Embed Size (px)

Citation preview

1

Robotics Market Overview

– Prepared for Intesa Sanpaolo Innovation Centre –

January 2017

2

Context and headlines (1/4)

• The current wave of activity in the robotics sector, sparked in particular by the advent of the IIoT, has

been characterised by some as a “4th Industrial Revolution”

• From a technology point of view, the market is moving rapidly from semi-automated to fully autonomous

machines that can act and make decisions independently

• Interest is not, however, only centred on industrial applications, with consumer robots the largest

segment on an absolute basis and the use of commercial robots for warehouse logistics and oceanic

exploration growing rapidly

• Consumer Robots

• Greater awareness of the time and effort-saving potential of consumer robots is driving interest from

many consumers; nonetheless, the relatively high acquisition and maintenance costs act as a

continuing disincentive to some customers

• On a geographical basis, North America and Asia lead the way but Europe is an emerging market from

a supply and demand perspective

• Frost & Sullivan segments the consumer robots space into four categories; Domestic & Task and

Security & Surveillance robots are expected to witness the most widespread adoption between 2016

and 2020 but there is also innovation across all four categories including Personal & Education and

Social & Home

• Commercial Robots: Warehouse Logistics

• In the logistics segment, the use of Automated Guided Vehicles (AGVs) is leading to more accurate

order picking and the faster transportation of pallets

3

Context and headlines (2/4)

• Commercial Robots: Warehouse Logistics (continued)

• Frost & Sullivan calculates that, for every dollar spent on 10 AGVs, a company stands to make a return

on its investment of $0.32

• Moving forward, aerial logistics and distribution systems will be key

• Seegrid is a company which is transforming material handling through the flexibility, simplicity and

affordability of its with Vision Guided Vehicles

• Commercial Robots: Oceanic Exploration

• The depletion of valuable resources on land has brought deep sea mining, enabled by Unmanned

Underwater Vehicles (UUVs), to greater prominence

• Frost & Sullivan calculates that, for every dollar spent on a UUV worth $5 million, a company stands to

make a return on its investment of $0.77

• Moving forward, oceanic exploration will witness the adoption of Autonomous Underwater Vehicles

(AUVs) with specialised robots for specific operations

• Bluefin Robotics modern generation of AUVs combine precise navigation and advanced software

making it a leader in the sub-sea robotics market

• Commercial Unmanned Aircraft Systems

• Commercial Unmanned Aircraft Systems (UAS) can be classified according to platforms with the

consumer segment leading demand in unit terms

4

Context and headlines (3/4)

• Commercial Unmanned Aircraft Systems (continued)

• Technological advances, computer chip manufacturing techniques and economies of scale have

driven, and will continue to drive, down costs; nonetheless, the presence of varying and often evolving

regulations both across and within regions will act as a restraint to greater deployment

• Frost & Sullivan expects unit shipment growth (51.2% CAGR, 2014-202) to outpace revenue growth

(45.8%) as prices continue to fall overall

• DJI is the clear market leader with a share of 24.9% in revenue terms, compared with just 2.5% for

Parrot/senseFly and (1.3%)

• From an application point of view, photography/video is the most common usage followed by

mapping/surveying but Inspection/monitoring and precision agriculture are emerging

o The inspection and monitoring services vertical is hard to define but typically includes the

periodic and regular evaluation of (largely) infrastructure assets

o Here, the market is underpinned by the very significant number of building, tower and property

inspections that are required each year; there is however a need for establishing global processes

and standards which allow the capture of universally comparable regulation-grade data

o On a regional basis, Europe is home to the top two oil & gas inspection companies which are

rapidly expanding their global footprint

o From a competitive point of view, drone service companies are partnering with third parties to

provide UAS operations which are specific to inspection/monitoring

o OEMs are also developing tailor-made solutions

5

Context and headlines (4/4)

• Commercial Unmanned Aircraft Systems (continued)

o The precision agriculture vertical has generated much interest in recent years with UASs now

finding concrete uses cases across a range of applications

o Drones have the potential to materially cut costs, save time and increase output across both arable

and livestock farming

o There remains some scepticism, however, as to whether they will be able to produce the return on

investment which has been suggested by the industry

o In Europe, Airinov has assisted over 5,000 farmers across the continent and is leading a project to

grow usage in Africa

o From a competitive point of view, large agriculture companies are rapidly integrating drones into

their smart farming product offerings

o Partnerships between OEMs and with software providers are also delivering scalable service

options for precision agriculture customers

6

Introduction

7

Mobile robots range from unmanned ground to humanoid legged, aerial and maritime

vehicles that can operate effectively on land, in the air and underwater

Mobile Robot by Classification, Global, 2016

Unmanned Ground Vehicles

Humanoid legged robot

Unmanned Aerial Vehicles

Unmanned Maritime Vehicles

1 2 3 4

Better mobility across

rough terrain using skid

steer drive

Superior traction –

ability to push/pull loads

better

Leg on wheels

For all types of terrains

4-6 legged robots most

successful and stable

Powered aerial vehicles

with pre-programmed

flight plans

Cost effect and

minimizes risk on life

Self programmed

robots gathering data

on certain parts of

water bodies

Frost & Sullivan

Images; wikimedia.org

8

The current wave of activity in the robotics sector, sparked in particular by the advent of

the IIoT, has been characterised by some as a “4th Industrial Revolution”

4th Industrial Revolution

Use of cyber-physical systems

3rd Industrial Revolution

Use of IT systems and automation

2nd Industrial Revolution

Use of Electricity

1st Industrial Revolution

Mechanical Manufacturing

Impact of Robotics on Industrial

Revolution

Industrial Revolution, 1800-2014

1st Robotic

Revolution

Industrial

automation

2nd Robotic

Revolution

Sensitive, safe

robot-based

automation

3rd Robotic

Revolution

Mobility

4th Robotic

Revolution

Intelligent and

perceptive

robot systems

Robots to

enable the

Self-

Programmed

and Smart

Factories of

Industry 4.0

Frost & Sullivan

9

Technology Roadmap for Robots, Timeline: 2000-2020

From a technology point of view, the market is moving rapidly from semi-automated to

fully autonomous machines that can act and make decisions independently

Autonomous Machines; Eg-

Collaborative Robots

>2020

Initial stages of Cognitive systems

2015

Semi-Autonomous Machines; Eg-

Remotely Operated Vehicles)

2010

Wearable Technology; Eg-

Exoskeletons

2005

Unmanned Machines; Eg- AGV’s

2000

Remotely Interfaced Systems

Period of sliding autonomy Full Autonomy

Machines controlled

remotely by telepresence-

nan extensions

Machines to make basic decisions

Common workplace with

very limited workplace

Intelligent machines with

human emotions that can converse fluently and adapt

to varied environments

Controlled by Ware-House-Management

systems

Frost & Sullivan

Images; wikimedia.org

10

Major robotic applications

2012 2020

Sales Unit

shipment

Sales- Unit

Shipment

CAGR

Logistics 1,400 95,000 69.4%

Defence 6,200 126,000 40.0%

Autonomous Cars Nil 180,000 Un-Defined

Consumer 4,000,000 25,000,000 25.7%

Oceanic Exploration 500 2,500 22.3%

4,008,100 units $25,403,500 units Total Sales Unit Shipment

1

2

3

4

5

Frost & Sullivan

Interest is however not only centred on industrial applications, with consumer robots

the largest segment on an absolute basis and the use of commercial robots for warehouse

logistics and oceanic exploration growing rapidly

All figures are rounded. The base year is 2012

Major robotic applications by sales penetration, 2012 and 2020

11

Consumer segment

1 2 3 4

12

Compared to humans performing a domestic chore using conventionally tools, consumer robots will be able to perform the same task

more efficiently with increased productivity and better end results. The robots can also help people avoid the drudgery of performing

household chores.

IMPACT

HIGH

MEDIUM

LOW

Dri

ve

rs

Perform tasks

more efficiently Time saving Improved safety

Eco- friendly and

easy to control Short-term

(1-2 years)

Long-term

(5-6 years)

Medium-term

(3-4 years)

Normally a person takes a few hours to complete a domestic task. By assigning a robot to perform the task, the user will be able to save

his/her own personal time, as the time taken to normally complete the task is greatly reduced.

Perform tasks

more efficiently

Time saving

Improved safety

Eco-friendly

and easy to

control

People are prone to hurting themselves while doing domestic work. By assigning a robot to perform the task, accidents and human error

can be totally eliminated.

People tend to generally more use excess resources, such as water, than is required to complete a domestic task. Consumer robots,

due to their high accuracy and precision, only use the amount of resources required to complete the task. At the same time, the user can

also track, monitor, and control the robot’s performance, activities, and resources used.

Greater awareness of the time- and effort-saving potential of robots is driving interest

from many private consumers

Consumer Robot: Drivers, Global, 2016–2020

Frost & Sullivan

13

Consumer Robot: Challenges, Global, 2016–2020

HIGH

MEDIUM

LOW

Ch

all

en

ge

s

Need for FundingAccurate mapping and

control features

User Acceptance of

robots

Nonetheless, the relatively high acquisition and maintenance costs act as a continuing

disincentive to some customers

Relatively high

costs

Frost & Sullivan

Short-term

(1-2 years)

Long-term

(5-6 years)

Medium-term

(3-4 years)

Consumer robots are developed using advanced robotic technology and equipped with state-of-the art components, such as sensors and

software for mapping, localization, and object detection along with communications capability. Therefore, the selling price of the bots can

be relatively high (although robot vacuum cleaners tend to be priced from a low of below $200 to around $1,200). At the same time, cost

associated with maintaining and changing the components of the robot is also expensive.

Robotic technology is still in the emerging or development stage, and it requires immense R&D to develop a robot to assist people.

Currently, the consumer robots in the market perform and complete the assigned task. They can require more accurate control features

and mapping systems to efficiently perform the task without constant monitoring from the user.

Relatively high

purchase and

maintenance

cost

Accurate

mapping and

control features

Need for

funding

User

acceptance of

robots

Companies and developers who have been innovating and building prototypes of robots capable of performing various tasks need the

required funding to bring the designs to a manufacturing scale and produce the robots.

One of the key hindrances to commercialization and wide-scale adoption is the individual’s mind-set and acceptance level to purchase

an expensive robot to perform domestic chores. People can be skeptical in giving control over to a robot to perform a task which they

have been doing for years.

IMPACT

14

Technology developments

Adoption

At present, the North American region is the

leader and largest contributor to the consumer

robot market. Key companies, such as Aqua

Products, iRobot Corporation, and Neato

Robotics Inc., are constantly designing and

developing new robotic technologies and

systems to assist humans with their day-to-day

life. The technology development and wide-

scale adoption intensity are very high in this

region. Many large companies such as

Whirlpool Corporation and Procter & Gamble

are investing in development of consumer

robots.

The APAC region has been tremendously

contributing toward the development of

consumer robots. With many robot

manufacturing facilities set up around this

region, countries such as China, Japan, and

Korea are major contributors toward the

consumer robotics technology advancement

and product development. Technology

development in relation to consumer robots is

high in this region, but at the same time wide-

scale adoption may be somewhat impeded

because of the high population and less

participation from countries such as Malaysia,

Indonesia, and India. Robot vacuums have

opportunities in APAC regions with a rising

standard of living and where dirt is created by

generations living in the same home.

The European region is an emerging market for

the consumer robots industry. This region is

considered to be a heterogeneous market

where both technology development and

technology adoption are at the same pace.

Technology developments in the European

region are presently at a medium intensity but

wide-adoption scale of this technology is

anticipated in the near future (2016–2020).

North America EuropeAsia-Pacific

Technology developments

Adoption

Technology developments

Adoption

Intensity of technology

development and adoption

footprint

On a geographical basis, North America and Asia lead the way but Europe is an emerging

market from a supply and demand perspective

Frost & Sullivan

High

Low

15

Overall, 18,500 patents have been filed over the last 4.5 years with the market expected to

double in size to $1.5b by 2020

A total of 18,550 patents have been filed across the globe in relation to consumer robots technology, product

design and development in the period from 1st January 2012 to 31st August 2016. From this analysis, it is clear

that the North American region has registered the most patents, followed by APAC and Europe.

Patent analysis

Market outlook

Providing advantages across applications, the development and adoption of consumer robot technology is

destined to significantly increase over the next 5 years from 2016 to 2020. Third party sources have predicted that

the revenue stemming from the market will quadruple and exceed 1.5 b USD by the end of 2020.

16

Frost & Sullivan segments the consumer robots space into four categoriesS

ecu

rity

& S

urv

eil

lan

ce

So

cia

l&

Ho

me

Do

me

sti

c&

Task

Pe

rso

na

l&

Ed

uc

ati

on

al Personal robots are designed and

developed to assist and help people with

their day-to-day tasks. These interactive

robots can listen to instructions and

commands from the user to perform various

tasks such as sending e-mails, messaging,

calendar scheduling, collect information,

and basically work as personal assistants.

Similarly, educational robots are programed

to teach and enhance the learning

experience to better reach and impact

students. Some robots are specially

developed to educate and help special

needs students to quickly grasp and learn

subjects.

Domestic and task robots are developed to

perform household chores and domestic

tasks such as vacuuming, cleaning (mopping

or scrubbing floors), gardening, cleaning

windows, or pools. Typically, users will be

able to monitor, track, and control these

robots to perform the task. These robots are

designed to work economically and are eco-

friendly. Owing to the advanced technology,

precision, and accuracy, these robots also

help in conserving resources such as water

and electricity, which are generally wasted

while performing domestic work.

One of the popular categories in consumer

robotics is security and surveillance robots.

With the increase in crime rates, the

adoption rate of these novel robots has

been increasing in the recent years. These

robots allow users to even remotely monitor

their homes, offices, and other building

spaces. Some robots in this category are

programed to even directly alarm the police

and family members during security threats

and even detect unusual circumstances

such as fire, burglary, and natural disasters.

Social and home robots are developed to

interact and communicate with humans.

These advanced robots are programed to

perform several tasks and assist humans

with their daily life. These robots can

perform several roles such as a security bot

that patrols the house for security breaches,

serving as an edutainment system for

children or even assisting in elder care.

Home robots are also programed to see,

hear, speak, and help in collecting and

delivering information, controlling the

environment, capturing pictures, and even

managing family activities.

Frost & Sullivan

17

Domestic & Task and Security & Surveillance robots are expected to witness the most

widespread adoption between 2016 and 2020

0

0,5

1

1,5

2

2,5

3

TechnologyReadiness

TechnicalFeaturers

Ability to ServeMarket Neds

Breadth ofApplication

No.of Patents

Wide-scaleadoption

Personal & Educational Security & Surveillance

Social & Home Domestic & Task

• The graph depicts the technology benchmarking of the

four main types of consumer robots (personal &

educational, security & surveillance, social & home, and

domestic & task robots) in the next 5 years (2016–

2020). Personal & educational and social & home

robots are expected to witness a significant change in

relation to technology readiness. These robots along

with domestic and task robots are expected to undergo

a radical impact in terms of ability to serve market

needs.

• Similarly, security & surveillance and domestic & task

robots in relation to technology readiness are expected

to undergo a radical change in the next 5 years.

• Constant development and innovations are being

implemented for the advancement of consumer robots.

A significant increase in the technical features of

personal & educational, security & surveillance, and

domestic & task robots can be anticipated in this 5

years’ time frame.

• Key players and start-ups have started to enter this

novel market and are developing more advance

consumer robotic solution. This has significantly

increased the number of patent filings in recent years.

Personal & educational and security & surveillance

robots are anticipated to undergo a significant change,

whereas social & home and domestic & task robots will

have a radical change with relation to the number of

patents being filed in the next 5 years (2016–2020).

Frost & Sullivan

Technology Benchmarking of Different Consumer Robots,

Global, 2016‒2020

18

Amaryllo International B.V. is one of the key players in

developing state-of-the-art home security robots with 360-

degree auto-tracking technology.

The company has developed an intelligent robotic security

solution called ATOM capable of recognizing and

interacting with people.

• Home security has always been an threat to people across

the world. With a growing crime rate, it is increasingly

dangerous to leave the house unmonitored.

• People are installing security devices and robots for their

own safety and protection. These devices may not have

sufficient performance to provide the necessary security

that is required.

• To cater this requirement, Netherlands-based Amaryllo

International B.V. has developed an intelligent security

robot called ATOM, which can recognize and interact with

people and at the same time autotrack intruders.

• This novel security robot is integrated with an advanced

high-powered CPU to detect and recognize people’s faces

immediately.

• ATOM is also programed to check e-mails every 2 mins

and notify the user with the help of a built-in speech

function. It is also programed to announce hourly time and

to greet people.

Description

Amaryllo International B.V. is headquartered in Amsterdam,

the Netherlands.

Technology Attributes

• ATOM is also powered by the company’s proprietary

standalone auto-tracking and 360-degree tracking

network technology, which allows the robot to see and

follow intruders 360 degrees even in complete darkness.

• The robot has top-notch 256-bit encryption technologies,

records video, and, with the help of the company’s peer-

to-peer video server, automatically adjusts video quality.

• ATOM includes unlimited cloud storage where all the

recorded videos are stored.

Requirement

Technology Readiness

Readiness Level 1 2 3 4 5 6 7 8 9

Innovation in the Security & Surveillance category

e.g. Amaryllo, Netherlands

Security & Surveillance

Frost & Sullivan

19

KinderLab Robotics focuses on developing interactive and

educational robotic toys for engaging young children to

learn advanced technology.

The company has developed a robot kit, KIBO, for young

children (under eight years old). Kids will be able to build

their own robots using the kit and can program the robot to

perform different activities such as racing and dancing.

• The learning process for children starts at a very young

age. Parents are focusing on investing money in toys,

which are engaging both, interactive and educational.

• With the arise in technology improvement for day-to-day

life, it has become a necessity that children start to learn

and implement these technologies from a very young age

for a better future.

• To aid children in the learning process, KinderLab Robotics

has developed a educational robot, KIBO.

• This novel educational robot was developed based on

intense research on learning technologies and child

development at Tufts University, US.

• Children will be able to build and customize the robot

according to their desires.

• The robot is equipped with motors, wheels, and integrated

with light, sound, and distance sensors for movement and

performing various actions.

Description

The company is headquartered in Massachusetts, US.

Technology Attributes

• Children will able to program and provide specific

instructions to the robot to perform a series of actions by

scanning a special set of wooden blocks representing a

different programing function provided with the robot kit.

• KIBO uses an open-ended platform allowing children to

set different sequences of code to provide a string of

continuous commands by scanning multiple blocks

before activating the robot.

Requirement

Technology Readiness

Readiness Level 1 2 3 4 5 6 7 8 9

Innovation in the Personal & Education category

e.g. KinderLab, US

Personal & Educational

Frost & Sullivan

20

InGen Dynamics Inc. concentrates on designing and

developing next-generation robotic solutions to assist

humans in their day-to-day life.

InGen Dynamics Inc. has developed an next-generation

personal home robot called Aido with advanced features

and capabilities.

• The key advances in the Internet-of-Things (IoT) have

been a major driver for the robotics industry. Companies

around the world are adopting advanced technologies to

develop robotic solutions to assist people.

• InGen Dynamics Inc. is one such company that has

developed an interactive personal home robot called Aido.

Aido is programed with state-of-the-art features and

capabilities to assist and ease people in their life and work.

• Aido is powered by two advanced operating systems and

has an Android Lollipop user interface.

• The robot is also compatible and runs on the Ubuntu

operating system.

• The bottom of the robot is designed to roll like a ball

omnidirectionally, allowing the robot to move freely and

maneuver around complex places. The robot has

microphones for voice commands, provides obstacle

recognition and avoidance, and has haptic touch sensors,

a Global Positioning System (GPS), and sensors to detect

light, air quality, noise, and pressure.

• With the help of the robot’s visual manager, homeowners

can create sets of activities for particular days or time

periods such as one’s vacation.

Description

The company is headquartered in California, US.

Technology Attributes

• Users will also be able to control, monitor, and even

create tasks for the robot using the Aido mobile app.

• Since Aido software kit uses C and python languages,

users will be able to program new features according to

their requirements.

• Aido is also integrated with an interactive head projector

and an optional multimedia projector to project the

required information on screen or on the wall.

Requirement

Technology Readiness

Readiness Level 1 2 3 4 5 6 7 8 9

Innovation in the Social & Home category

e.g. InGen Dynamics, US

Social & Home

Frost & Sullivan

21

Ecovacs Robotics develops robotic solutions to assist

consumers with household work. The company’s portfolio

includes floor and window cleaning solutions, amongst

others.

Ecovacs Robotics has designed and developed an ideal

vacuum and mopping robot called DEEBOT M85 falling

under its DEEBOT floor cleaning robot portfolio.

• Performing household chores has never been anyone's

cup of tea. Cleaning and maintaining floors have always

been difficult and require proper skill to clean the house to

perfection.

• Key companies have adopted robotic technology to

develop automated devices that are capable of performing

household chores.

• Ecovacs Robotics’ DEEBOT portfolio consists of advanced

floor cleaning robots. The latest addition to this series is the

DEEBOT M85, which is incorporated with advanced

features to perform floor cleaning actions very efficiently.

• The robot is incorporated with the company’s proprietary

SMART MOTION technology, which scans the floor for

dust and dirt and covers the particular area multiple times.

• A water reservoir equipped in the robot automatically

dampens half of the wet/dry cleaning cloth to clean heavy

stains and debris. The cleaning process is followed by a

mopping process to dry the floor thoroughly.

• The robot automatically returns to the docking station to

recharge when the battery is low and does not require any

human assistance for docking or charging.

Description

The company is headquartered in Japan with subsidiaries

in Europe, North America, and Japan. Ecovacs is among

the top 5 home robotics brands.

Technology Attributes

• The M85 robot is also equipped with anti-drop sensors to

prevent the robot from falling over when cleaning

elevated spaces and staircases.

• The anti-collision sensors also help the robot to detect

objects and obstacles. When the robot encounters an

obstacle, the sensor signals the robot to change its path.

• The robot can be operated using a remote control and at

the same time has multiple floor cleaning modes to

ensure efficient cleaning.

Requirement

Technology Readiness

Readiness Level 1 2 3 4 5 6 7 8 9

Innovation in the Domestic & Task category

e.g. Ecovacs, China

Domestic & Task

Frost & Sullivan

22

Commercial segment

Warehouse logistics

1 2 3 4

23

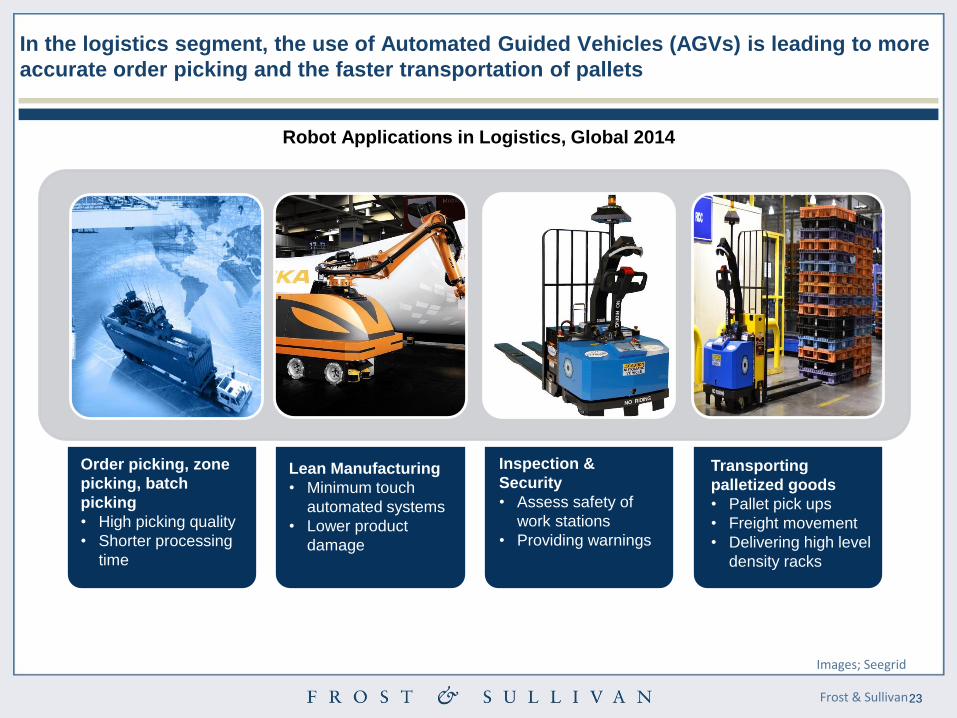

In the logistics segment, the use of Automated Guided Vehicles (AGVs) is leading to more

accurate order picking and the faster transportation of pallets

Inspection &

Security

• Assess safety of

work stations

• Providing warnings

Transporting

palletized goods

• Pallet pick ups

• Freight movement

• Delivering high level

density racks

Lean Manufacturing

• Minimum touch

automated systems

• Lower product

damage

Order picking, zone

picking, batch

picking

• High picking quality

• Shorter processing

time

Frost & Sullivan

Images; Seegrid

Robot Applications in Logistics, Global 2014

24

Without AGV

Type Number Rate Total Cost

Labor costs 1

(3 shifts)2

Manual forklift

Costs

+ Total

Costs

A

B

A B

1 2

$31,680

$41,000

12

6

1 2X =

1 2X =

$1,140,000

$41,000

$1,181,000 (=$1,140,000 + $41,000)

With AGV

Type Number Rate Total Cost

Labor reduction

(3 shifts)2

New Machinery

Investment-AGV

+ Total

Savings

A

B

A B

1 2

$31,680

$195,0004

63

10

1 2X =

=

$570,000

Nil4

$570,000 (=$570,000 + $0)

Calculating Yearly Return on Investment for AGV’s

Investment

Returns

Year 1 Year 2 Year 3 Year 5

Notes

1. Assume 12 laborers initially

2. Laborers work in 3 shifts for 8 hours/day,

22 days/month and 12 months

3. 10 AGV = 6 laborers

4. Investment not to be included to calculate

total cost savings as it is treated separately

5. Year 1 ROI calculation = cost of

investment of 10 AGV ($1.75 Million) +

maintenance cost ($50k) + installation

costs ($200k)

6. Year 2 ROI calculation= Maintenance cost

7. Information on the cost-benefit analysis

has been obtained from primary and

secondary sources

Net Savings Year 1 = Without AGV – With AGV = $611,000

Frost & Sullivan calculates that, for every dollar spent on 10 AGVs, a company stands to

make a return on its investment of $0.32

Year 4

Frost & Sullivan

25

Moving forward, aerial logistics and distribution systems will be key

Images; wikimedia.org

Jafza- Aerial Delivery

2022

Seegrid

2018

Mercury xPRESS

2016

Rapidstore Mini load ASRS

2012

Nissan Forklift- QX2 Series

1990

Fully Automated

warehouse -order picking

systems

Mini load

technologies-

Automated

storage and

retrieval systems

Radio Frequency

identification –

Voice recording

pick up

Automated unmanned

aerial logistics and distribution

Warehouse control

systems= Forklift

fleet with data

tracking sensor

Frost & Sullivan

Expanding capabilities of Automated Guided Vehicles, Timeline: 1990-2022

26

Seegrid is a company which is transforming material handling through the flexibility,

simplicity and affordability of its with Vision Guided Vehicles

Vision

Guided

System

Start Button

Easy to use

HMI screen

Safety, Anti

Collusion

sensors

Emergency

Stop

bumpers

Battery

Charger

24V(3) 510

amp/hr

batteries

CMOS

imager

Flexibility

Day one operation

No infrastructure required for functioning

Flexible & easy use- Changes routes as required

Manual & Automatic modes

Efficiency

↓ long inefficient manned guidance

24/7 functional

Enhances productivity with quick uptime

Safety

Zero product damage

Eliminates employee injuries

.↓ in equipment damage

Affordability

↓ in labour and maintenance costs

Rapid ROI’s

↓ cost of ownership

Seegrid’s Automated Guided Vehicles

System

&navigation

controller

Seegrid’s Vision Guided Technology

Frost & Sullivan

Images; Seegrid

27

Commercial segment

Oceanic exploration

1 2 3 4

28

The depletion of valuable resources on land has brought deep sea mining, enabled by

Unmanned Underwater Vehicles (UUVs), to greater prominence

Mining Support:

Production Support

Vehicle

Launch and Recovery

System: Riser and

Lifting

Systems

Sea-bed Mining

System: Sub-sea

Slurry Lift Pump

Deep-sea Mining System

Deep-sea mining refers to a new and experimental process

of retrieving the essential minerals such as poly-metallic

nodules and ferromanganese crusts from the sea floor

Estimated Value of Precious Metals and

Minerals, Global, 2030

Manganese (Yield Per Year)

$900–$950 M

$750–$800 M

$250–$300 M

$100–$150 M

Nickel (Yield Per Year)

Copper (Yield Per Year)

Cobalt (Yield Per Year)

$150 trillion

worth of gold on

seabed across the

globe—nearly 10

times the US GDP

$8.20 billion

estimated total value

of known seabed

minerals in the

Red Sea basins

Estimated Value of Economy, 2030

$140 million

Contribution of Papua

Guinea's deep-sea

mining project to the

country’s economy

$60 billion

Contribution of deep-

sea mining projects to

the UK economy

over the next 30 years

Frost & Sullivan

29

Without UUV

Type Number Rate Total Cost

Labor costs

(2 shifts)

Manned

machinery costs

+ Total

Costs

A

B

A B

1 2

$65,000

$3,000,000

16

1

1 2X =

1 2X =

$2,080,000

$3,000,000

$5,080,000 (=$2,080,000 + $3,000,000)

With UUV

Type Number Rate Total Cost

Labor reduction

(2 shifts)

New machinery

Investment-UUV

+ Total

Savings

A

B

A B

1 2

$65,000

$5,000,000

10

1

1 2X =

=

$1,300,000

Nil

$1,300,000 (=$1,300,000 + $0)

Investment

Returns

Year 1 Year 2 Year 3 Year 4 Year 5

Frost & Sullivan calculates that, for every dollar spent on a UUV worth $5 million, a

company stands to make a return on its investment of $0.77

Frost & Sullivan

Notes

1. 1UUV = 6 laborers

2. Crew men work in 2 shifts for 12

hours/day, 28 days/month and 12 months

3. Investment not to be included to calculate

total cost savings as it is treated separately

4. Year 1 ROI calculation = cost of

investment of 1 UUV ($5 Million) +

maintenance cost ($500k) + installation

costs ($250k

5. Year 2 ROI calculation= Maintenance cost

6. Information on the cost-benefit analysis

has been obtained from primary and

secondary sources

Net Savings Year 1 = Without UUV – With UUV = $3,780,000

Calculating Yearly Return on Investment for UUV’s

30

Images; Bluefin

Task specific hybrid robots

2025

Mature AUV platforms

2020

Autonomous Under-water Vehicles

2012

Remotely Operated Vehicles (ROV’s)

1990’s

Development of AUV’s Vs ROV’s

Use of mobile platforms for increased reliability

and endurance

Onboard sensor processing

Adoption of replicable mobile platforms

Specialized robots for particular operations

such as defense and oil and gas applications

ROV’s to play a key role alongside AUV’s

in future sub-sea explorations

Moving forward, oceanic exploration will witness the adoption of Autonomous Underwater

Vehicles (AUVs) with specialised robots for specific operations

Frost & Sullivan

Expanding Capabilities of UUV’s: Timeline 1990-2025

31

Images; Bluefin

Key points on Bluefin’s AUV

business

• Bluefin provides full service

autonomous underwater

vehicles, sub-sea power and

ROV’s

• Full AUV life-cycle provider

(R&D, production, testing,

training and operations)

• Bluefin stands second in the

market with its competitors

being Kongsberg, Gavia,,

International Submarine

Engineering –Canada

• Major Bluefin consumers for

oil & gas exploration – Shell,

Total, Mobil, etc

• Collaboration with major

institutes like MIT, University

of Victoria, and University of

central Florida for

Oceanographic research

Bluefin 21

• Ability to carry multiple sensors and payload at once

• High energy capacity for extended operations at great depth•Bluefin 12D

• Greater payload and energy capacity than its counterpart

• Efficient packaging customizable

Bluefin !2S

• Low cost navigation solution

• 4.5 kwh energy capacity

Bluefin 9M

• Lightweight 2-man portable AUV

• User-selected payloads for multiple applications •

Bluefin 9

• Lightweight 2-man portable AUV

• Side scan sonar and camera

HAUV

• High resolution imaging sonar•

Hawkes ROVs

• Lightweight portable AUV

• Side scan sonar

Bluefin’s Product Portfolio

Bluefin Robotics modern generation of AUVs combine precise navigation and advanced

software making it a leader in the sub-sea robotics market

Frost & Sullivan

32

Unmanned Aircraft Systems

1 2 3 4

33

Commercial ($50–100K)

4.3%, 0.4%

Aeryon Labs Scout

Enterprise (>$100K)

2.9%, 0.1%

Yamaha RMAX Fazer Edition

Fixed Wing

29.2%, 7.1%

senseFly eBee

Commercial Unmanned Aircraft Systems (UAS) can be classified according to platforms

with the consumer segment leading demand in unit terms

Consumer (<$1,500)

9.1%, 47.4%

Parrot Bebop

Prosumer ($1,500–$5,000)

25.8%, 36.8%

Steadidrone QU4D

Professional ($5–50K)

28.6%, 8.2%

senseFly eXom

Frost & Sullivan

Total Commercial UAS Market: Current Platform Segments with Sample Aircraft, Global, 2014

Images; Parrot, senseFly ltd. and Aeryon Labs photos used with permission

In italics, share of the overall market in revenue and unit terms in 2014

34

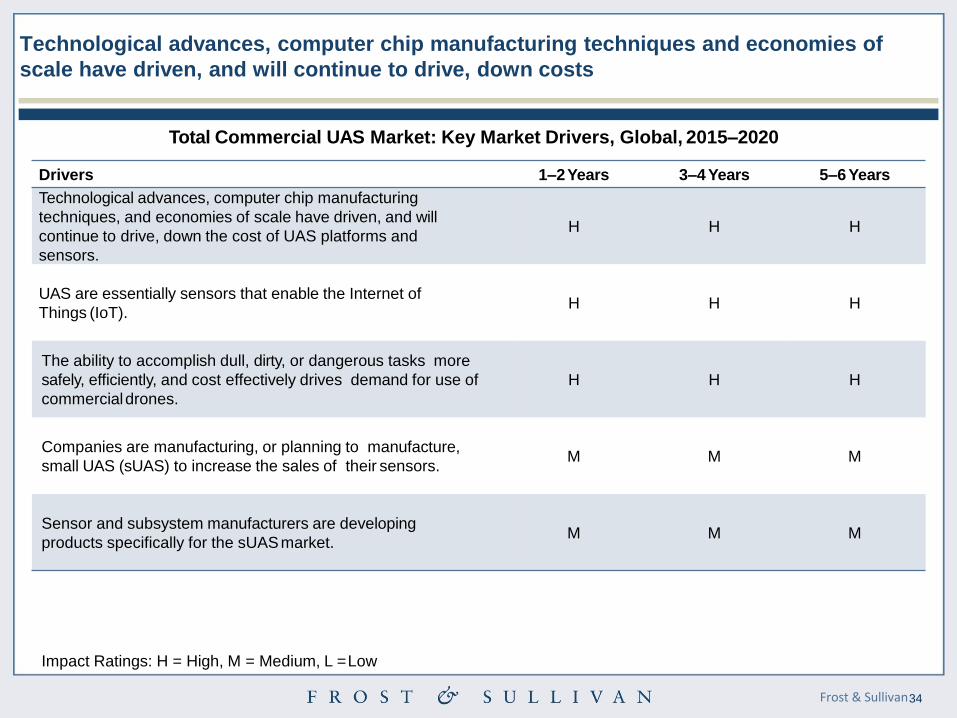

Drivers 1–2Years 3–4 Years 5–6 Years

Technological advances, computer chip manufacturing

techniques, and economies of scale have driven, and will

continue to drive, down the cost of UAS platforms and

sensors.

H H H

UAS are essentially sensors that enable the Internet of

Things (IoT).H H H

The ability to accomplish dull, dirty, or dangerous tasks more

safely, efficiently, and cost effectively drives demand for use of

commercialdrones.

H H H

Companies are manufacturing, or planning to manufacture,

small UAS (sUAS) to increase the sales of their sensors.M M M

Sensor and subsystem manufacturers are developing

products specifically for the sUASmarket.M M M

Impact Ratings: H = High, M = Medium, L =Low

Technological advances, computer chip manufacturing techniques and economies of

scale have driven, and will continue to drive, down costs

Frost & Sullivan

Total Commercial UAS Market: Key Market Drivers, Global, 2015–2020

35

Restraints 1–2 Years 3–4 Years 5–6 Years

Regulations for commercial drone use vary widely from

region to region.H H H

Many applications, like parcel delivery, will need to operate

beyond visual line of sight (BVLOS) which will require robust

sense and avoid (SAA) systems and dedicated command and

control (C2) spectrum bandwidth.

H H M

While technologies exist for accelerating UAS integration into

national airspace structures, there is no standardization for

deciding which technologies to use.

H H M

Personal privacy concerns will lead to drone use laws, and

the restrictiveness of those laws will likely be related to the

cultural norms of different regions.

H H M

While driving market growth, inexpensive platforms are

also limiting potential growth because inexperienced and

unlicensed users are causing a backlash.

M M M

Trade restrictions, lack of safety/software standards, and

uncertain terms for insurance underwriting could reduce the

impetus for starting or maintaining commercial operations.

M M M

Impact Ratings: H = High, M = Medium, L =Low

Nonetheless, the presence of varying and often evolving regulations both across and

within regions will act as a restraint to greater deployment

Frost & Sullivan

Total Commercial UAS Market: Key Market Restraints, Global, 2015–2020

36

All figures are rounded. The base year is 2014

1,800.0

1,600.0

1,400.0

1,200.0

1,000.0

800.0

600.0

400.0

200.0

0.00.0

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

7,000.0

Revenue ($ M)

2014

693.5

2015

1,425.6

2016

2,447.6

2017

3,942.9

2018

4,786.5

2019

5,686.1

2020

6,657.2

Units (000s) 140.5 289.5 520.6 898.6 1157.0 1397.5 1676.9

Un

its

(0

00

s)

Re

ve

nu

e($

Mil

lio

n)

Year

Revenue CAGR, 2014–2020 = 45.8%, Unit Shipment CAGR, 2014–2020 = 51.2%

Frost & Sullivan expects unit shipment growth (51.2% CAGR, 2014-202) to outpace

revenue growth (45.8%) as prices continue to fall overall

Frost & Sullivan

Total Commercial UAS Market: Unit Shipment and Revenue Forecast, Global, 2014–2020

37

DJI is the clear market leader with a share of 24.9% in revenue terms, compared with just

2.5% for Parrot/senseFly and (1.3%)

Company Strengths Weaknesses Opportunities Threats

Overwhelming

consumer and prosumer

market share in most

regions; strongest brand

recognition in overall

market

History of platform

flyaways and poor

customer service;

explosive growth potential

to lead to complacency;

only exposed to low-

priced drone market

Increased customer base

created with lower pricing;

partnerships with tech

leaders to exploit IoT; Matrice

100 developer platform for

higher-end applications

Huge number of low

cost competitors

angling to gain market

share; restrictive laws

and/or regulations;

privacy issues

Strong brand

recognition; strategic

acquisitions and

partnerships; excellent

network of global

resellers

Parrot platforms seen as

toys rather than drones;

use image stabilization

processors (ISPs) rather

than gimbals for stable

photos/video

Rapidly expanding market for

precision agriculture

applications and industrial

/utility inspections; eXom

platform for inspections; end-

to-end services via platform

and software offerings

FW aircraft with longer

endurances than eBee;

flood of entrants to

consumer market

Modifiable, open-source

code for UAS control

and operations; ability to

make drones to order;

drone applications

development

Limited distribution

network compared to DJI

and Parrot/senseFly;

recent problems filling

orders for newest Solo

platform and accessories

Underserved regions like the

Middle East and South

America; continued

partnerships with tech giants

like Intel to integrate into IoT

Huge amount of

competitors aiming to

gain market share;

privacy concerns;

regulatory obstacles;

unpredictable legal

challenges

Frost & Sullivan

Total Commercial UAS Market: SWOT Analysis, Global, 2014

38

Photography/Video

• Aerial photography and video is the largest application, by far,currently

conducted by commercial UAS platforms.

• Drones have been used for cinematic purposes for many years.Much

of the heavy lift professional UAS market arose from the need tocarry

large cinematic cameras for aerial shots without using expensive

helicopter rentals.

• In just the last few years, drones in the consumerand prosumer price

ranges have enabled users to capture HD aerial photos andvideos.

o Much of this capability came with the advent of affordableGoPro

action cameras.

o The GoPro Hero 3 can record in Ultra HD (4K) and the DJI Phantom

3 Professional, which retails for between $1,200 and $1,300,

includes its own 4K camera.

o Several small business owners like event photographers and real

estate agents have added drone photography and video to help

increase sales.

• Major players in photography/video include DJI, 3DR,

Parrot/senseFly, Yuneec, Freefly Systems, Aeronavics/Droidworks

and Tarot

From an application point of view, photography/video is the most common usage

followed by mapping/surveying (1/2)

39

Mapping/surveying

• UAS have the ability to launch very quickly and can utilize onboard

cameras and sensors to produce high-definition (HD), geo-referenced

images for input into geographic information systems (GIS).

o These images can be corrected and combined, or stitched,

together with image processing software to create orthomosaic

photos, which are accurate representations of the Earth‟s

surface.

o Geo-referenced images can also be used to develop 3-D

models, which are used for functions like building information

modeling (BIM), and digital elevation models (DEM), which are

useful to surveyors.

o Light detection and ranging (LIDAR) is increasingly being used

by mapping/surveying professionals to create even more

photogrammetric detail as LIDAR sensors become smaller and

cheaper.

• In 2013, Parrot‟s senseFly subsidiary launched 5 eBee drones to map

the Matterhorn. 3-D representations, with an average resolution of 20

cm, can be seen to the right.

• Major players in mapping/surveying, in addition to Parrot/senseFly,

include Trimble

From an application point of view, photography/video is the most common usage

followed by mapping/surveying (2/2)

Images; senseFly

40

Inspection/monitoring and precision agriculture are emerging verticals

Inspections/ Monitoring

14.8%12.3%

Energy

Infrastructure

Insurance

Telecom

Mapping/ Surveying

20.6%11.2%

3-DTerrain/Structure

Modeling

Construction

Mining

Resource Management

Photography/ Video52.1%67.7%

Marketing/ Advertising

Events

Real Estate

TV & Film

Precision Agriculture

6.2%3.5%

Crop Scouting/Pest

Control

Crop Status/Yield Estimating

Livestock Management

Variable Application

Reports

Research/ Training4.9%3.6%

Platform/Payload Testing

Operator Training

Wildlife Conservation

Surveillance/ Disaster

Response1.5%1.7%

Accident Response/

Investigations

SAR

Traffic Management

Frost & Sullivan

Energy

Infrastructure

Insurance

Construction

Mining

Marketing & Advertising

Events

Real EstateLivestock

Management

In italics, share of the overall market in revenue and unit terms in 2014

Total Commercial UAS Market: Current Applications with Sample Verticals, Global, 2014

41

Unmanned Aircraft Systems

Inspection/monitoring segment

1 2 3 4

42

The inspection and monitoring services vertical is hard to define but typically includes the

periodic and regular evaluation of (largely) infrastructure assets

Cellular and broadcast towers

Wind turbines

Pipelines

Oil & gas (flarestacks/oil rigs)

Ship interiors

Construction/building information modeling

(BIM)

Solar farms

Railroads

and yards

Inventory management

Frost & Sullivan

Insurance claims

Critical infrastructure

Overhead power lines/towers

Home improvement/repairs

UAS Inspection and Monitoring Services Market: Common Applications, Global,2016

43

Drones notably have the potential to materially cut costs and save time when checking

wind turbines, critical infrastructure and oil & gas installations

• Human inspections of wind turbines require about 4 hours to accomplish at a cost of about $1,500.

o Drones can accomplish required inspections in about 1 hour and at an estimated cost of $100.

o Autocopter presented a business case in which wind turbine inspections could cost as little as $15

each.

o When accounting for both the time and cost savings, drones can conduct an inspection in a quarter of

the time and at about 7% of the cost of inspections accomplished byhumans.

• Drone services can reduce the time required and cost to inspect criticalinfrastructure.

o The cost of bridge inspections is likely to drop from $10,000 to $15,000 per inspection to $1,000 to

$3,000 per inspection while the inspection time will be reduced from weeks todays.

o Transportation officials in the state of Michigan have estimated that a standard bridge deck inspection

requiring a 4-person crew working 8 hours at a cost of $4,600 can be accomplished by a 2-person crew

working for 2 hours at a cost of $250 when utilizing adrone.

o Utilizing UAS can reduce or eliminate the need for traffic control during inspections.

• Sewer inspections can cost up to $20,000 per mile when conducted by humans. It is estimated that drones

designed to operate in confined spaces could reduce that cost by 50%.

• Sky-Futures, a world-leading oil and gas inspection company utilizing drones, was able to help an

Egyptian oil and gas company save $3.75 million by reducing the shutdown time for the inspection of its

flare stacks by 5 days.

• Offshore oil rig inspection times using drones can be reduced by more than80%.

Frost & Sullivan

44

Drivers 1–2Years 3–4 Years 5–6 Years

A staggering number of building, tower, property,and

infrastructure inspections are required eachyear.H H H

Inspections with drones will make dangerous jobs safer and

reduce work-relatedcasualties.H H H

The US Federal Aviation Administration (FAA) recently issued a

new small UAS rule that enables the inspection of tall

structures.

H M M

Cost savings could lead many companies to engage in more

frequent inspections to ensure efficiency and safety.L L M

Impact Ratings: H = High, M = Medium, L =Low

Here, the market is also underpinned by the very significant number of building, tower and

property inspections that are required each year

Frost & Sullivan

UAS Inspection and Monitoring Services Market: Key Market Drivers, Global, 2016‒2021

45

Restraints 1–2Years 3–4 Years 5–6 Years

Robust processes for gathering regulatory-grade inspection

data must be developed, tested, and implemented.H H H

Regulations for conducting BVLOS operations are still

relatively strict worldwide.H H H

Specific limitations must be considered when utilizing small

UAS for inspections.H M M

The costs of drone operations are not truly knownyet. M M M

Many DSCs, do not fully understand what it takes to gather,

process, and analyze drone-collected data and present it in the

form of actionable information for the end user.

M L L

Future technologies could eliminate the need for certain

inspections.L M M

Impact Ratings: H = High, M = Medium, L =Low

There is however a need for establishing global processes and standards which allow the

capture of universally comparable regulation-grade inspection data

Frost & Sullivan

UAS Inspection and Monitoring Services Market: Key Market Restraints, Global, 2016‒2021

46

North America

Top telecom companies such as AT&T have

committed to using drones to inspect cell

towers and possibly provide streaming video

from live events. 33 US state transportation

departments are researching the use of

drones for bridge inspections.

Brazil

The country is using drones to

assist with the construction of the

world’s third-largest hydroelectric

dam.

China

The energy sector plans to enlist tens of

thousands of drones to inspect all

aspects of the national power grid.

Japan

The country recently introduced the i-

Construction initiative to increase the

productivity of construction workers by

50%. They will use drones and other

automated equipment to counteract a

projected decline in the Japanese

workforce.

Europe

The two top oil & gas drone inspection companies,

Sky-Futures and CyberHawk, are European

companies quickly expanding their global footprint.

UAS Inspection and Monitoring Services Market: Key Regional Highlights, Global, 2016

On a regional basis, Europe is home to the top two oil & gas inspection companies which

are rapidly expanding their global footprint

Africa

Cameroon and Namibia are

both attempting to jump-start

drone use in construction via

business-government

partnerships.

United Arab Emirates

Dubai Electricity and Water Authority is investing $136

million to develop 3D-printed UAS for monitoring water

and electricity production and distribution systems.

Frost & Sullivan

47

From a competitive point of view, drone service companies are partnering with third parties

to provide UAS operations which are specific to inspection/monitoring

• Railhead Corporation, a manufacturer of safety lighting, tools, mobile video surveillance, and locomotive

data recorders, teamed up with Volant UnmannedAerial Solutions to bring Lockheed Martin’s Indago drone

with Sentera’s OnTop platform to the rail industry. The companies plan to develop an inspection and

monitoring-focused package for marketing to railroad companiesglobally.

• Caterpillar and Redbird have teamed to provide construction customers with more cost-effectiveand

efficient work site data analytics that focus on progress and materialsmonitoring.

• ABS Group and Droneview Technologies have partnered to develop and implement professional energy

tower and wind turbine inspections.

o ABS Group specializes in energy inspections while Droneview specializes in professionaldrone

services.

o The partnership is one of several between energy industry professionals and drone operators to

establish specialized and standardized enterprise inspection solutions. Others include Advanced

Industrial Solutions and RetrixAS, Amey and VTOLTechnologies, Donan and Datawing, and T-Mobile

andAerialtronics.

• Sharper Shape and Edison Electric Institute (EEI) have partnered to create a safe and regulated

commercial framework for large-scale commercial UAS inspections includingBVLOS operations.

o The goal of this consortium is to accelerate the adoption of UAS for inspecting electricity transmission

and distribution lines.

o Sharper Shape has a similar partnership with Sterlite Power of India.

Frost & Sullivan

48

OEMs are also developing tailor-made solutions

• SenseFly, a Parrot company, developed its albris platform (formerly named eXom) specifically toconduct

inspections and mapping. It has several design characteristics paramount to conducting thorough

inspections including:

o An LED light for operating in darkplaces.

o A triple view, front-facing camera that allows the operator to select between HD video, thermalimaging,

or still photography during flight.

o Sensors around the aircraft that provide visual and acoustic feedback on distance from obstacles.

o An option for flying without global navigation satellite system (GNSS).

• Novadem, of France, developed its U130 with close inspection in mind. Unique features of theU130

include:

o A range finder that measures distance to inspected object.

o Laser pointers that provide a reference for determining size of defects or damage areas0

o An embedded digital video filter that easily finds crackedges.

o A proprietary software suite, called NovaEDITOR, specifically developed to provide users witha

simplified method for locating and visualizing close inspectiondefects.

• Two Swedish companies, Sky Eye Innovations and Spacemetric, have formed a partnership to develop

“an integrated and highly effective inspection tool for preventative maintenance and decision making that

uniquely combines imagery from UAVs, satellites and handheld sensor units.”

Frost & Sullivan

49

Unmanned Aircraft Systems

Agriculture services segment

1 2 3 4

50

The agricultural services vertical has generated much interest in recent years with UASs

now finding concrete uses cases across a range of applications

Crop planning

Crop scouting/monitoring

Irrigation management

Livestock management

Planting

Precision spraying/dusting

Frost & Sullivan

UAS Agricultural Services Market: Current and Potential Applications, Global,2016

51

Drones notably have the potential to improve efficiency and increase output in crop

scouting and livestock management

• Drones can scout hundreds of acres in 60 to 90 minutes. The same effort with ground-basedtechniques

would take hours or days and would not result in the complete coverage that drone imageryprovides.

• Manned aircraft for crop scouting commonly cost $600 to $1,000 per hour to hire.

o Agricultural drones can range from a few thousand to tens of thousands of dollars depending on

the platform robustness, capability, and, more importantly, the quality of sensorsutilized.

o Even high-cost UAS can be paid for by replacing manned aircraft flightswithin 1 or 2 growing seasons.

o A year of data services, including VRA and crop health reports, can be purchased for the amount it

costs to conduct 2 manned aircraft flights.

• One wheat farmer in Idaho who has been scouting crops with drones since 2006 reported a cost

savings of 20 to 25% while producing increases in yield.

• Owners of sheep and cattle farms are beginning to invest in drones to manage livestock.

o A farmer in New Zealand is using a $4,000 drone to search his entire farm for cast sheep in 20

minutes, a job that can take up to 2 hours by all-terrain vehicle. It is estimated that the farm will save

$40,000 per year in time and fuel costs.

o Farmers in British Columbia, Canada, are testing drones for rounding up free-grazing cattle via

RFID. Such a system is considerably cheaper than fitting cows with GPS-locator collars that can

cost up to $3,000 each.

Frost & Sullivan

52

Drivers 1–2Years 3–4 Years 5–6 Years

Growers and producers will likely favor DSCs over

purchasing and operating drones in-house.H H H

The US Federal Aviation Administration (FAA) recently issued

a new small UAS rule that reducesqualifications for drone

pilots.

M M M

UAS could help the environment by minimizing soil

erosion and overfertilization.L L M

Impact Ratings: H = High, M = Medium, L =Low

Here, the market is also supported by a relaxation in the rules regarding the qualifications

which are needed to pilot UASs

Frost & Sullivan

UAS Agricultural Services Market: Key Market Drivers, Global, 2016‒2021

53

Restraints 1–2Years 3–4 Years 5–6 Years

UAS in agriculture may not produce the ROI that is hyped

by the industry.H H H

Worldwide BVLOS and altitude-limiting regulations for UAS

are relatively restrictive and hamper many agriculture

applications.

H H H

It is very challenging to translate aerial imageryinto

actionable information for farmers.H M M

Some competing technologies can reducethe

requirement for drones.M M M

Farmers are generally resistant to change,especially when it

is technology that is not always simple to understand.M M L

Impact Ratings: H = High, M = Medium, L =Low

There remains some scepticism, however, as to whether they will be able to produce the

return on investment which has been suggested by the industry

Frost & Sullivan

UAS Agricultural Services Market: Key Market Restraints, Global,2016‒2021

54

North America

Drone and agriculture companies in the United

States and Canada are partnering at a blistering

pace to provide customers with the best data at the

cheapest price. Competition will only grow as the

FAA looks to make regulations more favorable for

commercial UAS operations.

Brazil

Qualcomm is working with the Brazilian

Agricultural Research Corporation

(Embrapa) and the Institute of Solidarity

Socioeconomics (ISES) to demonstrate

how drone applications can be utilized

to reduce environmental impact and

increase crop yields.

India

The Indian government

has launched a

collaborative research

project called Sensor-

Based Smart Agriculture

(SENSAGRI) involving the

use of drone technology in

the farming sector for crop

scouting and insurance

claims.

France

Airinov, a leading drone agricultural services

company, has assisted over 5,000 farmers

throughout Europe and is leading a project to

help the continent of Africa benefit from

agricultural drones.

UAS Agricultural Services Market: Key Regional Highlights, Global, 2016

In Europe, Airinov has assisted over 5,000 farmers across the continent and is leading a

project to grow usage in Africa

Africa

Governments in Uganda and

Tanzania have initiated UAS

programs to increase crop

yields and to correctly

assess the total amount of

crops grown.

China

Loughborough

University in the

United Kingdom is

conducting research

into how sensing

platforms such as

satellites, drones,

airships, and

unmanned ground

vehicles can be

utilized to achieve

sustainable

agriculture in China.

Frost & Sullivan

55

From a competitive point of view, large agriculture companies are rapidly integrating

drones into their smart farming product offerings

• Agribotix has integrated its FarmLens image processing and analysis product into John Deere’s

information management system in Australia. This allows John Deere customers to directly send drone-

collected data, analytics, vegetation index maps, and variable application reports to their John Deere

Operations Center account.

• AGCO Corporation recently teamed with 3D Robotics (3DR) to develop the Solo AGCO Edition. The

system includes a red, green, blue (RGB) camera and a near-infrared camera optimized for agricultural

applications.

• Syngenta acquiredAgConnections in late 2015 and is exploiting that acquisition to integrate drone

imagery into its AgriEdge Excelsior farm managementsystem.

• Airtractor, which offers the world’s largest product line of crop-spraying aircraft, purchased a UAS start-up

called Hangar 78 UAV. The company plans to integrate Hangar 78’s Yield Defender drone into its product

line.

• FarmersEdge, a leading global precision agriculture and data management company based in Canada,

recently partnered with drone systems and data analysis company GreenAero Tech.

o Green Aero Tech will provide FarmersEdge with RTK imagery to integrate intoFarmersEdge’s

FarmCommand comprehensive farm data management solution.

o The RTK-equipped drones of GreenAero Tech can provide elevation data accurate to within 5

centimeters.

• Wilbur-Ellis has been testing Honeycomb’sAgDrone for integration into its AgVerdict precision farming

solution.

Frost & Sullivan

56

Partnerships between OEMs and with software providers are also delivering scalable

service options for precision agriculture customers

• PrecisionHawk and DJI partnered to provide their Smarter Farming Package.

o This package integrates DJI hardware with PrecisionHawk’s Datamapper software to provide

customers with a multirotor drone option to supplement PrecisionHawk’s proprietary Lancaster fixed-

wing system.

o DJI recently announced its Agras MG-1 platform, which is designed for precision spraying. This

platform and capability could augment the Smart Farming Packagein the future.

• PrecisionHawk has also partnered with Agri-Trend to integrate PrecisionHawk’s UAS andDatamapper

systems into Agri-Trend’s Agri-Data Solution platform. The integration will allow users to collect and

analyze data from a wide range of sources for efficient data management and decision making.

• Trimble has partnered with MULTIROTOR Service-Drone of Germany to offer customers the vertical

takeoff and landing ZX5 platform. The ZX5 will supplement Trimble’s UX5 and UX5 HP fixed-wing line of

UAS to provide a full range of aerial imaging solutions.

• MicroMultiCopter (MMC), a growing Chinese drone manufacturer, has teamed with Agribotix to develop

the Swift UAS. The Swift combines multispectral imaging with an intelligent spraying system to provide

crop scouting and precision crop dustingin a single platform.

Frost & Sullivan

57

Appendices

58

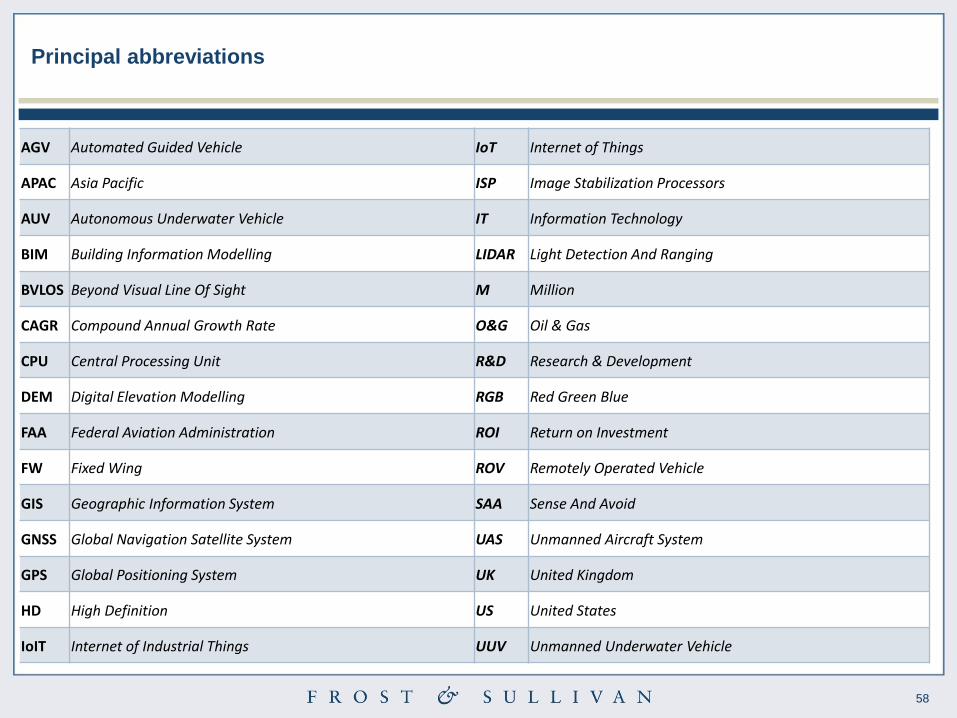

Principal abbreviations

AGV Automated Guided Vehicle IoT Internet of Things

APAC Asia Pacific ISP Image Stabilization Processors

AUV Autonomous Underwater Vehicle IT Information Technology

BIM Building Information Modelling LIDAR Light Detection And Ranging

BVLOS Beyond Visual Line Of Sight M Million

CAGR Compound Annual Growth Rate O&G Oil & Gas

CPU Central Processing Unit R&D Research & Development

DEM Digital Elevation Modelling RGB Red Green Blue

FAA Federal Aviation Administration ROI Return on Investment

FW Fixed Wing ROV Remotely Operated Vehicle

GIS Geographic Information System SAA Sense And Avoid

GNSS Global Navigation Satellite System UAS Unmanned Aircraft System

GPS Global Positioning System UK United Kingdom

HD High Definition US United States

IoIT Internet of Industrial Things UUV Unmanned Underwater Vehicle

59

Frost & Sullivan contacts

John DaviesSenior Consultant

Business & Financial Services

Tel +33 1 42 81 21 01

Livio VaninettiDirector

Italy

Tel +39 02 4851 6135

Luca RaffelliniHead

Business & Financial Services

Tel +44 20 7343 8384

60

Frost & Sullivanwww.frost.com

January 2017

![PDF] LG6R73PT Manual 0618 - Tractor Supply Company.039.045.050.24.30.34.38.024.029.034.038.19.24.27.31.019.024.027.030.13.16.18.20.012.015.018.020 41.8 51.2 59.2 66.4 ... N U M B E](https://img.pdfslide.us/doc/110x75/612d293f1ecc51586942045a/-lg6r73pt-manual-0618-tractor-supply-company039045050243034380240290340381924273101902402703013161820012015018020.jpg)