Embed Size (px)

Citation preview

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 1

Risk Integration

Dr. Ren-Raw Chen

Fordham University

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 2

Basel Accords

• First Accord in 1988

– orig meant for G10 countries

– now used over 100 nations

• Accord II in 1998

– formally published in 2004

• Accord III in 2011 (?)

– on going

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 3

Basel I

• The bank must maintain capital (Tier 1 Tier 2) equal to at least 8% of its RWA

– 0% - cash, any OECD government debt

– 0%, 10%, 20% or 50% - public sector debt

– 20% - development bank debt, OECD bank debt, OECD securities firm debt, non-OECD bank debt (under one year maturity) and non-OECD public sector debt, cash in collection

– 50% - residential mortgages

– 100% - private sector debt, non-OECD bank debt (maturity over a year), real estate, plant and equipment, capital instruments issued at other banks

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 4

Tier 1 Capital

• Tier 1 capital is the core measure of a bank's financial strength. It is composed of

– common stock and

– disclosed reserves (or retained earnings), but may also include

– non-redeemable non-cumulative preferred stock.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 5

Tier 1 Capital

• The Basel Committee also observed that banks have used innovative instruments over the years to generate Tier 1 capital; these are subject to stringent conditions and are limited to a maximum of 15% of total Tier 1 capital.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 6

Tier 2 Capital(supplementary capital)

• Tier 2 is limited to 100% of Tier 1 capital

– Undisclosed reserves

– Revaluation reserves

– General provisions/general loan-loss reserves

– Hybrid debt capital instruments

– Subordinated term debt

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 7

Tier 3 Capital

• Banks will be entitled to use Tier 3 capital solely to support market risks as defined in paragraphs 709 to 718(Lxix).

• Tier 3 capital will be limited to 250% of a bank’s Tier 1 capital that is required to support market risks.

– This means that a minimum of about 28½% of market risks needs to be supported by Tier 1 capital that is not required to support risks in the remainder of the book;

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 8

Capital

• Regulatory (reg) capital

– Fixed (8%)

– IRB

• Risk-adjusted return on capital (RAROC)

– = (Expected Return)/(Economic Capital)

– = (Expected Return)/(Value at Risk)

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 9

Capital

• Economic capital

– It is the amount of risk capital which a firm requires to cover the risks that it is running or collecting as a going concern, such as market risk, credit risk, and operational risk.

– Firms and financial services regulators should then aim to hold risk capital of an amount equal at least to economic capital.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 10

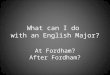

Capital Ratios

• Tier 1 capital ratio = Tier 1 capital / Risk-adjusted assets >=6%

• Total capital (Tier 1 and Tier 2) ratio = Total capital (Tier 1 and Tier 2) / Risk-adjusted assets >=10%

• Leverage ratio = Tier 1 capital / Average total consolidated assets >=5%

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 11

Capital Ratios

• Common stockholders’ equity ratio = Common stockholders’ equity / Balance sheet assets

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 12

Basel II

• Three pillars

– framework encompassing risk-based capital requirements for credit risk, market risk, and operational risk (Pillar 1);

– supervisory review of capital adequacy (Pillar 2);

– and market discipline through enhanced public disclosures (Pillar 3).

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 13

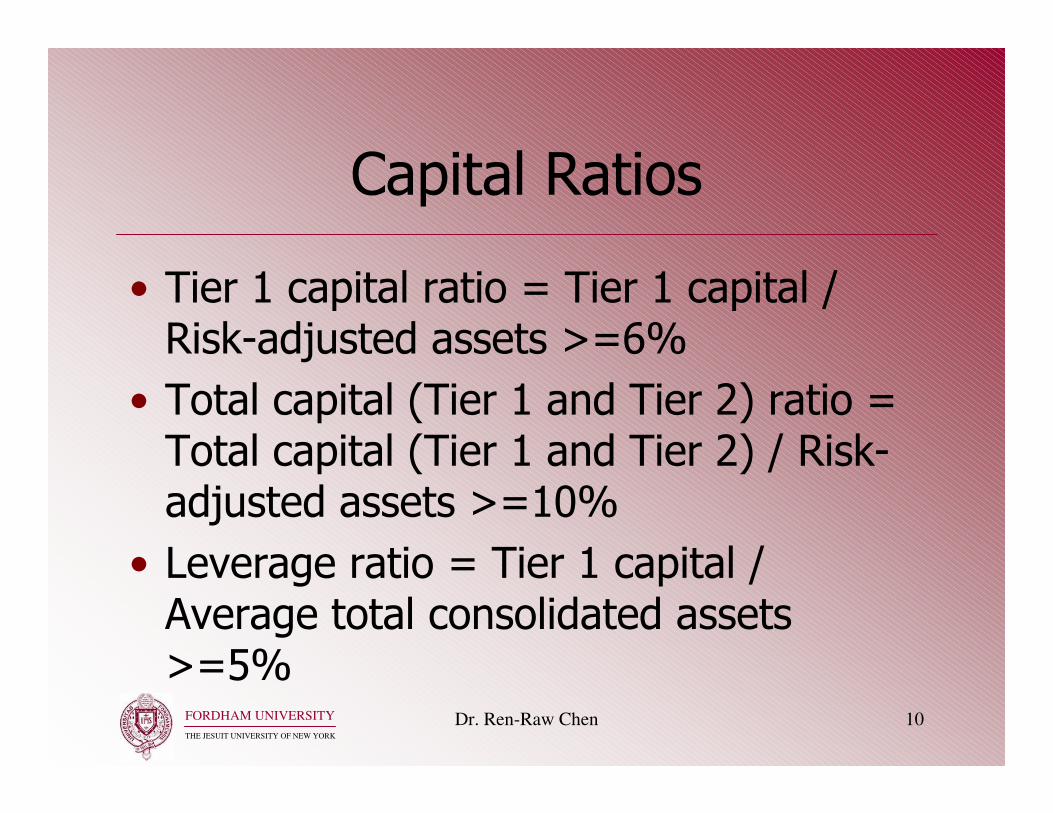

Basel II

• June 2006, A Revised Framework

– risk-based capital for credit risk and for operational risk

• December 7, 2007, OCC, FDIC, OTS issued a final rule

– advanced internal ratings-based approach for credit risk and the advanced measurement approach for operational risk

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 14

Basel II

– the advanced approaches rule defines a core bank as a bank that has consolidated total assets of $250 billion or more, has consolidated on-balance sheet foreign exposure of $10 billion or more, or is a subsidiary of a core bank.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 15

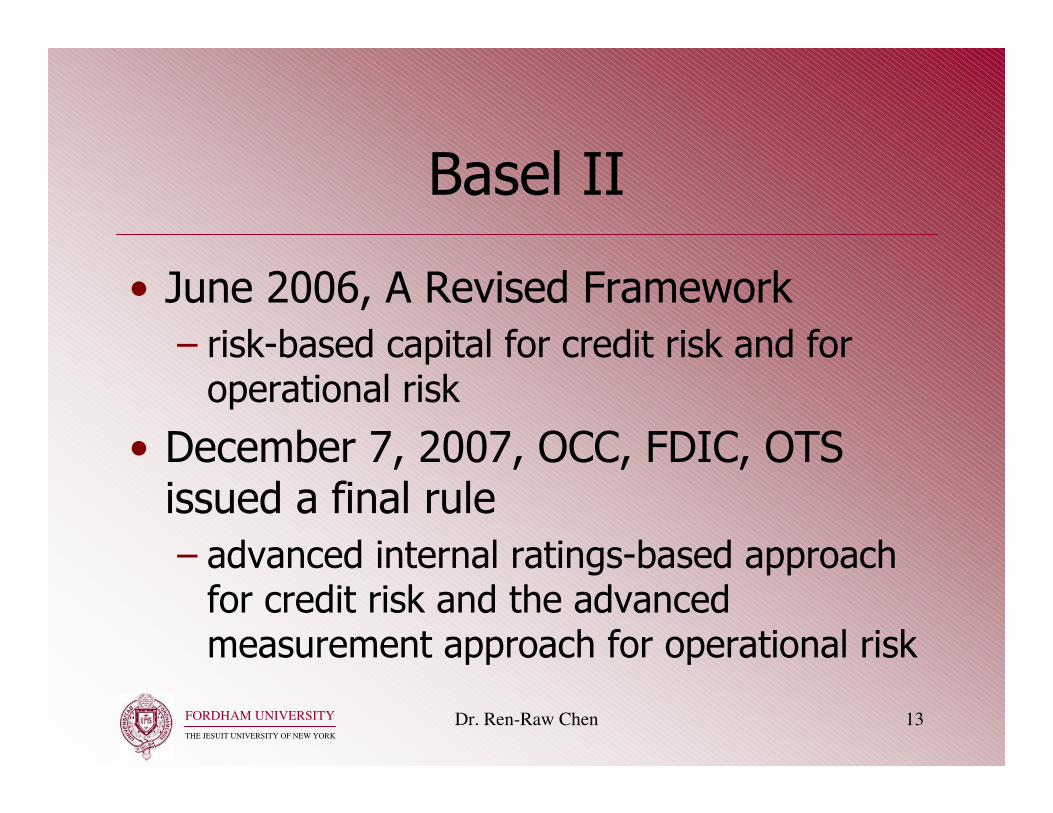

Basel III

• Increased overall capital requirement

– Between 2013 and 2019, the common equity component of capital (core Tier 1) will increase from 2% of a bank’s risk-weighted assets before certain regulatory deductions to 4.5% after such deductions.

– A new 2.5% capital conservation buffer will be introduced, as well as a zero to 2.5% countercyclical capital buffer.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 16

Basel III

• Increased overall capital requirement

– The overall capital requirement (Tier 1 and Tier 2) will increase from 8% to 10.5%over the same period.

• Increased capital charges

– Commencing 31 December 2010, re-securitization exposures and certain liquidity commitments held in the banking book will require more capital.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 17

Basel III

• Increased capital charges

– In the trading book, commencing 31 December 2010, banks will be subject to new “stressed” value-at-risk models, increased counterparty risk charges, more restricted netting of offsetting positions, increased charges for exposures to other financial institutions and increased charges for securitisation exposures.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 18

Basel III

• New leverage ratio

– A minimum 3% Tier 1 leverage ratio, measured against a bank’s gross (and not risk-weighted) balance sheet, will be trialled until 2018 and adopted in 2019.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 19

Basel III

• Two new liquidity ratios

– A “liquidity coverage ratio” requiring high-quality liquid assets to equal or exceed highly-stressed one-month cash outflows will be adopted from 2015.

– A “net stable funding ratio” requiring “available” stable funding to equal or exceed “required” stable funding over a one-year period will be adopted from 2018.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 20

Subprime Crisis

• Where this all began

– size of subprime

• prime is $8~10 trillion (secured by agencies)

• subprime is 4% of prime ($400 billion)

• recovery of prime 80~90% (due to loan to value requirement LTV>0.8)

• recovery of subprime 40% or so (LGD=0.6)

• total loss of subprime $240 billion = 1.7% of GDP

• So my assessment (talks in 2007) -- NO BIG DEAL

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 21

Subprime Crisis

• Why was it a crisis?

– subprime size grew (estimated to be 10% of prime = $1 trillion

– LGD went higher due to collapse of housing market

– so impact was higher

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 22

Bailout

• TARP (Troubled Asset Relief Program)

• Originally authorized expenditures of $700 billion

• Reduced to $475 billion

• Mostly repaid

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 23

Bailout

• AIG bailout $182 (total) / $50 (2008) billion

– Goldman $40 / $6 billion

– Deutsche Bank

– Societe Generale

• BofA’s (BAC) Merrill Lynch $50 billion ,

• Citigroup $27 billion of preferred stock

• IndyMac Bank $32 billion

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 24

Bailout

• Size of the crisis

– 1% of GDP

– compared to S&L (savings and loan) crisis in the 80’s 3.5% of GDP

• So why fear?

– panic

– bank runs

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 25

Issues of Crisis

• Marking to market

• Wall street bonus system – excess risk taking (free trader option)

• Regulation (1986 Act)

• Liquidity pricing (price of bailout)

• Rating agency reform (history based model)

• Financial innovations – hedge funds?Issues

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 26

Issues of Crisis

• Financial Education – ethics

• Prepare for a more-risky-than-ever future

– happens every time

• What are the opportunities

– risk management

– IT investment

– more difficult pricing modelssues

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 27

Impact of Crisis

• Is crisis really over

– double dip (W) or triple dip (WV or WW)

– in a situation never before – stock market high and yet unemployment high

– longest recession ever

• Past monetary weapons failed

– how to boost economy (i.e. reduce unemployment) and keep real estate cool

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 28

Impact of Crisis

• Change of landscape

– increase influence of China

– US remains a superpower?

• How to avoid TBTF in the future

– conflict of tight regulation

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 29

Impact of Crisis

• Is mathematical modeling dead or more live then ever

– conflict of MTM failure (failure of models) and high frequency trading (more use of models)

• Where are the jobs

– MBA dies and MQF lives???

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 30

Impact of Crisis

• Questioning marking to market

• Calibration is Wall street standard

– reliable market prices

– market prices better than any model (collective wisdom of the entire participants population)

– prevent model manipulation

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 31

Impact of Crisis

• Questioning of marking to market

• Is price under panic reliable?

– panic = liquidity

– how to model panic?

– without modeling panic, no MTM

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 32

Impact of Crisis

• Excess risk taking

• Wall street bonus system is wrong

– how to eliminate free trader option (talked about it last time)

– how to reward effort correctly

– how to eliminate principal-agent problem

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 33

Impact of Crisis

• Optimal regulation

– regulation should not impair free economy (the Invisible Hand)

• carefully choose tools

– regulation should not destroy innovations

– regulation should be liquidity driven

• liquidity index

– regulation should punish bad guys

• legal solution

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 34

Impact of Crisis

• Rating agency reform

• Modified historical based model

• Remove conflict of interest

– Arthur Anderson bankruptcy

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 35

Future Financial Innovations

• Is hedge funds our hope?

– somebody has to take risk

– there is a supply, as long as there is demand

– how hedge funds should be regulated

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 36

Future Financial Innovations

• How to teach ethics?

– learn from grandma’s laps, not from school

– learn by example, not by preaching

• Emphasize

– value of life

– happiness (utililty?) – Harvard popular course: How to be happy, positive psychology by Dr. Tal Ben-Shahar

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 37

Future Financial Innovations

• 2011 terrorist case in NYC

– last minute capture at the airport highlights the importance of fast information

– quick gathering of the ID of the suspect highlights the importance of information integration

• 2013 terrorist case in Boston

– failure to trace

• New technology in data mining

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 38

Future Financial Innovations

• Risk management more important than ever

• New derivatives

– liquidity derivatives

• More IT investment

• More pricing models

• Global market to play withunities

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 39

Quantitative Easing

• $700 billion and $800 billion of Treasury notes on its balance sheet before the recession

• November 2008, the Fed started buying $600 billion in Mortgage-backed securities (MBS)

• Peak at $2.1 trillion in June 2010

• Anticipate to fall (debt maturing) to $1.7 trillion by 2012

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 40

Quantitative Easing

• Fed's revised goal became to keep holdings at the $2.054 trillion level

– August 2010, bought $30 billion in 2–10-year Treasury notes

• November 2010, the Fed announced a second round of quantitative easing, buying $600 billion of Treasury securities by the end of the second quarter of 2011 (QE2)

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 41

Quantitative Easing

• QE3 was announced on 13 September

• 2012

– $40 billion per month, open-ended, purchasing of mortgage-backed securities

– Federal Open Market Committee (FOMC) announced to maintain the federal funds rate near zero "at least through 2015.“

– Because of open-ended, QE3 has earned the popular nickname of "QE-Infinity."

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 42

Quantitative Easing

– On 12 December 2012, the FOMC announced increased the amount of openended purchases from $40 billion to $85 billion per month.

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 43

Quantitative Easing

• Why QEs did not cause inflation (which is almost a certain consequence)

– China accounted for three-fourths of rise in non-oil goods trade deficit

• from $500 billion in 2010 to $558 billion in 2011, an increase of $58 billion (11.6 percent)

• increased surplus in services trade by $33.2 billion in 2011, resulting trade deficit in goods trade, from $645.9 billion to $737.1 billion (an increase of $91.2 billion or 14.1 percent)

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 44

Quantitative Easing

• QEs meant to boost liquidity

• QEs meant to build infrastructure

– push centralized trading of exotic products

– push centralized clearing

– build healthier smaller, regional banks (where most defaults occur)

– keep rates low so borrowings can be easy

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 45

Quantitative Easing

• Prices deviate from fundamental values

– prices high and fundamentals weak

• domestic

– unemployment high

– real estate weak

• global

– Euro crisis

– Japan recession

– China slow growth

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 46

Quantitative Easing

• Four consequences if QEs stop

– hurting stock market (converging to fundamentals?)

– rising inflation

• China growth slows down

– rising interest rates

• bonds being dumped back into the market

• hurting real estate (which has not been fully recover)

– banks unhealthy again (lack of liquidity)

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 47

Risk Integration

• Technology integration

– various platforms

• Model integration

– match technology platforms

– modulization (plug and play)

– different but consistent

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 48

Risk Integration

• Credit and liquidity are

– inseparable

– highly correlated

• Liquidity driven credit risk

– separate bankruptcy risk of credit from market risk of credit

– ultimate goal: probability of default (PD) and loss given default (LGD)

– importance of endogeneity

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 49

Risk Integration

• Equity = residual claim on assets = call– K = face value; D = current value

– spread = -ln[D/K] - risk free rate

– PD (probability of default) = Prob(A<K)

– LGD (loss given default) = A (when A<K)

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 50

Risk Integration

• Geske extends it to multiple debts

– term structures of PDs, LGDs, spreads

– possible to seek optimal capital structure

• LTD (long term debt) vs. STD (short term debt)

• debt vs. equity

– first theoretical pursuance of optimal capital structure

• as oppose to the mean-reversion empirical model

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 51

Risk Integration

• Structural models

– Two building blocks

– Degrees of endogeneity

– Applications

• Regulatory capital (Lehman case study)

• Liquidity pricing (bail out)

• MTM

• Free trader option

• Optimal capital structure

• Others ...

Standard

Model

Structure

52

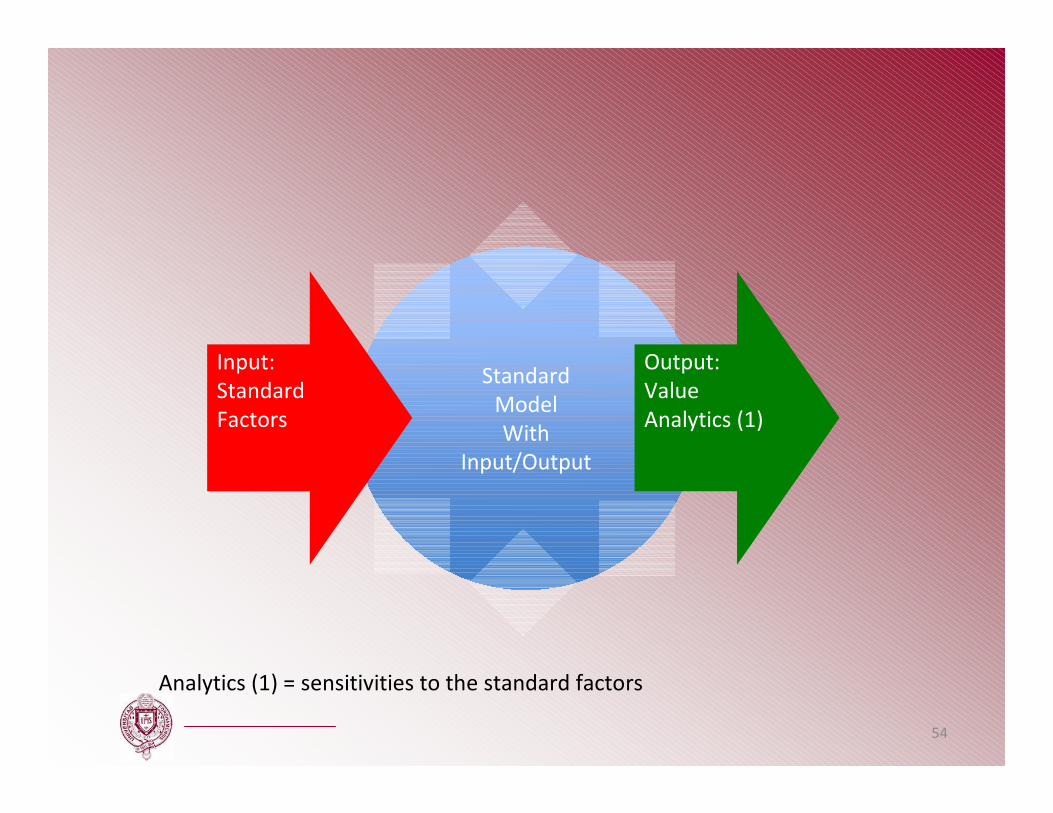

Standard

Model

With

Input/Output

53

Standard

Model

With

Input/Output

Input:

Standard

Factors

Output:

Value

Analytics (1)

Analytics (1) = sensitivities to the standard factors

54

Model

with

Ports for

Additional

Factors

Input:

Standard

Factors

Output:

Value

Analytics (1)

Analytics (1) = sensitivities to the standard factors

55

Model with

Additional Factor

Modules

“Plugged-in”

Input:

Standard

Factors

Output:

Value

Analytics (1)

Analytics (2)

F2

F1

F3

F5

F4 Fn

Analytics (1) = sensitivities to the standard factors

Analytics (2) = sensitivities to additional factors

Inputs for additional factor modules provided by the operator 56

Additional Factors

Imbedded

in the Model

Input:

Standard

Factors

Output:

Value

Analytics (1)

Analytics (2)

F2

F1

F3

F5

F4 Fn

Analytics (1) = sensitivities to the standard factors

Analytics (2) = sensitivities to additional factors

Inputs for additional factor parameters calculated within the model 57

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 58

Model Integration

• Problems with reduced-form models

– industry standards

– models are segmented

– models assume perfect market -- no longer true

• Example

– IR and credit are separated

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 59

Model Integration

• silos

– cannot model correlation properly

• What is the main core of modeling?

– what is a company?

– where do risks come from?

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 60

Reality to Plug-n-Play

Equity Credit

IR FX

Mortgage

...

Risk Neutral

Space Equity Credit

IR FX

Mortgage ...

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 61

IR Risk Considered

Risk Neutral

Space

IR

Forward

Measure Space Equity Credit

FX

Mortgage ...

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 62

Swap Risk Considered

Risk Neutral

Space

IR

Forward

Measure Space Swap Credit

FX

Equity ...

Swaption CMS

Swap related

derivatives

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 63

Credit Default Swap

Equity Credit

IR FX

Mortgage

...

Real World

Equilibrium

Measure

Equity Credit

IR FX

Mortgage Liquidity

Fundamentals Capital

Structure

Local

Economy

Global

Economy

FORDHAM UNIVERSITY

THE JESUIT UNIVERSITY OF NEW YORK

Dr. Ren-Raw Chen 64

Risk Integration

Equity Credit

IR FX

Mortgage

...

Risk

Neutral Equity Credit

IR FX

Fundamentals Capital

Structure

Local

Economy

Global

Economy

Real World

Equilibrium Mortgage Liquidity

![FORDHAM #3 of 3; Fordham v Hobson (Dewsash) (Home.B) [2013] NSWCTTT 590](https://img.pdfslide.us/doc/110x75/55cf29a9bb61ebb2668b4659/fordham-3-of-3-fordham-v-hobson-dewsash-homeb-2013-nswcttt-590.jpg)