Embed Size (px)

Citation preview

ROBUST MONETARY POLICY DESIGN FOR

DSGE MODELS

Lecture 1: The Basics

Paul Levine

University of Surrey and European Central Bank (Visiting Researcher)

July 18, 2005

Contents

1 The Problem of Uncertainty in Monetary Policy 1

2 Traditional Approaches to Uncertainty 1

2.1 Brainard (1967) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2.2 Poole (1970) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

3 Policy Rules with Only Exogenous Uncertainty 4

3.1 A DSGE Closed Economy Model . . . . . . . . . . . . . . . . . . . . . . . . 4

3.1.1 Households . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

3.1.2 Firms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

3.1.3 Equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

3.1.4 Summary of Full Model . . . . . . . . . . . . . . . . . . . . . . . . . 8

3.2 Zero-Inflation Steady State . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

3.3 The Efficient Steady State Output Level . . . . . . . . . . . . . . . . . . . . 10

3.4 The Inefficiency of the Natural Rate . . . . . . . . . . . . . . . . . . . . . . 11

3.5 Linearization about the Zero-Inflation Steady State . . . . . . . . . . . . . . 11

4 Optimal Monetary Policy 13

4.1 An Ad Hoc Central Bank’s Loss Function . . . . . . . . . . . . . . . . . . . 13

4.2 Welfare-Based Optimal Policies . . . . . . . . . . . . . . . . . . . . . . . . . 14

4.2.1 Costs of Inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

4.2.2 The Ex Ante Optimal (Ramsey) Non-Linear Problem . . . . . . . . 15

4.2.3 Linearization of Dynamics . . . . . . . . . . . . . . . . . . . . . . . . 17

4.2.4 Quadratification of Lagrangian . . . . . . . . . . . . . . . . . . . . . 18

4.2.5 Indexation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

4.2.6 The Time Consistent Solution . . . . . . . . . . . . . . . . . . . . . . 19

4.3 Optimal Policy with and without Commitment . . . . . . . . . . . . . . . . 20

4.4 Optimized IFB Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

5 Analytical Example 22

5.1 A Model without Habit and Indexing . . . . . . . . . . . . . . . . . . . . . . 22

5.1.1 The Ramsey Problem . . . . . . . . . . . . . . . . . . . . . . . . . . 24

5.1.2 Optimal Discretionary Policy and Optimized Rules . . . . . . . . . . 26

5.2 A Model without Habit, Indexing and Instrument Costs . . . . . . . . . . . 26

A Computation of Policy Rules 27

A.1 The Optimal Policy with Commitment . . . . . . . . . . . . . . . . . . . . . 27

A.1.1 Implementation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

A.1.2 Optimal Policy from a Timeless Perspective . . . . . . . . . . . . . . 29

A.2 The Dynamic Programming Discretionary Policy . . . . . . . . . . . . . . . 29

A.3 Optimized Simple Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

A.4 The Stochastic Case . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

B Software 32

0

1 The Problem of Uncertainty in Monetary Policy

“Uncertainty is not just an important feature of the monetary policy landscape; it is

the defining characteristic of that landscape.” Alan Greenspan1

Following Walsh (2003) it is useful to distinguish between different sources of uncer-

tainty facing the monetary authority by distinguishing between the ‘true’ model and the

economy and the policymaker’s perceived model. Suppose the former is given by

zt+1 = A1zt + A2zt,t + Bit + Cǫt+1 (1)

where zt is a state vector of macroeconomic variables confined for the time being to

predetermined variables, zt,t is the optimal current estimate of zt, it is the instrument and

ǫt+1 is a vector of exogenous white noise disturbances. The central bank’s perceived model

is

zt+1 = (A1 + A2)zt,t + Bit + Cǫt+1 (2)

where zt,t is their estimate of the current state. Hence the model’s misspecification error

is captured by

zt+1 − zt+1 = A1(z − zt,t)︸ ︷︷ ︸

imperfect information

+ (A − A)zt,t + (B − B)it + (C − C)ǫt+1︸ ︷︷ ︸

model uncertainty

+ A(zt − zt,t)︸ ︷︷ ︸

inefficient forecasting

(3)

where A = A1 + A2. These lectures will concentrate on the second of these sources of

uncertainty, that arising from uncertainty with respect to the parameters and structure of

the model.2

2 Traditional Approaches to Uncertainty

2.1 Brainard (1967)

The analysis of Brainard (1967) is conducted using a simple static model of the form

yt = atxt + ut (4)

1Federal Reserve Bank of Kansas (2003), Opening Remarks.2Walsh (2003) discusses the first source and concludes from his own analysis and a reading of the

literature that data uncertainty even with efficient forecasting has only modest implications for simple

rules.

1

where yt is a target macro-variable, xt is an instrument, at is a stochastic time varying

parameter with Et(at) = a, ut is a zero mean error term and variance-covariance matrix

given by

cov([ut at]) =

[

σ2u ρσaσu

ρσaσu σ2a

]

(5)

where ρ is the correlation coefficient. The policymaker’s problem at the beginning of each

period is to

minxt

Et−1[(yt − y∗)2] ≡ minxt

Λ0 (6)

subject to (4) where y∗ is a target value for yt. Since there are no dynamics in this problem

we can drop the time subscripts. Substituting for yt in (4) we have

Λ0 = E[(ax + u − y∗)2] = E[a2x2 + 2ax(u − y∗) + u2 − 2uy∗ + (y∗)2]

= (a2 + σ2a)x

2 + 2ρσaσux − 2xy∗a + σ2u + (y∗)2] (7)

where

σ2a ≡ E[(a − a2)] = E(a2) − a2 (8)

σ2u ≡ E[u2] (9)

ρ ≡E[(a − a)u]

σaσu(10)

Hence we can write

Λ0 = σ2ax

2 + 2ρσaσux + σ2u + (ax − y∗)2 (11)

The first order condition is therefore

σ2ax + ρσaσu + a(ax + y∗) = 0 (12)

giving the optimal choice of x as

x =ay∗ − ρσaσu

a2 + σ2a

(13)

In the absence of uncertainty we have x = xc = y∗

a so that (13) becomes

x =a2

a2 + σ2a

xc −ρσaσu

a2 + σ2a

(14)

There are two important features of this result

1. Unless σa = 0, the optimal policy depends on the covariance matrix of error terms

(5). With multiplicative uncertainty, optimal policy is not certainty equivalent, in

other words

2

2. x < xc iff ρ ≥ −σa(a2+σ2a)xc

σu. Thus large multiplicative uncertainty implies a more

conservative response by the policymaker. In fact as σa → ∞, then x → 0.

This analysis can be easily extended to more than one instrument. Consider

y = a1x1 + a2x2 + u (15)

Then if a1 and a2 are uncorrelated then

x1

x2=

a1σ2a,2

a2σ2a,1

(16)

and the policymaker should use both instruments with their relative intensity varying in-

versely with their respective variances.

2.2 Poole (1970)

Multiplicative uncertainty then causes certainty equivalence to fail. Another circumstance

in which CE fails is in the work of Poole. He starts by setting out an IS/LM model:

yt = −αit + ut (17)

mt = −βit + yt + vt (18)

where yt and mt are output and money supply in logs, it is the nominal interest rate and

ut and vt are error terms with E(ut) = E(vt) = cov(ut, vt) = 0. Eliminating it from (18)

we can write

yt =α(mt − vt) + βut

α + β= γmt + wt (19)

where

γ =α

α + β(20)

wt = −γvt +β

α + βut (21)

Equations (17) and (18) are two alternative instrument-target relationships, with the

interest rate and the money supply the respective targets. The question posed by Poole

is an interest-rate rule better than setting a target for the money supply?

To answer this question we compare two stochastic optimization problems

Λi0 = min

itEt−1(yt − y∗)2 subject to yt = −αit + ut (22)

and

Λm0 = min

mt

Et−1(yt − y∗)2 subject to yt = γmt + wt (23)

3

These calculations are special cases of those in Brainard without multiplicative uncertainty.

A little algebra leads to the solutions:

it = −y∗

α(24)

Λi0 = σ2

u + y∗2 (25)

and

mt =y∗

γ(26)

Λm0 = σ2

w + y∗2 (27)

Therefore an interest rate rule is better than a money supply target iff Λi0 < Λm

0 ; i.e., iff

σ2u < σ2

w. From (21) we have that

σ2w =

1

(α + β)2(α2σ2

v + β2σ2u) (28)

The condition for an interest rate rule to be better than a money supply target therefore

becomes

σ2v >

(

1 +2β

α

)

σ2u (29)

which holds if there is more exogenous uncertainty regarding money demand in the LM

relation than there is regarding output demand in the IS relation and if the interest

elasticity of demand far exceeds the interest elasticity of money demand.

The important point to emphasize here is that although each out the stochastic opti-

mization problems (22) and (23) has certainty equivalent solution for the relevant instru-

ment (since there is no multiplicative uncertainty), the choice of instrument itself depends

on second moments and is not certainty equivalent.

3 Policy Rules with Only Exogenous Uncertainty

3.1 A DSGE Closed Economy Model

In the rest of the lectures we will conduct the analysis in the context of a fairly standard

DSGE model. Our model in its most general form is essentially the Smets-Wouter model

without physical capital and wage stickiness, but with a distortionary tax on income and

habit formation in labour supply. There is a risk-free nominal bond. A final homogeneous

good is produced competitively using a CES technology consisting of a continuum of

differentiated goods. Intermediate goods producers and household suppliers of labor have

monopolistic power. Nominal prices of intermediate goods are sticky. We incorporate

habit formation in both consumption and labour supply. There is Calvo price setting with

4

indexing of prices for those firms who, in a particular period, do not re-optimize their

prices. Our model is stochastic with exogenous AR(1) stochastic processes for total factor

productivity in the intermediate goods sector, government spending and preferences. At

various stages in the lectures we will focus on various special cases of this general model.

3.1.1 Households

There are ν households of which a representative household r in the home bloc maximizes

E0

∞∑

t=0

βtUC,t

(Ct(r) − HC,t)1−σ

1 − σ+ UM,t

(Mt(r)

Pt

)1−ϕ

1 − ϕ− UN,t

(Nt(r) − HN,t)1+φ

1 + φ+ u(Gt)

(30)

where Et is the expectations operator indicating expectations formed at time t, β is the

household’s discount factor, UC,t, UM,t and UN,t are preference shocks3 Ct(r) is an index

of consumption, Nt(r) are hours worked, HC,t and HN,t represents the habit, or desire

not to differ too much from other households, and we choose HC,t = hCCt−1, where Ct =1ν

∑νr=1 Ct(r) is the average consumption index, HN,t = hN

Nt−1

ν , where Nt is aggregate

labour supply defined after (32) below and hC , hN ∈ [0, 1). When hC = 0, σ > 1 is the

risk aversion parameter (or the inverse of the intertemporal elasticity of substitution)4.

Mt(r) are end-of-period nominal money balances and u(Gt) is the utility from exogenous

real government spending Gt. We normalize the household number ν at unity.

The representative household r must obey a budget constraint:

PtCt(r)+Dt(r)+Mt(r) = Wt(1−Tt)(r)Nt(r)+(1+ it−1)Dt−1(r)+Mt−1(r)+Γt(r) (31)

where Pt is a price index, Dt(r) are end-of-period holdings of riskless nominal bonds with

nominal interest rate it over the interval [t, t + 1]. Wt(r) is the wage, Γt(r) are dividends

from ownership of firms and Tt is a tax on labour income. In addition, if we assume that

households’ labour supply is differentiated with elasticity of supply η, then (as we shall

see below) the demand for each consumer’s labor is given by

Nt(r) =

(Wt(r)

Wt

)−η

Nt (32)

where Wt =[∫ 1

0 Wt(r)1−ηdr

] 1

1−ηis an average wage index and Nt is average employment.

3In this incomplete financial markets setting we can only talk about the representative household if these

preference shocks are common. If they are household-specific we must assume there exist an complete set

of Arrow-Debreu securitites. These ensure that the marginal utility of consumption and labour supply

are identical across households and we can then aggregate across households. Both modelling assumptions

lead to the same behavioural equations.4When hC 6= 0, σ is merely an index of the curvature of the utility function.

5

Maximizing (30) subject to (31) and (32) and imposing symmetry on households (so

that Ct(r) = Ct, etc) yields standard results:

1 = β(1 + it)Et

[(UC,t+1(Ct+1 − HC,t+1)

−σ

UC,t(Ct − HC,t)−σ

)Pt

Pt+1

]

(33)

(Mt

Pt

)−ϕ

=(Ct − HC,t)

−σ

χPt

[it

1 + it

]

(34)

Wt(1 − Tt)

Pt=

UN,t

(1 − 1η )

(Nt − HN,t)φ(Ct − HC,t)

σ (35)

(33) is the familiar Keynes-Ramsey rule adapted to take into account of the consumption

habit. In (34), the demand for money balances depends positively on consumption relative

to habit and negatively on the nominal interest rate. Given the central bank’s setting of

the latter, (34) is completely recursive to the rest of the system describing our macro-

model. (35) equates the real post tax wage with the marginal rate of substitution between

work and consumption, marked up to reflect the market power of households arising from

their monopolistic supply of a differentiated factor input with elasticity η.

3.1.2 Firms

Competitive final goods firms use a continuum of non-traded intermediate goods according

to a constant returns CES technology to produce aggregate output

Yt =

(∫ 1

0Yt(m)(ζ−1)/ζdm

)ζ/(ζ−1)

(36)

where ζ is the elasticity of substitution. This implies a set of demand equations for each

intermediate good m with price Pt(m) of the form

Yt(m) =

(Pt(m)

Pt

)−ζ

Yt (37)

where Pt =[∫ 1

0 Pt(m)1−ζdm] 1

1−ζ. Pt is an aggregate intermediate price index, but since

final goods firms are competitive and the only inputs are intermediate goods, it is also the

domestic price level.

In the intermediate goods sector each good m is produced by a single firm m using

only differentiated labour with another constant returns CES technology:

Yt(m) = At

(∫ 1

0Nt(r, m)(η−1)/ηdr

)η/(η−1)

(38)

where Nt(r, m) is the labour input of type r by firm m and At is an exogenous shock

capturing shifts to trend total factor productivity (TFP) in this sector. Minimizing costs

6

∫ 10 Wt(r)Nt(r, m)dr and aggregating over firms and denoting

∫ 10 Nt(r, m)dm = Nt(r) leads

to the demand for labor as shown in (32). In an equilibrium of equal households and firms,

all wages adjust to the same level Wt and it follows that Yt = AtNt.

For later analysis it is useful to define the real marginal cost as the wage relative to

domestic producer price. Using (35) and Yt = AtNt this can be written as

MCt ≡Wt

AtPt=

UN,t

(1 − 1η )(1 − Tt)At

(Nt − HN,t)φ (Ct − HC,t)

σ (39)

Now we assume that there is a probability of 1 − ξ at each period that the price of

each intermediate good m is set optimally to P 0t (m). If the price is not re-optimized,

then it is indexed to last period’s aggregate producer price inflation.5 With indexation

parameter γ ≥ 0, this implies that successive prices with no re-optimization are given

by P 0t (m), P 0

t (m)(

Pt

Pt−1

)γ, P 0

t (m)(

Pt+1

Pt−1

)γ, ... . For each intermediate producer m the

objective is at time t to choose P 0t (m) to maximize discounted profits

Et

∞∑

k=0

ξkQt+kYt+k(m)

[

P 0t (m)

(Pt+k−1

Pt−1

)γ

−Wt+k

At+k

]

(40)

given it (since firms are atomistic), subject to (37), where Qt+k is the discount factor over

the interval [t, t + k]. The solution to this is

Et

∞∑

k=0

ξkQt+kYt+k(m)

[

P 0t (m)

(Pt+k−1

Pt−1

)γ

−1

(1 − 1/ζ)

Wt+k

At+k

]

= 0 (41)

and by the law of large numbers the evolution of the price index is given by

P 1−ζt+1 = ξ

(

Pt

(Pt

Pt−1

)γ)1−ζ

+ (1 − ξ)(P 0t+1)

1−ζ (42)

3.1.3 Equilibrium

In equilibrium, goods markets, money markets and the bond market all clear. Equating

the supply and demand of the consumer good we obtain

Yt = AtNt = Ct + Gt (43)

Assuming the same tax rate levied on all income (wage income plus dividends) a balanced

budget government budget constraint

PtGt = PtTtYt + Mt − Mt−1 (44)

5Thus we can interpret 1

1−ξas the average duration for which prices are left unchanged.

7

completes the model. Given interest rates it (expressed later in terms of an optimal or IFB

rule) the money supply is fixed by the central banks to accommodate money demand. By

Walras’ Law we can dispense with the bond market equilibrium condition and therefore the

government budget constraint that determines taxes τt. Then the equilibrium is defined

at t = 0 by stochastic processes Ct, Dt, Pt, Mt, Wt, Yt, Nt, given past price indices and

exogenous TFP and government spending processes.

In what follows we will assume a ‘cashless economy’ version of the model in which both

seigniorage in (44) and the utility contribution of money balances in (30) are negligible.

Then given the nominal interest rate, our chosen monetary instrument, we can dispense

altogether with the money demand relationship (34).

3.1.4 Summary of Full Model

We can summarize our non-linear DSGE cashless form of the model a concise form suitable

for both numerical simulations and the linear-quadratic approximation of the optimal

policy problem as:

Household Utility

Ω0 = E0

[∞∑

t=0

βtUC,t

[(Ct − hCCt−1)

1−σ

1 − σ− UN,t

(Nt − hNNt−1)1+φ

1 + φ

]]

(45)

Household Behaviour

1 = β(1 + it)Et

[(UC,t+1(Ct+1 − hCCt)

UC,t(Ct − hCCt−1)

)−σ 1

Πt+1

]

(46)

Wt

AtPt= MCt =

UN,t

(1 − 1η )(1 − Tt)At

(Nt − hNNt−1)φ(Ct − hNCt−1)

σ (47)

where

Πt ≡Pt

Pt−1= πt + 1 (48)

Firms:

Using Qt+k = βk MUCt

Pt+kwhere MUC

t = (Ct − hCCt−1)−σ is the marginal utility of con-

sumption (obtained from the household’s first-order conditions) the firms’ staggered price

setting can be succinctly described in terms of two difference equations6 :

Ht − ξβEt[Πζ−1t+1 Ht+1] = Yt(Ct − hCCt−1)

−σ (49)

Λt − ξβEt[Πζt+1Λt+1] =

UN,t

(1 − 1/ζ)(1 − 1/η)(1 − Tt)(Nt − hNNt−1)

φNt (50)

6This generalizes Benigno and Woodford (2003).

8

where

Πt ≡Πt

Πγt−1

(51)

(52)

Then defining

Φt ≡ P 0t /Pt (53)

the price-setting of firms and aggregate price index, (41) and (42) can be written as

ΦtHt = Λt (54)

with price index inflation given by

1 = ξΠζ−1t + (1 − ξ)Φ1−ζ

t (55)

Equilibrium

Yt = AtNt = Ct + Gt (56)

Tt =Gt

Yt(57)

Equations (46), (51) to (56) describe, in effect, 8 equations for Φt, Ct, Πt, Πt,

Ht, Λt, Yt, Nt given exogenous processes for It, UC,t, UN,t, Gt and At

representing a complete definition of the dynamic system. All variables dated (t − 1) are

predetermined at time t. Variables date t are non-predetermined or ‘jump’ variables.

In Batini et al. (2004) we have estimated a linearized special case of this model assuming

hN = 0 UC,t = 1 and UN,t = κ and we lump-sum non-distortionary taxes. We estimated

AR1 processes:

log At+1 = ρa log At + ǫa,t+1 (58)

log Gt+1 = ρg log Gt + ǫg,t+1 (59)

where ǫi,t+1 ∼ N(0, σ2i ), i = a, g. Estimated parameter values (for ‘model Z’) based on

quarterly data are: β = 0.99, ξ = 0.53, hC = 0.85, γ = 0.54, σ = 3.24, φ = 1.32, ρa = 0.94,

ρg = 0.93, σa = 0.72 and σg = 2.23. We have not estimated κ, η nor ζ. Plausible estimates

η = ζ = 4 and we put hN = hC . As we shall the latter ensures that the natural rate of

output is inefficient (see Choudhary and Levine (2005)).

To complete the model with need a rule for the interest rate that stabilizes the system.

The following one-period-ahead Inflation Forecast-Based (IFB) rules was assumed and

estimated in Batini et al. (2004).

it = i + θ(Et[Πt+1] − 1) (60)

9

where θ > 1 is a feedback parameter and i = 1β − 1 is the steady state value of it in a

zero-inflation steady state (Π = 1) consistent with the Euler equation (46).7

3.2 Zero-Inflation Steady State

A deterministic zero-inflation steady state, denoted by variables without the time sub-

scripts, Et−1(UC,t) = 1 and Et−1(UN,t) = κ is given by

W (1 − T )

P=

κ(1 − hN )φ(1 − hC)σ

1 − 1η

NφCσ (61)

1 = β(1 + i) (62)

Y = AN (63)

P = P 0 =W

A(

1 − 1ζ

) (64)

Y = C + G (65)

T =G

Y(66)

giving us in effect 7 equations to determine WP , i, C, N , Y , P

P 0 and T . The natural rate

of interest is determined by the private sector’s discount factor. In our cashless economy

the price level is indeterminate.

3.3 The Efficient Steady State Output Level

The natural rate of output is below the efficient rate because of monopoly power in output

and labour markets, but external habit in consumption works in the opposite direction.

To see this we solve for the deterministic socail planner’s problem.8 Using (45) the social

planner chooses trajectories for output and inflation to maximize

Ω0 =∞∑

t=0

βt

[(Ct − hCCt−1)

1−σ

1 − σ− κ

(Nt − hNNt−1)1+φ

(1 + φ)

]

(67)

where Ct = Yt − Gt and Nt = Yt

At. The first-order condition for the choice out output is

[Ct−hCCt−1]−σ−hCβ[Ct+1−hCCt]

−σ =κ

At

[[Yt

At− hN

Yt−1

At−1

]φ

− hNβ

[Yt+1

At+1− hN

Yt

At

]φ]

(68)

The efficient steady-state level of output Yt+1 = Yt = Yt−1 = Y ∗, say, is therefore given by

(Y ∗)φ(Y ∗ − G)σ =(1 − hCβ)A1+φ

κ(1 − hNβ)(1 − hC)σ(1 − hN )φ(69)

7This is saddlepath stable in a linearized form of the model.8We assume zero inflation and therefore no welfare costs from the dispersion of labour demand across

firms. We return to inflation costs from this source later.

10

3.4 The Inefficiency of the Natural Rate

From (61) to (65), after some manipulation, the steady-state level of output (the ‘natural

rate’), is given by

Y φ(Y − G)σ =(1 − T )

(

1 − 1ζ

) (

1 − 1η

)

A1+φ

κ(1 − hC)σ(1 − hN )φ(70)

Comparing (70) and (69), since (Y )φ(Y −G)σ is an increasing function of Y , we arrive at

Proposition

The natural level of output, Y , is below the efficient level, Y ∗, if and only if

(1 − T )

(

1 −1

ζ

) (

1 −1

η

)

<1 − hCβ

1 − hNβ(71)

In the case where there is no habit persistence for both consumption and labour effort,

hC = hN = 0, then (71) always holds. In this case tax distortions and market power

in the output and labour markets captured by the elasticities η ∈ (0,∞) and ζ ∈ (0,∞)

respectively drive the natural rate of output below the efficient level. If T = 0 and

η = ζ = ∞, tax distortions and market power disappear and the natural rate is efficient.

Another case where (71) always holds is where habit persistence for labour supply exceeds

that for consumption; i.e., hN ≥ hC . Some empirical estimates (though not in this paper)

suggest that hC > hN which leads to the possibility that the natural rate of output can

actually be above the efficient level (see Choudhary and Levine (2005)).

3.5 Linearization about the Zero-Inflation Steady State

We now linearize about the deterministic zero-inflation steady state. Output is then at

its sticky-price, imperfectly competitive natural rate and from (62) the nominal rate of

interest is given by ı = 1β − 1. Define all lower case variables as proportional deviations

from this baseline steady state except for rates of change which are absolute deviations.9

9That is, for a typical variable Xt, xt = Xt−X

X≃ log

(Xt

X

)where X is the baseline steady state. For

variables expressing a rate of change over time such as it, xt = Xt − X.

11

Then the linearization takes the form:

πt =β

1 + βγEtπt+1 +

γ

1 + βγπt−1 +

(1 − βξ)(1 − ξ)

(1 + βγ)ξ(mct + tt) (72)

mct = −(1 + φ − hN )

1 − hNat −

hN

(1 − hNat−1 +

σ

1 − hC(ct − hCct−1)

+φ

1 − hN(yt − hNyt−1) + uN,t (73)

ct =hC

1 + hCct−1 +

1

1 + hCEtct+1

−1 − hC

(1 + hC)σ(it − Etπt+1 + EtuC,t+1 − uC,t) (74)

yt = cyct + gygt where cy =C

Y; gy =

G

Y(75)

gt = tt (76)

uC,t+1 = ρCuC,t + ǫC,t+1 (77)

uN,t+1 = ρNuN,t + ǫN,t+1 (78)

gt+1 = ρggt + ǫg,t+1 (79)

at+1 = ρaat + ǫa,t+1 (80)

Variables yt, ct, mct, uC,t, uN,t, at, gt are proportional deviations about the steady state.

[ǫC,t, ǫN,t, ǫg,t, ǫa,t] are i.i.d. disturbances. πt, tt and it are absolute deviations about the

steady state. For later use we require the output gap the difference between output for the

sticky price model obtained above and output when prices are flexible, yt say. The latter,

obtained by setting ξ = 0 in (72) to (75), is in deviation form given by10

−(1 + φ − hN )

1 − hNat −

hN

(1 − hNat−1 +

σ

1 − hC(ct − hC ct−1)

+φ

1 − hN(yt − hN yt−1) + uN,t + gt = 0 (81)

yt = cy ct + gygt (82)

We can write this system in state space form as

[

zt+1

Etxt+1

]

= A

[

zt

xt

]

+ Bit + C

ǫC,t+1

ǫN,t+1

ǫg,t+1

ǫa,t+1

(83)

[

yt

yt

]

= E

[

zt

xt

]

(84)

10Note that the zero-inflation steady states of the sticky and flexi-price steady states are the same.

12

where zt = [uC,t, uN,t, at, gt, ct−1, ct−1, πt−1] is a vector of predetermined variables at time

t and xt = [ct, πt] are non-predetermined variables. Rational expectations are formed

assuming an information set zs, xs, s ≤ t, the model and the monetary rule. Table 2

provides a summary of our notation.

πt producer price inflation over interval [t − 1, t]

it, rt nominal and real interest rates over interval [t, t + 1]

mct marginal cost

yt, yt output with sticky prices and flexi-prices

ot = yt − yt output gap

tt tax rate

uC,t+1 = ρauC,t + ǫC,t+1 AR(1) process for factor preference shock, uC,t

uN,t+1 = ρauN,t + ǫN,t+1 AR(1) process for factor preference shock, uN,t

at+1 = ρaat + ǫa,t+1 AR(1) process for factor productivity shock, at

gt+1 = ρggt + ǫg,t+1 AR(1) process government spending shock, gt

β discount parameter

γ indexation parameter

hC , hN habit parameters

1 − ξ probability of a price re-optimization

σ risk-aversion parameter

φ disutility of labour supply parameter

Table 2. Summary of Notation (Variables in Deviation Form).

4 Optimal Monetary Policy

4.1 An Ad Hoc Central Bank’s Loss Function

Until recently the optimal policy literature adopted an ad hoc policymaker’s loss function

which plausibly described the actual objectives of central bankers. without model uncer-

tainty for now, a standard policy problem of the central bank in the home bloc at time

t = 1 is to choose in each period t = 1, 2, 3, · · · an interest rate rt so as to minimize a

standard expected loss function that depends on the variation of the output relative to an

an output target yt + k, CPI inflation and the change in the nominal interest rate:

Ω0 = E0

[

1

2

∞∑

t=0

βtc

[(yt − yt − k)2 + bπ2

t + c(it − it−1)2]

]

(85)

where βc is the discount factor of the central bank. The term k is ambitious target for

output that exceeds the natural level of output. It arises because the natural level of

13

output is not efficient owing to mark-up pricing in a monopolistically competitive inter-

mediate goods and retail sectors, market power in the labour market and habit persistence

associated with both consumption and labour supply. The output target k can be found

from (69) and (70) and putting k =(1 − Y

Y ∗

).

4.2 Welfare-Based Optimal Policies

Going back to the original non-linear DSGE the Ramsey problem is to maximize (45) sub-

ject to (46) to (56). Recent developments in numerical methods now allow the researcher

to go beyond linear approximations of their models and to conduct analysis of both the dy-

namics and welfare using higher-order (usually second-order) approximations.11 However

their are costs as well as benefits associated with this research strategy and linear-quadratic

(LQ) approximations to non-linear dynamic optimization problems such as this one are

still widely used, for very good reason. First, the characterization of time consistent and

commitment equilibria for a single policy maker, and even more so for many interacting

policymakers, are well-understood. Second, the certainty equivalence property results in

optimal rules that are independent of the variance-covariance matrix of additive distur-

bances. Third, policy can be conveniently decomposed into deterministic and stochastic

components. Fourth, even where simplicity of rules is imposed as a constraint on the prob-

lem and certainty equivalence disappears, additive uncertainty and some forms of model

uncertainty can analyzed by expressing the policymaker’s expected utility as a function

of the variance-covariance matrix of disturbances. Fifth, the stability of the system is

conveniently summarized in terms of eigenvalues. Finally for sufficiently simple models

linear-quadratic approximation allows analytical rather than numerical solution.

A common procedure for reducing this to a LQ problem is as follows. Linearize the

model about a deterministic steady state as we have already done. Then expand the utility

function as a second-order Taylor series. Much of the literature12 including Clarida et al.

(1999) then proceeds with the LQ problem of minimizing a quadratic loss function subject

the linearized model.

In general this procedure is incorrect unless the steady state is not to far from the

efficient outcome. There are two quite separate aspects to this problem. The first is the

11See, Kim and Sims (2003) and for an application to simple monetary policy rules, Juillard et al.

(2004). The latter paper compares welfare based rules with those based on an ad hoc loss function. By

varying the weights in the loss function the trade-off between inflation and output asymptotic variability

can be plotted. This is the Taylor efficiency frontier. Interestingly they find that the welfare based rule

lies almost directly on this frontier, so conventional analysis may be a good indication of (unconditional)

welfare-improving rules.12Some previous work of one of the author’s joins a distinguished list (see Currie and Levine (1993).

14

correct procedure for replacing a stochastic non-linear optimization problem with a linear-

quadratic approximation. The second is to take as the benevolent policymaker’s expected

utility the expected welfare of the representative agent within the model (see Benigno

and Woodford (2003), Levine et al. (2005)). To illustrate the correct linear-quadratic

procedure we confine ourselves to the case of no habit in labour supply (hN = 0), and

put hC = h, no government spending G = 0 and no indexing of prices γ = 0, though the

generalization to allow for these features is relatively straightforward.

4.2.1 Costs of Inflation

The costs of inflation take into account the effect of price dispersion, which has been

derived by Woodford (2003)

Dt = ξDt−1 +ξ

1 − ξ(lnΠt)

2 (86)

The impact of price dispersion arises from labour input being the same for each indi-

vidual, but dependent on demand for each intermediate good:

Nt =∑

Nt(m) =Yt

At

∑ Yt(m)

Yt=

Yt

At

∑(

Pt(m)

Pt

)−ζ

(87)

Now assume that that lnPt(j) is approximately normally distributed as N(µt, Dt); by

the law of large numbers, it follows that the overall price index Pt is given by

P 1−ζt = E[e(1−ζ)lnPt(j)] = e(1−ζ)µt+

1

2(1−ζ)2Dt (88)

Similarly one can obtain an approximate expression for the last term of (87):

∑

(Pt(j)

Pt)−ζ = P ζ

t E[e(−ζlnPit ] = eζµt+1

2ζ(1−ζ)Dte−ζµt+

1

2ζ2Dt = e

1

2ζDt (89)

From this it follows that

N1+φt

∼=

(Yt

At

)1+φ

(1 +1

2ζ(1 + φ)Dt) (90)

4.2.2 The Ex Ante Optimal (Ramsey) Non-Linear Problem

The Ramsey problem for non-linear stochastic problem is found by choosing a policy rule

for inflation to maximize

Ω0 = E0

[∞∑

t=0

βt

[

(Ct − hCZt)1−σ

1 − σ− κ

Y 1+φt

A1+φt (1 + φ)

(1 +1

2ζ(1 + φ)Dt)

]]

(91)

subject to the constraints (49) to (56) and (86) where we have defined for convenience a

new variable

Zt = hCt−1 (92)

15

Note that the Euler equation (46) does not feature in this problem as it only serves to

determine the interest rate necessary to put the economy on its optimal path.

We can now write the Lagrangian for the policymaker’s deterministic optimal control

problem as follows:

L = Ω0 +∞∑

t=0

βt[λ1t(Zt+1 − hYt) + λ2t(1 − ξΠζ−1t − (1 − ξ)Φ1−ζ

t )

+ λ3t(ΦtHt − Λt) + λ4t(Ht − ξβΠζ−1t+1 Ht+1 − Yt(Yt − Zt)

−σ)

+ λ5t

(

Λt − ξβΠζt+1Λt+1 −

κ

(1 − 1/ζ)(1 − 1/η)

Y 1+φt

A1+φt

)

+ λ6t(Dt − ξDt−1 −ξ

1 − ξ(lnΠt)

2)]

where we have put Ct = Yt.

First-order conditions are given by:

(Yt − Zt)−σ − hλ1t − κ

Y φt

A1+φt

(1 +1

2ζ(1 + φ)Dt)

−λ4t((Yt − Zt)−σ − σYt(Yt − Zt)

−σ−1) − λ5tκ(1 + φ)

(1 − 1/ζ)(1 − 1/η)

Y φt

A1+φt

= 0 (93)

β(1− ζ)ξλ2,t+1Πζ−2t+1 − λ4tξβ(ζ − 1)Πζ−2

t+1 Ht+1 − λ5tξβζΠζ−1t+1 Λt+1 −

2ξβ

1 − ξλ6,t+1

lnΠt+1

Πt+1= 0

(94)

−(Yt − Zt)−σ +

1

βλ1t−1 − λ4tσYt(Yt − Zt)

−σ−1 = 0 (95)

−λ2t(1 − ξ)(1 − ζ)Φ−ζt + λ3tHt = 0 (96)

λ3tΦt + λ4t − ξΠζ−1λ4,t−1 = 0 (97)

−λ3t + λ5t − ξΠζt λ5,t−1 = 0 (98)

−1

2κ(

Yt

At)1+φζ + λ6t − ξβλ6,t+1 = 0 (99)

Steady state values are given by

Π = Φ = 1 ; Λ = H =Y 1−σ(1 − h)−σ

1 − βξ; D = 0

(1 − h)−σ =κ

(1 − 1/ζ)(1 − 1/η)

Y σ+φ

A1+φ(100)

and, defining α = (1 − 1/ζ)(1 − 1/η)

λ5 =(1 − α − hβ)(1 − h)

σ(1 − hβ) + φ(1 − h)= −λ4 ; λ3 = (1 − ξ)λ5 ; λ2 =

Hλ5

(1 − ζ)

λ1 = βY −σ(1 − h)−σ ασ + φ(1 − h)

σ(1 − hβ) + φ(1 − h); λ6 =

κ

2(Y

A)1+φ ζ

1 − βξ(101)

16

Hence steady-state inflation is zero for the Ramsey problem. From (100) the steady state

output in the Ramsey problem is given by

(Y φ+σ) =

(

1 − 1ζ

) (

1 − 1η

)

A1+φ

κ(1 − h)σ(102)

which agrees with (70) found previously.

4.2.3 Linearization of Dynamics

We now confirm our original linearization of the dynamic equations about the zero-inflation

(Ramsey) steady state. For the moment, define ht, φt, λt, πt as deviations of Ht, Λt, Λt, Πt

from their steady state values, and ∆Yt, ∆Zt, ∆At as deviations from the steady state

values of Yt, Zt, At. Later we shall introduce yt = (Yt − Y )/Y etc. First note that

linearization of (54) and (55) yields

Hφt = λt − ht ξπt = (1 − ξ)φt (103)

Linearization of (92) yields

∆Zt = h∆Yt−1 ; zt = yt−1 (104)

and linearization of (49) and (50) yields

ht − βξ(ζ − 1)HEtπt+1 − βξEtht+1 = V −σ(yt − σY/V (∆Yt − h∆Yt−1)) (105)

λt − βξζΛEtπt+1 − βξEtλt+1 =κ(1 + φ)

(1 − 1/ζ)(1 − 1/η)

Y φ

A1+φ(∆Yt −

Y

A∆At) (106)

where V = (1−h)Y . Now subtract (105) from (106). Noting that Λ = H, and substituting

from (103) yields a Phillips curve relationship of the form:

πt = βEtπt+1 +(1 − ξ)(1 − βξ)

ξ

1

Y(φ∆Yt +

σ

1 − h(∆Yt − h∆Yt−1)−

(1 + φ)Y

A∆At) (107)

which can now be rewritten as:

πt = βEtπt+1 +(1 − ξ)(1 − βξ)

ξ(φyt +

σ

1 − h(yt − hyt−1) − (1 + φ)at) (108)

Note that what has been done here is to express φt in terms of πt and therefore λt − ht in

terms of πt.

17

4.2.4 Quadratification of Lagrangian

We can now obtain our required quadratic approximation of the household’s utility func-

tion by finding a quadratic approximation of the optimized Lagrangian at the steady state

values. The important feature to note is that by virtue of the first-order conditions for

the optimum, the linear terms drop out and we are left with the only the second order

terms. This quadratic form then incorporates the necessary second order terms from the

dynamics of the model.

Ignoring the steady state value of the Lagrangian, the remaining terms up to second

order are given by:

−1

2∆Y 2

t

[

κφY φ−1

A1+φ+ λ5

κ

αφ(1 + φ)

Y φ−1

A1+φ

]

− ∆Yt(∆Yt − ∆Zt)λ5σY −σ−1(1 − h)−σ−1

−1

2(∆Yt − ∆Zt)

2[σY −σ−1(1 − h)−σ−1 − λ5σ(σ + 1)Y −σ−1(1 − h)−σ−1]

+κY φ

A2+φ∆Yt∆At[1 + (1 + φ)λ5/α]

−ξβ

2π2

t+1((ζ − 1)(ζ − 2)λ2Πζ−3 + (ζ − 1)(ζ − 2)Πζ−3Hλ4 + ζλ5(ζ − 1)Πζ−2Λ +

2λ6

(1 − ξ)Π2)

−ξβπt+1λt+1ζλ5Πζ−1 − ξβπt+1ht+1(ζ − 1)λ4Π

ζ−2

+1

2q2t+1λ2β(1 − ξ)(1 − ζ)ζQ−1−ζ + qt+1ht+1βλ3 (109)

Subtracting (105) from (106) and using (103) and the fact that λ4 = −λ5, we can eliminate

λt − ht and qt from (109). Then after some effort we can show that (109) is equal to

−κY φ+1

2αA1+φ(φ(1 − h) + σ(1 − hβ))[y2

t φ(σα(1 − hβ) + (1 − α − hβ)(1 − h) + φ(1 − hβ)(1 − h))

+2yt(yt − zt)σ(1 − α − hβ) +(yt − zt)

2

1 − hσ(φ(1 − h) + σα − (1 − α − hβ))]

+κ(1 + φ)Y 1+φ

A1+φytat(1 + (1 + φ)λ5/α) −

1

2ξβ(ζHλ5 + 2λ6)/(1 − ξ)π2

t+1 (110)

Note that when h = 0 this reduces to

−κY φ+1

2αA1+φ(φ + σ)y2

t [φσα + φ(1 − α) + φ2 + 2σ(1 − α) + σφ + σ2α − σ(1 − α)]

+κ(1 + φ)Y 1+φ

A1+φytat(1 +

(1 + φ)(1 − α)

α(σ + φ)) −

1

2ξβ(ζHλ5 + 2λ6)/(1 − ξ)π2

t+1 (111)

After some further effort, using inflation dynamics (and subtracting an appropriate term

in a2t ) this further reduces to

−κY φ+1

2αA1+φ[(φ + σα + 1 − α)(y2

t −1 + φ

σ + φat)

2 +ζξ(φα + σα + 1 − α)

(1 − ξ)(1 − βξ)(σ + φ)π2

t ] (112)

18

Note for this case without habit, the single-period utility function is of the form

Ut = o2t + bπ2

t (113)

where ot = (yt−yt) is the output gap. Note also that the relative weights on the output gap

and inflation are independent of the household’s preference parameter κ and are expressed

in terms of fundamental parameters that are amenable to estimation in DSGE models by

Bayesian methods. With habit the welfare-based utility function is far more complicated

involving terms in yt − hyt−1 and with indexing terms in (πt − γπt−1)2 (see below).

Our welfare based utility function contains contains no terms penalizing interest rate

volatility per se. In Woodford (2003) a welfare based utility function of the form

Ut = o2t + bπ2

t + c(it − i∗)2 (114)

where i∗ > 0 is proposed to capture a binding zero interest-rate lower bound.

4.2.5 Indexation

If indexation is taken into account, it is straightforward to show that the price dispersion

term is transformed by changing Πt+1 to Πt+1/Πγt (Woodford 2004) shows that a similar

change is required for updating the price dispersion term Dt. It follows therefore that the

first-order conditions are as before under this transformation, and in particular the steady

state is still given by Π = 1. Thus there only two things that change.

Firstly, the Phillips curve equation now becomes which can now be rewritten as:

πt−γπt−1 = βEtπt+1−βγπt +(1 − ξ)(1 − βξ)

ξ(φyt +

σ

1 − h(yt−hyt−1)− (1+φ)at) (115)

Secondly, the quadratic term in π2t+1 in (110) is replaced by (πt+1 − γπt)

2.

4.2.6 The Time Consistent Solution

Suppose the policymaker is unable to commitment and conducts policy under discretion.

If we were to use the correct procedure and minimize (113) subject to our linearized model

the inflationary bias seems to disappear. What has happened here? The answer is that the

BW procedures imposes a long-run inflation rate that is only consistent with commitment

and which lacks credibility if policy is carried out under discretion.

In the light of these considerations, for what type of policy rules is the procedure above

appropriate? Our analyze suggests:

1. All types of rules for which the natural rate is almost efficient. Then for discretionary

policy the inflationary bias must be small.

19

2. Rules for which it is possible to commitment to a long-term low inflation rate, but

not to a state-contingent rule. Then the LQ approximation method can be used

to evaluate the stochastic components of discretionary and commitment policy and

assess the stabilization gain from commitment emphasized as characteristic of New

Keynesian macroeconomic models by Clarida et al. (1999).

3. Optimized simple rules such Inflation-Forecast Based Rules or Taylor Rules that

force the economy back on a particular long-run steady state.

In all these cases when comparing different policy rules, the second-order approxima-

tion of the loss function and the linearization of the dynamic equations needs only to be

done once and then applied to all types of rule. This is not the case for perturbation

methods and other numerical algorithms discussed.

If it is not possible to commit to a long-term low inflation rate then we need a different

LQ procedure that approximates the problem in the vicinity of a credible steady state

inflation rate. The correct LQ approximation is that obtained from the optimal policy (i.e.,

the Ramsey commitment policy) but approximated in the vicinity of a credible inflation

rate. To obtain this (and the LQ approximation for the Ramsey problem where Π > 1)

the following procedure is proposed.

1. Perform the LQ approximation above for any inflation rate Π 6= 1 necessarily ; i.e,

suppress the foc (94)

2. For the commitment case include foc (94) and proceed to the complete LQ approx-

imation above (possibly with Π = Πc 6= 1).

3. For the time consistent case perform the Lagrange multiplier problem above but take

expectations of future variables as given (as for our simple example). This leads to

a credible steady state inflation rate with bias Π = Πd > Πc.

4. Then use the same LQ as in 1. but with Π = Πd.

5. Note that to compare the commitment and discretionary cases we have to retain the

steady state values of the Lagrangian dropped in section 4.6.

4.3 Optimal Policy with and without Commitment

We first show how to compute the optimal policies where the policy maker can commit,

and the optimal discretionary policy where no commitment mechanism is in place.13 In

13Full details of the procedures used to compute optimal policies and optimized IFB rules are provided

in Appendix A.

20

our linear-quadratic framework optimal policies (including those for optimal IFB rules)

conveniently decompose into deterministic and stochastic components. Consider the ad

hoc form of the policymaker’s utility function. Let target variables in (85) be written as

sums of a deterministic stochastic components such as yt = yt + yt where all variables are

expressed in deviation form about the baseline zero-inflation deterministic steady state of

the known model. Then the expected loss function decomposes as

Ω0 =1

2

∞∑

t=0

βtc

[(yt − ot)

2 + bπ2t + c(it − it−1)

2 + E0

[(yt − ot)

2 + bπ2t + c(it − it−1)

2]]

= Ω0 + Ω0 (116)

say. The policymaker can then design an optimal policy consisting of an open-loop tra-

jectory that minimizes Ω0 subject to the deterministic model plus a feedback rule that

minimizes Ω0 subject to a stochastic model expressing stochastic deviations about the

open-loop trajectory. By the property of certainty equivalence for full optimal policies,

but not optimized simple rules, the feedback rule is independent of both the initial values

of the predetermined variables and the variance-covariance matrix of the disturbances.

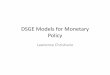

The optimal deterministic policy with k = 5% is shown in figures 1 and 2.

4.4 Optimized IFB Rules

We now turn to optimized IFB rules and optimal Taylor-type rules feeding back on either

current inflation alone or on inflation and the output gap. The general form of the rule

that covers integral and non-integral IFB as well as the Taylor-type rules is given by

it = ρit−1 + ΘEtπt+j + Θy(yt − yt) ; ρ ∈ [0, 1], Θ, Θy > 0, j ≥ 0 (117)

We focus exclusively on stabilization policy by putting k = 0 so there is no deterministic

component of policy in response to an ambitious output target.14 Given the estimated

variance-covariance matrix of the white noise disturbances, an optimal combination (Θ, ρ)

can be found for each rule defined by the time horizon j ≥ 0, and for the Taylor rule, and

optimal combination (Θ, Θy, ρ). Table 1 sets out our results for the model without habit

in labour supply and distortionary taxes (This model is estimated by Bayesian methods

in the second lecture).

A number of interesting observations emerge from these tables. First, from the output

equivalent loss (relative to the optimal commitment outcome) of ‘minimal control’, the

14Since the IFB rule assumes a commitment mechanism, the policymaker in principle should be able to

implement a policy it = it plus a feedback component such as (117) relative to it, where the latter is the

optimal deterministic trajectory found in the previous section.

21

closest saddle-path stable rule using current inflation to no feedback rule at all, we see

that there are significant though not dramatic gains from stabilization of 0.5% across the

three models. Second, the output equivalent loss from optimal discretion indicate only

small stabilization gains from commitment if the latter policy rule is implementable. By

far the main gain from commitment is the elimination of the inflationary bias which has

been ruled out in these results by putting k = 0. Third, if the policymaker can commit

using a simple rule, the best one in this respect is a Taylor integral rule, and this realizes a

large part of the potential stabilization gain. Third, for each model we search for optimized

rules within those that satisfy the determinacy conditions on ρ and θ for non-integral rules

and on Θ for integral rules. Our theory set out in Batini et al. (2004) has shown that this

requirement severely constrains the range of possible stabilizing rules as the horizon j in-

creases and as a result compared with the Taylor rule, IFBj rules perform increasingly less

well. In our results the transition from IFB3 to IFB4 is particularly dramatic involving

an output equivalent loss of 55%.

Rule ρ Θ Θy Loss Function % Output Equivalent

Minimal Feedback on πt 1 0.001 0 22.45 0.54

IFB0 1 1.25 0 0.88 0.01

Taylor Rule 1 1.25 0.11 0.88 0.01

IFB1 1 2.96 0 1.16 0.02

IFB2 1 5.0 0 1.45 0.02

IFB3 1 1.17 0 28.03 0.67

IFB4 0.87 0.40 0 2314 54.8

Optimal Commitment n.a. n.a. n.a 0.45 0

Optimal Discretion n.a. n.a. n.a 0.93 0.01

Table 1. Optimal Rules and Optimized Simple Rules Compared.

5 Analytical Example

This section illustrates these general solutions using two simplified forms of our DSGE

model.

5.1 A Model without Habit and Indexing

First we suppress habit, indexing and shocks to consumer preferences. Then putting

γ = hC = hN = uC,t = uN,t = 0, the model linearized around a zero-inflation steady state

22

reduces to

πt = βEtπt+1 + λ(mct + tt) where λ =(1 − βξ)(1 − ξ)

ξ(118)

mct = −(1 + φ)at + σct + φyt + uN,t (119)

ct = Etct+1 −1

σ(it − Etπt+1 + EtuC,t+1 − uC,t) (120)

yt = cyct + gygt (121)

gt = tt (122)

gt+1 = ρggt + ǫg,t+1 (123)

at+1 = ρaat + ǫa,t+1 (124)

As before, variables yt, ct, mct, at, gt are proportional deviations about the steady state.

[ǫC,t, ǫN,t, ǫg,t, ǫa,t] are i.i.d. disturbances. πt, tt and it are absolute deviations about the

steady state. The flexi-price level of output is found from

−(1 + φ)at + σct + φyt + gt = 0 (125)

yt = cy ct + gygt (126)

Hence from (125) and (126) we have

yt = yt(gt, at) =(1 + φ)at − gt

(

1 − σcy

)

σcy

+ φ(127)

Thus the flexi-price level of output increases with a positive technology shock and decreases

with a government spending shock if the tax distortion effect (the second term) outweighs

the switch from leisure to work as consumption is squeezed and the marginal utility of

consumption increases. The latter effect increases as the elasticity of consumption (σ)

increases.

We can write this system in state space form as

[

zt+1

Etxt+1

]

= A

[

zt

xt

]

+ Bit + C

[

ǫg,t+1

ǫa,t+1

]

(128)

[

yt

yt

]

= E

[

zt

xt

]

(129)

where zt = [uC,t, uN,t, at, gt] is a vector of predetermined variables at time t and xt =

[ct, πt] are non-predetermined variables. Rational expectations are formed assuming an

information set zs, xs, s ≤ t, the model and the monetary rule.

23

5.1.1 The Ramsey Problem

Since certainty equivalence applies to this optimal policy with commitment, we can derive

the optimal rule from the deterministic problem. Substitute out for output yt from (121)

and set up the Lagrangian

L0 =∞∑

t=0

βt

[1

2

[(yt − yt(at, gt))

2 + bπ2t + ci2t

]+ µ1,t+1(ρaat − at+1) + µ2,t+1(ρggt − gt+1)

+ µ3,t+1 (πt + λ(1 + φ)at − λ (σ + φcy) ct − λφgygt − βπt+1)

+ µ4,t+1

(

ct +1

σ(it − πt+1) − ct+1

) ]

(130)

The first order conditions with respect to ct, πt, it, at and gt are

ct : (yt − yt)cy − λ (σ + φcy)µ3,t+1 + µ4,t+1 −1

βµ4,t = 0 (131)

πt : bπt + µ3,t+1 − µ3,t −1

σβµ4,t = 0 (132)

it : cit +1

σµ4,t+1 = 0 (133)

at : −2(yt − yt)∂y

∂at+ µ1,t+1ρa −

1

βµ1,t + λ(1 + φ)µ3,t+1 = 0 (134)

gt : −2(yt − yt)∂y

∂gt+ µ2,t+1ρg −

1

βµ2,t + (yt − yt)gy + λφgyµ3,t+1 = 0 (135)

The transversality conditions

limt→∞

µi,t, i = 1, 2 (136)

and initial conditions

µi,0 = 0, i = 3, 4 (137)

a0, g0 given (138)

completes the solution to the Ramsey problem.

The optimal rule in feedback form suitable for a stochastic environment can be ex-

pressed in a number of forms. First, following the general procedure in Appendix A.1

it can be written as a feedback on exogenous shocks and co-states associated with jump

variables ct and πt:

it = D

at

gt

p3,t

p4,t

(139)

24

where we have defined pi,t =µi,t

β . These modified co-state variables are given by

[

p3,t+1

p4,t+1

]

= H21

[

at

gt

]

+ H22

[

p3,t

p4,t

]

(140)

where we need to solve a 4× Ricatti equation to calculate H.

The rule may also be expressed in two other forms. First let zt =

[

at

gt

]

. Then the

rule can be written as:

it = D1zt + D2H21

t∑

τ=1

(H22)τ−1zt−τ (141)

where D = [D1 D2] is partitioned conformably with zt and the co-state variables in (139).

The rule then consists of a feedback on the lagged shocks (the only predetermined variables

in this model) with geometrically declining weights with lags extending back to time t = 0,

the time of the formulation and announcement of the policy.

The Robust Optimal Explicit rule of Woodford (2003) is derived as follows. First

eliminate µ4,t from (131) and (132) using (133). Then use (131) to eliminate µ3,t from

(132). After some algebra this results in

it =

(

1 +1

β+

λ(σ + φcy)

βσ

)

it−1 −1

βit−2 +

λb (σ + φcy)

σcπt +

C

σcY∆(yt − yt) (142)

To complete the solution we need to specify the initial setting for the interest rate i0.

From the optimality initial conditions µ3,0 = µ4,0 = 0. Hence if a0 = g0 = 0 from (A.16)

we have that π0 = y0 = y0 = c0. Hence from (131) and (132) we have that µ3,1 = µ4,1 = 0

which leads us to conclude that π0 = 0 and there is no initial jump in the inflation rate.

However if there are initial displacements to at and gt, or there is an ambitious output

target in the loss function this conclusion does not hold. Then Woodford (2003) replaces

one initial condition µ3,t = 0 or µ4,t = 0 with π0 = 0 to give the optimal policy from a

timeless perspective.

A number of features of this rule should be emphasized. First unlike the previous form

of the optimal rule it only contains target variables that appear in the policymaker’s loss

function. Second, it is robust in the sense that it can be implemented without knowing the

form the exogenous processes for at or gt. Third, the rule displays inertia in the interest

rate. Finally the rule is relatively simple compared with the previous form of the rule, but

is still complex even for this very simple model.

25

5.1.2 Optimal Discretionary Policy and Optimized Rules

The ex ante optimal policy is time-inconsistent. The nature of the time inconsistency

problem can be seen from the first form of the optimal rule (139). If the policymaker

were to re-optimize at time t > 0 she would simply reset p3,t = p4,t = 0 is what could be

described as a cheating policy. A time consistent policy that removes this incentive has

the Markov-perfect structure

it = Dzt ; xt = −Nzt (143)

and can be found by the iterative dynamic programming solution set out in Appendix 2.

Even for this simple model this is not amenable to analytical solution. The same is true

for optimized simple rules of the form (117).

5.2 A Model without Habit, Indexing and Instrument Costs

Now suppose there are no instrument costs in the loss function. Then c = µ4,t+1 = 0 and

we can dispense with the Euler equation altogether. This is the model in Clarida et al.

(1999). Now it is possible to obtain closed-form solutions to all three types of policy rules.

In this model policy can be decomposed into two stages. First, set the inflation rate or

aggregate demand so as to minimize the loss function. Second use the Euler equation to

determine the interest rate that is require to achieve the desired path for the inflation rate

or aggregate demand.

The ROE rule is particularly simple for this model. From (131) and (132) with µ4,t+1 =

0 we can eliminate µ3,t to arrive at

πt = −C

bλ(σY + φC)∆(yt − yt) (144)

That is, policy “leans against the wind” with inflation responding positively to a decrease

in the change in the output gap.

Much of the analysis in Clarida et al. (1999) parallels an earlier literature within the

Barro-Gordon framework, but there are some important differences introduced by the

Keynesian rigidities. One of these is that there are stabilization gains from commitment

as well as those associated with eliminating the inflationary bias. They stress this result

and describe it as “less understood” in the literature.15

15The result is also shown in a number of papers reproduced in Currie and Levine (1993) using ad hoc

macro models without micro-foundations.

26

A Computation of Policy Rules

First consider the purely deterministic problem. The general model then takes the form[

zt+1

xet+1,t

]

= A

[

zt

xt

]

+ Bwt (A.1)

where zt is an (n − m) × 1 vector of predetermined variables including non-stationary

processed, z0 is given, wt is a vector of policy variables, xt is an m × 1 vector of non-

predetermined variables and xet+1,t denotes rational (model consistent) expectations of

xt+1 formed at time t. Then xet+1,t = xt+1 and letting y

Tt =

[zTt x

Tt

](A.1) becomes

yt+1 = Ayt + Bwt (A.2)

Define target variables st by

st = Myt + Hwt (A.3)

and the policy-maker’s loss function at time t by

Ωt =1

2

∞∑

i=0

βt[sTt+iQ1st+i + wTt+iQ2wt+i] (A.4)

which we rewrite as

Ωt =1

2

∞∑

i=0

βt[yTt+iQyt+i + 2y

Tt+iUwt+i + w

Tt+iRwt+i] (A.5)

where Q = MT Q1M , U = MT Q1H, R = Q2 + HT Q1H, Q1 and Q2 are symmetric

and non-negative definite R is required to be positive definite and β ∈ (0, 1) is discount

factor. The procedures for evaluating the three policy rules are outlined in the rest of this

appendix (or Currie and Levine (1993) for a more detailed treatment).

A.1 The Optimal Policy with Commitment

Consider the policy-maker’s ex-ante optimal policy at t = 0. This is found by minimizing

Ω0 given by (A.5) subject to (A.2) and (A.3) and given z0. We proceed by defining the

Hamiltonian

Ht(yt, yt+1, µt+1) =1

2βt(yT

t Qyt + 2yTt Uwt + w

Tt Rwt) + µt+1(Ayt + Bwt − yt+1) (A.6)

where µt is a row vector of costate variables. By standard Lagrange multiplier theory we

minimize

L0(y0, y1, . . . , w0, w1, . . . , µ1, µ2, . . .) =∞∑

t=0

Ht (A.7)

with respect to the arguments of L0 (except z0 which is given). Then at the optimum,

L0 = Ω0.

27

Redefining a new costate column vector pt = β−tµTt , the first-order conditions lead to

wt = −R−1(βBTpt+1 + UT

yt) (A.8)

βATpt+1 − pt = −(Qyt + Uwt) (A.9)

Substituting (A.8) into (A.2)) we arrive at the following system under control

[

I βBR−1BT

0 β(AT − UR−1BT )

] [

yt+1

pt+1

]

=

[

A − BR−1UT 0

−(Q − UR−1UT I

] [

yt

pt

]

(A.10)

To complete the solution we require 2n boundary conditions for (A.10). Specifying z0

gives us n−m of these conditions. The remaining condition is the ’transversality condition’

limt→∞

µTt = lim

t→∞

βtpt = 0 (A.11)

and the initial condition

p20 = 0 (A.12)

where pTt =

[p

T1t p

T2t

]is partitioned so that p1t is of dimension (n − m) × 1. Equation

(A.3), (A.8), (A.10) together with the 2n boundary conditions constitute the system under

optimal control.

Solving the system under control leads to the following rule

wt = −F

[

I 0

−N21 −N22

] [

zt

p2t

]

≡ D

[

zt

p2t

]

= −F

[

zt

x2t

]

(A.13)

[

zt+1

p2t+1

]

=

[

I 0

S21 S22

]

G

[

I 0

−N21 −N22

] [

zt

p2t

]

≡ H

[

zt

p2t

]

(A.14)

N =

[

S11 − S12S−122 S21 S12S

−122

−S−122 S21 S−1

22

]

=

[

N11 N12

N21 N22

]

(A.15)

xt = −[

N21 N22

][

zt

p2t

]

(A.16)

where F = −(R + BT SB)−1(BT SA + UT ), G = A − BF and

S =

[

S11 S12

S21 S22

]

(A.17)

partitioned so that S11 is (n − m) × (n − m) and S22 is m × m is the solution to the

steady-state Ricatti equation

S = Q − UF − F T UT + F T RF + β(A − BF )T S(A − BF ) (A.18)

28

The cost-to-go for the optimal policy (OP) at time t is

ΩOPt = −

1

2(tr(N11Zt) + tr(N22p2tp

T2t)) (A.19)

where Zt = ztzTt . To achieve optimality the policy-maker sets p20 = 0 at time t = 0. At

time t > 0 there exists a gain from reneging by resetting p2t = 0. It can be shown that

N22 < 0, so the incentive to renege exists at all points along the trajectory of the optimal

policy. This is the time-inconsistency problem.

A.1.1 Implementation

The rule may also be expressed in two other forms: First as

wt = D1zt + D2H21

t∑

τ=1

(H22)τ−1

zt−τ (A.20)

where D = [D1 D2] is partitioned conformably with zt and p2t. The rule then consists

of a feedback on the lagged predetermined variables with geometrically declining weights

with lags extending back to time t = 0, the time of the formulation and announcement of

the policy.

The final way of expressing the rule is express the process for wt in terms of the target

variables only, st, in the loss function. This in particular eliminates feedback from the

exogenous processes in the vector zt. Since the rule does not require knowledge of these

processes to design, Woodford (2003) refers to this as “robust” in describing it as the

Robust Optimal Explicit rule. This form of rule is demonstrated in the simple model in

section 5.1.

A.1.2 Optimal Policy from a Timeless Perspective

A.2 The Dynamic Programming Discretionary Policy

The evaluate the discretionary (time-consistent) policy we rewrite the cost-to-go Ωt given

by (A.5) as

Ωt =1

2[yT

t Qyt + 2yTt Uwt + w

Tt Rwt + βΩt+1] (A.21)

The dynamic programming solution then seeks a stationary solution of the form wt =

−Fzt in which Ωt is minimized at time t subject to (1) in the knowledge that a similar

procedure will be used to minimize Ωt+1 at time t + 1.

Suppose that the policy-maker at time t expects a private-sector response from t + 1

onwards, determined by subsequent re-optimisation, of the form

xt+τ = −Nt+1zt+τ , τ ≥ 1 (A.22)

The loss at time t for the ex ante optimal policy was from (A.8) found to be a quadratic

function of xt and p2t. We have seen that the inclusion of p2t was the source of the time

29

inconsistency in that case. We therefore seek a lower-order controller wt = −F zt with the

cost-to-go quadratic in zt only. We then write Ωt+1 = 12z

Tt+1St+1zt+1 in (A.21). This leads

to the following iterative process for Ft

wt = −Ftzt (A.23)

where

Ft = (Rt + λBTt St+1Bt)

−1(UTt + βB

Tt St+1At)

Rt = R + KTt Q22Kt + U2T Kt + KT

t U2

Kt = −(A22 + Nt+1A12)−1(Nt+1B

1 + B2)

Bt = B1 + A12Kt

U t = U1 + Q12Kt + JTt U2 + JT

t Q22Jt

J t = −(A22 + Nt+1A12)−1(Nt+1A11 + A12)

At = A11 + A12Jt

St = Qt − U tFt − F Tt U

T+ F

Tt RtFt + β(At − BtFt)

T St+1(At − BtF t)

Qt = Q11 + JTt Q21 + Q12Jt + JT

t Q22Jt

Nt = −Jt + KtFt

where B =

[

B1

B2

]

, U =

[

U1

U2

]

, A =

[

A11 A12

A21 A22

]

, and Q similarly are partitioned

conformably with the predetermined and non-predetermined components of the state vec-

tor.

The sequence above describes an iterative process for Ft, Nt, and St starting with some

initial values for Nt and St. If the process converges to stationary values, F, N and S say,

then the time-consistent feedback rule is wt = −Fzt with loss at time t given by

ΩTCt =

1

2zTt Szt =

1

2tr(SZt) (A.24)

A.3 Optimized Simple Rules

We now consider simple sub-optimal rules of the form

wt = Dyt = D

[

zt

xt

]

(A.25)

where D is constrained to be sparse in some specified way. Rule can be quite general. By

augmenting the state vector in an appropriate way it can represent a PID (proportional-

integral-derivative)controller.

30

Substituting (A.3) into (A.5) gives

Ωt =1

2

∞∑

i=0

βtyTt+iPt+iyt+i (A.26)

where P = Q + UD + DT UT + DT RD. The system under control (A.1), with wt given by

(A.3), has a rational expectations solution with xt = −Nzt where N = N(D). Hence

yTt P yt = z

Tt T zt (A.27)

where T = P11 − NT P21 − P12N + NT P22N , P is partitioned as for S in (A.17) onwards

and

zt+1 = (G11 − G12N)zt (A.28)

where G = A + BD is partitioned as for P . Solving (A.28) we have

zt = (G11 − G12N)tz0 (A.29)

Hence from (A.30), (A.27) and (A.29) we may write at time t

ΩSIMt =

1

2zTt V zt =

1

2tr(V Zt) (A.30)

where Zt = ztzTt and V satisfies the Lyapunov equation

V = T + HT V H (A.31)

where H = G11 − G12N . At time t = 0 the optimized simple rule is then found by

minimizing Ω0 given by (A.30) with respect to the non-zero elements of D given z0 using

a standard numerical technique. An important feature of the result is that unlike the

previous solution the optimal value of D, D∗ say, is not independent of z0. That is to say

D∗ = D∗(z0)

A.4 The Stochastic Case

Consider the stochastic generalization of (A.1)[

zt+1

xet+1,t

]

= A

[

zt

xt

]

+ Bwt +

[

ut

0

]

(A.32)

where ut is an n × 1 vector of white noise disturbances independently distributed with

cov(ut) = Σ. Then, it can be shown that certainty equivalence applies to all the policy

rules apart from the simple rules (see Currie and Levine (1993)). The expected loss at

time t is as before with quadratic terms of the form zTt Xzt = tr(Xzt, Z

Tt ) replaced with

Et

(

tr

[

X

(

ztzTt +

∞∑

i=1

βtut+iu

Tt+i

)])

= tr

[

X

(

zTt zt +

λ

1 − λΣ

)]

(A.33)

31

where Et is the expectations operator with expectations formed at time t.

Thus for the optimal policy with commitment (A.19) becomes in the stochastic case

ΩOPt = −

1

2tr

(

N11

(

Zt +β

1 − βΣ

)

+ N22p2tpT2t

)

(A.34)

For the time-consistent policy (A.24) becomes

ΩTCt = −

1

2tr

(

S

(

Zt +β

1 − βΣ

))

(A.35)

and for the simple rule, generalizing (A.30)

ΩSIMt = −

1

2tr

(

V

(

Zt +β

1 − βΣ

))

(A.36)

The optimized simple rule is found at time t = 0 by minimizing ΩSIM0 given by (A.36).

Now we find that

D∗ = D∗

(

z0zT0 +

β

1 − βΣ

)

(A.37)

or, in other words, the optimized rule depends both on the initial displacement z0 and on

the covariance matrix of disturbances Σ.

B Software

A number of packages exist to implement these procedures. Associated with Gerali and

Lippi (2002), Matlab programs to compute the optimal commitment and discretionary

policies are available on request from the authors. A feature of this package is that it

extends the procedures to the imperfect information case. At the ECB, Adalid et al.

(2005) report the use of Matlab programs to compute all three types of rules set out in

this lecture. The exercises reported here were carried out using software written by myself,

Joseph Pearlman and other co-authors. It is written in FORTRAN and is not user-friendly.

However we do intend to incorporate these routines into WinSolve, a well-known package

for non-linear as well as linear models written by Richard Pierce.

References

Adalid, R., Coenen, G., McAdam, P., and Siviero, S. (2005). The Performamnce and

Robustness of Interest-Rate Rules in Models of the Euro Area. International Journal

of Central Banking, 1(1), 95–132.

Batini, N., Justiniano, A., Levine, P., and Pearlman, J. (2004). Robust Inflation-Forecast-

Based Rules to Shield against Indeterminacy. IMF Discussion Paper, forthcoming, pre-

sented at the 10th International Conference on Computing in Economics and Finance,

Amsterdam, July 8-10, 2004, available at www.econ.surrey.ac.uk/people/index.htm.

32

Benigno, P. and Woodford, M. (2003). Optimal monetary and fiscal policy: A linear-

quadratic approach. presented at the International Research Forum on Monetary Policy

in Washington, DC, November 14-15, 2003.

Brainard, W. (1967). Uncertainty and the effectiveness of policy. American Economic

Journal, 47(2), 411–425.

Choudhary, A. and Levine, P. (2005). Idle Worship. Economic Letters. Forthcoming.

Clarida, R., Galı, J., and Gertler, M. (1999). The Science of Monetary Policy: A New

Keynesian Perspective. Journal of Economic Literature, 37(4), 1661–1707.

Currie, D. and Levine, P. (1993). Rules, Reputation and Macroeconomic Policy Coordi-

nation. CUP.

Federal Reserve Bank of Kansas (2003). Monetary Policy and Uncertainty: Adapting to

a Changing Economy. Kansas City: Federal Reserve Bank of Kansas City.

Gerali, A. and Lippi, F. (2002). Optimal Control and Filtering in Linear Forward-Looking

Economics: A Toolkit. Mimeo .

Juillard, M., Karam, P., Laxton, D., and Pesenti, P. (2004). Welfare-based monetary

policy rules in an estimated DSGE model in the US economy. unpublished manuscript,

Federal Reserve Bank of New York.

Kim, J., S. J. E. S. and Sims, C. (2003). Calculating and Using Second Order Accurate

Solutions of Discrete Time Dynamic Equilibriym Models. Mimeo .

Levine, P., Pearlman, J., and Pierse, R. (2005). A Users’ Guide to Linear-Quadratic

Approximation in Dynamic Macroeconomic Models. Mimeo .

Poole, W. (1970). Optimal choice of monetary policy instrument in a simple stochastic

macro model. Quarterly Journal of Economics, 84(2 (May)), 197–216.

Walsh, C. (2003). Implications of a changing Economic Structure for the Strategy of

Monetary Policy. In F. R. B. of Kansas City, editor, Monetary Policy and Uncertainty:

Adapting to a Changing Economy. Kansas City: Federal Reserve Bank of Kansas City.

Woodford, M. (2003). Foundations of a Theory of Monetary Policy. Princeton University

Press.

33

0 5 10 15 20 25 30−0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

TIME IN QUARTERS

INF

LAT

ION

DISCRETION

COMMITMENT

Figure 1: Quarterly Inflation

0 5 10 15 20 25 300

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.04

OU

TP

UT

GA

P

TIME IN QUARTERS

COMMITMENT

DISCRETION

Figure 2: The Output Gap

34