Embed Size (px)

Citation preview

2010

Gopi Suvanam Amit Trivedi

Fin Stream Advisors

8/18/2010

Risk Management for Indian Insurers

Risk Management for Indian Insurers

FinStream Page 1

Topic

Introduction

Page

2

Current Profile of Insurance Companies in India

2

Regulatory framework Investments Asset‐Liability and Solvency

234

Risk profile of Insurance Companies

4

Enterprise Risk Management (ERM) Insurance Risk Investments Risk Credit Risk Liquidity risk Asset‐Liability Management Risk

456899

ALM Pillars for ALM

910

Modeling and Managing Risk Step 1: Asset Liability Modeling Step 2: Market Modeling Step 3: Measuring Risk

10111415

Our Approach

16

Risk Management for Indian Insurers

FinStream Page 2

Introduction

Insurance sector in India is a colossal one and is growing at a speedy rate of 15‐20%. Today there are 14 general insurance companies including the ECGC and Agriculture Insurance Corporation of India and 14 life insurance companies operating in the country. Together with banking services, insurance services add about 7% to the country’s GDP. A well‐developed and evolved insurance sector is a boon for economic development as it provides long‐ term funds for infrastructure development at the same time strengthening the risk taking ability of the country. However, as the economic scenarios become increasingly complex and volatile, it is almost certain that there will be more deleveraged financial system and substantially different regulatory environments. In the midst of all this, what should insurers focus on in this changing environment? What changes to Asset/Liability Management (ALM) and Enterprise Risk Management (ERM) can help companies ride out of current crisis and come out even stronger. This paper focuses upon the changing dynamic of the insurance industry and suggestive risk management framework and practices.

Current Profile of Insurance companies in India

Currently, three major categories of insurers have their presence in India:‐

1. Life Insurance ‐ Insurance guaranteeing a specific sum of money to a designated beneficiary upon the death of the insured, or to the insured if he or she lives beyond a certain age.

2. Health Insurance ‐ Insurance against expenses incurred through illness of the insured.

3. Liability Insurance ‐ This insures property such as automobiles, property and professional/business mishaps.

All insurance companies carry similar exposure due to (1) Lump sum payments at the end of policy term and (2) Life annuities.

Regulatory Framework

There are four major regulatory authorities for Insurance sector in India, namely, Insurance Regulatory and Development Authority (IRDA), Tariff Advisory committee (which controls rates and terms and condition for general insurance industry), Insurance Association of India and Ombudsmen (to resolve claim‐settlement issues).

The most important rules specified and monitored by these authorities are those concerning ‘Asset, Liability and Solvency margin of Insurers’. More specifically, every insurer is required to invest and keep invested certain amount of assets as determined under the Insurance Act. The funds of the policyholders cannot be invested (directly or indirectly) outside India. Important regulations are specified below:-

Risk Management for Indian Insurers

FinStream Page 3

Investments

1) Life Insurance ‐ An insurer involved in the business of life insurance is required to invest and keep invested at all times assets, the value of which is not less than the sum of the amount of its liabilities to holders of life insurance policies in India on account of matured claims and the amount required to meet the liability on policies of life insurance maturing for payment in India, reduced by the amount of premiums which have fallen due to the insurer on such policies but have not been paid and the days of grace for payment of which have not expired and any amount due to the insurer for loans granted on and within the surrender values of policies of life insurance maturing for payment in India issued by him or by an insurer whose business he has acquired and in respect of which he has assumed liability. Every insurer carrying on the business of life insurance is required to invest and at all times keep invested his controlled fund (other than funds relating to pensions and general annuity business and unit linked life insurance business) in the following manner, free of any encumbrance, charge, hypothecation or lien:

2) General Insurance:‐

An insurer carrying on general insurance business is required to invest and keep invested at all times his total assets in approved securities in the following manner:

`

3) Pension and General Annuity:‐

Every insurer is required to invest and at all times keep invested in assets of pension buisness, general annuity business and group business in the followign manner:

Risk Management for Indian Insurers

FinStream Page 4

Valuation of Asset‐Liability and Solvency Margin

An insurer should maintain, at all times, an excess of the value of his assets over the amount of his liabilities of not less than the relevant amount arrived at in the following manner ("required solvency margin"):

(a) in the case of an insurer carrying on life insurance business, the required solvency margin shall be the higher of rupees five hundred million (one billion in case of re‐insurers) or the aggregate sum arrived at based on the calculations specified in the Insurance Act.

(b) in the case of an insurer carrying on general insurance business, the required solvency margin, shall be the highest of the following amounts: ‐

(i) rupees five hundred million (rupees one billion in case of a re‐insurer); or

(ii) a sum equivalent to twenty per cent of net premium income; or

(iii) a sum equivalent to thirty per cent of net incurred claims.

This shall be subject to credit for re‐insurance in computing net premiums and net incurred claims being actual but a percentage, determined by the regulations, not exceeding fifty per cent.

An insurer who fails to maintain the required solvency margin will be deemed to be insolvent and may be wound up by the court. An insurer is required under the IRDA (Assets, Liabilities and Solvency Margin of Insurers) Regulations, 2000, to prepare a statement of solvency margin in accordance with Schedule III‐A, in respect of life insurance business, and in Form KG in accordance with Schedule III‐B, in respect of general insurance business, as the case may be.

Risk profile of Insurance companies - ERM

For insurance companies, risk is more integral to business than it is in perhaps any other industry. The risk profile for insurance companies can be studied under the Enterprise Risk Management (ELM).

Enterprise Risk Management Defined

“Enterprise risk management is a process, effected by an entity’s board of directors, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives.”

The objectives in this case may be

1) Strategic – high‐level goals, aligned with and supporting its mission. 2) Operations – effective and efficient use of its resources. 3) Reporting – reliability of reporting. 4) Compliance – compliance with applicable laws and regulations.

Risk Management for Indian Insurers

FinStream Page 5

Further, Enterprise risk management consists of eight interrelated components. These are derived from the way management runs an enterprise and are integrated with the management process. There is a direct relationship between objectives, which are what an entity strives to achieve, and enterprise risk management components, which represent what is needed to achieve them. This relationship is depicted below. This depiction portrays the ability to focus on the entirety of an entity’s enterprise risk management, or by objectives category, component, entity unit, or any subset thereof.

Under the ERM framework, the following risks would be covered:

(1) Insurance Risk (2) Investments Risk (3) Credit Risk (4) Asset‐Liability Management Risk (5) Liquidity risk (6) Operational Risk (7) Environmental Risk

(1) Insurance Risk: The risk that inadequate or inappropriate product design, pricing, underwriting, claims management and reinsurance management will expose a life company to financial loss and the consequent inability to meet its liabilities. The major components of Insurance risks are:

• Product design risk: o The Type of risks that are underwritten (death,disability etc.) o The nature of any “guarantees” or “options” provided.

Guarantees: Minimum guaranteed interest rate, Annual/terminal surplus participation etc.

Options: Paid‐up option,Resumption option, Dynamic Premium Adjustment, Surrender options,Guaranteed annuity options etc.

• Underwriting risk: Weaknesses in the underwriting process and in the types and levels of controls and systems can expose a life company to the risk of incurring claims beyond the level assumed in pricing. This may threaten the long‐term viability of the life company.

Risk Management for Indian Insurers

FinStream Page 6

• Reinsurance risk: Reinsurance management is the process of selecting, monitoring, reviewing, controlling and documenting a life company’s reinsurance arrangements. Such arrangements may be used by life companies to manage large risks which lie outside the life company’s risk tolerance, to reduce profit volatility and for capital management and financing purposes.

Quantification / Management:

In order to control and mitigate the Insurance risks , the practices that are generally followed are to:

• Identify and assess the risks involved in designing and pricing the product. • Perform Scenario analyis to identify the impact of changes in assumptions such as claims,

discontinuance rates, expense costs, tax allowances or investment parameters on the profitability of the product at various price levels.

• Monitor the deviations of experience from that assumed (this will include the regular assessments of the insurer’s experience of mortality, disability,claim and discontinuance experience for different product types)

(2) Investments (Market or Financial) risk: Risk due to movements in the level of Financial variables such as interest rates, forex rates, stock prices etc. The main components of Market risk are:

• Interest‐rate risk – Losses due to change in Interest‐rates. The volatility in the yield of 10 year government bond in India in the past 10 years can be observed below:

• Equity and property risk – Losses due to drop in equity prices. The movement in NIFTY50 in the past 10 years can be seen below :

Risk Management for Indian Insurers

FinStream Page 7

• Currency risk – Losses due to adverse movements in Forex rates. The most traded currency contract on Indian exchanges is $/INR. The movements in the same are observable below

Quantification / Management:

Some Market risk analytics are:

GAP analysis • Calculating Gap over different time intervals at a given date • Mismatches between RSL and RSA • ∆GAP = RSA(∆ i) ‐ RSL(∆ i) = NII(∆ i) for each time bucket • Positive GAP ( RSA > RSL )

– Increasing Interest Rates would be beneficial for the company • Negative GAP ( RSL > RSA )

– Falling Interest Rates would be beneficial for the company

Risk Management for Indian Insurers

FinStream Page 8

• Interest‐rate sensitivity measures ‐ Duration and Convexity • Interest‐rate models ‐ No‐Arbitrage and Equilibrium • Use of Forward Rate Agreement (FRAs)

• An FRA is based on the idea of a forward contract, where the determinant of gain or loss is an interest rate. Under this agreement, one party pays a fixed interest rate and receives a floating interest rate equal to a reference rate. The actual payments are calculated based upon a notional principal amount and paid at intervals determined by the parties. Only a net payment is made ‐ the loser pays the winner, so to speak. FRAs are always settled in cash. A series of FRAs is similar to a swap (discussed below); however, in a swap all payments are at the same rate. Each FRA in a series would be priced at different rates (unless the term structure is flat)

A sample strategy using options is shown below

• VaR method ‐ Simulation.

• VaR is a measure of risk based on probability of loss and a specific time horizon • Key constituents of VaR are – Measurement horizon, Confidence Interval, and Loss

Distribution type. • VAR tells us that the “Portfolio can lose a maximum of Rs X over the next Y days

with a confidence level of 95%” • VaR translates portfolio volatility into a Rupee value and gives a measure of

uncertainty through confidence level. • Monte‐carlo simulation can be generated to determine various possible scenarios

and associated profit/loss in the portfolio can be estimated.

(3) Credit Risk: Risks due to default by and change in the credit rating of those to whom the company has an exposure. Ex‐ Re‐insurance companies, Companies in which we have invested funds.

The main components of credit risks are:

Risk Management for Indian Insurers

FinStream Page 9

• Business credit risk – Failure of a reinsurer. • Invested asset credit risk – Nonperformance of invested assets.

Quantification / Management:

The formula as suggested by the CEIOPS’s (Committee of European insurance and Occupational Pensions Supervisors ) advice on implementing measures on Solvency II (SCR standard formula – Calibration of Credit risk – Q1S3)

(4) Liquidity risk: Risk that Cash Sources (Cash inflows from Insurance products—Premiums and Deposits, Asset Cashflows, Asset sales etc.) are insufficient to meet Cash Needs( Product cash outflows, Operating cash outflows, contingent cash needs).

Quantification / Management:

Liquidity Stress Scenario analysis:

Goal‐‐‐‐‐To ensure sufficient liquidity in the asset portfolio to provide for timely payment of potential cash demands under both‐‐‐Normal and extreme business conditions.

Scenarios can be :

• Changing interest rates ‐ Increase in interest rates might result in more withdrawals due to availability of alternative investment options.

• Liquidity needs from insurance claims/ large operational loss • Loss of a key distributional channel.

(5) Asset‐Liability Management Risk: Risk arising due to mismatch on account of duration of Assets (bonds) and duration of Liabilities i.e. the mismatch of interest rate sensitivity to assets and liabilities leading to impact on company’s surplus.

Quantification / Management:

Scenario based analysis and stress testing by taking into account the various variables affecting the future value of Assets and Liabilities

ALM

The SOA defines ALM as “the practice of managing a business so that decisions on assets and liabilities are coordinated; or more broadly …..The ongoing process of formulating implementing monitoring and revisiting strategies related to assets and liabilities in an attempt to achieve financial objectives for a given set of risk tolerance and constraints”

Risk Management for Indian Insurers

FinStream Page 10

Why must we consider ALM

Mismatching could have serious implications for the financial viability, as evidenced by collapse of many life insurers.

ALM answers the strategic questions, viz.,

• availability of adequate capital for solvency in stressed scenario; • how to make a tradeoff between risk and return; • what is the optimal growth of premium, given the risk appetite; • adequacy of reinsurance arrangements; • optimal use of risk mapping and evaluation of alternative strategy

Pillars for ALM

The ALM process rests on three pillars:

In this paper we further elaborate on the framework we think is suited for pension fund and insurance company ALM management. We think risk management is not just a regulatory requirement but is necessary for the healthy running of any financial institutions.

Modeling and Managing Risk

ALM modeling can be split into a systematic process. We use our proprietary framework to analyze and

manage the interest rate and other risks of a bank.

ALM information System

•Management Information System •Information availability, accuracy, adequacy and expediency

ALM organization

•Structure and responsibilities•Level of top management involvement

ALM process

•Risk parameters•Risk identification•Risk measurement•Risk management•Risk policies and tolerance levels

Risk Management for Indian Insurers

FinStream Page 11

1. Getting the precise nature and cash‐flows of liabilities and fixed assets.

2. Modeling Interest Rate

a. Modeling risk premium

b. Modeling other economic factors like inflation

c. Modeling volatilities

d. Mean reversion

e. Modeling correlations and basis

3. Measuring Risk

4. Management of Risk: Evaluating and implementing various strategies

Step 1: Asset Liability Modeling

A simple stylistic modeling of the balance sheet of an insurance company would look something like this:

Assets Liabilities and Stockholder's Equity Goodwill Present value of Insurance Contracts

Intangible Assets Present value of contracts accounted as financial instruments

Borrowing Cost Employee benefits Property Plant and Equipment Provision and other liabilities Deferred Tax Asset Deferred tax liabilities Lease Asset Other long term borrowings Investments Derivatives

• Debt and Equity • Derivatives • Loans • Investment Property • Investment in subsidiaries • Investment in Associates

Interest bearing Liabilities Payables‐ Insurance Payables‐ Reinsurance Current tax payable Lease liability Bank overdraft

Financial assets EQUITY • Other receivables • Cash and cash equivalents • Receivables – insurance • Receivables – reinsurance • Current tax receivables

Issued Capital and Reserves Minority Interest

Insurance Contracts with a positive Net present Value TOTAL ASSETS Total Liability and Shareholder’s Equity

We will now evaluate the difference in duration of assets and liabilities on Life and P/C insurers and its

effect of a scenario analysis of changing interest rates.

Risk Management for Indian Insurers

FinStream Page 12

Difference in duration of Assets and Liabilities

Life insurance General Insurance

More long term assets

The payment stream from the issuer to the

annuitant has an unknown duration based

principally upon the date of death of the

annuitant

Difficult to predict duration of liabilities

due to uncertainty in prediction of claims

Life insurance pricing is highly sensitive to

long term interest rates. (bonds and life

insurance perceived as similar products)

Long dated bond portfolio is needed to

match guaranteed payments (liabilities)

If the guaranteed payments are not

hedged with long‐term bonds, the

insurance companies must buy options to

ensure the necessary payoff on the liability

side.

More active in trading IR and forex.

More short to mid‐term assets

Shorter duration of policies means more

certainty in assets and liabilities estimates.

More active in trading equity options and

forex derivatives.

Scenario Analysis ‐ Changing Interest Rates

Life insurance General Insurance

Duration of liabilities > Duration of assets

When interest rates rise value of assets,

liabilities and hedges fall

Value of liabilities falls more than value of

assets + hedge => net gain.

Duration of hedge should be chosen in

accordance with view on interest rates .

However, matching duration accurately

requires precise information of liabilities

and assets which is difficult to assess.

Duration of liabilities is more accurately

predictable

When interest rates rise value of assets,

liabilities and hedges fall

Depending of hedge ratio the effect of

rise/fall in IR can be mitigated.

Risk Management for Indian Insurers

FinStream Page 13

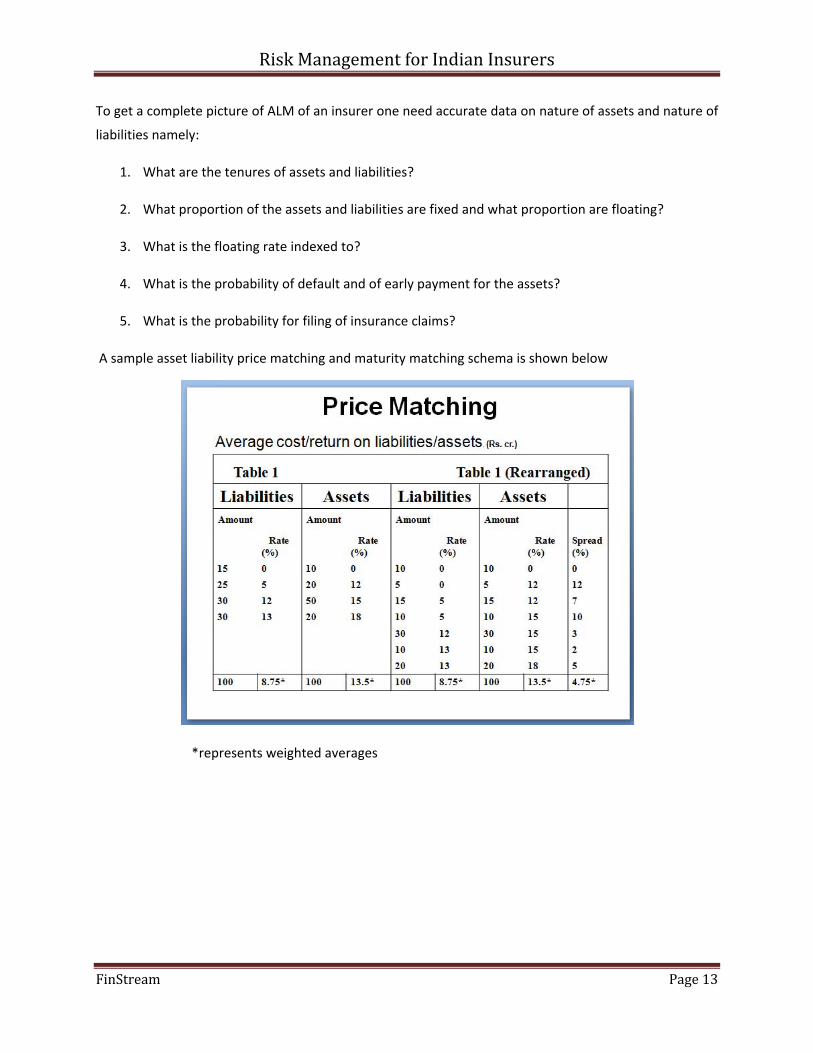

To get a complete picture of ALM of an insurer one need accurate data on nature of assets and nature of

liabilities namely:

1. What are the tenures of assets and liabilities?

2. What proportion of the assets and liabilities are fixed and what proportion are floating?

3. What is the floating rate indexed to?

4. What is the probability of default and of early payment for the assets?

5. What is the probability for filing of insurance claims?

A sample asset liability price matching and maturity matching schema is shown below

*represents weighted averages

Risk Management for Indian Insurers

FinStream Page 14

This brings us to the second aspect of risk modeling i.e. modeling interest rate movement.

Step 2: Market Modeling

Modeling the projected movement of interest rate is the key for analyzing risk in any financial

institutions. Several theoretical and statistical models are prevalently used in the industry. Certain

aspects that have to be kept in mind while modeling:

1. Risk Premium: Interest rates and bond prices have a risk premium embedded in them. In other

words investors demand higher premium for locking in money for longer term. This is also

referred to as the term premium of interest rates. The premium has to be accounted for to

build any realistic model. We have developed statistical methods to extract the risk premium.

2. Economic Factors: Economic factors influence every aspect of the balance sheet of a bank. A

growing economy on one hand will help on the asset side as quality of assets to improve but at

the same time interest costs on the liabilities would also increase and vice versa. Thus it is

crucial to generate several economic scenarios to see which scenario gives maximum risk.

3. Volatilities: It is important to get the volatilities of interest rates and other factors as that would

point us to the right risk factors which would be the most crucial to hedge. Volatilities can be

statistically modeled from time series data. All the factors like interest rates, FX, default rates

etc. can be modeled this way.

Risk Management for Indian Insurers

FinStream Page 15

4. Mean Reversion: although interest rates in the short‐term can fluctuate a lot in the long run

interest rates are range bound thus any spikes in interest rates would eventually correct. This is

a unique aspect of interest rates that’s not valid for other assets like equities.

5. Basis and Correlations: Although all assets and liabilities are affected by interest rate

movements, the movements are not perfectly correlated. For example floating rate loans might

be linked to PLR, which moves together with government bond yields but the relationship is not

perfect. Hence correlations and basis between various rates have to be modeled carefully.

Again we rely on statistical analysis for the same.

A sample strategy based on relation between interest rates and currency value is shown below

Suppose the company is expecting an appreciation in $/INR. This would mean that rupee will be

undervalued and hence the expected return on investment would also fall. To protect their investment

the company should buy $/INR calls. Since the bond rates will rise with a falling rupee, bond prices will

fall. Thus, the company should also sell 10 year bonds to hedge their position. Note that total hedging

may not be the optimal solution.

Step 3: Measuring Risk

Risk can be managed only if it is measurable. Various measures are being used currently by institutions.

Any measure should not only look at current position of the balance sheet but should also be forward

looking. For this purpose we think the following is a good list of risk measures to track.

1. Solvency ratio 2. Scenarios of solvency ratio 3. Duration Gap – Interest Rate sensitivity of PnL

FinStream

4. Va5. Pr6. Pr

Each of thabove me

Our Ap

At FinStregood risk bank/insu

Our appro

FinStrem

M‐Rix is oquant andour kerneany platfokernel robneeds.

m

aR and CVaR robability of rrobability of r

hese measureentioned stati

pproach a

eam we see rimanagement

urance compa

oach can be s

m risk kerne

our risk managd math basedel in stable anorm – web babust and stab

Risk Mof solvency/r

remaining solremaining >9

es can be obtaistical techniq

and Offeri

isk managemt can beat coany.

summarized in

el – M-RIX

gement tool td computationd powerful co

ased, desktopble, it offers th

Managemereturns lvent 5% etc.

ained by geneques.

ing

ent as a tool mpetition an

n the diagram

that is develon engine whicomputing env application, he great adva

ent for Inderating enoug

to enhance pd increase re

m below:‐

oped in moduch connects tvironment of client server

antage of bein

dian Insuregh scenarios o

profitability. Tturns for bon

ules. It is powhe various mC++. The fromodel etc. N

ng customiza

ers of the balanc

This comes frond and equity

ered by a kerodules. We hnt for the appot just is the ble for compa

Pa

e sheet using

om the fact thy holders of a

rnel which is ahave developeplication coulback end for any specific

ge 16

g the

hat

a ed d be our

Risk Management for Indian Insurers

FinStream Page 17

Measuring market risk

We quantize the following parameters as a measure of market risk:‐

Duration gap

Sensitivity to various factors like Interest rate, FX, Equities, Commodities (also called deltas)

Daily standard deviation of returns

Value at Risk

Extreme loss measures

Sharpe ratio (More for risk/return measurement)

Term structure risks

These risks become particularly important in view of a banking/insurance environment. Term structure risk is measured using key‐rate duration (KRD). KRD is the effect on Profit and Loss statement by change of one point on the term structure. Example of changes in the term structure could be:‐

Parallel shift ‐ It occurs when the interest rate on all maturities increases or decreases by the same number of basis points.

Non Parallel Shift – Generally, short term yield change more than long term yield rates

Risk Management for Indian Insurers

FinStream Page 18

Integrating with economics Post measurement of market risk we link it to macro‐economic trends. Sample macroeconomic drivers and their effect on bond, equities, IR and FX market can be observed below.

Driver Correlation Pattern

Economic growth/recession o ‐ve correlation between bonds and Equities (+ve with IR)

o +ve correlation between Equities and commodities

o +ve correlation between currency and equities

RBI policy/Liquidity o +ve correlation between bonds and Equities (‐ve with IR)

o ‐ve correlation between equities and FX

o +ve correlation with IR and FX

Inflation/Deflation o ‐ve correlation between commodities and equities

o +ve correlation between equities and bonds (‐ve with IR)

Diversification

Measured market risk along and macro‐economic factors clubbed with the detail analysis of balance sheet and P&L help us achieve the right diversification mix. The benefits of diversification can be observed below:‐

Risk Management for Indian Insurers

FinStream Page 19

Resulting Reports

Based on the same a hedging strategy is formulated which has strong analytical support.

Key Features

1) New product consideration ‐ Our solutions greatest strength lies in its ability to expand into a variety of products including:‐

a. Corporate bonds

b. Swaps on IR, Fx and Equities

c. Swaptions

d. Exotic options like barrier and Asian options

e. CDS

f. Commodities, Inflation etc.

L ist o f Re port s:

D urat io n K ey rate du ratio n

Cash flow s Basel II

Sensitiv ity to Equ ity/FX VaR Rep ort

R isk p ie Scen ario s

S im ulatio n re po rts

Risk Management for Indian Insurers

FinStream Page 20

2) Technological consideration – The main technological benefits of our solution are:‐

a. Robustness and reliability

b. Speed – It has a powerful and fast backend in C++

c. Flexibility – coming from the modular approach

d. Platform independence ‐ Delinking frontend and backed helps us to implement the software in any platform.

e. Ability to Integration with other software

Miscellaneous features

Time series analysis – Markets and Economics Benchmark analysis Generating automatic reports compliant with RBI Credit risk analysis and calibration (IMA based) Asset and liability combined view Derivative analysis Portfolio modification and hedging possibilities Integrable to data feeds from various sources viz. Bloomberg, Reuters and other treasury

systems Continuous upgrading and maintenance