Embed Size (px)

Citation preview

OCCASIONAL PAPER 180

Revenue Implications ofTrade Liberalization

Liam Ebrill, Janet Stotsky, and Reint Gropp

INTERNATIONAL MONETARY FUNDWashington DC

1999

©International Monetary Fund. Not for Redistribution

© 1999 International Monetary Fund

Production: IMF Graphics SectionTypesetting: Choon Lee

Figures: In-Ok Yoon

Library of Congress Cataloging-in-Publication Data

Ebrill, Liam P.Revenue implications of trade liberalization / Liam Ebrill, Janet

Stotsky, and Reint Gropp.p. cm.— (Occasional paper, ISSN 0251-6365 ; no. 180)

Includes bibliographical references.ISBN 1-55775-813-1 (alk. paper)

1. Revenue—Econometric models. 2. Free trade—Econometric models.3. International trade—Econometric models. I. Stotsky, Janet Gale.II. Gropp, Reint. III. Series: Occasional paper (International MonetaryFund) ; no. 180.HJ2305.E24 1999336.02—dc21 99-30339

CIP

Price: US$18.00(US$15.00 to full-time faculty members and

students at universities and colleges)

Please send orders to:International Monetary Fund, Publication Services

700 19th Street, N.W., Washington, D.C. 20431, U.S.A.Tel: (202) 623-7430 Telefax: (202) 623-7201

E-mail: [email protected]: http://www.imf.org

recycled paper

©International Monetary Fund. Not for Redistribution

Contents

Page

Prfeface v

I Introduction I

II Potential Revenue Implications of Trade Reform 3Reform of Quantitative Restrictions 3Tariff Reform 4Reduction of Export Taxes 6Development of Regional Trade Arrangements 6Revenue Implications of the Indirect and Interactive Effects

of Liberalization 6Conclusions 7

III Analysis of Trade Liberalization and Revenue Developments 9

Trade Liberalization Strategies and Revenue Implications:A Comparative Analysis 9

Trade Liberalization and Revenue Trends 13Econometric Analysis 15

IV Conclusions 26

Appendices

I Summary Measures for the Countries in theComparative Analysis 27

II Collected Tariff Rates and Tariff Revenue for Selected Countries 34

References 39

BoxesII 1. Efficiency Gains from Trade Liberalization and

the Budget Constraint 42. Best Practices 8

III 3. Trade Liberalization in Small, Open Economies 15

Tables

Section

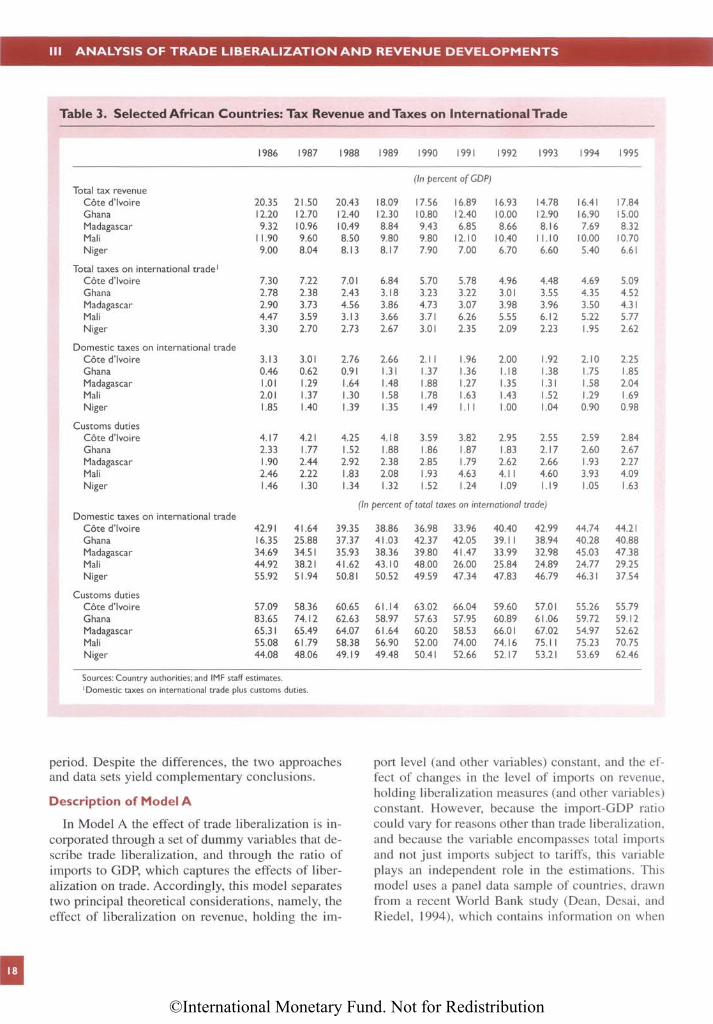

III 1. Collected Tariff Rates by World Region 142. Taxes on International Trade by World Region 163. Selected African Countries: Tax Revenue and Taxes

on International Trade 18

iii

©International Monetary Fund. Not for Redistribution

CONTENTS

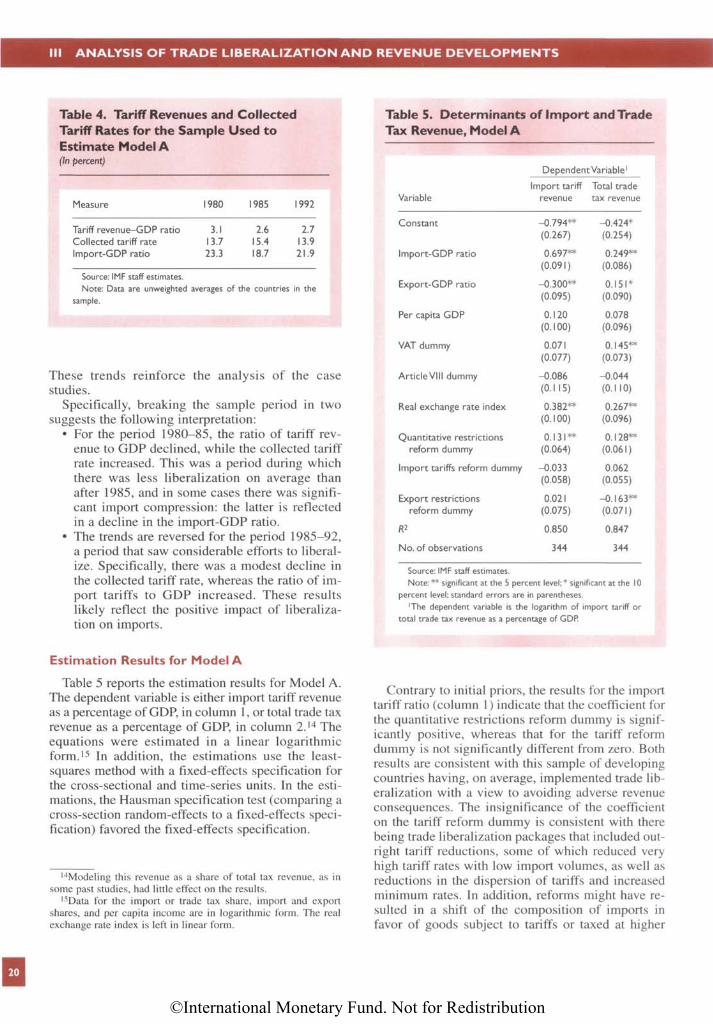

4. Tariff Revenue and Collected Tariff Rates for the SampleUsed to Estimate Model A 20

5. Determinants of Import and Trade Tax Revenue, Model A 206. Results of the Instrumental Variable Approach, Model B 237. Results of the Regional Instrumental Variable Approach, Model B 24

Appendix

I 8. Argentina: Summary Measures of Economic Performanceand Revenue Trends 28

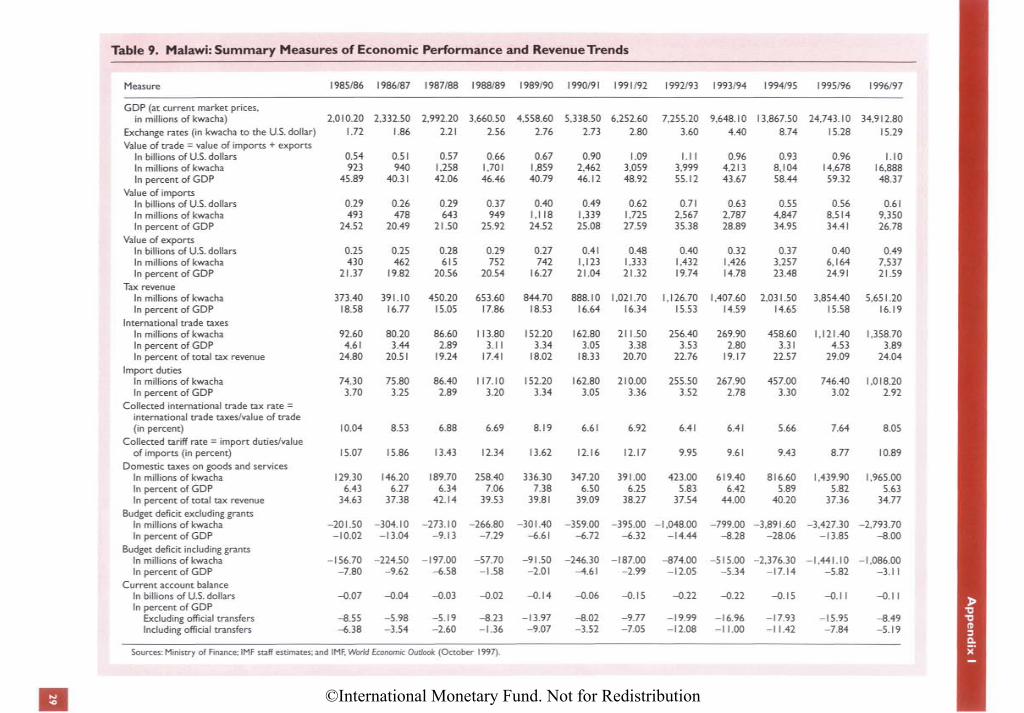

9. Malawi: Summary Measures of Economic Performanceand Revenue Trends 29

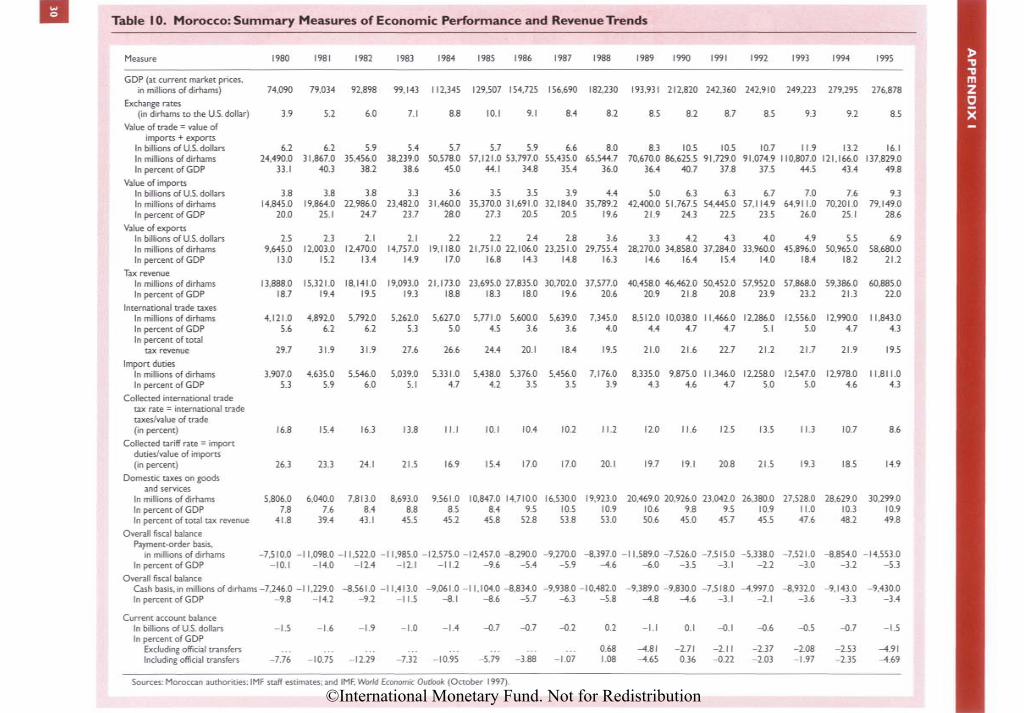

10. Morocco: Summary Measures of Economic Performanceand Revenue Trends 30

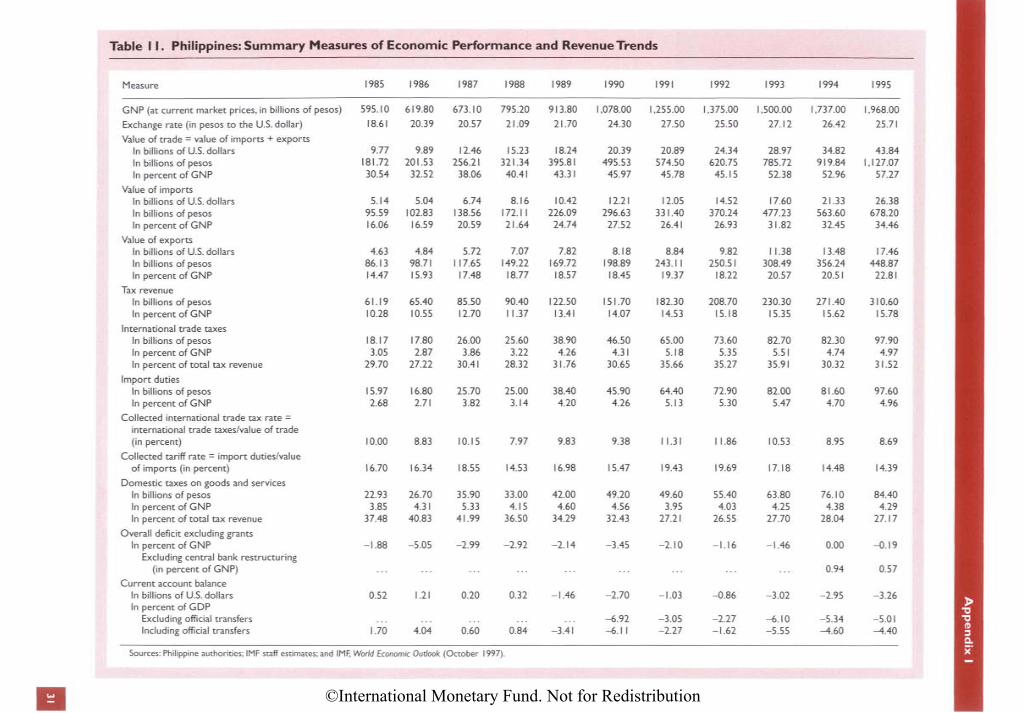

11. Philippines: Summary Measures of Economic Performanceand Revenue Trends 31

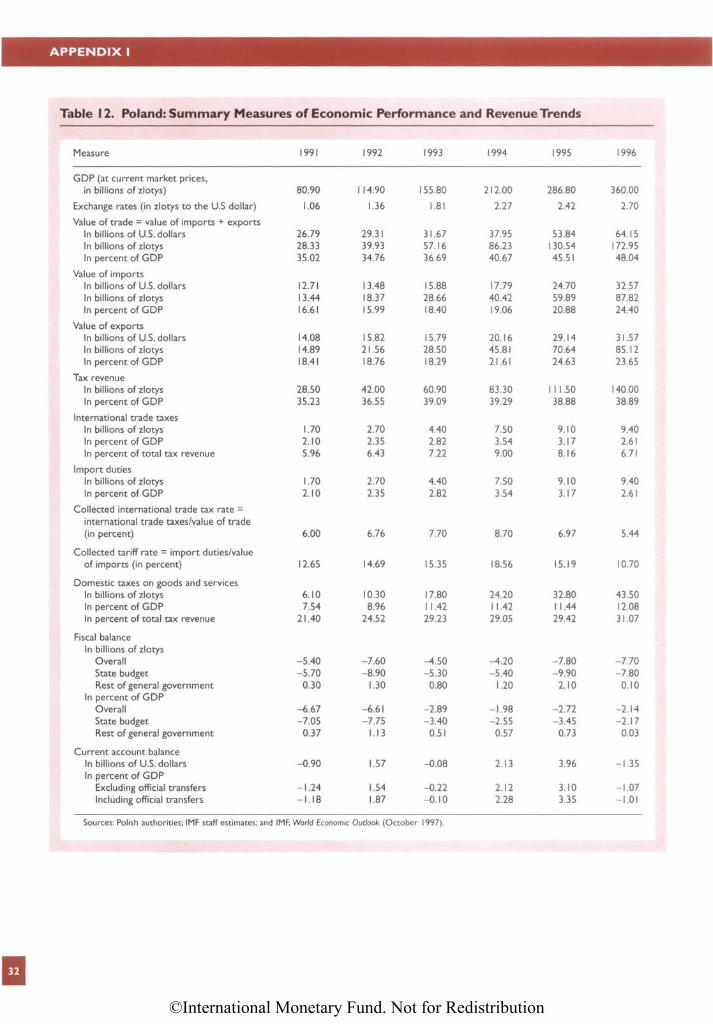

12. Poland: Summary Measures of Economic Performance andRevenue Trends 32

13. Senegal: Summary Measures of Economic Performance andRevenue Trends 33

II 14. Selected Countries: Collected Tariff Rates 3415. Selected Countries: Tariff Revenue 3616. Countries Included in the Sample for Model A 38

Figures

I 1. Taxes on International Trade by World Region 2III 2. Selected African Countries: Trends in Collected Tariff Rates

and Tariff Revenue-GDP Ratios 17

The following symbols have been used throughout this paper:

. . . to indicate that data are not available;

n.a. to indicate not applicable;— to indicate that the figure is zero or less than half the final digit shown, or that the item

does not exist;- between years or months (e.g., 1994-95 or January-June) to indicate the years or months

covered, including the beginning and ending years or months;/ between years (e.g., 1994/95) to indicate a crop or fiscal (financial) year."Billion" means a thousand million.Minor discrepancies between constituent figures and totals are due to rounding.The term "country," as used in this paper, does not in all cases refer to a territorial entity thatis a state as understood by international law and practice; the term also covers some territo-rial entities that are not states, but for which statistical data are maintained and providedinternationally on a separate and independent basis.

iv

©International Monetary Fund. Not for Redistribution

Preface

A recent Occasional Paper by the staff of the Fiscal Affairs Department of the IMFtitled Fiscal Reforms in Low-Income Countries: Experience Under IMF-SupportedPrograms observed that some countries with Structural Adjustment Facility (SAF)and Enhanced Structural Adjustment Facility (ESAF) programs with the IMF had tar-geted an increased reliance on revenue from international trade taxes or, in any event,had attained higher ratios of international trade taxes to GDP at the end of theSAF/ESAF-supported adjustment period. This had occurred despite the countries' ap-parent commitment to trade liberalization. More generally, for many developingcountries, taxes on international trade are still a significant source of revenue.Whereas export tax revenue has declined sharply since the mid-1970s, the same can-not be said of import tariff revenue. The taxation of imports, even as these countriespursued tariff reform, continued to account for a high proportion of total tax receiptsin the mid-1990s and were only marginally below the corresponding level in the mid-1970s.

The apparent contradiction between trade liberalization and continuing high tradetax revenue raises the important question of how, precisely, the one affects the other.Although policymakers generally recognize the long-term benefits of trade liberal-ization, some have argued for at least a slower pace, in part because of revenue con-cerns. This paper seeks to address these issues in three complementary ways: throughan overview of the factors that may have a bearing on the question, through a reviewof trends in trade tax revenue both globally and in selected countries, and througheconometric analysis.

The authors are especially indebted to George T. Abed for his overall guidance andhelpful suggestions on the various drafts. The authors also thank the IMF'sExecutive Board members for comments and suggestions and would like to recog-nize the comments received from numerous colleagues, notably Stanley Fischer,Jesus Seade, Robert Sharer, Michael Keen, Julio Escolano, Angelo Faria, VictoriaSummers, and Judy Dean. The comparative analysis of selected countries owesmuch to input received from Dominique Simard and Zuhtu Yucelik. AsegedechWoldeMariam worked tirelessly and with great precision at compiling the data un-derlying the tables and the econometric analysis. Administrative support was ablyprovided by Lyndsey Livingstone and Agnes Basilio. Michael Treadway and JuanitaRoushdy of the External Relations Department edited the paper and coordinated pro-duction of the publication.

The opinions expressed in the paper are those of the authors and do not necessarilyreflect the views of the IMF or its Executive Directors.

An IMF News Brief containing highlights of this paper and a summary of discus-sion at an IMF Executive Board seminar on the topic was released on February 25,1999, and is available at www.imf.org/external/np/sec/nb/1999/NB9908.HTM.

V

©International Monetary Fund. Not for Redistribution

This page intentionally left blank

©International Monetary Fund. Not for Redistribution

I Introduction

n recent decades many countries have dismantledtrade barriers and opened their economies to inter-

national competition. Trade liberalization is seen topromote economic efficiency, international competi-tiveness, and an expansion of trade, perhaps espe-cially in imperfectly competitive markets.1 Yet de-spite this progress in trade liberalization, asevidenced by the conclusion of the Uruguay Roundin 1994 and the establishment of the World TradeOrganization (WTO) in 1995,2 trade barriers are stillwidespread. Some economies and some sectors (e.g.,agriculture in many industrial countries) remain rel-atively insulated from the global economy by a vari-ety of nontariff and tariff barriers, even as importsubstitution continues to lose ground as a strategy foreconomic development.

The argument that trade liberalization enhanceseconomic efficiency and accelerates growth is nownearly universally accepted. However, because freertrade may lead to a loss of tax revenue as tariffs andother trade taxes are cut, it is important to evaluatethe revenue implications of trade liberalization, fo-cusing on what has actually happened to revenueduring liberalization, with a view to drawing policyimplications. Clearly, for countries with significantfiscal imbalances, any loss of revenue would be animportant consideration.3 Moreover, for many devel-oping countries, taxes on international trade are alarge source of revenue. Indeed, an impetus for thispaper was the observation, in a recent evaluation ofIMF-approved Structural Adjustment Facility (SAF)and Extended Structural Adjustment Facility (ESAF)programs, that some countries had targeted an in-

1See Escolano (1995), Farhadian-Lorie and Katz (1988),Helpman and Krugman (1989), Krueger (1995), andSubramanian, Ibrahim, and Torres-Castro (1993).

2In addition to progress on the multilateral front, trade liberal-ization has also resulted in an increased reliance on regional tradearrangements. See Harmsen and Leidy (1994).

3For example, the group of African countries that entered intoStructural Adjustment Facility or Extended Structural AdjustmentFacility arrangements with the IMF during the 1980s and 1990shad overall fiscal deficits averaging more than 9 percent of GDPin the year immediately preceding the program. See Abed andothers (1998).

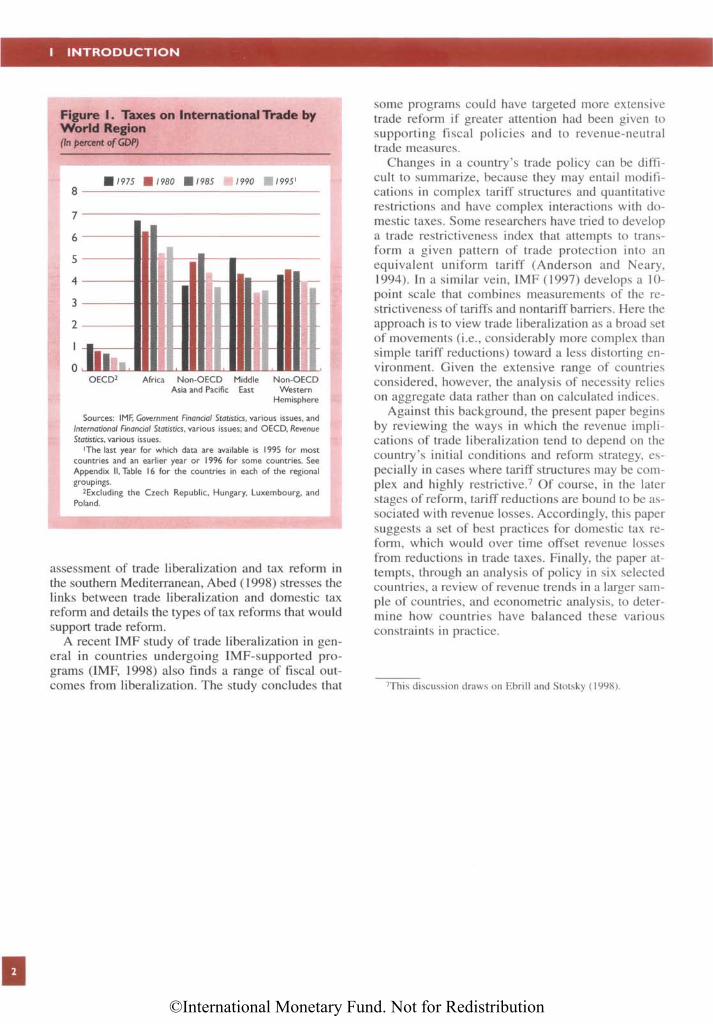

creased reliance on revenue from international tradetaxes or, in any event, had attained higher ratios ofinternational trade tax revenue to GDP at the end ofthe SAF/ESAF-supported adjustment period. Thishad occurred despite an apparent commitment totrade liberalization (Abed and others, 1998). Manyof these countries are in Africa, where despite a de-clining, if uneven, trend, trade taxes accounted forabout 5 1/2 percent of GDP on average in 1995 (Figure1).4

The revenue implications of trade liberalizationare, in general, uncertain. Blejer and Cheasty (1990)and Tanzi (1989) conclude that ultimately the net im-pact of trade reform on revenue is an empirical mat-ter.5 Similarly, in a case study analysis of the revenueimplications of World Bank-supported StructuralAdjustment Loans, Greenaway and Milner (1991)conclude that a range of outcomes is possible, de-pending on the country's initial conditions and thecomponents of the reform package. In related work,the World Bank has considered the interaction be-tween the reform of trade taxes and that of domestictaxes in World Bank programs. Rajaram (1994) ex-amines whether the revenue effects of tariff reformproposals were anticipated and complemented byother tax measures. He finds that in some but not allcases the revenue implications of trade reform andcomplementary reforms of the domestic tax systemwere considered. He suggests that a more systematicintegration of revenue and trade protection objectivesin World Bank programs is needed. Mitra (1992) andDatta-Mitra (1997) also conclude that, in some coun-tries with World Bank reform programs, greater em-phasis on revenue issues is called for.6 Finally, in an

4Because of data limitations, tariffs cannot always be separatedfrom other taxes, such as excise and sales taxes, that are also col-lected at customs (e.g., in Burkina Faso, Mali, and Tanzania). Inaddition, some countries in the CFA franc zone of West andCentral Africa levy charges on reexports (primarily to Nigeria),which cannot be distinguished from export taxes.

5In related analyses, Bevan (1995), Feltenstein (1992), andTokarick (1995) use applied general equilibrium analysis to eval-uate the effect of trade liberalization on fiscal variables.

6See also Thomas and others (1991) and Papageorgiou, Choksi,and Michaely (1990).

I

I

©International Monetary Fund. Not for Redistribution

I INTRODUCTION

Figure I. Taxes on International Trade byWorld Region(In percent of GDP)

Sources: IMF, Government Financial Statistics, various issues, andInternational Financial Statistics, various issues; and OECD, RevenuStatistics, various issues.

1The last year for which data are available is 1995 for mostcountries and an earlier year or 1996 for some countries. SeeAppendix II, Table 16 for the countries in each of the regionalgroupings.

2Excluding the Czech Republic, Hungary, Luxembourg, andPoland.

assessment of trade liberalization and tax reform inthe southern Mediterranean, Abed (1998) stresses thelinks between trade liberalization and domestic taxreform and details the types of tax reforms that wouldsupport trade reform.

A recent IMF study of trade liberalization in gen-eral in countries undergoing IMF-supported pro-grams (IMF, 1998) also finds a range of fiscal out-comes from liberalization. The study concludes that

some programs could have targeted more extensivetrade reform if greater attention had been given tosupporting fiscal policies and to revenue-neutraltrade measures.

Changes in a country's trade policy can be diffi-cult to summarize, because they may entail modifi-cations in complex tariff structures and quantitativerestrictions and have complex interactions with do-mestic taxes. Some researchers have tried to developa trade restrictiveness index that attempts to trans-form a given pattern of trade protection into anequivalent uniform tariff (Anderson and Neary,1994). In a similar vein, IMF (1997) develops a 10point scale that combines measurements of the restrictiveness of tariffs and nontariff barriers. Here theapproach is to view trade liberalization as a broad setof movements (i.e., considerably more complex thansimple tariff reductions) toward a less distorting en-vironment. Given the extensive range of countriesconsidered, however, the analysis of necessity relieson aggregate data rather than on calculated indices.

Against this background, the present paper beginsby reviewing the ways in which the revenue impli-cations of trade liberalization tend to depend on thcountry's initial conditions and reform strategy, es-pecially in cases where tariff structures may be com-plex and highly restrictive.7 Of course, in the laterstages of reform, tariff reductions are bound to be as-sociated with revenue losses. Accordingly, this papersuggests a set of best practices for domestic tax reform, which would over time offset revenue lossesfrom reductions in trade taxes. Finally, the paper at-tempts, through an analysis of policy in six selectedcountries, a review of revenue trends in a larger sam-ple of countries, and econometric analysis, to deter-mine how countries have balanced these variousconstraints in practice.

7This discussion draws on Ebrill and Stotsky (1998).

2

©International Monetary Fund. Not for Redistribution

II Potential Revenue Implications ofTrade Reform

conomists often rank trade liberalization reformsby order of importance, giving highest priority to

the reduction or removal of quantitative restrictionsand other nontariff barriers to trade or their conver-sion to tariffs. This is followed by reductions in boththe number of distinct tariff rates and the range thatthey cover (i.e., their dispersion) and finally by re-ductions in the levels of tariffs. Although this liberal-ization strategy is typically justified on economic ef-ficiency grounds (Box 1), the initial focus on theremoval of nontariff barriers also has the advantageof helping preserve the revenue yield. The agenda fortrade reform is also influenced by international prac-tice and agreements and, in particular, by WTO rulesand agreements on the design of trade reform.1

Reform of Quantitative Restrictions

In their study of countries undergoing WorldBank-assisted trade liberalization, Papageorgiou,Choksi, and Michaely (1990) conclude that signifi-cant reductions in quantitative restrictions have oftenbeen a component of successful liberalization.Takacs (1990) outlines the different methods of lib-eralizing import quotas. These include

• Gradually raising quota ceilings to nonbindinglevels.

• Converting quotas into equivalent tariffs (tariffi-cation), with the goal of later reducing these tar-iffs. The equivalent tariff is set at a rate equal tothe percentage difference between the domesticprice and the import (world) price under thequantitative restriction.

• Auctioning licenses or permits to import a spe-cific quantity of the item.2 The number of li-censes can then be gradually increased, or theselicenses can be converted into tariffs.

1In addition, trade and trade-related measures recommended bythe IMF should be consistent with members' obligations underWTO agreements.

2If license fees exceed the cost of issuing the license, there issome potential for license fees to violate WTO rules.

• Converting quotas to tariff quotas and then re-ducing the tariff rates. Under a tariff quota, onetariff rate is applied to some specified volume ofimports and a higher, often prohibitive, rate toany imports above that volume.

Of course, quantitative restrictions take manyforms other than quotas, including bans, restrictivegranting of import licenses, and state trading mo-nopolies. There may also be limits on the ability ofimporters to buy foreign exchange, which often giverise to black markets in foreign currencies. These re-strictions, which encourage rent seeking, have seri-ous efficiency and distributional implications.

Typically, countries liberalize quantitative restric-tions gradually, to minimize politically contentiousdisruptions to the domestic economy and to preventa surge in imports that could lead to balance of pay-ments problems. Maintenance of such restrictionsmay indeed temporarily limit imports, but balance ofpayments problems are best dealt with through ap-propriate macroeconomic policies, not through tradebarriers. Restrictions are also usually reduced oreliminated first on raw materials, intermediategoods, and other goods not viewed as competingwith domestic production. These reforms are thenextended to final goods, including those competingwith domestic production.

The channel by which the elimination of quantita-tive restrictions affects trade revenue will differ de-pending on the nature of the restriction and how it iseliminated. Tariffication of quotas that produces nochange in the level of imports, for example, wouldlead to an increase in revenue, as economic rents aretransferred to the government in the form of highertrade tax revenue. In addition, many goods subject toquotas are also subject to tariffs. Accordingly, if quo-tas are eliminated on these goods, revenue may in-crease as the value of imports of goods subject to tar-iffs increases (the volume is likely to increase, butthe price of these previously restricted imports islikely to fall).

The impact on import volumes and revenue of re-laxing quantitative restrictions also depends on theextent to which countries are able to improve their

3

E

©International Monetary Fund. Not for Redistribution

II POTENTIAL REVENUE IMPLICATIONS OF TRADE REFORM

Box I. Efficiency Gains from Trade Liberalization and the Budget Constraint

The design of an optimal trade or tax policy in theface of a government budget constraint is a com-plicated, second-best exercise whose solution dependson the range of tax instruments available to thegovernment and on the structure of the economy. Forone benchmark case—that of a small, open economywith the full range of commodity taxes available and noother distortions—the solution to the optimal tax prob-lem provides no role for tariffs, given the desirability ofsatisfying productive efficiency (see, e.g., Dixit, 1985;Dixit and Norman, 1980). More generally, however,there are no clear-cut solutions, particularly when onetries to take account of the implications of trade reformfor growth. Nonetheless, some practical judgments canbe made concerning the circumstances under whichtrade liberalization can be expected to yield significantefficiency gains, even taking the government's budgetconstraint into account. On balance, these gains aremost likely to be significant when

• Trade reform focuses on the removal of quantita-tive restrictions,

• The initial trade restrictions are high, and

• The existing tariff structure has multiple rates thatinduce evasion or avoidance.

The first condition is important because, besides gen-erating no revenue, quotas are associated with wastefulrent-seeking activities and undesirable, noncompetitivestrategic behavior, both of which typically result in ef-ficiency losses greater than the excess burden distor-tions associated with tariffs.

On the other hand, there are circumstances where theefficiency gains may be modest. In particular, the net ef-ficiency gains to liberalization are likely to be lower if acountry has already implemented a comprehensive lib-eralization package that eliminates quantitative restric-tions and rationalizes the tariff structure. In addition, thecosts of collecting different types of taxes may alter thepicture. If these costs are lower for trade taxes than fordomestic taxes, minimizing both the excess burden andthe cost of raising a given amount of revenue will gen-erally result in greater revenue from trade taxes than ifcollection costs are ignored (Mihaljek, 1992). However,there is little empirical evidence on the structure and rel-ative magnitude of collection costs for different taxes.

administrative capabilities. In an environment char-acterized by market prices rather than quantity con-trols on goods, customs administrations need to beable to certify the value of imports rather than relystrictly on physical control (Tanzi, 1994).

Tariff Reform

The second major element of trade reform is typi-cally the rationalization and reduction of tariff rates.There are several distinct dimensions to consider.

Characterization of Tariff Structures

Tariff structures resist easy characterization bysummary measures, and this complicates any analy-sis of the revenue implications of tariff reductions(Dean, Desai, and Riedel, 1994). Tariff schedulesmay contain dozens of different rates ranging fromzero to several hundred percent. For imports, the un-weighted average of tariff rates is sometimes takenas the simplest measure of the importance of tariffs.A simple average, however, is not very helpful be-cause, for instance, a few very high rates that applyto only a small volume of trade would weigh dispro-portionately in the average. A weighted average oftariff rates can be calculated by weighting these ratesby the percentage shares of imports to which theyapply. Although this measure is generally preferableto a simple average, one drawback is that the ob-

served demand for imports facing high tariffs islower than it would be in the absence of tariffs, andthis reduces the average. The collected tariff rate,calculated as the ratio of import tax collections toimport values, is another alternative. Although thecollected tariff rate reflects the level of statutory tar-iff rates, it also reflects the impact of evasion, ex-emptions, preferential tariffs, nontariff barriers, andchanges in import demand owing to high tariffs.Given the emphasis on revenue in this paper,changes in the collected tariff rate are used here asone indicator of trade liberalization. Finally, the dis-persion of tariff rates can be a useful supplementaryindicator of tariff structure, because a low averagerate may mask a large dispersion in rates, and hencepotentially high effective protection.

Complicating measurement is the sometimes con-siderable difference between explicit and implicittariff rates due to features of the trade regime thatdistort measurement of import values. For example,where foreign exchange controls are in effect, tariffsmay be applied to import values at the official rate ofexchange or at some other nonmarket exchange rate.This can result in implicit tariffs (the tariff chargedas a percentage of the market value of the goods)being considerably different from explicit tariffs (thetariff charged as a percentage of the goods' officialvalue). Or imported goods may be valued at refer-ence prices set by the government, which may notreflect market value. When tariff reform occurs atthe same time as reform of exchange rates and refer-

4

©International Monetary Fund. Not for Redistribution

Tariff Reform

ence prices, changes in explicit tariffs may be a mis-leading indicator of changes in implicit tariffs be-cause of these changes in valuation of the goods.

Reductions in Tariff Levels

The effect of tariff reductions on revenue dependson the levels and coverage of tariffs in effect beforethe reduction and on the extent to which they arethen reduced. The precise impact is difficult to pre-dict because it depends on complex economic re-sponses. If import values are unchanged, the imme-diate effect of a reduction in tariff rates is to lowerrevenue. If goods subject to trade taxes are includedin the base of domestic taxes on imports, this reduc-tion in trade taxes will also be accompanied by a re-duction in excise and value-added tax (VAT) collec-tions levied on imports.3

The value of imports, however, can be expected tochange in response to tariff reductions. If the priceelasticity of net demand for imports is sufficientlyhigh, the revenue gain due to increased demand forthe now-cheaper imports may compensate for or evenoutweigh the revenue loss due to the tariff cut itself.4

Although it is difficult to generalize, demand for im-ports of final consumption goods is likely to be moreprice elastic than that for imports of intermediategoods and raw materials (see, e.g., Clarida, 1996). Inmany developing countries, imports of consumergoods constitute only about 10 to 20 percent of totalimports but are often taxed at the highest rates. Sincemany trade liberalization programs involve a dispro-portionate reduction in higher tariff rates, the demandelasticity of those goods subject to tariff reductionsmight be quite high, mitigating the revenue losses.5

The response of import values also depends on theprice elasticity of supply of import substitutes. Theless elastic this supply, the smaller the reduction inoutput for a given fall in price and hence the smaller

3The precise outcome will depend on how the market prices ofgoods adjust. If, for instance, the market prices of goods that useimported inputs do not fall, then, implicitly, domestic value addedon these goods has risen and VAT revenue would not fall.

4The revenue impact of a tariff change actually depends on theelasticities of both demand and supply. The revenue-maximizingtariff will be t = (e s - e j)/-e s(1 + ed), where t is the ad valoremtariff rate, Es is the elasticity of import supply, and e d is the elas-ticity of import demand. See Blinder (1981) for an elaboration ofthis point. Note that the (absolute values of the) elasticities re-quired to ensure that the value of imports increases following atariff rate reduction would typically be less than those required toensure an increase in tariff revenue, since the share of the tariff inthe total price declines with the tariff rate reduction.

5Above-average tax rates are also often levied on inelasticallydemanded goods such as alcohol and tobacco, for both revenueand protection purposes. The focus of trade liberalization policiesin these cases should be on ensuring that domestic production isnot favored while satisfying revenue objectives.

the increase in import values. Moreover, since priceelasticities of demand and supply typically are notconstant over the entire range of prices, the startingpoint for tariff reform is also likely to affect the eco-nomic response. Indeed, if protectionist motives havedominated the setting of tariff rates, tariffs may beabove their revenue-maximizing levels.

Reduction in Tariff Dispersion

Although it depends somewhat on the circum-stances, reducing tariff dispersion is typically consis-tent with a reduction in average effective protection.The revenue implications of reducing tariff dispersionare more ambiguous. If tariff reform reduces the dis-persion of tariffs around an average value by lower-ing the higher tariffs and increasing the lower ones,the revenue effects would depend in part on the rela-tive price elasticities of demand of the goods affected.On the presumption that higher tariffs levied for pro-tection purposes apply mainly to elastically de-manded goods, a reduction in tariff dispersion willtend to increase revenue. To the extent that reductionsin tariff dispersion significantly reduce effective ratesof protection, tariff revenue effects will tend to be fur-ther mitigated as imports replace import-competingproduction. Alternatively, a reduction in the disper-sion of tariffs is often accompanied by an increase inthe minimum rate, which could imply some overallincrease in the average rate (at least temporarily), andthis also bolsters the prospect that revenue would in-crease. This approach, however, is less common andmay be restricted by WTO tariff bindings. (These arecommitments undertaken by countries within theWTO not to raise tariffs on certain goods above aspecified level.) Reducing tariff dispersion could alsobolster revenue by reducing tax evasion (see below).Taxes that are levied at a uniform rate tend to mini-mize evasion and administrative difficulties, espe-cially by reducing opportunities for misclassificationand valuation mistakes.

Tariff Exemptions and Tax Evasion

In a study of several developing countries, Pritch-ett and Sethi (1994) find a nonlinear relationship be-tween statutory tariff rates and rates actually col-lected. They argue that the higher the tariff rates, thegreater the incentive for importers to put effort intoseeking exemptions. As a result, revenue tends not toincrease in proportion to an increase in tariffs. Theconverse may also apply: reducing very high tariffsmay not always lead to a proportionate fall in rev-enue. Moreover, eliminating tariff exemptions cancontribute to trade reform while preserving revenue,by broadening the tax base. In addition to their directimpact on revenue, when exemptions become more

5

©International Monetary Fund. Not for Redistribution

II POTENTIAL REVENUE IMPLICATIONS OFTRADE REFORM

prevalent, the incentive to classify taxable productsas exempt also grows, further contributing to a lowerrate of compliance.

The extent of tax evasion is directly related to thepotential benefits to would-be evaders (Tanzi andShome, 1993). The lower the tariff, the lower themarginal benefit from evasion. On the other hand,customs evasion is associated with many costs to theevader. These include the need to find alternative—often more expensive—routes to avoid customscheckpoints, to package goods so as to conceal theirpresence or their true value, and to bribe corrupt of-ficials. Other costs include those stemming from thelack of proper invoices for subsequent use of thegoods, such as crediting under a VAT, and the costsassociated with punishment for those who arecaught. Any reduction in the marginal benefit of eva-sion is therefore likely to bolster revenue.

Reduction of Export Taxes

Export taxes are typically levied on important pri-mary commodities with relatively few exporters.There are three principal arguments for export taxes.First, they can be used as a substitute for the incometax, particularly in difficult-to-tax sectors such asagriculture. Second, they can be levied on windfallgains from changes in the international prices ofcommodities. And third, for goods in which thecountry has market power, they may reduce the sup-ply and thus increase the price of the commodity ex-ported. In the main, however, export taxes are mainlyan expedient to raise revenue; improvements in thedomestic tax system would be more desirable.Conversely, given that export taxes are often claimedto be substitutes for income taxes on hard-to-tax sec-tors, their elimination will be more likely if they areimplemented as part of an overall tax reform pack-age to broaden the tax base.

Export taxes often are levied as a combination ofa basic tax and a progressively rising rate on price in-crements. Alternatively, they may take the form ofimplicit taxes; examples include an overvalued cur-rency or a multiple exchange rate system, foreign ex-change surrender requirements at nonmarket ex-change rates, and the use of export marketing boardsthat do not pay producers market prices. These im-plicit taxes may distort the revenue picture in thatthey remain unrecorded.

Development of Regional TradeArrangements

Regional trade arrangements lower tariffs amongmembers but do not lower them for countries out-

side the arrangement. In the participating countries,many imports from within the region may arriveduty free, and trade tax revenue may thereforedecline even in the absence of changes in externaltariff rates. Foroutan (1993, p. 255) argues thatrevenue considerations in trade liberalization clashwith the conditions that minimize the likelihoodof trade diversion from outside the region to withinthe region. These conditions are, first, that thepartners have extensive trade links and, second,that they not raise their trade barriers with the restof the world. But the stronger the trade links amongthe partners, the greater the likelihood of a revenueloss from regional trade integration.6 In fact, how-ever, intraregional trade linkages among low-income countries participating in regional arrange-ments are often weak. Finally, the preexistence ofregional trade agreements may mitigate the revenueeffect of subsequent reductions in external tariffrates.7

Revenue Implications of the Indirectand Interactive Effects of Liberalization

Trade liberalization can interact with the domestictax system and the macroeconomic environment,with implications for economic growth, revenue, andthe overall budget.

Import Composition and Economic Growth

Both relaxation of quantitative restrictions and re-form of tariffs may lead to changes in the composi-tion of imports. It is difficult, however, to predictsuch changes, because they are likely to vary acrosscountries. In particular, if trade reforms diminish theshare of import-substituting industries in the econ-omy, imports of the goods produced by these indus-tries will increase. If these goods are taxed at ahigher-than-average rate, this might induce an in-crease in revenue.

Considerable evidence has accumulated over timethat trade liberalization is linked to higher rates ofeconomic growth, which is its main objective(Escolano, 1995). Trade liberalization leads both to abetter static allocation of resources and to a higherrate of output growth in the long run. This enhancedgrowth leads to expansion of tax bases, with a con-comitant expansion of revenue potential. Over time,the influence of economic growth on revenue may

6However, in assessing the revenue implications of regionaltrade arrangements, it should also be noted that such arrange-ments are typically implemented only over a transition period.

7Regional trade arrangements may also influence the likelihoodof further trade liberalization (Bhagwati and Panagariya, 1996).

6

©International Monetary Fund. Not for Redistribution

Revenue Implications of Indirect and Interactive Effects of Liberalization

dominate the influence of shorter-term changes inthe trade regime.8 To the extent that growth follow-ing liberalization is associated with an increased im-portance of trade, the ratio of trade taxes to GDPwould tend to increase for a given level of tariffs.That said, along with this growth, the composition ofrevenue is also likely to change over time, with in-creased reliance on domestic taxes and reduced re-liance on trade taxes, consistent with reductions intariff rates.

The Role of Domestic and InternationalTrade Taxes

Domestic indirect taxes may reinforce the protec-tive elements of trade taxes through several channels.One is through the differential application of VATs toimports and domestic production.9 Such discrimina-tion is rare, although in a few cases surcharges areadded to the VAT on imports. More common is thedifferential application of excise taxes to imports andto domestic production. Some countries apply twodifferent schedules of excise rates, levying lowerrates on imports than on domestic production—insome commonwealth countries, excise taxes applyonly to domestic production.

Interactions with Accompanying Policies

Reform of tax policy and of tax and customs ad-ministration, by protecting the revenue base, pro-vides essential support to trade liberalization. Suc-cessful trade liberalization can be greatly facilitatedif steps are taken to strengthen domestic taxes, espe-cially at the earliest stages of the process, because ittakes time for tax and customs administrations toimprove revenue collection. Box 2 outlines the criti-cal reforms needed to improve tax structure and ad-ministration in low-income countries. In Africa,where there is a particularly heavy reliance on tradetaxes, a number of countries have reformed theirtax systems. A relevant example is Benin, althoughother countries have also made substantial progress(Abed and others, 1998). However, even when pur-suing comprehensive tax reform, many countriesfacing fiscal imbalances have also resorted to short-

8Alternatively, the longer-term growth impact of trade liberal-ization works to alleviate concerns that measured elasticities ofsupply and demand are insufficiently high to offset the direct rev-enue consequences of tariff rate reductions.

9If a good is not produced domestically (e.g., automobiles inmany countries, wine in some industrial countries), an excise taxand a tariff will have an equivalent effect if levied at the samerate. However, a tariff may induce domestic firms to begin pro-ducing the good, because it would confer an advantage on them,whereas an excise tax, applied without discrimination to both im-ports and domestic production, would not.

term measures to mobilize revenue until the struc-tural reforms take effect. For example, an importantthrust of Kenya's fiscal reforms was to lower the av-erage rate of effective protection, reduce the disper-sion of rates, and phase out export duties. However,the authorities also planned to introduce a presump-tive tax of 5 percent on the value of gross sales ofagricultural products to offset the revenue loss fromeliminating the export tax on coffee and tea.

Interactions with MacroeconomicDevelopments

The economic adjustments to trade liberalizationmay include significant changes in the macroecon-omy as well. If trade balances initially worsen withtariff reductions, the currency may depreciate. In-deed, in many cases trade reform is accompanied byan intentional devaluation to forestall the need foroffsetting adjustments to fiscal and monetary policy.In general, the effect of a fall in value of the cur-rency on trade tax revenue is ambiguous (Tanzi,1989). One benchmark case, however, occurs whenthe demand for imports is relatively inelastic. Theincrease in the value of imports in domestic currencyterms following a depreciation can then bolster rev-enue, as was found in several successful stabilizationcases in African countries, where a large share of im-ports consists of price-inelastic necessities withoutclose domestic substitutes.

The 1994 devaluation of the CFA franc under-scores the importance of the circumstances sur-rounding a change in the value of a currency for taxrevenue. The CFA franc (the currency used by sev-eral francophone countries in West and CentralAfrica) had been overvalued prior to the devalua-tion, and imports had fallen because of weak eco-nomic activity in the region. Accordingly, when thecurrency was devalued as part of an overall adjust-ment package, imports by countries in the CFA franczone expanded sharply (from 25.4 percent of GDP in1993 to 34.8 percent in 1994) as a result of the over-all recovery in demand. This surge had a positiveimpact on revenue.10

Conclusions

The revenue implications of trade liberalizationwill depend significantly on the form of liberaliza-tion and the circumstances under which it occurs.What is important for the analysis that follows is thatcertain trade reform strategies can achieve consider-

10The CFA franc devaluation was also associated with a seriesof IMF-supported adjustment programs for the countries involved(Clement and others, 1996).

7

©International Monetary Fund. Not for Redistribution

II POTENTIAL REVENUE IMPLICATIONS OF TRADE REFORM

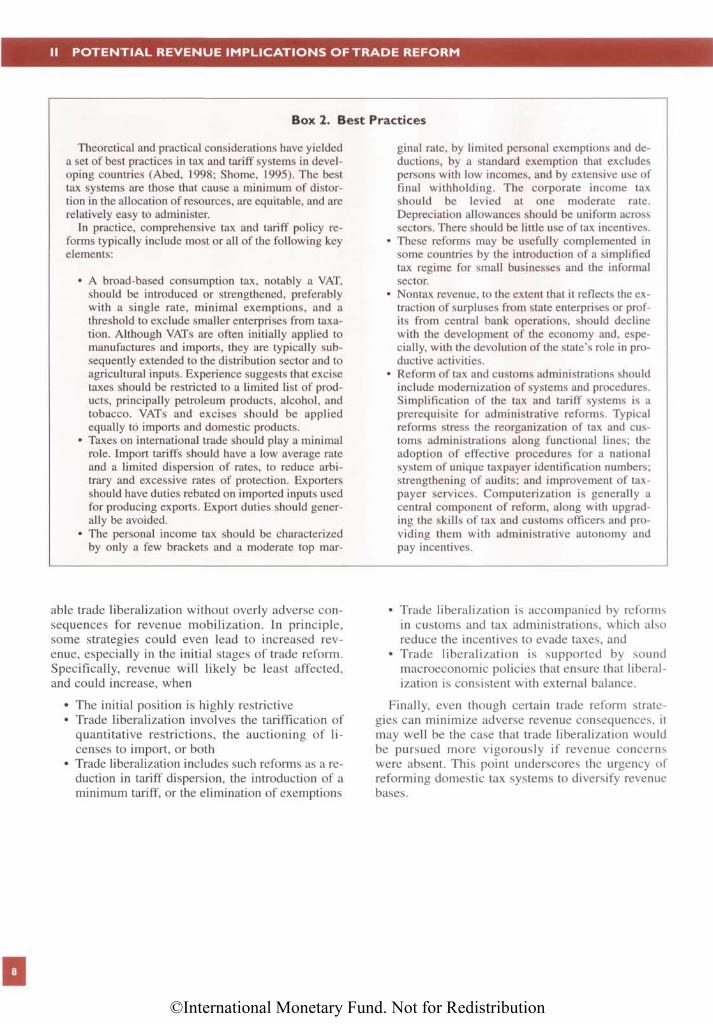

Box 2. Best Practices

Theoretical and practical considerations have yieldeda set of best practices in tax and tariff systems in devel-oping countries (Abed, 1998; Shome, 1995). The besttax systems are those that cause a minimum of distor-tion in the allocation of resources, are equitable, and arerelatively easy to administer.

In practice, comprehensive tax and tariff policy re-forms typically include most or all of the following keyelements:

• A broad-based consumption tax, notably a VAT,should be introduced or strengthened, preferablywith a single rate, minimal exemptions, and athreshold to exclude smaller enterprises from taxa-tion. Although VATs are often initially applied tomanufactures and imports, they are typically sub-sequently extended to the distribution sector and toagricultural inputs. Experience suggests that excisetaxes should be restricted to a limited list of prod-ucts, principally petroleum products, alcohol, andtobacco. VATs and excises should be appliedequally to imports and domestic products.

• Taxes on international trade should play a minimalrole. Import tariffs should have a low average rateand a limited dispersion of rates, to reduce arbi-trary and excessive rates of protection. Exportersshould have duties rebated on imported inputs usedfor producing exports. Export duties should gener-ally be avoided.

• The personal income tax should be characterizedby only a few brackets and a moderate top mar-

ginal rate, by limited personal exemptions and de-ductions, by a standard exemption that excludespersons with low incomes, and by extensive use offinal withholding. The corporate income taxshould be levied at one moderate rate.Depreciation allowances should be uniform acrosssectors. There should be little use of tax incentives.

• These reforms may be usefully complemented insome countries by the introduction of a simplifiedtax regime for small businesses and the informalsector.

• Nontax revenue, to the extent that it reflects the ex-traction of surpluses from state enterprises or prof-its from central bank operations, should declinewith the development of the economy and, espe-cially, with the devolution of the state's role in pro-ductive activities.

• Reform of tax and customs administrations shouldinclude modernization of systems and procedures.Simplification of the tax and tariff systems is aprerequisite for administrative reforms. Typicalreforms stress the reorganization of tax and cus-toms administrations along functional lines; theadoption of effective procedures for a nationalsystem of unique taxpayer identification numbers;strengthening of audits; and improvement of tax-payer services. Computerization is generally acentral component of reform, along with upgrad-ing the skills of tax and customs officers and pro-viding them with administrative autonomy andpay incentives.

able trade liberalization without overly adverse con-sequences for revenue mobilization. In principle,some strategies could even lead to increased rev-enue, especially in the initial stages of trade reform.Specifically, revenue will likely be least affected,and could increase, when

• The initial position is highly restrictive• Trade liberalization involves the tariffication of

quantitative restrictions, the auctioning of li-censes to import, or both

• Trade liberalization includes such reforms as a re-duction in tariff dispersion, the introduction of aminimum tariff, or the elimination of exemptions

• Trade liberalization is accompanied by reformsin customs and tax administrations, which alsoreduce the incentives to evade taxes, and

• Trade liberalization is supported by soundmacroeconomic policies that ensure that liberal-ization is consistent with external balance.

Finally, even though certain trade reform strate-gies can minimize adverse revenue consequences, itmay well be the case that trade liberalization wouldbe pursued more vigorously if revenue concernswere absent. This point underscores the urgency ofreforming domestic tax systems to diversify revenuebases.

8

©International Monetary Fund. Not for Redistribution

Ill Analysis of Trade Liberalization andRevenue Developments

his section considers the interplay between tradeliberalization and revenue from international

trade taxes in recent decades. The intent is to reviewwhat has actually occurred, in order to gain insightinto the factors that govern the revenue conse-quences of trade liberalization and the related issueof how countries have pursued liberalization.

Trade Liberalization Strategiesand Revenue Implications:A Comparative Analysis

A detailed comparison of country experiences is auseful way of examining the interaction among themany dimensions of trade liberalization, their rev-enue implications, and the economic circumstancesof individual countries. The six countries whose his-tories of trade liberalization are described in this sec-tion—Argentina, Malawi, Morocco, the Philippines,Poland, and Senegal—all have considerable experi-ence with trade reform, which has sometimesoccurred in phases. They were selected to provide arange of country experience, with a focus on Africa,where some of the issues concerning the revenueimpact of trade reform have received particularattention. The selection is not, however, intended tobe representative of other countries but merelyillustrative.

The discussion of Argentina focuses on that coun-try's reforms in two distinct periods: from 1987 to1991, and since 1991. The discussion of Malawi fo-cuses on the late 1980s and mid-1990s. In the case ofMorocco, a distinction can be made between themacroeconomic context of the reforms implementedin the 1980s and that of more recent reforms. In thePhilippines, trade reform was implemented at a timeof weak overall revenue performance in the mid-1980s. The discussion of Poland covers the periodsince 1990, the beginning of its transformation into amarket economy, and thus its trade policy reformsexemplify the case of a transition economy. InSenegal, the reform process can again be decom-posed into phases: an initial phase in the mid-1980sand a subsequent phase beginning in 1994.

Trade Liberalization Measures

How have these countries handled each of themany dimensions of trade reform? First, in the areaof reform of nontariff barriers, reducing quantitativerestrictions was a priority in all cases, although thepace and nature of that reform appear to have re-flected revenue concerns, among others. Poland in1990 placed a strong emphasis on eliminating quan-titative restrictions: their removal was integral to thecountry's "big bang" transformation. The 1991 tradereform package in Argentina included tariffication ofthe automobile import quota and the elimination ofsome reference prices. Both Malawi and Senegalpursued strategies in the late 1980s and the 1990sthat stressed bolstering the domestic tax systemwhile moving less rapidly with the outright elimina-tion of quantitative restrictions. Nonetheless, bothmade progress in reducing such restrictions.Malawi's trade liberalization program in the late1980s included a focus on eliminating foreign ex-change rationing. Similarly, Senegal embarked in1986 on a phased reduction of quantitative restric-tions, concentrating initially on goods not producedlocally. The Philippines focused on the tarifficationof quantitative restrictions during the initial phasesof its trade liberalization efforts. Finally, reflecting atrade liberalization strategy adopted in 1983,Morocco's reforms included a gradual elimination ofquantitative restrictions on imports and the abolitionof import deposit requirements.

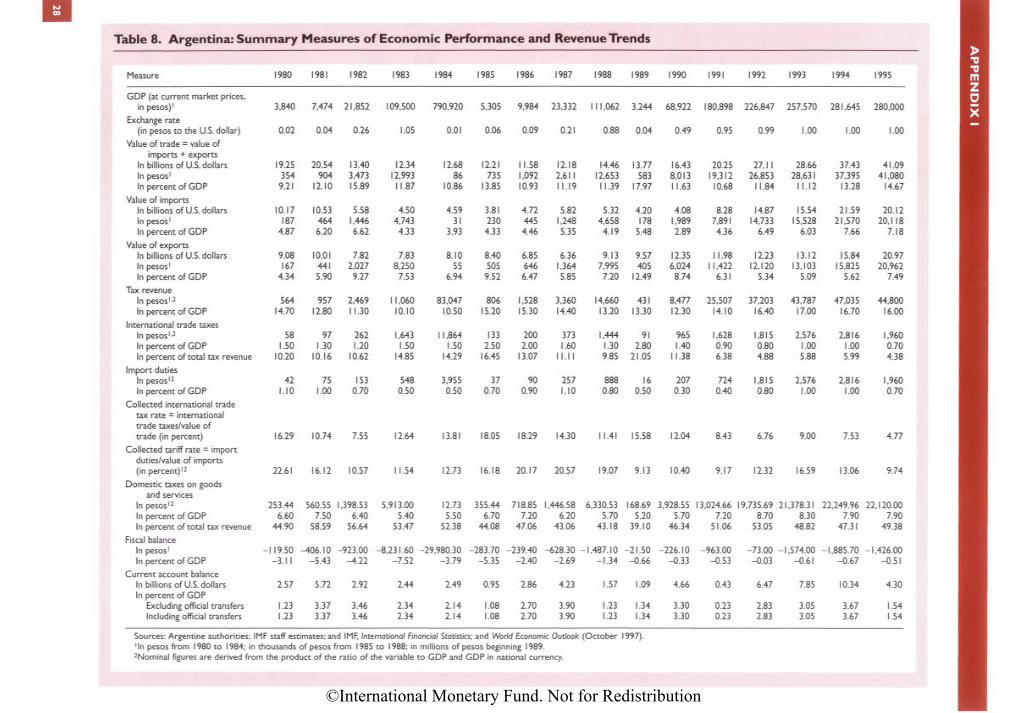

Again, all cases stressed tariff reductions in theirreform programs, although with hesitation at times.Morocco's reductions in statutory tariffs resulted in adecline in the collected tariff rate1 from 26.3 percentin 1980 to 14.9 percent in 1995 (Table 10 inAppendix I). This success owes much to improvedstabilization policies, which supported an opening ofthe economy that led to a strengthened performance

1As already mentioned, the collected tariff rate is the ratio ofimport tax collections to import values. Reference is also made inthis paper to the collected trade tax rate, which is the ratio of tradetaxes—including export taxes—to the value of trade (importsplus exports).

9

T

©International Monetary Fund. Not for Redistribution

Ill ANALYSIS OF TRADE LIBERALIZATION AND REVENUE DEVELOPMENTS

of domestic tax revenue. In contrast, Senegal's earlyliberalization efforts in the mid-1980s faltered in theface of weaknesses in macroeconomic managementand stagnant trade; as a consequence, tariff reduc-tions were accompanied by serious revenue short-falls, which led to a reversal of the tariff cuts.Senegal's second phase, implemented in conjunctionwith the 1994 devaluation of the CFA franc, wasmore successful. In the Philippines, reduced relianceon trade taxes has at times been constrained by theweakness of domestic tax mobilization. The tariffi-cation of quotas there has already been noted. In ad-dition, the Philippines imposed a temporary importsurcharge in the early 1990s. As a result, the col-lected tariff rate declined only slightly, from 16.7percent in 1985 to 14.4 percent in 1995 (Table 11 inAppendix I). Poland adopted comprehensive tradeliberalization at the outset of its transformation pro-gram in 1990, with a view to using internationalprices as a guide to price formation within the do-mestic economy. However, in the face of sharp out-put declines and revenue pressures, some reversalsoccurred, which have been overcome in recent yearsas reform of the economy more generally has takenhold. Finally, Malawi imposed a temporary exportlevy to address revenue shortfalls that compromisedits trade liberalization efforts.

Several of the countries accorded high priority toreducing tariff dispersion and consolidating tariffstructures. Between October 1988 and June 1991,Argentina reduced the dispersion of its existing tariffrates, in part through the introduction of a 5 percentminimum tariff in 1989; this reduction was partlyoffset by the introduction of specific duties on arange of goods. In the late 1980s, Malawi reducedthe range of its tariffs from 0-220 percent to 0-45percent; by August 1997 the maximum tariff rate hadbeen reduced to 35 percent. In its early reform ef-forts, Morocco considerably simplified and rational-ized its complex tariff schedules. The maximum tar-iff rate was reduced from 400 percent in 1982 to 60percent in 1984 and 35 percent in 1993; in addition,the number of tariff bands was reduced from 47 in1980 to 6 in 1996. Senegal also made progress in ra-tionalizing its tariff structure. In the Philippines,however, partly as a result of the tariffication of quo-tas, measured tariff dispersion was not reduced at theoutset, although later both tariff rates and tariff dis-persion were reduced.

In Argentina, as part of the 1991 reform package,which included steps to broaden the domestic taxbase, export taxes on many agricultural productswere eliminated, with the exception of unprocessedoilseeds. In Malawi in 1995, the opportunity to taxthe windfall gains associated with a sharp deprecia-tion of the currency and a deteriorating revenue per-formance led to an export levy being imposed on

certain agricultural exports, although this was ac-companied by a plan to phase it out. In Morocco, thead valorem taxes levied on exports were abolished in1995, leaving only raw phosphate exports subject toa specific tax.

Regional developments have also helped promotetrade liberalization in this group of countries.Malawi's trade reform efforts in recent years havebeen guided by its participation in regional trade ini-tiatives, principally the Cross-Border Initiative(CBI).2 Morocco currently faces the fiscal challengeposed by its 1996 Association Agreement with theEuropean Union (AAEU): Morocco must remove alltariffs on EU industrial goods imports over a 12-yearperiod. One estimate (Abed, 1998) suggests thatMorocco's resulting revenue loss might amount to asmuch as 2 to 2.6 percent of its GDP by the end of thetransition period.3

The countries in the sample also afford examplesof how domestic taxes can reinforce the protectionprovided by trade taxes. In Malawi, until the 1992/93fiscal year, the surtax (a broad-based sales tax) ef-fectively taxed imported goods that compete withdomestic goods at a higher rate than domestic goods,to strengthen protection. This differential was elimi-nated in that fiscal year, in combination with an up-ward adjustment in import duty rates on importedgoods previously carrying the higher effective surtaxrate as an offset. In Poland, excise tax rates on someitems were 5 percent higher on imports than on do-mestic production.

Experience in all the countries demonstrates theimportance of broadening the domestic tax base aspart of an overall liberalization package. In the late1980s Malawi embarked on a program to reform thetax system by, among other things, lowering mar-ginal tax rates and converting the sales tax into acredit-based VAT. Trade liberalization in Moroccohas been accompanied by improvements in the taxstructure, as exemplified by the introduction of aVAT in 1986 and, more recently, by a complete over-haul of the tax and customs administrations. In thePhilippines, both direct and indirect taxation werereformed, the latter through the introduction of aVAT; however, there was less progress in bolsteringtax administration. In Poland, as in many transitioneconomies, the imperative was to implement a mod-ern tax system to accommodate the rapid changes inthe underlying economic structure. However, as

2The CBI, endorsed at a ministerial-level meeting in 1993, callsfor countries in eastern and southern Africa and the Indian Oceanto pursue comprehensive trade reform by, among other things,dismantling quantitative restrictions on a reciprocal basis, and toestablish a common external tariff.

3The range reflects alternative assumptions about how muchMorocco will substitute EU imports for non-EU imports.

10

©International Monetary Fund. Not for Redistribution

Trade Liberalization Strategies and Revenue Implications

Poland discovered, even with rapid progress on taxreform the effective implementation of new taxesand associated administration structures is time-con-suming. This experience shows that revenue consid-erations can impede trade liberalization in the shortterm. Finally, Senegal has been successfully refiningits VAT (reducing the number of rates and expandingthe base) to bolster revenue mobilization.

The importance of administrative capacity has notalways been recognized. Malawi and Morocco bothundertook trade liberalization without first improv-ing customs administration. Only recently have bothcountries made customs administration reform a cen-tral component of trade reform.

Impact on Revenue

Clearly, many of the initial conditions and thetrade liberalization strategies that would be consis-tent with minimal revenue consequences, as dis-cussed above, were present to varying degrees and atdifferent times in each of the six countries. It is in-teresting to consider how these disparate elementswere reflected in actual trends in revenue in eachcountry.

During most of the first phase of reform inArgentina (1988-91), overall tax revenue perfor-mance was weak, and revenue from taxes on inter-national trade tended to fluctuate around a broadlyunchanged trend. Over this period the dispersion oftariffs and the average tariff rate were only slightlyreduced. The indications are that the failure to boostother sources of revenue and to achieve macroeco-nomic stability compromised trade reform in thatphase. However, in the post-1991 period, when thebase broadening of the VAT (which was extended tomost movable goods) took hold, and inflation wasreduced, overall revenue performance strengthened.Tax revenue increased from 12.3 percent of GDP in1990 to 16.0 percent in 1995 (Table 8 in Appendix I),and there was a reduced reliance on internationaltrade taxes, in relation to both total revenue andGDP.

Trade liberalization and economic reform inMalawi also went through phases. During the late1980s, complementary tax reforms were revenue en-hancing. Moreover, the liberalization of foreign ex-change restrictions and a 15 percent devaluation ofthe currency in 1988 resulted in a modest increase inimports as a percentage of GDP. As a result, from fis-cal year 1987 to fiscal year 1990, both the collectedtrade tax rate and the share of trade taxes in tax rev-enue declined modestly; in contrast, trade taxes as apercentage of GDP increased modestly (Table 9 inAppendix I). This would appear to be an examplewhere the initial focus on reducing quantitative re-strictions and tariff dispersion, together with the fa-

vorable impact of liberalizing the foreign exchangemarket and enhancing tax administration, resulted inboth strengthened revenue mobilization and a moreliberal trade regime. The more recent phase affordsan example of how difficult it can be to liberalize inthe face of weak domestic tax performance. Despitereductions in tariff rates in the mid-1990s, the col-lected trade tax rate tended to increase, in large partbecause of the imposition of a temporary export levyin 1995. The tendency for the collected import tariffrate to increase in recent years could also reflect im-provements in tax and customs administration.

As already noted, reform of the domestic tax sys-tem took place alongside a program of trade liberal-ization during the initial reform phase in Morocco inthe 1980s. The country was therefore able to main-tain a relatively high and stable tax revenue-GDPratio even as the collected trade tax rate and relianceon taxes from international trade tended to decline(Table 10 in Appendix I). More recent years havewitnessed a further decline both in the collectedtrade tax rate and in trade taxes as a share of tax rev-enue, reflecting, among other things, improved taxadministration and the pursuit of sound macroeco-nomic policies more generally.

The interesting phase of reform in the Philippinesbegan in 1986 against a background of weak overallrevenue performance: revenue was only about 10percent of GNP (Table 11 in Appendix I). Budgetarypressures constrained the reform, which conse-quently focused on the tariffication of quantitativerestrictions and reductions in tariff dispersion, whilerevenue was bolstered by, among other things, a newsurcharge on non-oil imports. Reflecting the liberal-ization, imports increased significantly as a percent-age of GDP. This increase in imports, in combinationwith the reform strategy that has been pursued, hasresulted in an increase in trade taxes as a percentageof GDP and of total tax revenue, even as the col-lected trade tax rate has declined modestly.

Poland illustrates the difficulties that transitioneconomies experience as they attempt to move to amarket-oriented economy. The initial liberalizationwas dramatic. However, a consequence of economictransformation is that the traditional sources of rev-enue (e.g., levies on state enterprises) tend to declinesharply even as expenditure pressures remain high.Hence the Polish authorities had to move rapidly toimplement the full range of modern taxes with sup-porting tax administrations. Perhaps inevitably, thisprocess was not always smooth. As a result, the paceof trade liberalization suffered some hesitations,which reflected in part the pressure to protect rev-enue in the face of a severe economic downturn andin part the fact that it took time for tax reform to con-tribute significantly to the budget. Between 1991 and1994 the collected international trade tax rate and the

I I

©International Monetary Fund. Not for Redistribution

Ill ANALYSIS OF TRADE LIBERALIZATION AND REVENUE DEVELOPMENTS

share of trade taxes in total revenue both rose—thelatter peaking in 1994 at about 9 percent (Table 12 inAppendix I). However, the reforms have since takenroot, and Poland was able to reduce tariff rates to thepoint where trade taxes as a percentage of tax rev-enue and of GDP have fallen, even as the value oftrade has soared. By 1996 the share of trade taxes intax revenue had declined to slightly above 6 1percent.

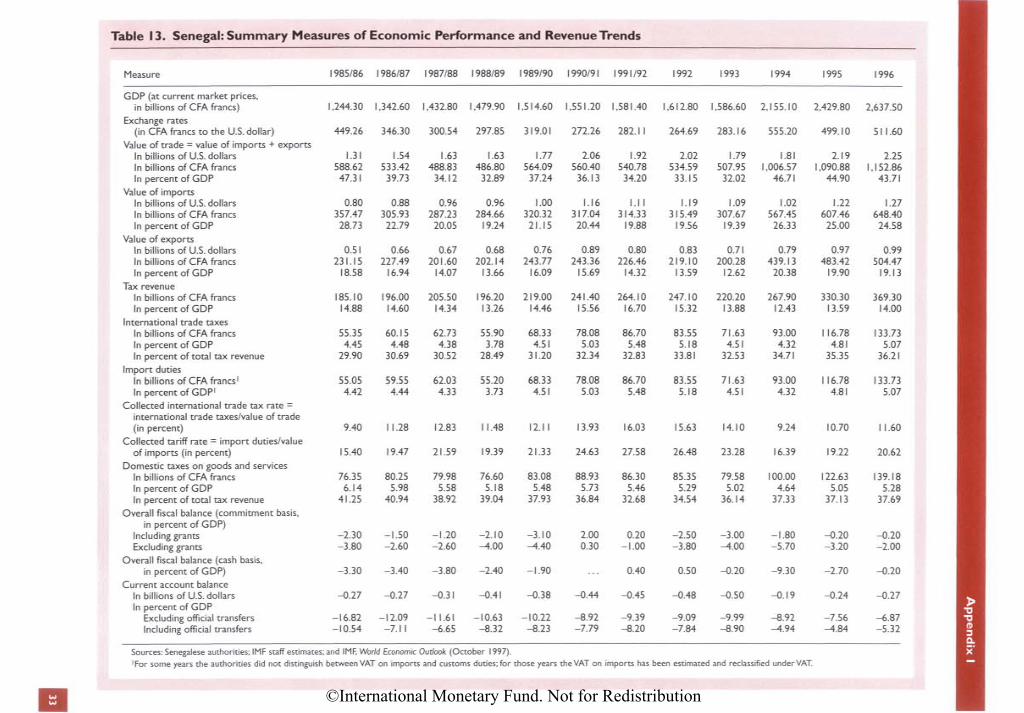

The early phase of reform in Senegal demon-strates how difficult it can be to pursue trade liber-alization in the absence of supporting macroeco-nomic and structural policies. From fiscal year1985/86 to fiscal year 1990/91, reliance on tradetaxes increased only modestly even though the col-lected trade tax rate increased by about 48 percent(Table 13 in Appendix I). These trends, combinedwith the fact that the ratio of trade taxes to GDP alsoincreased only modestly, imply that there was im-port compression (relative to GDP). This problemwas alleviated by the macroeconomic stabilizationmeasures implemented in 1994 in conjunction withthe devaluation of the CFA franc.4 Since 1994, im-port tax receipts have increased, and the revenue im-plications of significant tariff reductions have beenoutweighed by higher import levels and temporarytariff surcharges intended to ease the adjustmentprecipitated by the elimination of import licenses(an action analogous to tariffication of a quantitativerestriction).

Summary of Results and Implications forLiberalization Indicators

All of the countries discussed have implementedsubstantial trade reforms, but their experiences havediffered widely. As a prelude to the econometricanalysis reviewed below, consider how these experi-ences are reflected in the behavior of liberalizationindicators and in indicators of the countries' relianceon international trade taxes.

As already noted, a country's trade policy stanceresists easy statistical characterization. In the ab-sence of an ideal measure, this study presents twoeconometric models with complementary liberaliza-tion indicators to gauge the revenue implications oftrade liberalization. One of these models uses thecollected tariff rate as its indicator of trade liberal-ization. As is well known, this variable needs to beinterpreted carefully for several reasons.

First, because the collected tariff rate is a singlesummary measure that cannot distinguish between

4IMF staff reports from that time suggest that the high tariff andtax rates were encouraging the growth of the informal sector,which might help explain the reported drop in imports as a per-centage of GDP.

the various forms of trade liberalization, it cannotperfectly track trends in trade liberalization.5

Second, although it is related to the average statutorytariff, the collected tariff rate will be less than thecorresponding average statutory rate for several rea-sons. One reason is that some goods may receivepreferential treatment, such as exemptions or re-gional preferences. Another is that tariffs create anincentive to reclassify goods so as to qualify forlower tariff rates. Yet another is that tariffs create theincentive for outright evasion through smuggling.6 Itis worth noting that the correlation coefficient be-tween the collected tariff rate and the simple averagestatutory tariff rate, an alternative liberalization indi-cator for which limited observations were available,was about 0.7.7 Third, at some point the collectedtariff rate may decline even as the average statutoryrate increases, reflecting the impact of increased in-centives for evasion and lobbying for exemptions.More generally, under a highly restrictive tradingregime, tariff rates might be beyond the revenue-maximizing rates, a point that is considered furtherin the econometric analysis below.

Against this background, consider how move-ments in the collected tariff rate have tracked liber-alization trends in the six countries. Comparing, foreach country, the situation in the year prior to themost important recent trade reform episode with thatin the most recent year for which data are available,8

we find that the average collected tariff rate de-creased from 17.1 percent to 12.1 percent. This indi-cates that, for this sample, movements in the col-lected tariff rate have been tracking underlying

5For example, although the outright removal of quotas will tendto result in a decline in the collected tariff rate as imports increase,when quota reform takes the form of tariffication the collectedtariff rate and trade liberalization may move in oppositedirections.

6In the case of smuggling, neither the tariff due nor the actualimport is captured by customs-based trade data. This paper, how-ever, uses balance of payments import data, which often attemptto incorporate estimates of imports not captured by customs data.More generally, these points suggest that interpreting the absolutelevel of the collected tariff rate as a gauge of trade liberalizationwould be problematic.

7The data for the simple average tariff rate, which were limitedto a few observations—often from alternative sources—forArgentina, Morocco, the Philippines, Poland, and Senegal, areavailable from the authors upon request.

8Given that changes to trade regimes are typically ongoingrather than isolated events, deciding when the most significant re-cent reform phase began is inevitably somewhat arbitrary. One ofthe criteria used was whether trade reform occurred along withsupporting reforms, such as a strengthened domestic tax system,that might indicate a break in policy formulation. For the sixcountries, the prereform years were identified as follows:Argentina, 1990; Malawi, fiscal year 1986/87; Morocco, 1986;the Philippines, 1985 (i.e., the whole period for which data wereavailable); and Senegal, 1993. Poland is excluded from the calcu-lations given the short time period in that case.

12

©International Monetary Fund. Not for Redistribution

Trade Liberalization and Revenue Trends

liberalization trends (see Tables 8 to 13 in AppendixI). At the same time, reflecting an increase in the av-erage ratio of imports to GDP from about 16 percentto almost 25 percent, the share of trade taxes in taxrevenue rose modestly. Although the increase in im-ports could reflect independent considerations, theresults are consistent with the notion that one of theeffects of trade liberalization is an expansion of theimportance of trade.

Consider next the behavior of the ratio of interna-tional trade taxes to GDP, which was observed to in-crease in some countries with SAF/ESAF-supportedprograms. The experience of the country sampledemonstrates that interpreting this ratio as an indica-tor of liberalization can be misleading. Likewise re-flecting the import surge following liberalization, theaverage ratio of import duties to GDP increasedfrom 2.8 percent to 3.6 percent between the prere-form year and the latest year for which data areavailable. This is consistent with the notion that thecombination of the reform strategy and the positiveimpact of liberalization (notably, a surge in imports)has worked to bolster revenue for this sample ofcountries. Indeed, this increase in the ratio of importduties to GDP reinforces the interpretation of the col-lected rate as a liberalization indicator: had the de-cline in the collected rate reflected weakened cus-toms administrations, tariffs as a percentage of GDPwould also be expected to fall.

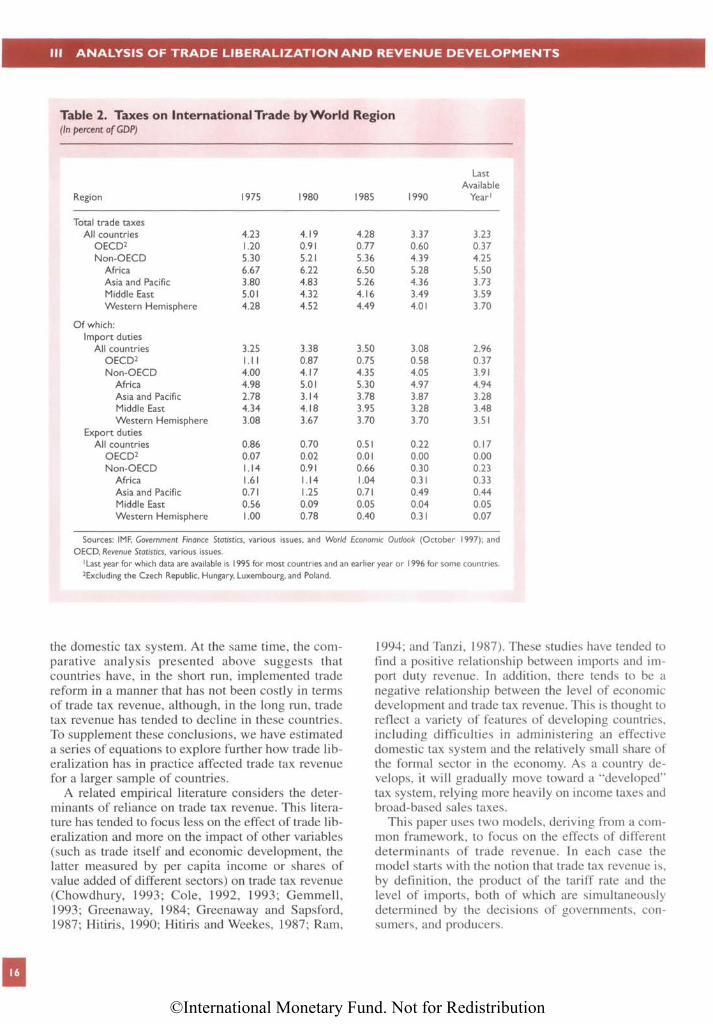

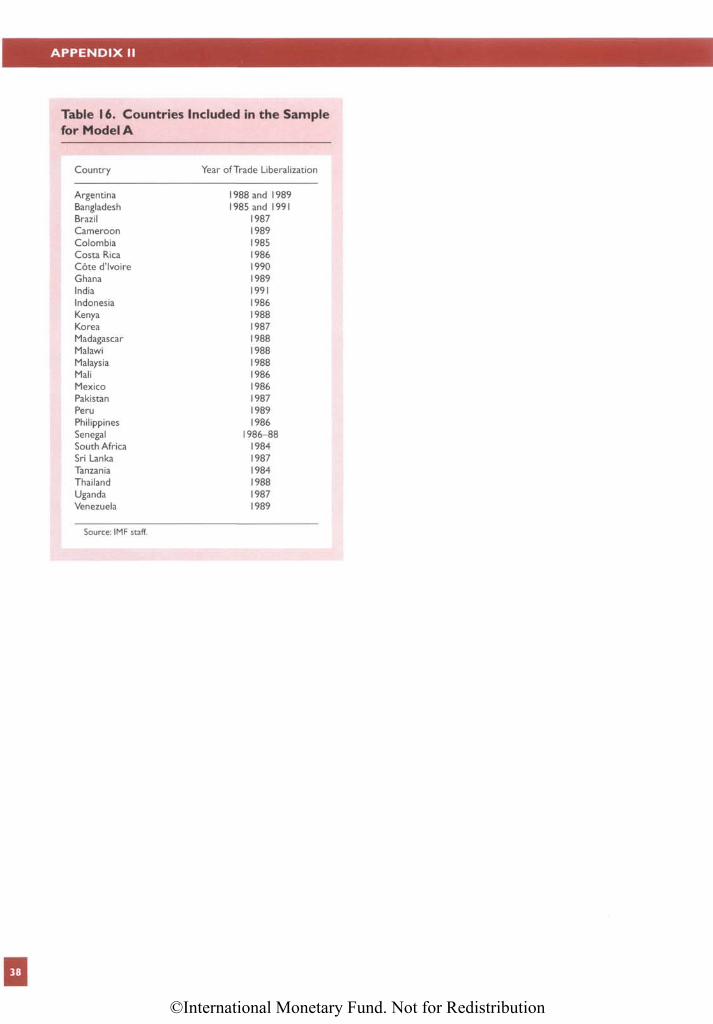

The data for the econometric analyses presentedbelow further corroborate the proposition that move-ments in the collected tariff rate correlate positivelywith trends in liberalization and are a better indicatorof liberalization than trends in the ratio of trade taxesto GDP. Specifically, the data sample of 27 develop-ing countries used in one of the econometric modelsreported below is reviewed for prominent trends. Asis elaborated there, most of the important trade liber-alization reforms for the sample were initiated after1984. For the period 1980-85, the average ratio oftariff revenue to GDP declined, while the averagecollected tariff rate increased; these trends were re-versed for the period 1985-92, when trade liberal-ization was more pronounced.

Trade Liberalization andRevenue Trends

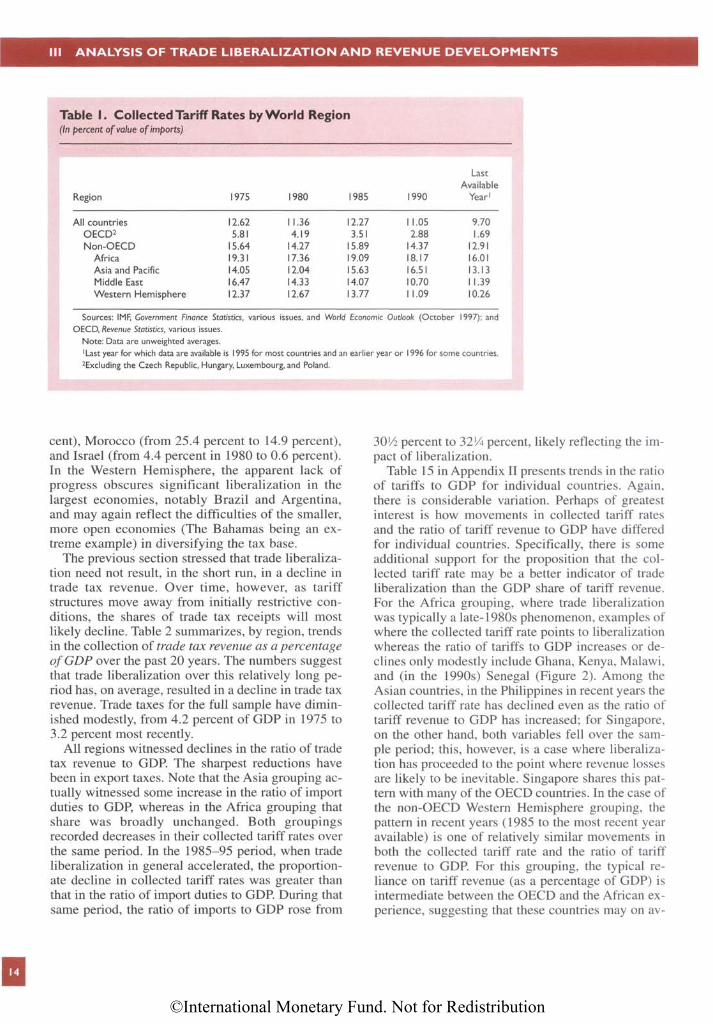

We now review trends in international trade rev-enue for a broad range of countries, focusing on im-port duties. Although movements in the collectedtariff rate clearly need to be interpreted with care,the previous results suggest that this variable is ofsome use as an indicator of whether countries are be-coming more open to international trade. For theglobal sample, the average collected tariff rate has

declined from 12.6 percent in 1975 to 9.8 percent inthe last year for which data are available (Table 1).Average collected tariff rates declined for all regions.The largest proportionate decline (71 percent be-tween 1975 and 1995) was in the grouping of coun-tries that are members of the Organization forEconomic Cooperation and Development (OECD).This likely reflects in part the relative ease withwhich those countries have been able to diversifytheir tax bases by means of the VAT and other taxes.The smallest proportionate decline was in the Asiagrouping (4 percent over the same period).9

The timing of the decline in the collected tariffrate varies markedly between the OECD region andthe non-OECD regions. In particular, the OECD re-gion appears to have reduced its reliance on tradetaxes gradually over the past 20 years. As a rough ap-proximation, the collected tariff rates for the otherregions were broadly unchanged between 1975 and1985, but all declined in the subsequent decade asthe pace of liberalization appears to have picked upmomentum.

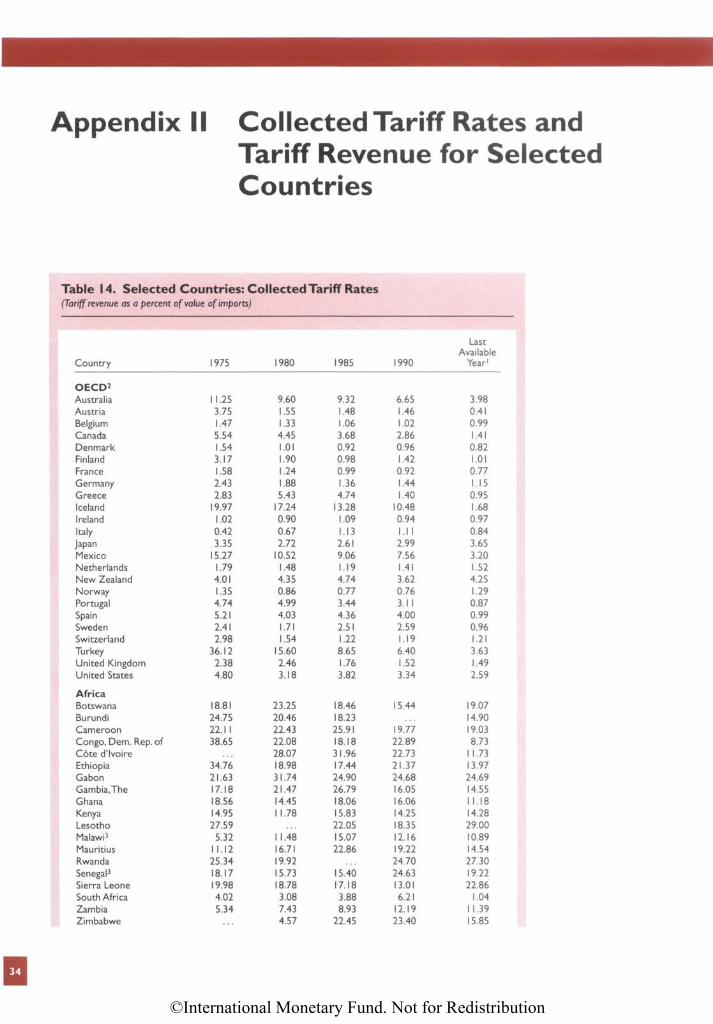

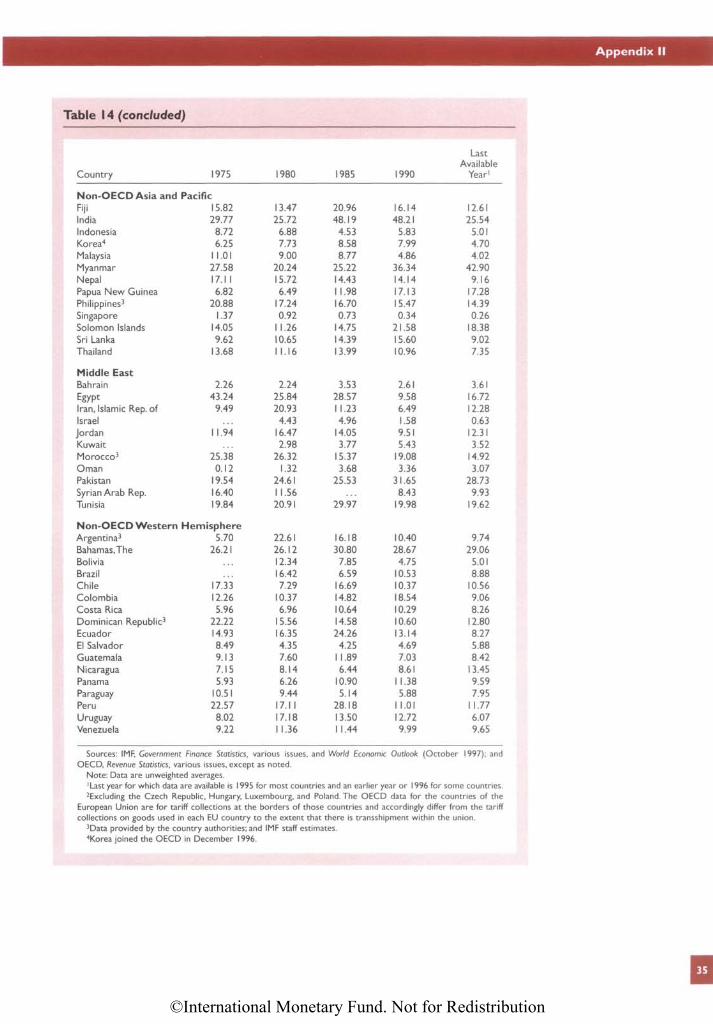

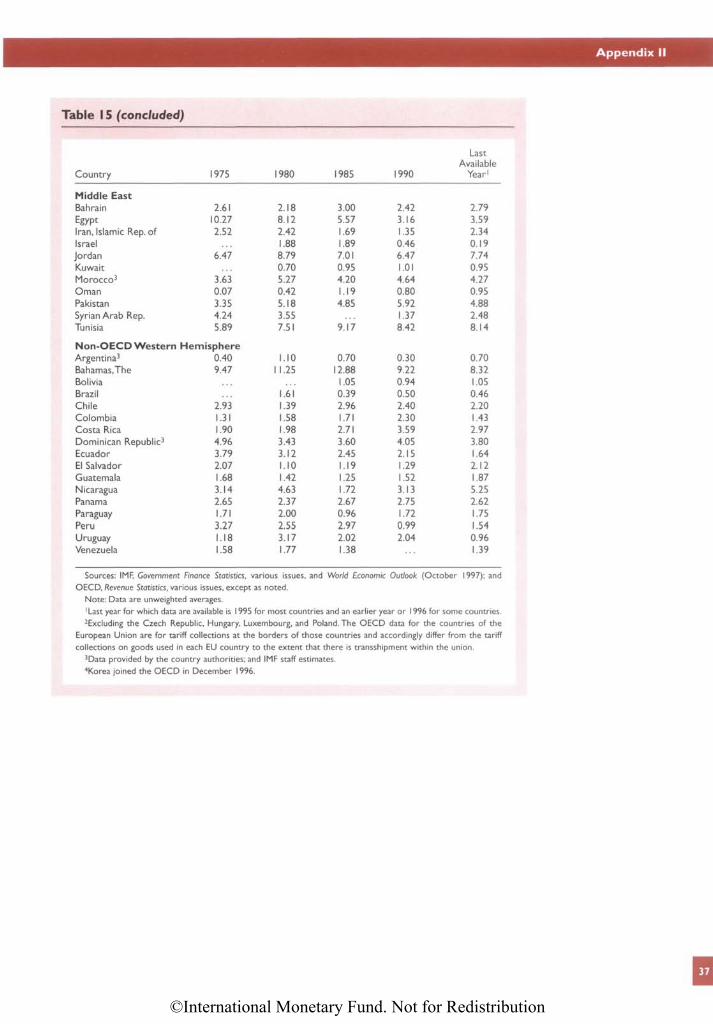

These outcomes, however, conceal considerablevariation within regions (Table 14 in Appendix II).Among countries in sub-Saharan Africa, the tax bur-den on trade varies widely, as have developmentsover time. Collected tariff rates declined in only 8 of17 countries between 1975 and most recently, al-though some did so dramatically (data on other sub-Saharan African countries are incomplete). The re-ductions were greatest in the Democratic Republicof Congo, Ethiopia, and South Africa, all of whichreduced collected tariff rates by more than 50 per-cent.10 Many of the larger economies in Asia(Indonesia, Korea, Malaysia, Singapore, andThailand) experienced lower collected tariff rates.In this region the unweighted average largely re-flects the lack of movement in smaller openeconomies (such as the Solomon Islands), where theimplications of revenue diversification toward do-mestic taxes raise conceptual issues (see Box 3), aswell as in India and Myanmar. In the Middle East,the average collected tariff rate fell in only a fewcountries. These included Egypt (from 43.2 percentin 1975 to 16.7 percent in the last available year),Syrian Arab Rebublic (from 16.4 percent to 9.9 per-

9The data for the European Union represent trade taxes col-lected by individual EU members and transferred to the centralEU budget. Since goods are freely transshipped within the union,collections for individual countries can overstate or understatetrade taxes on goods for domestic use. For example, the data forthe Netherlands include taxes levied on goods transshipped toGermany.

10Absent detailed information on these cases, the possibilitythat the fall in the collected tariff rate in individual cases reflecteda collapse in administrative abilities cannot be ruled out.

13

©International Monetary Fund. Not for Redistribution

Ill ANALYSIS OF TRADE LIBERALIZATION AND REVENUE DEVELOPMENTS

Table I. Collected Tariff Rates by World Region(In percent of value of imports)

Last

AvailableRegion 1975 1980 1985 1990 Year1

All countries 12.62 11.36 12.27 11.05 9.70

OECD2 5.81 4.19 3.51 2.88 1.69

Non-OECD 15.64 14.27 15.89 14.37 12.91

Africa 19.31 17.36 19.09 18.17 16.01

Asia and Pacific 14.05 12.04 15.63 16.51 13.13

Middle East 16.47 14.33 14.07 10.70 11.39

Western Hemisphere 12.37 12.67 13.77 11.09 10.26

Sources: IMF, Government Finance Statistics, various issues, and World Economic Outlook (October 1997); and

OECD, Revenue Statistics, various issues.

Note: Data are unweighted averages.1Last year for which data are available is 1995 for most countries and an earlier year or 1996 for some countries.

Excluding the Czech Republic, Hungary, Luxembourg, and Poland.

cent), Morocco (from 25.4 percent to 14.9 percent),and Israel (from 4.4 percent in 1980 to 0.6 percent).In the Western Hemisphere, the apparent lack ofprogress obscures significant liberalization in thelargest economies, notably Brazil and Argentina,and may again reflect the difficulties of the smaller,more open economies (The Bahamas being an ex-treme example) in diversifying the tax base.

The previous section stressed that trade liberaliza-tion need not result, in the short run, in a decline intrade tax revenue. Over time, however, as tariffstructures move away from initially restrictive con-ditions, the shares of trade tax receipts will mostlikely decline. Table 2 summarizes, by region, trendsin the collection of trade tax revenue as a percentageof GDP over the past 20 years. The numbers suggestthat trade liberalization over this relatively long pe-riod has, on average, resulted in a decline in trade taxrevenue. Trade taxes for the full sample have dimin-ished modestly, from 4.2 percent of GDP in 1975 to3.2 percent most recently.

All regions witnessed declines in the ratio of tradetax revenue to GDP. The sharpest reductions havebeen in export taxes. Note that the Asia grouping ac-tually witnessed some increase in the ratio of importduties to GDP, whereas in the Africa grouping thatshare was broadly unchanged. Both groupingsrecorded decreases in their collected tariff rates overthe same period. In the 1985-95 period, when tradeliberalization in general accelerated, the proportion-ate decline in collected tariff rates was greater thanthat in the ratio of import duties to GDP. During thatsame period, the ratio of imports to GDP rose from

30 1/2 percent to 32 1/4 percent, likely reflecting the im-pact of liberalization.

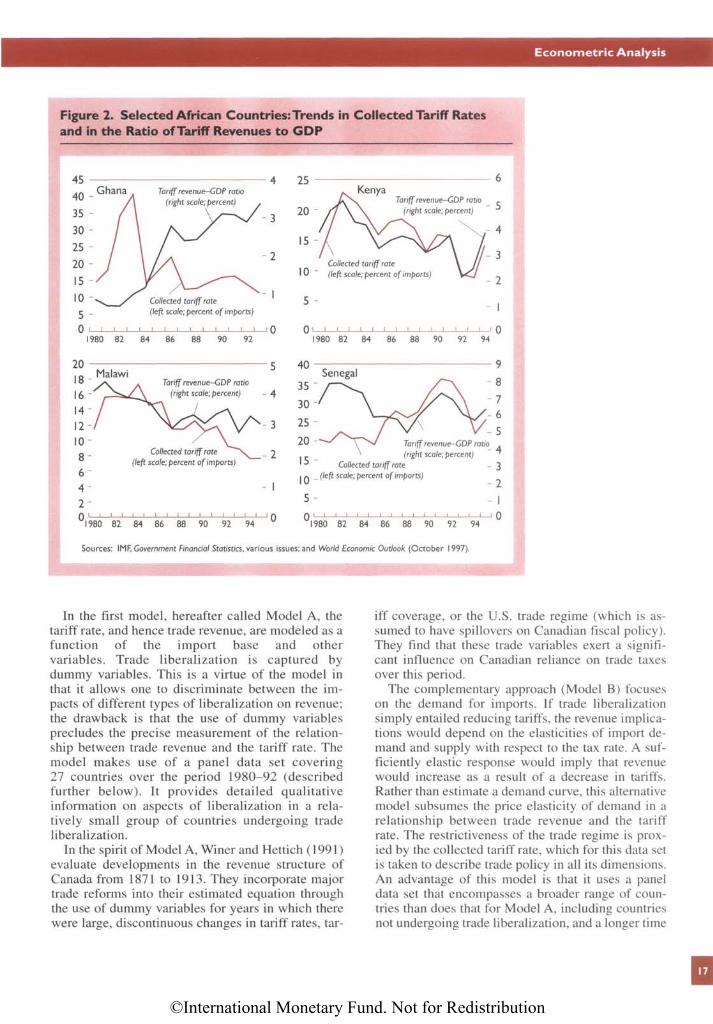

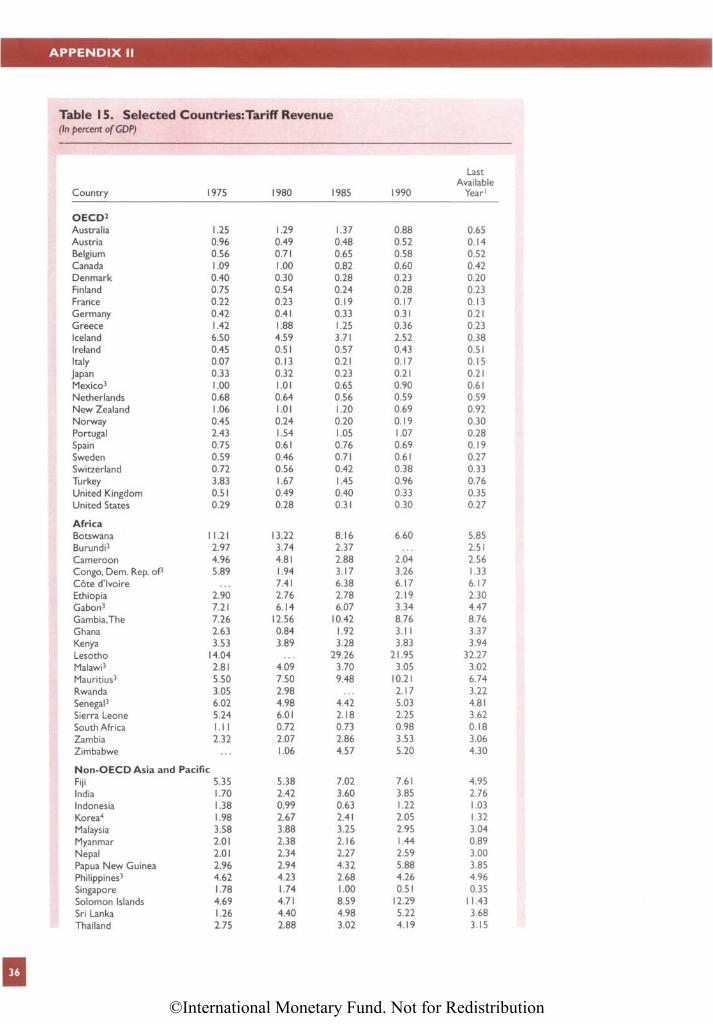

Table 15 in Appendix II presents trends in the ratioof tariffs to GDP for individual countries. Again,there is considerable variation. Perhaps of greatestinterest is how movements in collected tariff ratesand the ratio of tariff revenue to GDP have differedfor individual countries. Specifically, there is someadditional support for the proposition that the collected tariff rate may be a better indicator of tradeliberalization than the GDP share of tariff revenue.For the Africa grouping, where trade liberalizationwas typically a late-1980s phenomenon, examples ofwhere the collected tariff rate points to liberalizationwhereas the ratio of tariffs to GDP increases or declines only modestly include Ghana, Kenya, Malawi,and (in the 1990s) Senegal (Figure 2). Among theAsian countries, in the Philippines in recent years thecollected tariff rate has declined even as the ratio oftariff revenue to GDP has increased; for Singapore,on the other hand, both variables fell over the sample period; this, however, is a case where liberaliza-tion has proceeded to the point where revenue lossesare likely to be inevitable. Singapore shares this pat-tern with many of the OECD countries. In the case ofthe non-OECD Western Hemisphere grouping, thepattern in recent years (1985 to the most recent yearavailable) is one of relatively similar movements inboth the collected tariff rate and the ratio of tariffrevenue to GDP. For this grouping, the typical re-liance on tariff revenue (as a percentage of GDP) isintermediate between the OECD and the African ex-perience, suggesting that these countries may on av-

14

©International Monetary Fund. Not for Redistribution

Econometric Analysis

Box 3. Trade Liberalization in Small, Open Economies

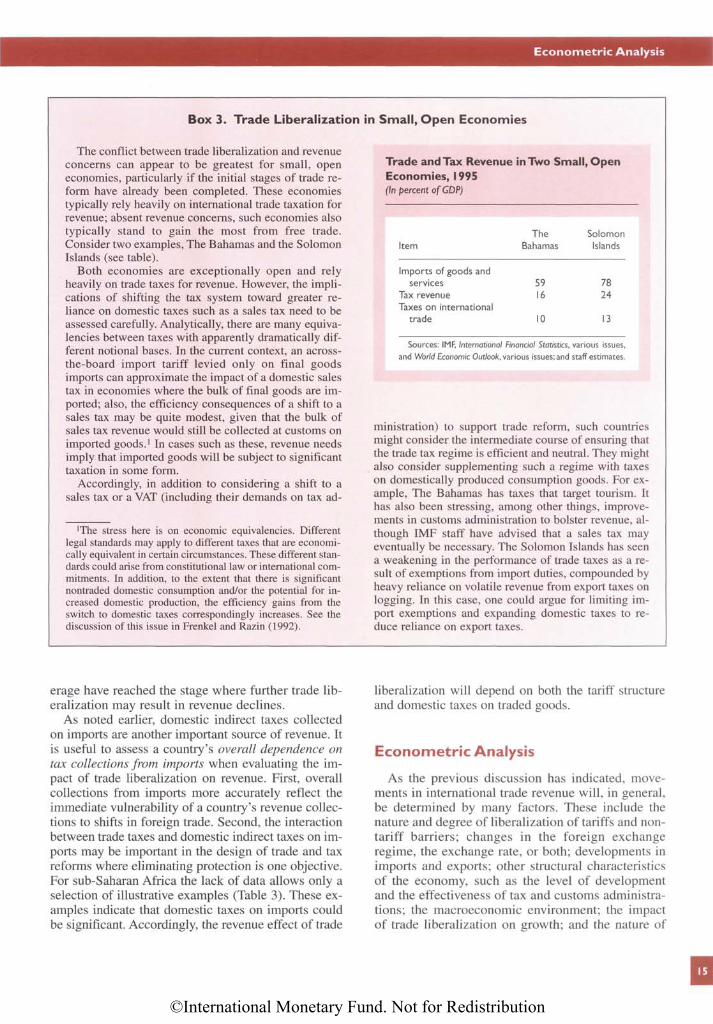

The conflict between trade liberalization and revenueconcerns can appear to be greatest for small, openeconomies, particularly if the initial stages of trade re-form have already been completed. These economiestypically rely heavily on international trade taxation forrevenue; absent revenue concerns, such economies alsotypically stand to gain the most from free trade.Consider two examples, The Bahamas and the SolomonIslands (see table).

Both economies are exceptionally open and relyheavily on trade taxes for revenue. However, the impli-cations of shifting the tax system toward greater re-liance on domestic taxes such as a sales tax need to beassessed carefully. Analytically, there are many equiva-lencies between taxes with apparently dramatically dif-ferent notional bases. In the current context, an across-the-board import tariff levied only on final goodsimports can approximate the impact of a domestic salestax in economies where the bulk of final goods are im-ported; also, the efficiency consequences of a shift to asales tax may be quite modest, given that the bulk ofsales tax revenue would still be collected at customs onimported goods.1 In cases such as these, revenue needsimply that imported goods will be subject to significanttaxation in some form.

Accordingly, in addition to considering a shift to asales tax or a VAT (including their demands on tax ad-