Embed Size (px)

Citation preview

Inte

rest

Rate

Derivatives

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

Proprietary information. © 2015 Bloomberg L.P. All rights reserved.

/ /

Proprietary information. © 2015 Bloomberg L.P. All rights reserved.

RISK MANAGEMENT

TOOLSIndependent, Transparent, On Demand

Beth Kostick

June 16, 2016

Program

• News • Natural Language Search• PAP on Bloomberg

• Single Security Risk Tools• Equity• Fixed Income

• Portfolio Management and Risk Tools• Allocation• Value At Risk • Scenarios

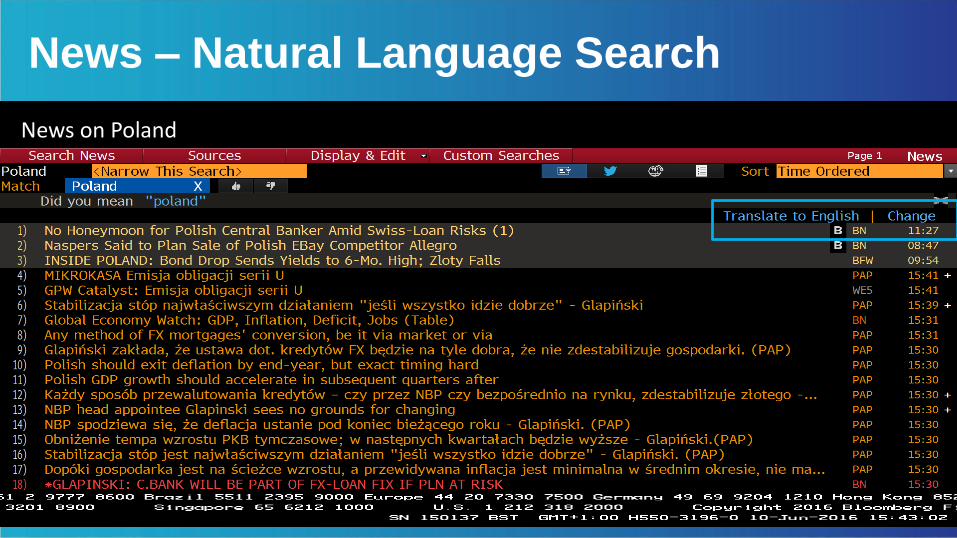

News – Natural Language Search

News on Poland

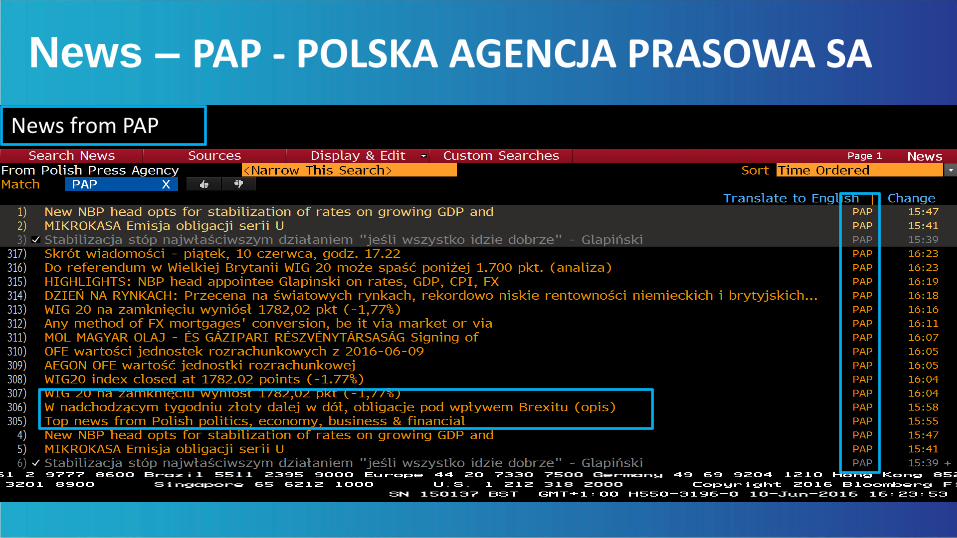

News – PAP - POLSKA AGENCJA PRASOWA SA

News from PAP

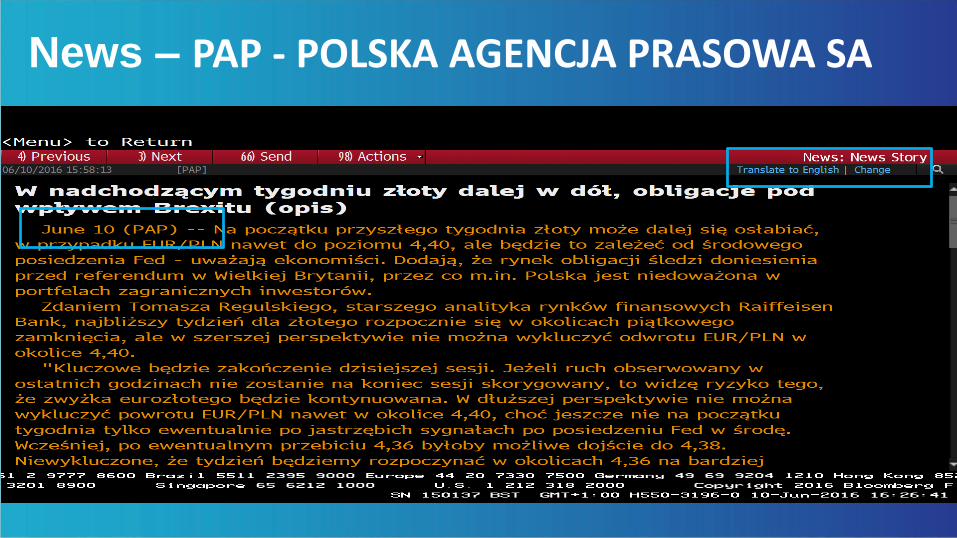

News – PAP - POLSKA AGENCJA PRASOWA SA

Single Security Risk – Company Risk

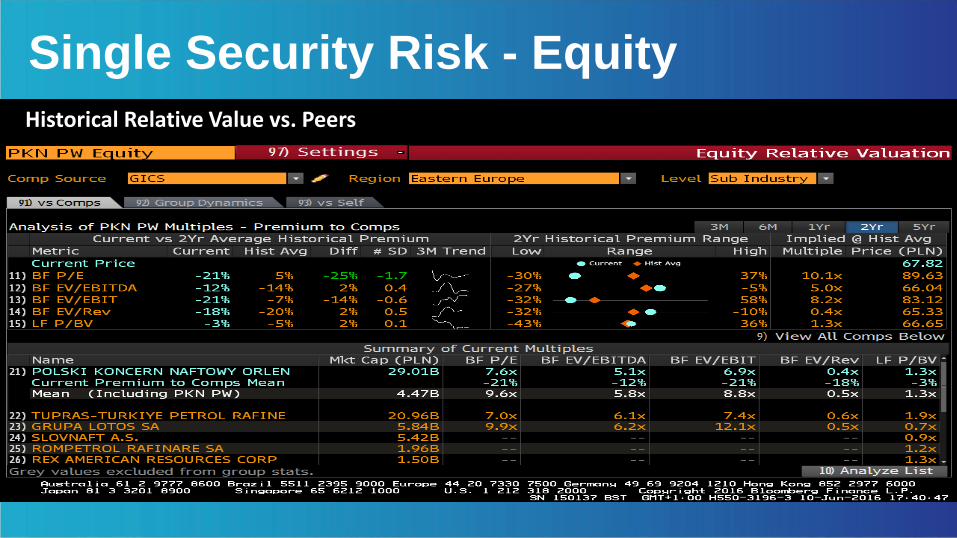

Single Security Risk - Equity

Single Security Risk - Equity

Historical Relative Value

Single Security Risk - Equity

Historical Relative Value vs. Peers

Single Security Analysis – Fixed Income Description

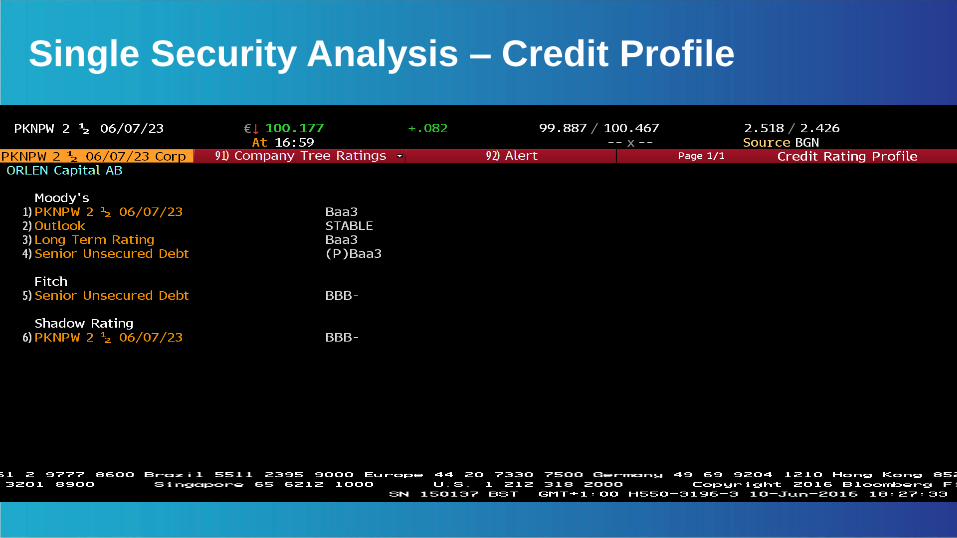

Single Security Analysis – Credit Profile

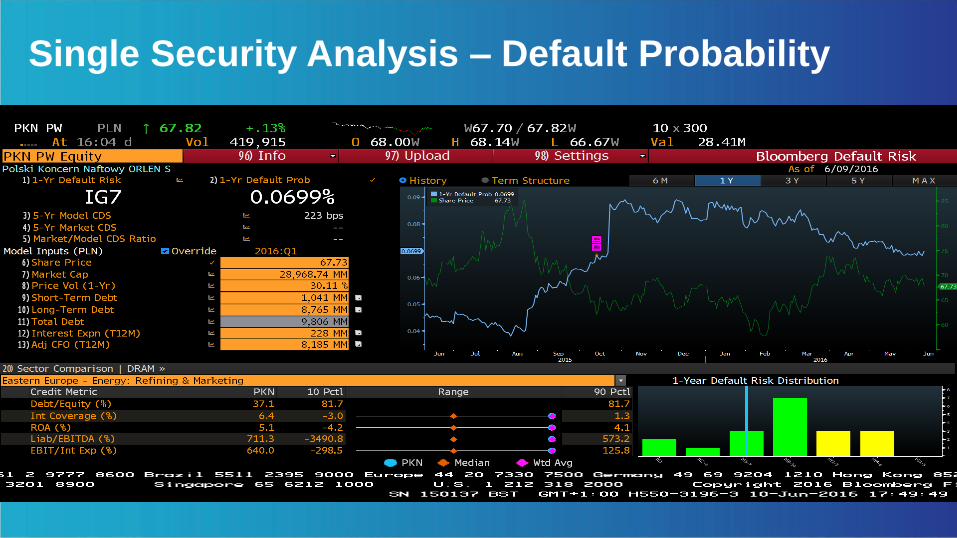

Single Security Analysis – Default Probability

Single Security Analysis – Debt Distribution

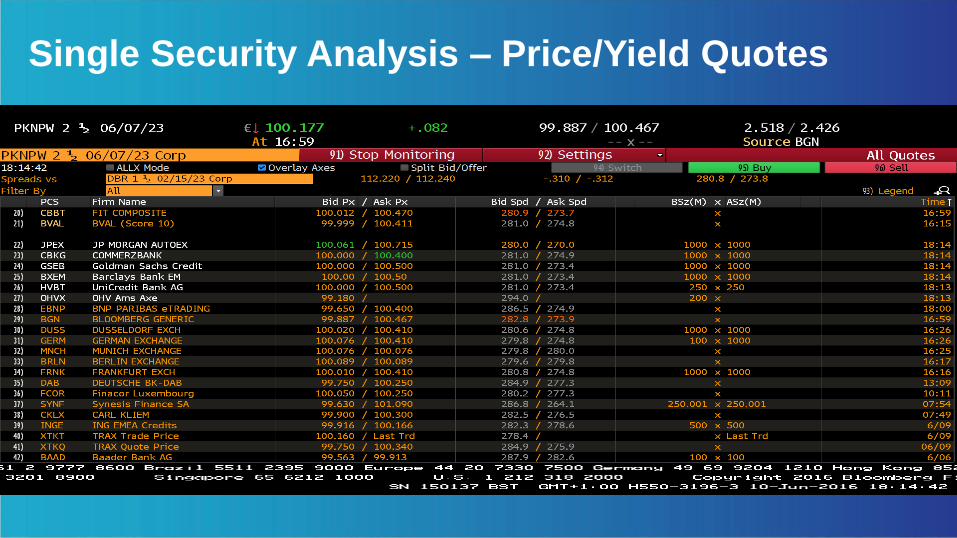

Single Security Analysis – Price/Yield Quotes

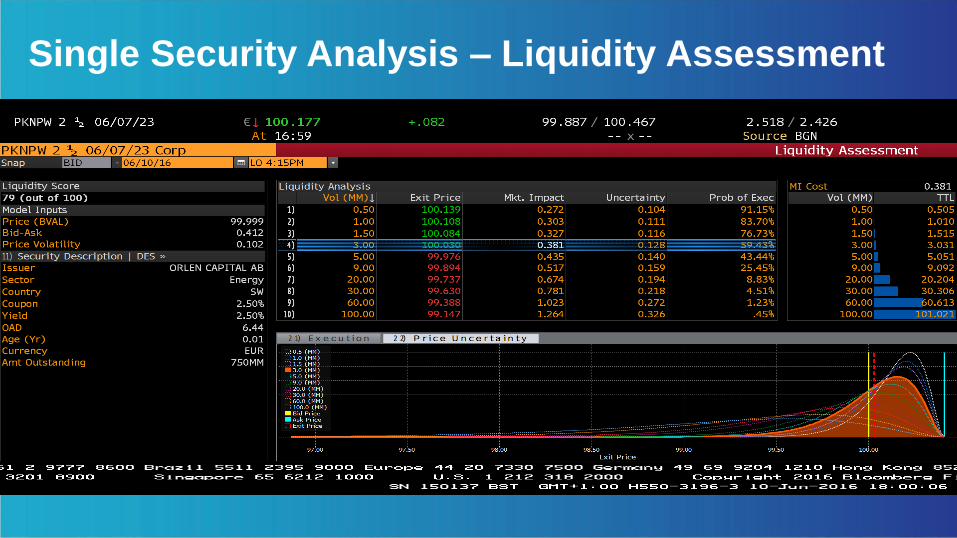

Single Security Analysis – Liquidity Assessment

PORT<GO> Overview

PORT as portfolio management work-flow solution

Characteristics Performance RiskPortfolio

construction

Portfolio – Characteristics

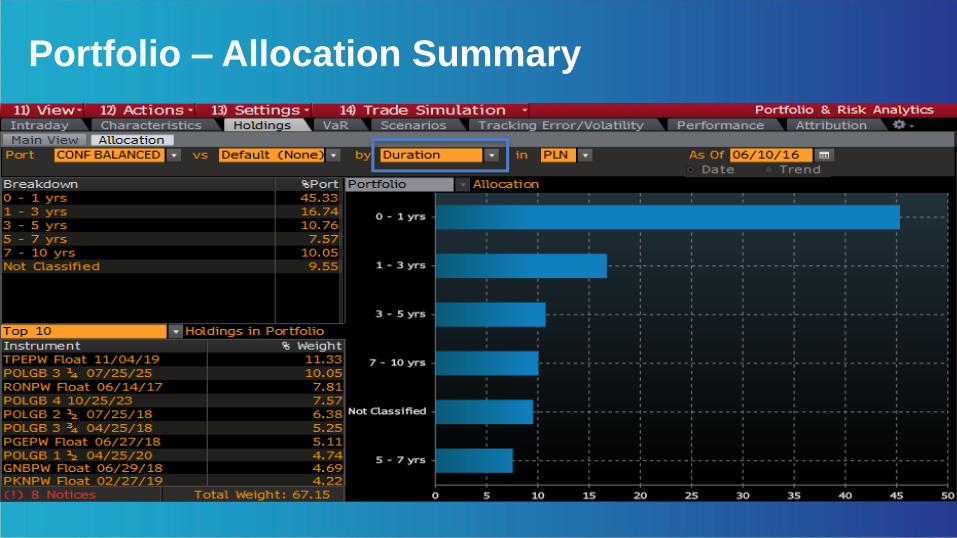

Portfolio – Allocation Summary

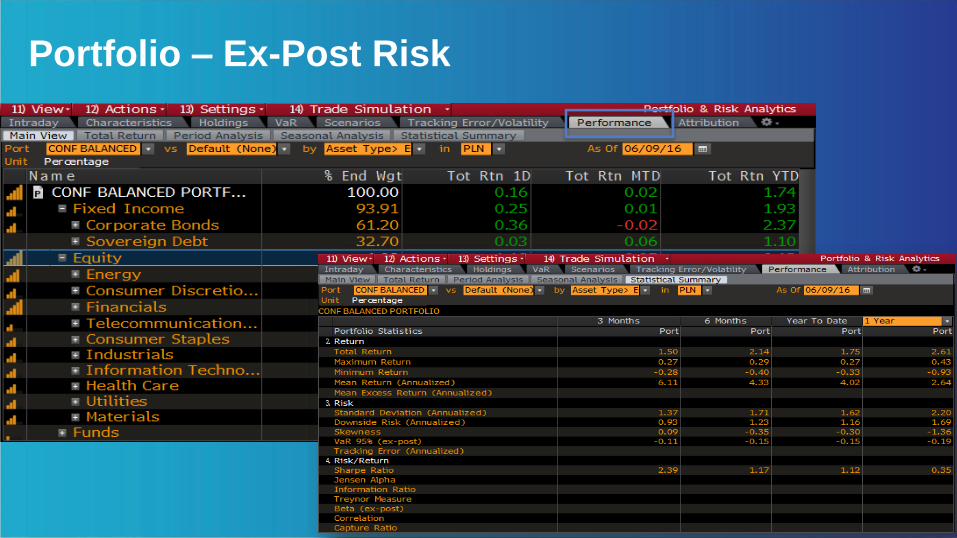

Portfolio – Ex-Post Risk

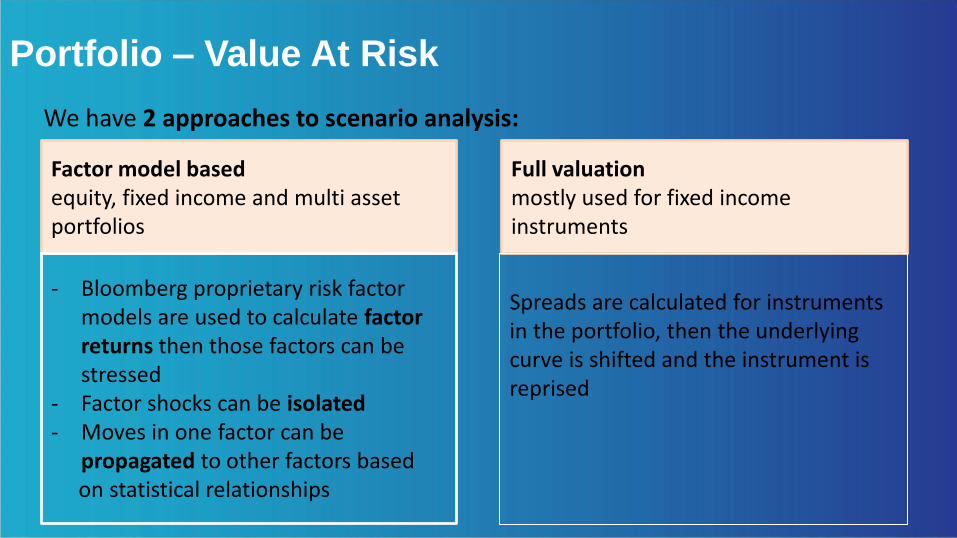

Portfolio – Value At Risk

Portfolio – Value At Risk

We have 2 approaches to scenario analysis:

Factor model based equity, fixed income and multi asset portfolios

Full valuation mostly used for fixed income instruments

- Bloomberg proprietary risk factor models are used to calculate factor returns then those factors can be stressed

- Factor shocks can be isolated - Moves in one factor can be

propagated to other factors based on statistical relationships

Spreads are calculated for instruments in the portfolio, then the underlying curve is shifted and the instrument is reprised

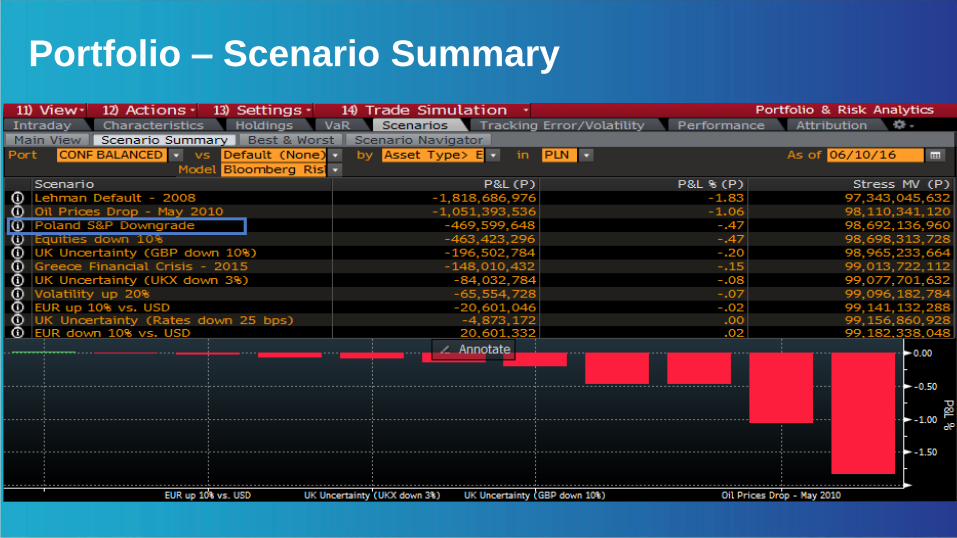

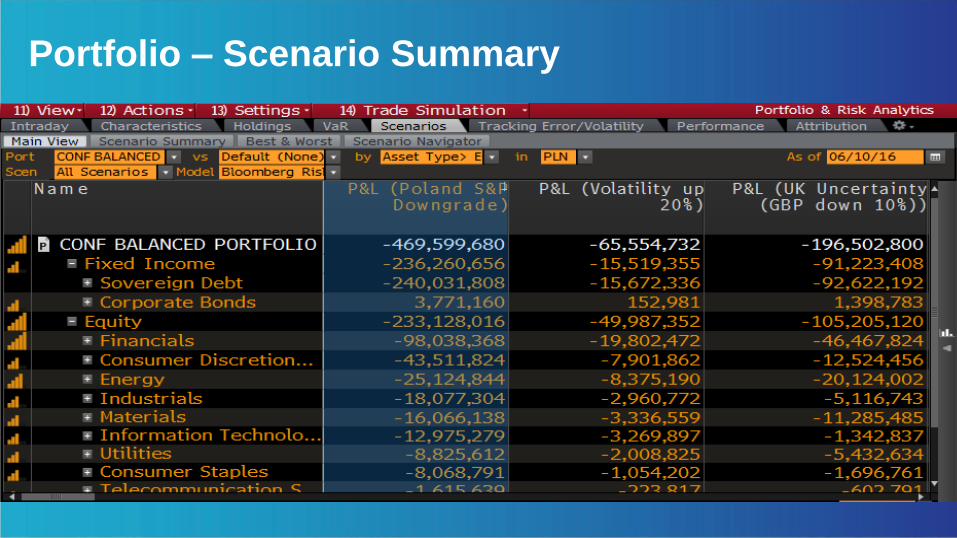

Portfolio – Scenario Summary

Portfolio – Scenario Summary

Inte

rest

Rate

Derivatives

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

>>

Proprietary information. © 2015 Bloomberg L.P. All rights reserved.

/ /

Proprietary information. © 2015 Bloomberg L.P. All rights reserved.

Dziᶒkujᶒ