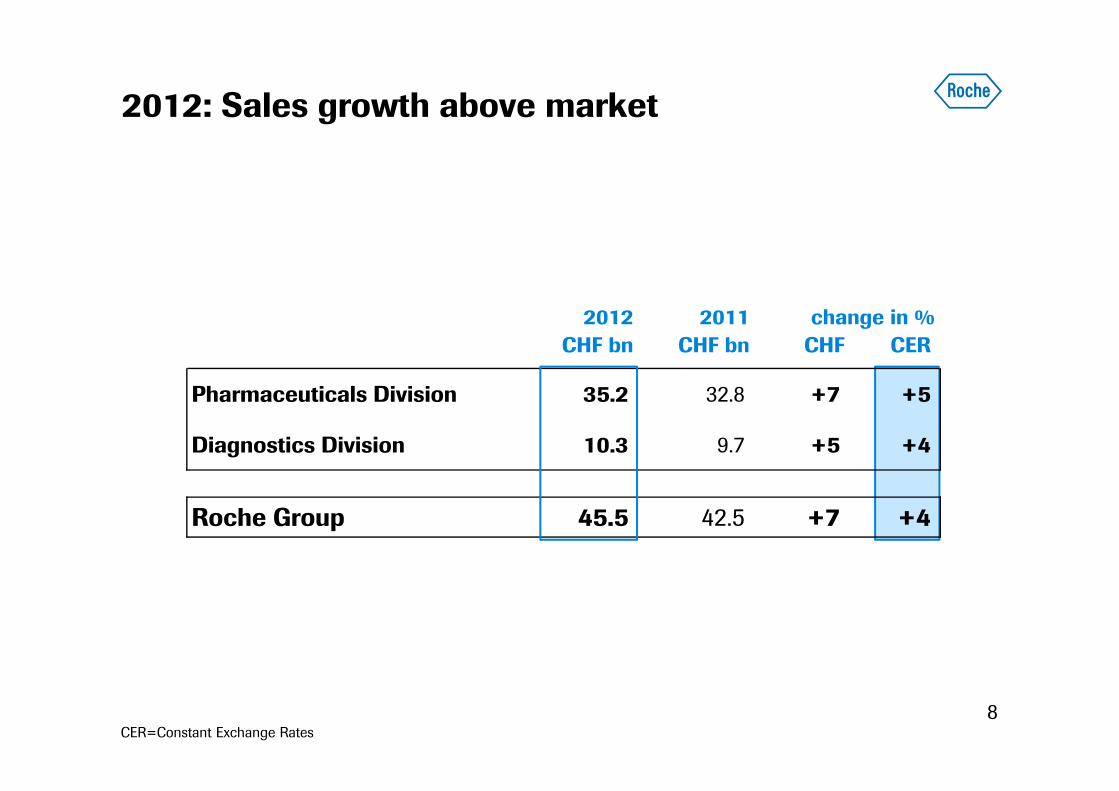

2012: Sales growth above market

8CER=Constant Exchange Rates

2012 2011 change in %CHF bn CHF bn CHF CER

Pharmaceuticals Division 35.2 32.8 +7 +5

Diagnostics Division 10.3 9.7 +5 +4

Roche Group 45.5 42.5 +7 +4

2012: +4%

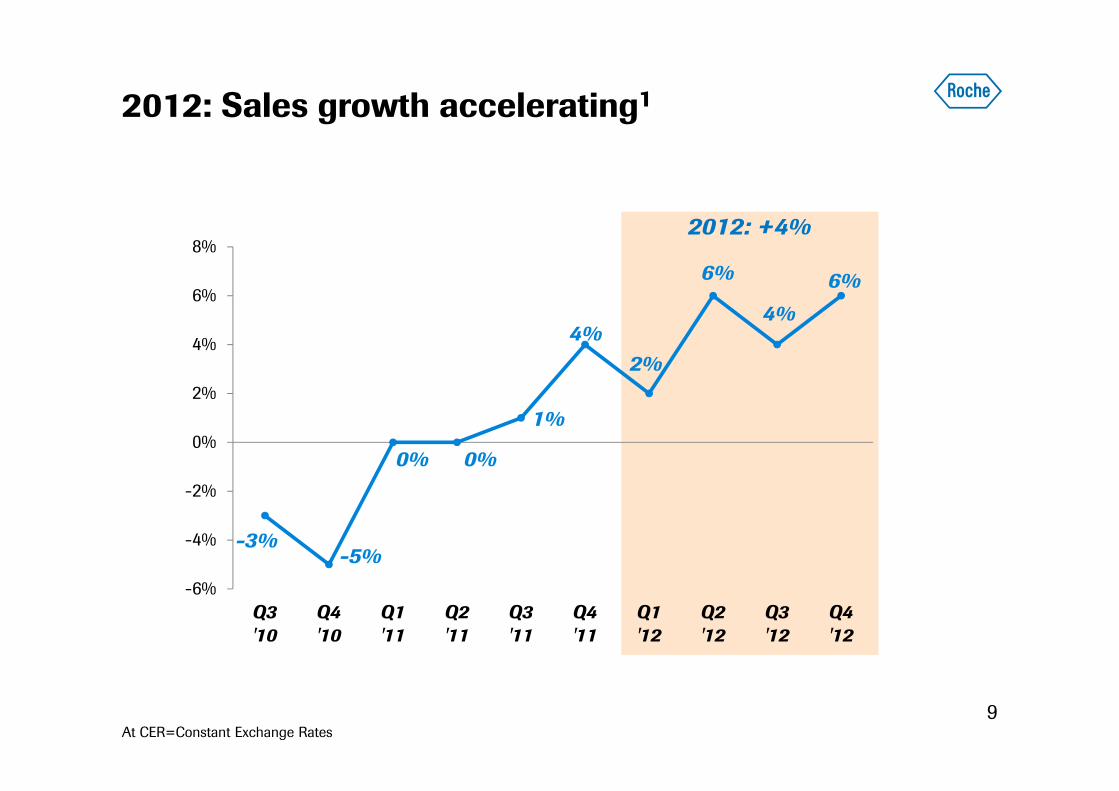

2012: Sales growth accelerating1

9At CER=Constant Exchange Rates

-3%-5%

0% 0%

1%

4%2%

6%

4%6%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Q3'10

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Q2'12

Q3'12

Q4'12

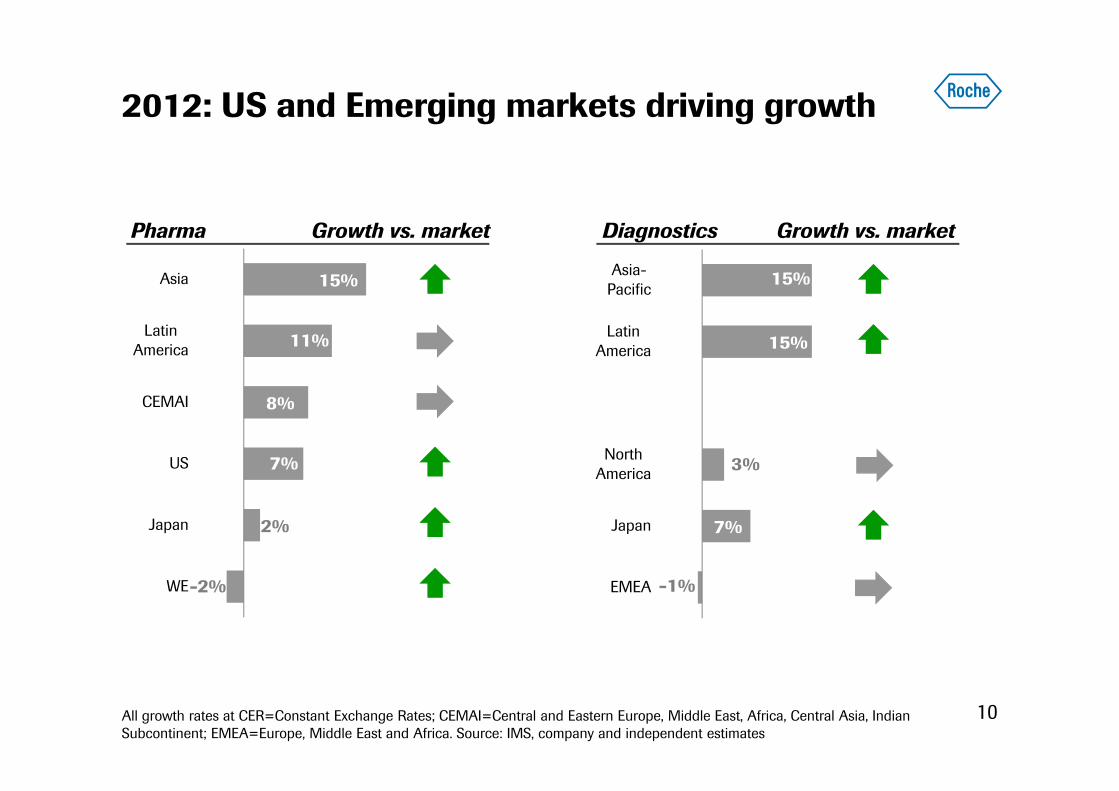

2012: US and Emerging markets driving growth

10

-2%

2%

7%

8%

11%

15%

WE

Japan

US

CEMAI

LatinAmerica

Asia

-1%

7%

3%

15%

15%

EMEA

Japan

NorthAmerica

LatinAmerica

Asia-Pacific

Pharma DiagnosticsGrowth vs. market Growth vs. market

All growth rates at CER=Constant Exchange Rates; CEMAI=Central and Eastern Europe, Middle East, Africa, Central Asia, Indian Subcontinent; EMEA=Europe, Middle East and Africa. Source: IMS, company and independent estimates

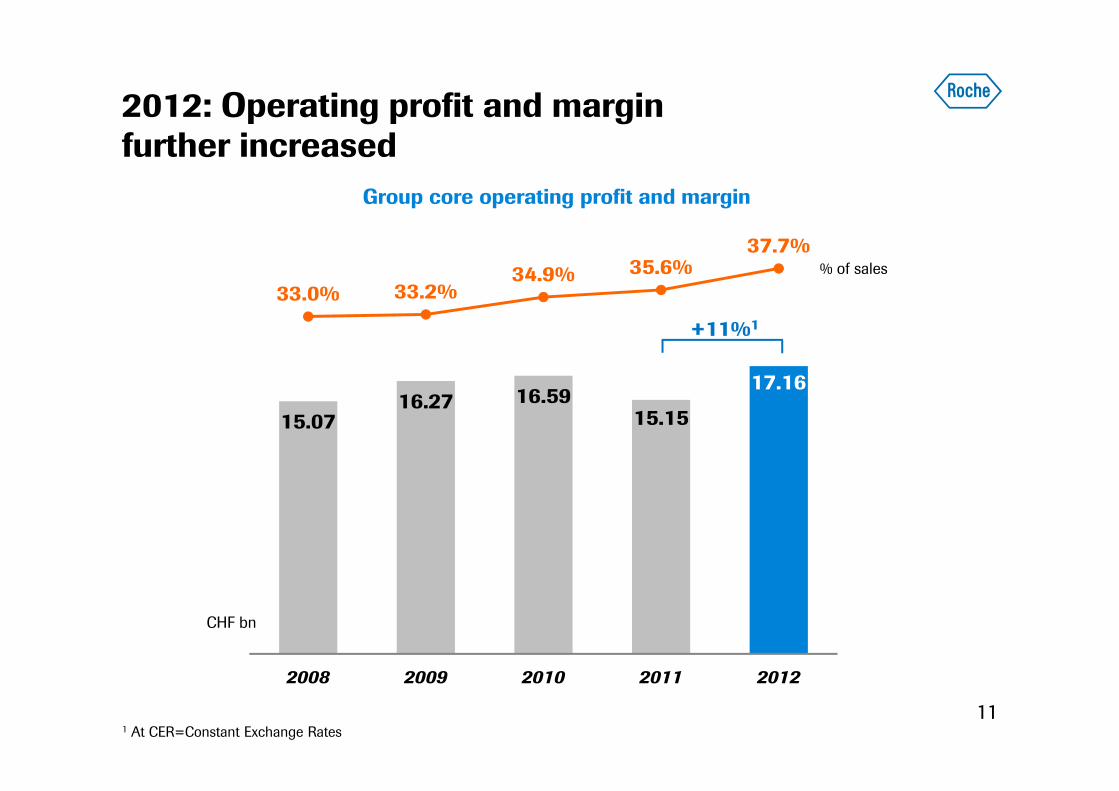

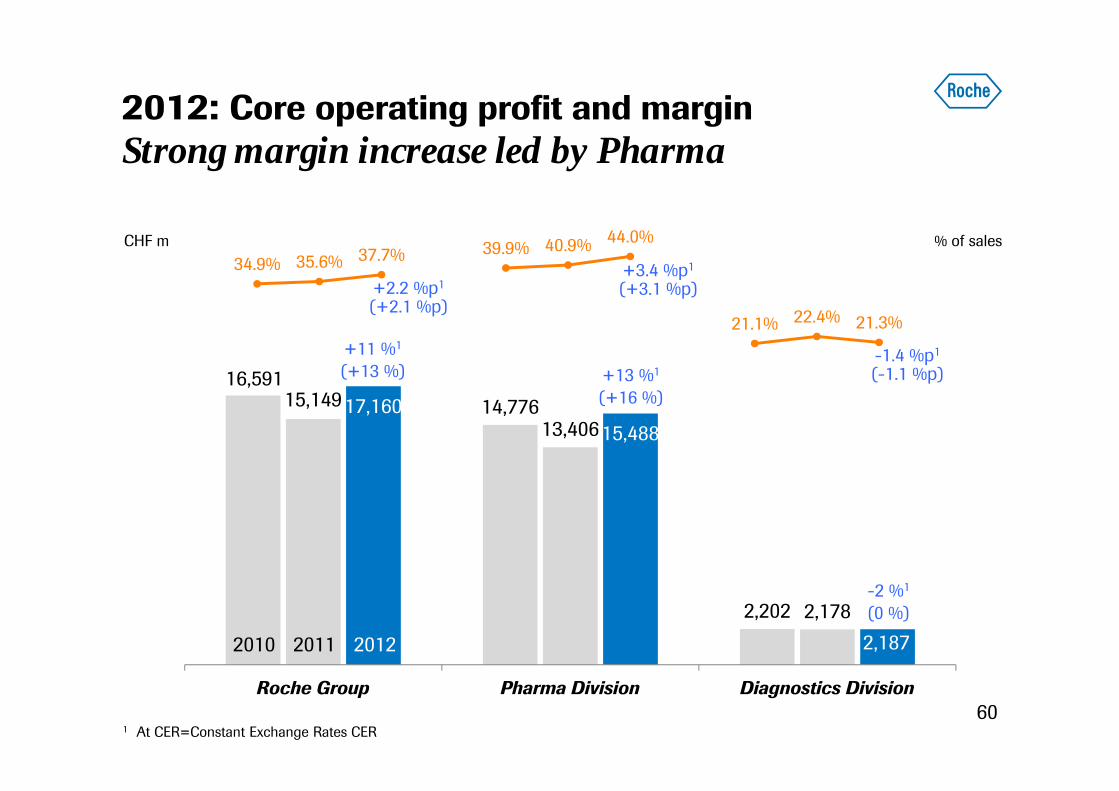

Group core operating profit and margin

15.0716.27 16.59

15.15

17.16

33.0% 33.2%34.9% 35.6%

37.7%

2008 2009 2010 2011 2012

+11%1

1 At CER=Constant Exchange Rates

2012: Operating profit and marginfurther increased

11

CHF bn

% of sales

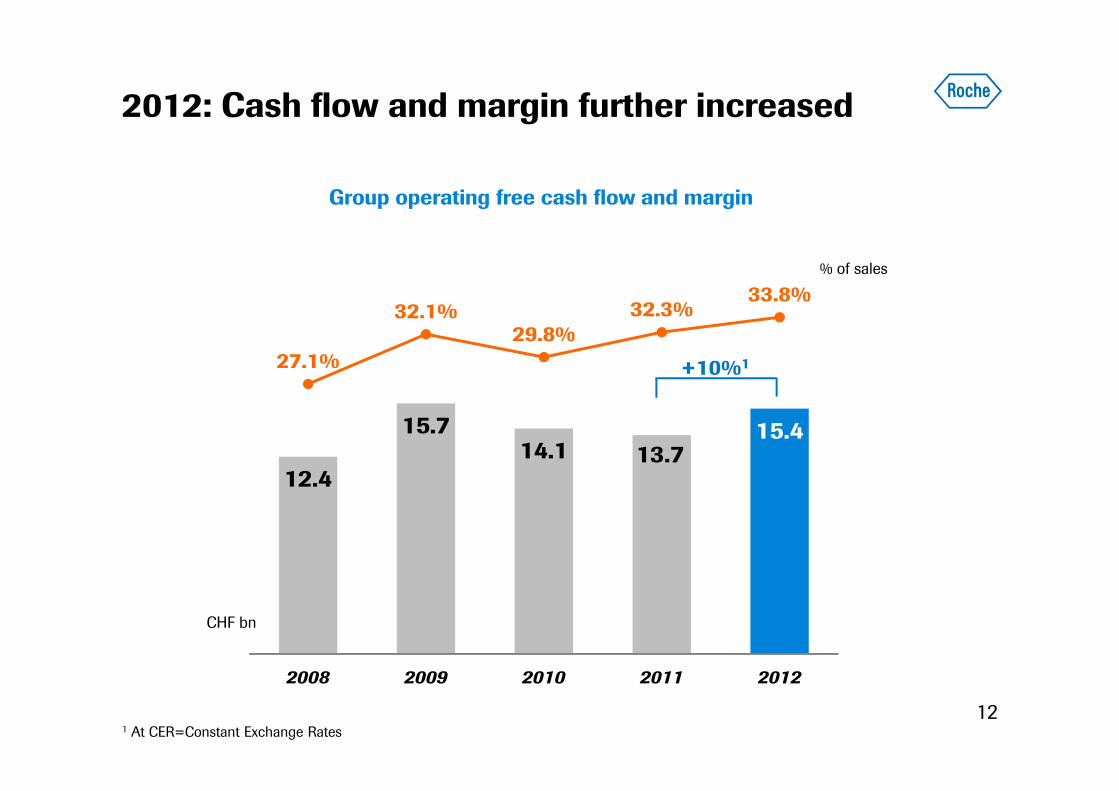

2012: Cash flow and margin further increased

12

12.4

15.714.1 13.7

15.4

27.1%

32.1%29.8%

32.3%33.8%

2008 2009 2010 2011 2012

Group operating free cash flow and margin

+10%1

CHF bn

% of sales

1 At CER=Constant Exchange Rates

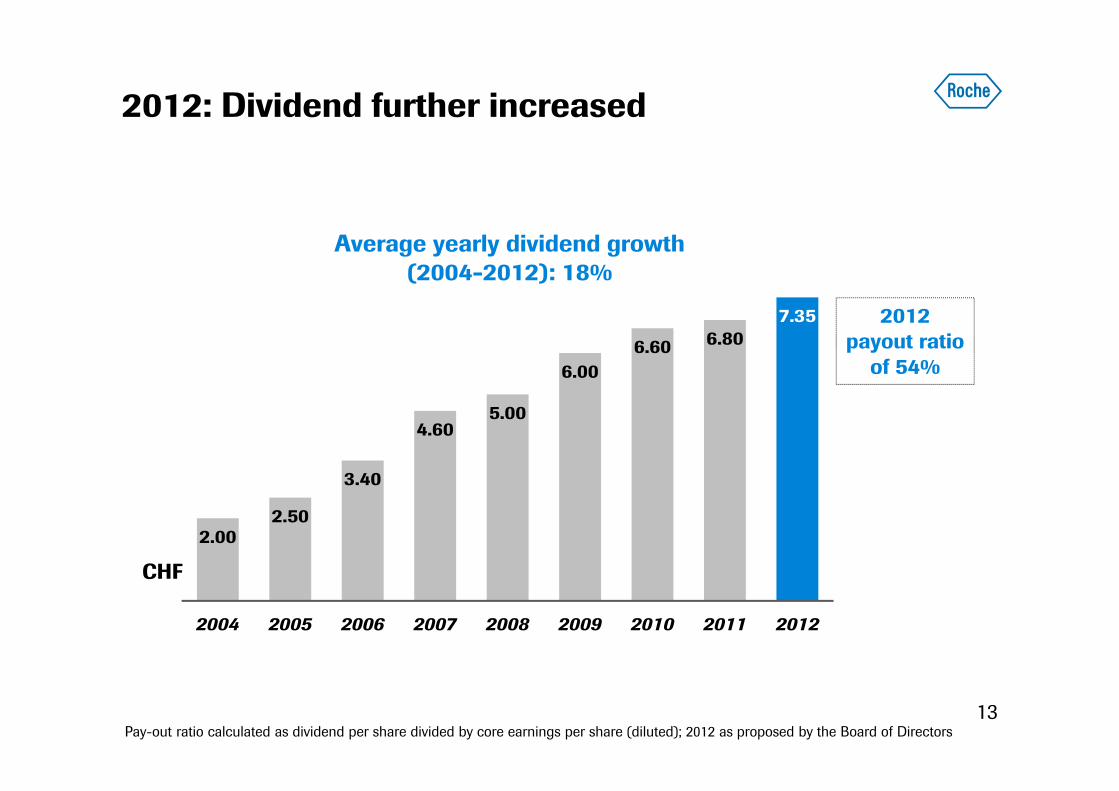

2012: Dividend further increased

13

2.002.50

3.40

4.605.00

6.006.60 6.80

7.35

2004 2005 2006 2007 2008 2009 2010 2011 2012

CHF

1 compound annual growth rate

2012payout ratio

of 54%

Pay-out ratio calculated as dividend per share divided by core earnings per share (diluted); 2012 as proposed by the Board of Directors

Average yearly dividend growth (2004-2012): 18%

14

Solid results 2012

Outlook

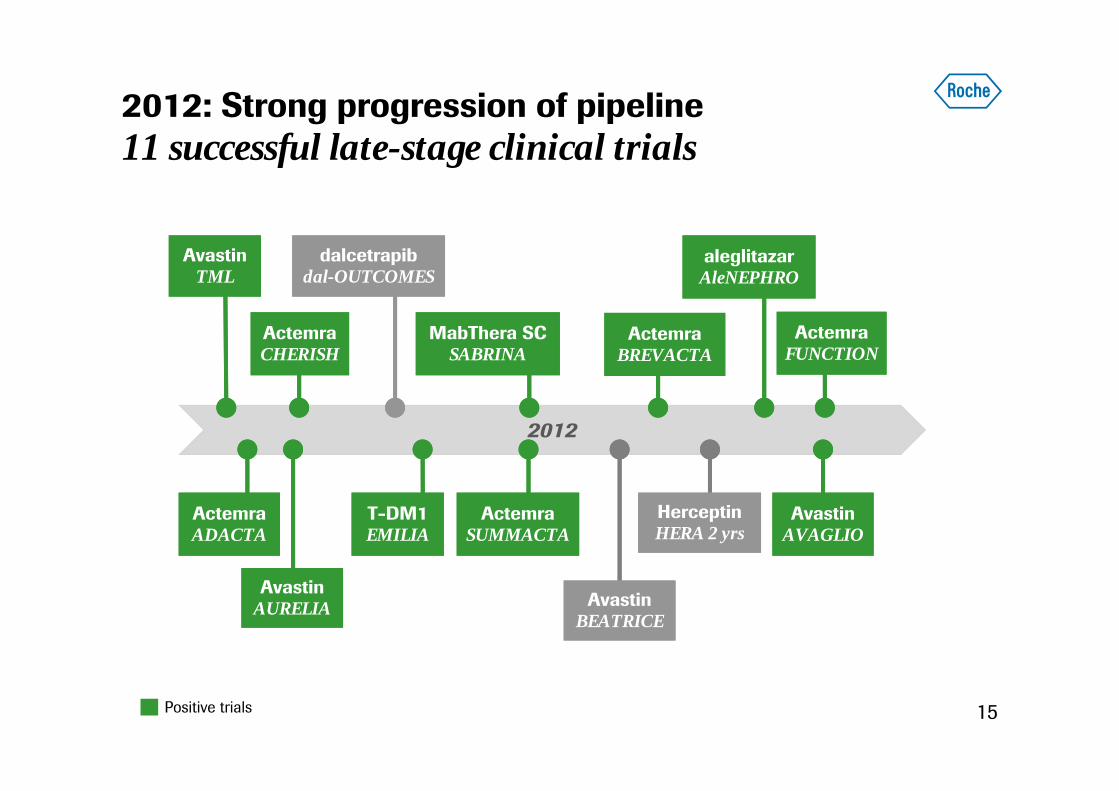

2012: Strong progression of pipeline11 successful late-stage clinical trials

15Positive trials

2012

ActemraADACTAActemraADACTA

AvastinTML

AvastinTML

ActemraCHERISHActemraCHERISH

dalcetrapibdal-OUTCOMES

dalcetrapibdal-OUTCOMES

AvastinAURELIAAvastin

AURELIA

MabThera SCSABRINA

MabThera SCSABRINA

AvastinBEATRICE

AvastinBEATRICE

ActemraSUMMACTA

ActemraSUMMACTA

AvastinAVAGLIOAvastin

AVAGLIOT-DM1EMILIAT-DM1EMILIA

aleglitazarAleNEPHROaleglitazar

AleNEPHRO

ActemraBREVACTA

ActemraBREVACTA

ActemraFUNCTIONActemra

FUNCTION

HerceptinHERA 2 yrsHerceptinHERA 2 yrs

dual PI3 kinase/mTORsolid tumours

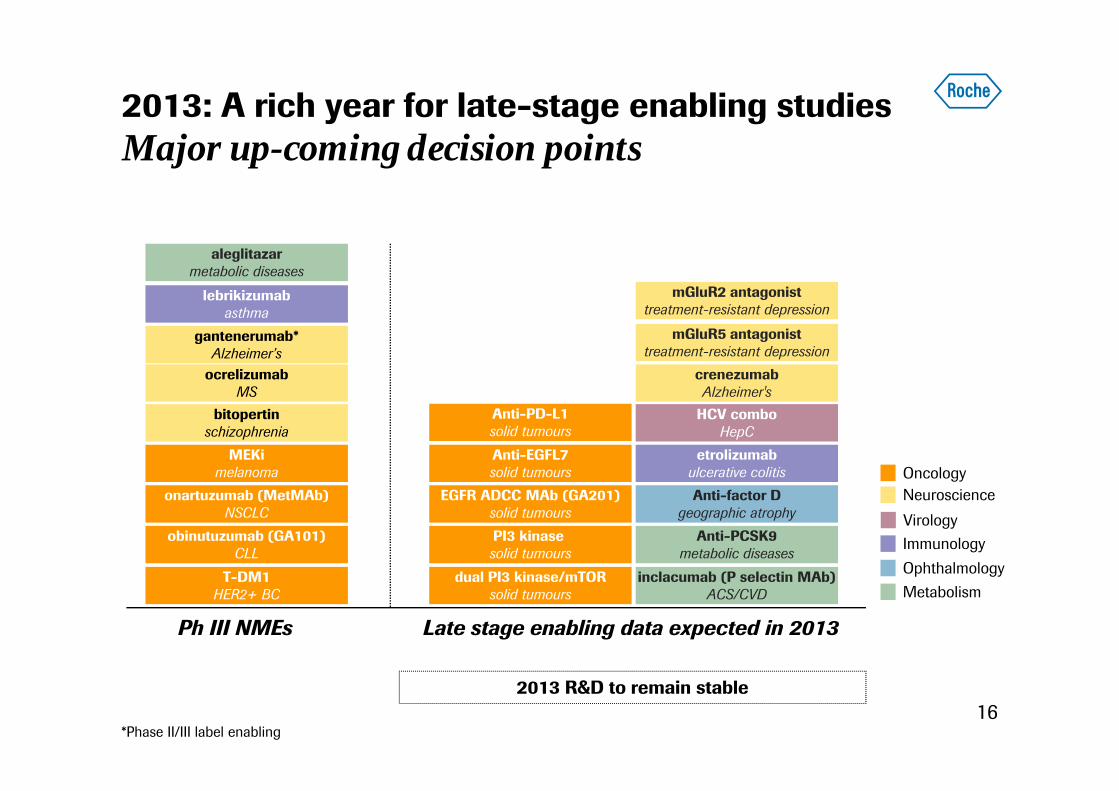

2013: A rich year for late-stage enabling studiesMajor up-coming decision points

16

EGFR ADCC MAb (GA201)solid tumours

OncologyNeuroscience

MetabolismOphthalmology

PI3 kinase solid tumours

Anti-EGFL7solid tumours

Anti-PCSK9metabolic diseases

crenezumabAlzheimer's

mGluR5 antagonisttreatment-resistant depression

Anti-factor Dgeographic atrophy

mGluR2 antagonisttreatment-resistant depression

Anti-PD-L1solid tumours

etrolizumabulcerative colitis

Immunology

inclacumab (P selectin MAb)ACS/CVD

onartuzumab (MetMAb)NSCLC

ocrelizumabMS

MEKimelanoma

obinutuzumab (GA101)CLL

T-DM1HER2+ BC

bitopertinschizophrenia

aleglitazarmetabolic diseases

lebrikizumabasthma

Ph III NMEs Late stage enabling data expected in 2013

gantenerumab*Alzheimer’s

HCV comboHepC

Virology

*Phase II/III label enabling

2013 R&D to remain stable

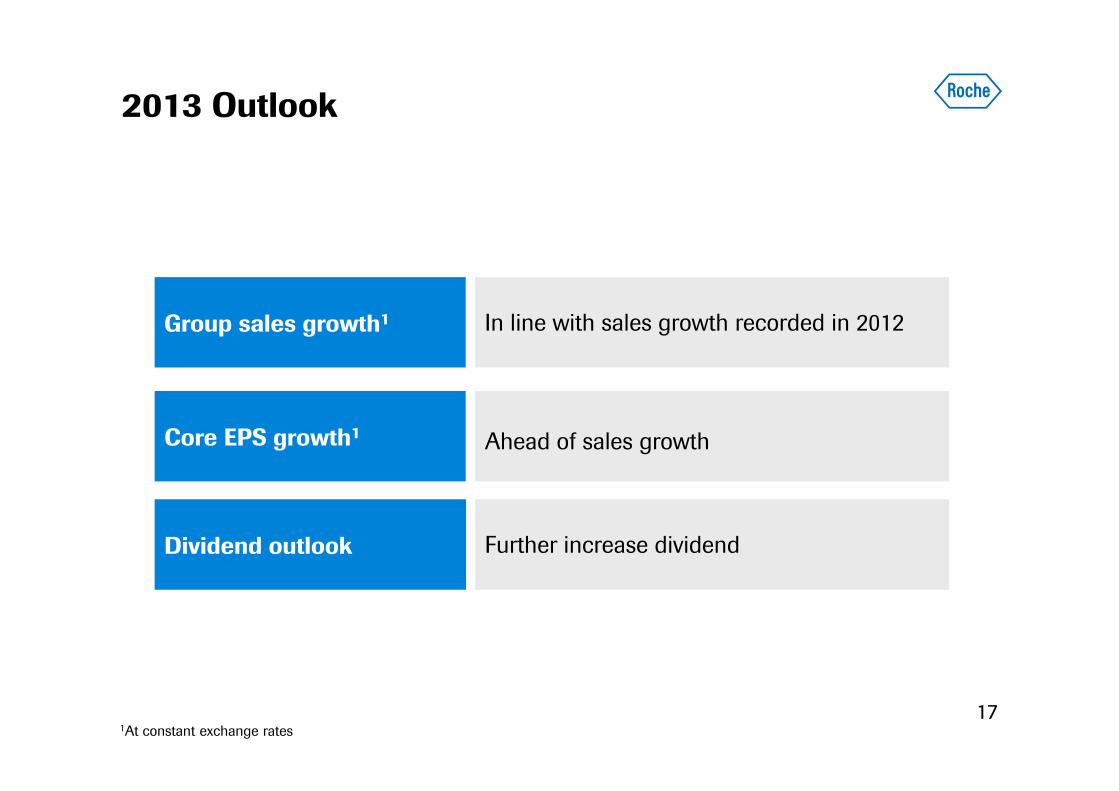

2013 Outlook

171At constant exchange rates

Group sales growth1 In line with sales growth recorded in 2012

Core EPS growth1 Ahead of sales growth

Dividend outlook Further increase dividend

18

Pharmaceuticals DivisionDaniel O’DayCOO Roche Pharmaceuticals

2012 results

Growth drivers

Outlook

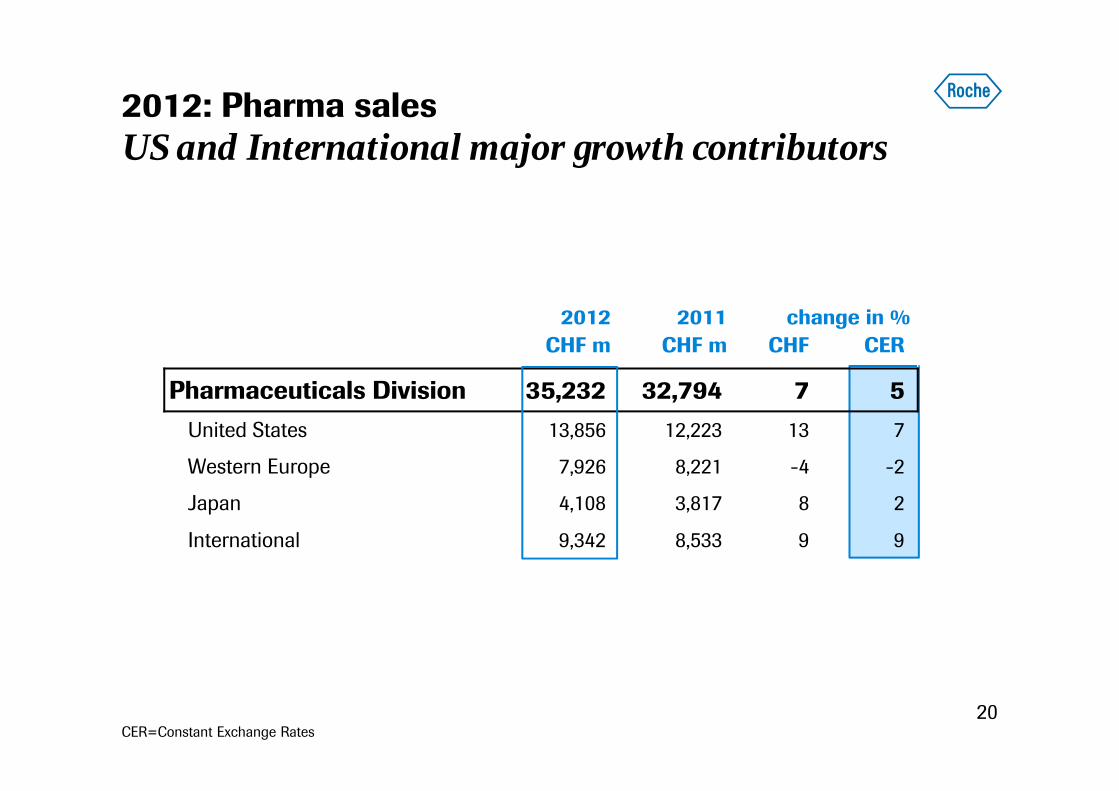

2012: Pharma salesUS and International major growth contributors

20

2012 2011 change in %CHF m CHF m CHF CER

Pharmaceuticals Division 35,232 32,794 7 5United States 13,856 12,223 13 7

Western Europe 7,926 8,221 -4 -2

Japan 4,108 3,817 8 2

International 9,342 8,533 9 9

CER=Constant Exchange Rates

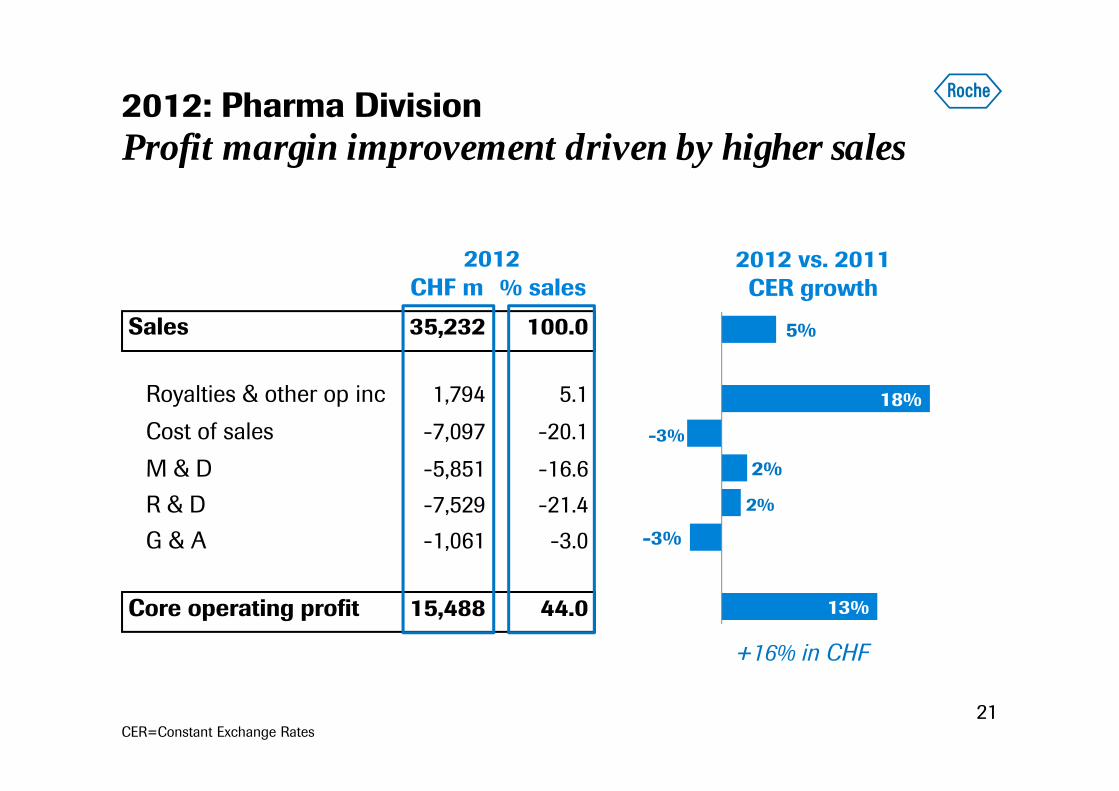

2012: Pharma Division Profit margin improvement driven by higher sales

21

Sales 35,232 100.0

Royalties & other op inc 1,794 5.1Cost of sales -7,097 -20.1M & D -5,851 -16.6R & D -7,529 -21.4G & A -1,061 -3.0

Core operating profit 15,488 44.0

2012 vs. 2011CER growth

2012CHF m % sales

13%

-3%

2%

2%

-3%

18%

5%

+16% in CHF

CER=Constant Exchange Rates

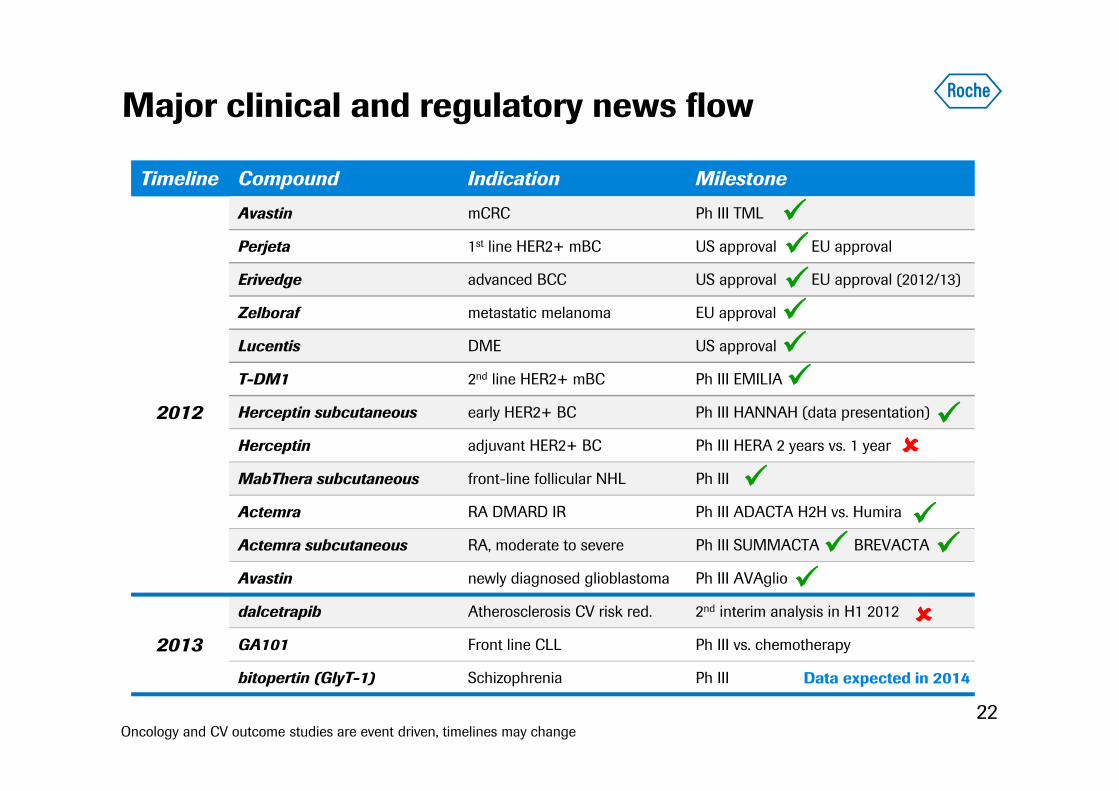

Major clinical and regulatory news flow

22

Timeline Compound Indication Milestone

Avastin mCRC Ph III TML

2012

Perjeta 1st line HER2+ mBC US approval EU approval

Erivedge advanced BCC US approval EU approval (2012/13)

Zelboraf metastatic melanoma EU approval

Lucentis DME US approval

T-DM1 2nd line HER2+ mBC Ph III EMILIA

Herceptin subcutaneous early HER2+ BC Ph III HANNAH (data presentation)

Herceptin adjuvant HER2+ BC Ph III HERA 2 years vs. 1 year

MabThera subcutaneous front-line follicular NHL Ph III

Actemra RA DMARD IR Ph III ADACTA H2H vs. Humira

Actemra subcutaneous RA, moderate to severe Ph III SUMMACTA BREVACTA

Avastin newly diagnosed glioblastoma Ph III AVAglio

2013

dalcetrapib Atherosclerosis CV risk red. 2nd interim analysis in H1 2012

GA101 Front line CLL Ph III vs. chemotherapy

bitopertin (GlyT-1) Schizophrenia Ph III

Oncology and CV outcome studies are event driven, timelines may change

Data expected in 2014

2012 results

Growth drivers

Outlook

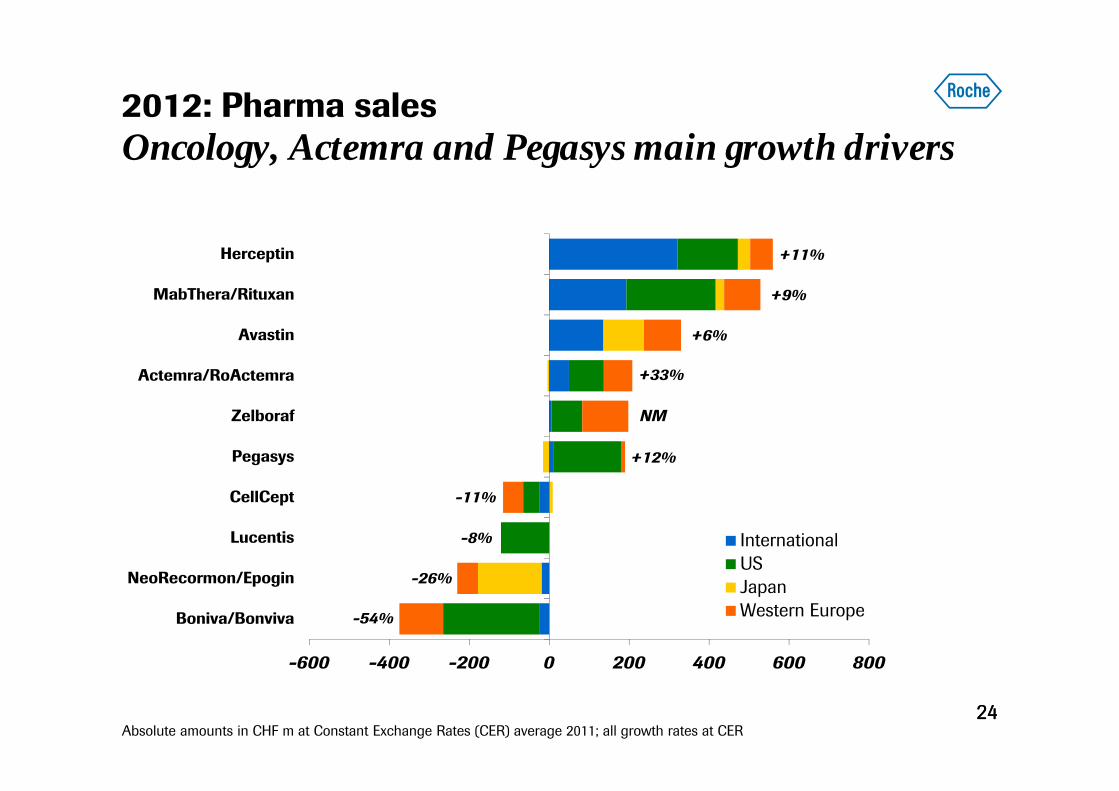

2012: Pharma salesOncology, Actemra and Pegasys main growth drivers

2424Absolute amounts in CHF m at Constant Exchange Rates (CER) average 2011; all growth rates at CER

-600 -400 -200 0 200 400 600 800

Boniva/Bonviva

NeoRecormon/Epogin

Lucentis

CellCept

Pegasys

Zelboraf

Actemra/RoActemra

Avastin

MabThera/Rituxan

Herceptin

InternationalUSJapanWestern Europe

+11%

+9%

+6%

+33%

NM

-11%

-26%

+12%

-8%

-54%

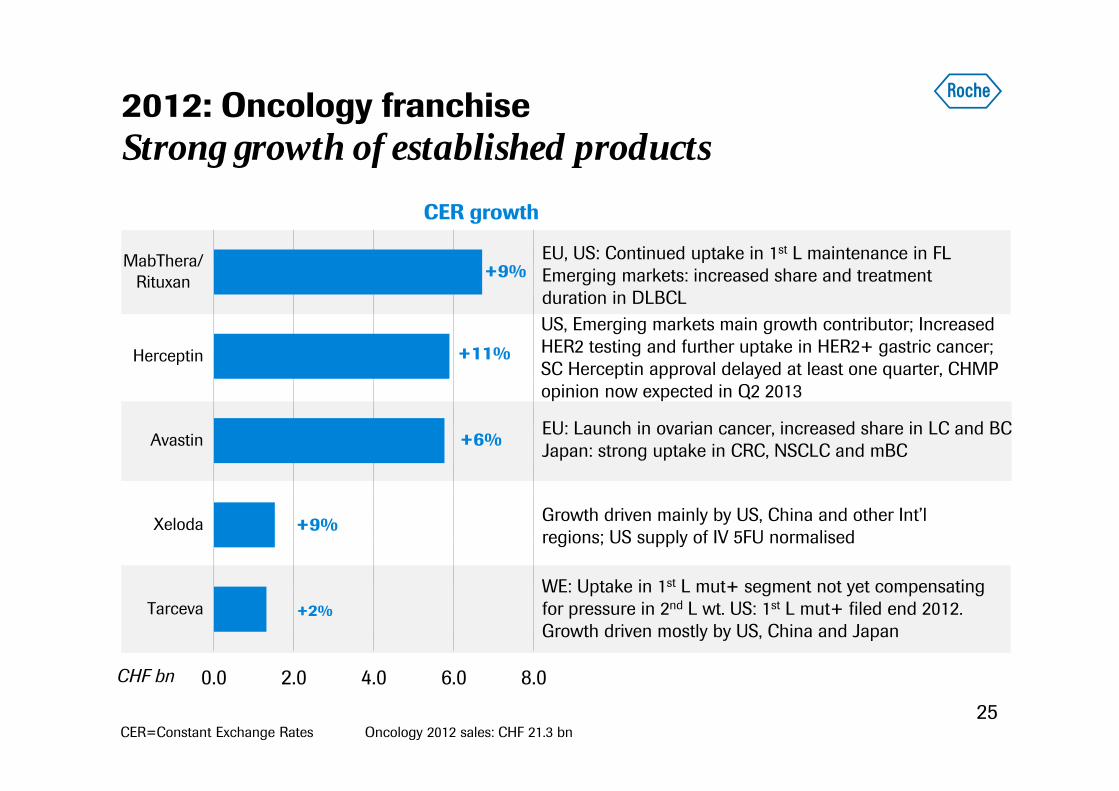

2012: Oncology franchise Strong growth of established products

25

CER growth

CER=Constant Exchange Rates Oncology 2012 sales: CHF 21.3 bn

WE: Uptake in 1st L mut+ segment not yet compensating for pressure in 2nd L wt. US: 1st L mut+ filed end 2012.Growth driven mostly by US, China and Japan

Growth driven mainly by US, China and other Int’l regions; US supply of IV 5FU normalised

EU: Launch in ovarian cancer, increased share in LC and BCJapan: strong uptake in CRC, NSCLC and mBC

EU, US: Continued uptake in 1st L maintenance in FL Emerging markets: increased share and treatment duration in DLBCL

0.0 2.0 4.0 6.0 8.0

Tarceva

Xeloda

Avastin

Herceptin

MabThera/Rituxan +9%

+11%

+9%

+6%

+2%

CHF bn

US, Emerging markets main growth contributor; Increased HER2 testing and further uptake in HER2+ gastric cancer;SC Herceptin approval delayed at least one quarter, CHMPopinion now expected in Q2 2013

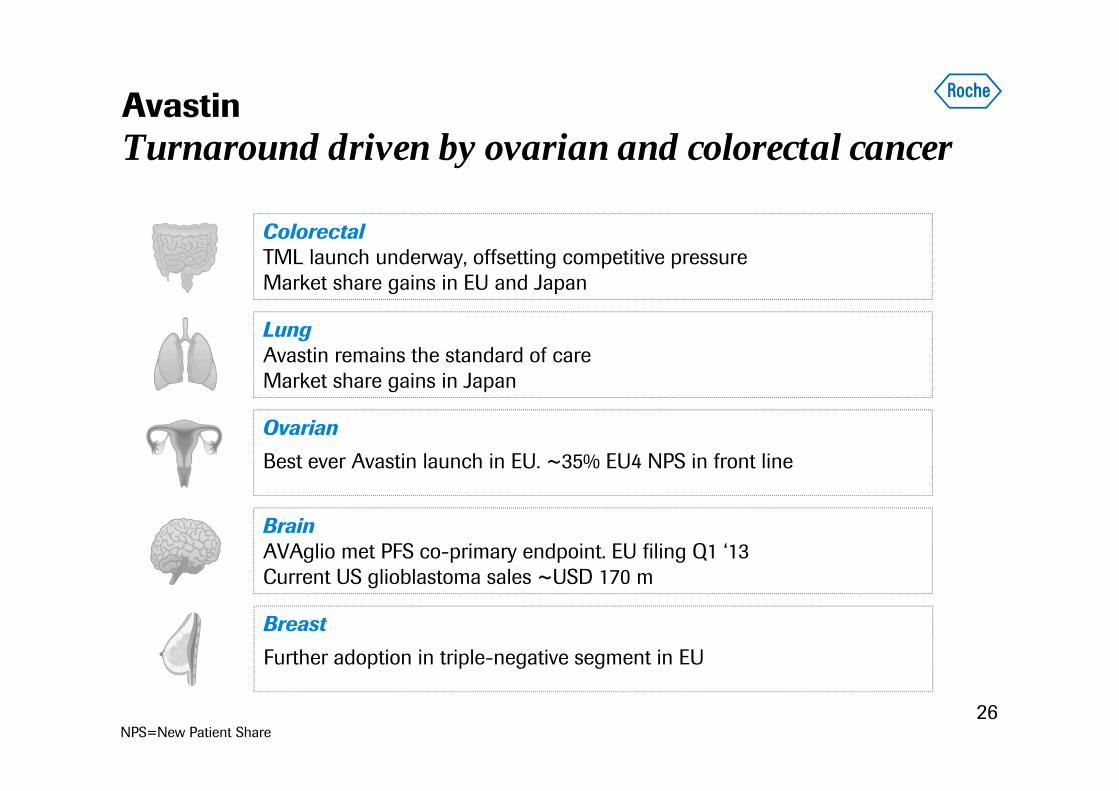

AvastinTurnaround driven by ovarian and colorectal cancer

26

ColorectalTML launch underway, offsetting competitive pressure Market share gains in EU and Japan

LungAvastin remains the standard of careMarket share gains in Japan

OvarianBest ever Avastin launch in EU. ~35% EU4 NPS in front line

BrainAVAglio met PFS co-primary endpoint. EU filing Q1 ‘13Current US glioblastoma sales ~USD 170 m

BreastFurther adoption in triple-negative segment in EU

NPS=New Patient Share

2012: Oncology franchiseNew products

27

• Good launch in US• Positive CHMP opinion in Dec ’12

• US: Market fully penetrated at ~85% 1st line NPS • WE: More than half of global sales, main growth region in 2013• Ph III in combination with MEKi started

• US: Broad prescriber base, need for education on disease definition and eligibility

• EU: Approval expected in 2013

• US PDUFA 26 February 2013, EU H2 2013• MARIANNE study data expected H1 2014

(based on current event rate)

NPS=New Patient Share

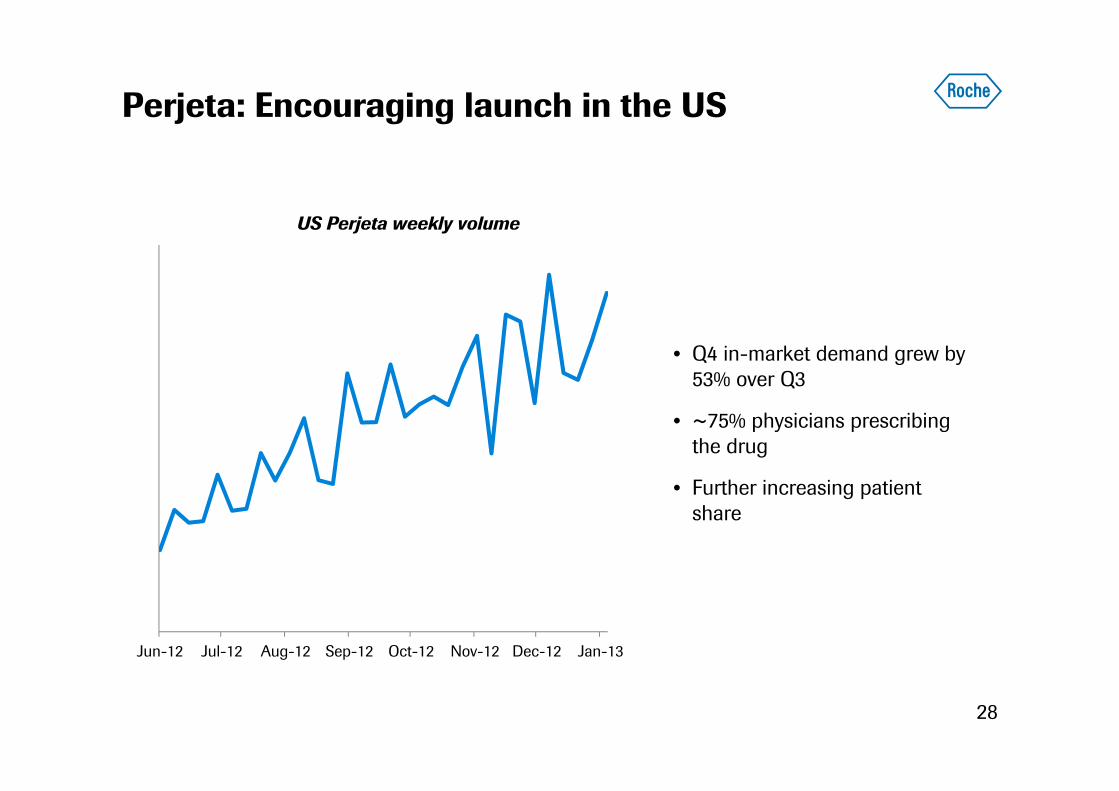

Perjeta: Encouraging launch in the US

28

Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13

US Perjeta weekly volume

• Q4 in-market demand grew by 53% over Q3

• ~75% physicians prescribing the drug

• Further increasing patient share

200

300

400

500

Q1'10

Q2'10

Q3'10

Q4'10

Q1'11

Q2'11

Q3'11

Q4'11

Q1'12

Q2'12

Q3'12

Q4'12

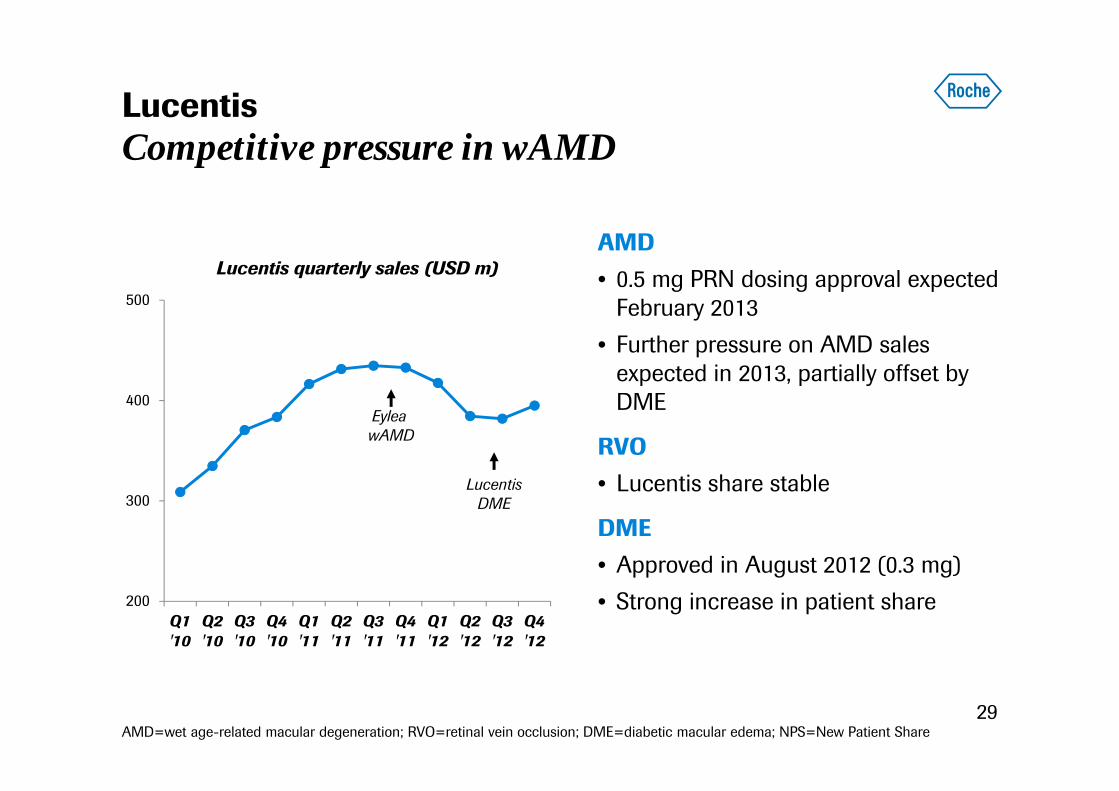

LucentisCompetitive pressure in wAMD

29AMD=wet age-related macular degeneration; RVO=retinal vein occlusion; DME=diabetic macular edema; NPS=New Patient Share

AMD • 0.5 mg PRN dosing approval expected

February 2013• Further pressure on AMD sales

expected in 2013, partially offset by DME

RVO• Lucentis share stable

DME• Approved in August 2012 (0.3 mg)• Strong increase in patient share

Lucentis quarterly sales (USD m)

EyleawAMD

LucentisDME

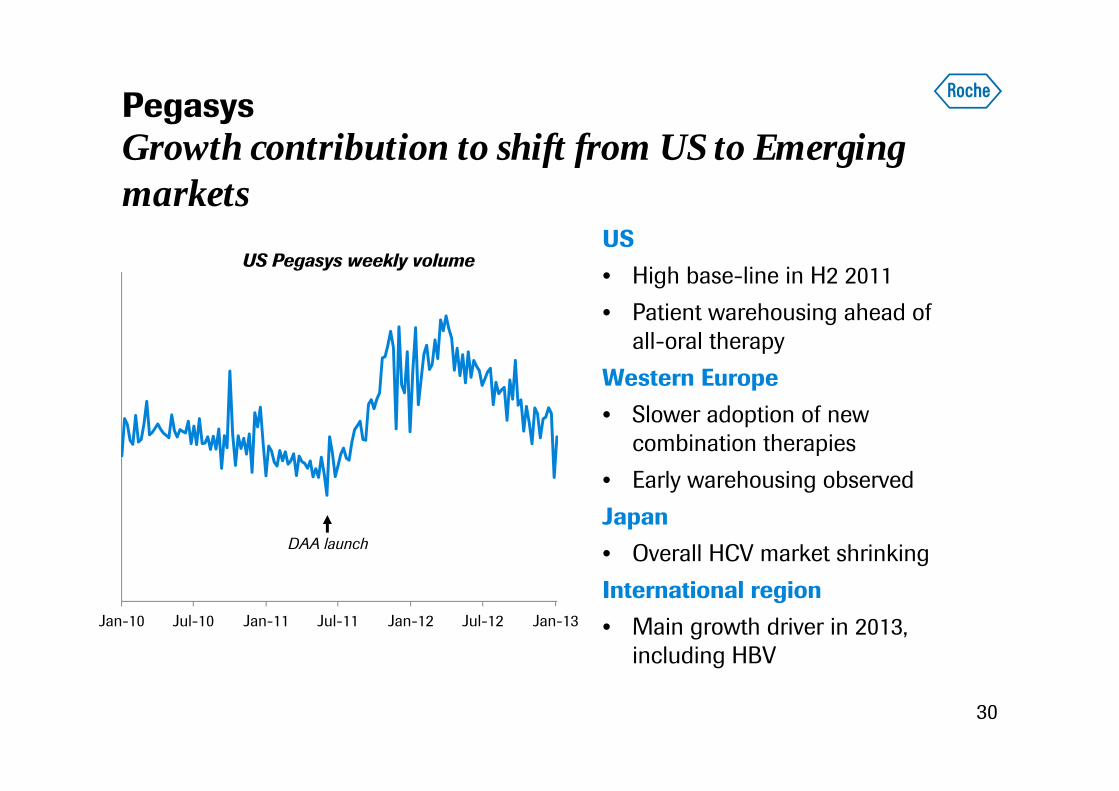

PegasysGrowth contribution to shift from US to Emerging markets

30

US• High base-line in H2 2011 • Patient warehousing ahead of

all-oral therapyWestern Europe• Slower adoption of new

combination therapies• Early warehousing observedJapan• Overall HCV market shrinkingInternational region• Main growth driver in 2013,

including HBV

US Pegasys weekly volume

DAA launch

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13

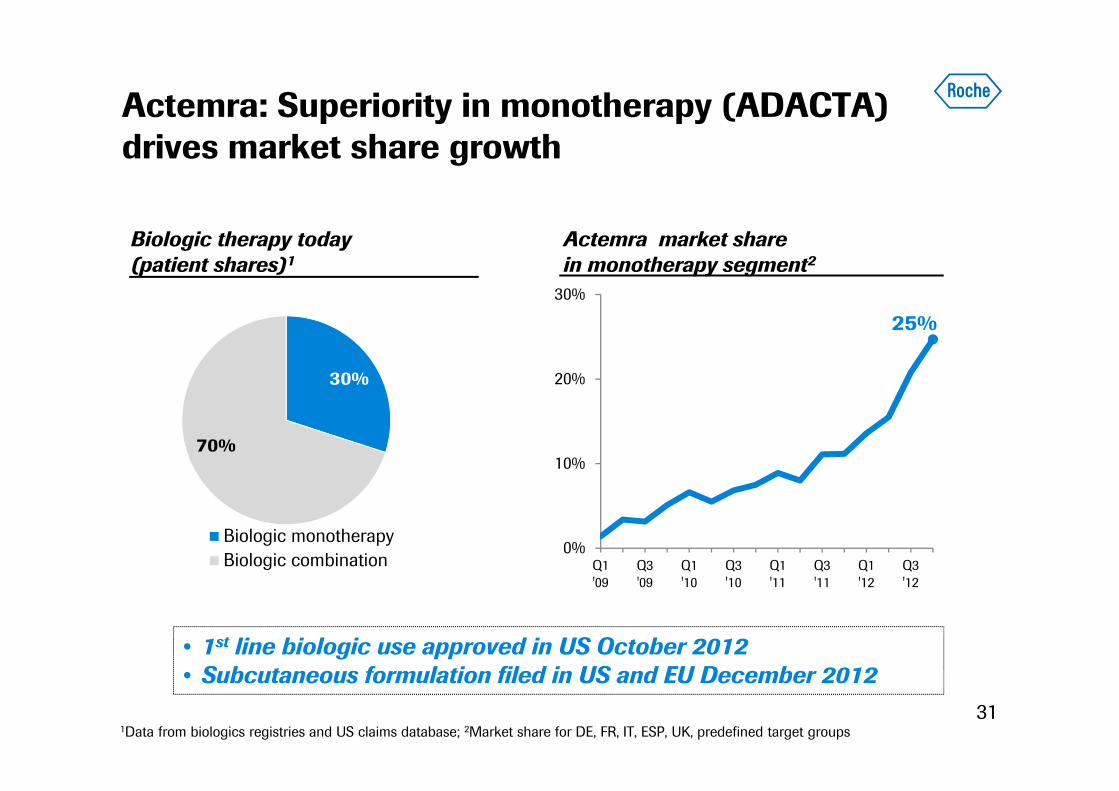

Actemra: Superiority in monotherapy (ADACTA) drives market share growth

31

25%

0%

10%

20%

30%

Q1'09

Q3'09

Q1'10

Q3'10

Q1'11

Q3'11

Q1'12

Q3'12

Actemra market sharein monotherapy segment2

30%

70%

Biologic monotherapyBiologic combination

Biologic therapy today(patient shares)1

• 1st line biologic use approved in US October 2012• Subcutaneous formulation filed in US and EU December 2012

1Data from biologics registries and US claims database; 2Market share for DE, FR, IT, ESP, UK, predefined target groups

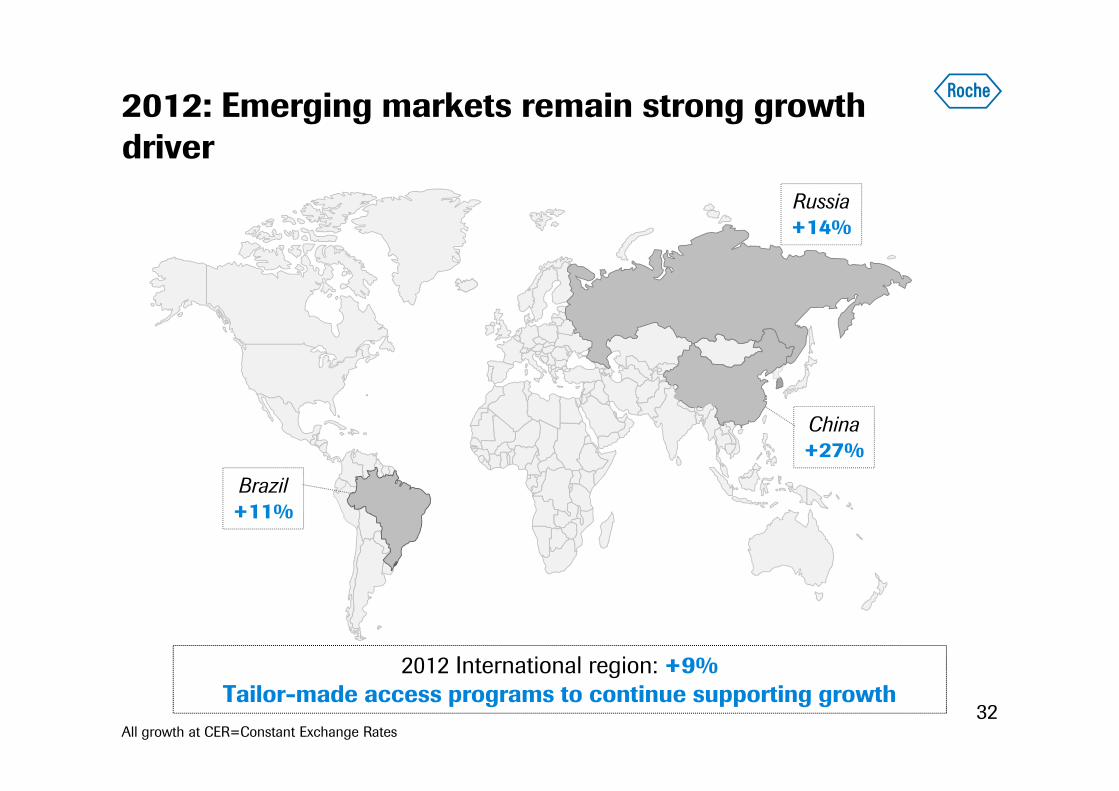

2012: Emerging markets remain strong growth driver

32

Brazil+11%

China+27%

Russia+14%

2012 International region: +9%Tailor-made access programs to continue supporting growth

All growth at CER=Constant Exchange Rates

2012 results

Growth drivers

Outlook

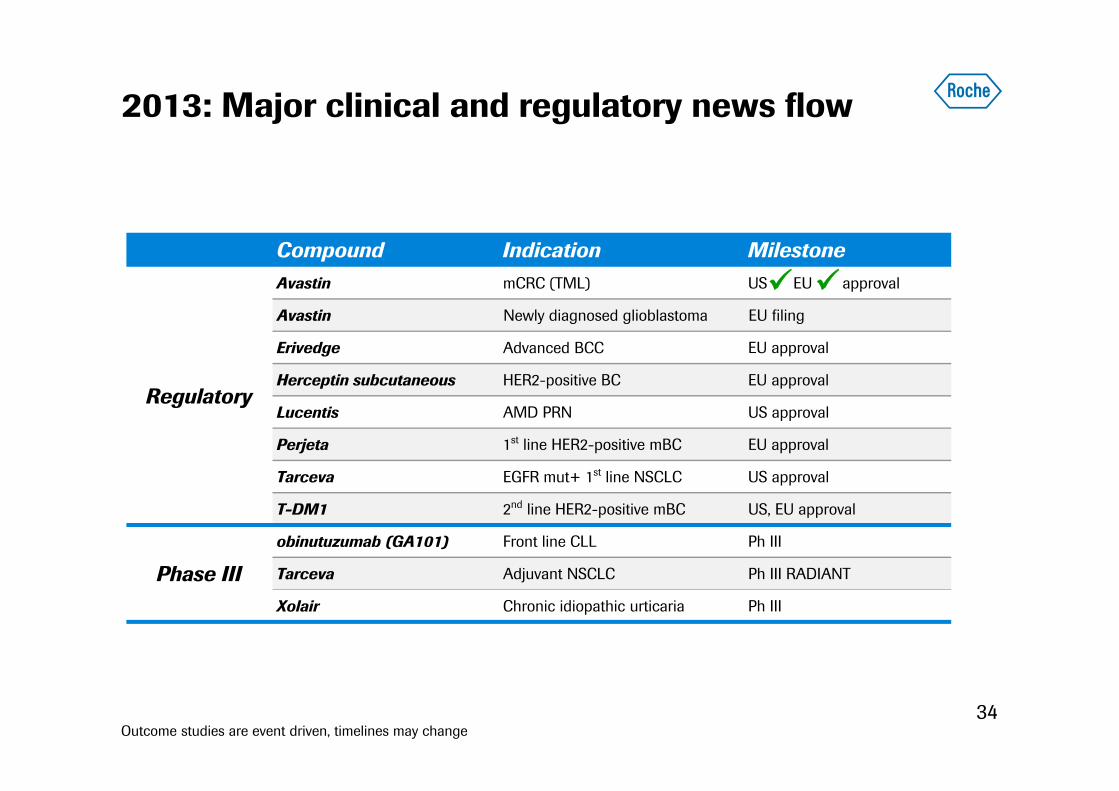

2013: Major clinical and regulatory news flow

34Outcome studies are event driven, timelines may change

Compound Indication Milestone

Regulatory

Avastin mCRC (TML) US EU approval

Avastin Newly diagnosed glioblastoma EU filing

Erivedge Advanced BCC EU approval

Herceptin subcutaneous HER2-positive BC EU approval

Lucentis AMD PRN US approval

Perjeta 1st line HER2-positive mBC EU approval

Tarceva EGFR mut+ 1st line NSCLC US approval

T-DM1 2nd line HER2-positive mBC US, EU approval

Phase III

obinutuzumab (GA101) Front line CLL Ph III

Tarceva Adjuvant NSCLC Ph III RADIANT

Xolair Chronic idiopathic urticaria Ph III

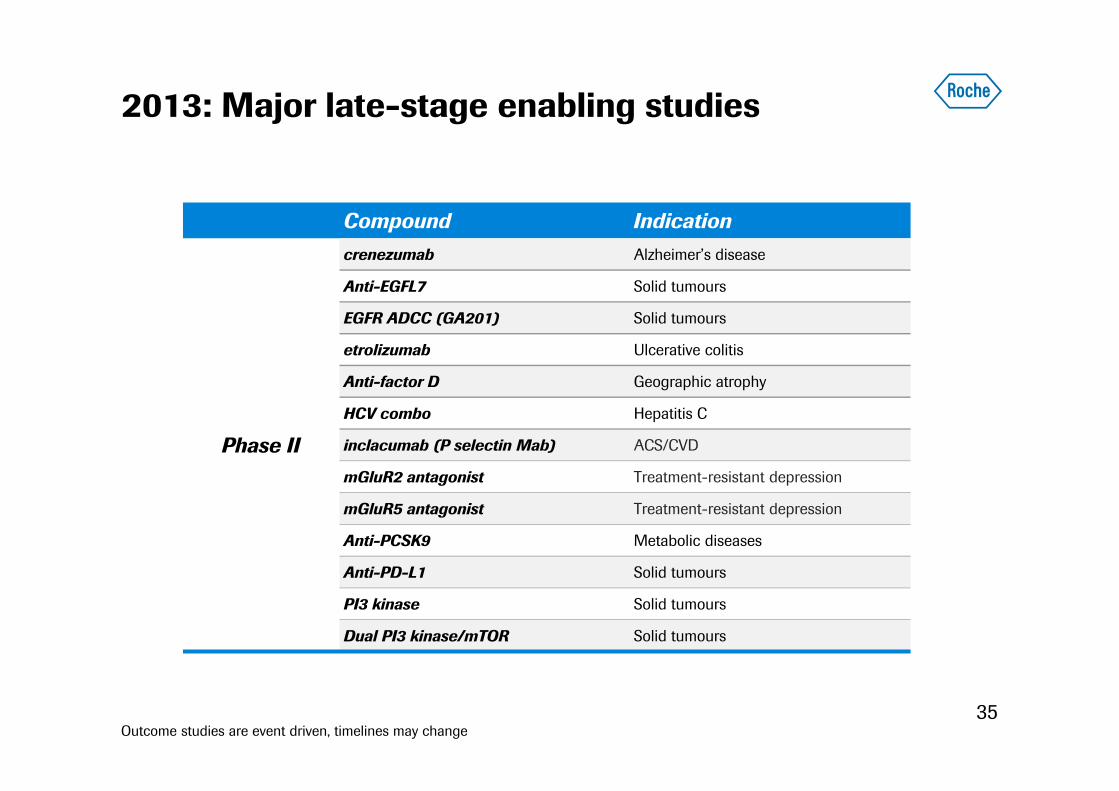

2013: Major late-stage enabling studies

35

Compound Indication

Phase II

crenezumab Alzheimer’s disease

Anti-EGFL7 Solid tumours

EGFR ADCC (GA201) Solid tumours

etrolizumab Ulcerative colitis

Anti-factor D Geographic atrophy

HCV combo Hepatitis C

inclacumab (P selectin Mab) ACS/CVD

mGluR2 antagonist Treatment-resistant depression

mGluR5 antagonist Treatment-resistant depression

Anti-PCSK9 Metabolic diseases

Anti-PD-L1 Solid tumours

PI3 kinase Solid tumours

Dual PI3 kinase/mTOR Solid tumours

Outcome studies are event driven, timelines may change

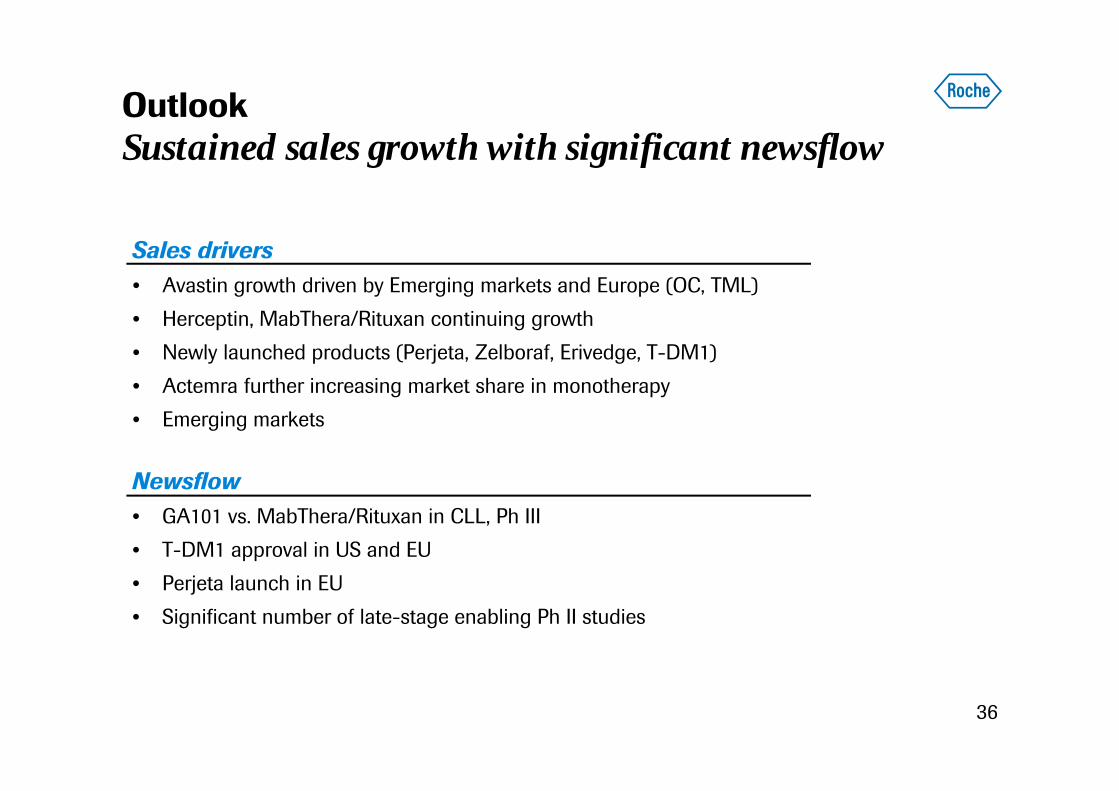

OutlookSustained sales growth with significant newsflow

36

Sales drivers• Avastin growth driven by Emerging markets and Europe (OC, TML)• Herceptin, MabThera/Rituxan continuing growth• Newly launched products (Perjeta, Zelboraf, Erivedge, T-DM1)• Actemra further increasing market share in monotherapy• Emerging markets

Newsflow• GA101 vs. MabThera/Rituxan in CLL, Ph III• T-DM1 approval in US and EU• Perjeta launch in EU• Significant number of late-stage enabling Ph II studies

Diagnostics DivisionRoland DiggelmannCOO Roche Diagnostics Picture

37

38

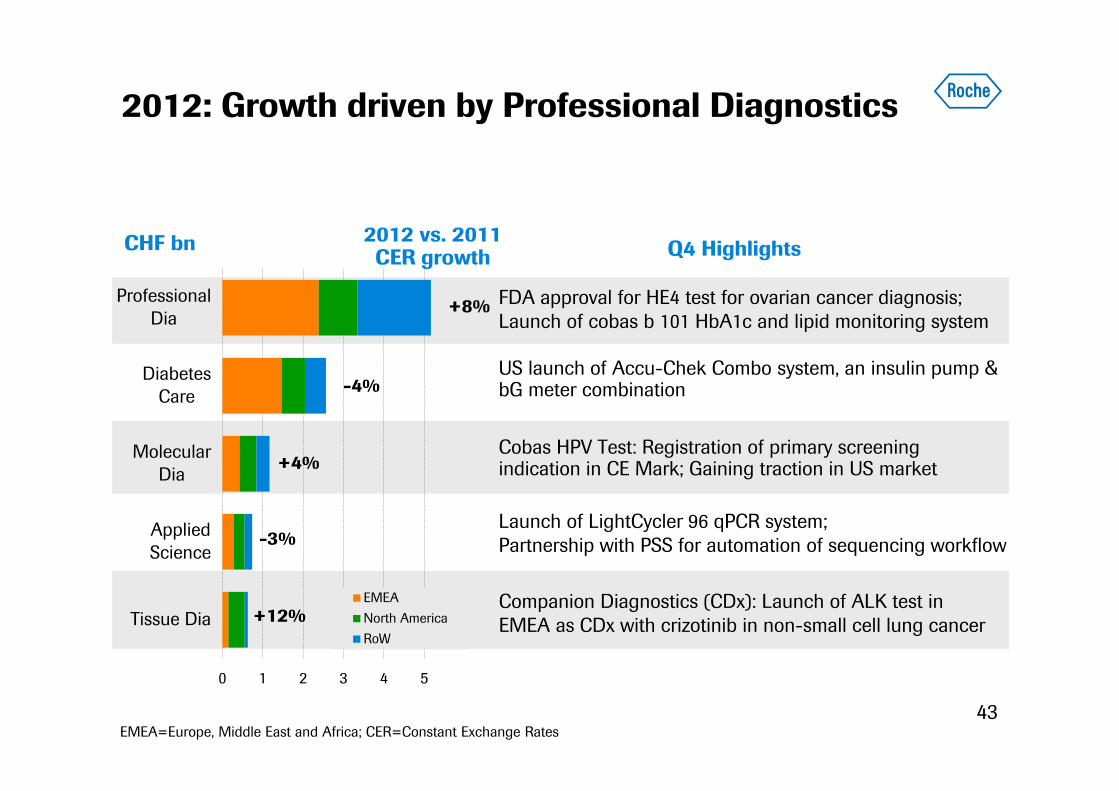

2012: Professional Diagnostics main growth driver

Refining Diabetes Care and Applied Science

Companion Diagnostics

2011 2012 CHF in %CHF m CHF m growth CER

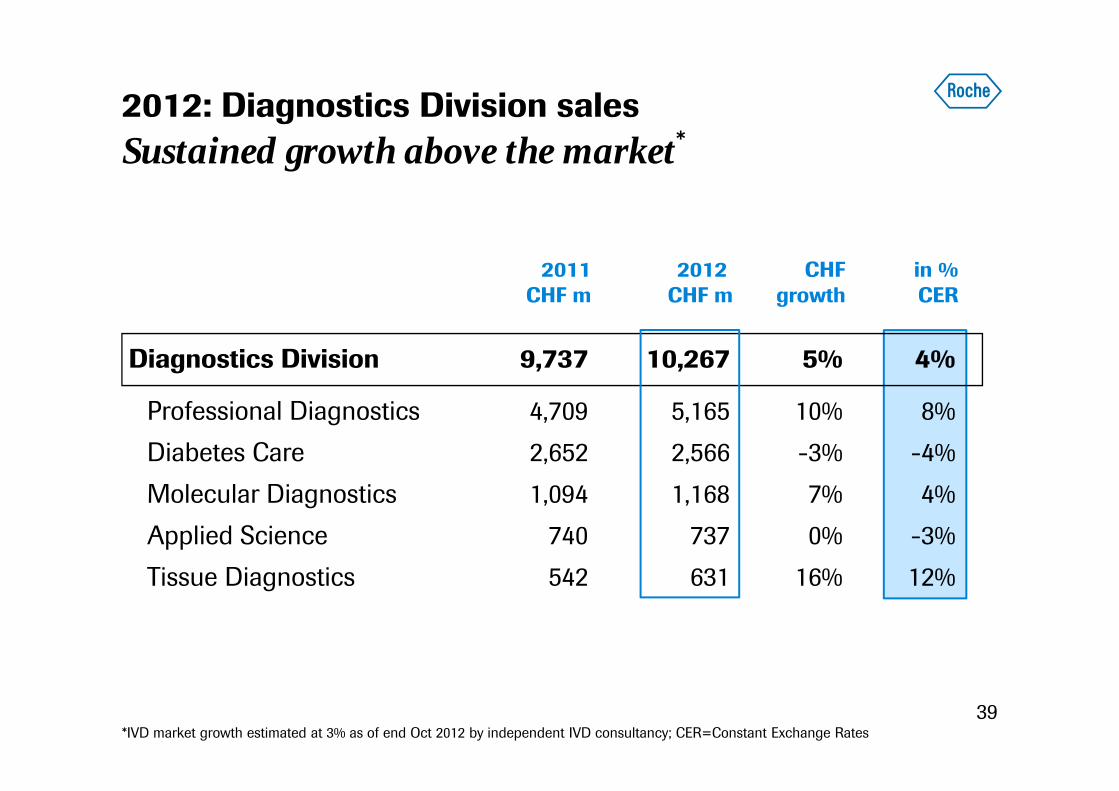

2012: Diagnostics Division sales Sustained growth above the market*

39

Diagnostics Division 9,737 10,267 5% 4%

Professional Diagnostics 4,709 5,165 10% 8%Diabetes Care 2,652 2,566 -3% -4%Molecular Diagnostics 1,094 1,168 7% 4%Applied Science 740 737 0% -3%Tissue Diagnostics 542 631 16% 12%

*IVD market growth estimated at 3% as of end Oct 2012 by independent IVD consultancy; CER=Constant Exchange Rates

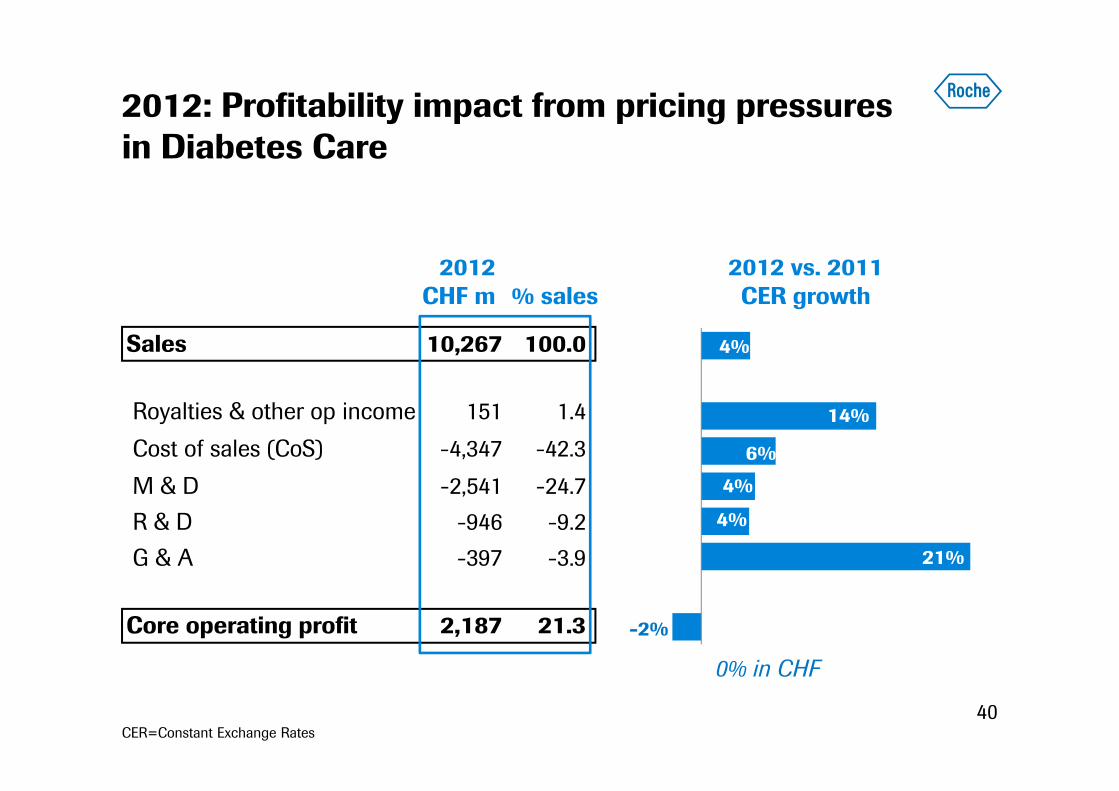

2012: Profitability impact from pricing pressures in Diabetes Care

40

2012 vs. 2011CER growth

2012 CHF m % sales

Sales 10,267 100.0

Royalties & other op income 151 1.4Cost of sales (CoS) -4,347 -42.3M & D -2,541 -24.7R & D -946 -9.2G & A -397 -3.9

Core operating profit 2,187 21.3 -2%

21%

4%

4%

6%

14%

4%

CER=Constant Exchange Rates

0% in CHF

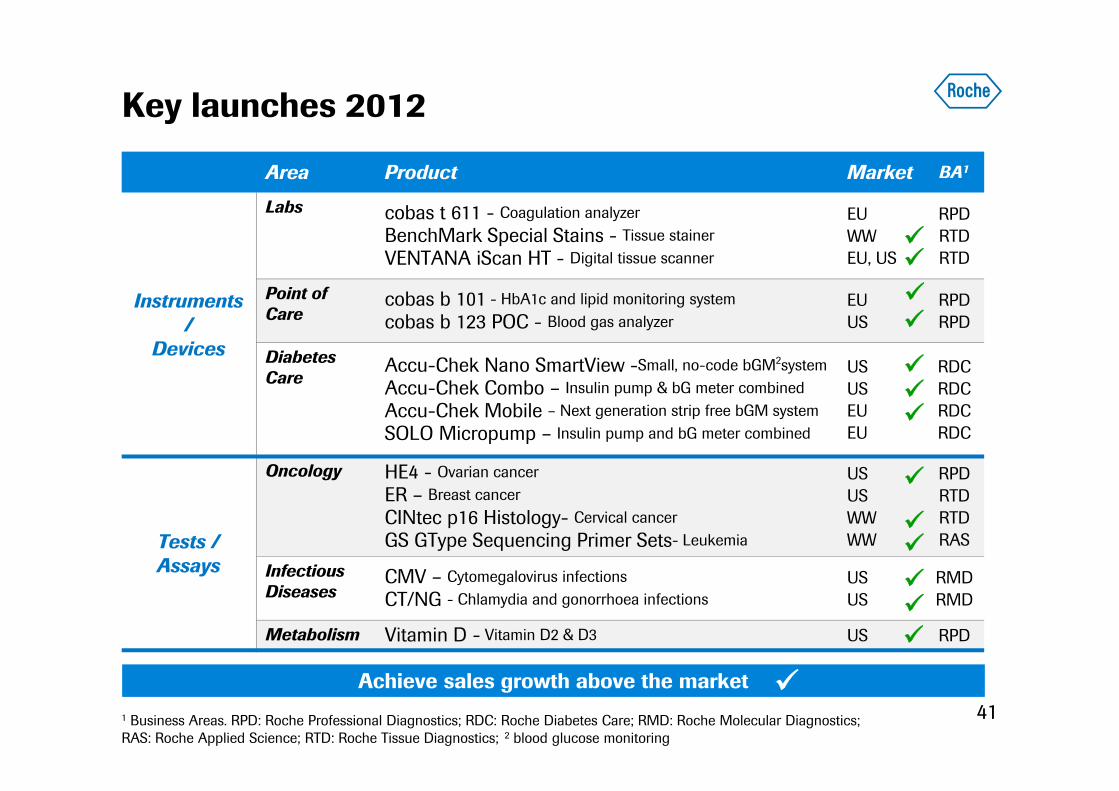

Key launches 2012

41

Area Product Market BA1

Instruments/

Devices

Labs cobas t 611 - Coagulation analyzer BenchMark Special Stains - Tissue stainerVENTANA iScan HT - Digital tissue scanner

EUWWEU, US

RPDRTDRTD

Point of Care

cobas b 101 - HbA1c and lipid monitoring systemcobas b 123 POC - Blood gas analyzer

EUUS

RPDRPD

Diabetes Care

Accu-Chek Nano SmartView -Small, no-code bGM2systemAccu-Chek Combo – Insulin pump & bG meter combinedAccu-Chek Mobile – Next generation strip free bGM systemSOLO Micropump – Insulin pump and bG meter combined

USUSEUEU

RDCRDCRDCRDC

Tests /Assays

Oncology HE4 - Ovarian cancerER – Breast cancerCINtec p16 Histology- Cervical cancerGS GType Sequencing Primer Sets- Leukemia

USUSWWWW

RPDRTDRTDRAS

Infectious Diseases

CMV – Cytomegalovirus infectionsCT/NG - Chlamydia and gonorrhoea infections

USUS

RMDRMD

Metabolism Vitamin D - Vitamin D2 & D3 US RPD

Achieve sales growth above the market

1 Business Areas. RPD: Roche Professional Diagnostics; RDC: Roche Diabetes Care; RMD: Roche Molecular Diagnostics;RAS: Roche Applied Science; RTD: Roche Tissue Diagnostics; 2 blood glucose monitoring

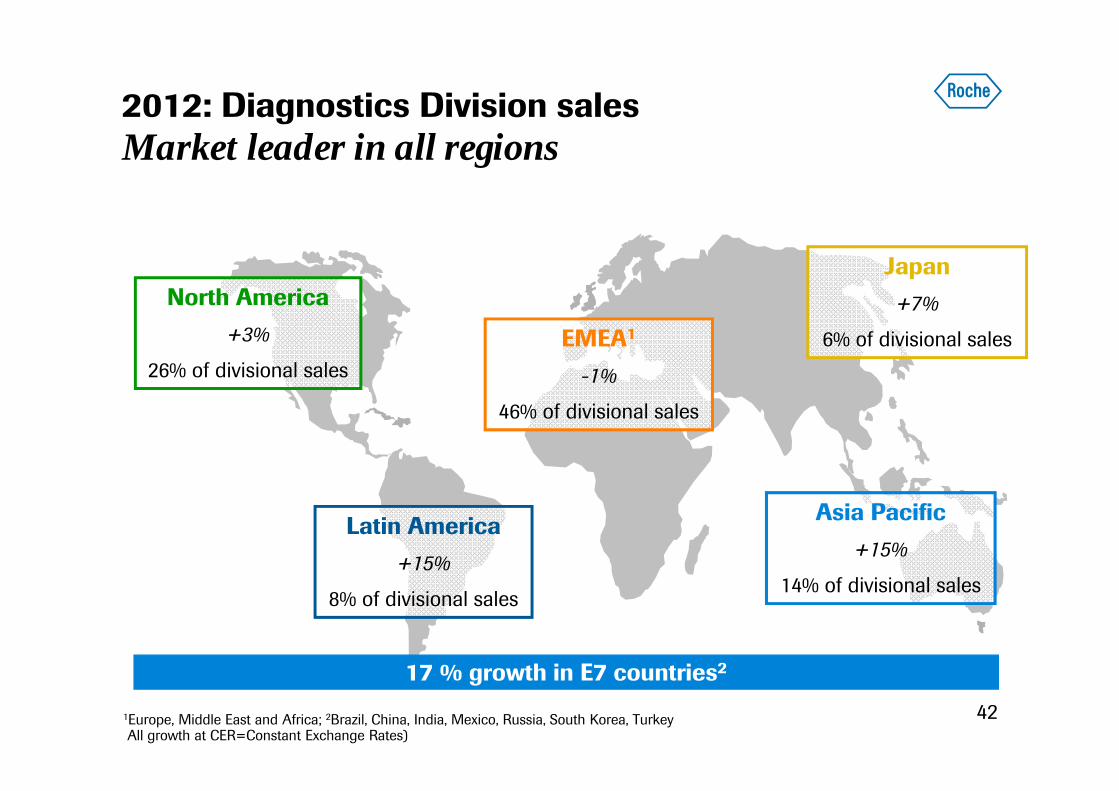

North America+3%

26% of divisional sales

Latin America+15%

8% of divisional sales

Japan+7%

6% of divisional salesEMEA1

-1%

46% of divisional sales

2012: Diagnostics Division sales Market leader in all regions

42

Asia Pacific+15%

14% of divisional sales

1Europe, Middle East and Africa; 2Brazil, China, India, Mexico, Russia, South Korea, Turkey All growth at CER=Constant Exchange Rates)

17 % growth in E7 countries2

2012: Growth driven by Professional Diagnostics

43

CHF bn 2012 vs. 2011CER growth

+8%

-4%

+4%

-3%

+12%

Launch of LightCycler 96 qPCR system; Partnership with PSS for automation of sequencing workflow

Cobas HPV Test: Registration of primary screening indication in CE Mark; Gaining traction in US market

US launch of Accu-Chek Combo system, an insulin pump & bG meter combination

FDA approval for HE4 test for ovarian cancer diagnosis; Launch of cobas b 101 HbA1c and lipid monitoring system

Companion Diagnostics (CDx): Launch of ALK test in EMEA as CDx with crizotinib in non-small cell lung cancer

EMEA=Europe, Middle East and Africa; CER=Constant Exchange Rates

Q4 Highlights

0 1 2 3 4 5

Tissue Dia

AppliedScience

MolecularDia

DiabetesCare

ProfessionalDia

EMEANorth AmericaRoW

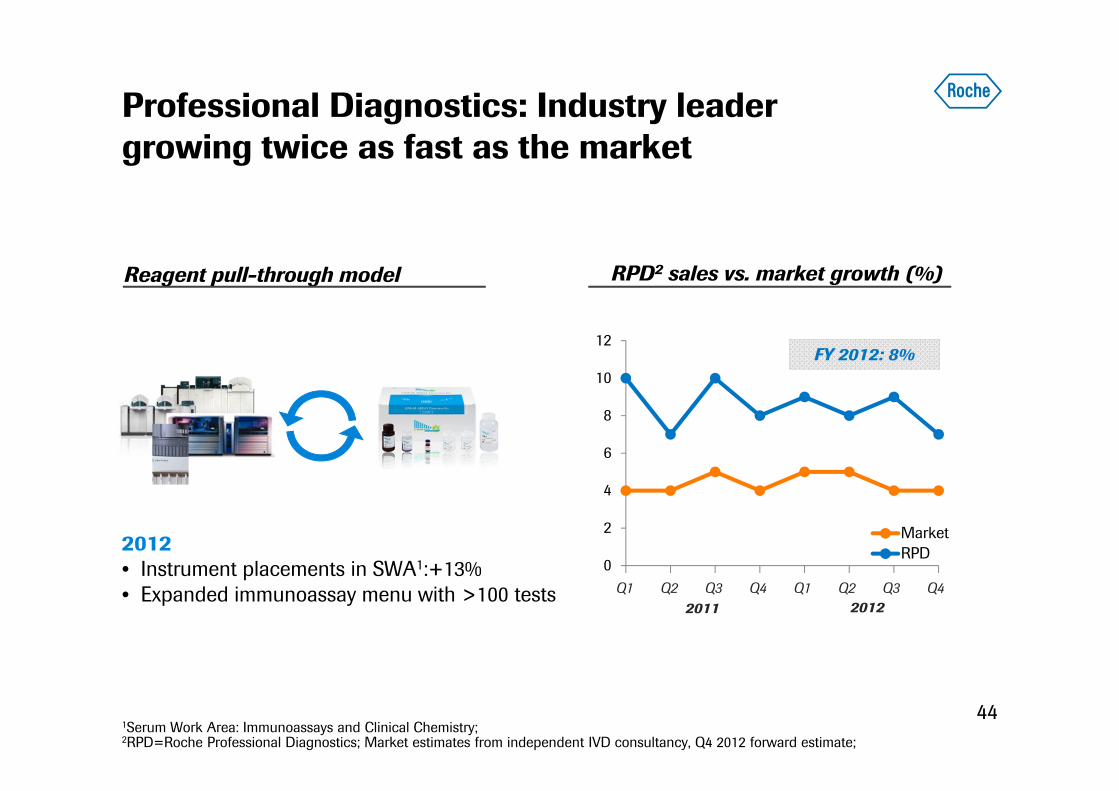

Professional Diagnostics: Industry leader growing twice as fast as the market

44

Reagent pull-through model

2012• Instrument placements in SWA1:+13%• Expanded immunoassay menu with >100 tests

1Serum Work Area: Immunoassays and Clinical Chemistry;2RPD=Roche Professional Diagnostics; Market estimates from independent IVD consultancy, Q4 2012 forward estimate;

RPD2 sales vs. market growth (%)

20122011

FY 2012: 8%

0

2

4

6

8

10

12

MarketRPD

Q3Q2Q1Q4Q3Q2Q1 Q4

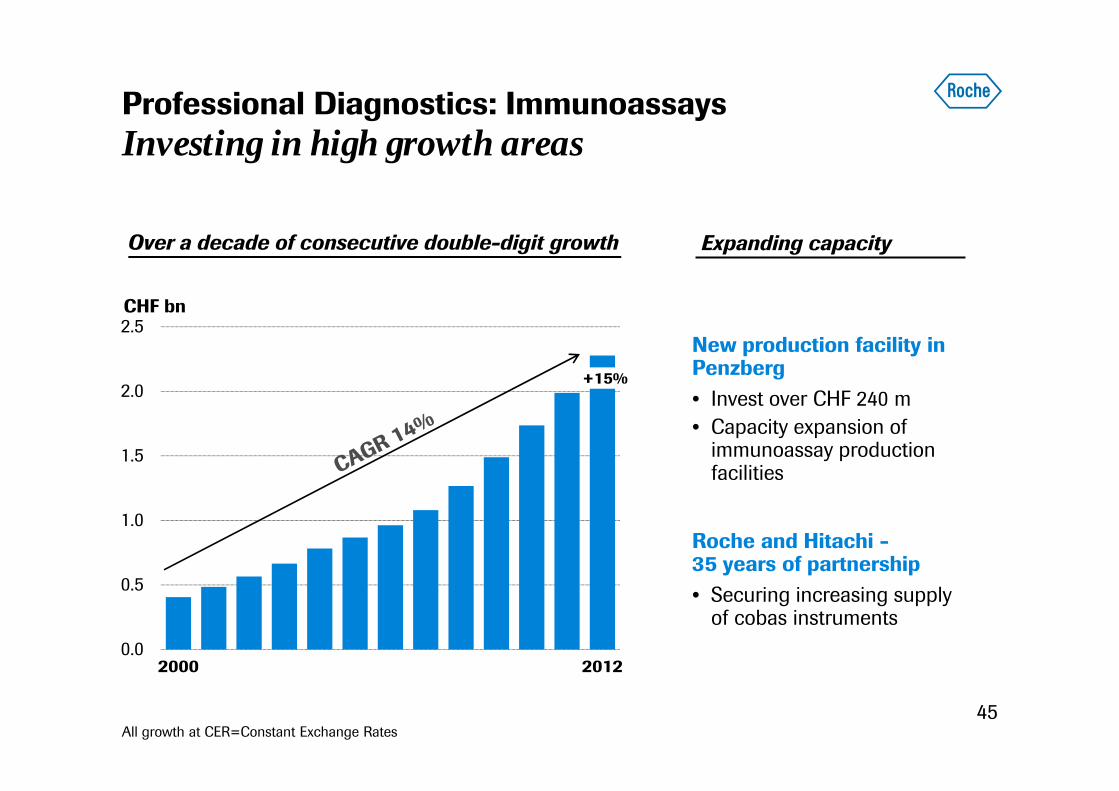

Professional Diagnostics: ImmunoassaysInvesting in high growth areas

45

0.0

0.5

1.0

1.5

2.0

2.5

2000 2012

+15%

New production facility in Penzberg• Invest over CHF 240 m • Capacity expansion of

immunoassay production facilities

Over a decade of consecutive double-digit growth

CHF bn

Roche and Hitachi -35 years of partnership• Securing increasing supply

of cobas instruments

Expanding capacity

All growth at CER=Constant Exchange Rates

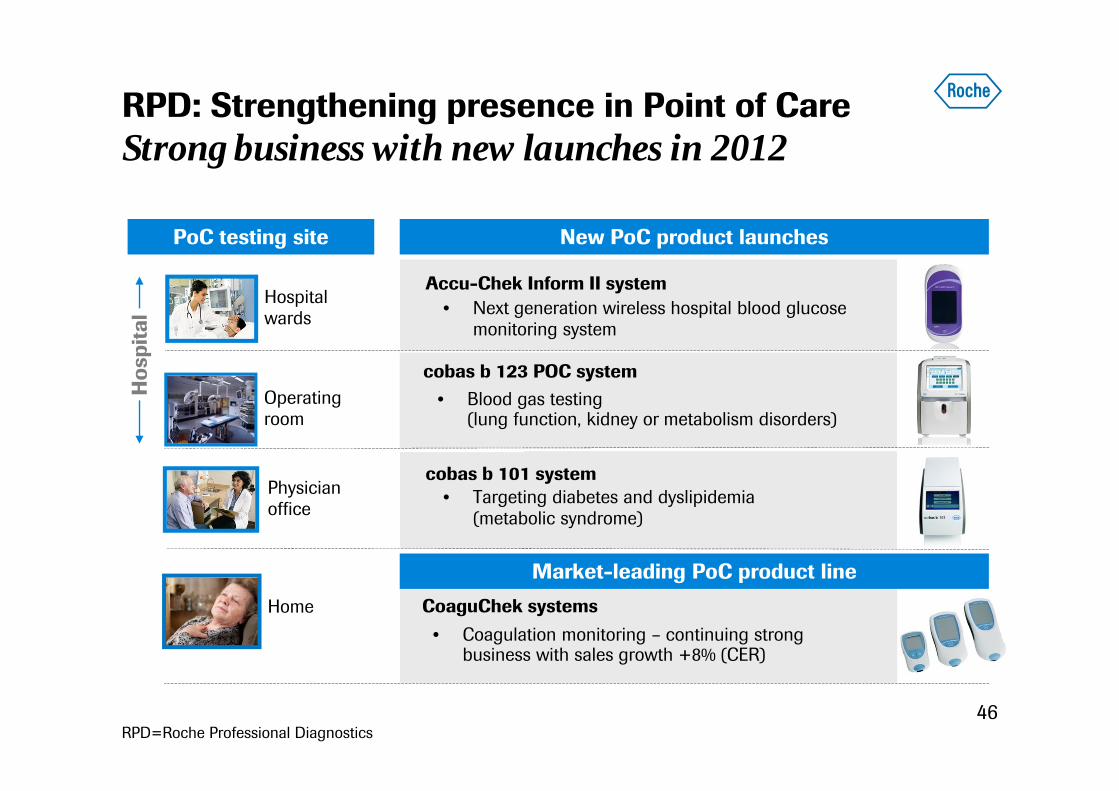

RPD: Strengthening presence in Point of CareStrong business with new launches in 2012

46

Operating room

Hospital wards

Hos

pita

l

Home

Accu-Chek Inform II system

cobas b 123 POC system

• Next generation wireless hospital blood glucosemonitoring system

• Blood gas testing (lung function, kidney or metabolism disorders)

New PoC product launchesPoC testing site

Market-leading PoC product line

• Coagulation monitoring – continuing strong business with sales growth +8% (CER)

CoaguChek systems

RPD=Roche Professional Diagnostics

Physician office

• Targeting diabetes and dyslipidemia(metabolic syndrome)

cobas b 101 system

47

2012: Professional Diagnostics main growth driver

Refining Diabetes Care and Applied Science

Companion Diagnostics

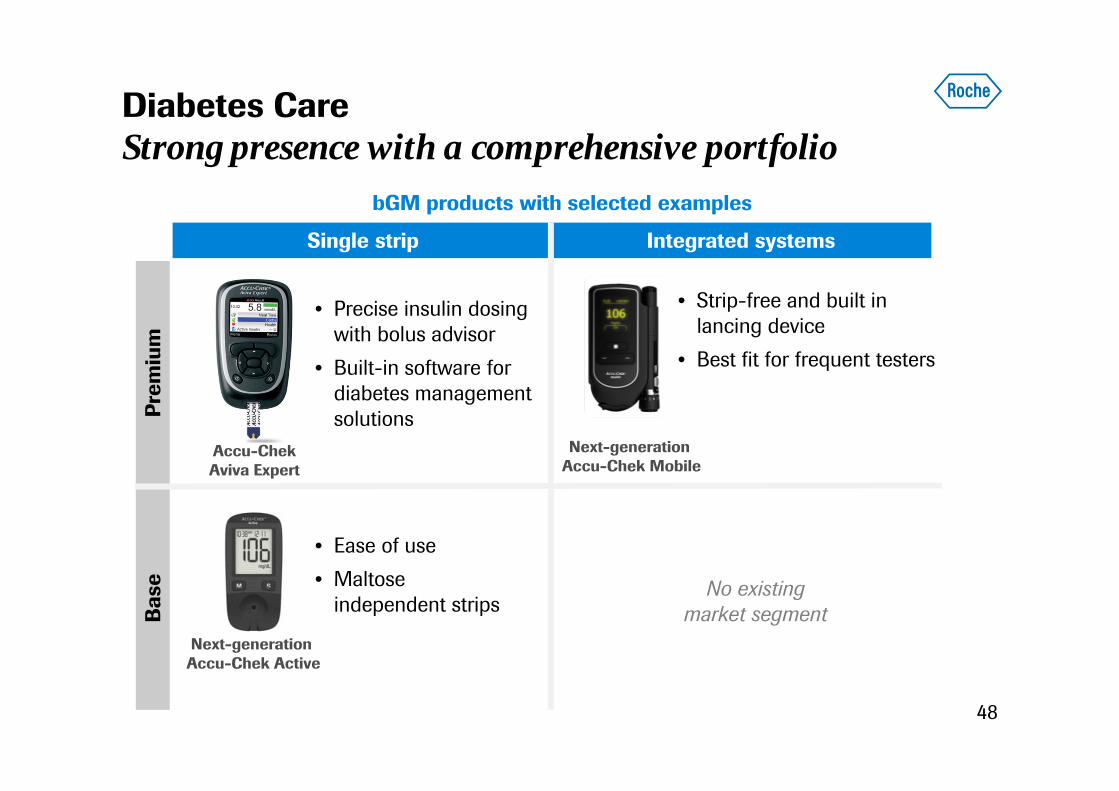

Diabetes CareStrong presence with a comprehensive portfolio

48

Next-generation Accu-Chek Mobile

Next-generation Accu-Chek Active

Integrated systems

Prem

ium

Single strip

bGM products with selected examples

Bas

e

• Strip-free and built in lancing device

• Best fit for frequent testers

No existing market segment

• Ease of use• Maltose

independent strips

• Precise insulin dosing with bolus advisor

• Built-in software for diabetes management solutions

Accu-ChekAviva Expert

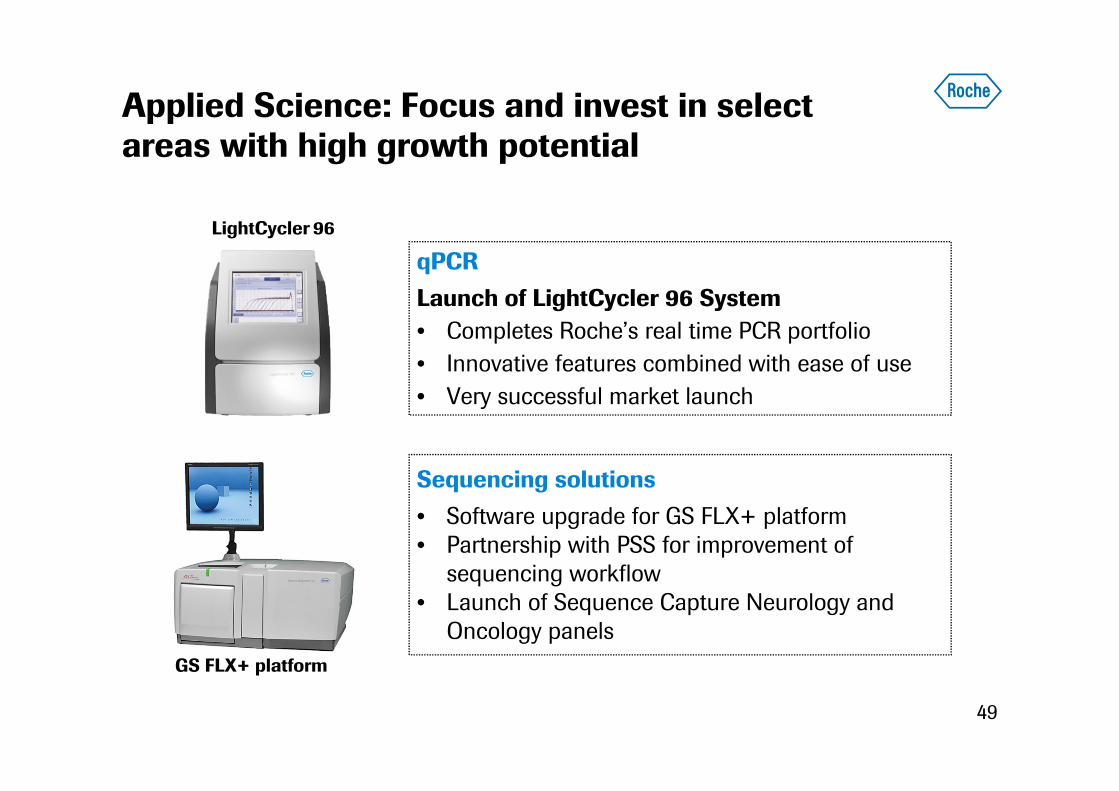

Applied Science: Focus and invest in selectareas with high growth potential

49

qPCRLaunch of LightCycler 96 System • Completes Roche’s real time PCR portfolio• Innovative features combined with ease of use• Very successful market launch

Sequencing solutions• Software upgrade for GS FLX+ platform • Partnership with PSS for improvement of

sequencing workflow• Launch of Sequence Capture Neurology and

Oncology panels

LightCycler 96

GS FLX+ platform

50

2012: Professional Diagnostics main growth driver

Refining Diabetes Care and Applied Science

Companion Diagnostics

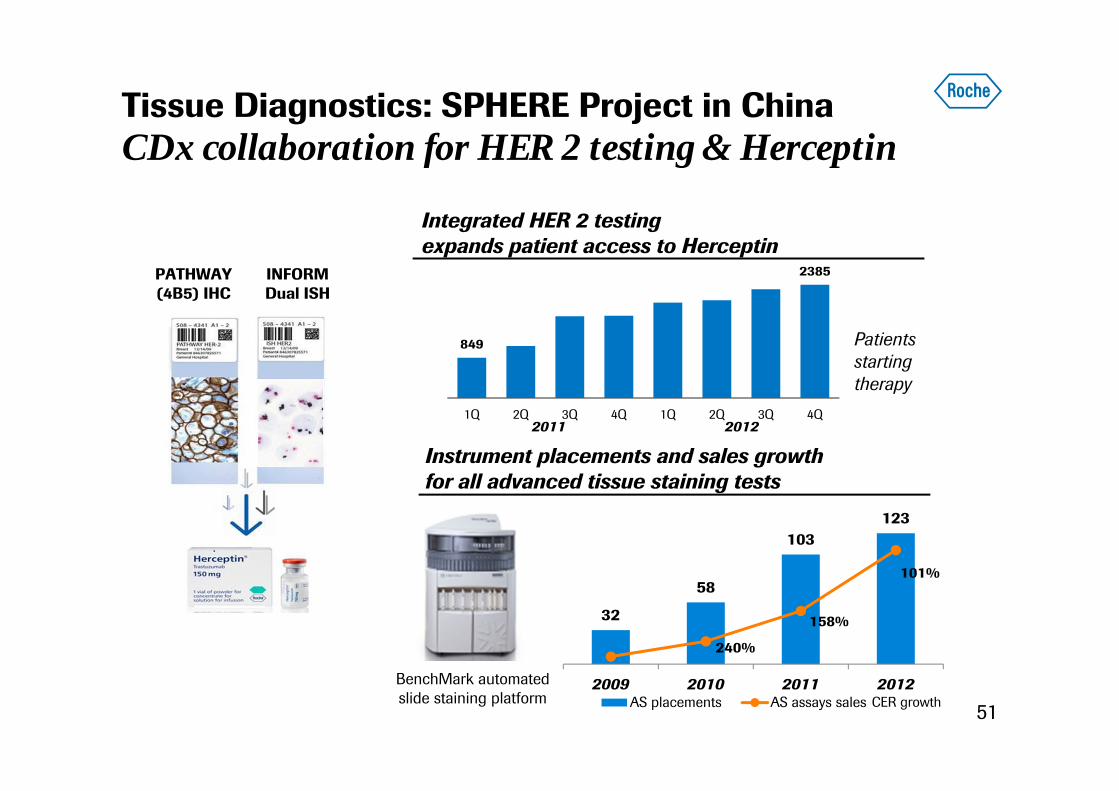

Tissue Diagnostics: SPHERE Project in ChinaCDx collaboration for HER 2 testing & Herceptin

51

PATHWAY (4B5) IHC

INFORM Dual ISH

BenchMark automatedslide staining platform CER growth

20122011

849

2385

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

Instrument placements and sales growthfor all advanced tissue staining tests

Integrated HER 2 testingexpands patient access to Herceptin

Patients starting therapy

32

58

103123

240%

158%

101%

2009 2010 2011 2012AS placements AS assays sales

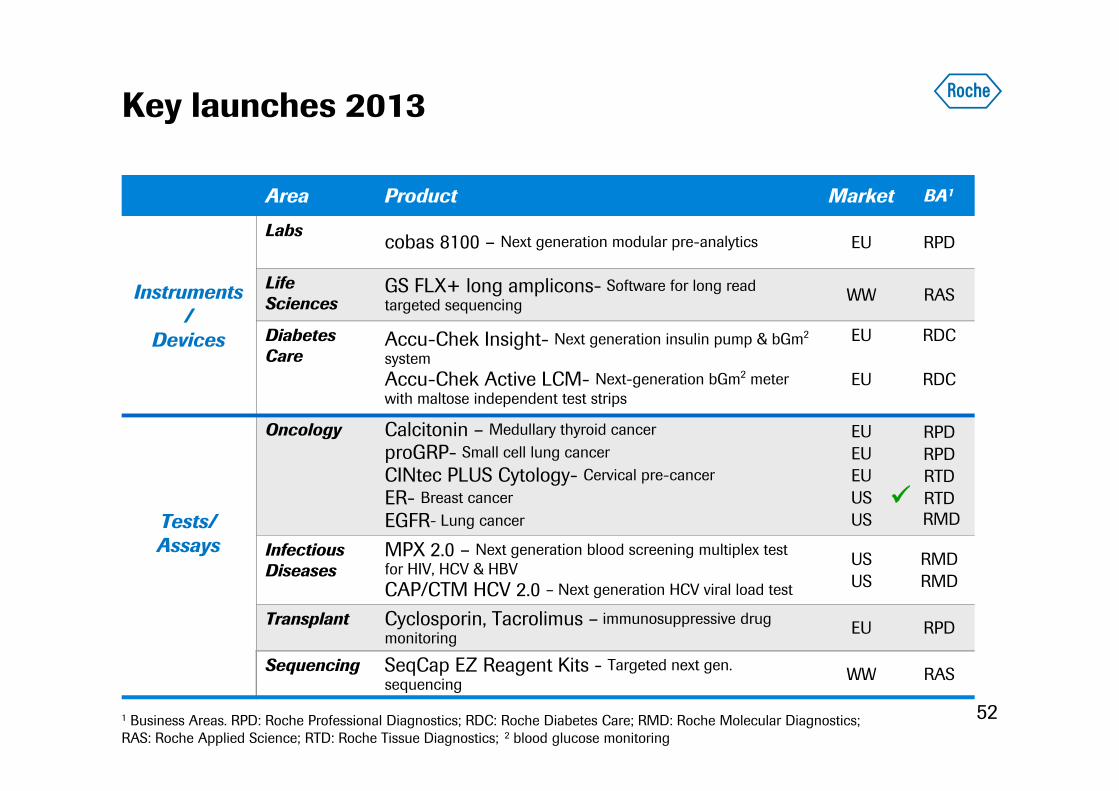

Key launches 2013

52

Area Product Market BA1

Instruments/

Devices

Labs cobas 8100 – Next generation modular pre-analytics EU RPD

Life Sciences

GS FLX+ long amplicons- Software for long read targeted sequencing WW RAS

Diabetes Care

Accu-Chek Insight- Next generation insulin pump & bGm2

systemAccu-Chek Active LCM- Next-generation bGm2 meter with maltose independent test strips

EU

EU

RDC

RDC

Tests/Assays

Oncology Calcitonin – Medullary thyroid cancerproGRP- Small cell lung cancerCINtec PLUS Cytology- Cervical pre-cancerER- Breast cancerEGFR- Lung cancer

EUEUEUUS US

RPDRPDRTDRTDRMD

Infectious Diseases

MPX 2.0 – Next generation blood screening multiplex test for HIV, HCV & HBVCAP/CTM HCV 2.0 – Next generation HCV viral load test

USUS

RMDRMD

Transplant Cyclosporin, Tacrolimus – immunosuppressive drug monitoring EU RPD

Sequencing SeqCap EZ Reagent Kits - Targeted next gen. sequencing WW RAS

1 Business Areas. RPD: Roche Professional Diagnostics; RDC: Roche Diabetes Care; RMD: Roche Molecular Diagnostics;RAS: Roche Applied Science; RTD: Roche Tissue Diagnostics; 2 blood glucose monitoring

OutlookSustained sales growth driven by leading IVD business

53

Drivers

• Further growth of installed base • Expansion of test menu• Emerging markets• Stabilise Diabetes Care• Increasing CDx collaborations

54

GroupAlan HippeChief Financial Officer

55

2012: Continued strong profit growth

Deleveraging

Focus on cash

Outlook

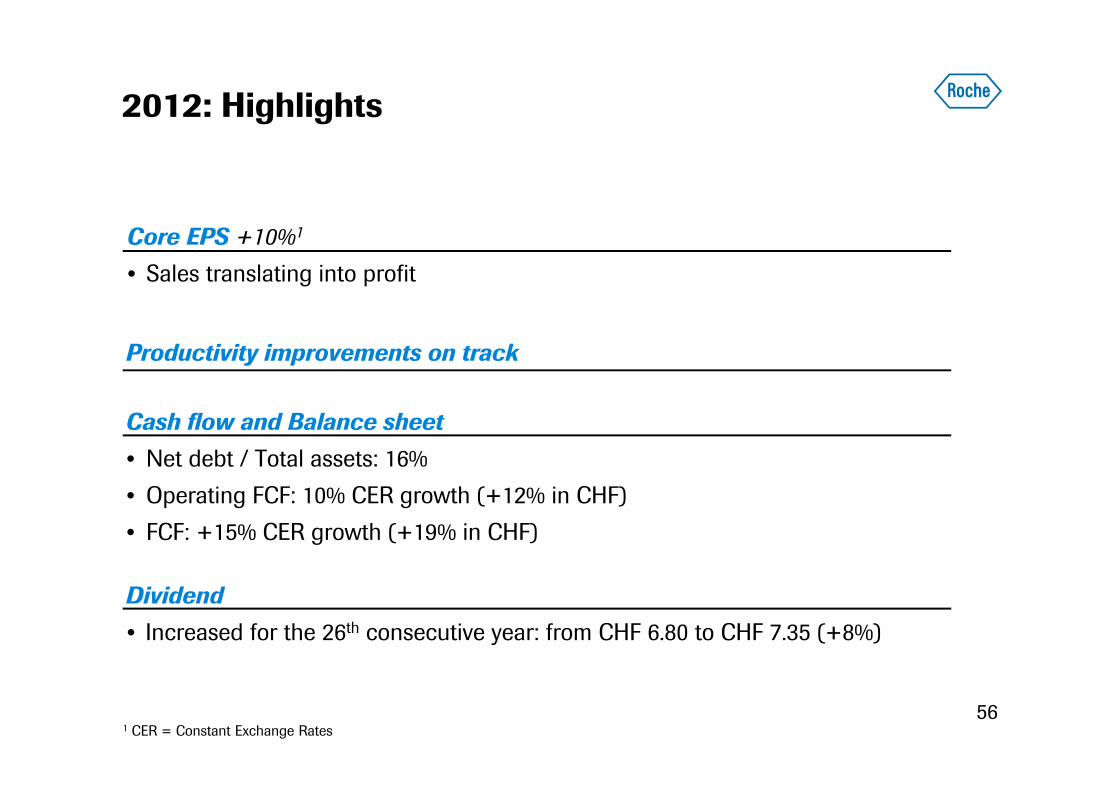

2012: Highlights

56

Core EPS +10%1

• Sales translating into profit

Productivity improvements on track

Cash flow and Balance sheet• Net debt / Total assets: 16%• Operating FCF: 10% CER growth (+12% in CHF)• FCF: +15% CER growth (+19% in CHF)

1 CER = Constant Exchange Rates

Dividend• Increased for the 26th consecutive year: from CHF 6.80 to CHF 7.35 (+8%)

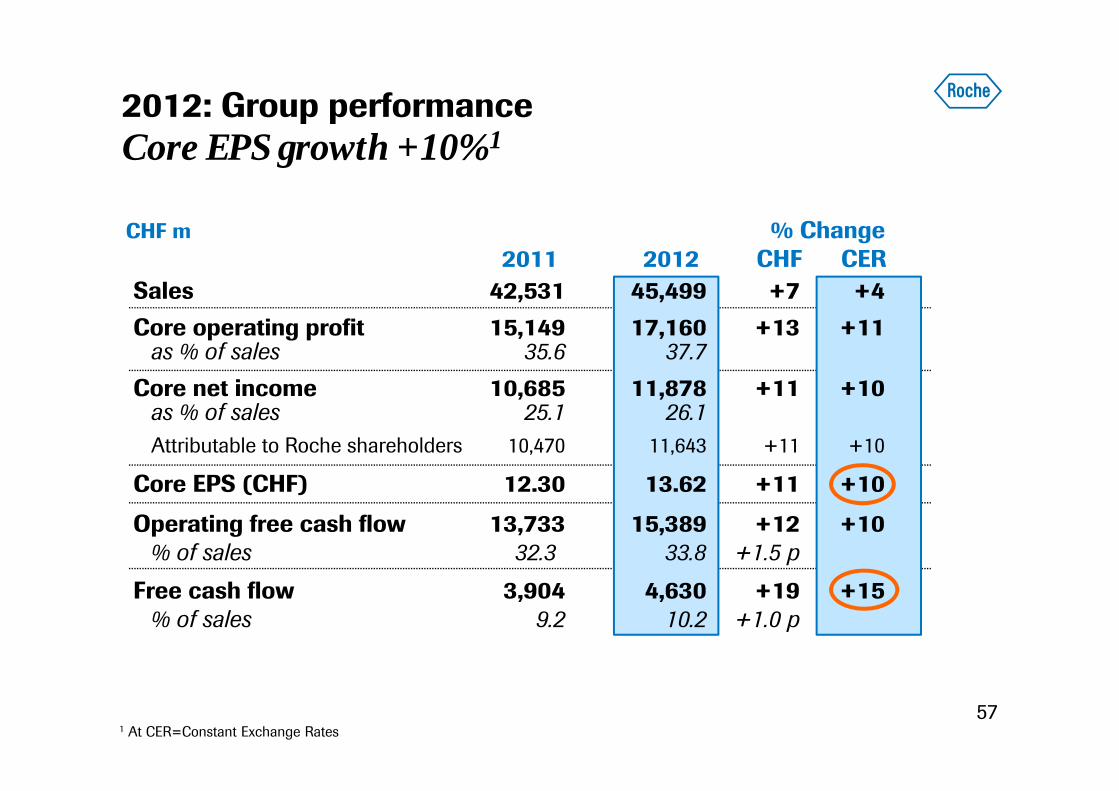

Sales 42,531 45,499 +7 +4Core operating profit 15,149 17,160 +13 +11

as % of sales 35.6 37.7Core net income 10,685 11,878 +11 +10

as % of sales 25.1 26.1Attributable to Roche shareholders 10,470 11,643 +11 +10

Core EPS (CHF) 12.30 13.62 +11 +10

Operating free cash flow 13,733 15,389 +12 +10% of sales 32.3 33.8 +1.5 p

Free cash flow 3,904 4,630 +19 +15% of sales 9.2 10.2 +1.0 p

2012: Group performance Core EPS growth +10%1

57

CHF m % Change2011 2012 CHF CER

1 At CER=Constant Exchange Rates

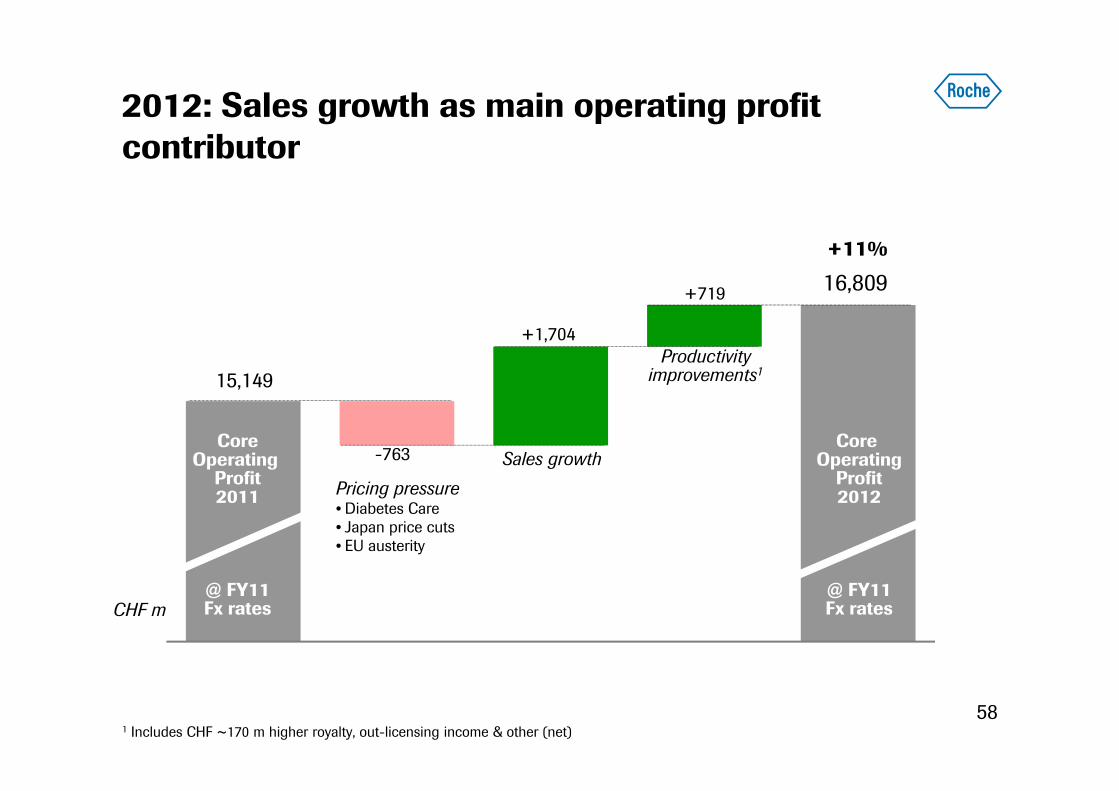

15,149

16,809

-763

+1,704Productivity

improvements1

Sales growthCore

OperatingProfit2012

@ FY11Fx rates

CoreOperating

Profit2011

@ FY11Fx rates

Pricing pressure• Diabetes Care• Japan price cuts• EU austerity

+11%

+719

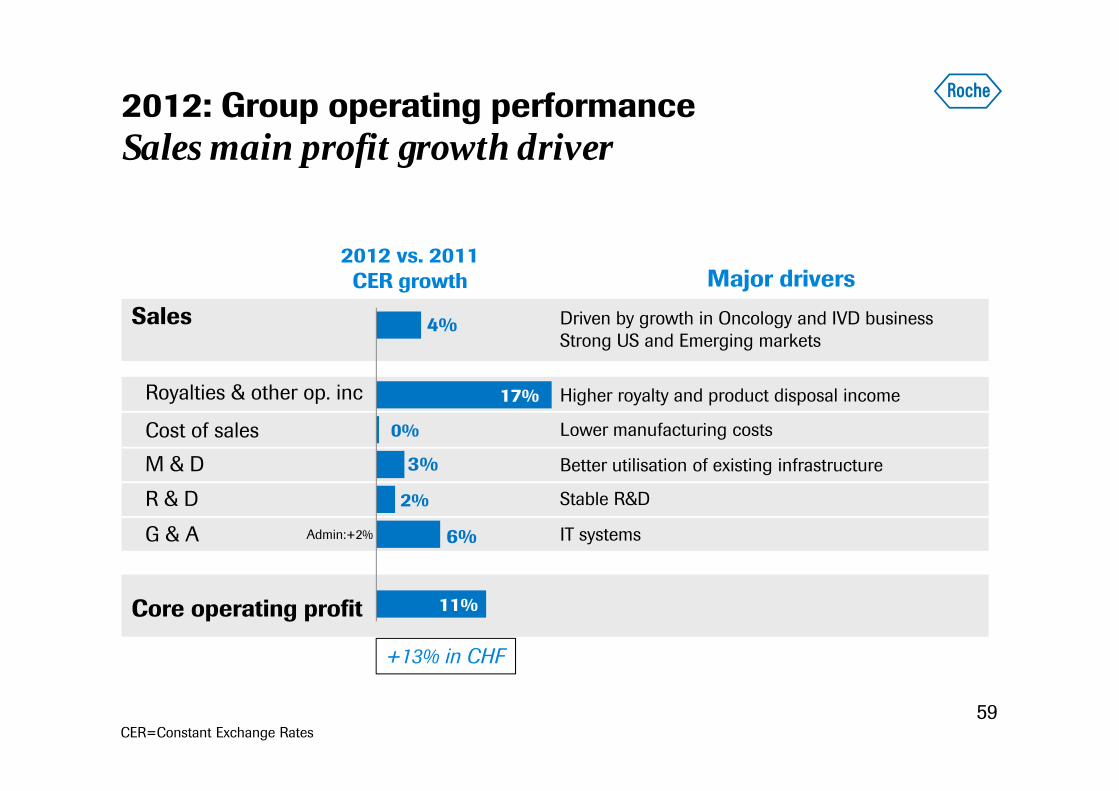

2012: Sales growth as main operating profit contributor

58

CHF m

1 Includes CHF ~170 m higher royalty, out-licensing income & other (net)

11%

6%

2%

3%

0%

17%

4%

2012: Group operating performance Sales main profit growth driver

59

+13% in CHF

Higher royalty and product disposal income

Lower manufacturing costs

Better utilisation of existing infrastructure

Stable R&D

IT systems

Major driversSales

Royalties & other op. inc

Cost of salesM & D

R & D

G & A

Core operating profit

2012 vs. 2011CER growth

Driven by growth in Oncology and IVD businessStrong US and Emerging markets

CER=Constant Exchange Rates

Admin:+2%

16,59114,776

2,202

15,14913,406

2,178

17,16015,488

2,187

Roche Group Pharma Division Diagnostics Division

34.9% 35.6% 37.7% 39.9% 40.9% 44.0%

21.1% 22.4% 21.3%

2012: Core operating profit and marginStrong margin increase led by Pharma

60

CHF m % of sales

+2.2 %p1

(+2.1 %p)

-1.4 %p1

(-1.1 %p)

+3.4 %p1

(+3.1 %p)

-2 %1

(0 %)

+13 %1

(+16 %)

+11 %1

(+13 %)

2011 20122010

1 At CER=Constant Exchange Rates CER

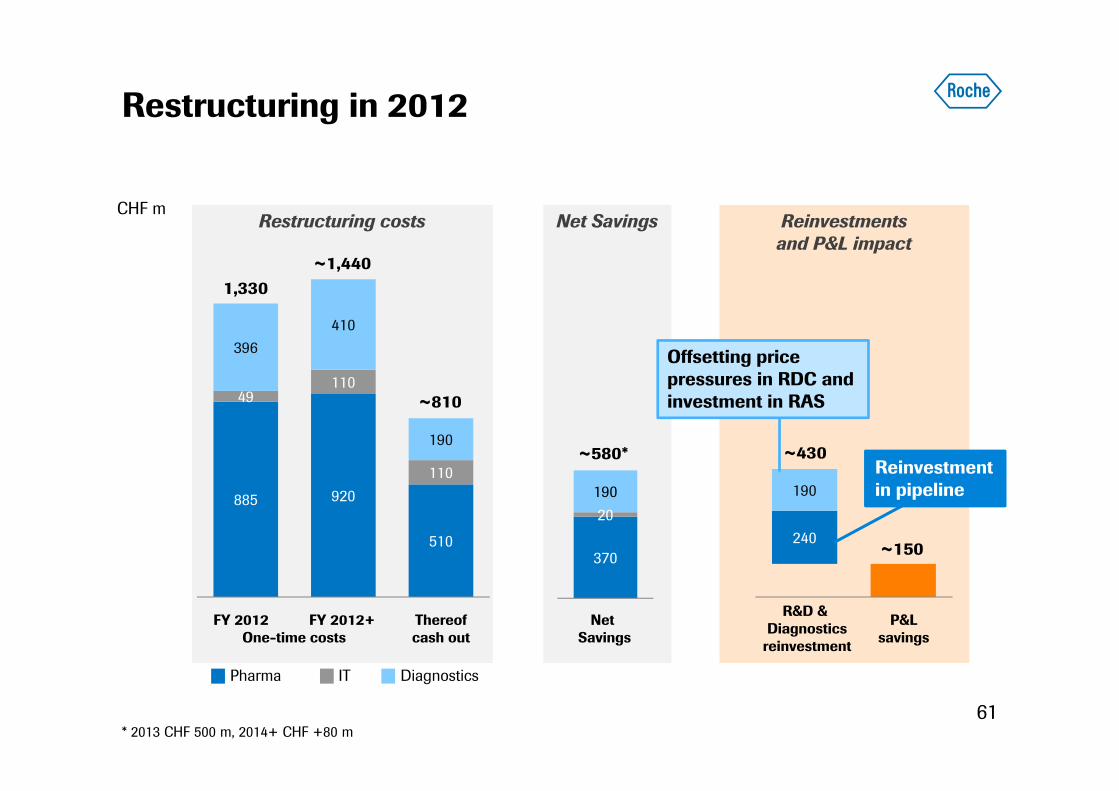

Restructuring in 2012

61

Reinvestments and P&L impact

Net SavingsRestructuring costs

885 920

510

49110

110

396410

190

~1,440

~810

Thereof cash out

Net Savings

FY 2012 FY 2012+One-time costs

CHF m

240

190

DiagnosticsPharma IT

R&D & Diagnostics

reinvestment

P&Lsavings

~430

~150370

20190

~580*

1,330

Offsetting price pressures in RDC and investment in RAS

Reinvestment in pipeline

* 2013 CHF 500 m, 2014+ CHF +80 m

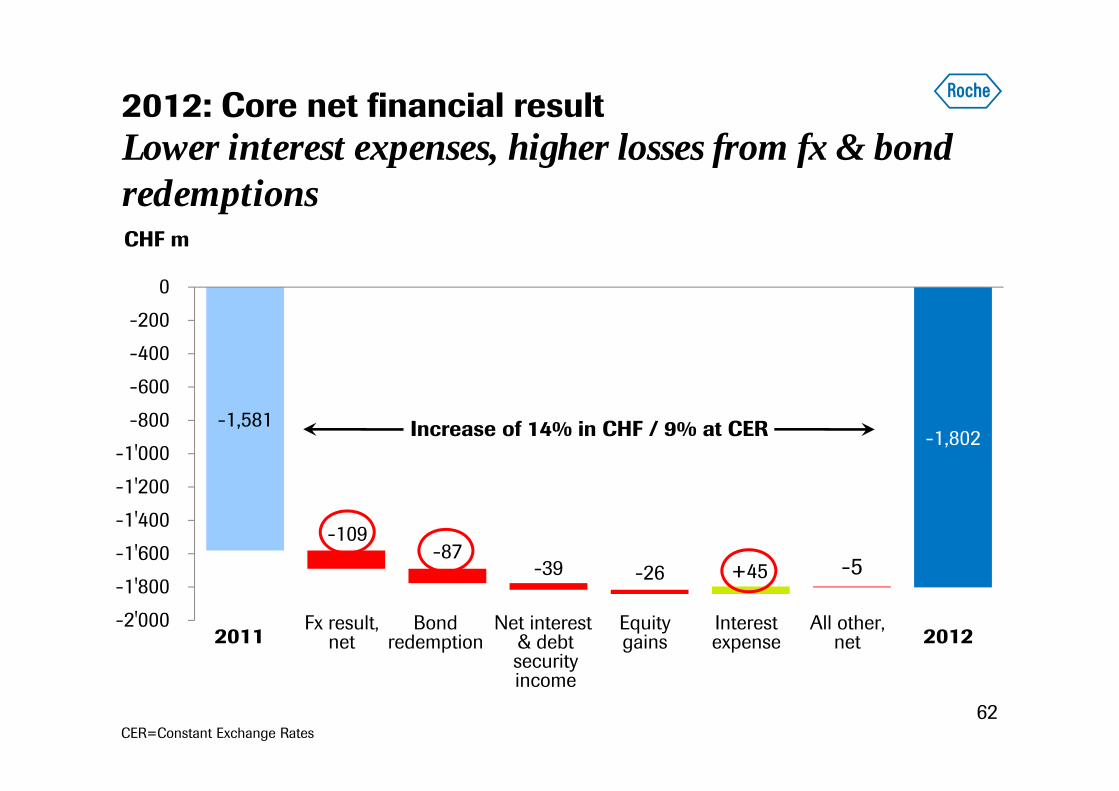

2012: Core net financial resultLower interest expenses, higher losses from fx & bond redemptions

62

-1,581 -1,581 -1,690 -1,777 -1,816 -1,797 -1,797 -1,802

-109-87

-39 -26 +45 -5

-2'000-1'800-1'600-1'400-1'200-1'000

-800-600-400-200

0

CHF m

Net interest & debtsecurityincome

Bondredemption2011 2012

Interestexpense

Fx result,net

CER=Constant Exchange Rates

All other,net

Equitygains

Increase of 14% in CHF / 9% at CER

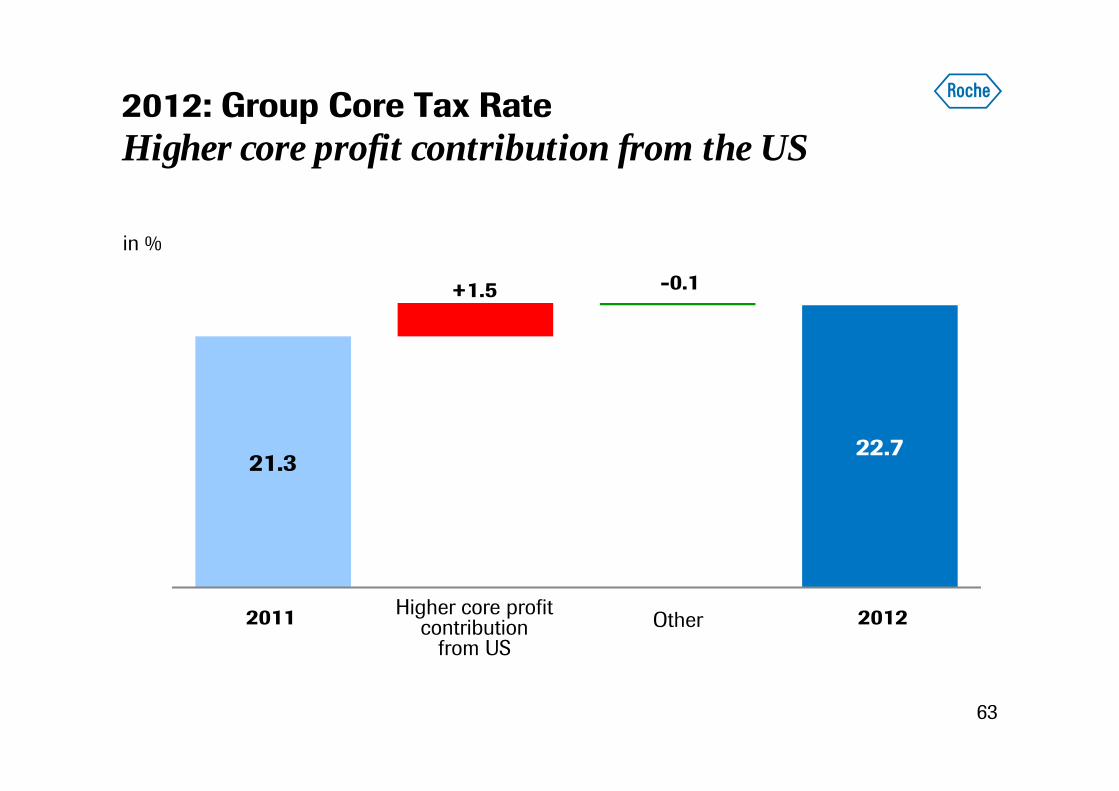

21.3 ,21.3,22.7 22.7

+1.5 -0.1

in %

Other2011 2012Higher core profit contribution

from US

2012: Group Core Tax Rate Higher core profit contribution from the US

63

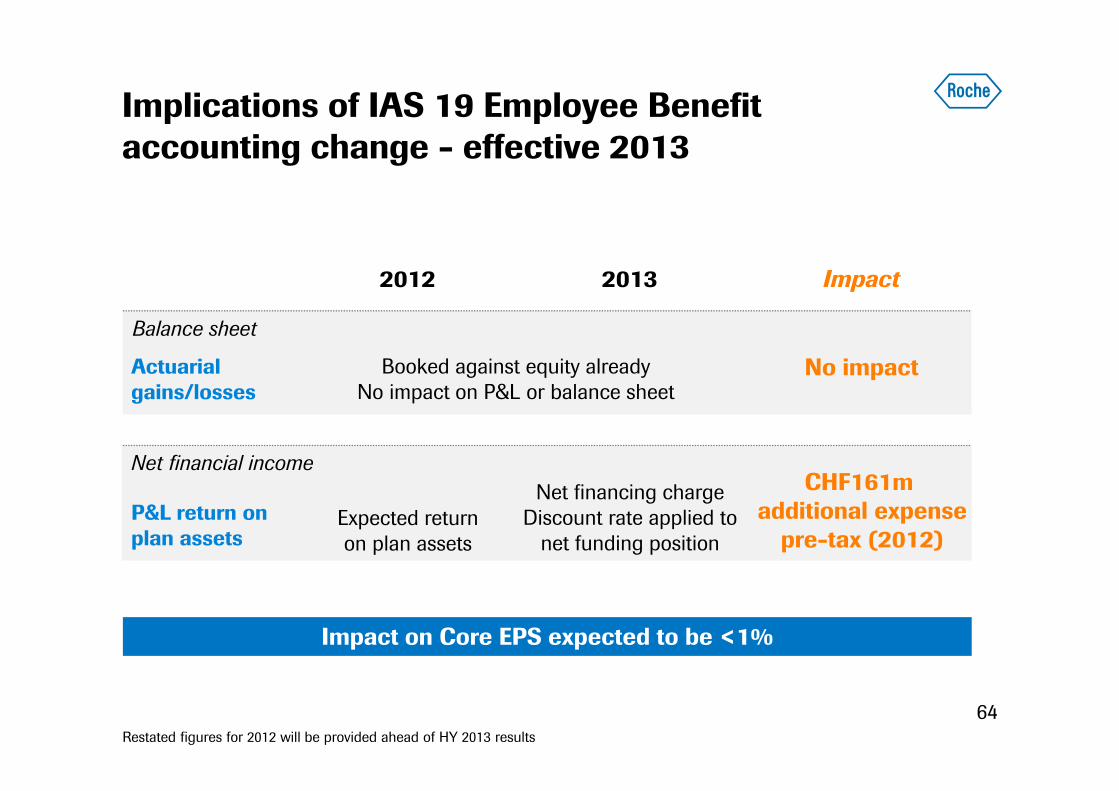

Implications of IAS 19 Employee Benefit accounting change - effective 2013

64

Balance sheet

Net financial income

2012 2013

Actuarialgains/losses

P&L return on plan assets

Booked against equity alreadyNo impact on P&L or balance sheet

Expected return on plan assets

Net financing chargeDiscount rate applied to

net funding position

Impact

No impact

Impact on Core EPS expected to be <1%

CHF161m additional expense

pre-tax (2012)

Restated figures for 2012 will be provided ahead of HY 2013 results

65

2012: Continued strong profit growth

Deleveraging

Focus on cash

Outlook

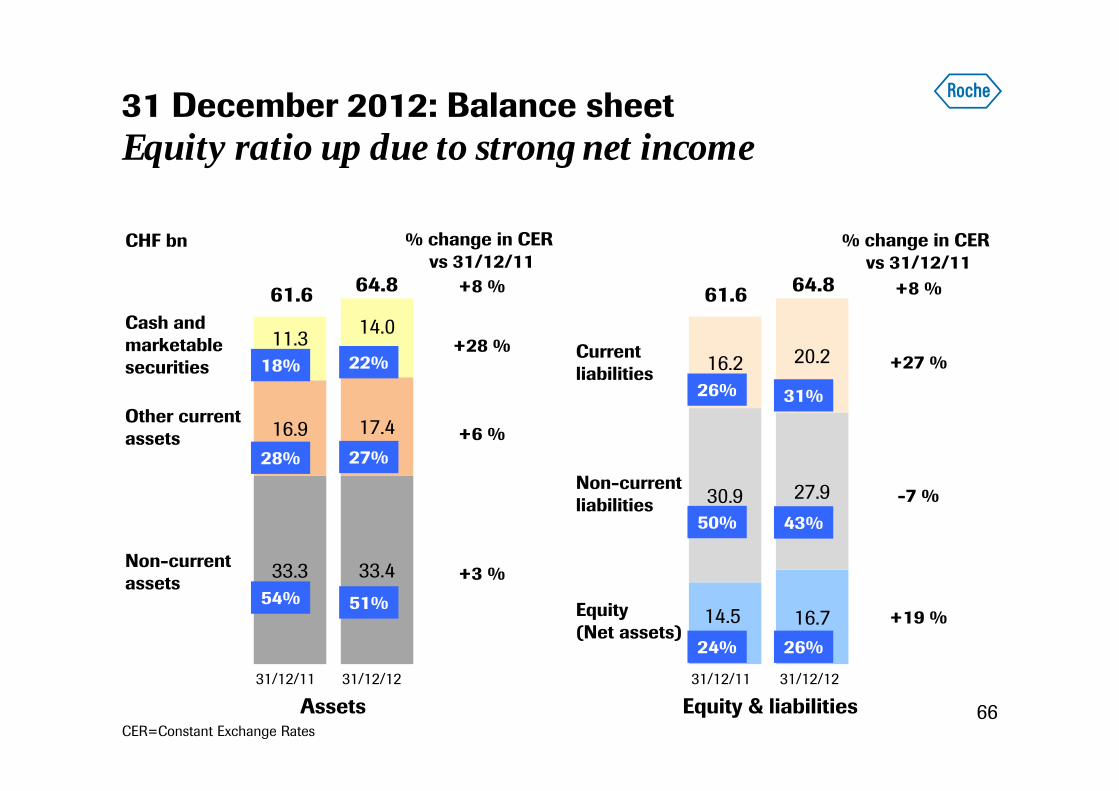

31 December 2012: Balance sheetEquity ratio up due to strong net income

66

33.3 33.4

16.9 17.4

11.3 14.0

14.5 16.7

30.9 27.9

16.2 20.2

Non-currentassets

Assets Equity & liabilities

Non-currentliabilities

Equity(Net assets)

Other currentassets

Cash andmarketablesecurities

Currentliabilities

CHF bn

64.8 64.861.6

24% 26%

54%

28%

18%

51%

27%

22%

50% 43%

26% 31%

61.6

31/12/11 31/12/12 31/12/11 31/12/12

+28 %

+6 %

+3 %

+27 %

-7 %

+19 %

+8 % +8 %

% change in CER vs 31/12/11

% change in CER vs 31/12/11

CER=Constant Exchange Rates

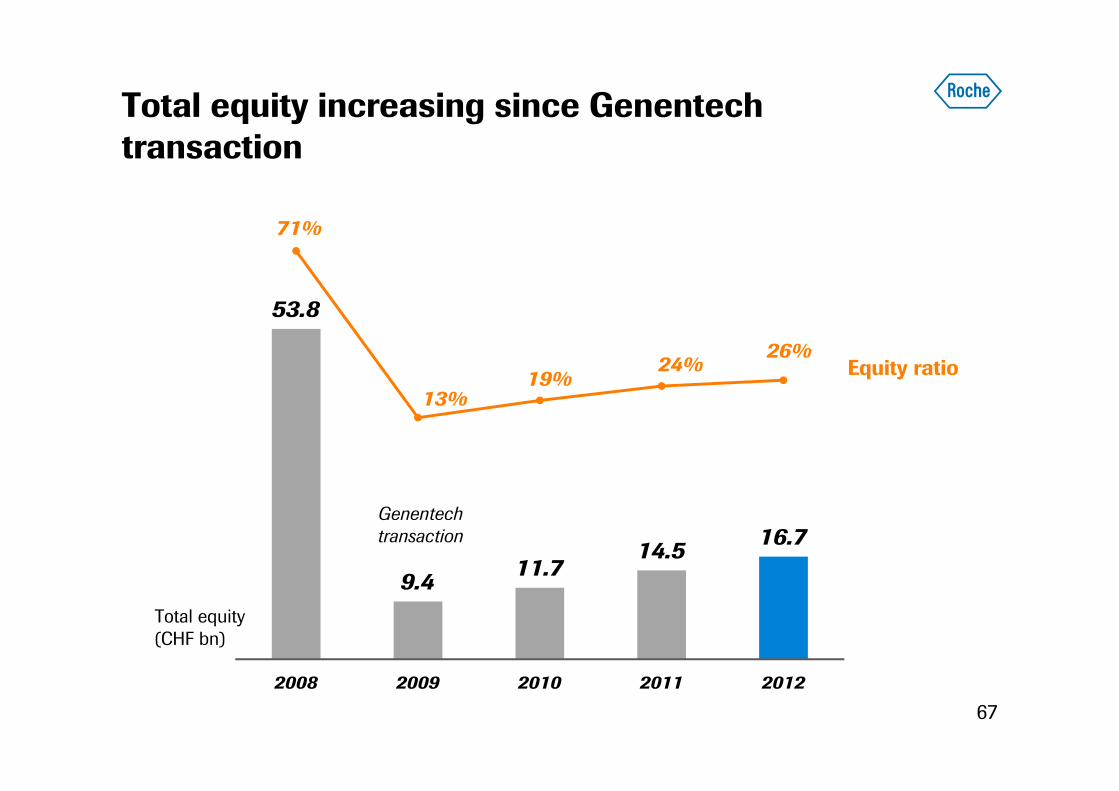

Total equity increasing since Genentech transaction

67

53.8

9.4 11.714.5 16.7

2008 2009 2010 2011 2012

Genentechtransaction

71%

13%19%

24%26%

Total equity(CHF bn)

Equity ratio

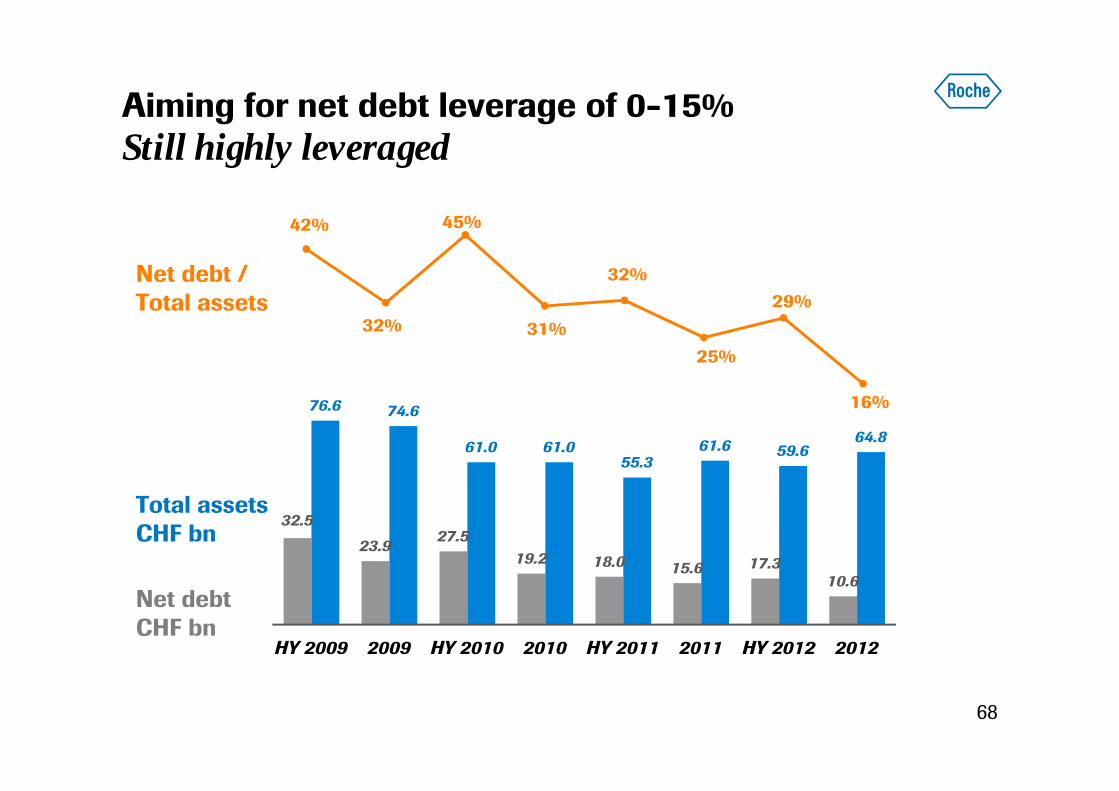

Aiming for net debt leverage of 0-15%Still highly leveraged

68

32.5

23.9 27.519.2 18.0 15.6 17.3

10.6

76.6 74.6

61.0 61.055.3

61.6 59.664.8

HY 2009 2009 HY 2010 2010 HY 2011 2011 HY 2012 2012

Net debtCHF bn

Total assetsCHF bn

Net debt /Total assets

42%

32%

45%

31%

32%

25%

29%

16%

0

1

2

3

4

5

6

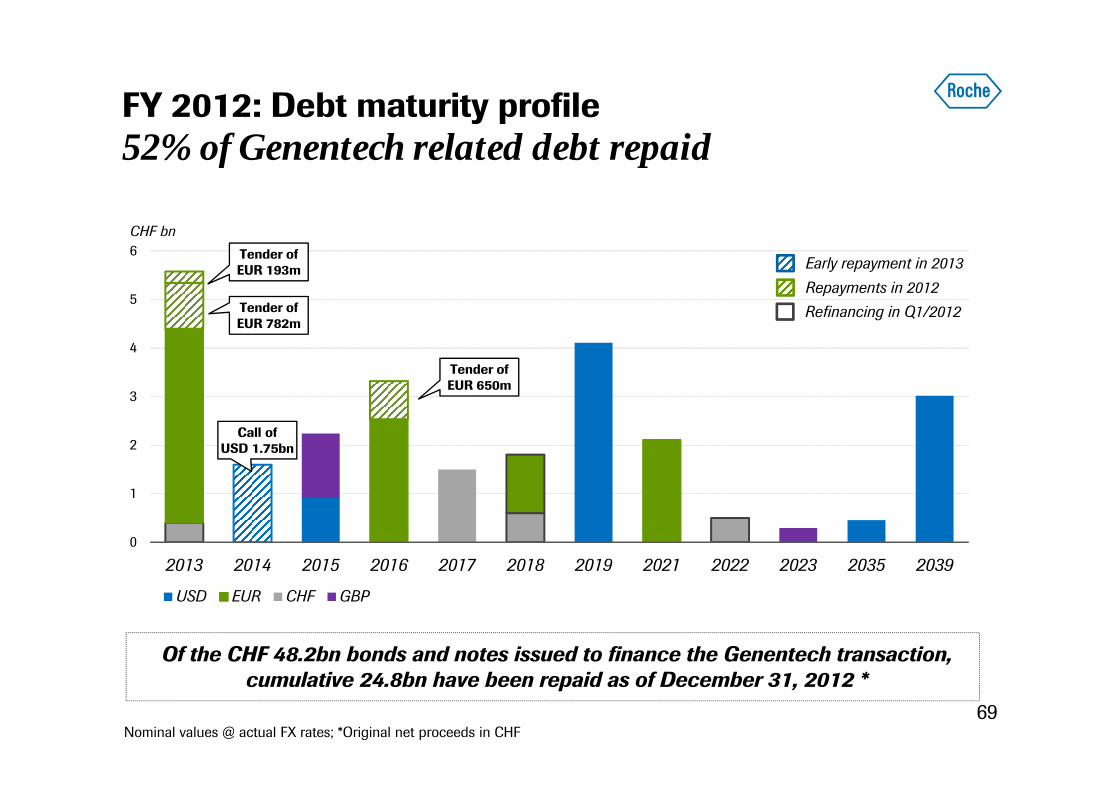

2013 2014 2015 2016 2017 2018 2019 2021 2022 2023 2035 2039

USD EUR CHF GBP

FY 2012: Debt maturity profile52% of Genentech related debt repaid

69Nominal values @ actual FX rates; *Original net proceeds in CHF

Of the CHF 48.2bn bonds and notes issued to finance the Genentech transaction, cumulative 24.8bn have been repaid as of December 31, 2012 *

CHF bn

Tender ofEUR 782m

Early repayment in 2013Repayments in 2012

Tender ofEUR 193m

Tender ofEUR 650m

Refinancing in Q1/2012

Call ofUSD 1.75bn

70

2012: Continued strong profit growth

Deleveraging

Focus on cash

Outlook

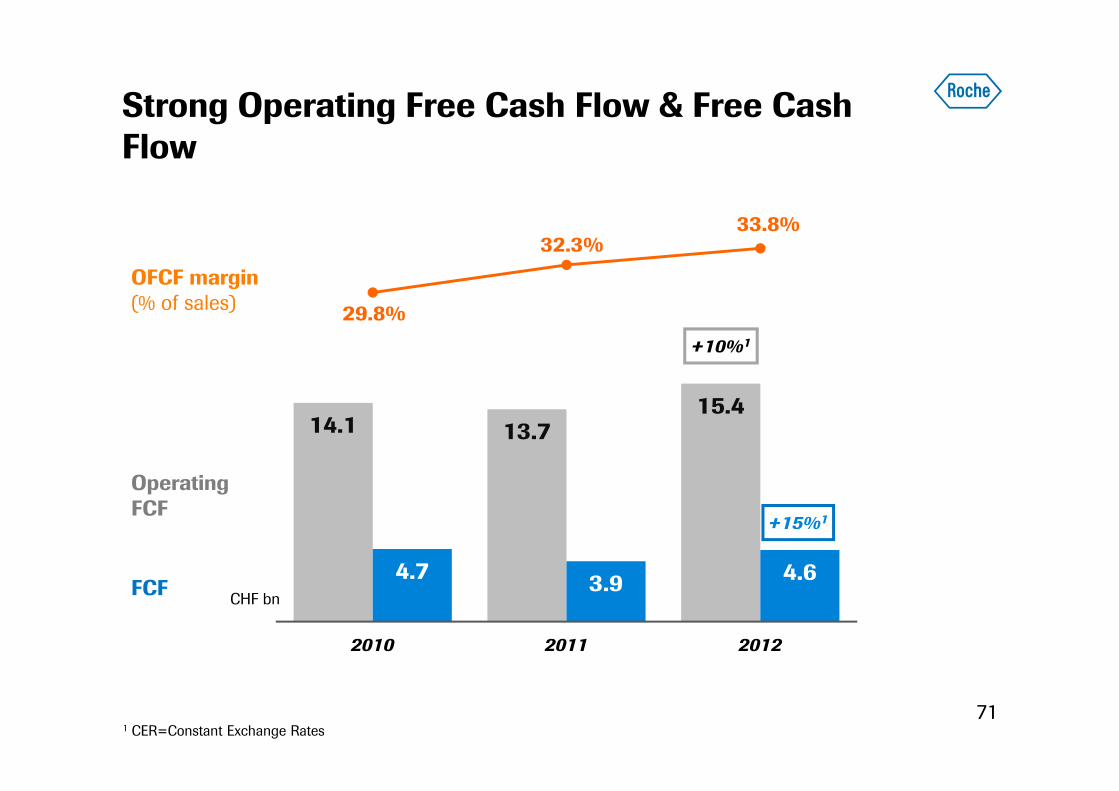

Strong Operating Free Cash Flow & Free Cash Flow

71

14.1 13.715.4

4.7 3.9 4.6

29.8%

32.3%33.8%

2010 2011 2012

+10%1

CHF bn

OFCF margin(% of sales)

1 CER=Constant Exchange Rates

OperatingFCF

FCF

+15%1

14,14912,933

1,634

13,733 12,914

1,259

15,38914,052

1,826

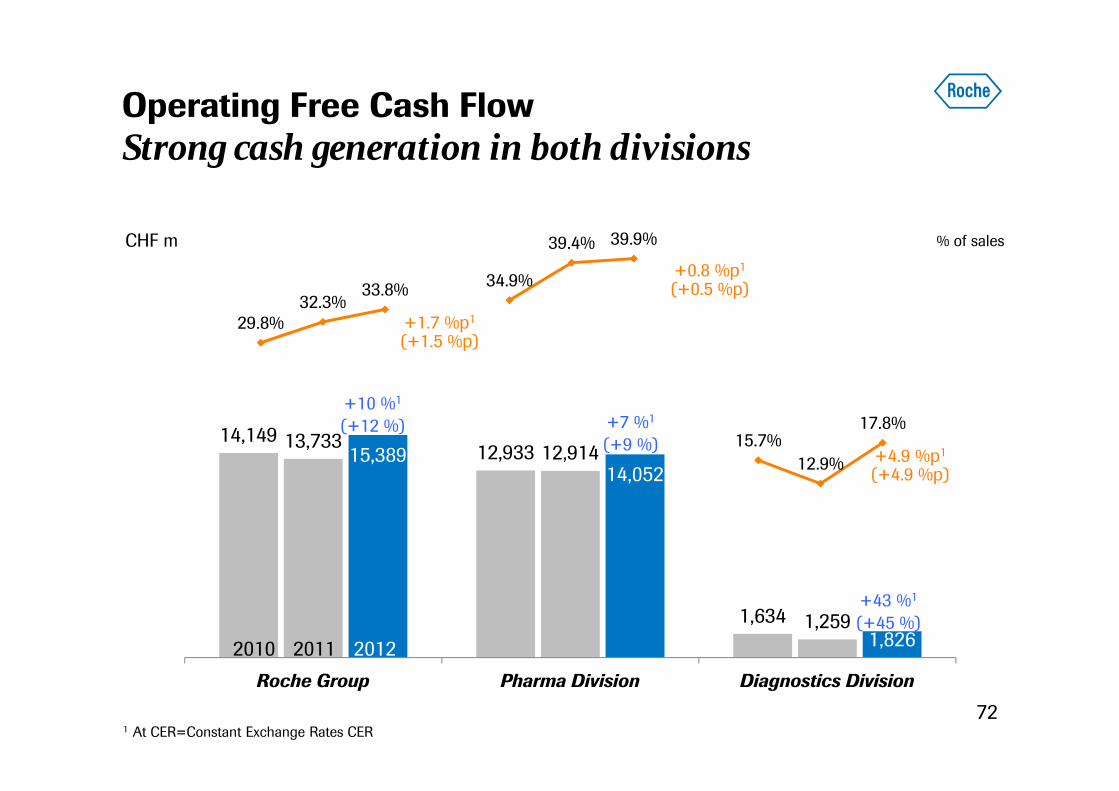

Roche Group Pharma Division Diagnostics Division

29.8%32.3%

33.8% 34.9%

39.4% 39.9%

15.7%12.9%

17.8%

Operating Free Cash FlowStrong cash generation in both divisions

72

% of sales

+4.9 %p1

(+4.9 %p)

+43 %1

(+45 %)

+7 %1

(+9 %)

+10 %1

(+12 %)

2011 20122010

1 At CER=Constant Exchange Rates CER

CHF m

+1.7 %p1

(+1.5 %p)

+0.8 %p1

(+0.5 %p)

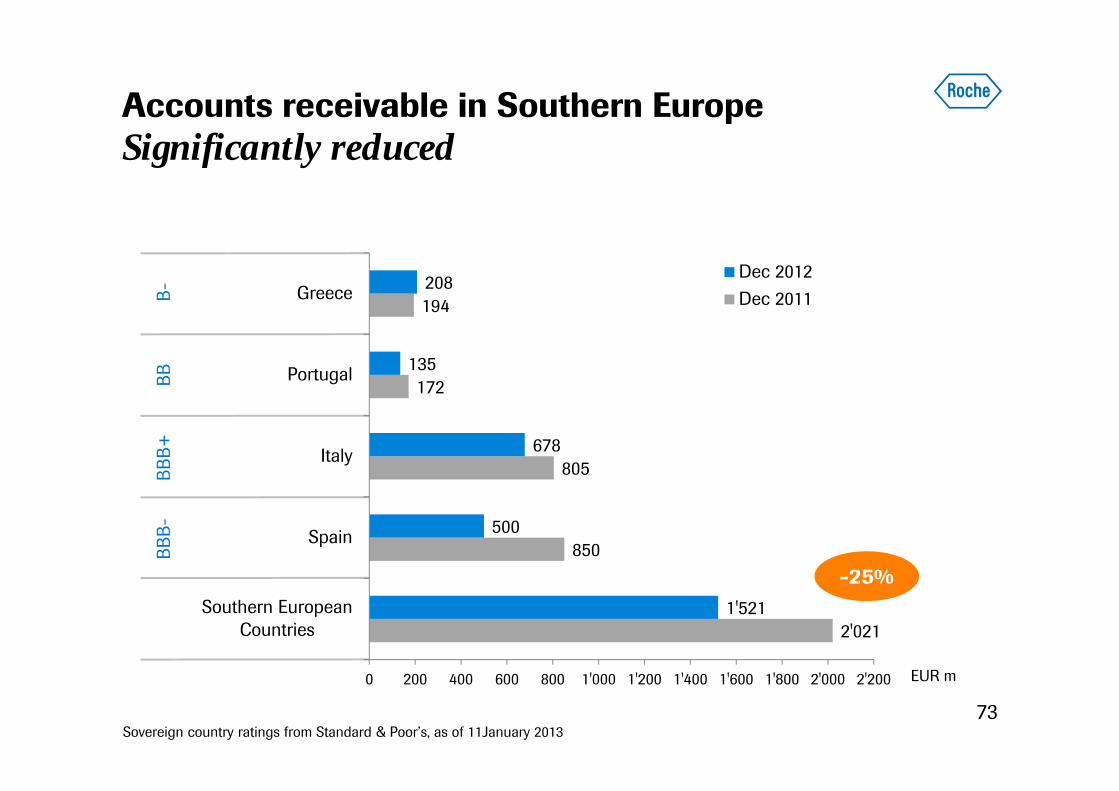

Accounts receivable in Southern EuropeSignificantly reduced

73

B-BB

BBB+

BBB-

EUR m

Sovereign country ratings from Standard & Poor’s, as of 11January 2013

2'021

850

805

172

194

1'521

500

678

135

208

0 200 400 600 800 1'000 1'200 1'400 1'600 1'800 2'000 2'200

Southern EuropeanCountries

Spain

Italy

Portugal

GreeceDec 2012Dec 2011

-25%

74

2012: Continued strong profit growth

Deleveraging

Focus on cash

Outlook

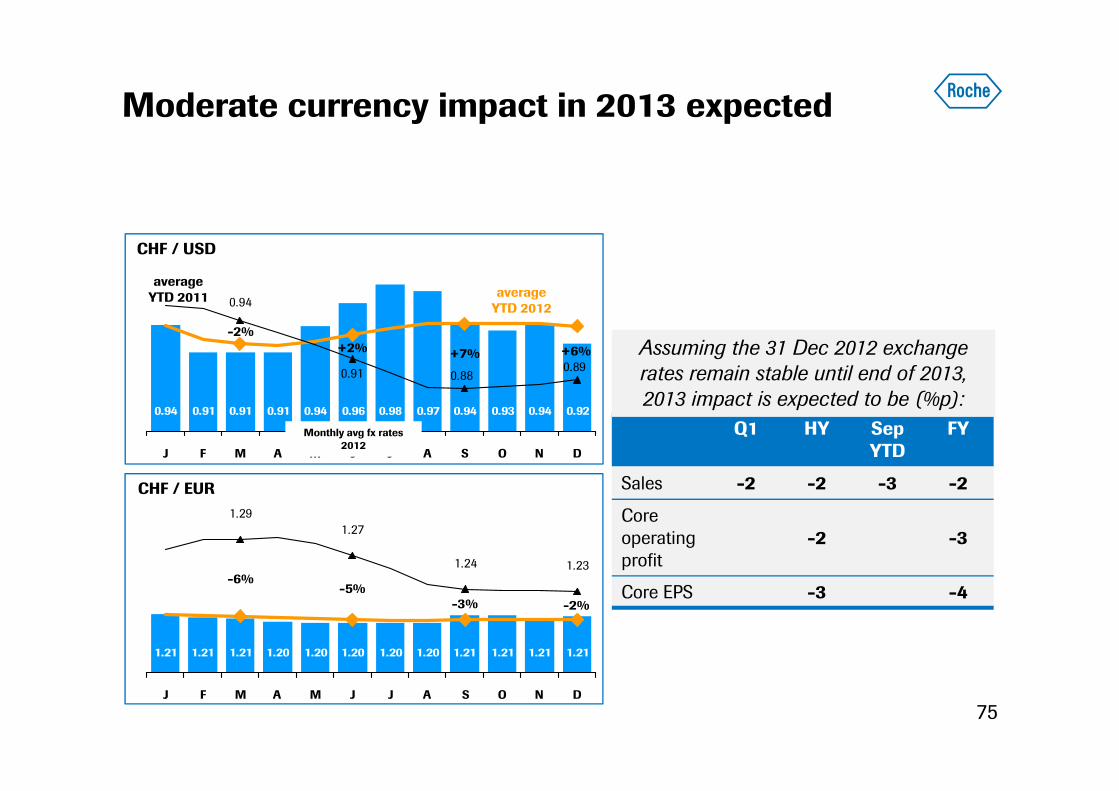

Moderate currency impact in 2013 expected

75

Q1 HY Sep YTD

FY

Sales -2 -2 -3 -2

Core operating profit

-2 -3

Core EPS -3 -4

Assuming the 31 Dec 2012 exchange rates remain stable until end of 2013, 2013 impact is expected to be (%p):

0.94 0.91 0.91 0.91 0.970.980.94 0.96 0.94 0.920.930.94

0.890.91 0.88

0.94

J F M A M J J A S O N D

CHF / USD

1.21 1.21 1.21 1.20 1.20 1.20 1.20 1.20 1.21 1.21 1.21 1.21

1.27

1.231.24

1.29

J F M A M J J A S O N D

CHF / EUR

averageYTD 2011

-2%+2% +7% +6%

-6%-5%

-3% -2%

averageYTD 2012

Monthly avg fx rates 2012

2013 Outlook

761At constant exchange rates

Group sales growth1 In line with sales growth recorded in 2012

Core EPS growth1 Ahead of sales growth

Dividend outlook Further increase dividend

77

7878

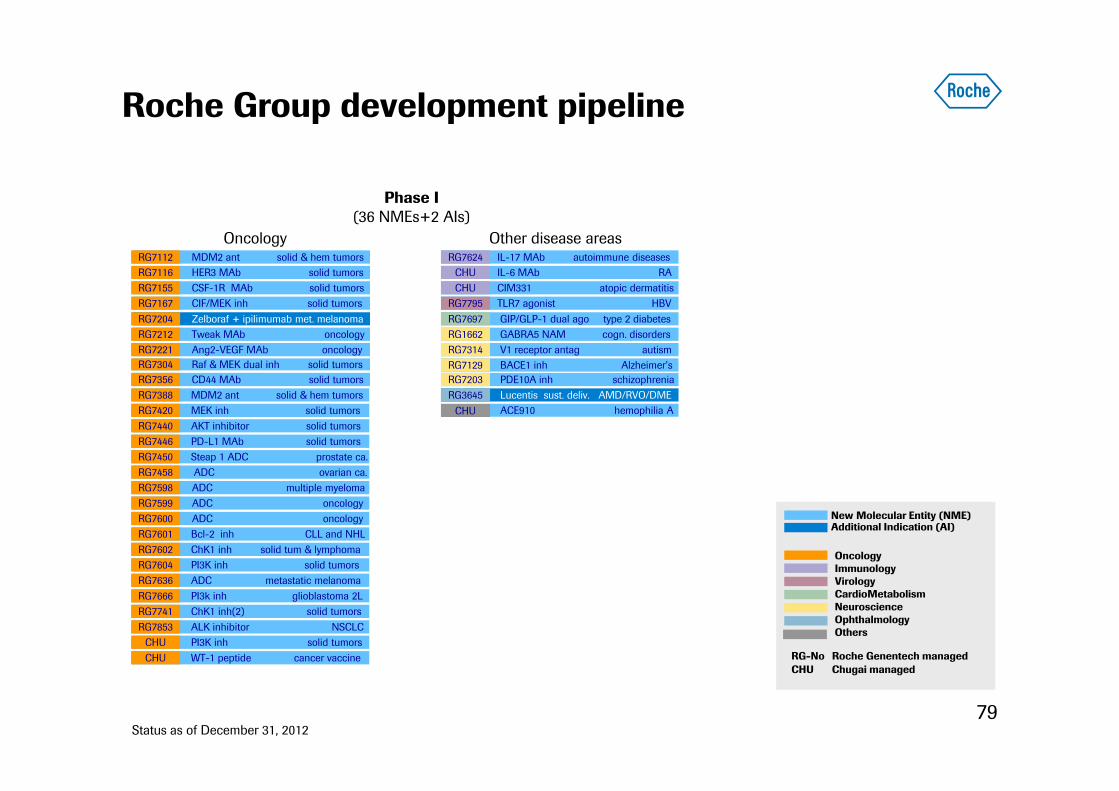

Roche Group development pipeline

Marketed products development programmes

Roche Pharma global development programmes

Roche Pharma research and early development

Genentech research and early development

Roche Group 2012 results

Diagnostics

Foreign exchange rate information

Phase I (36 NMEs+2 AIs)

CIF/MEK inh solid tumorsRG7167

Raf & MEK dual inh solid tumorsRG7304

PD-L1 MAb solid tumorsRG7446

BACE1 inh Alzheimer’s RG7129

GABRA5 NAM cogn. disordersRG1662

MEK inh solid tumorsRG7420AKT inhibitor solid tumorsRG7440

GIP/GLP-1 dual ago type 2 diabetesRG7697

PI3K inh solid tumorsRG7604

Steap 1 ADC prostate ca.RG7450ADC ovarian ca.RG7458

CD44 MAb solid tumorsRG7356

ALK inhibitor NSCLCRG7853PI3K inh solid tumorsCHU

Bcl-2 inh CLL and NHLRG7601

ADC ADC oncologyRG7599

ChK1 inh solid tum & lymphomaRG7602

Tweak MAb oncologyRG7212V1 receptor antag autism RG7314

ADC ADC multiple myelomaRG7598

Oncology Other disease areas

WT-1 peptide cancer vaccineCHU

IL-6 MAb RACHU

Status as of December 31, 2012

MDM2 ant solid & hem tumorsRG7112HER3 MAb solid tumorsRG7116CSF-1R MAb solid tumorsRG7155

MDM2 ant solid & hem tumorsRG7388

Zelboraf + ipilimumab met. melanomaRG7204

IL-17 MAb autoimmune diseases RG7624

TLR7 agonist HBVRG7795

ADC ADC oncologyRG7600

Lucentis sust. deliv. AMD/RVO/DMERG3645

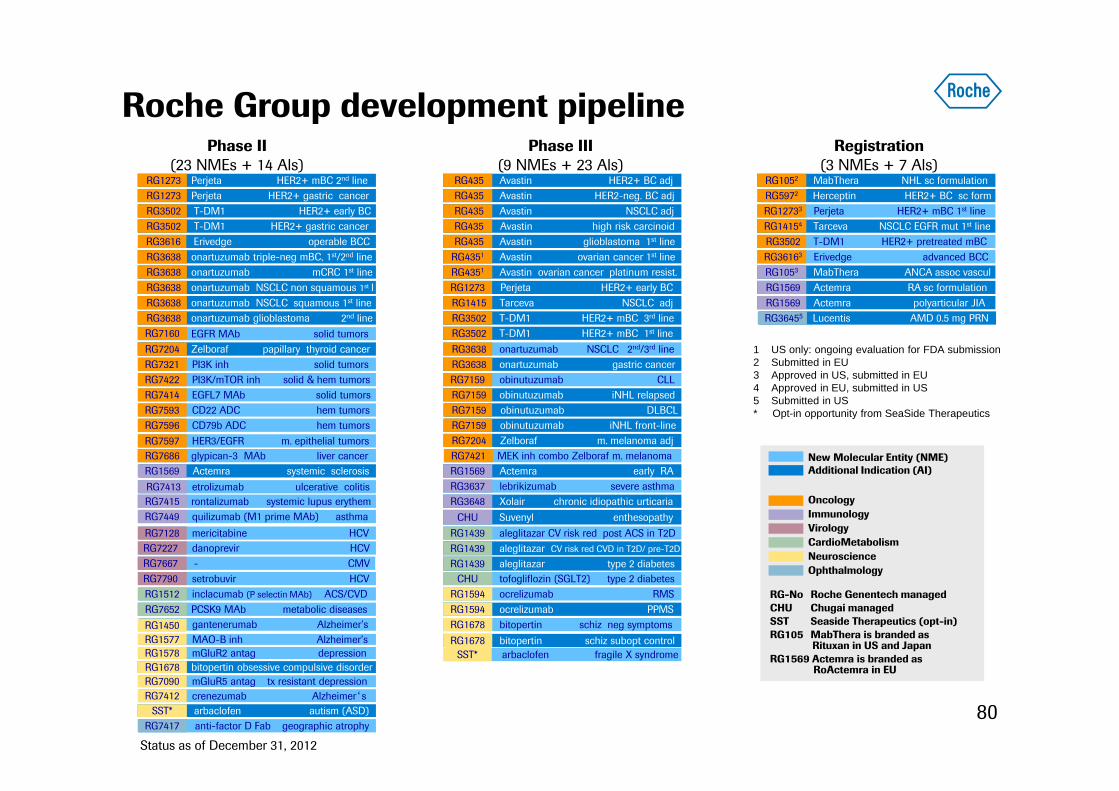

Roche Group development pipeline

79

ADC metastatic melanomaRG7636PI3k inh glioblastoma 2L RG7666ChK1 inh(2) solid tumorsRG7741

CIM331 atopic dermatitis CHU

ACE910 hemophilia ACHU

New Molecular Entity (NME)Additional Indication (AI)

OncologyImmunologyVirologyCardioMetabolismNeuroscienceOphthalmologyOthers

RG-No Roche Genentech managedCHU Chugai managed

PDE10A inh schizophrenia RG7203

Ang2-VEGF MAb oncologyRG7221

Phase II (23 NMEs + 14 Als)

Phase III(9 NMEs + 23 Als)

Registration(3 NMEs + 7 Als)

1 US only: ongoing evaluation for FDA submission 2 Submitted in EU3 Approved in US, submitted in EU4 Approved in EU, submitted in US5 Submitted in US* Opt-in opportunity from SeaSide Therapeutics

New Molecular Entity (NME) Additional Indication (AI)

RG-No Roche Genentech managedCHU Chugai managedSST Seaside Therapeutics (opt-in) RG105 MabThera is branded as

Rituxan in US and JapanRG1569 Actemra is branded as

RoActemra in EU

onartuzumab NSCLC 2nd/3rd lineRG3638

Perjeta HER2+ early BC RG1273

Avastin ovarian cancer 1st lineRG4351

Xolair chronic idiopathic urticariaRG3648

Avastin HER2+ BC adjRG435

Avastin NSCLC adjRG435

bitopertin schiz neg symptomsRG1678

Avastin HER2-neg. BC adjRG435

Avastin high risk carcinoidRG435Avastin glioblastoma 1st lineRG435

aleglitazar CV risk red post ACS in T2D RG1439

obinutuzumab iNHL relapsedRG7159

Tarceva NSCLC adjRG1415

Actemra early RA RG1569

T-DM1 HER2+ mBC 1st lineRG3502

obinutuzumab CLLRG7159

ocrelizumab RMSRG1594

bitopertin schiz subopt controlRG1678

obinutuzumab DLBCLRG7159obinutuzumab iNHL front-lineRG7159

tofogliflozin (SGLT2) type 2 diabetesCHU

ocrelizumab PPMSRG1594

T-DM1 HER2+ mBC 3rd lineRG3502

Suvenyl enthesopathyCHU

lebrikizumab severe asthmaRG3637

Avastin ovarian cancer platinum resist.RG4351

arbaclofen fragile X syndrome SST*

Perjeta HER2+ mBC 1st lineRG12733

Herceptin HER2+ BC sc formRG5972

Erivedge advanced BCCRG36163

Lucentis AMD 0.5 mg PRN RG36455

Tarceva NSCLC EGFR mut 1st lineRG14154

MabThera ANCA assoc vasculRG1053

MabThera NHL sc formulationRG1052

Actemra polyarticular JIA RG1569

T-DM1 HER2+ pretreated mBCRG3502

Perjeta HER2+ mBC 2nd lineRG1273

Zelboraf papillary thyroid cancerRG7204

mericitabine HCVRG7128

onartuzumab triple-neg mBC, 1st/2nd lineRG3638onartuzumab mCRC 1st lineRG3638

danoprevir HCVRG7227

mGluR5 antag tx resistant depressionRG7090

inclacumab (P selectin MAb) ACS/CVDRG1512

quilizumab (M1 prime MAb) asthmaRG7449

etrolizumab ulcerative colitisRG7413

anti-factor D Fab geographic atrophyRG7417

EGFL7 MAb solid tumorsRG7414

crenezumab Alzheimer‘sRG7412

MAO-B inh Alzheimer’s RG1577

EGFR MAb solid tumorsRG7160

mGluR2 antag depressionRG1578

PI3K/mTOR inh solid & hem tumorsRG7422

setrobuvir HCVRG7790

Perjeta HER2+ gastric cancerRG1273

PI3K inh solid tumorsRG7321

glypican-3 MAb liver cancerRG7686Actemra systemic sclerosisRG1569

HER3/EGFR m. epithelial tumorsRG7597

onartuzumab NSCLC non squamous 1st lRG3638

PCSK9 MAb metabolic diseasesRG7652

onartuzumab NSCLC squamous 1st line RG3638onartuzumab glioblastoma 2nd line RG3638

Erivedge operable BCCRG3616

onartuzumab gastric cancerRG3638

T-DM1 HER2+ early BCRG3502T-DM1 HER2+ gastric cancerRG3502

CD22 ADC hem tumorsRG7593CD79b ADC hem tumorsRG7596

Zelboraf m. melanoma adjRG7204

Roche Group development pipeline

80

gantenerumab Alzheimer’sRG1450

aleglitazar CV risk red CVD in T2D/ pre-T2DRG1439

Status as of December 31, 2012

bitopertin obsessive compulsive disorderRG1678

rontalizumab systemic lupus erythemRG7415

arbaclofen autism (ASD)SST*

- CMV RG7667

MEK inh combo Zelboraf m. melanomaRG7421

Actemra RA sc formulationRG1569

aleglitazar type 2 diabetesRG1439

OncologyImmunologyVirologyCardioMetabolismNeuroscienceOphthalmology

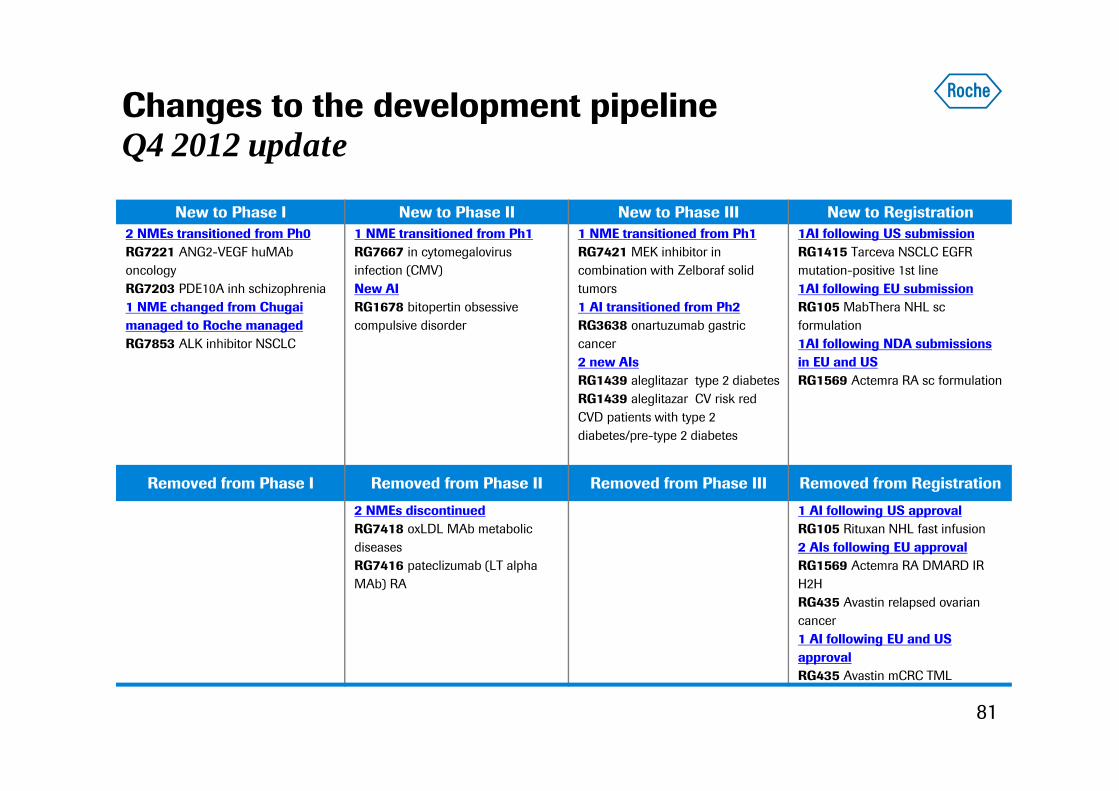

Changes to the development pipelineQ4 2012 update

81

New to Phase I New to Phase II New to Phase III New to Registration2 NMEs transitioned from Ph0RG7221 ANG2-VEGF huMAboncologyRG7203 PDE10A inh schizophrenia1 NME changed from Chugaimanaged to Roche managedRG7853 ALK inhibitor NSCLC

1 NME transitioned from Ph1RG7667 in cytomegalovirusinfection (CMV)New AIRG1678 bitopertin obsessive compulsive disorder

1 NME transitioned from Ph1 RG7421 MEK inhibitor in combination with Zelboraf solid tumors 1 AI transitioned from Ph2RG3638 onartuzumab gastric cancer2 new AIsRG1439 aleglitazar type 2 diabetesRG1439 aleglitazar CV risk red CVD patients with type 2 diabetes/pre-type 2 diabetes

1AI following US submissionRG1415 Tarceva NSCLC EGFR mutation-positive 1st line1AI following EU submissionRG105 MabThera NHL sc formulation1AI following NDA submissionsin EU and US RG1569 Actemra RA sc formulation

Removed from Phase I Removed from Phase II Removed from Phase III Removed from Registration

2 NMEs discontinuedRG7418 oxLDL MAb metabolic diseasesRG7416 pateclizumab (LT alpha MAb) RA

1 AI following US approvalRG105 Rituxan NHL fast infusion2 AIs following EU approvalRG1569 Actemra RA DMARD IR H2HRG435 Avastin relapsed ovariancancer1 AI following EU and US approvalRG435 Avastin mCRC TML

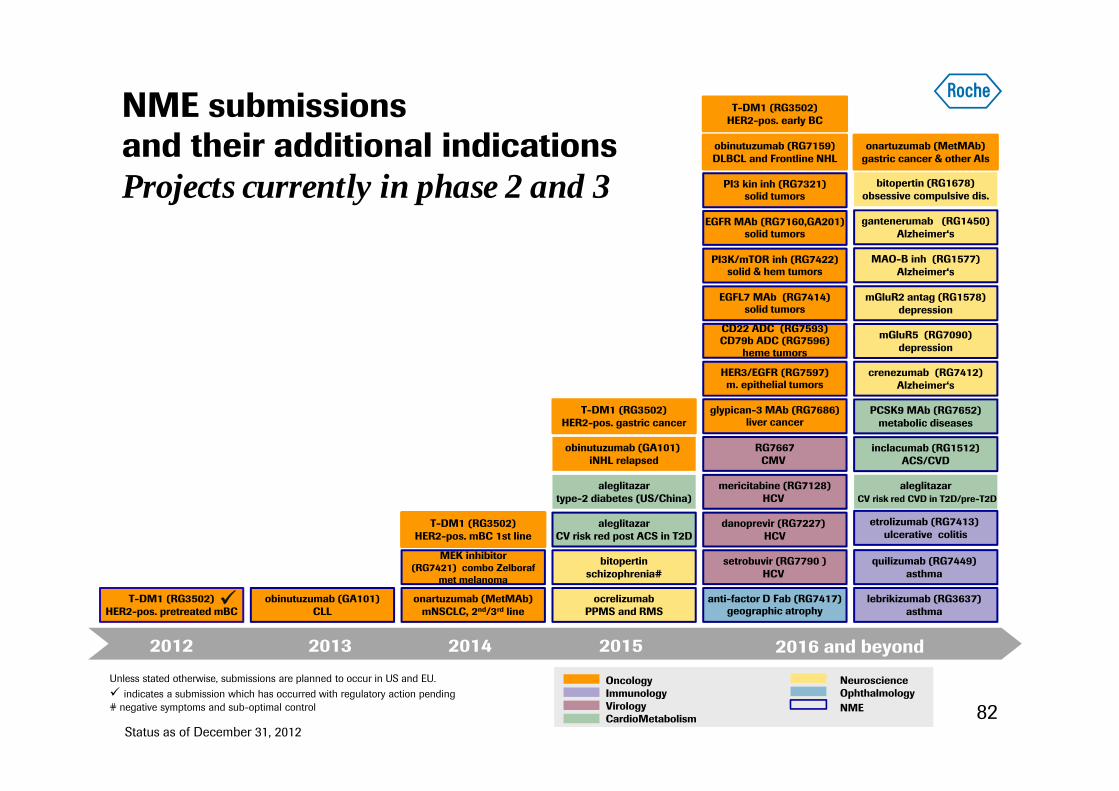

NME submissions and their additional indicationsProjects currently in phase 2 and 3

82

Unless stated otherwise, submissions are planned to occur in US and EU. indicates a submission which has occurred with regulatory action pending# negative symptoms and sub-optimal control

NeuroscienceOphthalmologyNME

OncologyImmunologyVirologyCardioMetabolism

bitopertinschizophrenia#

obinutuzumab (GA101)CLL

onartuzumab (MetMAb)mNSCLC, 2nd/3rd line

T-DM1 (RG3502)HER2-pos. mBC 1st line

ocrelizumabPPMS and RMS

2016 and beyondaleglitazarCV risk red post ACS in T2D

obinutuzumab (GA101) iNHL relapsed

Status as of December 31, 2012

T-DM1 (RG3502)HER2-pos. pretreated mBC

MEK inhibitor(RG7421) combo Zelboraf

met melanoma

T-DM1 (RG3502)HER2-pos. gastric cancer

aleglitazartype-2 diabetes (US/China)

obinutuzumab (RG7159)DLBCL and Frontline NHL

mericitabine (RG7128)HCV

danoprevir (RG7227) HCV

EGFR MAb (RG7160,GA201)solid tumors

PI3 kin inh (RG7321)solid tumors

setrobuvir (RG7790 )HCV

mGluR5 (RG7090)depression

inclacumab (RG1512)ACS/CVD

PCSK9 MAb (RG7652)metabolic diseases

crenezumab (RG7412)Alzheimer‘s

gantenerumab (RG1450)Alzheimer‘s

MAO-B inh (RG1577)Alzheimer‘s

mGluR2 antag (RG1578)depression

PI3K/mTOR inh (RG7422)solid & hem tumors

EGFL7 MAb (RG7414)solid tumors

CD22 ADC (RG7593)CD79b ADC (RG7596)

heme tumors

HER3/EGFR (RG7597)m. epithelial tumors

glypican-3 MAb (RG7686)liver cancer

quilizumab (RG7449) asthma

anti-factor D Fab (RG7417)geographic atrophy

lebrikizumab (RG3637) asthma

etrolizumab (RG7413) ulcerative colitis

bitopertin (RG1678)obsessive compulsive dis.

aleglitazarCV risk red CVD in T2D/pre-T2D

2012 2013 2014 2015 2016 and beyond

onartuzumab (MetMAb)gastric cancer & other AIs

RG7667CMV

T-DM1 (RG3502)HER2-pos. early BC

TarcevaNSCLC adj (US)

AvastinNSCLC adj

Tarceva (US)NSCLC EGFR mut. 1st line

2012 2013 2014 2015 and beyond

Avastinglioblastoma 1st line

AvastinHER2-pos. BC adj

AvastinHER2-neg BC adj

Actemraearly RA

Xolair (US)chronic idiopathic urticaria

ActemraRA DMARD IR H2H (EU)

Avastinovarian cancer 1st line (US)

OncologyImmunologyVirologyCardioMetabolism

NeuroscienceOphthalmology

Actemrasc formulation

MabTheraNHL sc formulation (EU)

indicates submission to Health Authorities has occurred.

Unless stated otherwise, submissions are planned to occur in US and EU.

Avastinrelapsed ovarian cancer (US)

TarcevaNSCLC adj (EU)

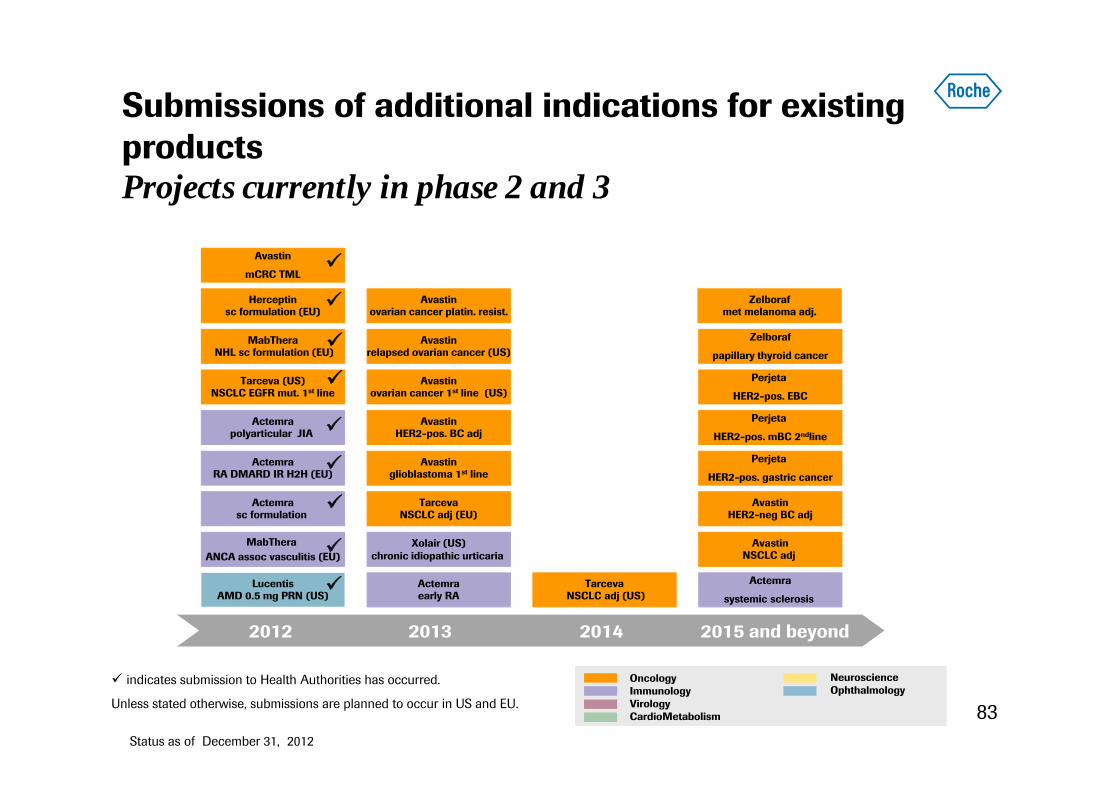

Submissions of additional indications for existing productsProjects currently in phase 2 and 3

83Status as of December 31, 2012

Actemra

systemic sclerosis

Zelboraf

papillary thyroid cancer

Herceptinsc formulation (EU)

LucentisAMD 0.5 mg PRN (US)

Perjeta

HER2-pos. EBC

Perjeta

HER2-pos. mBC 2ndline

Perjeta

HER2-pos. gastric cancer

Avastinovarian cancer platin. resist.

Avastin

mCRC TML

Actemrapolyarticular JIA

MabThera ANCA assoc vasculitis (EU)

Zelborafmet melanoma adj.

EU

US

Approved Pending approvals

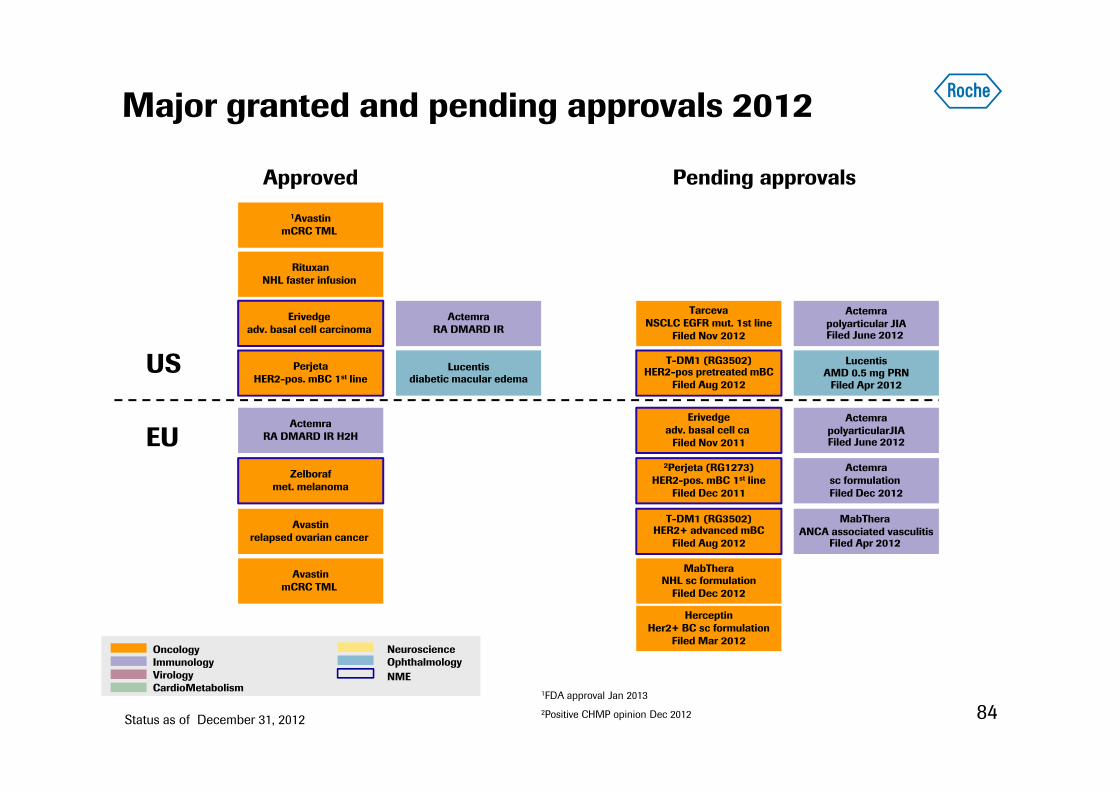

Major granted and pending approvals 2012

84

ActemraRA DMARD IR

RituxanNHL faster infusion

Avastinrelapsed ovarian cancer

Lucentisdiabetic macular edema

HerceptinHer2+ BC sc formulation

Filed Mar 2012

LucentisAMD 0.5 mg PRN

Filed Apr 2012

Status as of December 31, 2012

Actemrapolyarticular JIAFiled June 2012

ActemrapolyarticularJIAFiled June 2012

MabThera ANCA associated vasculitis

Filed Apr 2012

T-DM1 (RG3502)HER2-pos pretreated mBC

Filed Aug 2012

T-DM1 (RG3502)HER2+ advanced mBC

Filed Aug 2012

AvastinmCRC TML

PerjetaHER2-pos. mBC 1st line

Erivedgeadv. basal cell carcinoma

2Perjeta (RG1273)HER2-pos. mBC 1st line

Filed Dec 2011

Zelborafmet. melanoma

NeuroscienceOphthalmologyNME

OncologyImmunologyVirologyCardioMetabolism

Erivedgeadv. basal cell ca

Filed Nov 2011

TarcevaNSCLC EGFR mut. 1st line

Filed Nov 2012

MabTheraNHL sc formulation

Filed Dec 2012

Actemrasc formulation Filed Dec 2012

ActemraRA DMARD IR H2H

1AvastinmCRC TML

2Positive CHMP opinion Dec 2012

1FDA approval Jan 2013

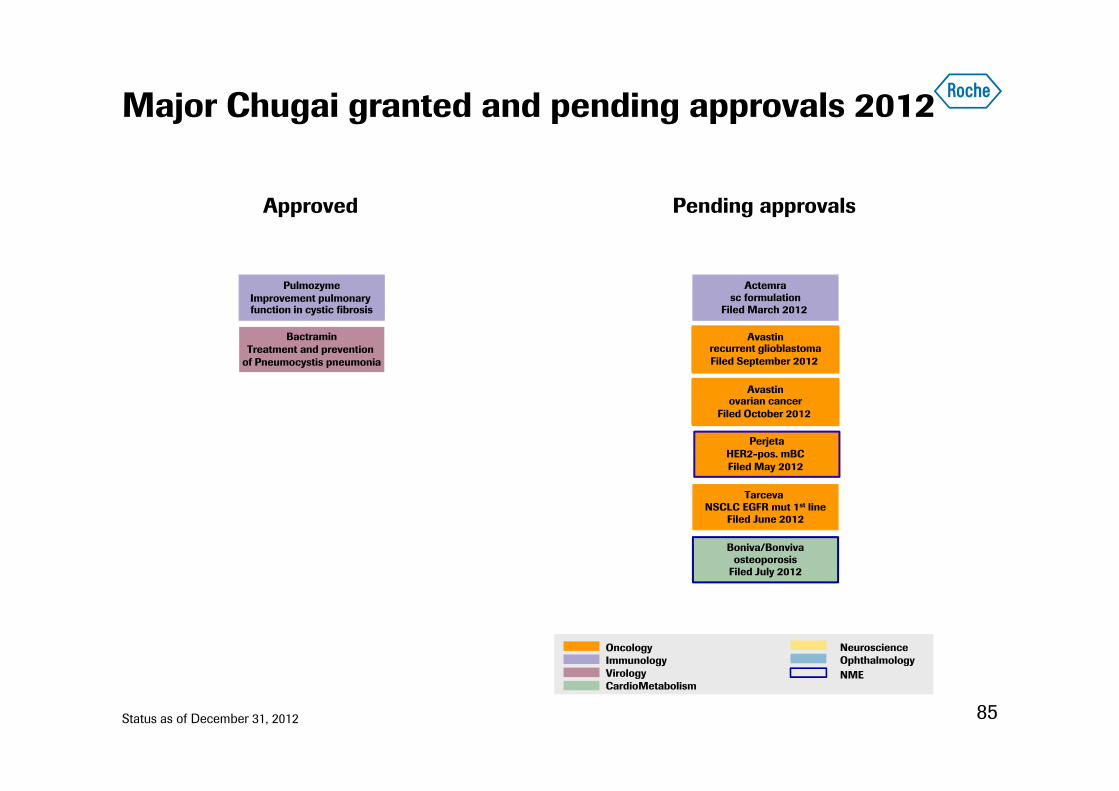

Major Chugai granted and pending approvals 2012

85

Pending approvals

Actemrasc formulation

Filed March 2012

PulmozymeImprovement pulmonaryfunction in cystic fibrosis

Status as of December 31, 2012

TarcevaNSCLC EGFR mut 1st line

Filed June 2012

Boniva/Bonvivaosteoporosis

Filed July 2012

NeuroscienceOphthalmologyNME

OncologyImmunologyVirologyCardioMetabolism

Avastinovarian cancer

Filed October 2012

Avastinrecurrent glioblastomaFiled September 2012

Approved

PerjetaHER2-pos. mBCFiled May 2012

BactraminTreatment and prevention

of Pneumocystis pneumonia

86

We Innovate Healthcare