Embed Size (px)

Citation preview

Revenue Equivalence and Bidding Behavior in a Multi-Unit Auction Market: An EmpiricalAnalysisAuthor(s): Rafael TenorioSource: The Review of Economics and Statistics, Vol. 75, No. 2 (May, 1993), pp. 302-314Published by: The MIT PressStable URL: http://www.jstor.org/stable/2109436 .

Accessed: 24/06/2014 21:13

Your use of the JSTOR archive indicates your acceptance of the Terms & Conditions of Use, available at .http://www.jstor.org/page/info/about/policies/terms.jsp

.JSTOR is a not-for-profit service that helps scholars, researchers, and students discover, use, and build upon a wide range ofcontent in a trusted digital archive. We use information technology and tools to increase productivity and facilitate new formsof scholarship. For more information about JSTOR, please contact [email protected].

.

The MIT Press is collaborating with JSTOR to digitize, preserve and extend access to The Review ofEconomics and Statistics.

http://www.jstor.org

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

REVENUE EQUIVALENCE AND BIDDING BEHAVIOR IN A MULTI-UNIT AUCTION MARKET:

AN EMPIRICAL ANALYSIS

Rafael Tenorio*

Abstract-Revenue-equivalence of competitive and discrimi- natory formats is a major result for private-value multi-unit auctions with risk-neutral bidders. Among the factors that may cause this result to break down, the most notorious ones are risk-aversion, value-affiliation, and endogenous bidder participation. Using data from competitive and discriminatory auctions undertaken in the Zambian foreign exchange market, I analyze revenue-equivalence and other bidding phenomena. The results indicate that (i) competitive auctions were rev- enue-superior due to higher participation; (ii) high bidders adjusted with delay to an auction format change; and (iii) a reservation bid was used as a policy instrument.

I. Introduction

M ultiple unit auctions have been extensively used for allocating financial and monetary

instruments in a large number of countries. Trad- ing of securities, bonds, and bills has taken place using these auctions for several decades and, more recently, several countries have also used them in their foreign exchange markets.

In these auctions, bidders bid for both prices and quantities. Two formats have been used: discriminatory, where bidders pay their own bid prices for each unit they get; and competitive, where bidders pay the lowest accepted bid price for each unit they get.' The desirability of these rules has been debated at both the theoretical

and policy levels. The revenue-generating capa- bilities of the different formats has been among the foremost issues at debate.2

An important result in auction theory is the "revenue-equivalence" theorem (Vickrey, 1961, 1962), which states that under certain conditions various auction formats yield the same expected revenue to the auctioneer. Much of the literature following Vickrey analyzes the robustness of this result to the introduction of alternative bidding setups.

Controlled experiments have been used to ana- lyze revenue-equivalence. Smith (1982) reports the results of a number of experiments for multi- unit auctions in which bidders submit single unit bids. No conclusive support (or lack thereof) for revenue-equivalence was found in these experi- ments.3

Several studies have also focused on the com- parison of revenues from the sealed-bid and open timber auctions in the U.S. Pacific Northwest. Mead (1966) does not find significant revenue differences between the high bids observed under both auctions. Johnson (1979) using an extended data set finds that sealed-bid auctions yield larger high bids than open auctions. However, Hansen (1985, 1986) notes that these studies fail to cor- rect for auction method selection bias. After cor- recting for this bias, Hansen's results show that the difference in high bids in both auctions is statistically insignificant. Received for publication February 8, 1991. Revision ac-

cepted for publication April 3, 1992. * University of Notre Dame. This paper is based on chapter 6 of my Ph.D. thesis at Johns

Hopkins University. I thank my advisors Edi Karni and Joe Harrington, Jr. for guidance and valuable suggestions. Ron Balvers, Jeff Bergstrand, Steve Blough, Gabriella Bucci, Roberto Chang, Tom Cosimano, Ken Hendricks, Rich Shee- han, participants at the Spring 1991 Mid-West International Economics Conference at Northwestern University and the 1992 Winter Meetings of the Econometric Society at New Orleans, and three anonymous referees also offered useful comments. The usual disclaimer applies.

1The multi-unit equivalent of a second-price auction has not been used in practice. This would be an auction where all winners paid the highest rejected bid price for every unit they received.

2 For the debate on alternative T-Bill auction systems, see Brimmer (1962), Friedman (1963, 1964), and Rieber (1964). Krumm (1985) and Tenorio (1992b) survey foreign exchange auctions.

3These results arise from a number of both common and private value experiments. With common values, in eight of fourteen cases the revenue is larger in competition than in discrimination. With private values, the revenue is larger in discrimination with inelastic demand, and larger in competi- tion with elastic demand. Harris and Raviv (1981) summarizes some results that reinforce this lack of conclusiveness.

[ 302 ] Copyright ? 1993

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

REVENUE-EQUIVALENCE AND BIDDING BEHAVIOR 303

In this paper I use information from the Zam- bian foreign exchange auction market to analyze bidding behavior, with emphasis on revenue- equivalence. This country sequentially used first competitive and then discriminatory auctions on a weekly basis from late 1985 to-early 1987. Since this sequentiality allows the comparison of bid- ding behavior across formats, I use it to statisti- cally test the effects of the regime change on auction prices.

The tests presented seek to determine whether or not, controlling for relevant factors, the change in format introduced a "shock" to the behavior of bidders. If revenue-equivalence holds, a regime change should exert no perceivable shock on the motion of the clearing rate or average revenue at the auction.4 If revenue-equivalence is rejected, specific characteristics of the bidding environ- ment provide an explanation for the resulting non-equivalence. Section IIB elaborates on this point.

The statistical approach used is a mixture of intervention analysis (Box and Tiao, 1975), and transfer function models (Box and Jenkins, 1970). This approach allows one to (a) ascertain the effects of exogenous interventions over the mo- tion of target variables, and (b) control for other factors that may affect the targets.

The results of these tests uniformly indicate that the competitive auction yielded a higher average revenue than the discriminatory auction. This revenue disparity is statistically explained by a higher effective bidder participation under the competitive format. Differences in effective par- ticipation, in turn, may priginate in the different costs that bidders incur in preparing bidding strategies under each format. This result is recon- cilable with the theoretical prediction that strate- gies are more straightforward to compute in com- petitive auctions than in discriminatory auctions. Additional results suggest that representative agents who consistently bid high showed delayed adjustment to the regime change, and that the minimum bid was likely a dummy bid entered by the auctioneer.

II. Analytical Issues

A. The Bidding Environment

This market consists of n bidders competing for the purchase of D divisible units. D is an- nounced prior to the auction and bidders submit bids of the form:

si= (xi,qi) (1)

where xi is the per-unit price that bidder i is willing to pay, and qi is the number of units i wants to purchase. These bids are then arranged in decreasing price order, and the cutoff between successful and unsuccessful bidders is determined at si, where (x >2 * * * > xi 2 * * x1) and Ej'qi = D. If this equality is not satisfied for any j, bidder j gets a residual quantity. In the competi- tive auction, winners pay xi for each unit they get. In the discriminatory auction, winners pay their own bid prices for each unit they get, and the clearing rate is a quantity-weighted average of all winning prices.

To analyze bidder i's problem, suppose that he is a producer endowed with the technology ,pi(.,. ), which uses two inputs to produce a good to be sold in the domestic market at the price Pi. The first input k is a fixed factor domestically acquired at a given price Pk. The second input is an intermediate good m which is purchased in the international market at an exogenous price denominated in foreign currency Pm. If i pays a price y per unit of foreign exchange, his con- strained utility function is

Ui(m, y) = UiQ PiAi(k, m) - Pkk - Ymm], (2a)

subject to Pmm = qi where Ui is a Von Neu- mann-Morgenstern utility function (Ui' > 0), and bars over variables indicate that they are given. The constraint is a strict equality because, by auction rules, winning bidders should spend the foreign exchange on the imported good.5 Substi-

4Although the revenue-equivalence theorem is stated in exante terms, it is common to use expost realizations of auctions' outcomes to test its predictions.

SThe likelihood of speculation or inventory holding is prac- tically eliminated by the auction rules. These rules restrict entry to importers holding import licenses, and even pro-forma import invoices in some cases.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

304 THE REVIEW OF ECONOMICS AND STATISTICS

tuting the constraint into the utility function:

Ui(qi/pm, y)

= Ui [ PiAi(k, qi/Pm)-Pik-yqi] (2b)

Since k and Pm are fixed, we may rewrite Ai(-, *)as ui(qi), where u'(qi) > 0. Omitting constant terms, and normalizing Pij to one:

Ui(qi, y) = Ui[ui(qi) -yqi]. (3)

Accordingly, i's payoffs in each auction are (a) Discriminatory Auction:

Ui [ui( qi) - xiqi], Xi > Yd

pid = i UiNu(i) - Xi'i] Xi =Yd (4)

t0, Xi < Yd

where Yd is the lowest accepted bid, i=

Min{qi, D - Eqj} is the quantity awarded to bid- der i, and Eq, is the sum of the quantities of all non-marginal winners (xj > Yd).

(b) Competitive Auction:

Ui[uif qi)- ycqi], Xi > Yc

piC Lui[ui(qi) -

xiji], xi = Yc (5)

(sO, xi < Yc

where yc is the minimum accepted bid and iji and Eqj remain as defined before.

Given these structures, an analytical approach to these auctions would make some assumptions about bidders' valuations and beliefs, and formu- late the problems as incomplete information games where bidders maximize their expected payoffs. Since this is a highly complex problem, no general model has been developed, and equi- libria have only been derived for special versions of the payoff functions.

B. Expected Revenue in Multi-Unit Auctions

Using an independent private values (i.p.v.) model, Vickrey (1962) first established revenue- equivalence of discriminatory and competitive multi-unit auctions where each bidder bids for one unit (qi = 1).6 This result holds when bidders are risk-neutral (Ui" = 0), symmetric (ui's are

drawn from a common distribution), and valua- tions are independent (ui's are independent draws).

Two important extensions have been derived in the qi = 1 case. Harris and Raviv (1981) showed that even with i.p.v., revenue-equivalence fails to hold if bidders are risk-averse (Ui' < 0). The dis- criminatory auction is revenue-superior in this case. Finally, Weber (1983) broke away from i.p.v. and studied "affiliated" valuations (ui's are non- independent draws).7 He showed that the com- petitive auction yields a higher revenue under these conditions.

Bidder collusion and bidder asymmetries also break down revenue-equivalence in i.p.v. auc- tions. Robinson (1985) showed that collusion is stable in second-price auctions, and unstable in first-price auctions. Thus, the auctioneer should expect a lower revenue under a second-price for- mat. With asymmetric bidders, Maskin and Riley (1985) showed that either format may yield a higher expected revenue.

Endogeneity of qi adds a new dimension to the problem. Engelbrecht-Wiggans (1988) extended revenue-equivalence to i.p.v. auctions where the risk-neutral bidders may take any subset of D subject to each unit going to the bidder that values it the most. This would be possible only if bids were full-demand schedules, or if bidders submitted a separate bid price for each unit. Since demand schedules are not allowed, a com- mon practice is to submit "lumpy" bids, i.e., several units demanded at the same price. This practice may originate in minimum required bid quantities, and costs of bid preparation or sub- mission (Krumm, 1985, and Tenorio, 1992a).

Tenorio (1992a), using a lumpy bid model with i.p.v. and risk-neutral bidders, shows that (i) rev- enue-equivalence holds only if equilibrium quan- tity profiles are equal across auctions, and (ii) expected revenue is higher when bidders bid for larger shares of the object, irrespective of the auction method. Intuitively, if bidders bid for larger shares, this raises the probability that any single bidder may face rationing. Thus, price bid- ding behavior becomes more aggressive. Since

6 Most of the uniform price auctions studied in the litera- ture are auctions where bidders pay the highest rejected rather than the lowest accepted price for each unit they get. Vickrey (1962) shows that, in i.p.v. environments, the expected revenue is the same under both formats.

7Affiliation encompasses both independence and correla- tion of random variables. In simple terms, if a bidder's valua- tion is high, affiliation makes it more likely but does not necessarily imply that other bidders' valuations will also be high.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

REVENUE-EQUIVALENCE AND BIDDING BEHAVIOR 305

this phenomena is format-independent, no spe- cific revenue superiority arises from this model.

All of the previous revenue comparisons are valid if the number of bidders is exogenous. The endogenous participation or "free entry" ap- proach to revenue comparisons establishes that different formats may yield different expected revenues because they attract different sets of bidders (Mathews, 1984, Harstad, 1990, and Samuelson, 1990). Bidder participation depends on factors like reserve prices, information acqui- sition opportunities, and bid preparation costs. If these conditions make participation more attrac- tive under a specific format, the auctioneer can benefit from the increased competitiveness that this represents.8

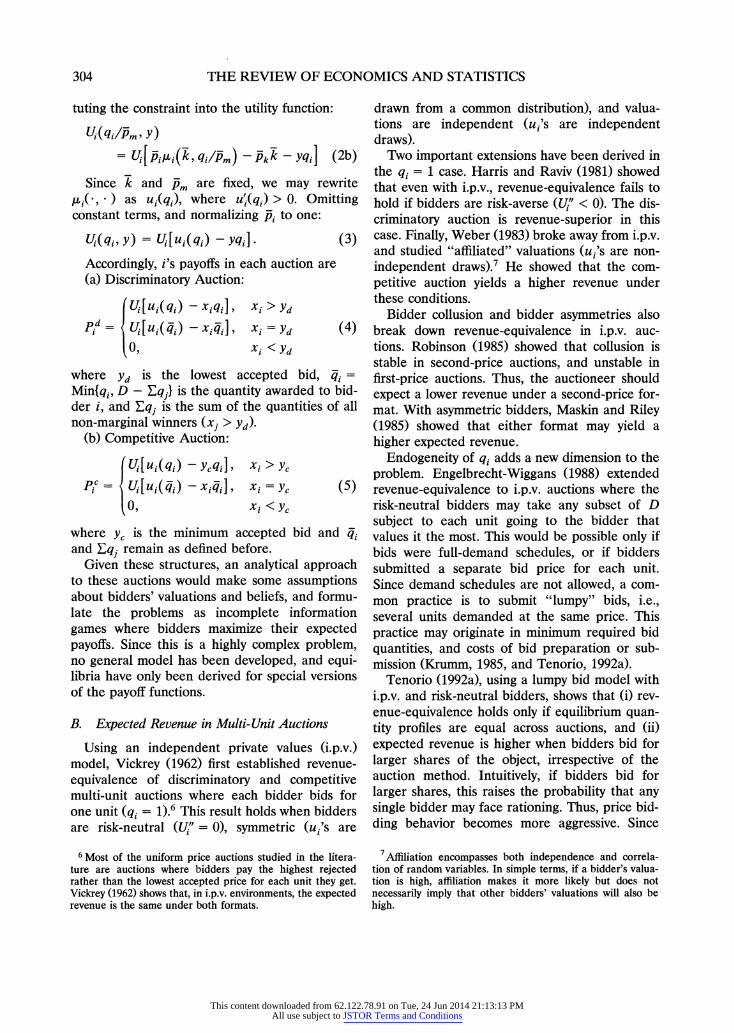

Table 1 summarizes the factors that influence expected revenue comparisons.

Since each model makes specific assumptions in establishing these revenue comparisons, the theory does not tell us what would result from the interaction of all these factors. This lack of gener- ality imposes limitations on the empirical analysis of revenue-equivalence. In particular, as pointed out by McAfee and McMillan (1987a), an ideal test of this hypothesis would require first testing the underlying conditions present in the specific market. In the absence of appropriate informa- tion for such testing in the Zambian case, I pro- ceed to assess the presence of each factor in order to get a more meaningful interpretation of the results.

(a) Affiliation: Since exchange rate forecasts usually depend on both private and public infor- mation, value affiliation will be present in this market. Unfortunately, the extent of its presence is not distinguishable from the bidding data.

(b) Risk-aversion: If the value of individual bids is relatively small with respect to a bidder's total assets, a likely scenario, risk-neutrality or mild risk-aversion appear as reasonable assump- tions. Again, this aspect is not empirically distin- guishable with the information at hand.

(c) Asymmetry: The expected revenue effects of this factor depend on the specific type of asymmetry.9 Since this is unobservable, its impact is ambiguous.

(d) Endogenous quantity choice: Since lumpy bidding is a common practice, the value-mono- tonic case can be ruled out so that revenue non- equivalence is likely. The effects of lumpy bidding can be statistically isolated by controlling for the average quantity demanded at the auction.

(e) Collusion: This is perhaps the least likely factor to be present in this market. The presence of a large number of relatively small bidders is not conducive to the formation of collusive ar- rangements.

(f) Endogenous participation: With no format- specific reserve prices or information acquisition opportunities, bid preparation costs may play a role in attracting bidders and hence in affecting expected revenues. Auction theory predicts that

8 Harstad (1990) actually reaches the opposite conclusion, i.e., that auctions with fewer participants may yield higher expected revenues. However, he acknowledges that this pre- diction is contrary to most empirical evidence.

9Maskin and Riley (1985) conjecture that, with asymmetric bidders, a first-price auction yields a higher expected revenue than an English auction if the bidders have similar valuation distributions but with different supports. No general conclu- sions can be extracted from their exercises.

TABLE 1.-FACrORS AFFEcrING ExPEcrED REVENUES IN MULTI-UNIT AucrIONS

Bidders' Bidders' Bidders' Bid Bidding Revenue Valuations Attitudes Attributes Quantity Behavior Ranking

Independent Risk-Neutral Symmetric Unit Competitive ERd = ERC Affiliated Risk-Neutral Symmetric Unit Competitive ERd < ERC Independent Risk-Averse Symmetric Unit Competitive ERd > ERC Independent Risk-Neutral Asymmetric Unit Competitive ER d?ERC Independent Risk-Neutral Symmetric Endogenous1 Competitive ER d?ERC Independent Risk-Neutral Symmetric Endogenousvm Competitive ERd = ERC Independent Risk-Neutral Symmetric Unit Collusive ERd > ERC

Endogenous bidder participation ERd?ERC

Notes: -Endogenous, denotes lumpy bidding -Endogenousvm denotes bidding that leads to value-monotonic allocations. -"?" denotes uncertainty regarding the direction of the inequality.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

306 THE REVIEW OF ECONOMICS AND STATISTICS

bidding strategies are easier to compute in com- petitive auctions so that "non-specialists" may have less incentive to participate in discrimina- tory auctions.'0 Since the number of bids is ob- servable, this factor can be empirically isolated.

How likely and relatively important is the pres- ence of each factor? Without a panel of data on bidders' attributes and choices, not all of the factors' relative strengths are distinguishable. The results of the revenue-equivalence tests will allow us to indirectly assess these relative bidding forces in the Zambian auction.

III. Data and Methodology

A. The Zambian Foreign Exchange Auction

A foreign exchange auction market was created in Zambia in October 1985.1" The stated goals were to attain a more desirable allocation of foreign exchange and to give greater flexibility to the implementation of stabilization policies.

The auction was conducted by a committee headed by the Bank of Zambia. Auctionable funds came primarily from export proceeds-which were to be surrendered to the monetary authority -and from foreign aid. The weekly supply of U.S. dollars was initially set at $5 million. Al- though always pre-announced, this amount was subsequently managed with flexibility.

Entry was granted to agents holding import licenses. Bids were submitted through commer-

cial banks, specifying the dollar amount desired and the per-unit willingness to pay. A deposit equal to the value of the bid was required.

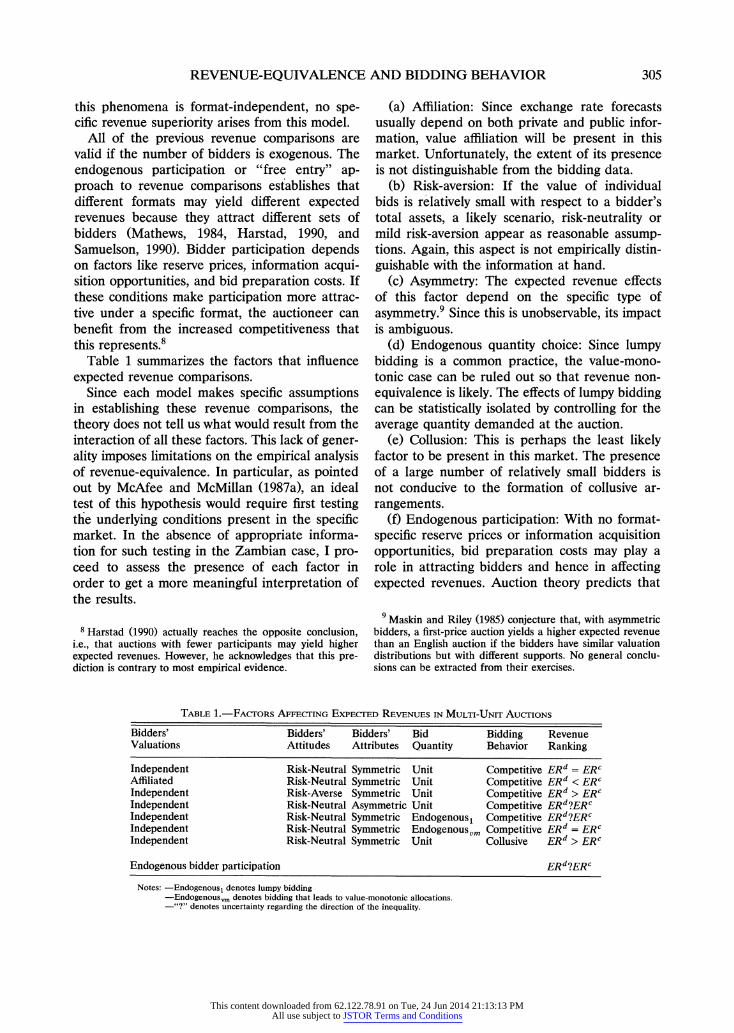

Tables 2 and 3 and graphs 1-3 show the vari- able definitions, summary statistics, and time- series plots of the auction variables. These are based on sixty-eight weekly observations of prices (equilibrium and extreme), total quantities sup- plied and demanded, and numbers of qualified and accepted bids.12

10 Friedman (1963, 1964), in the context of the T-Bill auc- tion, argues that discrimination limits the market to "special- ists" that seek to minimize the premium that they pay over the marginally accepted bid. His argument has recently resur- faced as a result of the bidding irregularities at the U.S. T-Bill auction.

11 Panayotacos (1987) and Aron and Elbadawi (1991) ana- lyze the Zambian experience.

12 Since the supply is perfectly inelastic the terms supply and quantity supplied are used equivalently. The term demand is used to describe the total quantity demanded at an auction, not at the clearing rate. The term "qualified bids" denotes the total number of bids that were considered valid by the auc- tioneer. Bids that failed to meet some requirement are not recorded in this aggregate.

TABLE 2.-VARiABLE DEFINITIONS

BIDS: Number of qualified bids ACBIDS: Number of accepted bids SUPPLY: Amount of dollars auctioned (millions) DEMAND: Amount of dollars demanded (millions) RATE: Clearing rate (Kwacha/Dollar) LOBID: Lowest bid price (Kwacha/Dollar) HIBID: Highest bid price (Kwacha/Dollar) AVGQD: Average quantity of dollars demanded

(= (DEMAND /BIDS) * 106)

CONSTANT: Constant term TREND: Linear time trend

CHANGE: f1, between auctions 43 and 68 0, between auctions 1 and 42

OVERSU: f 1, if SUPPLY < 8.8 \, Oif SUPPLY < 8.8

DOCUM: 1, between auctions 40 and 51 \ 0, otherwise

ADJ: f 1, at auction 43 \ 0, otherwise

Notes: -A superscript "e" will be added to a variable to denote its estimated value.

-The nth lage of a variable x is denoted by x(-n).

TABLE 3.-SUMMARY STATISTICS OF AuCrION VARIABLES

Competitive Discriminatory Total (auctions 1-42) (auctions 43-68) (auctions 1-68)

Period Mean Std. Dev. Mean Std. Dev. Mean Std. Dev.

BIDS 289.29 96.94 458.12 185.03 353.84 160.08 ACBIDS 177.60 48.45 196.96 144.11 185.00 97.36 SUPPLY 5.58 1.59 6.31 3.77 5.86 2.67 DEMAND 8.84 3.54 14.97 5.60 11.19 5.35 RATE 6.57 0.70 10.11 3.39 7.93 2.77 LOBID 5.14 1.10 5.49 0.59 5.28 0.95 HIBID 8.00 1.48 11.56 3.53 9.36 3.02 AVGQD 30584 5901 33384 4530 31655 5586

Data Source: Panayotacos (1987).

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

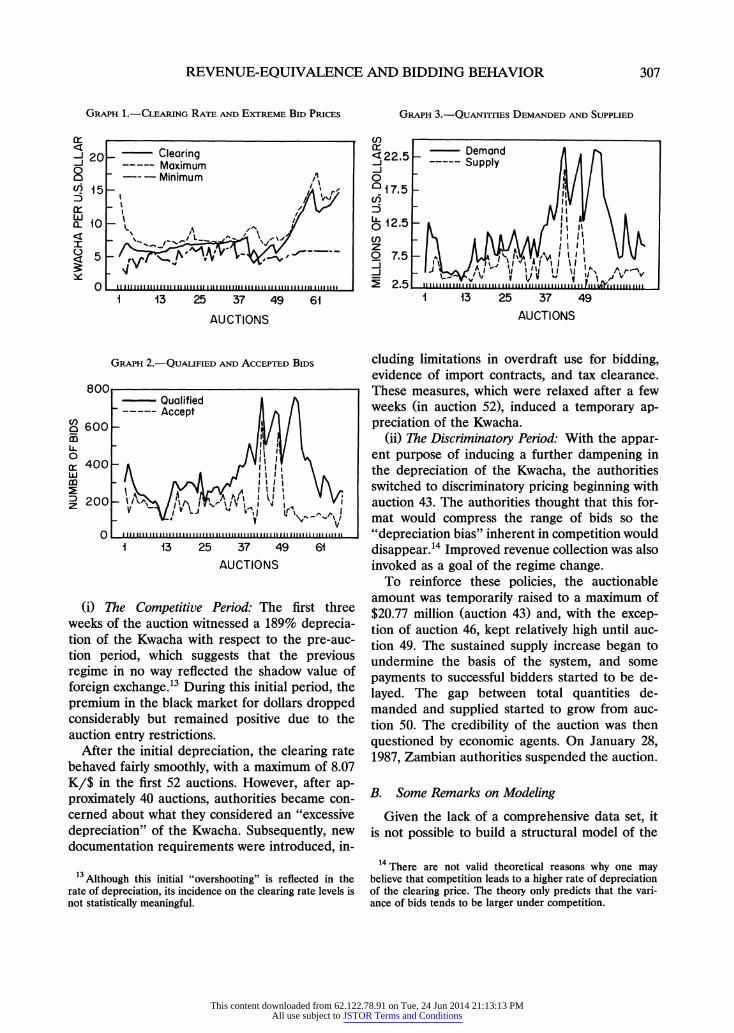

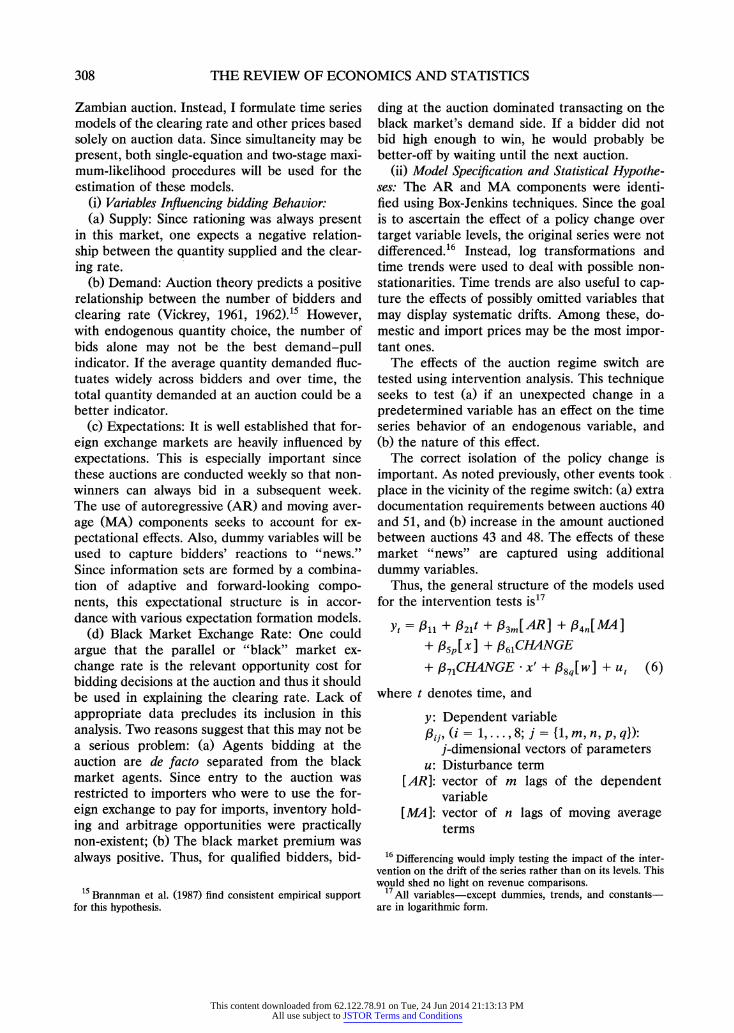

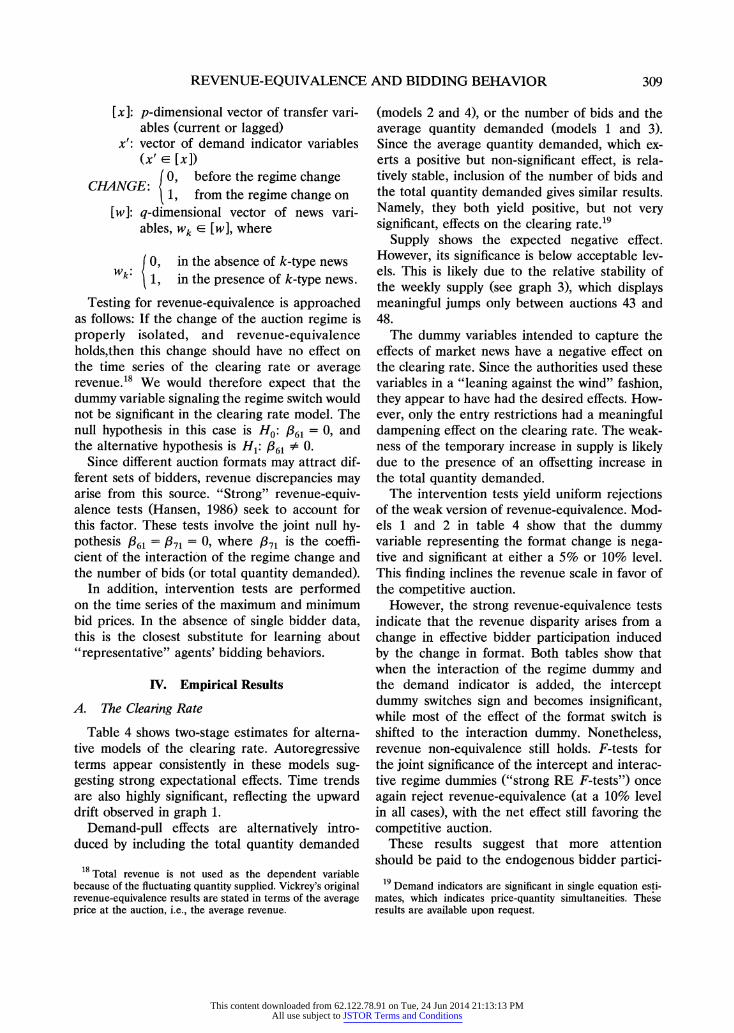

REVENUE-EQUIVALENCE AND BIDDING BEHAVIOR 307

GRAPH 1.-CLEARING RATE AND EXTREME BID PRICES

GRAPH 2.-QUALIFIED AND ACCEPTED BIDS

(i) The Competitive Period: The first three weeks of the auction witnessed a 189% deprecia- tion of the Kwacha with respect to the pre-auc- tion period, which suggests that the previous regime in no way reflected the shadow value of foreign exchange.13 During this initial period, the premium in the black market for dollars dropped considerably but remained positive due to the auction entry restrictions.

After the initial depreciation, the clearing rate behaved fairly smoothly, with a maximum of 8.07 K/$ in the first 52 auctions. However, after ap- proximately 40 auctions, authorities became con- cerned about what they considered an "excessive depreciation" of the Kwacha. Subsequently, new documentation requirements were introduced, in-

cluding limitations in overdraft use for bidding, evidence of import contracts, and tax clearance. These measures, which were relaxed after a few weeks (in auction 52), induced a temporary ap- preciation of the Kwacha.

(ii) The Discriminatory Period: With the appar- ent purpose of inducing a further dampening in the depreciation of the Kwacha, the authorities switched to discriminatory pricing beginning with auction 43. The authorities thought that this for- mat would compress the range of bids so the "depreciation bias" inherent in competition would disappear.14 Improved revenue collection was also invoked as a goal of the regime change.

To reinforce these policies, the auctionable amount was temporarily raised to a maximum of $20.77 million (auction 43) and, with the excep- tion of auction 46, kept relatively high until auc- tion 49. The sustained supply increase began to undermine the basis of the system, and some payments to successful bidders started to be de- layed. The gap between total quantities de- manded and supplied started to grow from auc- tion 50. The credibility of the auction was then questioned by economic agents. On January 28, 1987, Zambian authorities suspended the auction.

B. Some Remarks on Modeling

Given the lack of a comprehensive data set, it is not possible to build a structural model of the

GRAPH 3.-QUANTITIES DEMANDED AND SUPPLIED

13Although this initial "overshooting" is reflected in the rate of depreciation, its incidence on the clearing rate levels is not statistically meaningful.

14 There are not valid theoretical reasons why one may believe that competition leads to a higher rate of depreciation of the clearing price. The theory only predicts that the vari- ance of bids tends to be larger under competition.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

308 THE REVIEW OF ECONOMICS AND STATISTICS

Zambian auction. Instead, I formulate time series models of the clearing rate and other prices based solely on auction data. Since simultaneity may be present, both single-equation and two-stage maxi- mum-likelihood procedures will be used for the estimation of these models.

(i) Variables Influencing bidding Behavior: (a) Supply: Since rationing was always present

in this market, one expects a negative relation- ship between the quantity supplied and the clear- ing rate.

(b) Demand: Auction theory predicts a positive relationship between the number of bidders and clearing rate (Vickrey, 1961, 1962).15 However, with endogenous quantity choice, the number of bids alone may not be the best demand-pull indicator. If the average quantity demanded fluc- tuates widely across bidders and over time, the total quantity demanded at an auction could be a better indicator.

(c) Expectations: It is well established that for- eign exchange markets are heavily influenced by expectations. This is especially important since these auctions are conducted weekly so that non- winners can always bid in a subsequent week. The use of autoregressive (AR) and moving aver- age (MA) components seeks to account for ex- pectational effects. Also, dummy variables will be used to capture bidders' reactions to "news." Since information sets are formed by a combina- tion of adaptive and forward-looking compo- nents, this expectational structure is in accor- dance with various expectation formation models.

(d) Black Market Exchange Rate: One could argue that the parallel or "black" market ex- change rate is the relevant opportunity cost for bidding decisions at the auction and thus it should be used in explaining the clearing rate. Lack of appropriate data precludes its inclusion in this analysis. Two reasons suggest that this may not be a serious problem: (a) Agents bidding at the auction are de facto separated from the black market agents. Since entry to the auction was restricted to importers who were to use the for- eign exchange to pay for imports, inventory hold- ing and arbitrage opportunities were practically non-existent; (b) The black market premium was always positive. Thus, for qualified bidders, bid-

ding at the auction dominated transacting on the black market's demand side. If a bidder did not bid high enough to win, he would probably be better-off by waiting until the next auction.

(ii) Model Specification and Statistical Hypothe- ses: The AR and MA components were identi- fied using Box-Jenkins techniques. Since the goal is to ascertain the effect of a policy change over target variable levels, the original series were not differenced.16 Instead, log transformations and time trends were used to deal with possible non- stationarities. Time trends are also useful to cap- ture the effects of possibly omitted variables that may display systematic drifts. Among these, do- mestic and import prices may be the most impor- tant ones.

The effects of the auction regime switch are tested using intervention analysis. This technique seeks to test (a) if an unexpected change in a predetermined variable has an effect on the time series behavior of an endogenous variable, and (b) the nature of this effect.

The correct isolation of the policy change is important. As noted previously, other events took place in the vicinity of the regime switch: (a) extra documentation requirements between auctions 40 and 51, and (b) increase in the amount auctioned between auctions 43 and 48. The effects of these market "news" are captured using additional dummy variables.

Thus, the general structure of the models used for the intervention tests iS17

Yt = f11 + f21t + 3m[AR] + 834A[MA]

+f35p[X] +J361CHANGE

+ )371CHANGE x' + P8q[W] + Ut (6)

where t denotes time, and

y: Dependent variable Pij, (i = 1...8; j = {1,m,n, p,q}):

j-dimensional vectors of parameters u: Disturbance term

[AR]: vector of m lags of the dependent variable

[MAL]: vector of n lags of moving average terms

15 Brannman et al. (1987) find consistent empirical support for this hypothesis.

16 Differencing would imply testing the impact of the inter- vention on the drift of the series rather than on its levels. This would shed no light on revenue comparisons.

17 All variables-except dummies, trends, and constants- are in logarithmic form.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

REVENUE-EQUIVALENCE AND BIDDING BEHAVIOR 309

[x]: p-dimensional vector of transfer vari- ables (current or lagged)

x': vector of demand indicator variables (x' E [x])

CHAL4NGE ?0, before the regime change 1 , from the regime change on

[w]: q-dimensional vector of news vari- ables, Wk E [w], where

( O, in the absence of k-type news Wk: 1 , in the presence of k-type news.

Testing for revenue-equivalence is approached as follows: If the change of the auction regime is properly isolated, and revenue-equivalence holds,then this change should have no effect on the time series of the clearing rate or average revenue.18 We would therefore expect that the dummy variable signaling the regime switch would not be significant in the clearing rate model. The null hypothesis in this case is Ho: f61 = 0, and the alternative hypothesis is Hl: f61 $ 0.

Since different auction formats may attract dif- ferent sets of bidders, revenue discrepancies may arise from this source. "Strong" revenue-equiv- alence tests (Hansen, 1986) seek to account for this factor. These tests involve the joint null hy- pothesis f61 - =71 = 0, where f71 is the coeffi- cient of the interaction of the regime change and the number of bids (or total quantity demanded).

In addition, intervention tests are performed on the time series of the maximum and minimum bid prices. In the absence of single bidder data, this is the closest substitute for learning about ''representative" agents' bidding behaviors.

IV. Empirical Results

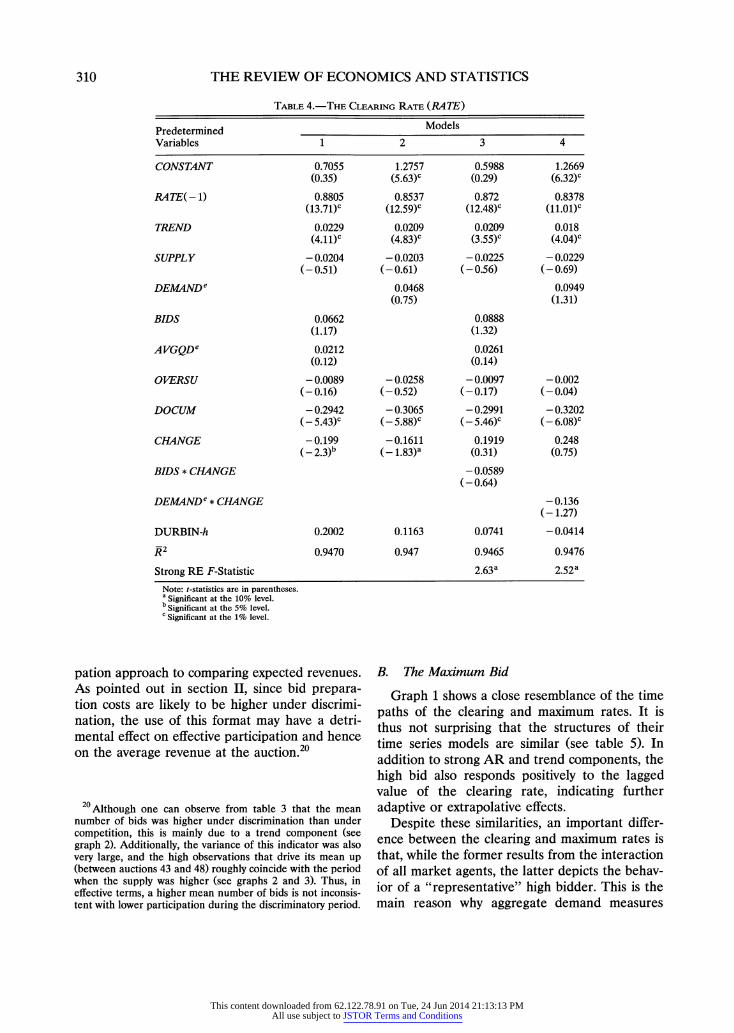

A. The Clearing Rate

Table 4 shows two-stage estimates for alterna- tive models of the clearing rate. Autoregressive terms appear consistently in these models sug- gesting strong expectational effects. Time trends are also highly significant, reflecting the upward drift observed in graph 1.

Demand-pull effects are alternatively intro- duced by including the total quantity demanded

(models 2 and 4), or the number of bids and the average quantity demanded (models 1 and 3). Since the average quantity demanded, which ex- erts a positive but non-significant effect, is rela- tively stable, inclusion of the number of bids and the total quantity demanded gives similar results. Namely, they both yield positive, but not very significant, effects on the clearing rate.19

Supply shows the expected negative effect. However, its significance is below acceptable lev- els. This is likely due to the relative stability of the weekly supply (see graph 3), which displays meaningful jumps only between auctions 43 and 48.

The dummy variables intended to capture the effects of market news have a negative effect on the clearing rate. Since the authorities used these variables in a "leaning against the wind" fashion, they appear to have had the desired effects. How- ever, only the entry restrictions had a meaningful dampening effect on the clearing rate. The weak- ness of the temporary increase in supply is likely due to the presence of an offsetting increase in the total quantity demanded.

The intervention tests yield uniform rejections of the weak version of revenue-equivalence. Mod- els 1 and 2 in table 4 show that the dummy variable representing the format change is nega- tive and significant at either a 5% or 10% level. This finding inclines the revenue scale in favor of the competitive auction.

However, the strong revenue-equivalence tests indicate that the revenue disparity arises from a change in effective bidder participation induced by the change in format. Both tables show that when the interaction of the regime dummy and the demand indicator is added, the intercept dummy switches sign and becomes insignificant, while most of the effect of the format switch is shifted to the interaction dummy. Nonetheless, revenue non-equivalence still holds. F-tests for the joint significance of the intercept and interac- tive regime dummies ("strong RE F-tests") once again reject revenue-equivalence (at a 10% level in all cases), with the net effect still favoring the competitive auction.

These results suggest that more attention should be paid to the endogenous bidder partici-

18 Total revenue is not used as the dependent variable because of the fluctuating quantity supplied. Vickrey's original revenue-equivalence results are stated in terms of the average price at the auction, i.e., the average revenue.

19 Demand indicators are significant in single equation esti- mates, which indicates price-quantity simultaneities. These results are available upon request.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

310 THE REVIEW OF ECONOMICS AND STATISTICS

TABLE 4. -THE CLEARING RATE (RATE)

Predetermined Models Variables 1 2 3 4

CONSTANT 0.7055 1.2757 0.5988 1.2669 (0.35) (5.63)c (0.29) (6.32)c

RATE(- 1) 0.8805 0.8537 0.872 0.8378 (13.71)c (12.59)c (12.48)c (11.01)c

TREND 0.0229 0.0209 0.0209 0.018 (4.11)c (4.83)c (3.55)C (4.04)c

SUPPLY - 0.0204 - 0.0203 - 0.0225 - 0.0229 (-0.51) (-0.61) (-0.56) (-0.69)

DEMANDe 0.0468 0.0949 (0.75) (1.31)

BIDS 0.0662 0.0888 (1.17) (1.32)

AVGQDe 0.0212 0.0261 (0.12) (0.14)

OVERSU - 0.0089 - 0.0258 - 0.0097 - 0.002 (-0.16) (-0.52) (-0.17) (-0.04)

DOCUM - 0.2942 - 0.3065 - 0.2991 - 0.3202 ( _ 5.43)C (- 5.88)c (- 5.46)C ( 6.08)c

CHIANGE -0.199 -0.1611 0.1919 0.248 (_2.3)b (-1.83)a (0.31) (0.75)

BIDS * CIIANGE - 0.0589 (-0.64)

DEMANDe * CHANGE -0.136 (-1.27)

DURBIN-h 0.2002 0.1163 0.0741 - 0.0414

R2 0.9470 0.947 0.9465 0.9476

Strong RE F-Statistic 2.63a 2.52a

Note: t-statistics are in parentheses. a Significant at the 10% level. b Significant at the 5% level. c Significant at the 1% level.

pation approach to comparing expected revenues. As pointed out in section II, since bid prepara- tion costs are likely to be higher under discrimi- nation, the use of this format may have a detri- mental effect on effective participation and hence on the average revenue at the auction.20

B. The Maximum Bid

Graph 1 shows a close resemblance of the time paths of the clearing and maximum rates. It is thus not surprising that the structures of their time series models are similar (see table 5). In addition to strong AR and trend components, the high bid also responds positively to the lagged value of the clearing rate, indicating further adaptive or extrapolative effects.

Despite these similarities, an important differ- ence between the clearing and maximum rates is that, while the former results from the interaction of all market agents, the latter depicts the behav- ior of a "representative" high bidder. This is the main reason why aggregate demand measures

20Although one can observe from table 3 that the mean number of bids was higher under discrimination than under competition, this is mainly due to a trend component (see graph 2). Additionally, the variance of this indicator was also very large, and the high observations that drive its mean up (between auctions 43 and 48) roughly coincide with the period when the supply was higher (see graphs 2 and 3). Thus, in effective terms, a higher mean number of bids is not inconsis- tent with lower participation during the discriminatory period.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

REVENUE-EQUIVALENCE AND BIDDING BEHAVIOR 311

play practically no role in explaining this variable, a fact that is also reflected in the insignificance of the documentation dummy. As seen in table 5, since a high bidder will win even when the supply is low, the quantity supplied is also insignificant. A somewhat surprising result is the positive-and borderline significant in one case-effect exerted by the oversupply dummy. This may be explained by a price-quantity correlation of optimal bids.2'

Model 1 in table 5 shows that the regime switch dummy is negative and significant at a 10% level. This supports the theoretical claim that a representative agent's bid should be lower under discrimination than under competition. If this bid depicts the behavior of a representative

agent that bids consistently high, one could spec- ulate that its behavior may not be very responsive to the arrival of new information. A relevant question then arises: does the representative high bidder adjust differently to the regime change than the average bidder?

One can obtain a rough answer to this question by moving the intervention dummy one week forward. Since the absolute value of this variable is larger and more significant than at the time of the change (see model 2), this suggests that high bidders displayed a stronger adjustment to the regime change with a one-week delay (perhaps after realizing that some money had been left on the table!). A more polished test of this conjec- ture is to include an adjustment dummy at the week of the change, and to forward the regime dummy one week ahead. This version, shown in model 3, supports the previous result, indicating

21 Tenorio (1992a) shows that when bidders bid for more units, a "fear of rationing" effect may also induce them to bid for higher prices.

TABLE 5.-THE MAXIMUM BID PRICE (HIBID)

Predetermined Models Variables 1 2 3

CONSTANT 1.1408 1.53 1.3108 (3.2)c (4.44)C (3.51)c

HIBID -1) 0.7549 0.7792 0.8219 (12.65)c (14.43)c (17.09)c

TREND 0.0139 0.017 0.0216 (4.05)c (4.24)c (4.4)C

RATE(- 1) 0.3512 0.2232 0.2084 (3.42)c (2.01)b (1.89)a

SUPPLY -0.004 -0.0144 -0.015 (-0.14) (-0.49) (-0.54)

BIDS -0.234 -0.0618 -0.0418 (-0.5) (-1.33) (-0.89)

OVERSU 0.6457 0.0492 0.0914 (1.26) (1.06) (1.85)a

DOCUM -0.0249 -0.0389 -0.0288 (-0.49) (-0.77) (-0.58)

CHANGE -0.1596 (-1.86)a

CHANGE( + 1) -0.1844 -0.3324 (-_2.33) b ( _ 3.07)C

ADJ -0.1535 (-1.83)a

DURBIN-h 1.4382 1.033 1.1842

Rj2 0.9396 0.9408 0.9391

Note: t-statistics are in parentheses. a Significant at the 10% level. b Significant at the 5% level. c Significant at the 1% level.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

312 THE REVIEW OF ECONOMICS AND STATISTICS

modest adjustment during the first week and a stronger adjustment thereafter.22'23

C. The Minimum Bid

The time-series models for the minimum bid show important differences compared to the clearing and maximum prices. Graph 1 shows that the minimum bid does not display any mean- ingful trend, which explains this term's absence in the models of table 6. In addition, besides an AR term, this variable also displays a significant MA component, and the R2 -is substantially lower than in the other cases.

These differences suggest that there may be something inherently different about the mini-

mum bid compared to the clearing and maximum prices. Two features stand out when assessing the determinants of this variable. First, as was the case with the maximum bid, the minimum bid's behavior is associated to a specific set of agents. Second, it is also possible that, although not explicitly documented, this variable was a reser- vation bid entered by the auctioneer.24 This bid would reflect the Bank's minimum valuation for foreign exchange, and would prevent the clearing rate from hitting rather low levels. Hence it is likely that at some points in time this variable was determined by bidding behavior, while at other times it was an instrument.

The results in table 6 support the suggested presence of a reservation bid. Model 1 shows that

22 This finding, although intuitively appealing, does not have a theoretical counterpart.

23 This delayed adjustment is unique to the maximum bid. The clearing rate does not display the same feature. Results are available upon request.

24 Explicit reservation bids have been common in other foreign exchange auctions. Dominguez (1991) discusses the Bolvian case.

TABLE 6.-THE MINIMUM BID PRICE (LOBID)

Predetermined Models Variables 1 2 3 4

CONSTANT 1.722 1.0836 1.3906 1.3247 (4.37)C (3.60)c (3.55)C (3.67)c

LOBID(- 1) 0.917 0.8083 0.927 0.9139 (31.04)c (8.89)c (23.26)c (26.15)c

AL4(1) -1.141 -0.6872 -1.1787 -1.1526 (-10.09)c (-4.34)C (- 9.41)c ( 10.06)c

RATE( - 1) 0.0984 0.3031 0.2925 0.294 (0.81) (3.08)c (2.83)c (3.00)c

SUPPLY 0.0718 0.062 0.0311 0.0225 (1.11) (1.27) (0.63) (0.46)

DEALAND -0.1045 -0.0321 -0.0855 -0.0611 (-1.56) (-0.48) (-1.23) (-0.90)

DOCUM -0.1433 (- 1.85)a

OVERSU - 0.0146 (-0.13)

CHL4NGE - 0.0178 - 0.0789 (-0.25) (-1.19)

CAL4NGE( - 1) - 0.1357 (_ 1.99)a

CAL4NGE( - 2) -0.1399 (2.23)b

DURBIN-h 1.0801 0.8421 1.1665 1.2455

Rj2 0.5921 0.4793 0.611 0.6027

Note: t-statistics are in parentheses. aSignificant at the 1% level. bSignificant at the 5% level. cSignificant at the 1% level.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

REVENUE-EQUIVALENCE AND BIDDING BEHAVIOR 313

the regime dummy is not significant at the time of the change, whereas the entry restriction dummy is negative and significant. This could indicate correlation of policy instruments-reservation bid, documentation, and oversupply-aimed to- wards pushing the clearing rate down.

Furthermore, if one drops the two counter-sec- ular dummies, the size and significance of the regime dummy are enhanced, especially when lagged once or twice. This is strong evidence of multicollinearity. The significance at lag 2 is espe- cially meaningful since it represents the drop of the minimum bid to a lower plateau (see graph 1) that coincides with the extra documentation de- mands (auction 41). Dominguez (1991) finds evi- dence of a similar policy correlation int he Boli- vian case.

V. On Repeated Auctions and Learning Effects

The expected revenue results sumnmarized in section II referred to single-shot auctions. How- ever, the Zambian foreign exchange auction is a repeated game where bidding behavior is likely to be influenced by learning and dynamic considera- tions, which may not be captured in a static framework. Furthermore, there are no general results on expected revenues or comparative bid- ding strategies in repeated multi-unit auctions.25 Thus one could argue that the empirical results of this paper cannot be contrasted with a theoret- ical counterpart.

This lack of correspondence should not flaw the interpretation of these results for two rea- sons. First, learning is aimed towards better assessing the opponents' valuations, and thus forecasting the clearing rate more accurately. However, bidders are uncertain about the num- ber and identity of their opponents. This is a sealed bid auction and although some bidders may overlap over time, a single bidder has no way of knowing who participates in each auction. Al- though this weakens the influence of learning, it opens the question of bidding against an under- tain group of bidders (see McAfee and McMillan, 1987b; Harstad et al., 1990). In single object auctions, revenue-equivalence between first and second price auctions has been shown to hold for this case.

Second, since the intervention tests entail com- paring average outcomes of the two auction regimes, even if bidders learn, this will carry no biases as long as the learning opportunities are comparable under both regimes. Since the avail- able information under both regimes was the same, there is no reason to think that bidders will learn more under a particular format.26 Thus, even with learning, misspecification or misinter- pretation of the tests is not likely to arise.

VI. Conclusions

Using data from the Zambian foreign exchange auction, econometric tests are carried out to ana- lyze the effects of a format change on bidders' behaviors in multi-unit auctions. The results sug- gest that, after controlling for other relevant effects, the competitive format yields a higher average revenue than the discriminatory format. Additional results of intervention tests suggest that (a) bidders that bid consistently higher than average showed slower adjustment to the format change; and (b) the minimum bid was likely the auctioneer's reservation bid.

Multi-unit auction theory suggests several fac- tors that may break down revenue-equivalence. The most notable factor favoring a higher rev- enue under competition is the affiliation of bid- ders' valuations. Thus, on the surface, one could interpret the revenue-superiority of the competi- tive auction as arising from the prevalence of public information in forming exchange rate fore- casts.

However, revenue-equivalence tests that endo- genize bidder participation indicate that the revenue-superiority of the competitive auction originates in higher effective bidder participation under this format. The relative attractiveness of competition is likely related to the standard theo- retical finding that bidding strategies are simpler to compute in these kinds of auctions (Vickrey, 1961). This result points towards placing more

25 Weber (1983) derives some equivalence results for the unit-demand case.

26 With affiliated values there are two major uncertainty sources. The first relates to the value of the objects; and the second refers to the distribution of the opponents' valuations. Since a dominant strategy does not exist in the competitive auction, the second source of uncertainty does not disappear under this format. Also, since the lengths of the auction periods were not markedly different, no major disparities appear to exist regarding learning incentives and opportuni- ties in both formats.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions

314 THE REVIEW OF ECONOMICS AND STATISTICS

emphi s on studying entry decisions into auc- tions, and incorporating the costs of information acquisition and bid preparation more routinely into auction models.

Although the Zambian case offers a real-life experimental ground for analyzing some of the empirical properties of multi-unit auctions, the peculiarities of this experience makes it impossi- ble to extract general conclusions or widespread policy prescriptions. More comprehensive tests based on various experiences and, perhaps, con- trolled experiments should be pursued in the future to analyze these issues.

REFERENCES

Aron, Janine, and Ibrahim Elbadawi, "Foreign Exchange Auction, the Parallel Rate Premia, and Exchange Rate Unification: A Macroeconomic Analysis for Zambia," mimeo, The World Bank (1991).

Box, G. E. P., and G. M. Jenkins, Time Series Analysis, Forecasting and Control (San Francisco: Holden Day, 1970).

Box, G. E. P., and G. C. Tiao, "Intervention Analysis with Applications to Economic and Environmental Prob- lems," Joumal of the American Statistical Association 70 (1975), 70-79.

Brannman, Lance, J. Douglass Klein, and Leonard W. Weiss, "The Price Effects of Increased Competition in Auc- tion Markets," this REVIEW 69 (Feb. 1987), 24-32.

Brimmer, Andrew F., "Price Determination in the U.S. Trea- sury Bill Market," this REVIEW 44 (1962), 178-183.

Dominguez, Kathryn M., "Do Exchange Rate Auctions Work? An Examination of the Bolivian Experience," N.B.E.R. Working Paper No. 3683 (1991).

Engelbrecht-Wiggans, Richard, "Revenue Equivalence in Multiple Object Auctions," Economics Letters (26) (1988), 15-19.

Friedman, Milton, "Price Determination in the United States Treasury Bill Market: A Comment," this REVIEW 45 (1963), 318-320. , "Comment on Collusion in the Auction Market for Treasury Bills," Journal of Political Economy 72 (1964), 513-514.

Hansen, Robert G., "Empirical Testing of Auction Theory," American Economic Review 75 (2) (1985), 156-159. , "Sealed-Bids versus Open Auctions: The Evidence," Economic Inquiry 24 (1986), 125-142.

Harris, Milton, and Arthur Raviv, "Allocation Mechanisms and the Design of Auctions," Econometrica 49 (1981), 1477-1499.

Harstad, Ronald, "Alternative Common Value Auction Pro-

cedures: Revenue Comparisons with Free Entry," Journal of Political Economy 98 (1990), 421-429.

Harstad, Ronald, John Kagel, and Dan Levin, "Equilibrium Bid Functions for Auctions with an Uncertain Number of Bidders," Economics Letters 33 (1990), 35-40.

Johnson, Ronald, "Oral Auctions versus Sealed Bids: An Empirical Investigation," Natural Resources Journal 19 (1979), 315-335.

Krumm, Kathie, "Exchange Auctions: A Review of Experi- ences," C.P.D. Discussion Paper No. 1985-22, The World Bank (1985).

Maskin, Eric, and John Riley, "Auction Theory with Private Values," American Economic Review 75 (1985), 150-155.

Mathews, Steven, "Information Acquisition in Discriminatory Auctions," in Marcel Boyer and Richard Khilstrom (eds.), Bayesian Models in Economic Theory. (Amster- dam: North-Holland, 1984), 181-208.

McAfee, R. Preston, and John McMillan, "Auctions and Bidding," Journal of Economic Literature 25 (1987a), 699-738. , "Auctions with a Stochastic Number of Bidders,"

Journal of Economic Theory 43 (1987b), 1-19. Mead, Walter, Competition and Oligopsony in the Douglas Fir

Lumber Industry (Berkeley: University of California Press, 1966).

Panayotacos, Paul, "Transition Issues in Exchange Rate Uni- fication: The Case of Zambia," mimeo, The World Bank (1987).

Rieber, Michael, "Collusion in the Auction Market for Trea- sury Bills," Journal of Political Economy 72 (1964), 509-512.

Robinson, Marc, "Collusion and the Choice of an Auction," Rand Journal of Economics 16 (1985), 141-143.

Samuelson, Larry, "Optimal Auctions and Market Structure," in Richard E. Quandt and Dusan Triska (eds.), Opti- mal Decisions in Market and Planned Economies (Boulder: Westview, 1990).

Smith, Vernon, "Microeconomics Systems as an Experimental Science," American Economic Review 72 (5) (1982), 923-955.

Tenorio, Rafael, "Strategic Price-Quantity Choice in Multi- Unit Auctions," mimeo, College of Business Adminis- tration, University of Notre Dame (1992a). , "Foreign Exchange Auctions," in The New Palgrave Dictionary of Money and Finance (London: Macmillan Reference Books, 1992b).

Vickrey, William, "Counterspeculation, Auctions, and Com- petitive Sealed Tenders," Journal of Finance 16 (1961), 8-37. , "Auctions and Bidding Games," in 0. Morgenstern and A. Tucker (eds.), Recent Advances in Game Theory (Princeton: Princeton University, 1962), 15-27.

Weber, Robert J., "Multiple Object Auctions," in R. Engel- brecht-Wiggans, M. Shubik and R. Stark (eds.), Auc- tions, Bidding and Contracting (New York: New York University Press, 1983), 165-191.

This content downloaded from 62.122.78.91 on Tue, 24 Jun 2014 21:13:13 PMAll use subject to JSTOR Terms and Conditions