Embed Size (px)

Citation preview

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 1/286

Accounting for Business

Combinations and Related TopicsA Roadmap to Applying FASBStatements 141(R), 142, and 160

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 2/286

Port ions of various FASB pronoun cements, copyrigh t by t he Financial Account ing Foundat ion, 401 M errit t 7, PO Box 5116, Norw alk, CT 06856-5116, are reproduced

wit h permi ssion. Complete copies of th ese documents are available fr om t he FAF.

APB Opinions and Accounti ng Research Bullet ins: Copyrigh t 2008, by t he American Instit ute of Certi fied Public Accountant s, Inc. All ri ght s reserved. Reproduced w ith

permission.

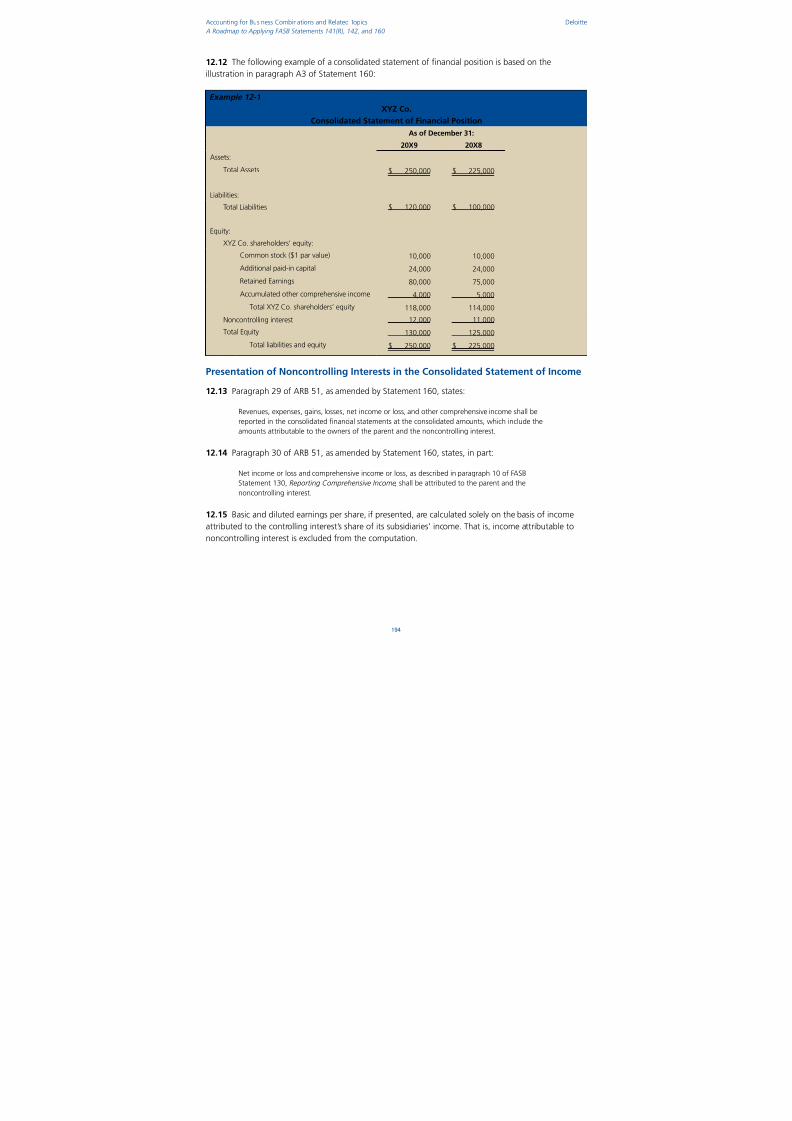

This publication i s provided as an inf ormat ion service by the Accountin g Standard s and Communicatio ns Group of Deloit te & Touche LLP. It d oes not address all

possible f act patt erns and the gu idance is subject t o change. Deloitt e & Touche LLP is not, b y means of t his publicatio n, rendering account ing, bu siness, fi nancial,

investm ent, l egal, tax, or ot her prof essional advice or services. This publication is not a substitu te f or such prof essional advice or services, nor should it be used as a

basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a

qualif ied pro fessional advisor. Deloitt e & Touche LLP shall no t b e responsible f or any lo ss sustained by any person w ho reli es on t his publication .

January 2009

i

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 3/286i i

Contents

Executive Summary 2

Background 2

EffectiveDateandTransition 3

OverviewofSignificantAccountingChanges 3

HowThisRoadmapIsStructured 7

Section 1 — Scope of Statement 141(R) 9

OccurrenceofaBusinessCombination 9

ObtainingControl 9

DefinitionofaBusiness 10

AcquiringNetAssetsorEquityInterestsThatDoNotMeettheDefinitionofaBusiness 12IdentifyingaBusinessDuringtheAssessmentofReportingRequirementsUnderSECRegulationS-X 14

VariableInterestEntities 15

CombinationsBetweenTwoorMoreMutualEntities 16

LeveragedBuyoutTransactions 17

Additional Scope Considerations 17

ControlObtainedbutLessThan100PercentoftheBusinessIsAcquired(i.e.,PartialAcquisitions) 17

BusinessCombinationsAchievedinStages 18

AcquisitionofaNoncontrollingInterestofaSubsidiary 19

Roll-UporPut-TogetherTransactions 19

FormationofaJointVenture 19

Recapitalizations 20

TransactionsBetweenEntitiesUnderCommonControl 20

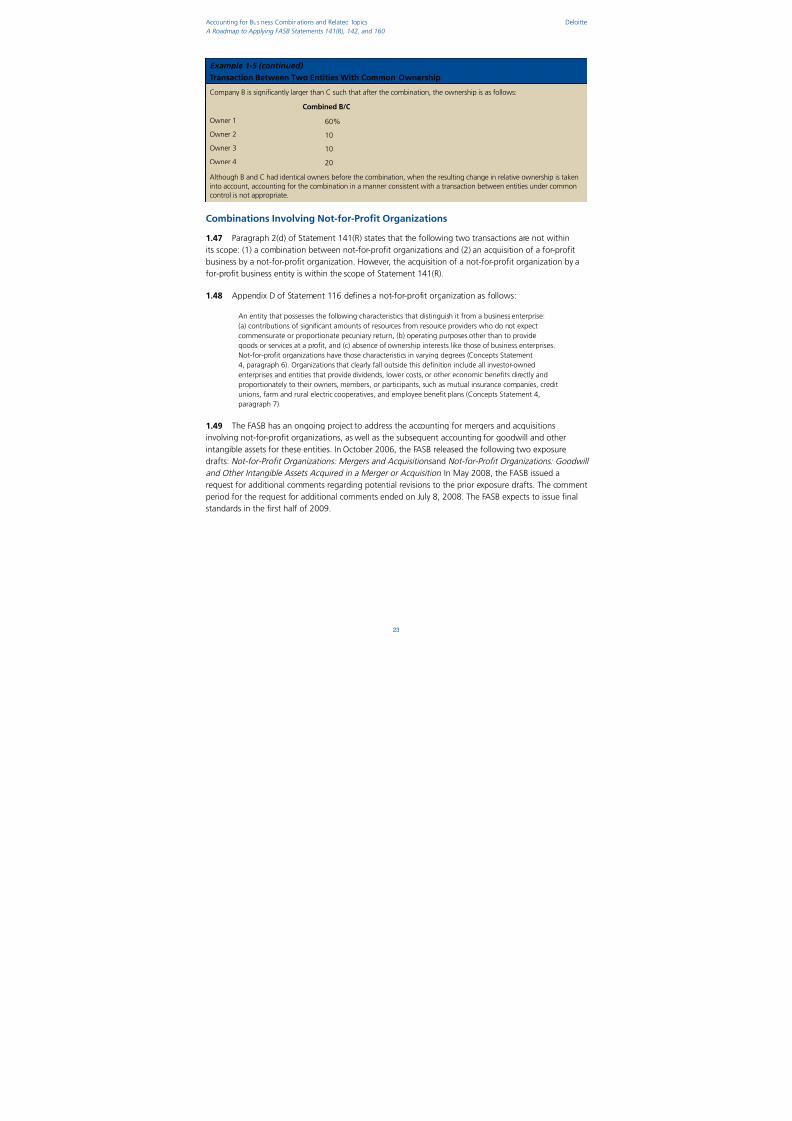

CombinationsBetweenEntitiesWithCommonOwnership 22

CombinationsInvolvingNot-for-ProfitOrganizations 23

Section 2 — Identifying the Acquirer 24

BusinessCombinationsEffectedPrimarilybyTransferringCashorOtherAssetsorbyIncurring

Liabilities 24BusinessCombinationsEffectedPrimarilybyExchangingEquityInterests 24

ConsiderationoftheRelativeVotingRightsintheCombinedEntityAftertheBusinessCombination 25

ConsiderationoftheExistenceofaLargeMinorityVotingInterestintheCombinedEntityIfNoOtherOwnerorOrganizedGroupofOwnersHasaSignificantVotingInterest 25

ConsiderationoftheCompositionoftheGoverningBodyoftheCombinedEntity 26

ConsiderationoftheCompositionoftheSeniorManagementoftheCombinedEntity 26

ConsiderationoftheTermsoftheExchangeofEquitySecurities 27

ConsiderationoftheRelativeSizeoftheCombiningEntities 27

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 4/286ii i

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

BusinessCombinationsInvolvingMoreThanTwoEntities 27

UseofaNewEntitytoEffectaBusinessCombination 27

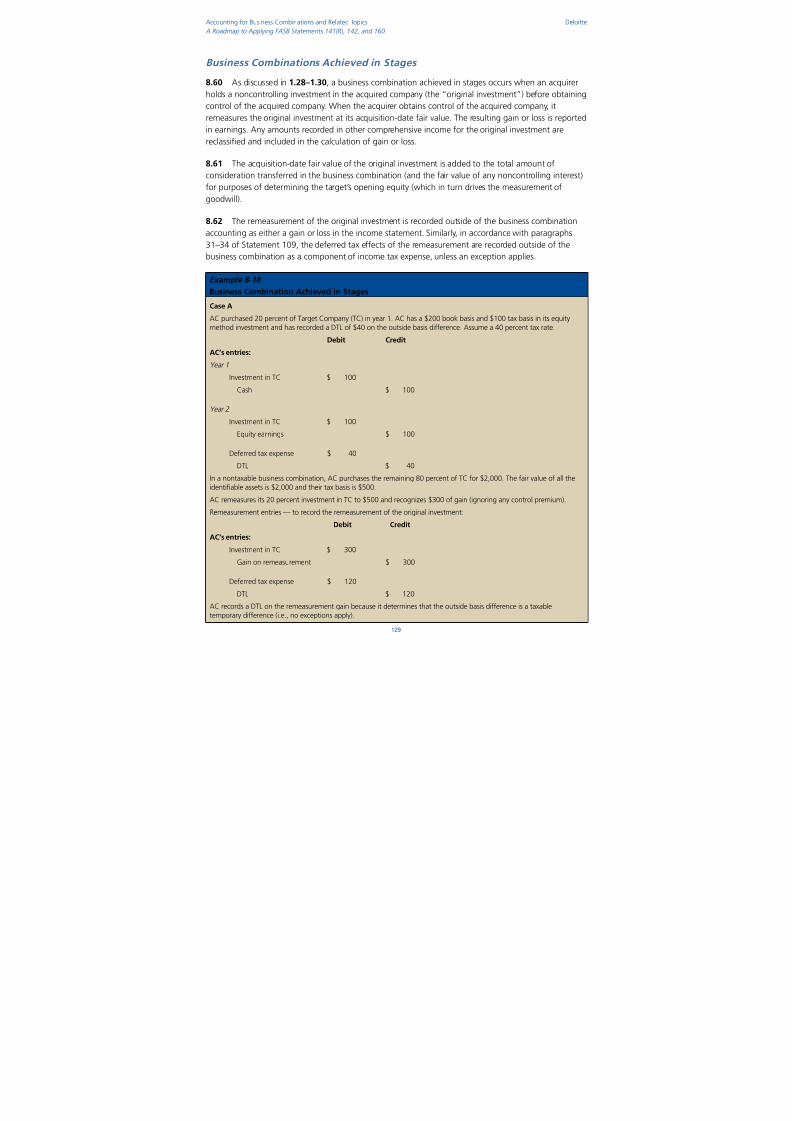

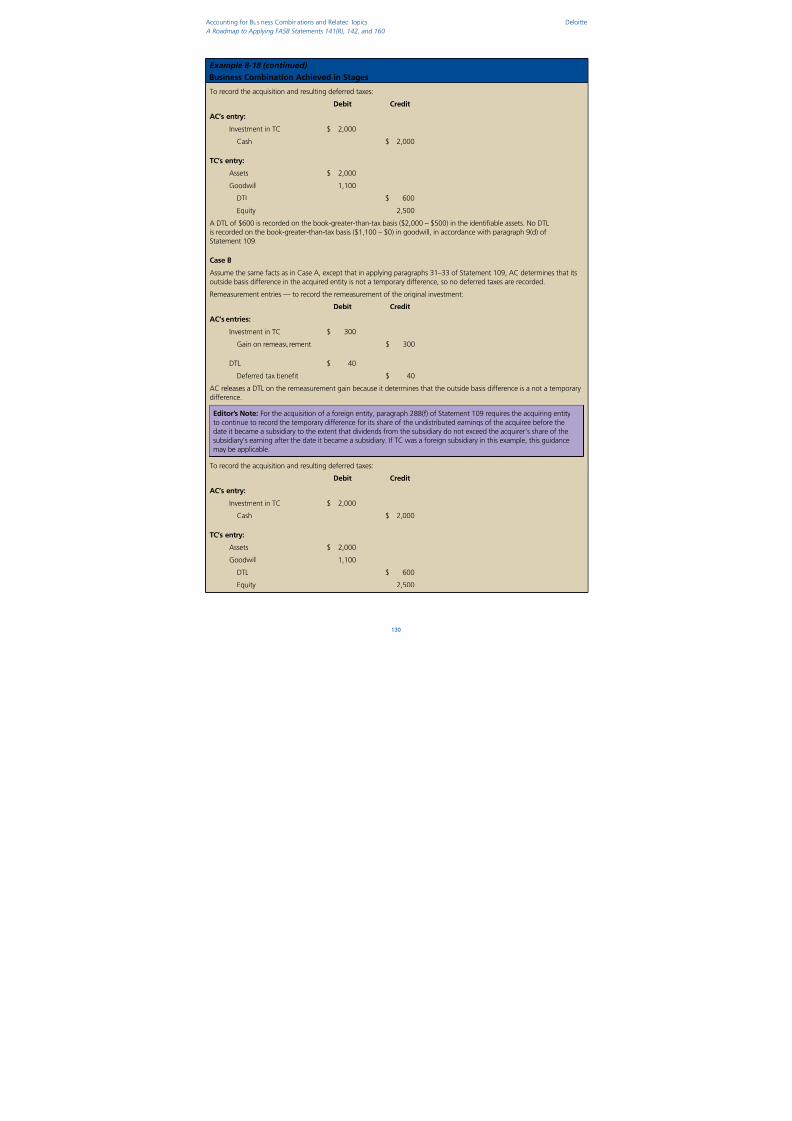

ReverseAcquisitions 28

MergersofaPrivateOperatingCompanyIntoaNonoperatingPublicShellCorporation 30

Section 3 — Recognizing and Measuring Assets Acquired and LiabilitiesAssumed — General 31

DateofAcquisition 31

RecognitionandMeasurementPrinciples 31

MeasurementPeriod 34

ImpactonSECRegistrants 36

DeterminingWhatIsPartoftheBusinessCombinationTransaction 37

FairValueMeasurementsinBusinessCombinations 41

FairValueMeasurements—TaxAmortizationBenefits 47

UseofaThird-PartySpecialisttoAssistintheMeasurementofFairValue 48

ElectionDatefortheFairValueOption 49

UseoftheResidualMethodtoValueAcquiredIntangibleAssetsOtherThanGoodwill 50

Section 4 — Recognizing and Measuring Assets Acquired and Liabilities Assumed(Other Than Intangible Assets and Goodwill) 51

Specific Guidance for Recognizing and Measuring Assets and Liabilities at Fair Value 51

TangibleAssetsThattheAcquirerIntendsNottoUseortoUseinaWayOtherThanTheirHighestandBestUse 51

AssetsWithUncertainCashFlows(ValuationAllowances) 51Inventory 52

Property,Plant,andEquipment 52

MiningAssets 53

Leases 53

Guarantees 54

LossContractsandUnfavorableContracts 55

AmountsDuetoEmployeesoftheAcquireeUponaChangeinControl 55

LiabilitiesforExitinganActivityofanAcquiredEntity,InvoluntaryTerminationBenefits,andRelocationCosts 56

RecognitionofLiabilitiesforContractualTerminationBenefitsorChangingBenefitPlanAssumptionsinAnticipationofaBusinessCombination 56

Exceptions to the Recognition and Measurement Principles 57

AssetsandLiabilitiesArisingFromContingencies 57

IncomeTaxes 58

EmployeeBenefits 59

IndemnificationAssets 60

Share-BasedPaymentAwards 61

AssetsHeldforSale 61

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 5/286iv

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Section 5 — Recognizing and Measuring Acquired Intangible Assets andGoodwill 62

Intangible Assets 62

ExamplesofIntangibleAssetsThatAreIdentifiable 62

IntangibleAssetsThatAreNotIdentifiable 64AssembledWorkforce 64

IntangibleAssetstheAcquirerIntendsNottoUseortoUseinaWayOtherThanTheirHighestandBestUse 64

GroupingComplementaryAssets 66

CustomerLists 66

OrderorProductionBacklog 67

CustomerContractsandRelatedCustomerRelationships 67

CustomerLoyaltyPrograms 68

OverlappingCustomers 68

NoncontractualCustomerRelationships 69

ConsiderationsRegardingValuationTechniquesandAssumptionstoBeUsedinMeasuringFairValueofCustomer-RelationshipIntangibleAssets 69

In-ProcessResearchandDevelopmentAssets 70

ReacquiredRights 72

FavorableorUnfavorableOperatingLeasesWhentheAcquireeIstheLessee 73

Valuing“At-the-Money”Contracts 73

IntangibleAssetsAssociatedWithIncome-ProducingRealEstate 73

Goodwill 74

MeasurementofGoodwill 74

BargainPurchases 76

Section 6 — Recognizing and Measuring the Consideration Transferred ina Business Combination 78

ConsiderationTransferredbytheAcquiringEntitytotheFormerOwnersoftheAcquiree 78

EquitySecuritiesIssuedasConsideration 78

Share-BasedPaymentAwards 78

GainsorLossesonAssetsTransferredasConsiderationbytheAcquiringEntity 83

ContingentConsideration 84

Acquisition-RelatedCostsoftheBusinessCombination 86

Separate Transactions Not Included in the Accounting for a Business Combination 87

CompensationtoEmployeesorFormerOwnersoftheAcquireeforFutureProductsorServices 87

FactorstoConsiderinAssessingWhetherContingentPaymentIsPartoftheConsiderationTransferred 88

ReimbursementMadetotheAcquireefortheAcquirer’sAcquisition-RelatedCosts 89

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 6/286v

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Section 7 — Noncontrolling Interests 90

ScopeofStatement160 90

RecognizingandMeasuringNoncontrollingInterestsasoftheAcquisitionDate 91

MeasuringNoncontrollingInterestsinReverseAcquisitions 92

FullGoodwillApproach 92AttributingNetIncome(Loss)andComprehensiveIncome(Loss)totheParentandNoncontrolling

Interest 92

LossesinExcessoftheCarryingAmountoftheNoncontrollingInterest 93

ChangesintheParent’sOwnershipInterestinaSubsidiaryWhenThereIsNoChangeinControl 94

FormerParentRetainsaNoncontrollingInterestofaSubsidiaryAfterControlIsLost 96

MultipleArrangementsAccountedforasaSingleDisposalTransaction 97

NonreciprocalTransferstoOwners 98

ConsiderationsforaPrimaryBeneficiaryofaVariableInterestEntity 99

Section 8 — Income Tax Considerations 100

Income Taxes — General 100

Tax Treatment of Business Combinations 100

TaxStatusoftheEnterprise 100

TaxableandNontaxableTransactions 100

The Basic Model — Tax Effects of Basis Differences 101

TheBasicModel 101

ImpactofTaxPlanningandBusinessIntegrationSteps 102

Push-DownofAcquisitionAccounting 102

ProcessforRecordingDeferredTaxes 102

BasisDifferences 104

Temporary Differences and Carryforwards 106

In-ProcessResearchandDevelopment 106

ContingentEnvironmentalLiability—TaxableBusinessCombination 107

AssetsHeldforSale 107

Preexisting Relationships Between Parties to a Business Combination and Reacquired

Rights 107

PreexistingRelationshipsBetweenPartiestoaBusinessCombination 107

ReacquiredRights 109

Tax Rates 111

TaxHolidays 111

StateTaxFootprint 112

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 7/286v i

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Costs of the Business Combination 112

Acquisition-RelatedCosts 112

Acquisition-RelatedCostsIncurredinaPeriodBeforetheBusinessCombination 114

DebtIssueCosts 114

CostsofRegisteringandIssuingEquitySecurities 114

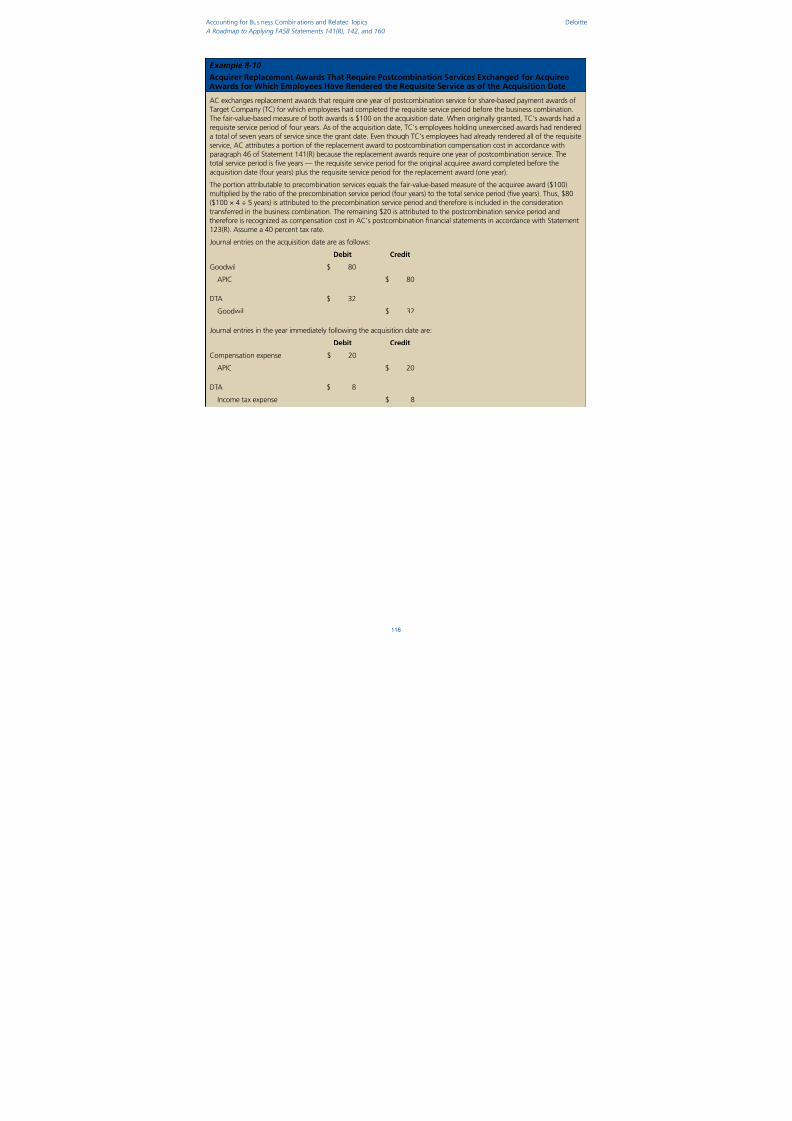

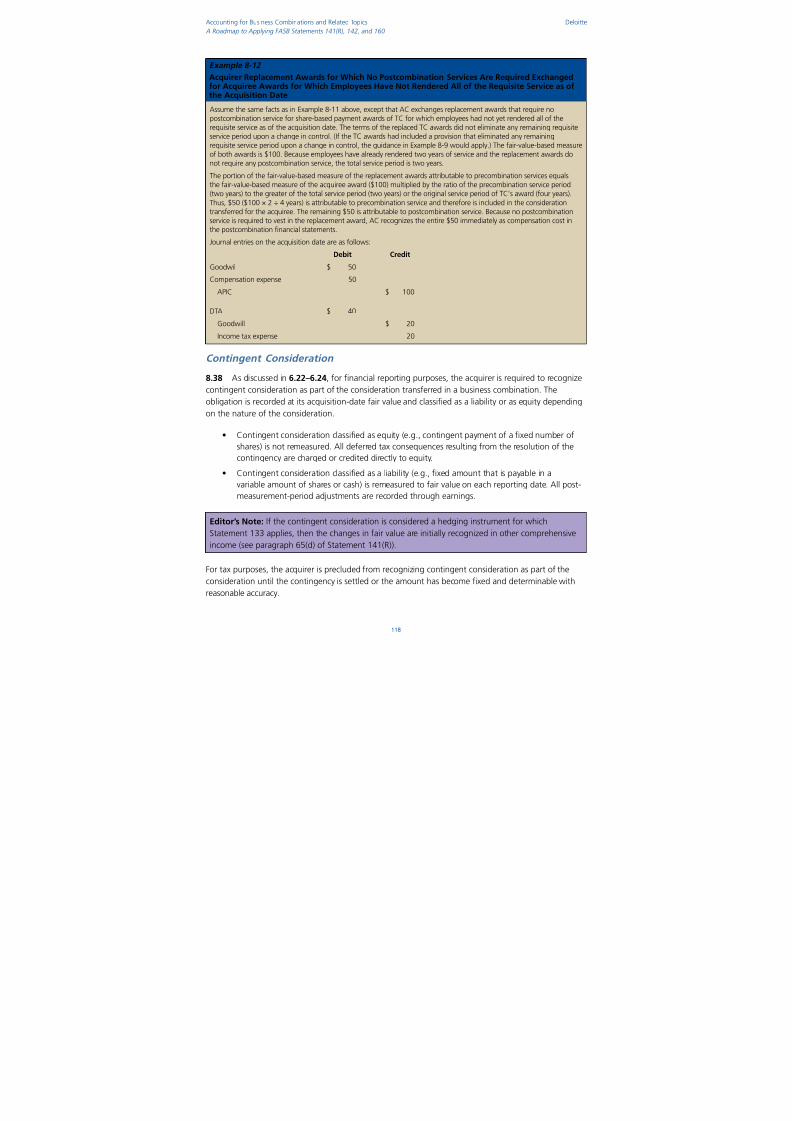

Share-Based Payment Awards Exchanged for Awards Held by the Acquiree’s Employees 115

Contingent Consideration 118

InitialMeasurementofDeferredTaxesasoftheAcquisitionDate 119

AccountingforDeferredTaxesAftertheAcquisitionDate 119

Acquirer’s Valuation Allowance 121

ChangeinanAcquirer’sValuationAllowanceasaResultofaBusinessCombination 121

Acquired Uncertain Tax Position Measurement and Recognition 121

UncertainTaxPositions—SellerIndemnification 122

Goodwill 122

GoodwillComponents 122

BookBasisExceedsTaxBasis 123

TaxBasisExceedsBookBasis 123

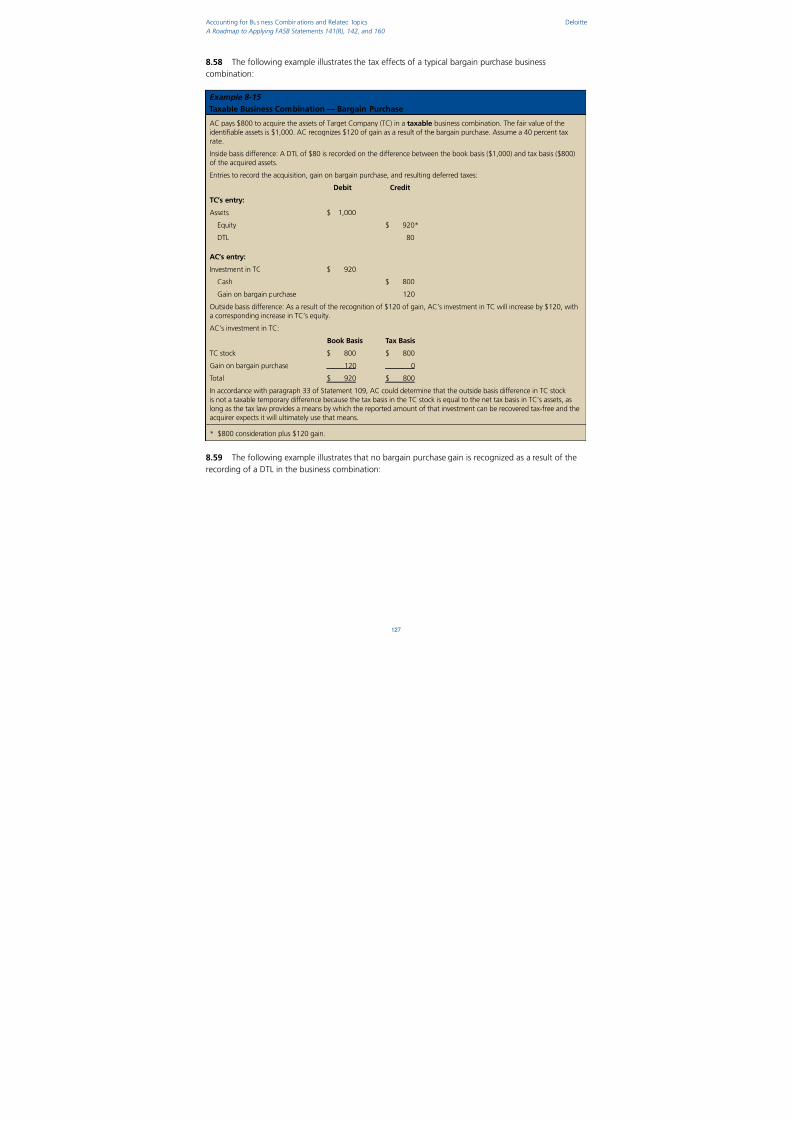

Bargain Purchases 126

Business Combinations Achieved in Stages 129

International Tax Considerations 131

InsideBasisDifferencesinaForeignAcquiredEntity 131

OutsideBasisDifferencesinaForeignAcquiredEntity 131

Transition Provisions 131

AcquiredUncertainTaxPositions 132

AcquiredDeferredTaxAssetValuationAllowances 133

DeferredTaxAssetforDeductibleTaxGoodwillinExcessofFinancialReportingGoodwill 133

Income Tax Disclosures for Business Combinations 136

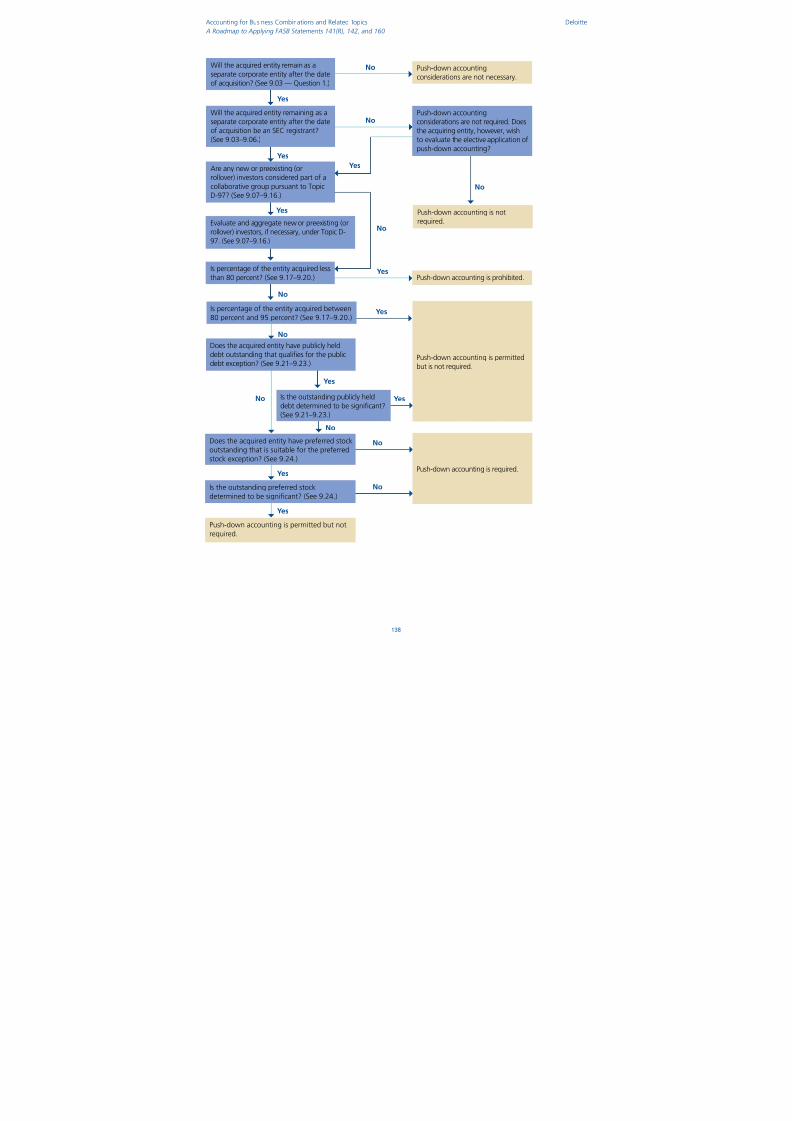

Section 9 — Push-Down Basis of Accounting 137

EvaluatingtheApplicabilityofPush-DownAccounting 137

SECStaffAccountingBulletinTopic5.J—Push-DownBasisofAccountingRequiredinCertainLimitedCircumstances 139

AdditionalSECStaffViews—ApplicabilityofEITFTopicD-97toCertainTransactions 140

ApplicabilityofPush-DownAccountingtoCompaniesThatAreNotSECRegistrants 141

CollaborativeGroups—TopicD-97 141

AdditionalConsiderationsinDeterminingthePresenceofaCollaborativeGroupUnderTopicD-97 144

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 8/286vi i

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

DeterminingWhetheraCompanyHasBecomeSubstantiallyWhollyOwned 146

EvaluatingtheAvailabilityofthePublicDebtException 147

EvaluatingtheAvailabilityofthePreferredStockException 147

SubsequentApplicationofPush-DownAccounting 148

Push-DownofGoodwilltoaSubsidiaryofanAcquiredCompany 148

Section 10 — Subsequent Accounting for Intangible Assets (Other ThanGoodwill) 149

FiniteUsefulLifeVersusIndefiniteUsefulLife 149

InternallyDevelopedIntangibleAssets 149

Determining the Useful Life of an Intangible Asset 150

AnalyzingtheExpectedUseoftheAsset 151

AnalyzingtheRelationshipoftheIntangibleAssettoOtherAssets 151

AnalyzingLegal,Regulatory,orContractualProvisionsThatMayLimitUsefulLife 152AnalyzingtheEntity’sOwnHistoricalExperienceWithRenewingorExtendingSimilar

Arrangements 152

AnalyzingtheEffectsofObsolescence,Demand,Competition,andOtherEconomicFactors 154

AnalyzingtheLevelofMaintenanceExpenditures 154

DeterminingWhetheranIntangibleAssetHasanIndefiniteUsefulLife 154

Intangible Assets Subject to Amortization 155

DeterminingtheUsefulLifeofanIntangibleAssetSubjecttoAmortizationEachReportingPeriod 155

AccountingforaChangeinRemainingUsefulLifeofanIntangibleAssetSubjecttoAmortization 155

IntangibleAssetstheAcquirerIntendsNottoUseortoUseinaWayOtherThanTheirHighestandBestUse 156

RecognitionandMeasurementofanImpairmentLossforIntangibleAssetsSubjecttoAmortization 156

MethodofAmortization 157

Intangible Assets Not Subject to Amortization 158

DeterminingtheUsefulLifeofanIntangibleAssetNotSubjecttoAmortizationEachReportingPeriod 158

In-ProcessResearchandDevelopmentIntangibleAssetsAcquiredinaBusinessCombination 158

RecognitionandMeasurementofanImpairmentLossforIntangibleAssetsNotSubjecttoAmortization 159

TimingoftheAnnualImpairmentTest 160

UnitofAccountingforImpairmentTestingofIndefinite-LivedIntangibleAssets 160

DeterminingtheCarryingAmountofanIndefinite-LivedIntangibleAssetWhenRemovingThatAssetFromaUnitofAccounting 163

CarryingForwardtheFairValueMeasurementsofIndefinite-LivedIntangibleAssetsFromOneYeartotheNext 164

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 9/286vi i i

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Section 11 — Subsequent Accounting for Goodwill 166

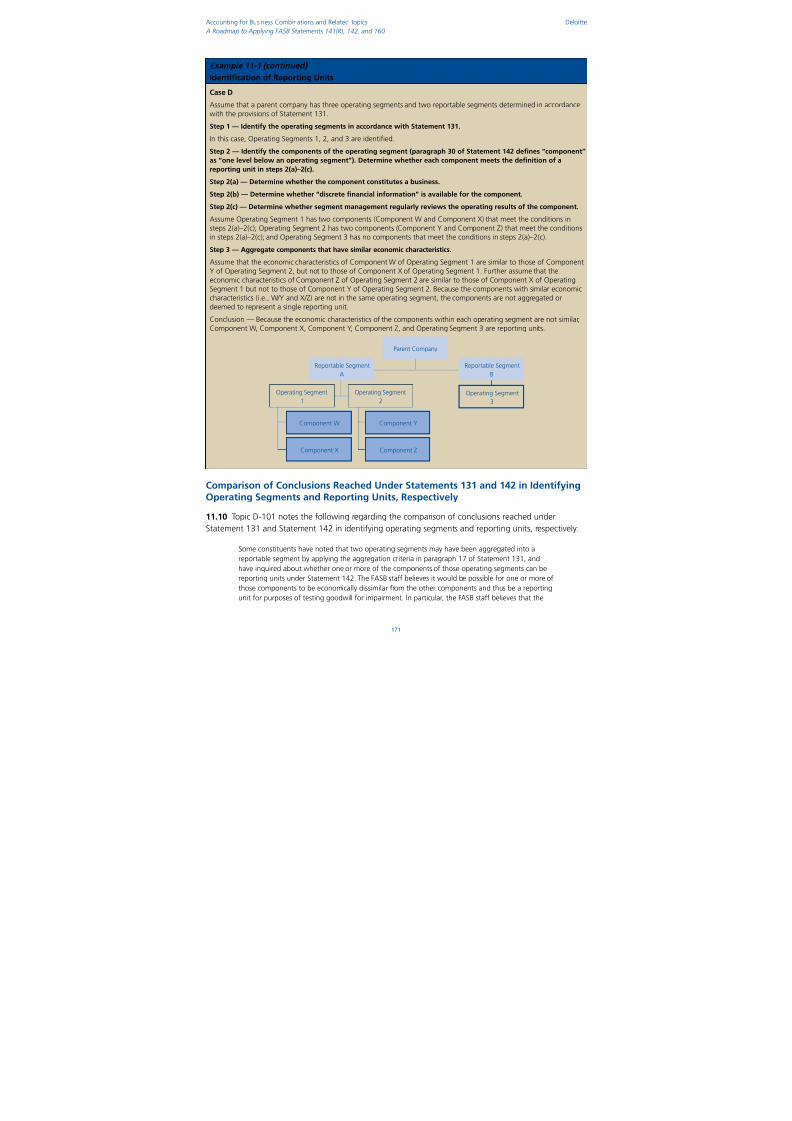

IdentificationofReportingUnits 166

EquityMethodInvestmentsasReportingUnits 169

DisclosureConsiderationsRegardingReportingUnitDeterminations 169

IdentificationofReportingUnits—Examples 169ComparisonofConclusionsReachedUnderStatements131and142inIdentifyingOperating

SegmentsandReportingUnits,Respectively 171

AssigningAssetsandLiabilitiestoReportingUnits 172

AssigningAssetsandLiabilitiesWhenanEntityHasOnlyOneReportingUnit 174

AssigningAccumulatedForeignCurrencyTranslationAdjustmentstoaReportingUnit 174

AssigningGoodwilltoReportingUnits 175

AllocationofGoodwilltoReportingUnitsforaMiningEnterprise 177

ReorganizationofReportingStructure—ReassigningAssets,Liabilities,andGoodwill 177

WhentoTestGoodwillforImpairment 177

ChangeinDateoftheAnnualGoodwillImpairmentTest—PreferabilityLetterRequirements 178

PerformingtheTwo-StepGoodwillImpairmentTest 179

InteractionoftheGoodwillImpairmentTestandtheLong-LivedAssetImpairmentTest 181

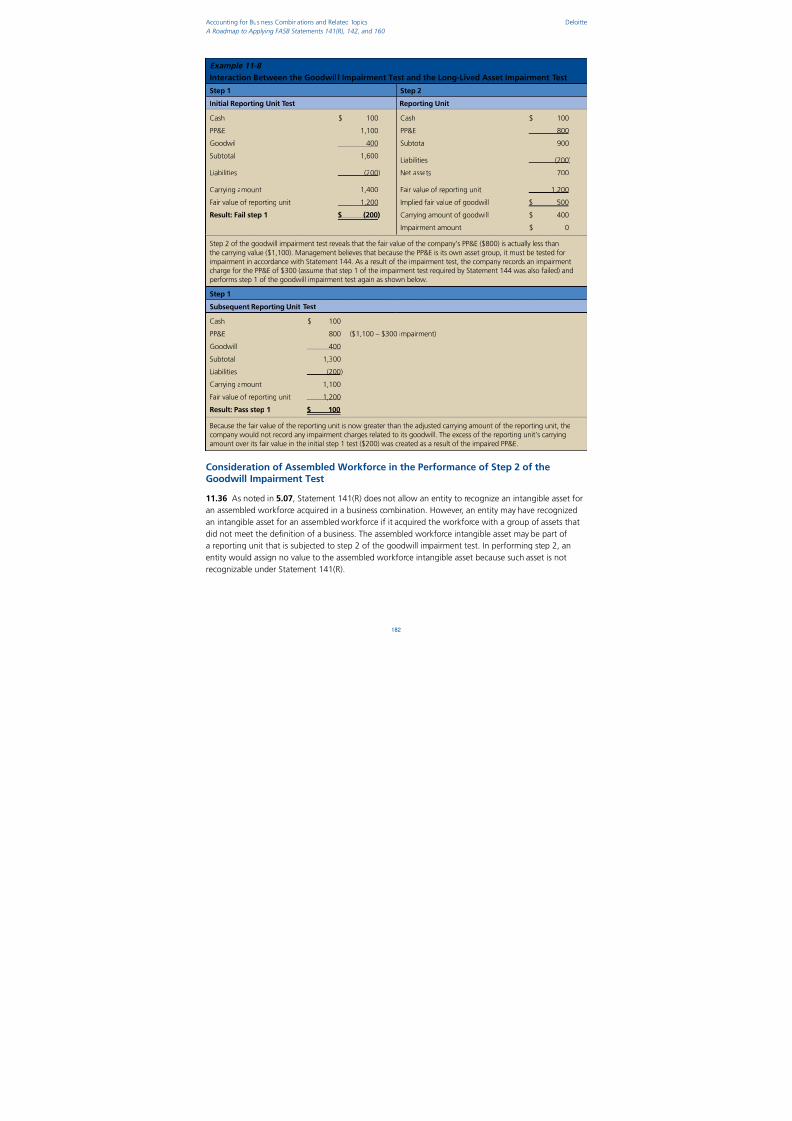

ConsiderationofAssembledWorkforceinthePerformanceofStep2oftheGoodwillImpairmentTest 182

FairValueMeasurements 183

DeterminingFairValueWhenanEntityHasOnlyOneReportingUnit 184

ChangingtheMethodofDeterminingtheFairValueofaReportingUnit 184

CarryingForwardtheFairValueofaReportingUnitFromOneAnnualTestingDatetotheNext 185

ApplyingtheGoodwillImpairmentTesttoaReportingUnitWithaNegativeCarryingValue 185DeferredIncomeTaxConsiderationsinApplyingtheGoodwillImpairmentTest 186

ReportingRequirementsWhenStep2oftheGoodwillImpairmentTestIsNotComplete 187

GoodwillImpairmentTestingbyaSubsidiary 187

DisposalofAlloraPortionofaReportingUnit 188

GoodwillImpairmentTestingandDisposalofAlloraPortionofaReportingUnitWhentheReportingUnitIsLessThanWhollyOwned 188

AssessingtheImpactofGoodwillAssignmentsontheDeterminationofGainorLossonDisposalofaReportingUnit 189

EquityMethodInvestments 190

Section 12 — Financial Statement Presentation Requirements 192

Intangible Assets 192

PresentationofIntangibleAssetsintheConsolidatedStatementofFinancialPosition 192

PresentationofIntangibleAssetAmortizationExpenseandImpairmentLossesintheConsolidatedIncomeStatement 192

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 10/286ix

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Goodwill 193

PresentationofGoodwillintheConsolidatedStatementofFinancialPosition 193

PresentationofGoodwillImpairmentLossesintheConsolidatedIncomeStatement 193

Noncontrolling Interest in a Subsidiary 193

PresentationofNoncontrollingInterestsintheConsolidatedStatementofFinancialPosition 193

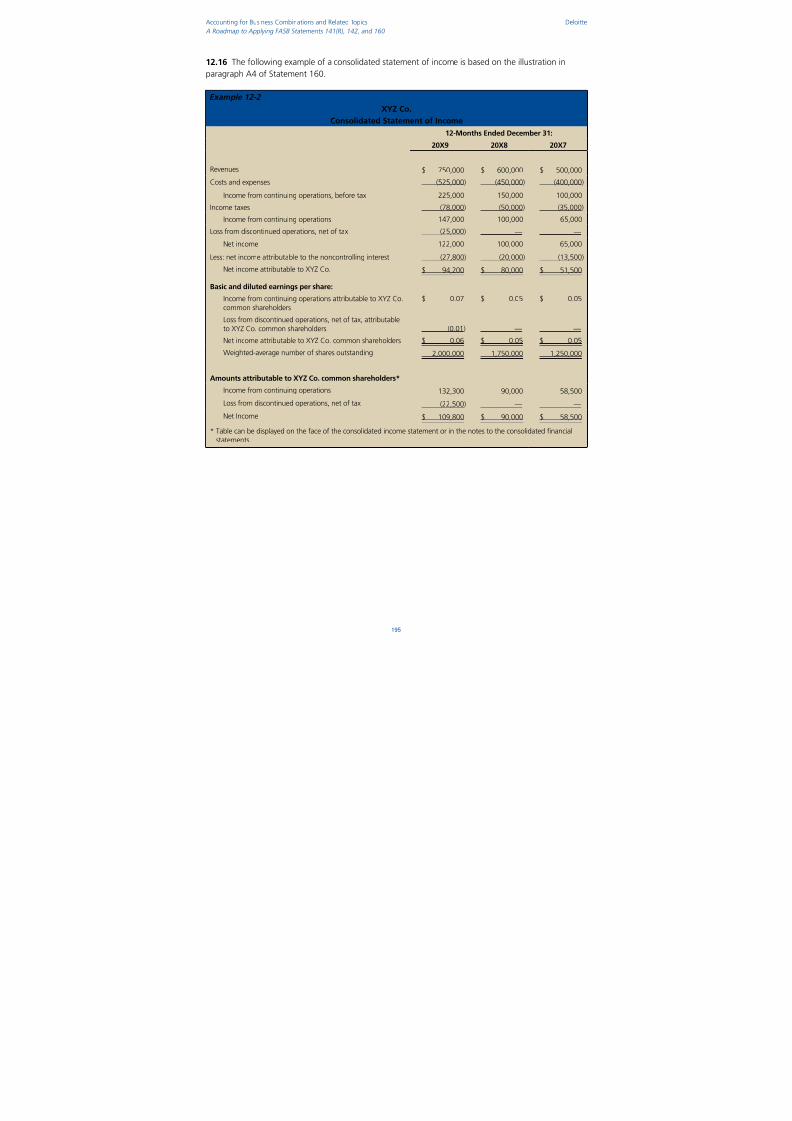

PresentationofNoncontrollingInterestsintheConsolidatedStatementofIncome 194

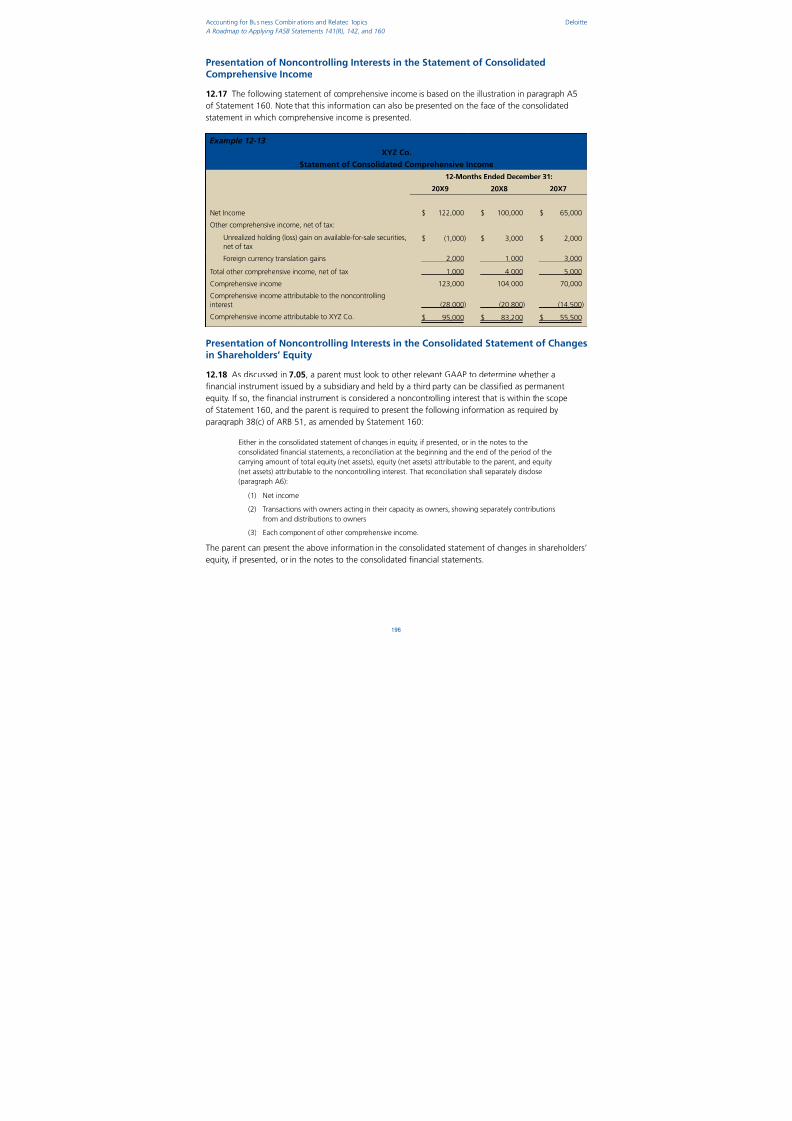

PresentationofNoncontrollingInterestsintheStatementofConsolidatedComprehensiveIncome 196

PresentationofNoncontrollingInterestsintheConsolidatedStatementofChangesinShareholders’Equity 196

Statement of Cash Flows 197

PresentationofAcquisition-RelatedCosts 197

Section 13 — Financial Statement Disclosure Requirements 198

Business Combination Disclosures 198

GeneralDisclosures 198

ConsiderationTransferred 198

ContingentConsiderationandIndemnificationAssets 199

AcquiredReceivables 199

AssetsAcquiredandLiabilitiesAssumedbyMajorClass 199

AssetsandLiabilitiesArisingFromContingencies 200

Goodwill 200

TransactionsRecognizedSeparatelyFromtheBusinessCombination 201

BargainPurchases 201

PartialAcquisitions 201

AdditionalDisclosuresbyaPublicBusinessEnterprise 202

ImmaterialBusinessCombinations 203

BusinessCombinationsCompletedAftertheBalanceSheetDate 203

InitialAccountingfortheBusinessCombinationIsNotComplete 203

Statement157DisclosureConsiderations(Postcombination) 204

InterimFinancialInformation 204

Goodwill and Intangible Assets Disclosures 205

DisclosuresinthePeriodofAcquisition 205

Disclosures,IncludingSegmentInformation,inEachPeriodPresented 205

IntangibleAssetsSubjecttoRenewalorExtension 206

IntangibleAssetImpairments 207

GoodwillImpairments 207

DisclosureConsiderationsRegardingReportingUnitDeterminations 207

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 11/286x

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Noncontrolling Interest in a Subsidiary Disclosures 207

ChangesinaParent’sOwnershipInterestinaSubsidiary 208

ExcessLosses 209

Other 209

Deconsolidations 209

IncomeTaxes 210

Section 14 — Transition Requirements and Other Adoption Considerations 211

Statement 141(R) 211

IncomeTaxes 211

ContingentConsideration 213

RestructuringandExitCostsoftheAcquiree 214

Acquisition-RelatedCostsIncurredonCurrentTransactions 215

GoodwillImpairmentConsiderations 216

SAB74Disclosures 218

SECAmendments 219

MutualEntities 219

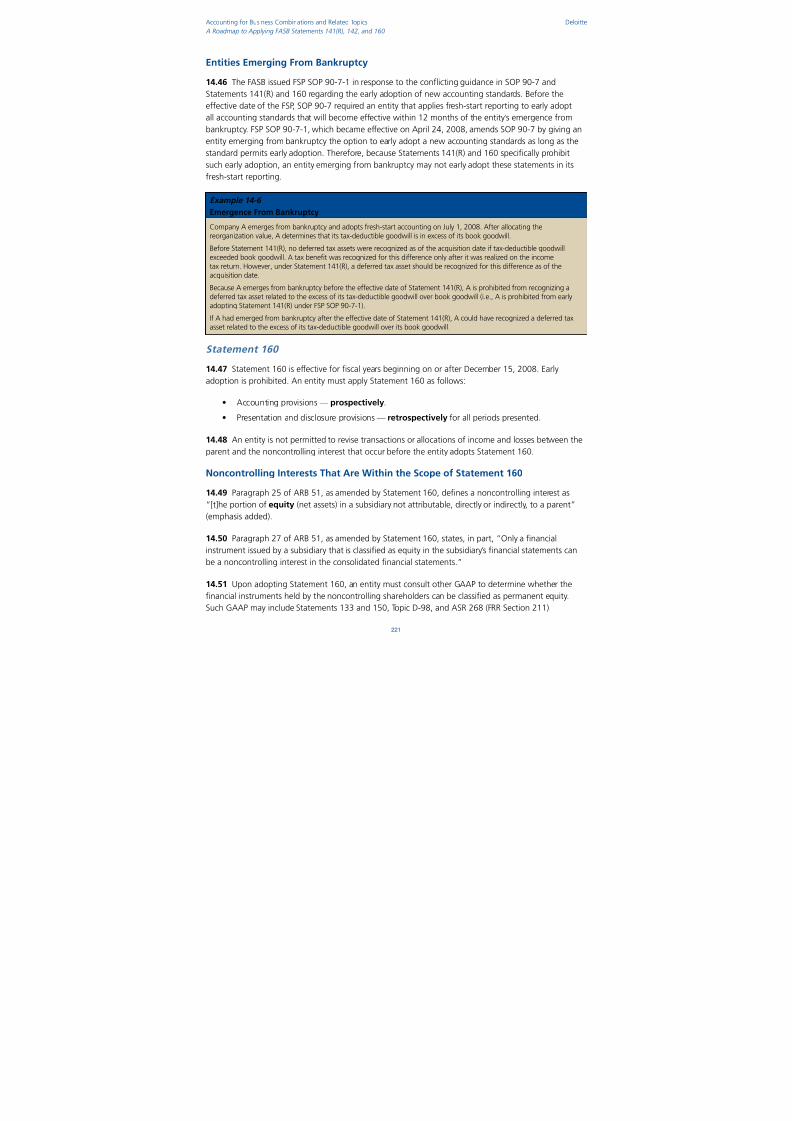

EntitiesEmergingFromBankruptcy 221

Statement 160 221

NoncontrollingInterestsThatAreWithintheScopeofStatement160 221

CalculationofEarningsperShare 222

ChangesinaParent’sOwnershipInterestinaSubsidiary 222

AttributingNetIncomeorLosstotheParentandtheNoncontrollingInterest 223

AttributionofLossesThatExceedtheCarryingAmountoftheNoncontrollingInterestinaSubsidiary 223

GoodwillImpairmentConsiderations 225

SAB74Disclosures 228

SECAmendments 229

Appendix A — Differences Between Statements 141 and 141(R) 230

Scope 230

DefinitionofaBusiness 230

DeterminingtheAcquisitionDate 231

MeasurementDateforMarketableEquitySecuritiesoftheAcquirerIssuedtoEffectaBusinessCombination 231

ProvisionalMeasurementofAssetsAcquiredandLiabilitiesAssumed 232

AdjustmentstoValuationAllowancesforAcquiredDeferredTaxAssetsandUncertainTaxPositions 233

RecognitionofDeferredTaxAssets 234

Acquisition-RelatedCosts 235

PartialAcquisitions 235

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 12/286x i

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

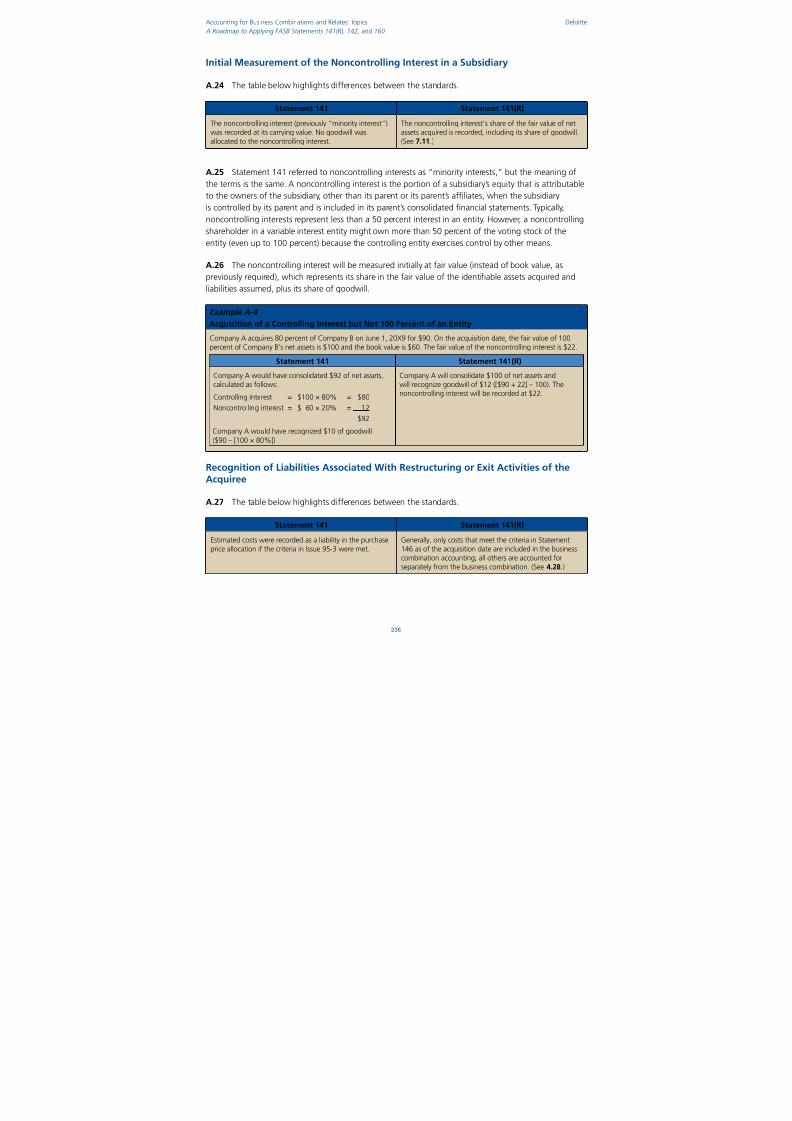

InitialMeasurementoftheNoncontrollingInterestinaSubsidiary 236

RecognitionofLiabilitiesAssociatedWithRestructuringorExitActivitiesoftheAcquiree 236

ReacquiredRights 237

In-ProcessResearch&Development(IPR&D) 237

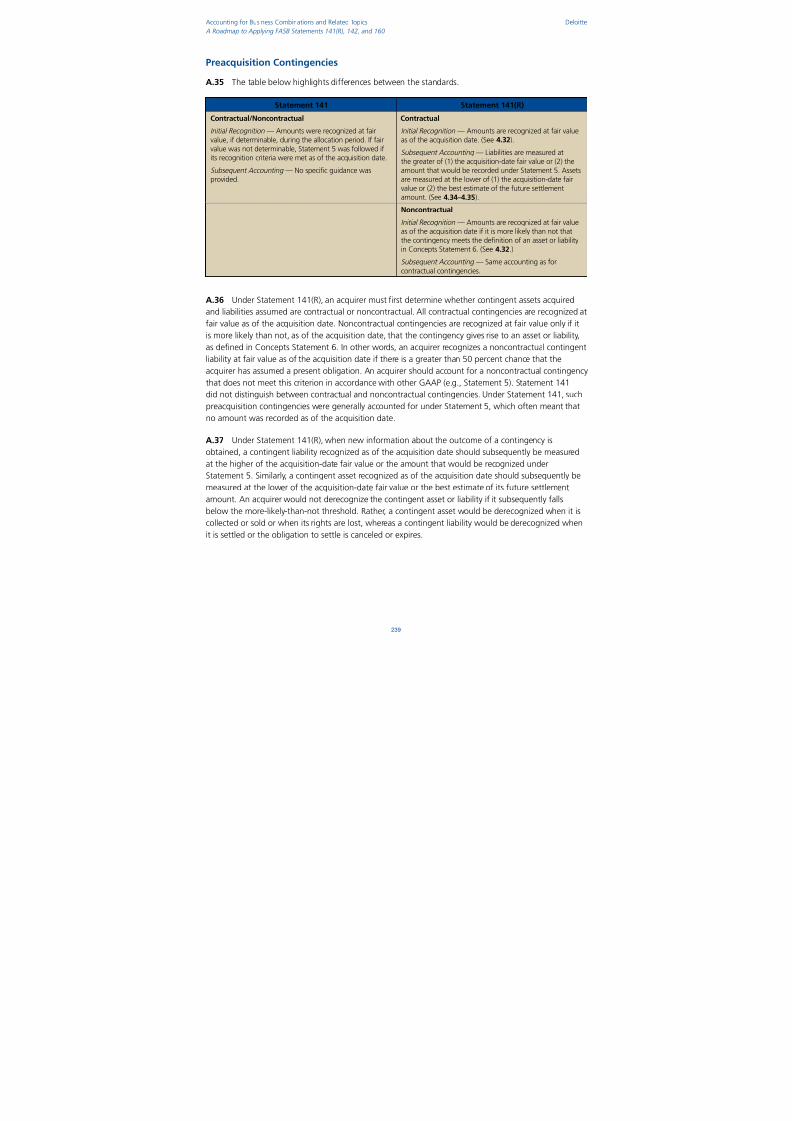

PreacquisitionContingencies 239

ContingentConsideration 240

IndemnificationAssets 240

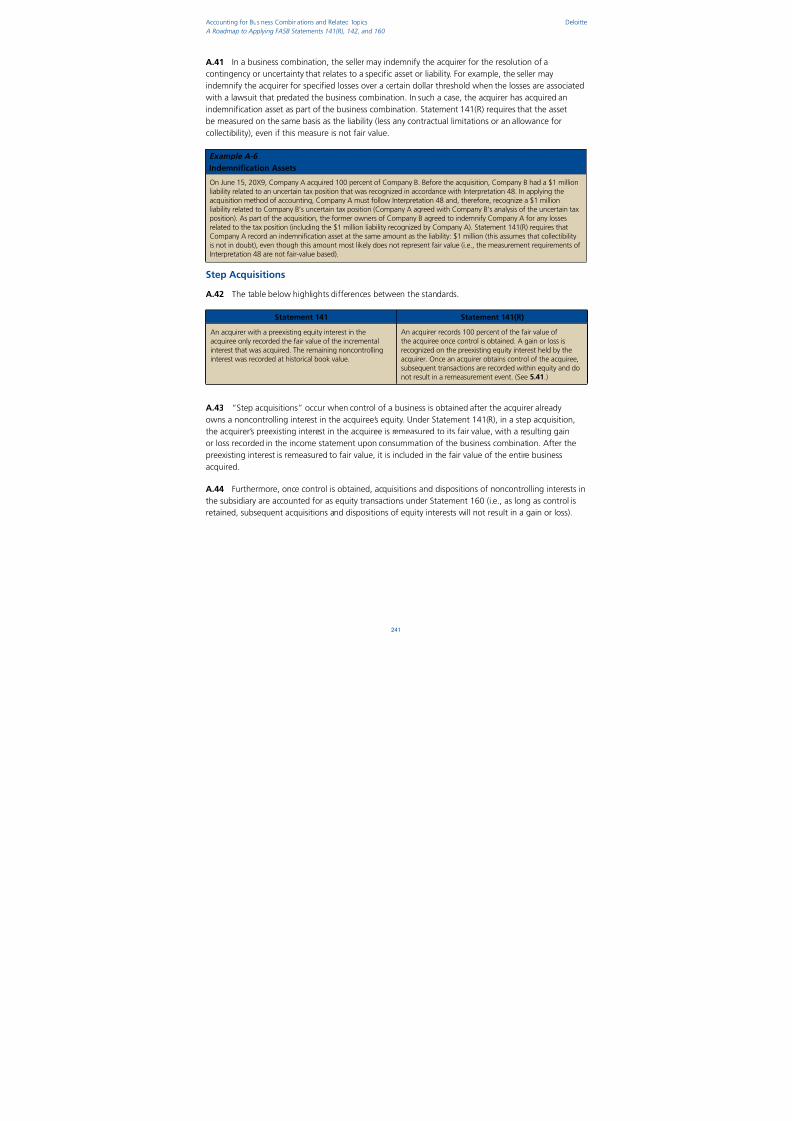

StepAcquisitions 241

ValuationAllowanceforAssetsRecordedatFairValue 242

AssetsThatanAcquirerIntendsNottoUseorUseinaWayOtherThanTheirHighestandBestUse 243

BargainPurchase(anExcessofFairValueofAcquiredNetAssetsOverCost) 243

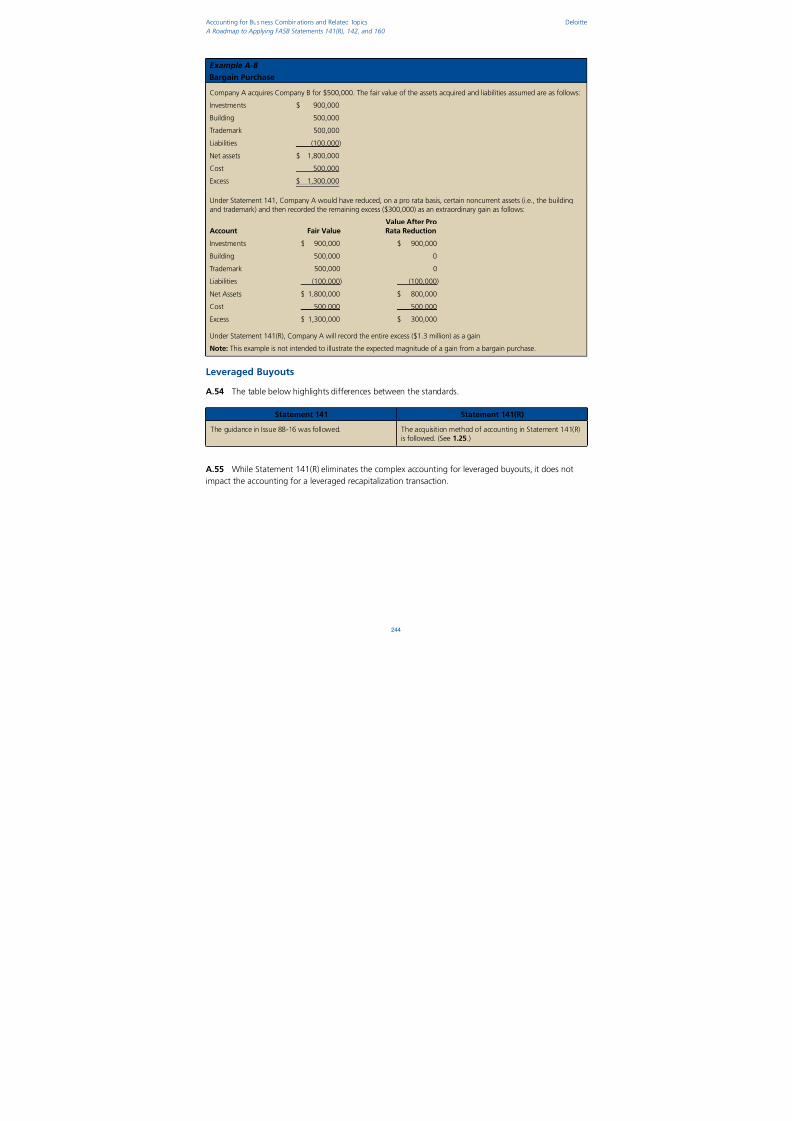

LeveragedBuyouts 244

Share-BasedPaymentAwardsExchangedforAwardsHeldbytheAcquiree’sEmployees 245

PensionandOtherPostretirementBenefitObligations 245

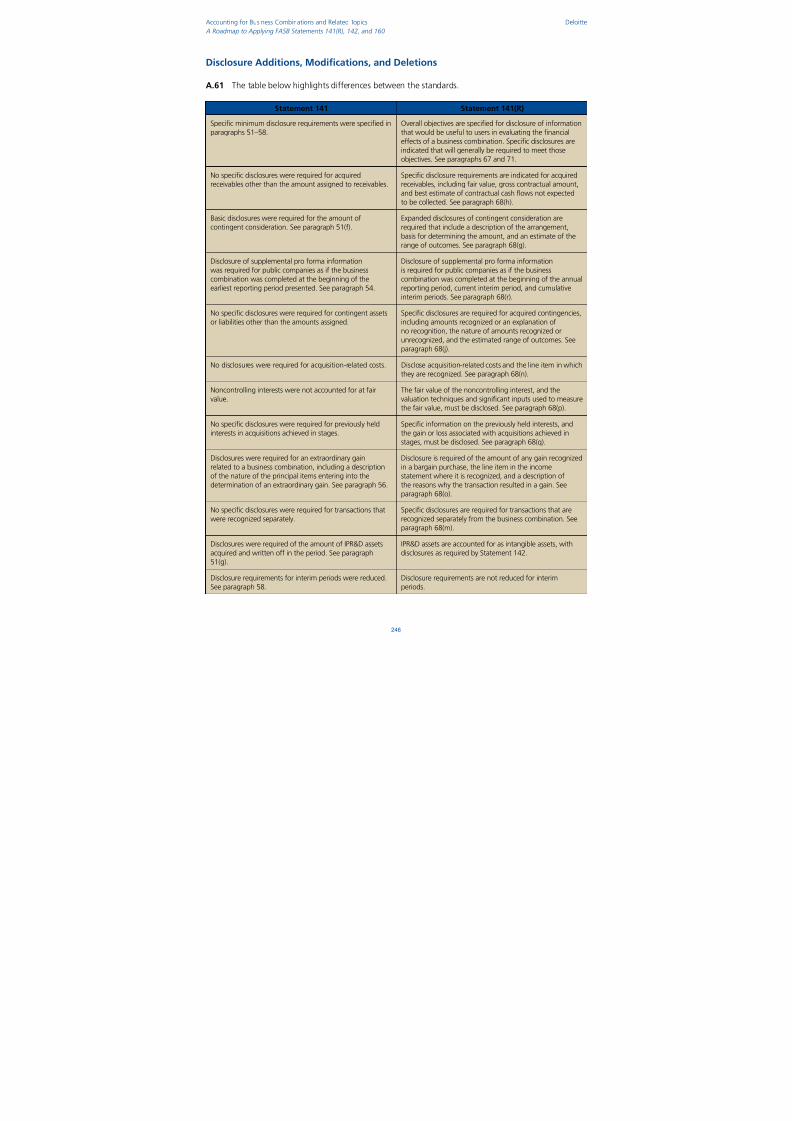

DisclosureAdditions,Modifications,andDeletions 246

Appendix B — Differences Between Pre-Amended ARB 51 and Statement 160 247

PresentationofNoncontrollingInterests—ConsolidatedStatementofFinancialPosition 247

PresentationofNoncontrollingInterests—ConsolidatedStatementofIncome 248

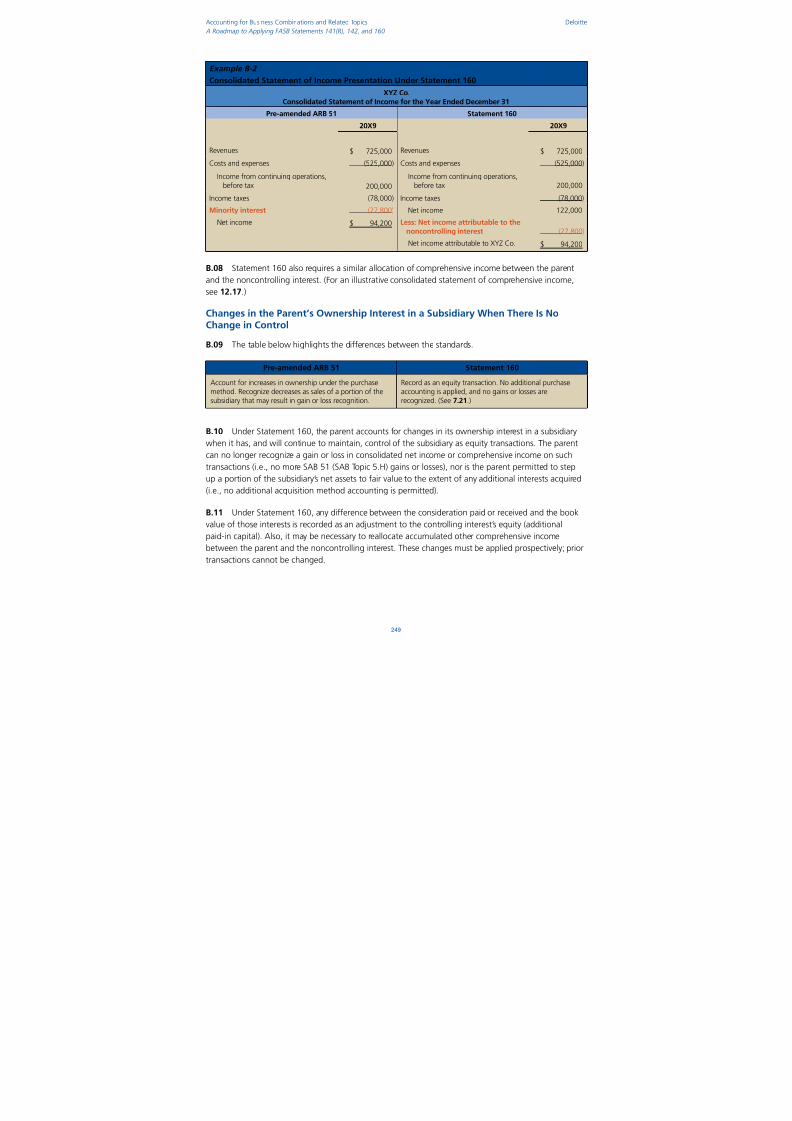

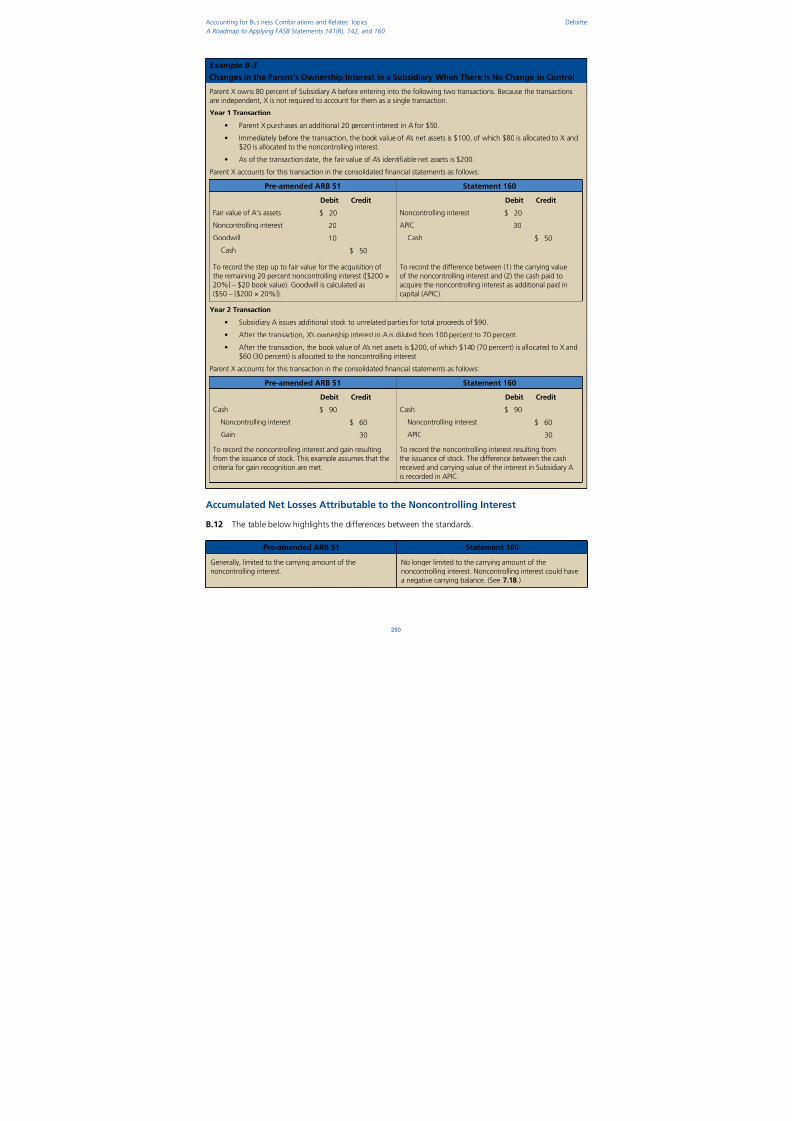

ChangesintheParent’sOwnershipInterestinaSubsidiaryWhenThereIsNoChangeinControl 249

AccumulatedNetLossesAttributabletotheNoncontrollingInterest 250

ParentDeconsolidatesaSubsidiarybutRetainsaNoncontrollingInvestment 251

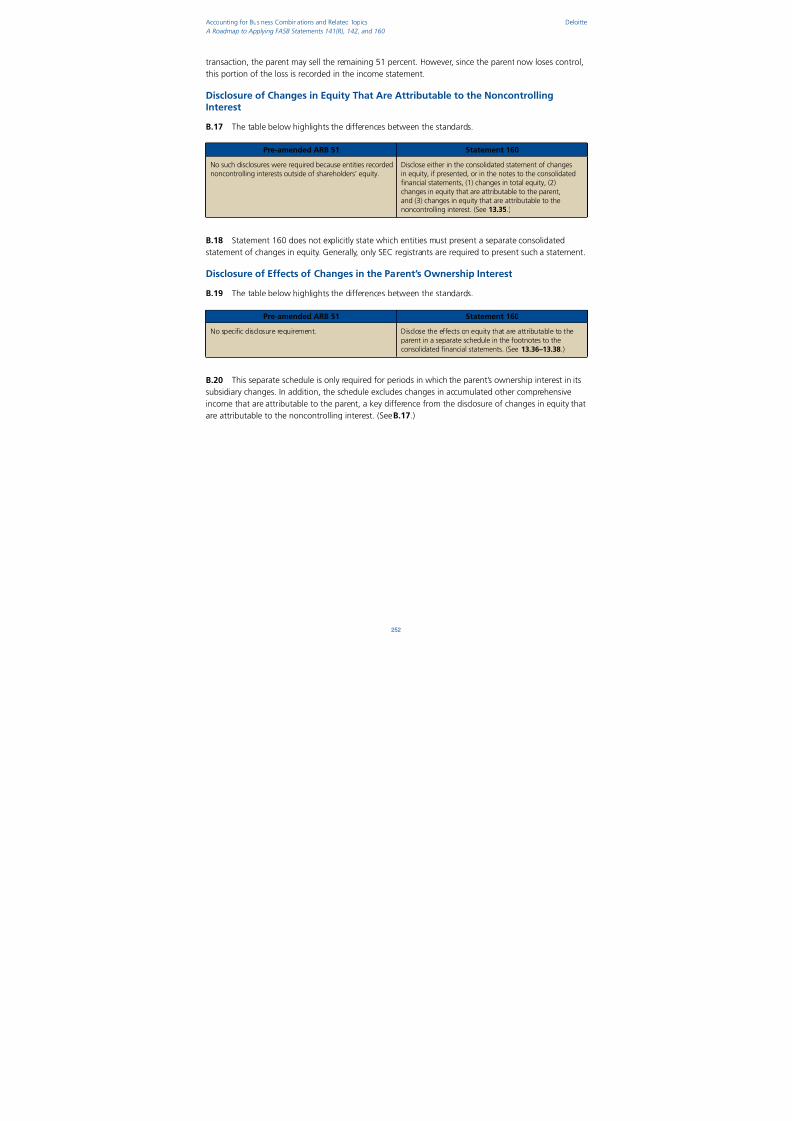

DisclosureofChangesinEquityThatAreAttributabletotheNoncontrollingInterest 252

DisclosureofEffectsofChangesintheParent’sOwnershipInterest 252

Appendix C — Differences Between U.S. GAAP and IFRSs 253

Differences Between Statement 141(R) and IFRS 3(R) 253

Different Conclusions Reached During the Joint Business Combinations Convergence

Project 253

EffectiveDateandTransition 253

Scope 254

NoncontrollingInterests—InitialMeasurement 255

AcquiredContingencies—InitialMeasurement 256

AcquiredContingenciesRecognizedasoftheAcquisitionDate—SubsequentMeasurement 257OperatingLeasesinWhichtheAcquireeIstheLessor 257

ContingentConsiderationClassifiedasaLiability—SubsequentMeasurement 258

Disclosures—ProFormaFinancialInformation 258

Disclosures—GainorLossRecognizedAftertheAcquisitionDateforNetAssetsAcquired 259

Disclosures—Goodwill 259

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 13/286xi i

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Differences Outside the Scope of the Joint Business Combinations Convergence Project 260

DefinitionofControl 260

DefinitionofFairValue 260

ContingentConsideration—InitialClassification 260

DeferredTaxesandUncertainTaxPositions 261

EmployeeBenefits 261

Share-BasedPaymentAwards—InitialMeasurement 261

ReplacementShare-BasedPaymentAwards—AllocationofAmountstoConsiderationTransferred 261

Disclosures—AcquiredContingencies 262

Differences Between Statement 160 and IAS 27(R) 262

Differences Between Statement 142 and IAS 36/38 262

LevelofImpairmentTestingforGoodwill 262

GoodwillImpairmentTesting 263

ImpairmentTestingofIndefinite-LivedIntangibleAssets 265

IntangibleAssetRevaluations 265

InternallyDevelopedIntangibleAssets 266

AdvertisingCosts 267

Appendix D — Glossary of Standards and Regulations 268

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 14/2861

Acknowledgments

Thispublicationistheresultofacollaborativeeffort,bringingtogetherthethoughtfulleadership

ofourassuranceandtaxprofessionals.WearegratefulforthecontributionsofChrisBarton,Jason

Embick,TrevorFarber,MarkFisher,HeatherJurek,RobinKramer,ConnieLee,DerekMalmberg,Michelle

Marseglia,JeffMinick,MichaelMorrissey,RichardPaul,MikeScheiner,StefanieTamulis,andStephanie

Wolfe.Inaddition,wewouldliketoacknowledgethehardworkofourProductionGroup,specifically

LynneCampbell,DianeCastro,YvonneDonnachie,MichaelLorenzo,JoanMeyers,JeaninePagliaro,

andJosephRenouf.StuartMosssupervisedtheoverallpreparationofthispublicationandwouldliketo

acknowledgethecontributionsoftheseprofessionals,extendingtothemhisdeepestappreciation.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 15/2862

Executive Summary

Background

InDecember2007,theFASBcompletedthesecondphaseofitsbusinesscombinationsproject.Thefirstphase,completedin2001,hadresultedintheissuanceofStatements1411and142andincluded

suchchangesastheeliminationofthepooling-of-interestmethodofaccountingandtheamortization

ofgoodwill.Thesecondphaseconstitutedamajoroverhauloftheaccountingrulesforbusiness

combinationsandnoncontrollinginterests(formerlyreferredtoas“minorityinterests”)thatwerenot

reconsideredinthefirstphase(e.g.,manyaspectsofthepurchasemethodofaccounting).

TheFASBissuedthefollowingtwostandardsattheendofthesecondphase:

• StatementNo.141(R),BusinessCombinations .

• StatementNo.160,NoncontrollingInterestsinConsolidatedFinancialStatements—an

amendmentofARBNo.51.

Thenewstatementswillgenerallyrequire:

• Additionaluseoffairvaluemeasurements,bothasoftheacquisitiondateandin

postcombinationperiods,whichmayresultinincreaseduseofthird-partyvaluationspecialists.

• Recognitionofadditionalassetsandliabilities,asoftheacquisitiondateandinpostcombination

periods,inaccountingforthebusinesscombination.Theseassetsandliabilitiesinclude(1)

preacquisitioncontingencies,(2)contingentconsideration,(3)assetsthatanacquirerdoesnot

intendtouse(e.g.,defensiveintangibleassets),and(4)acquiredassetsassociatedwithresearch

anddevelopmentactivities(i.e.,acquiredin-processresearchanddevelopment(IPR&D)).• Theaccountingforcertainitems,suchasacquisitioncostsandrestructuringchargesrelatedto

theacquiredbusiness,outsideofbusinesscombinationaccounting.Thisrequirementmayresult

inearningsvolatilitybothbeforeandafterconsummationofthebusinesscombination.

• Enhanceddisclosuresaboutcompletedbusinesscombinations.

SomeoftherecentchangestobusinesscombinationaccountingwillaffectnotonlyU.S.companiesbut

alsocompaniesreportingunderIFRSs.Inthesecondphaseoftheproject,theFASBworkedwiththe

IASBtosubstantiallyconvergetheaccountingforbusinesscombinationsandnoncontrollinginterests

underU.S.GAAPandIFRSs.Thishasbeenthemostsignificantconvergenceprojecttodateandhas

helpedpavethewayforfutureconvergenceprojectsinotherareas.AfewdifferencesbetweenU.S.GAAPandIFRSsintheaccountingforbusinesscombinationsstillremain,includingthedelayedeffective

datefortheIASB’sstandardsIFRS3(R)andIAS27(R)(annualperiodsbeginningonorafterJuly1,2009)

andtheinitialmeasurementofnoncontrollinginterestsinbusinesscombinations.

Inaddition,notethatStatements141(R)and160affectareasotherthanbusinesscombinations,

including(1)theaccountingforexistingnoncontrollinginterests,(2)goodwillimpairmenttesting

(regardlessofwhenthegoodwillwasrecognized),and(3)accountingforchangesintheparent’s

ownershipinterestinasubsidiary(includingdeconsolidations).Significantchangesfromtheprevious

accountingunderU.S.GAAParedescribedinmoredetailbelow.

1 ThetitlesofthestandardsandregulationsreferencedinthisRoadmaparedefinedinAppendix D.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 16/2863

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Effective Date and Transition

Thestatements’accountingprovisionsrequireprospectiveapplicationtotransactionsconsummated

infiscalyearsbeginningonorafterDecember15,2008,withoneexceptionforcertainincometax

balances.2Earlyadoptionisprohibited.Therefore,forcalendar-year-endcompanies,thenewstatements

onlyaffecttransactionsclosingonorafterJanuary1,2009.Statement160requiresretrospective

applicationofitspresentation and disclosureprovisionsforallpriorperiodspresentedinthefinancial

statements.

Overview of Significant Accounting Changes

Contingent Consideration—Manypurchaseagreementscontaincontingentconsideration

arrangements(commonlyreferredtoas“earnouts”).Thesearrangementstypicallyobligatethe

acquirertotransferadditionalconsiderationtotheformerownersoftheacquireeifafutureeventor

conditionismet(e.g.,acontingencybasedonthepostcombinationperformanceoftheacquiredentity).

UnderStatement141(R),theacquirermust(1)recognizethearrangementintheacquisitionmethod

accountingatfairvalueand(2)classifytheamountaseitheraliabilityorequityinaccordancewith

otherexistingU.S.GAAP.Theacquirerrecognizessubsequentchangesinfairvalueofaliabilityinits

postcombinationearnings,butdoesnotadjustamountsclassifiedasequity.Underpreviousguidance,

theacquirertypicallyadjusteditspurchaseaccountingwhenthecontingencywassettledorpaid,with

nodirecteffectonpostcombinationearnings.

Thedeterminationoffairvalueinthesearrangementsandclassificationasaliabilityorequityisoften

difficultandmayrequiretheassistanceofthird-partyvaluationandfinancialinstrumentspecialists.The

structureofmanycontingentconsiderationarrangementswillmostlikelyresultinliabilityclassification

underthenewguidance,whichmayleadtopostcombinationearningsvolatility.Therefore,under

Statement141(R),entitiesmaychangethestructure,timing,anduseofearnoutsinfuturedealsto

avoiduncertaintiesintheirpostcombinationearnings.

Measurement Date of the Acquirer’s Equity Securities Issued —Statement141(R)requiresthat

equitysecuritiesissuedasconsiderationinabusinesscombinationberecordedatfairvalueasof

theacquisitiondate.Underpreviousguidance,theacquirer’sequitysecuritiesweregenerallyvalued

overareasonableperiodbeforeandafterthetermsofthebusinesscombinationareagreedtoand

announced.Becausethevalueofsecuritiesmaychangesignificantlybetweentheannouncementdate

andtheacquisitiondate,underStatement141(R),substantiallydifferentamountsmightberecordedas

considerationtransferredandthusasgoodwill.

Preacquisition Contingencies3—Theaccountingforanacquiredcontingencydependsonwhether

itiscontractualornoncontractual.Contractualcontingenciesarerecognizedattheiracquisition-datefairvalue.Noncontractualcontingenciesarerecognizedattheiracquisition-datefairvalue,butonlyif

itismorelikelythannot(i.e.,morethan50percentlikely)thatthecontingencymeetsthedefinition

ofanassetoraliability.Inotherwords,foranoncontractualcontingentliability,ifitismorethan50

percentlikelythatanacquirerhasassumedapresentobligation,therecognitionthresholdismet.If

not,noamountisrecognized.Therefore,underStatement141(R),moreacquiredcontingencieswill

2 Statement141(R)requiresthatanentityrecord,asacomponentofincometaxexpense,adjustmentsafterthemeasurementperiod(andadjustmentsduringthemeasurement

periodthatrelatetofactsandcircumstancesthatdidnotexistasoftheacquisitiondate)to(1)valuationallowancesforacquireddeferredtaxassetsand(2)uncertaintaxpositions

oftheacquiredentity.UnderthetransitionprovisionsofStatement141(R),thisrequirementappliestoallbusinesscombinations,regardlessoftheconsummationdate(i.e.,itcould

affectpriordeals).

3 Paragraph1ofStatement5definesacontingencyas“anexistingcondition,situation,orsetofcircumstancesinvolvinguncertaintyastopossiblegain...orloss...toanentity

thatwillultimatelyberesolvedwhenoneormorefutureeventsoccurorfailtooccur.”Theaccountingforcontingentconsiderationarrangementsisdiscussedseparately.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 17/2864

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

bemeasuredatfairvalueasoftheacquisitiondate.Underpreviousguidance,whenaccountingfor

acquiredcontingencies,entitiesoftendidnotrecordanyamountinthepurchaseaccountingand

generallyfollowedtheguidanceinStatement5.

Inaddition,unlikepreviousguidance,Statement141(R)coverssubsequentmeasurementof

contingenciesrecordedatfairvalueasoftheacquisitiondate.UnderStatement141(R),ifnew

informationbecomesavailableaftertheacquisitiondate,acontingentliabilityrecognizedasofthe

acquisitiondatemustberemeasuredatthehigherofitsacquisition-datefairvalueortheamount

thatwouldberecognizedunderStatement5.Acontingentassetisremeasuredatthelowerofits

acquisition-datefairvalueorthebestestimateofitsfuturesettlementamount.Inaddition,anacquired

contingencyisderecognizedonlyuponitsresolution.

Editor’s Note: OnDecember15,2008,theFASBissuedproposedFSPFAS141(R)-a,whichwould

amendStatement141(R)torequirethatpreacquisitioncontingenciesgenerallybemeasuredatfair

valueasoftheacquisitiondateifsuchamountscanbereasonablydetermined.Itisexpectedthatthe

guidanceintheproposedFSPwouldresultintherecognitionofmorecontingentassetsandliabilities

atfairvaluethantheguidanceinStatement141,butfewerthanthecurrentStatement141(R)guidance.ThisRoadmapwillbeupdatedforthefinalguidanceonceitisissuedbytheFASB.

Assets That the Acquirer Intends Not to Use or to Use in a Way Other Than Their Highest

and Best Use (e.g., Defensive Value Intangible Assets) —Anacquirermaydecidenottouse

anacquiredassetforcompetitiveorotherreasons(e.g.,atradenameofanacquireethatcompetes

withtheacquirer’sowntradename),butitwouldstilldefendtheassetsothatotherscannotuseit.

UnderStatement141(R),anacquirermustrecognizeanacquiredassetandmeasureitatfairvaluein

accordancewithStatement157,evenifitdecidesnottousethatacquiredasset.Thisvaluationwould

needtoreflecttheasset’shighestandbestusefromamarketparticipant’spointofview(i.e.,someone

elsemaybewillingtopayforthisasset).Underthepreviousguidance,theacquirertypicallyassignedlittleornovaluetotheseacquiredassets.

Partial Acquisitions —Incertainbusinesscombinations,theacquirerobtainscontrol,butdoesnot

acquirea100percentinterestintheacquiree.UnderStatement141(R),onceanacquirerobtains

control,itwillmeasure100percentoftheacquirednetassetsatfairvalue(itmustmeasurefairvaluein

accordancewithStatement157)regardlessofitsownershipinterest.Underpreviousguidance,onlythe

portionofnetassetspurchasedbytheacquirerwasmeasuredatfairvalue;theremainderwasmeasured

athistoricalbookvalue.

UnderStatement141(R),anacquisitionofacontrollinginterestinanotherentitythatislessthan100

percentownedmayresultintherecognitionofhigher(1)netassetbalances,(2)depreciationandamortizationexpensesinpostcombinationperiods,and(3)assetimpairmentcharges,ascomparedwith

previousguidance.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 18/2865

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Noncontrolling Interests—Statement141(R)requiresthatthenoncontrollinginterestinabusiness

combination,ifany,bemeasuredinitiallyatfairvalue,includingitsshareofgoodwill.Inaddition,

Statement160requiresthattheparent(acquirer)presentthenoncontrollinginterestasaseparate

componentofshareholders’equity.4Underpreviousguidance,thenoncontrollinginterestwasrecorded

athistoricalbookvalue,goodwillwasonlyrecordedfortheacquirer’sinterest,andthenoncontrolling

interestwaspresentedaseithermezzanine(ortemporary)equityoraliability.

Statement141(R)’s“fullgoodwill”method(i.e.,goodwillrepresentsamountsattributabletoboththe

parentandthenoncontrollinginterest)willresultinhigherinitialamountsofgoodwillthandidthe

previousguidance.Thismayleadtolargergoodwillimpairmentchargesinpostcombinationearnings.

Furthermore,theclassificationofthenoncontrollinginterestinpermanentequitymayaffectsomekey

financialstatementratiosusedbymanagementorinvestorsandincludedindebtcovenants(e.g.,debt-

to-equityratio).

Restructuring and Exit Costs—Restructuringandexitcostsarecoststhatanacquirerexpectsto

incurforexitinganactivity,involuntarilyterminatingemployees,orrelocatingemployeesofanacquiree.

UnderStatement141(R),anacquirerwillgenerallyrecordthesecostsoutsideofacquisitionmethodaccountingthroughachargetopostcombinationearnings.Thepreviousguidancewaslessstringent

and,aslongascertaincriteriaweremet,generallyresultedinanacquirer’srecordingliabilitiesrelatedto

afuturerestructuringaspartofitspurchaseaccounting(i.e.,generallyasacomponentofgoodwill).

Acquired IPR&D—Beforeabusinesscombination,anacquireemayhaveincurredcostsassociated

withresearchanddevelopmentactivities.Thesecostsmostlikelywouldhavebeenexpensed,with

noresultingassetrecordedontheacquiree’sbooks.Inabusinesscombination,theresearchand

developmentactivitiesmostlikelyrepresentanassettotheacquirer.Statement141(R),likeprevious

guidance,requiresthatthefairvalueofsuchanassetbemeasuredasoftheacquisitiondate.However,

Statement141(R)differsfrompreviousguidanceregardingtheaccountingfortheasset.Underthe

previousguidance,theacquirerimmediatelyexpensedtheentirefairvalueoftheIPR&D(assumingit

hadnoalternativefutureuse)inthepostcombinationincomestatement.Conversely,underStatement

141(R),theacquiredIPR&Discapitalizedasanindefinite-livedintangibleassetandtestedforimpairment

atleastannually.Oncetheresearchanddevelopmentactivitiesarecomplete,theintangibleassetis

amortizedintoearningsovertherelatedproduct’susefullife.Iftheprojectissubsequentlyabandoned,

thecarryingamountwouldgenerallybeexpensedatthattime.Therefore,underStatement141(R),the

timingofwhentheacquiredIPR&Dwillaffectpostcombinationearningsislesscertain.

Adjustments to Certain Acquired Tax Balances—Statement141(R)requiresthatanentity

record,generallythroughincometaxexpense,adjustmentsmadeafterthemeasurementperiod(and

adjustmentsduringthemeasurementperiodthatrelatetofactsandcircumstancesthatdidnotexistas

oftheacquisitiondate)to(1)valuationallowancesforacquireddeferredtaxassetsand(2)acquiredtax

uncertainties.UponadoptingStatement141(R),anentitymustalsoapplythisnewguidancetotax

balancesrecordedbeforetheStatement’seffectivedate.Therefore,thisnewguidancemayaffect

remainingvaluationallowancesfordeferredtaxassetsandtaxuncertaintybalancesfrompriordeals

and,consequently,mayaffectfutureearnings.Thisnewguidancediffersfrompreviousguidancein

whichadjustmentstothesetaxbalancesweregenerallyrecordedasanadjustmenttogoodwill(i.e.,

earningsweregenerallynotdirectlyaffected).

4 Indeterminingtheappropriateclassificationofanoncontrollinginterest,anentitymustlooktootherrelevantGAAPtodeterminewhetherthefinancialinstrumentissuedbya

subsidiarycanbeclassifiedaspermanentequity(e.g.,Statements133and150,EITFTopicD-98,andSECAccountingSeriesReleaseNo.268).Morecomplexfinancialinstruments

(e.g.,thosewithcertaincallorputfeatures)maybeoutsidethescopeofStatement160and,therefore,classifiedineithermezzanine(ortemporary)equityorasliabilities.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 19/2866

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Acquisition-Related Costs—Statement141(R)requiresthattheacquirerexpenseallacquisition-

relatedcostsasincurred,eventhoseincurredbytheacquireeonbehalfoftheacquirer.However,

certaindirectcostspaidtoregisterdebtorequitysecuritiesaspartofabusinesscombinationmaystill

berecordedonthebalancesheetinaccordancewithotherapplicableU.S.GAAP.Acquisition-related

coststhatwillbeexpensedincludefeespaidtoinvestmentbankers,lawyers,accountants,valuation

specialists,andotherconsultants.Underthepreviousguidance,incrementalanddirectcostsofanacquisitionwerecapitalizedandgenerallyrecordedaspartofgoodwill.

Measurement-Period Adjustments—Likethepreviousguidance,thenewguidancegivesanacquirer

uptooneyear(formerlyreferredtoasthe“allocationperiod”)tofinalizeitsbusinesscombination

accounting,aslongasanyadjustmentsmadetoprovisionalamountsrelatetofactsandcircumstances

thatexistedasoftheacquisitiondate(e.g.,theacquirermaybewaitingonathird-partyvaluation

specialist’sreportthatdetailsthefairvalueofcertainassetsandliabilities).However,Statement141(R)

nowrequiresthattheacquirerrevisecomparativeprior-periodinformationforanyadjustmentsmade

toprovisionalamountsduringthemeasurementperiod(i.e.,adjustmentsaremaderetrospectively

asoftheacquisitiondate).Thisrepresentsasignificantchangefromprevailingpriorpractice,in

whichadjustmentstoprovisionalamountsweregenerallyaccountedforprospectivelyasachangeinaccountingestimate.

Therevisedguidancewillrequirethatanentityapplyadditionaleffortinrecordingmeasurement-

periodadjustments.Forexample,anentitythatsubsequentlyadjustsadepreciableasset’sprovisional

balancemustalsoretrospectivelyadjusttheasset’sdepreciationoramortizationexpense,accumulated

depreciationoramortization,andretainedearningsforallpriorperiodspresented.Additional

communicationanddisclosurestofinancialstatementusersmayalsoberequired.Publicentities

mayneedtoupdatefinancialstatementsandinformationincludedinaregistrationstatementifa

measurement-periodadjustment(1)isrecordedaftertheissuanceofthoseitemsand(2)wouldhavea

materialeffectontheamountsrecordedinthosefilings.

Bargain Purchases—Bargainpurchasesoccurwhenthefairvalueoftheconsiderationtransferred

islessthanthefairvalueofthenetassetsacquiredfromtheacquiree(thatdifferenceisreferredtoas

the“excess”).Statement141(R)requirestheacquirertorecordtheentireexcessinearnings.Under

thepreviousguidance,theacquirerwouldfirstreducethevalueassignedtocertainnoncurrentassets

acquired.Theacquirerwouldthenrecordanyremainingexcess,afterreducingthosenoncurrentassets

tozero,asanextraordinary gain.Therevisedguidancemayresultintherecognitionofalargergainby

theacquirer.Note,however,thatbargainpurchasesarenotexpectedtobecommon.

Definition of a Business—Statement141(R)significantlybroadensthedefinitionofabusiness(e.g.,

development-stageentitiesmayqualifyasabusinessunderStatement141(R),whereastheydidnot

underthepreviousguidance).Theexpandeddefinitionnotonlyaffectsthedeterminationofwhether

atransactionqualifiesasabusinesscombinationoranassetacquisition,butmayalsohaveaneffect

on(1)thegoodwillimpairmentanalysis(seebelow),(2)theconsolidationanalysisunderInterpretation

46(R),and(3)theallocationofgoodwillwhenaportionofreportingunitissoldorotherwisedisposed

of.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 20/2867

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Changes in the Parent’s Ownership Interest—UnderStatement160,afteraparent(acquirer)

obtainscontroloverasubsidiary,theparentmustaccountforadditionalpurchasesandsalesof

asubsidiary’sstockasequitytransactions(aslongascontrolisretained).Thus,theparentcannot

recognizeagainorlossinearningsondispositions,norcanitapplyadditionalacquisitionmethod

accountingforincrementalinterestsacquired.Underthepreviousguidance,salesofthesubsidiary’s

stocktothirdpartiesmayhaveresultedingainsorlossesinearningsandapurchaseofthesubsidiary’ssharesbytheparentmayhaverequiredadditionalpurchaseaccounting(whichcouldhavealsoresulted

inadditionalgoodwill).

Goodwill Impairment Testing —Statement142requiresentitiestotestgoodwillforimpairment

atleastannually.Step2ofthegoodwillimpairmenttestrequiresthattheentitycomputethecurrent

impliedfairvalueofgoodwill.Theentitythencomparesthatbalancetothecurrentcarryingamount

ofthegoodwilltodeterminewhetheranimpairmentisrequired.Theimpliedfairvalueofgoodwill

isdeterminedinthesamemannerasgoodwillrecognizedinabusinesscombination.Inotherwords,

beforetheadoptionofStatement141(R),anentitywouldrefertoStatement141forthisanalysis.After

theentityadoptsStatements141(R)and160,itmustperformstep2ofthegoodwillimpairmenttestin

accordancewithStatement141(R).Therefore,Statement141(R)willmostlikelyaffectthemechanicsinwhichstep2ofthegoodwillimpairmentanalysisisperformed.

Inaddition,goodwillimpairmenttestingisperformedatthereporting-unitlevel.Akeyfactorin

determininganentity’sreporting-unitstructureistoidentifywhichcomponentsarebusinesses,as

definedintheaccountingliterature.Aspreviouslynoted,Statement141(R)significantlybroadensthe

definitionofabusiness.Therefore,uponadoptionofStatement141(R),anentityshouldcarefullyreview

whetherthenewguidancewillaffectitsreporting-unitstructureandthusitsgoodwillimpairment

testing.

How This Roadmap Is Structured

Thispublicationconstitutesasinglesourceforboththeaccountingrequirementsfor,andtheavailable

interpretiveguidanceon,thefollowingtopics:

Initial Acquisition Accounting

• Businesscombinations.

Post-Acquisition Accounting

• Goodwillandotherintangibleassets.

• Push-downaccounting.

• Noncontrollinginterests.

Whereappropriate,wehaveincludedourownviews,whicharebasedonourexperiencewithand

understandingoftheunderlyingprinciples.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 21/2868

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

TheRoadmapisstructuredasfollows:

Accounting for Business Combinations

Section1—ScopeofStatement141(R)

Section2—IdentifyingtheAcquirer

Section3—RecognizingandMeasuringAssetsAcquiredandLiabilitiesAssumed—General

Section4—RecognizingandMeasuringAssetsAcquiredandLiabilitiesAssumed(OtherThanIntangibleAssetsandGoodwill)

Section5—RecognizingandMeasuringAcquiredIntangibleAssetsandGoodwill

Section6—RecognizingandMeasuringtheConsiderationTransferredinaBusinessCombination

Accounting for Noncontrolling Interests During andAfter a Business Combination

Section7—NoncontrollingInterests

Income Tax Considerations for Business Combinations Section8—IncomeTaxConsiderations

Accounting After a Business Combination

Section9—Push-DownBasisofAccounting

Section10—SubsequentAccountingforIntangibleAssets(OtherThanGoodwill)

Section11—SubsequentAccountingforGoodwill

Presentation and Disclosure Considerations

Section12—FinancialStatementPresentationRequirements

Section13—FinancialStatementDisclosureRequirements

Transition Issues and ConsiderationsSection14—TransitionRequirementsandOtherAdoption

Considerations

Comparisons to IFRSs and Previous U.S. GAAP

AppendixA—DifferencesBetweenStatements141and141(R)

AppendixB—DifferencesBetweenPre-AmendedARB51andStatement160

AppendixC—DifferencesBetweenU.S.GAAPandIFRSs

Index of Standards and Regulations ReferencedThroughout the Roadmap

AppendixD—GlossaryofStandardsandRegulations

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 22/2869

Section 1 — Scope of Statement 141(R)

Occurrence of a Business Combination

1.01 Paragraph3(e)ofStatement141(R)definesa“businesscombination”asfollows:

Abusinesscombination isatransactionorothereventinwhichanacquirerobtainscontrol[see

1.02–1.07]ofoneormorebusinesses[see 1.08–1.11].Transactionssometimesreferredtoas“true

mergers”or“mergerofequals”alsoarebusinesscombinationsasthattermisusedinthisStatement.

[Emphasisadded]

Obtaining Control

1.02 ParagraphA2ofStatement141(R)providesthefollowingexamplesoftransactionsoreventsthat

mayresultinanentity’sobtainingcontrolofanotherbusiness:

• Transfersofcash,cashequivalents,orotherassets(includingnetassetsthatconstituteabusiness).

• Incurrenceofliabilities.

• Issuanceofequityinterests.

• Issuanceofmorethanonetypeofconsideration.

• Othertransactionsoreventsthatdonotinvolvethetransferofconsideration,includingby

contractalone(see1.05–1.07).

1.03 Inspecifyinghowentitiesdeterminewhethertheyhaveobtainedcontrolofanotherbusiness,

Statement141(R)referstothedescriptionof“controllingfinancialinterest”inparagraph2ofARB51,

asamendedbyStatement160,whichstates:

Theusualconditionforacontrolling financial interestisownershipofamajorityvotinginterest,

and,therefore,asageneralruleownershipbyonecompany,directlyorindirectly,ofoverfiftypercent

oftheoutstandingvotingsharesofanothercompanyisaconditionpointingtowardconsolidation.

[Emphasisadded]

1.04 Acontrolassessmentisnotnecessarilybasedsolelyonavotinginterestmodelsuchasthat

describedinARB51.Entitiesmustalsodeterminewhethertheyhaveacontrollingfinancialinterestina

variableinterestentity(VIE)inaccordancewithInterpretation46(R).ControlunderInterpretation46(R)is

assessedonthebasisofeconomicrisksandrewardstotheinvestorandisnotdependentonthevoting

interest.See1.17–1.21foradiscussionoftheinteractionbetweenVIEsandStatement141(R).

1.05 Anacquirermayobtaincontrolofanacquireewithouttransferringconsiderationtotheformer

owners.Paragraph49ofStatement141(R)listscertaincircumstancesinwhichthismayoccur:

a. Theacquireerepurchasesasufficientnumberofitsownsharesforanexistinginvestor(the

acquirer)toobtaincontrol.

b. Minorityvetorightslapsethatpreviouslykepttheacquirerfromcontrollinganacquireein

whichtheacquirerheldthemajorityvotinginterest.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 23/28610

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

c. Theacquirerandacquireeagreetocombinetheirbusinessesbycontractalone.Theacquirer

transfersnoconsiderationinexchangeforcontrolofanacquireeandholdsnoequity

interestsintheacquiree,eitherontheacquisitiondateorpreviously.Examplesofbusiness

combinationsachievedbycontractaloneincludebringingtwobusinessestogetherina

staplingarrangementorformingaduallistedcorporation.[See1.06.]

1.06 Staplingarrangementsandtheformationofdual-listedcorporationsdonotoccurfrequentlyinpracticeandmostofteninvolveforeignentities.Characteristicsofsucharrangementsareasfollows:

• Staplingarrangements—Thesearegenerallycontractualagreementsbetweentwopartiesin

whichtheissuedequitysecuritiesofonelegalentityarecombinedwiththeissuedsecuritiesof

anotherlegalentity.Thesesecurities,oftenreferredtoas“stapled,”arethenquotedatasingle

marketpriceandcannotbeseparatelytradedortransferred.

• Dual-listedcorporation—Insuchtransactions,noconsiderationisexchangedbyeitherentity,

andcontractsareexecutedbetweenthepartiesthatequalizetherightsoftherespective

shareholders.Suchrightsoftenincludevoting,dividends,governance,andexecutive

managementdecisions.Althoughseparatelegalentitiesareretained(i.e.,thesecuritiesofeach

respectiveentityareusuallyseparatelyquotedandtradedinthecapitalmarkets),adual-listedcorporationissubstantivelysimilartoabusinesscombinationinthattheshareholdersofthe

respectiveentitiesbothshareintherisksandrewardsofthetwoentities.Historically,theSEC

hasrequiredsuchtransactionstobeaccountedforasabusinesscombination,andStatement

141(R)isnotexpectedtosignificantlychangethispractice.

1.07 Businesscombinationsachievedwithoutthetransferofconsiderationareaccountedforunder

theacquisitionmethodofaccounting.Paragraph50ofStatement141(R)statesthatforthoseachieved

bycontractalone,“theacquirershallattributetotheequityholdersoftheacquireetheamountofthe

acquiree’snetassetsrecognized.”Inotherwords,thenoncontrollinginterestshouldberecognizedin

theacquirer’spostcombinationfinancialstatementseveniftheresultisthatitrepresents100percentof

theacquiree’snetassets.

Definition of a Business

1.08 Anentitymayobtaincontrolofabusinessbyacquiringitsnetassetsoritsequityinterests.For

abusinesscombinationtobewithinthescopeofStatement141(R),theentityoverwhichcontrolis

obtainedmustbeabusiness.Paragraph3(d)ofStatement141(R)definesabusinessasfollows:

Abusiness isanintegratedsetofactivitiesandassetsthatiscapableofbeingconductedand

managedforthepurposeofprovidingareturnintheformofdividends,lowercosts,orother

economicbenefitsdirectlytoinvestorsorotherowners,members,orparticipants.

1.09 Statement141(R)nullifiesthedefinitionofabusinessthatwasinIssue98-3andsignificantly

broadenswhatisconsideredabusiness(seeA.05).

1.10 ParagraphsA4–A9ofStatement141(R)provideimplementationguidancetohelpentitiesidentify

whatconstitutesabusiness:

A4.ThisStatementdefinesabusinessasanintegratedsetofactivitiesandassetsthatiscapableof

beingconductedandmanagedforthepurposeofprovidingareturnintheformofdividends,lower

costs,orothereconomicbenefitsdirectlytoinvestorsorotherowners,members,orparticipants.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 24/28611

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Abusinessconsistsofinputsandprocessesappliedtothoseinputsthathavetheabilitytocreate

outputs.Althoughbusinessesusuallyhaveoutputs,outputsarenotrequiredforanintegratedsetto

qualifyasabusiness.Thethreeelementsofabusinessaredefinedasfollows:

a. Input :Anyeconomicresourcethatcreates,orhastheabilitytocreate,outputswhenone

ormoreprocessesareappliedtoit.Examplesincludelong-livedassets(includingintangible

assetsorrightstouselong-livedassets),intellectualproperty,theabilitytoobtainaccessto

necessarymaterialsorrights,andemployees.

b. Process :Anysystem,standard,protocol,convention,orrulethatwhenappliedtoaninputor

inputs,createsorhastheabilitytocreateoutputs.Examplesincludestrategicmanagement

processes,operationalprocesses,andresourcemanagementprocesses.Theseprocesses

typicallyaredocumented,butanorganizedworkforcehavingthenecessaryskillsand

experiencefollowingrulesandconventionsmayprovidethenecessaryprocessesthatare

capableofbeingappliedtoinputstocreateoutputs.(Accounting,billing,payroll,andother

administrativesystemstypicallyarenotprocessesusedtocreateoutputs.)

c. Output :Theresultofinputsandprocessesappliedtothoseinputsthatprovideorhavethe

abilitytoprovideareturnintheformofdividends,lowercosts,orothereconomicbenefits

directlytoinvestorsorotherowners,members,orparticipants.

A5.Tobecapableofbeingconductedandmanagedforthepurposesdefined,anintegratedsetof

activitiesandassetsrequirestwoessentialelements—inputsandprocessesappliedtothoseinputs,

whichtogetherareorwillbeusedtocreateoutputs.However,abusinessneednotincludeallofthe

inputsorprocessesthatthesellerusedinoperatingthatbusinessifmarketparticipantsarecapableof

acquiringthebusinessandcontinuingtoproduceoutputs,forexample,byintegratingthebusiness

withtheirowninputsandprocesses.FASBStatementNo.157,FairValueMeasurements ,describes

marketparticipantsas:

...buyersandsellersintheprincipal(ormostadvantageous)marketfortheassetorliability

thatare:

a. Independentofthereportingentity;thatis,theyarenotrelatedparties

b. Knowledgeable,havingareasonableunderstandingabouttheassetorliabilityand

thetransactionbasedonallavailableinformation,includinginformationthatmightbe

obtainedthroughduediligenceeffortsthatareusualandcustomary

c. Abletotransactfortheassetorliability

d. Willingtotransactfortheassetorliability;thatis,theyaremotivatedbutnotforcedor

otherwisecompelledtodoso.[Paragraph10;footnotereferenceomitted.]

A6.Thenatureoftheelementsofabusinessvariesbyindustryandbythestructureofanentity’s

operations(activities),includingtheentity’sstageofdevelopment.Establishedbusinessesoftenhave

manydifferenttypesofinputs,processes,andoutputs,whereasnewbusinessesoftenhavefew

inputsandprocessesandsometimesonlyasingleoutput(product).Nearlyallbusinessesalsohave

liabilities,butabusinessneednothaveliabilities.

A7.Anintegratedsetofactivitiesandassetsinthedevelopmentstagemightnothaveoutputs.Ifnot,

theacquirershouldconsiderotherfactorstodeterminewhetherthesetisabusiness.Thosefactors

include,butarenotlimitedto,whethertheset:

a. Hasbegunplannedprincipalactivities

b. Hasemployees,intellectualproperty,andotherinputsandprocessesthatcouldbeappliedto

thoseinputs

c. Ispursuingaplantoproduceoutputs

d. Willbeabletoobtainaccesstocustomersthatwillpurchasetheoutputs.

Notallofthosefactorsneedtobepresentforaparticularintegratedsetofactivitiesandassetsinthe

developmentstagetoqualifyasabusiness.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 25/28612

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

A8.Determiningwhetheraparticularsetofassetsandactivitiesisabusinessshouldbebasedon

whethertheintegratedsetiscapableofbeingconductedandmanagedasabusinessbyamarket

participant.Thus,inevaluatingwhetheraparticularsetisabusiness,itisnotrelevantwhetheraseller

operatedthesetasabusinessorwhethertheacquirerintendstooperatethesetasabusiness.

A9.Intheabsenceofevidencetothecontrary,aparticularsetofassetsandactivitiesinwhich

goodwillispresentshallbepresumedtobeabusiness.However,abusinessneednothavegoodwill.

1.11 WhileStatement141(R)providesusefulfactorstoconsider,itdoesnotprescribeadefinitive

checklistforentitiestofollowwhenassessingwhetheragroupofassetsconstitutesabusiness.

Therefore,professionaljudgmentshouldbeused.

Acquiring Net Assets or Equity Interests That Do Not Meet the Definition of aBusiness

1.12 Theaccountingrequirementsforanacquisitionofnetassetsorequityintereststhatisnot

deemedtobeabusinesscombination(see1.01)willdifferincertainrespectsfromthoseusedfor

businesscombinations.Thefollowingtableshighlightsuchdifferences.

Cost of the Acquisition

Business CombinationAcquisition of an Asset Group

Determined Not to Be a Business

Paragraph39ofStatement141(R)states:

Theconsiderationtransferredinabusinesscombinationshallbemeasuredatfairvalue,whichshallbecalculatedasthesumoftheacquisition-datefairvaluesoftheassetstransferredbytheacquirer,theliabilitiesincurredbytheacquirertoformerownersoftheacquiree,andtheequityinterestsissuedbytheacquirer.

(However,anyportionoftheacquirer’sshare-basedpaymentawardsexchangedforawardsheldbytheacquiree’semployeesthatisincludedinconsiderationtransferredinthebusinesscombinationshallbemeasuredinaccordancewithparagraph32ratherthanatfairvalue.)Examplesofpotentialformsofconsiderationincludecash,otherassets,abusinessorasubsidiaryoftheacquirer,contingentconsideration(paragraphs41and42),commonorpreferredequityinstruments,options,warrants,andmemberinterestsofmutualentities.

Thefairvalueoftheconsiderationtransferred excludesthe transaction coststheacquirerincurstoeffectabusinesscombination(acquisition-relatedcosts).

ParagraphD4ofStatement141(R)states,inpart:

Assetsarerecognizedbasedontheircosttotheacquiringentity,whichgenerallyincludes thetransaction costs of the asset acquisition,andnogainorlossisrecognizedunlessthefairvalueofnoncashassetsgivenasconsiderationdiffersfromtheassets’carryingamountsontheacquiringentity’sbooks.[Emphasisadded]

Theaccountingforcontingentconsiderationdoesnotfollowtheguidanceinparagraphs41and42ofStatement141(R).ContingentconsiderationismeasuredinaccordancewithotherapplicableGAAP,includingStatement5andStatement133,asappropriate.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 26/28613

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Measuring the Assets Acquired and Liabilities Assumed

Business Combination

Acquisition of an Asset Group

Determined Not to Be a Business

Paragraph20ofStatement141(R)providesthatthe“acquirershallmeasuretheidentifiableassetsacquired,theliabilitiesassumed,andanynoncontrollinginterestintheacquireeattheiracquisition-datefairvalues.”

Paragraph34ofStatement141(R)indicatesthatgoodwillshouldberecordedasthesumofthe(1)considerationtransferred,(2)fairvalueofanynoncontrollinginterest,and(3)fairvalueoftheacquirer’spreviouslyheldinterestintheacquiree,ifany,lesstheacquisition-datefairvalueofthenetassetsacquired.

InaccordancewithStatement141(R),contractualcontingenciesarerecognizedatfairvalueasoftheacquisitiondate,whereasnoncontractualcontingenciesarerecognizedatfairvalueonlyif,asoftheacquisitiondate,itismorelikelythannotthatthecontingencymeetsthedefinitionofanassetorliabilityinaccordancewithConceptsStatement6.*

*OnDecember15,2008,theFASBissuedproposedFSPFAS141(R)-a,whichwouldamendStatement141(R)torequirethatpreacquisitioncontingenciesgenerallybemeasuredatfairvalueasoftheacquisitiondateifsuchamountscanbereasonablydetermined.ItisexpectedthattheguidanceintheproposedFSPwouldresultintherecognitionofmorecontingentassetsandliabilitiesatfairvaluethantheguidanceinStatement141,butfewerthanthecurrentStatement141(R)guidance.ThisRoadmapwillbeupdatedforthefinalguidanceonceitisissuedbytheFASB.

ParagraphD6ofStatement141(R)states,inpart:

Acquiringassetsingroupsrequiresnotonly

ascertainingthecostoftheasset(ornetasset)groupbutalsoallocatingthatcosttotheindividualassets(orindividualassetsandliabilities)thatmakeupthegroup.ThecostofsuchagroupisdeterminedusingtheconceptsdescribedinparagraphsD4andD5.Thecostofagroupofassetsacquiredinanassetacquisitionisallocatedtotheindividualassetsacquiredorliabilitiesassumedbasedontheirrelativefairvaluesanddoesnotgiverisetogoodwill.

AcquiredcontingentassetsandassumedcontingentliabilitiesareaccountedforinaccordancewithStatement5,generallyresultingin(1)norecognitionofacquiredcontingentassetsand(2)recognitionofacontingentliabilityonlyifitisprobablethataliabilityhasbeenincurredandtheamountcanbereasonablyestimated.

1.13 Whenanentityallocatesthecostofanassetgroupnotdeterminedtobeabusiness,itcannot

recognizethedifferencebetweenthetotalcostandtheamountsassignedtotheassets(andliabilities)

asgoodwill.If,uponreviewoftheinitialmeasurementsofthetangibleandintangibleassetsacquired,

theentitydoesnoteliminatethatdifference,itmustallocateit.Ifthedifferenceisanexcessofcost,the

differenceshouldbeallocatedprorataonthebasisofrelativefairvaluestoincreasetheassetsacquired,

exceptforfinancialassets(otherthaninvestmentsaccountedforbytheequitymethod)andassets

subjecttofairvalueimpairmenttesting,suchasinventoriesandindefinite-livedintangibleassets,since

increasingthevalueofsuchassetswouldmostlikelyresultinanimpairmentasofthenexttestingdate.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 27/286

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 28/28615

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

requiredinadditiontothesefinancialstatements.

1.15 Severalfactorsgovernwhetherfinancialstatementsfortheacquireearerequired,including

whethertheacquiredortobeacquiredassetsandliabilitiesmeettheSEC’sdefinitionofabusiness.SEC

RegulationS-X,Rule11-01(d),states:

Forpurposesofthisrule,thetermbusinessshouldbeevaluatedinlightofthefactsandcircumstances

involvedandwhetherthereissufficientcontinuityoftheacquiredentity’soperationspriortoand

afterthetransactionssothatdisclosureofpriorfinancialinformationismaterialtoanunderstanding

offutureoperations.Apresumptionexiststhataseparateentity,asubsidiary,oradivisionisa

business.However,alessercomponentofanentitymayalsoconstituteabusiness.Amongthe

factsandcircumstanceswhichshouldbeconsideredinevaluatingwhetheranacquisitionofalesser

componentofanentityconstitutesabusinessarethefollowing:

(1) Whetherthenatureoftherevenue-producingactivityofthecomponentwillremaingenerally

thesameasbeforethetransaction;or

(2) Whetheranyofthefollowingattributesremainwiththecomponentafterthetransaction:

(i) Physicalfacilities,

(ii) Employeebase,

(iii) Marketdistributionsystem,

(iv) Salesforce,

(v) Customerbase,

(vi) Operatingrights,

(vii)Productiontechniques,or

(viii)Tradenames.

1.16 BecausethedefinitionofabusinessinSECRegulationS-X,Rule11-01(d),differsfromthat

inStatement141(R),SECregistrantsmustundertakeaseparateanalysisunderRule11-01(d)when

evaluatingthereportingrequirementsofSECRegulationS-X.However,webelievethatthechangesto

thedefinitionofabusinessinStatement141(R)morecloselyaligntheFASB’sdefinitionwiththeSEC’s

thandidthepreviousguidance.

Variable Interest Entities

1.17 Statement141(R)amendstheinitialconsolidationguidanceforVIEsthatareaccountedforunder

Interpretation46(R).Inaddition,Statement141(R)amendsInterpretation46(R)tomakethedefinition

ofabusinessconsistentwiththatinStatement141(R)(see1.08).

1.18 Theprimarybeneficiaryisalwaystheacquirerwhentheacquisitionmethodofaccountingisused

(see2.02).RegardingdeterminationoftheVIE’sprimarybeneficiary,paragraph9ofStatement141(R)

states,inpart:

Thedeterminationofwhichparty,ifany,istheprimarybeneficiaryofavariableinterestentityshall

bemadeinaccordancewithFASBInterpretationNo.46(revisedDecember2003),Consolidation

ofVariableInterestEntities ,asamended,notbyapplyingeithertheguidanceinARB51orthatin

paragraphsA11–A15[ofStatement141(R)].

1.19 IfaVIEmeetsthedefinitionofabusiness(see1.08),theprimarybeneficiary’sinitialconsolidation

oftheVIEmustbeaccountedforasabusinesscombinationunderStatement141(R).

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 29/28616

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

1.20 IfaVIEdoesnotmeetthedefinitionofabusiness,theprimarybeneficiary’sinitialmeasurement

oftheVIE’sassets(exceptgoodwill)andliabilitieswouldfollowthemeasurementguidanceofStatement

141(R).However,theprimarybeneficiaryisprohibitedfromrecognizinggoodwill,andwouldinstead

recognizealoss.Inaddition,paragraphs21(a)and21(b)ofInterpretation46(R),asamendedby

Statement141(R),state:

a. Theprimarybeneficiaryinitiallyshallmeasureandrecognizetheassets(exceptforgoodwill)

andliabilitiesofthevariableinterestentityinaccordancewithparagraphs12–33ofStatement

141(R).However,theprimarybeneficiaryshallinitiallymeasureassetsandliabilitiesthatithas

transferredtothatvariableinterestentityat,after,orshortlybeforethedatethattheentity

becametheprimarybeneficiaryatthesameamountsatwhichtheassetsandliabilitieswould

havebeenmeasurediftheyhadnotbeentransferred.Nogainorlossshallberecognized

becauseofsuchtransfers.

b. Theprimarybeneficiaryshallrecognizeagainorlossforthedifferencebetween(1)the

fairvalueofanyconsiderationpaid,thefairvalueofanynoncontrollinginterests,andthe

reportedamountofanypreviouslyheldinterestsand(2)thenetamountofthevariable

interestentity’sidentifiableassetsandliabilitiesrecognizedandmeasuredinaccordance

withStatement141(R).Nogoodwillshallberecognizedifthevariableinterestentityisnota

business.

1.21 ParagraphB21ofStatement141(R)explainstheFASB’srationalefortheamendmentsto

Interpretation46(R):

TheFASBconcludedthatvariableinterestentitiesthatarebusinessesshouldbeaffordedthesame

exceptionstofairvaluemeasurementandrecognitionthatareprovidedforassetsandliabilitiesof

acquiredbusinesses.TheFASBalsodecidedthatupontheinitialconsolidationofavariableinterest

entitythatisnotabusiness,theassets(otherthangoodwill),liabilities,andnoncontrollinginterests

shouldberecognizedandmeasuredinaccordancewiththerequirementsof[Statement141(R)],

ratherthanatfairvalueaspreviouslyrequiredbyInterpretation46(R).TheFASBreachedthatdecision

forthesamereasonsdescribedabove,thatis,ifthisStatementallowsanexceptiontofairvalue

measurementforaparticularassetorliability,itwouldbeinconsistenttorequirethesametypeofassetorliabilitytobemeasuredatfairvalue.Exceptforthatprovision,theFASBdidnotreconsider

therequirementsinInterpretation46(R)fortheinitialconsolidationofavariableinterestentitythatis

notabusiness.

Combinations Between Two or More Mutual Entities

1.22 BusinesscombinationsbetweentwoormoremutualentitiesarewithinthescopeofStatement

141(R).Paragraph3(m)ofStatement141(R)definesa“mutualentity”asfollows:

Amutualentity isanentityotherthananinvestor-ownedentitythatprovidesdividends,lowercosts,

orothereconomicbenefitsdirectlytoitsowners,members,orparticipants.Forexample,amutual

insurancecompany,acreditunion,andacooperativeentityareallmutualentities.

1.23 Sinceacombinationofmutualentitiesinvolvesanexchange,albeittypicallyofmembership

interests,Statement141(R)makesnoconcessiontoitsusualrequirementsregardingapplyingthe

acquisitionmethodofaccounting.Consequently,anacquirermustbeidentifiedinanycombinationof

mutualentitiesusingtheStatement141(R)criteria(seeSection 2).

1.24 MutualentitiesdidnotfollowtheguidanceinStatement141becauseitseffectivedatewas

deferreduntilinterpretiveguidancewasissuedfortransactionsinvolvingsuchentities.Seeadditional

Statement141(R)transitionguidanceformutualentitiesin14.39–14.45.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 30/28617

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Leveraged Buyout Transactions

1.25 Statement141(R)nullifiesIssue88-16,whichpreviouslyprovidedguidancetoentitiesthat

participatedinleveragebuyout(LBO)transactions.Issue88-16describedLBOtransactionsasfollows:

[T]heLBOshouldbeeffectedinasinglehighlyleveragedtransactionoraseriesofrelatedand

anticipatedhighlyleveragedtransactionsthatresultintheacquisitionbyNEWCOofallpreviouslyoutstandingcommonstockofOLDCO;thatis,therecanbenoremainingminorityinterest.[footnote

2omitted]ThisIssueexcludesLBOtransactionsinwhichexistingmajoritystockholdersutilizea

holdingcompanytoacquireallofthesharesofOLDCOnotpreviouslyowned.Stepacquisition

accountingcontinuestobeappropriateinsuchtransactions.

UpontheiradoptionofStatement141(R),entitiesmustnowconsidertheprovisionsofStatement141(R)

fortransactionsthatwouldhavebeenpreviouslyaccountedforunderIssue88-16.NotethatStatement

141(R)doesnotprovideguidanceoramendtheaccountingforrecapitalizationtransactions,including

leveragedrecapitalizations(see1.37).

Additional Scope Considerations

1.26 Businesscombinationscanbeachievedinavarietyofways.Itmaynotalwaysbeclearwhether

aspecifictransactionformiswithinthescopeofStatement141(R),isotherwiseaddressedinStatement

141(R),orisaddressedinotherauthoritativeliterature.Transactionsdiscussedelsewhereinthis

Roadmapareasfollows:

• Controlobtainedbutlessthan100percentofthebusinessisacquired(see1.27).

• Businesscombinationsachievedinstages(see1.28–1.30).

• Acquisitionofanoncontrollinginterestofasubsidiary(see1.31).

• Roll-uporput-togethertransactions(see1.32–1.33).

• Formationofajointventure(see1.34–1.36).• Recapitalizations(see1.37).

• Transactionsbetweenentitiesundercommoncontrol(see1.38–1.44).

• Combinationsbetweenentitieswithcommonownership(see1.45–1.46).

• Combinationsinvolvingnot-for-profitorganizations(see1.47–1.49).

Control Obtained but Less Than 100 Percent of the Business Is Acquired (i.e., PartialAcquisitions)

1.27 Statement141(R)appliestotransactionsoreventsinwhichanentityobtainscontrolofone

ormorebusinesses(see1.01).Inatransactionoreventinvolvingequityinterests,controlisgenerallyindicatedbyownershipbyoneentity,directlyorindirectly,ofover50percentoftheoutstandingvoting

sharesofanotherentity(see1.02–1.07).Accordingly,abusinesscombinationmayoccurwhenan

entityacquiresenough,butlessthan100percentof,votingsharestoobtaincontrol.Insuchcases,the

acquirerrecognizesinitsconsolidatedfinancialstatementstheassetsacquired,liabilitiesassumed,and

thenoncontrollinginterestat100percentoftheiracquisition-datefairvalues(withcertainexceptions

specifiedinStatement141(R)),regardlessofitslevelofcontrollinginterest.TheFASBhasindicatedthat

onceanacquirerobtainscontrolofanentity,itcontrols100percentofitsassets,notjustaportionof

them.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 31/28618

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Example 1-2

Control Obtained but Less Than 100 Percent of the Business Is Acquired

CompanyA,withnopriorownershipinterestinCompanyB,acquired80percentoftheequityinterestinCompanyBinabusinesscombinationfor$1,600.Thefairvalueofthenoncontrollinginterestis$400(assumingnocontrolpremium).ThefairvalueofallidentifiablenetassetsofCompanyBasoftheacquisitiondatewas$1,500.

Initsconsolidatedfinancialstatements,CompanyAwillreflecttheacquisitionoftheequityinterestinCompanyBasfollows:

Identifiablenetassets

Goodwill

Noncontrollinginterest(aseparatecomponentofshareholders’equity)

CompanyA’sinvestmentinB

$ 1,500

500

(400)

$ 1,600

FullfairvalueofCompanyB’snetassets

Calculatedas([$1,600+$400]–$1,500)

Fairvalue

Business Combinations Achieved in Stages

1.28 Abusinesscombinationachievedinstagesoccurswhencontrolofabusinessisobtainedafter

theacquireralreadyownsanoncontrollinginterestintheacquiree’sequity.Suchacquisitionsarecommonlycalledstepacquisitions.UnderStatement141(R),theacquirerappliesStatement141(R)’s

acquisitionmethodaccountingonthedatecontrolisobtained.Inaddition,theacquirer’spreexisting

interestintheacquireeisremeasuredtoitsfairvalue,witharesultinggainorlossrecordedinearnings

uponconsummationofthebusinesscombination.Inpriorperiods,thepreviouslyheldinterestmayhave

beenremeasuredtofairvaluewithchangesrecognizedinothercomprehensiveincome(e.g.,ifitwas

classifiedasavailableforsale).Insuchcases,theamountofothercomprehensiveincomerelatedtothe

previouslyheldinterestshouldbereclassifiedandincludedinthegainorloss.

1.29 ParagraphB384ofStatement141(R)explainstheFASB’srationalefortheaccountingtreatment:

TheBoardsconcludedthatachangefromholdinganoncontrollinginvestmentinanentityto

obtainingcontrolofthatentityisasignificantchangeinthenatureofandeconomiccircumstances

surroundingthatinvestment.Thatchangewarrantsachangeintheclassificationandmeasurement

ofthatinvestment.Onceitobtainscontrol,theacquirernolongeristheownerofanoncontrolling

investmentassetintheacquiree.Asinpresentpractice,theacquirerceasesitsaccountingforan

investmentassetandbeginsreportinginitsfinancialstatementstheunderlyingassets,liabilities,

andresultsofoperationsoftheacquiree.Ineffect,theacquirerexchangesitsstatusasanownerof

aninvestmentassetinanentityforacontrollingfinancialinterestinalloftheunderlyingassetsand

liabilitiesofthatentity(acquiree)andtherighttodirecthowtheacquireeanditsmanagementuse

thoseassetsinitsoperations.

1.30 See7.20–7.23regardingadditionalacquisitionsofnoncontrollinginterestsinasubsidiaryafter

controlisobtained.

8/14/2019 Roadmap_Business Combinations - Deloitte

http://slidepdf.com/reader/full/roadmapbusiness-combinations-deloitte 32/28619

AccountingforBusinessCombinationsandRelatedTopics Deloitte

ARoadmaptoApplyingFASBStatements141(R),142,and160

Example 1-3

Business Combination Achieved in Stages

ACpurchasesa35percentinterestinTargetCompany(TC)for$2,000onJanuary1,20X8(exampleignoresdeferredtaxaccountingimplications).ACusestheequitymethodtoaccountforits35percentinterestinTC.OnDecember31,20X9:

• ACpurchasesanadditional40percentofTCfor$4,000.

• ThefairvalueofTC’sidentifiablenetassetsis$8,000.

• Thefairvalueofthe25percentnoncontrollinginterestis$1,800.

• ThefairvalueofAC’s35percentofTCis$3,500.Thebookvalueofthatinterestis$2,500.

• TCconstitutesabusiness.

Theacquisitionofthe40percentinterestresultsinAC’sobtainingcontrolofTC.Therefore,thattransactionisaccountedforasabusinesscombination.

AC’sexisting35percentinterestinTCisremeasuredto$3,500,resultinginagainof$1,000($3,500lessthe$2,500bookvalue)intheincomestatement.

ACrecognizesTC’sidentifiablenetassetsatthefullamountoftheirfairvalues($8,000).ACalsorecognizesgoodwillof$1,300([$4,000+$1,800+$3,500]–$8,000)(see5.38–5.41).

IfACpurchases(ordisposesof)additionalinterestsinTCinthefuture(providedthatcontrolisretained),thoseinterests