Embed Size (px)

Citation preview

Reverse Mortgage Conversation Starter KitProvided by the HECM Advisors Group

Don Graves, RICP® , President - Chief Conversation StarterAdjunct Professor, Retirement Income - The American College of Financial Services

Voted One of the Top 11 Retirement Income Leaders to Read

HECM Advisors Group |The HECM Institute25 Washington Lane, 10A | Wyncote PA, 19095

Direct (215) 732-0814 | Mobile: (484) 442-0732 Toll-free/E-fax (800) [email protected] | www.HECMAdvisorsGroup.com

In the lead summit presentation, Don Graves discussed 4 ways to discover new leads that may be closer than you think: start with who you have, scratch where it itches, speak to their children, and set up a series of conversation starters. The questions below all pertain these 4 discovery methods.

o Power Question 1: Start with Who You Have/Scratch Where It Itches

What would retirement be like if you didn’t have to make a monthly mortgage payment?

This question is important because 50% or more of retiring Baby Boomers will be carrying some sort of mortgage/home equity loan payment into retirement. There are two possible responses to this question:

(a) They are comfortable making the monthly payments.

Question: If there were a way those monthly payments could be used to reduce your outstanding balance, while remaining accessible to you in a growing reserve account, would you be interested in learning how it works?

(b) They would enjoy not having to make the monthly payments.

Question: How would you use the dollars that you’re no longer spending on a mortgage payment?

Question: If there were a way to eliminate that monthly mortgage payment, so that you could do…would you want me to tell you about it?

o Power Question 2: Speak to Their Children

Do your parents currently own their home?

Are your parents 100 percent certain they’ll have a great retirement?

Some advisors have more interaction with the children (or grandchildren) of Boomers than they do with Boomers directly. The good news is that most children are aware of the financial concerns that their parents have. They hear them on holidays and at family gatherings and during telephone conversations. Using the 2 questions above will create curiosity and open new opportunities to engage with Boomers.

Question: If there were a proven resource that allowed your parents to create cash flow, preserve their assets, reduce risks, and even add new money back into their savings, do you think they’d be open to hearing more?

Conversation StartersPresentation by Don Graves 4 ways to discover new leads

C O N V E R S A T I O N S T A R T E R S

The following four articleswere compiled by leading financial thought leaders and are designed to provide an educational overview of how the newly restructured Home Equity Conversion Mortgage (Reverse Mortgage) is being used in retirement income planning.

ocial Security benefits represent the largest

retirement income asset for most Americans, supplying roughly two-thirds of retirees with more than half of their retirement income, according the Employee Benefits Research Institute (EBRI). For many Americans, what they have saved for retirement will prove to be inadequate, especially if one of their most valuable assets is ignored. “Few people consider monetizing their housing wealth, yet home equity is often between 60 and 70 percent of their net worth according to the U.S. Census Bureau.

This asset is hiding in plain sight, an asset that retirees have been saving for via regular mortgage payments throughout their lives, but is virtually invisible when clients enter the decumulation phase. For much of middle America, it is like trying to retire on just 35 percent, or less, of their accumulated wealth,” stated Shelley Giordano, Chair of the Funding Longevity Task Force at the American College of Financial Services. Recent research led by the Task Force demonstrates that, despite playing a lesser role

in the retirement income story, home equity can be a significant resource. Including a discussion of the housing asset is an appropriate component in careful retirement income planning.

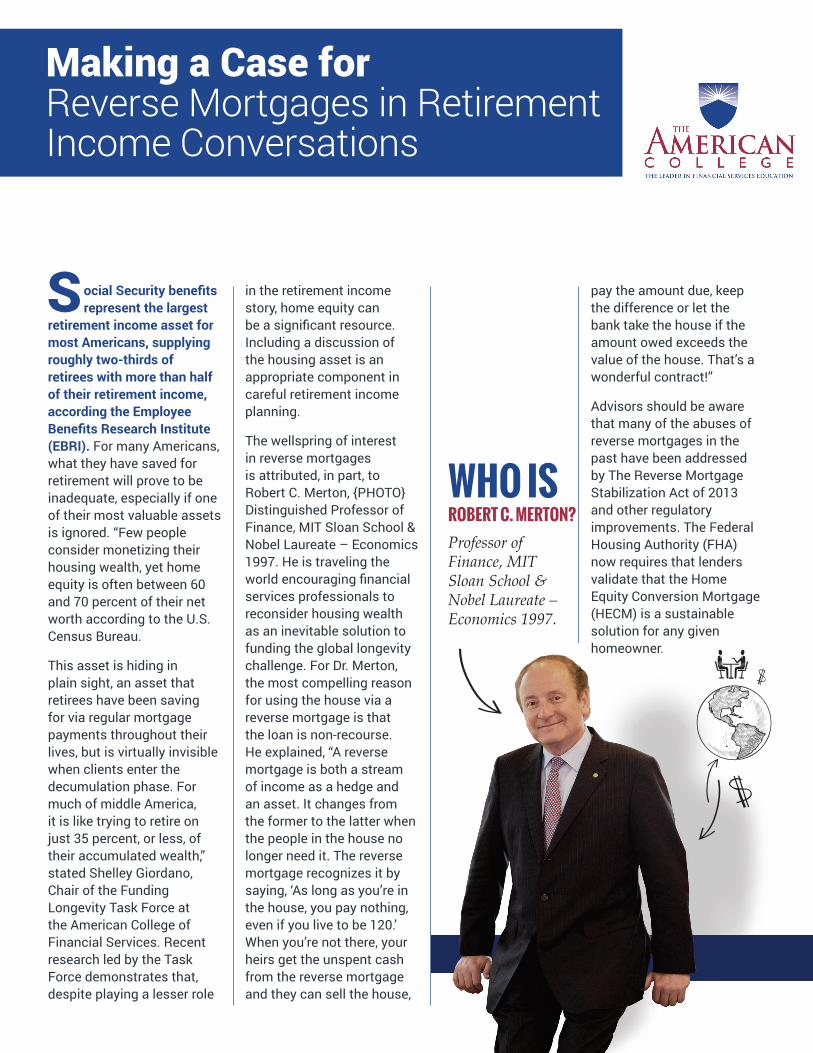

The wellspring of interest in reverse mortgages is attributed, in part, to Robert C. Merton, {PHOTO} Distinguished Professor of Finance, MIT Sloan School & Nobel Laureate – Economics 1997. He is traveling the world encouraging financial services professionals to reconsider housing wealth as an inevitable solution to funding the global longevity challenge. For Dr. Merton, the most compelling reason for using the house via a reverse mortgage is that the loan is non-recourse. He explained, “A reverse mortgage is both a stream of income as a hedge and an asset. It changes from the former to the latter when the people in the house no longer need it. The reverse mortgage recognizes it by saying, ‘As long as you’re in the house, you pay nothing, even if you live to be 120.’ When you’re not there, your heirs get the unspent cash from the reverse mortgage and they can sell the house,

Making a Case for Reverse Mortgages in RetirementIncome Conversations

pay the amount due, keep the difference or let the bank take the house if the amount owed exceeds the value of the house. That’s a wonderful contract!”

Advisors should be aware that many of the abuses of reverse mortgages in the past have been addressed by The Reverse Mortgage Stabilization Act of 2013 and other regulatory improvements. The Federal Housing Authority (FHA) now requires that lenders validate that the Home Equity Conversion Mortgage (HECM) is a sustainable solution for any given homeowner.

S

WHO IS ROBERT C. MERTON?Professor of Finance, MIT Sloan School & Nobel Laureate – Economics 1997.

In an interview with The American College of Financial Services, Donald Graves, RICP®, of the HECM Advisors Group and president of the HECM Institute, discussed several ways to support retirement income strategies with a reverse mortgage, specifically, a reverse mortgage line of credit.

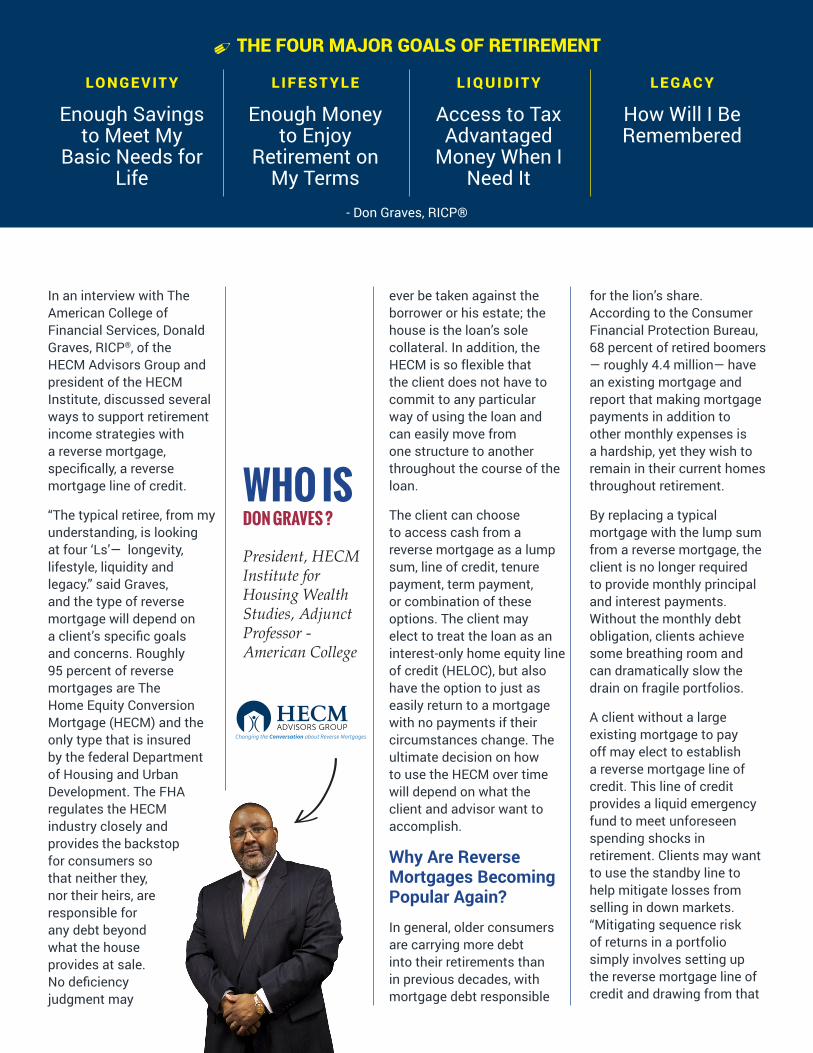

“The typical retiree, from my understanding, is looking at four ‘Ls’— longevity, lifestyle, liquidity and legacy.” said Graves, and the type of reverse mortgage will depend on a client’s specific goals and concerns. Roughly 95 percent of reverse mortgages are The Home Equity Conversion Mortgage (HECM) and the only type that is insured by the federal Department of Housing and Urban Development. The FHA regulates the HECM industry closely and provides the backstop for consumers so that neither they, nor their heirs, are responsible for any debt beyond what the house provides at sale. No deficiency judgment may

LO N G E V IT Y

Enough Savings to Meet My

Basic Needs for Life

L I F E S T Y L E

Enough Money to Enjoy

Retirement on My Terms

L I Q U I D IT Y

Access to Tax Advantaged

Money When I Need It

L E G AC Y

How Will I Be Remembered

0 THE FOUR MAJOR GOALS OF RETIREMENT

ever be taken against the borrower or his estate; the house is the loan’s sole collateral. In addition, the HECM is so flexible that the client does not have to commit to any particular way of using the loan and can easily move from one structure to another throughout the course of the loan.

The client can choose to access cash from a reverse mortgage as a lump sum, line of credit, tenure payment, term payment, or combination of these options. The client may elect to treat the loan as an interest-only home equity line of credit (HELOC), but also have the option to just as easily return to a mortgage with no payments if their circumstances change. The ultimate decision on how to use the HECM over time will depend on what the client and advisor want to accomplish.

Why Are Reverse Mortgages Becoming Popular Again?

In general, older consumers are carrying more debt into their retirements than in previous decades, with mortgage debt responsible

for the lion’s share. According to the Consumer Financial Protection Bureau, 68 percent of retired boomers — roughly 4.4 million— have an existing mortgage and report that making mortgage payments in addition to other monthly expenses is a hardship, yet they wish to remain in their current homes throughout retirement.

By replacing a typical mortgage with the lump sum from a reverse mortgage, the client is no longer required to provide monthly principal and interest payments. Without the monthly debt obligation, clients achieve some breathing room and can dramatically slow the drain on fragile portfolios.

A client without a large existing mortgage to pay off may elect to establish a reverse mortgage line of credit. This line of credit provides a liquid emergency fund to meet unforeseen spending shocks in retirement. Clients may want to use the standby line to help mitigate losses from selling in down markets. “Mitigating sequence risk of returns in a portfolio simply involves setting up the reverse mortgage line of credit and drawing from that

WHO IS DON GRAVES ?

President, HECM Institute for Housing Wealth Studies, Adjunct Professor - American College

- Don Graves, RICP®

if the preceding year is flat or negative,” explained Graves. In addition to increasing longevity of a client’s retirement assets, removing the need to spend assets during a market downturn can increase satisfaction in retirement.

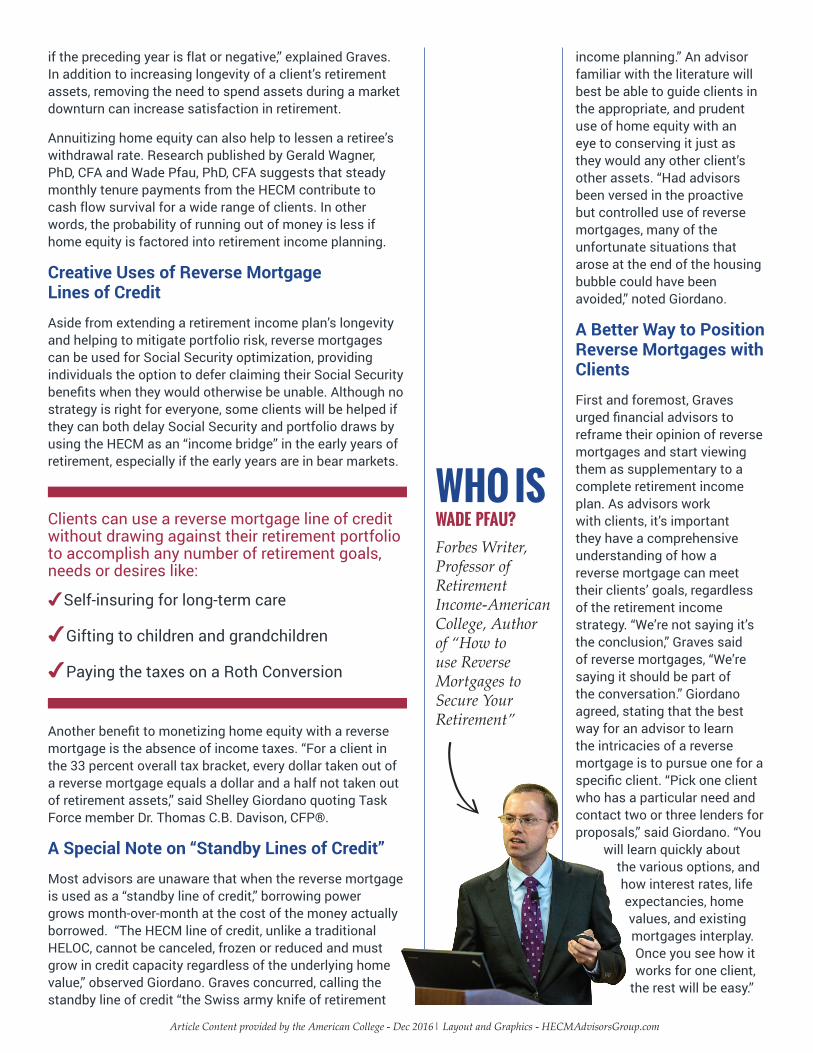

Annuitizing home equity can also help to lessen a retiree’s withdrawal rate. Research published by Gerald Wagner, PhD, CFA and Wade Pfau, PhD, CFA suggests that steady monthly tenure payments from the HECM contribute to cash flow survival for a wide range of clients. In other words, the probability of running out of money is less if home equity is factored into retirement income planning.

Creative Uses of Reverse Mortgage Lines of Credit

Aside from extending a retirement income plan’s longevity and helping to mitigate portfolio risk, reverse mortgages can be used for Social Security optimization, providing individuals the option to defer claiming their Social Security benefits when they would otherwise be unable. Although no strategy is right for everyone, some clients will be helped if they can both delay Social Security and portfolio draws by using the HECM as an “income bridge” in the early years of retirement, especially if the early years are in bear markets.

Clients can use a reverse mortgage line of credit without drawing against their retirement portfolio to accomplish any number of retirement goals, needs or desires like:

4Self-insuring for long-term care

4 Gifting to children and grandchildren

4 Paying the taxes on a Roth Conversion

Another benefit to monetizing home equity with a reverse mortgage is the absence of income taxes. “For a client in the 33 percent overall tax bracket, every dollar taken out of a reverse mortgage equals a dollar and a half not taken out of retirement assets,” said Shelley Giordano quoting Task Force member Dr. Thomas C.B. Davison, CFP®.

A Special Note on “Standby Lines of Credit”

Most advisors are unaware that when the reverse mortgage is used as a “standby line of credit,” borrowing power grows month-over-month at the cost of the money actually borrowed. “The HECM line of credit, unlike a traditional HELOC, cannot be canceled, frozen or reduced and must grow in credit capacity regardless of the underlying home value,” observed Giordano. Graves concurred, calling the standby line of credit “the Swiss army knife of retirement

income planning.” An advisor familiar with the literature will best be able to guide clients in the appropriate, and prudent use of home equity with an eye to conserving it just as they would any other client’s other assets. “Had advisors been versed in the proactive but controlled use of reverse mortgages, many of the unfortunate situations that arose at the end of the housing bubble could have been avoided,” noted Giordano.

A Better Way to Position Reverse Mortgages with Clients

First and foremost, Graves urged financial advisors to reframe their opinion of reverse mortgages and start viewing them as supplementary to a complete retirement income plan. As advisors work with clients, it’s important they have a comprehensive understanding of how a reverse mortgage can meet their clients’ goals, regardless of the retirement income strategy. “We’re not saying it’s the conclusion,” Graves said of reverse mortgages, “We’re saying it should be part of the conversation.” Giordano agreed, stating that the best way for an advisor to learn the intricacies of a reverse mortgage is to pursue one for a specific client. “Pick one client who has a particular need and contact two or three lenders for proposals,” said Giordano. “You

will learn quickly about the various options, and how interest rates, life expectancies, home values, and existing mortgages interplay. Once you see how it works for one client,

the rest will be easy.”

WHO IS WADE PFAU?Forbes Writer, Professor of Retirement Income-American College, Author of “How to use Reverse Mortgages to Secure Your Retirement”

Article Content provided by the American College - Dec 2016| Layout and Graphics - HECMAdvisorsGroup.com

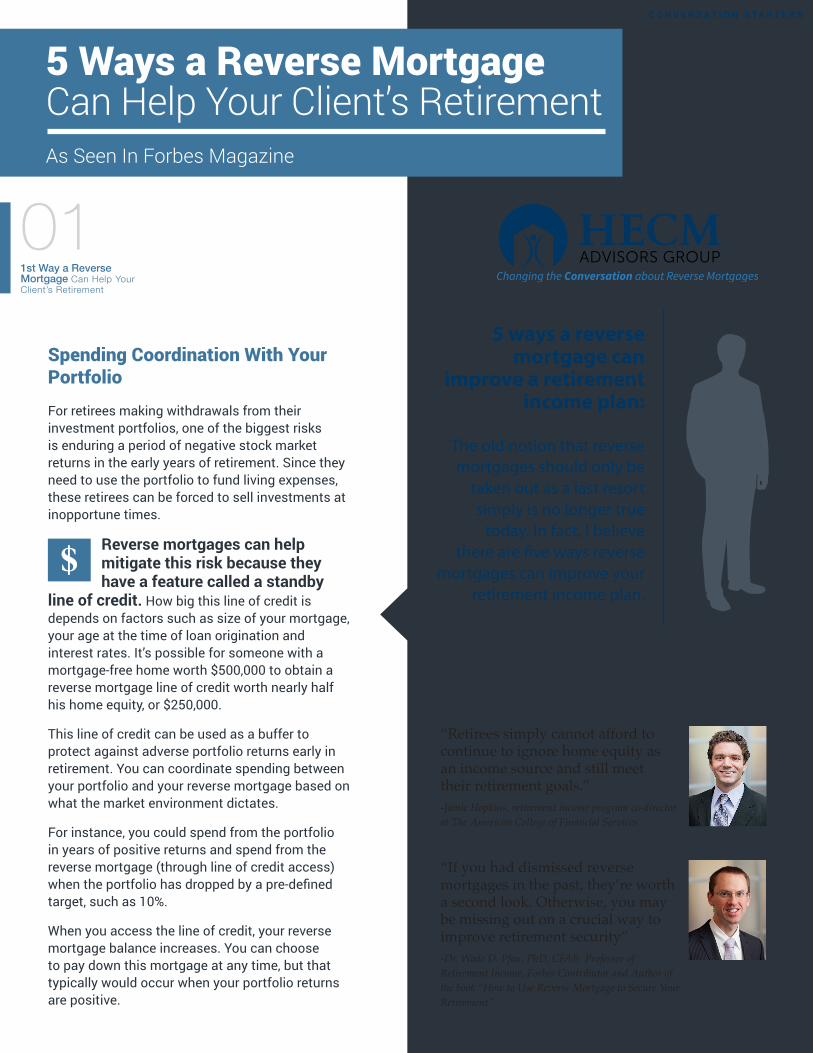

Spending Coordination With Your Portfolio

For retirees making withdrawals from their investment portfolios, one of the biggest risks is enduring a period of negative stock market returns in the early years of retirement. Since they need to use the portfolio to fund living expenses, these retirees can be forced to sell investments at inopportune times.

Reverse mortgages can help mitigate this risk because they have a feature called a standby

line of credit. How big this line of credit is depends on factors such as size of your mortgage, your age at the time of loan origination and interest rates. It’s possible for someone with a mortgage-free home worth $500,000 to obtain a reverse mortgage line of credit worth nearly half his home equity, or $250,000.

This line of credit can be used as a buffer to protect against adverse portfolio returns early in retirement. You can coordinate spending between your portfolio and your reverse mortgage based on what the market environment dictates.

For instance, you could spend from the portfolio in years of positive returns and spend from the reverse mortgage (through line of credit access) when the portfolio has dropped by a pre-defined target, such as 10%.

When you access the line of credit, your reverse mortgage balance increases. You can choose to pay down this mortgage at any time, but that typically would occur when your portfolio returns are positive.

5 ways a reverse mortgage can

improve a retirement income plan:

The old notion that reverse mortgages should only be

taken out as a last resort simply is no longer true

today. In fact, I believe there are five ways reverse

mortgages can improve your retirement income plan.

011st Way a Reverse Mortgage Can Help Your Client’s Retirement

5 Ways a Reverse Mortgage Can Help Your Client’s RetirementAs Seen In Forbes Magazine

“Retirees simply cannot afford to continue to ignore home equity as an income source and still meet their retirement goals.”-Jamie Hopkins, retirement income program co-director at The American College of Financial Services

“If you had dismissed reverse mortgages in the past, they’re worth a second look. Otherwise, you may be missing out on a crucial way to improve retirement security”-Dr. Wade D. Pfau, PhD, CFA® Professor of Retirement Income, Forbes Contributor and Author of the book “How to Use Reverse Mortgage to Secure Your Retirement”

C O N V E R S A T I O N S T A R T E R S

022nd Way a Reverse Mortgage Can Help Your Client’s Retirement

Bridge Income for Delaying Social Security Benefits

Many financial planners recommend clients delay claiming Social Security benefits for as long as possible, up to age 70. That’s because benefits increase roughly 6 to 8% per

year for delaying claiming between ages 62 and 70.

Social Security benefits can be claimed as early as age 62, though, leaving someone a potential eight-year window without a stable source of non-portfolio income. Setting up a reverse mortgage with a term payout that lasts eight years is one idea to consider in this scenario. It can produce a “bridge” income to replace all or a portion of the income

Social Security would have provided.

MONTHLY BENEFIT AMOUNTS DIFFER BASED ON THE AGE YOU DECIDE TO START RECEIVING BENEFITS

MO

NT

HLY

BE

NE

FIT

AM

OU

NT

AGE YOU CHOOSE TO START RECEIVING

$1,500

$1,200

$900

$600

$300

$0

62 63 64 65 66 67 68 69 70

$750 $8

00

$866 $9

33

$1,0

80

$1,1

60

$1,2

40

$1,3

20

This example

assumes a benefit

of $1,000 at a full

retirement age of

66

“Today’s retiree needs every legitimate tool available to meet their retirement goals. Historically, the more affluent have either simply dismissed the reverse mortgage or relegated them to use as a last resort. However, as we have seen,

much has changed in the last few years. The strategic use of reverse mortgages have now been proven to be able to dramatically improve retirement outcomes.”-Don Graves, RICP®, President – HECM Advisors Group, Adjunct Professor – The American College

“..researchers believe reverse mortgages could solve some of the income challenges of retirees who saved too little to finance a retirement that could last decades” - Mary Beth Franklin, CFP® syndicated columnist, author contributing editor at InvestmentNews

“Reverse mortgages can help seniors manage their finances if used responsibly. They come with costs and risks. We urge homeowners thinking about reverse mortgages to make informed decisions and carefully weigh all of their options before proceeding”- Financial Regulatory Agency {FINRA 2014}

033rd Way a Reverse Mortgage Can Help Your Client’s Retirement

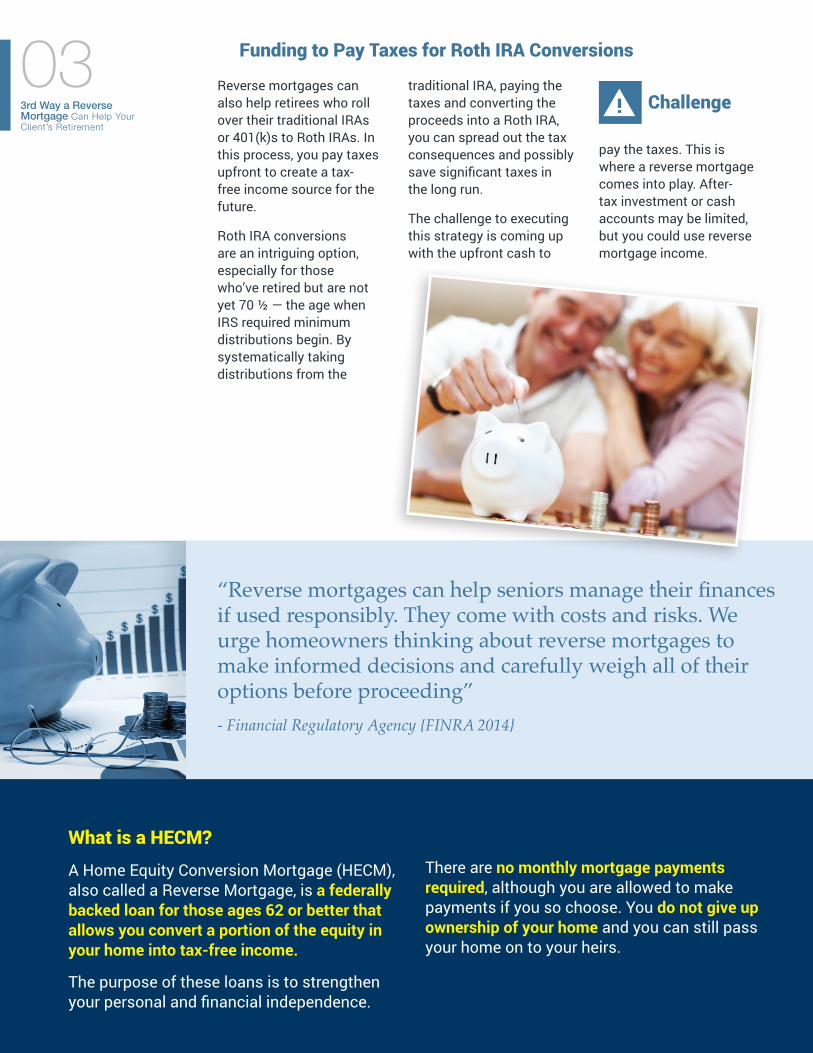

Reverse mortgages can also help retirees who roll over their traditional IRAs or 401(k)s to Roth IRAs. In this process, you pay taxes upfront to create a tax-free income source for the future.

Roth IRA conversions are an intriguing option, especially for those who’ve retired but are not yet 70 ½ — the age when IRS required minimum distributions begin. By systematically taking distributions from the

traditional IRA, paying the taxes and converting the proceeds into a Roth IRA, you can spread out the tax consequences and possibly save significant taxes in the long run.

The challenge to executing this strategy is coming up with the upfront cash to

pay the taxes. This is where a reverse mortgage comes into play. After-tax investment or cash accounts may be limited, but you could use reverse mortgage income.

Funding to Pay Taxes for Roth IRA Conversions

Challenge!

What is a HECM?

A Home Equity Conversion Mortgage (HECM), also called a Reverse Mortgage, is a federally backed loan for those ages 62 or better that allows you convert a portion of the equity in your home into tax-free income.

The purpose of these loans is to strengthen your personal and financial independence.

There are no monthly mortgage payments required, although you are allowed to make payments if you so choose. You do not give up ownership of your home and you can still pass your home on to your heirs.

The HECM Advisors Group is an education and training resource for advisors, whose primary conviction is that Housing Wealth must be considered when doing comprehensive financial planning.

By no means do we suggest that a Reverse Mortgage is right for every client, but we do advocate (as well as the most recent academic data supports) the importance of including it as part of the

retirement planning conversation.

Article’s original content was provided by Neil Krishnaswamy, CFP®, RICP®, EA and used by permission

©2016 HECMAdvisorsGroup.com 1-800-762-6315

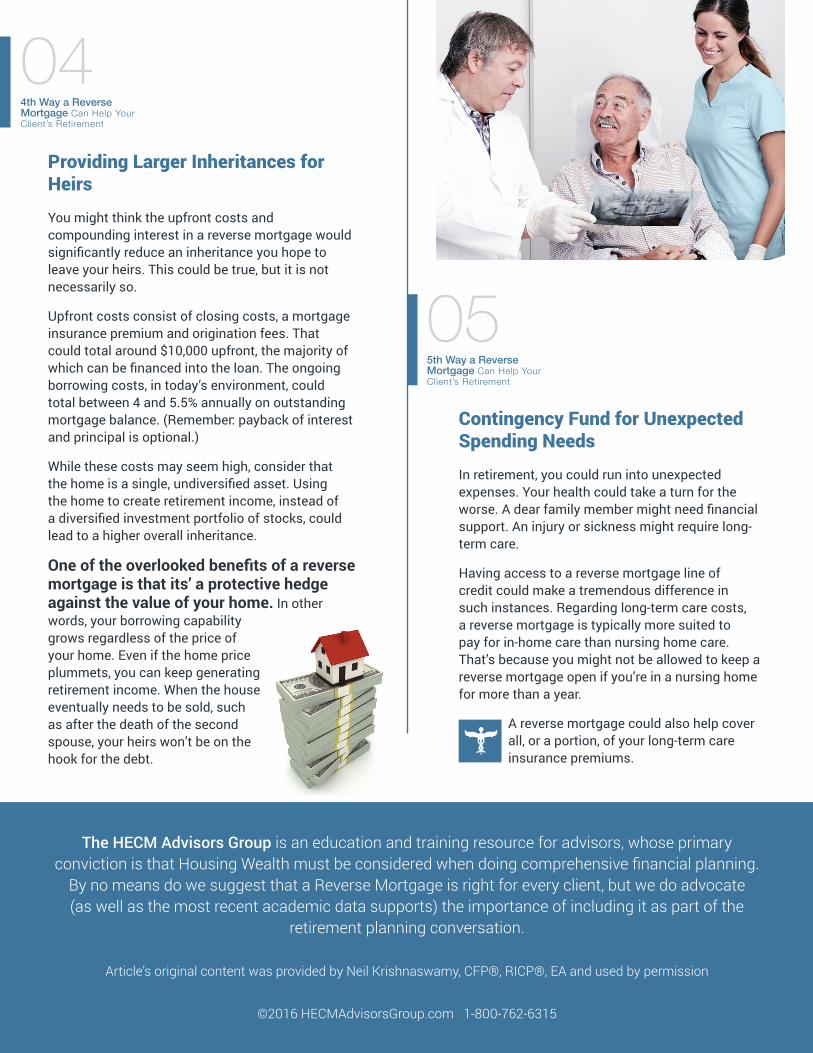

Contingency Fund for Unexpected Spending Needs

In retirement, you could run into unexpected expenses. Your health could take a turn for the worse. A dear family member might need financial support. An injury or sickness might require long-term care.

Having access to a reverse mortgage line of credit could make a tremendous difference in such instances. Regarding long-term care costs, a reverse mortgage is typically more suited to pay for in-home care than nursing home care. That’s because you might not be allowed to keep a reverse mortgage open if you’re in a nursing home for more than a year.

A reverse mortgage could also help cover all, or a portion, of your long-term care insurance premiums.

Providing Larger Inheritances for Heirs

You might think the upfront costs and compounding interest in a reverse mortgage would significantly reduce an inheritance you hope to leave your heirs. This could be true, but it is not necessarily so.

Upfront costs consist of closing costs, a mortgage insurance premium and origination fees. That could total around $10,000 upfront, the majority of which can be financed into the loan. The ongoing borrowing costs, in today’s environment, could total between 4 and 5.5% annually on outstanding mortgage balance. (Remember: payback of interest and principal is optional.)

While these costs may seem high, consider that the home is a single, undiversified asset. Using the home to create retirement income, instead of a diversified investment portfolio of stocks, could lead to a higher overall inheritance.

One of the overlooked benefits of a reverse mortgage is that its’ a protective hedge against the value of your home. In other words, your borrowing capability grows regardless of the price of your home. Even if the home price plummets, you can keep generating retirement income. When the house eventually needs to be sold, such as after the death of the second spouse, your heirs won’t be on the hook for the debt.

044th Way a Reverse Mortgage Can Help Your Client’s Retirement

055th Way a Reverse Mortgage Can Help Your Client’s Retirement

Reverse mortgages allow homeowners age 62 or better to convert the equity in their primary residence into a liquid, tax-free asset.

Borrowers can take their money in a lump sum, a monthly payment or set up a line of credit. Interest accrues only on the borrowed funds and the unused portion of line of credit continues to grow at the same compounded interest rate as the loan.

o Pay Off an Existing Mortgage

Using a lump sum from a reverse mortgage to pay off a traditional mortgage balance instantly increases a retiree’s monthly cash flow and reduces portfolio withdrawal needs. “It really improves the odds for retirement success to not carry a mortgage into retirement,” said Wade Pfau, Professor of Retirement Income at The American College of Financial Services.

o Replace a Home Equity Line of Credit

Unlike a HELOC, a reverse mortgage line of credit can never be reduced, frozen or cancelled. There are no monthly loan repayment requirements. A reverse mortgage is not due until the borrowers sell the home, move out permanently or die. The estate or heirs can never owe more than the house is worth, even if it is less than the amount borrowed. The Reverse Mortgage line of credit has a built in guaranteed growth factor.

o Pay it Off and Pay it Down

Eliminating a mandatory monthly mortgage payment by getting a reverse mortgage can be a huge relief for many. But one little known strategy is to continue making a monthly mortgage payment on a new reverse mortgage. For every dollar you pay, the outstanding balance goes down, but the available line of credit goes up. This, in essence, means you are creating a type of deferred income annuity for the future. With no payment required, you can create financial flexibility month by month.

o Protect Your Portfolio

Should your portfolio decline significantly in value, borrow from the line of credit for your needs, then repay the loan when your portfolio recovers,” said John Salter, Associate Professor of Personal Financial Planning at Texas Tech University. Interest payments are tax-deductible, if retirees itemize their deductions on their income tax returns.

12 Smart, Savvy and Surprising Waysto Use a Reverse MortgageAs Seen in InvestmentNews

“Financial advisers who

dismissed reverse mortgages in the

past may want to take a second

look. Leading researchers

believe reverse mortgages could

solve some of the income challenges of retirees who

saved too little to finance a retirement

that could last decades”

- Mary Beth Franklin, CFP® syndicated columnist, author

contributing editor at InvestmentNews

C O N V E R S A T I O N S T A R T E R S

o Fund Future Long-Term Care or Income Needs

A 62-year-old couple with no long-term-care insurance may want to set up a reverse mortgage line of credit. With a home worth $625,000, their initial line of credit at current interest rates would be worth $327,375. Left untouched, the equity line would be worth $613,365 in 10 years and $1,149,143 in 20 years. The couple could tap the loan for future long-term care costs, as long as they remained in their home, or to serve as a deferred annuity if they needed additional income in the future.

o Create a Social Security Bridge

Supplement income with monthly payments from a reverse mortgage either for a set number of years (term) or for as long as you live in your home (tenure). Term payments can provide an income bridge to allow a retiree to delay claiming Social Security until benefits are worth the maximum amount at age 70.

o Manage Taxes

Proceeds from a reverse mortgage are tax-free. Tapping a reverse mortgage can decrease withdrawals from taxable retirement accounts, reducing income taxes and the amount of Social Security benefits subject to income taxes. For higher-income retirees, tax-free reverse mortgage payments can reduce their modified adjusted gross income that can trigger higher monthly Medicare premiums.

o Pay Roth Conversion Taxes

Sometimes the only thing preventing a retiree from converting a traditional retirement account to a Roth IRA is the amount of income taxes owed on the converted amount. Tax-free proceeds from a reverse mortgage can pay Roth conversion taxes all at once or over several years, reducing future income taxes and possibly reducing future Medicare premiums.

o Buy a New Home

A reverse mortgage can be used to purchase a new home. Rather than using all of the proceeds from a home sale, downsizers can use some of the sale profits and take out a reverse mortgage to make up the balance. This results in a new home without monthly payments and additional cash to add to savings for future needs or to supplement current income.

o Gray Divorce Strategy

Older couples can use a reverse mortgage to divide a marital housing asset in a divorce. In one scenario, the spouse remaining in the home can take a lump sum distribution from a reverse mortgage to buy out the other spouse. In a second scenario, the marital home can be sold and each ex-spouse can use some of the proceeds from the home sale. Subsequently, each of them can get a reverse mortgage to buy their respective new homes.

o Leave a Legacy Now

Most retirees have some desire to pass on a financial legacy to their heirs. According to the student loan giant Sallie Mae, the cost of higher education continues to grow, as well as increased reliability on family contributions just to keep up. However, in order to maintain and remain viable in this economy, a College education has become a necessity for most. A Reverse Mortgage could allow a grandparent to assist with small monthly tuition stipend, a gift or even a low or no interest loan to their grandchildren.

o Get More Out of the Month

Many retirees have a budget that is designed to sustain them over the long haul, but sometimes leaves something lacking month by month. Converting the reverse mortgage into a monthly payment can accomplish two things.

(1) It may reduce the amount drawn from savings therefore allowing them to last longer or

(2) It could increase the amount that they can spend monthly giving them more enjoyment.

The HECM Advisors Group is an education and training resource for advisors, whose primary conviction is that Housing Wealth must be considered when doing comprehensive financial planning.

By no means do we suggest that a Reverse Mortgage is right for every client, but we do advocate (as well as the most recent academic data supports) the importance of including it as part of the

retirement planning conversation.

Some Excerpts used are from an Investment News Article by Mary Beth Franklin.

©2016 HECMAdvisorsGroup.com 1-800-762-6315

25 Ways to Use a Reverse MortgageA Few Ideas for Advisors and Their Clients

C O N V E R S A T I O N S T A R T E R S

Reverse Mortgages allow homeowners age 62 or better to convert the equity in their primary residence into a liquid, tax-free asset.

o Pay off your forward mortgage to reduce your monthly expenses.

o Re-model your home to accommodate aging limitations.

o Maintain a line of credit (that grows) for health emergencies and surprises.

o Cover monthly expenses and hold on to other assets while their value continues to grow.

o Cover monthly expenses and avoid selling assets at depressed values.

o Pay for health insurance during early retirement years until Medicare eligible at 65.

o Pay your Medicare Part B and Part D costs.

o Combine life tenure payments with Social Security and income generated by assets to replace your salary and maintain your monthly routine of paying bills from new income.

o Pay for your children’s or grandchildren’s college or professional education.

o Maintain a “standby” cash reserve to get you through the ups and downs of investment markets and give you more flexibility

o Combine proceeds with sale of one home to buy a new home without a forward mortgage and monthly mortgage payments.

o Pay for long-term care needs

o Fill the gap in a retirement plan caused by lower than expected returns on your assets.

o Pay for short term in-home care or physical therapy following an accident or medical episode.

o Pay for a retirement plan, estate plan or a will.

o Convert a room or basement to a living facility for an aging parent, relative or caregiver.

o Set up transportation arrangements for when you are no longer comfortable driving.

o Create a set aside to pay real estate taxes and property insurance.

o Delay collecting Social Security benefit until it maxes out at age 70.

o Eliminate credit card debt and avoid building new credit debt.

o Cover monthly expenses in between jobs or during career transition without utilizing other saved assets.

o Cover expenses and avoid capital gains tax consequences of selling off other assets.

o Purchase health-related technology that enables you to live in home alone.

o Pay for an Uber or Lyft account so you have mobility and access to appointments and social activities.

o Help your adult children through family emergencies.

© 2016 HECMAdvisorsGroup.com 1-800-72-6315