Embed Size (px)

Citation preview

1

PT EXCELCOMINDO PRATAMA Tbk. (XL)

Q1 2007 Results PresentationApril 2007

PT EXCELCOMINDO PRATAMA Tbk. (XL)

1H 2007 Performance ResultsJuly 2007

2

Key Drivers – Product, Network & Distribution

Operating & Financial Results

2007 Outlook

Financial Highlights & Other Declarations

Market Updates

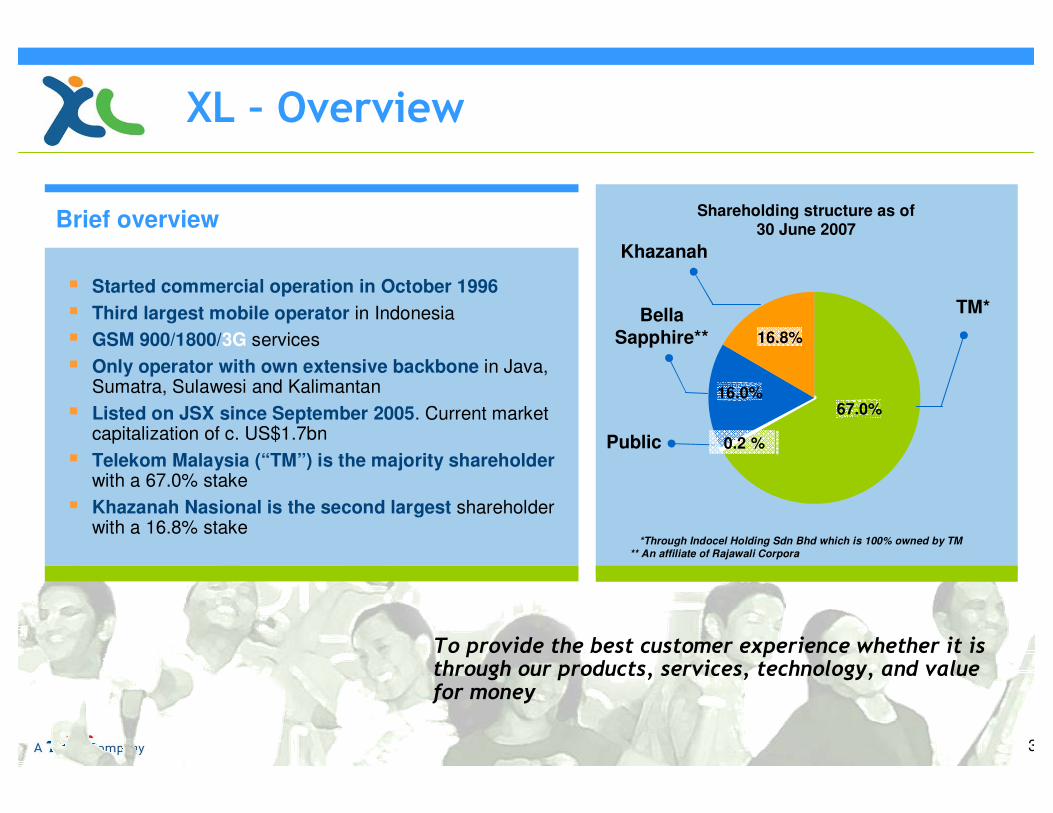

3

Brief overview

*Through Indocel Holding Sdn Bhd which is 100% owned by TM** An affiliate of Rajawali Corpora

TM*

67.0%

Bella Sapphire**

Public

Khazanah

16.8%

16.0%

0.2 %

������������� ��� ������������������� ������������������ �� ���� �����������������������������

� Started commercial operation in October 1996� Third largest mobile operator in Indonesia� GSM 900/1800/3G services� Only operator with own extensive backbone in Java,

Sumatra, Sulawesi and Kalimantan� Listed on JSX since September 2005. Current market

capitalization of c. US$1.7bn� Telekom Malaysia (“TM”) is the majority shareholder

with a 67.0% stake� Khazanah Nasional is the second largest shareholder

with a 16.8% stake

Shareholding structure as of 30 June 2007

���� � �����

4

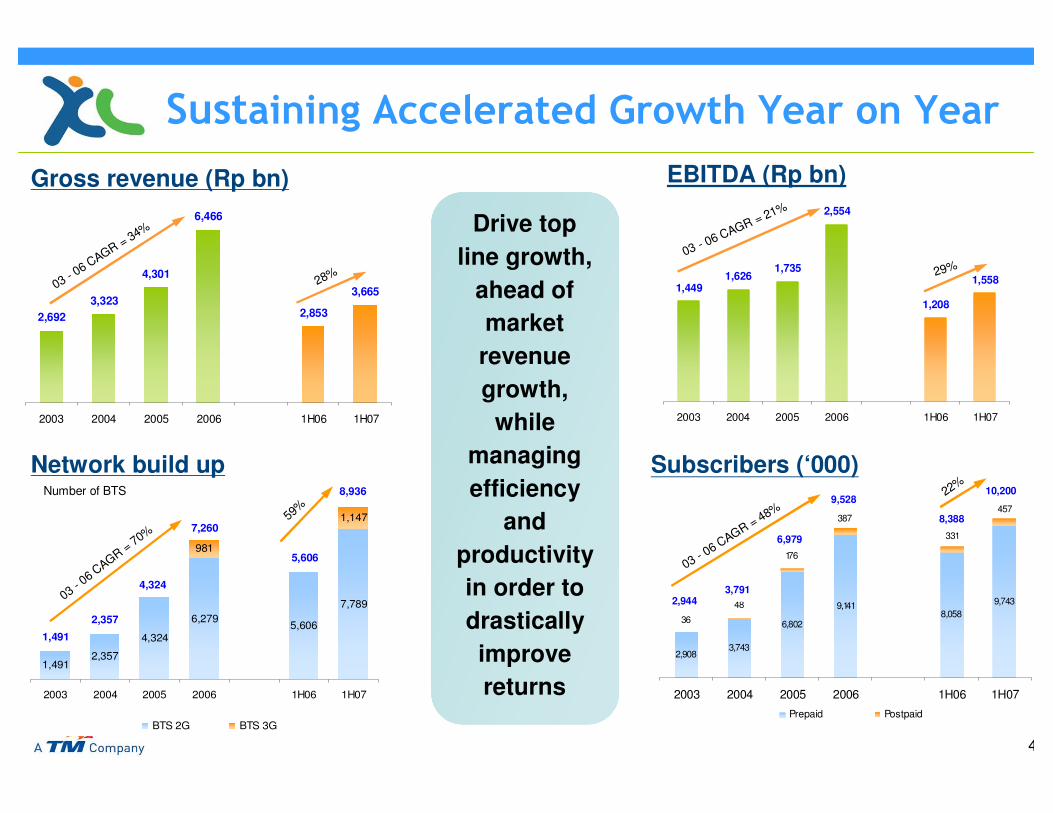

2,9083,743

6,802

9,1418,058

9,743

36

48

176

387

331

457

2003 2004 2005 2006 1H06 1H07

Prepaid Postpaid

8,388

2,9443,791

6,979

9,52810,200

1,4912,357

4,324

6,2795,606

7,789

981

1,147

2003 2004 2005 2006 1H06 1H07

BTS 2G BTS 3G

1,491

2,357

4,324

7,260

5,606

8,936

1,4491,626

1,735

2,554

1,208

1,558

2003 2004 2005 2006 1H06 1H07

2,6923,323

4,301

6,466

2,853

3,665

2003 2004 2005 2006 1H06 1H07

�� ������������������� �� ���������������

EBITDA (Rp bn)

Subscribers (‘000)

03 - 06 CAGR = 21%

03 - 06 CAGR = 48%

29%

22%Network build up

Number of BTS

Gross revenue (Rp bn)

03 - 06 CAGR = 34%

03 - 06 CAGR = 70%

28%

59%

Drive top line growth,

ahead of market revenue growth,

while managing efficiency

and productivity in order to drastically improve returns

5

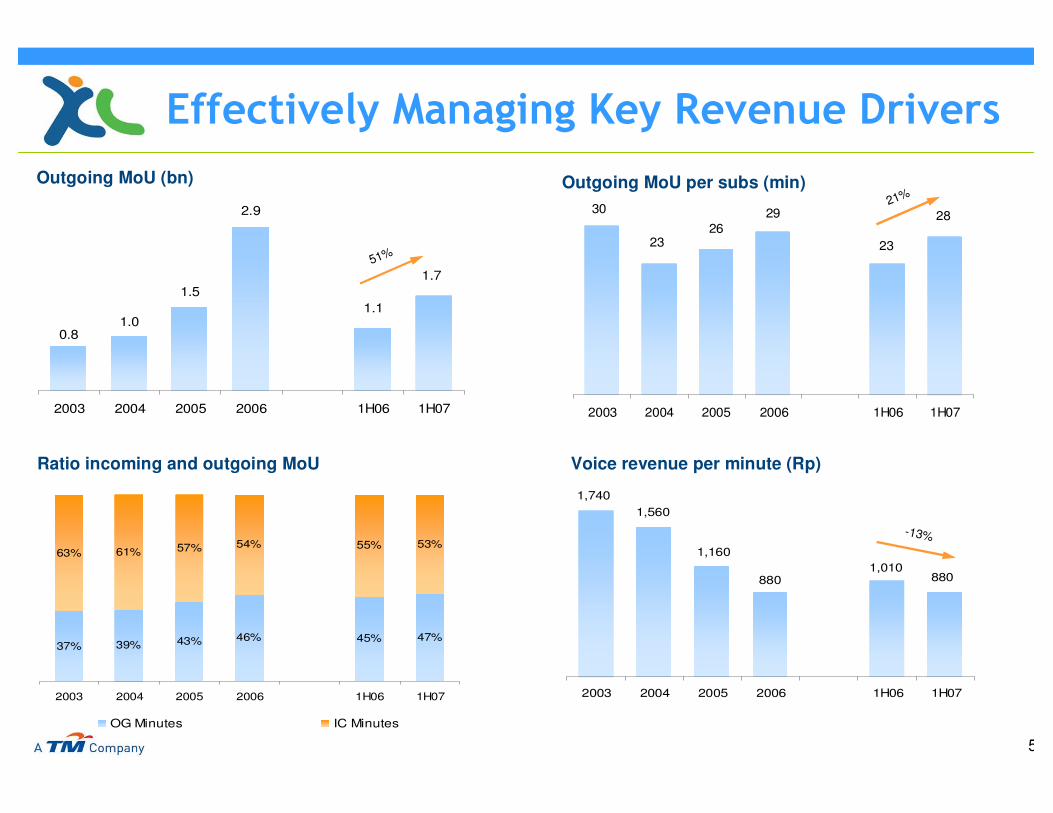

Outgoing MoU (bn) Outgoing MoU per subs (min)

Ratio incoming and outgoing MoU Voice revenue per minute (Rp)

������������ ������������������� ����

1.7

2.9

1.11.5

1.00.8

2003 2004 2005 2006 1H06 1H07

45% 47%

63% 61% 57% 54% 55% 53%

46%37% 39% 43%

2003 2004 2005 2006 1H06 1H07

OG Minutes IC Minutes

2829

2326

23

30

2003 2004 2005 2006 1H06 1H07

880

1,7401,560

1,1601,010

880

2003 2004 2005 2006 1H06 1H07

51%

21%

-13%

6

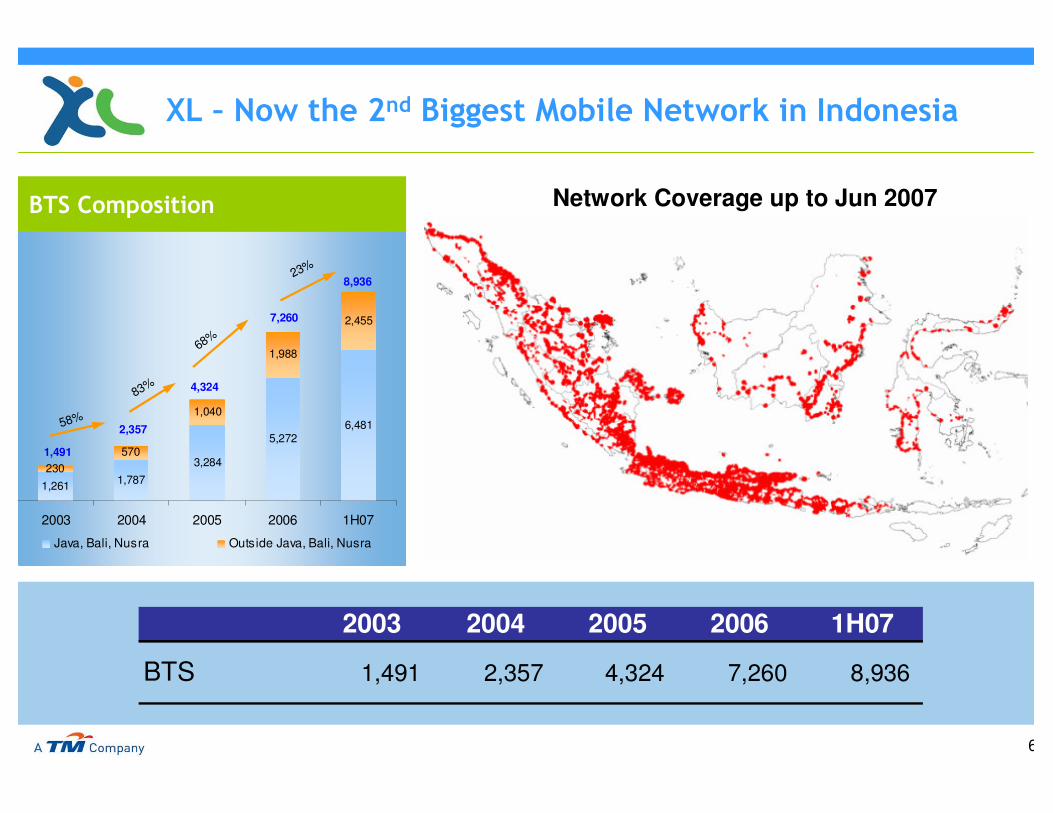

!"��#�$ %� ��� Network Coverage up to Jun 2007

230570

1,040

1,988

6,4815,272

1,261 1,7873,284

2,455

2003 2004 2005 2006 1H07

Java, Bali, Nusra Outside Java, Bali, Nusra

1,491

2,357

4,324

7,260

8,936

2003 2004 2005 2006 1H07

BTS 1,491 2,357 4,324 7,260 8,936

58%

83%

68%

23%

���� & � �����'�� !��� ��� �(���& �� ��)���*����� �

7

Key Drivers – Product, Network & Distribution

Operating & Financial Results

2007 Outlook

Financial Highlights & Other Declarations

Market Updates

8

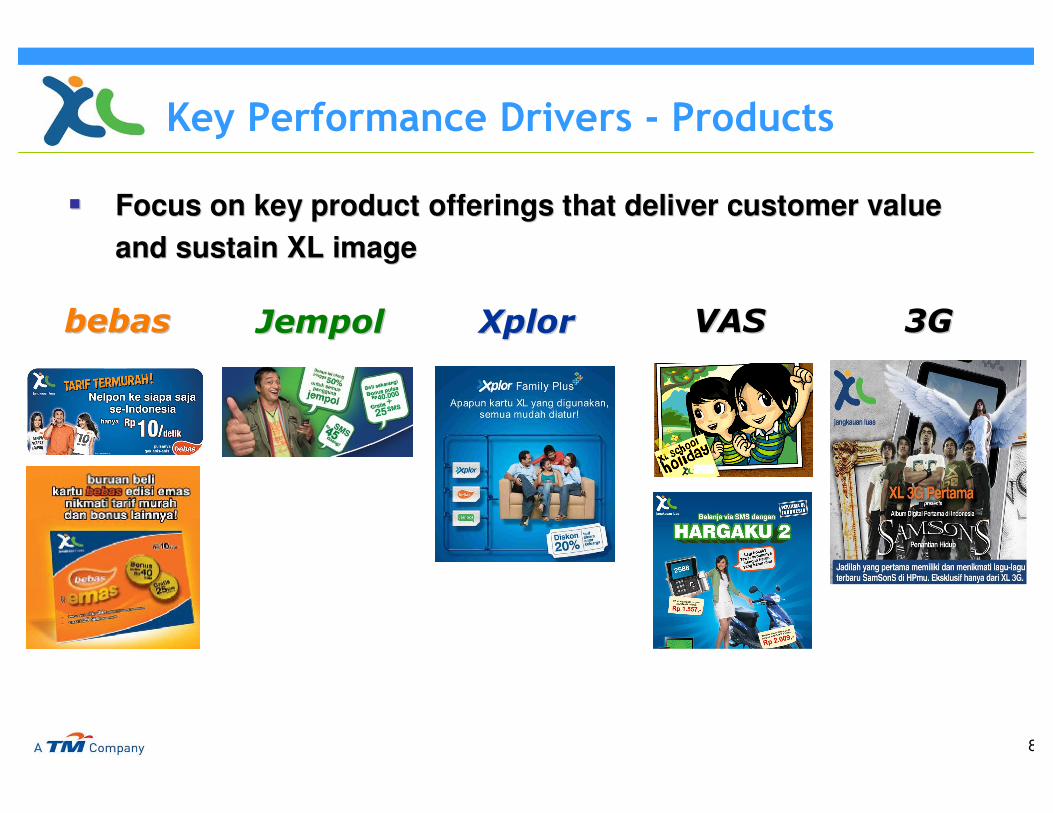

����+�����$ ����� ���� �, +������

�� Focus on key product offerings that deliver customer value Focus on key product offerings that deliver customer value and sustain XL imageand sustain XL image

���������� ���������� ���� � ���������

9

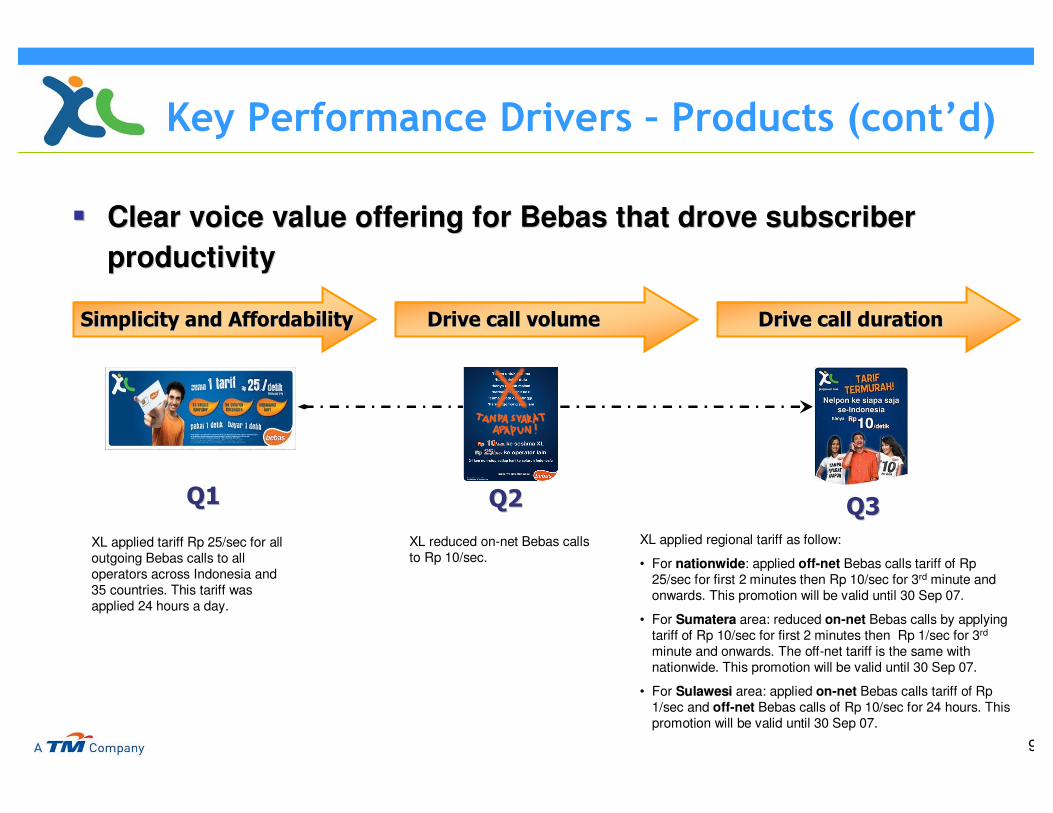

�� Clear voice value offering for Clear voice value offering for BebasBebas that drove subscriber that drove subscriber productivityproductivity

XL applied tariff Rp 25/sec for all outgoing Bebas calls to all operators across Indonesia and 35 countries. This tariff was applied 24 hours a day.

XL reduced on-net Bebas calls to Rp 10/sec.

����

XL applied regional tariff as follow:

• For nationwidenationwide: applied off-net Bebas calls tariff of Rp25/sec for first 2 minutes then Rp 10/sec for 3rd minute and onwards. This promotion will be valid until 30 Sep 07.

• For SumateraSumatera area: reduced on-net Bebas calls by applying tariff of Rp 10/sec for first 2 minutes then Rp 1/sec for 3rd

minute and onwards. The off-net tariff is the same with nationwide. This promotion will be valid until 30 Sep 07.

• For SulawesiSulawesi area: applied on-net Bebas calls tariff of Rp1/sec and off-net Bebas calls of Rp 10/sec for 24 hours. This promotion will be valid until 30 Sep 07.

������������ �������������� ��

���� ����

���������� ��������������� �������������������������������������������������������

����+�����$ ����� ���� �� +������ �-����.�/

10

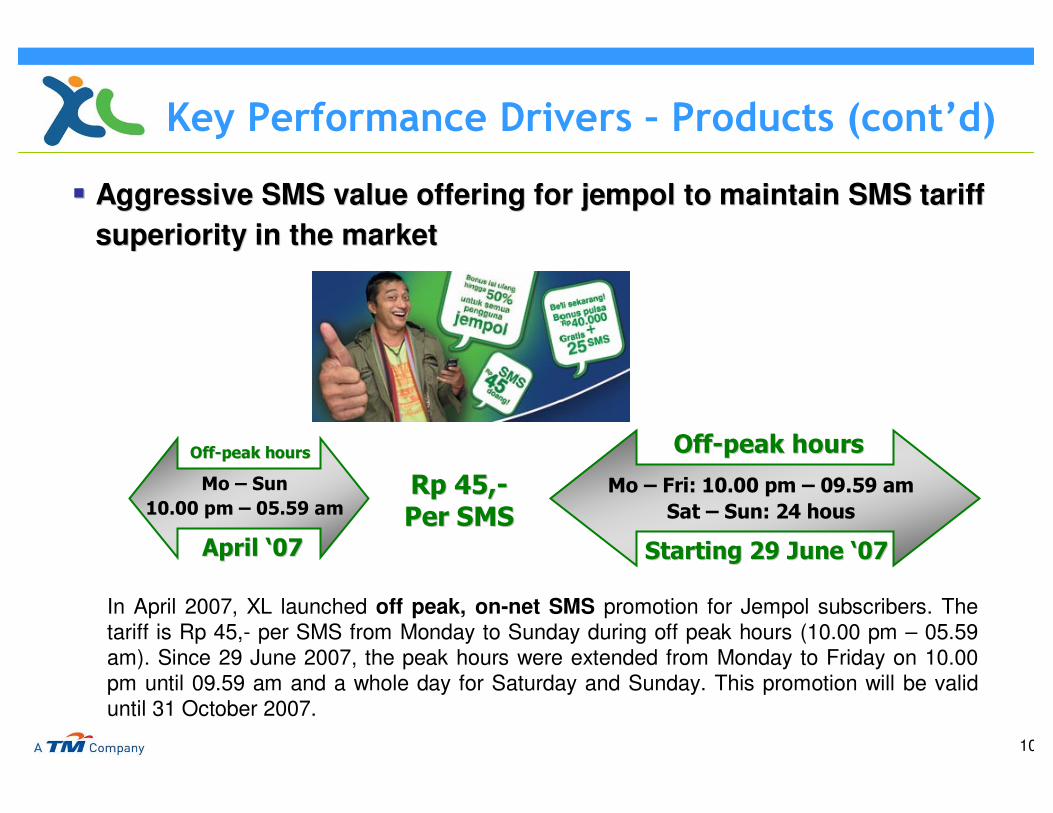

�� Aggressive SMS value offering for Aggressive SMS value offering for jempoljempol to maintain SMS tariff to maintain SMS tariff superiority in the marketsuperiority in the market

In April 2007, XL launched off peak, on-net SMS promotion for Jempol subscribers. The tariff is Rp 45,- per SMS from Monday to Sunday during off peak hours (10.00 pm – 05.59 am). Since 29 June 2007, the peak hours were extended from Monday to Friday on 10.00 pm until 09.59 am and a whole day for Saturday and Sunday. This promotion will be valid until 31 October 2007.

�������������� �������� ��

�������������� ! !

�������������� �������� ��

������"��#�$ ���������"��#�$ ����� ! !

%��& � �

� ' ����& ('(#��%��& )��*�� ' ����& #'(#��

���& � �*��+��� �,�,�+(-+(-��

.����%�.����%�

����+�����$ ����� ���� �� +������ �-����.�/

11

�� Significant expansion of distribution networkSignificant expansion of distribution networkStarting Jan 07, XL has changed its distribution channel by having large national distributors.

As of 30 June XL had more than 400k retail outlets.

�� Create network quality excellenceCreate network quality excellence

�� Expand network coverage outside Java to strengthen market Expand network coverage outside Java to strengthen market position in the nonposition in the non--Java marketJava market

����+�����$ ����� ���� �� & �� ��)�0 � ��(����

12

Accomplishments

XL - Overview

Indonesian Market

Financial performance

XL Focus

Key Drivers – Product, Network & Distribution

Operating & Financial Results

Market Updates

Financial Highlights & Other Declarations

2007 Outlook

13

� ��)���1 %���� �, *����� ���� �(���*��� ���

.�����.�����

� Currently there are 11 players in the market with around 20 different products

� 3 big GSM players still dominate the market

� SIM Penetration rate in 1Q07: 31%

/����������/����������

� CDMA players expanding their coverage

� CDMA players offer low tariffs� New players offer aggressive rates� The 3 big players started to lower their

tariffs

Impact to XLImpact to XL

XL achieved 1H07 XL achieved 1H07 performance under performance under hyperhyper--competitive competitive industry situation industry situation brought about by brought about by aggressive play aggressive play from CDMA from CDMA operatorsoperators

14

� The new interconnection regulation (cost based vs revenue share) has been implemented since 1 January 2007.

� Government plans to tender USO projects in 2007.

� The Government plans to revise KM No. 12/2006 and set the floor price as operational regulation on retail voice tariff.

� Government has announced and open the selection process of IDD on 28 June 2007. The winner of the selection process will be granted IDD license in 3Q 2007.

� Industry is waiting for the Government action to open up BWA license selection process early next year.

� On 3 July 2007, the Government issued PP no.76/2007 and 77/2007 that limited foreign ownership in Indonesia up to 65% for cellular operators and 49% for fixedwireless operators. This regulation applied to new investors.

Regulations:

� ��)���1 %���� �, ���������

15

Key Drivers – Product, Network & Distribution

Operating & Financial Results

Market Updates

Financial Highlights & Other Declarations

2007 Outlook

16

�� Sustain relevant value offerings for XL productsSustain relevant value offerings for XL products

�� Further strengthen network quality in Java and sustain expansionFurther strengthen network quality in Java and sustain expansionoutside Javaoutside Java

'223�� �����)

�� Revenue will grow by about 30%Revenue will grow by about 30%

�� EBITDA margin will be comparable or slightly higher than 2006EBITDA margin will be comparable or slightly higher than 2006

�� Blended ARPU will likely be around 2006 level or slightly higherBlended ARPU will likely be around 2006 level or slightly higher

�� CapexCapex plan for 2007 is USD 700mn to add more than 3,000 BTSplan for 2007 is USD 700mn to add more than 3,000 BTS

Pursuing Key Business Performance Drivers

Pursuing Key Financial Measures

17

Key Drivers – Product, Network & Distribution

Operating & Financial Results

2007 Outlook

Financial Highlights & Other Declarations

Market Updates

18

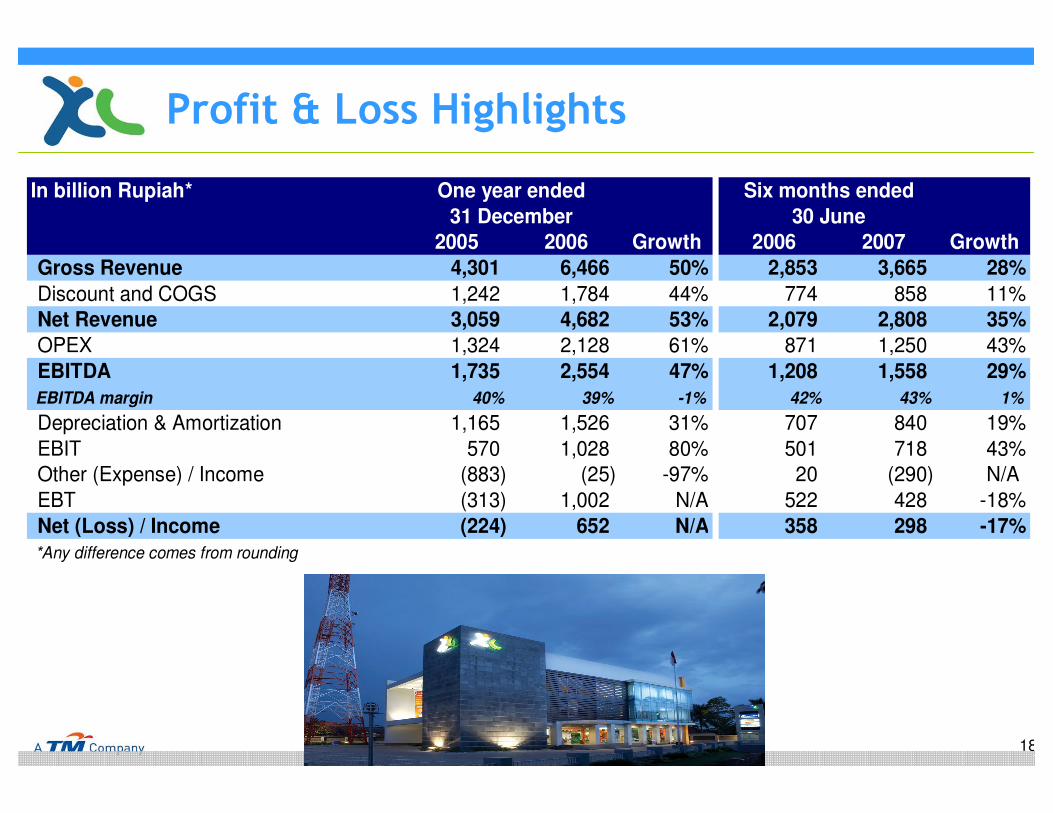

+�����0 ��� �4 ������

In billion Rupiah*

2005 2006 Growth 2006 2007 GrowthGross Revenue 4,301 6,466 50% 2,853 3,665 28%Discount and COGS 1,242 1,784 44% 774 858 11%Net Revenue 3,059 4,682 53% 2,079 2,808 35%OPEX 1,324 2,128 61% 871 1,250 43%EBITDA 1,735 2,554 47% 1,208 1,558 29%EBITDA margin 40% 39% -1% 42% 43% 1%Depreciation & Amortization 1,165 1,526 31% 707 840 19%EBIT 570 1,028 80% 501 718 43%Other (Expense) / Income (883) (25) -97% 20 (290) N/AEBT (313) 1,002 N/A 522 428 -18%Net (Loss) / Income (224) 652 N/A 358 298 -17%*Any difference comes from rounding

Six months ended30 June

One year ended31 December

19

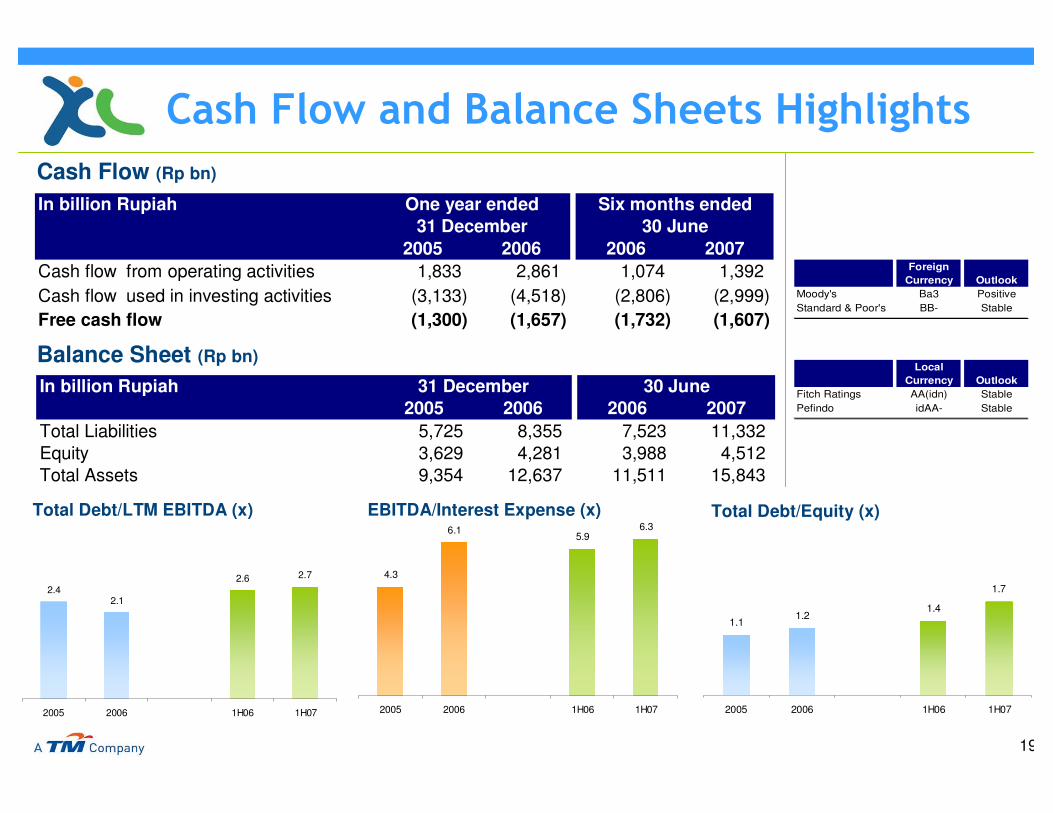

#� ��5�� �����!������������ �4 ������

Total Debt/LTM EBITDA (x) EBITDA/Interest Expense (x) Total Debt/Equity (x)

Cash Flow (Rp bn)

Balance Sheet (Rp bn)

Moody'sStandard & Poor's Stable

Foreign Currency Outlook

Ba3 PositiveBB-

Fitch RatingsPefindo idAA- Stable

AA(idn) Stable

Local Currency Outlook

In billion Rupiah

2005 2006 2006 2007Cash flow from operating activities 1,833 2,861 1,074 1,392 Cash flow used in investing activities (3,133) (4,518) (2,806) (2,999) Free cash flow (1,300) (1,657) (1,732) (1,607)

Six months ended30 June

One year ended31 December

In billion Rupiah2005 2006 2006 2007

Total Liabilities 5,725 8,355 7,523 11,332 Equity 3,629 4,281 3,988 4,512 Total Assets 9,354 12,637 11,511 15,843

30 June31 December

2.42.1

2.6 2.7

2005 2006 1H06 1H07

4.3

6.15.9

6.3

2005 2006 1H06 1H07

1.11.2

1.4

1.7

2005 2006 1H06 1H07

20

#�����������(���

� XL has a potential exposure on WHT on interest on the USD bonds issued through a Netherlands entity, due to a pending resolution on interpretation of the tax treaty between Indonesia and the Netherlands.

� In Jun 2006, XL received 2004 tax assessment result on WHT applicable for offshore interest for a total amount of Rp 34.3 bn. The tax assessment was based on WHT rate of 10%. XL has submitted an objection letter but until now has not received the result from DGT.

� In Jun 2007, XL received 2005 tax assessment result for the similar issue amounting to Rp 86.7 bn. The tax assessment was based on WHT rate of 20%.

� XL has not yet recorded the WHT for both 2004 and 2005 in IncomeStatement. The total WHT for 2004 – 2007 periods possibly to be recorded in 2007 is estimated to be approximately Rp 332 bn.

WHT issue