Embed Size (px)

Citation preview

Retirement Road Map Seminar

Retirement Ahead

As you approach or enter retirement, it can be frightening since you don’t know what lies ahead.

What’s beyond the next curve? What is over the next hill?

Should there be a warning sign—retirement ahead?

How should you deal with the changes coming?

This seminar is designed to help take some of the uncertainty out of your retirement plans and help you plan for your retirement journey.

When Retirement Concerns Shift

Retirement changes do not happen all at once.

It may not be a complete change, but just a shift in your focus.

One of your major concerns for retirement is how you think of your money and savings.

Throughout this script, there are additional comments, quotes,

and facts that may be incorporated into the presentation, or used

to answer questions or stimulate discussion.

As the couple in this slide review their retirement plans, what are they thinking?

He’s thinking, “That retirement road map has certainly helped us enjoy our retirement.”

She’s thinking, “I’m glad he asked directions this time!”

You lay awake some nights thinking about various decisions—did I buy the right stock? Should I have sold that property? Then, one night you wake up asking yourself will I run out of money in retirement? You don’t go back to sleep—you just made the “retirement shift.”

Nick Murray speaking at the NAVA Marketing Meeting, Feb. 2006.

The top two things people worry about are terrorism and saving for retirement. These issues trump other worries, including family, current finances, getting into an accident, health, and careers.

Article: “Americans worried about retirement,”

Boomer Market Advisor, Newsletter, 2006.

Retirement Road Map Seminar PowerPoint Script Page 2 of 23

When retirement concerns shift from “How should you accumulate funds for retirement?” to “Will your retirement funds last throughout your retirement?”

[Answer questions with next slide]

You Need a Retirement Road Map

You need a retirement road map to help you plan for your retirement journey.

Think about how you plan a trip.

• You decide when to start

• What routes to take

• How long it should take

• What will you need on the trip

• Stops along the way

• Contingency plans should the unexpected happen

You plan or “map” your trip.

Planning for retirement is much the same.

A “Retirement Road Map” helps you plot your retirement journey.

Your Retirement Road Map will help you understand the uncertainties, questions, and changing concerns of retirement.

Re-Defining Retirement

• 49% of Boomers expect to retire after age 65

• 65% anticipate working after they retire

o 39% for financial necessity

o 28% desire—mostly high net worth

• 7 million retirees returned to work within 1 ½ years

Robert C. Pozen, Chairman,

MFS Investment Management,

NAVA Marketing Meeting, 2006

Retirement Road Map Seminar PowerPoint Script Page 3 of 23

Shifting Retirement Concerns

Let’s look at investing concerns, starting with investing for retirement.

Prior to retirement, your concern or investment objective is to accumulate as much as possible, or simply stated, “maximize accumulations.”

Prior to retirement, your concern is the greatest growth and appreciation—growth is more important than income, especially when taxation is considered.

The risk you are willing to take with investments for retirement are based on how far away retirement is—risks based on time horizons.

Just a quick comment, your investments should always

be consistent with your personal risk tolerances. If

you are not a risk taker, you should take fewer risks.

We mentioned taxes a few minutes ago, prior to retirement when we are in our peak earning years and maximum tax brackets; we try to defer taxation whenever possible.

[Advance slide]

How do these same investment concerns shift during retirement?

Your investment objectives shift from accumulations to preserving principal.

Your concerns for growth shift to seeking greater income.

The time-horizon of retirement has arrived and your focus now is on reducing risks.

And with taxes, you are not trying to defer them, because it may be harder to pay them later, you are shifting more emphasis on reducing taxes.

You have all of these concerns before and during retirement.

Retirement Road Map Seminar PowerPoint Script Page 4 of 23

However, with retirement, your emphasis is what shifts.

Understanding the shifting of concerns during retirement helps you to remove some of the “mystery” or uncertainties with retirement.

How long will your retirement last?

One of the largest uncertainties of retirement is how long it will last?

We know that 25% of men age 65 will still be alive 20 years later at age 85.

Forty percent of women age 65 will be alive 20 years later at age 85.

For a married couple each age 70, there is more than a 50% chance that one of them will be alive at age 92.

How long do some of the people in your family live?

That is a good indicator of how long you may expect to live.

Life expectancy tables can predict how long we will live on average—but averages usually mean that half live longer and half live less. Which half will you be?

[Advance slide]

Are you planning for enough years?

Let’s imagine…you are planning a long trip.

How do you plan for gas?

How are you going to be sure that you have enough money for gas?

Would you take just the amount necessary based on your average gas mileage?

Would you make allowances for extra stops? Getting lost? Heavy traffic? Detours?

Of course, you would.

You’re not going to risk running out of gas—or worse yet—running out of money for gas.

Retirement Road Map Seminar PowerPoint Script Page 5 of 23

You should not base your retirement on just living the average number of years.

Are you planning for enough years? Will you run out of money?

If you plan for just the average, you are taking a huge risk that you may run out of money by living too long.

However, it illustrates an important point: How long to plan for is just as important as how much to plan for.

Your Life Phases

Think about your life up to this point.

How did you plan for it? Was it all at one time?

No. It was probably in phases, a few years at a time making changes along the way.

You made your plans based on “your life phases.”

The common element in each of these “life phases” usually centered on a major activity.

For example, as a young adult in the “Learning Phase,” your major activities evolved around your education.

In the “Getting Started Phase” of your life the major activities were all new—new jobs, new homes, and new relationships.

The “Family Phase” may be the most active with marriage, children, and new homes all creating a variety of new activities.

Your time is spent at baseball and soccer games, dance recitals, scouts, and school plays.

What does it mean to run out of money during retirement? It means four things: You lose your lifestyle. You lose your independence. You lose your dignity. In addition, you lose the ability to look your grandchild or family member in the eye to explain why you cannot do the things you want to do for them. It is why the fear of running out of money is so terribly frightening!

Nick Murray speaking at the 2006 NAVA Marketing Meeting:

Retirement Road Map Seminar PowerPoint Script Page 6 of 23

The “Career and Education Phase” centered most of your activities on your career as well as providing education for your children.

Finally, you reached the “Empty Nest Phase.” The children are grown and out of the house (you hope).

After all these years, it is just the two of you.

Your activities change again with more time doing the things you want to do.

You have been living your life by phases.

Your life phases have been based on the main activities during those years.

The type and frequency of the activities often has been directly related to expenses for that phase.

Your investments were usually based on the funding of these various life phases.

Can the lessons you learned throughout these life phases be used to eliminate some of the uncertainties of retirement and help you plan?

Retirement Lifestyle Phases

Your retirement journey can be thought of similar to your life journey thus far—in phases—“Retirement Lifestyle Phases.”

Retirement planning seems almost overpowering if you try to plan for all retirement years at one time.

Retirement could easily span an amount of time equal to or greater than the time you spent working for any one employer.

Trying to plan for all your retirement years at one time is very difficult and almost impossible to feel completely confident that what you are doing will work.

You didn’t sit down when you were a young adult and make every decision for your life up until now, did you?

Retirement Road Map Seminar PowerPoint Script Page 7 of 23

You planned for each of the life phases.

The same approach works for retirement planning!

Pre-Retirement

One of the important phases of retirement actually occurs before retirement—“Pre-Retirement Phase.”

How do you know how much gas you need for your trip if you don’t have a clear destination?

Pre-Retirement planning is not only making plans and decisions for retirement, but it is also getting a clearer understanding of your destination.

The decisions made planning a trip will greatly affect the trip.

The decisions made in the “Pre-retirement Phase” will greatly affect your retirement.

Some of the decisions made prior to or at the start of retirement cannot be undone.

Some of these decisions consist of:

• When should you retire?

• How do you take your pension?

• Do you take Social Security now or later?

• What about health care decisions dealing with insurance and Medicare?

• Do you move closer to your children?

• Downsize your home?

• Purchase that retirement cottage?

• Continue working part-time?

A recent study showed that the most anxious period of retirement was the ten-year period starting five years before retirement and continuing through the first five years of retirement.

David R. Odenath, Jr., president of Prudential Annuities,

speaking at NAVA Marketing Meeting 2006.

Retirement Road Map Seminar PowerPoint Script Page 8 of 23

The Pre-Retirement phase often scares people the most since you cannot change some of the decisions later.

“Pre-Retirement Phase” is the time to gather information so you will make wise decisions.

It is a time for attending meetings like this one to get more answers and options.

Your retirement lifestyle starts in this “Pre-Retirement Phase.”

Initial Retirement

The initial retirement years are what we’ve worked a lifetime for!

You are feeling fresh and energetic and can’t wait to do all those activities that you planned.

Travel, hobbies, golf, tennis, clubs, grandchildren, loafing, relaxing, a new adventure—those first few retirement years are filled with activities.

Even after the newness of retirement wears off, the “Initial Retirement” years are usually some of the most active retirement years.

How much will it cost for these active retirement years?

“Retirement is going to cost,” says Sara Max in an article from the 3/28/05 issue of CNN-Money, “70% of earnings in peak years is the minimum amount most often quoted by financial planners.”

Life continues to be an exploration for boomers.

Microsoft, “What do boomers want in 2006?” Joanna L. Krotz.

Optimism on Retirement Lifestyles

• 7 out of 10 Boomers expect to maintain current lifestyle

• As retirement approaches, Boomers likely to acknowledge the need to downsize their lifestyles

Ann Cutts Hughes speaking at NAVA Marketing Meeting 2006, summarizing the Study of

American Investing Habits by ING and Roper Public Affairs

Retirement Road Map Seminar PowerPoint Script Page 9 of 23

What does this mean?

This means that your “Basic Needs” in retirement will cost at least 70% of your pre-retirement income.

Basic needs are those expenses during retirement that are necessary for you to maintain your lifestyle—expenses that pertain to your daily living and other necessities.

Although 70% is a common estimate, it may vary.

The types of expenses included with the 70% vary with age as well.

Other studies have found that the percentage of income spent on healthcare is small at the start of retirement, but grows as a percentage of income as you age.

Other expenses such as mortgages and housing often decline with age during retirement.

70%, adjusted for inflation, is usually referred to as a minimum or average amount needed for these basic needs.

What about all those extra activities such as travel and hobbies we talked about?

In the first few years of retirement these extra “wants” may add another 20% to 50% to the basic needs.

Activities and expenses go hand in hand.

During your Initial Retirement when activities are high, you need to allow for an extra 20% of your pre-retirement income, adjusted for inflation.

After-tax lifestyle expenses go down as you age. Almost all expenses went down 40% to 60%, except healthcare that went up by 46%. Housing which required the largest portion of income before retirement usually had the largest decease after retirement. When inflation was considered, the total expenses remain relatively level, however, the mix of expenses was greatly changed due to healthcare.

Source: U. S. Department of Labor, Bureau of Labor Statistics,

Consumer Expenditure Survey 2002.

Retirement Road Map Seminar PowerPoint Script Page 10 of 23

That means you need to plan for a minimum of 90% of your pre-retirement income, during each year of this phase.

Seasoned Retirement

As the newness of retirement begins to wear-off, you enter the slower phase of retirement called “Seasoned Retirement.”

This is the more relaxed, slower portion of your retirement.

The amount of activities, travel, and hobbies begin to decrease, and you stay closer to home.

The grandkids can come see you instead of you going to see them.

Your basic needs are still 70% of your pre-retirement income, adjusted for inflation.

Now, since your activities are less, you only need an additional 10% for the extra activities.

Again, these amounts should be adjusted for inflation, and vary with each individual.

Matured Retirement

The “Matured Retirement” years have much less activities, usually due to health or finances.

Extra activities become few and far between and a large amount of time is spent focusing on health concerns and maintaining the day-to-day necessities.

As the activities decrease, so do the expenses—you just need the basic.

70% of your pre-retirement income, adjusted for inflation, should cover your basic needs during this phase.

Remember, a large portion of this 70% will probably be due to rising healthcare costs, more than offsetting any reduction in other expenses.

Retirement Road Map Seminar PowerPoint Script Page 11 of 23

Survivorship Years

At some point, you lose your life partner—your spouse.

Retirement needs don’t stop when one spouse dies.

Although one spouse is gone, the lifestyle basic needs of the survivor typically cost 60% of your pre-retirement income, adjusted for inflation. (Estimate provided by Social Security Administration.)

Planning for the survivorship years is essential to peace-of-mind during retirement.

These are the retirement lifestyle phases, and as you have seen, they resemble your lifestyle phases leading up to retirement.

Retirement lifestyle phases, manageable time periods of 6 to 10 years, reduce the complexity of planning for 20, 30, or 40 years of retirement.

The retirement lifestyle phases also help you estimate the costs, since activities are associated with the phases, and costs are associated with the activities.

Retirement lifestyle phases simplify your retirement planning process.

Retirement Must Consider Inflation

You’ve heard me mention “Adjusted for inflation” several times throughout this presentation.

This chart shows how inflation has increased over the past 20+ years.

Does anyone here think there will not be similar inflation during your retirement?

If inflation continues as it has in the past, your retirement income will need to increase during retirement for you to maintain your desired lifestyle.

Retirement Road Map Seminar PowerPoint Script Page 12 of 23

If inflation averaged 3% during retirement, your income would need to double in 24 years just to maintain the same lifestyle.

Many of you had parents or grandparents who were retired on fixed incomes during the 80’s when inflation was double-digits.

You know how important considering inflation is.

Doesn’t this make retirement planning even more uncertain and complex?

Fortunately there are computers today that can make those adjustments for us—we just have to be sure that it is taken into account.

Computers make it possible to express all of the values in terms of “today’s dollars,” then it adjusts them accordingly—thinking in terms of needs and income today makes retirement planning much simpler.

So how does all of this come together?

How is this going to help you understand if you have enough?

Let’s look at your retirement journey step by step.

Your Retirement Journey Step 1

What do you need to do first?

You need to determine the likely times and duration of each phase for you.

U. S. Inflation Rates for Selected Years

Year 1975 1980 1985 1990 1995 2000 2004

Rate of Inflation

7.0% 12.4% 3.8% 6.1% 2.5% 3.4% 3.3%

Consumer Price Index (CPI) as reported by the Federal Reserve Board

Retirement Road Map Seminar PowerPoint Script Page 13 of 23

Your plan will be different from those of others.

The important thing is to be realistic.

For many, an estimate of 8 to 10 years per phase is not unusual.

So, what’s next?

Your Retirement Journey Step 2

Examine lifestyle requirements for each phase.

Think about the activities you have planned for each phase.

Remember, there is a direct link between the activities and the expenses during a phase.

How do you determine the amount you need for each phase?

[Advanced slide]

You start by estimating “Basic Needs.”

You may want to use the 70% of current income suggestion that was discussed earlier.

[Advanced slide]

You estimate your “Additional Wants” based on the extra activities you associate with that phase.

[Advanced slide]

The “Total Desired Income” for each phase of your retirement is the sum of your “Basic Needs” and “Additional Wants.”

“Seniors often thank me for not making reference to ‘buckets’ or ‘pots of money’ when referring to the assets and investments that they depend upon for their entire financial security. They often comment that they appreciate not having the phases of their retirement called by ‘cute’ names. Seniors take their retirement very seriously.”

J. Maxey Sanderson, CLU, ChFC,

VP Product Development,

Impact Technologies Group, Inc.

Retirement Road Map Seminar PowerPoint Script Page 14 of 23

You now have the amount of income you desire for each phase, expressed in terms of today’s dollar.

Your Retirement Journey Step 3

Next, you need to compile all your “known” sources of retirement income.

Do you know what is meant by “known” sources?

Known sources are the incomes you know you are going to receive and you have a good idea of the monthly amount.

The typical known sources of retirement income are Social Security, pensions, qualified retirement plans like an IRA or 401(k), or annuity payments.

Your Retirement Journey Recap Steps 1, 2

& 3

Let’s review…

So far, you have determined:

• Your retirement phases, when they will occur, and how long they will last

• Your desired income needed to live the retirement lifestyle you desire

• Your known income from various sources, such as Social Security, IRAs, or 401(k)s

Putting everything together comes next.

Your Retirement Journey Step 4

Calculating the remaining requirements is the biggest challenge.

You must compare your desired monthly income with the sum of your known income, which is given in a monthly retirement amount, and your retirement investments and assets, which have a total “value” today.

Retirement Road Map Seminar PowerPoint Script Page 15 of 23

For example, if you add $2,000 of monthly Social Security income to $200,000 of mutual funds, what does that give you?

This is like adding “apples and oranges”—it just tends to add to the uncertainty.

So, what do you do?

[Advance slide]

You start with your “Desired Income Required”—the sum of your needs and wants for retirement.

[Advance slide]

You then reduce that by your “Known Income.”

Your Social Security, IRAs, 401(k)s, etc.

[Advance slide]

This will give you your “Remaining Requirement.”

This is where we put the computers to work.

The remaining requirements, adjusted for inflation, are determined for each year.

Based on the start of each phase, the amount necessary today to provide the remaining requirements is determined.

It should be noted that the investment strategy

recommended for each phase is used to determine the

amount needed for that phase. We’ll discuss that

strategy in a moment.

Risk Tolerance

The degree of uncertainty that an investor can handle in regards to a negative change in the value of their portfolio.

An investor's risk tolerance varies according to age, income requirements, financial goals, etc. For example, a 70-year old retired widow would generally have a lower risk tolerance than a single 30-year old executive.

http://www.investopedia.com/terms/r/risktolerance.asp.

Retirement Road Map Seminar PowerPoint Script Page 16 of 23

Now you have an amount, valued in “today’s dollars,” that is necessary to provide the remaining income required.

Now, we simply compare our retirement assets and investments with the amount required to see if we have enough.

This method makes it possible for you to know exactly where you are relative to retirement.

Knowing where you stand lets you make reasonable plans.

With this calculation, you know how much is available for other purposes.

Or, whether you need to use some assets you were hoping not to use for retirement.

Or, that you may need to work a little longer or at least part-time for a few years.

Having this one number lets you make plans.

Your Retirement Journey Step 5

Shortfalls during retirement can be a disaster.

However, if you know about them in advance, you can plan accordingly.

Knowing the likely shortfalls can help you decide if you need to downsize your home during retirement.

Perhaps you need to reconsider some of your wants and additional activities.

Regardless of what you decide to do, you can take comfort in the fact that you have a clear understanding of your situation and can make an informed decision regarding your retirement.

A 2004 survey by Employee Benefit Research Institute suggests that only 42 percent of Americans have tried to calculate how much they need to save for retirement.

“Taking the Mystery Out of Retirement Planning,” U. S. Department of Labor,

Employee Benefits Security Administration, 2006.

Retirement Road Map Seminar PowerPoint Script Page 17 of 23

The recommended investment strategy was mentioned earlier. What investment strategy should be used to fund the remaining requirements?

Phases gave you the guide for your needs; it can also provide the guide for your investments.

Investing By Phases

Investing by phases means you don’t have to change all your retirement funds at one time when you retire—you shift investments based on your retirement phases.

You want an investment strategy of retirement assets based on phases. Each of your phases has its own time horizon.

Time horizons simply help determine when you will start using a particular investment.

Time horizons tell you when a phase begins.

Knowing when a phase begins allows you to invest accordingly, and shift investments by phases.

The assets you are using in a phase to supply income should be invested very conservatively—seeking low risk; for example, money markets, short-term CDs, etc.

For the assets to be used in the next phase, your objective should be to minimize fluctuations, even when it means less yields.

When you are ready to shift those assets to provide income, you don’t want to wait on a market change.

For the assets being used to fund the later phases, you want to seek high yields.

For those future phases, how aggressive you are depends on how long until those fund will be used—their time horizons.

Now your investment strategy for the retirement assets is simple: reallocate assets at the start of each phase.

Retirement Road Map Seminar PowerPoint Script Page 18 of 23

This strategy allows you to have fewer worries about your month-to-month income and lets you continue to seek the higher yields with funds that will not be used for a number of years.

A special note: these investment suggestions are

based only on the time horizons: you must also invest

within your personal risk tolerances.

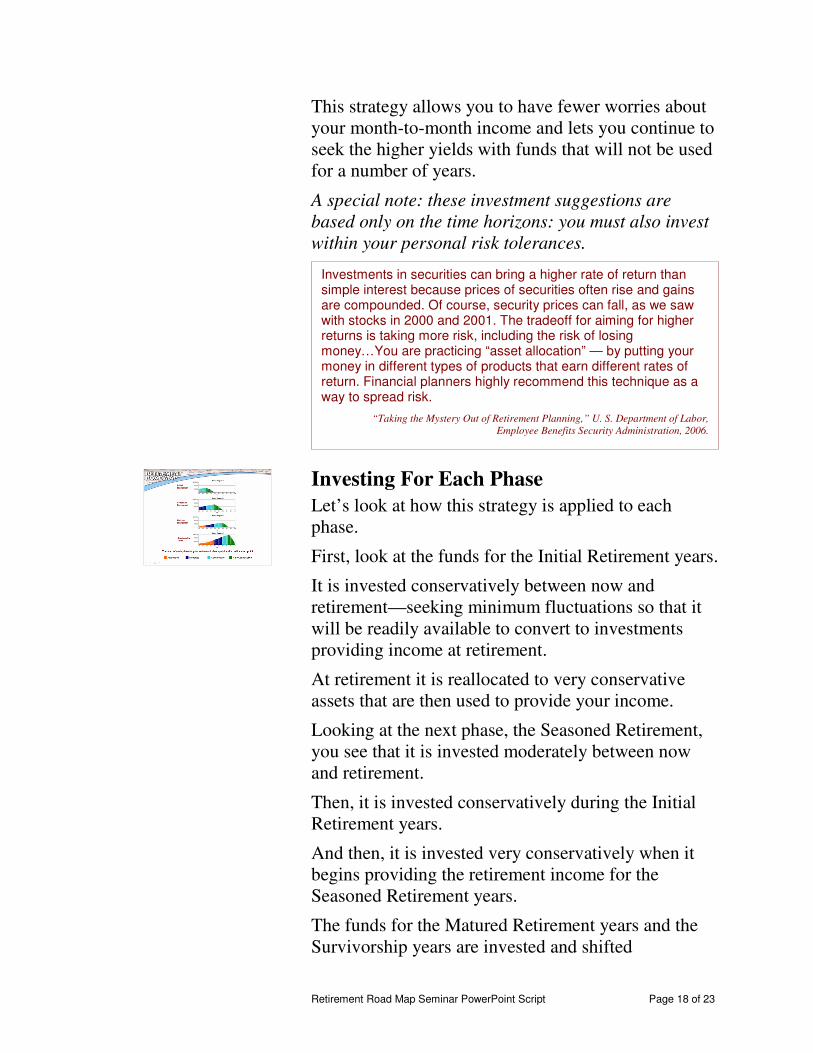

Investing For Each Phase

Let’s look at how this strategy is applied to each phase.

First, look at the funds for the Initial Retirement years.

It is invested conservatively between now and retirement—seeking minimum fluctuations so that it will be readily available to convert to investments providing income at retirement.

At retirement it is reallocated to very conservative assets that are then used to provide your income.

Looking at the next phase, the Seasoned Retirement, you see that it is invested moderately between now and retirement.

Then, it is invested conservatively during the Initial Retirement years.

And then, it is invested very conservatively when it begins providing the retirement income for the Seasoned Retirement years.

The funds for the Matured Retirement years and the Survivorship years are invested and shifted

Investments in securities can bring a higher rate of return than simple interest because prices of securities often rise and gains are compounded. Of course, security prices can fall, as we saw with stocks in 2000 and 2001. The tradeoff for aiming for higher returns is taking more risk, including the risk of losing money…You are practicing “asset allocation” — by putting your money in different types of products that earn different rates of return. Financial planners highly recommend this technique as a way to spread risk.

“Taking the Mystery Out of Retirement Planning,” U. S. Department of Labor,

Employee Benefits Security Administration, 2006.

Retirement Road Map Seminar PowerPoint Script Page 19 of 23

accordingly—reallocated at the start of each phase, so that they are more conservative with each phase, until they are used to provide the retirement income for that phase.

[Advance slide]

This is a lot of information for one slide, so let’s look at it a different way.

If you look at just the pre-retirement years, you see the funds for the Initial Retirement years invested conservatively;

the funds for Seasoned Retirement years invested moderately;

the funds for the Matured Retirement years and the Survivorship years invested aggressively.

[Advance slide]

If you look at just the Initial Retirement years, you see the funds providing income—green—invested very conservatively.

The funds for Seasoned Retirement years have been reallocated to conservative assets since they will be used next.

The funds for the Matured Retirement years have been reallocated to moderate assets.

And the assets for the Survivorship years continue to be invested aggressively as there are a number of years before they will be providing the income.

[Advance slide]

During the Seasoned Retirement years, the funds providing the income are green—very conservative.

The funds for the Matured years are now conservative since they will be used next.

And the funds for the Survivorship years are now moderate.

Retirement Road Map Seminar PowerPoint Script Page 20 of 23

[Advance slide]

During the Matured Retirement years, those funds are now providing the income.

The funds for the Survivorship years are now conservative.

Do you see how this strategy works?

The funds providing the income for each phase is coming from assets that vary the least so that you don’t have to check on the stock market to see if you can afford to go see your grandchild that month.

Yet, for the funds that will not be used for a number of years, you continue to invest for maximum yields.

As we discussed earlier, we have always invested based on phases.

This strategy allows you to continue to invest by phases throughout your retirement.

When you apply all of these principles to your retirement plans, you have what we refer to as a “Retirement Road Map.”

How do you get a “Retirement Road Map” for your worry free retirement?

Action Plan

One of my favorite quotes is from the late Frank Sullivan: “If you don’t change directions, you’ll end up where you’re going.”

That can be a good thing – or that can be a bad thing.

If you are on course, you need an action plan to stay the course.

If you need to make changes, you need a plan of action.

Retirement Road Map Seminar PowerPoint Script Page 21 of 23

[Advance slide]

In the materials in front of you, you will see a Retirement Road Map Brochure.

You may want to take a moment to get this.

[Advance slide]

This brochure is a summary of this meeting.

You may find it helpful when you get home and want to review what we have talked about.

[Advance slide]

Inside you will also see six questions.

• When do you plan to retire?

• How much monthly income do you need?

• What is the current value of your retirement plans?

• Current value of other assets specifically set aside for retirement?

• Would you like to illustrate Social Security?

• And do you have any other retirement income?

If you know this information now, please take a few minutes to answer these questions.

Retirement Road Map calculates known retirement incomes including Social Security, pensions and annuities, compares that to retirement needs, and then calculates the value today necessary to make up the difference. As a result, there is a single number to compare with assets or investments. Impact makes complex calculations easy to understand so clients can make important decisions. Retirement Road Map shows a strategy for each year of retirement to assure predictable income while maximizing investments.

Financial Advisor,

http://www.fa-mag.com/issues.php?id_content=2&idIssue=104&show=advisor

Retirement Road Map Seminar PowerPoint Script Page 22 of 23

[Advance slide]

Whether or not you complete the brochure here today or at home in the next few days, this is the information that is needed to get your retirement road map started.

[Advance slide]

With this information, an appointment can be arranged to discuss it and your personal goals and objectives.

[Advance slide]

In that appointment, we will review

• Your retirement phases

• Your lifestyle needs

• Your income sources

• Your remaining needs

• And, if any shortfalls, a plan of action

With this information, we can then prepare “Your Retirement Road Map.”

[Advance slide]

Once your road map is completed, you can sit back, relax, and enjoy the ride.

If you don't know where you are going, you will probably end up somewhere else.

Laurence J. Peter

US educator & writer (1919 - 1988)

Retirement Road Map Seminar PowerPoint Script Page 23 of 23

Personalize Your Road Map

Your personalized Retirement Road Map can take some of the uncertainties and mystery out of retirement.

Before you go, take a minute to fill out the Wrap-up form in front of you.

Be sure to indicate the best time to contact you.

Also, if you can think of anyone that might be interested in a Retirement Road Map for themselves, please write their name at the bottom of your sheet, or take one of my cards and a Retirement Road Map Brochure to them.

I want to thank you for coming today.

Remember, if you don’t change directions, you will end up where you are going!

We want to help you go in the direction of a worry-free retirement by providing you a personal “Retirement Road Map!”

What will you be thinking ten years into your retirement? “Please don’t let it be, we should have stopped and got directions.”